Editor’s note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

Business

Innovative Aerosystems: Looks Fairly Priced With Lower Intermediate Growth Ahead (NASDAQ:ISSC)

Investment research, primarily oriented towards uncelebrated/under-covered stocks and ETFs, across North America, Latin America, Europe and Asia. Seeks to combine both fundamental and technical disciplines while making an investment/trading proposition.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Continue Reading

onimate/iStock via Getty Images

The WisdomTree Quantum Computing Fund ETF (WQTM) is an exchange-traded fund that aims to give investors access to a diversified portfolio of companies engaged in, or with exposure to, various aspects of quantum computing, such as the development of quantum hardware and software, enabling technologies, and necessary supporting infrastructure.

What Is WQTM?

WQTM is a U.S.-listed thematic equity ETF designed to provide investors with targeted exposure to companies participating in the emerging quantum computing ecosystem. WQTM started trading on October 9, 2025, and seeks to track the WisdomTree Classiq Quantum Computing Index, which was created through a collaboration between WisdomTree and Classiq, a quantum software firm. The investment strategy outlined by WisdomTree covers quantum hardware, quantum software, quantum infrastructure, and enabling technologies, as well as companies that focus on quantum technology and larger companies that offer a diversified range of technologies.

WQTM is essentially a frontier-technology fund, not a broad technology ETF or a simple semiconductor or AI proxy. It is instead designed to capture companies associated with the long-term commercialization of quantum computing through its mandate. While this is potentially appealing, it is also speculative because quantum computing is new, and most of its business models are still developing rather than mature.

What Does the Wisdom Tree Quantum Computing Fund Offer Investors?

Instead of forcing investors to pick specific quantum-related stocks on their own, the WQTM ETF is designed to provide exposure to a rules-based basket of companies that WisdomTree views as relevant to the quantum value chain. As a result, this fund is primarily for capital appreciation, with a distribution yield of 0.00%, and not for income purposes.

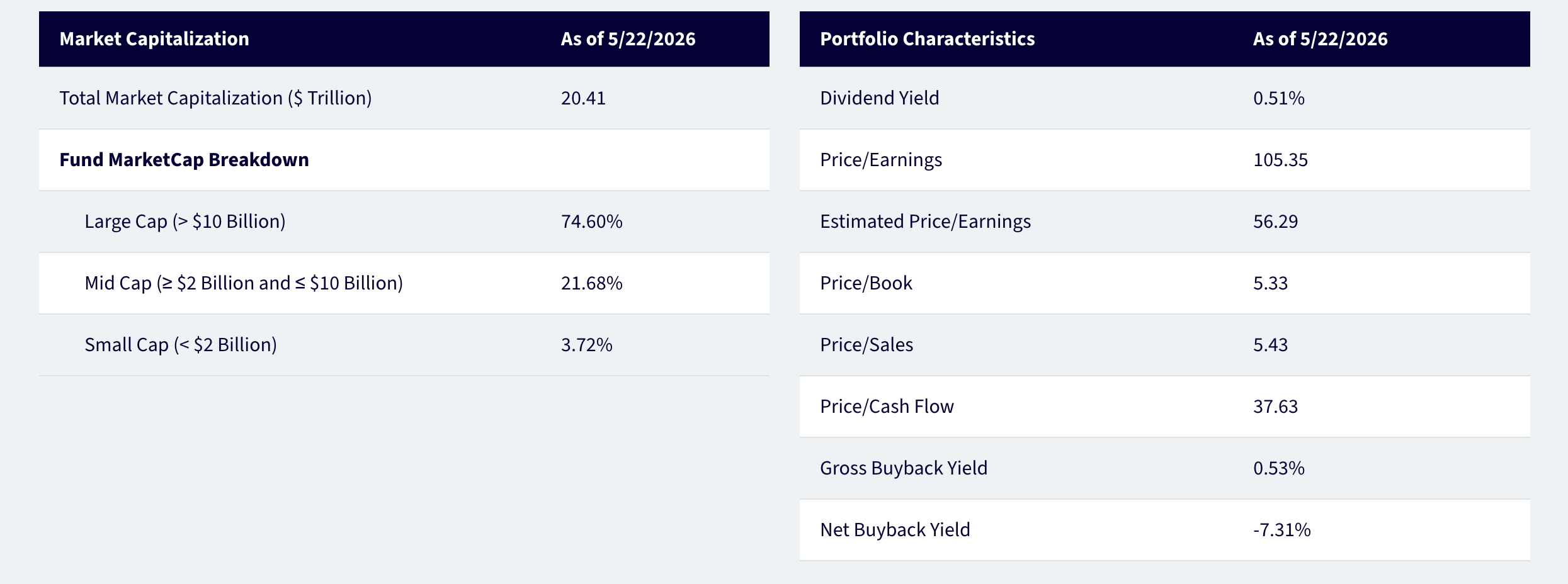

WQTM’s Market Capitalization and Portfolio Characteristics (WisdomTree Product Sheet)

As the portfolio exhibits a financial profile consistent with a high-growth thematic strategy, WisdomTree’s reported portfolio characteristics reflect higher valuation metrics, including a price-to-earnings ratio greater than 100 and an estimated price-to-earnings ratio greater than 50, based on the underlying holdings. This does not mean the fund is unattractive; however, it does raise the bar for future growth.

As of May 22, 2026, WisdomTree reported that roughly three-quarters of the fund’s market-cap exposure was to large-cap stocks, with most of the remainder in mid-cap names. This large-company focus may lessen some of the single-company risks inherent in fully speculative technology plays. All the same, this does not remove thematic risk. Should enthusiasm for quantum computing wane, or should commercialization take longer than expected, WQTM could experience volatility.

Who Might Consider WQTM?

WQTM may work for investors with broad-based, diversified core positions who want a more specific satellite investment in a long-duration technology theme. WQTM is best considered a focused, specialized investment rather than a substitute for a broad stock-market fund. It gives investors more direct exposure to quantum computing than many traditional technology ETFs.

The fund may be most relevant for investors who expect quantum computing research and experimentation to ultimately trend toward commercial adoption but prefer diversified ETF exposure rather than individually selecting particular companies or stocks. The fund may also suit investors who are prepared to bear early-stage uncertainty, high valuations, and limited operating history at the fund level. As WQTM is newly created, it has a very limited performance history.

More cautious investors, investors looking for income, or investors who are not comfortable with big price swings may find WQTM too focused or too risky.

What’s Inside WQTM? A Closer Look at Its Top Holdings

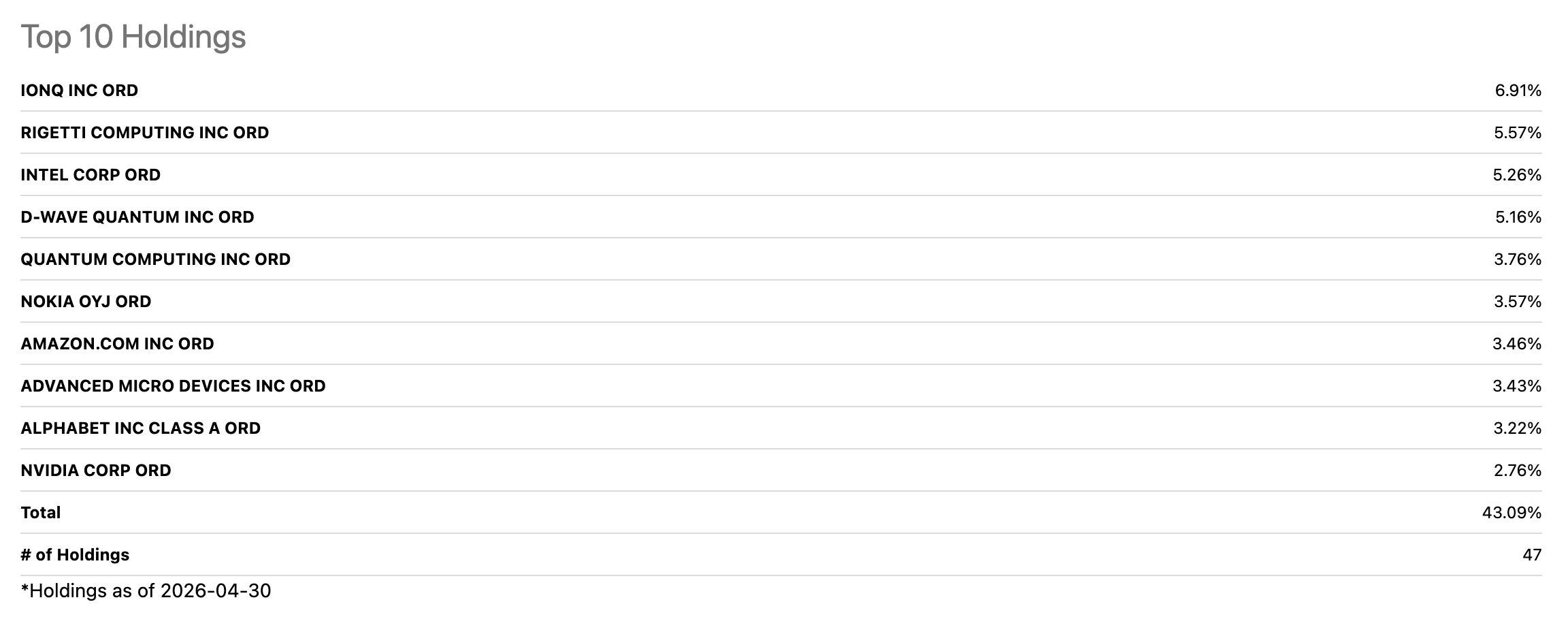

WQTM’s Top 10 Holdings (Seeking Alpha )

1) IonQ Inc. (IONQ) – 6.91%

The largest company held by WQTM is IonQ, making it one of WQTM’s most direct connections to the stand-alone quantum computing industry. IonQ is focused on developing trapped-ion quantum systems, offering cloud-based access to quantum computers, and developing business applications for quantum computing. This makes it more closely connected to the quantum-computing theme than other larger and more diversified technology companies included in the fund.

2) Rigetti Computing Inc. (RGTI) – 5.57%

Rigetti Computing is a quantum-computing company focused on building quantum-computer hardware. The company produces superconducting quantum processors and supplies quantum systems to local research organizations, national laboratories, and quantum research centers. The reason Rigetti has such appeal as a stock investment is that it is directly addressing one of the largest obstacles facing quantum computing right now: hardware.

3) Intel Corp. (INTC) – 5.26%

Intel contributes to WQTM through a distinct type of exposure. Although Intel is not considered a pure quantum computing business, it has still made itself valuable to the overall quantum-computing market through its role in the semiconductor manufacturing industry, its lengthy history in chip design, and its extensive research and development activities.

4) D-Wave Quantum Inc. (QBTS) – 5.16%

Over several years, D-Wave has remained commercially active in quantum systems. The company is primarily associated with quantum annealing, a specialized approach aimed at solving optimization-based problems; yet, D-Wave has also positioned itself as a company focused on providing enterprise-level services and developing applications based on quantum technologies.

5) Quantum Computing Inc. (QUBT) – 3.76%

Quantum Computing Inc. is a higher-risk stock, as it is a smaller and more volatile company that adds another level of pure-play exposure to the quantum computing sector. The company develops integrated photonics-based quantum computers for use in computing, artificial intelligence, cybersecurity, and sensing. While the company’s progress is notable, it remains early-stage by public-market standards.

6) Nokia Oyj (NOK) – 3.57%

Nokia may seem less obvious at the outset, but its inclusion in the fund reflects quantum’s involvement with networks, security, and advanced communications through Bell Labs and its related research activities. It gives the fund exposure to quantum-computing infrastructure and related research. This can help balance out the smaller, riskier companies in the fund that focus more directly on quantum computing.

7) Amazon.com Inc. (AMZN) – 3.46%

Thanks to its cloud infrastructure and quantum access, Amazon.com gives WQTM exposure to quantum computing. The Amazon Braket managed service allows researchers and developers to run experiments on quantum computers, use simulators, and run hybrid workflows through AWS.

8) Advanced Micro Devices Inc. (AMD) – 3.43%

Within the context of an enabling technology company, AMD fits WQTM because of its position in supporting quantum innovation through the use of its chips, GPUs, FPGAs, and system components in high-performance computing environments. These technologies allow scientists to simulate, control, and integrate quantum workloads. AMD is not selling a mainstream quantum computer. Nevertheless, progress in quantum computing may still depend on the powerful traditional computing technology that AMD provides.

9) Alphabet Inc. Class A (GOOG) – 3.22%

WQTM has access to one of the deepest corporate quantum research initiatives globally through Alphabet’s Class A shares. Google Quantum AI is focused on developing large-scale, error-corrected quantum computers, and Alphabet has positioned itself as a serious long-term competitor in quantum computing. Alphabet is certainly not a pure-play quantum stock. Advertising, cloud, and its other businesses account for the majority of its earnings. However, the research being done in quantum computing provides investors with meaningful research-backed exposure.

10) NVIDIA Corp. (NVDA) – 2.76%

NVIDIA’s place in the top ten is representative of acceleration rather than direct quantum ownership. Its CUDA-Q platform allows quantum processors to connect with both GPUs and CPUs, allowing developers to create hybrid quantum-classical applications before fully mature quantum hardware exists. Quantum computing will most likely need classical computing for simulation, control, and error correction.

WQTM Performance Overview

WQTM’s Momentum Stats (Seeking Alpha)

The data signals to investors that WQTM is a newer ETF with strong near-term momentum, reasonable fees, and a risk profile with many unknowns. The most recent returns are likely what will primarily catch investor attention, as they have been very large for an exchange-traded fund. The one-month return of 22.24% and six-month return of 58.31% are extremely high compared to median returns for other ETFs of 1.34% and 9.58%, respectively. Additionally, the YTD price return of 48.03% is significantly greater than the S&P 500’s (SP500) gain of 9.17%.

WQTM’s Momentum Stats (Seeking Alpha)

Basically, WQTM is built to capture one specific technology theme. When that theme is working, the returns can move quickly. The one-week price return of 12.64% makes that clear.

Market sentiment can change quickly in favor of high-growth tech, speculative innovation, and quantum-related stocks, which may lead to a sharp rise in WQTM and therefore a significant return. Nonetheless, the downside also cuts both ways.

WQTM Dividend Scorecard

The fund’s lack of a dividend also clarifies how it should be viewed. Instead, most of the potential return depends on the fund’s price going up. This is common for funds focused on emerging technologies.

WQTM: Expenses

WQTM’s Expense Stats (Seeking Alpha)

0.45% is a fair expense ratio for a specialized thematic ETF, and it falls below the 0.50% median for all ETFs. Most thematic funds will have higher fees than broad-index ETFs, and these higher costs can reduce returns over time.

State Street SPDR S&P 500 ETF Expenses (Seeking Alpha)

In this case, it will not be as cost-effective as a broad-based S&P 500 ETF (SPY). Investors are essentially paying for narrow exposure to a particular idea rather than basic market exposure.

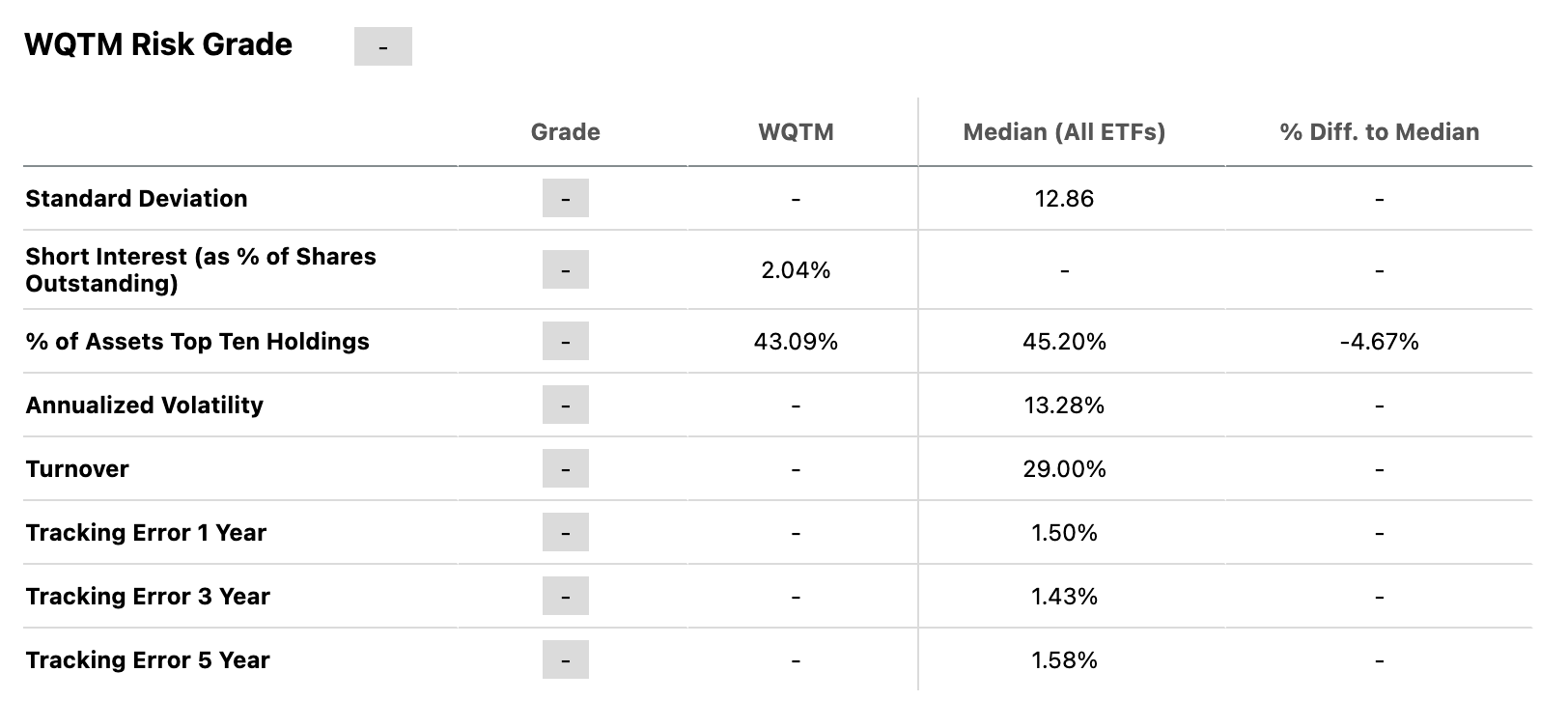

WQTM: Risks

Here are the downsides to WQTM: risk metrics are mixed and incomplete. Standard deviation, annualized volatility, turnover, and tracking error are missing, making it difficult to assess the level of risk with the same confidence as a traditional ETF that has existed for many years.

WQTM’s Risk Metrics (Seeking Alpha)

Even so, we do have a concentration figure. The top ten holdings represent 43.09% of the fund’s assets, which is just under the overall ETF median of 45.20%. Therefore, while WQTM does not seem to be especially concentrated when compared to other ETFs, this may not be a good comparison for evaluating WQTM because many of its top ten holdings have similar investment themes.

Short interest at 2.04% of shares outstanding is not a high percentage. Nevertheless, it is enough to show that some investors have taken positions against the ETF. It suggests these investors are either hedging their exposure to the fund or speculating that there may be a downturn. This does not prove that investors are becoming strongly negative on WQTM. Notwithstanding, it does show that the market is not treating WQTM as a safe, widely agreed-upon investment.

Should You Invest In WQTM?

Investors interested in having a small slice of quantum computing without picking their own quantum stocks can use WQTM. Although quantum computing is still an early-stage technology, it is making progress. The best opportunity to take advantage of WQTM investments may come if you have already built an established, diversified portfolio and are comfortable with the possibility that this investment may drop sharply and stay down for an extended period during the time required for the fund’s strategy to prove itself, which may take years. WQTM provides no meaningful income. Therefore, if you need a source of dividend income or steady returns, you may need to find other investment vehicles.

This article answers three main questions about WQTM:

- What are the benefits and risks of investing in WQTM?

- How volatile is WQTM compared to the overall market?

- Are there concentration risks with WQTM?

Anadolu | Anadolu | Getty Images

American Airlines plans to outfit more than 500 of its narrow-body aircraft with Starlink, handing another win to Elon Musk‘s SpaceX unit that has made inroads with major carriers for in-flight Wi-Fi.

American was evaluating Starlink and Amazon Leo as recently as March for the service.

The airline announced Tuesday it would install Starlink on about 500 of its narrow-body Airbus planes, like the A321neo, starting early next year. American spokesman said the carrier doesn’t have immediate plans to change providers on its Boeing fleet, which uses a mix of Viasat and Panasonic.

American in January rolled out free in-flight Wi-Fi for members of its frequent flyer program, following United Airlines, Delta Air Lines and others.

Delta in March said it would use Amazon Leo for in-flight Wi-Fi for hundreds of jets starting in 2028. United, Southwest Airlines and Alaska Airlines, which merged with Hawaiian Airlines in 2024, have selected Starlink.

Carriers are battling for higher-spending customers, including by upgrading once-slow, expensive and clunky in-flight internet to higher speeds. They have also been weighing other revenue streams, like personalized ads for travelers.

SpaceX, meanwhile, is preparing to go public in what’s likely to be a record IPO next month. Its connectivity unit, which includes Starlink, posted revenue of $11.39 billion last year, making up 61% of total sales, SpaceX said in a filing for its initial public offering earlier this month.

Some online casino players stick to the same slot titles for years. Others open a gaming site, scroll for ten minutes, then leave because nothing feels fresh.

That gap matters more now than ever. Players want variety, faster gameplay, smoother graphics, and features that feel worth their time. A stale game library quickly pushes people away. A fresh release, though, can keep someone engaged for hours without forcing the experience. That shift is changing how gaming platforms compete, how developers launch titles, and how players decide where to spend their time online.

Many players now search for gaming platforms with new games to explore, as newer titles often offer smarter bonus rounds, shorter loading times, and more creative themes. Some focus on quick play sessions. Others add layered rewards that slowly build over time. This guide explains why fresh casino games matter, what features set them apart, and how players can choose titles that match their style without wasting time. We will also cover simple ways to test games, spot quality mechanics, and avoid titles that look exciting but offer little real value. Let’s be honest, nobody enjoys clicking through ten dull slots just to find one decent game.

The online casino space changes fast. One month, cluster pays dominate the market. Next month, crash games will suddenly pull huge audiences. Players who understand these trends usually make better choices. They also enjoy gaming more because they know what to look for before spinning the reels. That is exactly what this guide aims to help with, clearly and practically.

What makes fresh casino releases more appealing to players

New casino games often feel smoother because developers build them for current devices and player habits. Older slots may still work well, but many feel slow or repetitive over time. Fresh releases usually include cleaner menus, faster animations, and simpler controls. You also see more variety in themes. One title may focus on ancient legends, while another uses sports, music, or comic-inspired visuals. That mix keeps players curious and willing to try something different. People enjoy feeling surprised by a game rather than predicting every feature within minutes.

Another reason newer releases stand out is the reward structure. Developers now add layered bonuses that unlock gradually over the course of play. That creates stronger engagement without making the game too hard to understand. Some titles include random mini-events or daily tasks to keep gameplay active. You might notice that newer games also explain mechanics better than older slots. Instructions are shorter and easier to follow.

Here are a few features players now expect from modern casino games:

- Faster loading and mobile support

- Simple bonus explanations

- Shorter but more active gameplay rounds

- Better sound design and smoother visuals

- Flexible betting options for different budgets

Players also pay attention to fairness and transparency. Many newer titles clearly show return percentages. That helps users compare games before spending money. Small details like this build trust faster than flashy graphics alone.

How to choose games that match your playing style better

Choosing the right casino game is not only about graphics or jackpots. Your personal habits matter more than most people think. Some players enjoy quick rounds during short breaks. Others prefer longer sessions with story-driven features. Picking a game that fits your pace usually leads to a better experience. A fast-paced game may frustrate someone who enjoys slow, strategic play.

In the same way, a detailed slot can feel tiring for someone who wants quick action. You might be wondering if there is a perfect game type for everyone. There really is not. The goal is to find balance.

Players should first check how bonus systems work before starting. Some games rely heavily on random rewards. Others let progress build over time through missions or unlockable rounds. Reading the game details for two minutes can save a lot of disappointment later. RTP percentages also matter because they give a rough idea of long-term returns. That number does not guarantee wins, but it helps fairly compare titles.

A simple approach can help narrow your choices:

- Check the game speed: Fast rounds suit short sessions better. Slower games often focus more on strategy and bonus depth.

- Review the reward system: Some players enjoy random jackpots. Others prefer smaller but steady features.

- Test the demo version first: Free modes help you understand gameplay before spending money.

- Compare mobile performance: A game should run smoothly on phones and tablets without lag.

Taking a few minutes to compare these points makes gaming feel less random and more enjoyable overall.

Why mobile gaming has changed casino game development

Mobile gaming has pushed developers to rethink nearly every aspect of casino design. A few years ago, many games worked best on desktop screens. Today, most players use phones first. That shift forced studios to simplify controls, improve loading times, and design games that work smoothly on smaller displays. People no longer want long waits or cluttered menus. They want instant access and clear layouts that make sense within seconds.

Developers also changed how they structure gameplay because mobile users behave differently. Many players open games during travel, lunch breaks, or short free moments. That means sessions are shorter but more frequent. New titles now include quicker bonus triggers and simpler navigation to fit those habits. Some games even reduce unnecessary animations because players care more about speed than dramatic effects.

Several mobile-focused trends now shape modern casino games:

- Vertical screen support for easier phone use

- Touch-friendly controls with fewer buttons

- Faster round transitions

- Lightweight graphics for smoother performance

- Short gameplay loops that suit busy schedules

Battery usage matters too, oddly enough. Heavy games drain phones’ batteries quickly, so developers now optimise performance more carefully. Players may not notice those technical changes directly, but they feel the difference during play. A smooth experience keeps people engaged longer. A laggy game usually gets closed within minutes. That reality shapes nearly every new casino release today.

Where smarter gaming choices can lead next

We have covered how fresh casino games improve player experiences, why mobile design matters, and how choosing the right titles can make gaming more enjoyable. Online gaming is constantly evolving, and players who stay informed often get more value from their time online. New releases continue shaping player habits, bonus systems, and gameplay styles across the industry. By staying curious and trying different formats, players can discover games that feel more rewarding and entertaining. We always encourage balanced gaming, smart decisions, and careful exploration so the experience stays fun, engaging, and enjoyable over the long term without unnecessary pressure or frustration.

Business

Princes CEO Simon Harrison moving to Ultimate Products as Salter owner reveals ‘momentous’ succession plan

Analysts call it a ‘great new CEO appointment’

Ultimate Products has named Simon Harrison as its next CEO(Image: Ultimate Products)

Consumer goods group Ultimate Products has appointed Princes Group CEO Simon Harrison as its first external boss in a ‘momentous’ move welcomed by analysts today. Ultimate Products (UP) will also see its founder and current CEO stand down from their executive roles to become board members after decades growing the Oldham business.

Mr Harrison will succeed Andrew Gossage, who will be standing down in October following more than 20 years in executive roles at UP. After a short sabbatical, Mr Gossage will rejoin UP as a non executive director from May 1 next year.

Simon Showman, who founded the group in 1997 and was CEO until 2024, will continue as president when he moves to a non-executive director role from June 1 this year.

Mr Harrison joined Liverpool’s Princes Group as chief commercial officer in 2021 and became CEO in 2024. He was in charge when Princes was taken over by Newlat and listed on the Stock Exchange. Before Princes, he spent almost 20 years at Coca Cola European Partners.

He will join UP as CEO designate on September 5 this year before becoming chief executive on October 26. UP’s share price rose as much as 10% in morning trading after the morning update.

UP bills itself as “the home of brands”, with 12 product divisions. Its brands include kitchen equipment specialist Salter as well as Beldray, which traces its history back to 1872 and which invented the adjustable ironing board.

In a research note this morning, analysts Clive Black and Darren Shirley at Shore Capital said the board changes were “momentous” but that Mr Harrison was a “great new CEO appointment”.

They said: “For the employees of UP, the announcements of Messrs. Gossage and Showman’s departures as executives will be a momentous one, noting the very special corporate culture that this management team has engendered over more than two decades, a very special component, in truth, of the commercial community in Greater Manchester.

“However, in Mr Harrison, we see an experienced and capable executive who has the basis to nurture what is already special, whilst exploring the next chapters for customers, shoppers, and shareholders to collectively harvest to beneficial effect. We commend Andy Gossage and Simon Showman on their collective achievements and congratulate Mr Harrison on his appointment, wishing all well for the future.”

Christine Adshead, chair of UP, said: “We are delighted to welcome someone of Simon Harrison’s calibre to Ultimate Products. He brings outstanding leadership qualities, strong operating discipline and considerable commercial experience, and we are confident that he has the right credentials to take Ultimate Products forward into its next chapter. We look forward to welcoming him to the team.

“Andrew has made an extraordinary contribution to Ultimate Products in more than two decades with the group. He was a driving force behind UP’s evolution from a sourcing business into the Home of Brands, navigated the business through the operational challenges of the COVID period, and played a leading role in building the Group’s online business, which has grown twelvefold since IPO. He was also central in establishing our graduate development scheme, and more recently, has overseen the group’s ground-breaking automation programme.

“Without Simon Showman, who founded the business and led it for 27 years, there would be no Ultimate Products. He has been fundamental to UP’s development from a founder‑led sourcing business into the multi‑brand homewares group it is today. Simon’s entrepreneurial approach and sharp commercial instincts have shaped the business and the fast-moving culture that underpins it. Under his leadership, the group built a diversified portfolio of brands, established deep and enduring retailer relationships, and expanded its international footprint, while remaining rooted in the values and ambition that have defined it from the outset.

“I know I speak for everyone at Ultimate Products in thanking Andrew and Simon for their exceptional endeavours, dedication and loyalty, and we are delighted that they will remain with the group as non-executive directors.”

Simon Harrison, incoming chief of UP, said: “Ultimate Products is a business with significant potential, based on a portfolio that includes some of the best-known brands in UK homeware, and supported by long-standing customer relationships and a scalable commercial model.

“I am delighted to be taking on the CEO role from Andrew Gossage, who alongside Simon Showman, has built and developed the business into the strong platform it is today. This represents an exciting personal opportunity for me, and I look forward to working with the board and the wider team to lead the business into what I am confident will be a bright future.”

Ultimate Products’ CEO and co-founder Simon Showman and current CEO Andrew Gossage(Image: Harry Page Images)

Andrew Gossage, outgoing chief executive, said: “Ultimate Products has been a hugely important part of my life for the past two decades, and I am enormously proud of the successful, diversified business we have built.

“As CEO, part of my focus has been to ensure the business is well prepared for the future, including putting in place the right leadership, structure and succession plan to support its long-term development. With those strong foundations now established, this feels like the right time for me to step back from my day-to-day responsibilities and, after a short break, take on a non-executive director role with the group. I would like to thank colleagues past and present whose commitment has made my time at Ultimate Products so rewarding.”

Simon Showman, president and founder, added: “I am hugely excited about the next phase for Ultimate Products. The business has a strong executive team in place, with the ability to continue delivering the wide range of beautiful, more sustainable products we are known for.

“I am also delighted to welcome Simon Harrison to the business as our first external CEO. His FMCG leadership experience makes him ideally placed to build on the momentum we have created. I am also pleased to remain involved with the group as a non-executive director, and look forward to seeing our excellent team realise the substantial opportunity ahead.”

NEW YORK — Shares of Firefly Aerospace Inc. jumped more than 20% on Tuesday, reaching $59.60 in morning trading as investors responded to the company’s expanding role in national security programs and continued strong demand for its space infrastructure solutions.

The Texas-based space and defense technology company has seen its stock climb sharply in recent sessions, driven by a series of contract wins with the U.S. Space Force and progress on key lunar and orbital programs. Firefly’s Alpha rocket and advanced spacecraft capabilities have positioned it as a key player in both commercial and government space initiatives.

The latest surge reflects growing confidence in Firefly’s ability to execute on its ambitious backlog and capitalize on increasing government investment in resilient space architecture. With a record $498 million backlog at the end of the first quarter, the company has substantial visibility into future revenue streams as it scales production across multiple programs.

Firefly reported record first-quarter revenue of $80.9 million in early May, up 40% from the prior quarter. The results were driven by integration of recent acquisitions and ramp-up of major government programs, including the FORGE missile warning system and contributions to the Golden Dome space-based interceptor initiative.

The company reiterated its full-year 2026 revenue guidance of $420 million to $450 million, assuming continued execution on its launch manifest and spacecraft solutions. Management highlighted steady progress across its launch business, successful Alpha Flight 7 mission, and Blue Ghost lunar lander milestones as key drivers of momentum.

Firefly’s subsidiary SciTec recently received an agreement to advance the Space Force’s space-based missile defense efforts under the Golden Dome program. The company has also been selected for multiple tactically responsive space demonstrations, showcasing its ability to deliver rapid, reliable access to orbit for national security payloads.

The stock’s performance comes amid broader strength in the aerospace and defense sector. Increased U.S. and allied spending on space technology and uncrewed systems has created favorable conditions for specialized providers like Firefly. Its focus on affordable launch services, in-space manufacturing and advanced spacecraft has resonated with both government and commercial customers.

Analysts have grown increasingly positive on Firefly’s outlook. Several firms have raised price targets in recent months, citing structural tailwinds from AI-driven data demands, lunar exploration programs and national security priorities. The company’s ability to secure long-term contracts provides earnings predictability that differentiates it from more cyclical peers.

Firefly’s Alpha rocket successfully returned to flight in March with the Stairway to Seven mission, validating key Block II upgrades ahead of more frequent launch cadence. The company is targeting late summer for the debut of its upgraded Alpha Block II configuration, which promises improved reliability and performance for both commercial and defense missions.

The company continues expanding its manufacturing footprint. Recent announcements include an expanded campus and innovation lab in Central Texas to accelerate spacecraft production. These investments support growing demand for Firefly’s Blue Ghost lunar landers and other orbital platforms.

Firefly’s strategic positioning has attracted significant investor interest. The stock has shown strong momentum throughout 2026, reflecting the market’s appetite for companies at the intersection of commercial space and national security. Tuesday’s move extends a powerful rally that has seen shares more than double in recent months.

For investors, Firefly represents exposure to multiple high-growth themes. The company’s launch services address the increasing need for responsive and affordable access to space, while its spacecraft and payload solutions support everything from Earth observation to lunar infrastructure development.

The company’s leadership has emphasized disciplined execution and operational scaling. CEO Jason Kim highlighted the team’s focus on meeting demand for frequent lunar landings, regular launch cadence and critical national security missions. This balanced approach has helped Firefly build credibility with both government and commercial customers.

Challenges remain, including competition from larger players like SpaceX and Blue Origin, as well as the technical risks inherent in space operations. However, Firefly’s niche focus on medium-lift launch and specialized spacecraft has allowed it to carve out a distinctive market position.

The latest stock surge adds to what has been a remarkable period for Firefly shareholders. The company’s transition from startup to public company with substantial government contracts demonstrates the commercial potential of innovative space technology.

As Firefly continues executing on its backlog and pursuing new opportunities, investors will watch closely for further evidence of margin expansion and successful mission outcomes. The company’s ability to deliver on its guidance will be a key test of management’s ability to scale operations effectively.

Tuesday’s trading volume was significantly elevated as the stock broke through recent resistance levels. The move suggests broad participation from institutional and retail investors drawn to Firefly’s compelling growth narrative in the space and defense sectors.

The aerospace industry continues attracting capital as nations and companies invest in next-generation capabilities. Firefly’s focus on responsive launch and advanced spacecraft positions it well within this expanding market, where reliability, cost-effectiveness and rapid deployment are increasingly valued.

Looking ahead, Firefly has a busy manifest with multiple Alpha launches planned for the remainder of 2026. Successful execution on these missions, combined with continued contract wins, could provide additional catalysts for the stock.

The company’s story exemplifies the commercialization of space and the growing intersection between private industry and government priorities. For Firefly, this convergence has created substantial opportunities that are now translating into financial performance and market recognition.

As the trading day continues, Firefly shares will likely remain in focus. The significant move highlights the stock’s sensitivity to positive contract news and broader sentiment around space infrastructure spending.

The defense and commercial space sector’s momentum appears intact, with Firefly leading gains on strong operational progress. Investors will continue monitoring developments in launch cadence, spacecraft deployments and new contract awards as the year progresses.

NEW YORK — Shares of United Microelectronics Corporation jumped more than 17% on Tuesday, climbing to $21.34 as investors responded to robust April revenue figures and growing optimism about the company’s position in the expanding artificial intelligence semiconductor market.

The Taiwanese foundry operator, one of the world’s largest contract chipmakers, reported April consolidated sales of NT$22.66 billion, up 10.8% from the same month a year earlier. The strong monthly performance contributed to year-to-date sales of NT$83.70 billion, representing a 6.88% increase over the first four months of 2025.

The surge in UMC stock reflects renewed confidence in the semiconductor sector’s recovery and the company’s ability to benefit from rising demand for advanced chips used in artificial intelligence applications, automotive electronics and consumer devices. UMC has been expanding its capacity in higher-margin segments, including 22-nanometer and 28-nanometer processes, which are seeing strong utilization rates amid global supply constraints.

Analysts noted that UMC’s April results signal improving momentum after a period of softer demand in certain end markets. The company has benefited from increased orders from fabless chip designers seeking capacity outside of leading-edge foundries dominated by TSMC. This diversification strategy has helped UMC maintain stable utilization rates even as the broader industry navigates cyclical pressures.

United Microelectronics reported solid first-quarter 2026 earnings earlier this month, with revenue and earnings per share beating Wall Street expectations. The results were driven by strong performance in specialty technologies and steady contributions from its 12-inch wafer fabs. Management highlighted improving customer demand and disciplined cost management as key factors supporting profitability.

The company’s focus on mature and specialty process nodes has proven advantageous in the current market environment. While leading-edge nodes remain dominated by a few players, UMC’s expertise in 28nm, 22nm and specialty technologies serves a broad base of customers in automotive, industrial and communications sectors. These markets are seeing sustained demand driven by electrification, automation and 5G/6G infrastructure buildouts.

UMC’s strategic partnerships and capacity expansion plans have also drawn positive attention. The company continues investing in its global manufacturing footprint, with ongoing upgrades at facilities in Taiwan and Singapore. These investments are aimed at meeting growing demand for power management, display driver and embedded memory solutions.

Tuesday’s sharp move in UMC shares extended a strong performance for semiconductor stocks tied to AI and specialty applications. The Philadelphia Semiconductor Index has posted solid gains this year, supported by expectations of continued capital spending by technology companies building out artificial intelligence infrastructure.

Investors appear to be rewarding UMC’s conservative approach and focus on profitability rather than chasing leading-edge market share. The company has maintained a disciplined capital expenditure program while generating strong free cash flow, providing flexibility for dividends, share buybacks and strategic investments.

Analysts have generally maintained positive outlooks on UMC. Several firms have raised price targets in recent weeks, citing improving industry fundamentals and UMC’s attractive valuation relative to peers. The stock’s current levels reflect expectations of sustained mid-single-digit revenue growth and margin expansion through 2027.

The semiconductor industry continues navigating a complex environment. Geopolitical tensions, particularly around U.S.-China technology restrictions, have created both challenges and opportunities for foundry operators. UMC has focused on compliance and diversification to mitigate risks while capitalizing on demand from customers seeking stable, non-restricted capacity.

For UMC, the current upcycle in specialty semiconductors provides a favorable backdrop. Automotive and industrial customers are increasing orders for chips used in electric vehicles, renewable energy systems and factory automation. These long-cycle markets offer more predictable demand patterns compared to consumer electronics.

The company’s April sales figures mark the second consecutive month of double-digit year-over-year growth, suggesting the inventory correction that weighed on the industry in 2025 has largely run its course. Management has expressed confidence that utilization rates will continue improving through the remainder of 2026.

United Microelectronics maintains a strong balance sheet with low debt levels and healthy cash reserves. This financial flexibility allows the company to weather cyclical downturns while pursuing growth opportunities. The firm has consistently paid dividends, providing income alongside potential capital appreciation for shareholders.

As the trading day progressed, UMC shares remained among the top performers in the semiconductor sector. The move highlights the market’s rotation toward companies with strong fundamentals and exposure to multiple growth drivers rather than pure AI plays that have commanded premium valuations.

Looking ahead, UMC’s second-quarter results, expected in July, will be closely watched for further confirmation of its guidance and margin trends. Analysts anticipate continued sequential improvement as seasonal demand patterns and new capacity come online.

The broader semiconductor outlook remains constructive. Artificial intelligence, automotive electrification and industrial digitization are creating multi-year demand tailwinds. UMC’s specialty focus positions it well to capture a meaningful share of this growth while avoiding direct competition in the most capital-intensive leading-edge nodes.

For investors, UMC offers exposure to a more stable segment of the semiconductor value chain. While not immune to industry cycles, the company’s diversified customer base and focus on essential technologies provide downside protection compared to more volatile memory or leading-edge logic suppliers.

Tuesday’s trading volume was significantly elevated as the stock broke through recent resistance levels. The move suggests broad participation from both institutional and retail investors drawn to UMC’s improving fundamentals and attractive valuation.

The semiconductor sector’s momentum appears intact, with UMC joining other specialty players in posting strong gains on positive industry data. Investors will continue monitoring global chip demand, inventory levels and geopolitical developments as the year progresses.

United Microelectronics’ performance this year demonstrates the market’s appreciation for consistent execution and strategic focus. As the company advances its capacity expansion and technology roadmap, it remains well-positioned to deliver value for shareholders in an increasingly digital and connected world.

Phoenix is a developer and manufacturer of fragrance and flavor extracts.

Business

Intuitive Machines Shares Surge 15% on Strong Lunar Program Momentum and NASA Contract Wins

NEW YORK — Intuitive Machines Inc. shares climbed more than 15% on Tuesday, reaching $44.17 in morning trading as investors cheered the company’s continued progress on key NASA lunar missions and expanding commercial opportunities in the rapidly growing space infrastructure sector.

The Houston-based space technology company, known for its Odysseus lunar lander and advanced robotic systems, has emerged as a leader in commercial lunar services. Tuesday’s sharp move reflects growing confidence in Intuitive Machines’ ability to execute on its backlog of government and private contracts while positioning itself at the forefront of the U.S. return to the Moon.

Intuitive Machines reported strong first-quarter results earlier this month, with revenue exceeding expectations and significant milestones achieved on its IM-2 and IM-3 missions. The company has secured multiple NASA Commercial Lunar Payload Services contracts and is advancing preparations for crewed lunar operations under the Artemis program.

Analysts have grown increasingly bullish on the company’s outlook. Several firms raised price targets in recent weeks, citing accelerating demand for lunar landing services and Intuitive Machines’ technological edge in precision navigation and payload delivery. The stock’s performance this year has been exceptional, with shares more than tripling as investors rotate into companies benefiting from increased government and commercial space spending.

The latest rally was fueled by positive updates on the company’s upcoming missions and strategic partnerships. Intuitive Machines recently completed critical testing for its next lunar lander, demonstrating improved reliability and payload capacity. The company is also expanding its manufacturing capabilities to meet growing demand from both NASA and private customers seeking lunar surface access.

Intuitive Machines’ success builds on the foundation of its Odysseus mission, which achieved the first U.S. commercial lunar landing in 2024. That milestone established the company as a credible player in a market previously dominated by government agencies. Subsequent missions have refined landing precision and expanded scientific capabilities, strengthening customer relationships and competitive positioning.

The broader space economy continues expanding rapidly. NASA’s Artemis program, commercial satellite deployments and emerging lunar resource initiatives are driving demand for reliable transportation and infrastructure services. Intuitive Machines is well-positioned to capture a meaningful share of this market through its flexible lander designs and end-to-end mission support.

Company executives have expressed confidence in the long-term opportunity. CEO Steve Altemus has highlighted the transition from development to operational cadence, with multiple missions planned annually. This increased flight rate is expected to drive revenue growth and margin expansion as fixed costs are spread across a larger number of launches.

Intuitive Machines reported first-quarter revenue of $41.2 million, up significantly from the prior year. The company maintains a healthy backlog that provides visibility into future quarters. Management has guided for continued revenue growth through 2026 as new contracts are executed and commercial opportunities mature.

The stock’s surge also comes amid broader strength in the aerospace and defense sector. Increased government investment in space technology, combined with private sector interest in lunar commerce, has created favorable conditions for specialized providers like Intuitive Machines. The company’s focus on lunar logistics and surface operations differentiates it from pure launch providers.

Analysts project strong growth for Intuitive Machines over the next several years. Consensus estimates call for revenue to more than double by 2027 as mission cadence increases and new services are introduced. Profitability is expected to improve as scale benefits materialize and higher-margin contracts contribute more significantly to the mix.

For investors, Intuitive Machines represents exposure to one of the most compelling secular growth stories in technology and aerospace. The combination of government contracts, commercial partnerships and expanding lunar economy creates multiple avenues for value creation. However, the stock’s volatility reflects typical risks associated with space companies, including technical challenges and dependence on large government programs.

Tuesday’s trading volume was significantly elevated as the stock broke through recent resistance levels. The move suggests broad participation from both institutional and retail investors drawn to the company’s progress and the expanding space economy narrative.

Intuitive Machines continues investing in research and development to maintain its competitive edge. Recent advancements in autonomous navigation, thermal management and payload integration have strengthened its offering for future missions. The company is also exploring opportunities in space infrastructure, including potential lunar communications and power services.

The space sector’s momentum appears intact, with Intuitive Machines joining other players in posting strong gains on positive operational updates. Investors will continue monitoring mission outcomes, new contract awards and financial performance as the year progresses.

For long-term investors, Intuitive Machines offers exposure to the commercialization of space and the growing lunar economy. The company’s achievements to date demonstrate technical capability and execution strength, positioning it for potential leadership in an industry still in its early stages of development.

As markets digest the latest gains, attention will turn to upcoming mission milestones and earnings reports. Intuitive Machines’ ability to deliver on its ambitious targets will determine whether current enthusiasm translates into sustained shareholder value in the years ahead.

The latest surge adds another chapter to what has been a remarkable period for Intuitive Machines shareholders. The stock’s performance underscores the market’s appetite for high-growth stories in strategically important sectors, even as broader economic uncertainties persist.

With multiple missions planned and expanding commercial opportunities, Intuitive Machines stands at the center of the next phase of space exploration. Its success could play a significant role in shaping humanity’s return to the Moon and beyond.

A long-term investor focused on quality growth stocks at a reasonable price. My investment objective is to identify market asymmetries with positive reward-to-risk. I invest in high-quality, wide-moat companies that generate strong cash flow and trade at a fair price relative to their value. Please feel free to subscribe to my channel to support its development.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of RDDT, META either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Running a children’s home in England means living under a level of scrutiny that most businesses never experience. Ofsted’s oversight is relentless, and rightly so.

The stakes are extraordinarily high. Yet despite how central inspection is to the sector, a surprising number of myths persist about how the process actually works.

These misconceptions aren’t harmless. They lead providers to drop their guard at the wrong moment, misread their compliance obligations, or waste energy preparing for inspections that aren’t coming while being caught off guard by ones that are.

Let’s set the record straight.

Myth 1: “Outstanding homes barely get inspected”

This is perhaps the most dangerous myth in the sector. The logic sounds reasonable – if a home has already proven it’s excellent, surely Ofsted focuses its attention elsewhere?

Not so. Every registered children’s home in England receives at least one full inspection every year, regardless of its previous grade. Outstanding, Good, Requires Improvement, Inadequate – the minimum annual full inspection applies to all. There is no inspection holiday for high performers.

What a strong previous judgement can influence is whether a home also receives an interim inspection within that same regulatory year, but it certainly doesn’t remove the home from Ofsted’s calendar.

Myth 2: “You’ll know when inspectors are coming”

Some providers still operate as though inspection is an event they can prepare for in the weeks before it arrives. This is a fundamental misunderstanding.

All Ofsted inspections of children’s homes are unannounced. There is no notice period. Inspectors prepare internally the day before, but the home itself receives no warning. The first you’ll know about a full inspection is when the inspector arrives at your door.

This is precisely why inspection readiness cannot be a project; it has to be a culture. Homes that perform well under inspection are the ones running to the same standard on a quiet Tuesday in February as they are the week after a previous visit.

Myth 3: “If no one has complained, we won’t get a monitoring visit”

Monitoring visits are often misunderstood as something triggered solely by complaints or serious incidents. In reality, Ofsted uses a much broader range of intelligence to decide when to make an additional visit.

Regulation 44 and Regulation 45 reports are completed by the independent person and typically by a member of the home’s management team respectively. These key monitoring tools feed directly into Ofsted’s risk picture. Notifications of specific incidents, changes in staffing, or patterns in missing episodes can all prompt a monitoring visit without any formal complaint ever being made.

Monitoring visits are also unannounced and, while they don’t produce an overall grade, a standard progress outcome is given and Ofsted’s findings can influence the next full inspection.

Myth 4: “How often does Ofsted inspect depends mainly on your rating”

When people ask how often does Ofsted inspect, the instinct is to assume the answer is a simple sliding scale linked to your grade. In practice, Ofsted’s approach is risk-based, and rating is only one input.

Factors including the profile of children currently placed, how accurately the home identifies and manages individual risks, recent notifications and safeguarding concerns, and intelligence gathered from a range of sources all shape Ofsted’s decisions. A home rated Good that has recently seen a pattern of serious incidents may attract more scrutiny than an Inadequate home that is demonstrably improving.

Understanding this helps providers think about compliance differently – not as a performance put on for inspectors, but as an ongoing discipline in risk management and documentation.

Myth 5: “The inspection framework stays the same year to year”

Given how much operational pressure providers are already under, it’s tempting to assume that once you understand the framework, it stays fixed. It doesn’t.

The Social Care Common Inspection Framework (SCCIF) for children’s homes has evolved significantly in recent years, with substantial changes coming into effect from April 2026. These updates are specifically designed to encourage homes to accept children with higher and multiple needs which has been a long-standing tension in the sector where providers have historically been reluctant to take more complex placements for fear of the impact on their Ofsted rating.

Staying current with framework changes isn’t optional. What inspectors are looking for, how they weigh specific findings, and how interim inspections work can all shift between regulatory years.

What this means in practice

The common thread running through all of these myths is the same: inspection is not a discrete event that happens to you once a year. It is a continuous regulatory relationship.

Providers who understand this build their quality assurance, their supervision practices, their record-keeping, and their risk management around year-round standards rather than inspection preparation. They are the ones who consistently perform well when inspectors do arrive.

The homes that struggle are often not the ones doing bad work. They’re the ones whose good work isn’t visible, documented, or embedded in the way inspectors need to see it.

Sports32 seconds ago

Venkatesh Iyer holes out for 19 right after hitting a sublime scoop shot for 6 against Kagiso Rabada in RCB vs GT IPL 2026 Qualifier 1 match [Watch]

Tech2 minutes ago

HiFiMAN HE1000 WiFi Review: Can Wireless Planar Headphones Finally Replace Cables?

NewsBeat4 minutes ago

Low Parks Museum to host programme of Scottish musical events

-

Crypto World5 days ago

Crypto World5 days agoBlockchain.com files with SEC for U.S. IPO

-

Fashion4 days ago

Fashion4 days agoHoliday Weekend Open Thread – Corporette.com

-

Business4 days ago

Business4 days agoDell Technologies DELL Stock Surges 15% on AI Server Momentum and Analyst Upgrades in 2026

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Accumulation Weakens as BTC Realized Losses Hit $600M

-

Crypto World4 days ago

Crypto World4 days agoSpace X IPO Is ‘Bad News’ for Tech Stocks: But What About Bitcoin?

-

Crypto World3 days ago

Crypto World3 days agoRobinhood crypto COO Tanya Denisova exits

-

Politics4 days ago

Politics4 days agoMakerfield: a tale of two social-media histories

-

Business2 days ago

Business2 days agoNYT Strands Answers May 24 2026 Revealed for Puzzle No. 812 Theme Summer Essentials

-

Crypto World5 days ago

Crypto World5 days agoMicroStrategy’s Saylor Says Miners No Longer Set Bitcoin Price, Another Force Has Taken Over

-

Tech5 days ago

Tech5 days agoWhatsApp ads could make Irish debut after discussions with DPC

-

Crypto World4 days ago

Crypto World4 days agoAI infrastructure race heats up as IREN pitches full-stack strategy, WhiteFiber lands $160M deal

-

Tech4 days ago

Tech4 days agoA 0.12% parameter add-on gives AI agents the working memory RAG can’t

-

Tech5 days ago

Tech5 days agoYou Can Now Add ChatGPT To PowerPoint

-

NewsBeat5 days ago

NewsBeat5 days agoCharity run by Reform leader Malcolm Offord accused of ‘law breaking’ over Scottish registration

-

Business4 days ago

Business4 days agoTrump Invests $1M-$5M in Kura Sushi USA Chain With 27 California Locations

-

Sports5 days ago

Sports5 days ago2026 CJ Cup Byron Nelson leaderboard: Brooks Koepka finds putting stroke in Round 1

-

Crypto World6 days ago

Crypto World6 days agoExa Labs raises $250 million in funding led by a16z

-

Business4 days ago

Goldman Sachs reinstates Ageas stock coverage with neutral rating

-

Tech1 day ago

Tech1 day agoMicrosoft’s quiet Claude Code retreat and the real cost of enterprise AI

-

Crypto World4 days ago

Crypto World4 days agoVerus Bridge Hacker Returns $8.5M ETH, Keeps $2.8M as Bounty

You must be logged in to post a comment Login