Crypto World

JPMorgan says debasement trade has fallen out of favor

The “debasement trade” that drove strong demand for bitcoin and gold during recent geopolitical tensions is beginning to lose momentum, according to JPMorgan analysts led by Nikolaos Panigirtzoglou.

In a report on Thursday, the bank argued investors have started pulling capital from both bitcoin and gold exchange-traded funds (ETFs) at the same time as institutions reduced exposure in futures markets tied to both assets.

That shift signals a broader retreat from macro hedge trades that became popular earlier this year amid fears of inflation and global instability stemming from tensions in the Middle East.

Bitcoin ETFs have seen significant outflows over the past two weeks, according to data from Farside Investors, in line with gold ETFs, while positions in CME bitcoin and gold futures have weakened over the same period.

Panigirtzoglou argued that the move does not appear to reflect investors rotating from bitcoin into gold, but rather that both assets are seeing softer demand at the same time.

“Bitcoin had been the main manifestation of the debasement trade since the start of the Iran conflict,” the report said.

The debasement trade refers to investor positioning in assets viewed as stores of value during periods of inflation fears or currency weakness. Bitcoin and gold often benefit when traders expect governments and central banks to increase spending, expand debt or keep monetary policy loose.

Those concerns intensified earlier this year after renewed conflict in the Middle East pushed oil prices higher and heightened worries about inflationary pressures returning.

JPMorgan said the recent pullback may reflect growing expectations that tensions between the United States and Iran could ease.

The report suggested investors may be positioning ahead of a possible diplomatic agreement between the two countries, reducing the need for inflation and geopolitical hedges that had supported bitcoin and gold.

Earlier this month, Bitmine raised roughly $274 million through the sale of 3.5 million shares of 9.50% Series A Perpetual Preferred Stock. The preferred shares, which trade on the New York Stock Exchange under the ticker BMNP, pay weekly cash dividends.

Lee has argued that the company’s staking operation provides recurring cash flow to support those obligations. Bitmine currently has 4.72 million ETH staked — more than 83% of its holdings.

The company projects annualized staking revenue of roughly $223 million, with potential staking rewards reaching $268 million annually through its MAVAN staking platform.

The firm announced another round of scheduled dividend payments extending through August, paying $0.1847 per shares.

Crypto spring

Lee reiterated his view that the crypto market is in the early stages of a recovery from the downturn that began with the October 2025 liquidation shock.

At Consensus Miami last month, he argued the bear market would be “definitely” over if bitcoin closed May above $76,000. Instead, BTC finished the month below $74,000 before briefly falling under $60,000 in early June.

Still, Lee said the recent pullback has not changed his broader outlook.

“We believe we are in the early stages of crypto spring,” he said.

Lee also reaffirmed his long-term bullish stance on Ethereum, arguing that growing demand from tokenization and artificial intelligence applications will drive adoption of the network in the years ahead.

Mining economics have deteriorated in 2026, the analysts noted, with bitcoin trading below its estimated production cost for five consecutive months. Citing CoinShares’ first-quarter mining report, JPMorgan said roughly 20% of miners are currently estimated to be unprofitable.

Financial pressure has prompted miners to sell more bitcoin holdings. Publicly traded mining companies liquidated more than 32,000 BTC in the first quarter, exceeding their combined sales for all of 2025, according to data cited by the report.

As a result, even relatively small price moves are increasingly affecting network activity. When bitcoin falls below production costs, higher-cost operators tend to shut down equipment, causing hashrate to decline and mining difficulty to adjust lower. The bank pointed to the second week of June, when mining difficulty dropped 10%, the second decline of that magnitude this year.

Looking ahead, the analysts expect heightened sensitivity in hashrate and mining difficulty to persist as long as bitcoin remains below its estimated production cost, which the bank currently puts at about $78,000. The world’s laregst cryptocurrency was trading around $64,700 at publication time.

Bitcoin miners are increasingly turning to artificial intelligence and high-performance computing (HPC) to diversify revenue as mining margins come under pressure.

The appeal is straightforward: AI hosting contracts can provide stable, multi-year revenue streams and higher margins than the more volatile economics of bitcoin mining, which have been squeezed by rising network competition and the 2024 halving.

Michael Saylor and his embattled Strategy (MSTR) sold more common stock last week, using the proceeds to add a relatively small amount of bitcoin and $300 million in cash to its balance sheet.

The company sold about 2.7 million shares of MSTR, according to a Monday morning filing, raising $335.5 million. About $35 million of that was used to acquire 520 bitcoin at an average price of $67,068 each. The other $300 million was added to cash already on the balance sheet, bringing reserves to $1.4 billion.

The latest acquisition brings Strategy’s total bitcoin holdings to 847,363 BTC, acquired at a total cost of roughly $64.01 billion, or an average purchase price of $75.651 per coin.

The Bank of England has scrapped its proposed holding caps for UK stablecoins, replacing them with a temporary £40 billion ($52.9 billion) limit on how much of any single systemic coin can be issued.

The change arrived Monday with a draft Code of Practice. It eases a rule that worried issuers. Yet it leaves Britain capping issuance of its own currency stablecoin, something neither the US nor the EU does.

From Per-User Caps to a Single Ceiling

In November 2025, the central bank proposed limiting individuals to £20,000 and businesses to £10 million per coin. Issuers called the plan costly and hard to enforce.

The reversal followed pressure at home. In June, the House of Lords Financial Services Regulation Committee urged the Bank to reconsider the limits. It warned they diverged from global norms and had alarmed crypto founders.

The Bank has now swapped those proposed holding limits for one £40 billion ceiling per coin. It says the cap shields bank lending while letting households and firms transact freely.

Why UK Stablecoin Rules Stand Alone

The contrast abroad is sharp. The US GENIUS Act, signed in July 2025, demands full cash and Treasury reserves but caps no issuance.

Europe’s MiCA stablecoin rules cap only foreign-currency coins used heavily for payments, a brake meant to defend the euro. They place no ceiling on euro stablecoins themselves.

That leaves the UK alone in capping issuance of a coin in its own currency. It is fencing a market that barely exists in sterling.

About 99% of stablecoins in circulation are dollar-denominated, the ECB reported in November.

A ceiling on supply restrains the issuer, not the user. Even that softer form of stablecoin holding caps has no parallel among big economies.

The Bigger Test is Tokenization

Issuers must back coins with 70% short-term UK government debt and 30% in deposits at the central bank. They cannot pay interest, though payment-linked rewards stay allowed.

That backing rule reaches into the gilt market. The Treasury and the Debt Management Office have flagged sterling stablecoins as possible structural demand for Treasury bills. Both plan new short-dated issuance to meet it.

Coins used mainly for trading, such as Tether (USDT) and USD Coin (USDC), stay under the Financial Conduct Authority. Redemptions must clear within 24 hours of a complete request.

The unresolved question is whether these coins can settle wholesale market trades. That answer will shape the country’s tokenization plans, and the Bank says the work continues.

“This is a major milestone in delivering greater choice and innovation in UK payments… This is truly a world leading regime,” Sarah Breeden, the Bank’s Deputy Governor for Financial Stability, said the regime builds trust for a new form of money.

Follow us on X to get the latest news as it happens

Feedback on the draft closes 22 September. The Bank aims to finalize the code by the end of 2026. That keeps the UK’s 2026 stablecoin timeline on track for the first issuers in 2027.

The supply cap lasting that long may decide if sterling stablecoins scale at home or grow elsewhere.

The post Bank of England Drops Stablecoin Holding Caps but Keeps $53 Billion Issuance Limit appeared first on BeInCrypto.

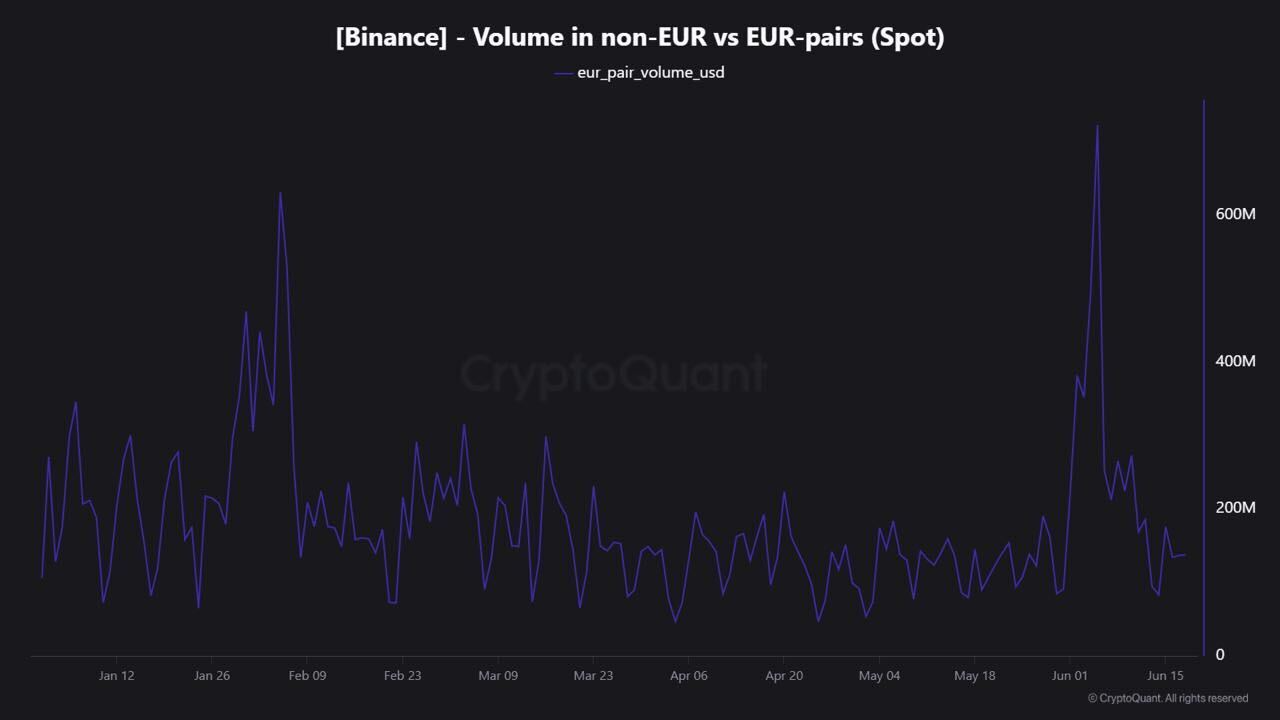

Euro-denominated trading accounts for only a small share of Binance’s activity, as the exchange faces uncertainty over its European licensing prospects under the Markets in Crypto-Assets Regulation (MiCA).

Euro (EUR) trading accounts for around 1% of Binance’s spot volume, CryptoQuant analyst Maartunn told Cointelegraph.

“Binance’s inflows remain globally distributed, which may limit the impact of potential MiCA-related setbacks,” Maartunn said, pointing to the exchange’s diversified user base across regions.

Source: CryptoQuant

The data comes as Greek regulators are reportedly preparing to reject Binance’s licensing application ahead of MiCA’s transitional deadline on July 1, a move that could complicate the exchange’s ability to serve EU residents.

Binance ranks among Europe’s biggest crypto exchanges

Even though EUR trading represents only about 1% of Binance’s global spot volume, the exchange still processes hundreds of millions of dollars in euro-denominated trades.

According to CryptoQuant data, Binance’s daily EUR-pair volumes have ranged from roughly $100 million to $250 million in 2026, with occasional spikes above $600 million.

Source: CryptoQuant

According to a December 2024 report by Kaiko, Binance, alongside Bitvavo, Kraken and Coinbase, accounted for more than 85% of all euro-denominated crypto trading volume.

Related: WhiteBIT secures MiCA license in Austria ahead of July 1 EU deadline

Unlike Binance, Bitvavo, Kraken and Coinbase are among the major exchanges that have already secured MiCA authorization, allowing them to offer services across the EU under the framework’s passporting regime.

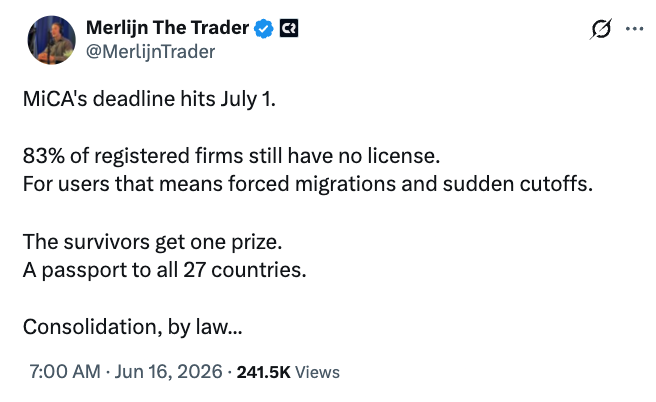

83% of CASPs have yet to receive a MiCA license

Binance’s licensing uncertainty comes as many crypto asset service providers (CASPs) are still adapting to MiCA’s requirements.

According to estimates based on European Securities and Markets Authority (ESMA) data cited by market analyst Merlijn Geurds, only around 210 of more than 1,200 firms operating under pre-MiCA registration regimes have obtained full authorization under the new framework.

Source: Merlijn Geurds

Geurds told Cointelegraph the gap reflects the cost and complexity of compliance, which requires governance standards, compliance controls and operational safeguards that many smaller firms lack.

“The result is consolidation by design,” Geurds said, adding: “A smaller group of well-capitalized, licensed players gets a passport to all 27 states, while a long tail faces forced migrations or cutoffs.”

Cointelegraph contacted Binance for comment on the size of its European business and the potential impact of MiCA-related restrictions but had not received a response by publication.

Magazine: SBF will never get a pardon, Trump peace deal boosts Bitcoin: Hodlers Digest June 14-21

Ripple’s CEO said the company might do “something special” for XRP holders if it ever goes public. The XRP community heard a promise. What he actually said was a maybe, attached to an IPO he calls a non-priority. Here is the real picture, separated from the hype.

Summary

- Ripple has not promised an IPO reward for XRP holders.

- Garlinghouse only left the door open to a possible future benefit.

- Ripple equity and XRP are separate assets with no automatic holder link.

- The real XRP case still depends on utility, regulation, adoption, and demand.

One sentence from Ripple’s chief executive set the XRP community alight. Asked on a podcast whether XRP holders might benefit if Ripple ever went public, Brad Garlinghouse said there could be a scenario where the company does “something special” for people who hold XRP, then immediately added that it was not something for the immediate term.

Within hours, the remark had been clipped, shared, and amplified into something close to a promise, with community members urging others to “hold accordingly.” But the gap between what Garlinghouse actually said and what the community heard is wide, and it matters.

The difference between a hinted-at maybe and a planned reward is the difference between a reasonable hope and a misplaced expectation. This piece separates the two, laying out exactly what was said, what it could mean, what stands in the way, and what an XRP holder should realistically take from it.

The subject sits at the intersection of two real questions: whether and when Ripple will go public, and whether holding XRP, which is a separate asset from Ripple equity, entitles you to any share of Ripple’s corporate success. These are questions the XRP community has debated for years, and Garlinghouse’s comments touched the nerve directly without resolving it.

This guide covers what Garlinghouse actually said and the precise wording that matters, the crucial distinction between Ripple the company and XRP the token, the theoretical mechanisms a holder benefit could take, why Ripple says an IPO is not a priority right now, the case that XRP holders already benefit indirectly, and what all of it adds up to for someone holding XRP today.

The goal is to give you the real picture, neither dismissing the possibility nor inflating it into the certainty the hype implied.

What Garlinghouse actually said

Precision matters here, because the entire community reaction hinges on a few words, and those words were more careful and more conditional than the excitement suggested.

Speaking with a journalist on a podcast, Garlinghouse was asked directly whether XRP holders could benefit from Ripple’s success if the company eventually launched an IPO. He did not deflect the question, but he did not commit to anything either.

His framing began with the indirect benefit Ripple already provides. He said he hopes XRP holders feel they are benefiting from Ripple’s existence through the work the company does to catalyze activity in the XRP ecosystem.

Then came the sentence that set off the excitement. Asked whether Ripple would do something specific for XRP holders if and when it goes public, he said, “Maybe. But I mean, that’s not in the immediate term.”

That is the entirety of the supposed promise: a maybe, explicitly qualified as not near-term, offered in response to a direct question, not volunteered as a plan.

The careful reading of those words reveals how conditional they are. Garlinghouse did not announce a program, describe a mechanism, or commit to any action.

He acknowledged a possibility, the way anyone might concede that something could happen without saying it will. He was explicit that it was not in the immediate term, and he attached it to an IPO that, as the next sections show, he describes as not a priority.

He also did not endorse any specific structure, declining when asked about a token buyback or another mechanism that would let holders share in Ripple’s wealth. Instead, he pointed to the indirect benefits Ripple already creates.

So the accurate summary is that Garlinghouse left a door open without walking through it. He acknowledged that a future, post-IPO benefit for XRP holders is possible while making clear it is neither planned nor imminent nor defined.

The community heard “Ripple will do something special for holders.” What Garlinghouse said was “maybe, someday, if we go public, which is not a priority.” Those are very different statements, and the difference is the whole story.

Ripple the company versus XRP the token

To understand why a holder benefit is even a question, you have to understand a distinction that confuses many people: Ripple and XRP are not the same thing, and owning one does not mean owning the other.

Ripple is a private technology company that builds payment and liquidity products, some of which use the XRP Ledger. XRP is a cryptocurrency, the native asset of the XRP Ledger, which is a decentralized, open-source blockchain that Ripple does not control.

When XRP was created, a large portion of the supply was allocated to Ripple to fund its development and promote adoption, which is why Ripple is closely associated with XRP and is in fact the largest single holder of the asset. But the association is not ownership in the corporate sense.

Holding XRP gives you a cryptocurrency, not equity in Ripple. It gives you no shares, no dividend rights, and no claim on the company’s profits or assets.

If Ripple goes public and its stock soars, that benefits Ripple’s shareholders, the holders of its equity. XRP holders are not automatically among them simply by holding the token.

This distinction is exactly why the “something special” question exists and why it is not trivially answered. Because XRP and Ripple equity are separate assets, there is no automatic, built-in mechanism by which Ripple’s corporate success, including a successful IPO, flows to XRP holders.

Any such benefit would have to be a deliberate corporate decision, a choice Ripple made to extend something to holders of a token that is legally distinct from its stock. There is no existing structure, no dividend, no buyback, and no holder-equity link that does this today.

This is what makes Garlinghouse’s maybe notable: it gestures at the possibility of Ripple voluntarily creating a link between its corporate success and XRP holders that does not currently exist and is not required to exist. The community’s hope is precisely that Ripple would choose to build such a bridge between the two separate assets.

The reality is that no such bridge exists, none is planned, and the entire question is whether Ripple might someday decide to construct one. That is a very different thing from a benefit that flows automatically.

What a holder benefit could theoretically look like

If Ripple ever did decide to do “something special,” what could it actually be? Several theoretical mechanisms have circulated, and walking through them clarifies both the possibilities and their limits.

The most discussed possibilities involve giving XRP holders some form of access to or stake in Ripple’s equity. One idea is early or preferential access to Ripple shares during an IPO, an allocation phase where verified long-term XRP holders could buy into the offering.

Another is a community-based reward structure tied to long-term XRP holding, rewarding holders who have held for a certain period. A third, more exotic idea is a tokenized representation of Ripple equity made available to eligible holders, using blockchain to give XRP holders some claim linked to Ripple stock.

Each of these would, in effect, create the bridge between Ripple equity and XRP holders that does not currently exist. It would extend a piece of the company’s success to token holders through a deliberately constructed mechanism.

These are the kinds of structures the community imagines when it hears “something special.” But they remain imagined structures, not announced ones.

The important caveat is that all of these are speculation, not plans, and each faces real practical and legal limits. Because Ripple equity and XRP are separate assets, any direct financial benefit to XRP holders would depend entirely on corporate decisions made during an IPO process that may never happen.

Such decisions carry legal, regulatory, and securities-law complications that make them far from straightforward. Linking a cryptocurrency’s holding to equity benefits raises exactly the kind of securities questions that XRP’s long legal history has been about, and Ripple would have to navigate those carefully.

Other, less direct possibilities are also floated, such as Ripple using IPO proceeds to fund ecosystem growth that indirectly benefits XRP through increased adoption and liquidity. That is closer to what Ripple already does.

The honest framing is that while several mechanisms are conceivable, ranging from share access to tokenized equity to ecosystem investment, none is announced, all face real hurdles, and the more direct and exciting versions are also the most legally complicated. The possibilities are real as possibilities. They are not, on any current evidence, plans.

Why Ripple says an IPO is not a priority

The “something special” was explicitly tied to Ripple going public, so the holder-benefit question is downstream of a prior question: will Ripple even have an IPO? And Garlinghouse has been clear that it is not a priority.

Garlinghouse stated plainly that Ripple has not prioritized going public, and he gave concrete reasons. He pointed to the recent underperformance of crypto-related public listings, citing companies whose stock has not done particularly well after going public and noting that another major exchange had reportedly delayed its own listing plans.

He also emphasized the benefits of staying private, joking that being private lets him speak freely without lawyers constraining every word. Beneath the humor was a real point about the disclosure burden and constraint that public-company status imposes.

The picture he painted was of a company that sees little reason to rush into public markets that have treated its peers poorly, and that values the flexibility of remaining private. An IPO, in his framing, is a distant possibility, not an imminent plan.

This matters enormously for the holder-benefit question, because it pushes the entire scenario further into the uncertain future. The “something special” was conditioned on Ripple going public, and Ripple going public is itself not a near-term priority.

So the holder benefit is a maybe contingent on an event that is itself a maybe. Stacking those conditionals, a possible benefit attached to a possible IPO that is explicitly not a priority and not near-term, shows how far the exciting headline is from anything concrete.

For an XRP holder, this means the “something special” should be understood as a distant, doubly conditional possibility, not as a catalyst to expect on any near horizon. Ripple may eventually go public, and if it does, it may eventually do something for holders.

But both halves of that sentence are uncertain and neither is imminent. That is a very different proposition from the one the hype implied. The IPO that the benefit depends on is not on the calendar.

The case that XRP holders already benefit

Set against the speculation about a future special benefit is Garlinghouse’s actual, stated position: that XRP holders already benefit from Ripple’s existence, indirectly but intentionally, and this argument deserves fair consideration.

Garlinghouse’s framing is that Ripple’s commercial activity is designed to benefit XRP even without any direct financial mechanism. He argues that Ripple is the most interested party in seeing XRP succeed, noting that the company remains the largest holder of XRP on the planet and therefore has the strongest economic incentive to increase the token’s value and adoption.

In his telling, Ripple’s strategy is built around making XRP the most useful, most liquid, and most trusted digital asset. Every acquisition, investment, and partnership the company pursues is evaluated partly through the lens of how it drives XRP adoption and utility.

The benefit to holders, on this view, is real but indirect. By growing the ecosystem, expanding XRP’s use in payments and settlement, and increasing its liquidity and trust, Ripple makes the XRP that holders own more valuable and more useful, which is a benefit even without any dividend or equity link.

This is where Ripple’s real-world strategy matters more than the IPO speculation. XRP’s long-term case is strongest when it is tied to actual institutional settlement, tokenization, liquidity, and demand, not to hopes of a future equity-linked reward.

This argument has genuine merit and should not be dismissed as spin. Because Ripple is the largest XRP holder, its incentives really are aligned with XRP holders in a meaningful way: Ripple profits when XRP rises, just as holders do, so the company has a built-in reason to drive the token’s value that does not require any special program.

Ripple’s actual activities, the partnerships, the payment integrations, and the institutional adoption work, do plausibly increase XRP’s utility and demand over time, which is a real if indirect benefit to anyone holding the token. That is also why XRP’s institutional catalysts matter: the strongest version of the XRP thesis comes from regulation, ETF demand, and utility aligning, not from IPO speculation alone.

The honest counterpoint is that this indirect benefit is exactly what the community finds insufficient, because it is diffuse and uncertain instead of a concrete share of Ripple’s specific corporate success. Garlinghouse’s maybe on direct benefits is precisely a response to that dissatisfaction.

But the indirect-alignment case is not nothing. It is a reasonable argument that holding XRP already ties you, loosely, to Ripple’s success through the company’s incentive to grow the token.

Whether that loose tie is enough is the debate, and it is one Garlinghouse’s comments intensified without settling.

Why the regulatory backdrop matters

The IPO question is speculative, but XRP’s regulatory backdrop is not, and it shapes why the community reacted so strongly to Garlinghouse’s remark.

XRP holders are not just hoping for a corporate reward. They are watching a year in which regulatory clarity, ETF inflows, tokenized settlement tests, and the CLARITY Act have all become part of the XRP investment story.

The CLARITY Act is especially important because it could turn XRP’s current regulatory position into a clearer statutory framework. That would matter more directly to XRP than any vague IPO benefit, because it could reduce the legal uncertainty that has constrained institutional adoption.

That does not mean the law guarantees price appreciation, and it does not mean Ripple’s IPO would automatically reward holders. But it explains why the community is primed to treat every Ripple-related signal as part of a broader XRP catalyst stack.

The problem is that not all catalysts are equal. CLARITY passage, ETF inflows, exchange-reserve changes, and real payment or settlement usage are observable market or regulatory developments.

A possible IPO reward is not. It is a speculative possibility attached to a corporate decision that has not been made.

This is why reading XRP signals carefully matters. Some signals describe actual supply, demand, usage, or regulation, while others describe hopes about what Ripple might one day decide to do.

For XRP holders, the discipline is to separate the two. The regulatory and institutional backdrop is real; the IPO reward remains hypothetical.

What it means for XRP holders

For someone holding XRP and watching this story, the practical question is what to actually make of it, and the answer is a matter of holding the possibility and its limits in proper proportion.

The realistic reading is that a direct XRP holder benefit from a Ripple IPO is a genuine possibility but a distant and unplanned one. It is contingent on an IPO that Ripple says is not a priority and structured through mechanisms that face real legal hurdles and do not currently exist.

An XRP holder should neither dismiss the idea entirely, since Garlinghouse did deliberately leave the door open and Ripple’s incentives are truly aligned with holders, nor treat it as a reason to expect a windfall. Nothing is planned, announced, or near-term, and the whole scenario depends on conditions that may not materialize.

Buying or holding XRP specifically in expectation of an IPO reward would be building on speculation about a maybe attached to a maybe, which is a weak foundation for any financial decision. The sensible stance is to regard a potential holder benefit as a possible future upside that is not to be counted on, instead of as a catalyst to position around.

The more grounded takeaway is to focus on what is actually known rather than on the speculation. What is known is that Ripple is closely tied to XRP, is the largest holder of the asset, and has strong incentives to grow its value, which provides a real if indirect benefit to holders.

What is known is that XRP and Ripple equity are separate, with no current mechanism linking the two. And what is known is that Garlinghouse acknowledged a possible future benefit while explicitly declining to plan or promise one, tied to an IPO he does not prioritize.

An XRP holder is better served evaluating the token on its actual merits: its use in payments and settlement, its regulatory position, its adoption trajectory, and institutional positioning in XRP. Those are measurable signals.

The IPO story is worth knowing, but it is a speculative possibility at the edge of the picture, not the center of any sound reason to hold XRP. That is the price reality behind the hope: bullish narratives only matter when the market can connect them to actual token demand.

None of this is investment advice; it is a frame for reading a piece of news that the community has inflated well beyond what was actually said.

A maybe, not a promise

The story that “Ripple will do something special for XRP holders when it goes public” is, on close inspection, a story about a carefully hedged maybe.

Garlinghouse, asked directly, acknowledged that a post-IPO benefit for XRP holders was possible while immediately adding that it was not in the immediate term. He declined to describe any mechanism and pointed instead to the indirect benefits Ripple already provides.

The community heard a promise. What was actually offered was a conditional acknowledgment of a possibility, attached to an IPO that Ripple says is not a priority, structured through mechanisms that do not exist and would face real legal hurdles.

The gap between those two readings is the entire substance of the story.

The grounding facts cut through the excitement. Ripple and XRP are separate assets, so no benefit flows automatically; any link would be a deliberate, unplanned corporate choice.

The IPO that a benefit depends on is itself not near-term by Ripple’s own account. And the benefit that does exist today is the indirect one Garlinghouse emphasized: Ripple, as the largest XRP holder, has genuine incentives to grow the token’s value, which loosely aligns the company’s success with holders’ even without any special program.

For an XRP holder, the honest conclusion is that a direct IPO reward is a distant possibility worth knowing about but not worth counting on. It is a maybe at the edge of the picture rather than a catalyst at its center.

The door Garlinghouse left open is real, but it is just a door left open, not a path being walked. The difference is exactly the difference between a reasonable hope and the windfall the hype imagined.

Frequently asked questions

Did Ripple promise to reward XRP holders if it goes public?

No. Ripple CEO Brad Garlinghouse, asked whether XRP holders could benefit from a Ripple IPO, said the company might do something special but immediately added that it was not in the immediate term. He did not announce a program, describe a mechanism, or commit to anything; he acknowledged a possibility in response to a direct question. The community amplified this into a promise, but what was actually said was a carefully hedged maybe, attached to an IPO Ripple says is not a priority.

Are Ripple and XRP the same thing?

No, and the distinction is crucial. Ripple is a private technology company that builds payment products, some using the XRP Ledger. XRP is a cryptocurrency, the native asset of the decentralized XRP Ledger, which Ripple does not control. Holding XRP gives you a cryptocurrency, not equity in Ripple, no shares, dividends, or claim on company profits. Ripple is the largest single holder of XRP, but that association is not ownership. That is why a holder benefit would require a deliberate corporate decision.

What could a holder benefit theoretically look like?

Several speculative mechanisms have circulated: early or preferential access to Ripple shares during an IPO allocation, a reward structure tied to long-term XRP holding, or a tokenized representation of Ripple equity for eligible holders. Ripple could also use IPO proceeds to fund ecosystem growth that indirectly benefits XRP. All of these are speculation, not plans, and the more direct versions face real legal and securities-law hurdles, since linking a cryptocurrency to equity benefits raises exactly the questions XRP’s legal history has been about.

Is Ripple going to have an IPO soon?

Not according to Garlinghouse, who said going public is not a priority for Ripple. He cited the underperformance of recent crypto-related public listings as evidence the environment is unfavorable, and emphasized the benefits of staying private. Since the something special was tied to an IPO, and the IPO itself is not near-term, the holder benefit is a possibility contingent on an event that is itself uncertain and not imminent. That pushes the whole scenario into the distant and doubly conditional future.

Do XRP holders benefit from Ripple’s success at all?

Indirectly, yes, by Garlinghouse’s argument. Ripple is the largest XRP holder, so its incentives are genuinely aligned with holders; it profits when XRP rises, just as they do. Ripple’s strategy aims to make XRP the most useful, liquid, and trusted digital asset, and its partnerships and adoption work plausibly increase XRP’s value over time. This indirect benefit is real, though the community finds it insufficient compared to a concrete share of Ripple’s corporate success, which is the dissatisfaction Garlinghouse’s maybe was responding to.

Should I hold XRP because of a possible IPO reward?

A possible IPO reward is a weak basis for a financial decision, because it is a maybe attached to a maybe: an unplanned, undefined benefit contingent on an IPO Ripple does not prioritize. It is better regarded as a distant possible upside not to be counted on than as a catalyst to position around. An XRP holder is better served evaluating the token on its actual merits, its use in payments, its regulatory position, and its adoption, than on speculation about an IPO reward that exists only as a hedged maybe. This is not investment advice.

As of June 21, 2026. Statements and corporate plans can change; this concerns speculative, unannounced possibilities. This article is information, not investment advice.

XRP traders are watching a cluster of signals that, if they play out, could set up a short-term relief rally and potentially a larger recovery attempt later in the year. Multiple technical indicators point to a market that may be nearing an oversold phase, with key levels around $1.39–$1.40 attracting attention.

As of Monday, XRP was trading near $1.13, while its longer-term trend gauges and momentum readings suggested the downside move may be losing steam—at least in the near term. At the same time, derivatives positioning data points to a potential “price magnet” effect that could pull the market toward higher liquidation zones.

Key takeaways

- XRP’s 20-week EMA is close to crossing below its 200-week EMA, a weekly “death cross” scenario that has historically been followed by mean-reversion rebounds.

- A move back toward the $1.39–$1.40 zone would align with prior post-cross behavior and could represent roughly the mid-20% upside range from around $1.13.

- CoinGlass liquidation heatmap data for XRP/USDT shows heavier short liquidation liquidity above spot, concentrated around approximately $1.37–$1.40.

- An analyst framework from Cryptollica argues XRP could be approaching conditions similar to previous washed-out phases, with long-term targets framed near $8 if a broader bottom develops.

The “mean-reversion” setup targeting $1.39–$1.40

One of the main triggers behind the bullish short-term outlook is XRP’s positioning relative to two long-horizon moving averages. According to TradingView data referenced in the report, XRP’s 20-week exponential moving average (20-week EMA) was near $1.40 and appeared on the verge of dropping below the 200-week EMA (around $1.39).

If XRP prints a confirmed weekly close below the 200-week EMA, that would mark a relatively uncommon “death cross” between the two trend indicators—an event that traders often associate with sustained weakness. However, the article argues that XRP’s past instances of 20-week/200-week EMA crosses have not led only to further declines; instead, they were followed by relief rebounds back toward the 200-week EMA.

Historically, the cited examples include a roughly 20% recovery in 2019 and a much larger 82.7% rebound in 2022 after similar cross events. Under that same mean-reversion logic, the $1.39–$1.40 band becomes the focal point, implying potential upside on the order of about 23%–25% from XRP’s referenced price near $1.13—timed, in the report’s estimate, toward July.

Momentum data adds another layer. XRP’s weekly relative strength index (RSI) was hovering just above the oversold threshold of 30 on Monday. RSI readings near 30 often indicate that selling pressure may be nearing exhaustion, which can increase the odds of a short-term rebound even if the larger trend remains under pressure.

Derivatives positioning: liquidation liquidity above spot

Beyond charts and momentum, the report also points to derivatives microstructure using CoinGlass data. Specifically, it references a Binance XRP/USDT liquidation heatmap that shows the distribution of liquidation levels above and below the current price.

In that view, there is a heavier concentration of short liquidation liquidity above spot than long liquidation liquidity below it. The largest upside cluster is reported at roughly $236.5 million located in the $1.37–$1.40 zone, according to the CoinGlass liquidation heatmap for XRP/USDT.

Liquidation heatmaps are commonly interpreted as maps of where leveraged positions may be forced to close. If XRP begins rebounding from around $1.13, shorts positioned above the market may face buyback pressure, which can create an accelerant toward nearby liquidation clusters—potentially reinforcing a push toward $1.39–$1.40.

It’s important to note the conditional nature of this mechanism: liquidation “magnets” typically work best when price action already turns upward, because liquidation levels alone do not guarantee direction. Still, the asymmetry highlighted by the heatmap suggests the market’s levered risk may be skewed toward higher prices if a bounce begins.

Longer-term framing: a potential broader bottom toward $8

The story does not stop at near-term levels. A separate long-term chart shared by analyst Cryptollica is used to argue that XRP may be entering another stage consistent with major market washouts.

Cryptollica’s framework, shared in a Sunday post on X (linked in the source), highlights XRP’s 10-day RSI hovering near the low-30s—near the range that has historically appeared around major accumulation phases. The post also makes a broader historical claim that, over “13 years,” XRP has only been this “washed out” three times.

“The first 2 times, the crowd laughed, ignored it, and only understood the setup after price had already left,” Cryptollica said in the referenced post.

In the same chart-based thesis, Cryptollica also points to XRP trading above the lower boundary of a large ascending channel. This channel is described as a support structure that has connected multiple macro lows since 2017. The lower boundary is shown near $0.75, implying the asset may still need another downside sweep before a larger recovery phase begins.

The report frames that potential sequence as: a retest of the channel support area near $0.75 first, followed by a transition into a broader bull-market phase. In that case, the channel’s upper boundary is cited as placing a long-term target near $8.

Because this portion of the narrative relies on technical pattern interpretation rather than a measurable, real-time indicator with a universally accepted trigger, the $8 target should be treated as conditional. What matters for now is the setup being claimed: oversold momentum near key thresholds and the possibility that XRP could remain supported by the channel structure—even if additional downside occurs before any large reversal.

What to watch next for XRP

Traders monitoring this thesis should focus on whether XRP can maintain an oversold bounce without losing the $1.13 area too aggressively, and whether a weekly close develops that confirms the 20-week/200-week death cross scenario. On the derivatives side, pay attention to whether price moves toward the $1.37–$1.40 liquidation cluster instead of stalling below it; and for longer-horizon investors, keep an eye on whether XRP holds above the ascending channel’s lower boundary near $0.75, since that level is positioned as the next checkpoint before any larger recovery attempt.

Bitcoin price is trading under pressure and a bad prediction, down 1.57% over 24 hours and hovering in the mid-$60K range. A hawkish Fed from last week, rising bond yields, and deteriorating chart structure are compressing the setup.

Pseudonymous analyst Doctor Profit, who correctly called BTC’s bull-market peak at $126,000 and the subsequent selloff, flagged a textbook bear flag forming on the daily timeframe. The pattern uses Bitcoin’s drop from the May high of $82,000 to sub-$60,000 as the pole, with the recent bounce to $68,000 forming the flag.

His stated target: an initial flush to the $54,000–$56,000 region, followed by sideways action and then a deeper leg toward $40,000–$50,000. That call is getting corroboration from options flow. Even last week, traders were actively buying puts with strikes down to $52,000.

#Bitcoin – What's Next? — Doctor Profit

The Big Sunday Report: All We Need to Know TA / LCA / Psychological Breakdown:

TA / LCA / Psychological Breakdown:

Everyone bullish here is making a big mistake, and don't misunderstand my words. I clearly speak about those who are buying now long term, believing the bottom was in.… pic.twitter.com/yxjGmjmVNw

(@DrProfitCrypto) June 21, 2026

(@DrProfitCrypto) June 21, 2026

The macro backdrop is not helping. Combined exchange volumes dropped 3.45% in May to $4.41 trillion, the lowest reading since September 2024. Thin volume environments are also holding any directional moves.

Discover: The Best Crypto to Diversify Your Portfolio

Bitcoin Price Prediction: $54K as the Bear Flag Breaks Down?

Bitcoin’s current technical structure is deteriorating on multiple timeframes. The immediate problem: BTC has lost the $72,000 zone that previously acted as key support. Our analyst notes that daily closes below that region keep downside risk elevated, with $54,800 identified as the next high-timeframe demand cluster, the point where structural support and the 0.618 Fibonacci retracement converge.

Below the spot, the ladder of support runs through $60,000–$58,000 (near the 200-day SMA) before reaching the $54,000 zone. This adds a wrinkle: a liquidity-grab push toward $77,000–$78,000 is possible before the flush, which would shake out short positions before resuming the downtrend. Bear flags fail, and that’s resuming the bull, and a reclaim of $78,300 on a daily close would invalidate the pattern entirely.

Given current options positioning and volume trends, there is continued pressure. On-chain models, including Willy Woo’s CVDD floor (near $45,500) and metrics like Active Price and Cointime Price cluster the probable cycle bottom between $46,000 and $54,000, which means $54K may be a floor worth defending rather than a midpoint on the way lower.

A bear flag pattern confirmation, on the other hand, triggers a measured move that cuts through $54K toward the $46,000–$50,000 range. Some bottom signals are beginning to surface, but confirmation hasn’t arrived.

Discover: The Best Token Presales

Bitcoin Hyper Targets Early Mover Upside as Bitcoin Tests Key Levels

Spot Bitcoin grinding toward a multi-month low isn’t a comfortable holding environment, especially when the measured-move math points to another 15–20% of potential downside. Rotation into early-stage infrastructure plays has historically picked up when BTC consolidates at cycle lows, with capital looking for asymmetric return profiles that spot BTC cannot offer at current valuations.

Bitcoin Hyper is positioning directly inside that thesis. The project is the first Bitcoin Layer 2 integrating the Solana Virtual Machine, delivering sub-second finality and low-cost smart contract execution on top of Bitcoin’s security model.

Hyper is addressing Bitcoin’s three structural constraints: slow transactions, high fees, and no native programmability. The presale itself has raised numbers close to $33 million at a current price of just $0.0136, with staking available at a high APY for early participants. With Hyper, a decentralized canonical bridge handles BTC transfers natively.

Review the Bitcoin Hyper presale details here.

The post Bitcoin Price Prediction: Analyst Flags $54K as Bear Flag Forms appeared first on Cryptonews.

Alan Greenspan, the longtime Federal Reserve chairman known as “the Maestro” who became one of the most influential economic policymakers of his era and famously warned of “irrational exuberance,” has died. He was 100.

The influential economist died Monday from complications of Parkinson’s Disease, said his wife of 29 years, Andrea Mitchell, the chief Washington correspondent and chief foreign affairs correspondent for NBC News.

Greenspan was appointed Fed chairman in 1987 by President Ronald Reagan and held the position — through busts and booms — until retiring in 2006. His tenure was the second longest, four months short of that of William McChesney Martin, who presided over the central bank from 1951 to 1970.

It was his unusual frankness in one televised speech, on Dec. 5, 1996, that set off a bit of market madness. Discussing the challenges of setting monetary policy, he said:

“How do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions as they have in Japan over the past decade? … We should not underestimate or become complacent about the complexity of the interactions of asset markets and the economy.”

The phrase “irrational exuberance” was interpreted as a signal that Greenspan thought the market was overvalued. The Tokyo stock market, which was open at the time, sank 3% on the comment, and other markets subsequently tumbled. However, the markets quickly recovered and continued to climb until the dot-com bust in 2001.

Years earlier, in 1974, when he was chairman of the White House Council of Economic Advisers, Greenspan had to explain on Capitol Hill why the administration wasn’t whipping inflation now, as the Ford administration dubbed its war on rising prices. In a sure-to-befuddle Greenspanism, he said: “It is a tricky problem to find the particular calibration in timing that would be appropriate to stem the acceleration in risk premiums created by falling incomes without prematurely aborting the decline in the inflation-generated risk premiums.”

“Some folks, especially money managers who shovel vast amounts of cash from one pile to another, think about Greenspan a lot,” Linton Weeks and John M. Berry wrote in The Washington Post in March 1997. “They watch his every word, mark his every move, graph his every grin. Because second to the president, Alan Greenspan is arguably the nation’s most powerful person. … With a couple of choice words he can momentarily send the stock market to heaven or hell.”

In an apparent bid to avoid rocking the markets or not showing the Fed’s hand until it was time, Greenspan would cloak his utterances in language that left the sharpest minds — including those of contentious members of Congress — scratching their heads.

“His long, convoluted sentences seem to take away at the end what they have given at the beginning as they flow to new levels of incomprehensibility,” The Washington Post’s Bob Woodward said in his 2000 biography “Maestro: Greenspan’s Fed and the American Boom.”

After his retirement from the Fed, Greenspan confessed his strategy for using perplexing language with a clear explanation.

“It’s a language of purposeful obfuscation to avoid certain questions coming up, which you know you can’t answer, and saying ‘I will not answer’ or basically ‘no comment’ is, in fact, an answer,” he said in a 2007 interview on CNBC. “So, you end up with when, say, a congressman asks you a question, and [you] don’t want to say, ‘no comment,’ or ‘I won’t answer,’ or something like that. So, I proceed with four or five sentences which get increasingly obscure. The congressman thinks I answered the question and goes on to the next one.”

Some folks, especially money managers who shovel vast amounts of cash from one pile to another, think about Greenspan a lot. They watch his every word, mark his every move, graph his every grin. Because second to the president, Alan Greenspan is arguably the nation’s most powerful person. … With a couple of choice words he can momentarily send the stock market to heaven or hell.”

Linton Weeks and John M. Berry

The Washington Post, March 1997.

Greenspan was born to Jewish parents on March 6, 1926, in New York’s Washington Heights. His father was a stockbroker and financial analyst. As a boy growing up in the 1930s during the Great Depression, the future Fed chairman received an allowance of a quarter a week.

“Twenty-five cents, I will tell you, bought a lot more then than it does these days,” Greenspan told an audience in 2003.

Greenspan played the clarinet and saxophone and briefly attended the Juilliard School. He played in Woody Herman’s jazz band (as did another future White House official, Leonard Garment), before he enrolled in New York University, earning bachelor’s and master’s degrees in economics by 1950. He eventually received his Ph.D. in 1977 — at age 51.

Among his teachers and mentors were the future Fed Chairman Arthur Burns and the free-market proponent Ayn Rand, to whom Greenspan was introduced by his first wife, the artist Joan Mitchell.

Alan Greenspan

Andrew Harrer | Bloomberg | Getty Images

By the time he received his doctorate, he had worked at Brown Brothers Harriman, the National Industrial Conference Board and the Townsend-Greenspan consulting firm, which closed after he was nominated as Fed chairman. His three-decade stint at Townsend-Greenspan was interrupted when he served as chairman of President Gerald Ford’s Council of Economic Advisers from 1974 to 1977. From 1981 to 1983, he was chairman of the National Commission on Social Security Reform.

His first job as an economist didn’t pay much more than his childhood allowance: He got $45 a week.

The first of his five terms at the Fed began just before the 1987 financial crisis. The Senate confirmed his nomination to succeed Paul Volcker on Aug. 11.

That was only 69 days before “Black Monday” crushed Wall Street on Oct. 19. The Dow Jones Industrial Average sank 508 points — 22.6% — in the session, the biggest one-day sell-off in history. The next day, Greenspan affirmed the Fed’s readiness “to serve as a source of liquidity to support the economic and financial system.” His central bank lowered short-term interest rates to encourage banks to lend on their usual terms.

The strategy helped calm the jitters and avoid a recession and banking crisis. Within two days, the Dow regained more than 50% of its Black Monday losses. The bravado also helped earn Greenspan the sobriquet “Maestro” from supporters. Years later, critics blamed the easy money policy — the “Greenspan put” he used to help calm market panics — for conditions that brought on the Great Recession.

“It’s HIS economy, stupid,” Fortune magazine declared in March 1996, throwing back at President Bill Clinton the campaign slogan he used in defeating President George H.W. Bush four years earlier. “In Greenspan We Trust,” the article’s headline said.

After that white-knuckle start, he led the Fed through two recessions, the 1997 Asian financial crisis, the 1998 Russian financial default, the 1998 bailout of the hedge fund Long-Term Capital Management, the Sept. 11, 2001, terrorist attacks, and the dot-com boom and bust of the late ’90s through 2001.

Throughout, he focused on fighting inflation over promoting full employment. His supporters say he presided over the longest economic expansion in U.S. history, but critics said Greenspan’s low interest rate policies set the stage for the housing bubble that burst into the Great Recession a year after his successor, Ben Bernanke, took the Fed helm.

“Sometimes I get criticized, and I deserve to be criticized, and that’s part of the game,” Greenspan told USA Today in 2007. “But this one, I’m innocent.”

Greenspan acknowledged that he knew about the questionable lending practices that encouraged subprime borrowers to opt for risky adjustable-rate mortgages.

“While I was aware a lot of these practices were going on, I had no notion of how significant they had become until very late,” he said in a 2007 interview with CBS’ “60 Minutes.” “I really didn’t get it until very late in 2005 and 2006.”

And in his best-selling memoir “The Age of Turbulence,” he defended the low-rate policy, which encouraged people to buy homes: “I believed then, as now, that the benefits of broadened homeownership are worth the risk. Protection of property rights, so critical to a market economy, requires a critical mass of owners to sustain political support.”

Greenspan wrote the book in longhand, mostly while soaking in a bathtub because of a back injury. In fact, most of his speeches were penned that way after he injured his back in 1971.

After he left the Fed, Greenspan opened his own consulting firm, Greenspan Associates.

Greenspan’s first marriage ended in divorce after less than a year. In 1997, he married NBC journalist Andrea Mitchell, also a Washington denizen and fellow classical music aficionado 20 years his junior, in a ceremony officiated by the late Supreme Court Justice Ruth Bader Ginsburg.

In his 2007 memoir, he praised presidents Ford and Clinton, but harshly criticized President George W. Bush for not reining in spending.

President George W. Bush (L) with Alan Greenspan (R) after Ben Bernanke was sworn in as Federal Reserve chairman, Washington, Feb. 6, 2006.

Jim Watson | AFP | Getty Images

“Little value was placed on rigorous economic policy debate or the weighing of long-term consequences,” the self-described libertarian Republican wrote. “They swapped principle for power. They ended up with neither. They deserved to lose.”

He also was critical of President Donald Trump’s first-term bashing of the Fed in an effort to get interest rates lower. Appearing on CNBC’s “Squawk on the Street” shortly after a December 2019 Trump tweet aimed at the central bank, Greenspan said: “He’s wrong in even discussing the issue. The Federal Reserve is a very professional outfit. They know more about the economy’s functioning, how it affects the money markets and the interest rate structure, far more than he does. … The best thing to do is to just disregard it. I didn’t hear this morning that the president made a statement. I’m sure it was ill-advised.”

During Trump’s second term, in January 2026, Greenspan signed a joint statement with a handful of other former Fed and Treasury officials to denounce a criminal probe of Fed Chair Jerome Powell.

“The reported criminal inquiry into Federal Reserve Chair Jay Powell is an unprecedented attempt to use prosecutorial attacks to undermine that independence,” read the statement, backed by Greenspan and more than a dozen other signatories.

Greenspan recognized the limits of the Fed’s influence. Asked during a 2008 interview on CNBC whether the central bank should be given more power to regulate investment banks, he responded:

“What I am concerned about is basically the Fed being given the role to oversee the financial stability system. I don’t think anyone can do that, and I’m most worried that were the Fed to take that job on and fail, as everyone else has and will, you cannot anticipate the future. I think it undermines the credibility of the central banking system.”

Ultimately, he realized that despite all the science involved in economics, financial risk management can’t win in meltdown situations like the Great Recession.

“Fear and euphoria are dominant forces, and fear is many multiples the size of euphoria,” he told The Associated Press after publication of his book “The Map and the Territory 2.0” in 2013. “Bubbles go up very slowly as euphoria builds. Then fear hits, and it comes down very sharply. When I started to look at that, I was sort of intellectually shocked. Contagion is the critical phenomenon which causes the thing to fall apart.”

Correction: Bob Woodward’s book on Alan Greenspan published in 2000. An earlier version misstated the year. Hedge fund Long-Term Capital Management was bailed out in 1998. An earlier version misstated the name of the firm.

Every time you trade on-chain, an invisible competition decides the order of transactions in the next block, and whoever controls that order can extract value from yours. That is MEV. It funds a hidden industry, quietly taxes ordinary users, and shapes the design of every modern blockchain.

Summary

- MEV lets block producers profit by controlling transaction order, creating opportunities such as arbitrage, liquidations, and sandwich attacks.

- Flashbots and MEV Boost transformed MEV into a structured marketplace, allowing validators to earn rewards without directly extracting value themselves.

- Private transaction routes and MEV aware trading platforms can help users reduce exposure to predatory forms of MEV and improve trade execution.

MEV, which stands for maximal extractable value, is the profit that can be captured by whoever controls the ordering of transactions within a block on a blockchain. Because the entity that builds a block can choose which transactions to include, exclude, and in what order, that power can be turned into money by slotting a profitable trade ahead of yours, squeezing a transaction between two others, or grabbing an arbitrage the moment it appears.

The term was originally “miner extractable value,” coined when miners ordered blocks, and it became “maximal extractable value” after Ethereum moved to validators, but the idea is the same: transaction ordering is valuable, and that value gets extracted. MEV is often called crypto’s invisible tax, because most users never see it even as they pay for it through worse prices and higher fees.

This guide explains MEV in plain English, with no technical background assumed. It covers what MEV actually is, why it exists at all, the main forms it takes from harmless arbitrage to predatory sandwich attacks, the hidden supply chain of searchers, builders, and validators that has grown up around it, the Flashbots infrastructure that reshaped how MEV works, the difference between MEV that helps markets and MEV that harms users, and the tools that ordinary people and protocols now use to fight back.

By the end, you will understand why MEV is a permanent feature of any public blockchain, why billions of dollars have flowed through it, and why the battle is not to eliminate it but to control who captures it and how.

What MEV actually is

At its core, MEV comes from a simple fact about blockchains: transactions do not settle the instant you send them. They wait, and someone decides the order in which they are processed, and that someone can profit from the decision.

When you submit a transaction, a swap on a decentralized exchange, a loan repayment, a token purchase, it does not go straight into the permanent record. It enters a waiting area, and eventually a block producer gathers a batch of pending transactions, arranges them in an order, and adds them to the chain as a block. Here is the key: the block producer has discretion over that order.

They can put your transaction first or last, include it or leave it out, and slip their own transactions, or transactions from others who pay them, into any position they like. Whenever the order of transactions affects how much money can be made, that potential profit is MEV, and the people who chase it design their actions specifically to win the ordering game.

The clearest way to grasp it is by analogy. In traditional stock markets, a broker who can see your large order coming and trade ahead of it is front-running, which is illegal. On a public blockchain, your pending transaction is visible to everyone, and reordering it for profit is not against any law, it is just how the system works, so the same behavior that is banned in regulated markets is an open, competitive industry on-chain.

One researcher famously called the public mempool a “dark forest,” a place where any transaction you broadcast can be hunted by predators watching for prey. MEV is the value those predators, and also some entirely useful actors, extract from the simple power to order transactions.

Why MEV exists: the mempool and ordering

To understand why MEV is unavoidable, you have to look at the waiting room where transactions sit before they are confirmed, because that is where the whole game is played.

On a chain like Ethereum, a transaction you broadcast lands first in the mempool, a public, shared pool of pending transactions that have not yet been included in a block. The mempool is visible to anyone running a node, which means that for a brief window your intended trade is public knowledge before it is final.

Specialized bots watch this pool constantly, scanning every pending transaction for opportunities, and when they spot one, they craft their own transactions designed to profit from the order in which everything will be processed. They then compete, often by bidding higher fees, to have their transactions placed in exactly the right position relative to yours.

This is why MEV is intrinsic to public blockchains rather than a bug to be patched away. As long as there is a gap between sending a transaction and finalizing it, as long as that pending transaction is visible, and as long as someone has the power to order the block, the opportunity to extract value from ordering will exist.

The mechanics differ by network: Ethereum has a public mempool that makes pending transactions visible, Solana has no mempool in the Ethereum sense and routes transactions straight to validators, and Layer 2 networks often use a single sequencer that orders transactions first come first served.

But the underlying dynamic, that whoever controls ordering can extract value, follows the structure of how blockchains reach agreement, which is why researchers describe MEV as a permanent feature of the technology rather than a temporary flaw.

The main forms of MEV

MEV is not one behavior but a family of them, and they range from useful to openly predatory. Sorting them out is the difference between fearing MEV and understanding it.

Arbitrage is the most common and the least controversial. When the same asset trades at slightly different prices on two decentralized exchanges, a bot can buy on the cheaper one and sell on the dearer one in the same block, pocketing the difference. This is MEV, but it is widely seen as neutral or even helpful, because it pushes prices on different venues back into line and makes markets more efficient.

Liquidations are similar. In lending protocols, when a borrower’s collateral falls below the required threshold, their position becomes eligible to be liquidated, and bots compete to be the one that repays the loan and claims the collateral at a discount. This too is generally seen as beneficial, because prompt liquidations keep lending protocols solvent and protect lenders. These two forms are sometimes called “good” MEV, since the extraction performs a function the system actually needs.

Then there is the predatory end. The most notorious form is the sandwich attack, where a bot spots your large pending swap, buys the asset just before you to push the price up, lets your trade execute at that worse price, and then sells immediately after for a profit, leaving you with a worse rate than you would have gotten.

Your transaction is the filling, squeezed between the bot’s buy and sell. Front-running more broadly means jumping ahead of a known transaction to profit from it, and back-running means slipping in immediately after a transaction to capture an opportunity it created.

These forms extract value directly from ordinary users, worsening their prices and inflating fees, which is why this is the MEV that earns the “invisible tax” label. The same power to order transactions enables both the helpful arbitrage that keeps markets efficient and the harmful sandwich that quietly skims from regular traders, which is exactly why MEV is so hard to simply ban.

The MEV supply chain: searchers, builders, validators

What began as lone bots has matured into a structured, multi-party industry, and knowing the roles makes the whole system legible.

At the front are searchers, the operators who run sophisticated bots scanning the mempool and the chain for profitable opportunities, arbitrage, liquidations, sandwiches, and who construct bundles of transactions designed to capture that value. Searchers are the prospectors, finding the gold.

They do not usually build blocks themselves; instead, they hand their bundles, along with a fee they are willing to pay, to builders. Builders are specialists who assemble complete, profit-maximizing blocks out of the transactions and bundles they receive, competing to construct the single most valuable block possible.

They are the ones who actually solve the ordering puzzle at scale. Finally, the assembled block goes to a validator, the participant chosen by the network to propose the next block. The validator does not need to do the complex work of finding and arranging MEV; it simply selects the most valuable block offered to it and proposes it, collecting a share of the value as reward.

This division of labor, searchers find, builders assemble, validators propose, is the modern structure of MEV, and it exists because separating these roles turned out to be more efficient and, importantly, fairer than the alternative where every validator had to extract MEV themselves. That separation is not an accident. It was deliberately engineered, and the system that engineered it is the most important piece of MEV infrastructure in existence.

Flashbots, MEV-Boost, and proposer-builder separation

The story of how MEV went from a chaotic free-for-all to an organized market is largely the story of one organization, Flashbots, and the infrastructure it built.

In the early days, MEV extraction was destructive in a way that threatened the whole network. Searchers competing for the same opportunity would wage “gas wars,” bidding transaction fees up by ten or twenty times to win the ordering race, which spiked costs for every ordinary user and clogged the chain with failed attempts.

Worse, the competition risked pushing power toward whoever could extract MEV most aggressively, threatening to centralize the network. Flashbots, a research organization, set out to defang this by moving the MEV competition off the public chain and into a private, orderly auction, so searchers could bid for transaction ordering without flooding the network with gas wars.

The centerpiece is the architecture known as proposer-builder separation, or PBS, implemented through software called MEV-Boost. PBS splits the job of proposing a block from the job of building it, exactly the searcher-builder-validator structure described above. A validator running MEV-Boost does not build its own block; it connects to a marketplace of competing builders, receives their best offers through intermediaries called relays, and simply chooses the most valuable one to propose.

This lets even a small, solo validator earn a fair share of MEV without the technical sophistication to extract it, which keeps validating accessible and the network more decentralized. Adoption has been overwhelming, with well over ninety percent of Ethereum validators running MEV-Boost, because outsourcing block construction to specialists pays better than building blocks themselves.

The tradeoff is concentration: a handful of builders and relays now route the large majority of blocks, which is its own centralization worry, and it is why the Ethereum community is working to move PBS directly into the protocol itself, an upgrade often called enshrined PBS, as a priority for 2026. Flashbots also pursued more ambitious redesigns, and while some of those research efforts were wound down, the core insight, turn MEV into a transparent, competitive market instead of a destructive scramble, has stuck.

Good MEV, bad MEV, and the invisible tax

It is tempting to treat MEV as simply theft, but the honest picture is more divided, and the division is exactly why the problem is hard.

Some MEV is genuinely useful. Arbitrage keeps prices consistent across exchanges, and liquidations keep lending markets solvent, and both of these are services the decentralized economy needs someone to perform. The searchers who do this work are, in a sense, paid for keeping the system efficient.

The amounts are not trivial: cumulative MEV across chains crossed one billion dollars by 2025, and Flashbots’ tracking found well over six hundred thousand ether of MEV extracted on Ethereum over the years it measured, a reminder that this is real money, not a theoretical edge.

But a meaningful slice of MEV is extracted directly from ordinary users at their expense, and that is the invisible tax. When a sandwich bot worsens your swap price, the difference comes straight out of your pocket, and you may never realize it happened, because the trade still went through, just at a worse rate than it should have. Multiply that across millions of transactions and the cost to regular users is substantial.

The encouraging news is that the harm is shrinking where protection has taken hold. Data from MEV researchers shows the monthly value extracted from sandwich attacks on Ethereum fell sharply through 2024 and 2025, from roughly ten million dollars a month to a fraction of that, as more transactions moved through protected routes.

The picture, then, is not “MEV is theft” but something more nuanced: MEV is the price of having open, ordered, permissionless blockchains, part of it pays for useful work, part of it is skimmed from users, and the entire industry’s effort is now bent toward shifting the balance away from the skimming.

How users and protocols fight back

You are not helpless against MEV, and one of the most useful things a guide can do is explain the practical defenses, because they have become remarkably effective.

The first line of defense is to keep your transaction out of the public mempool entirely. Private transaction services, often called private RPCs, send your transaction directly to builders instead of broadcasting it to the public pool, so the predatory bots never see it coming.

Flashbots Protect is a widely used free option that does exactly this, hiding your transaction and even returning some recovered value, and switching to it is usually a one-line change in your wallet settings; it has shielded tens of billions of dollars of trading volume across millions of accounts.

MEV Blocker, built by the team behind CoW Protocol, is another private route that goes further by running a searcher auction and paying a large share of any recovered value back to you as a rebate, and it too has protected tens of billions in volume.

A second approach is to trade on venues designed to neutralize MEV structurally. CoW Swap settles trades in batches at a single uniform clearing price, so that everyone in a batch gets the same rate regardless of ordering, which removes the front-running advantage by design, and aggregators such as UniswapX use auction mechanisms with a similar protective effect. A third, emerging idea is to flip the model entirely, with systems that capture the MEV your transaction creates and rebate it back to you, turning the invisible tax into a refund.

The networks themselves also shape your exposure. On many Layer 2 networks, a single sequencer currently orders transactions first come first served with no public mempool, which sharply reduces sandwich risk today, though it concentrates ordering power in one operator and that protection will change as those networks decentralize their sequencing. On Solana, the lack of a traditional mempool changes the dynamics, but MEV still exists through validator-level bundle systems.

The practical takeaway for a regular user is concrete: route your important trades through a private RPC like Flashbots Protect or MEV Blocker, prefer MEV-aware venues for large swaps, and you remove yourself from the dark forest for almost no effort and no cost.

A sandwich attack, step by step

The most infamous form of MEV becomes far less abstract when you watch it happen to a single trade, so follow one swap through a sandwich, because it shows exactly how the invisible tax is collected.

You want to swap ten thousand dollars of a stablecoin for a mid-sized token on a decentralized exchange. You set your trade and broadcast it, and for a brief moment it sits in the public mempool, visible to anyone watching, waiting to be included in the next block. A searcher’s bot, scanning the pool constantly, sees your pending swap and recognizes that a trade your size will push the token’s price up on that exchange’s liquidity pool. It has found its prey.

The bot acts in three moves, all landing in the same block, all arranged by the ordering it pays to control. First, the front-run: the bot buys the same token just before your transaction, nudging the price up. Second, your trade executes, but now at the higher price the bot just created, so you receive fewer tokens than you would have, paying more than the rate you saw when you clicked.

Third, the back-run: immediately after your trade pushes the price up further, the bot sells the tokens it bought a moment earlier, cashing out at the elevated price your own swap helped produce. The bot is the bread on both sides, your trade is the filling, and the profit it skimmed came directly out of your execution. You still got your tokens, the transaction succeeded, and you may never realize anything was taken, which is precisely why it is called an invisible tax.

Now notice how the defenses described earlier would have stopped it. Had you routed the swap through a private transaction service like Flashbots Protect or MEV Blocker, your trade would never have entered the public mempool, so the bot would never have seen it coming, and the sandwich would have been impossible.

Had you traded on a batch-auction venue like CoW Swap, everyone in your batch would have settled at one uniform price, removing the ordering advantage the bot relied on. One swap shows both the attack and the cure, and it explains why the simple habit of keeping important trades out of the public mempool is the single most effective thing an ordinary user can do.

Why MEV is permanent, and why that is not the end of the story

The honest conclusion is that MEV will never be fully eliminated, because the underlying source, the value of controlling transaction ordering, is woven into how blockchains reach agreement. Any system where transactions are ordered, and where that order affects who profits, will have MEV. Pretending otherwise is a fantasy, and the most serious people working on the problem say so plainly.

But permanence is not defeat, because the real question was never whether MEV exists. It is who captures it, how transparently, and at whose expense. On that question, the progress has been substantial. A destructive free-for-all of gas wars became an orderly, mostly private auction. Predatory sandwich extraction has fallen as protection spread. Solo validators can earn a fair share of MEV without being extraction experts. Ordinary users can shield their trades with a single setting, and new designs are starting to rebate MEV back to the people who generate it.

The trajectory is from opaque and extractive toward transparent and redistributive, and the protocols are working to pull the whole auction into the base layer where it can be made fairer still. MEV is the hidden machinery beneath every on-chain trade, and understanding it changes how you transact, because once you can see the dark forest, you can choose to walk around it.

Frequently Asked Questions

What is MEV in simple terms?