Crypto World

Three signs from APEC that the U.S., China remain far apart on trade

China’s Commerce Minister Wang Wentao held a press conference on May 23, 2026, at the end of the APEC trade ministers’ meeting in Suzhou, China.

CNBC | Evelyn Cheng

SUZHOU, China — Just over a week after the U.S. and Chinese presidents met in Beijing, the world’s two largest economies are sending different messages about their priorities for Asia.

First is tariffs.

China’s economy relies significantly on exports — and the free-flow trade — as it accounts for about 28% of the goods made globally, according to CNBC calculations of World Bank data.

Beijing’s statements on Chinese President Xi Jinping and U.S. President Donald Trump’s summit last week have noted how duties will remain lower for longer, while the U.S. did not mention tariffs.

Then on Saturday, China’s Commerce Minister Wang Wentao told reporters that affirming the “vision” of a free trade agreement was a key outcome of the just-concluded Asia-Pacific Economic Cooperation trade ministers meeting.

“In the context of rising uncertain and destabilizing factors in global and regional economic development, members redirected their attention to the FTAAP (Free Trade Area of the Asia Pacific) with commitment to continuing advancing economic integration through the FTAAP agenda,” Wang said in Chinese, according to an official English translation.

However, when CNBC a day earlier asked a member of the U.S. delegation about FTAAP and free trade, the response focused on balanced trade, part of the Trump administration’s rationale for tariffs.

“FTAAP, is really, it’s more an agenda than it is a kind of destination,” said Casey K. Mace, the U.S. Senior Official to the APEC Forum. He noted the U.S. has been “active” in elements of FTAAP such as competitiveness, labor standards and trade facilitation.

China is the host for this year’s APEC meetings, set to culminate in November with a high-level gathering in Shenzhen. Trump and Xi are also expected to meet alongside that event.

‘Constructive strategic stability’

Second is what’s next for the U.S. and China.

There’s little detail yet on how the two sides will move forward with implementing “constructive strategic stability,” beyond China’s purchase of 200 Boeing airplanes and $17 billion annually in U.S. agricultural products through 2028.

A Chinese readout released early Saturday said Wang met Thursday in Suzhou with Rick Switzer, the U.S. Deputy Trade Representative and head of the U.S. delegation for the APEC trade ministers meeting.

The readout said both sides hoped to reach an agreement as soon as possible on the details of economic outcomes from the Trump-Xi meeting — an indication that differences still remain.

The U.S. embassy in Beijing and the U.S. State Department did not immediately respond to a request for comment.

The AI race

Third is a broadening of the U.S. and Chinese tech race into Asia.

The APEC trade ministers’ meeting reached a “new consensus” on digital trade cooperation, Wang said.

When asked to elaborate, Lin Feng, director-general of the Chinese Commerce Ministry’s department of international trade and economic relations, noted plans to make it easier for e-commerce companies to do business in the region, and a “commitment to strengthening trade exchanges related to AI.”

Lin noted efforts to “narrow the digital divide” but did not mention Chinese AI companies in particular.

While the U.S. has restricted the ability of Chinese companies to access advanced semiconductors for training AI models, Chinese businesses have tended to release AI models that are cheap – if not free – to use, and with capabilities that increasingly narrow the gap with their U.S. rivals.

On the U.S. side, Mace emphasized plans “to continue to position the U.S. tech companies, digital companies, as the leaders in the region.”

Mace said U.S. tech firms would be giving workshops at an APEC “digital week” in Chengdu in July. While China is the host of the event, “it’s an opportunity to engage with all 21 [APEC] economies,” he added.

The U.S. is one of the 12 founding members of APEC, which was launched in 1989 in Australia as an informal forum for discussions on free trade and economic cooperation. The multilateral trade organization now has 21 members, including mainland China, Hong Kong and “Chinese Taipei,” which joined the forum in 1991.

Wang did not comment on the “urgent official business” that had prevented him from chairing the opening session on Friday.

TLDR:

- XRP’s Open Interest has spiked sharply, pointing to aggressive position-taking in the futures market.

- XRP’s stable Market Cap suggests large holders are not yet distributing, reducing short-term crash risk.

- An overheated NVT Ratio shows XRP’s valuation is outpacing on-chain activity, making rallies fragile.

- The most probable XRP near-term scenario is an upside squeeze followed by a sharp correction afterward.

XRP is showing early signs of building short-term bullish pressure as several market indicators align. Open Interest has spiked in the futures market, reflecting fresh position accumulation among traders.

The NVT Ratio, however, continues producing irregular spikes while remaining at elevated levels. Market Cap has stayed stable, with no aggressive sell-off recorded from large holders.

These combined signals point to a potential squeeze setup, though overall market conditions remain fragile.

Rising Open Interest Signals Active Accumulation in XRP Futures

Open Interest in XRP’s futures market has risen sharply, reflecting aggressive position-taking by active traders. This type of OI increase, when paired with price support, typically strengthens short-term bullish momentum conditions.

The current market structure reflects that environment, though price follow-through will ultimately be the deciding factor. This pattern has historically served as a precursor to sharp directional moves in crypto.

Analyst PelinayPA flagged this pattern in a recent post, noting that XRP’s Market Cap has held steady. This stability suggests large investors are not yet actively exiting or distributing positions.

The probability of a sharp near-term downside crash therefore remains relatively low given the current setup.

That said, risks grow if OI keeps climbing while XRP fails to break new price highs. In that scenario, long squeeze pressure could intensify and produce sudden downside wicks in the market.

Traders watching the OI-versus-price relationship must stay alert for early divergence signals as conditions evolve.

Conversely, a breakout above resistance on rising OI could produce a short but powerful upside move. The current structure leans slightly bullish in the near term, though clear risks continue to persist.

Price action confirmation in coming sessions will separate genuine breakouts from false moves.

Overheated NVT Ratio Raises Fragility Concerns in XRP’s Market

The NVT Ratio is one of the key risk factors currently present in XRP’s broader market picture. It remains extremely elevated and continues producing irregular spikes.

A high NVT means the asset’s market valuation is growing faster than actual on-chain transaction volume. This disconnect between price and network activity is widely associated with fragile and unstable rallies.

Network usage is not expanding at the same rate as the broader market cap growth. That gap suggests price moves are not fully supported by genuine organic demand from the network. Short-term rallies built primarily on futures activity carry a notably elevated risk of sudden reversal.

Given elevated NVT alongside surging OI, an upside squeeze followed by a sharp pullback looks most likely. The initial move higher could be fast and aggressive, driven primarily by futures-market positioning.

Without stronger on-chain activity to support valuations, any rally in XRP remains structurally vulnerable to reversal.

For XRP traders, monitoring how both OI and NVT develop will remain a key priority. Should OI keep rising while XRP breaks new price highs, the squeeze could extend further to the upside.

But if network activity fails to catch up with market cap, correction risk stays persistently elevated across sessions.

The Clarity Act’s biggest outcome may be the creation of an entirely new market for “yield-as-a-service,” according to Joe Vollono, chief commercial officer at stablecoin infrastructure firm STBL.

At the center of the debate is Section 404 of the proposed legislation, which would prohibit Digital Asset Service Providers (DASPs) and their affiliates from offering yield solely as a function of holding a digital asset.

The provision could fundamentally reshape how crypto users earn returns, pushing the market away from passive “hold-to-earn” products and toward more active, compliant yield-generation strategies.

“What this effectively does is shift the industry from a hold-to-earn market to a use-to-earn market,” Vollono told CoinDesk in an interview. “You’re going to need compliant yield strategies to generate rewards on what would otherwise be idle capital.”

The Clarity Act has already cleared the Senate Banking Committee and is now expected to move into the full Senate to be merged with the Senate Agriculture Committee version of the bill before House reconciliation, with an optimistic timeline pointing to a full vote as early as July. Regulators would then have roughly 12 months to implement the framework.

Vollono, who spent more than seven years at Morgan Stanley and served at SIFMA, where he worked on industry advocacy and market structure issues, said the implications of the Clarity Act extend far beyond yield products themselves. Regulatory clarity, he argued, could finally unlock large-scale institutional participation in crypto markets.

“Once these issues are resolved, it allows capital at scale to enter the market,” he said. “That’s the real catalyst here.”

Passage of the Clarity Act is widely viewed as a potential inflection point for crypto markets because it would establish the first comprehensive U.S. regulatory framework for digital assets, ending years of uncertainty over whether and how tokens fall under Securities and Exchange Commission (SEC) or Commodity Futures Trading Commission (CFTC) jurisdiction.

The legislation would create clearer rules for exchanges, brokers, stablecoin issuers and decentralized finance platforms, a move many analysts say is necessary before large institutional investors, banks and asset managers can commit capital at scale. Supporters argue that regulatory clarity could reduce legal risk, improve consumer protections and give traditional financial firms the compliance framework needed to build crypto products and services in the U.S. rather than offshore.

The role of AI

The likely result, Vollono said, is the emergence of a middle layer of infrastructure providers focused on compliant yield generation. He said he expects many of those services to be powered by artificial intelligence acting as an orchestration layer for regulated capital flows.

Among the potential beneficiaries are decentralized finance (DeFi) infrastructure providers, vault curators, collateral management platforms, automated treasury services, lending markets and rewards systems.

“All of this can be automated by AI in a regulated market,” he said.

The underlying technology stack already exists, Vollono said, pointing to smart contracts, oracles, DeFi rails and API-based infrastructure that could be adapted to fit within a regulated framework.

“This creates a whole new world,” he said.

Legislation

The debate around the legislation has also exposed tensions between traditional banks and the crypto industry, particularly over stablecoins and deposit migration.

“There’s a lot at stake,” Vollono said. “Banks are worried about deposit flight, but I think that concern is largely overstated.”

He said that the traditional fractional reserve banking model depends on banks maintaining large capital bases that can be lent out to create credit and liquidity. If deposits migrate into tokenized dollars or yield-bearing blockchain products, that model could come under pressure.

Still, Vollono said he sees the eventual compromise as beneficial for incumbents rather than existentially threatening.

“Smart incumbents are going to compete,” he said. “Banks don’t necessarily have to give up market share.”

He suggested banks could eventually collateralize reserves to issue their own stablecoins and generate compliant yield under the Clarity framework, opening the door to entirely new business models.

Stablecoin 2.0

That dynamic is central to STBL’s own pitch.

The company describes itself as “stablecoin 2.0,” arguing for a shift away from the traditional centralized issuer model that dominates the market today.

Instead, STBL is building infrastructure that allows users to mint real-world-asset-backed stablecoins while retaining the economics generated by the underlying reserves.

“Users that provide value into the ecosystem should participate in the economics,” Vollono said.

The company’s infrastructure is designed to support compliant yield management while allowing users, rather than centralized issuers, to capture the yield generated by reserve assets.

For Vollono, the Clarity Act could provide the regulatory framework needed to accelerate that transition. “I’ll tell you what the Act makes clear: money-as-a-service has arrived,” he added.

Read more: Crypto Clarity bill has 30% chance of passing this year, Wintermute’s Hammond says

Ethereum’s native token has taken the most recent crypto market correction hard, with the asset diving to just over $2,000 earlier today, which became its lowest price point in almost two months.

Moreover, it has dropped by 17% since its monthly high at $2,425, and the overall landscape seems quite bearish. Although Santiment Intelligence believes this could be the necessary factor for a major trend reversal, the current environment is nothing short of underwhelming, to say the least.

More Trouble Ahead?

After it was stopped at $2,400, $2,300, $2,200, and $2,100 earlier this week, the latest crucial support to give in was the $2,050 level during today’s decline. According to popular analyst Ted Pillows, this opens the door for more profound corrections. Moreover, he warned that if ETH loses the psychological $2,000 support as well, new lows “will just be a matter of time.”

Fellow analyst CW noted that a large amount of ETH longs were liquidated on the way down. More specifically, data from CoinGlass shows that the total value of liquidated ETH longs is over $250 million on a daily scale, second only to bitcoin’s $380 million.

CW added that as short positions closed, the Open Interest declined significantly and the Net Position Delta increased. They concluded that high-leverage longs are getting wrecked, while bearish bets are closing, which could lead to some market calmness.

During the decline, $ETH long positions were liquidated in large amount.

Subsequently, as short positions closed, the Open Interest (OI) decreased and the Net Position Delta increased.

High-leverage long positions are being liquidated, and bearish bets are closing. pic.twitter.com/bTYuT7tjnG

— CW (@CW8900) May 23, 2026

OG Whale Returns

The silver lining for the Ethereum ecosystem at the moment is the return of an OG whale, as reported by Lookonchain. The analytics company’s data shows that this market participant, who is known for pocketing a 376x return on their initial ETH investment from 10 years ago, has started accumulating again.

On-chain data reveals that this whale has acquired over $8 million worth of ETH at prices of around $2,050. Previously, they sold when the altcoin stood above $2,850.

As the market drops, another #EthereumOG who made $34.2M(376x return) is buying the dip on $ETH!

10 years ago, this OG received 12,001 $ETH from ShapeShift at just $7.58 each.

Over a year ago, he sold them for 34.3M $USDC at $2,856, making $34.2M in profit – a 376x return.… pic.twitter.com/vSfrYyo2Bl

— Lookonchain (@lookonchain) May 23, 2026

The post Ethereum Tanks to 2-Month Low: Whales Return but Sub-$2K Fears Mount appeared first on CryptoPotato.

The European Central Bank has pushed back against proposals to expand euro stablecoin issuance, warning that broader access to stablecoins could undercut bank lending and complicate monetary policy. The concerns surfaced as a Brussels think tank argued in favor of loosening liquidity requirements for stablecoin issuers and potentially granting them access to ECB funding, a step aimed at boosting euro-denominated tokens in a market still dominated by dollar-backed rivals. The debate unfolds as Europe remains a major hub for stablecoin activity but remains a small player in terms of euro-denominated supply.

The pushback came after Bruegel, a Brussels-based think tank, presented a policy paper at an informal meeting of EU finance ministers in Nicosia, Cyprus. The authors argued that easing liquidity rules for euro stablecoin issuers and enabling some form of ECB liquidity or funding access could help the euro’s stablecoin market close the gap with dollar equivalents. The core question at the meeting: should Europe tilt toward central bank-style support for stablecoin issuers to improve competitiveness, or preserve traditional banking rails and monetary policy channels?

Key takeaways

- Bruegel’s proposal asks for looser liquidity requirements for euro stablecoin issuers and possible access to ECB funding to spur euro-denominated tokens in a market currently led by the dollar.

- The ECB’s position, led by President Christine Lagarde, signals potential risks to traditional banking: widespread stablecoin issuance could shift deposits away from banks and complicate monetary policy transmission.

- Despite heavy activity in Europe, euro stablecoins remain a tiny share of the market — euro-denominated tokens account for roughly 0.3% of total stablecoin supply, even as Europe conducts about 38% of global stablecoin transactions.

- EURC, the largest euro stablecoin, sits about 12th in global rankings, underscoring the gap to dollar-backed counterparts and the uphill battle to compete on issuance scale.

- As the EU reconsiders MiCA, regulators are weighing how to balance stability with innovation, with central banks cautious about granting new lenders-of-last-resort-style facilities to non-bank issuers.

ECBs stance vs. Bruegel’s case for euro stablecoins

Reuters reported that ECB finance ministers were warned that proposals to expand euro stablecoin issuance could weaken bank lending and complicate monetary policy. The tension centers on whether extending central bank-style support to stablecoin issuers would disintermediate traditional banks and hamper the ECB’s ability to steer interest rates and liquidity conditions. The Bruegel policy paper argues that in a euro-stablecoin market poised to compete with dollar tokens, reducing liquidity barriers and offering some ECB-friendly funding could unlock greater euro adoption.

The central bank perspective, however, remains skeptical. Lagarde and other senior policymakers have argued that even targeted support for stablecoins carries outsized risks. A prominent concern is the potential for stablecoins to pull value from banks during stress, destabilizing deposit bases and increasing funding costs for lenders. Over time, this could erode the effectiveness of the ECB’s policy transmission mechanism. Reuters notes that several central bankers at the meeting questioned the Bruegel proposal to treat stablecoin issuers as lenders-of-last-resort beneficiaries — a role currently reserved for regulated banks.

In a broader context, Lagarde has consistently warned about the trade-offs of widespread euro stablecoins. In a speech at the Banco de España LatAm Economic Forum, she highlighted that while euro stablecoins could raise demand for euro-area safe assets, the associated financial-stability risks, redemption pressures, and potential dampening of monetary policy transmission could outweigh benefits. Rather than pursuing a coin-based approach, Lagarde advocates a tokenized financial infrastructure anchored by central bank money, exemplified by initiatives like the Eurosystem’s Pontes project for wholesale settlement and the Appia roadmap for interoperable tokenized finance.

Officials at the informal Nicosia session also debated whether Europe should pursue tighter controls on redemptions of both US- and EU-issued stablecoins to guard against reserve runs, rather than expanding access to ECB funding. The discussion mirrors a broader regulatory crosswinds as the EU reviews its Markets in Crypto-Assets regulation (MiCA), which already requires stablecoin issuers to hold substantial reserves in liquid assets, in contrast to the lighter-touch approach seen in the US under the GENIUS Act.

For readers tracking regulatory momentum, the juxtaposition is clear: Europe is weighing how to encourage stablecoin innovation without destabilizing banks or undermining monetary policy. The MiCA review remains a live process, and how Brussels resolves the tension between stability and growth will shape the contours of euro stablecoins for years to come.

The euro stablecoin landscape: a market of contrasts

Even as European activity in stablecoins is sizable, the euro-denominated tokens have not translated into a proportional share of the global supply. Bruegel notes that Europeans conduct roughly 38% of global stablecoin transactions, yet euro-denominated tokens account for a mere 0.3% of total supply. In this context, Circle’s EURC stands as the largest euro stablecoin but ranks only 12th among all stablecoins by market presence, according to CoinMarketCap data.

The metrics spotlight a broader market dynamic: even with substantial regional activity, the euro-stablecoin ecosystem remains comparatively underdeveloped relative to the dollar-dominated landscape. This disconnect underscores why regulators and policymakers are anxious about sanctioning broader access to central bank-style liquidity for euro stablecoins. A deeper liquidity pool and stronger policy clarity could be necessary to lure more users and issuers into the euro stablecoin framework, but doing so risks amplifying channeling effects on banks’ balance sheets if not carefully calibrated.

From an investor and market participant perspective, the numbers imply a measured approach to euro-stablecoin exposure. While a more robust euro-stablecoin rail could facilitate cross-border payments and fintech use cases within the euro area, it could also compress bank funding dynamics if stablecoins offer a compelling alternative for redemption and settlement. The contrast between robust stablecoin activity in Europe and the relatively small euro-stablecoin supply highlights the opportunity for growth, but also the regulatory and systemic risks that policymakers want to manage.

Regulatory backdrop: MiCA, the US regime, and what investors should watch

The MiCA framework has been a central piece of Europe’s attempt to bring stability and oversight to the crypto markets, including stablecoins. Under MiCA, stablecoin issuers are expected to hold sizable reserves in liquid assets to back redemptions and maintain clear governance standards. Critics argue MiCA’s guardrails are more conservative than those seen in other jurisdictions, potentially slowing innovation, while supporters say they are essential for consumer protection and financial stability.

In the United States, the GENIUS Act has been cited as a contrasting approach, often viewed as lighter-touch than European rules. The regulatory divergence between the EU and US is part of the broader debate about which model best fosters innovation while preserving financial stability. The Bruegel paper’s call for closer ECB involvement would represent a further step toward a hybrid framework that blends central bank influence with market-based stablecoins, but it also intensifies questions about sovereignty over monetary policy transmission and the steadiness of the banking sector.

As EU policymakers monitor these tensions, observers will want to watch several indicators: the pace of MiCA updates, the direction of any policy shifts toward or away from lender-of-last-resort-style support for issuers, and the real-world adoption of euro stablecoins by businesses and consumers. For traders and institutions with euro exposure, policy clarity could reduce regulatory risk, while ambiguity could keep headlines and volatility elevated as the regulatory calculus evolves.

One point of ongoing interest is how European banks and payments networks might respond to a more fully realized euro-stablecoin architecture or to a tokenized-finance ecosystem anchored by central-bank money. If the region leans into tokenized settlements as a complement to existing rails, as Lagarde and the Eurosystem have suggested, stablecoin issuance could become part of a broader shift toward interoperable, digital-first financial infrastructure — a trend that could shape liquidity patterns, settlement costs, and cross-border flows in the years ahead.

For investors and builders focused on the euro digital ecosystem, the key takeaway is that the regulatory and central-bank stance remains evolving and nuanced. While Bruegel’s proposals aim to bridge the euro stablecoin gap, the ECB’s current policy posture prioritizes financial stability and the integrity of monetary policy transmission. In practice, this means any move to widen ECB support for stablecoin issuers will likely come with stringent safeguards and clear actuarial metrics to avoid destabilizing bank funding or triggering unintended liquidity stress scenarios.

Looking ahead, market participants should monitor two threads: first, whether the EU logistics and MiCA reform process yields a policy path that meaningfully enhances euro-stablecoin viability without compromising stability; second, whether technology-led solutions like tokenized finance infrastructures—publicly backed by central-bank money—gain traction as the favored route for cross-border settlement and wholesale finance. The outcome will influence not only euro-stablecoins but the broader trajectory of digital finance within the euro area and beyond.

As this regulatory dialogue unfolds, readers should keep an eye on how the balance between innovation and stability shifts. The next milestones to watch include the next formal statements from the ECB on stablecoins, updates to MiCA proposals, and any concrete policy instruments that could align euro-stablecoins with central-bank-backed settlement frameworks while preserving the monetary authority’s ability to manage inflation and banking stability.

Market observers will want to watch for continued disclosures about stablecoin liquidity, reserve composition, and redemptions during periods of stress. If Europe signs on to a pathway that marries tokenized finance with robust oversight, euro-stablecoins could gradually grow from a fringe instrument into a meaningful component of the region’s digital-finance toolbox — provided the balance between accessibility and resilience is maintained.

Source mentions and context include Reuters’ reporting on ECB pushback, Bruegel’s policy paper presented in Nicosia, and CoinMarketCap’s ranking data for euro stablecoins. For readers seeking deeper background, cross-references to related coverage on MiCA reviews and Lagarde’s public remarks offer a fuller view of how EU policymakers are framing the path ahead.

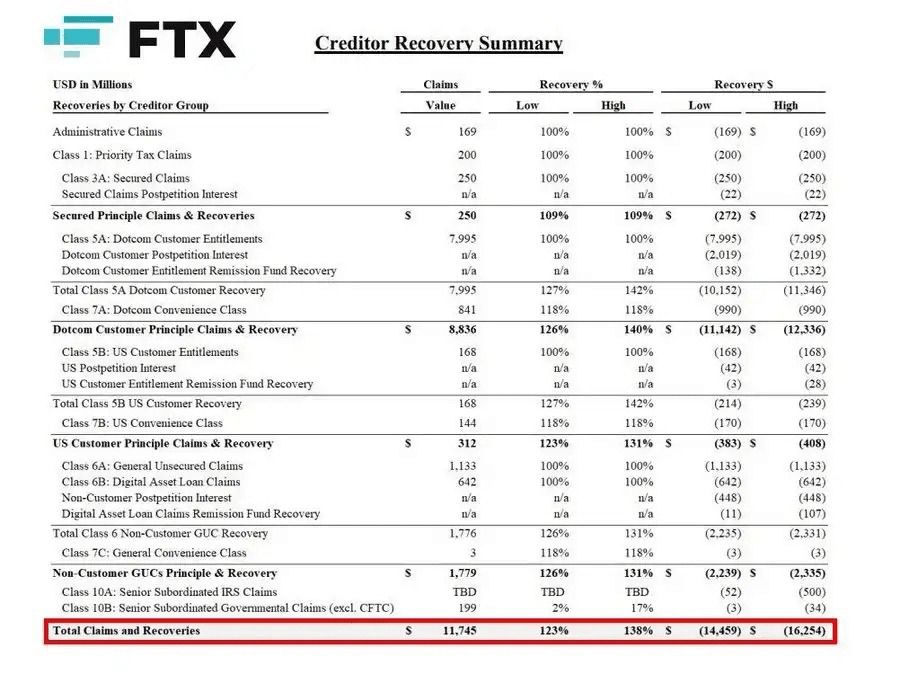

Fenwick & West, FTX’s former lead outside counsel, agreed to pay $54 million to settle claims. The claims allege that the firm helped enable the exchange’s $8 billion fraud.

The federal court filed the preliminary settlement in Miami and requires judicial approval. Litigator David Boies, representing the plaintiffs, said the deal was reasonable and would spare both sides prolonged, complex litigation.

From Advisor to Defendant

Silicon Valley law firm Fenwick advised FTX as it grew into one of the largest crypto platforms globally before its November 2022 collapse.

Plaintiffs alleged the firm went beyond routine legal counsel, arguing Fenwick crafted strategies that enabled FTX’s fraud and built legal structures that allowed customer funds to be commingled with those of Alameda Research, FTX’s sister trading firm.

Fenwick pushed back, maintaining the firm had no knowledge of wrongdoing at FTX. In a statement, the firm said:

“…was not aware of the fraud at FTX, stands by the integrity of its legal work, and disputes wrongdoing of any kind, as we have consistently stated throughout this matter.”

The firm, which employs more than 500 lawyers, said it looks forward to moving past the matter.

Second Wave of FTX Legal Actions

The $54 million deal forms part of a broader second wave of agreements in the legal saga. It follows earlier asset-recovery lawsuits targeting former executives and counterparties. A separate $525 million suit against Fenwick and its partners remains active, leaving significant exposure unresolved.

The court sentenced FTX founder Sam Bankman-Fried in 2024 to 25 years in prison for stealing $8 billion from customers. He has appealed his conviction.

The bankruptcy estate has since distributed over $5 billion to creditors as part of its structured recovery plan, completed a third creditor repayment round in September 2025, and operated under a court-approved FTX compensation plan that formalized the victim recovery process.

Whether the Fenwick agreement signals further settlements from other professional advisors tied to FTX remains to be seen as the litigation’s second wave continues.

The post Fenwick Agrees to Pay $54 Million to Settle FTX Customer Claims appeared first on BeInCrypto.

TLDR:

- Polymarket lost over $600K after attackers exploited an outdated backend operational key.

- Blockchain investigators tracked stolen funds moving through 16 wallets and ChangeNOW.

- User funds and market resolution contracts remained secure despite the Polygon wallet breach.

- The exploit exposed how legacy permissions and weak key rotation create major security risks.

A private key compromise hit Polymarket on May 22, 2026, draining over $600,000 in internal operational funds. The incident affected a wallet tied to backend infrastructure on the Polygon network.

Polymarket later confirmed that user funds remained safe and that market resolution was not disrupted. The breach traced back to an old private key that still held too much operational access, raising questions about internal key management practices across decentralized platforms.

How the Drain Unfolded

On-chain activity first flagged unusual fund movements from Polymarket-linked infrastructure on Polygon. Blockchain investigator ZachXBT identified the movement as a possible exploit early on.

Shortly after, PeckShieldAlert confirmed that two attacker addresses had drained roughly $520,000. Part of those funds was then routed to the exchange service ChangeNOW.

On-chain analytics platform Bubblemaps tracked the attacker pulling approximately 5,000 POL tokens every 30 seconds. The speed of the drain pushed loss estimates upward throughout the day.

Figures moved from $520,000 to $600,000, then approached $700,000 across different trackers. The stolen funds were split across 16 separate addresses and funneled through centralized exchanges and other services.

Early confusion arose because the affected wallet had ties to Polymarket’s market-resolution setup. Many observers initially suspected something had gone wrong with the platform’s outcome contracts. Those concerns turned out to be unfounded, as the contracts themselves were not involved.

Polymarket team member ShantikiranC clarified that the issue stemmed from an old private key used for internal reward payouts.

The key was not linked to core contracts or user-facing infrastructure. However, it still carried enough access to allow the attacker to drain a significant amount of funds.

Containment Steps and Key Management Review

Following the breach, Polymarket began rotating backend service keys immediately. ShantikiranC confirmed the team was also auditing other internal secrets to check for further exposure. The response followed a standard protocol for private key and backend secret leaks.

Developer Josh Stevens noted that the affected wallet’s permissions had been revoked. He added that the team was migrating keys to a Key Management System, commonly known as KMS. A KMS provides a more secure environment for storing and handling sensitive cryptographic keys.

The incident raised a broader question about how an outdated internal key retained that level of access for so long.

In decentralized platforms, operational keys often accumulate permissions over time without regular audits. This case showed how legacy access can become a liability even when core contracts are secure.

The Polymarket incident serves as a reminder that internal operational security requires the same level of attention as smart contract audits.

Key rotation, permission scoping, and secure storage are not optional steps. For platforms handling large volumes of on-chain activity, these practices are a basic operational requirement.

Grayscale named four blockchains as the top Clarity Act winners in a research note published on May 22.

Summary

- Grayscale named Ethereum, Solana, BNB Chain and Canton Network as the four chains best placed for institutional capital after the Clarity Act passes.

- The four chains lead the market by tokenised asset value, stablecoin supply and DeFi total value locked, which Grayscale uses as its primary ranking criteria.

- Grayscale also named Avalanche, Base, Arbitrum, Hyperliquid and Tron as secondary beneficiaries with significant on-chain finance exposure.

Grayscale published a research note on May 22 identifying Ethereum, Solana, BNB Chain, and Canton Network as the four blockchains best placed to absorb institutional capital once the Clarity Act is signed into law. “Regulatory clarity is coming, and a rising tide will likely lift digital assets broadly,” Grayscale wrote.

The four chains were selected because they lead across three key metrics: tokenized asset value, stablecoin supply and transaction volume, and DeFi total value locked. Ethereum leads in tokenized assets, followed by BNB Chain and Solana, while Canton Network rounds out the list as the leading institutional settlement network.

Why Grayscale puts Canton Network ahead of Cardano

Canton Network’s inclusion over Cardano corrects some initial misreporting from other outlets. Canton holds over $348 billion in tokenized real-world asset value, hosts the DTCC’s tokenized Treasury pilot, and counts JPMorgan, HSBC, and Visa among its validators.

“$350 billion settles daily on Canton, with over $6 trillion in tokenized real-world assets and institutions like JPMorgan and DTCC building in production,” the Canton Network said recently.

Zach Pandl, Grayscale’s head of research, noted Bitcoin will also benefit from regulatory clarity as the industry’s most secure asset. Crypto.news has reported on Grayscale’s December 2025 outlook predicting bipartisan legislation would unlock a new institutional era for digital assets.

What the secondary tier of Clarity Act beneficiaries looks like

Grayscale also flagged Avalanche, Base, Arbitrum, Hyperliquid, and Tron as networks with significant on-chain finance exposure that would benefit from greater regulatory clarity. These chains sit below the primary four in tokenized asset value but have established DeFi ecosystems.

Crypto.news has tracked Grayscale’s active ETF expansion strategy across multiple chains, reflecting the same analytical framework that underpins its Clarity Act beneficiary list.

The Clarity Act cleared the Senate Banking Committee on a 15-9 bipartisan vote on May 14. It now needs a Senate floor vote, House reconciliation, and a presidential signature before Grayscale’s picks become regulated beneficiaries.

Crypto.news has covered the compressed legislative calendar that gives the bill its final window before the 2026 midterms. The Ethereum (ETH) page tracks price reaction as the bill’s prospects develop.

The European Central Bank (ECB) signaled serious caution on proposals to widen euro stablecoin issuance, warning that such moves could weaken bank lending and complicate the conduct of monetary policy. The concerns emerged as Brussels-based think tank Bruegel published a policy paper ahead of an informal gathering of EU finance ministers, urging lighter liquidity requirements for stablecoin issuers and even potential access to ECB funding to help euro-denominated tokens compete with dollar-backed rivals.

According to Bruegel’s analysis, Europe accounts for about 38% of global stablecoin activity, yet euro-denominated tokens represent roughly 0.3% of total supply. Circle’s EURC, the largest euro stablecoin, sits around 12th in the global ranking by market size, according to CoinMarketCap. The policy paper was presented during a two-day informal meeting of the Economic and Financial Affairs Council in Nicosia, Cyprus, and has since drawn a pointed response from the ECB leadership.

The central question debated in Nicosia was whether Europe should close the euro-stablecoin gap by extending central-bank-style support to issuers. For now, the ECB’s position appears resistant to such a shift.

Key takeaways

- ECB officials publicly warned that broadening euro-stablecoin issuance could undermine traditional banking models and complicate monetary policy transmission.

- Bruegel proposed easing liquidity requirements for stablecoin issuers and granting them access to ECB funding to spur euro-stablecoin competitiveness against dollar tokens.

- European stablecoins handle a substantial share of global activity (38%), but euro-denominated tokens remain a small fraction of supply (about 0.3%), with EURC ranking 12th globally by market size.

- ECB President Christine Lagarde led the opposition to central-bank-backed stability facilities for issuers, highlighting risks to bank deposits, disintermediation, and higher funding costs for banks.

- The debate sits within a broader policy framework, including MiCA regulation, the US GENIUS Act, and ongoing consideration of tokenized financial infrastructure backed by central-bank money.

Policy proposals and regulatory context

The Bruegel paper presented at the Nicosia meeting advocates a more permissive stance toward euro-stablecoin issuers, arguing that easing liquidity requirements and providing potential ECB funding access would help euro tokens compete with dollar-dominated equivalents. Proponents contend that an integrated, euro-backed stablecoin market could bolster EU financial sovereignty and efficiency in cross-border payments, while leveraging the ECB’s balance-sheet capacity to support liquidity needs in times of stress.

ECB leadership, however, has signaled a different path. In the discussions surrounding the paper, ECB officials underscored potential destabilizing effects of stablecoin issuance on traditional banks, particularly through the displacement of deposits from banks to stablecoin issuers. At scale, this disintermediation could raise bank funding costs and hamper the central bank’s ability to steer policy through traditional channels. Reuters reported that Lagarde and fellow policymakers questioned whether the ECB should assume a lender-of-last-resort role for stablecoin firms—a function currently reserved for regulated banks—thereby challenging a core aspect of the euro-area financial safety net.

The broader regulatory backdrop includes the EU’s Markets in Crypto-Assets framework, or MiCA, which is under review as the bloc weighs how to adapt rules for stability tokens. MiCA already imposes requirements on stablecoin issuers to hold substantial reserves in liquid assets, a regime that contrasts with the more permissive posture seen in some other jurisdictions, such as the US GENIUS Act. The Bruegel position raises a legal and policy question: should EU policy converge toward centralized funding and explicit backstops for stablecoins, or should it preserve sharper distinctions between digital assets and fiat-backed money?

Banking stability, monetary policy, and market structure

Central bankers at the Nicosia gathering largely dismissed the Bruegel notion of extending an ECB lender-of-last-resort facility to stablecoin issuers. The ECB’s stance reflects a precautionary calculus: stablecoins can alter the balance between banks and non-bank funding channels, potentially reducing the resilience of the traditional banking system and weakening monetary policy transmission mechanisms. Lagarde’s comments emphasize that, while euro-stablecoins could stimulate demand for euro-area safe assets, the associated trade-offs—especially financial stability risks, redemption pressures, and diminished policy effectiveness—outweigh the perceived benefits.

Beyond stability concerns, Lagarde has repeatedly highlighted the importance of building tokenized financial infrastructure with central-bank money at its core. She pointed to Europe’s ongoing initiatives—such as the Eurosystem’s Pontes project for wholesale settlement and the Appia roadmap for interoperable tokenized finance—as more predictable avenues for modernizing payments and settlement without compromising monetary sovereignty. This stance aligns with a policy preference for regulated, assets-backed digital finance that retains direct anchorage to central bank money, rather than broad market expansion of private-issued stablecoins.

At the same time, Bruegel’s authors cautioned that stricter EU rules relative to the United States could hasten digital dollarization, pushing stablecoin activity beyond the bloc’s borders. While some participants acknowledged the risk, others argued for targeted measures to manage redemptions from European-issued stablecoins and to limit reserve runs, thereby shielding the euro-area financial system from abrupt shifts in liquidity.

EU regulatory landscape and international considerations

The ongoing MiCA review sits at the center of EU policy discussions about crypto regulation, with implications for issuers, exchanges, and institutional players operating across European borders. A stricter regime—potentially complemented by efforts to restrict redemptions of both US- and EU-issued stablecoins within the bloc—could offer a bulwark against reserve runs but may also dampen innovation and competitiveness in a global market where dollar-backed tokens have established a deep liquidity pool.

Comparative regulatory dynamics are evident in the US framework, where the GENIUS Act and other legislative developments reflect a more permissive stance toward certain digital assets, albeit under ongoing oversight. Proponents of the euro-area approach argue that clear, robust requirements—aligned with MiCA—are essential for safeguarding financial stability and ensuring that any expansion of euro-stablecoin activity remains within the ECB’s reach to guard against macroeconomic spillovers.

Institutional implications extend to licensing, supervisory oversight, and cross-border cooperation. As European institutions weigh the balance between fostering a competitive euro-stablecoin market and preserving the integrity and resilience of the banking system, firms operating in the space should assess how MiCA provisions, any future ECB facilities, and potential liquidity or redemption controls could shape European operations, capital planning, and compliance programs.

Closing perspective

EU policymakers are navigating a delicate equilibrium between unlocking the strategic benefits of euro-stablecoins and maintaining robust financial stability and monetary policy effectiveness. The debate in Nicosia reflects deeper questions about the role of central-bank money in a digitized payments landscape and the institutional safeguards required to prevent destabilizing shifts in liquidity. As MiCA modernization progresses and cross-border dynamics evolve, banks, issuers, and institutional investors should monitor regulatory alignments, potential lender-of-last-resort considerations, and the trajectory of Europe’s tokenized-finance infrastructure—alongside ongoing assessments of how these policy choices will affect cross-border payments, reserve management, and compliance frameworks.

The U.S. Securities and Exchange Commission has cleared Nasdaq’s plan to bring cash-settled Bitcoin index options to the Philadelphia Stock Exchange, a move that could broaden regulated exposure to Bitcoin for traders across institutions and retail alike.

The contracts are European-style and reference the Nasdaq Bitcoin Index, a benchmark that tracks one-hundredth of the CME CF Bitcoin Real Time Index. The index updates with data from major cryptocurrency venues roughly every 200 milliseconds. The SEC’s order granting accelerated approval was published on Friday.

Unlike options on spot Bitcoin ETFs, these are cash-settled instruments. At expiration, holders receive the difference between the Bitcoin spot price and the strike price, with no physical Bitcoin delivered and no risk of early assignment. This structure provides a streamlined route for market participants to express views on Bitcoin’s price without handling the underlying asset.

Trading will occur under the QBTC ticker on Phlx. Each contract moves in $0.01 increments, and the order sets a per-side limit of 24,000 contracts. The SEC notes this cap corresponds to roughly 0.12% of Bitcoin’s circulating supply, underscoring the scale of regulated exposure being introduced to the market.

Key takeaways

- Nasdaq’s cash-settled QBTC options cleared by the SEC for listing on Phlx, expanding regulated Bitcoin exposure.

- Contracts are European-style and cash-settled, with no Bitcoin delivery or early assignment risk.

- Minimum tick of $0.01 and a per-side cap of 24,000 contracts (about 0.12% of circulating Bitcoin).

- Trading cannot begin until the CFTC grants exemptive relief, due to Bitcoin’s commodity status and CFTC jurisdiction.

- The move reflects a broader, more crypto-friendly tilt in the SEC, including talks of policy innovations to enable tokenized trading on decentralized platforms.

CFTC relief and the jurisdiction puzzle

Even with SEC clearance, QBTC options cannot commence trading until the Commodity Futures Trading Commission provides its own exemptive relief. The CFTC’s involvement is required because Bitcoin is classified as a commodity, placing such instruments under the agency’s purview. In a filing, CME Group argued last year that these contracts fall squarely under the CFTC’s exclusive jurisdiction.

The SEC noted that Section 717 of the Dodd-Frank Act does not confine its reach to “novel derivative products” and can contemplate concurrent jurisdiction where the CFTC grants relief. The agency pointed to existing examples—such as mixed swaps and security futures—to illustrate how the two regulators can share oversight in practice.

A broader turn toward crypto-friendly regulation and innovation

The approval arrives amid a shift in the SEC’s approach to crypto regulation. Under Chairman Paul Atkins, the agency has moved to reduce select enforcement actions from the previous administration and has signaled a desire for clearer rules that foster innovation. In related coverage, the agency has been exploring pathways to facilitate blockchain-based trading and other novel mechanisms within a coherent regulatory framework.

Industry observers have noted that the SEC is actively examining an “innovation exemption” that could permit tokenized trading of public company shares on decentralized platforms, potentially circumventing company-level consent in certain scenarios. This concept, reported by Cointelegraph, highlights the push toward more permissive, yet thoughtfully regulated, on-chain financial activity. You can read Cointelegraph’s coverage on the proposed exemption here: Cointelegraph on the innovation exemption.

As the market digests this development, investors and traders will need to watch three things: whether the CFTC relief is granted on a timely basis, how liquidity and price discovery develop for QBTC, and what broader regulatory clarifications might emerge around other Bitcoin-linked derivatives. The new QBTC product sits at the intersection of regulated access, price accuracy (owing to the tight 200 ms index updates), and the evolving boundary between traditional markets and crypto-native mechanisms.

Ultimately, the QBTC rollout could offer a useful gauge of how institutional-grade Bitcoin exposure can coexist with a robust regulatory perimeter. If liquidity builds and the CFTC clears the path, QBTC may become a meaningful complement to existing futures and other Bitcoin derivatives, shaping hedging and speculation in a landscape that remains dynamic and occasionally unsettled.

Look for updates on the CFTC decision timeline and early trading activity, as well as any additional SEC policy signals that could influence the design and appetite for future crypto-linked instruments in regulated exchanges.

TLDR:

- Bitcoin fell to $74,300 Saturday as US military preparations against Iran rattled crypto markets badly.

- Nearly $945 million in leveraged crypto positions were liquidated, mostly long bets caught off guard.

- The total crypto market cap dropped 3% to $2.5 trillion within 24 hours, per CoinGecko data released.

- Pakistan and Qatar are brokering talks, but negotiators report no real progress on any drafted deal.

Bitcoin dropped below $75,000 on Friday, extending losses into Saturday as geopolitical tensions between the United States and Iran rattled crypto markets.

The broader digital asset market shed roughly 3% of its total value within 24 hours, pushing the combined market cap to $2.5 trillion.

Leveraged traders absorbed the brunt of the damage, with nearly $945 million in positions wiped out across crypto exchanges during the period.

Source: Coingecko

Geopolitical Pressure Pushes Bitcoin to $74,300

Bitcoin touched a low of $74,300 on Saturday morning as risk sentiment deteriorated sharply. Reports emerged that the US military and intelligence community were preparing for possible strikes against Iran.

CBS News cited sources who confirmed preparations were underway, though no final decision had been reached on Friday.

President Trump canceled his planned attendance at Donald Trump Jr.’s wedding and returned to the White House.

This schedule change raised concern among traders and market observers watching the developing situation. Such visible shifts in presidential movement often signal heightened urgency behind closed doors.

The White House maintained its position that Iran must not obtain a nuclear weapon or retain enriched uranium. Officials reiterated that all military options remain on the table if Tehran rejects the latest American proposal.

Iran’s Revolutionary Guard responded by warning of severe retaliation and a possible widening of conflict beyond the Middle East region.

A new US proposal was delivered Wednesday through intermediaries, including Pakistan and Qatar. Both countries are working urgently to broker a last-minute agreement between the two sides.

However, negotiators described the process as difficult, with drafts exchanged daily but no meaningful progress recorded.

Leveraged Traders Take the Hardest Hit Amid Market Selloff

The sudden drop in sentiment caught many leveraged traders completely off guard in crypto markets. CoinGlass data shows approximately $945 million in leveraged positions were liquidated during the market downturn.

The bulk of those losses came from long positions, meaning traders were betting on continued price increases.

Ethereum and major altcoins followed Bitcoin lower as selling pressure spread across the market. The total crypto market capitalization fell 3% to $2.5 trillion within 24 hours, according to CoinGecko data.

Broad-based losses of this kind typically reflect macro-driven fear rather than any crypto-specific development.

Fears around the Strait of Hormuz added another layer of concern for markets already on edge. A disruption to that critical oil shipping lane could push energy prices higher and complicate inflation expectations globally. Rising inflation tends to reduce appetite for speculative assets, including cryptocurrencies.

The fragile ceasefire reached in early April between the US and Iran had briefly stabilized conditions. That calm now appears increasingly uncertain as military preparations and diplomatic tensions run parallel.

Until clearer signals emerge from negotiations, crypto markets are likely to remain sensitive to any escalation in the region.

THE CFTC CHAIR IS ABOUT TO UNLEASH XRP! (HUGE NEWS!)

Family of sisters who drowned in Brighton ‘don’t have answers’ about why they were there | News UK

Firefly Aerospace FLY Stock Surges 15% on Strong Q1 Results and Defense Contracts

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

Register Renaming | Hackaday

THE CFTC CHAIR IS ABOUT TO UNLEASH XRP! (HUGE NEWS!)

Ripple XRP 309-PAGE BILL EXPOSED! (NEW CLARITY Act, $8 Billion ETF Pipeline & The May 21 Deadline)

#music #vikram #automobile #money #luxury #viral #trendingshorts #lamborghinni

-

Crypto World2 days ago

Crypto World2 days agoBlockchain.com files with SEC for U.S. IPO

-

Fashion19 hours ago

Fashion19 hours agoHoliday Weekend Open Thread – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoIntesa Sanpaolo’s crypto holdings jump to $235M as XRP enters

-

Business23 hours ago

Business23 hours agoDell Technologies DELL Stock Surges 15% on AI Server Momentum and Analyst Upgrades in 2026

-

Crypto World23 hours ago

Crypto World23 hours agoSpace X IPO Is ‘Bad News’ for Tech Stocks: But What About Bitcoin?

-

Fashion6 days ago

Fashion6 days agoOn the Scene at Gucci’s Cruise Show in New York City: Mariah Carey, Kim Kardashian, Lindsay Lohan, Iman, and More!

-

Politics19 hours ago

Politics19 hours agoMakerfield: a tale of two social-media histories

-

Crypto World3 hours ago

Crypto World3 hours agoRobinhood crypto COO Tanya Denisova exits

-

Tech1 day ago

Tech1 day agoA 0.12% parameter add-on gives AI agents the working memory RAG can’t

-

Crypto World23 hours ago

Crypto World23 hours agoAI infrastructure race heats up as IREN pitches full-stack strategy, WhiteFiber lands $160M deal

-

Fashion6 days ago

Fashion6 days agoAmazon Sundays: Memorial Day Hosting

-

Entertainment6 days ago

Entertainment6 days agoOff Campus Easter Eggs Explained: Characters, Stories, More

-

Crypto World1 day ago

Crypto World1 day agoBitcoin Accumulation Weakens as BTC Realized Losses Hit $600M

-

Crypto World5 days ago

Revolut Launches Dogecoin Debit Card Across UK and EU

-

Tech2 days ago

Tech2 days agoWhatsApp ads could make Irish debut after discussions with DPC

-

NewsBeat2 days ago

NewsBeat2 days agoCharity run by Reform leader Malcolm Offord accused of ‘law breaking’ over Scottish registration

-

Sports2 days ago

Sports2 days ago2026 CJ Cup Byron Nelson leaderboard: Brooks Koepka finds putting stroke in Round 1

-

Business6 days ago

Australia defends property tax changes designed to fix ‘broken’ housing

-

Crypto World1 day ago

Crypto World1 day agoTrump Media’s Bitcoin Stash Shrinks Again as 2,650 BTC Lands on Crypto.com

-

Business1 day ago

Business1 day agoTrump Invests $1M-$5M in Kura Sushi USA Chain With 27 California Locations

You must be logged in to post a comment Login