Crypto World

Banks vs the CLARITY Act

The CLARITY Act cleared the Senate Banking Committee 15-9 on May 14, 2026, but the biggest threat to its passage was never the crypto skeptics or the SEC holdouts. It was the American Bankers Association. The ABA spent April and May running an emergency lobbying campaign to close what it calls the “stablecoin yield loophole” in the bill, a provision that lets crypto exchanges pay activity-based rewards on stablecoin balances. The ABA’s own research estimates that yield-bearing stablecoins could grow the market from $300 billion to $2 trillion at the direct expense of bank deposits, reducing lending capacity by 20 percent or more. The fight is not about consumer protection or financial stability. It is about banks defending a profit model built on zero-yield checking accounts against a structurally superior alternative. This is the political fight nobody is properly explaining.

Summary

- The CLARITY Act’s stablecoin rewards provision has become the main flashpoint between the crypto industry and U.S. banking groups over fears of deposit migration from traditional banks.

- The American Bankers Association warned that yield-bearing stablecoins could expand the market to $2 trillion and reduce lending capacity across consumer, small business, and agricultural sectors.

- Crypto industry advocates argued that banks are defending low-yield deposit models as exchanges push for activity-based stablecoin rewards under the proposed legislation.

What the loophole actually is

The CLARITY Act, in its current form, contains a provision that has become the most contested single fight in crypto legislation in 2026. Most coverage refers to it vaguely as “stablecoin yield provisions” without explaining what is actually at stake. The specifics matter.

The 2025 GENIUS Act, which established federal stablecoin regulation, prohibits stablecoin issuers from paying interest or yield on payment stablecoins. The ban applies to the issuer (Circle for USDC, Tether for USDT, Ripple for RLUSD, Paxos for various tokens). The intent was to keep stablecoins working as payment instruments rather than competing with bank deposits.

The CLARITY Act contains language that, as currently drafted, lets crypto exchanges and digital asset service providers offer rewards on stablecoin balances held with them, even though the underlying issuer cannot pay yield directly. The Tillis-Alsobrooks compromise language, released in early May, refined the original draft. The compromise prohibits rewards that are “economically or functionally equivalent to the payment of interest or yield on an interest-bearing bank deposit.” But it allows rewards tied to “activity-based” participation in exchange membership programs, including rewards calculated by reference to balance, duration, and tenure.

That last clause is the loophole the banking industry is fighting. From the ABA’s perspective, an exchange offering a 4 percent reward on USDC balances held in a membership program is functionally identical to a bank paying 4 percent interest on a checking account. The fact that the reward is technically tied to “activity” rather than balance does not change the economic reality for the consumer. The depositor sees yield. The depositor moves money. The bank loses the deposit.

The banking industry is correct this is a loophole in the original GENIUS Act framework. Whether it should be closed is the political fight that has dragged CLARITY’s path through the Senate Banking Committee.

The deposit flight argument

The American Bankers Association’s central argument against the CLARITY language is the threat of deposit flight, and the numbers the ABA cites are striking enough to deserve serious examination.

On April 13, 2026, the ABA published its own commissioned study estimating that yield-bearing stablecoins could grow the global stablecoin market from approximately $300 billion today to $2 trillion within several years. The growth, the ABA argues, would come largely at the direct expense of traditional bank deposits, particularly checking accounts and money market accounts that currently pay little or no interest.

A coalition of banking trade groups, including the ABA, Bank Policy Institute, Independent Community Bankers of America, Consumer Bankers Association, and Mid-Size Bank Coalition of America, wrote to Senate Banking Committee leaders in early May, warning that “research indicates deposit flight driven by the widespread adoption of yield-bearing stablecoins could reduce consumer, small-business, and agricultural lending by one-fifth or more.”

This is the headline number that gets cited in coverage. A 20 percent reduction in lending capacity would be a material macroeconomic event. Banks fund commercial loans, mortgages, small business credit, and agricultural lending substantially from deposit bases. If deposits flee to yield-bearing stablecoins, the funding capacity for those loans shrinks proportionally. The banks’ argument is that this is not a marginal concern. It is a structural threat to the way credit flows through the US economy.

The argument has surface plausibility. The FDIC’s own analysis of the 2023 spring bank failures (Silicon Valley Bank, Signature Bank, First Republic) found depositors with substantial uninsured funds were far more likely to run during stress events than insured retail depositors. The pattern suggests deposit stability is more fragile than banks publicly admit, particularly for uninsured balances and sophisticated depositors who actively manage cash positions.

What the deposit flight argument leaves out is the most important context. American checking accounts currently pay close to nothing. The national average interest rate on checking accounts is approximately 0.07 percent. On savings accounts, the average is approximately 0.43 percent. Both numbers have stayed near zero through the entire post-2008 era of low interest rates and have not risen materially even as the Federal Reserve raised the federal funds rate to over 5 percent in 2024.

The gap between what banks pay depositors and what banks earn on those same deposits has been one of the most profitable elements of the banking business for over a decade. Banks take in deposits at near-zero cost, lend them out at much higher rates, and capture the spread. The arrangement works for banks precisely because depositors have had no comparable alternative.

Yield-bearing stablecoins backed by US Treasuries can offer 3 to 5 percent returns to holders, depending on the underlying yield environment. The math is not subtle. A depositor with $10,000 in a zero-yield checking account is giving up roughly $400 per year in potential interest income. A depositor with $100,000 across various bank accounts is giving up roughly $4,000. The choice between zero yield in a bank account and 4 percent yield in a tokenized money market alternative is not a choice most rational consumers would make in favor of the bank, if the alternative existed at scale.

This is what the ABA’s deposit flight argument actually means in plain English. Banks are afraid the loophole will let consumers earn what their deposits should arguably have been earning all along. The “deposit flight” the ABA is warning about is, in part, consumers rationally responding to a better product.

What the banks are actually defending

The honest framing of the banking industry’s position requires understanding what banks are actually trying to protect.

The first thing banks are protecting is the zero-yield checking account business model. American banks currently hold approximately $17 trillion in customer deposits. A substantial portion of those deposits are in non-interest-bearing checking accounts or low-interest savings accounts. The interest rate banks pay on these deposits has been compressed near zero for over a decade. The income banks generate from lending these deposits at market rates is, in turn, one of the most reliable profit streams in the industry.

If stablecoins offering 4 to 5 percent yield became widely available and easy to access, the economic logic for keeping money in zero-yield bank accounts would weaken substantially. Banks would face a choice: raise deposit rates to compete (which would compress their net interest margins and reduce profitability), or lose deposits to stablecoin alternatives (which would force them to seek more expensive funding sources or reduce lending).

The second thing banks are protecting is the regulatory moat. Banks run under extensive regulatory requirements (capital adequacy, liquidity coverage, FDIC insurance assessments, Community Reinvestment Act obligations, Bank Secrecy Act compliance) stablecoin issuers do not face in the same form. The CLARITY Act would let stablecoin-related products compete with bank deposits without imposing equivalent regulatory burdens on the stablecoin side. Banks argue this creates an unlevel playing field. The argument has merit.

The third thing banks are protecting is the structural role of banks in credit creation. Under the current US banking system, deposits at commercial banks are the primary funding source for consumer and commercial lending. If deposits migrate to stablecoins, the funding model has to adjust. Banks would need to raise capital through wholesale funding (more expensive and less stable), or the lending capacity of the system would shrink, or some combination of both. The ABA’s argument this could reduce lending by 20 percent or more is contested but not implausible.

The fourth thing banks are protecting is their political position. Banking is one of the most heavily regulated industries in the United States, and the banking industry has spent decades building relationships with Congress, regulators, and the Federal Reserve. The political infrastructure banks have built gives them significant influence over financial legislation. Allowing stablecoins to compete with deposits would, over time, shift some of that political power to a new industry (the crypto industry) banks have historically opposed. Banks are not just defending their economic interests. They are defending the political ecosystem that protects those interests.

None of this is necessarily improper. Industries lobby for their interests. Banks have legitimate concerns about deposit funding, regulatory parity, and systemic stability. The argument is not that the banking industry’s position is illegitimate. The argument is the banking industry’s position is being framed as consumer protection and financial stability when it is, more straightforwardly, a defense of the existing profit model against a competitive threat.

The crypto industry’s response

The crypto industry’s pushback against the ABA campaign has been unusually pointed for what is typically a politically careful sector.

Paul Grewal, Chief Legal Officer at Coinbase, responded directly to the ABA’s lobbying campaign in early May. His argument was that banks have already had their preferred outcome in the GENIUS Act, which banned yield payments by stablecoin issuers themselves. Banks won “idle yield killed,” in Grewal’s framing, which was already a loss for consumers but a clear win for banks. The CLARITY Act compromise on activity-based rewards represents a further concession to banking industry concerns, and Grewal’s view is that the banks should “take yes for an answer.”

Cody Carbone, Chief Policy Officer at The Digital Chamber, was sharper. He criticized the banking industry for “waiting until the final days before the markup to raise objections.” The framing was that the banks had multiple opportunities to negotiate the language during the months of bipartisan negotiations and chose to wait until the eleventh hour to mount an emergency campaign. “The arrogance is astounding,” Carbone wrote in a public post.

The crypto industry’s substantive argument against the ABA is twofold. First, the deposit flight concern is overstated because banks can easily mitigate the issue by raising deposit rates to competitive levels. If banks paid 3 percent interest on checking accounts, the relative attractiveness of yield-bearing stablecoins would diminish considerably. The fact banks have chosen not to raise rates, even as the federal funds rate has stayed elevated for years, is a strategic choice rather than an unavoidable constraint.

Second, the lending capacity argument assumes banks are the only legitimate source of credit creation in the US economy. The reality is non-bank lending has grown substantially over the past decade. Private credit funds, fintech lenders, peer-to-peer platforms, and now potentially stablecoin-funded lending platforms all extend credit outside the traditional banking system. The deposit flight argument treats banks as irreplaceable. The economic reality is capital flows to where it can be deployed productively, and the structural role of banks has been gradually eroding for years.

The White House has taken a position broadly aligned with the crypto industry on this specific question. Patrick Witt, Executive Director of the President’s Council of Advisors on Digital Assets, publicly criticized the ABA’s late-stage lobbying effort, noting the bankers had been invited to the White House in February to discuss the compromise language and had not made themselves available at that time. The administration’s view is the Tillis-Alsobrooks compromise language is final, and the ABA’s continued lobbying is an attempt to relitigate a settled question.

Why the compromise still leaves space the banks oppose

The Tillis-Alsobrooks compromise language is the result of months of negotiation between crypto industry advocates and banking industry concerns. The language has been narrowed several times in response to bank lobbying. The current draft is, by ABA’s own admission, improved from earlier versions. But the banks are still fighting because the compromise still permits the specific mechanism that worries them most.

Under the current language, stablecoin issuers cannot pay yield directly. That part is unchanged from the GENIUS Act. Exchanges and crypto intermediaries cannot pay rewards “in a manner that is economically or functionally equivalent to the payment of interest or yield on an interest-bearing bank deposit.” This is the new restriction the compromise added.

But the language permits exchanges to pay rewards for “user participation in an exchange’s membership program,” with rewards potentially calculated by reference to duration, balance, and tenure. This is the loophole the banks want closed.

In practice, this means a crypto exchange could offer a membership program with tiered benefits. Higher membership tiers receive rewards based on the user’s overall engagement with the platform, including their stablecoin holdings. The rewards could be calculated as a percentage of the user’s average stablecoin balance over a given period, denominated in stablecoins or other tokens. The structure would be technically distinct from interest payments on a bank deposit, but the economic effect for the user would be similar.

The banking industry’s position is this structure is a designed workaround. The ABA’s letter to senators called the activity-based rewards provision “a significant loophole” that would let exchanges offer “interest-like incentives” through marginally different legal structures. If the goal of the GENIUS Act ban was to prevent stablecoins from competing with bank deposits, the ABA argues, the CLARITY language undermines that goal by allowing the same competition through a different mechanism.

The crypto industry’s position is activity-based rewards are not the same as yield payments and serve legitimate user engagement purposes exchanges should be allowed to design. The compromise language, on this view, is the correct balance: it bans the most direct form of stablecoin yield while preserving exchanges’ ability to compete on user experience.

The actual answer probably lies between the two positions. The activity-based rewards mechanism is, in practice, a partial substitute for direct yield. Whether it is enough of a substitute to trigger the deposit flight banks are warning about is an empirical question nobody can answer with certainty in advance. The compromise language is a bet that the answer is “no, or not by enough to cause systemic concern.” The banks’ continued lobbying is a bet that the answer is “yes, eventually, and the cost will be too high to undo.”

What this fight tells you about CLARITY’s real politics

The stablecoin yield fight reveals something about CLARITY’s broader political dynamics that most coverage misses.

The bill is being treated as a crypto industry victory in many headlines. The reality is that CLARITY is the product of extensive compromises with multiple stakeholder groups, each of which had to be partially accommodated for the bill to advance. The banking industry got the GENIUS Act ban on direct stablecoin yield. The crypto industry got the activity-based rewards carve-out. The progressive Democrats got partial ethics provisions that have not yet been finalized. The administration got the Anti-CBDC Surveillance State Act language. The CFTC got expanded jurisdiction over digital commodities. The SEC retained jurisdiction over digital securities.

The bill that emerged from this process is a negotiated settlement among multiple powerful interest groups, not a clean crypto industry win. The banks were not the only stakeholders who had to compromise. The crypto industry made substantial concessions, too. The bill that exists is the bill that could be negotiated, not the bill that any single party wanted.

This is normal for major financial legislation. The Dodd-Frank Act of 2010 was a similar product of multi-stakeholder compromise. The Bank Secrecy Act amendments over the years have been similarly negotiated. The legislative process is, in many ways, a process of finding the minimum acceptable set of concessions that lets a bill move forward.

What is unusual about CLARITY is that the banking industry is openly trying to extract additional concessions during the floor vote stage, after the committee process has completed. This is a high-risk strategy for the banks. If they push too hard and Democrats walk away from the bipartisan compromise, CLARITY could stall on the Senate floor. If they push successfully and the language is further restricted, crypto industry support could weaken, and Republican senators could face pressure from their own constituents to vote against a bill that no longer accomplishes what was promised.

The banks are betting they have enough political leverage to extract further concessions without killing the bill. The crypto industry is betting the banks have already overplayed their hand. Both bets cannot be right.

The realistic outcome

Based on the current political dynamics, several outcomes are plausible for the stablecoin yield provisions in the final CLARITY Act.

The first possibility is that the compromise language survives substantially unchanged. The Tillis-Alsobrooks framework was the product of months of negotiation. Both senators have indicated they consider the language final. If the Senate floor vote happens in June or July 2026, as the White House targets, the compromise language could move through with only minor technical refinements. This is the outcome the crypto industry wants, and the banks are trying to prevent.

The second possibility is that the language gets tightened during floor amendments. Democrats negotiating for the bipartisan votes needed to overcome a filibuster could demand additional restrictions on activity-based rewards in exchange for their support. The ABA’s lobbying campaign is designed to create this dynamic. If banks can convince Democrats that the loophole is too large, the floor amendment process could narrow the rewards mechanism further.

The third possibility is that the language gets removed entirely during conference reconciliation with the House version. The House passed its version of crypto market structure legislation in 2024 (FIT21), and the final CLARITY Act will need to reconcile differences between the House and Senate versions. The conference committee process is opaque and often produces unexpected outcomes. The stablecoin yield provisions could be substantially modified during reconciliation.

The fourth possibility is that CLARITY stalls or fails entirely. If the stablecoin yield fight becomes too contentious, or if the broader ethics provisions and law enforcement issues cannot be resolved, the bill could miss its July 4 White House signing target and slip past the 2026 midterm elections. Senator Cynthia Lummis warned that failure to clear the committee before Memorial Day could push the next viable legislative window past November 2026. The bill cleared the committee on May 14, but the broader timeline pressure is real.

The fifth possibility, which gets less attention, is that the law passes substantially as drafted, but the agency-level rulemaking process narrows the rewards mechanism in implementation. CLARITY would direct the SEC and CFTC to develop joint rules on stablecoin-related products. The rulemaking process, which stretches into 2027 and 2028, would let regulators apply more restrictive interpretations than the statutory language strictly requires. This is the outcome banks may quietly prefer if they cannot win during the legislative phase.

What this tells you about banks and crypto going forward

The CLARITY Act stablecoin yield fight is, in many ways, a preview of the larger battle between banks and crypto that will play out over the rest of the decade.

The fundamental dynamic is that crypto-native infrastructure (stablecoins, decentralized exchanges, on-chain settlement) can offer customers economic terms that traditional banks cannot match while protecting their existing profit models. The crypto industry’s competitive advantage is not the underlying technology. It is the lack of legacy infrastructure costs and regulatory overhead that lets crypto firms pass through more value to end users.

For banks, the existential question is whether they can adapt their business models to compete with crypto-native alternatives or whether they need to keep regulatory moats that prevent direct competition. The CLARITY Act fight is one specific instance of this larger question. Future fights over central bank digital currencies, tokenized deposits, programmable money, and DeFi lending will all touch on the same fundamental issue.

The banking industry’s preferred strategy, visible in the ABA’s CLARITY campaign, is to use regulatory and political channels to constrain crypto competition rather than adapt to it. This strategy has worked historically. Banks have successfully constrained money market funds, peer-to-peer lending, and other deposit substitutes through regulatory and political pressure for decades. The question is whether the strategy keeps working as crypto becomes more established and politically powerful.

The crypto industry’s preferred strategy is to win the legislative fights that establish clear rules for digital assets and then compete on the merits in the resulting regulated market. The CLARITY Act, in its current form, would give crypto firms a clearer legal framework than they have ever operated under in the United States. If the bill passes substantially as drafted, the crypto industry would have a structural opportunity to compete with banks on more level terms than has ever existed before.

Whether the banks succeed in narrowing the CLARITY language further, or whether the crypto industry holds the line on the compromise, will be determined over the next two to three months. The vote count on the Senate floor will be the proximate indicator. The ABA’s lobbying intensity in the coming weeks will be the leading signal.

For readers tracking the fight, three things are worth watching. First, whether Senator Tillis or Senator Alsobrooks shows any signs of reopening the compromise language under pressure from banking constituents. Second, whether the ABA’s deposit flight studies gain traction with moderate Democrats who could shift the floor vote dynamics. Third, whether crypto industry advocacy groups (Blockchain Association, Digital Chamber, Coinbase’s policy team) successfully counter-mobilize their own grassroots networks in the way the banking industry has done.

The bottom line

The CLARITY Act is on a path to becoming law in 2026, but the path is narrower than the headlines suggest. The single biggest obstacle is not the SEC, the CFTC, the Democrats opposing the bill on ethics grounds, or the libertarian objections to government oversight of crypto. It is the American Bankers Association and the broader banking industry coalition fighting to close the stablecoin yield loophole the Tillis-Alsobrooks compromise created.

The fight is not about consumer protection or financial stability, despite how the ABA frames it. It is about banks defending a profit model built on zero-yield deposits against a structurally superior alternative. The deposit flight scenario the banks warn about is, in part, consumers rationally responding to a better product. The lending capacity reduction is a real concern, but the underlying issue is whether banks should be the only legitimate channel for credit creation in the US economy, which is a contestable proposition.

The CLARITY Act, in its current form, represents a negotiated compromise that gives banks substantial concessions (the GENIUS Act ban on direct stablecoin yield) while preserving some space for stablecoin-related products to compete (the activity-based rewards mechanism). The compromise is not perfect from either industry’s perspective. It is, by the standards of major financial legislation, a reasonable balance.

What happens next will be determined by which side overplays its hand. If the banks push for further restrictions and Democrats walk away from the bipartisan compromise, CLARITY could stall on the Senate floor and miss its 2026 window entirely. If the crypto industry holds the line and the bill passes substantially as drafted, banks will face a structural competitive threat they have not faced in decades.

Both outcomes are plausible. Neither is guaranteed.

For crypto.news readers, the practical lesson is to watch the floor vote dynamics, the conference reconciliation process, and the agency rulemaking that will follow passage. The legislative outcome will set the framework. The administrative implementation will determine how much of that framework actually works in practice. Both phases will be shaped by ongoing pressure from the banking industry that is unlikely to stop just because the bill becomes law.

The banks are not trying to kill CLARITY because they oppose crypto regulation. They are trying to kill the specific version of CLARITY that lets stablecoins compete with bank deposits on terms banks cannot match without raising their own deposit rates. The fight is, in its essentials, about who gets to capture the spread between zero-yield deposits and Treasury-backed yields.

The answer to that question will shape American banking for the next decade.

This article is for informational purposes and does not constitute legal, financial, or investment advice. Legislative outcomes and policy debates evolve quickly; the analysis described reflects reporting available as of late May 2026. Always do your own research and consult appropriate counsel for specific regulatory matters.

Key Highlights

- Coinbase achieved record crypto trading-volume market share during Q1 2026

- Prediction markets platform scaled to $100M annualized revenue within two months of U.S. debut

- Coinbase One subscriber base crossed ~1 million users; Q1 subscription/services revenue projected at $550M–$630M

- Workforce reduction of approximately 700 employees (~14% staff) implemented amid market turbulence

- Analyst consensus on COIN stands at Hold with $252.20 average price target over 12 months

The Coinbase of today bears little resemblance to the platform from three years back. What began as a retail-focused crypto exchange has transformed into a diversified financial services company spanning subscriptions, stablecoin operations, institutional services, custody solutions, derivatives trading, and now prediction markets.

The prediction markets offering particularly captured attention. Reaching $100 million in annualized revenue by March 2026 — merely two months post-U.S. launch — represents one of the fastest product scaling achievements in the company’s timeline. The numbers speak for themselves.

First quarter 2026 delivered encouraging results across multiple fronts. The exchange posted an unprecedented high in crypto trading-volume market share while simultaneously demonstrating the prediction markets momentum.

Subscription and services revenue has emerged as a critical narrative component. Coinbase projected Q1 2026 subscription and services revenue within the $550 million to $630 million range. This matters substantially because revenue from these sources demonstrates greater stability compared to transaction fees that fluctuate dramatically with crypto market conditions.

The Coinbase One subscription service reached approximately 1 million users. Platform-held USDC volumes also touched record levels, underscoring the company’s expanding stablecoin market presence.

Building a More Resilient Revenue Engine

Historical Coinbase performance correlated directly with spot trading activity. Today’s platform operates with significantly more diversification. Revenue streams now include subscriptions, stablecoins, custody operations, institutional trading services, and emerging products — extending far beyond basic retail transactions.

Reuters coverage from May 2 indicated that Coinbase announced agreement on a critical provision within major Senate crypto legislation. Enhanced regulatory clarity would disproportionately advantage established operators like Coinbase compared to smaller competitors lacking comparable infrastructure and policy influence.

Should this regulatory development proceed, it could represent a substantial catalyst for long-term business expansion.

Workforce Reductions Reflect Market Realities

Notwithstanding platform advancement, Coinbase eliminated approximately 700 positions in early May — representing roughly 14% of total staff. Management characterized the decision as strategic repositioning for artificial intelligence integration while controlling expenses throughout crypto market uncertainty.

The messaging appears somewhat contradictory. Leadership emphasizes platform strength while simultaneously reducing personnel. However, the action demonstrates fiscal discipline, which investors typically value over unchecked expenditure.

The fundamental Coinbase investment thesis tension persists: improved business fundamentals operating within an unpredictable environment. Declining crypto valuations and trading volume contractions continue impacting stock performance significantly.

Wall Street maintains a measured stance on the equity. Coinbase currently carries a Hold consensus from 33 MarketBeat analysts — comprising 19 buy ratings, 10 hold ratings, and 4 sell ratings. The consensus 12-month price target stands at $252.20.

This divided perspective reveals substantial insight. Analysts acknowledge legitimate platform diversification progress. Simultaneously, they recognize COIN’s vulnerability to sharp declines when crypto sentiment deteriorates.

The immediate focus remains the Q1 2026 subscription and services revenue guidance of $550M–$630M, which upcoming earnings results will either validate or challenge.

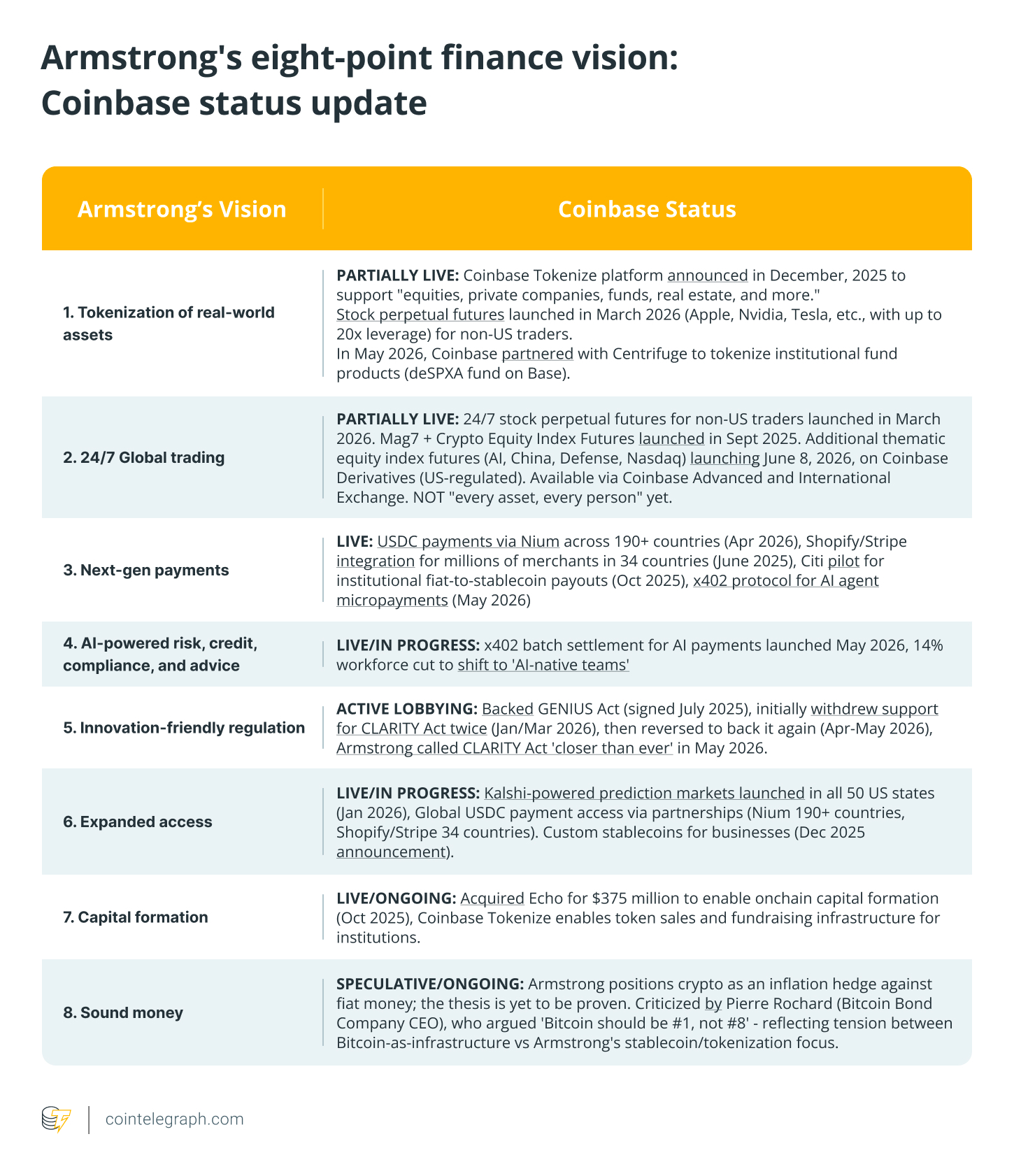

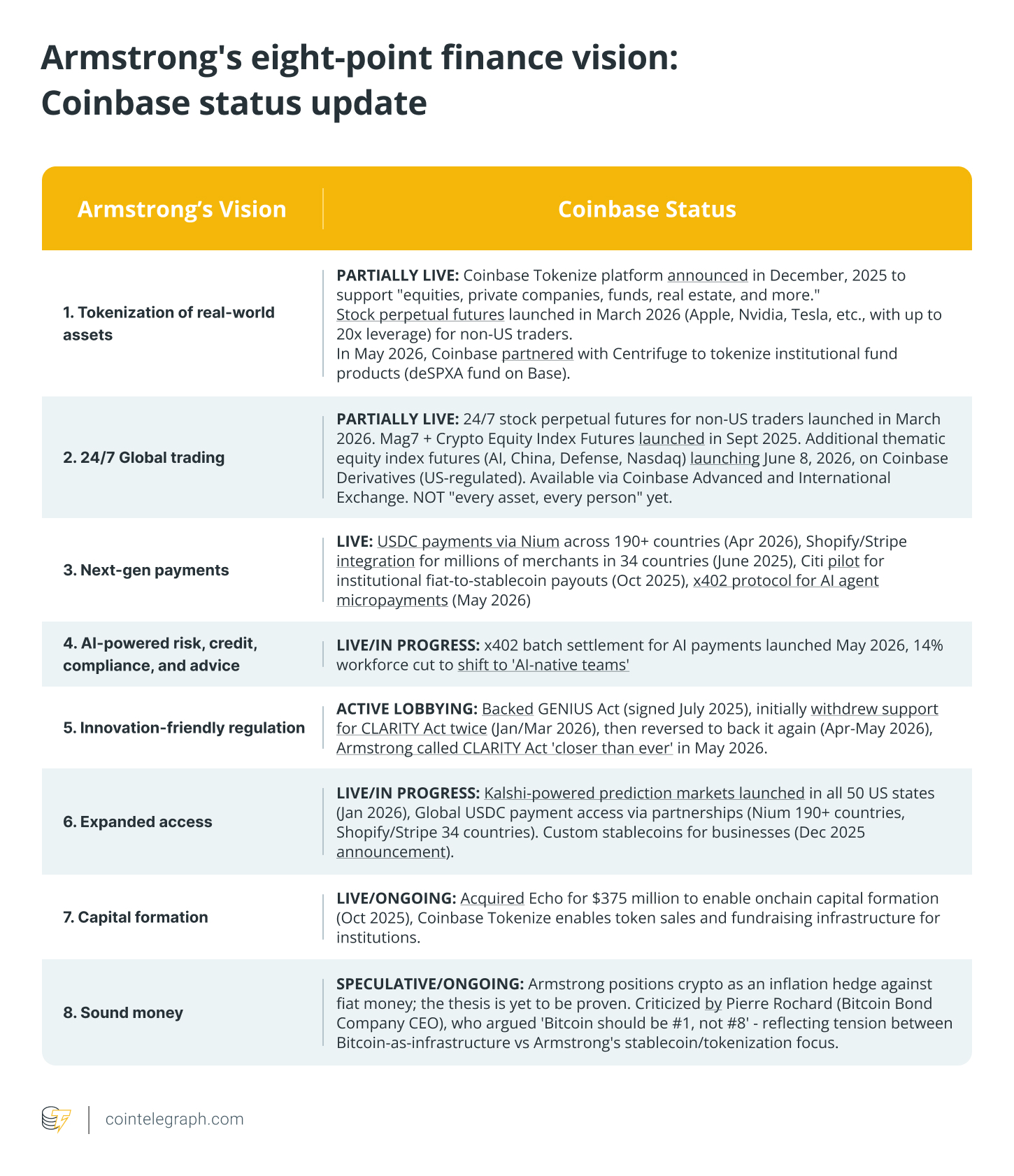

Brian Armstrong posted an eight-point blueprint for upgrading global finance Monday, which closely tracks Coinbase’s expansion into stocks, prediction markets and stablecoin infrastructure, as the exchange continues its push to become an “everything” platform.

The Coinbase CEO’s priorities, posted Monday on X, include tokenized real-world assets, 24/7 global trading, stablecoin payments, AI-powered compliance, open access, capital formation, regulation and sound money.

Coinbase is broadening beyond crypto trading into payments, tokenized assets and financial infrastructure as exchanges compete to capture a larger share of global capital markets. The exchange is positioning itself against rivals like Binance and Kraken, which offer equity perpetuals and synthetic stock exposure under varying regulatory frameworks.

Some of Armstrong’s priorities already align with live products, while others remain aspirational. Armstrong’s call for “tokenization of real-world assets” and “24/7 global trading,” for example, aligns with Coinbase’s March rollout of stock perpetual futures for non-US traders, offering round-the-clock, leveraged exposure to Apple, Nvidia and major indices in 26 European countries.

The company earlier launched perpetual futures contracts for institutional clients via Coinbase International Exchange, extending crypto-style derivatives into equity products, though access remains restricted to accredited investors in select jurisdictions rather than “every person” globally as Armstrong envisions.

Brian Armstrong’s 8-point finance vision.

On “next-gen payments,” Coinbase partnered with Singapore fintech Nium in April to integrate USD Coin stablecoin settlement across more than 190 countries, enabling businesses to fund cross-border payouts on demand without prefunding multi-jurisdiction accounts.

The company also collaborated with Shopify and Stripe in June 2025 to roll out USDC payments to millions of merchants across 34 countries, with automatic fiat conversion and zero foreign-exchange fees.

In October 2025, Coinbase announced a collaboration with Citigroup to explore fiat-to-stablecoin payout methods for institutional clients, further integrating crypto infrastructure with traditional finance systems.

Related: KuCoin launches perpetual futures tracking Tesla and Strategy stocks

Expanding access and capital formation

Armstrong’s mention of expanded access through “open protocols” and capital formation also reflects live initiatives. Coinbase launched Kalshi-powered prediction markets in all 50 US states in January, allowing users to trade event contracts on sports, politics and culture.

The launch puts Coinbase in a market Bernstein estimates will reach $240 billion in volume this year and $1 trillion annually by 2030.

The priority for “innovation-friendly regulation” tracks Coinbase’s lobbying for the Digital Asset Market Clarity Act. After publicly withdrawing support twice, Armstrong said that CLARITY was closer than ever in early May after Senate compromises on stablecoin yield and decentralized finance provisions.

Coinbase also championed the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act, signed into law in July 2025, to establish federal stablecoin oversight with one-to-one dollar backing requirements.

On “AI-powered risk, credit, compliance,” Coinbase backed the x402 payment protocol in May, adding batch settlement to enable AI agents to authorize micropayments below $0.0001. The feature launched weeks after Armstrong cut 14% of Coinbase’s workforce, citing a shift to “smaller AI-native teams” using automation tools to boost output.

Related: Binance launches SpaceX-linked perpetual futures ahead of IPO

Sound money as an inflation hedge

Armstrong’s final point, “sound money” as an inflation hedge, drew pushback from Pierre Rochard, chief executive of The Bitcoin Bond Company, who stated that Bitcoin should be the top priority, rather than left for last.

The pushback reflects a deeper divide: Bitcoin advocates believe it should be the foundation of a new financial system, not just a backup option when fiat currencies fail.

“Bitcoin is #1,” echoed Blockstream chief executive Adam Back, who was rumored to be Bitcoin’s anonymous creator Satoshi Nakamoto earlier this year.

Magazine: Guide to the top and emerging global crypto hubs — Mid-2026

TLDR

- Micron achieved unprecedented fiscal Q2 2026 revenue of $23.86 billion with Q3 guidance pointing to approximately $33.5 billion

- SK Hynix delivered exceptional Q1 2026 revenue of KRW 52.57 trillion, fueled by accelerating AI memory sales

- These semiconductor giants dominate high-bandwidth memory (HBM) production critical for AI server infrastructure

- Wall Street remains optimistic on both stocks: Micron earns a Buy recommendation while SK Hynix commands a Strong Buy

- Investment thesis differs: Micron provides diversified memory market access; SK Hynix represents a concentrated AI memory position

The artificial intelligence memory revolution has created two standout investment opportunities: Micron and SK Hynix. While both companies are capitalizing on explosive AI demand, their investment profiles differ significantly. Micron dominates as America’s premier memory manufacturer, delivering comprehensive exposure across DRAM, NAND, and high-bandwidth memory segments. Meanwhile, SK Hynix has established itself as the frontrunner in HBM technology, the specialized memory architecture essential for powering advanced AI processors.

For investors tracking the AI infrastructure expansion, these companies control critical nodes in the technology supply ecosystem.

Micron’s Performance Reaches Unprecedented Heights

Micron delivered exceptional fiscal Q2 2026 results with revenue reaching $23.86 billion, accompanied by an impressive gross margin of 74.4% and net income totaling $13.79 billion. The semiconductor manufacturer generated $11.9 billion in operating cash flow during this single quarter.

Looking ahead, the company projects fiscal Q3 revenue around $33.5 billion with gross margins climbing toward 81%. These metrics represent extraordinary performance across any industry sector.

Micron’s Cloud Memory Business Unit contributed $7.75 billion in quarterly sales. The Core Data Center division generated an additional $5.69 billion. Consumer electronics no longer dominate the revenue mix. Hyperscale cloud providers and AI-focused data centers now drive the company’s growth trajectory.

MarketBeat data reveals analyst sentiment favoring Micron with a Buy consensus across 39 professionals. The breakdown includes 5 Strong Buy recommendations, 30 Buy ratings, and 4 Hold positions, with zero Sell calls.

SK Hynix Emerges as the Pure-Play AI Memory Investment

SK Hynix announced exceptional Q1 2026 performance with revenue hitting KRW 52.57 trillion alongside operating profit of KRW 37.61 trillion. Management indicated that AI processor demand will outstrip their production capabilities, highlighting ongoing HBM supply limitations.

Following announcements from leading American technology companies about intensified AI data center investments in early May, SK Hynix stock experienced substantial gains. This price movement demonstrates the tight correlation between SK Hynix’s valuation and AI infrastructure capital expenditure.

Compared to diversified competitors like Samsung, SK Hynix presents a more straightforward investment narrative. Shareholders are essentially wagering on sustained HBM demand growth. This singular focus represents both the investment opportunity and the potential vulnerability.

Investing.com data shows SK Hynix commanding a Strong Buy consensus among 38 analysts, comprising 36 Buy ratings, 2 Hold recommendations, and zero Sell opinions.

Understanding the Key Differences

Micron delivers comprehensive memory market participation spanning DRAM, NAND, and HBM technologies, supported by robust cash flow generation and convenient U.S. exchange listing. SK Hynix offers investors a more focused, aggressive position targeting AI server memory specifically.

While both securities often trade in tandem, the underlying drivers diverge. Micron’s performance mirrors overall memory market conditions. SK Hynix’s valuation tracks AI infrastructure investment velocity.

Analyst sentiment favors both companies strongly. The investment decision ultimately depends on whether portfolio managers prefer diversified memory sector exposure or concentrated AI hardware demand correlation.

Ethereum co-founder Vitalik Buterin said the Ethereum Foundation will choose “longevity over breadth,” reduce ETH sales and narrow its focus to CROPS: censorship resistance, capture resistance, openness, privacy and security.

In a lengthy post on X, Buterin detailed that the Ethereum Foundation holds roughly 0.16% of all ETH, well below the 10% to 50% he said it’s common for the central foundations of other blockchains to hold.

Nearly 90% of his own net worth sits in ETH, with the remaining roughly $40 million in onchain fiat already earmarked for open-source biotech, software and hardware initiatives, Buterin added.

His influence within the EF will continue to decrease as the board expands, aligning with his desire to be less influential there. However, he also hedged his words, saying, “This is only my own view. The board is not just me, and I have no extra special powers on the board that the other board members do not.”

He framed the EF as “one node, with a defined purpose, alongside other nodes,” not the center of Ethereum. Addressing throughput, Buterin said it would be a mistake for Ethereum to maximize it.

“Being as fast and as scalable as possible, and only a small epsilon more decentralized than the others, is a route to mediocrity, and if we try it, we will lose.”

Instead, Buterin pointed to Ethereum striving to be “deeply impressive” in what he called the “CROPS dimension.” That involves making Ethereum provably bug-free, which is argued to be within reach given AI-powered verification.

The post landed after at least 8 senior EF contributors left or announced departures in 2026, 5 in May alone, reigniting debate over the foundation’s direction.

Crypto community reacts

Prominent Ethereum voices were supportive of Buterin.

Anthony Sassano, an independent Ethereum educator, angel investor and advisor, replied directly to the post, thanking Buterin. A separate quote tweet from Sassano focused on Buterin’s framing of ETH as the most high-value “product” of the Ethereum blockchain.

Author and early Ethereum advisor William Mougayar quote-tweeted the post: “Basically, Ethereum just got its own Clarity Act over the weekend. It was a crystal clear message, and the road ahead is super clear. Ethereum is untouchable.”

Developer Suhail Kakar also replied directly, calling the post “bullish.” “A foundation voluntarily shrinking its own power is the rarest thing in crypto. genuinely the most cypherpunk thing I’ve read in a long time.”

Meanwhile, core developers picked at the CROPS framework.

Go-Ethereum developer Marius van der Wijden replied that security was being underdiscussed: “When people talk about CROPS, they seem to focus on the CR, OS and Privacy part. The security part is in my opinion the most important! Without a secure L1 none of this makes any sense and we have taken Ethereum’s base layer security for granted by now.”

Consensus layer developer Potuz followed up in the thread, noting that “one of Ethereum’s biggest selling points is the no downtime since genesis” and that the record made every fork a concentrated risk.

Laura Shin, host of Unchained, asked the governance question the post left open: “What’s the process for adding new members to the board?” Buterin did not publicly answer at the time of writing. DeFiPrime founder Nick Sawinyh noted the EF now sounded “less like a cathedral and more like a protocol commons operator.”

Others criticized the cryptocurrency’s performance. Ether has fallen nearly 60% against bitcoin over the last five years, to 0.02738 BTC. Over that period, bitcoin’s price nearly doubled from $35,600 to $77,500 at the time of writing.

Read more: Ethereum’s identity crisis is deepening after high-profile ‘brain drain’ frustrates the community

Jeremy “jercos” Sturdivant, the recipient of the historic Bitcoin Pizza Day transaction, has confirmed he spent his 10,000 Bitcoin (BTC) on a road trip across the United States after running out of money.

The story resurfaced after Adam Back, CEO of Blockstream, reposted a video clip of Sturdivant discussing the exchange. The post spread quickly across crypto social media and drew fresh attention to one of Bitcoin’s most often-cited transactions.

The 10,000 BTC That Funded a Road Trip

On May 22, 2010, Sturdivant received 10,000 BTC from developer Laszlo Hanyecz. The payment covered two Papa John’s pizzas ordered on Sturdivant’s credit card. That transaction is now observed annually as Bitcoin Pizza Day and stands as the first documented commercial use of Bitcoin.

Sturdivant said he never considered the BTC an investment. He treated the coins as functional currency and spent them as their value gradually climbed. He emphasized that Bitcoin was meant to be used, not stored as a speculative asset. When a cross-country road trip left him short on funds, the Bitcoin covered the gap.

Bitcoin reached an all-time high of approximately $126,000 in October 2025. At that price, the original 10,000 BTC would have been worth over $1.26 billion. BTC traded near $77,787 on Pizza Day 2026, still placing the notional value of that stack above $770 million.

Bitcoin Pizza Day Revives an Old Debate

Back stands among Bitcoin’s most prominent advocates. He has been vocal about long-term holding strategies as fiat currencies weaken. Just days before reposting the clip, he urged investors to buy BTC at current price levels. His decision to amplify Sturdivant’s remarks was notable for the contrast it implied.

Sturdivant’s approach was to use the coins as money, not accumulate them. Back’s position represents the opposite view. That divide sits at the center of a Bitcoin in culture debate that has persisted since the network’s earliest transactions. Sturdivant wanted BTC to function as a living currency. Back has argued that people should treat it as a hard monetary asset.

Sturdivant has said he has no regrets. The transaction was worth roughly $41 at the time. How that philosophy holds up depends on where the current Bitcoin price cycle ends up.

The post Bitcoin Pizza Day Recipient Speaks Out: How the 10,000 BTC Was Spent appeared first on BeInCrypto.

A New York civil action filed on May 1 seeks a court ruling that ownership of 39,069 dormant Bitcoin addresses rests with the plaintiffs—Noah Doe and two Wyoming-based limited liability companies, ABC Company and XYZ Company. The suit claims the coins tied to these addresses constitute abandoned property discovered by the plaintiffs and reported to the New York Police Department, with a claim under New York Lost Property Law.

According to Cointelegraph, the filing argues that the wallets contain Bitcoin belonging to a spectrum of historic holders, including early miners and addresses attributed to the Bitcoin creator, Satoshi Nakamoto, along with other lost or unidentified entities. The action foregrounds long-standing questions about how inactive Bitcoin should be treated under property regimes and what ownership means when private keys are not accessible.

Industry observers note that even a court’s recognition of ownership would face fundamental, real-world constraints: the Bitcoin network has no mechanism to reallocate funds without the private keys that authorize transactions. The case underscores a core tension between legal theories of property and the operational realities of a distributed ledger.

“The network has no mechanism to reassign funds without a private key,” said Noveleader, lead research analyst at Castle Labs. “The one narrow exception would be if any of these coins are moved to a regulated custodian or exchange, at which point a court could compel that intermediary to act.”

The research perspective added that many of the coins cited in the suit may belong to deceased holders, lost keys, or long-term holders who have not transacted—further complicating claims of legal abandonment.

ABC Company, XYZ Company, Noah Doe, lawsuit against John Does holding 39,069 BTC. Source: ilawconotices.com

Key takeaways

- The suit seeks a court declaration that ownership of 39,069 dormant Bitcoin addresses rests with the plaintiffs under New York Lost Property Law, raising questions about how abandoned crypto assets could be treated legally.

- Even with a favorable ruling, direct reallocation of funds would be technically unfeasible without private keys; enforcement would likely depend on custodians or exchanges under court direction.

- Notice concerns arise from the address formats used: notices were sent to Pay-to-Public-Key-Hash (P2PKH) identifiers, while the coins may reside in Pay-to-Public-Key (P2PK) outputs, potentially undermining abandonment notices.

- The addresses include references to historically significant targets (Satoshi-era wallets and Mt. Gox-related addresses), but the bulk of assets may belong to non-responsive or deceased holders, complicating a clean legal claim of abandonment.

- Independent estimates suggest a substantial dormant BTC stock, underscoring the scale at stake for property-law interpretation and regulatory oversight in a modern digital asset regime.

- The case sits at the intersection of property law, digital custody, and regulatory policy, with potential implications for exchanges, custodians, and cross-border enforcement frameworks.

Legal contours of the NY case and the ownership question

The 901-page filing seeks to establish that the Bitcoin tied to tens of thousands of addresses constitutes abandoned property that the plaintiffs discovered and reported to law enforcement, thereby creating a potential claim under New York’s lost-property framework. In practical terms, abandonment claims hinge on whether the asset has a demonstrable holder who manifests an intent to relinquish ownership, a determination that is technically inapplicable given the cryptographic nature of Bitcoin ownership and the absence of a traditional custodian.

According to Cointelegraph, the inclusion of addresses associated with historic wallets—some linked to Satoshi Nakamoto and others tied to high-profile incidents like the Mt. Gox hack—raises questions about actual ownership and provenance. Even if a court issued a declaration, the inability to transfer funds without private keys would severely circumscribe the practical effect of any ruling.

Noveleader’s commentary emphasizes a narrow, regulatory pathway: a court could compel a regulated intermediary (for example, a custodian or exchange) to act if coins were moved into such a venue. Outside of that scenario, the on-chain protocol cannot effect a reallocation of the assets, creating a discrepancy between legal recognition and technical feasibility.

Dormant Bitcoin stock and regulatory context

Beyond the legal dispute, the case highlights the broader phenomenon of substantial dormant Bitcoin. Industry data indicate that a sizable portion of the supply has not circulated on-chain for many years. Reports estimate that roughly 3.5 million BTC have been dormant for the past decade, with about 6.6 million BTC dormant for more than five years, representing hundreds of billions of dollars in value at current price levels. These figures underscore how a large, potentially inaccessible stock of coins intersects with questions of property rights, loss, and potential regulatory oversight.

From a policy perspective, the dispute touches on core regulatory questions about how authorities categorize and treat crypto assets that lack active holders or known keys. If courts begin to recognize ownership claims on dormant addresses, this could prompt a reevaluation of record-keeping for crypto assets, influence custodial standards, and shape enforcement approaches in jurisdictions facing diverging rules on crypto property, licensing, and consumer protection.

In the broader policy landscape, the case intersects with ongoing debates around MiCA in the European Union, U.S. enforcement priorities from agencies such as the SEC, CFTC, and DOJ, and the development of AML/KYC frameworks for crypto entities. It also raises practical considerations for licensing, regulatory oversight, and cross-border cooperation in asset recovery, as well as implications for stablecoins and their banking integration where custody and ownership rights must be established under legal regimes.

Analysts note that the outcome may influence how exchanges and custodians approach dormant or inaccessible holdings, including any need for standardized procedures to address abandoned assets within regulatory-compliant frameworks. While a ruling could set a legal precedent, the technical infeasibility of reassigning funds without keys remains a fundamental constraint on enforcement and real-world recovery.

Closing perspective

As regulators and financial institutions continue to refine crypto-property frameworks, this NY case underscores the need for clear, interoperable rules governing dormant assets, custody, and enforcement. The next developments—whether the court dismisses, rules in part, or awaits subsequent proceedings—will be watched for signals about how jurisdictions reconcile traditional property concepts with decentralized digital assets and their unique technical realities.

May 25, 2026 — Canton Foundation, Toss, BitGo Among Co-Hosts at Private Event; Token Launch Slated for Second Half of 2026.

On May 21, ARIQO, an on-chain financial platform, made its first public appearance at Southeast Asia Blockchain Week (SEABW) in Bangkok.

Earlier that day on the conference floor, ARIQO co-founder Emanuel Escobar Duro (CBO) spoke with teams from Orca and Viva Republica (Toss) about the shifting role of DeFi platforms and the trajectory of institutional RWA adoption. The broad direction, he noted, is already clear — institutional capital is moving on-chain. The open question is which platforms actually have the infrastructure to receive it, and on that front, the field is still thin.

That evening, ARIQO hosted a private networking event, Alpha After Dark: Where Liquidity Meets Opportunity. Canton Foundation, Viva Republica (Toss), BitGo, Bitkub Exchange, and BLOCKSTREET joined as co-hosts. Running from 8 p.m. to midnight, the gathering brought together institutional investors, liquidity providers, and protocol teams.

The conversations centered on three threads. The first was the structural gap in today’s RWA market: institutional demand for tokenized real-world assets is climbing fast, but the infrastructure to actually trade and manage them onchain remains early-stage. The second was the liquidity bootstrap problem — the cold start that new onchain venues keep running into, where there are no traders without liquidity and no liquidity without traders, and how to break that loop. The third was what it takes for institutional capital to move into the DeFi layer: transparency of yield structures, smart contract audits, predictability of capital management — and how far current protocols actually meet those bars. Attendees traded candid views on each.

It was hard to read the event as a routine networking night. The fact that a project still ahead of launch could bring Canton Foundation, Viva Republica (Toss), BitGo, Bitkub Exchange, and BLOCKSTREET to the table as co-hosts speaks to the credibility ARIQO has already built. The discussion carried weight, too. Real, unsolved problems — the structural gaps in RWA, the DEX cold start, the conditions for institutional inflows — were put on the table, and attendees spoke frankly about them.

ARIQO defines itself not as a single product but as a three-phase financial infrastructure strategy. Where most blockchain projects work backward from a token launch, ARIQO builds the revenue-generating infrastructure first and places the token on top of it. The team sums up its principle in one line: “Capital first. Flow second. Native market last.”

The first phase is the Vault, set to launch in Q3 this year. It runs multiple stablecoin vaults with distinct risk-return profiles, and the TVL gathered here becomes the capital base for every phase that follows. The aim at this stage is not to win an APY race, but to establish ARIQO first as a platform that manages capital reliably.

The second is the Terminal, a trade-aggregation layer that sits on top of existing exchanges. Users keep trading on Binance, OKX, and the venues they already use; by connecting through ARIQO’s interface, rebates are optimized across exchanges and can be automatically reinvested into the Vault. At this stage, ARIQO absorbs external trading flow into its own layer without building a new exchange.

The last is the native RWA Perp DEX. An orderbook-based perpetuals exchange covering crypto, commodities, indices, and synthetic real-world assets, it launches at a point when TVL from the Vault and a trader base from the Terminal already exist — a design that structurally sidesteps the cold start problem, the hardest part of any DEX launch. Fee revenue at this stage flows into $AQV buybacks and back to the Vault, closing the full loop.

The $AQV TGE is scheduled for the second half of this year, after the Vault and Terminal are live. CTO Julius Nielsen, who leads technical implementation, and CSO Daniel J. Aldridge, who handles operational strategy, round out the team alongside co-founders Jin Tang (COO) and Emanuel Escobar Duro (CBO).

The Q3 Vault launch marks the first step of this strategy. Official information and the waitlist are available at ariqo.com, with updates on @ARIQO_X.

Everything else has gone direct-to-consumer. Live events are still controlled by gatekeepers. Here’s why that’s about to change.

The Contradiction Nobody Notices

You can buy a Tesla directly from Elon. You can invest in SpaceX through secondary markets. You can own a piece of a podcast through equity crowdfunding.

Direct-to-consumer has become the default everywhere.

Except live events.

If you want to attend a concert, a festival, a sporting event—you go through Ticketmaster. You pay their fees. You accept their terms. You have no ownership. No stake. No say.

It’s the last frontier of pure gatekeeping in an otherwise disintermediated world.

And the market is $1.5 trillion annually.

Why Live Events Got Frozen in Time

This wasn’t an accident. It happened because live events have a constraint that other industries don’t: physical scarcity.

You can only sell so many tickets. There’s only so much space. The venue has limits.

That scarcity created gatekeepers. Promoters. Ticketing platforms. Middlemen who controlled access.

For decades, that made sense. Physical constraints meant you needed someone to manage capacity, coordinate logistics, handle the complexity.

But here’s what changed: the value of live events shifted from the event itself to the community around it.

Nobody goes to a music festival just for the music. They go for the experience. The crowd. The community. The shared moment.

That community value can be monetized, shared, and distributed. But only if you remove the gatekeepers first.

What Direct-to-Consumer Actually Means

When Tesla sold directly to consumers, they eliminated dealerships and their markup.

When Substack creators went direct, they eliminated publishers and their take.

When crowdfunding platforms appeared, they eliminated traditional venture and their gatekeeping.

Direct-to-consumer means: the creator and the customer can transact without intermediaries.

Live events should work the same way.

An artist or promoter should be able to:

- Sell tickets directly

- Let fans invest in the event

- Share revenue transparently

- Build community ownership

Instead, they go through Ticketmaster. Pay fees. Have no direct relationship with their audience.

The technology to do direct-to-consumer live events has existed for years. Blockchain. Smart contracts. Community tokens. Revenue-sharing protocols.

But the infrastructure wasn’t there. The business models weren’t proven. The platforms didn’t exist.

The Gatekeepers Fought Hard To Keep It That Way

Ticketmaster didn’t become a monopoly by accident.

Live Nation (which owns Ticketmaster) understood something crucial: whoever controls ticketing controls the entire live events ecosystem.

Control the tickets, control pricing. Control pricing, control margins. Control margins, control the industry.

So they built walls. They made exclusive deals with venues. They bundled ticketing with promotion with artist management. They made it nearly impossible to operate outside their system.

And for 20+ years, it worked.

But markets don’t freeze forever. Eventually, the pressure builds.

Why Now? Three Things Changed

1. Blockchain made community investment possible.

You can now tokenize event rights. Let fans own a piece of the upside. Distribute revenue transparently. No intermediary needed.

2. Crypto proved direct-to-community works.

Every successful crypto project did what live events should do: build community, give ownership, share revenue. The playbook exists.

3. Creators are desperate to escape gatekeepers.

Artists are tired of Ticketmaster fees. Promoters are tired of venue cuts. Venues are tired of promoter margins. Everyone’s squeezed by the system.

The moment someone showed a better way, the entire structure would collapse.

What Direct-to-Consumer Live Events Actually Look Like

Imagine:

An artist decides to hold a festival. Instead of going through a promoter and Ticketmaster:

- They sell tickets directly to fans

- Fans can invest in the event (get tokenized equity)

- The event happens

- Revenue gets distributed transparently (artist, community investors, venue, crew—all proportional)

- Fans who invested get their return

Now the artist has:

- Direct relationship with their audience

- Higher margins (no Ticketmaster fees)

- Community owners who care about success

- Data about their audience

- Future bookings based on direct relationships

The fans have:

- Actual ownership (not just a ticket)

- Transparency (see exactly where money goes)

- Upside (if the event succeeds, they profit)

- Community (they’re investors, not just consumers)

The venue has:

- Full capacity guaranteed (community investors bought in)

- Direct relationship with the promoter (no middleman)

- Higher per-ticket revenue (no third-party cuts)

Everyone wins except the gatekeepers.

Why The $1.5 Trillion Hasn’t Moved

The infrastructure exists. The technology works. The incentives are aligned.

So why is the live events market still operating like it’s 1995?

Because changing it requires attacking the most powerful players in entertainment: Live Nation, AEG, the major promoters. They’ve spent decades building moats.

But moats can be crossed.

The moment a legitimate alternative platform launches—one that makes it easy for artists to go direct, for fans to own, for venues to participate—the entire structure becomes optional.

And when something becomes optional, it ceases to be the default.

What Breaking Free Actually Changes

If the live events industry went direct-to-consumer, it wouldn’t just be a business model shift. It would be a structural change to who captures value.

Right now: Ticketmaster and Live Nation capture the majority of upside. Artists, fans, venues get squeezed.

Direct-to-consumer: Value distributed to everyone who creates it. Artists, fans, venues all participate in upside.

That’s not just better business. That’s a realignment of incentives.

And that’s terrifying to anyone profiting from the current system.

The Inevitable Outcome

Every industry that had gatekeepers has had them disrupted eventually.

Retail had Amazon. Media had YouTube. Finance had crypto. Education has online courses.

Live events will too.

The question isn’t whether it will happen. It’s when. And who builds it.

Someone will create a platform that makes it trivial for artists to sell directly. That lets fans own pieces of events. That distributes revenue transparently.

And the moment that works at scale, Ticketmaster becomes optional.

What Comes Next

The infrastructure is almost ready. The incentives are aligned. The technology works.

What’s missing is: a platform that makes going direct easier than going through gatekeepers.

That’s not about technology. That’s about business model design.

How do you make direct-to-consumer so frictionless that artists choose it? How do you make community investment so attractive that fans participate? How do you make the revenue model so transparent that venues trust it?

Answer those questions, and you’ve built the platform that disrupts a $1.5 trillion market.

The last market still operating like it’s 1995.

Someone’s Already Building This

This isn’t theoretical. Stoyan Angelov and the Atmosphera team are designing exactly this: a platform that lets communities invest in live events and share revenue transparently.

They understand what the industry has been too comfortable to admit: gatekeepers exist because nobody’s built a better infrastructure yet.

Atmosphera is attempting to change that equation. Direct artist-to-fan relationships. Community ownership. Transparent revenue sharing. All of it designed to make gatekeeping optional.

Whether they succeed or not, the attempt itself proves something important: the alternative is buildable.

Once you can see what’s possible, you can’t unsee it. And the industry can’t pretend the current model is inevitable anymore.

The question shifts from “Is this possible?” to “Why would anyone choose Ticketmaster once there’s a better option?”

The Uncomfortable Truth

Ticketmaster exists because we’ve accepted gatekeeping as inevitable.

But it’s not. It’s just the path of least resistance.

Direct-to-consumer live events aren’t a future possibility. They’re the logical endpoint of a trend that’s already disrupted every other industry.

The only question is: how much longer until the alternative becomes undeniable?

Someone like Stoyan’s team at Atmosphera is already showing us what that alternative looks like. Not hype. Not theoretical. Actual infrastructure designed around community ownership and transparent economics.

The moment that works at scale, Ticketmaster becomes optional.

And when something becomes optional, it ceases to be the default.

What would make you leave Ticketmaster? Drop your answer—but make it grounded in what you actually want, not what the industry tells you to want.

Ethereum is trading at $2,120 as the final week of May begins, caught in a tug-of-war with the 100-day MA that encapsulates everything frustrating about this cycle.

Having briefly reclaimed the moving average in late April for the first time since the correction began, ETH surrendered it again during the May breakdown and is now trading just below it.

Yet, the moving average is close enough that a single strong daily close could flip the script, but it has been unable to do so with the momentum currently available.

The next few days will determine whether that reclaim sticks or the key $1.8K demand zone finally becomes the next topic of conversation.

Ethereum Price Analysis: The Daily Chart

On the daily chart, it is evident that ETH briefly reclaimed the declining 100-day moving average in late April, only to lose it again during the May breakdown. The price is now trading just below it at approximately $2.1K, with the 100-day moving average sitting a short distance overhead and acting as resistance once more rather than support.

The RSI has also recovered from its low last week near 30 to approximately 40, which is a modest bounce with no directional conviction yet.

The dynamic has shifted subtly but meaningfully, as this is no longer a case of the 100-day MA sitting far above as an aspirational target. It is close enough to touch, and the daily closes around $2.1K represent an ongoing battle to reclaim it.

A sustained close above the moving average and the $2.2k level would confirm the reclaim and shift the structure back toward neutral. On the other hand, a close below $2,000 would simultaneously breach the ascending channel’s lower boundary, leaving $1.8k as the only remaining structural support before a full reassessment of the recovery thesis.

ETH/USDT 4-Hour Chart

The 4-hour chart shows the price compressing into an increasingly tight range between the $2k support zone below and the $2.15k area overhead. The RSI is recovering from oversold territory to just above 50, which is enough to stabilize the market without yet generating upside momentum.

The white ascending channel’s lower boundary at $2.08k converges with the lower boundary of the $2.15k resistance zone, making that band the last technical defense before $1.8k.

The first meaningful target above is the $2.25k zone, which is the level that acted as support through most of April and early May before the breakdown.

A 4-hour close back above it would signal that the worst of the selling pressure has passed and open a path toward $2.4k. Until that reclaim happens, the tight range between $2.15k and $2k is likely to continue as the market waits for a catalyst in either direction.

Sentiment Analysis

ETH’s funding rate has been predominantly positive throughout most of the corrective phase, with only brief negative spikes rather than the sustained red dominance.

The notable exception was late April, when funding tilted mostly negative for an extended stretch, which coincided with the period where price stalled repeatedly at $2.4k and eventually broke down.

That negative phase appears to have cleared, as funding has returned to positive and has recently printed some of the higher green readings of the past two to three months. The current reading of +0.005 sits at the upper end of what has been a muted range.

The timing of this shift matters. Funding turning aggressively positive while price is sitting at $2.1k, closer to the multi-month lows than to resistance, suggests that a fresh cohort of longs is building positions at current levels with conviction rather than chasing a breakout.

The current setup is more structurally sound, as longs are accumulating near support rather than at the ceiling. Whether that conviction is rewarded depends entirely on whether the $2k channel floor holds and the 100-day moving average is reclaimed again.

-

Source: TradingView

The post Ethereum Price Prediction: ETH Battles 100-Day MA as $2K Support Holds the Key appeared first on CryptoPotato.

Binance Wallet has rolled out Event Rush, a 42.space powered dApp on BNB Chain that lets verified users buy and trade tokens representing real world event outcomes using USDT on BSC.

Summary

- Event Rush lets users speculate on sports, crypto prices, and news outcomes via event tokens

- Pricing uses a bonding curve model instead of fixed odds or a traditional order book

- Users can sell tokens before settlement or hold to share in the USDT prize pool at expiration

- Access is limited to KYC verified Binance Wallet users and excludes restricted regions

According to the official announcement, Event Rush is integrated directly into Binance Wallet and “transforms real world outcomes into tradable tokens” on BNB Chain, with users able to access the feature through the dApp section of the wallet interface.

The product is built on the 42.space protocol, and Binance explains that “Event Rush is where token trading meets real world events,” allowing users to buy event tokens on topics including sports scores, cryptocurrency price targets, and news developments.

How does Binance Event Rush work as an on chain prediction venue?

FinanceFeeds reports that each outcome is represented by a distinct event token, and prices are set via a bonding curve that automatically adjusts based on supply and demand rather than a central bookmaker or external market maker.

Every purchase mints event tokens along the curve, pushing the price higher as demand increases, while selling burns tokens and moves the price back down, which keeps a two sided price available even when liquidity is thin.

Per Binance, users fund trades with USDT on BNB Smart Chain, can exit positions at any time before settlement by selling back into the curve, or hold through resolution to claim a share of the USDT collateral pool if their chosen outcome is correct.

FinanceFeeds notes that winners “share the entire USDT collateral pool, including value from losing tokens,” creating theoretically uncapped upside for popular, correctly priced outcomes while losers forfeit their stake.

The structure blends speculative trading and pari mutuel style payoff mechanics, since all stakes on losing outcomes are redistributed proportionally to winning token holders at settlement rather than paid out at fixed odds.

Binance states that Event Rush is available to “all verified Binance Wallet users” but that it “may not be accessible in certain restricted regions,” framing the product as a Web3 feature distinct from centralized derivatives even as it clearly enables real money betting on future events.

Is Event Rush a prediction market or entertainment product?

From a design perspective, Event Rush functions much like an on chain prediction market, but Binance consistently brands the product around “event tokens” and “trading real world events” rather than using the language of betting or derivatives in its public communications.

This linguistic choice comes as some regulators have started classifying decentralized prediction platforms as unlicensed gambling, with ChainCatcher pointing to a recent Reuters report on Indonesia’s ban of Polymarket for offering “bets and speculation on events that have not yet concluded.”

At the same time, Binance is clearly leaning into this narrative space inside its wallet stack, following earlier experiments with bonding curve based token launches and the Meme Rush feature that merged speculation and community driven assets.

FinanceFeeds highlights that Event Rush “eliminates the necessity for external market makers” because the bonding curve contract itself ensures a continuous price, which is a marked contrast to centralized products like futures where liquidity is warehoused by professional desks.

The launch also comes amid a broader push to use wallet level interfaces as distribution for experimental markets, echoing what Unchained has described in coverage of Binance’s Pump fun style bonding curve model and earlier bonding curve token launches.

For now, Event Rush sits in a regulatory grey zone between derivative exposure and entertainment, but by routing activity through BNB Chain and the 42.space protocol while limiting access to KYC users, Binance appears to be betting it can keep the infrastructure sufficiently “on chain” to frame the product as a Web3 event trading layer rather than a conventional sportsbook.

If that positioning holds, Event Rush could become a template for how large exchanges front end decentralized prediction rails, much as DeFi options and perpetuals have already blurred the line between on chain protocols and exchange style user experiences.

Fly-tippers could face five years in prison under government crackdown

Britain’s navy prepares to clear mines in the Strait of Hormuz while waiting for a peace deal

Coinbase (COIN) Stock: Has the Crypto Giant Evolved Into a Buy Opportunity?

-

Crypto World4 days ago

Crypto World4 days agoBlockchain.com files with SEC for U.S. IPO

-

Fashion3 days ago

Fashion3 days agoHoliday Weekend Open Thread – Corporette.com

-

Crypto World3 days ago

Crypto World3 days agoBitcoin Accumulation Weakens as BTC Realized Losses Hit $600M

-

Business3 days ago

Business3 days agoDell Technologies DELL Stock Surges 15% on AI Server Momentum and Analyst Upgrades in 2026

-

Crypto World3 days ago

Crypto World3 days agoSpace X IPO Is ‘Bad News’ for Tech Stocks: But What About Bitcoin?

-

Politics3 days ago

Politics3 days agoMakerfield: a tale of two social-media histories

-

Crypto World2 days ago

Crypto World2 days agoRobinhood crypto COO Tanya Denisova exits

-

Crypto World4 days ago

Crypto World4 days agoMicroStrategy’s Saylor Says Miners No Longer Set Bitcoin Price, Another Force Has Taken Over

-

Business22 hours ago

Business22 hours agoNYT Strands Answers May 24 2026 Revealed for Puzzle No. 812 Theme Summer Essentials

-

Crypto World3 days ago

Crypto World3 days agoAI infrastructure race heats up as IREN pitches full-stack strategy, WhiteFiber lands $160M deal

-

Tech3 days ago

Tech3 days agoA 0.12% parameter add-on gives AI agents the working memory RAG can’t

-

Tech4 days ago

Tech4 days agoWhatsApp ads could make Irish debut after discussions with DPC

-

Tech4 days ago

Tech4 days agoYou Can Now Add ChatGPT To PowerPoint

-

Business3 days ago

Business3 days agoTrump Invests $1M-$5M in Kura Sushi USA Chain With 27 California Locations

-

Crypto World7 days ago

Crypto World7 days agoRevolut Launches Dogecoin Debit Card Across UK and EU

-

NewsBeat4 days ago

NewsBeat4 days agoCharity run by Reform leader Malcolm Offord accused of ‘law breaking’ over Scottish registration

-

Sports4 days ago

Sports4 days ago2026 CJ Cup Byron Nelson leaderboard: Brooks Koepka finds putting stroke in Round 1

-

Crypto World3 days ago

Crypto World3 days agoTrump Media’s Bitcoin Stash Shrinks Again as 2,650 BTC Lands on Crypto.com

-

Business3 days ago

Goldman Sachs reinstates Ageas stock coverage with neutral rating

-

Crypto World5 days ago