Crypto World

Hyperscalers Break U.S. Bond Market With $725B AI Spending Spree, Go Global for Debt

TLDR:

- Hyperscalers committed $725B in 2026 capex, up 77% from 2025’s record $410B set just a year prior.

- Non-USD bond issuance rose from zero in 2024 to 48% of hyperscaler funding by mid-2026.

- Alphabet set borrowing records in yen, CAD, CHF, and sterling within a single calendar year 2026.

- Global AI debt issuance is projected at $570B for 2026, nearly four times the 2022 total level.

Hyperscalers are reshaping global bond markets as their AI infrastructure spending reaches unprecedented levels. Amazon, Google, Microsoft, and Meta have committed $725 billion in capital expenditure for 2026 alone.

That figure is up 77% from the $410 billion record set in 2025. Goldman Sachs projects combined capex from 2026 through 2031 will reach $7.6 trillion. The scale of this spending has pushed tech giants into foreign currency debt markets at a record pace.

Non-Dollar Bond Issuance Surges Across Major Currencies

In 2024, hyperscalers issued zero bonds in non-USD currencies. By 2025, all new non-USD issuance was entirely fresh territory. Now, non-USD currencies account for 48% of hyperscaler bond funding in 2026.

The euro leads that slice at 52%, followed by the Japanese yen at 15%, the Canadian dollar at 14%, sterling at 12%, and the Swiss franc at 7%.

Bank of America confirmed that hyperscalers have doubled their non-dollar bond share to 30% of total issuance this year. As noted by Milk Road AI, this shift has moved so fast it has strained the American bond market’s capacity to absorb it. The U.S. market simply cannot accommodate the full volume of debt these companies now need to raise.

Individual deals reflect how quickly this trend has accelerated. In May, Alphabet issued ¥576.5 billion, roughly $3.6 billion, in yen-denominated bonds. That was the largest yen bond ever sold by a non-Japanese company, topping Berkshire Hathaway’s 2019 record.

Alphabet has now set borrowing records in yen, Canadian dollars, Swiss francs, and sterling within a single calendar year. That is a level of multi-currency debt activity rarely seen from any single corporate issuer at this pace.

AI Debt Issuance on Track to Quadruple 2022 Levels

Amazon entered Canada’s bond market in June with a C$14 billion issuance, the largest corporate bond ever sold in that market.

Investor orders reached nearly C$28 billion, almost double what was ultimately sold. That deal surpassed Alphabet’s own Canadian record of C$8.5 billion set just weeks earlier in May.

Morgan Stanley projects euro borrowing by hyperscalers will hit €50 billion in 2026. That would potentially make the United States the single largest source of corporate debt in the entire eurozone, ahead of France. The shift carries broad consequences for European fixed-income markets.

Global AI-related debt issuance is on track to reach $570 billion for the full year 2026, according to Morgan Stanley. That is more than double the pace recorded during the same period last year. It is also nearly four times the 2022 level.

Even companies holding over a trillion dollars in combined cash, including Apple, Microsoft, Alphabet, Amazon, and Meta, have concluded that self-funding this buildout is not feasible.

The AI infrastructure race has grown too capital-intensive for even the world’s most cash-rich firms to finance independently.

BitGo is expanding its custody and compliance infrastructure into Europe with a new “crypto-as-a-service” offering designed to align with the European Union’s Markets in Crypto-Assets Regulation (MiCA). The move arrives as exchanges and other regulated crypto firms prepare for a key transition point: the EU-wide requirement for authorization to continue serving customers across member states.

BitGo Europe launched the platform with the explicit aim of supporting MiCA readiness for partners that need to meet regulatory obligations for custody, trading connectivity, onboarding and wallet-related functions. According to Cointelegraph, the company is positioning its regulated setup as a way for service providers to reduce the time required to operationalize compliance measures during the licensing transition.

Key takeaways

- BitGo Europe has launched a MiCA-oriented crypto-as-a-service platform aimed at exchanges and fintech firms.

- The platform is designed to connect partners to regulated custody, trading, onboarding and wallet systems via APIs, while keeping customer-facing control with the partner.

- Compliance tooling referenced by BitGo includes programmatic KYC checks, transaction controls and settlement of supported digital assets.

- BitGo’s expansion builds on prior regulatory authorization: BaFin granted BitGo a MiCA-related license in May 2025.

- Regulatory uncertainty remains across the EU as firms seek MiCA authorizations ahead of the July 1 deadline.

BitGo Europe launches MiCA-focused crypto-as-a-service

BitGo Europe’s new platform is intended to help other crypto businesses meet MiCA requirements through a modular integration model. In its announcement shared with Cointelegraph, the company said partners can use BitGo’s infrastructure for core regulated functions instead of building all compliance and custody capabilities internally.

From an operational standpoint, the approach matters because MiCA compliance is not limited to one-off licensing paperwork. It requires firms to have ongoing systems in place that can support customer onboarding, risk controls, and transaction processing consistent with the regulation’s standards. BitGo’s service model—using application programming interfaces (APIs) to connect services—targets the practical challenge of standing up compliant workflows quickly across multiple EU jurisdictions.

BitGo stated that the service is especially relevant for companies seeking to maintain service continuity while regulatory decisions and authorization timelines evolve. In comments shared publicly by CEO Mike Belshe, he argued that regulated infrastructure can help firms keep operations moving safely and compliantly during licensing delays.

What the platform covers: custody, onboarding, controls and SEPA payments

BitGo’s MiCA-focused offering is built around connectivity to regulated custody and related functions. The company said exchanges and fintech platforms can integrate with BitGo systems for custody, trading integration, onboarding processes and wallet operations.

The service includes features intended to support compliance and operational risk management, such as programmatic KYC checks, transaction controls and settlement of supported digital assets. These capabilities are central to meeting MiCA’s expectations for regulated crypto-asset activity, where firms must demonstrate they can manage customer onboarding and transaction handling in a controlled and auditable manner.

BitGo also referenced support for euro payments through SEPA rails in eligible regions. For institutions and payment operators, the inclusion of fiat connectivity can be a significant part of operational compliance: regulated on- and off-ramp design typically intersects with AML/KYC procedures, transaction monitoring and other controls expected by regulators.

Regulatory pressure ahead of the July 1 MiCA deadline

The launch comes as EU crypto regulation transitions from fragmented national approaches toward a unified framework under MiCA. Under MiCA’s timetable, July 1 is a critical date for authorization requirements governing entities that continue offering crypto-asset services in the EU.

Recent reporting highlighted the possibility that some major exchanges may face difficulties securing authorizations in time. While BitGo did not provide details on whether its infrastructure would allow specific platforms to continue serving EU users if an authorization application is rejected, the broader compliance timing risk is evident: market participants need clarity on regulatory status, and delays can create operational and legal exposure.

Cointelegraph reported that Greek regulators may reject Binance’s MiCA license application, underscoring uncertainty surrounding the licensing pipeline for large venues. For institutions monitoring market structure, these outcomes are material not just from a business perspective, but because they affect where and how regulated service providers can legally operate across borders.

Beyond authorization decisions, MiCA-related implementation also interacts with national transition rules. BitGo pointed to markets where legacy registration regimes are being phased out as the EU-wide framework takes effect. In Lithuania, the transition period for legacy virtual asset service providers ended on Dec. 31, 2025. In Poland, implementation remains unsettled, leaving some companies navigating unclear timelines for how national approvals will map into the new EU system.

Institutional and compliance implications for crypto firms

BitGo’s move reflects a broader trend in European crypto markets: regulated infrastructure providers are increasingly central to how exchanges and fintechs build compliance capabilities. For compliance teams, outsourcing or integrating certain regulated functions can affect the internal control framework, including who is responsible for customer due diligence workflows, how transaction monitoring is performed, what audit trails exist, and how regulatory obligations are allocated across the service chain.

MiCA also creates supervisory expectations around governance, operational resilience and risk controls. While BitGo’s model is designed to enable partners to meet the MiCA standard, regulated counterparties will still need to perform their own due diligence on vendor controls and ensure that contractual and operational arrangements support ongoing compliance. This includes verifying how KYC checks are executed, how transaction controls are enforced, and how fiat-related processes interface with AML/KYC requirements.

From a historical and regulatory context, BitGo’s European expansion is not starting from zero. The company previously obtained authorization under the MiCA framework, with BaFin issuing a license in May 2025. That detail is important for institutional readers because it indicates the company is operating under an EU supervisory authorization rather than operating purely as an offshore service. In turn, this can reduce—but not eliminate—regulatory uncertainty for partners seeking integrations that align with EU oversight.

However, unresolved questions remain across the sector. Licensing decisions for major firms can change quickly, and the legal landscape will continue to evolve through regulator guidance, enforcement actions and court-related developments where applicable. Partners evaluating integrations will need to track not only the vendor’s authorization status but also the regulatory expectations for their own licensed activities.

What to watch next

BitGo Europe’s launch will likely be tested by how exchanges and fintech providers operationalize MiCA compliance under real-world timelines and regulatory outcomes across member states. Market participants and compliance teams should monitor MiCA authorization decisions, evolving national implementation details, and how regulators interpret responsibility for customer onboarding and transaction controls within multi-party infrastructure models.

BitGo says it has launched “crypto-as-a-service” in Europe, positioning the firm’s regulated custody and compliance infrastructure as a practical bridge for exchanges and fintech companies rushing to meet the EU’s Markets in Crypto-Assets Regulation (MiCA). The move comes as the July 1 MiCA authorization deadline approaches and uncertainty grows around how certain large platforms will handle licensing in individual member states.

According to a statement shared with Cointelegraph, BitGo Europe’s platform is designed to help service providers connect core functions—custody, trading support, onboarding and wallet capabilities—through APIs, rather than building an entire compliance stack from scratch. The company framed the launch as a way to keep businesses operating “safely and compliantly” during regulatory transitions, with BitGo CEO Mike Belshe arguing that regulated infrastructure can reduce downtime when licenses are delayed.

Key takeaways

- BitGo Europe launched a MiCA-oriented crypto-as-a-service platform aimed at exchanges and fintech firms that need regulated infrastructure.

- The service is presented as an API-based way to integrate regulated custody, programmatic KYC checks, transaction controls, and settlement.

- BitGo’s EU approach is tied to MiCA readiness ahead of the EU-wide July 1 authorization deadline.

- The firm says the need is acute in markets such as Poland and Lithuania, where legacy registration pathways are being phased out.

- BitGo did not clarify whether its infrastructure would allow specific exchanges to continue operating in the EU if a license application is rejected.

MiCA deadline pressure reshapes the EU custody race

MiCA sets a common authorization standard across the European Union for crypto-asset firms that wish to continue serving customers. The July 1 deadline is particularly significant for platforms that have not yet secured the required authorization to operate under the new regime.

Recent reporting highlighted the potential for uneven outcomes as regulators decide on major firms’ applications. Earlier coverage from Cointelegraph noted that Greek regulators may reject Binance’s MiCA license application, raising questions about how the largest exchange by trading volume might adjust its EU footprint if authorization does not go through.

In that environment, BitGo’s pitch is aimed at reducing friction for businesses that must comply with MiCA while continuing to offer products during the transition. While BitGo did not explicitly state how its platform would work in the event of a rejected license for a specific exchange, the emphasis on “keeping you moving” suggests an intent to support continuity where regulatory readiness is still in progress.

What BitGo Europe’s “crypto-as-a-service” includes

BitGo Europe said the product is built for integration-heavy use cases. Rather than asking partners to replace their customer-facing systems, the platform is designed to let exchanges and fintech companies plug into BitGo’s services via APIs.

BitGo’s Europe push reportedly builds on earlier groundwork: the firm obtained authorization under the relevant framework more than a year ago, and Germany’s Federal Financial Supervisory Authority (BaFin) issued the license in May 2025. With that license as a foundation, BitGo is now marketing an operational suite intended to reduce the time and cost involved in reaching MiCA-aligned operations.

Among the components BitGo describes are:

- Programmatic KYC checks that can be executed through the platform.

- Transaction controls intended to enforce rules around activity.

- Settlement support for supported digital assets.

- Euro payments via SEPA rails in eligible regions, aimed at connecting fiat on- and off-ramps to a regulated operating setup.

For exchanges and intermediaries, the practical value of this approach is that regulatory capabilities—particularly custody and compliance workflow—can be sourced from a licensed infrastructure provider. The model also potentially shifts the compliance burden away from each partner building bespoke controls, while still allowing the partner to keep direct ownership of its customer-facing products.

Regional transition gaps in Poland and Lithuania

BitGo’s statement also emphasized that MiCA transition pressures vary by country. The firm highlighted markets including Poland and Lithuania, where older national registration regimes are being phased out as the EU-wide system takes effect.

In Lithuania, BitGo points to the end of a transition period for legacy virtual asset service providers on Dec. 31, 2025. In Poland, it says implementation remains unresolved, leaving some firms in a state of uncertainty regarding which approvals they can rely on as the MiCA framework rolls forward.

This matters for operators because the compliance timeline is not uniform across jurisdictions. Even when MiCA is the overarching EU structure, companies often face a multi-layer regulatory reality—national requirements, transition rules, and regulator-by-regulator outcomes—that can affect product availability, onboarding, and the ability to process fiat rails.

BitGo CEO Mike Belshe argued that Europe is moving toward a more unified and durable regulatory framework for digital assets. In his view, MiCA readiness is not only about obtaining authorization but also about having systems that can continue functioning during licensing delays. He said the company was built for such moments and positioned BitGo Europe as a route for businesses to meet the MiCA standard while continuing to serve the market.

Open questions: continuity, licensing outcomes, and partner readiness

While BitGo’s launch is clearly aimed at helping partners operationalize MiCA compliance, important uncertainties remain. The company did not confirm whether its infrastructure would specifically allow an exchange to continue operating if a MiCA license application is ultimately rejected. Cointelegraph attempted to request clarification but did not receive a response by publication time.

For the market, the bigger takeaway is that regulated custody and compliance tooling are becoming a competitive differentiator as the EU transition tightens. Investors and industry participants will likely watch how quickly exchanges and fintech providers are able to integrate licensed infrastructure, and whether regulator decisions—such as those affecting major firms’ applications—drive further consolidation in compliance services.

With MiCA authorization decisions approaching, the next phase will hinge on how effectively exchanges and service providers can translate “license readiness” into real operational continuity—especially in countries where legacy pathways have already ended or remain unresolved.

Pre-IPO perpetual futures volume on crypto exchanges reached roughly $12 billion in June, a 6,000-fold jump from March.

The notable growth came as traders chased exposure to technology giants.

Pre-IPO Perpetuals Now Drive 55% of Crypto Equity Trades

Pre-IPO perpetual futures let traders speculate on private companies before their shares reach public markets. The contracts track expected valuations without the ownership of shares.

Volume in these products climbed from $2 million in March to $715 million in May, according to CryptoQuant data. June then pushed the figure to about $12 billion.

Pre-IPO products form part of a wider push to trade traditional assets on crypto rails. Exchanges have added oil, metals, and equity perpetuals.

Consequently, pre-IPO contracts accounted for 55% of all perpetual equity trading on crypto exchanges in June. That share stood at just 5% in May.

“This growth coincides with increased market interest in Pre-IPO perpetuals including SpaceX, OpenAI and Quantinuum, as well as the launch of additional equities offerings on crypto platforms,” the report read.

Follow us on X to get the latest news as it happens

Binance Captures 83% of Pre-IPO Perpetuals Market in June Boom

Meanwhile, CryptoQuant data shows Binance leading the segment by a wide margin. The exchange recorded $10.3 billion in pre-IPO perpetual volume in June. That figure marks a 20-fold increase over its May total.

Binance now holds an 83% share of all pre-IPO perpetual trading. Bitget trails in second place with $1.3 billion in June volume.

Notably, several private companies have gone public in June. Quantinuum listed on Nasdaq under the ticker QNT on June 4. SpaceX followed on June 12, trading under the ticker SPCX. OpenAI has not set an IPO date. However, the company filed a confidential S-1 with the SEC.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Pre-IPO Perpetual Trading Grows 6,000x Since March on Tech Bets appeared first on BeInCrypto.

Bitcoin (BTC) fell below $65,000 on Wednesday as traders predicted the impact of a key macro event.

Key points:

- Bitcoin approaches the next Fed interest-rate decision near important support.

- BTC price analysis warns that “bearish” moves typically accompany FOMC days.

- $55,000 remains on the table as a target next.

BTC price analysis: FOMC could “set the tone” for June

Data from TradingView showed intraday lows of $64,782 on Bitstamp.

BTC/USD one-hour chart. Source: Cointelegraph/TradingView

The US Federal Reserve was due to decide on changes to interest rates at 2pm Eastern time — a move that formed the week’s main volatility catalyst.

The meeting of the Federal Open Market Committee (FOMC) would be the first under new Fed chair, Kevin Warsh, making his remarks at the subsequent press conference just as important as the overall outcome.

As Cointelegraph reported, Warsh had been under pressure to cut rates despite the inflationary impact of the US-Iran war.

“FOMC could set the tone for the rest of the month,” trader Killa wrote in an X post on the topic.

Killa noted that BTC price action tended to weaken around Fed decisions.

“Right now, BTC is forming a bullish narrative into the event, but as I always say, the outcome is usually priced in before the news is released,” they continued.

“If recent history is any indication, we have generated far more bearish reactions than bullish ones.”

BTC/USD chart with FOMC meetings marked. Source: Killa/X

On Tuesday, Bitcoin already experienced a loss of momentum, even as stocks headed higher on Iran relief. Analysis had already warned that price would likely stall above $67,000 as demand remained subdued.

“We need to maintain bullish market structure from here… (64K). If not, there’s a strong chance we revisit the $60K lows after this pivot,” Killa warned.

Bitcoin trader preserves $55,000 target

Other perspectives included a “short-term bounce” for Bitcoin before the resumption of the bear market.

Related: Bitcoin miner ‘capitulation’ comes as trader sees later 2026 bear-market bottom

“FOMC meeting is happening today, exactly when the US-Iran peace deal is very close,” Niels, cofounder of marketing agency STABL, told X followers.

“IMO, Bitcoin could show some strength but eventually it’s going to $55,000.”

BTC/USDT one-day chart. Source: Niels/X

A more optimistic take came from analytics account Cryptic Trades, which saw the rebound continuing after the FOMC.

BTC/USD, it said, had rejected at two key moving averages that together form Bitcoin’s daily bull market support band.

BTC/USD one-day chart with bull market support band. Source: Cointelegraph/TradingView

“However, after this pullback, the next big leg up is coming,” Cryptic Trades predicted.

BTC/USD one-day chart. Source: Cryptic Trades/X

Cathie Wood bought $529.7 million of SpaceX stock on its first day of trading and sold Tesla shares at the same time. Both companies belong to Elon Musk, but Wood’s conviction has clearly shifted.

The trades came on June 12, SpaceX’s IPO day, when shares surged 19% and Musk’s net worth crossed $1 trillion for the first time. ARK bought 3.29 million SpaceX shares at the IPO price of $135, a position worth $529.7 million at closing. ARK then trimmed Tesla alongside Advanced Micro Devices, Rocket Lab, Roku, and Baidu on the same day.

Why Wood Is Moving On From Tesla

Tesla has been one of ARK’s core holdings for years, and Wood has publicly defended it through multiple down cycles. But the EV maker faces a different landscape today: Chinese rivals have narrowed the gap, margins are under pressure, and Musk’s political visibility has become a liability for some buyers.

SpaceX is a different proposition. Its Starlink satellite internet division is the company’s only profitable business, and it is growing fast. Wood first bought SpaceX in late 2023, and the stake became the largest holding in ARK’s roughly $1 billion internal venture fund. The IPO gave ARK the chance to scale that conviction in public markets.

The SpaceX Trade and Its Risks

The $529.7 million buy is a large commitment, even by ARK’s standards. SpaceX priced its IPO at $135 and closed 19% higher on day one.

SpaceX carries an accumulated deficit of $41.3 billion as of March 31. And the IPO’s retail allocation sits at 30% of the offering, three to six times the typical level.

ARK’s Performance Context

The ARK Innovation ETF is up 1.61% year to date, while the S&P 500 has gained around 9%. Over the past 12 months, the fund recorded roughly $294 million in net outflows. A Morningstar analysis found the fund wiped out $7 billion in investor wealth from 2014 to 2024.

Wood’s IPO bets follow a pattern. ARK bought Coinbase after its 2021 listing and CoreWeave more recently, each time seeking early exposure to high-conviction names. SpaceX is the biggest version of that bet yet.

Whether SpaceX turns that deficit into durable profit, or this becomes ARK’s next painful lesson, is a question the market will spend years answering.

The post Cathie Wood Swaps Tesla for SpaceX in $529M Elon Musk Pivot appeared first on BeInCrypto.

The Fixed Range Volume Profile (FRVP) is a technical analysis tool that allows traders to spot where trading volume has concentrated within a chosen price range. It shows the trading volume traded at each price level. Traders read these levels to gauge market participation and to locate potential support and resistance levels. Higher-volume prices tend to mark stronger areas of interest.

The Fixed Range Volume Profile (FRVP) is a popular tool among traders as it provides a wide range of signals. However, its complex appearance can put some traders off. In this article, we’ll take a deep dive into the FRVP, how to use it in a trading strategy, and some common mistakes to avoid.

What Is Fixed Range Volume Profile (FRVP)?

The Fixed Range Volume Profile (FRVP) is an advanced tool that plays an important role in assessing market activity. It provides a comprehensive view of the market by shedding light on trading volume and price data over a specific period. Unlike traditional price-based indicators, the FRVP incorporates volume data, offering a deeper insight into market liquidity and supply and demand dynamics.

Most chart indicators measure market activity against time. The FRVP measures it against price instead. It groups the volume traded at each price level inside a fixed range. This shows where buyers and sellers were most active. Compared with other volume indicators that plot volume bar by bar, the FRVP reveals which prices mattered, not which moments. This makes imbalances between supply and demand more straightforward. A price with heavy volume saw strong participation. A price with light volume saw little.

The FRVP presents a distribution of trading activity, represented by horizontal bars at various price levels, typically from one key swing point to another (e.g. a swing high to a swing low). It shows areas of high and low activity and may help traders spot areas where the market has spent considerable time and where it traded through easily.

Traders anchor the FRVP between two swing points because that range captures one complete move. The profile then reflects only the volume traded during that leg. This keeps the analysis focused, rather than spread across the whole chart. Many traders bracket a trend leg, a range, or a sharp news-driven move. The result is a clearer read of where value built up inside that move.

How Fixed Range Volume Profile Works

So how does the Fixed Range Volume Profile work? The FVRP indicator measures volume at price across a range you define. You pick a start point and an end point on the chart. The indicator then adds up the volume traded at each price level and stacks the totals sideways. The longer the horizontal bar, the more volume changed hands at that price.

In trading, volume measures the total units traded over a given period. It signals how much interest sits behind a price move. High volume points to strong participation and an active market. Low volume points to weaker interest and a more passive one. The Fixed Range Volume Profile indicator takes that idea and ties it to price, not the clock.

This is where volume profile trading differs from standard volume bars. A tall bar shows a price where the market was active. This reflects acceptance, a core idea in auction market theory and price discovery. A short bar shows a price the market passed through fast. Acceptance builds value. Rejection moves price on. Reading the two together shows where business was actually done.

The calculation runs in four steps:

- Select the range. You mark a start and end point, usually a swing high to a swing low.

- Split the range into rows. The tool divides the price range into thin horizontal bands.

- Allocate the volume. It assigns the volume from each bar to the price rows it covers.

- Plot the profile. It draws the totals as a sideways histogram showing volume by price.

The result locks to the move you chose. Scrolling or zooming the chart does not change it.

Components of FRVP

The Fixed Range Volume Profile can be broken down into several key components. Each one marks a different type of price behaviour inside your selected range. Read together, they show where the market built value and where it moved on. These definitions follow standard volume profile methodology used across charting platforms.

Point of Control (POC)

The Point of Control (POC) is the price level with the highest traded volume within the selected range. The POC can be considered as the price level where the market found the most acceptance and is usually plotted as a red line. It is often the most watched level in the whole profile. Traders treat the POC as a balance point. Price tends to return to it over time. That makes the POC a level where support or resistance can form.

Value Area

The Value Area represents the price range where a specified percentage of total volume has occurred, typically 70%. It demonstrates the levels at which most trading activity has transpired. The upper boundary is the Value Area High (VAH). The lower boundary is the Value Area Low (VAL). Traders treat the VAH and VAL as the boundaries of fair value. Price inside the Value Area points to balance. A move beyond either edge can signal the market is seeking new value. Both edges often draw reactions when price tests them.

High Volume Nodes (HVN)

A High Volume Node (HVN) represents a peak in volume at a price level. It marks a price the market accepted and traded heavily. HVNs often act as strong support and resistance, as price tends to slow around them. Several HVNs can sit close together to form a wider zone of interest.

Low Volume Nodes (LVN)

A Low Volume Node (LVN) represents a trough in volume at a price level. It marks a price the market rejected and moved through quickly. Price tends to travel fast across LVNs toward the next HVN. These thin zones often highlight potential breakpoints in a move.

Both nodes play key roles in volume profile analysis. With the POC, they give traders reference points for reading market structure.

FRVP Applications in Market Analysis

Now that we’ve answered, ‘What is the Fixed Range Volume Profile?’, let’s take a look at three ways to incorporate the indicator into a strategy. The tool is rarely used on its own. A sound Fixed Range Volume Profile strategy combines it with price action and risk management. The profile shows where volume sits. Price action confirms how the market reacts there.

If you’d like to see how it works for yourself, you can consider heading over to FXOpen’s TickTrader platform and test the Fixed Range Volume Profile.

Identifying Trend Continuation with FRVP

One of the most common applications of the Fixed Range Volume Profile is its use in gauging market trends. The interaction of price with high and low-volume areas can give valuable insights into market sentiment.

When analysing market trends using the FRVP, traders first pay close attention to areas of low volume, or LVNs. These areas, characterised by limited trading activity, often suggest an imbalance between supply and demand where the market moved rapidly. As such, they create a price gap or vacuum in the profile.

In the markets, these low-volume gaps are likely to be filled over time. An asset’s price usually tends to move quickly through these areas in search of the next area of value, represented by HVNs. As such, LVNs can act as powerful directional indicators, pointing to the potential for swift price movements, either upward or downward, to reach the next HVN, where market acceptance is greater.

This is the core of HVN and LVN trading: price tends to travel from one value area to the next. It moves fast through thin LVN zones and slows at dense HVN ones. In a bullish case, price clears an LVN and runs up toward a higher HVN. In a bearish case, it drops through an LVN toward a lower HVN. Traders watching for trend continuation often note a few things:

- Where the nearest LVN sits relative to current price

- Which HVN is the likely target once the LVN is crossed

- Whether the wider trend agrees with that direction

- How price behaves on the first test of the HVN

HVNs and LVNs as Support and Resistance Zones

The FRVP can be an invaluable tool in identifying support and resistance levels. HVNs often indicate levels of strong support or resistance as they reflect periods where a significant amount of trading has occurred. These are areas where the market has shown acceptance, often making them difficult to breach.

Conversely, LVNs, with their relatively lower trading activity, often highlight potential breakpoints. Because these are levels at which the market has shown rejection. They are less likely to act as strong support or resistance areas, and the price is more likely to pass through them more quickly.

The split comes down to acceptance versus rejection. Where the market accepted price, volume built up and a zone holds. Where it rejected price, volume stayed thin and the zone gives way. Using the Fixed Range Volume Profile for support and resistance rests on reading that difference. The table below summarises how the two nodes tend to behave.

Therefore, traders can use HVNs and LVNs as a basis to establish potential entry and exit points in their trading strategies. For example, a trader may consider entering a long position when the price breaks above an HVN (an area of resistance). Similarly, an LVN above the current price might be a good target for this long trade, as the price could rise quickly to this level.

Point of Control (POC) in Market Analysis

In addition to HVNs and LVNs, the Point of Control (POC) is another widely used element within the Fixed Range Volume Profile. Price often revisits the POC because it marks the range’s balance point. It is where the most business was done, so the market treats it as fair value.

In an upward-trending market, the POC often acts as a support level, where buyers may enter or add to long positions, expecting the price to bounce back upwards. Conversely, in a downward-trending market, the POC can serve as a resistance level, where sellers might consider short positions, anticipating market rejection.

In a broader Fixed Range Volume Profile strategy, traders often look at:

- Whether price stalls or pushes straight through the POC

- How volume behaves as price returns to the level

- Where the POC sits against the wider price action

Fixed Range Volume Profile vs Session Volume Profile vs Visible Range

The Fixed Range Volume Profile is one of three common volume profile types. The other two are the Session Volume Profile and the Visible Range Volume Profile (VRVP). All three plot volumes by price. They differ in how the range is set.

The Fixed Range Volume Profile vs Session Profile vs Visible Range Volume Profile question comes down to control. With FRVP, you pick the start and end points by hand. The profile then stays locked to that move. The Session Volume Profile sets its own range. It resets automatically at the open of each trading session. The Visible Range Volume Profile uses whatever bars are on screen. It redraws as you scroll or zoom.

Traders pick the tool to match the question. FRVP is used for a completed move traders want to study closely. The Session Volume Profile is popular for intraday work, where each day’s value matters. The Visible Range Volume Profile is applied for a fast read of the wider chart. Many traders run more than one together. A fixed range over a key leg, paired with the current session, can give context that neither offers alone.

Selecting the Range for FRVP Analysis

The range you choose shapes everything the FRVP shows you. The same chart can produce different profiles depending on where you start and finish. So the choice of range is the important decision when using the tool. A well-chosen range captures one clean phase of market activity. A poorly chosen one mixes unrelated moves and blurs the read.

Most traders anchor the profile between two clear points. A swing high to a swing low is the common choice, as it brackets a single move. This ties the profile to a defined piece of market structure rather than an arbitrary stretch of chart.

Several range types tend to suit the tool:

- Trend legs: a single push from one swing point to the next, to see where volume built during the move.

- Consolidations: a sideways range or period of consolidation, to find the levels the market kept returning to.

- News-driven moves: a sharp reaction to an event, to map where volume settled once the move calmed.

- Swing ranges: a full swing from high to low, often used alongside a swing trading approach.

Because the output depends on the input, two traders can read the same chart differently. One brackets the whole trend. Another brackets only the latest leg. Both profiles are valid, but they answer different questions. Many traders test a few ranges over the same area. They look for levels that hold up across more than one selection, since those tend to carry more weight.

FRVP Example: Analysing a Market Range

In this example, we see the market cooling off after a prolonged uptrend to the left (finishing just on the edge of the chart). The price fell sharply, finding a bottom. Given the distinct high and low points, the FRVP tool is set to those two points. The walkthrough below breaks the move into five steps.

- Set the range. With clear high and low points in place, the profile is anchored from the swing high to the swing low. This brackets the full move for analysis.

- Read the POC. The first area to notice is the POC, which acted as strong resistance within the multi-day range. Traders could have anticipated this area to hold, using other forms of technical analysis to find entries on a lower timeframe.

- Mark the LVN target. The POC area was eventually pierced through, indicating that it may be time for the price to come and meet the LVN toward the top of the range. This level represented the area with the lowest volume in the entire range. Combined with the prior bullishness offscreen, traders could have been confident that the price would at least reach this area, acting as a solid target if they had bought earlier near the POC.

- Watch the HVN reaction. However, it moved higher to tap the HVN (blue line). Notice that it’s the area with the highest volume besides the POC. After reaching the HVN, the price quickly reversed.

- Confirm the turn. Similar to the POC, traders could have anticipated bearishness from this area. The shooting star pattern here acted as confirmation.

Common FRVP Mistakes

So what are the common mistakes many traders make when using the Fixed Range Volume Profile indicator? The list below covers the ones that catch traders out most often.

- Misreading volume nodes: Traders may assume all HVNs or LVNs carry equal weight. Their importance shifts with the broader market context, so strong bullishness can see an HVN traded straight through.

- Ignoring other indicators: Relying on the FRVP alone makes for a one-dimensional approach. A sound strategy pairs it with tools that confirm reversals, like the Relative Strength Index (RSI) or MACD.

- Over-relying on historical data: The FRVP maps past activity, not future moves. Fundamental drivers still matter and belong in the analysis.

- Selecting the wrong range: A poorly chosen range mixes unrelated moves and distorts the profile. The levels it produces then carry little meaning.

- Ignoring higher timeframes: A profile read in isolation can clash with the wider trend. Checking a higher timeframe gives needed context.

- Treating nodes as exact prices: HVNs and LVNs mark zones, not precise lines. Expecting prices to turn at a single level often disappoints.

- Skipping risk management: Using the FRVP without risk management leaves a strategy exposed when a level fails to hold.

Advantages and Limitations of FRVP

Like any tool, the FRVP indicator has clear strengths and real limits. Knowing both may help traders use it in the right place. It reads volume well, but it does not act as a standalone system.

On the plus side, the volume profile indicator shows where genuine activity occurred, not just when. It ties volume directly to price, which standard volume bars cannot do. It also locks to a chosen move, so the analysis stays focused. That makes it useful for marking support, resistance and likely target zones.

The limits matter just as much. The FRVP reflects past activity, so it offers no guarantee about future moves. Its output depends entirely on the range you select, which adds a layer of judgement. On forex charts, the volume shown is often tick volume rather than true traded volume. And the tool is always combined with other forms of analysis.

Key Takeaways

The Fixed Range Volume Profile may help traders analyse where trading activity was concentrated within a selected price range. By highlighting key areas such as the Point of Control, Value Area, High Volume Nodes, and Low Volume Nodes, it provides additional context on where the market found acceptance or rejection.

Like any technical tool, the FRVP is commonly used alongside price action analysis, market structure, and risk management. Since the profile’s output depends heavily on the range selected, traders typically take care to choose ranges that reflect meaningful market swings or trading sessions.

With an understanding of how to use the FRVP indicator, you might consider opening a trading account with FXOpen to access over 700 markets across forex and CFDs.

FAQ

What Is Fixed Range Volume Profile (FRVP)?

Fixed Range Volume Profile (FRVP) is a volume analysis tool that displays how much trading activity occurred at different price levels within a user-defined range. Instead of focusing on volume over time, it organises volume by price, which may help traders identify areas where the market spent the most and least effort transacting.

What Does the Point of Control Mean in FRVP?

The Point of Control (POC) is the price level that recorded the highest trading volume within the selected range. Traders often monitor the POC because it can represent a key area of market acceptance, where buyers and sellers were most active, and where price may later find support, resistance, or balance.

What Are HVNs and LVNs?

High Volume Nodes (HVNs) are price levels where a large amount of trading occurred, often indicating areas of market acceptance and potential support or resistance. Low Volume Nodes (LVNs) are levels with relatively little trading activity and may represent zones of rejection where price can move through more quickly.

How Is FRVP Different From Session Volume Profile?

The main difference is that FRVP analyses a manually selected price range, allowing traders to focus on specific market swings, consolidations, or trends. Session Volume Profile, by contrast, automatically calculates volume distribution for predefined trading sessions without requiring manual range selection.

Can FRVP Identify Support and Resistance Levels?

Many traders use FRVP to identify potential support and resistance areas. High Volume Nodes and the Point of Control often highlight prices where significant trading activity occurred, which can attract future market interest. However, these levels are not guaranteed to hold and are typically assessed alongside other forms of technical analysis.

What Is the Value Area in a Volume Profile?

The Value Area is the range of prices that contains approximately 70% of the total traded volume within the selected profile. It is bounded by the Value Area High (VAH) and Value Area Low (VAL). Traders often use these levels to assess whether price is trading in an area of perceived value or moving beyond it.

Which Markets Can FRVP Be Used On?

FRVP can be applied to a wide range of markets, including forex and CFDs. The tool is particularly popular among traders who analyse market structure and volume distribution, as it may help highlight areas where significant trading activity has taken place.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

A spot Litecoin ETF is trading, Litecoin is a commodity by law, and the price sits at $44, down 89% from its peak. The gap between the regulatory milestone and the dead-flat chart is the most important lesson of the coming altcoin ETF wave.

Summary

- The Litecoin ETF proves access alone does not create demand.

- Litecoin has regulatory clarity, but its price still reflects weak market appetite.

- The next altcoin ETFs will succeed only if real capital is waiting behind the wrapper.

- ETF approval is a door, not a guaranteed price catalyst.

The first spot Litecoin ETF began trading in 2026 under the ticker LTCC, launched by Canary Capital after a filing the previous year, making Litecoin one of the first altcoins to win a regulated US exchange-traded fund. Around the same time, the SEC and CFTC formally classified Litecoin as a commodity, removing one of the largest regulatory obstacles that has hung over altcoins since the start of the crypto era.

On paper, this is everything Litecoin holders spent years asking for: a regulated ETF that lets institutions buy the asset through a brokerage account, and a clear legal status that ends the question of whether the token is a security. The catalyst arrived. The validation arrived.

And Litecoin trades at $44, down roughly 89% from its all-time high above $400.

That gap, between the regulatory milestone and the lifeless price, is the most instructive thing about the entire altcoin ETF story, and it is the question every investor watching the coming wave of altcoin funds should sit with. The ETF era for altcoins is truly arriving, with Litecoin already live, Dogecoin and XRP products advancing, and Solana widely seen as the strongest next candidate.

But Litecoin is the first real-world test of a thesis the market has taken on faith, the thesis that an ETF is a price catalyst, and the early result is sobering. This piece examines what the Litecoin ETF actually delivered, why the price has not responded, which altcoins come next, and what the Litecoin experience teaches about what an ETF can and cannot do.

What the Litecoin ETF actually is

The milestone itself comes first, because it is real and worth understanding before examining why it underwhelmed.

A spot Litecoin ETF holds actual Litecoin and lets investors buy exposure to its price through an ordinary brokerage account, with no wallet, no private keys, and no crypto exchange. Canary Capital launched the product under the ticker LTCC after filing with the SEC, and it stands as one of the first regulated US ETFs for an asset other than Bitcoin or Ethereum.

The accompanying regulatory development was the formal classification of Litecoin as a commodity by the SEC and CFTC, which matters because it places Litecoin under the same legal category as Bitcoin, gold, and oil, rather than leaving it in the contested securities limbo that has clouded most altcoins. For an asset class long shadowed by the question of whether each token is an unregistered security, a clear commodity classification is a meaningful piece of regulatory clarity.

Litecoin was a natural first mover for several reasons. It is one of the oldest cryptocurrencies, launched in 2011 as an early fork of Bitcoin, and it shares Bitcoin’s proof-of-work design and decentralized, mined structure, which makes the commodity classification straightforward in a way it is not for tokens with central issuers or pre-mined supplies.

It has a long operating history, deep liquidity, and none of the legal baggage that surrounds assets tied to specific companies or foundations. If any altcoin was going to clear the regulatory bar first, Litecoin’s clean, Bitcoin-like profile made it the obvious candidate, which is exactly why it became the test case for whether an altcoin ETF moves the price.

Why the price has not responded

Now the uncomfortable part, the one the ETF optimists would rather not dwell on.

Litecoin got the ETF and the commodity status, and the price did essentially nothing. At $44, Litecoin trades down roughly 89% from its all-time high above $400, and the ETF launch did not change that trajectory in any meaningful way.

The inflows into the product have been thin, far short of the demand that would re-rate the asset, and the reasons reveal the limits of the ETF thesis. The first is demand: an ETF is a vessel, not a magnet.

It makes an asset easy to buy, but it does not create the desire to buy it, and if institutional and retail appetite for Litecoin specifically is weak, a convenient wrapper does not manufacture that appetite. Litecoin is an old asset with a well-understood, relatively static value proposition as a payments-focused coin, and it does not carry the narrative momentum, the developer ecosystem, or the speculative story that pulls capital toward newer assets.

The ETF gave people an easy way to buy something many of them simply did not want.

The second reason is that Litecoin’s fundamentals did not change. An ETF and a commodity classification alter how an asset can be bought and how it is legally treated, but they do nothing to its underlying usage, adoption, or competitive position.

Litecoin remains what it was: a functional, secure, fast payments coin in a market that has shifted its attention to smart-contract platforms, decentralized finance, and newer narratives. No wrapper changes that competitive reality.

The third reason is the broader market. Litecoin launched its ETF into a period of crypto weakness, with Bitcoin in correction and altcoins under particular pressure, which is the worst possible backdrop for a catalyst that depends on fresh capital flowing in.

A catalyst that needs demand to work cannot work in the weak market the Litecoin ETF launched into.

The lesson is not that the ETF was worthless. It is that an ETF is necessary but not sufficient.

It removes a barrier to buying, which matters, but it does not supply the reason to buy, which is the part that actually moves a price. Litecoin proved that you can give an asset every piece of regulatory and structural validation it ever wanted and still watch it sit at an 89% drawdown if the underlying demand is not there.

That is also why access and certainty are different catalysts. One opens the door to buyers, while the other helps determine whether the largest buyers are allowed or willing to walk through it.

The altcoin ETF wave that is coming

Litecoin is the first, not the last, and the pipeline behind it is the reason this story matters beyond one underperforming coin.

A wave of altcoin ETFs is advancing through the regulatory system. Dogecoin has seen real progress, with an exchange certifying approval for a spot Dogecoin product, a meaningful procedural step.

XRP, fresh off its own commodity classification, is one of the most discussed altcoin ETF candidates, with strong issuer interest and a regulatory framework now in place for qualifying products. It remains a leading next-wave altcoin ETF candidate because the access story is paired with a stronger institutional narrative than Litecoin has today.

Solana is widely viewed as the single strongest next-wave candidate, given its scale, liquidity, and ecosystem. A longer tail of assets, including Avalanche, Cardano, Hedera, and Polkadot, sits further back in the queue, plausible candidates that look less advanced than the leaders.

The infrastructure that took years to build for Bitcoin and Ethereum is now being extended across the altcoin market, and the regulatory clarity flowing from the commodity classifications and the broader post-CLARITY framework is what makes it possible. It is part of the broader institutionalization of crypto, where listed products, public-market access, and regulatory wrappers increasingly shape how capital enters the asset class.

This is a real structural shift, and it deserves to be taken seriously as a long-term development. A market where the major altcoins are all accessible through regulated ETFs is a different market from the one that existed a few years ago, when buying anything beyond Bitcoin meant navigating crypto-native exchanges and self-custody.

The ETF wrapper opens altcoins to the enormous pool of capital that can only or prefers to invest through traditional brokerage and advisory channels, pension allocations, registered advisors, and conservative institutions. That access, over years, could matter a great deal.

The altcoin ETF era is real, and it is arriving. It is also increasingly tied to another new structured crypto product, as Wall Street moves from simple spot exposure toward a wider menu of regulated crypto funds.

But Litecoin is the warning label on the whole wave. Each of these assets will get its ETF, and each ETF will face the same test Litecoin just failed: whether there is real demand behind the access.

The assets with genuine narratives, ecosystems, and capital interest, an XRP with its institutional and payments story, a Solana with its developer base and scale, may see their ETFs draw meaningful flows. The assets that are mature, static, and out of narrative favor may see their ETFs launch to the same thin demand and flat price that met Litecoin.

The ETF is the same wrapper for all of them. What differs is whether anyone wants what is inside.

What the Litecoin experience teaches

The single most valuable thing an investor can take from the Litecoin ETF is a corrected model of what an ETF does, because the popular model is wrong in a way that costs money.

The popular model treats an ETF as a price catalyst, an event that, by its arrival, drives the underlying asset higher. This model has some support from the Bitcoin experience, where spot ETF approval in early 2024 preceded a major run, and it is the implicit assumption behind much of the excitement around altcoin ETF filings.

The reflexive belief is that ETF approval equals price appreciation. Litecoin demolishes that model.

The ETF arrived, the commodity status arrived, and the price stayed at an 89% drawdown, because the Bitcoin ETF did not drive Bitcoin’s price by the mere fact of existing. It drove the price because there was enormous, pent-up institutional demand for Bitcoin that the ETF finally unlocked.

The wrapper released demand that already existed. Where that latent demand is absent, as with Litecoin, the same wrapper releases nothing.

The corrected model is the one this analysis points toward: an ETF is an access mechanism whose price impact depends entirely on the demand waiting behind it. For an asset with deep, frustrated institutional demand, an ETF can be transformative, unlocking capital that was blocked only by the lack of a convenient, regulated vehicle.

For an asset without that latent demand, an ETF is a non-event, a door opened onto an empty room. The investor who understands this stops treating every altcoin ETF filing as a guaranteed catalyst and starts asking the only question that matters.

Is there real demand for this specific asset that the wrapper would unlock, or is the wrapper all there is? Litecoin answered that question for itself, and the answer was no.

What it means for investors

For anyone trading the altcoin ETF wave, the Litecoin lesson translates into a concrete discipline: separate the access story from the demand story.

The access story is the same for every altcoin getting an ETF, and it is clearly positive at the structural level. The demand story is different for each asset, and it is the variable that determines whether the ETF moves the price.

Before treating any altcoin ETF as a bullish catalyst, the disciplined investor asks whether the asset has the narrative, the ecosystem, the institutional interest, or the capital momentum that would translate access into flows. An XRP with its payments-and-institutions story and a Solana with its ecosystem scale clear that bar more convincingly than a mature, static payments coin does, and the ETF flows are likely to reflect that difference.

The wrapper is not the catalyst; the demand behind the wrapper is, and assessing that demand honestly is the whole game.

For Litecoin specifically, the ETF does not change the investment case, which rests on whether the asset can rediscover relevance and demand in a market that has moved past it. The fund makes Litecoin easier to buy for anyone who wants it, but it does nothing to increase the number of people who do, and at $44 the market is delivering a clear verdict on current demand.

Whether Litecoin’s own roadmap, including its planned smart-contract layer and its 2027 halving, can revive interest is the real question for the asset, and it is entirely separate from the ETF. None of this is investment advice; it is a framework for reading a wave of products that are arriving fast and that many investors are misreading as automatic catalysts.

The door and the room

Litecoin’s ETF is a real milestone wrapped around a sobering lesson. A regulated spot ETF, trading on a US exchange, backed by a clean commodity classification, is exactly the validation altcoin holders have wanted for years, and Litecoin now has it.

The altcoin ETF era it helps open is real, with Dogecoin, XRP, Solana, and a longer tail of assets advancing toward their own products, extending to the broad altcoin market the access infrastructure that transformed Bitcoin’s investor base.

And yet Litecoin sits at $44, down 89% from its peak, because an ETF opens a door but cannot fill the room behind it. The Bitcoin ETF worked because a crowd was waiting at that door; the Litecoin ETF underwhelmed because the room was nearly empty.

That is the lesson the coming wave will teach again and again, asset by asset: the ones with real demand behind the door will see their ETFs draw the crowd and move the price, and the ones without it will watch a regulated, validated, perfectly built product launch into silence.

The altcoin ETF era is here. What it delivers for each asset depends not on the wrapper, which is the same for all of them, but on whether anyone actually wants to walk through.

Litecoin walked through first, and found out how much the door alone is worth.

Frequently asked questions

Is there a Litecoin ETF?

Yes. The first spot Litecoin ETF began trading in 2026 under the ticker LTCC, launched by Canary Capital after filing with the SEC. It holds actual Litecoin and lets investors buy exposure through a regular brokerage account without a wallet or crypto exchange. Around the same time, the SEC and CFTC classified Litecoin as a commodity, giving it the same legal status as Bitcoin and removing a major regulatory obstacle.

Why has the Litecoin ETF not raised the price?

Litecoin trades around $44, down 89% from its all-time high, and the ETF did little to change that, because an ETF makes an asset easy to buy but does not create demand for it. Litecoin is a mature, payments-focused coin without the narrative, ecosystem, or speculative momentum that pulls capital toward newer assets, so the convenient wrapper unlocked little appetite. The fund also launched into a weak crypto market, the worst backdrop for a catalyst that depends on fresh inflows.

Which altcoins are getting ETFs next?

A wave is advancing. Dogecoin has seen an exchange certify approval for a spot product. XRP, recently classified a commodity, is among the most discussed candidates with strong issuer interest. Solana is widely viewed as the strongest next-wave candidate given its scale and ecosystem. Avalanche, Cardano, Hedera, and Polkadot sit further back in the queue as plausible but less advanced candidates.

Does an ETF guarantee a crypto’s price will rise?

No, and Litecoin is the clearest proof. An ETF is an access mechanism whose price impact depends entirely on the demand waiting behind it. The Bitcoin ETF drove Bitcoin higher because enormous pent-up institutional demand existed that the wrapper finally unlocked. Where that latent demand is absent, as with Litecoin, the same wrapper produces little. Investors should ask whether real demand exists for a specific asset rather than assuming ETF approval automatically means price appreciation.

Why was Litecoin one of the first altcoin ETFs?

Litecoin’s profile made it a natural first mover. Launched in 2011 as an early Bitcoin fork, it shares Bitcoin’s proof-of-work, decentralized, mined design, which makes a commodity classification straightforward in a way it is not for tokens with central issuers or pre-mined supplies. It has a long history, deep liquidity, and none of the legal baggage tied to company-linked assets, so it cleared the regulatory bar before more complex altcoins.

Should I buy the Litecoin ETF?

This article does not provide investment advice. The ETF makes Litecoin easy to buy but does not change its underlying investment case, which rests on whether the asset can rediscover demand in a market that has moved past it. At $44, the market is signaling weak current demand despite the ETF and commodity status. Litecoin’s future depends on its own roadmap and relevance, separate from the wrapper, and any decision should weigh that rather than treating the ETF as an automatic catalyst.

As of June 16, 2026. Cryptocurrency and ETF markets are volatile and information can change quickly; verify current details before relying on this analysis. This article is information, not investment advice.

Australia’s High Court has unanimously ruled 7-0 in favor of the Australian Securities and Investments Commission, finding that Block Earner’s former fixed-yield crypto product required a financial services licence under existing law.

Summary

- Australia’s High Court ruled 7 to 0 that Block Earner’s former fixed yield crypto product required a financial services licence.

- The decision overturns a 2025 appeal court ruling and sends the case back to the Full Federal Court to consider penalties.

- Block Earner has since exited yield products and is developing crypto backed home loans after securing an Australian Credit Licence in 2026.

According to a June 17 court document, the High Court determined that the product offered by Web3 Ventures Pty Ltd, which operates as Block Earner, functioned as a facility for financial investment and also met the legal definition of a derivative. The court found that investor returns depended on movements in underlying digital asset values and exchange rates.

As a result of the ruling, the case will return to the Full Federal Court, which will now consider ASIC’s appeal relating to penalties tied to earlier proceedings against the company.

ASIC said in a statement on Wednesday that it launched civil penalty proceedings against Block Earner in November 2022 over concerns that the Earner product had been offered without the required licence. According to the regulator, investors who used the product did not receive important protections available under Australia’s financial services framework.

High Court overturns earlier appeal decision

Court records and ASIC’s statement show the dispute has moved through several stages of Australia’s judicial system over the past two years.

The Federal Court ruled in February 2024 that Block Earner had operated an unregistered managed investment scheme. Although the court later decided in June 2024 not to impose financial penalties, ASIC challenged that outcome and filed an appeal the same month.

Soon afterward, Block Earner lodged a cross-appeal on July 9, 2024. The Full Federal Court sided with the company in April 2025, allowing the cross-appeal and dismissing ASIC’s challenge. Wednesday’s High Court judgment overturned that decision.

Welcoming the outcome, ASIC Chair Sarah Court said the ruling supports the regulator’s long-held view that Australia’s financial product laws apply to new technologies without requiring legislative changes.

“This reinforces ASIC’s long-standing position that the definition of financial product is broad and technology neutral and so captures new and emerging products without the need to amend the legislation,” Court said.

Block Earner continues crypto lending plans

Although the legal dispute centered on the Earner yield product, Block Earner voluntarily shut down the offering in November 2022 and has since redirected its business toward lending services.

In May 2026, the company received an Australian Credit Licence and announced plans to develop crypto-backed home loans. At the time, Block Earner said the product would allow borrowers to use Bitcoin as collateral for home financing without selling their holdings.

The licence was notable because it represented the first time a digital asset platform in Australia had been authorized to provide credit products under its own licence.

Earlier company statements also linked the initiative to growing interest in integrating digital assets into traditional mortgage markets. Similar discussions have emerged in the United States, where federal housing authorities and lawmakers have explored frameworks that could allow certain regulated crypto holdings to be considered during mortgage assessments.

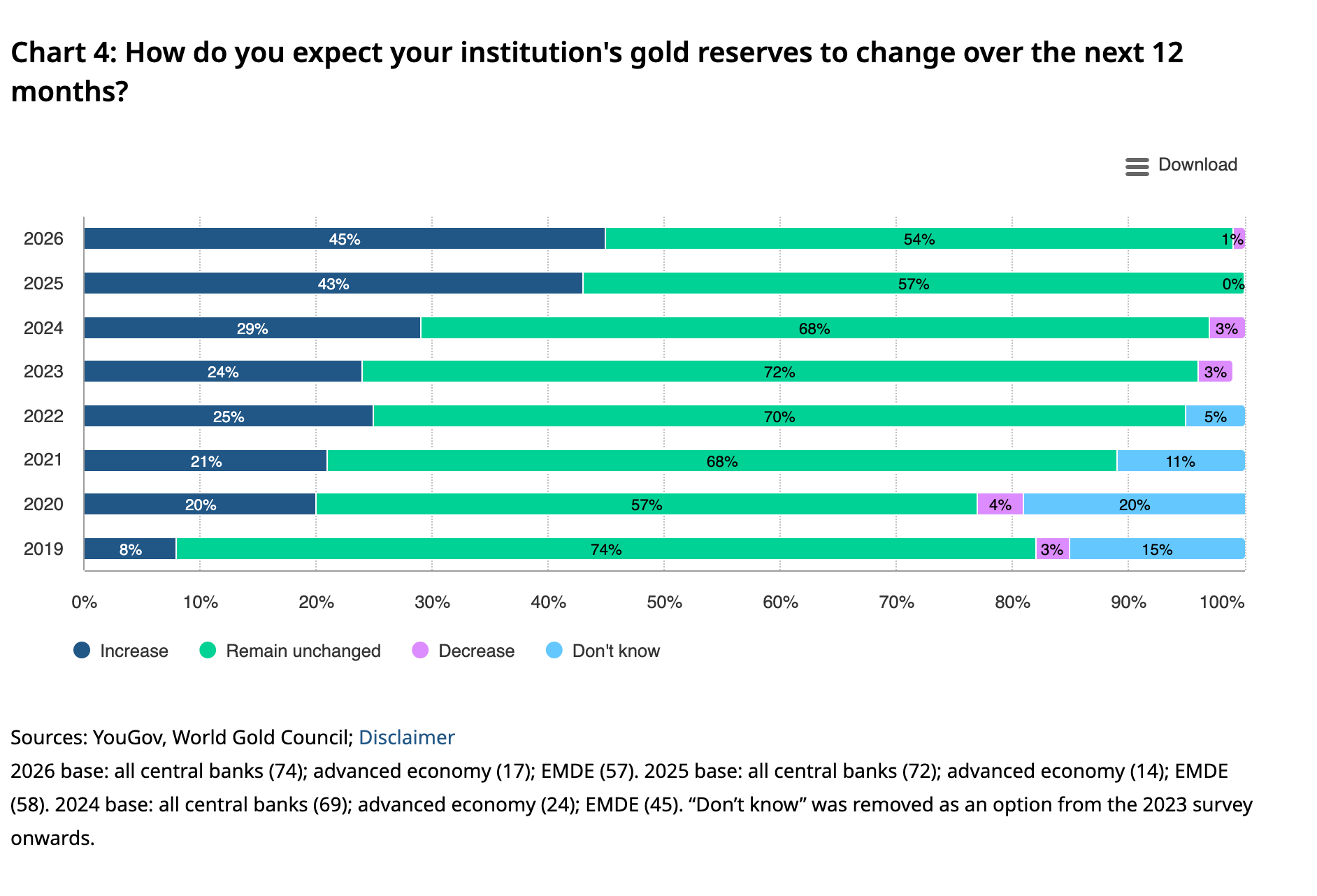

45% of central banks intend to grow their gold reserves over the next 12 months, the highest level on record in the World Gold Council survey.

The annual study also found that 89% of central banks expect global central bank gold holdings to rise, while just 1% anticipate a decline.

Follow us on X to get the latest news as it happens

Why Central Banks Keep Stockpiling Gold

Central banks have bought an average of 1,000t of gold since 2022. That pace is double the 500 tonnes averaged over the previous decade.

Recent monthly data reinforces the trend. Official buyers resumed net purchases in April, adding 19 tonnes after recording net sales in March.

Poland led the month with 14 tonnes, raising its 2026 total to 45 tonnes. China added 8 tonnes, its 18th consecutive month of buying.

Not all activity points in one direction. Russia extended a selling streak with 6 tonnes in April, while Turkey kept its reserves broadly flat.

What Is Driving the Gold Demand

Meanwhile, respondents pointed to familiar reasons for holding gold. Its role as a long-term store of value, its performance in a crisis, and its diversification benefits remain the core motivations.

“90% of respondents indicated that gold’s performance during times of crisis is highly or somewhat relevant to their organisation, a record high for this factor. 84% of respondents indicated that gold’s role as a store of value was a relevant factor, while 83% pointed to gold’s attribute as a portfolio diversifier,” the findings revealed.

Economic and geopolitical signals also shaped reserve decisions. Interest rate levels topped the agenda at 92%, the same as last year. Geopolitical instability and inflation followed.

Instability has now edged ahead of inflation, a shift the report ties to the war in Iran. Most responses arrived after the Middle East conflict began in early 2026.

At the same time, confidence in the dollar continues to weaken. Around 74% of respondents expect their reserve share to fall over five years, while 84% expect gold’s share to rise.

“We expect that there will be a downward shift in the share of total reserves held in US dollars. This reduction will come primarily from countries whose relationships with the US are likely to be affected by US foreign policy and political relations,” a respondent said.

Not every signal points higher. Bearish options bets target a 40% decline in gold prices by 2028, with Citigroup trimming its forecast to $4,000.

The divergence sets up a clear test for the market. Steady official demand would need to offset any cooling in private investor appetite to hold prices firm.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post New Survey Shows Central Banks Far From Done Buying Gold appeared first on BeInCrypto.

GRAM dropped between 2% after India ordered Google and Apple to delist Telegram from their app stores, cutting off access for an estimated 104 to 150 million users, and Pavel Durov is not happy. It’s cutting Telegram’s single largest national user base.

Executed under Section 69A of India’s Information Technology Act, it is explicitly temporary, tied to the NEET-UG medical entrance re-examination scheduled for June 21.

The entire investment thesis for the TON blockchain and its native token rests on Telegram as a distribution moat, a billion-user platform that embeds the chain natively into daily messaging. One government’s Section 69A order just demonstrated that the moat has a trapdoor.

This will likely affect the crypto market too, with India as one of the largest countries with active crypto holders, and Telegram, alongside X, are where crypto communities are spending their days.

— TALK TO CRYPTO (@talktocrypto2) March 14, 2026

#BTC #Global Ranking:- Countries with the most Bitcoin holders

#BTC #Global Ranking:- Countries with the most Bitcoin holders

1.  India:- 93 million

India:- 93 million

2.  United States:- 46 m..

United States:- 46 m..

3.  China:- 41 mil..

China:- 41 mil..

4.  Nigeria:- 18 mil..

Nigeria:- 18 mil..

5.  Vietnam:- 17 mil..

Vietnam:- 17 mil..

6.  Indonesia:- 14 mil..

Indonesia:- 14 mil..

7.  Turkey:- 12 million

Turkey:- 12 million

8.  Philippines:10 mil.. pic.twitter.com/ewje351bst

Philippines:10 mil.. pic.twitter.com/ewje351bst

Discover: The Best Crypto to Diversify Your Portfolio

What Has The Indian Government Done?

India’s Ministry of Electronics and Information Technology, acting on a formal request from the National Testing Agency, invoked Section 69A of the IT Act to restrict access to Telegram ahead of the NEET-UG re-exam. The National Testing Agency had canceled the original May 3 exam amid allegations of paper leak, with Telegram channels implicated in distributing, and in some cases fabricating, leaked materials.

A separate government direction requires Telegram to disable its message-editing feature for Indian users until June 30. This is targeting the specific mechanism that investigators say cheating networks used to create backdated fake leak evidence.

As of today, the delisting order runs until June 22, 2026, or one day after the re-exam.

Telegram CEO Pavel Durov responded on X with a sharp counter-allegation, accusing India telecom Reliance of using BGP hijacking. He noted that they are specifically abusing the Border Gateway Protocol via autonomous system number AS18101 to reroute and disrupt Telegram access for users outside India, including in the UAE.

BGP hijacking is a technique where a network operator broadcasts false routing information to redirect internet traffic; if genuine, it would mean Telegram’s connectivity problems extend well beyond the Indian government order. Pave; Durov also alleged that Reliance and WhatsApp lobbied jointly to impose the India ban, citing Reliance’s partial ownership by Meta as a motive.

— Mario Nawfal (@MarioNawfal) June 17, 2026

India just banned Telegram for 150M users to stop exam cheating ahead of the NEET-UG re-test on June 21.

Its CEO Pavel Durov pushed back immediately: "This punishes 150M+ ordinary users, not the insiders who leaked the exam materials. The leaks just moved to other apps."

And… pic.twitter.com/xvW7CMzZtF

A senior India telecom industry source flatly rejected the claims, telling the Economic Times that Pavel Durov conflated two entirely separate entities. Reliance Communications, which operates subsea cables and holds AS18101, and Reliance Industries Ltd, the parent of Jio, in which Meta holds only a minority stake with no operational role.

The source called the conflation either a misunderstanding of the sector or deliberate misinformation. Telegram, Jio, Meta, and Reliance Communications had not responded to media queries at the time of publication.

Discover: The Best Token Presales

Not Just Pavel Durov, Crypto Takes a Hit by India Decision

The bull case for Gram, or TON blockchain, has always been distribution, so is crypto in general. Telegram’s crypto funnel is running at scale. India, with 104 to 150 million Telegram users, is the largest single node in that funnel. Per the report, the disruption of crypto hit tap-to-earn games, daily quiz apps, and Web3 mini-apps immediately, with Indian users locked out of on-chain participation overnight.

The distinction between Durov’s two claims matters for the investment calculus. If the Indian ban is purely regulatory, a government acting on legitimate exam-integrity concerns, then it is bound by those concerns and ends when they are resolved.

— Indian Tech & Infra (@IndianTechGuide) June 17, 2026

Do you think blocking Telegram is the right decision?

Do you think blocking Telegram is the right decision?

If Durov’s allegation holds, and WhatsApp and Reliance entities lobbied to suppress a competitor, then the ban is an instrument of competitive warfare. Competitive suppression is episodic and typically reversible when the political cost rises. Genuine regulatory action can evolve into something structural.

The BGP hijacking claim, if verified, would be independently alarming; it would mean disruption to Telegram access is being manufactured at the routing layer, outside any government order, affecting users in third countries like the UAE.

Discover: The Best Crypto to Diversify Your Portfolio

The post India Bans Pavel Durov Telegram: GRAM and Crypto Hammered, Whatsapp Accused appeared first on Cryptonews.

Shrek 5 Trailer Has Just Launched Without Zendaya

2026 World Cup parlay, best bets: Top picks for matches on Wednesday include Portugal and England

Stop Killing Games Fails To Secure EU Law Despite 1.3 Million Signatures

-

Business3 days ago

Business3 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Crypto World6 days ago

Crypto World6 days agoOppenheimer backs SpaceX as $70 billion retail frenzy builds

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoMarkets Rally as SpaceX IPO Looms Amid Iran Tensions and Inflation Surge

-

Crypto World2 days ago

Zimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Tech4 days ago

Tech4 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Tech5 days ago

Tech5 days agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

Crypto World4 days ago

Crypto World4 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Tech6 days ago

Tech6 days agoDutton Ranch star claims they ‘didn’t see any disruption’ on set following Chad Feehan’s exit from Yellowstone spinoff fueled by Taylor Sheridan clash rumors

-

NewsBeat6 days ago

NewsBeat6 days agoEl Nino has formed in the Pacific and could set records, forecasters say

-

Politics6 days ago

Politics6 days agoPolitics Home | Healey Resignation Is “Colossal Failure Of Government”, Says Former Labour Defence Secretary

-

Entertainment6 days ago

Entertainment6 days agoDonnie Wahlberg & More Heat Up Las Vegas at Circa’s Barry’s Downtown Prime

-

Tech6 days ago

Tech6 days agoOpendoor Ends India Operations, Fueling a Bigger Conversation About AI and Outsourcing

-

Sports6 days ago

Sports6 days agoFirst Time Since 1971: Australia Register Historic Low In ODI Cricket

-

Politics6 days ago

Politics6 days agoBelfast burns, while Met chief points finger at Iran and Russia

-

Business6 days ago

Business6 days agoAT&T: Verizon's 27% Outperformance Sets Up A Solid Entry Point

-

NewsBeat5 days ago

NewsBeat5 days agoFBI searches office of Ohio voter registration group

-

Tech5 days ago

Tech5 days agoAnthropic is spending $150M to embed 1,000 AI fellows inside nonprofits. No degree required.

-