Crypto World

Crude Oil Volatility Intensifies as US Retaliates Against Iran Near Hormuz Strait

TLDR

- Brent crude plunged more than 4% to approximately $72 per barrel Friday; WTI declined 3% to roughly $69

- Commercial traffic through the Strait of Hormuz climbed to the highest volume since conflict escalated in late February

- An Iranian attack drone targeted a Singapore-flagged container vessel on Thursday

- US forces retaliated Friday with strikes against Iranian drone storage facilities, missile depots, and radar installations

- Crude prices staged a partial comeback in late Friday trading following confirmation of American military action

Crude oil markets experienced dramatic volatility on Friday, plunging in early trading before staging a recovery after the United States conducted military operations against Iranian targets in response to a drone assault on a commercial ship navigating the Strait of Hormuz.

Brent crude tumbled over 4% during regular trading hours, settling near the $72 per barrel level. West Texas Intermediate experienced a roughly 3% decline to approximately $69 — marking its first closing price beneath $70 since the Iran conflict intensified in late February. Both benchmark grades have now surrendered approximately 25–27% of their value during the past month.

The initial selloff occurred as maritime traffic navigating through the Strait of Hormuz climbed to its most robust levels since hostilities commenced. This development alleviated concerns regarding potential oil supply interruptions and applied downward pressure on crude valuations.

Factors Behind the Crude Selloff

Washington and Tehran finalized a 60-day memorandum of understanding during the previous week, temporarily halting active conflict. The agreement incorporates provisions for restoring commercial shipping operations through the Strait of Hormuz, alongside nuclear negotiations contingent upon sanctions relief.

As maritime vessels resumed more normal transit patterns through the strategic waterway, market participants reduced the conflict-related risk premium that had accumulated in oil futures.

Dennis Kissler, senior vice president at BOK Financial, cautioned on Thursday that the price correction might be excessive. “While the Strait of Hormuz is moving oil, there still exists the possibility of mines in the area as well as rogue Iranian militia continuing to make threats on shipping lanes,” he said. “The latest sell-off in prices is likely overstating the true near-term fundamentals,” he added.

The Drone Attack That Shifted Market Sentiment

On Thursday, Iran launched an attack on the Singapore-flagged container vessel Ever Lovely using what American officials characterized as a one-way attack drone. The commercial ship suffered damage during its passage through the strait.

President Trump expressed dissatisfaction with the assault on Friday. “I don’t like the fact that they took a shot,” he told reporters. “They shouldn’t be doing that.”

US Central Command announced that American military aircraft targeted Iranian missile storage locations, drone facilities, and coastal radar systems on Friday. The command characterized the operation as a “powerful response to yesterday’s attack.”

Iran’s Islamic Revolutionary Guard Corps claimed its forces “successfully repelled the attack.”

The military exchange generated renewed uncertainty about the sustainability of the ceasefire arrangement. Trump had previously indicated he would authorize resumed military operations if Iran breached the agreement’s provisions.

Notwithstanding the strikes, commercial shipping maintained its movement through the strait on Friday. Central Command confirmed it would continue facilitating safe passage coordination for commercial maritime traffic.

An outstanding issue involves whether Iran will implement transit fees for vessels passing through Hormuz. Oman informed European officials that certain tolls might eventually be imposed — a matter of continuing dispute between Washington and Tehran.

Crude oil prices climbed back above session lows in late Friday trading after confirmation of the US military strikes.

Hyperliquid traded near $63 on June 26 after pulling back from its all-time high of $76.70 earlier this month.

Summary

- HYPE holds above $60 support while whales continue buying during the wider crypto market pullback.

- Multicoin’s $319 target depends on Hyperliquid keeping revenue growth, market share and buybacks strong.

- Technical indicators show cooling momentum, with bulls needing $65-$70 to regain stronger control soon.

According to crypto.news data, the token is down over the past week, but it still holds a large gain over the past year.

The latest Hyperliquid price data shows HYPE trading between $59.48 and $65.17 over the past 24 hours. The token holds a top-10 market rank, with a market cap above $14b and fully diluted value above $60b.

HYPE’s recent move looks like a consolidation phase after a sharp rally from the low $30s in March. Price has cooled near $63, but the $60 area remains the main short-term support zone.

A clean break below $60 would put the next support area near $55-$58 back in focus. A move above $65 would show early strength, while a close above $70 would give bulls a stronger case for a retest of the recent high.

Hyperliquid whales keep buying during pullback

Whale activity remains one of the stronger parts of the HYPE setup. According to Lookonchain, a newly created wallet withdrew 222,493 HYPE, worth about $14.41m, from Coinbase Prime. Another whale received 44,986 HYPE, worth about $2.87m, from FalconX.

Those transfers do not prove long-term holding, but they show large buyers are still active during the pullback. Traders often watch Coinbase Prime and FalconX flows because they can reflect institutional or high-net-worth activity.

Derivatives data also shows active trading. CoinGlass data shows HYPE volume rose 29.79% to $4.59b, while open interest slipped 1.15% to $2.52b. Options open interest rose 10.62%, but options volume fell sharply, showing that most activity remains in spot and perpetual futures.

As previously reported, HYPE rallied more than 40% in one week in May as derivatives activity, ETF demand and protocol buybacks supported the move. The current pullback is testing whether that demand can keep absorbing profit-taking.

Multicoin target lifts long-term debate

Multicoin Capital has published a bullish valuation report on HYPE. In the full analysis, the firm said HYPE is now one of the largest positions in its liquid fund and that it has been accumulating since February.

The firm said Hyperliquid generated about $873m in revenue across roughly $2.9t in trading volume in 2025. It also said the platform grew from about 301,000 to 923,000 users and ended the year with about $6b in open interest.

Multicoin argued that Hyperliquid is taking share from centralized exchanges. It said monthly perpetuals volume is now about 17% of Binance’s level, while open interest has reached about 21% of Binance’s level.

The firm also pointed to HIP-3, HIP-4, portfolio margining, prediction markets, tokenized assets and HyperEVM growth as future drivers.

“We believe Hyperliquid is becoming the everything exchange,” it said.

As crypto.news reported, Multicoin backed a $319 HYPE target by 2028 under its base case. The firm also listed risks, including regulation, governance, competition, bad debt and technical pressure.

Technical signals show cooling momentum

The HYPE/USDT daily chart still shows a broader uptrend from March. Price climbed from the low $30s to above $70 before pulling back. That structure keeps the larger trend constructive, but short-term momentum has cooled.

The Accumulation/Distribution indicator is near 2.32m. It remains elevated after rising sharply earlier in June, which suggests buying pressure improved during the rally. The line has flattened recently, showing that accumulation is no longer accelerating.

The Aroon Oscillator is positive near 28.57. That keeps the short-term trend bias slightly bullish, but the reading has weakened from stronger levels. This means the uptrend remains alive but has lost some speed.

In a previous article, crypto.news discussed HYPE’s double-top risk after its pullback from the all-time high. That pattern put the $65 and $62 areas in focus. Price is now trading near that same zone.

Previously, crypto.news exploredwhether HYPE can reach $100 in 2026. That scenario depends on buybacks, volume growth, token unlocks and wider market strength.

For now, HYPE remains in a mixed setup. Whales are buying, Multicoin has issued a strong long-term case, and the broader trend still holds above $60. But momentum has cooled, and bulls need a move back above $65-$70 to confirm that the next upside phase is starting.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

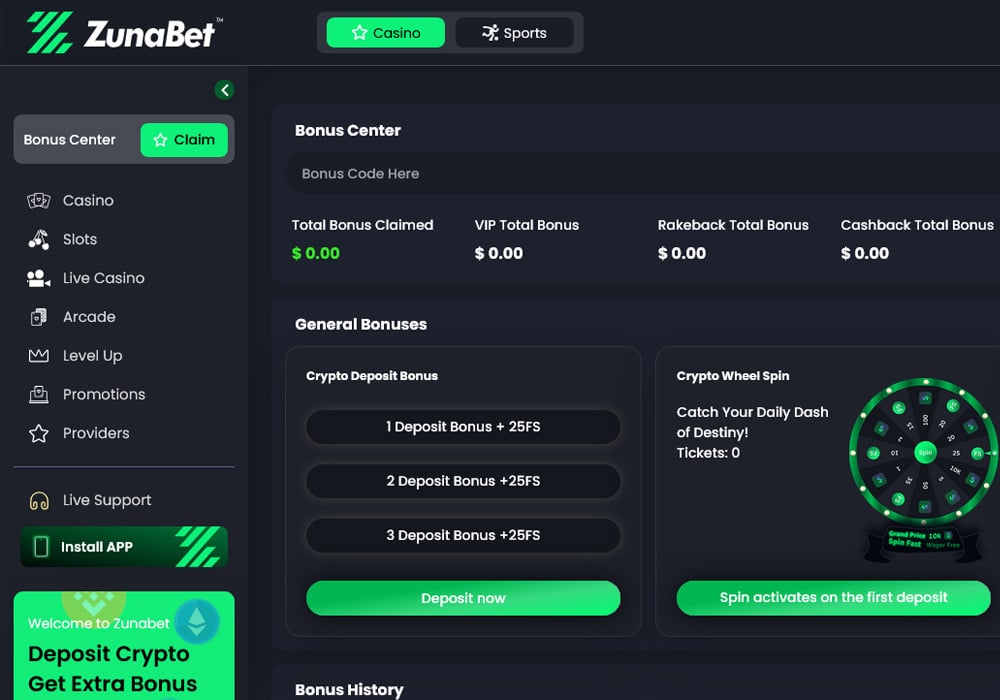

Bet365 and 888casino sit among the most recognized names in online betting, with decades of operation behind each of them. The space they helped shape, though, keeps evolving — and lately, players comparing the veterans have started looking past them too. ZunaBet, which launched in 2026, is one of the names appearing more often in those side-by-side conversations as the crypto-first model continues to gain ground.

What follows is a look at how the established names compare today, and why ZunaBet is drawing attention as players widen the field.

The Veterans of the Space

Bet365 has been running since 2000. Built from the UK and now a global brand, it brings sportsbook, casino, poker, and bingo under one account. Funding moves through cards, bank transfers, and e-wallets, and the operator carries licenses in every region it serves.

888casino goes back even further, to 1997. As one of the first online casinos to launch, it operates under the 888 Holdings umbrella and continues to hold steady positions in European regulated markets and parts of North America. The library leans on slots, table games, and live dealer rooms. Like Bet365, it works on fiat banking under regional licensing.

Both deliver the dependability that long-standing brands tend to provide. Both also work within constraints baked into that model — fiat-only banking, withdrawal speeds tied to chosen methods, libraries smaller than what global crypto brands carry, and loyalty programs that stay close to long-running structures.

ZunaBet Enters the Comparison

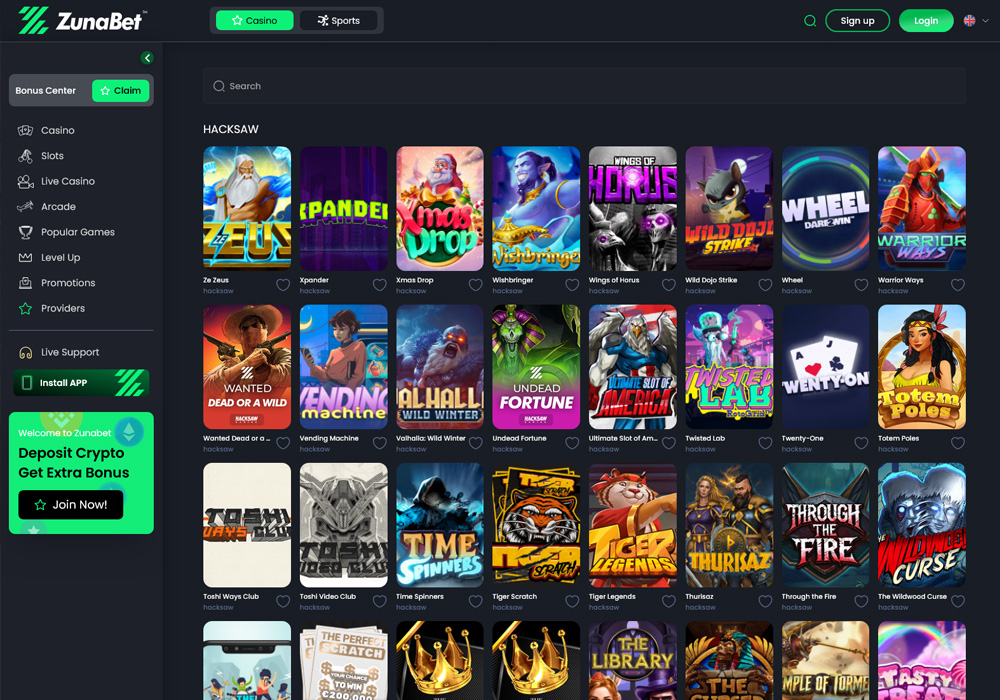

ZunaBet went live in 2026 under Strathvale Group Ltd with an Anjouan gaming license. The defining difference between it and the established names is structural. Crypto wasn’t introduced later — the platform was built around it from the start.

The game catalogue reaches more than 11,000 titles from over 60 providers, including Pragmatic Play, Hacksaw Gaming, Yggdrasil, BGaming, and Evolution. That ranks it among the larger crypto-focused libraries on the market and pushes past what Bet365 and 888casino offer in most of their licensed regions. Slots, table games, and live dealer rooms all share a single account.

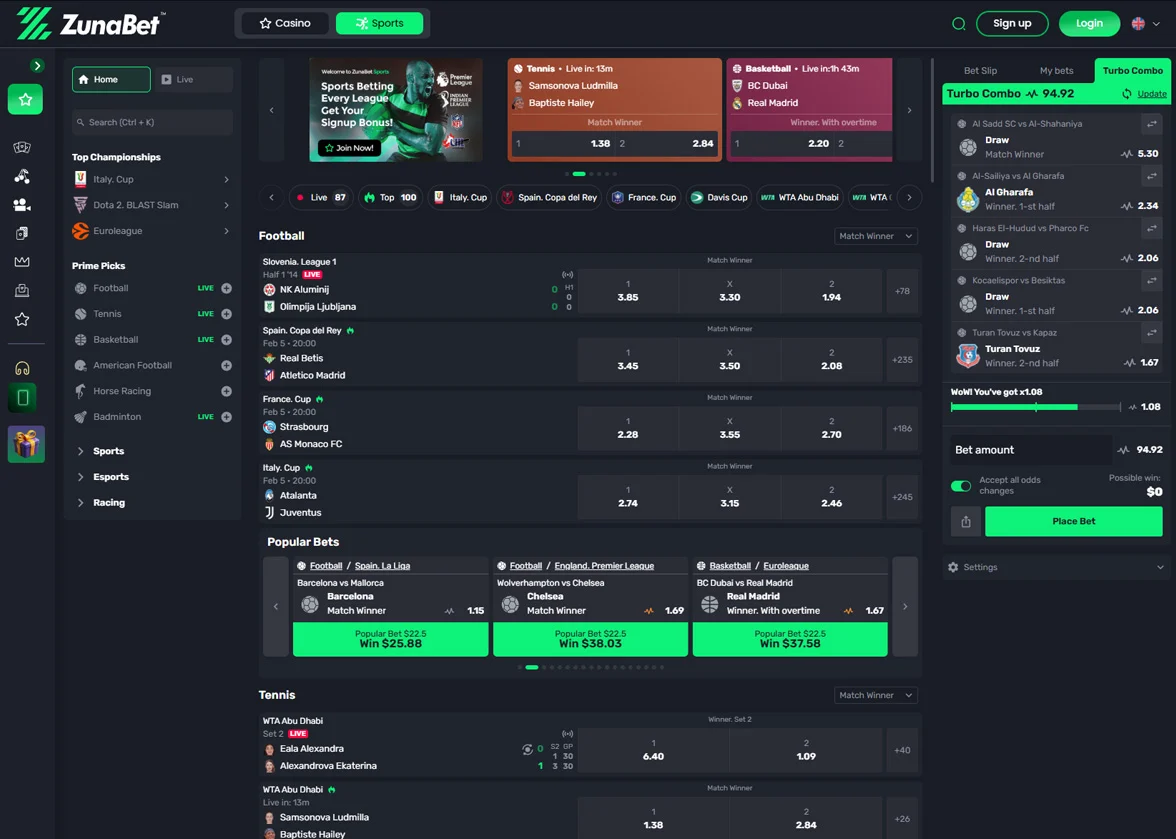

The sportsbook is built into the platform too. Football, basketball, tennis, NHL, and the other major sports sit alongside CS2, Dota 2, League of Legends, and Valorant. Virtual sports and combat sports finish the menu. That makes ZunaBet a hybrid in the same category as Bet365, with wider market coverage under one roof.

How the Payment Models Compare

The operating gap shows up most clearly in banking. Bet365 and 888casino move money through traditional rails. The cost is processing windows, possible holds, and withdrawal speeds that depend on which method players chose.

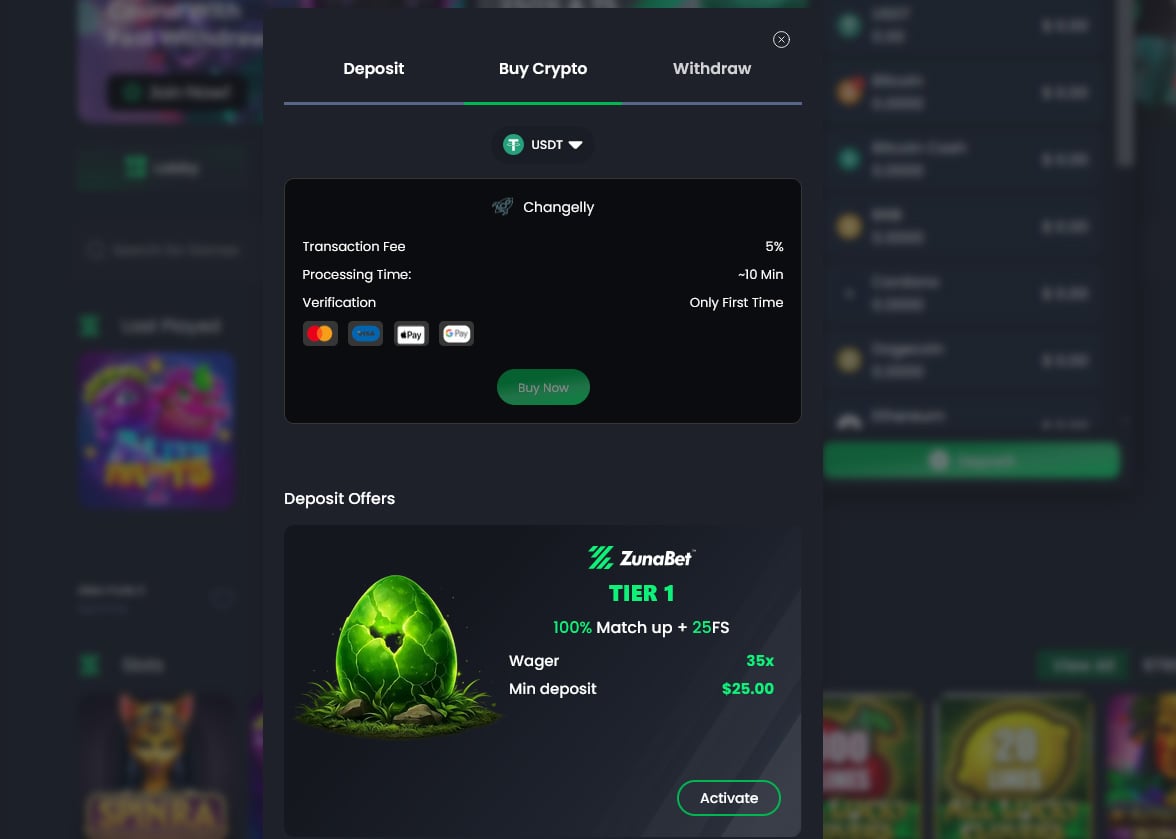

ZunaBet’s payment stack is entirely crypto. More than 20 currencies are supported, covering Bitcoin, Ethereum, USDT across multiple chains, Solana, Dogecoin, Cardano, and XRP. No platform fees apply, and withdrawals settle fast. For players already comfortable with crypto, the experience cuts out the slower elements that come with banking.

Reach matters here too. Crypto-first operators aren’t tied to the same region-by-region licensing requirements that govern fiat brands. ZunaBet’s full setup is available across many regions where older brands face restrictions. For players already moving in digital, crypto-friendly contexts, that aligns with how they expect modern platforms to work.

Welcome Bonuses Compared

Bet365 and 888casino structure welcome offers by region. Deposit matches or smaller new-player bonuses are typical, with wagering requirements that need close reading on the casino side.

ZunaBet’s welcome package goes up to $5,000 plus 75 free spins, spread across three deposits. The first matches 100% up to $2,000 plus 25 spins. The second adds 50% up to $1,500 plus 25 spins. The third returns to 100% up to $1,500 plus another 25 spins. Marketed as a 250% bonus across three deposits, it gives new players more depth to explore the platform than a single-deposit bonus offers.

Loyalty: Different Approaches

Bet365 takes a low-key approach to loyalty, with personalised offers reaching player accounts based on activity rather than a structured tier system. 888casino runs a more traditional VIP setup with points, free spins, and elevated promos at higher tiers. Both work, but both stay close to the standard loyalty card format.

ZunaBet changes the structure. The program runs on a dragon evolution theme, with a mascot called Zuno guiding players through six tiers. Squire opens at 1% rakeback, then Warden at 2%, Champion at 4%, Divine at 5%, Knight at 10%, and Ultimate at the top with 20% rakeback.

Higher tiers unlock more than rakeback. Tier-based free spins reach up to 1,000 spins, with VIP club access and double wheel spins layered through the journey. The whole format feels closer to progressing through a game than working through a points card. For players already familiar with that kind of mechanic, it changes the feel of regular play.

Why Players Are Looking at ZunaBet

Bet365 and 888casino remain dependable for players who value regulation and a long track record. Neither brand is in any danger of losing its place. But the bar for what an online betting platform should deliver keeps moving. Fast withdrawals, deep libraries, and engaging loyalty mechanics are now expected as standard rather than upsells.

ZunaBet was designed around those expectations from day one. The crypto-first core delivers quick payments and low fees. The library reaches beyond what most established brands carry. The sportsbook integrates traditional sports and esports together. The dragon loyalty program adds direction and progression to regular play.

For players who want speed, variety, and a more current feel, ZunaBet ranks among the more interesting platforms to track right now. It’s still in its early growth phase, but the direction is clear. A new generation of players treats crypto support, gamified rewards, and global access as starting points rather than features that need to be requested.

Bet365 and 888casino built the online betting world that exists today. ZunaBet is one of the platforms shaping what comes next — and the players who notice early are the ones getting the first look.

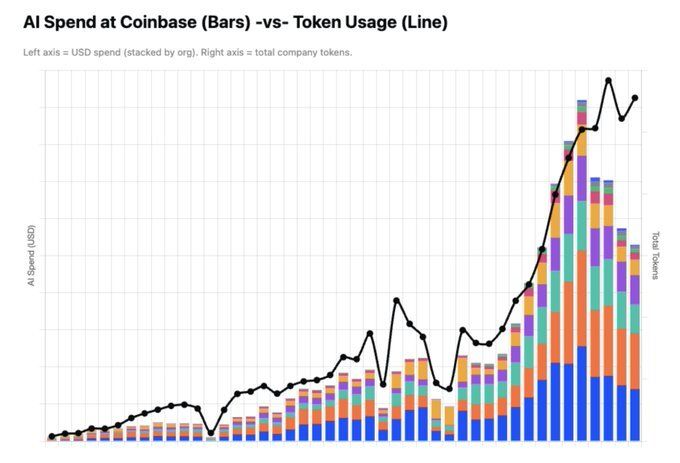

Coinbase CEO Brian Armstrong said the company cut its AI spending nearly in half while token usage grew exponentially, outlining an infrastructure playbook he believes any firm can use to scale AI adoption without treating cost as a ceiling.

Armstrong also offered a sharp reframe of the current Bitcoin (BTC) market cycle

AI Routing, Caching, and Open-Weight Models

Armstrong outlined three techniques behind the savings. The first is smarter model routing, which matches tasks to the cheapest model capable of completing them.

“How to keep AI spend flat while token usage grows exponentially: Not with friction and spend alerts. With better defaults, routing, and caching,” the Coinbase CEO said.

The second is aggressive caching, which eliminates redundant outputs for repeated queries. The third is a shift toward cheaper open-weight models for routine tasks where frontier-model performance adds no value.

The objective, Armstrong clarified, is not to cap usage but to build the infrastructure layer that enables sustainable scale. In early June, he examined AI’s largest bottleneck, contending that access to energy and compute matter more than model quality. The new spending data adds routing efficiency to that framework.

The framing positions cost reduction not as a constraint, but as a prerequisite for broader adoption. As a result, efficiency gains create headroom for usage to compound rather than triggering budget friction later on.

Armstrong did not disclose the absolute cost figures. Still, a company that halves AI spend while usage compounds at an exponential rate has effectively decoupled consumption from cost.

Bitcoin Dip “Barely Even a Winter”

On the Bitcoin front, Armstrong took direct aim at bearish sentiment. He described the current drawdown as far milder than anything long-term holders have seen before.

The data backs that read. River’s historical chart shows the 2025–2026 cycle has erased roughly 53% from Bitcoin’s October 2025 peak of $126,073.

That makes it the shallowest bear market on record. Prior cycles wiped out between 77% and 93%, with two exceeding 12 months.

Armstrong made a $60,000 bottom prediction in mid-June. However, on-chain data has not yet confirmed the capitulation signals that historically mark cycle lows. That gap between price and signal has been a persistent feature of this cycle.

The Coinbase CEO has backed Bitcoin’s four-year cycle consistently and projects prices far above current levels by 2030. Still, the 500-day halving signal most analysts track does not trigger until November 2026. The recovery timeline may be further out than Armstrong implies.

The post Coinbase CEO Halved AI Costs, Calls Bitcoin Downturn a Cool Breeze appeared first on BeInCrypto.

Cardano wallet provider SecondFi says it has built a recovery route for users impacted by a Tuesday exploit that exposed private keys for a portion of its customer base. In an update shared Saturday, SecondFi’s developer Emurgo indicated that asset returns should begin after completion of security testing and internal verification, with the first payouts expected in roughly two weeks.

The company’s CEO, Phillip Pon, said Emurgo finished forensic investigations and designed the process around SecondFi’s existing wallet states—an approach Pon warned users not to disrupt by moving funds independently or following instructions from unofficial sources.

Key takeaways

- SecondFi/Emurgo completed forensics and mapped a recovery pathway for affected users after Tuesday’s Cardano wallet exploit.

- Emurgo expects to start returning assets in about two weeks, after a week building the solution and a subsequent week of testing.

- SecondFi previously linked the incident to an address-level problem in its Cardano web wallet generation software that exposed private keys.

- The wallet provider says it is coordinating recovery without requiring user participation for key handling, and it is warning users about scams that may imitate official guidance.

- SecondFi secured a portion of funds (reported as 129 million ADA) via emergency measures and moved them to an independent third-party custodian for verification.

Recovery plan targets affected users after forensics

According to a Saturday statement from Emurgo CEO Phillip Pon posted on X, SecondFi has reached the stage of producing a recovery solution after finishing forensic work and establishing a pathway intended to safely return assets.

Pon said the immediate focus is the construction phase over the coming week, followed by an additional week of testing and security review before withdrawals or refunds begin. While the company has not published a full technical explanation of the exploit mechanics, its plan is designed to restore user assets in a controlled manner rather than through ad hoc user action.

Crucially, Pon urged users not to migrate assets or take steps outside official instructions during the recovery period. He characterized the workflow as dependent on the wallet states already recorded at the time of the incident, warning that independent actions could complicate efforts to securely reconcile and return funds.

What the Tuesday breach involved

SecondFi disclosed the breach earlier in the week, stating that the incident affected approximately 16 million ADA across 374 addresses. At the time of disclosure, SecondFi estimated the value at about $2.4 million.

In its initial reporting, SecondFi attributed the underlying cause to an address-level issue within its Cardano web wallet generation software. The company said this issue resulted in private keys being exposed for affected users.

Beyond identifying the exposure, SecondFi also said it took emergency measures to secure about 129 million ADA. Those funds were reportedly transferred to an independent third-party custodian and will remain there until the verification and recovery process is fully complete. The separation between the custodied funds and the ongoing recovery workflow underscores the company’s emphasis on verification before any broad asset return.

Scam warnings while recovery is still underway

As SecondFi works toward the next steps of its recovery program, it says scammers are trying to take advantage of the situation. In a separate Saturday update, SecondFi warned that malicious actors have been circulating fraudulent messages impersonating the wallet during the recovery window.

The company said no recovery actions requiring user participation have started. It also reiterated that SecondFi will not ask users for private keys, seed phrases, wallet credentials, or direct wallet access.

SecondFi further cautioned that any message instructing users to submit sensitive wallet information, migrate assets, or act immediately outside of its verified communication channels should be treated as fraudulent. For users seeking help, the company advised submitting a ticket through its official support portal while the recovery process continues.

Why the “two-week” timeline and “no user action” rule matter

The most practical part of SecondFi’s update for impacted users is the operational timeline. By stating that building and testing will consume about two weeks in total before asset returns begin, Emurgo is effectively communicating that this is not a one-day rollback or an instant unlock—rather, it is a staged process with security reviews intended to reduce the risk of further loss.

Just as important is the instruction to avoid migrating funds on one’s own. For wallet incidents, independent user actions can sometimes reduce the amount of verifiable data available to an operator or complicate address-level reconciliation. SecondFi’s stated approach—designing recovery around “existing wallet states”—signals that its engineers are working from a known set of conditions and that changing balances or moving assets independently could create mismatches between what is stored in the wallet records and what needs to be restored.

At the same time, the company’s scam warnings highlight the danger of acting on unofficial guidance. If users were to follow instructions from imposters—especially those asking for seed phrases or direct access—the consequences could compound the original exploit. SecondFi’s emphasis on never requesting private keys or credentials is therefore central to the security posture during recovery.

Still, some key uncertainties remain for the broader community. SecondFi has not published a comprehensive post-mortem that details the full vulnerability or how attackers executed the exploit. Until more technical information is shared, investors and users will likely focus on whether the scheduled testing and review periods end on time and whether asset returns proceed smoothly for all affected addresses.

For users affected by the Tuesday incident, the next watch points are whether SecondFi begins asset returns on the expected schedule and whether the company continues to provide clear, verified updates while discouraging any off-platform recovery attempts. For the wider ecosystem, the incident also serves as a reminder of how web wallet key-generation and address-level logic can become high-risk components—and why disciplined verification during recovery can be as important as the initial patch.

The spot exchange-traded funds tracking the two largest cryptocurrencies by market cap have continued their highly adverse streak, making it now seven consecutive weeks in the red.

The last five trading days were particularly painful as the spot BTC ETFs recorded their second-worst performance in terms of net flows since their inception two and a half years ago.

Spot BTC ETFs Bleed Hard

CryptoPotato has repeatedly reported on the poor performance of the spot Bitcoin ETFs, but the two weeks before the one that ended on June 26 brought some glimmer of hope. Although both were still in the red, the actual withdrawals were more modest, $316 million and $227 million, respectively, down from the $1.72 billion during the first week of June.

However, investors stepped up on the withdrawal button hard once again, pulling out $1.79 billion in total from the funds. This made it the worst week in terms of net flows since late February 2025, when the number stood at $2.61 billion.

The cumulative total net inflows have dropped to $51.61 billion. Recall that the number stood at above $59.30 billion by the middle of May. This means that the ETFs have lost almost $8 billion in less than two months.

If we break the data down to daily net outflows, Thursday stands out as the most painful day with $696 million leaving the funds, followed by $469 million on Wednesday, $444.5 million on Friday, and a more modest $90.66 million on Monday and $68 million on Tuesday.

The continuous outflows from the ETFs are among the most evident reasons why the underlying asset’s price keeps struggling as it plunged to a new multi-year low of $58,000 a few days ago. Analysts are convinced that the flows have to stabilize before BTC has a chance of a more profound recovery.

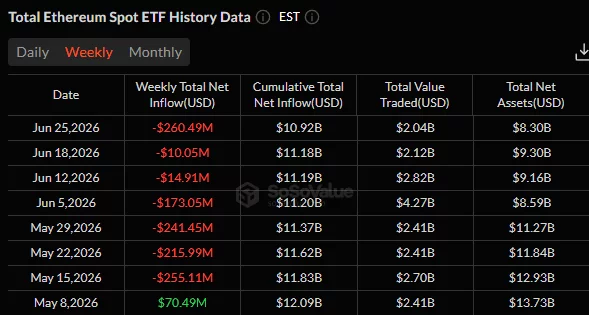

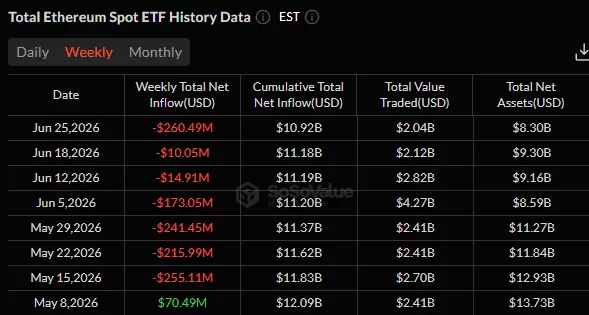

ETH ETFs in Red, Too

The landscape around the spot Ethereum ETFs is not that much different, just the scale is smaller. The funds have been in the red for seven consecutive weeks as well, and the net outflows from the past week were a lot higher than the previous two. More specifically, the ETFs bled $15 million during the second week of June and $10 million during the third. During the last one, though, investors took out $273.34 million.

The total net flows have dropped from $12.09 billion in mid-May to well under $11 billion as of Friday’s close. Tuesday and Thursday saw the most net withdrawals, with $82.35 million and $81.87 million, respectively.

The post Bitcoin ETFs Set Another Anti-Record as $1.8B Leave the Funds Weekly appeared first on CryptoPotato.

Crypto World

Binance founder CZ blames crypto’s sour 2026 on mix of AI, global tension, 4-year cycle

CZ acknowledged that there is a gambling component to prediction markets, but he said that is also true in other financial markets.

“With any financial instrument, there’s always some speculators,” he said. “The speculators actually provide the liquidity, so it’s good that you have that speculation.”

Policy futures

The U.S.’s potential signature crypto policy legislation — the Digital Asset Market Clarity Act (known as the Clarity Act) — may become a law by the end of the year if lawmakers can work out some remaining issues, including an ethics provision for government officials, chiefly the president.

But he said the Clarity Act and other individual bills are “sort of small, tactical things, which are really important, but those are not gonna impact the growth of crypto longer-term.”

Even if the Clarity Act does not become law this year, CZ said he expected the U.S. would continue to take a leading role in crypto regulation, adding that other countries were continuing to introduce their own regulations governing digital assets.

The U.S. would likely still compete with other countries to introduce rules, and it already has the stablecoin-focused Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, he said.

“I, of course, hope to see it get passed, and then every other country will probably copy it to some extent,” he said. “If it gets delayed … other countries may move forward first.”

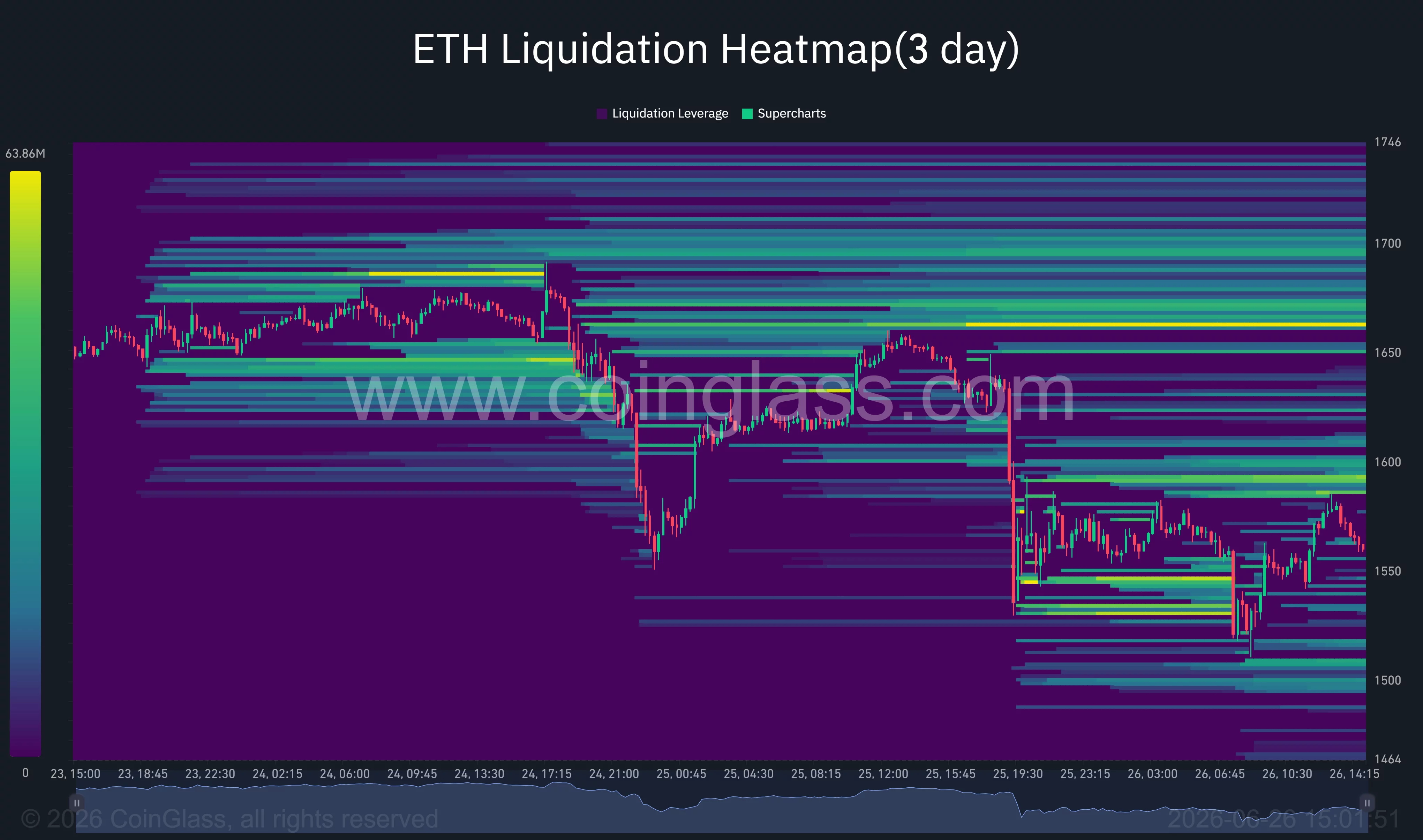

Ethereum has extended its weekly decline as a multi-billion-dollar options expiry, institutional selling, and a hawkish Federal Reserve outlook have driven the token back toward its key $1,500 support.

Summary

- Ethereum has fallen 14.4% from its June 22 high as ETF outflows, a $10.63 billion options expiry, and macro pressure fueled the selloff.

- Technical indicators show bears remain in control, with $1,500 acting as the key support and $1,750 the first major recovery level.

- CryptoQuant data show major Ethereum whale cohorts have slipped into unrealized losses, adding to concerns over near-term market sentiment.

According to data from crypto.news, Ethereum (ETH) fell about 7% to an intraday low of $1,517 on June 26 before stabilizing around $1,550 at press time. The asset has dropped nearly 14.4% from its June 22 high of $1,773.

The selloff gathered pace after Ethereum lost its 200-day moving average near $1,668, triggering a wave of leveraged long liquidations.

Meanwhile, U.S. spot Ethereum ETFs recorded roughly $260 million in net outflows this week, a sharp jump from the previous weeks, as institutional investors reduced exposure ahead of expectations for three Federal Reserve rate hikes this year.

Additional pressure emerged after the Ethereum Foundation announced a 20% workforce reduction and a 40% cut to its operating budget. The restructuring raised fresh questions about the network’s development pace and funding outlook while traders were already navigating heightened volatility around the $11 billion options expiry.

Ethereum’s $1,500 support has become the market’s main test

Ethereum’s daily chart shows that the token has broken below the $1,805 support area, turning a former demand zone into overhead resistance. The next major support sits near $1,414, while the current rebound attempt has remained limited after buyers defended the $1,500–$1,520 region.

On the four-hour chart, Ethereum has been moving inside a descending channel since its June 15 peak near $1,849. The Fib retracement map places immediate resistance near $1,584, followed by $1,641, $1,681, and $1,720. A stronger recovery would need a clean move above $1,750, which also matches a key level watched by traders.

According to analyst Ted Pillows, Ethereum’s momentum remains weak after retesting the lows.

“ETH tapped the lows again. The momentum is still weak due to market correction. But if Ethereum manages to reclaim the $1,750 level from here, we could see a relief rally next month.”

Momentum indicators remain soft. The four-hour RSI is near 35, keeping Ethereum close to oversold territory without confirming a strong reversal. The MACD remains below the zero line, although its histogram has started to flatten, showing that bearish pressure has slowed after the sharp drop.

The daily Aroon setup still favors sellers. Aroon Down is at 100%, while Aroon Up sits near 21%, showing that Ethereum recently printed fresh lows while upside momentum remains limited. The daily MACD also remains negative, with both signal lines deep below zero.

Liquidation clusters keep pressure on both sides of the trade

CoinGlass’ three-day liquidation heatmap shows heavy leverage around $1,590 to $1,610 and a larger cluster near $1,660. If Ethereum rebounds through those zones, short liquidations could fuel a move toward $1,700 and then $1,750.

Below the spot price, the heatmap shows liquidation interest around $1,520 and $1,500 levels. A break under that area would expose the $1,464–$1,414 region, where the daily chart shows the next major support band.

Whale positioning has also weakened. CryptoQuant analyst Darkfost noted that three large Ethereum holder groups are now underwater, with unrealized profit ratios at -0.26 for 1,000–10,000 ETH holders, -0.21 for 10,000–100,000 ETH holders, and -0.05 for wallets holding more than 100,000 ETH.

According to Darkfost, this condition has not appeared since 2019, as even the largest Ethereum whales stayed in profit during the 2022 bear market. The analyst added that Ethereum has remained “fairly resilient” despite the pressure, as similar whale stress periods have historically appeared near major bottom zones.

Downside risks remain high if Ethereum loses the $1,500 area with volume. A daily close below that level would weaken the double-bottom setup and increase the risk of a deeper move toward $1,414. A hawkish Federal Reserve, stronger U.S. dollar, rising Treasury yields, and continued ETF outflows would add pressure if institutional demand fails to recover.

The bullish invalidation level is now clear. Ethereum needs to reclaim $1,750 and then $1,805 to prove that the latest decline was a liquidity-driven flush rather than the start of another breakdown. Until then, the market remains trapped between forced selling below $1,600 and short-covering risk above $1,660.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

The CLARITY Act has the votes and the momentum to become law, having cleared the House and a key Senate committee. It is stuck anyway. The deepest reason is not crypto skepticism but a fight over the president’s own crypto empire, estimated in the billions, and whether the rules should restrain it.

Summary

- The CLARITY Act, the U.S. crypto market-structure bill, has cleared the House and the Senate Banking Committee and reached the Senate calendar, yet it remains stuck.

- The deepest obstacle is not crypto skepticism but an ethics fight over President Trump’s family crypto interests, estimated at roughly $2.3 billion or more, spanning World Liberty Financial, the USD1 stablecoin, and the TRUMP memecoin.

- Democrats led by Senator Gillibrand say there is no bill without ethics language restricting officials from profiting on digital assets, and a committee amendment to that effect failed on a party-line vote.

- The White House argues that ethics limits must apply uniformly and not single out the president, and a target to sign the bill by July collapsed when the ethics talks broke down.

- With a hard deadline before the August recess and a 60-vote threshold that needs several Democratic votes, the bill’s fate now turns on whether credible ethics language can be agreed, not on crypto policy itself.

The CLARITY Act is the bill the American crypto industry has wanted for years, the one that would finally settle how digital assets are regulated in the U.S., and by the ordinary logic of legislation it should be on a path to becoming law.

It passed the House of Representatives with bipartisan support, cleared the Senate Banking Committee on a 15-to-9 vote, and was placed on the Senate calendar, formally eligible for a floor vote. The industry is mobilized behind it, with hundreds of companies urging passage, and analysts have spent the year handicapping when, not whether, it would be signed.

And yet it is stuck.

The reason it is stuck has surprisingly little to do with crypto policy itself, on which a workable consensus largely exists, and a great deal to do with something the bill’s authors never intended it to be about: the president’s own crypto business.

President Trump and his family hold crypto interests estimated in the billions of dollars, and the question of whether a law regulating crypto should also restrain officials who profit from it has become the obstacle that crypto policy alone never was.

This piece explains how a bill with the votes to pass got trapped by the president’s crypto empire, and why that fight is harder to resolve than any technical dispute over digital assets.

This is a politically charged subject, and the aim here is to lay out the situation factually and fairly, presenting what each side argues rather than taking a position. The dispute touches genuine disagreements about ethics, executive power, and the proper scope of a market-structure bill, and reasonable people land in different places on all of them.

What follows covers what the CLARITY Act would do, the two obstacles blocking it, the scale and nature of the president’s crypto holdings, the conflict-of-interest concerns that critics raise, the responses from the White House and its allies, why the impasse is so hard to break, and the deadline that now governs the bill’s fate.

The goal is to make a complicated and contested situation legible, not to argue for an outcome.

A bill that should pass, and cannot

Begin with the puzzle, because it is genuinely strange.

The CLARITY Act has cleared the procedural hurdles that kill most legislation. It advanced through the House with broad bipartisan support, survived markup in the Senate Banking Committee with two Democrats crossing over to join Republicans in a 15-to-9 vote, and landed on the Senate legislative calendar, meaning it is formally ready for floor consideration.

Behind it stands an unusually unified industry. Hundreds of crypto companies and organizations have publicly pressed Senate leaders to bring it to a vote, arguing that clear federal rules are needed to keep digital-asset innovation in the U.S.

By the normal measures of legislative momentum, this is a bill on track.

And yet it has not moved to a floor vote, and the window to do so is closing. The reason is not that the Senate cannot agree on how to regulate crypto.

The core architecture of the bill, which divides oversight between regulators and gives the market the legal certainty it has long wanted, commands fairly broad support.

As crypto.news previously explained in the bill explained in full, the CLARITY Act is designed to create defined lanes for digital assets rather than leave the market trapped between agencies.

The bill is stuck on two provisions that have little to do with that core architecture, and the deeper of the two has nothing to do with crypto regulation at all.

It concerns ethics, specifically whether the law should restrict government officials, up to and including the president, from profiting on the very digital assets the law would legitimize.

That question has fractured the fragile coalition the bill needs, and it has done so at the worst possible moment, against a hard deadline.

The bill that should pass cannot, because it has become entangled with the president’s personal financial interests in a way its authors did not design and cannot easily escape.

What the CLARITY Act would do

To understand what is at stake, it helps to know what the bill actually does, because the prize is substantial and explains why the industry is so eager.

The CLARITY Act creates a comprehensive federal framework for digital assets, resolving the long-running uncertainty over which regulator oversees what.

In broad terms, it grants the commodities regulator primary jurisdiction over the spot markets for digital commodities, assets that function more like commodities than securities, while leaving the securities regulator in charge of assets sold as investment contracts.

For tokens like the major cryptocurrencies, this would provide the clear legal classification the industry has sought for years, removing the cloud of uncertainty that has hung over the market and deterred some institutional participation.

The bill also creates new pathways for crypto projects to raise money and operate within defined legal boundaries, including a tailored exemption that lets certain projects raise capital from the public without the full weight of traditional securities requirements, subject to disclosure rules and caps.

The overall effect would be to bring the American crypto market inside a defined regulatory perimeter, with clear rules for who is overseen by whom, how tokens are classified, and what protections apply to consumers.

For an industry that has spent years operating amid legal ambiguity, and watching some activity move offshore as a result, this clarity is the entire point.

It is why hundreds of companies are lobbying for passage, and why supporters argue that failing to pass it would leave the U.S. behind as other jurisdictions write their own rules.

That comparison matters because how other regions wrote their rules has become part of the pressure campaign in Washington. Europe has MiCA, stablecoin issuers have the GENIUS Act framework, and the U.S. market still lacks a full digital-asset structure.

The substance of the bill, in other words, is broadly what the industry wanted. The trouble lies in the provisions attached around it.

The two obstacles

Two distinct disputes have blocked the bill from a floor vote, and it is worth distinguishing them, because they are different in kind.

The first concerns a provision, carried over from a separate piece of legislation and folded into the bill, that shields software developers who do not control customer funds from being treated as money transmitters subject to certain financial-crime obligations.

The crypto industry considers this provision essential, arguing that developers who merely write code, without ever holding anyone’s money, should not face the legal exposure of a money-transmitting business. Without this protection, builders argue the broader bill would fail to deliver the certainty they need.

Opposing it, several law-enforcement organizations and other groups have warned that the exemption is too broad and could create blind spots that sophisticated criminals exploit, making it harder to trace illicit activity.

This is a substantive policy disagreement, and it is negotiable in the ordinary way, through tighter drafting and compromise language.

The second obstacle is the one this piece focuses on, because it is deeper and far harder to resolve.

It concerns ethics, and specifically whether the law should bar senior government officials, including the president, the vice president, and members of Congress, from issuing, promoting, or profiting from digital assets while in office.

This dispute is not really about how to regulate crypto. It is about whether a crypto law should constrain the people writing and enforcing it, at a moment when the most powerful of those people has a large personal stake in the industry.

Where the developer-shield fight is a technical disagreement that careful drafting might bridge, the ethics fight runs into something structural and personal: the president’s own crypto business, and the question of whether the rules should touch it.

That is why, of the two obstacles, the ethics one has proven the more intractable, and why it, more than anything in the bill’s actual crypto provisions, now threatens to sink the whole effort.

The president’s crypto empire

To understand the ethics fight, you have to understand the scale and nature of the president’s involvement in crypto, which is unprecedented for a sitting head of state and which both sides acknowledge as a fact even as they dispute its significance.

President Trump and his family hold crypto interests that have been estimated at roughly $2.3 billion, with some broader estimates running considerably higher.

The holdings span several ventures. There is World Liberty Financial, a crypto venture the Trump family launched in 2024, in which the family holds a large ownership stake and which issues a dollar stablecoin called USD1.

There is the TRUMP memecoin, a token bearing the president’s name that trades largely on political news and has been highly volatile. And there are further crypto-adjacent ties through the family’s media company, including an arrangement involving a major exchange.

That is why the USD1 stablecoin at issue is not just another stablecoin in this debate. It sits at the intersection of crypto policy, payment regulation, and presidential financial exposure.

Several features of these holdings have drawn particular scrutiny.

The stablecoin venture received a large investment from a fund linked to a foreign government for a significant ownership stake, a transaction that routed substantial sums to entities associated with the family, and the same stablecoin was used in a multibillion-dollar transaction involving a major exchange whose founder was later pardoned by the president.

Critics point to the timing and structure of these deals as raising questions about whether regulatory and policy decisions and private financial interests have become entangled.

Supporters and the White House dispute that characterization.

What is not in dispute is the basic situation: a sitting president and his family have a large, active financial stake in the crypto industry, at the same time that the president’s administration is shaping crypto regulation and enforcement.

It is that overlap, unprecedented in modern times, that the ethics fight in the CLARITY Act is ultimately about.

The conflict at the center of the bill

The concern that critics raise is, at its core, a conflict-of-interest argument, and it is worth stating in the terms its proponents use.

The objection is that the same administration writing and enforcing crypto rules is personally exposed to those rules, which creates at least the appearance, and potentially the reality, of decisions being shaped by private financial interest rather than public good.

Ethics experts, watchdog organizations, and Democratic lawmakers have argued that a president whose personal wealth is tied to crypto ventures has an incentive to favor policies and enforcement choices that benefit those ventures.

They also argue that allowing such an arrangement to stand without guardrails sets a troubling precedent.

Some have characterized specific transactions, particularly the foreign investment in the stablecoin venture, as self-dealing, and have warned about the entanglement of a sitting president’s personal finances with assets the government regulates.

From this vantage, the logic of insisting on ethics provisions in the CLARITY Act is direct.

If the law is going to legitimize and regulate digital assets, the argument goes, it should also ensure that the officials overseeing that regulation cannot personally profit from it, precisely because the current situation shows how real the conflict can become.

Democratic senators have made this case the basis of their conditional support, with one prominent senator stating flatly that there is no version of the bill she will support without ethics language addressing it.

The concern, in this framing, is not partisan obstruction but a principled insistence that a law regulating an industry should not enrich the people enforcing it.

Whether one finds this argument compelling or overstated, it is the substance of the objection, and it is what has made the ethics provisions a condition rather than a preference for the senators whose votes the bill needs.

The White House and Republican response

The other side of the dispute deserves equal weight, because the White House and its allies have substantive responses, and the disagreement is genuine instead of one-sided.

The central counterargument, advanced by the administration’s crypto policy lead, is that ethics limits should apply uniformly to all officials and should not be written to single out the president or his family.

From this view, crafting provisions targeted at one administration is itself improper, a politicization of what should be a neutral market-structure bill, and the appropriate approach is general ethics rules applied evenly instead of bespoke language aimed at a particular person.

The White House has stated directly that the president has acted in the public interest and that there are no conflicts of interest, rejecting the premise of the critics’ case.

Republicans have added a jurisdictional argument, contending that sweeping ethics provisions restricting officials’ financial conduct fall outside the proper scope of a banking and market-structure bill, and belong, if anywhere, in dedicated ethics legislation instead of bolted onto a crypto framework.

They have also emphasized the cost of letting the ethics dispute sink the whole bill, arguing that the country needs the regulatory clarity the CLARITY Act provides and that allowing a fight over the president’s holdings to block it would harm the broader industry and cede ground to other jurisdictions.

The companies and individuals named in connection with specific transactions have, for their part, disputed the characterizations of those deals as conflicts, offering their own accounts of how and why they occurred.

The result is a real clash of principles: one side insisting that a crypto law must restrain officials who profit from crypto, the other insisting that singling out the president is improper and that the bill’s substance should not be held hostage to that fight.

Both positions have coherent logic, which is part of why the impasse has been so difficult to resolve.

Why this is so hard to break

The reason the ethics dispute has proven nearly intractable, where the technical disagreements in the bill are negotiable, is that it sits on a genuine structural conflict that compromise language struggles to dissolve.

The fault line runs straight through the coalition the bill needs.

Because passage in the Senate requires clearing a 60-vote threshold, the bill needs support from several members of the minority party, and the Democratic senators whose votes are in play have tied their support to meaningful ethics guardrails.

Meanwhile, the White House and Republican leadership have resisted provisions they see as targeting the president.

These positions are not easily reconciled, because the thing one side considers essential, language that would restrain officials including the president from profiting on crypto, is close to the thing the other side considers unacceptable, language singling out the president.

An attempt to write a provision strong enough to satisfy the senators demanding guardrails tends to be exactly the kind of provision the White House rejects, and vice versa.

The negotiations have borne this out. A committee amendment that would have barred senior officials from holding crypto business interests failed on a party-line vote, signaling that the dispute splits cleanly along partisan lines instead of admitting an easy middle.

A separate effort to craft an enforcement mechanism collapsed when it was withdrawn, leaving the central question unresolved.

Each attempt to find compromise language has run into the same wall: the gap is not really about wording but about whether the rules should reach the president’s business at all, and that is a question of principle, not phrasing.

Add the personal and political stakes, in which any provision becomes a referendum on the president’s crypto dealings, and the difficulty compounds.

This is why a bill that commands broad agreement on its actual crypto provisions cannot get to a vote.

The obstacle is not a drafting problem that a skilled negotiator can solve over a weekend. It is a structural conflict between the votes the bill needs and the interests of the administration whose cooperation it also needs.

The clock, and what comes next

All of this is now racing against a hard deadline, which is what gives the impasse its urgency.

The practical window to pass the bill runs up against the Senate’s summer recess, and the consensus among those tracking it is that if the CLARITY Act does not clear the Senate before that recess, its prospects deteriorate sharply.

Some of the bill’s own architects have suggested that a failure to act could push comprehensive crypto legislation back by years.

Negotiators have set out a compressed timeline, aiming to publish updated text and then move to floor action within weeks, but the ethics dispute has already caused a target to sign the bill earlier in the summer to collapse.

The calendar is unforgiving, with the Senate facing competing legislative demands for its limited remaining time.

The market for predictions reflects the uncertainty. Wagering on whether the bill passes this year has fallen sharply over the course of a month, from comfortable odds to roughly a coin flip, as the ethics and developer-shield disputes hardened.

Independent analysts have likewise moved toward viewing passage as genuinely uncertain instead of likely.

The path forward, if there is one, runs through some compromise on the ethics language credible enough to win the Democratic votes the bill needs without provoking the White House into withdrawing support, a needle that has so far proven extremely difficult to thread.

What happens next will be decided not by any argument over how to regulate digital assets, on which the bill is largely settled, but by whether the parties can resolve a fight about the president’s personal crypto interests under intense time pressure.

If they can, the U.S. gets its long-awaited crypto framework. If they cannot, the most consequential crypto legislation in years may die not over crypto, but over the crypto business of the man whose signature it would require.

That is the irony at the center of the whole affair, and it is the truest summary of where the CLARITY Act stands: its obstacle was never the technology. It was the president’s stake in it.

Frequently asked questions

What is the CLARITY Act?

The CLARITY Act is a U.S. crypto market-structure bill that would set up a comprehensive federal framework for digital assets. It resolves which regulator oversees what, broadly granting the commodities regulator primary jurisdiction over digital-commodity spot markets while keeping the securities regulator over assets sold as investment contracts, and it would create defined pathways for crypto projects to raise money and operate.

For the industry, it would deliver the long-sought legal clarity that removes regulatory uncertainty. It has cleared the House and the Senate Banking Committee and reached the Senate calendar, but it has not yet received a floor vote.

Why is the CLARITY Act stuck if it has the votes?

Because two provisions attached around the bill’s core have fractured the coalition it needs, and the deeper one concerns ethics instead of crypto. The core crypto framework commands fairly broad support, but the bill has stalled over a developer-protection provision that law enforcement opposes and, more intractably, over whether the law should restrict officials, including the president, from profiting on crypto. The second dispute runs into the president’s own large crypto holdings, making it a fight about personal financial interests instead of crypto policy, which is far harder to resolve through ordinary compromise.

What are the president’s crypto holdings?

President Trump and his family hold crypto interests estimated at roughly $2.3 billion, with some estimates higher. They include World Liberty Financial, a crypto venture in which the family holds a large stake and which issues the USD1 stablecoin, the TRUMP memecoin, and further crypto-adjacent ties through the family media company.

Particular scrutiny has fallen on a large investment in the stablecoin venture from a fund linked to a foreign government, and on the stablecoin’s use in a major exchange transaction. The basic fact, undisputed by both sides, is that a sitting president has a large active stake in the industry his administration regulates.

What is the conflict-of-interest concern?

Critics, including ethics experts, watchdog groups, and Democratic lawmakers, argue that the same administration writing and enforcing crypto rules is personally exposed to those rules, creating at least the appearance, and potentially the reality, of decisions shaped by private financial interest.

They contend a president whose wealth is tied to crypto has an incentive to favor policies benefiting those ventures, and that a law legitimizing digital assets should ensure officials cannot personally profit from it. Some have characterized specific transactions as self-dealing. This concern is the basis for Democratic senators conditioning their support on ethics guardrails.

How does the White House respond?

The White House and its allies argue that ethics limits should apply uniformly to all officials and not be written to single out the president, viewing targeted provisions as an improper politicization of a neutral bill. The White House has stated that the president acted in the public interest and that there are no conflicts of interest. Republicans add that sweeping ethics provisions fall outside the proper scope of a market-structure bill and belong in dedicated ethics legislation, and they warn that letting the dispute sink the bill would harm the industry and cede ground to other countries. Parties named in specific deals dispute that they were conflicts.

What happens if the CLARITY Act does not pass soon?

The practical deadline is the Senate’s summer recess. The consensus among those tracking the bill is that if it does not clear the Senate before then, its prospects deteriorate sharply, and some of the bill’s own architects have suggested failure could delay comprehensive crypto legislation by years. Passage requires a 60-vote threshold needing several Democratic votes, which are tied to ethics guardrails the White House resists. Prediction markets have moved from comfortable odds toward roughly a coin flip. If a credible compromise on the ethics language cannot be reached under time pressure, the bill may not pass this year.

This article is information, not legal, financial, or political advice. It describes a contested and fast-moving legislative situation, and presents the positions of the parties involved instead of endorsing any of them. Vote counts, holdings estimates, deadlines, and negotiations reflect reporting available as of June 26, 2026, and can change quickly. Verify current developments through primary sources.

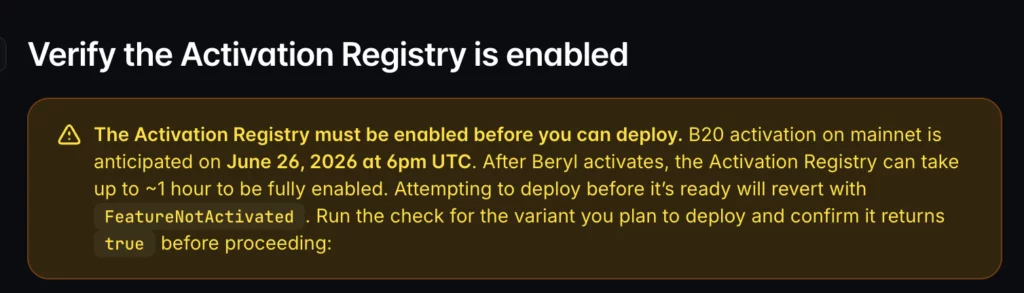

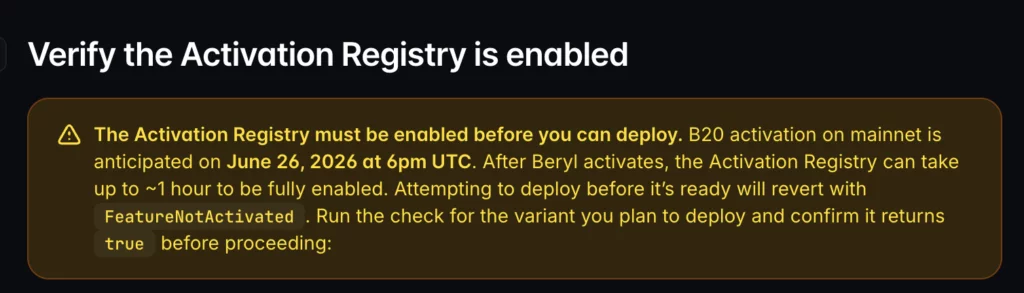

Base has delayed its Beryl mainnet upgrade by one day to ensure the B20 Activation Registry is fully operational before the hard fork goes live.

Summary

- Base postponed its Beryl mainnet upgrade to June 26 after delaying activation by one day to complete B20 Activation Registry initialization.

- Beryl introduces the native B20 token standard, cuts the standard Base to Ethereum withdrawal period from seven days to five days, and integrates Reth V2.

- Base said the recent two hour network outage was caused by a separate consensus issue and was unrelated to the Beryl upgrade.

Base announced that Beryl will now activate on mainnet on June 26 at 18:00 UTC instead of the previously scheduled June 25 launch.

Source: basedocs.

The Ethereum layer 2 network attributed the delay to a timing dependency involving the B20 Activation Registry, which must complete its initialization before developers can deploy native B20 tokens.

The network explained that the Activation Registry controls whether B20 feature flags become available after the hard fork. Base added that the registry can take up to one hour to come online after activation, making the additional delay necessary before the upgrade proceeds.

B20 rollout and withdrawal changes

Beryl is Base’s second independent network upgrade after Azul, which reached mainnet in May. The release introduces B20, a protocol level token standard that allows issuers to create stablecoins and real-world asset tokens directly within Base’s node software instead of deploying conventional ERC 20 smart contracts.

Base previously said B20 remains compatible with the ERC 20 specification and supports ERC 2612 permit functionality, allowing existing wallets, exchanges, and indexers to work without modification. The protocol also includes an Issuer Toolkit that offers role-based permissions, mint and burn controls, transfer restrictions, optional supply limits, and freeze and seizure features for regulated issuers.

The hard fork also shortens the standard withdrawal period from Base to Ethereum from seven days to five days for the route used by most bridging providers. Base has previously attributed the reduction to improvements introduced through Azul’s Multiproofs framework, which reduced reliance on the original fault-proof challenge window.

Beryl also integrates Reth V2, which the network said reduces storage requirements for nodes by up to 50% while supporting higher block gas targets.

Outage occurred before planned activation

Base originally scheduled Beryl for June 25, the same day the network experienced a block production outage that lasted for nearly two hours. The engineering team identified a consensus issue after an invalid block entered the sequencing pipeline and temporarily stopped new block creation.

Engineers restored normal block production later that day, while Base confirmed the incident was unrelated to the planned Beryl upgrade.

Base creator Jesse Pollak also stated that user funds remained safe during the outage while acknowledging that network halts were unacceptable for infrastructure intended to support global financial activity.

Base has scheduled its next network upgrade, Cobalt, for September. The company expects that release to introduce native account abstraction, protocol level smart accounts, gas sponsorship, transaction batching, additional B20 capabilities, and a unified node binary that combines consensus and execution clients.

Every time you send crypto from one exchange to another above a certain amount, your identifying information may travel with it, shared between the platforms behind the scenes. That is the Travel Rule, a decades-old banking standard now reshaping crypto. This guide explains what it requires, why it exists, and what it means for your privacy.

Summary

- The Travel Rule is an anti-money-laundering requirement that obliges crypto service providers to collect, share, and retain identifying information about the sender and recipient of transfers above a set threshold.

- It originated in traditional banking under the US Bank Secrecy Act and was extended to crypto in 2019 by the Financial Action Task Force, the global anti-money-laundering body.

- The information travels off-chain through secure messaging between providers, so it does not appear on the blockchain itself, and it applies to exchanges, custodial wallets, and similar businesses, not direct peer-to-peer transfers.

- Thresholds vary widely by country, from the US figure of $3,000 to the European Union’s zero threshold, where every transfer requires compliance regardless of amount.

- The rule reduces the anonymity once associated with crypto and raises privacy and data-security questions, while its uneven global adoption, known as the sunrise problem, leaves gaps in enforcement.

The Travel Rule is an anti-money-laundering requirement that obliges financial institutions and crypto service providers to collect, share, and retain identifying information about both the sender and the recipient of a transfer above a certain value, so that the data effectively travels alongside the transaction. In the crypto context, this means that when you send digital assets above a threshold from one regulated platform to another, your platform may be required to transmit details about you, and to receive details about the recipient, behind the scenes.

The name comes from this idea of information traveling with the transfer, and the concept is not new: it has governed bank wire transfers for decades. What is new, and what makes it one of the most consequential pieces of crypto regulation in 2026, is that the same standard now applies to virtual assets, bringing crypto transfers under the kind of anti-money-laundering scrutiny long applied to traditional bank wires

For users accustomed to thinking of crypto as private or pseudonymous, the Travel Rule represents a significant shift, because it weaves identity and traceability into transfers that once felt anonymous.

Understanding the Travel Rule matters because it sits at the intersection of three related concepts that often get confused: know-your-customer checks, anti-money-laundering frameworks, and the specific obligation to share counterparty information on transfers. It also has real, practical consequences for how exchanges operate, what information they must gather from you, and how much privacy you can expect when moving crypto between regulated platforms.

This guide explains where the Travel Rule came from, how it was extended to crypto, exactly what information must be shared and how, who is covered and who is not, the wide variation in thresholds across countries, how the rule fits together with know-your-customer and anti-money-laundering obligations, a concrete worked example, and the genuine limits and privacy questions the rule raises.

The goal is to give you a clear picture of a regulation that increasingly shapes the everyday experience of using crypto, without either downplaying its reach or exaggerating its grip.

Where the Travel Rule came from

The Travel Rule did not begin with crypto; it began with banks, and its history explains both its logic and its name. In the United States, the rule traces back to the Bank Secrecy Act, the long-standing law designed to combat money laundering, and to guidance issued by the Financial Crimes Enforcement Network in the 1990s.

For decades, banks have been required to include identifying information, such as names and account numbers, when they pass funds from one institution to another in a wire transfer above a certain amount. The purpose was straightforward: by making identifying information travel with the money, regulators gained the ability to trace funds and flag suspicious activity, creating an auditable trail that makes it harder for illicit money to move undetected through the financial system. This original Travel Rule applied to traditional financial institutions and the wires they sent between one another.

When cryptocurrency emerged, and transactions began happening globally and at scale, regulators recognized that the same money-laundering risks applied, and that crypto’s pseudonymity could make it attractive for moving illicit funds.

The body that drove the extension to crypto is the Financial Action Task Force, an international organization that sets anti-money-laundering standards that countries around the world adopt into their own laws. In 2019, the Financial Action Task Force updated its guidance, specifically a provision known as Recommendation 16, to make clear that the Travel Rule should apply to virtual assets and to the businesses that handle them.

This extension meant that crypto exchanges, custodians, and similar providers would need to follow rules similar to those long applied to banks, collecting and sharing sender and recipient information on qualifying transfers. The guiding principle the Financial Action Task Force articulated was same risk, same rules: activities that carry similar money-laundering risks should face similar standards regardless of the technology involved.

Since 2019, countries have been writing their own versions of the crypto Travel Rule into national law, which is why the rule now exists worldwide but with meaningful variations from one jurisdiction to the next.

What information must be shared, and how

The substance of the Travel Rule is the specific information that must accompany a qualifying transfer, and understanding it clarifies what the rule actually does. When a transfer crosses the relevant threshold, the service provider of the sender, often called the originator, must share identifying details about that sender with the service provider of the recipient, often called the beneficiary, and in turn receive the beneficiary’s details. The information typically includes the names of both parties, their account or wallet identifiers, and, in some cases, additional details such as a physical address or an identification number. The aim is to attach a verifiable identity to both ends of the transfer so that, if needed, authorities can trace who sent value to whom.

A point that often surprises people is where this information goes, and the answer is that it does not go on the blockchain. The Travel Rule data is shared off-chain, through secure messaging channels directly between the two service providers, rather than being written into the public ledger. This design preserves the efficiency and privacy characteristics of the blockchain transaction itself while still meeting the compliance requirements, since the sensitive personal information moves through a separate, private channel between the regulated institutions. To make this work across a global industry, the sector has developed standardized messaging formats and protocols that let different providers exchange the required data reliably, along with services that help a provider verify the identity of the counterparty institution before sending personal information to it.

These solutions address a genuine technical challenge: a provider must confirm that the receiving institution is who it claims to be and can handle the data securely before transmitting a customer’s personal details, because sending such information to the wrong party would itself be a serious problem. The result is an off-chain layer of identity infrastructure running alongside the on-chain transactions, invisible to most users but increasingly central to how regulated crypto transfers work.

Who is covered and who is not

A crucial question for any user is whether the Travel Rule applies to them, and the answer depends on whether a regulated intermediary is involved. The rule applies to the businesses that handle crypto on behalf of customers, known in the relevant frameworks by various labels: virtual asset service providers, crypto-asset service providers, or money services businesses, depending on the jurisdiction. The covered entities include crypto exchanges, custodial wallet providers, over-the-counter trading desks, crypto payment processors, and regulated financial institutions that deal in digital assets. The common thread is that these are intermediaries that accept and transmit customer value, and the obligation falls on them, not on individual users directly, though the practical effect is that users of these services must provide the identifying information the providers are required to collect and share.

Equally important is what the Travel Rule does not cover. It generally does not apply to direct peer-to-peer transfers between two private, self-hosted wallets, sometimes called unhosted wallets, where no regulated intermediary is involved, because there is no service provider in the middle to collect and transmit the data. That said, the picture is more nuanced at the edges: when a regulated provider sends funds to or receives funds from an unhosted wallet, the provider may still be required to collect information about the transfer even if it cannot share it with a counterparty institution that does not exist.

Decentralized finance protocols and other non-custodial services occupy a genuinely ambiguous space because they often lack a clear intermediary to bear the obligation, and regulators are actively exploring how, or whether, to extend the rules to them. For most ordinary users, the practical takeaway is that transfers between regulated exchanges and custodial services are squarely within the rule’s scope and will involve information sharing, while transfers between two wallets you control personally generally are not, even as the boundaries around decentralized and self-custodied activity remain unsettled and under regulatory review.

How thresholds vary around the world

One of the most important practical features of the Travel Rule is that there is no single global threshold or authority; instead, each jurisdiction sets its own rules, and the variation is substantial. In the United States, the Travel Rule derives from the Bank Secrecy Act and is enforced by the Financial Crimes Enforcement Network, with a long-standing threshold of three thousand dollars for the obligation to attach identifying information, although proposals have circulated to lower that figure significantly for international transfers.

The European Union has taken the strictest approach through its Transfer of Funds Regulation, which took effect at the end of 2024 and applies a zero threshold to crypto transfers, meaning that every single crypto transfer between providers, regardless of amount, requires full Travel Rule compliance. This regulation operates alongside the broader Markets in Crypto-Assets framework, together forming Europe’s comprehensive crypto compliance regime across all member states.

Other major jurisdictions fall at various points along this spectrum. The United Kingdom introduced its own Travel Rule requirements in 2023, applying them to all transfers regardless of amount. Canada enforces the rule through its financial intelligence agency with a threshold of around 1,000 Canadian dollars, making it relatively strict. Switzerland has adopted one of the toughest versions, requiring firms to identify both parties even for amounts below the thresholds used elsewhere, reflecting its emphasis on strict financial oversight.

Several Asian financial centers, including South Korea, Singapore, and Hong Kong, have implemented firm Travel Rule obligations, often pushing the industry toward standardized compliance technology, while other regions are still developing their frameworks. For users and businesses operating across borders, this patchwork is a genuine challenge, because the same transfer might be subject to full compliance in one jurisdiction and none in another, and a provider serving customers in multiple countries must navigate the strictest applicable requirements. The variation is not a sign of confusion so much as a reflection of how recently and unevenly the global standard has been adopted into national law.

How the Travel Rule fits with KYC and AML

The Travel Rule is often mentioned alongside know-your-customer and anti-money-laundering obligations, and clarifying how the three relate helps make sense of the broader compliance picture. Anti-money-laundering, usually shortened to AML, is the umbrella framework, the overall body of laws and practices designed to prevent the financial system from being used to launder the proceeds of crime or finance illicit activity. Within that framework sit specific obligations, and two of the most important are know-your-customer checks and the Travel Rule, which address different points in the lifecycle of a customer relationship and a transaction.

Know-your-customer, or KYC, refers to the process by which a service provider verifies the identity of its own customers, typically at the point of onboarding, by collecting documents and information to confirm who they are. It answers the question of whether the provider knows who its customer is. The Travel Rule addresses a different moment: it governs what happens when that customer makes a transfer, requiring the provider to share the customer’s identifying information with the counterparty provider on the other end of a qualifying transaction.

In other words, know-your-customer confirms identity at the door, while the Travel Rule makes that identity information move with transfers between institutions. The two interlock, because the provider can only share accurate sender information under the Travel Rule if it has properly verified that sender through know-your-customer in the first place. Sanctions screening adds a further layer, since providers must also check the parties to a transfer against sanctions lists to avoid processing transactions for prohibited persons.

Together, these obligations form a connected compliance system: know-your-customer identifies the customer, the Travel Rule shares that identity across transfers, sanctions screening checks it against prohibited lists, and the whole apparatus serves the overarching anti-money-laundering goal of keeping illicit funds out of the system.

A worked example: a transfer between two exchanges

A simple example makes the mechanics tangible. Suppose you hold Bitcoin on one regulated exchange, call it Exchange A, and you want to send an amount worth more than the applicable threshold, say more than $3,000 in a jurisdiction using that figure, to your account on another regulated exchange, Exchange B. When you initiate the transfer, the Bitcoin itself moves on the blockchain from Exchange A’s systems toward Exchange B’s, exactly as any Bitcoin transaction would. That part is visible on the public ledger, as Bitcoin transactions always are. What happens alongside it, invisibly to you, is the Travel Rule compliance.