Crypto World

Ethereum at risk of drop if $2K support breaks, traders warn

Ether (ETH)is shaping up for a potentially sharper slide as a bearish continuation pattern tightens on the daily chart. A break below the lower boundary of a bear flag around $2,000 could accelerate selling, with the measured target pointing toward roughly $1,075—about a 49% decline from prevailing levels. The sequence would echo a similar breakdown seen in January, when ETH tumbled more than 41% from its highs.

Beyond the chart look, the risk matrix includes potential liquidity shocks for leveraged longs and a cooler stance from large holders. If prices slip past $2,000, market data projects over $1.7 billion in long ETH liquidations across major exchanges, underscoring the fragility of bullish bets in a downward-biased setup. At the same time, holders’ behavior signals growing caution among big and mid-size players, even as ETH attempts a rebound toward the $2,400 area earlier this week.

Key takeaways

- Bear flag target for ETH sits near $1,075, implying about a 49% drop from current levels if the pattern resolves to the downside.

- A break below $2,000 could unleash more than $1.7 billion in leveraged long liquidations across exchanges, amplifying downside momentum.

- Whale activity has cooled, with mega‑whales (addresses holding more than 10,000 ETH) at a 10‑month low and large holders reducing exposure, signaling waning mid‑term conviction.

- Technical and momentum signals are deteriorating, including a potential death cross and weakening daily and weekly RSI readings, increasing the risk of a sustained pullback.

Bear flag dynamics and historical context

Market technicians describe a bear flag as a bearish continuation pattern that forms after a sharp decline followed by a brief consolidation within a rising channel. The pattern’s measured move is calculated by taking the prior downtrend’s height and projecting it from the breakdown point. In ETH’s case, a breakdown below the $2,000 level yields a target near $1,075, representing a substantial retracement from the current zone.

Analysts have pointed to a January breakdown as a recent precedent for how such patterns can unfold. The price action then produced a meaningful correction, reinforcing the idea that the flag’s target is not merely theoretical but anchored in actual price history.

Beyond the chart, sentiment around ETH’s near‑term path remains fragile. If price cannot hold above the trend line around $2,000, a sequence of lower supports could come into play, potentially widening the slide toward the mid‑$1,000s. Some observers stressed that if the bear flag fails to hold, risk can extend to around $1,300 before any stabilizing relief appears, though this remains contingent on the speed and depth of selling pressure.

Liquidity risk and positioning implications

When price nears critical supports, the risk of cascading liquidations increases for leveraged traders. Data aggregators project that a decisive break below $2,000 could trigger more than $1.7 billion in long ETH liquidations across exchange platforms, reflecting the heavy exposure that buyers carried into the current setup. This dynamic tends to feed a self‑reinforcing cycle: as liquidations mount, selling pressure intensifies and price tends to move lower still.

The scale of potential liquidations aligns with a broader narrative of thinning bullish conviction in the immediate term. For many traders, that means a heightened emphasis on risk controls, tighter stop placement, and a readiness to adapt to evolving price signals rather than assume a bottom is at hand simply because ETH rebounded from a dip.

Whale and holder dynamics

On the ownership front, Glassnode and related trackers have shown a cooling in large‑holder activity. The number of mega‑whale wallets—those holding more than 10,000 ETH—has fallen to a 10‑month low, around 1,050 addresses, signaling a reduction in the willingness of the biggest players to back sizable ETH bets at current levels. The tier just below, wallets holding between 1,000 and 10,000 ETH, also declined to a nine‑month low of about 4,750, with a negative month‑over‑month shift continuing to weigh on mid‑sized holders.

Taken together, the data paints a picture of retreat rather than accumulation among top cohorts, a trend that can magnify downside risk if price breaks lower. The broader pattern suggests a shift toward de‑risking and exit for many large holders, consistent with a market seeking clearer directional catalysts before re‑loading.

Coin participants have also pointed to inflows into exchanges as a signal of potential selling pressure building in the near term. In an environment where big holders are trimming exposure and leveraged long bets face a liquidity squeeze, such institutional dynamics can help explain why the path of least resistance remains downward in the short horizon.

What to watch next

Traders should monitor the $2,000 level closely, as a decisive move beneath it would raise the odds of a test of the bear flag’s lower targets and invite a wave of liquidations. On the other hand, sustained price action above $2,000 and a successful hold above nearby support could inject relief into the market, especially if momentum indicators turn more constructive on the daily and weekly timeframes. The confluence of a potential death cross, deteriorating RSI signals, and the ongoing distribution among top wallet cohorts forms a complex risk picture that remains sensitive to macro and on‑chain developments.

As the market weighs these technicals against broader crypto and macro trends, investors will be watching for signs of a revival in conviction—whether through renewed accumulation by large holders, a shift in exchange flows, or a macro‑driven bid that can flip the near‑term downbeat narrative. Until then, ETH remains vulnerable to a test of the lower boundary of its current pattern, with the next few trading sessions likely to reveal whether the bears have the upper hand or a new catalyst emerges to re‑ignite momentum.

Bitcoin (BTC) halted its latest recovery at Wednesday’s Wall Street open as US traders sold off.

Key points:

- Bitcoin nears $78,000 before the US open spoils momentum, continuing a trend from earlier in the week.

- US stock markets await Nvidia earnings amid a tense macro atmosphere.

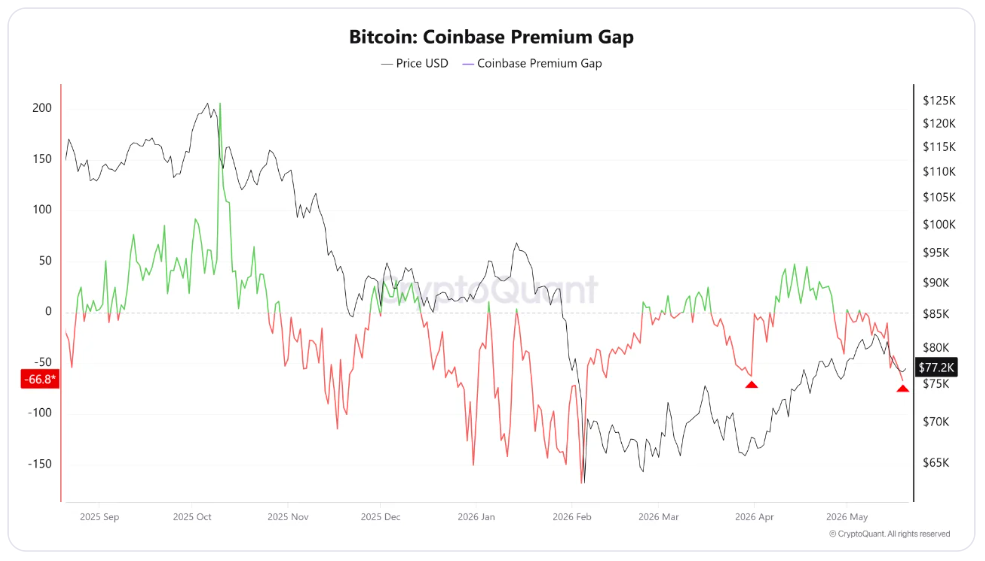

- Bitcoin’s Coinbase Premium sees multi-month lows in a sign of “soft” US demand.

BTC price stops short of $78,000 ahead of Nvidia numbers

Data from TradingView showed BTC/USD reaching $77,678 on Bitstamp before the US trading session sparked fresh losses.

BTC/USD one-hour chart. Source: Cointelegraph/TradingView

Copying its moves from the week’s first two trading days, Bitcoin faced tailwinds as US market sentiment stayed bearish on the macroeconomic outlook.

The S&P 500 fell 1.3% before rebounding, with traders waiting for the week’s key potential volatility catalyst: Q1 earnings from tech company Nvidia.

On Monday, trading resource The Kobeissi Letter described the numbers as the “biggest earnings event of the quarter.”

Continuing, it noted the role of tech stocks in driving S&P 500 strength — even as the US-Iran war and associated inflation risk spooked other markets.

“A handful of tech stocks are driving the entire market,” it summarized in a post on X.

S&P 500 one-hour chart. Source: Cointelegraph/TradingView

Bitcoin Coinbase Premium reflects “soft” demand

In crypto circles, attention focused on the Coinbase Premium Index, which highlighted the ongoing lack of bullish sentiment during US trading sessions.

Related: BTC price ‘bull trap’ at $76.5K? Five things to know in Bitcoin this week

The Index, which measures the difference in price between Coinbase’s BTC/USD and Binance’s BTC/USDT pairs, fell to its lowest levels since February on the day.

Commenting in one of its QuickTake blog posts, onchain analytics platform CryptoQuant said that spot Bitcoin demand “remains soft.”

“The latest Coinbase Premium Gap reading stands near -$66.8, meaning Bitcoin is trading at a lower price on Coinbase Pro’s USD pair compared with Binance’s USDT pair. This is deeper than the late-March reading of around -$62.6, when Bitcoin was trading near $68,000,” contributor Amr Taha wrote.

“The comparison is important because Bitcoin is now trading much higher, around $77,200, yet the Coinbase discount versus Binance is wider than it was when BTC was nearly $9,000 lower.”

Bitcoin Coinbase Premium gap (screenshot). Source: CryptoQuant

Others monitored familiar trend lines, including the 21-week exponential moving average (EMA).

As Cointelegraph reported, BTC/USD reclaimed that level on weekly time frames in late April, only to lose it again this week.

“Bitcoin has Weekly Closed below the 21-week EMA (green) which technically positions price to potentially turn it into new resistance on any upcoming rebound,” trader and analyst Rekt Capital told X followers on Tuesday while analyzing the weekly chart.

“Turning the 21-week EMA into new resistance would fully confirm the breakdown from it.”

BTC/USD one-week chart. Source: Rekt Capital/X

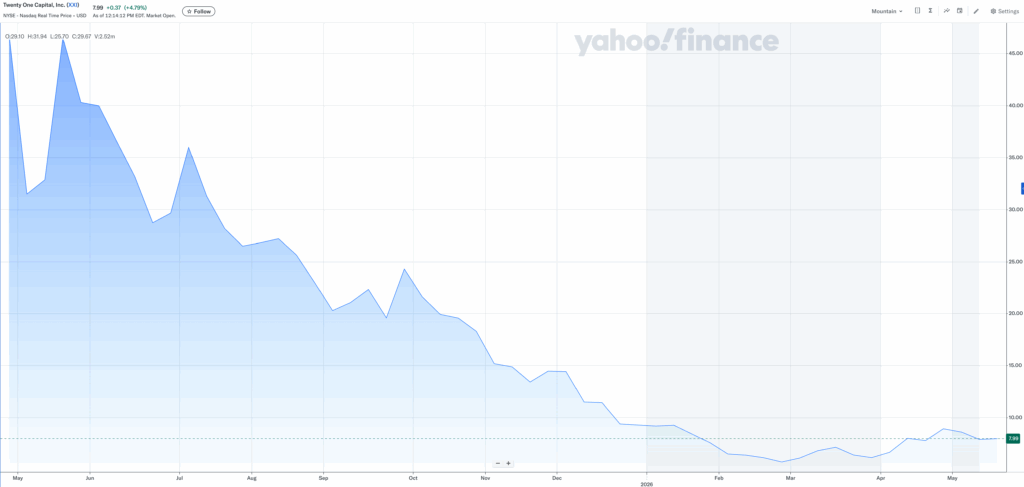

Tether International has announced acquiring Japanese multinational investment firm SoftBank’s minority stake in the Bitcoin-focused treasury company, Twenty One Capital (XXI).

At the closing of the transaction, SoftBank’s representatives on the XXI Board of Directors stepped down in line with the shareholder agreement.

Tether Absorbs SoftBank Position

In its official blog post, Tether stated that the transaction “reflects the continued development of XXI as the company builds on its foundation and advances its long-term Bitcoin strategy.” With the transaction finalized, SoftBank’s role in governance has now concluded.

Commenting on the latest development, Tether CEO Paolo Ardoino said,

“SoftBank’s involvement gave XXI the kind of institutional depth that few early-stage companies ever have. Their experience backing some of the most consequential technology companies in the world brought credibility, perspective, and discipline to XXI during a critical period of formation. They leave behind a company with a stronger foundation, a clearer mandate, and an ambitious path ahead. Tether’s conviction in XXI has only deepened, and we look forward to building on that foundation as the company enters its next chapter.”

In April 2025, Twenty One Capital was launched as a new crypto venture with Strike founder Jack Mallers named as CEO. The company was backed at launch by Tether International and Bitfinex as majority owners, alongside SoftBank Group and Cantor Fitzgerald as initial investors. It was disclosed that the company would begin with about $3.6 billion in Bitcoin held in its treasury. SoftBank was included as a minority stakeholder at formation, while Tether held controlling ownership.

Twenty One Capital went public in December of the same year through a SPAC merger in New York.

Merger Proposal

Last month, Tether put forward a multi-step plan involving Twenty One Capital, which included merging the company first with Strike. After that initial step, the plan proposes a second stage where the combined entity would then merge with the bitcoin mining company Elektron Energy.

Meanwhile, according to the latest data, Twenty One Capital is currently the second-largest public company holder of Bitcoin, with 43,514 BTC. It trails Michael Saylor-led business intelligence firm, Strategy, which holds 843,738 BTC.

The post Tether Acquires SoftBank Stake in Bitcoin-Focused Treasury Company XXI appeared first on CryptoPotato.

Cryptocurrency custody firm Copper has been out shopping itself, seeking a buyer willing to pay about $500 million for the platform, according to two people familiar with the matter.

Wall Street investment bank Cantor Fitzgerald has been appointed to help sell Copper, the people said.

Copper and Cantor didn’t respond to requests for comment.

The jewel in Copper’s crown is the ClearLoop settlement system, which enables network participants to do delivery versus payment (DvP) from within custody without bringing assets onchain, thereby eliminating settlement risk.

Copper closed its enterprise custody business in 2023 to focus on ClearLoop, launched in 2020 and caters to dozens of institutional firms. The firm boasts more than 1,000 active counterparties and over $50 billion in monthly notional trading volume, according to its website.

Copper was said to be weighing an IPO earlier this year, potentially following in the footsteps of crypto custodian Bitgo, with whom Copper forged a partnership on the ClearLoop application. However, with bitcoin trading below $80,000, and artificial intelligence soaking up most of the capital, the crypto IPO market has been on a holding pattern this year.

Meanwhile, the deal-making in the crypto market has been active this year, as crypto-native, traditional and fintech firms are looking to expand their digital asset capabilities through acquisitions.

Earlier this year, Mastercard agreed to buy U.K.-based stablecoin infrastructure firm BVNK for as much as $1.8 billion. Kraken’s parent company, Payward, agreed to acquire the derivatives platform Bitnomial, while Bullish, owner of CoinDesk, announced a $4.2 billion deal to buy Equiniti, aimed at combining transfer agency services with tokenization infrastructure.

And just this week, London-based bank Standard Chartered said it will buy the remaining shares of Zodia Custody, its cryptocurrency custodian subsidiary, that it doesn’t already own. The deal came just weeks after the bank’s venture capital division reportedly took a stake in crypto trading firm GSR at a valuation of more than $1 billion.

SoftBank has sold its stake in Jack Mallers-led Twenty One Capital to Tether, according to the stablecoin giant.

Twenty One Capital (also known as XXI) is a bitcoin (BTC) treasury firm that was founded with Tether providing the BTC and getting the controlling share, SoftBank purchasing a stake from Tether, and the entity being publicly listed by utilizing a reverse merger with a Cantor Fitzgerald-affiliated special purpose acquisition company.

Tether’s announcement details how it has “acquired SoftBank’s stake in XXI,” which it claims “reflects the continued development of XXI.”

Read more: How Tether-backed Twenty One plans to rival MicroStrategy

The combined firm was first listed on December 9, 2025.

Since then, the price of the stock has fallen by 23%, from approximately $10.74 to $7.85.

However, the peak for this stock came after the announcement and before the merger, when it reached a peak value of approximately $49.62 on May 21.

The price has fallen approximately 84% since this peak.

Despite these travails for the equity of this firm, Tether chief executive Paolo Ardoino said, “Tether’s conviction in XXI has only deepened and we look forward to building on that foundation.”

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Crypto World

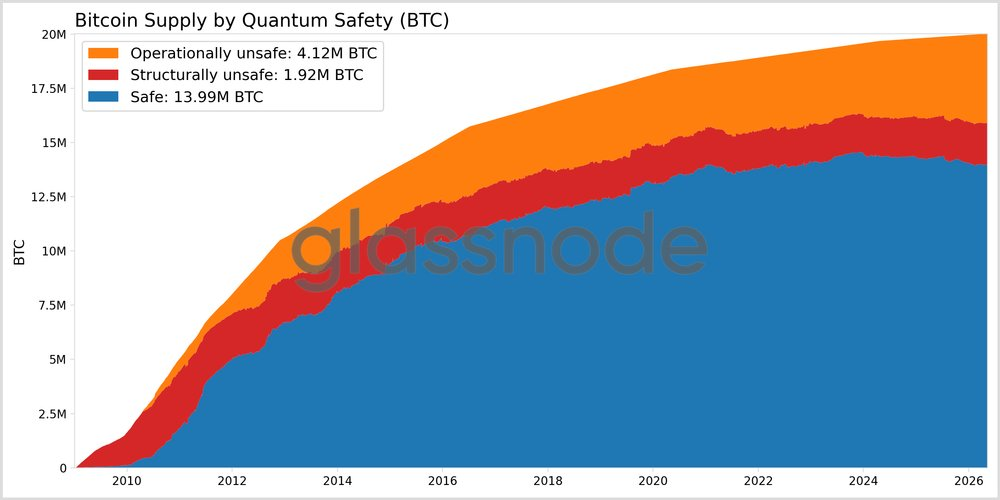

Nearly 10% of Bitcoin Supply is ‘Structurally Unsafe’ from Quantum Computing: Glassnode

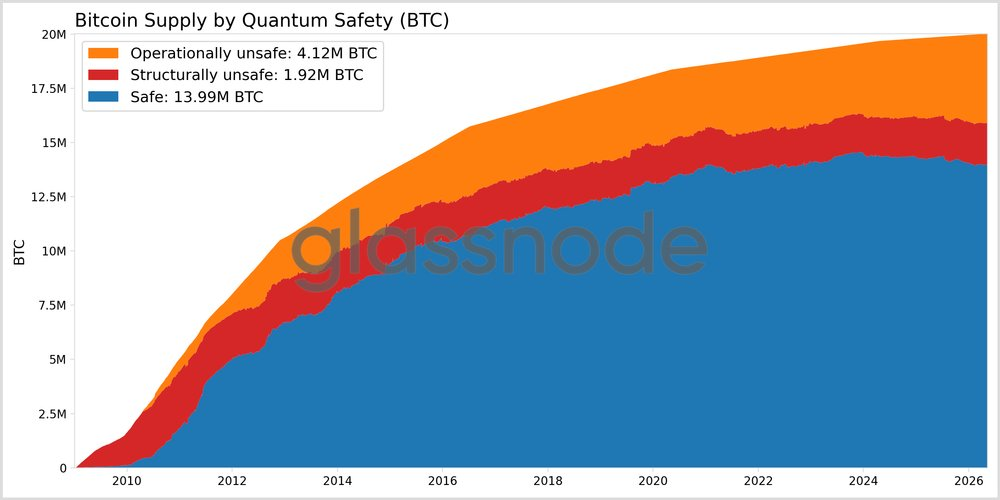

Nearly 10% of the total Bitcoin supply is considered “structurally unsafe” due to a quantum computing breakthrough, as their output type reveals the public key by design, regardless of address management practices, according to data analytics platform Glassnode.

Totaling about 1.92 million Bitcoin (BTC), the group includes BTC from early Satoshi-era Pay-to-Public-Key (P2PK) outputs, legacy multi-sig structures such as Pay-to-Multisig (P2MS) and modern Pay-to-Taproot (P2TR) outputs, which reveal the public key or public key-equivalent by design, wrote Glassnode in a Wednesday X post.

Bitcoin creator Satoshi Nakamoto’s coins represent about 1.1 million or 5.5% of the vulnerable supply, following another 620,000 Satoshi-era coins or 3.1% of the supply and about 200,000 coins or 1% of the supply in Taproot addresses.

Choosing how to implement PQC [post-quantum cryptography] and deploy it on-chain should remain decoupled from the question of what to do about coins that remain quantum vulnerable. Yet the two matters often are conflated, the controversy around the latter often clouding discussions of the former – ARK Invest

The findings underscore the need to implement a quantum-proof path for Bitcoin, such as the adoption of BIP-360’s proposed Pay-to-Merkle-Root (P2MR) output type, which seeks to remove Taproot’s quantum-vulnerable key path spend, though it does not itself add post-quantum digital signatures.

While 9.6% of the total supply remains structurally exposed, a significant part of this exposure “could be reduced if wallet infrastructure, address standards, and user behavior evolve,” added Glassnode.

However, this supply would only be vulnerable to quantum theft if quantum computers can break Bitcoin’s elliptic curve cryptography (ECC), which would require about 2,330 logical qubits and tens of millions to billions of quantum gates, according to a March white paper published by US investment manager Ark Invest.

Source: Glassnode

Nearly 70% of Bitcoin’s supply is safe from quantum computing threat

Glassnode estimates that about 13.99 million Bitcoin, representing 69.8% of the total supply, remain unexposed to a quantum computing threat, which is largely in line with Ark Invest’s figures, which show that 65% of the supply was safe, Cointelegraph reported in March.

Still, the analytics provider notes that about 4.12 million BTC, or 20.6% of the total supply, are “operationally unsafe,” meaning that these coins are exposed due to a key or address management issue.

Source: Glassnode

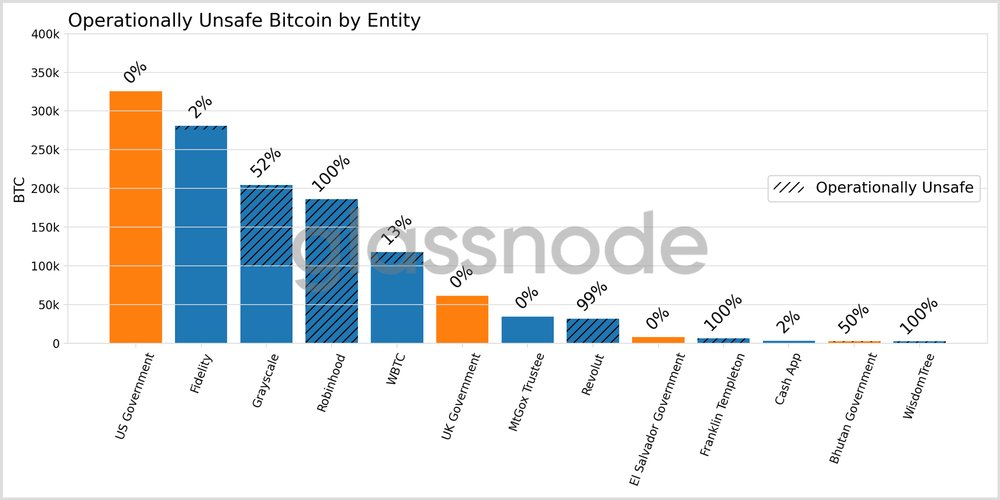

Entity-level data shows that the holdings of some large corporate entities are exposed. This includes 100% of BTC held by Franklin Templeton, WisdomTree and Robinhood, 99% of neobank Revolut’s Bitcoin, 52% of Grayscale’s holdings and just 2% of Fidelity’s Bitcoin stash.

Related: Bernstein says Bitcoin market already priced in quantum risk

Looking at the exposed tokens of cryptocurrency exchanges, only about 5% of BTC held on Coinbase is exposed, compared to 85% of Binance’s BTC and about 100% of the holdings on Bitfinex exchange.

To reduce exposure, exchanges and custodians are advised to reduce key reuse, improve address hygiene and plan a migration into a quantum-proof format to position for a future quantum breakthrough, wrote Glassnode.

Magazine: Bitcoin vs. the quantum computer threat — Timeline and solutions (2025–2035)

OpenAI is preparing to file for an IPO very soon, potentially as early as this Friday, according to a new exclusive Wall Street Journal report.

The ChatGPT maker is working with bankers at Goldman Sachs and Morgan Stanley on a confidential draft prospectus for regulators.

The post OpenAI IPO Filing Looms: Crypto Liquidity Crunch Incoming? appeared first on BeInCrypto.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Hyperliquid highlights shift in crypto design as user experience overtakes token-first product narratives.

Summary

- Hyperliquid shows crypto is shifting from token-driven hype to product-driven usage, dominating perpetual futures volume without incentives.

- Nika Finance builds on this shift with a mobile-first, non-custodial trading app combining spot, perps, staking, yield, and prediction markets.

- Nika reflects the new model where small teams ship fast, integrate proven infra like Hyperliquid, and compete on product rather than token narratives.

For most of the last decade, a useful generalization about crypto products was that the token mattered more than the product. The user experience could be inelegant, the workflow could be confusing, the latency could be poor, and most of it could be explained away by the technical constraints of the underlying chain. The promise was that the token would carry the product, and the product itself could catch up later.

That generalization is no longer holding. The clearest evidence is Hyperliquid.

According to multiple industry trackers, Hyperliquid now processes more monthly perpetual futures volume than its next several competitors combined. There is no airdrop campaign explaining it. There are no incentives war driving the migration. There is no narrative cycle propping up the volume. Users are using Hyperliquid because the product is materially better than the alternatives at the specific thing it does. That is, by crypto standards, an unusual thing to say about a piece of category infrastructure. It is also the correct thing to say.

What makes Hyperiquid different?

What Hyperliquid demonstrated is not a particular technical breakthrough. The matching engine performance is excellent, but the more important fact about it is that the user can feel the difference. The fees are predictable. The order book is deep. The execution is quick. The funding rates are visible. The UI behaves like a serious trading interface rather than a DEX demo. Each of those is a small thing. The accumulation of them is the story.

This is the part the industry spent the last cycle convincing itself was not necessary. The theory was that the token would carry the product. Yield farming, airdrops, retroactive distribution, points programs, all of these were the engines of growth. The product itself could be rough; the user would tolerate it for the upside. For a few years that theory worked, because the upside was real. When the upside thinned out, so did the user base, and what remained was a category full of products that had never had to earn their users in the first place.

A wave of products is forming around the opposite premise. The pattern is consistent across the teams, making the most credible runs at their categories right now: deep investment in product, very little investment in narrative, and an unusually short distance between user feedback and shipped change. None of these teams use the word “discipline” about themselves. This is not ideology. It is an adaptation. They are responding to the same observable fact, which is that the product is now the unit of competition, not the token or the narrative around either.

There are reasons this happened, and they are not personal to the founders running the products. The user base that drove the last cycle has either left or grown more discerning. The capital that used to subsidize narrative-heavy teams is not coming back at the same valuations. Most importantly, on-chain transparency made it possible to compare products against each other on metrics that are real rather than reported. A product that does not perform at the level its marketing claims gets caught within weeks. The penalty is immediate, and the recovery is slow.

Nika is building on top of what Hyperliquid started

A useful example of how this pattern looks at the consumer-facing application layer is Nika Finance, a non-custodial application combining spot trading, perpetuals, staking, yield, and prediction markets powered by Polymarket across multiple chains in a mobile-first interface. The product is live. The team operating it is three people. The traction has accumulated without a marketing engine.

The relevant point about Nika in the context of this argument is not that it competes with Hyperliquid. It does not. Nika’s perpetuals layer is powered by Hyperliquid through builder codes, which is a concrete instance of what the new pattern looks like in practice: a consumer application built on top of the perps infrastructure Hyperliquid set the new bar for. The argument is not that Nika has built a better Hyperliquid. The argument is that Hyperliquid’s product quality has made it the underlying engine for a generation of consumer applications, and Nika is one of them.

“For most of the last cycle, crypto products competed primarily on token incentives and financial engineering. Hyperliquid showed that users will move aggressively toward products that are simply better to use. We are building with that same assumption,” said Daniel Brinzan, founder of Nika Finance.

The implication for the next few years is that the easy part of crypto product strategy is over. The token mechanics that used to substitute for product work are still possible to deploy, but they will produce smaller and shorter-lived returns than they did during the cycle just past. The work that was previously deferable, the work of making the user experience genuinely good, is no longer deferable. Teams that internalize this early will compound faster than teams that arrive at the same conclusion through losing users.

Hyperliquid did not change the rules by getting bigger. It changed them by being noticeably, durably better in its category than its competitors. That distinction matters for the next wave of teams trying to build serious products in serious categories. The audience has now seen what good actually looks like. It is going to be harder, after this, to convince users to put up with less.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Key Highlights

- MDT stock declined 1.44% following the $650M SPR Therapeutics acquisition reveal.

- SPR’s temporary 60-day peripheral nerve stimulation technology enhances Medtronic’s pain therapy range.

- Strategic move targets chronic pain market affecting approximately 50 million Americans.

- Transaction reinforces Medtronic’s position in the neuromodulation sector.

- Transaction anticipated to finalize during first half of Fiscal 2027.

Shares of Medtronic (MDT) retreated 1.44% to close at $77.45, pulling back from earlier session peaks around $79. The stock’s decline came after the medical device giant revealed plans to acquire SPR Therapeutics, Inc. through an all-cash transaction valued at $650 million. This strategic purchase is designed to bolster Medtronic’s neuromodulation capabilities and pain therapy solutions.

Strategic Expansion of Pain Therapy Solutions

Medtronic plans to acquire all outstanding shares of SPR, a pioneering company in temporary peripheral nerve stimulation technology. This strategic acquisition enhances Medtronic’s capacity to deliver minimally invasive, short-duration pain management alternatives. The deal is consistent with the company’s broader initiative to reinforce its core business segments.

SPR’s FDA-approved SPRINT PNS System provides temporary pain relief for up to 60 days without requiring permanent device implantation. The technology seamlessly fits into current clinical practices and facilitates early-stage treatment intervention. This methodology expands treatment availability and minimizes reliance on permanent surgical procedures.

With chronic pain impacting approximately 50 million adults across the United States and restricting everyday activities, the acquisition enables Medtronic to serve this substantial patient demographic more comprehensively. Furthermore, the transaction reflects increasing market preference for non-opioid, minimally invasive therapeutic options.

Industry Position and Business Rationale

Medtronic brings more than five decades of expertise in neuromodulation technology and offers the most comprehensive pain therapy portfolio in the industry. The peripheral nerve stimulation market segment is experiencing robust expansion, supported by substantial clinical data and widening insurance coverage. Clinical results from more than 6,100 patients who received the SPRINT PNS System showed that over 71% achieved significant pain reduction or enhanced quality of life.

The acquisition adds depth to Medtronic’s neuromodulation product range across various treatment phases. It works in conjunction with the company’s existing permanent implantable devices and temporary intervention options. The combined offerings are projected to improve patient results and accelerate clinical implementation.

The deal remains contingent upon standard regulatory clearances and closing requirements. Both Medtronic and SPR will continue autonomous operations pending transaction completion. The anticipated closing timeframe falls within the opening half of Medtronic’s Fiscal Year 2027.

Investment and Growth Considerations

The $650 million transaction represents a significant commitment to Medtronic’s expansion plans. It demonstrates the company’s dedication to advancing patient-focused innovation within pain management. SPR’s specialized platform strengthens Medtronic’s competitive stance in the dynamic neuromodulation marketplace.

Market observers may view the acquisition as an extension of Medtronic’s ongoing efforts to enhance its therapeutic product lineup. The transaction emphasizes the company’s concentration on minimally invasive, clinically validated treatments. This move could impact future revenue performance and competitive positioning.

Medtronic’s move to purchase SPR mirrors larger healthcare technology market dynamics. Industry leaders are increasingly pursuing therapies that shorten recovery periods and enhance patient well-being. The acquisition corresponds with prevailing sector movements toward early-stage, temporary, and non-opioid pain management solutions.

Welcome to our institutional newsletter, Crypto Long & Short. This week:

- Alec Beckman on why BTC-backed lending is not a crypto story, but a capital efficiency story.

- Serena Sebastiani on how stablecoins aren’t a crypto product; they’re becoming the settlement infrastructure global finance forgot.

- Top headlines institutions should pay attention to by Francisco Rodrigues.

- “Ethena’s Solana lending markets cross $1B in 4 days” in Chart of the Week.

Thanks for joining us!

Expert Insights

Bitcoin-backed loans belong in the cost-of-capital conversation

By Alec Beckman, VP of the Americas, Psalion

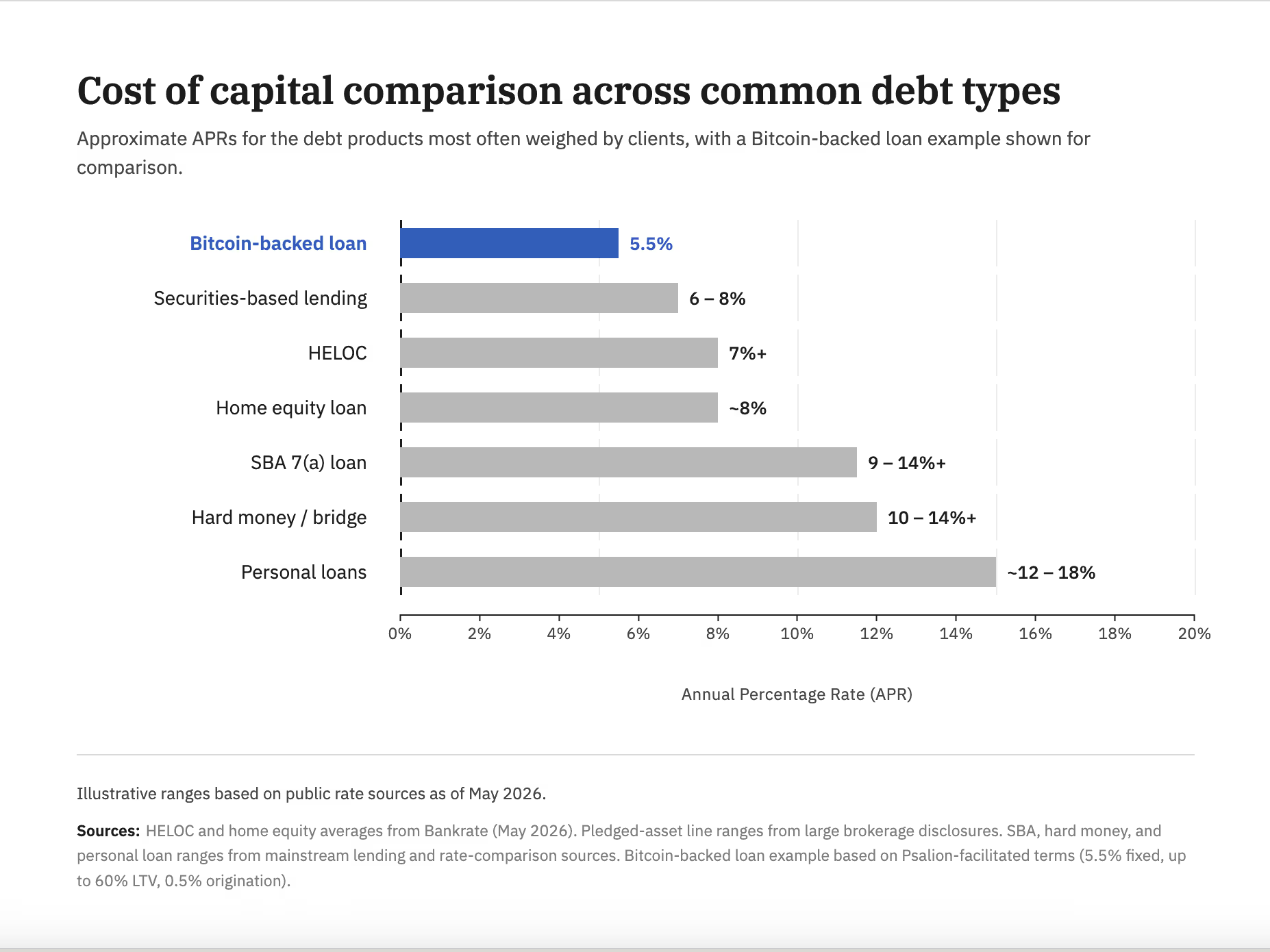

The argument is not about whether to buy bitcoin or not. It is for advisors, real estate investors, small business owners and founders who already own it, or work with clients who do. The practical question is simple: if a client carries meaningful debt, why is BTC-backed lending not in the capital stack discussion? Debt-heavy professionals already compare collateral, rate, fees, speed and covenants. Bitcoin-backed loans should be evaluated the same way.

The debt menu is familiar. HELOCs are tied to home equity, often variable, and currently sit above 7% for many borrowers. Hard money and bridge loans can move quickly, but often price around 10% to 14% plus points. Securities-based lending can be efficient, but rates often begin around 6% to 8% and require sizable brokerage assets in one place. Personal loans frequently land in the low-to-mid teens. SBA loans can be useful, but the all-in cost, documentation and time to fund are not trivial.

Bitcoin-backed lending changes the collateral, not the math. The borrower pledges BTC, receives dollars or stablecoins and repays under agreed terms. The asset is liquid, verifiable and easy to monitor. Market rates still vary widely, but more competitive structures are emerging. At Psalion, for example, we facilitate access to Bitcoin-backed loans at a 5.5% fixed rate, up to 60% LTV, with a 0.5% origination fee. That is one data point, but it shows why the category belongs in a serious debt comparison.

Rate matters first. For someone already holding BTC, the relevant question is not “Should I borrow?” It is “Where should I borrow?” Against a house? A business? A securities portfolio? Or BTC? If BTC collateral produces cheaper capital than the borrower’s existing debt, it can reduce the blended cost of capital.

Fees matter next. Hard money can carry points on origination. SBA structures can include guarantee fees, closing costs and advisory costs. Personal loans may embed higher APR through origination. Lower fee bitcoin-backed lending can make the all-in economics materially cleaner.

Friction matters too. Traditional credit often requires income verification, tax returns, appraisals, operating statements, personal guarantees, covenants and time. BTC-backed lending is collateral-first. The collateral can be verified quickly and monitored continuously. Faster access to liquidity is not just convenience. It can change the economics of a refinance, acquisition, tax payment or bridge need.

Advisors should care because BTC is now part of more client balance sheets. Too often, BTC sits idle while the same client pays higher rates elsewhere. If the client can borrow against BTC and replace more expensive debt, the advisor has improved the balance sheet without forcing a sale and potentially creating a taxable gain.

There is a second use case: yield on spread. Some real estate investors, founders and business owners see opportunities where expected returns exceed their cost of capital, such as private credit, commercial real estate lending, inventory or operating expansion.

Borrowing against BTC to pursue those opportunities can make sense when the borrower understands both sides of the trade: the yield opportunity and the collateral risk.

That risk is real. Bitcoin is volatile. If the price falls enough, LTV can breach agreed thresholds and trigger margin calls or liquidation. Liquidation can create a taxable event. This is not for every client. It is for borrowers who understand BTC volatility, maintain liquidity and size loans conservatively below maximum LTV.

For clients who already own bitcoin and already carry debt, BTC-backed lending is not a crypto story. It is a capital efficiency story. Ignoring it may mean leaving cheaper capital, or a valuable spread opportunity, on the table.

Principled Perspectives

Stablecoins are now infrastructures

By Serena Sebastiani, chief strategy officer and head of government and regulatory affairs, Fuze

There’s a kind of financial friction that becomes invisible when you live inside it long enough.

From New York or London, cross-border payments work. From Nairobi, Jakarta or Almaty, they don’t.

An SME in Nairobi pays a supplier in Karachi. The money leaves Monday. It arrives Thursday. Along the way it passes through two correspondent banks, absorbs fees on both ends, gets hit with an FX spread on the USD conversion and triggers multiple compliance checks. Both the buyer and the supplier absorb the friction by pricing it into the deal and extending the credit note.

This is how it actually works to operate across the fastest-growing trade corridors globally: Gulf to South Asia, intra-African trade, CIS to MENA, and Southeast Asia remittances.

Multiply that by the $136 billion SME trade finance gap in Africa alone. Multiply it by the $100 billion in annual remittances flowing into the continent. Multiply it across the Gulf-to-South-Asia corridor, CIS-to-MENA and intra-ASEAN. And also account for the cost of sending money into Sub-Saharan Africa, which remains the most expensive region in the world, at 8.3% on average (almost three times the UN’s 3% target). In live corridors today, stablecoin rails are already operating at under 1%. What we’re looking at is not simply a matter of optimizing the margins, but a structural gap in the fastest-growing regions of the global economy.

SWIFT was built for a specific world: large banks, large tickets and major financial centres. It works perfectly for that world. Yet the supplier payment in Nairobi, the remittance from Riyadh to Manila, or the trade settlement between Almaty and Istanbul has been making do with infrastructure designed for someone else’s economy.

That’s the gap stablecoins are moving into, and they’re not a product but real plumbing.

Chart 1: The Remittance Cost Gap

Sources: World Bank (Q1 2025); UN SDG 10.c; Transak / Operational corridor data

What we observe from the ground

I spent time with regulators and market operators across high-growth corridors and a pattern that emerges is that people closest to the friction are the least ideological about the solution. They are the ones actually trying to integrate stablecoins into the existing financial system.

In Kigali for example, the framing isn’t “crypto adoption.” Rwanda’s National Bank launched a CBDC pilot in February with cross-border interoperability as the explicit design priority. A draft Virtual Assets Law now in parliament applies a clean two-tier structure: Central Bank oversight for payment stablecoins and Capital Markets Authority for investment instruments. A fintech license passporting agreement with Kenya, signed in March, is already being designed as a template for the East African Community. This is regulatory infrastructure being built with precision, for a specific problem, by people who understand their own market.

The insight is not Rwanda-specific, but Africa-wide, where mobile money already functions as the default financial layer. With over a billion registered accounts, 96% financial inclusion in markets like Rwanda, this distribution infrastructure took decades to build. What mobile money never solved for is cross-border interoperability. Stablecoins fit that gap naturally, not replacing fiat currencies, but acting as the settlement layer that makes mobile money efficient.

The same logic, four corridors

Middle East

The Central Bank of UAE’s Payment Token Services Regulation treats stablecoins as settlement infrastructure rather than speculative securities. That regulatory framing is practical and allows banks to issue AED stablecoins that can be used directly as a means of payment, and banks and licensed fintechs can build on stablecoin rails without treating every transaction as a liability. In this way, the Gulf stablecoin settlement is happening inside regulated perimeters.

CIS markets

In Kazakhstan, Uzbekistan and Georgia, the driver is dollar access. Domestic currency volatility creates structural demand for USD, and formal banking doesn’t reliably provide them. Stablecoin adoption here is dollarization leveraging a new distribution channel. The institutional opportunity is providing that access inside a compliance framework, with the custody and reserve standards that make it durable.

Southeast Asia

In Southeast Asia, the driver is cost and speed. In corridors like Gulf-Indonesia or Gulf-Philippines for remittances, stablecoin rails eliminate the need for pre-funding and speed up settlement from days to minutes (often under 20 minutes, 24/7). Cost reductions of 40–80% are already observable in operational flows.

I engaged with regulators, banks and fintechs in these markets. The question here is: how can we facilitate higher volumes on stablecoin rails and give back to the households?

Africa

Remittances are expensive, but the B2B case is urgent as well. Intra-African trade only accounts for 16% of total trade, against 68% for Europe and 59% for Asia. The AfCFTA created the legal architecture for a $3.4 trillion market, but the payment infrastructure hasn’t kept up. Chinese traders sourcing African goods are already settling in USDT because it is superior for their transaction sizes and timelines. To make this properly institutional and largely adopted, the essence is to guarantee that the activity happens compliantly, with proper rails.

Chart 2: Intra-Regional Trade Share — Africa vs Peers

Sources: UNCTAD / AfDB / WTO; World Bank / African Union (AfCFTA projection)

Stablecoins are infrastructure

Global banks and fintechs are still largely approaching stablecoins as a product to distribute to customers. The more significant opportunity is treating them as infrastructure to build on, particularly in remittances and B2B payment flows: treasury management, supplier payments and FX settlement. These are flows where the speed improvement and cost reduction are measurable (minutes vs days, basis points), and where the compliance trails on well-designed digital rails are demonstrable and trackable. These include on-chain transaction monitoring, wallet attribution and automated regulatory reporting that produces a compliance record that informal transfer channels structurally cannot. The data generated by these rails is what gets correspondent banking relationships restored in markets where de-risking has cut them.

Solving the friction

What remains to be solved for the infrastructure to properly work at scale? Regulatory frameworks that define reserve standards and redemption rights, cross-border supervisory coordination and AML/CFT laws interoperability.

All this is being worked through, and more in the market that matters (high-growth) than in established developed countries.

From experience working with regulators and now proactively engaging with them, I learned that the pattern that works is: 1. A phased licensing framework that lets regulators learn alongside the market; 2. Proportionate requirements scaled to institutional size and risk profile; 3. Bilateral passporting agreements that make compliance portable across corridors.

The corridors where this infrastructure is most needed are not waiting for global standards to arrive but are actively building. The question for global institutions is whether they’re part of that architecture or arriving late to fintech-leading infrastructure.

Headlines of the Week

This week’s headlines show structural progress on Wall Street’s onchain push, with a market-structure bill clearing its biggest hurdle, JPMorgan extending its tokenization stack, and asset managers tackling the redemption-speed problem. Solana has meanwhile kept quietly cementing its infrastructure for institutional use.

- Clarity Act clears U.S. Senate committee, on its way to a final test in Congress: Chairman Tim Scott secured a 15-9 bipartisan vote with Democrats Gallego and Alsobrooks crossing over, though unresolved law enforcement and government-ethics provisions still stand between the bill and a floor vote before the summer recess.

- JPMorgan files to launch new tokenized fund as Wall Street tokenization race heats up: The Ethereum-based JLTXX fund, run through JPMorgan’s Kinexys blockchain unit, is structured to satisfy GENIUS Act stablecoin reserve requirements — landing days after BlackRock filed for its own tokenized Treasury vehicle.

- BlackRock, Janus Henderson tokenized funds get instant redemptions with new $1 billion facility: Grove’s Basin facility advances stablecoin liquidity against approved redemptions from BlackRock’s $2.2 billion BUIDL and Janus Henderson’s $1.1 billion JTRSY, targeting the multi-day settlement gap that has held back the $15 billion tokenized Treasury market.

- Mike Novogratz’s Galaxy receives New York BitLicense for institutional crypto push: NYDFS cleared GalaxyOne Prime NY to serve hedge funds, RIAs and family offices on a $9 billion platform, making Galaxy only the second firm to win a BitLicense in 2026 after Strike.

- Solana is shedding its memecoin reputation as big banks move billions into its ecosystem: A Messari report shows Solana’s tokenized RWA market cap jumped 43% QoQ to $2.01 billion, with BlackRock’s BUIDL, Ondo, Franklin Templeton and a Citigroup-PwC trade finance PoC live on the network, alongside payments integrations from Visa, Stripe, PayPal and Western Union.

Chart of the Week

Ethena’s Solana lending markets cross $1B in 4 days

Combined USDe and USDG supply across the Bitwise-curated Jupiter Lend market and the Kamino Ethena market rose from $401M on launch day (May 12) to $1.06B on May 16 – driven almost entirely by looper-led growth on Jupiter Lend, where supply climbed from $201M to $812M while Kamino’s Ethena Prime vault held steady around $250M.

Listen. Read. Watch. Engage.

Looking for more? Receive the latest crypto news from coindesk.com and market updates from coindesk.com/institutions.

MoneyGram has become Tempo’s anchor remittance validator in a new strategic blockchain partnership designed to enhance cross-border payment infrastructure.

Is The UK Really Reducing Oil Sanctions On Russia?

Authentic Brands Is Finally Going Public

Bitcoin Price Fails to Retake $78,000 as Markets Eye Nvidia Earnings

![These 4 Things Terrify Me About Bitcoin Right Now [URGENT!!]](https://wordupnews.com/wp-content/uploads/2026/05/1779296261_maxresdefault-80x80.jpg)

-

Crypto World5 days ago

Crypto World5 days agoBloFin War of Whales 2026 Grand Prix opens registration for $5M trading championship

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Theory – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoE-Estate Announces 1 Year Live: Washington DC Summit as Real Estate Tokenization Enters Its Next Phase

-

Tech5 days ago

Tech5 days agoTech Moves: Microsoft AI leader jumps to OpenAI; former AI2 exec joins Meta; and more

-

Tech5 days ago

Tech5 days agoGoogle reimburses Register sources who were victims of API fraud

-

Crypto World6 days ago

Crypto World6 days agoGoogle’s Gemini AI Predicts Incredible Solana Price by the End of 2026

-

Business5 days ago

Business5 days agoH&R Real Estate Investment Trust (HR.UN:CA) Q1 2026 Earnings Call Transcript

-

Entertainment6 days ago

Entertainment6 days agoZara Larsson Has Blunt Response To Chris Brown Diss

-

Sports5 days ago

Sports5 days agoNapoleonic enters 2026 Doomben 10,000 field via Abounding withdrawal

-

Crypto World7 days ago

Crypto World7 days agoTwo AI Tokens Lead May Rally, But Risks Are Rising

-

Crypto World5 days ago

Crypto World5 days agoBeInCrypto 100 Institutional Awards Nomination: KAST for Best Digital Assets Neobank and Best Digital Assets Fintech

-

Fashion4 days ago

Fashion4 days agoOn the Scene at Gucci’s Cruise Show in New York City: Mariah Carey, Kim Kardashian, Lindsay Lohan, Iman, and More!

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Battles US Bond Nerves With BTC Price Dip Toward New May Lows

-

Crypto World5 days ago

Crypto World5 days agoWall Street’s Boldest Gold Prediction Has Russians Rushing to Buy

-

Fashion4 days ago

Fashion4 days agoTrending Western Style Vests Perfect for Summer

-

Crypto World5 days ago

Crypto World5 days agoICE and CME urge US regulators to curb Hyperliquid energy trading

-

Politics6 days ago

Politics6 days agoDWP PIP Timms review continues to be an absolute farce

-

Entertainment5 days ago

Entertainment5 days agoDavid Letterman Returns to Late Show, Blasts Cancellation

-

Fashion4 days ago

Fashion4 days agoAmazon Sundays: Memorial Day Hosting

-

Crypto World5 days ago

Crypto World5 days agoIREN closes $3 billion convertible notes deal amid AI infrastructure expansion

You must be logged in to post a comment Login