Crypto World

Win for Crypto Pricing, Loss for Tokenized Access

SpaceX’s hotly anticipated public debut on June 12 raised $75 billion at $135 per share, valuing the company at more than $2 trillion and turning its founder, Elon Musk, into the world’s first trillionaire.

And it’s not only Musk getting wealthier. Buyers who got in at the offer price made roughly 20% almost overnight, while early private investors saw far larger gains.

Crypto traders, meanwhile, were abruptly cut out of the deal, left holding pre-IPO subscription tokens on platforms like Binance, Bybit and Bitget with no allocation to SpaceX at all.

As SPCX shares soared, key tokenized equity pipelines broke down. Intermediaries failed to secure allocations, campaigns were abruptly canceled, and platforms scrambled to issue refunds and damage control.

In effect, it’s a stress test for the “tokenized IPO access” narrative; price discovery worked, but access to the underlying shares did not.

Pre-IPO perps as a parallel price signal

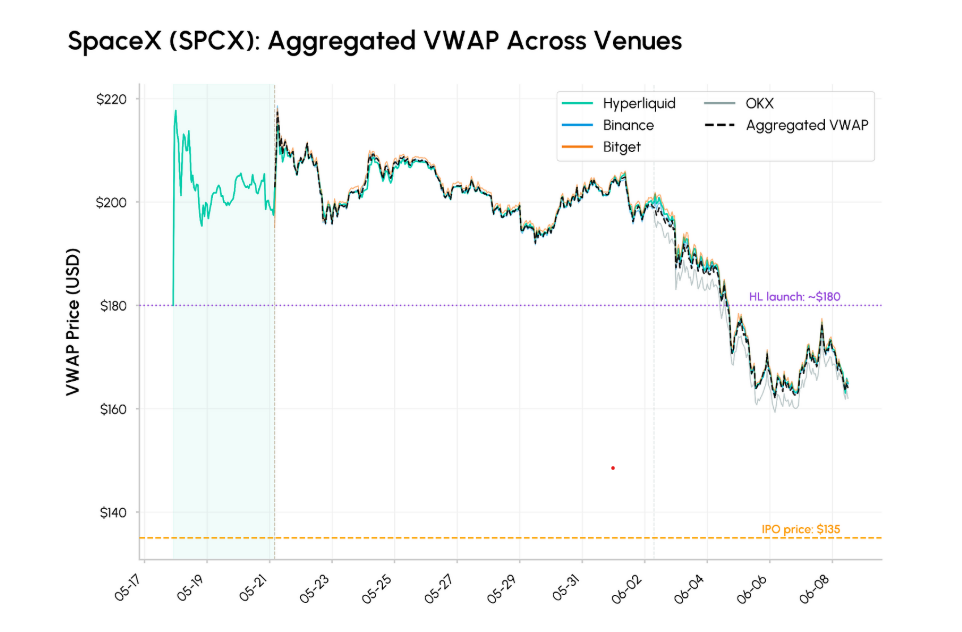

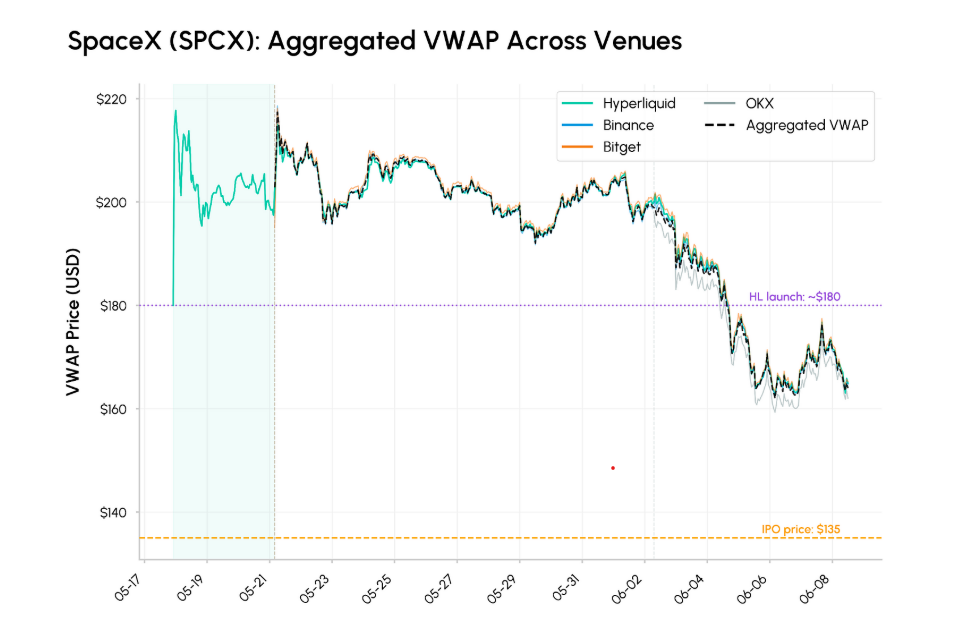

According to Talos Research data shared with Cointelegraph on June 15, in the 30 minutes before the Nasdaq open, SPCX perpetuals traded at a volume-weighted average price (VWAP) of $159.89 across Hyperliquid, Binance and OKX, around 6.6% above the opening print, while Cerebras (CBRS) perps on Hyperliquid were within 1.3% of the Nasdaq open.

It’s also worth noting SPCX perps peaked above $220 in mid-May before gradually converging lower toward the IPO date as traders incorporated more realistic valuation expectations, Talos Research said.

SpaceX aggregated VWAP across venues, May 17 – June 8. Source: Talos

Pre-IPO perpetuals on derivatives platforms showed that onchain traders could generate credible price discovery and deep liquidity for a hot tech unicorn before a single share changed hands. They flashed a real-time indication of where speculators thought the stock would land by the opening bell.

Related Crypto Biz: SpaceX fuels tokenization’s next boom

“These signals will become increasingly difficult for underwriters and retail-facing platforms to ignore,” Samar Sen, head of international markets at Talos, told Cointelegraph, “particularly for high-profile listings where there is already active global demand before the IPO.”

He said these markets could “become a useful supplementary input alongside institutional orders, private market marks and comparable-company analysis.”

Why tokenized SpaceX “IPO access” collapsed at the last mile

The problem, then, was not with synthetic, futures-style exposure to SpaceX’s valuation. Pre-IPO perpetuals “functioned as intended,” Sen said, proving to be “a venue for continuous trading and price discovery ahead of the listing.”

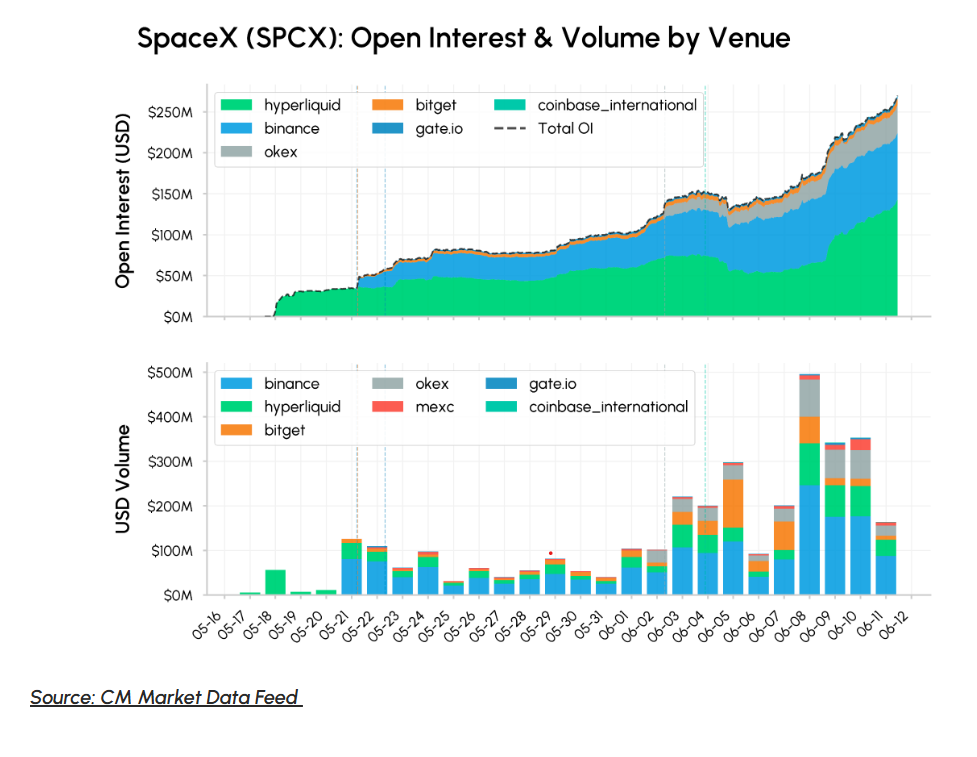

Talos Research showed that SPCX perpetual markets recorded roughly $4.6 billion in trading volume on the day of IPO, with total open interest peaking near $500 million across eight venues, including Hyperliquid, Binance, OKX and Kraken, while Cerebras (CBRS) on Hyperliquid saw $281 million in IPO day volume.

Perpetuals traders were able to monetize both the pre-IPO volatility and the post-listing convergence. But investors who bought tokenized claims on SpaceX IPO shares missed out on the upside entirely.

The SpaceX IPO was four times oversubscribed, leaving many retail investors with too few shares, tiny fills, or even zero allocation.

SpaceX open interest by volume and venue, May 16 – June 12. Source: Talos

SpaceX-linked tokenized shares on major exchanges collapsed at the last mile, with platforms like Binance, Bybit and Bitget Wallet all canceling their campaigns and issuing refunds after xStocks failed to deliver the underlying allocation.

Alvin Kan, chief operating officer of Bitget Wallet, told Cointelegraph that users subscribed to participate in a tokenized IPO offering facilitated through Kraken’s xStocks, and that the tokens, “if issued,” would represent economic exposure to SpaceX shares.

Related: Bybit to offer tokenized SpaceX IPO access through xStocks

The tokens never came. Kraken was unable to satisfy demand from its own users, let alone serve as a distribution hub for third-party platforms, since the bottleneck was the availability of underlying IPO shares, rather than the onchain plumbing itself.

How exchanges responded when the allocation pipeline broke

Users were left empty-handed as platforms issued notices citing “circumstances outside” their control, causing them to cancel their campaigns and return the subscribed funds.

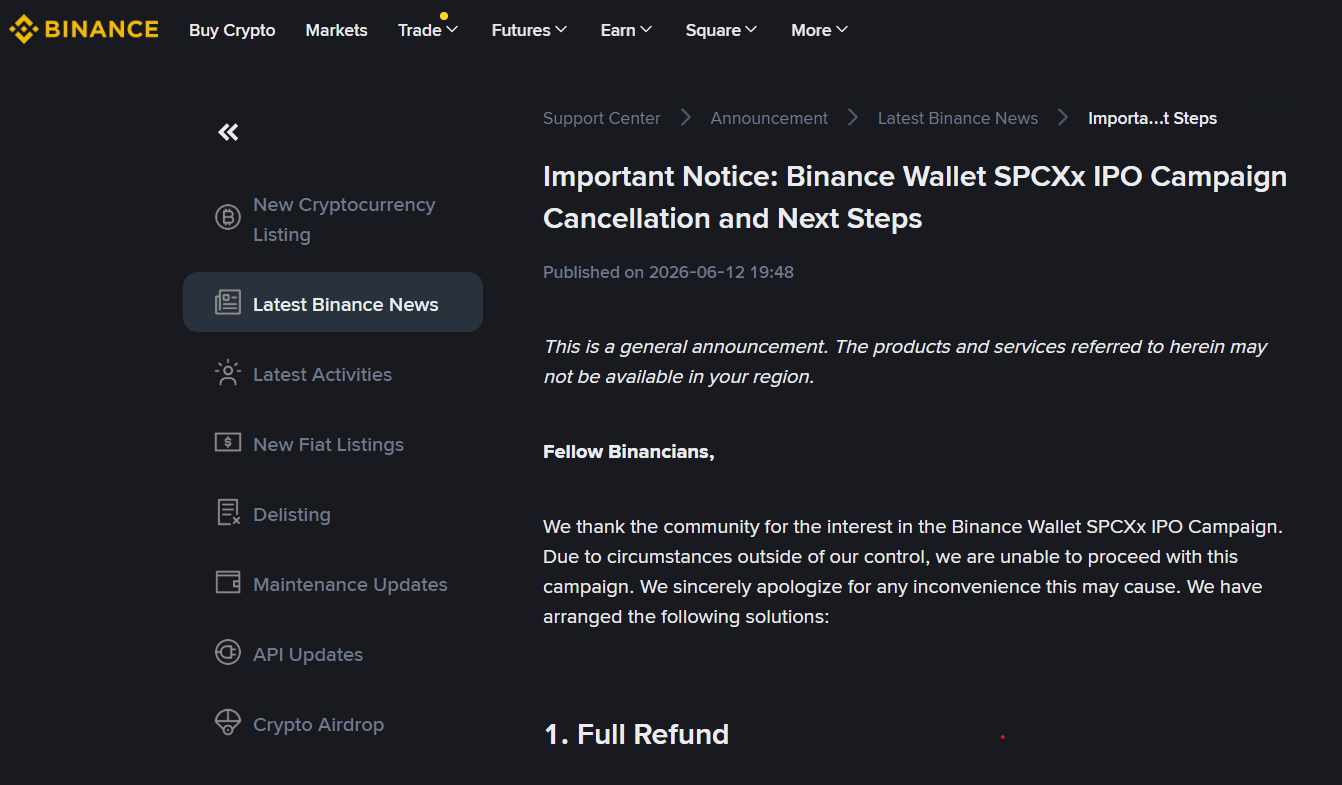

Binance founder and former chief executive Changpeng Zhao posted the notice on X with the comment, “Protect users when things don’t go as planned,” which triggered a litany of furious replies from retail traders.

Binance customer notice, SpaceX IPO campaign cancelation. Source: Binance

One user stated, “last in the queue, again,” and pointed to the $557 million in crypto capital raised across “three of the world’s biggest exchanges” to buy tokenized SpaceX shares.

“All cancelled. Zero shares delivered… Turns out you still need the underlying asset. Blockchain doesn’t magic shares into existence when Wall Street decides who gets the allocation.”

A Binance Wallet representative told Cointelegraph its role in the campaign was limited to technical and support services. Binance Wallet was not responsible for “pricing, issuance, backing or redemption,” they said, and user-facing materials stated allocation was not guaranteed.

Despite also getting clogged in the xStocks blockage, Bitget, after canceling its pre-market subscriptions and refunding users, responded by switching to Reality, a real-world asset platform backed by the exchange.

Related: Kraken offers SpaceX IPO access through xStocks

Bitget chief executive Gracy Chen told Cointelegraph that Reality provides 1:1 tokenized SpaceX shares (rSPCX) on the spot market, held with a broker, replacing the exchange’s third-party initiative with xStocks.

She said that for users, that means access to “properly backed” US equities, rather than short-term structures chasing a single hot IPO.

The gap between onchain exposure and real allocations

At the heart of the SpaceX mess is a simple structural gap. Crypto venues can create synthetic or tokenized exposure to a stock, but they can’t control the primary market allocations that only underwriters with broker-dealer networks can provide.

Pre-IPO perpetuals gave a strong real-time signal of where traders thought SPCX should trade, but the tokenized IPO campaigns depended on a single upstream allocation pipe that ultimately ran dry.

Sen argued this is exactly why pre-IPO derivatives should be treated as “signals” not substitutes for the IPO machinery itself, and the SpaceX episode reinforces the “need for greater caution around how different forms of pre-IPO exposure are structured, marketed and understood.”

Kan said the episode points to a “broader reality facing the tokenized RWA space,” adding that onchain infrastructure for distribution and settlement is ready, but the mechanisms for crypto-native channels to access primary market allocation are still developing.

Retail demand, he said, is growing faster than the supply-side infrastructure, and closing that gap will require “closer collaboration between crypto platforms, traditional intermediaries and regulators.”

Tokenization can improve access, but it can’t create shares

The legal constraints also help explain why the SpaceX IPO was never going to happen onchain in the first place.

Brogan Law’s Aaron Brogan noted that a token sold to raise $75 billion for SpaceX and marketed on the company’s future performance would fall squarely on the securities side of the Securities and Exchange Commission’s (SEC) recent token guidance line.

Related: SEC plan to scrap ‘Rule 611’ positive for tokenized US stocks: Galaxy

Between securities law, tax uncertainty and the scrutiny a mega-deal would invite, he argued, “there is no path to do so reliably,” making a full-blown token sale an unrealistic substitute for a traditional IPO for a company of SpaceX’s size.

A spokesperson from the SEC declined to comment on whether the regulator had concerns around crypto platforms’ promotion of IPO access or whether securities regulations adequately address tokenized equity offerings.

Statement on Tokenized Securities. Source: SEC

In a January 2026 staff statement on tokenized securities, however, the SEC stressed that tokenized stocks remain full securities subject to registration and disclosure rules, explicitly distinguishing between custodial, issuer-sponsored tokenization and synthetic or third-party wrappers.

The future of tokenized IPO access

For all the drama around the SpaceX IPO, none of the key players believe it has killed the tokenized equity story, but rather sharpened the conditions under which it can work.

Dinari, a tokenized equities platform whose tokenized $SPCX maintained continuous uptime as the allocation pipe ran dry, chief executive Gabriel Otte told Cointelegraph the long-term opportunity is to “extend the reach of public markets, not reinvent them.”

He said that was achievable by starting with real underlying securities, regulated custody and clear legal rights, then using tokenization to improve access and settlement rather than to sidestep the rules.

Chen, for her part, said the exchange has learned to avoid short-term, third-party structures and instead build 1:1, broker-backed tokens it can stand behind.

For Brogan, the SpaceX IPO exposed the difference between pricing a stock and allocating one. Crypto markets were able to generate liquidity and price discovery ahead of the listing, but access to actual IPO shares remained firmly in the hands of traditional market participants.

Sen concluded that, while investors may be more cautious about products promising exposure to underlying private company shares, the scale of activity surrounding SpaceX shows these markets are “becoming increasingly difficult to ignore.”

Magazine: How to fix suspected insider trading on Polymarket and Kalshi

Key Takeaways

- Three Solana digital asset treasury companies—Solana Company (HSDT), Brera Holdings, and SkyAI—declined or ignored Forward Industries’ acquisition proposals

- Forward Industries commands the largest Solana DAT position with more than 7 million SOL tokens valued at approximately $525 million

- Forward’s shares climbed up to 8.6% on Tuesday despite the acquisition setbacks

- Solmate leveled accusations against Forward, alleging undisclosed coordination with market maker RockawayX and investor Viktor Fischer in what it characterized as a hostile takeover effort—claims Forward has refuted

- Industry observers suggest smaller DAT operators face pressure to merge as many cannot sustain basic operational expenses

Forward Industries launched an ambitious campaign to merge smaller Solana treasury operations under its umbrella, only to encounter resistance from three prospective acquisition targets.

Solana Company, which operates under the HSDT ticker symbol, turned down Forward’s all-stock acquisition proposal on June 12. The offer would have granted HSDT stakeholders 0.386 Forward shares for every share they owned, effectively pricing HSDT at $1.63 per share.

HSDT’s board determined the proposal “substantially undervalues the company” and failed to serve shareholder interests. In a unanimous decision, the board rejected the bid and stated it would not pursue additional negotiations.

Brera Holdings similarly dismissed Forward’s nonbinding all-stock proposal submitted June 9, which assigned a $7.19 valuation to each Brera share. Meanwhile, SkyAI received a distinct offer pricing its shares at $1.55, but the company allowed the proposal to lapse without providing any formal reply.

Forward expressed being “disappointed and surprised” by HSDT’s refusal to engage in any dialogue before rejecting the proposal.

Accusations of Coordinated Takeover Strategy

Solmate, yet another acquisition candidate, delivered a more aggressive response to Forward’s overtures. In its June 12 rejection letter, Solmate alleged that Forward was operating in secret coordination with market maker RockawayX and investor Viktor Fischer as an undisclosed collective—positioning the move as a hostile takeover scheme.

Forward firmly rejected these allegations, dismissing them as unfounded accusations driven by Solmate’s strategic interest in derailing the transaction.

Despite facing multiple rejections, Forward’s stock price surged as much as 8.6% during Tuesday’s trading session. HSDT shares fell by as much as 6% the same day. Solmate posted gains exceeding 11%, while SkyAI shares advanced 2%.

The Case for Solana DAT Consolidation

Forward controls more than 7 million SOL tokens, establishing its position as the preeminent Solana digital asset treasury operator by holdings volume. The firm initiated its treasury approach in September 2025 and has placed the majority of its token holdings in staking arrangements.

According to CoinGecko metrics, Forward’s SOL position carries a current market value near $525 million. Reports indicate the company spent nearly $1.6 billion acquiring these holdings, resulting in an unrealized loss exceeding $1 billion.

Forward’s Chief Investment Officer Ryan Navi highlighted that numerous smaller DAT operations may struggle to meet their operating expenses even when maximizing staking rewards. He projected Forward’s quarterly selling, general, and administrative expenses at approximately $4.5 million.

“I don’t think there needs to be 20 Solana DATs,” Navi said.

Forward is scheduled for inclusion in both the Russell 2000 and Russell 3000 indexes at June’s conclusion, a development anticipated to attract institutional and passive investment flows into the stock.

August Widmer, a partner at Echo Base, characterized consolidation as potentially the sole sustainable path forward for the sector. He suggested the recent rejections indicate smaller players have not yet acknowledged this market reality.

“There’s still further to fall in this market before that reality is accepted,” Widmer said.

Kohl’s KSS -3.95%decrease; down pointing triangle named a former Foot Locker executive as its next chief operating officer, marking the department-store chain’s latest leadership appointment as it continues its turnaround efforts.

Elliott Rodgers will assume the role on Sept. 9, taking on responsibility for Kohl’s enterprise operations including its stores, global supply chain and distribution centers, procurement and loss prevention, the retailer said Monday.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

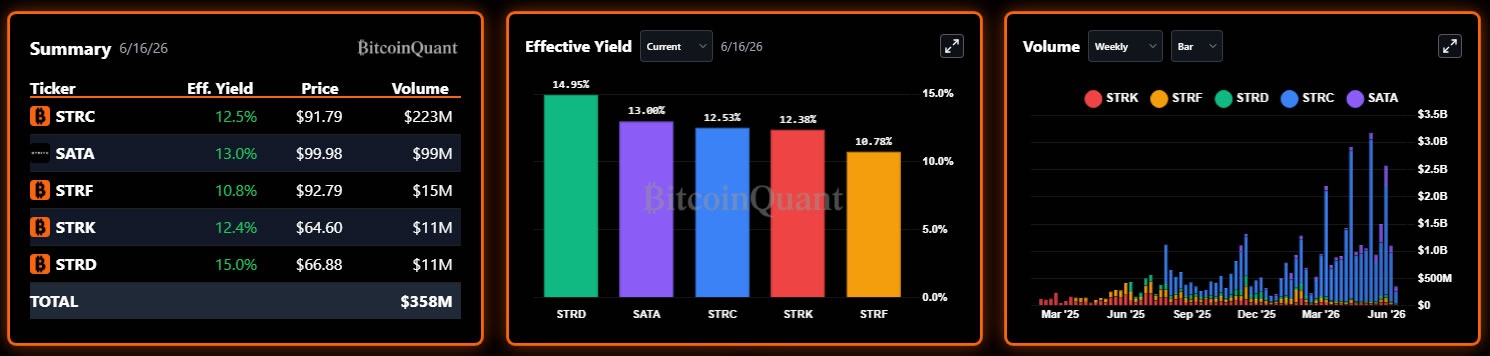

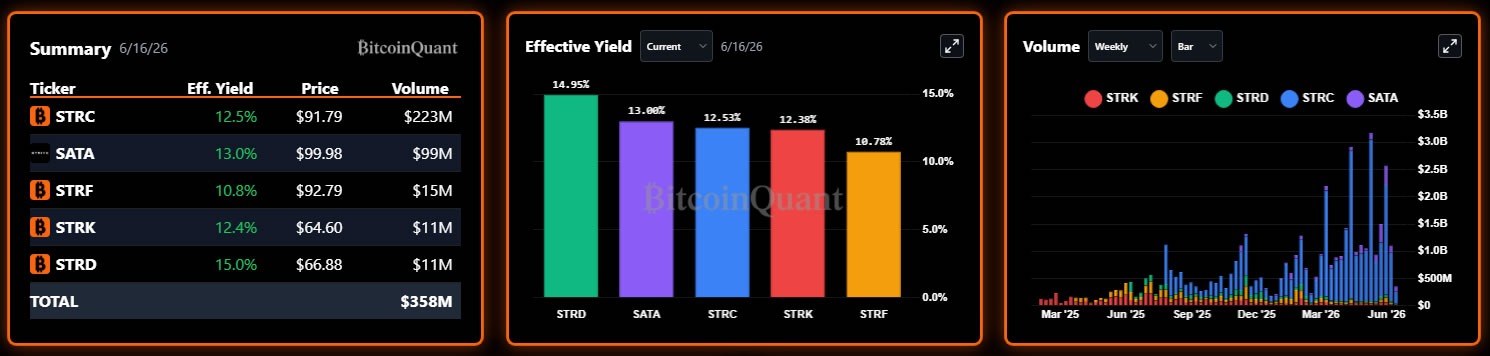

Strategy’s perpetual preferred stock STRC fell near record lows on Tuesday as investors seemingly balked at the company’s latest Bitcoin acquisitions.

Michael Saylor’s variable-rate perpetual “Stretch” Bitcoin yield product declined by 3.58% to $91.79 on Tuesday, 8.2% below its target value of $100. Markus Thielen, CEO of 10x Research, said the dip is linked to Strategy’s recent Bitcoin buying.

“The market would rather see [Strategy] not acquiring more BTC and rather keep the cash for dividend payments,” Thielen told Cointelegraph. “It appears traders are seeing the latest BTC acquisition as an unsustainable path for STRC.”

Stretch is designed to return a dividend of 11.5%, trading at a par value of $100, but the current effective yield, now that the shares have dipped, is 12.5%. This means the firm may need the cash to support the yield rather than spending it to buy more BTC.

On Monday, Strategy said it acquired 1,587 Bitcoin for around $100 million last week. The week before, it purchased 1,550 BTC, also for about $100 million. The combined purchases brought its holdings to 846,842 Bitcoin.

Risk-off sentiment and pressure from competitors

Nick Ruck, director of LVRG Research, told Cointelegraph that “broader risk-off sentiment in crypto markets has weighed on investor appetite.”

“While the variable dividend delivers an effective yield above 12% to anchor the perpetual preferred near its $100 par value, persistent selling pressure and concerns over Strategy’s expanding capital structure and ATM issuance appear to be testing that resilience in the near term,” he added.

Related: Strategy’s Saylor signals BTC buy as preferred dividend pay date vote looms

The company’s stock (MSTR) has also taken a hit this week, dropping 6.35% on Tuesday to end the day at $122.81, down 67% over the past 12 months.

Meanwhile, Stretch is also facing stiff competition from the Strive perpetual variable-rate preferred shares (SATA), which are trading at $100 and offering an effective yield of about 13%.

BTC variable-rate perps comparison. Source: BitcoinQuant

Magazine: China’s 107 Bitcoin memory thief, Bithumb CEO booked: Asia Express

Crypto World

Casual Dining’s Comeback Is Winning Over Wall Street. Cava and Dutch Bros Are Worth a Look.

Casual dining isn’t usually where investors look for market leaders. But some restaurant chains are quietly outperforming expectations, delivering steady traffic, healthier profits, and stock gains that have outpaced much of the broader consumer sector.

The US House and Senate have reached a deal to move forward with a housing bill that includes a ban on the Federal Reserve creating a central bank digital currency (CBDC) until 2030.

A bipartisan group of House and Senate leaders released an updated version of the 21st Century Road to Housing Act on Tuesday, which aims to address housing affordability and bans institutional investors from buying existing single-family homes to rent out.

The bill has included a CBDC ban since the Senate passed it in March. The House also passed its version of the bill with strong support in May, but the House and Senate disagreed on some aspects. The Senate has now added further amendments that will be put before the House for a final vote.

The bill is likely to pass quickly and would hand a win to Republicans who have tried to pass a CBDC ban for years, as earlier standalone bills had stalled in Congress. Crypto advocates have long criticized CBDCs, which they see as an attempt by governments to repurpose crypto technology to a centrally-controlled asset.

Source: US Senate Banking Committee GOP

The deal also means Congress can focus on passing other legislation before the August recess and the November midterm elections, in particular, the crypto-regulating CLARITY Act that many lawmakers have been pushing to advance.

House Republican leaders plan to put the bill up for a vote after the House returns from recess on June 23, two people familiar with the plan told Politico.

The housing bill includes language that says the Federal Reserve may not, directly or indirectly, “issue or create a central bank digital currency or any digital asset that is substantially similar to a central bank digital currency.”

Related: South Carolina governor signs bill protecting Bitcoin miners, banning CBDC

It adds the clause will expire on Dec. 31, 2030, and creates a carveout for crypto stablecoins, or “dollar-denominated currency that is open, permissionless, and private.”

The clause revives much of the language from Republican Representative Tom Emmer’s Anti-CBDC Surveillance State Act, which was introduced in June 2025, passed by the House the next month, but was never picked up in the Senate.

US President Donald Trump signed an executive order in January 2025 banning federal agencies from all work related to CBDCs, saying they threatened “the stability of the financial system, individual privacy, and the sovereignty of the United States.”

Magazine: How crypto laws changed in 2025 — and how they’ll change in 2026

The days of altcoins making money from token launches and hype alone are over.

This is according to CryptoQuant CEO Ki Young Ju, who says there are now only three categories that can survive into the future.

The Era of Narrative-Only Tokens Is Over

The analyst made his blunt assessment in an early Wednesday thread on X, where he started by pointing out that “altcoins aren’t dead,” but those that only made money from selling narratives would soon disappear from the crypto world.

He then made a structured case for why a selective exposure to a small subset of the asset class still makes sense in 2026, putting emphasis on those with real revenue, real businesses, and alignment with where global finance is actually heading.

The first category he identified is what he called “global internet companies with tokenized market layers,” where he pointed to Binance’s BNB Coin and the TON blockchain’s recently rechristened GRAM token. According to Ju, such tokens are backed by businesses with revenue, have an established user base, and have shown long-term operational commitment. He suggested that for such companies, it sometimes made more sense to issue a token and list it on a crypto exchange than to pursue traditional equity listings.

The second group the market watcher identified were DeFi protocols also with actual revenue. Here, he namechecked Hyperliquid’s DEX, noting that tokens from such “high-quality” projects can still offer huge upside, especially if the teams behind them are credible, they have money coming in, and their governance systems respect holders.

Highlighting Hyperliquid was no mistake on Ju’s part, considering the HYPE token associated with the platform has been doing crazy numbers lately, jumping over 31% in the last seven days and almost 70% across the last month. That push, supported by ETF inflows and strong trading activity tied to SpaceX-linked perpetual contracts, saw it reach a new all-time high just above $76 on June 16.

Lastly, the analyst also suggested that projects “aligned with broader financial trends,” including stablecoins and real-world asset tokenization, as well as AI agents, which he believes could be a “major growth area.”

Market Shifts Push Investors Toward Utility and Revenue

Ju’s take reflects a wider change in crypto markets, with the speculative sectors that dominated past cycles currently struggling for traction. For instance, data recently published by CryptoRank showed that meme coins, which once boasted a collective market cap north of $135 billion, have seen their value shrink to just $24.5 billion in the last two years, with the sector falling by about 31% this year alone.

Meanwhile, according to the on-chain technician, there’s been growing interest in stablecoins and tokenized stocks, sectors which, in his view, are showing where blockchain technology can support actual business activity rather than just speculative trading.

The post Analyst Identifies 3 Altcoin Sectors Positioned to Survive Market Shakeout appeared first on CryptoPotato.

The US House and Senate have reached an agreement on a housing package that includes a ban on the Federal Reserve creating a central bank digital currency (CBDC) until the end of 2030, according to an updated bill text released by bipartisan lawmakers on Tuesday. The deal also addresses housing affordability and would block institutional investors from buying existing single-family homes to rent them out.

The updated version of the 21st Century Road to Housing Act will now move back to the House for consideration after the Senate added additional amendments. House Republican leaders are expected to put the measure to a vote after members return from recess on June 23, two people familiar with the plan told Politico.

Key takeaways

- The housing bill would restrict the Federal Reserve from issuing or creating a CBDC (or a substantially similar digital asset) until Dec. 31, 2030.

- The restriction includes a stated carveout for certain dollar-denominated stablecoins that are described as open, permissionless, and private.

- The Senate and House versions previously differed; the Senate’s added amendments must be approved by the House before final passage.

- Backers expect the agreement to advance quickly, potentially freeing Congress to focus on other crypto-related legislation, including the proposed CLARITY Act.

- The CBDC language revives concepts similar to an earlier House-passed “Anti-CBDC Surveillance State Act.”

How the CBDC ban ends up inside a housing bill

A bipartisan group of House and Senate leaders released updated bill text on Tuesday, launching the next stage of the 21st Century Road to Housing Act’s path to a final vote. As in earlier versions, the measure includes a CBDC prohibition aimed at limiting federal experiments with central-bank-issued digital money.

The CBDC ban was first added after the Senate passed the amendment in March, and the House supported its own version in May. But the two chambers could not immediately reconcile differences, leaving the bill in limbo. The new agreement reflects the latest round of negotiations, with Senate amendments now requiring House approval.

Crypto advocates have criticized CBDCs for what they view as the potential for government-controlled financial infrastructure and surveillance concerns—criticisms that have helped shape years of congressional pushback against standalone CBDC proposals.

What the law would actually restrict

The housing package’s CBDC language states that the Federal Reserve may not, directly or indirectly, “issue or create a central bank digital currency or any digital asset that is substantially similar to a central bank digital currency.” The provision is time-limited and would expire on Dec. 31, 2030.

Importantly for market participants, the clause includes a carveout for specific stablecoins—described as “dollar-denominated currency that is open, permissionless, and private.” That wording matters because it suggests the bill’s authors are drawing a boundary between central-bank-issued digital currency and privately issued stablecoins that meet the bill’s stated attributes.

In practical terms, the decision to embed this restriction in a housing bill may influence the bill’s momentum: housing legislation typically attracts broader coalitions than narrow crypto bills, potentially giving CBDC opponents a more workable legislative vehicle.

Connections to earlier CBDC proposals

The clause in the updated bill “revives much of the language” from Republican Rep. Tom Emmer’s Anti-CBDC Surveillance State Act, which was introduced in June 2025 and passed by the House the following month—but did not advance in the Senate.

That history highlights a key tension in Washington’s approach: even when House support for CBDC limits is strong, Senate action has been less predictable. By folding CBDC language into a broader measure, the current bill may sidestep some of that earlier gridlock.

The broader policy pressure also follows executive action. US President Donald Trump signed an executive order in January 2025 directing federal agencies to avoid work related to CBDCs, arguing the technology would threaten “the stability of the financial system, individual privacy, and the sovereignty of the United States,” as described in the order published by the White House.

What happens next for Congress and the crypto policy agenda

Lawmakers expect the housing bill to pass quickly once the House considers the Senate’s updated amendments. If House leadership proceeds on the June 23 timeline mentioned by Politico, the legislation could clear the final procedural hurdle before the August recess and the November midterm elections.

That timing may also shape what comes next on crypto regulation. The agreement is expected to allow Congress to devote attention to other proposals, including the CLARITY Act, which many lawmakers have pushed to advance. While the housing bill focuses on CBDCs and housing affordability, a separate regulatory framework would determine how the industry is supervised in the absence of a CBDC.

For investors and builders, the immediate watch-items are procedural: whether the House adopts the Senate’s amendments without further changes, and how the carveout for “open, permissionless, and private” dollar-denominated stablecoins is interpreted once lawmakers move from text to implementation.

Until the final vote and any subsequent clarification, market participants should also monitor whether the time-limited nature of the ban—ending at Dec. 31, 2030—affects planning for any future central-bank digital currency efforts, including how regulators and policymakers might revisit the question after the expiration date.

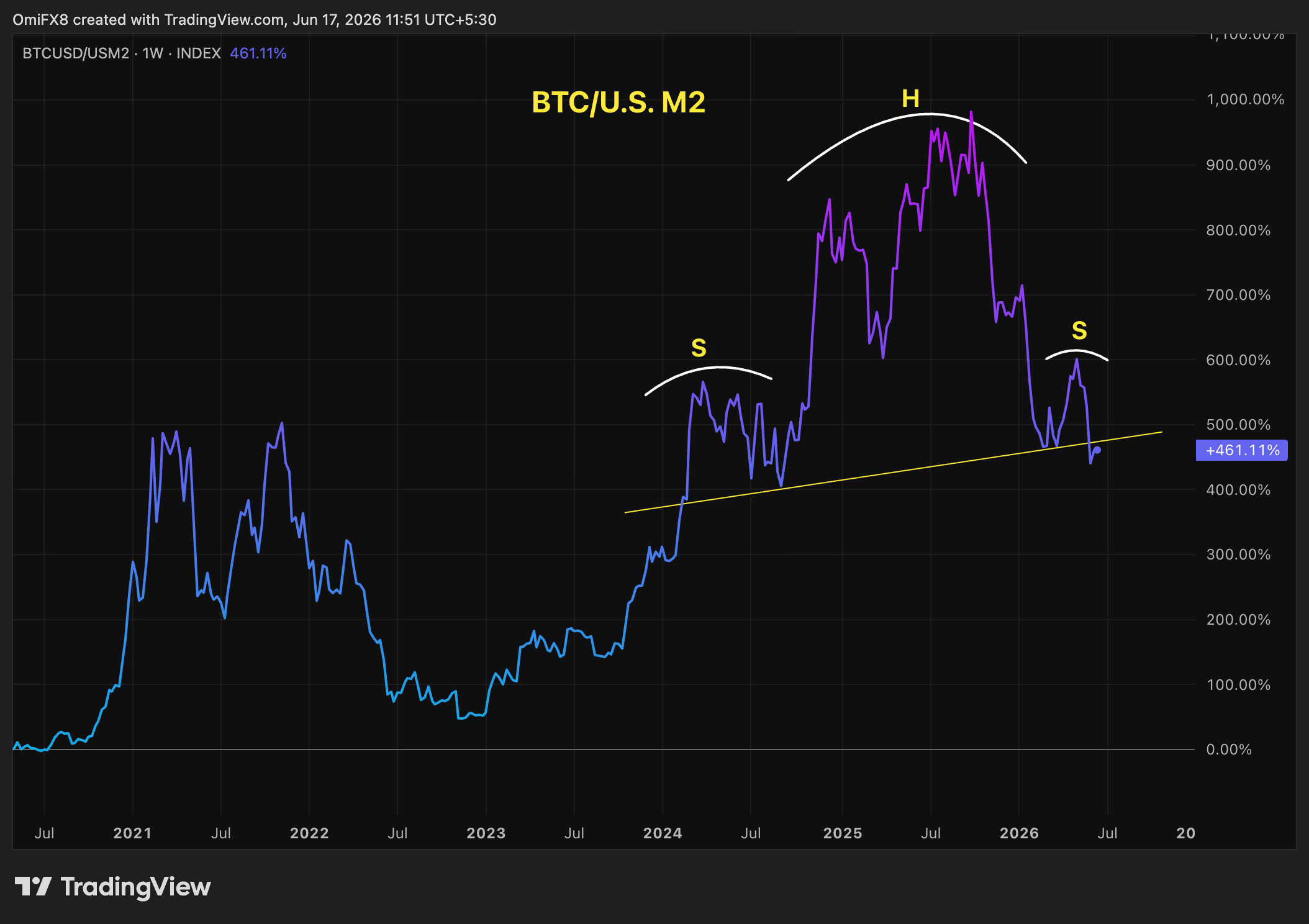

If you’re only looking at the dollar price of your portfolio, you may be missing part of the picture, which is significantly shaped by money supply growth.

To the casual observer, the markets look like business as usual. While bitcoin has nearly halved to $66,000 since its $126,000 peak in October of last year, the decline could be dismissed as just another brutal, quadrennial crypto bear market. Meanwhile, the S&P 500 continues to hover near record highs.

But beneath the surface, a more interesting signal emerges when both prices are adjusted for the U.S. M2 money supply. M2 is the Federal Reserve’s estimate of liquid assets, including cash on hand, money deposited in checking and savings accounts, and other short-term saving vehicles such as money market funds and certificates of deposit.

Monetary exhaustion?

Some observers see bitcoin as a high-beta barometer for dollar liquidity, and the BTC/M2 ratio, bitcoin’s price adjusted for money supply growth, is now flashing a warning. The ratio, after a sharp climb from 2023 through 2025, appears to have formed what technical analysts call a head-and-shoulders pattern, typically read as a bearish signal.

If the pattern holds, it would suggest bitcoin’s exponential edge over money supply growth — the dynamic that let it outrun debasement so convincingly in prior cycles — is fading. Bitcoin’s ability to outpace the flood of new dollars may be approaching diminishing returns, at least for now.

Eligible businesses may also continue to evaluate or pursue their own MiCA-focused crypto asset service provider (CASP) licenses in parallel while integrating BitGo Europe’s infrastructure, BitGo said.

The final deadline for crypto firms to have transitioned to the MiCA regime is the end of this month, a regulatory reckoning that will force some firms to close down their businesses.

Industry estimates suggest that Europe had more than 3,000 registered crypto firms as of 2024, with Poland alone accounting for over 1,400 registrations. As of May 2026, there are 194 authorised CASPs (including credit institutions) and it is expected that around 75% of the pre-MiCA population will lose registration status as transitional periods expire, according to law firm Hogan Lovells.

Belshe said firms don’t need to go bust because of MiCA’s regulatory requirements, adding that regulators are aware of BitGo’s compliance-enhancing infrastructure offering. In terms of fees for the crypto compliance service, Belshe said it’s relatively cheap and varies product by product.

“There’s some amount of monthly minimum that you pay similar to what’s always been there. That’s a couple of $1,000 a month type of thing that can scale with volume,” he said. “Then clients can either go to variable-based plans, where they’re paying per transaction more, or they can use static-based plans, where they have kind of a fixed fee, and they pay less.”

Why Fertilizer Stocks Didn’t Sell Off on Iran Peace Deal Announcement

‘Andy Burnham Has The Chance To Transform Britain By Closing The Respect Gap’

Microsoft working on Defender patch for RoguePlanet zero-day

Is Cain Dingle leaving Emmerdale and does he die? | Soaps

-

Business3 days ago

Business3 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Crypto World6 days ago

Crypto World6 days agoOppenheimer backs SpaceX as $70 billion retail frenzy builds

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoMarkets Rally as SpaceX IPO Looms Amid Iran Tensions and Inflation Surge

-

Crypto World2 days ago

Zimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Tech4 days ago

Tech4 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Tech5 days ago

Tech5 days agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

Crypto World4 days ago

Crypto World4 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Tech6 days ago

Tech6 days agoDutton Ranch star claims they ‘didn’t see any disruption’ on set following Chad Feehan’s exit from Yellowstone spinoff fueled by Taylor Sheridan clash rumors

-

NewsBeat5 days ago

NewsBeat5 days agoEl Nino has formed in the Pacific and could set records, forecasters say

-

Tech7 days ago

Tech7 days ago‘This is Seattle’s position on AI’: City Council votes unanimously to pause big new data centers

-

Politics6 days ago

Politics6 days agoPolitics Home | Healey Resignation Is “Colossal Failure Of Government”, Says Former Labour Defence Secretary

-

Entertainment6 days ago

Entertainment6 days agoDonnie Wahlberg & More Heat Up Las Vegas at Circa’s Barry’s Downtown Prime

-

Tech6 days ago

Tech6 days agoOpendoor Ends India Operations, Fueling a Bigger Conversation About AI and Outsourcing

-

Sports6 days ago

Sports6 days agoFirst Time Since 1971: Australia Register Historic Low In ODI Cricket

-

Politics6 days ago

Politics6 days agoBelfast burns, while Met chief points finger at Iran and Russia

-

Business6 days ago

Business6 days agoAT&T: Verizon's 27% Outperformance Sets Up A Solid Entry Point

-

NewsBeat5 days ago

NewsBeat5 days agoFBI searches office of Ohio voter registration group

-

Tech5 days ago

Tech5 days agoAnthropic is spending $150M to embed 1,000 AI fellows inside nonprofits. No degree required.

-

Politics6 days ago

Politics6 days agoModi thanks Trump for wishes as US attacks Indian seafarers

You must be logged in to post a comment Login