Crypto World

What is proof of reserves? How exchanges prove they hold your crypto

After FTX vanished with billions in customer money, “proof of reserves” became the phrase every exchange started using. This guide explains what it really proves, what it quietly leaves out, and how to tell a meaningful attestation from a marketing badge.

Summary

- Proof of reserves lets crypto exchanges verify on chain holdings against customer liabilities instead of relying only on trust.

- Merkle trees and zero knowledge proofs help exchanges prove customer balances are included without exposing private account data.

- Proof of reserves improves transparency but cannot fully confirm off chain obligations or guarantee long term solvency.

Proof of reserves is a cryptographic method an exchange uses to show that it actually holds the crypto assets its customers have deposited, by publishing verifiable evidence of its on-chain holdings and, in the stronger versions, matching them against what it owes. The first sentence of that definition is the part exchanges love to advertise. The second part, the matching against what it owes, is the part that separates a genuine solvency proof from a reassuring graphic, and it is where most of the difficulty lives.

The idea moved from a niche cryptographic curiosity to an industry standard almost overnight in late 2022, when FTX, one of the largest exchanges in the world, collapsed and revealed an estimated eight-billion-dollar hole between what it claimed to hold and what it actually had. In the panic that followed, every surviving exchange rushed to prove it was not the next FTX, and “proof of reserves” became the phrase they reached for. This guide explains what proof of reserves is, how the cryptography works, what a credible implementation looks like, the serious limitations every user should understand, and how to read an exchange’s attestation without being lulled by a green checkmark.

The reason this matters is simple and uncomfortable. When you deposit crypto on a centralized exchange, you generally do not hold those coins yourself; the exchange holds them and owes them back to you, exactly as a bank holds your deposit. That arrangement works only if the exchange truly has the assets, keeps them separate from money it gambles or lends, and can return them on demand. FTX proved that an exchange can claim all of this while secretly using customer funds to plug losses elsewhere, and that by the time the truth surfaces, the money is gone.

Proof of reserves is the industry’s attempt to make that kind of fraud detectable in advance, by replacing “trust us” with “verify it yourself.” Whether it succeeds depends entirely on how it is done, and the gap between the strong and weak versions is the most important thing this guide will teach you.

The problem proof of reserves is trying to solve

To understand proof of reserves, start with what an exchange actually is from a financial standpoint. A centralized exchange custodies assets on behalf of millions of users, pooling them in wallets it controls. Your balance on the screen is not a coin with your name on it; it is an entry in the exchange’s database, a promise that the platform owes you that amount and will pay it when you withdraw. As long as everyone does not ask for their money at once, and as long as the exchange truly holds what it owes, the system runs smoothly.

The danger appears when an exchange quietly spends, lends, or loses customer assets while still showing full balances on screen. Users see numbers that look real, but the coins behind them are gone, and the shortfall stays hidden until a wave of withdrawals exposes it.

This is precisely the failure FTX embodied. It took customer deposits and funneled them to an affiliated trading firm, which lost them, while customer account balances continued to display as though the money were safe. When users tried to withdraw en masse, the exchange could not pay, and the missing billions came to light only in the collapse. The episode burned a lesson into the industry: an exchange’s own assurances are worthless, because a fraudulent or insolvent platform will keep claiming everything is fine right up until it implodes.

What users needed was a way to check, independently and cryptographically, that an exchange held the assets it claimed, without having to trust the exchange’s word or wait for an auditor’s annual report. Proof of reserves was the answer the industry converged on, a mechanism designed to make solvency, or its absence, visible to anyone willing to verify, ideally before a platform fails rather than after.

The two halves: assets and liabilities

The single most important concept in proof of reserves is that real solvency requires proving two separate things, and that an exchange holds enough assets is only one of them. The first half is proof of assets: showing that the exchange controls a certain quantity of crypto in its wallets. This is the easier half, because blockchains are public. An exchange can point to its wallet addresses and let anyone see the balances on-chain, or it can cryptographically sign a message from those addresses to prove it controls them. Either way, the assets side is relatively straightforward to show, because the blockchain itself is the evidence.

The second half is proof of liabilities: showing the total amount the exchange owes to all of its customers combined. This is the hard half, and it is the half that weak implementations skip. Without knowing the total liabilities, proving assets means nothing, because solvency is a comparison. An exchange holding one billion dollars of crypto looks healthy until you learn it owes customers two billion, at which point it is catastrophically insolvent. Proof of assets alone tells you what is in the vault; only proof of liabilities tells you whether what is in the vault is enough.

A complete proof of reserves therefore pairs the two: it shows that total assets held are greater than or equal to total customer liabilities, which is the actual definition of solvency. When an exchange publishes a glossy page showing its wallet holdings but says nothing rigorous about what it owes, it has proven assets and called it solvency, and that substitution is the most common way the term gets watered down into marketing.

How Merkle-tree proof of reserves works

The clever cryptography in proof of reserves is mostly on the liabilities side, because proving what an exchange owes without exposing every customer’s private balance is the genuinely hard problem. The standard tool is a structure called a Merkle tree. Picture every customer’s balance as a leaf at the bottom of a tree. Each leaf is hashed, meaning run through a one-way cryptographic function that turns it into a fixed string of characters.

Pairs of hashes are then combined and hashed again, level by level, climbing the tree until everything condenses into a single hash at the very top called the Merkle root. That root is a compact fingerprint of every balance in the system at once, and crucially, changing any single balance anywhere in the tree would change the root entirely.

The exchange publishes the Merkle root, which represents its total customer liabilities, along with the total asset figure, ideally verified by a third party. Each individual user can then independently confirm that their own balance was included in the calculation. The exchange gives the user the specific branch of hashes connecting their leaf to the root, and the user can recompute the path and check that it produces the published root. If it does, the user has proven their balance was counted in the total, without the exchange ever revealing anyone else’s balance.

The privacy is the point: the Merkle tree lets the exchange prove a true, complete total of what it owes while keeping each customer’s individual figure hidden from everyone else. If enough users perform this check and find themselves correctly included, the published liability total becomes credible, and it can be compared against the proven assets to assess solvency. The catch, which we will return to, is that this only works well if users actually perform the check and if the asset side is honestly and independently verified.

The zero-knowledge upgrade

The basic Merkle-tree approach has a subtle weakness that more advanced systems have moved to close. To fully trust the liability total, you ideally want assurance that the exchange did not cheat in constructing the tree, for instance by sneaking in fake negative balances to make its total liabilities look smaller than they really are, or by excluding certain accounts. The plain Merkle tree proves your balance is included, but it does not, on its own, prove that every entry in the tree was non-negative and that the math behind the total was honest. A sophisticated exchange could, in principle, manipulate the construction in ways an ordinary user checking a single branch would not catch.

The fix that leading exchanges have adopted is to layer a zero-knowledge proof on top of the Merkle tree, using a cryptographic technique called a zk-SNARK. A zero-knowledge proof lets one party prove a statement is true without revealing the underlying data. Applied to proof of reserves, a zk-SNARK can prove that every user balance in the tree was included, that no balance was negative, and that the total was computed correctly, all without exposing any individual balance or even aggregate patterns.

The exchange proves, in effect, “the sum of all real, non-negative customer balances equals this published number, and here is mathematical proof we did not fake it,” and anyone can verify that proof. The founder of Ethereum publicly proposed exactly this kind of zk-SNARK enhancement as the right way to do proof of reserves, and major exchanges now run zk-SNARK systems atop their Merkle trees. This is the current state of the art on the liabilities side: a privacy-preserving, tamper-evident proof that the total owed is honest and complete.

The limitations every user must understand

Even the most sophisticated proof of reserves has serious limitations, and understanding them is what separates an informed user from someone soothed by a checkmark. The first and most damning is the snapshot problem. Proof of reserves captures a single moment in time. An exchange short on assets could borrow funds, perhaps from another exchange or a lender, hold them just long enough to pass the snapshot, prove healthy reserves, and return the borrowed money the next day. The proof would be technically accurate and completely misleading, because the assets were never really there outside the photographed instant. Frequent or continuous proofs reduce this risk but do not eliminate it, and many exchanges publish only periodically.

The second limitation is that proving assets does not prove they are unencumbered. An exchange can genuinely hold the coins it shows while having secretly borrowed them, pledged them as collateral, or owing them to a third party. The blockchain shows the coins sitting in the wallet; it does not show the hidden loan agreement that means those coins are not really free to cover customer withdrawals. The third limitation is the liabilities honesty problem already noted: a proof of assets with no rigorous, independently verified proof of liabilities is not a solvency proof at all, and many advertised implementations stop at assets.

Fourth, off-chain assets and obligations sit entirely outside the blockchain’s view, so an exchange holding fiat currency, real-world assets, or off-chain debts cannot have those captured by an on-chain proof. The honest summary is that proof of reserves can show an exchange has assets at a moment, but it struggles to prove those assets are sufficient, unencumbered, continuously present, and matched against an honest accounting of everything owed. It is a meaningful check, not a guarantee.

Why auditors and skeptics both have a point

Because the cryptography alone cannot close every gap, third-party auditors have become central to credible proof of reserves, and their role is both valuable and contested. An independent auditor or specialized verification firm can examine an exchange’s wallets, confirm control of the assets, review the liability construction, and attest that, at the time examined, assets exceeded liabilities by some margin. Several firms now perform this work, publishing reserve ratios for exchanges that show assets comfortably above liabilities, figures above one hundred percent meaning the exchange holds more than it owes. Some exchanges go further, combining independent accountant reviews with user verifiable identifiers so individuals can confirm their own inclusion. This blend of cryptographic proof and human attestation is currently the strongest form of assurance an exchange can offer short of full, traditional financial audits.

Yet skeptics raise a point worth taking seriously, and it is best captured by the prominent executive who refused to publish proof of reserves for his own company’s holdings, calling it a bad idea. His argument was not that hiding assets is good, but that proof of reserves as commonly practiced can mislead: it can create a false sense of security by proving assets while saying little verifiable about liabilities, off-chain obligations, or whether the assets are encumbered, and a sophisticated bad actor can satisfy the letter of a proof while remaining insolvent in substance. The skeptics and the auditors are, in a sense, both right. Proof of reserves done well, with honest liabilities, independent attestation, and frequent snapshots, is a real improvement over the pre-FTX world of pure blind trust. Proof of reserves done poorly, as a one-time assets-only graphic, can be worse than nothing if it lulls users into a confidence the proof does not actually earn. The technique is a tool, and like any tool it can be wielded honestly or as theater.

A cautionary tale that proves the point

The limitations are not hypothetical, and a fresh example shows exactly how a proof-of-reserves regime can fail in practice. In early 2026, an investigation by an on-chain forensics firm revealed that a European exchange’s main Bitcoin holding wallet had collapsed from around fifty-six Bitcoin to a fraction of a single coin, a drop of more than ninety-nine percent, even as the platform continued to assure users it was solvent.

Tens of thousands of customers were potentially affected, and observers described it as one of the most significant European exchange failures since FTX itself. The episode landed as a direct reminder that an exchange claiming solvency, and even one gesturing at reserves, can be hollow underneath, and that the gap between a public claim and verifiable on-chain reality is exactly where users lose money.

The lesson is not that proof of reserves is useless; it is that the quality and continuity of verification are everything. Had that exchange’s reserves been continuously proven, independently audited, and matched against honestly constructed liabilities, the draining of its main wallet would have been visible to anyone watching, and users could have withdrawn before the collapse rather than after. Instead, the assurance was a claim rather than a living, verifiable proof, and the on-chain reality diverged catastrophically from the story being told.

This is the practical case for treating proof of reserves as a process to scrutinize instead of a badge to trust. A meaningful proof is recent, frequent, independently attested, and covers both halves of the solvency equation. A claim of solvency with none of that behind it is precisely the kind of reassurance that history keeps showing to be worthless at the worst possible moment.

Proof of reserves versus a real audit

A point of confusion worth clearing up is the difference between proof of reserves and a traditional financial audit, because exchanges sometimes blur the two and they are not the same thing. A full audit, of the kind applied to a public company, examines far more than whether assets exceed liabilities at a moment. It scrutinizes the quality and ownership of those assets, whether they are encumbered or pledged, the accuracy of the books over a period instead of a snapshot, the internal controls that govern how money moves, the company’s other obligations and debts, and the truthfulness of management’s representations, all signed off by an accountable auditing firm that stakes its reputation and faces legal consequences for getting it wrong.

Proof of reserves, even in its strongest cryptographic form, does much less: it shows on-chain assets and, ideally, customer liabilities at a point in time, but it does not examine the off-chain business, the encumbrances, the controls, or the conduct of management.

This gap matters because the marketing around proof of reserves can imply a level of assurance closer to a full audit than the technique actually provides. An exchange can truthfully say it published a proof of reserves while its off-chain finances, its corporate debts, its commingling of funds, or its risky lending remain entirely unexamined. The early scramble after the FTX collapse made this gap vivid: some auditing firms that had begun providing proof-of-reserves attestations stepped back from the work, wary of the reputational risk of appearing to vouch for an exchange’s overall solvency when their procedures covered only a narrow, point-in-time slice.

The lesson is not that proof of reserves is dishonest, but that it occupies a specific and limited place. It is a cryptographic check on a particular question, do the on-chain assets cover the customer liabilities right now, and it is truly useful for that. It is not a substitute for the comprehensive, ongoing, accountable scrutiny that a real audit provides, and an exchange that has only published a proof of reserves has not been audited in the full sense, however much the language might suggest otherwise.

The practical upshot is to hold two ideas at once. Proof of reserves is a meaningful advance over the pre-FTX world, in which users had nothing but blind faith, and a strong, frequent, independently attested, two-sided proof truly lowers the risk of a hidden insolvency. At the same time, it is a narrow instrument that cannot see the off-chain obligations, the encumbrances, or the management conduct that have featured in many exchange failures.

The most informed users treat a credible proof of reserves as one positive signal among several, alongside an exchange’s regulatory standing, its track record, its transparency, and the protections of the jurisdiction it operates in, instead of as a complete verdict on safety. Combining the cryptographic check with these other signals, and keeping meaningful holdings in self-custody, is the realistic way to manage exchange risk, because no single proof, however clever, captures everything that can go wrong.

How to read an exchange’s proof of reserves

Putting it together, here is how to evaluate any exchange’s proof of reserves instead of taking the headline at face value. First, check whether it proves liabilities, not just assets. A page showing only wallet balances is proof of assets, and on its own it tells you nothing about solvency, because you cannot see what the exchange owes. Look for a Merkle-tree liability commitment, ideally strengthened by a zero-knowledge proof, and the ability to verify your own balance’s inclusion. Second, check for independent attestation.

A reserve ratio confirmed by a reputable third party carries far more weight than a self-published graphic, because it means someone with professional accountability examined the wallets and the liability construction instead of the exchange grading its own homework.

Third, check recency and frequency. A proof from many months ago tells you little about today, and a single annual snapshot is easy to game with borrowed funds; frequent or continuous proofs are far harder to fake. Fourth, keep the structural limitations in mind even when all of the above is present: a proof cannot easily show that assets are unencumbered, cannot capture off-chain obligations, and cannot guarantee the assets stay there after the snapshot. The most important practical takeaway sits above all the cryptography.

Proof of reserves reduces the trust you must place in an exchange, but it does not eliminate it, and the only way to remove custody risk entirely is to hold your own keys in self-custody, where no exchange stands between you and your coins. For assets you do keep on an exchange, favor platforms with frequent, independently audited, two-sided proofs, treat assets-only graphics with skepticism, and remember the lesson FTX taught at great cost: an exchange will keep telling you everything is fine right up until it is not, so verification, not reassurance, is what protects you.

Frequently Asked Questions

What is proof of reserves in simple terms?

Proof of reserves is a way for a crypto exchange to show, with verifiable evidence instead of just its word, that it actually holds the assets customers have deposited. In its strong form it proves two things: that the exchange controls a certain amount of crypto in its wallets (proof of assets), and that this amount is greater than or equal to everything it owes customers (proof of liabilities). Together those show solvency. It became an industry standard after the FTX collapse in late 2022 revealed an estimated eight-billion-dollar gap between claimed and actual reserves.

How does proof of reserves actually work?

The asset side is shown using the blockchain itself, since an exchange can reveal its wallet holdings or cryptographically sign messages proving it controls them. The liability side uses a Merkle tree: every customer balance is hashed and combined upward into a single fingerprint called a Merkle root, which represents the total owed. Each user can verify their own balance was included without seeing anyone else’s. Leading exchanges add a zero-knowledge proof (a zk-SNARK) on top to prove no balances were negative or omitted and the total is honest, all without exposing individual figures.

What are the main weaknesses of proof of reserves?

Several. It is a snapshot, so an exchange could borrow assets briefly to pass the check and return them afterward. It does not prove the assets are unencumbered, meaning they could be secretly borrowed or pledged as collateral. Many implementations prove only assets and skip a rigorous, independently verified proof of liabilities, which means they do not actually prove solvency. And it cannot capture off-chain assets or obligations. So proof of reserves is a meaningful check but not a guarantee that an exchange is truly solvent and safe.

Why did some people refuse to publish proof of reserves?

A prominent executive declined to publish proof of reserves for his company’s holdings, arguing it is a bad idea because it can mislead. The concern is that an assets-only proof creates false confidence: it can show coins in a wallet while saying nothing verifiable about liabilities, off-chain debts, or whether the assets are encumbered, and a sophisticated bad actor can satisfy the surface of a proof while remaining insolvent underneath. The point is not that hiding assets is good, but that a weak proof of reserves can be worse than none if it lulls users into unearned trust.

Does proof of reserves mean my money is safe on an exchange?

Not by itself. A strong, frequent, independently audited, two-sided proof of reserves meaningfully reduces the risk that an exchange is secretly insolvent, which is real protection. But no proof can guarantee the assets stay there after the snapshot, that they are unencumbered, or that off-chain obligations are covered. The only way to remove exchange custody risk entirely is self-custody, holding your own private keys so no platform stands between you and your coins. For assets kept on an exchange, prefer platforms with credible, recent, two-sided proofs, but do not treat any proof as an absolute guarantee.

How can I tell a credible proof of reserves from marketing?

Check four things. Does it prove liabilities, not just assets, with a Merkle-tree commitment and ideally a zero-knowledge proof, plus the ability to verify your own balance? Is it independently attested by a reputable third party instead of self-published? Is it recent and frequent instead of a stale annual snapshot? And does the explanation acknowledge the limitations instead of implying total safety? A two-sided, independently audited, frequently updated proof is credible. An assets-only graphic with no liability proof, no third party, and an old date is closer to a marketing badge than a solvency proof.

This article is educational information, not financial or investment advice. Exchange practices, reserve ratios, and verification methods change, and figures reflect reporting available as of June 25, 2026. Always confirm an exchange’s current proof-of-reserves details from primary sources, and remember that self-custody is the only way to fully remove exchange custody risk.

TLDR

- BlackRock transferred 3,410 BTC and 5,132 ETH to Coinbase Prime.

- The combined value of the transfers reached approximately $217 million.

- Bitcoin transfers accounted for about $209.64 million of the total value.

- Ethereum transfers were valued at approximately $8.43 million.

- Lookonchain tracked the transactions across multiple blockchain transfers.

BlackRock transferred another $217 million worth of Bitcoin and Ethereum to Coinbase Prime on June 25. The transactions followed continued ETF outflows across both products and renewed attention on the asset manager’s blockchain activity. Lookonchain tracked the transfers, while BlackRock did not disclose the purpose behind the deposits.

BlackRock Moves Bitcoin and Ethereum to Coinbase Prime

Lookonchain reported that BlackRock deposited 3,410 BTC and 5,132 ETH to Coinbase Prime through several transactions. The transfers carried an estimated value of $209.64 million in Bitcoin and $8.43 million in Ethereum. The movement occurred on Thursday, June 25.

Blockchain data showed about seven transfers during the operation. Nearly every Bitcoin transaction moved 300 BTC to Coinbase Prime. One separate transaction carried the Ethereum holdings to the same platform.

Market participants linked the transfers with recent ETF withdrawals because similar activity appeared during previous outflow sessions. However, BlackRock did not issue a statement explaining the latest deposits. The company also provided no public update regarding the destination of the transferred assets.

Exchange deposits often attract attention because they can precede trading activity. However, blockchain transfers alone do not confirm that an asset manager has sold any holdings. The available on-chain data only confirms the movement between wallets.

Bitcoin and Ethereum Transfers Follow ETF Withdrawals

The latest deposits arrived while both Bitcoin and Ethereum exchange-traded funds continued recording withdrawals. BlackRock has transferred digital assets to Coinbase Prime during earlier outflow periods. Those previous transactions also prompted market discussion about possible sales.

Some traders interpreted the latest deposits as preparation for another disposal of holdings. Others pointed out that Coinbase Prime supports institutional custody and settlement services. Therefore, wallet transfers alone cannot establish whether any sale occurred.

BlackRock has not confirmed any direct sale connected to the June 25 transfers. The company also has not addressed market speculation surrounding the transactions. As a result, only the blockchain records remain publicly available.

Lookonchain’s published wallet activity showed that the combined transfers reached about $217 million. Bitcoin represented most of the transferred value, while Ethereum accounted for a smaller portion. The deposits reached Coinbase Prime through multiple wallet movements.

Previous blockchain records showed similar transfer patterns during sessions with ETF redemptions. Those observations have contributed to continued discussion whenever BlackRock moves assets to Coinbase Prime. Still, no public filing connected the latest transfers to completed market sales.

The recorded transfers included 3,410 BTC and 5,132 ETH. Based on prices during execution, the combined value reached approximately $217 million. BlackRock has not released any further information regarding the June 25 wallet activity.

Jiang Zhuoer, one of China’s best-known Bitcoin (BTC) miners, sees the Bitcoin bottom landing between $42,000 and $44,000 in late 2026, closely matching Arthur Hayes’ recent $40,000 call.

The founder of mining pool BTC.TOP laid out the forecast in a post, building it on a bearish signal from Strategy’s stock, MSTR. His timing and target both land near the BitMEX co-founder’s.

Strategy’s mNAV Discount Echoes the 2022 Low

Jiang’s case rests on Strategy’s mNAV, which he pegs at 0.72. The metric weighs the stock against the Bitcoin the company holds per share. A reading under 1.0 leaves the firm valued below its own Bitcoin.

The level sits near the 0.7 trough from May 2022, the last time its mNAV collapsed this far. Jiang treats that as the signal, not the timer.

In that cycle, the mNAV bottomed in May with Bitcoin near $31,000. The price then kept sliding to about $15,650 by late November, as the FTX collapse deepened the rout. That gap ran about six months.

“But note that the mNAV low is not the BTC price low,” he added.

Follow us on X to get the latest news as it happens

His broader timing comes from a four-year cycle model, one he likens to a bouncing ball losing height. It points to a bottom around October 31, 2026.

Jiang, who has mined through several halving cycles, is already short and plans to buy back near the low.

Hayes Points to a Similar Bitcoin Bottom

Arthur Hayes reached a similar destination by a different route. The BitMEX co-founder laid out the call to content creator EllioTrades on June 12. He sees the Bitcoin bottom near $40,000 within six months.

The bet is tactical, not structural. Hayes holds put spreads as a hedge even as his core positions stay heavily long. His year-end target still runs above $200,000.

Bitcoin recently traded near $61,345, down 2.3% in 24 hours. Jiang’s range sits roughly 30% below that level, while Hayes’ $40,000 floor implies a drop closer to 35%.

Whether mNAV leads price by six months once more is the real test, and it will shape Bitcoin price forecasts heading into late 2026.

The post China’s Top Bitcoin Miner Suggests Arthur Hayes Is Right About BTC Bottom appeared first on BeInCrypto.

TLDR

- XRP Ledger validators warned users about fake JPYSC tokens using the stablecoin’s ticker.

- SBI launched JPYSC on June 24 through SBI VC Trade for account holders only.

- SBI has not confirmed any JPYSC issuance on the XRP Ledger or other public chains.

- JPYSC currently cannot move to external wallets or public blockchain networks.

- SBI said public-chain circulation is ready but still awaits tax and regulatory approval.

XRP Ledger (XRPL) validators warned users against fake JPYSC tokens after SBI launched its yen stablecoin. The alert followed claims about a possible XRPL issue. SBI has not confirmed any release.

XRP Ledger Community Flags Fake JPYSC Claims

XRPL validator Vet, Hussein Zangana, said SBI has made no public JPYSC issue on XRPL. Therefore, any current JPYSC ticker remains suspicious.

The warning followed the June 24 launch of JPYSC by SBI Holdings through SBI VC Trade. The launch drew attention because SBI has links with Ripple.

Another XRP community member said monitoring tools now track trustlines linked to known SBI addresses. Those systems could help detect official activity later.

Community checks focus on issuer addresses, trustlines, and token metadata on the XRP Ledger. However, validators said users need SBI confirmation before treating any asset as valid.

The alerts target scam tokens that may copy the JPYSC name or ticker. Such tokens can appear quickly on public ledgers because anyone can create assets.

Vet said JPYSC has received no public XRPL announcement from SBI. As a result, he urged users to verify sources before any interaction.

JPYSC Remains Limited to SBI VC Trade

SBI launched JPYSC as a yen stablecoin for SBI VC Trade account holders. SBI Shinsei Trust Bank issues the token, while SBI VC Trade distributes it.

The stablecoin came from a joint effort between SBI and Startale Group. It operates as a trust-type electronic payment instrument under Japan’s framework.

SBI said this structure removes the ¥1 million transaction cap applied to some payment products. The company presented JPYSC as a regulated yen stablecoin.

For now, SBI keeps JPYSC inside SBI VC Trade accounts. Users cannot withdraw the token to external wallets or blockchains.

SBI said it has completed technical and operational work for public blockchain circulation. Yet the company still awaits regulatory and tax treatment before transfers.

The company has not named any public chain for JPYSC deployment. Therefore, XRP Ledger links remain unconfirmed despite community speculation.

SBI Chairman and CEO Yoshitaka Kitao called blockchain migration in finance “irreversible.” He described JPYSC as part of Japan’s blockchain finance infrastructure.

Startale founder Sota Watanabe said external wallet transfers are technically ready. He said remaining issues relate mainly to regulation and tax rules.

No SBI statement has connected JPYSC to the XRP Ledger. Community members continue tracking issuer activity while warning users against fake tokens.

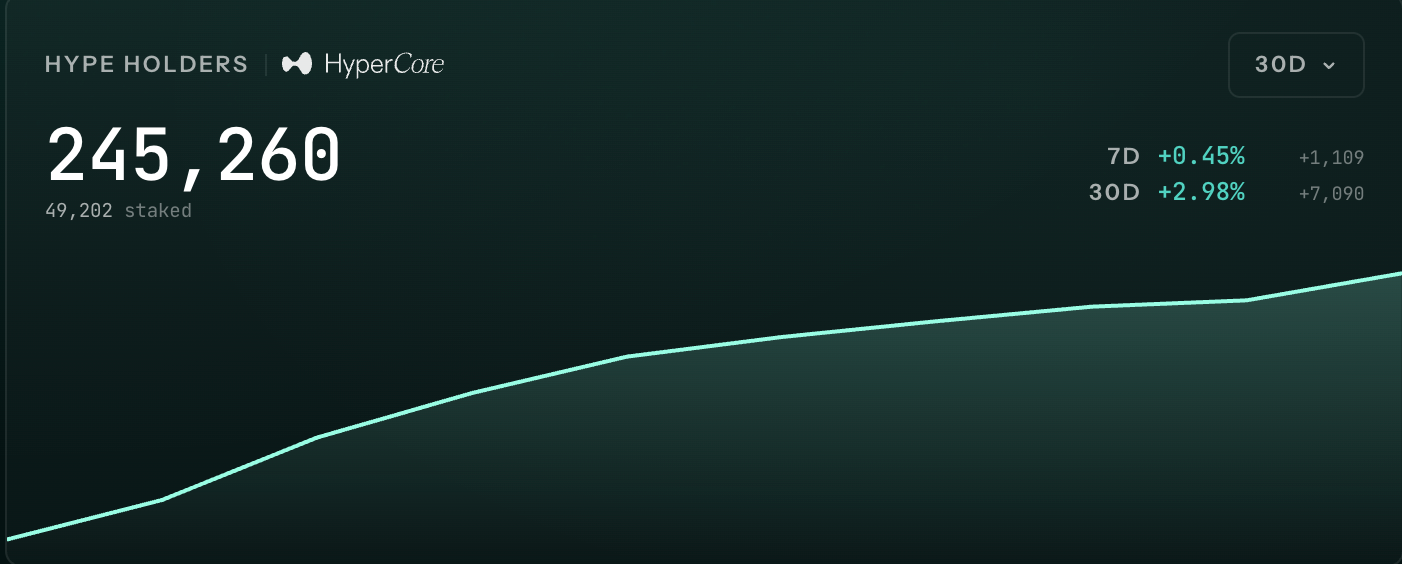

Hyperliquid (HYPE) has trended lower since hitting a record high, shedding 17% amid broader market weakness. Yet, the network behind it tells a steadier story.

Several on-chain and ecosystem metrics indicate that user participation and capital activity have remained resilient despite the recent price decline.

User Growth Continues Despite Price Weakness

Network activity increased even as HYPE moved lower. On-chain data showed that HyperCore daily active addresses rose 17.4% over the past 24 hours to 68,600.

The number of HYPE holders also expanded during the decline. Over the last seven days, wallet count increased by 1,109 addresses, or 0.45%, while the token fell 12.5%.

Follow us on X to get the latest news as it happens

Longer-term growth remained intact as well. Total holders reached 245,260 in June, up roughly 3% over the past month.

Capital trends also paint a different picture from the broader DeFi market. As BeInCrypto reported, DeFi total value locked (TVL) has declined every month in 2026, falling 39% overall.

Hyperliquid has been a notable exception. Alongside TRON, it was one of only two top-10 chains to record TVL growth this year, indicating that capital has continued flowing into the ecosystem despite the wider sector slowdown.

Revenue and Buybacks Support the Ecosystem

Meanwhile, an on-chain analyst noted that Hyperliquid repurchased $135 million of HYPE over 90 days, while $64 million was unlocked for the team.

The imbalance suggests that buy-side demand generated by the protocol has outpaced the additional supply entering the market from token unlocks, helping absorb potential selling pressure.

Protocol revenue backs the trend. DefiLama data shows revenue climbed for three consecutive months, rising from $44.85 million in April to $53.80 million in June.

It’s worth noting that gain is a recovery, not a record. April was the weakest month of 2026, while January revenue was nearly $63.94 million.

HYPE Demand Holds Despite a Broader Downtrend

Lastly, larger market participants remained active despite the correction. According to Lookonchain, a new wallet, 0x987f, withdrew 278,827 HYPE, worth approximately $17.45 million, from Coinbase Prime.

Meanwhile, whale address 0x2386 pulled 96,930 HYPE valued at roughly $6.01 million from BitGo after a month-long pause in activity.

Institutional interest has also remained positive. While spot Bitcoin and Ethereum ETFs have recorded continuous outflows in recent weeks, HYPE investment products attracted $27.9 million in inflows last week. This marked their strongest weekly inflow since late May, according to SoSoValue data.

Price and these signals now point in opposite directions. The coming weeks will test whether they pull HYPE back toward its record high. At press time, HYPE traded at $63.4, up 1.91% over the previous 24 hours.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post HYPE Drops 17% From Record High but Hyperliquid Fundamentals Remain Strong appeared first on BeInCrypto.

South Korea’s Personal Information Protection Commission (PIPC) has ordered cryptocurrency exchange Bithumb to pay a $136,000 fine after finding that the platform violated the country’s personal data protection rules by transferring user information overseas without obtaining separate consent.

In a notice published Thursday, the regulator said the breach occurred during Bithumb’s processes for sharing order books and transferring virtual assets with overseas exchanges. The PIPC’s findings place additional compliance pressure on major South Korean trading venues as authorities tighten both privacy and financial-crime controls.

Key takeaways

- The PIPC fined Bithumb $136,000 for transferring personal data abroad without separate consent during certain exchange-to-exchange operations.

- The regulator linked the violation to order book sharing and virtual asset transfers tied to overseas platforms.

- PIPC acknowledged that anti-money laundering (AML) needs can justify data provision, but said overseas personal data transfers still require strict adherence to legal procedures and the data subjects’ self-determination rights.

- Bithumb’s case comes amid heightened scrutiny from South Korean regulators and law enforcement, following past enforcement actions and reported raids.

PIPC’s rationale: AML use is not a blanket permission

According to the PIPC, Bithumb transferred personal information overseas in connection with order book sharing and virtual asset transfers involving foreign exchanges. The regulator concluded that the exchange handled personal data in a way that did not satisfy the consent and procedural requirements set out under South Korea’s Protection Act.

The notice also explained the logic of its decision. The PIPC said there is a necessity to provide personal information for AML purposes when transferring virtual assets to other exchanges. However, when it comes to overseas transfers of personal data, the PIPC emphasized that the data subject’s right to control their information must be respected through strict compliance with required procedures.

“As this is a closely related matter, it is necessary to strictly comply with the requirements and procedures stipulated in the Protection Act,” the PIPC said in its notice (translation).

The PIPC’s published decision is available on the regulator’s website.

Tether order-book sharing and overseas exchange data handling

While privacy regulators rarely disclose every operational detail in enforcement notices, the PIPC’s account connected Bithumb’s breach to specific activities. The regulator said the incident was related to Bithumb sharing Tether (USDT) order books with BingX between September and November 2025.

The PIPC noted that Bithumb had obtained consent to share data with Stellar, but the order-book sharing described in the notice involved an overseas exchange partner—where the regulator determined separate consent for the overseas personal data transfer was not obtained.

In addition to the order book-sharing matter, the PIPC said the violation also involved Bithumb sharing user information with 13 overseas exchanges. Taken together, the regulator’s framing suggests the problem was not limited to a single counterpart; rather, it reflected how personal data was handled across multiple foreign relationships during exchange operations.

Why this matters for South Korea’s crypto compliance landscape

South Korea has been one of the most actively regulated crypto markets in Asia, and enforcement actions have increasingly targeted more than just anti-money laundering. The PIPC’s decision underscores that exchanges operating locally must manage privacy obligations with the same rigor they apply to financial compliance.

For investors and market participants, the practical effect is straightforward: compliance failures can lead to fines and reputational damage, and repeated regulatory scrutiny can influence how quickly exchanges adapt their systems for data handling, third-party information sharing, and cross-border workflows.

Just as importantly, the PIPC’s reasoning draws a line between AML-related data sharing needs and what it described as the separate right of data subjects regarding self-determination. In other words, AML necessity does not automatically override consent and procedural safeguards when personal data crosses borders.

Bithumb under pressure amid broader enforcement and public attention

Bithumb is among the largest crypto exchanges in South Korea, and the PIPC fine adds to an already difficult regulatory environment for the platform.

Earlier, South Korea’s financial watchdog imposed a six-month suspension on Bithumb’s activities in March over alleged violations of the country’s Financial Information Act. A court later reversed that decision in April, but the history shows that Bithumb’s compliance challenges have been a recurring theme.

More recently, police reportedly raided Bithumb’s offices as part of an investigation into alleged nepotism involving South Korean lawmaker Kim Byung-gi. While that matter is separate from the PIPC’s personal data ruling, it contributes to the perception that the exchange remains at the center of multiple, overlapping investigations.

Related coverage in earlier reporting noted: Cointelegraph previously reported on the financial watchdog’s suspension decision (link).

South Korea crypto regulation isn’t slowing: taxes and law-enforcement upgrades

The fine arrives as other policy and enforcement developments continue to shape the South Korean crypto market. The country’s Finance Ministry confirmed in May that a 22% tax on cryptocurrency gains will be imposed starting in January 2027, after earlier timelines shifted away from an expected 2025 start. According to the Yonhap news agency, about 16 million South Koreans were invested in digital assets as of March 2025.

Separately, Chainalysis said it signed a memorandum of understanding with the Korean National Police Agency (KNPA) aimed at building investigative capability within South Korea’s law enforcement. Earlier coverage tied the pact to efforts to combat North Korea-linked crypto attacks, with police “at the forefront” of tackling these threats.

Earlier coverage mentioned: Cointelegraph reported on the Chainalysis and KNPA memorandum of understanding (link).

For traders, developers, and users, the combined picture is clear: compliance requirements in South Korea are broadening across privacy, taxation, and investigative capability—meaning operational choices like cross-border data sharing during exchange partnerships are now likely to be scrutinized more closely.

Going forward, market watchers should focus on how major exchanges revise consent management and cross-border data-transfer processes, and whether South Korean regulators publish additional guidance or enforcement actions that clarify how AML-driven data provision should be implemented alongside privacy protections.

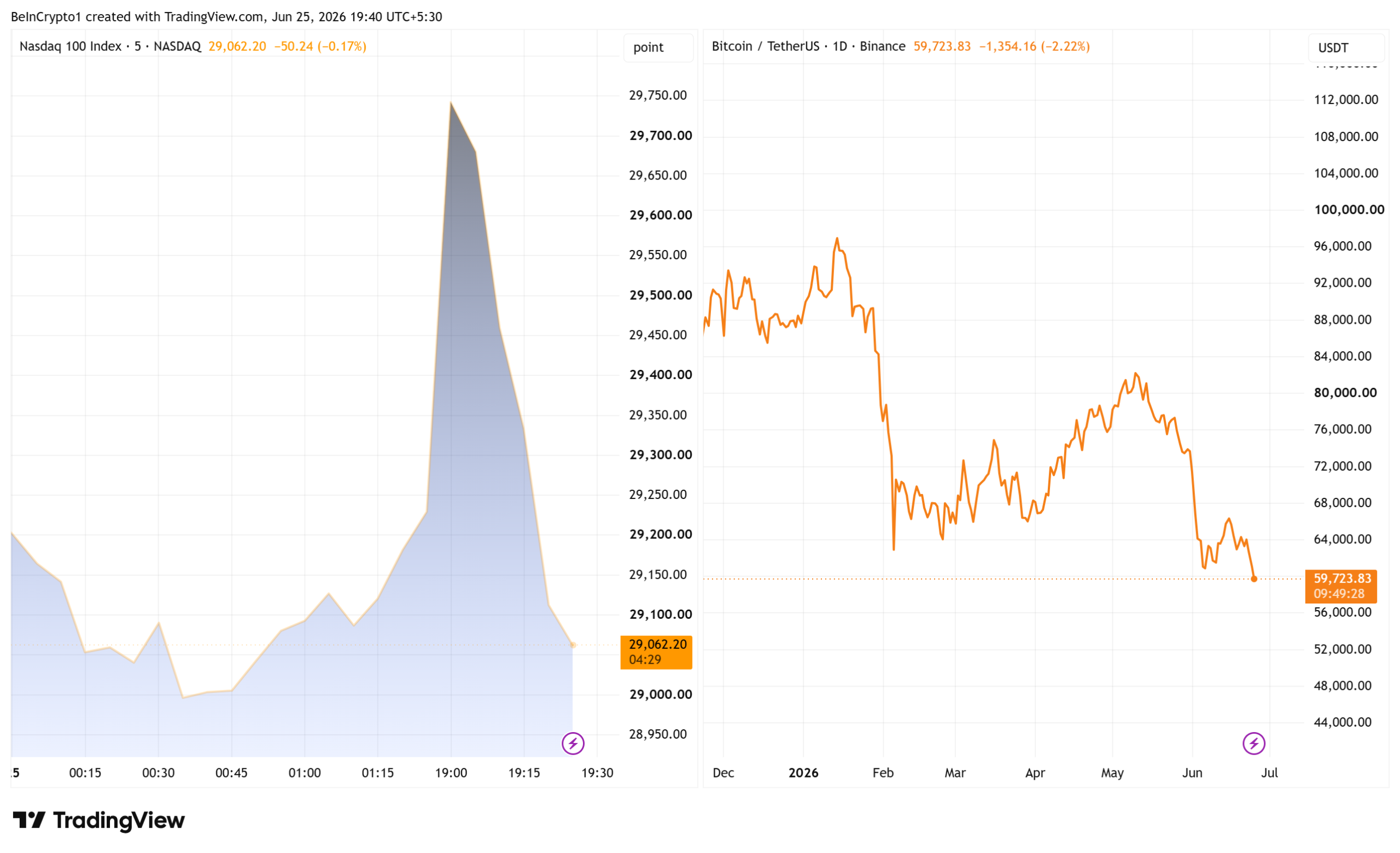

The Bitcoin (BTC) price fell to about $58,000 on Thursday, its lowest level since September 2024, after hotter US inflation dimmed hopes for near-term Federal Reserve rate cuts.

US stocks slid in tandem, with the Nasdaq 100 erasing an intraday rally. Both markets turned lower after the Fed’s preferred inflation gauge rose faster than expected in May.

Hot Inflation Dims Rate-Cut Hopes

The Personal Consumption Expenditures (PCE) price index rose 4.1% in May from a year earlier, its highest reading since April 2023. That was up from 3.8% in April, according to the government report. Core PCE, which strips out food and energy, climbed 3.4%.

The figures pointed to a resilient economy rather than a slowing one. Consumer spending rose 0.7% in May, above forecasts, while first-quarter gross domestic product was revised up to 2.1% from 1.6%. Some economists now see room for possible rate hikes instead of cuts.

Under Chair Kevin Warsh, the Fed held its benchmark rate at 3.5% to 3.75% in June and projected higher rates ahead. It tied part of the price pressure to energy supply shocks from the Middle East conflict. That stance has weakened Fed rate-cut hopes across markets, where traders had expected easing this year.

Follow us on X to get the latest news as it happens

Bitcoin Price Slide Mirrors Nasdaq Reversal

BTC had traded above $61,800 earlier in the session before the Bitcoin price decline accelerated. The token changed hands near $59,200 afterward, down about 2.6% on the day. That left it roughly 53% below its October 2025 record of $126,080.

The drop triggered a wave of forced selling. More than $450 million in leveraged long positions were liquidated within roughly an hour.

Across the market, total crypto liquidations reached $1.26 billion among more than 209,000 traders over 24 hours, according to Coinglass.

Crypto and tech stocks have tracked each other closely this year. The Nasdaq 100 had climbed before reversing, echoing a big tech selloff earlier in June that also dragged Bitcoin lower. \

Higher rates raise the cost of holding risk, weighing on both.

Whether $58,000 marks a floor may hinge on the Fed’s next meeting in late July. With inflation rising and growth steady, policymakers have little reason to cut. That leaves risk assets exposed to further swings.

The post PCE Inflation Shakes Markets: Nasdaq Rally Collapses, Bitcoin Falls to New 2026 Low appeared first on BeInCrypto.

Indonesia parliament just passed the revised crypto law, formally cementing OJK’s authority over crypto as a regulated financial asset just as Europe’s MiCA transitional window closes on July 1. Two of the world’s most consequential crypto jurisdictions are hardening their frameworks in the same month, from opposite sides of the globe.

The structural logic is identical: reclassify crypto from a peripheral asset into a supervised financial instrument, require licensing, and push non-compliant platforms out. The era of operating across major markets on thin regulatory registrations is closing simultaneously in Jakarta and Brussels.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Indonesia Crypto Law: OJK Gets Full Authority

The P2SK Law revision, passed by the Indonesia Parliament expands OJK’s mandate across banking, capital markets, fintech, and digital financial assets, consolidating supervisory authority that was previously fragmented between OJK, Bappebti, and Bank Indonesia. For crypto specifically, this completes a reclassification that tokens are no longer traded commodities sitting inside Bappebti’s commodity-futures perimeter.

OJK can now impose bank-style prudential requirements on exchanges, capital adequacy, custody segregation, governance standards, and conduct rules. The law also amends Indonesia’s Capital Markets Act to expand the definition of securities to include investment contracts in digital form that confer economic benefits, opening the door for certain tokens and DeFi instruments to fall under full securities regulation. That is a direct structural parallel to MiCA’s treatment of asset-referenced tokens.

— Nael (@nael_idrx) June 25, 2026

BREAKING: Indonesia Elevates Stablecoin and Digital Financial Assets to Statutory Recognition Under the P2SK Law

BREAKING: Indonesia Elevates Stablecoin and Digital Financial Assets to Statutory Recognition Under the P2SK Law

Indonesia has officially recognized and regulated digital financial assets under the Financial Sector Development and Strengthening Law (P2SK), placing them at… pic.twitter.com/gSsZrgP3W1

The immediate compliance pressure point governing governance and risk management for fintech innovation platforms, including digital asset providers, takes effect on July 1, 2026. Indonesian OJK crypto regulation now has its own hard deadline running in parallel with Europe’s. Exchanges operating in Indonesia crypto markets that have not completed their transition from Bappebti-era structures face an enforcement exposure window starting this month.

Tokocrypto CEO Calvin Kizana welcomed the revision but flagged the implementation gap that matters most to operators.

“We are also waiting and looking forward to the final draft being distributed to industry players so that they can see in more detail what changes will affect the ecosystem,” Kizana said. He added that “strong, clear, and adaptive regulations will be the key to increasing public confidence and accelerating the growth of the Indonesian crypto industry.”

That reads as an implicit acknowledgment that the law’s passage is a narrative event, the implementing rulebooks from OJK are the execution events that will define actual compliance costs.

Although not all industry voices are welcoming. The Indonesian Blockchain Association has raised concerns that draft provisions requiring all digital asset activity to flow through a single exchange could reduce existing platforms to brokers, concentrating market power in ways the original framework never intended.

Discover: The Best Token Presales

MiCA July 1 Hard Deadline: The Compliance Cull Arrives

Europe’s MiCA deadline is not a narrative event. July 1 is the date after which unlicensed crypto-asset service providers lose legal access to the EU’s 450 million users across all 27 member states.

As of today, of the approximately 3,000 firms that previously operated under national transitional arrangements, just about 230 have cleared the ESMA MiCA register. This has left the overwhelming majority either in the process of exiting EU markets or racing to complete authorization before enforcement begins.

Luxembourg is officially our MiCA home — Coinbase

We're looking forward to welcoming users from across the EU to Coinbase. https://t.co/6YiRoJRdJA

(@coinbase) June 24, 2026

(@coinbase) June 24, 2026

Coinbase Luxembourg opened its MiCA hub on June 24, securing a single EU passport from the Luxembourg CSSF that covers all 27 member states. Ripple also secured preliminary CASP approval under MiCA, positioning RLUSD for compliant EU distribution. Kraken is similarly cleared.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

However, Binance, the biggest crypto exchange in the world by volume, withdrew its Greek license application days before the deadline, leaving it absent from the ESMA register. Binance’s $4.3 billion DOJ settlement from 2023 is now a live liability in the EU authorization process.

The USDT situation underscores the reach of the regulation. Several EU exchanges delisted Tether ahead of the deadline because USDT does not meet MiCA’s e-money token requirements, while Circle’s USDC, structured to comply, retained listings.

Discover: The Best Crypto to Diversify Your Portfolio

The post Indonesia Crypto Overhaul and Europe’s MiCA Deadline: Who Gets Cut from Major Markets appeared first on Cryptonews.

Bitcoin slid to fresh 21-month lows Thursday at the Wall Street open, falling back toward the $58,000 area as a hotter-than-expected US inflation print rattled risk assets. The move underscored how tightly BTC trading has been tied to broader market volatility when macro data hits.

According to TradingView data cited in the report, BTC/USD on Bitstamp dipped to $58,035—an area last seen in September 2024. The pressure intensified shortly after the release of the May Personal Consumption Expenditures (PCE) report, with equities swinging sharply at the open.

Key takeaways

- BTC returned to levels last traded in September 2024, dropping to about $58,035 on Bitstamp during Thursday’s Wall Street open.

- US May PCE inflation came in at 4.1%, a three-year high for the year-over-year measure, contributing to fast, broad-market sell-offs.

- CoinGlass data cited in the coverage shows more than $600 million in liquidations across crypto within a single hour as BTC fell.

- Traders flagged potential “squeeze” dynamics around key psychological levels below $60,000.

- Technical commentary highlighted weakening $60,000 support and potential new resistance closer to $65,000.

Inflation hits, equities wobble—and BTC follows

The catalyst was the May PCE inflation release. The Bureau of Economic Analysis (BEA) reported that the PCE price index rose 4.1% year over year in May—recording a three-year high. In the monthly comparison, BEA said the PCE price index increased 0.4%, while excluding food and energy it rose 0.3%.

“From the same month one year ago, the PCE price index for May increased 4.1 percent. Excluding food and energy, the PCE price index increased 3.4 percent from one year ago.”

Markets reacted quickly. The report notes that the Nasdaq 100 dropped about 2% within roughly 30 minutes at the open, while the Nasdaq Composite was down modestly around the time of writing. The S&P 500, by contrast, managed a small gain—highlighting dispersion between large-growth and broader benchmarks as investors repriced near-term rate expectations.

Bitcoin’s decline mirrored that “risk-off” impulse. In the minutes after the open, BTC pushed lower in a move that traders often interpret as forced positioning rather than purely discretionary selling—especially given what followed in the derivatives market.

Liquidations top $600 million in an hour

As BTC slid through key levels, derivatives leverage appears to have accelerated the down move. CoinGlass, as referenced in the coverage, logged cross-crypto liquidations totaling more than $600 million over a single hour.

That kind of liquidation burst typically happens when price moves trigger margin calls for leveraged long positions, forcing liquidations that mechanically add to selling pressure. It also tends to increase volatility, making support levels harder to defend in the short term.

The report also included commentary from market participants who suggested the drop may have been intensified by order-book dynamics. A pseudonymous trader identified as “Killa” told X followers that BTC was in a “manipulation phase,” arguing that trading below $60,000 corresponded with a notable “swing low” region and that the orderbook was “stacked below” current pricing.

Bear-market analogies and the $60,000 test

Beyond the immediate macro-driven move, the article frames the latest dip within a broader bear-market pattern. Crypto analyst and trader Niels Klaver, cofounder of STABL Agency, characterized BTC/USD as moving toward what he called the “final leg down” of the current bear market. Klaver referenced a short-term target of $55,000, aligning with earlier popular bearish scenarios circulating among traders.

Other technical commentary focused on whether the market can stabilize after breaking below a key psychological level. The report cites Rekt Capital saying $60,000 support is “clearly weakening,” implying that any attempted rebound may face selling pressure from participants who sell after a breakdown or re-test.

Rekt Capital also pointed to the idea that the current market is behaving similarly to 2022, noting that a widely watched trend indicator—the 50-month exponential moving average (EMA)—is expected to become a resistance area. While that does not guarantee a rejection, it gives investors a concrete “where would resistance show up?” reference point if BTC tries to reclaim higher levels.

Another development highlighted in the report: Rekt Capital suggested that once June’s monthly close arrives, traders will be better able to judge whether July could produce a relief rally “from which price” the market can potentially pivot. This matters because monthly closes often influence how traders assess trend structure, risk management, and the probability of a reversal versus continued breakdown.

What to watch next: support, resistance, and follow-through

For investors and traders, the immediate question is whether BTC can regain and hold above the broken support zone around $60,000, or whether it turns into resistance as liquidation effects dissipate. The report’s cited technical views also imply that any rebound attempt could encounter selling pressure closer to the $65,000 area, with the broader bear-market analogy keeping downside risk in focus.

Going forward, the next macro releases and—just as importantly—whether the market sees sustained follow-through on either side of $60,000 and toward the $55,000 target will likely determine if this is a continuation leg or a transition into consolidation.

Crypto World

Polish Crypto Raid: FBI-Backed Arrests Hit Alleged SIM-Swap Gang Behind Millions in Theft

Poland’s Central Bureau for Combating Cybercrime (CBZC) arrested four members of an alleged crypto crime gang. The group drained cryptocurrency through SIM swap attacks, the FBI and Homeland Security Investigations revealed.

The suspects face charges that include running an organized criminal group, theft by hacking computer systems, and money laundering. All four remain in pre-trial detention and could face up to 25 years in prison.

How the Crypto Crime Gang Ran its SIM Swap Scheme

Investigators say the group broke into the IT systems of firms that work with telecom operators. Social engineering, rather than brute-force hacking, gave the attackers their initial foothold. They also obtained access to employee email accounts using specialized software.

That access let them run SIM swap attacks, which clone or hijack a victim’s phone number. With control over SMS and email, the group reset passwords, bypassed two-factor protections, and seized accounts on cryptocurrency exchanges.

Once inside, they drained the digital assets held in those accounts. The method exploits a known weakness, since many platforms still lean on phone-based recovery despite repeated telecom security failures.

The FBI counted more than $68 million in U.S. SIM-swap losses in 2021, taken from bank and virtual currency accounts.

Laundering and Cross-Border Cooperation

Police say the stolen funds moved quickly through a spread-out financial network. Prosecutors add that the suspects treated the thefts as a steady source of income. The group used personal bank accounts in Poland and abroad, payment platforms, and multi-currency crypto wallets.

Officials estimate the laundered total exceeds tens of millions of Polish zlotys, or several million dollars. The scale places it alongside other European crypto laundering networks disrupted this year.

U.S. prosecutors have pursued similar crews. Federal indictments describe the same playbook against cryptocurrency exchanges. One of the largest involved roughly $400 million stolen from the failed exchange FTX in 2022.

The Regional Prosecutor’s Office in Krakow supervises the case. The role of the FBI and HSI points to victims or infrastructure outside Poland. Such international crypto crime cases increasingly depend on cooperation across borders, echoing earlier FBI SIM swap arrests.

The CBZC, formed in 2022, has not named any suspect or released identifying photos, citing the active investigation. It did publish video of the operation on its official channels.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

Unverified social media speculation has linked one detainee to a known online alias, “Merry.”

Police have not confirmed the claim. Officials say the case is still developing, and more arrests could follow as the inquiry continues.

The post Polish Crypto Raid: FBI-Backed Arrests Hit Alleged SIM-Swap Gang Behind Millions in Theft appeared first on BeInCrypto.

Remember BlackBerry? Yes, that BlackBerry: The phone with a physical keyboard that everyone used and suddenly became obsolete after Apple introduced the iPhone.

Well, it’s making a comeback.

The new BlackBerry isn’t a mobile device, but it’s a “mission-critical software layer in the physical AI stack,” and the stock is surging.

BlackBerry hasn’t made a consumer mobile device in years. Instead, it has quietly transformed into a high-tech powerhouse focused entirely on the world of “Physical AI” and robotics.

The secret weapon? The rock-solid software framework called QNX that acts as the “uncrashable” nervous system for autonomous machines. That means BlackBerry’s software is being used by massive chipmakers such as Nvidia and AMD to build smart cars and warehouse robots. The software makes sure those machines move safely with zero lag.

“As intelligent machines become increasingly autonomous and operate around people, the requirements for safety, security, reliability and real-time determinism become even more important,” CEO John Giamatteo said during an earnings call. “Unlike probabilistic AI systems, QNX technology is deterministic and safety certified, which is exactly why it is so hard to replicate and why customers trust it for systems where failure is not an option.”

Did Keir Starmer ‘drag the party to the right’? Readers discuss

Okta Is Vindicated As Agentic AI Winner, But It’s Time To Say Goodbye (NASDAQ:OKTA)

BlackRock Sends $217M in Bitcoin and Ethereum to Coinbase Prime

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Blockchain.com files with SEC for U.S. IPO

Weekend Open Thread: Miami – Corporette.com

Bitcoin Bear Flag Alert: Massive Dump Coming?

“Your Daily Habits Decide Your Financial Future” l Ft Wealthy Sandeep l Wealth Management l

Money view loan kaise milega 2026 | Moneyview personal loan kaise le | Moneyview personal loan app

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment5 days ago

Entertainment5 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports2 days ago

Sports2 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech3 days ago

Tech3 days agoMicrosoft accidentally kills epic Outlook email threads

-

Business5 days ago

Business5 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics5 days ago

Politics5 days agoAndy Burnham and the meaning of Makerfield

-

Crypto World2 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

NewsBeat6 days ago

NewsBeat6 days agoKeir Starmer Allies Question His Chances For No 10

-

Crypto World1 day ago

Crypto World1 day agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Politics7 days ago

Politics7 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Business2 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business6 days ago

Business6 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Crypto World5 days ago

Crypto World5 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World6 days ago

Crypto World6 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World5 days ago

Crypto World5 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Entertainment6 days ago

Entertainment6 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Tech4 days ago

Tech4 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Sports4 hours ago

Sports4 hours agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Tech3 days ago

Tech3 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Sports7 days ago

Sports7 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

You must be logged in to post a comment Login