Crypto World

Former Ripple CTO Talks About Meme Coins as Investment

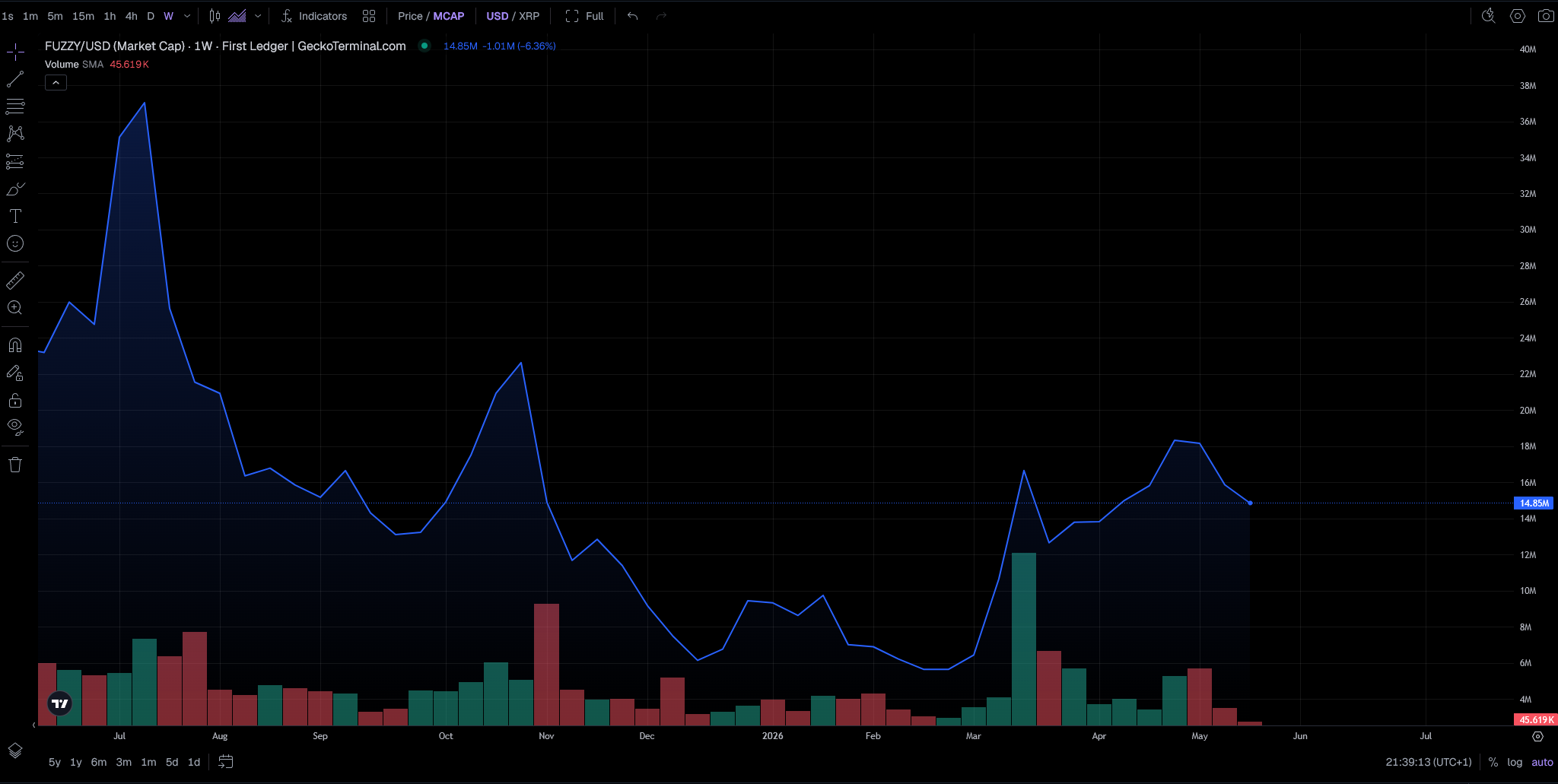

Ripple Chief Technology Officer Emeritus David Schwartz said treating a meme coin as an investment feels distasteful. The Ripple veteran brushed aside XRP holders who urged him to endorse the FUZZY token on the XRP Ledger.

Schwartz, known on X as JoelKatz, made the remark during a weekend exchange about FUZZY. The meme coin references a wallet Ripple activated when the XRP Ledger launched in 2013.

Schwartz Pushes Back on FUZZY Endorsement Pressure

The conversation started after Schwartz opened a technical trust line for FUZZY. Some community members read the move as a quiet signal of approval.

The token’s name nods to the historic Fuzzybear wallet. That wallet placed a famous trade of 1 XRP for 1 BTC in the early days of the ledger.

Schwartz rejected that interpretation. He told followers that opening a trust line is a routine network step. It is not a vote of confidence in any specific project. He added that he has no direct involvement with FUZZY and knows no more about it than any other observer.

The Ripple veteran also explained why he avoids public endorsements even when nothing negative surfaces about a project. He said the risk of unintentionally promoting bad actors keeps him cautious. He also stressed he has no reason to think poorly of FUZZY itself.

Meme coin Skepticism Cuts Across XRP Ledger Token Surge

His comments arrive as the meme coin scene on XRP Ledger continues to draw retail attention. Tokens such as ARMY, PHNIX, and RIPPY have posted sharp gains over the past few months. The activity has driven heavier trading on platforms like First Ledger and Magnetic.

Other users argued that meme coins lack intrinsic value and trade purely on the hope of a higher bidder. Schwartz agreed. He said attempts to build a serious portfolio around such tokens look ridiculous. Meme coins themselves still have a place in internet culture, he added.

The skepticism aligns with how Schwartz has framed his wealth and Ripple’s broader posture. He has drawn a line between community tokens built for fun and assets that warrant serious position sizing.

The post drew sharp reactions from XRP supporters. Some argued that meme coin liquidity tied to XRP supports the wider ecosystem regardless of their personal view. Others backed his caution and asked influencers to stop pressuring developers into public endorsements.

The post Former Ripple CTO Talks About Meme Coins as Investment appeared first on BeInCrypto.

Billions of dollars in prediction market positions settle every month based on a machine for deciding truth that most traders have never examined. This guide explains how UMA’s optimistic oracle turns real-world events into on-chain payouts, why the system usually works, the cases where it has failed spectacularly, and the rival settlement designs trying to replace it.

Prediction markets had their breakout year in 2026. Combined volume across the major venues hit $44.8 billion in June alone, driven by a World Cup that turned Polymarket into a multi-billion-dollar sportsbook. The trading side of these platforms is easy to understand: shares in Yes or No, priced between zero and one dollar, paying out one dollar if you are right. The hard part is invisible until it breaks. Someone, or something, has to decide what actually happened.

That decision layer is called resolution, and it is the load-bearing wall of the entire sector. A prediction market is only as good as its ability to decide truth, and a blockchain cannot observe the real world. It cannot see who won an election, whether a company sold an asset, or whether a bill passed. The bridge between reality and the smart contract is an oracle, and for the largest on-chain prediction market, that oracle is UMA. Understanding how it works, and how it fails, is the single most useful piece of due diligence a prediction market trader can do.

The oracle problem, event edition

Crypto solved one version of the oracle problem years ago. Price feeds from networks like Chainlink and Pyth deliver asset prices on-chain by aggregating data from many independent publishers. That works because prices are public, continuous, machine-readable, and available from dozens of redundant sources.

Event markets break every one of those assumptions. The questions are one-off rather than continuous. The answers often live in press releases, court rulings, regulatory filings, or a referee’s whistle. And the phrasing matters enormously: a market asking whether a politician says a specific word five times needs a resolution process that can read, interpret, and withstand challenge. No price feed can answer questions like that. What the sector needed was an oracle for arbitrary facts, with a built-in way to contest wrong answers.

Enter UMA and optimistic verification

UMA, short for Universal Market Access, is an oracle protocol built by Risk Labs. Its core product, the Optimistic Oracle, resolves outcomes for Polymarket’s main venue, which cleared around $14 billion in monthly volume during the World Cup peak. The word optimistic describes the design philosophy: submitted answers are assumed true unless someone challenges them, with economic incentives doing the policing instead of a central referee.

The flow for a typical Polymarket market runs through a version of the oracle called OOv2, and it has four stages:

- Request. When a market’s end conditions are met, the market contract asks the oracle for the outcome, referencing the exact resolution criteria written when the market was created.

- Proposal. A proposer submits the answer, Yes or No, and posts a bond of $750 in USDC. If the proposal is wrong, the bond is forfeited. If it stands, the proposer earns a reward.

- Challenge window. The proposal sits open for two hours. Anyone who believes it is wrong can dispute it by posting a matching bond.

- Escalation. If a dispute lands, the question goes to UMA’s Data Verification Mechanism, the DVM, where UMA token holders research the question and vote on the correct answer. Voters who side with the final outcome earn rewards; voters who miss or vote against it lose a slice of their stake. The DVM’s ruling is final, the losing bond pays the winner, and the market settles.

To make that concrete, follow one uncontested market through its whole life. A market opens asking whether a central bank cuts rates at its June meeting, with resolution criteria naming the official statement as the source. Traders price Yes at 70 cents through the month. The decision lands at 2 p.m., the statement confirms a cut, and within minutes an approved proposer submits Yes with the $750 bond. For two hours, anyone on earth with a matching bond could object; nobody does, because the statement is public and unambiguous. The window closes, the oracle reports Yes to the market contract, and every Yes share becomes redeemable for one dollar in USDC. Total elapsed time from event to payout: under three hours, no human authority involved, no appeal needed. That is the experience for the overwhelming majority of markets, and it is why the system scaled.

The bond arithmetic deserves a sentence of its own, because it is the whole security model in miniature. Seven hundred fifty dollars sounds trivial next to markets carrying tens of millions in open interest, and read one way, it is: a wrong proposal on a whale-scale market risks $750 to potentially swing a payout worth thousands of times that. The design’s answer is that the bond does not defend the market alone, the challenge window does. A false proposal only profits if nobody in the world notices for two hours, on a venue where every large market has thousands of position holders watching resolution like hawks and a matching bond waiting for whoever catches the error. The bond prices the cost of forcing a dispute, not the value of the market, and the escalation layer is supposed to carry the real weight. That framing also locates the true weak point precisely: the system is only as strong as the layer disputes escalate to.

The percentages favor the happy path. Roughly 99% of assertions since 2021 have gone undisputed, meaning most markets settle in the two-to-four-hour window after an event without any human argument. The system processes upward of 7,000 proposals per month, and Risk Labs has automated much of the pipeline: language models draft proposals for around half a cent per request, and bots like OOTruthBot summarize evidence threads and flag suspicious submissions, cutting routine resolution from hours to seconds.

Inside the DVM: what a token vote actually looks like

Since the DVM is the backstop everything escalates to, its mechanics deserve a closer look than most traders ever give them.

When a dispute triggers a vote, the question enters a voting round for UMA token holders who have staked into the voting system. Voting runs in two phases. In the commit phase, each voter submits an encrypted vote, hidden from everyone including other voters, which prevents late voters from simply copying the visible majority. In the reveal phase, voters decrypt and publish what they committed. Votes are weighted by staked tokens, and the outcome that carries the stake-weighted majority becomes the oracle’s answer.

The incentive design is the load-bearing part. Voters who land with the final outcome earn rewards from protocol emissions. Voters who miss a round or land against the outcome lose a slice of their stake. The design intends to pay for diligence, and it mostly does, but it carries a known theoretical flaw inherited from every majority-rewarded oracle: the profitable strategy is voting with the expected majority, not with the truth, and in ordinary cases those two targets coincide. The failure cases are the ones where they separate, and where a large holder can make the majority whatever they need it to be.

There is also a timing cost. An undisputed market settles within hours; a disputed one waits for the full commit and reveal cycle, stretching resolution to days while positions stay frozen and traders argue in evidence threads. For anyone holding size, a dispute is not just a risk to the payout but a lockup on capital.

In November 2025 the system got its most significant overhaul, the Managed Optimistic Oracle V2. MOOv2 restricted the right to propose resolutions to 37 pre-approved addresses, a mix of Risk Labs staff and Polymarket users with high historical accuracy, while keeping disputes open to anyone. The change targeted premature and spam proposals, which had been a chronic source of delays and gamesmanship. Proposing became curated; challenging stayed permissionless.

Where the machine breaks

The design has one structural soft spot, and 2026 has stress-tested it in public: the final arbiter is a token vote, and tokens can be bought, concentrated, and conflicted. The numbers behind that concern are not speculative. A Wall Street Journal investigation published in May found that in most disputed Polymarket markets, more than half of the UMA votes came from the ten largest wallets. At least 60% of active UMA voters could be linked to live Polymarket accounts, and roughly one in five disputes had at least one voter with a financial stake in the market they were ruling on. The dispute pipeline itself is swelling: Polymarket logged more than 1,150 disputed markets in the first five months of 2026, already past its full-year 2025 total.

Two cases show what that looks like in practice.

The first was a 2025 market on a United States minerals agreement, where a single large UMA holder cast five million tokens across three accounts, about 25% of the vote in that dispute round, pushing a contested market to resolve early against the plain reading of events. Traders on the wrong side of that ruling lost roughly $7 million. The vote was legal under the system’s rules. That was precisely the criticism.

The second came in June 2026 and drew more than $60 million in volume: a market asking whether Strategy would sell any Bitcoin by May 31. A regulatory filing published on June 1 disclosed that the company had sold 32 BTC between May 26 and May 31 at an average price of $77,135, its first disposal since 2022, inside the market’s cutoff. Two proposed resolutions were challenged, the question escalated to a token vote, and the market ultimately resolved No. Shares tracking the documented answer traded at 12 cents while the dispute ran. Critics across the industry framed the episode as a structural verdict: when ambiguous rules meet concentrated voting power, the payout can diverge from the facts, and the holders of the settlement token can be the same people holding positions in the market being settled.

None of this means most markets resolve wrongly. The overwhelming majority settle cleanly and fast. It means the tail risk is governance-shaped: the worst outcomes cluster in high-volume, ambiguously worded markets where a motivated whale has both the tokens and the position.

Why Polymarket keeps the system anyway

Given the 2026 dispute record, the obvious question is why the largest on-chain venue has not replaced its oracle. The answer is a stack of practical reasons that critics tend to skip.

The happy path really is that good. Ninety-nine percent of markets settling within hours, at a cost of fractions of a cent per automated proposal, across every category from elections to award shows, is a service level no alternative currently matches for open-ended questions. Deterministic settlement cannot touch subjective markets at all, and regulated clearing brings jurisdiction constraints that would gut the international product.

The system also iterates. MOOv2 was a direct response to the proposal-spam era and measurably cut premature resolutions. The language model pipeline and evidence bots were responses to speed and quality complaints. Bond sizes, challenge windows, and proposer sets are all tunable parameters, and Risk Labs has shown willingness to tune them under pressure. Whether tuning can fix a voting-power concentration problem is the open question, since the DVM backstop itself is the part no parameter change reaches.

And there is a structural argument: for a venue whose regulatory story leans on decentralization, outsourcing truth to an external token-holder process is a feature. Polymarket does not decide outcomes, and that sentence has legal value. The company’s answer to the United States market was not to change the oracle but to split the product, running the domestic venue through a CFTC-regulated framework while the international book kept UMA. The two-track structure is itself a verdict on where each settlement model belongs.

The rival designs

The dispute wave has made resolution architecture a competitive battleground, and three alternative models are now live at scale.

Deterministic validator settlement. Hyperliquid’s HIP-4 outcome markets, live since May 2026, remove the token vote entirely. Settlement runs through the chain’s validator set executing automated resolution against pre-specified objective data sources: no dispute window, no escalation, no path for a market participant to vote on a market. The constraint is scope, since deterministic settlement only fits questions with clean data sources, which is why the first HIP-4 contracts are Bitcoin price thresholds. Our companion guide to HIP-3 and HIP-4 covers the full design, and the market has been pricing Hyperliquid’s prediction market ambitions since the February announcement.

Regulated clearing. Kalshi reaches finality through the opposite architecture: a centralized exchange clearinghouse, registered with the CFTC as a derivatives clearing organization since August 2024, resolving markets under rules filed with a federal regulator and publishing results on-chain through Pyth and RedStone. Disputes go through exchange procedures, not token votes. The model trades decentralization for accountability, and its structured markets rarely face the ambiguity problems that plague open-ended questions. Polymarket’s separate United States venue, itself a CFTC-registered designated contract market that did $3.04 billion in June, follows the same regulated path, while the international venue still settles through UMA.

Purpose-built feeds. For objective, high-frequency questions, oracles built for prices work fine, and Polymarket already uses Chainlink to settle its fast crypto price markets, where no public discourse about the answer is needed. FIFA’s own licensed prediction market partner for the World Cup runs on Chainlink infrastructure, part of the tournament’s broader crypto buildout. Further out, web proof systems could let a resolution cite a cryptographically verified source document instead of a screenshot, a use case covered in our zkTLS explainer.

History adds a warning label to all of it, because decentralized resolution has been tried before and the graveyard is instructive. Augur, the sector’s first major attempt, launched in 2018 with REP token staking where reporters earned by landing with the consensus outcome, and the platform learned quickly that rewarding agreement with the majority is not the same as rewarding truth, especially once invalid and ambiguously worded markets entered the mix. Omen outsourced disputes to Kleros, a decentralized juror court whose participants were likewise paid for voting with the crowd, and inherited the same incentive plus slow rulings and heavy gas costs. Both platforms also discovered that resolution is a liquidity problem in disguise: traders avoid venues where the payout rules feel lottery-shaped, so unreliable settlement starves the order books that make prediction markets useful at all. Every resolution design since is a wager about which failure mode is most tolerable: token capture, institutional discretion, or narrow scope.

What traders should actually check

Resolution risk is checkable before entry, and the checklist is short.

Read the resolution criteria as literally as a hostile lawyer would, because the oracle will. The Strategy market turned on exact wording and an exact cutoff. If the criteria name a specific source, that source is the truth regardless of what every news outlet reports. Check the venue’s settlement path: UMA-resolved international Polymarket, a CFTC clearinghouse, a validator-settled chain, and a Chainlink price feed are four different risk profiles wearing the same Yes and No interface. Prefer markets with objective, single-source answers when size matters, since ambiguity is the raw material of every resolution scandal. And in a disputed market, watch the UMA vote rather than the news cycle, because the vote is what pays.

Two habits separate professionals from tourists here. The first is position sizing by resolution clarity: the same trader who is comfortable with six figures on a rate decision, where the source is official and the answer binary, keeps ambiguous cultural or political wording to entertainment-sized stakes. The second is tracking the dispute docket itself. Markets with pending UMA votes, and the wallets voting in them, are public on-chain information, and the recurring names in contested rulings are known to anyone who looks. In a system where the referee list is visible, not reading it is a choice.

One more number worth holding in mind: UMA’s entire token traded around a $63 million market capitalization earlier this year, while the markets it settles cleared billions per month. The economic security of a token-voted oracle is bounded by the cost of acquiring the tokens, and that ratio is the quiet argument behind every alternative design now gaining ground.

Truth as infrastructure

Prediction markets are routinely praised as truth machines, better than polls and faster than newsrooms. The praise is half-earned. Prices aggregate beliefs brilliantly, but the settlement layer decides which beliefs get paid, and that layer is built from bonds, challenge windows, token votes, clearinghouse rules, and validator scripts, each with a distinct way of being wrong. The sector’s next phase will be decided as much by resolution engineering as by volume, because traders forgive losing on the outcome and do not forgive losing on the ruling. The machinery for deciding truth is now a product category of its own. It deserves to be read as carefully as the odds.

Frequently asked questions

How does Polymarket decide who won a market?

Polymarket’s international venue outsources resolution to UMA’s Optimistic Oracle. After an event, an approved proposer submits the outcome with a $750 USDC bond, and a two-hour challenge window opens. If nobody disputes, the market settles on that answer, usually within two to four hours. If a dispute lands, UMA token holders vote through the Data Verification Mechanism, and their ruling is final.

What is UMA’s optimistic oracle?

It is an oracle protocol by Risk Labs for bringing arbitrary real-world facts on-chain. It is called optimistic because proposed answers are assumed true unless challenged during a dispute window, with bonds and rewards making honesty profitable and false proposals costly. Around 99% of assertions since 2021 have gone undisputed, and contested cases escalate to a token-holder vote.

What happens when a Polymarket resolution is disputed?

The disputer posts a bond matching the proposer’s, and the question escalates to UMA’s Data Verification Mechanism. UMA token holders research the question and vote, with rewards for voting with the final outcome and penalties for missing or voting against it. The losing side’s bond pays the winning side. Disputes stretch resolution from hours to days, and the DVM ruling cannot be appealed.

Why is UMA’s system controversial in 2026?

Concentration and conflicts. A Wall Street Journal investigation found most disputed markets saw over half their votes come from the ten largest wallets, and about one in five disputes included a voter holding a position in the market being judged. More than 1,150 markets were disputed in the first five months of 2026, and a $60 million market on a Strategy Bitcoin sale resolved against a documented regulatory filing.

What was the Strategy Bitcoin market dispute?

A Polymarket contract asked whether Strategy would sell any Bitcoin by May 31, 2026. A June 1 regulatory filing showed the company sold 32 BTC between May 26 and May 31, inside the window. The resolution was challenged twice, went to a UMA token vote, and the market resolved No anyway. The episode became the leading exhibit in the argument against token-voted settlement.

What is MOOv2?

The Managed Optimistic Oracle V2, deployed in November 2025, restricted resolution proposals to 37 pre-approved addresses with strong accuracy records while keeping disputes open to everyone. Paired with language model automation that drafts proposals for fractions of a cent and bots that summarize evidence, it cut spam proposals and sped up routine settlement without changing the token-vote backstop.

How do Kalshi and Hyperliquid settle markets differently?

Kalshi resolves through its CFTC-registered clearinghouse under federally filed rules, then publishes results on-chain via Pyth and RedStone, with disputes handled by exchange procedure. Hyperliquid’s HIP-4 uses deterministic settlement by the validator set against pre-specified data sources, with no dispute window at all. Neither involves a token vote, and both are positioned as answers to UMA’s governance risk.

Can a prediction market resolve incorrectly and stay that way?

Yes. DVM rulings are final, and Polymarket has honored controversial outcomes rather than overriding the oracle. The practical defenses are all pre-trade: read the resolution criteria literally, check which settlement system the venue uses, prefer objectively verifiable questions for larger positions, and treat ambiguous wording as a risk factor priced into the odds.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 3, 2026.

The biggest sporting event on Earth has become the biggest liquidity event in prediction market history. Billions in tournament volume, a $45 billion June across the sector, one very expensive longshot trap, and a CFTC probe arriving right on schedule.

Summary

- Polymarket processed about $5 billion in World Cup trading as the tournament drove prediction market volumes to record highs across the sector.

- The expanded World Cup format and deeper liquidity pushed crypto based event markets into mainstream scale while attracting a large wave of first time users.

- The surge in activity also brought regulatory scrutiny and raised questions over whether the new liquidity will remain after the tournament concludes.

Four years ago, during the Qatar World Cup, Polymarket processed a grand total of $138,000 in tournament bets. That is not a typo missing some zeros. One hundred thirty-eight thousand dollars, roughly the price of a nice car, across the entire biggest sporting event on the planet.

This summer, the same platform blew through $5 billion in World Cup trading before the knockout rounds finished forming, with tournament totals now estimated around $6.4 billion and climbing. The flagship winner market alone has turned over more volume than many mid-cap tokens see in a month. Across the whole prediction market sector, June closed at $44.8 billion in combined monthly volume, a 75% jump from May, and Bernstein analysts project World Cup wagering could top $10 billion by the July 19 final at MetLife Stadium. Measured against its own 2022 self, Polymarket’s World Cup business grew by a factor of more than forty thousand.

Something changed between Qatar and now, and it was not football. The 2026 tournament has become the moment crypto-native prediction markets stopped being a curiosity and started operating at the scale of the industries they intend to eat. It has also, in the same six weeks, exposed exactly where the model creaks: a longshot problem hiding $1.6 billion of dubious positioning, a regulatory net closing from two directions, and an open question about what happens to all this liquidity on July 20.

The numbers, and why they are absurd

The tournament kicked off on June 11 with a format built for market makers: 48 teams instead of 32, 104 matches instead of 64, three host countries, and a brand-new Round of 32 that added an extra layer of binary, elimination-stakes events. Every match is a market. Every market is several: winner, draw, total goals, advancement. The expanded format nearly doubled the tradeable surface area of the world’s most-watched event.

The results by the numbers:

- Polymarket’s World Cup-linked contracts passed $2 billion in the group stage, $3.3 billion days later, and roughly $6.4 billion at the latest count, against $138,000 for the entire 2022 tournament.

- Kalshi, the CFTC-regulated rival, processed about $7.4 billion in World Cup trades, more than its entire March Madness, with its flagship winner market alone drawing over $832 million.

- Combined June volume across Kalshi, Polymarket, and Polymarket’s new US-regulated exchange hit $44.8 billion, up 75% from May’s $25.66 billion. Kalshi grew 87% month over month to $31.5 billion; Polymarket did $14 billion across both venues, including $3.04 billion on the US platform.

- Weekly sector volume peaked at a record $14.5 billion, with open interest holding at a record $1.6 billion for three consecutive weeks. Kalshi’s open interest alone crossed $1.16 billion.

- Reports put Polymarket’s revenue run-rate at $1 billion annualized on World Cup flow.

Individual matches show how deep the liquidity runs. A group-stage fixture between Algeria and Austria, two mid-tier footballing nations, drew $2.82 million. England versus Panama drew $1.76 million even though Panama arrived as the weakest side in the field and left without scoring a goal. Even Paraguay versus Australia, a match with all the global glamour of a Tuesday, cleared $329,000. When dead rubbers between minnows clear six figures, the order book is no longer a novelty. It is a market with depth at every rung of the attention ladder, which is exactly what market makers need before committing balance sheet.

Pricing on the big question has stayed remarkably stable through the chaos. France leads the winner market at roughly 23% to 24% implied probability, with Argentina at 20% to 21%, a rematch scenario the finalist markets take seriously: France at 39% and Argentina at 38% to reach the July 19 final. Argentina has drawn about $81 million in winner-market volume, France $77 million, Portugal $76 million, Spain $68 million, and England $61 million.

How the machine works, for the newcomers it just onboarded

Given how many of this tournament’s traders are first-timers, the mechanics deserve a plain-language pass, because they explain both the volume numbers and the regulatory fight.

A prediction market contract is a share that pays $1 if an outcome happens and nothing if it does not. France to win the World Cup trading at 24 cents means the market assigns France a 24% implied probability; buy at 24 cents and a French title returns $1 per share. Prices move with news, form, and money flow exactly like any order book, and because every share is a token settling on-chain, positions trade continuously until resolution. Polymarket runs on Polygon with markets denominated in USDC, and outcomes resolve through an oracle process, with the UMA optimistic oracle as the traditional backstop where disputes over real-world results get adjudicated by token-holder vote. Kalshi runs the same economic structure through a CFTC-regulated exchange with dollars instead of stablecoins.

The tradability is the entire difference from a sportsbook, and it is why volume comparisons flatter prediction markets. A bettor who backs France at a book locks the position until the final; a Polymarket trader might turn the same conviction over dozens of times, buying strength, selling wobbles, rotating into match markets and back. High turnover on stable open interest, precisely Polymarket’s tournament signature, is the fingerprint of trading behavior layered on top of betting behavior. It also means the platforms earn their status as information machines honestly in one respect: continuous two-sided pricing on live global events, updating in seconds, visible to anyone. During the group stage, Polymarket priced a draw as the most likely single outcome in Paraguay versus Australia at 42.5% while traditional books had Paraguay clearly favored, the kind of public disagreement between market structures that quants notice and harvest.

From election-night stunt to billion-dollar business

The tournament did not create Polymarket’s scale from nothing. It compounded an arc three cycles in the making.

The platform’s first mainstream moment came with the 2024 US election, when its presidential market became a media fixture and its pricing beat several polling aggregates to the result. That visibility arrived with a compliance hangover: Polymarket had operated outside US jurisdiction since a 2022 CFTC settlement barred it from serving American users, and the election spotlight brought raids, investigations, and a long regulatory negotiation. The resolution came in 2025, when the platform acquired a regulated derivatives venue and resumed limited US operations through a compliant exchange, the entity now posting $3.04 billion monthly volumes as Polymarket US.

Kalshi ran the mirror-image path: US-regulated from birth, it fought the CFTC in court for the right to list election contracts, won, and then leveraged the precedent into sports-adjacent event contracts that state gaming regulators now contest. Its reported $1 billion funding round earlier in 2026 and its $31.5 billion June say the strategy found product-market fit at scale.

The World Cup is the first event both platforms entered at full institutional strength, regulated venues live, market-maker relationships mature, mobile products polished, and the $45 billion June is what that maturity looks like when the biggest audience on Earth shows up. For perspective on how completely the sector has outgrown its origins: the entire prediction market industry’s 2022 World Cup handle would not cover thirty seconds of this tournament’s average volume.

The longshot trap: $1.6 billion of hope

Underneath the headline volume sits the tournament’s strangest statistic, and the one that says the most about who is actually trading. Roughly $1.6 billion, a quarter or more of Polymarket’s World Cup total, has been wagered on teams priced at 1% implied probability or less.

Think about what that means. Traders have committed nine figures to the proposition that sides the market gives essentially no chance will lift the trophy. Some of that is rational lottery-ticket buying, one-cent shares that pay a hundredfold if the miracle lands. Some is liquidity provision and hedging that looks stranger in aggregate than it is in detail. But a large share is the oldest pattern in betting: retail money chasing the thrill of the impossible payout, in a venue where the thrill is dressed up as trading.

Prediction market advocates have spent years arguing these venues are information machines, truth engines that price reality better than pundits. The longshot trap complicates the pitch. Markets in which a quarter of the money sits on near-impossible outcomes are not purely information machines. They are also entertainment products, and entertainment money behaves differently: it arrives for the event, it does not shop for edge, and it leaves when the confetti drops. Both things can be true at once, the sharp pricing at the top of the book and the lottery counter at the bottom, but the ratio between them decides what these platforms are when the World Cup is not on.

The user data leans the same direction. A Bitget Wallet study of 857,000 active Polymarket users found 60% had no prior on-chain trading history of any kind. Prediction markets are onboarding people crypto never reached, an achievement by any adoption metric, and those people are arriving to bet on football, not to discover decentralized finance.

What the tournament proved about the rails

Strip out the froth and the infrastructure story is the strongest one here. Positions on Polymarket are tokens settling on-chain via Polygon, which means the tournament has doubled as a live stress test of whether blockchain rails can host institutional-scale event trading. The answer, six weeks in, is yes. You can buy France at 24% today, watch a shaky quarterfinal drop the price, and sell before the next whistle. Positions are tradeable instruments with a live order book, not slips waiting for settlement, and the distinction is precisely why turnover figures dwarf what a sportsbook handle would show for the same interest.

The flow data show the two market leaders running different races. Polymarket’s open interest has held roughly flat while volume spiked, the signature of heavy turnover, traders rotating in and out around every match. Kalshi’s open interest has climbed steadily, pointing to stickier positioning from a user base that skews more institutional and holds through events. Kalshi also entered the tournament with a war chest, having closed a reported $1 billion funding round earlier in 2026, and its $31.5 billion June says the money is being put to work against sportsbooks as much as against Polymarket.

Competition is arriving from inside crypto too. World, a Solana-based prediction market, went live inside the Phantom wallet during the tournament, using Chainlink oracles and taking direct aim at the duopoly, while ADI Predictstreet operates as FIFA’s own first official prediction market partner. The sector that spent 2024 as an election-night curiosity now has a governing-body partnership, a regulated US exchange, and venue competition on three chains. That maturation is happening alongside the industry’s broader mainstream moment at this tournament, with Kraken serving as FIFA’s first official crypto exchange partner across the same six weeks, a deal we examine in full in a companion feature.

Six weeks of price discovery, match by match

The aggregate numbers hide the part traders actually enjoyed: watching the market metabolize a football tournament in real time.

The favorites’ pricing barely moved through six weeks of chaos, France oscillating between 23% and 24% and Argentina between 20% and 21%, a stability that says the market treated group-stage drama as noise around strong priors. The action was in the tails and the match markets. Cape Verde drawing with both Spain and Uruguay to escape Group H repriced an entire bracket path in minutes. DR Congo reaching their first knockout stage since 1974 sent their sub-1% title shares on the kind of hundredfold percentage ride that longshot buyers live for, right up until Harry Kane ended it with two goals in the final fifteen minutes. Panama, priced as the group’s doormat, performed exactly to market: three losses, zero goals, and $1.76 million traded on the England fixture anyway, proof that liquidity follows attention rather than quality.

The draw markets produced the tournament’s most interesting structural signal. Prediction market traders repeatedly priced draws as the most likely single outcome in tight fixtures, 42.5% in Paraguay versus Australia, 46.5% in Algeria versus Austria, while traditional books held moneyline favorites. Two market structures, two different opinions about the same ninety minutes, and a standing arbitrage question for anyone with accounts on both. Group-stage match markets settled into a reliable $500,000 to $2 million volume band regardless of the teams involved, which is the statistic that best captures what changed: four years ago, the entire tournament did $138,000; now that is a slow first half.

The quiet winners underneath the order book

Every trade in this boom runs on infrastructure that predates it, and the tournament has been a revenue and relevance event for the stack beneath the platforms.

Polygon carries Polymarket’s settlement, which means tens of millions of tournament transactions and billions in USDC transfer volume ran through a network that spent two years searching for a flagship consumer use case and found one wearing football boots. Circle benefits wherever the collateral pool grows, since every open position is USDC sitting on-chain. Chainlink’s oracle infrastructure gained a governing-body endorsement through ADI Predictstreet, FIFA’s own first official prediction market partner, and powers World, the Solana prediction market that launched inside Phantom mid-tournament to contest the duopoly on faster rails, one more front in the widening execution-layer contest between Solana and Ethereum. Even the losers of the platform war stand to inherit something: liquidity programs, market-making firms, and resolution tooling built for this tournament become sector infrastructure that any new entrant can rent.

That is the pattern worth filing away. Prediction markets have become the rare crypto vertical whose growth mechanically feeds the base layers underneath it, stablecoin float, L2 throughput, oracle demand, without requiring anyone to believe a new narrative. The World Cup did not just make Polymarket bigger. It made the case that event markets are a durable consumer category for the chains that host them, which is why Solana wants in and why the next cycle of this fight will be fought partly on infrastructure costs.

The real opponent is DraftKings, not each other

Frame the tournament as Polymarket versus Kalshi and you miss the actual contest. The $2 billion-plus that crypto prediction markets processed in World Cup contracts is being measured in real time against sportsbook scale, and the next four weeks decide whether the platforms keep that capital or hand it back to DraftKings and FanDuel when the novelty fades.

The traditional books still dwarf the challengers on absolute handle; US regulated sportsbooks process tens of billions per year on football alone, with decades of brand, state licenses, and parlay products engineered for maximum hold. What prediction markets attack is the margin structure. A sportsbook builds roughly 4% to 6% vig into a standard two-way line and far more into parlays; a prediction market charges the spread plus small fees, with two-sided order flow compressing costs toward exchange levels. For a sharp bettor, the difference between negative-5% expected value at a book and near-zero at an exchange is the difference between a hobby and a career, which is why professional money migrated first.

The Mexico versus England Round of 16 fixture made a clean case study: a high-attention knockout tie where Polymarket’s pricing stayed tight under both retail flood and institutional size, the market-maker backbone absorbing volume without spreads blowing out. Passing liquidity tests like that, repeatedly, on the sport’s biggest stage, is how an exchange steals a customer segment that never comes back to paying vig. The books know it; their lobbying against event-contract sports markets in state legislatures is the sincerest compliment the sector has received.

The structural irony is that prediction markets may win the comparison while losing the framing. The more their World Cup product resembles a better-priced sportsbook, the stronger the state regulators’ argument that it is one.

The regulators arrive at the party

A $5 billion-plus event was always going to draw the state’s attention, and it has, from two directions at once.

The federal track came first: the Wall Street Journal reported the CFTC has opened an investigation into Polymarket, landing just as the platform’s volumes peaked and barely a year after it resumed limited US operations through its regulated exchange. The probe’s scope remains unclear, which in practice means everything from market manipulation surveillance to the perimeter question of which event contracts count as legitimate derivatives.

The state track is broader. More than a dozen state-level authorities have taken legal action against Kalshi and Polymarket, accusing them of offering unlicensed sports betting to residents. The legal theory war here is existential for the sector: if a World Cup winner contract is a financial derivative, the CFTC owns it and federal preemption shields the platforms; if it is a sports bet, thirty-plus state gaming commissions get a vote, and the compliance map fragments overnight. Consumer protection advocates have pushed the second reading hard, and the tournament’s own success is their best exhibit. It is difficult to argue that $1.6 billion of one-percent longshots is hedging activity.

The jurisdictional map adds a third layer of mess, because this World Cup spans three host countries with three different rulebooks. American users navigate the federal-versus-state fight described above. Canadian provinces run their own gaming monopolies with their own views on event contracts. Mexican users face a framework that barely contemplates the product category at all. A tournament marketed as borderless is being traded through one of the most fragmented compliance environments in consumer finance, and every platform’s growth team is effectively running fifty different products wearing one interface.

The platforms are betting that regulated structure wins the argument, and the irony is thick enough to trade: prediction markets are now the subject of the kind of binary, high-stakes, externally resolved event they would normally list. Traders being traders, they occasionally do list it. The outcome will land on an industry already conditioned by this cycle’s macro whiplash, where risk assets have traded like leveraged tech exposure and volume booms have repeatedly decoupled from underlying token prices.

The question that matters: July 20

Every liquidity boom tied to a calendar event carries the same asterisk, and this one expires at full time on July 19.

The bear case writes itself. Fan-adjacent crypto products have a documented post-tournament decay pattern; volumes tied to the Qatar cycle collapsed within weeks of the final. If June’s $44.8 billion was mostly football, July’s number tells us so immediately, and the sector’s valuation narratives, including that billion-dollar Polymarket run-rate, deflate with it. Sixty percent of those 857,000 users have no other on-chain footprint to return to. They came for the World Cup. The World Cup ends.

The bull case is quieter but has data behind it. The June figures functioned as a stress test, and the infrastructure passed: record open interest held for three straight weeks, spreads on marquee matches stayed tight under institutional size, and non-sports volume across Kalshi and Polymarket reached $3.6 billion during the same window, meaning roughly a third of the boom had nothing to do with football at all. Elections, Fed decisions, crypto prices, and cultural events all inherited liquidity and market-making muscle built for the tournament. If even a modest fraction of the new cohort stays, the World Cup becomes the sector’s customer-acquisition event of the decade, acquired at zero marketing cost.

The honest position is that nobody knows the retention number, and the retention number is the entire question. What the tournament has already settled is capacity: prediction markets can absorb global-event liquidity at sportsbook scale on crypto rails without breaking. Whether they can keep it is the trade still open on the board.

Full time approaches

The 2026 World Cup will crown a champion at MetLife Stadium on July 19, and the winner market says it will probably be France or Argentina, though a combined $1.6 billion in longshot money is praying otherwise. For the prediction market industry, the trophy has arguably been lifted already: a forty-thousand-fold improvement on its 2022 self, a June that redefined the sector’s ceiling, and proof that on-chain event trading can operate at the scale of the businesses it wants to replace. The costs of that visibility, a federal probe, a state-by-state legal siege, and a user base of unknown loyalty, all come due in the quiet weeks after the final whistle. The tournament turned Polymarket into a $5 billion market. The off-season decides whether it stays one.

Disclaimer: This article is for informational purposes only and does not constitute investment or betting advice. Prediction markets carry significant financial and regulatory risk, and availability varies by jurisdiction. Always do your own research. Information current as of July 3, 2026.

President Donald Trump has denied knowing about the at least $1.4 billion in crypto income disclosed in his latest financial filing, while defending both his personal gains and his family’s involvement in the digital asset industry.

Summary

- Donald Trump said he was unaware of the at least $1.4 billion in crypto income disclosed in his latest financial filing.

- The disclosure attributes most of the earnings to licensing deals tied to the TRUMP meme coin and WLFI token sales.

- Trump renewed his call for U.S. crypto leadership as the CLARITY Act faces political and ethics-related hurdles in Congress.

According to a CNBC interview, Trump said he was unaware of the amount of money generated from his crypto ventures, adding that he could know if he wanted to and insisting there was nothing illegal about such earnings. His comments came after the release of his 2025 financial disclosure, which has renewed scrutiny over potential conflicts of interest tied to his family’s crypto businesses.

The financial disclosure, released earlier this week, showed that Trump earned at least $1.4 billion from cryptocurrency-related activities during the reporting period. The filing attributed most of the income to licensing agreements connected to the Official Trump (TRUMP) meme coin and token sales conducted by Trump-backed World Liberty Financial (WLFI).

Earlier, as reported by crypto.news, Trump responded to questions about the disclosure by pointing to gains from the stock market rally but did not address the crypto-related income. His latest remarks are the first direct comments on the digital asset earnings disclosed in the filing.

Financial disclosure renews scrutiny of Trump’s crypto interests

The disclosure has again drawn attention to the Trump family’s expanding presence in the cryptocurrency sector. Critics have previously argued that the family’s business interests could create conflicts while Trump serves as president, particularly as his administration continues to shape U.S. digital asset policy.

Separate criticism has also focused on the launch of the TRUMP and MELANIA meme coins, with opponents alleging the projects extracted liquidity from retail investors. Meanwhile, WLFI, the native token of World Liberty Financial, was also introduced last year. All three tokens remain well below their respective all-time highs following strong declines after launch.

Despite the criticism, Trump maintained in the CNBC interview that there was nothing improper about benefiting from crypto investments. He did not indicate that he planned to distance himself or his family from their digital asset ventures.

Trump continues to push for U.S. crypto leadership

Alongside his comments on the disclosure, Trump repeated his view that the U.S. must remain the global leader in cryptocurrency development. During the interview, he argued that failing to take the lead could allow countries such as China or Japan to dominate what he described as a very large industry.

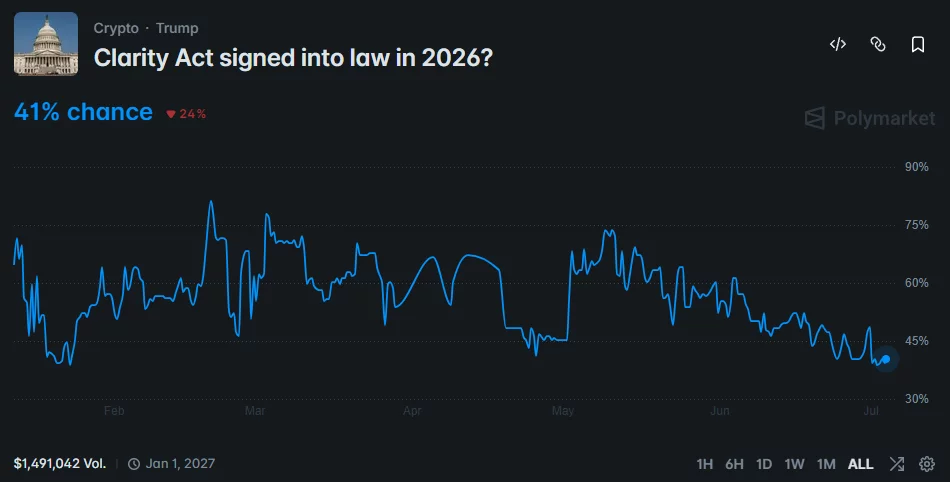

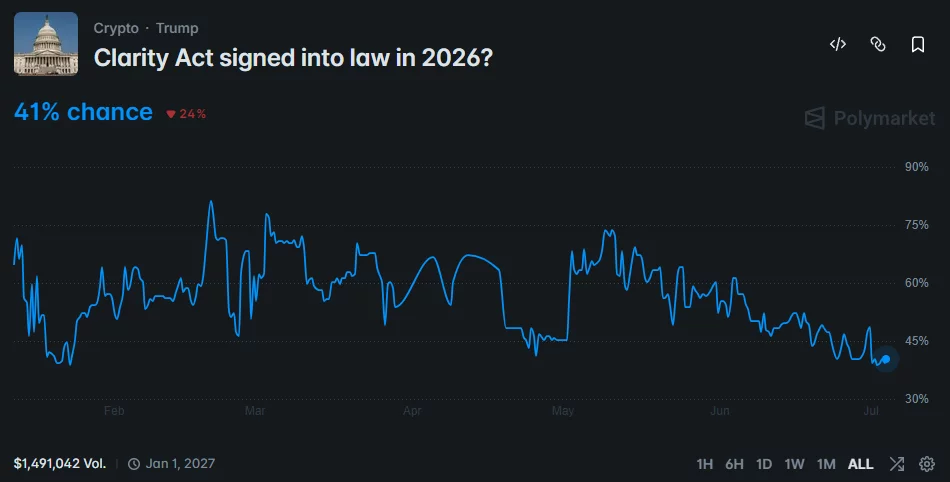

The president has repeatedly linked that position to his administration’s plan to make the United States the global center for digital assets. As part of that effort, he has urged lawmakers to approve the CLARITY Act, legislation designed to establish a clearer regulatory framework for the crypto industry.

Even so, the bill faces growing political uncertainty. According to prediction market platform Polymarket, traders currently assign a 41% probability that Trump will sign the CLARITY Act into law before the end of the year.

Ethics concerns surrounding Trump’s financial interests in cryptocurrency remain one of the main obstacles cited by Democratic lawmakers. With the Senate expected to begin its August recess in the coming weeks, the legislation now faces a narrowing window to advance through Congress before lawmakers leave Washington.

The CLARITY Act has regained momentum after Senator Bill Hagerty outlined a revised Senate timeline that points to floor action after lawmakers return from the July recess.

Summary

- Bill Hagerty said the Senate could release the final CLARITY Act text this weekend before a post-recess vote.

- Bloomberg Intelligence now estimates the bill has about a 60% chance of passing this month.

- NOBLE backed the legislation, while the DOJ disputed claims that it would weaken crypto crime enforcement.

According to reports citing Senator Bill Hagerty, the U.S. Senate is expected to publish the final text of the CLARITY Act this weekend, giving lawmakers and the digital asset industry their clearest look yet at the legislation before debate resumes.

The updated schedule has replaced earlier expectations of a July 4 signing, with Hagerty indicating that a Senate vote is more likely after Congress reconvenes on July 13.

Although the timetable has slipped, political support for the bill has continued to grow. Bloomberg Intelligence recently estimated that the probability of the CLARITY Act passing this month has risen to about 60%, adding to optimism among crypto market participants awaiting a federal market structure framework.

Senate schedule now points to a post-recess vote

Hagerty’s latest comments have shifted attention from an immediate vote to the legislative process expected later this month. Before the Senate can consider the measure, lawmakers are expected to review the final legislative text, which could clarify several provisions that have attracted debate in recent weeks.

Passing the bill will still require at least 60 votes in the Senate. Republicans currently hold 53 seats, meaning the legislation cannot advance without support from several Democrats. During committee consideration, Democratic Senators Angela Alsobrooks and Ruben Gallego voted in favor of the bill, although both later said their committee votes should not be interpreted as commitments to support the legislation on the Senate floor.

Time also remains a factor. As previously reported by crypto.news, the Senate has limited floor time before its August recess, making the period after lawmakers return on July 13 particularly important. If the bill fails to advance during that window, its next realistic opportunity could slip into 2027.

Support from NOBLE strengthens the bill’s position

Alongside the revised timeline, the legislation has gained support from new constituencies. Senator Tim Scott recently argued that businesses innovate more effectively when operating under predictable regulatory rules.

Scott said the CLARITY Act would establish clear standards for digital assets, improve consumer protections, and help keep financial innovation in the U.S.

Another notable endorsement came from the National Organization of Black Law Enforcement Executives (NOBLE), which became the first major law enforcement organization to publicly back the CLARITY Act, including the Blockchain Regulatory Certainty Act provisions contained in Section 604.

NOBLE’s position differs from concerns previously raised by four U.S. law enforcement organizations, which argued that Section 604 could make investigations into crypto-related financial crime more difficult by preventing certain non-custodial developers and software providers from automatically being treated as money transmitters. Supporters of the provision have maintained that developers who never control customer assets should not be regulated like financial intermediaries.

The debate expanded after the U.S. Department of Justice disputed claims that the legislation would create major enforcement gaps. As previously reported by crypto.news, the DOJ said criticism of the bill’s law enforcement provisions was inaccurate.

In its endorsement letter, NOBLE similarly argued that the legislation would not weaken existing federal criminal authorities covering money laundering, unlicensed money transmission, sanctions violations, conspiracy, and related offenses.

Industry groups have also continued lobbying lawmakers ahead of the Senate’s return. Stand With Crypto recently urged supporters to contact senators and push for a vote once Congress reconvenes.

The organization argued that prolonged delays could encourage crypto companies, investment, and jobs to move outside the U.S. while the country waits for clearer digital asset regulations.

Standard Chartered has secured a MiCA passport as the European Securities and Markets Authority has added 57 newly authorized crypto firms to its register following the end of the EU’s transition period.

Summary

- ESMA has expanded its MiCA register to 300 authorized crypto firms after approving 57 new providers.

- Standard Chartered and FalconX have secured MiCA licenses, gaining passporting rights across all 27 EU member states.

- The July 1 MiCA deadline has reshaped the EU crypto market, with only licensed firms allowed to serve new customers.

According to the European Securities and Markets Authority (ESMA), its latest interim register now lists 300 authorized crypto-asset service providers, up from 243 on June 26, after a wave of approvals arrived around the July 1 Markets in Crypto-Assets deadline.

The updated list includes major banks, institutional trading firms, and digital asset companies that can now offer regulated services across the European Union under a single authorization.

Standard Chartered joins expanding MiCA register

Among the biggest additions is Standard Chartered, which received MiCA authorization from Luxembourg’s financial regulator, the Commission de Surveillance du Secteur Financier (CSSF), on June 25.

The bank also obtained an Electronic Money Institution license, allowing it to use MiCA’s passporting system to provide crypto services throughout all 27 EU member states without seeking separate approvals in each country.

Institutional crypto trading firm FalconX also entered the register after receiving authorization from Malta’s Financial Services Authority shortly before the July 1 deadline.

ESMA’s latest update further added digital asset bank Sygnum Europe, Ronin EM, and CACEIS, the asset servicing business owned by Crédit Agricole and Santander.

Separately, crypto.news recently reported that CACEIS is in exclusive talks to acquire French crypto investment platform Meria, a deal that would add a retail crypto business with about 150,000 users and roughly €350 million in assets under management. The reported discussions followed Meria’s own MiCA CASP authorization in France.

Recent approvals have also extended beyond traditional financial institutions. As crypto.news previously reported, Stripe-owned Bridge secured both MiCA CASP authorization and an Electronic Money Institution license in Luxembourg, enabling the company to provide regulated crypto services across the European Union under the same passporting framework.

MiCA deadline has reshaped Europe’s regulated crypto market

The surge in approvals followed the end of MiCA’s transitional period on July 1, 2026. During that grace period, crypto companies already operating in individual EU countries could continue serving customers while applying for full authorization.

With the transition now complete, firms that failed to obtain a MiCA license must stop onboarding new customers and begin winding down regulated operations within the bloc. ESMA’s updated register provides public confirmation of which providers have completed the authorization process.

MiCA establishes a single regulatory framework covering crypto exchanges, custody providers, portfolio managers, and crypto-asset issuers across the European Union. Under its passporting rules, authorization from one national regulator, such as Luxembourg’s CSSF or Malta’s MFSA, gives firms access to customers across the entire bloc.

The new regulatory environment has already produced visible market changes. As crypto.news reported, Tether’s $186 billion USDT no longer has a MiCA-compliant route to remain on regulated EU exchanges following the July 1 deadline.

Consequently, MiCA-authorized exchanges including Coinbase, Kraken, and Crypto.com have removed USDT trading for European users, ending the stablecoin’s presence on regulated order books despite remaining the world’s largest stablecoin by market capitalization.

For institutional investors and asset managers, ESMA’s expanding register now offers a verified reference point for identifying regulated counterparties operating under the European Union’s unified crypto framework, while passporting continues to reduce the need for firms to secure separate licenses in each member state.

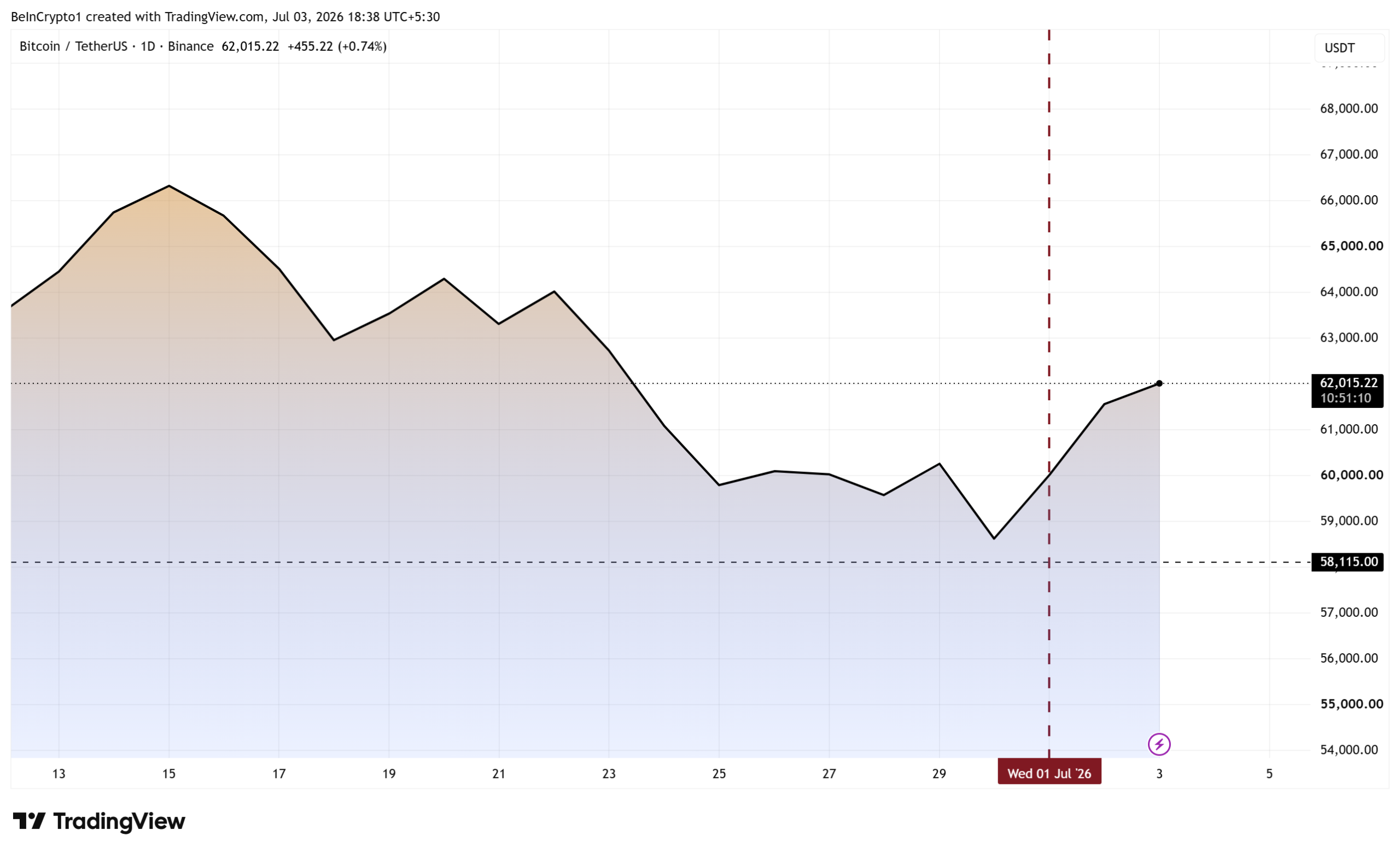

Speculation about another Bitcoin sale from MicroStrategy intensified after an unconfirmed on-chain transfer showed 491 BTC leaving a company-linked wallet on July 1. Neither MicroStrategy nor its Executive Chairman, Michael Saylor, has confirmed any sale.

The rumor spread across X (Twitter) on Friday. Meanwhile, Bitcoin (BTC) traded higher after July 1, suggesting the market easily absorbed the alleged transaction.

Did Saylor Sell More Bitcoin?

Pseudonymous trader Light flagged the transfer, worth roughly $30 million at current prices. That equals just 0.058% of the 847,363 BTC Strategy reported in its latest SEC disclosure. The stack covers about 4% of bitcoin’s 21 million coin supply.

The timing explains the attention. Strategy adopted a Bitcoin monetization framework plan on June 29, authorizing up to $1.25 billion in tactical sales to fund dividends and buybacks. Its raised 12% STRC preferred dividend took effect on July 1, the same day as the alleged transfer.

The company also completed its first Bitcoin sale since 2022 in late May, offloading 32 BTC to cover preferred stock dividends. Its only earlier sale came in December 2022.

Back then, it sold 704 BTC for $11.8 million to harvest tax losses, then repurchased 810 BTC within days. It had already been rebuilding its cash reserves this year while slowing new purchases.

“Michael Saylor’s Strategy may have just sold 491 BTC on July 1st. The transaction hasn’t been confirmed yet, but if true, this would be one of the first signs of Strategy reducing its Bitcoin position after years of “never sell” narratives…” analyst Crypto Rover amplified the claim in a post.

Follow us on X to get the latest news as it happens

Bitcoin Shrugs Off the Sale Speculation

Bitcoin showed little stress. The coin opened at $61,492 on Friday, up 2.5% from Thursday, and traded for $62,016 as of this writing, up by 1.35% in the last 24 hours. With this, the pioneer crypto is up by over 7% from the July 1 low of $57,800.

The strength tracked a weak June jobs report rather than treasury headlines. It extends a fragile Bitcoin price recovery after the worst month for prices in four years.

Reactions on X (Twitter) split between traders calling the amount a rounding error and others warning repeated sales could sour sentiment.

The calm contrasts with JPMorgan’s recent warning that the new sales policy adds risk to the crypto market. Even so, a fully absorbed $30 million transfer suggests demand currently outweighs those concerns.

Confirmation now rests with Strategy’s own disclosures. The firm reported its May sale within days, so a filing this week would show whether the transfer was a sale, a custody move, or an internal shuffle.

The post MicroStrategy Reportedly Sold More Bitcoin, But Market Didn’t React appeared first on BeInCrypto.

Robinhood has emerged as a key platform in the rollout of the Trump Accounts program, with U.S. Treasury-backed child investment accounts scheduled to begin transfers ahead of the initiative’s July 4 launch.

Summary

- Robinhood is expected to help roll out the Trump Accounts program ahead of its July 4 launch.

- Eligible children will receive a $1,000 government contribution, with annual private contributions capped at $5,000.

- Trump also floated a possible SpaceX stock donation, though neither Elon Musk nor SpaceX has confirmed any plans.

According to information surrounding the program, Robinhood is expected to help facilitate the new accounts, which are designed to give eligible children access to long-term investment portfolios through federally supported savings accounts.

The transfer process is expected to open through the U.S. Treasury before the official launch, bringing brokerage firms into one of the administration’s newest financial initiatives.

Robinhood is expected to handle access to the new accounts

Under the program, children under 18 whose parents have a valid Social Security number will qualify for an account. The federal government will contribute an initial $1,000, while families and other approved contributors may add up to $5,000 per child each year through IRS Form 4547.

The framework brings together the U.S. Treasury, the Internal Revenue Service, brokerage firms responsible for custody, and retail investment companies that will offer account access. Although officials have not formally named Robinhood as the exclusive provider, the company is widely expected to play a central role in making the accounts available to eligible users.

Because Robinhood already combines stock investing with cryptocurrency trading in a single application, the arrangement could eventually allow users to manage government-backed investment accounts alongside their existing brokerage portfolios if regulators permit such functionality. The current Trump Accounts structure, however, does not include cryptocurrency investments or blockchain technology.

Speaking in an interview with CNBC’s Joe Kernen on Thursday, President Donald Trump also said he believes Elon Musk could contribute SpaceX stock to the Trump Accounts initiative, although he acknowledged he had not recently spoken with the billionaire.

Trump added that business leaders including Michael Dell and Micron have shown support for the children’s investment program. Neither Musk nor SpaceX has announced any plan to donate shares, leaving Trump’s comments as his expectation rather than a confirmed commitment.

Following those remarks, SpaceX ticker SPCX recovered from an intraday low near $155 to close about 3% higher at roughly $162 on July 3 as buyers returned after early selling pressure, as previously reported by crypto.news.

Regulators continue separating traditional investments from digital assets

While the accounts focus on conventional investment products, their launch comes as U.S. regulators continue defining the legal boundaries between securities and digital assets. The program adds another example of regulated custodial investment products becoming part of mainstream financial services, even though cryptocurrencies are not included in the current design.

Research previously published by Messari has identified retail investment applications as an important entry point for individuals investing in risk assets. If brokerages integrate the new accounts into existing investing platforms, regulated long-term investing could become more accessible to younger users through familiar financial apps.

The political backdrop surrounding the initiative remains active. As previously reported by crypto.news, President Trump’s 2025 financial disclosures showed at least $1.4 billion in crypto-related income tied to ventures including his memecoin and World Liberty Financial, prompting continued ethics discussions while lawmakers negotiate the CLARITY Act. Trump later denied knowledge of those earnings and said there was “nothing illegal” about them.

Although the Trump Accounts program currently excludes digital assets, brokerage participation and ongoing regulatory work could influence future discussions about how government-backed investment products and regulated digital asset offerings coexist within the U.S. financial system.

Solana’s SOL token climbed to a level not seen in more than 30 days, briefly trading around $83, and the move is drawing attention because it doesn’t look like a simple altcoin sympathy rally. Instead, market data points to a mix of rising tokenized-asset activity on Solana, renewed memecoin momentum, and improving flows tied to stablecoin liquidity.

The question now for traders is whether this renewed bid can push SOL back through the $90 area—or whether the market is already cooling off as leverage comes off the table. Recent derivative and on-chain indicators suggest enthusiasm may be more selective than it was earlier in the week.

Key takeaways

- SOL hit a 30-day high near $83, showing signs of decoupling from the broader altcoin market’s weakness.

- Tokenized trading activity on Solana accelerated as cumulative tokenized stock transfers surpassed $10 billion around June 23.

- Memecoins and prediction-market activity boosted short-term attention, but leveraged positioning cooled quickly.

- Futures annualized funding fell to about 3% on Friday from an 11% peak earlier, implying less appetite for chasing gains to $90.

Tokenized assets bring a new tailwind to Solana

One of the clearest narratives behind SOL’s strength is the renewed growth in tokenized asset activity on the Solana network. According to data referenced from RWA.xyz, Solana’s tokenized assets rose to a record-high $3.5 billion on Wednesday—up from $2.7 billion about one month earlier.

The same dataset also points to what’s driving that expansion. The article cites tokenization products related to corporate credit and market indexes such as the S&P 500 and the Nasdaq-100. In addition, RWA.xyz data shows Solana leading the tokenized industry by active addresses, with 294,274, compared with Ethereum’s 204,955.

On the “why it matters” side for investors and builders: when tokenized assets expand, it generally increases demand for on-chain infrastructure—settlement, custody, trading venues, and related DeFi rails. Even if tokenized flows don’t translate immediately into SOL spot buying, they can reinforce the perception that Solana is capturing practical usage, not only speculative demand.

Memecoin revival and ecosystem features support short-term momentum

Beyond tokenization, the rally also appears to have been helped by a memecoin resurgence. The article highlights the Sunday airdrop of The Black Bull (ANSEM), which launched on Pump.fun. ANSEM reportedly reached a market capitalization of $60 million by Tuesday, with the developer directing roughly 65% of the supply to Ansem’s public wallet; the launch rollout reportedly involved about 74,000 addresses over the initial three days. The distribution is described as lacking full transparency.

That kind of attention can matter because memecoin activity often spurs retail trading and related network usage—especially on ecosystems where token launches and trading are tightly integrated. In this case, multiple Solana memecoins gained, but the article notes that the biggest winner was the Pump.fun platform token (PUMP). PUMP added about 27% on the week, returning to the top 100 by market capitalization and reaching an estimated $630 million valuation. ANSEM itself reportedly extended gains on Friday, reaching an all-time high market capitalization of $112 million.

Alongside memecoins, the article also ties SOL’s renewed interest to prediction-market functionality. It cites the integration of a “World prediction markets” experience into the Phantom wallet, reporting nearly $890,000 in total value locked over two days, framed as an effort to compete with Polymarket during the World Cup betting cycle. It also mentions that Jupiter has prediction markets under beta testing, with a reference to a June 29 launch.

Leverage cools: derivatives signal traders are less willing to chase

If tokenized-asset growth and memecoins helped ignite the move, derivatives data suggests the market is no longer as eager to press higher prices. The article points to a sharp decline in bullish leveraged appetite after Wednesday, when SOL rose above $75 for the first time in 30 days.

Specifically, the SOL perpetual futures annualized funding rate fell to 3% on Friday from an 11% peak just two days earlier. The piece references Laevitas for those funding figures, and notes that under “neutral conditions,” the funding rate should typically sit in a range from 6% to 12% to balance the capital cost.

That shift is important for traders because funding rates often reflect whether longs are crowding the trade. A cooling funding environment can mean new longs are less willing to pay up for exposure to SOL, which can reduce the momentum needed to sustain a breakout attempt—especially if spot demand doesn’t keep pace.

In other words, the market may be congratulating itself on earlier gains while becoming more cautious about a further push toward $90. The article’s framing emphasizes that investors may not want to bet on SOL widening its performance gap over other altcoins based solely on temporary memecoin-driven attention. Without sustained blockchain activity that converts into durable demand—rather than short-lived hype—there may be fewer reasons for leverage to build again quickly.

What to watch next for SOL and Solana activity

For SOL to realistically challenge the $90 zone, the next signal to track is whether the tokenized-asset expansion and broader on-chain usage can offset any fading retail-driven flows. If tokenized trading volume continues to grow and prediction-market participation sustains, the narrative supporting SOL may broaden beyond memes. Conversely, if leveraged sentiment stays subdued and funding remains below the levels typically associated with healthy upside positioning, SOL may consolidate even if it remains resilient versus the rest of the altcoin market.

Shielded Labs has raised the possibility of delaying Zcash’s Ironwood network upgrade, citing readiness concerns among exchanges, mining pools and wallet providers ahead of the planned late July activation.

Summary

- Shielded Labs says Zcash’s Ironwood upgrade may be delayed as ecosystem participants need more preparation time.

- Exchanges, wallets and mining pools are simultaneously migrating from zcashd to the new Z3 software stack.

- Ironwood is designed to secure Zcash’s shielded supply after the Orchard “infinity” bug was disclosed.

According to a July 3 X post on the Zcash community forum by Shielded Labs executive director Jason McGee, the network is attempting to complete two major changes at the same time. Alongside Ironwood, infrastructure providers are also expected to replace Zcash’s long-running node and wallet software, zcashd, with a new software suite known as the Z3 stack.

McGee said feedback from ecosystem participants showed mixed levels of preparedness. While some operators believe they can complete the migration before the planned activation window, others have indicated they will require additional time to deploy and test the new software. He added that no decision has been made to postpone Ironwood.

Infrastructure migration remains the biggest hurdle

As part of the transition, Zcash is retiring zcashd, which has long been used by exchanges, wallets and other network operators to connect to the blockchain and process transactions. Its replacement consists of Zebra for running network nodes, Zaino for blockchain data services and Zallet for wallet functionality.

According to Zcash’s official migration guidance, some features available in zcashd will not have direct replacements, meaning operators may need to modify their own infrastructure before switching to the new stack. McGee also said both Zallet and Zaino remain under development and are not yet considered production-ready, making deployment timelines uncertain for some ecosystem participants.

The overlap between the software migration and Ironwood activation has created a practical challenge. Delaying Ironwood could extend uncertainty around Zcash’s shielded supply, while proceeding without sufficient preparation could leave exchanges, mining pools, and wallet providers struggling to complete the migration safely.

Ironwood is designed to secure Zcash’s shielded supply

Ironwood was proposed after researchers identified an “infinity” bug in Orchard, Zcash’s primary shielded transaction pool. According to the development team, the vulnerability could theoretically have allowed an attacker to create an unlimited amount of counterfeit ZEC inside Orchard without immediate detection. Developers also said they found no evidence that the flaw had ever been exploited.

Because Orchard’s privacy protections prevent anyone from proving that no counterfeit coins were created, Ironwood introduces a replacement shielded pool and closes Orchard to new activity. Funds leaving Orchard would pass through an accounting checkpoint that prevents more ZEC from exiting than originally entered, allowing users to verify that the circulating supply stays within the protocol’s intended limits.

Earlier this year, developers temporarily disabled Orchard transactions through an emergency network update after disclosing the vulnerability while work on Ironwood continued. The upcoming upgrade forms the permanent solution intended to restore confidence in the network’s shielded supply.

Meanwhile, Zcash founder Zooko Wilcox said recent security reviews have not uncovered any additional serious vulnerabilities in the new implementation. He added that developers are continuing to verify the upgraded system before Ironwood is activated, while discussions remain ongoing over whether additional preparation time is needed for ecosystem participants before the network upgrade proceeds.

A formal complaint has asked Parliament’s standards watchdog to examine whether Reform UK leader Nigel Farage breached lobbying rules. This comes after Farage received donations from billionaire Christopher Harborne, who reportedly holds a 12% stake in Tether’s USDT stablecoin.

Labour MP Phil Brickell filed the complaint on July 2. He asked Parliamentary Commissioner for Standards Daniel Greenberg to review Farage’s private meeting with Bank of England Governor Andrew Bailey in September 2025.

The Rule Behind the Farage Crypto Lobbying Complaint

Official UK parliamentary guidance prohibits MPs from approaching ministers or officials on behalf of recent benefactors.

“Paid lobbying is prohibited. An MP who has received a benefit such as hospitality, a gift or payment must not for 12 months after receipt engage in … any approach to a minister, other MP or public official which would provide (or seek to provide) a financial or material benefit for the person or organisation which provided them with that … payment.”

The restriction is younger than it looks. The British Parliament doubled the ban from 6 to 12 months in March 2023, after Owen Paterson resigned in 2021. The standards committee found he lobbied for two firms paying him more than £100,000 ($133,500) a year.

Brickell, chair of Parliament’s anti-corruption group, reported Farage to Commissioner Daniel Greenberg. This is according to a report by The Guardian,

“This is not simply a debate about cryptocurrency. It is about whether an MP who has received millions from one individual should be lobbying for policies that could increase the value and profitability of that donor’s investments.”

Follow us on X to get the latest news as it happens

How the Timeline Tests the Rule

Farage reportedly accepted a £5 million gift from Harborne before the July 2024 general election. Greenberg is already examining whether that gift should have been declared, according to the BBC.