Crypto World

Prediction Markets Pick Their FIFA World Cup Winner as Knockout Rounds Start

Bettors on Polymarket and Kalshi are favoring France as the most likely winner of the 2026 FIFA World Cup, edging out Argentina in both regulated and decentralized prediction markets.

On Polymarket, France leads the winner market at 23% probability, with Argentina close behind at 22%. Spain sits third at 11%, England fourth at 10%, and Brazil rounds out the top five at 6%.

Kalshi, the US-regulated prediction market, mirrors the same top-two order, with France at 20% and Argentina at 16%.

France and Argentina Dominate Prediction Capital

Together, France and Argentina account for more than 45% of all winning predictions on Polymarket. That concentration points to a genuine two-horse race in the eyes of most bettors.

France enters the later rounds as the statistical favorite, while Argentina, the defending world champion, draws strong backing from those who trust Lionel Messi’s squad to repeat.

This market pattern tracks what analysts identified earlier in the tournament. BeInCrypto’s FIFA World Cup money flow analysis found that capital clustered around a small group of elite nations from the opening group stage.

Meanwhile, Kalshi partnered with ADI and PredictStreet ahead of the tournament, expanding regulated soccer betting access for US users.

Record Attendance Marks a Commercial Breakthrough

Off the pitch, the 2026 tournament has already shattered records. FIFA confirmed that total stadium attendance has surpassed 3.6 million fans, a new high for any World Cup edition.

The expanded three-nation format, hosted across the United States, Canada, and Mexico, gave the tournament a wider venue footprint that made the record possible.

Fan token markets have moved in step with the excitement. World Cup fan tokens rallied sharply at the close of the group stage, reflecting demand from supporters following their national teams.

The broader World Cup betting action on Polymarket and Kalshi has also drawn mainstream attention as prediction platforms use the tournament to build name recognition.

FIFA Eyes a 64-Team Format for 2038

Beyond the current tournament, commercial momentum may drive structural changes. Sports Business Journal reports that FIFA is internally considering expanding to a 64-team format by 2038.

The existing 48-team structure, introduced at this edition, already stretched host nation logistics considerably.

For crypto traders, the timing carries a familiar signal. An analysis of the Bitcoin and FIFA four-year cycle found that prior World Cup years have historically aligned with above-average Bitcoin (BTC) returns.

Whether that pattern holds in 2026 may become clearer as the knockout rounds conclude.

The post Prediction Markets Pick Their FIFA World Cup Winner as Knockout Rounds Start appeared first on BeInCrypto.

Tether is expanding the use of Tether Gold as crypto lender Ledn adds support for XAU₮.

Summary

- Tether is expanding XAU₮ utility by bringing tokenized gold into Ledn’s lending platform this year.

- XAU₮ holders will be able to borrow against gold without selling the underlying tokenized bullion.

- The move follows Tether’s wider shift toward gold, Bitcoin mining, AI, and infrastructure assets.

The move will let users hold and trade tokenized gold on Ledn, with gold-backed loans expected later this year.

The plan extends Tether’s wider gold strategy at a time when tokenized bullion is gaining more use in crypto markets. Each XAU₮ token represents one fine troy ounce of physical gold stored in Swiss vaults.

XAU₮ joins Ledn’s lending platform

Ledn said it has added support for XAU₮ alongside Bitcoin, USD₮ and USA₮. The platform said users can now hold and trade XAU₮, while borrowing against the tokenized gold product will come later in 2026.

The product follows the same structure Ledn has used for Bitcoin-backed loans. Users can access liquidity while keeping exposure to the underlying asset instead of selling it for cash.

Ledn said client collateral remains held 1:1 and is not lent out or used to generate yield. That point matters after the 2022 crypto lending failures, when weak risk controls and rehypothecation hurt many customers.

The company said demand is growing for services that combine long-term asset ownership with financial flexibility.

“As digital assets become an increasingly important part of the global economy, demand is growing for solutions that combine long-term ownership with financial flexibility,” Tether CEO Paolo Ardoino said.

Tether expands its gold strategy

Tether Gold has grown sharply over the past year as demand for tokenized gold increased. Tether said XAU₮ reserves reached 707,747.139 fine troy ounces by March 31, 2026.

That was up from 520,089.350 fine troy ounces at the end of 2025. Tether said XAU₮’s market value rose from about $2.25 billion to more than $3.3 billion during the first quarter.

The wider $23 billion gold figure refers to Tether’s broader bullion position across its products. Reuters reported that Tether held about 132 metric tons of gold for USDT reserves at the end of March, valued near $19.8 billion, while XAU₮ accounted for about 22 tons.

Tether has also moved to focus more on XAU₮ after closing Alloy and aUSDT. As previously reported, users can redeem aUSDT and recover XAU₮ until Sept. 17 before Alloy support ends.

Gold-backed loans mirror Bitcoin lending

Gold-backed lending is not new in traditional finance. Banks, bullion dealers and large financial firms have long used physical gold as collateral.

Tether and Ledn are trying to bring that model into digital asset markets. Tokenized gold can move on blockchain rails while still tracking ownership of physical bullion held in custody.

This setup may appeal to users who want to keep gold exposure but still need liquidity. A borrower could use XAU₮ as collateral and receive stablecoins without selling the gold-backed asset.

The model also gives Tether another way to add use cases around XAU₮. Instead of acting only as a tokenized gold holding, XAU₮ could become collateral inside crypto lending markets.

Tokenized gold push widens

The Ledn plan follows other recent moves around Tether Gold. Tether and Fasset launched a Visa card with XAU₮ rewards, allowing eligible users to spend through the card and earn up to 6% cashback in tokenized gold.

That product placed XAU₮ closer to everyday payments. It also showed how Tether is testing uses for tokenized gold beyond storage and trading.

The company has also invested beyond stablecoins. Tether has backed Bitcoin mining, renewable energy projects, AI infrastructure, Gold.com and Antalpha as part of a wider technology and infrastructure push.

For Tether, the Ledn deal gives XAU₮ another practical role. Users may soon be able to borrow against tokenized gold in a structure closer to Bitcoin-backed lending, without giving up exposure to the underlying bullion.

Polymarket’s latest security incident has grown larger after blockchain intelligence firm AMLBot updated the estimated losses to about $3.1 million.

Summary

- Polymarket’s frontend phishing attack now shows $3.1 million in losses across 11 user wallets.

- The platform says a compromised third-party vendor injected malicious code into parts of its frontend.

- The refund pledge comes as lawmakers press regulators over alleged deceptive prediction market advertising practices.

The prediction market platform had earlier promised to refund affected users after saying a third-party vendor compromise allowed malicious code to reach some users through its frontend.

Hack losses rise to $3.1M

AMLBot said hackers stole about $3.1 million in PUSD from 11 user wallets. The firm said the funds were taken from Polygon and quickly bridged to Ethereum.

The update raises the loss figure from earlier estimates near $2.94 million. Specter Analyst had first flagged the attack as a phishing campaign that drained funds from at least 11 wallets holding PUSD.

Polymarket said in a June 25 post that it found a third-party vendor had been compromised. The company said the vendor issue allowed attackers to inject a malicious script into the platform’s frontend for some users.

“We’ve contained it & removed the affected dependency.” It also said it was contacting affected users and “refunding them in full,” the platform said.

Frontend attack targeted user wallets

The attack appears to have targeted users through the website interface rather than the core protocol. That type of attack can trick users into approving harmful wallet activity while they believe they are using the normal platform.

PeckShield said the attacker bridged stolen funds from Polygon to Ethereum and swapped them into about 1,893 ETH. Specter also said the funds were consolidated into an Ethereum address after the phishing activity.

A frontend attack can be difficult for users to detect in real time. The site may look normal, but the code loaded in the browser can create unsafe wallet prompts.

The incident also puts focus on third-party dependencies. Even if a platform’s smart contracts remain unchanged, outside code used in a website can create risk for users who connect wallets.

Earlier incidents add pressure

The latest incident follows other Polymarket security issues. In March, blockchain investigator ZachXBT flagged a suspected breach after more than $520,000 was reportedly drained from two Polygon smart contracts.

Polymarket later said funds were safe in that case. In December, the platform also confirmed an incident on its Discord channel after users reported missing funds and suspicious login attempts.

A previous report said the latest attack was recorded by DefiLlama as the 89th crypto security breach of the second quarter. The same report said that count made the quarter the highest on record by number of reported incidents.

The growing incident count shows why platforms now face closer checks across smart contracts, wallets, login systems, frontend code and outside vendors.

Regulatory scrutiny widens

The hack also arrives as Polymarket faces new regulatory attention. A recent report said U.S. Senators Adam Schiff and John Curtis urged the CFTC to review allegations tied to deceptive advertising practices.

The senators asked whether Polymarket promoted markets through simulated trading websites, staged transactions and undisclosed paid influencer campaigns. They also questioned whether the CFTC has enough tools to oversee prediction markets and protect users.

Polymarket and Kalshi are also part of a wider legal fight over sports event contracts. Kentucky has accused prediction market firms of offering unlicensed sports betting, while the CFTC has argued that federally regulated event contracts fall under its authority.

As previously reported, the cases may help decide whether sports-linked prediction markets answer mainly to federal derivatives rules or state gambling laws.

Binance founder Changpeng “CZ” Zhao says the crypto market’s weak 2026 cannot be blamed on one event.

Summary

- CZ says crypto’s 2026 sell-off has no single cause behind Bitcoin’s sharp yearly decline.

- AI funding, global tension and the four-year cycle now sit at the center of debate.

- CZ remains long-term bullish, saying demand for financial technology should keep growing across crypto markets.

He pointed to capital moving into AI, global tension and the usual crypto market cycle as possible reasons for the downturn.

Bitcoin has fallen sharply from its October 2025 peak above $126,000 and now trades near $60,000. The wider market has also struggled as investors reduce risk and move capital into other high-growth sectors.

CZ says there is no single cause

In a CoinDesk interview, CZ said there is no simple answer for why crypto has fallen so much in the first half of 2026. He said geopolitical tension, the AI boom and the four-year crypto cycle may all be weighing on prices.

The comments come after Bitcoin opened 2026 near $89,000, briefly moved above $96,000, and then dropped toward $60,000. That fall has raised new questions about whether the current market is following an old cycle or entering a new structure.

CZ said his long-term view has not changed. He said, “Over the long run, the industry will develop,” pointing to rising demand for financial technology and more digital transactions over time.

His view lines up with earlier comments that blockchain could become part of daily life within five years. As previously reported, CZ has argued that countries that fail to adopt blockchain and AI may face economic disadvantages.

AI draws capital from crypto

CZ said “new industries like AI” are taking some “hot money” away from crypto. He framed that movement as a temporary capital rotation, not a long-term rejection of digital assets.

The AI boom has become one of the strongest competing themes in global markets. Investors have pushed money into AI infrastructure, chips, cloud computing and robotics while crypto prices have weakened.

This shift has also changed market attention. A recent report on crypto search interest found that public interest fell to a one-year low even though Bitcoin remained far above its 2022 bear market bottom.

That weaker attention matters because retail demand often helps drive crypto rallies. When AI stocks attract more attention, crypto may struggle to find the same level of fresh demand.

Four-year cycle debate grows

CZ also pointed to the four-year crypto cycle as one reason for the decline. Bitcoin has often moved through boom-and-bust cycles linked to halving periods, liquidity shifts and investor behavior.

The question now is whether that cycle still works in 2026. A recent Bitcoin price prediction report noted that Bitcoin trades near $60,000, more than 50% below its 2025 peak, while traders debate whether the old cycle remains useful.

Another cycle analysis said Bitcoin’s drawdown from the October peak looked severe but still fit parts of past market behavior. The report also noted that analysts remain split over whether the downturn marks a normal cycle reset or the end of the bull market.

That debate remains open because institutional flows have changed Bitcoin’s market structure. Spot ETFs, corporate treasuries and derivatives now play a larger role than in earlier cycles.

Policy and prediction markets stay in focus

CZ also said U.S. crypto policy remains important, though he described bills such as the CLARITY Act as tactical steps rather than the only driver of long-term growth. A related report said the CLARITY Act could help bring more crypto activity back to the U.S. by giving firms clearer rules.

He also spoke about prediction markets, saying they can help price events and provide liquidity. CZ said prediction markets could be “good for the population,” while also noting that speculation exists in many financial products.

As previously reported, CZ has supported activity in the BNB Chain prediction-market sector. He praised Predict.fun’s acquisition of Probable as a move that could combine liquidity and talent.

For now, CZ’s message is cautious but not bearish on the long term. He sees the 2026 slump as the result of several pressures hitting the market at once, while still expecting the crypto industry to keep growing as financial technology demand expands.

Brad Garlinghouse said one word, “maybe,” and the XRP community heard a promise. Asked whether holders could get a piece of Ripple if it goes public, he nodded toward a “special arrangement.” This is what was actually said, what holders could realistically receive, and the downside almost nobody is talking about.

Summary

- Ripple chief executive Brad Garlinghouse said that “if and when” Ripple goes public, the company might do “something special” for XRP holders, then immediately added it was “not in the immediate term.”

- That hedged “maybe” was offered in response to a direct question, not volunteered as a plan, and he declined to commit to any mechanism such as a token buyback.

- Ripple and XRP are legally and financially separate assets: holding XRP grants no shares, no dividends, and no claim on Ripple’s corporate profits, and no bridge between the two currently exists.

- The mechanisms holders imagine, preferential IPO share access, long-term holding rewards, or tokenized Ripple equity, are all unannounced and face serious securities-law hurdles given XRP’s legal history.

- The overlooked risk is that a Ripple IPO could actually pressure XRP, by drawing institutional capital toward Ripple stock and pushing the company to monetize its escrow holdings to satisfy public-market investors.

One word from Ripple’s chief executive set the XRP community alight, and that word was “maybe.” Speaking on the “Crypto In America” podcast with journalist Eleanor Terrett, Brad Garlinghouse was asked the question XRP holders have wanted answered for years: if Ripple ever goes public, could the people who hold XRP get a piece of it. He did not say no. He gestured first at the indirect benefits Ripple already provides, then, pressed on whether the company would do something specific for holders in an initial public offering, he said, “Maybe, but that is not in the immediate term.”

That was the entire substance of it, a hedged possibility wrapped in a qualification, offered in answer to a direct question rather than announced as a plan. And yet within hours it had been clipped, shared, and reshaped across XRP social media into something close to a corporate commitment, with community members urging one another to “hold accordingly.” The gap between what Garlinghouse actually said and what the community heard is the real story here, because the difference between a hinted-at maybe and a planned reward is the difference between a reasonable hope and a misplaced expectation.

The reason the remark landed so hard is the situation it landed into. XRP holders have spent 2026 watching Ripple collect exactly the kind of institutional wins the community long predicted, settlements with JPMorgan, stablecoin launches with major partners, a steady drumbeat of bank deals, while the token itself has stayed pinned near a dollar and change, beneath every major moving average. That combination, corporate triumph paired with token stagnation, breeds a particular hunger: the sense that the wins are real but are somehow not reaching holders, and that some missing mechanism could finally connect the two. Into that hunger dropped Garlinghouse’s nod, and it did what a catalyst does in a starved market.

This piece separates the hope from the reality. It covers exactly what was said and the precise wording that matters, the crucial distinction between Ripple the company and XRP the token, the mechanisms a holder benefit could theoretically take and why each is harder than it sounds, why Ripple may not even go public soon, the indirect benefit Ripple genuinely does provide, and the downside almost nobody is discussing: that an IPO could actually work against XRP. The goal is the real picture, neither dismissing the possibility nor inflating it into the certainty the hype implied.

What Garlinghouse actually said

Precision matters here, because the entire community reaction rests on a few carefully chosen words, and those words were more conditional than the excitement suggested. Garlinghouse did not volunteer the remark; he was asked directly whether XRP holders could share in Ripple’s success if the company eventually launched an initial public offering. His first instinct was to point to the indirect benefit Ripple already provides, saying he hopes XRP holders feel they benefit from Ripple’s existence through the work the company does to grow the XRP ecosystem. Only when pressed on whether Ripple would do something specific for holders in an IPO scenario did he offer the line that ignited everything: “Maybe, but that is not in the immediate term.”

When pushed further on concrete mechanisms, including a possible token buyback, he declined to commit to any of them, pointing back instead to what Ripple already does for the ecosystem. So the full extent of the supposed promise is a “maybe,” qualified as not near-term, given in response to a direct question rather than offered as a plan, with no program described, no mechanism named, and no action committed to. The community heard “Ripple will do something special for holders.” What Garlinghouse actually said was closer to “maybe someday, if we go public, which is not happening soon.”

Those are not the same statement, and stacking the two conditionals reveals how far the exciting headline sits from anything concrete: a possible benefit, attached to a possible IPO, that he himself describes as not a priority. It is worth adding that days earlier, at an industry conference, Garlinghouse had been cooler still on the idea of going public at all, emphasizing that staying private gives Ripple flexibility. Read in that context, the podcast remark was a hint, not a plan and certainly not a promise. Any honest assessment of what holders would actually get has to begin from that fact rather than from the amplified version that spread online.

Ripple is not XRP: the distinction that decides everything

To understand why this question is so charged, and so easily misunderstood, you have to grasp a distinction that still confuses many people: Ripple and XRP are legally and financially separate assets, and owning one does not mean owning the other. Ripple is a private technology company that builds payment and liquidity products, some of which use the XRP Ledger. XRP is a cryptocurrency, the native asset of the XRP Ledger, which is a decentralized, open-source blockchain that Ripple does not control. Holding XRP gives you ownership of that token and nothing else.

It confers no shares in Ripple, no dividends, no voting rights, and no claim whatsoever on Ripple’s corporate profits or assets. The two are different things with different value drivers, and the price of one does not automatically move the other. That distinction is why the company-versus-token gap keeps resurfacing across Ripple’s 2026 story. Ripple can win institutional business, launch products, and deepen its corporate value without automatically delivering a direct benefit to XRP holders.

This separation is the foundation of the entire holder-payout question, because it means there is no existing structure, no dividend, no buyback mechanism, no holder-equity bridge, that currently connects Ripple’s corporate fortunes to the people who hold XRP. Any such benefit would require a deliberate corporate decision: Ripple choosing to extend something to holders of a token that is legally distinct from its stock. That is precisely what makes Garlinghouse’s “maybe” notable, because it gestures at the possibility of Ripple voluntarily building a connection that does not exist and is not required to exist. The community’s hope is that Ripple might someday decide to construct that bridge.

The reality is that no bridge exists today, none is planned, and the entire question is whether Ripple might ever choose to build one. Everything that follows, every imagined mechanism and every obstacle, flows from this single fact: a Ripple IPO would, by default, do nothing for XRP holders, because the token and the company are separate. Only an affirmative, deliberate choice by Ripple could change that. Until such a choice is announced, a holder payout remains speculation, not entitlement.

The mechanisms holders imagine

Once the “maybe” spread, the community began filling in the blank with specific mechanisms, and it is worth laying them out, because they define the range of what “something special” could plausibly mean. The most discussed idea is preferential access to IPO shares, an arrangement in which verified long-term XRP holders, or users staking on the XRP Ledger, would be granted priority subscription rights to buy into a Ripple offering at favorable terms before the general public. This is the version that most directly answers the community’s wish, because it would let XRP holders transition, at least partly, into Ripple shareholders. It would turn token loyalty into an equity stake.

A second imagined mechanism is a long-term holding reward, a community-based structure that would give some benefit to holders who have kept XRP for a defined period, rewarding loyalty without necessarily handing over equity. A third, more technically ambitious idea is tokenized Ripple equity: a blockchain-based representation of Ripple stock made available to eligible token holders, which would use the very tokenization technology the industry is racing to build in order to bridge the gap between Ripple shares and XRP. Some in the community have also floated the notion of an “equity-token-bound” proof of entitlement, a digital claim linking XRP holding to some future right in Ripple. Each of these would, in its own way, construct the bridge between Ripple equity and XRP holders that currently does not exist.

The crucial thing to hold in mind is that all of them remain imagined, not announced. Garlinghouse named none of them; he declined, in fact, to endorse any specific structure when asked. They represent the community’s wish list of what “something special” might be, not a menu Ripple has offered. The distance between a fan’s plausible idea and a company’s actual program is considerable, especially when the imagined benefit touches securities law, global compliance, investor eligibility, and the legal separation between Ripple equity and XRP.

Why each mechanism is harder than it sounds

The reason Garlinghouse spoke in hints instead of specifics is almost certainly that nearly every concrete version of a holder benefit collides with serious obstacles, and understanding those obstacles is essential to a realistic view. The largest is securities law, and it is a particularly sharp problem for XRP of all tokens. Linking a cryptocurrency’s holding to equity benefits raises exactly the kind of securities-law questions that defined Ripple’s long and costly legal battle, the years-long fight over whether XRP sales amounted to unregistered securities transactions. Building a formal bridge that rewards XRP holders with equity or equity-like rights risks recreating the very entanglement between the token and the company that Ripple spent years and enormous legal resources trying to separate.

The company would have to navigate that terrain with extreme care, because a poorly designed holder-benefit program could reintroduce the argument that XRP is a security tied to Ripple’s enterprise, which is the last thing Ripple wants. That is why the catalyst that matters more than the IPO is still statutory clarity from the CLARITY Act, not an undefined corporate reward. Federal clarity can strengthen XRP’s status without blurring the line between the token and Ripple equity. A holder-equity program, by contrast, could blur that line if designed carelessly.

Beyond securities law, the practical obstacles multiply. A preferential-share program would require verifying who is a genuine long-term holder, drawing cutoff lines that would inevitably be seen as arbitrary or unfair, and managing the identity and compliance machinery to do it at scale across a global, pseudonymous holder base. A holding-reward structure raises questions of how to fund it and how to avoid favoring large holders over small ones. Tokenized equity would face the full weight of securities regulation governing who can own and trade company stock, plus the technical and legal work of making a regulated equity instrument function on a blockchain.

Each mechanism, in other words, is not just a matter of Ripple deciding to be generous; it is a tangle of legal exposure, fairness problems, and operational complexity, any one of which could sink it. This is why the most dramatic interpretations of “special arrangement” are also the least likely. A sober reading has to weight the modest possibilities, a governance gesture, a symbolic recognition, or simply Ripple structuring its business so more value flows through XRP over time, far more heavily than the windfall the community imagined.

Why Ripple may not even go public soon

The entire holder-benefit scenario is downstream of a prior question that often gets lost in the excitement: will Ripple even go public at all, and if so, when. On this, Garlinghouse has been consistent and notably unenthusiastic. He has repeatedly described an IPO as not a priority, and his reasoning is grounded in the current state of the public markets for crypto companies. He has pointed to the underwhelming performance of crypto-related public listings, citing peers whose post-listing stock has struggled, and noted reports that at least one major exchange had delayed its own listing plans.

His view, in short, is that the public markets have not treated Ripple’s peers well, and that there is little reason to rush into that environment. He has also made a positive case for staying private, arguing that it preserves flexibility, including, he joked, the freedom to speak openly without lawyers drafting every word. This is not the posture of a company on the verge of ringing the opening bell. It means the holder-benefit question is built on a foundation that is itself uncertain: a possible reward contingent on an IPO that the chief executive describes as neither planned nor imminent.

That is the sense in which the whole thing is a maybe attached to a maybe. For an XRP holder weighing what they might receive, this is the most important practical point, because even the most generous imaginable holder benefit is irrelevant unless and until Ripple actually decides to go public. By Garlinghouse’s own account, that decision is not on the calendar. The community’s hope therefore rests on two sequential uncertainties: first that Ripple goes public, and second that, having done so, it chooses to extend something to holders it is under no obligation to help.

Either link breaking is enough to make the whole scenario evaporate. That is why the IPO hint should not be treated like a near-term catalyst, even if it tells holders something about how Ripple thinks about its community. The comment matters as a signal of openness, but it does not change the current legal structure, the current IPO timeline, or the current token economics. XRP holders should separate those categories carefully.

The indirect benefit Ripple already provides

Set against the speculation is Garlinghouse’s actual, stated position, which deserves a fair hearing because it is not a trivial argument: that XRP holders already benefit from Ripple’s existence, indirectly but intentionally. The foundation of this argument is a simple fact: Ripple is the largest single holder of XRP. That gives the company a stronger economic incentive than anyone else to increase the token’s value and adoption, because Ripple profits when XRP rises, just as holders do. Its incentives are genuinely aligned with holders, even without any formal program linking the two.

Every commercial partnership Ripple pursues, every payment corridor it opens, every institutional deal it closes, and every regulatory battle it fights is evaluated, at least in part, through the lens of how it drives XRP utility and liquidity. Garlinghouse’s framing is that this alignment is the real benefit, that Ripple’s entire strategy is built around making XRP the most useful, liquid, and trusted digital asset in payments and settlement, and that by growing the ecosystem it makes what holders own more valuable, even without a dividend or an equity link. That is where XRP’s actual utility remains central to the long-term case. The token’s real thesis has to rest on usage, liquidity, and settlement demand, not on implied ownership of Ripple.

Garlinghouse has pointed to concrete examples of this posture, including Ripple’s backing of XRP treasury companies such as Evernorth, which is working to build a large XRP treasury business with Ripple’s support, an effort Garlinghouse frames as helping XRP holders, the XRP community, and Ripple shareholders at the same time. This argument has genuine merit and should not be dismissed as spin. The company’s commercial work plausibly does increase XRP’s utility and demand over time, which is a real, if diffuse, benefit to anyone holding the token. The counterpoint, and the reason the “maybe” resonated, is that many in the community find this indirect alignment insufficient.

They want a concrete share of Ripple’s corporate success, not an incentive structure that may or may not translate into token-price appreciation. That dissatisfaction is precisely the nerve Garlinghouse’s remark touched. His indirect-benefit argument is, in effect, his answer to it: you already benefit, just not in the direct way you want. Whether that answer satisfies holders depends on whether Ripple’s wins eventually become visible in XRP demand rather than simply in Ripple’s corporate valuation.

The downside nobody mentions: an IPO could hurt XRP

Here is the part of the story that the bullish excitement almost entirely skips: a Ripple IPO is not unambiguously good for XRP, and there is a credible case that it could actively work against the token, at least in the near term. The first channel is competition for capital. Today, an institution that wants exposure to Ripple’s success has essentially one liquid way to get it: buy XRP, the token associated with the company’s ecosystem. If Ripple goes public, that changes.

Suddenly there is a direct way to own a piece of Ripple itself, a regulated equity that offers what a token cannot: potential dividends, audited financial transparency, ownership of the company’s actual assets and cash flows, and the compliance comfort of a listed stock. Faced with that choice, institutional capital that might have flowed into XRP as a proxy for Ripple could instead flow into Ripple stock, siphoning off the very institutional demand the XRP bull case depends on. The IPO, in this reading, would give the market a cleaner instrument for the Ripple thesis, and XRP could lose its role as the default vehicle for it. That is the uncomfortable side of where XRP trades while holders wait: the market wants direct token demand, not merely a story about Ripple’s corporate success.

The second channel is selling pressure from Ripple itself. As a private company, Ripple has long been criticized for selling XRP from its large escrow holdings, a persistent source of new supply. After an IPO, that pressure could intensify instead of ease, because a public company answers to Wall Street’s quarterly demands for cash flow and profitability. To satisfy those demands and bolster its financial reports, Ripple’s board could face strong incentives to monetize tens of billions of XRP from its escrow accounts in a more systematic and aggressive way, creating an invisible, long-term overhang on the token’s price.

None of this is certain, and a well-managed IPO could be handled in ways that limit these effects, but the point is that the community’s framing of an IPO as pure upside for holders is incomplete. The honest version acknowledges that going public is a double-edged sword for XRP. It could, in the bullish case, come bundled with a “special arrangement” that rewards holders, or it could, in the bearish case, drain attention and capital away from the token while increasing the supply pressure on it. Holders hoping for the first should at least weigh the second.

What it means for holders today

So what should an XRP holder actually take from all of this, standing in the present with the token trading near a dollar and the “special arrangement” still nothing more than a hedged remark? The disciplined answer is to give the IPO hint the weight it actually carries, which is to say very little, and to keep attention on the catalysts that truly move XRP. A possible IPO reward is a weak basis for any decision, because it is a maybe attached to a maybe: an unplanned, undefined benefit contingent on an IPO that Ripple does not prioritize. It is better regarded as a distant possible upside not to be counted on than as a catalyst to position around.

The things that will actually determine XRP’s path are observable and concrete: whether the CLARITY Act passes and writes XRP’s commodity status into federal law, whether spot ETF flows compound or trickle, whether the network’s settlement usage grows enough to translate into real token demand against the escrow supply, and where Bitcoin drags the broader market. Those are the signals worth watching, and the IPO hint is not among them. This does not mean the remark is meaningless. It reveals something real about Ripple’s posture toward its community, a willingness to at least entertain the idea of connecting corporate success to holders, which is more than many companies would offer.

But revealing a posture is not the same as making a commitment, and the most useful thing a holder can do is to enjoy the signal for what it shows about Ripple’s attitude while declining to build any expectation on top of it. The community heard a promise. What Garlinghouse offered was a maybe, and in investing the difference is everything. An XRP holder is better served by evaluating the token on its actual merits, its use in payments, its regulatory position, its adoption, and its supply dynamics, than by speculating about an IPO reward that exists only as a hedged possibility.

That possibility is attached to an IPO that may never come, and that could, in some scenarios, hurt the token as much as help it. The hope is understandable. The discipline is to keep it in proportion. If Ripple ever announces a real program, holders can judge the terms then; until then, the “special arrangement” is a signal, not a strategy.

Frequently asked questions

Did Ripple promise XRP holders a payout from its IPO?

No. Ripple chief executive Brad Garlinghouse said that “if and when” Ripple goes public, the company might do “something special” for XRP holders, then immediately added that it was “not in the immediate term.” That was a hedged “maybe” offered in response to a direct question, not a plan, a program, or a commitment, and he declined to endorse any specific mechanism such as a token buyback. The community amplified the remark into something close to a promise, but no payout has been announced, no mechanism has been described, and the comment was explicitly conditional on an IPO that Garlinghouse describes as not a priority.

Does holding XRP give me any ownership of Ripple?

No. Ripple and XRP are legally and financially separate assets. Ripple is a private technology company that builds payment and liquidity products, some of which use the XRP Ledger. XRP is the native cryptocurrency of the XRP Ledger, a decentralized blockchain that Ripple does not control. Holding XRP grants no shares in Ripple, no dividends, no voting rights, and no claim on the company’s profits or assets.

What could a “special arrangement” actually look like?

The mechanisms the community imagines include preferential access to Ripple IPO shares for verified long-term XRP holders, long-term holding rewards for those who keep XRP for a defined period, and tokenized Ripple equity made available to eligible holders. All of these are unannounced and remain speculation instead of anything Ripple has offered. Each also faces serious obstacles, especially securities law, because linking token holding to equity benefits raises exactly the questions Ripple fought during its long legal battle over XRP. More modest possibilities, such as a governance gesture or simply structuring the business so more value flows through XRP, are more realistic than a direct equity windfall.

Is Ripple actually going to have an IPO?

It is uncertain, and Garlinghouse has repeatedly described going public as not a priority. He has cited the weak post-listing performance of crypto-company peers and reports of a major exchange delaying its own plans, and he has argued that staying private preserves flexibility. This matters because the entire holder-benefit question is downstream of an IPO happening at all. Even the most generous imaginable reward is irrelevant unless Ripple first decides to go public and then chooses to extend something to holders.

Could a Ripple IPO actually be bad for XRP?

It could, and this is the part the bullish framing tends to skip. An IPO would give institutions a direct way to own Ripple through regulated stock that offers dividends, financial transparency, and ownership of company assets, potentially drawing capital that might otherwise have flowed into XRP as a proxy for Ripple. Separately, as a public company answerable to quarterly earnings expectations, Ripple could face stronger incentives to monetize its large XRP escrow holdings more aggressively, adding long-term selling pressure on the token. Going public is therefore a double-edged sword for XRP, with credible downside as well as the hoped-for upside, and holders should weigh both.

What should XRP holders actually focus on?

On the observable catalysts that truly move the token instead of the IPO hint. Those include whether the CLARITY Act passes and codifies XRP’s commodity status, whether spot XRP ETF flows compound or stall, whether the network’s settlement usage grows into real token demand against the escrow supply, and the direction of Bitcoin and the broader market. The “special arrangement” remark is best treated as a small signal about Ripple’s posture toward its community, given minimal weight in any actual view of XRP’s prospects. Evaluating XRP on its real merits, utility, regulatory position, adoption, and supply, is far sounder than positioning around a hedged maybe.

This article is information, not investment advice. Prices, corporate plans, and statements reflect reporting available as of June 28, 2026, and can change quickly. Brad Garlinghouse’s comments were conditional and did not constitute a commitment or a program. Nothing here is a recommendation to buy or sell XRP or any security. Verify current details from primary sources and consider your own circumstances before making any decision.

Binance logged more than $400 million in net outflows over the week starting June 22, according to exchange-reserve tracking by DefiLlama. The move follows the exchange’s decision to withdraw its application for Markets in Crypto-Assets Regulation (MiCA) licensing in Greece, a setback that comes as the European Union approaches its July 1 MiCA transition deadline.

DefiLlama data reviewed by Cointelegraph shows Binance’s seven-day net outflows totaled roughly 0.3% of its $133.3 billion in tracked assets. When excluding Binance’s native token, BNB, the outflows still account for about 0.35% of Binance’s $113.8 billion in tracked crypto assets—small in percentage terms, but large in absolute value.

Key takeaways

- Binance recorded weekly net outflows of more than $400 million after withdrawing its MiCA license application tied to Greece.

- DefiLlama tracking puts the outflows at about 0.3% of Binance’s tracked assets (or 0.35% excluding BNB), suggesting the effect is limited relative to total holdings.

- Outflows intensified midweek, including a reported $1.96 billion net outflow day linked to Binance’s Greece decision, followed by two more multi‑billion flow days.

- Rival exchanges have been courting users ahead of July 1, but it is not yet clear who will capture the displaced volume.

- Binance says it is still taking MiCA and the EU seriously, while ESMA requires unlicensed providers to wind down and limit services after July 1.

Outflows spike as Greece MiCA application is withdrawn

The outflow period began just before the final week leading into the EU’s MiCA transition deadline. Binance’s latest reported withdrawal in Greece appears to have driven a noticeable acceleration in daily flows: DefiLlama-linked figures show net outflows reached $1.96 billion on Wednesday, the day Binance announced the withdrawal, before continuing with $2.52 billion and $1.46 billion in net outflows over the following two days.

While multi‑billion dollar daily flow swings are not unusual for Binance—something Cointelegraph notes is consistent with its broader historical pattern—the data does show that regulatory uncertainty can coincide with heavy movement out of tracked exchange wallets. The DefiLlama dataset used here also does not indicate where funds end up or which jurisdictions they originate from.

Starting July 1, Binance plans to restrict onboarding and some services for affected EU users, reflecting the compliance timetable under MiCA. In other words, this is not a headline “exit” from Europe, but a narrowing of EU operating routes tied to local authorization status.

Rivals court Binance users—yet ESMA’s register muddies the picture

As the deadline nears, several competing crypto exchanges have tried to position themselves as alternatives for users concerned about service continuity. DefiLlama exchange-reserve tracking—covering reserves disclosed through exchange reserve wallets, including proof-of-reserves disclosures—shows OKX recorded about $285.5 million in net inflows over the same seven-day period.

OKX received MiCA authorization in Malta in January 2025, making it one of the more prominent exchanges signaling readiness for the bloc’s new rules. However, the weekly net inflow ranking was led by other exchanges: Bitget reported approximately $710 million and Bitfinex about $400 million in net inflows, placing OKX third.

At the same time, neither OKX nor the other leading inflow exchanges appear to be listed on the European Securities and Markets Authority’s (ESMA) interim MiCA register, which was last updated on Friday at the time of Cointelegraph’s reporting. That gap can matter for investors and traders trying to determine whether particular venues are actually positioned to operate broadly under MiCA authorization.

Binance insists Europe remains a priority

Despite the Greece licensing setback reflected in the outflow data, Binance’s internal messaging points to continued commitment to the EU. A CryptoQuant analyst, Maartunn, previously told Cointelegraph that euro trading accounts for just 1% of Binance spot volume, suggesting that EU-specific regulatory frictions may not translate into a major proportion of trading activity.

Still, Binance’s public stance is that it intends to keep pursuing MiCA licensing even if the firm is on track to miss the July 1 “buzzer.” Binance co-founder Yi He said in a post on Friday that the company takes the EU market seriously, describing it as a “small part” of its business but an “important one” for customers.

Operationally, Binance has also started telling some EU users to move funds to self-custodial wallets or to other exchanges. In a response to Cointelegraph, a Binance representative said restrictions vary depending on users’ jurisdictions and that no action is required for users not served through a locally registered entity. The practical takeaway for users is that the impact is expected to be uneven—based on jurisdiction and whether a local registered structure applies.

Regulators are tightening the rules regardless of intent

ESMA’s position is direct: in a June 23 statement, the regulator said crypto service providers that are not authorized by July 1 must take “immediate steps” to wind down EU activities. ESMA also emphasized limiting services to actions such as selling, transferring, relocating assets, or closing positions.

This creates a high-stakes compliance window for exchanges that are still in the authorization process. Even if a firm publicly signals commitment to licensing, ESMA’s guidance effectively forces operational narrowing after the deadline. For market participants, the difference between “seeking” authorization and being “authorized” by July 1 can show up quickly—in access changes, user migrations, and shifts in where assets sit.

For traders, this means liquidity and route selection may change as venues adjust to compliance requirements. For investors and analysts, the weekly net outflow numbers—while modest as a percentage of tracked assets—provide a real-time clue that regulatory headlines can coincide with large, fast fund reallocations.

Going forward, the next things to watch are whether Binance clarifies which specific user groups face restrictions after July 1, and how flows redistribute among exchanges that appear ready for MiCA-compliant operations. ESMA’s register updates and the pace of licensing decisions will likely determine whether “winners” emerge—or whether users mostly shift toward temporary alternatives until authorization gaps close.

Michael Saylor has again hinted at a possible Strategy Bitcoin purchase after posting the company’s Bitcoin tracker with the line, “We’re gonna need more charts.”

Summary

- Saylor’s latest Bitcoin tracker post arrived as Strategy’s mNAV fell below 1 this cycle.

- Strategy’s old equity-funded buying model faces pressure because issuing shares below NAV can hurt holders.

- Investors now watch whether Strategy keeps buying BTC or rebuilds its market premium first.

The timing has drawn attention because Strategy’s mNAV has fallen below 1.0 for the first time this cycle. That means the company now trades below the market value of the Bitcoin it holds.

Saylor posts another Bitcoin tracker hint

Saylor’s post followed a familiar pattern. In past cases, similar Bitcoin tracker updates came before Strategy disclosed new BTC purchases through public filings or company updates.

Strategy’s latest disclosed purchase came on June 22. The company bought 520 BTC for about $35 million at an average price of $67,068 per coin, lifting total holdings to 847,363 BTC, according to its official purchase tracker.

The new hint now raises the question of whether another purchase is coming next week. It also puts fresh focus on how Strategy funds new Bitcoin buys while its market valuation weakens.

Saylor has kept a clear public stance in favor of long-term Bitcoin accumulation. Still, the current market setup is different from the one that helped Strategy build its large BTC position.

mNAV drop tests the Bitcoin flywheel

Strategy’s old model worked best when its stock traded above the value of its Bitcoin. The company could issue shares at a premium, buy BTC, and raise Bitcoin per share for existing holders.

That loop becomes harder when mNAV falls below 1. As previously reported, Strategy’s mNAV dropped to about 0.80 as Bitcoin broke below $60,000, weakening the premium-funded engine that supported years of buying.

Management has previously indicated that issuing new equity below roughly 1.22x mNAV can become value-destructive on a per-share basis. That level matters because it separates accretive fundraising from dilution risk.

If Strategy issues common equity below that threshold, existing holders may end up with less Bitcoin per share. That is why some investors now ask whether Strategy should keep buying BTC or focus on restoring the valuation premium first.

STRC pressure adds another challenge

The pressure is not limited to common equity. Strategy has also used preferred shares, including STRC, as part of its funding stack for Bitcoin purchases and dividend obligations.

As related coverage noted, STRC has traded at a record discount while Strategy’s Bitcoin position sits billions below cost. That has made the company’s capital structure a larger part of the Bitcoin market debate.

Preferred stock can help Strategy raise cash without selling common shares. But when STRC trades far below its $100 target level, the cost of issuing more preferred stock rises.

That creates a difficult setup. Strategy can still buy Bitcoin, but each funding route now comes with closer market scrutiny.

Investors weigh buying against valuation repair

The bull case is simple. Supporters argue that Strategy should keep buying Bitcoin while prices are lower because the company’s long-term thesis has not changed.

They also point to Strategy’s large Bitcoin stack and its history of surviving sharp market declines. Saylor has argued before that the company’s reserves and capital access give it room to keep executing.

The bear case focuses on funding quality. Critics say buying more BTC while mNAV is below 1 may not help shareholders if the company uses expensive capital or value-destructive equity issuance.

For now, the market has no confirmed new purchase. Saylor’s post is only a signal, but traders know his signals often come before official disclosures.

The next update will show whether Strategy keeps adding Bitcoin despite the mNAV discount. It will also show whether Saylor’s buying machine can still run when the stock no longer trades at a clear premium to its BTC holdings.

Crypto World

Tokenization is becoming the financing layer for AI and robotics, Framework bets with $400 million fund

Traditional securitization markets struggle to package individual servers or computing equipment into investable products, Anderson said. Stablecoins — with more than $300 billion circulating onchain — create a new source of capital for asset-backed lending.

“We have the capital onchain to finance this industry,” he said.

The same thinking extends to energy. Framework has invested in Daylight, which finances residential solar projects through a distributed energy network, and Uranium Digital, which is building a tokenized marketplace for physical uranium.

A different generation

There’s also a notable shift in the profile of founders building today’s crypto companies, Anderson said.

Rather than anonymous crypto-native developers launching speculative protocols, Anderson said, many founders now come from traditional finance, energy or industrial technology, bringing deep expertise while using blockchain as the underlying financial infrastructure to solve real-world problems.

Framework’s recent investments already reflect that trend. They include TVL Capital, founded by former members of Morgan Stanley’s digital assets team; robotics startup Mecka AI, which supplies training data to frontier AI companies; and Plasma, a blockchain-based banking platform built around stablecoin payments.

The venture firm’s strategy mirrors a broader shift across the digital asset industry. Global banks and asset managers are increasingly using blockchain rails to issue, trade and settle traditional financial assets, while stablecoins are becoming part of cross-border payments and treasury operations as banks and fintechs look to modernize payment rails.

TLDR:

- El Salvador purchased another 8 BTC, increasing its official Bitcoin treasury to 7,696.37 BTC.

- Official treasury data shows the country continues making regular Bitcoin acquisitions each week.

- Bitcoin reserve growth has continued despite reforms affecting Bitcoin’s domestic payment framework.

- El Salvador remains one of the world’s most closely watched sovereign Bitcoin holders.

El Salvador has increased its national Bitcoin treasury once again after adding eight more BTC during the past week. The latest purchase lifted the country’s total holdings to 7,696.37 BTC, extending its steady accumulation strategy.

The update arrives as sovereign Bitcoin reserves remain a closely watched theme across the crypto market. Government-backed digital asset holdings continue attracting attention despite changing market conditions.

El Salvador Bitcoin Treasury Grows to 7,696.37 BTC

Official data from El Salvador’s Ministry of Finance shows the country acquired another eight Bitcoin over the last seven days. The purchase raised the national treasury balance to 7,696.37 BTC.

The latest addition keeps El Salvador’s long-running Bitcoin reserve strategy active. Weekly purchases have become a consistent feature of the country’s treasury approach.

The country’s Bitcoin Office continues tracking the national reserve through official holdings data. That transparency has made El Salvador one of the most closely monitored sovereign Bitcoin holders.

X posts from Whale Factor and That Martini Guy also highlighted the latest treasury increase. Both noted that El Salvador continues expanding its Bitcoin position while many governments still debate broader Bitcoin adoption.

El Salvador Maintains Bitcoin Strategy Despite IMF Reforms

The latest purchase comes after El Salvador revised parts of its Bitcoin legislation following its agreement with the International Monetary Fund. The legal changes focused on Bitcoin’s role in everyday commercial activity.

Private businesses are no longer required to accept Bitcoin as payment under the amended framework. However, Bitcoin remains part of the country’s legal structure.

While the payment policy has evolved, the national treasury strategy has continued without interruption. Official reserve data shows the government’s Bitcoin holdings have continued growing through regular acquisitions.

The reserve policy now operates separately from Bitcoin’s role as a payment option. That distinction has become more visible since the legislative amendments.

Each weekly purchase adds to El Salvador’s sovereign Bitcoin position while reinforcing its long-term reserve strategy. The latest update pushes the country’s holdings to 7,696.37 BTC and keeps its treasury among the world’s most closely followed government Bitcoin reserves.

Ethereum is trading near the $1,570 to $1,580 area after a calm weekend that failed to ease the pressure on the second-largest cryptocurrency.

Summary

- Ethereum trades near $1,570 as ETF outflows and whale selling pressure keep buyers cautious.

- Analysts see $1,583 as a key support level after whales sold 550,000 ETH this week.

- A clean move above $1,800 could ease pressure, while losing $1,583 may deepen losses.

The price has stayed mostly range-bound, even as new tension in the Middle East tested risk appetite across global markets.

The calm move does not mean the market has turned strong. ETH remains below the $1,800 level that many traders see as a key recovery zone. The asset is also under pressure from ETF outflows, whale selling, and weak spot demand.

ETF outflows weigh on Ethereum sentiment

U.S. spot Bitcoin and Ethereum ETFs recorded their seventh straight day of outflows on June 26, according to SoSoValue data. Spot Bitcoin ETFs saw about $445 million in net outflows, while spot Ethereum ETFs posted $12.848 million in net outflows.

The Ethereum outflow was smaller than Bitcoin’s, but the streak matters because ETFs can act as a source of steady spot demand. When flows stay negative for several days, that support weakens. This can make it harder for ETH to recover when traders are already cautious.

Earlier Ethereum ETF coverage showed that ETH had already been testing major support as fund withdrawals mounted. That pressure has continued into late June, keeping the market focused on whether institutional demand can return.

Another price analysis noted that ETH traded near $1,600 even after BitMine reportedly bought another 75,000 ETH. That showed that large purchases have not been enough to reverse the wider downtrend.

Whales sell into weak support

Analyst Ali Martinez said large holders sold about 550,000 ETH over the past week. At current prices, that sale equals roughly $880 million in fresh supply hitting the market.

The analyst said this selling helped push Ethereum below its immediate $1,633 support level. ETH is now testing volume support near $1,583, a level traders are watching closely because a clean break could open the way for deeper losses.

Ali said if selling continues into next week, the next high-volume demand areas could sit near $1,237 and $1,089. These levels are not guaranteed targets, but they show where past trading activity may attract buyers if ETH breaks lower.

This pressure matches the current chart structure. ETH continues to print lower highs, and buyers have not yet shown enough strength to reclaim the $1,800 area.

Analysts split on ETH’s next move

Money Ape warned that Ethereum could post three straight red quarters for the first time. The analyst said ETH may fall below $1,000 if market confidence keeps weakening.

That view reflects the bearish side of the current setup. Ethereum has failed to recover quickly from its slide, and traders remain worried about ETF outflows, whale activity, and weak momentum.

Michaël van de Poppe offered a different view. He said anything below $1,800 is not attractive for day trading but may be a strong opportunity for longer-term accumulation.

He also said ETH may be forming a bullish divergence across several timeframes. In his view, a clear break above $1,800 would be more useful than trying to catch every small move inside the current downtrend.

Van de Poppe also pointed to lower levels near $1,505 and $1,385 as possible buying zones if ETH sweeps liquidity. He said he doubts the market is eager to move much lower, but he still wants to see a clean recovery above $1,800.

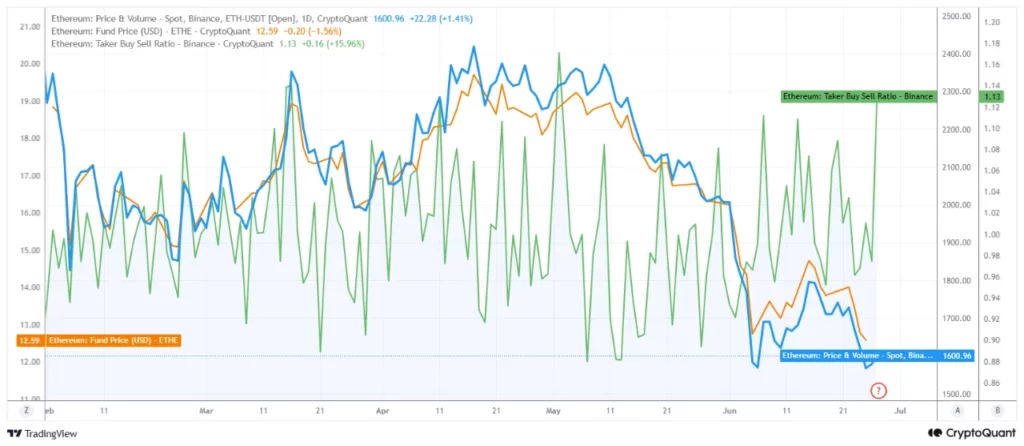

Derivatives data shows sellers still in control

CryptoQuant analyst PelinayPA said Ethereum’s taker buy/sell ratio on Binance remains above 1. That usually points to stronger buying activity, but ETH has not reacted with a strong recovery.

The analyst said this muted response suggests larger sellers may be absorbing buy orders. In simple terms, buyers are active, but they are not strong enough to push the price higher.

The same report said Ethereum’s fund price has been falling since April. That suggests traders are reducing long exposure in derivatives markets and taking less risk.

This creates a weak setup for ETH. Even when buying activity rises, price action remains soft. That can happen when whales use short rallies to sell into demand.

The analyst said ETH still forms lower highs while fresh lows keep developing. That confirms the broader bearish structure remains in place until Ethereum breaks its current downtrend.

Ethereum price outlook

Ethereum’s near-term outlook now depends on the $1,583 support area. If buyers defend this zone, ETH could attempt another move toward $1,633 and then $1,800.

A clean break above $1,800 would be the first stronger sign that bulls are regaining control. It could also shift attention back toward higher resistance zones after weeks of weak trading.

If ETH loses $1,583, traders may look toward $1,505 and $1,385. A deeper sell-off could bring the $1,237 and $1,089 demand zones into focus if whale selling continues.

For now, Ethereum is stable but not strong. The price is calm near $1,570, yet ETF outflows, whale distribution, and weak derivatives demand keep the risk tilted toward another test of lower support.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

California’s Digital Financial Assets Law will take effect on July 1. It requires any firm conducting digital asset business activity with state residents to hold a DFAL license, and have a completed application on file with the DFPI, or cease covered operations. Right now, as of public records, no Ripple entity appears among applicants. XRP price has fallen below the $1.10 level at this moment of uncertainty.

DFAL covers the exchange of digital assets for fiat or other digital assets, their transfer between persons, custody, and the issuance of reserve-backed instruments. It maps directly onto Ripple’s California-facing operations: payments infrastructure, custody services, and the issuance and redemption of RLUSD, Ripple’s dollar-pegged stablecoin.

— SMQKE (@SMQKEDQG) June 26, 2026

BEGINNING JULY 1 2026 ONLY LICENSED CRYPTO COMPANIES WILL BE ALLOWED TO OPERATE IN CALIFORNIA

BEGINNING JULY 1 2026 ONLY LICENSED CRYPTO COMPANIES WILL BE ALLOWED TO OPERATE IN CALIFORNIA

Documented below.

https://t.co/0KRRRyDe1u pic.twitter.com/T1VIzh8AVR

https://t.co/0KRRRyDe1u pic.twitter.com/T1VIzh8AVR

Ripple’s existing portfolio of 40-plus U.S. money transmitter licenses does not automatically satisfy DFAL; the law is a separate regime administered by the DFPI through the Nationwide Multistate Licensing System.

However, there are three paths to legal compliance by July 1: hold a DFAL license, have a completed application pending with the DFPI, or qualify under a narrow statutory exemption, primarily available to banks, certain trust companies, and SEC- or CFTC-registered entities operating within already-regulated activity.

— WrathofKahneman (@WKahneman) June 19, 2026

Key date for @Ripple – July 1.

Key date for @Ripple – July 1.

Ripple previously engaged CA's DFPI for a DFAL license noting firms can keep operating if submit by 7/1/26. Public docs through March '26 don't list any Ripple entities, though likely filed. Necessary for all CA offerings, issue/redeem/custody. pic.twitter.com/xfQK4Z3IBc

Ripple has engaged with the process as the company submitted a formal comment letter to the DFPI, pushing to eliminate redundant money transmitter license requirements for DFAL-licensed firms. However, engagement is not the same as a filed application.

Law firms, including Chambers-ranked practices, have described DFAL as one of the most expansive state-level digital asset licensing regimes in the country.

Discover: The Best Crypto to Diversify Your Portfolio

Can XRP Price Hold $1 If Ripple Misses the DFAL Deadline?

XRP is trading near $1.10, far below the expected $2.50 many predicted. Recent price action reflects weak momentum, with sellers repeatedly capping rallies around the $1.15 to $1.20 area. Despite ongoing attention on Ripple’s regulatory developments, the market has yet to price in a decisive positive outcome.

Meanwhile, investors remain focused on several legal and regulatory milestones involving Ripple. The court’s earlier finding that XRP itself is not inherently a security removed a major uncertainty. However, the remaining penalty and injunction issues still matter because they could influence Ripple’s future business operations and market sentiment.

From a technical perspective, XRP must first reclaim the $1.15 to $1.20 zone before traders can discuss a stronger trend reversal. If buyers regain control and regulatory developments remain favorable, the next resistance area could emerge around $1.30 to $1.50. A sustained move above those levels would likely require a meaningful catalyst.

On the downside, support remains clustered around $1.05 and $1.00. If regulatory expectations weaken or broader crypto markets turn lower, those levels could come under pressure. The $1.00 mark remains an important psychological threshold, as a decisive break could invite additional selling.

For now, the market appears to be waiting for confirmation rather than trading on assumptions. Regulatory progress could improve sentiment, yet XRP’s longer-term trajectory will likely depend on both legal clarity and stronger demand returning to the market.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post California’s DFAL Clock Is Ticking: XRP Price Hanging in the Balance appeared first on Cryptonews.

The Bitcoin Charts Everyone Is Ignoring!

Galway v Dublin LIVE score updates and more from the All-Ireland SFC quarter-final

Virtual Models That Actually Help You Decide

-

Sports5 days ago

Sports5 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech6 days ago

Tech6 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics2 days ago

Politics2 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics3 days ago

Politics3 days agoPotential 2028er World Cup attendee leaderboard

-

Business2 days ago

Business2 days agoAsia stock markets slide as tech shares slump

-

Tech3 days ago

Tech3 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World4 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World3 days ago

Crypto World3 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business5 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World1 day ago

Crypto World1 day agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports2 days ago

Sports2 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World2 days ago

Crypto World2 days agoRTX holders must register wallets before token distribution begins

-

Crypto World2 days ago

Hyperliquid Named on Singapore MAS Investor Alert Register

-

Sports3 days ago

Sports3 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Crypto World2 days ago

The DATA Foundation Launches to Tackle AI’s Multi-Billion Dollar Training Data Bottleneck

-

Crypto World3 days ago

Crypto World3 days agoStrategy (MSTR) has a 10-month cash runway for dividends, but retail investors are losing faith

-

Crypto World2 days ago

Crypto World2 days agoAAVE price tests 9-month trendline after 17% rebound as breakout hopes build

-

Crypto World2 days ago

Crypto World2 days ago21Shares Cuts 2026 Crypto Forecasts as Institutional Demand Rises

You must be logged in to post a comment Login