Crypto World

TD Cowen slashes Strategy target despite Michael Saylor’s Bitcoin plan

Strategy stock has remained under pressure after TD Cowen cut its price target despite backing Michael Saylor’s latest capital strategy and maintaining a bullish rating on the company.

Summary

- TD Cowen cut its Strategy price target to $260 while maintaining a buy rating on the stock.

- The brokerage cited a weaker long-term Bitcoin outlook, not concerns over Strategy’s new capital plan.

- Investors are closely watching whether Strategy will resume Bitcoin purchases as mNAV remains below 1.0.

According to a recent TD Cowen research note, the brokerage reduced its price target for Strategy (MSTR) from $400 to $260 while keeping a “buy” rating on the stock. The firm attributed the lower valuation to a more conservative long-term outlook for Bitcoin (BTC), rather than concerns over Strategy’s newly announced Digital Credit Capital Framework.

Despite the reduction, TD Cowen said the revised target still implies roughly 200% upside from current trading levels.

The revision came a day after Strategy shares rallied more than 12% as investors reacted to the company’s latest financing framework. Although the stock gave back part of those gains in the following session, TD Cowen described the new capital plan as a positive step that could improve the company’s financial flexibility over time.

Bitcoin outlook has driven the target reduction

TD Cowen’s report separates its Bitcoin expectations from its view on Strategy’s corporate actions. Instead of questioning the company’s latest financial decisions, the brokerage lowered its valuation because it expects a weaker long-term Bitcoin price than previously forecast.

The updated assessment arrives as Strategy continues adjusting how it manages its Bitcoin treasury. In a regulatory filing dated June 29, the company introduced its Digital Credit Capital Framework, giving it the ability to raise up to $1.25 billion through Bitcoin sales.

According to the filing, proceeds could be used to maintain U.S. dollar reserves, fund preferred dividend payments, meet interest obligations, increase cash holdings, and finance future share repurchases.

Alongside the new framework, Strategy authorized the repurchase of up to $1 billion of its Digital Credit Securities, including STRC, STRF, STRD, and STRK, if management determines that buybacks would strengthen the company’s capital structure.

The company also disclosed that it has paused additional Bitcoin purchases while selling about $1.15 billion worth of MSTR shares as part of its capital management strategy.

Strategy faces new questions over Bitcoin accumulation

Attention has also turned to whether Strategy can continue expanding its Bitcoin holdings under current market conditions.

On June 28, Michael Saylor posted Strategy’s Bitcoin tracker on social media alongside the message, “We’re gonna need more charts.” Similar tracker posts have preceded previous Bitcoin purchase announcements, leading some investors to speculate that another acquisition could be disclosed.

Strategy’s most recent reported purchase came on June 22, when it acquired 520 BTC for approximately $35 million at an average price of $67,068 per coin. The purchase increased the company’s total holdings to 847,363 BTC, according to its official Bitcoin purchase tracker.

Recent market conditions, however, have complicated the company’s long-running accumulation model. As previously reported, Strategy’s mNAV has fallen below 1.0 for the first time during this market cycle, dropping to around 0.80 after Bitcoin slipped below $60,000.

Trading below the value of its Bitcoin holdings makes it harder for the company to issue new shares at a premium and use those proceeds to buy additional BTC without diluting existing shareholders.

Management has previously indicated that issuing common equity below roughly 1.22 times mNAV can become value-destructive on a per-share basis. As a result, some investors have questioned whether restoring the valuation premium should take priority over further Bitcoin purchases.

Strategy’s updated framework has also sparked criticism from some market participants because it allows limited Bitcoin monetization. Critics argue that selling Bitcoin could weigh on market sentiment, while Ripple CEO Brad Garlinghouse has publicly criticized Strategy’s role during the recent crypto market decline.

The debate has gained additional attention because Saylor has consistently encouraged long-term Bitcoin holding even as the company evaluates new ways to manage its balance sheet.

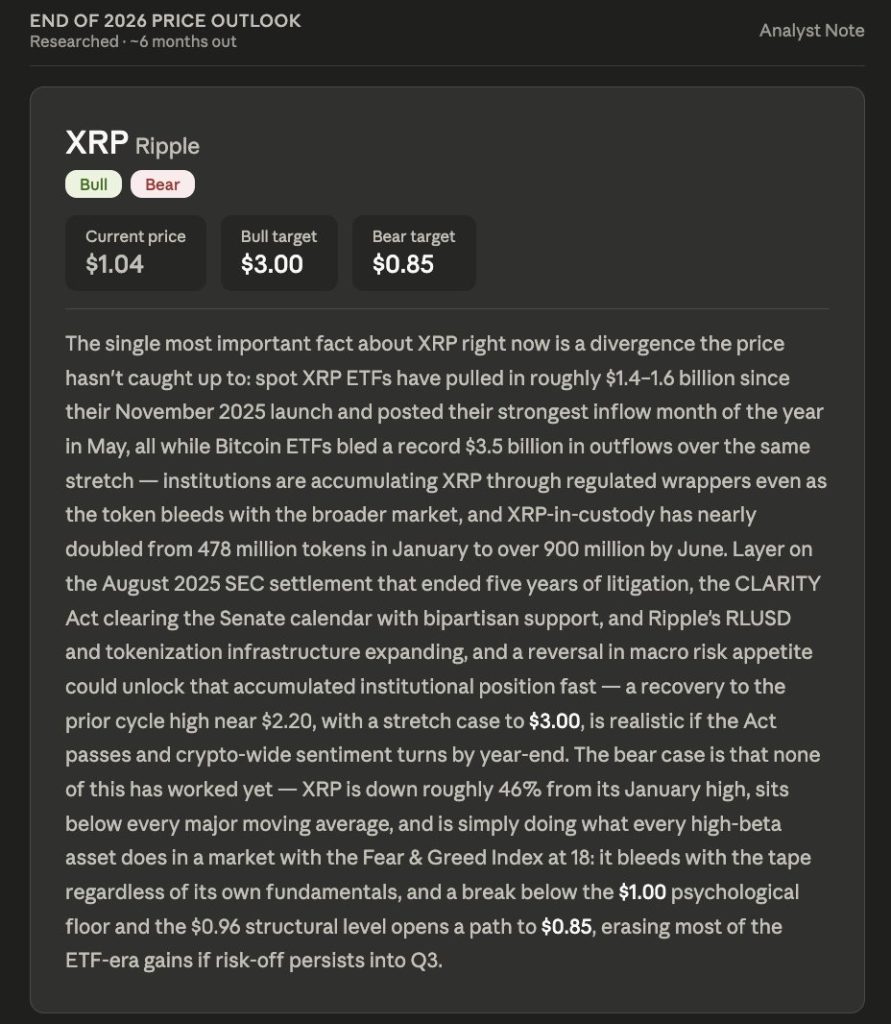

Claude AI Opus 4.8 just zeroed in on a divergence between price action and institutional behavior that most people watching XRP price prediction have completely missed. The model predicts a bull target of $3.00, with a more grounded recovery case sitting near $2.20.

The bull case rests on one core fact that XRP price simply has not caught up to yet. Spot XRP ETFs have pulled in roughly $1.4 to $1.6 billion since their November 2025 launch, and they actually posted their strongest inflow month of the entire year in May, all while bitcoin ETFs were bleeding a record $3.5 billion in outflows over that same stretch.

That kind of divergence matters because it shows institutions are accumulating XRP through regulated wrappers even as the token bleeds alongside the broader market.

XRP price in custody has nearly doubled too, climbing from 478 million tokens in January to over 900 million by June, which is real on chain evidence of accumulation rather than just a headline number.

Layer on top of that the August 2025 SEC settlement that ended five years of litigation, the CLARITY Act clearing the Senate calendar with bipartisan support, and Ripple’s RLUSD and tokenization infrastructure continuing to expand, and you get a fundamental backdrop that looks far stronger than the price chart suggests.

If macro risk appetite reverses, the model sees that accumulated institutional position unlocking fast, with a recovery to the prior cycle high near $2.20 being realistic, and a stretch case toward $3.00 if the Act actually passes and crypto wide sentiment turns more broadly bullish by year end.

The bear case is blunt about where things actually stand today. None of this has worked yet. XRP is down roughly 46% from its January high, sits below every major moving average, and is simply doing what every high beta asset does in a market with the Fear and Greed Index sitting at just 18, meaning it bleeds with the broader tape regardless of its own underlying fundamentals.

A break below the $1.00 psychological floor and the $0.96 structural level beneath it opens a path straight to $0.85, which would erase most of the gains built up during the entire ETF era if risk off conditions persist into the third quarter.

XRP Price Prediction: XRP Sits On A Pile Of Institutional Buying The Chart Refuses To Show

The daily chart shows XRP at $1.04718 after a long, grinding decline from highs above $3.65 set back in July of last year. That slide has been almost uninterrupted, with the steepest leg coming in October when price collapsed from the $2.70 zone down through $1.60 within a matter of weeks.

Since February, price has mostly drifted lower in a series of smaller steps, currently sitting right at the exact $1.00 psychological floor called out as the critical level in this prediction.

That kind of test right at a major round number after such a long downtrend usually marks a real decision point rather than just another stop along the way.

Resistance sits first near $1.40, the level price has failed to reclaim during recent bounce attempts, then a much heavier ceiling near $2.20, which lines up directly with the prior cycle high mentioned as the realistic recovery target.

Support holds right around the current $1.00 to $1.03 zone, with the $0.96 structural level sitting just beneath as the next real test if this floor gives way.

The broader pattern here is a clean series of lower highs and lower lows stretching back nearly a full year, which fits the bear case description of a high beta asset simply bleeding with a weak overall market.

Momentum on the daily candles looks weak and still leaning lower, without much evidence yet of the kind of basing action that typically shows up before a real reversal.

Given how directly current price sits on top of the exact floor named in this prediction, the next move through $1.00 looks like the moment that decides whether this divergence between institutional buying and price finally starts to close.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Discover: The best crypto to diversify your portfolio with

Here is What Claude AI Predicts For LiquidChain Near Future, Very Bullish

Sitting at resistance is not a strategy. It is a queue.

Bitcoin, Ethereum, and XRP are stuck under the same ceilings. The catalyst is always one print away. The inflows are always next quarter.

Small cap infrastructure plays by different rules. Capital that is noise at Bitcoin’s scale can reshape an undiscovered project entirely. The real asymmetry lives in the gap between what something is worth and what the market has priced it at. That gap closes the moment it gets found.

Cross-chain fragmentation has taxed DeFi since the first bridge launched. Bitcoin, Ethereum, and Solana grew up disconnected. Every transaction crossing those lines pays in fees, slippage, and failures. Bridges were supposed to fix it. They became the toll booth instead.

LiquidChain removes the toll. All 3 networks inside one execution layer. One deployment reaches everywhere. No cross-chain fee, anywhere.

Claude AI flagged it as worth watching. The presale sits at $0.01454 with just over $860,000 raised.

Execution is unproven. Adoption is unknown. Established assets offer a calmer climb toward a ceiling everyone can already see. LiquidChain stays an opportunity only as long as it stays unnoticed.

The post Claude AI Opus Predicts Stunning XRP Price by End of 2026 appeared first on Cryptonews.

Stablecoins are moving quickly from “crypto rails” toward mainstream corporate payment tools, according to a new survey from payments infrastructure firm Cybrid. The report suggests that a large share of businesses are already using stablecoins for cross-border transfers—and that confidence in further adoption will hinge heavily on clearer regulation.

Cybrid’s findings indicate that 42% of surveyed companies are using stablecoins for cross-border payments today, while 88% of respondents said they are likely or very likely to use them within the next 12 months. Among those benefits cited, cost savings stand out: businesses reported average cross-border payment cost reductions of 35%, with firms processing more than $100 million per month reporting average savings up to 47%.

Key takeaways

- Adoption is already underway: 42% of Cybrid’s surveyed businesses report using stablecoins for cross-border payments.

- Momentum looks set to accelerate: 88% said they expect to use stablecoins within the next year.

- Cost savings are a primary driver: average cross-border payment costs are reported down 35%, rising to as much as 47% for higher-volume firms.

- Regulatory clarity is the confidence lever: 71% of respondents said regulation matters more than trusted infrastructure providers or integration with existing systems.

- Stablecoin growth remains concentrated: CoinGecko data places total stablecoin market cap at $307.64 billion, with USDT and USDC leading.

Corporate stablecoin use is expanding beyond niche payments

Cybrid’s report is based on a survey of 468 executives and business leaders conducted between April 28 and May 4. Respondents represented technology, financial services, and ecommerce sectors across the United States, Canada, and the United Kingdom, including C-suite executives as well as finance and treasury, payments, and operations leadership.

While cross-border payments are the headline use case, the survey also points to a range of corporate applications. Payroll and contractor payments were cited as the most common use case after cross-border transfers, followed by supplier and vendor payments. Additional reported activities included customer payments and uses tied to investment and yield generation, along with treasury and liquidity management.

That breadth matters for investors and operators because it suggests stablecoins are not being evaluated solely as an alternative to one payment moment. Instead, businesses appear to be testing stablecoins across operating workflows—particularly where speed, settlement, and international reach can reduce friction.

Cost advantages reported by businesses

Cybrid’s survey quantifies the economic appeal. Businesses using stablecoins reported average cross-border payment cost savings of 35%. For companies handling more than $100 million in monthly payment volume, the average savings reportedly increased to as much as 47%.

These figures are particularly relevant because stablecoin adoption often depends on whether the technology can deliver measurable improvements over established banking and remittance channels. Cybrid also noted that only 2% of respondents described themselves as “committed” users of traditional payment rails, a contrast that implies stablecoin workflows may be winning share where they provide clearer cost or operational benefits.

Regulation is emerging as the deciding factor

Beyond pricing, the survey highlights a key decision-making variable: regulatory clarity. According to Cybrid, 71% of respondents said it would increase their confidence to expand stablecoin use—and did so more than other considerations such as trusted infrastructure providers or integration with existing systems.

This emphasis aligns with broader market dynamics. The report points to momentum driven by U.S. legislation for payment stablecoins. It references the emergence of GENIUS Act-compliant stablecoins, noting that these have reached a combined market cap above $76 billion—marking the first federal regulatory framework for payment stablecoins in the United States.

At the same time, the survey’s geography and respondent profile indicate that corporations are actively looking for frameworks that can be relied on at the point of operational deployment, not just pilot testing.

Stablecoin market size continues to grow as infrastructure upgrades

The Cybrid report arrives as stablecoins continue to scale. CoinGecko data cited in the report puts total stablecoin market cap at $307.64 billion. Tether’s USDT leads at $184.7 billion, followed by Circle’s USDC at $73.51 billion. The same data set is referenced to highlight how GENIUS Act-compliant stablecoins have grown to more than $76 billion in market cap.

Additional industry signals cited alongside Cybrid’s survey reinforce the shift toward business demand. Paybis previously said business customers accounted for nearly 98% of stablecoin payout volume processed through its platform in the first four months of 2026, up from 36% in 2023. Paybis also referenced McKinsey research estimating that business-to-business transactions represent roughly 60% of the $390 billion in global stablecoin payment volume recorded in 2025.

Meanwhile, major infrastructure providers continue expanding regulated pathways for stablecoin issuance, custody, and transfers. In May, Falcon Finance debuted fUSD—a dollar-backed stablecoin—through Anchorage Digital Bank’s federally regulated issuance platform, aiming at institutional trading, collateral, and treasury workflows. More recently, BNY expanded its digital asset custody platform to support Circle’s USDC, enabling institutional clients to store, transfer, mint, and redeem the stablecoin through the bank.

Together, these developments suggest that corporate interest is increasingly meeting operational capability. For businesses, the practical question is no longer whether stablecoins can move value, but whether they can be integrated into compliant, bank-adjacent processes that reduce operational risk.

What to watch in the next 12 months

Cybrid’s survey indicates stablecoin adoption is likely to intensify, but the data also implies that expansion may depend on continued regulatory progress and on how quickly corporate infrastructure becomes easier to deploy. Investors and teams should watch whether compliance-driven infrastructure keeps pace with demand—and whether businesses that are “likely” to use stablecoins convert into consistent, long-term users.

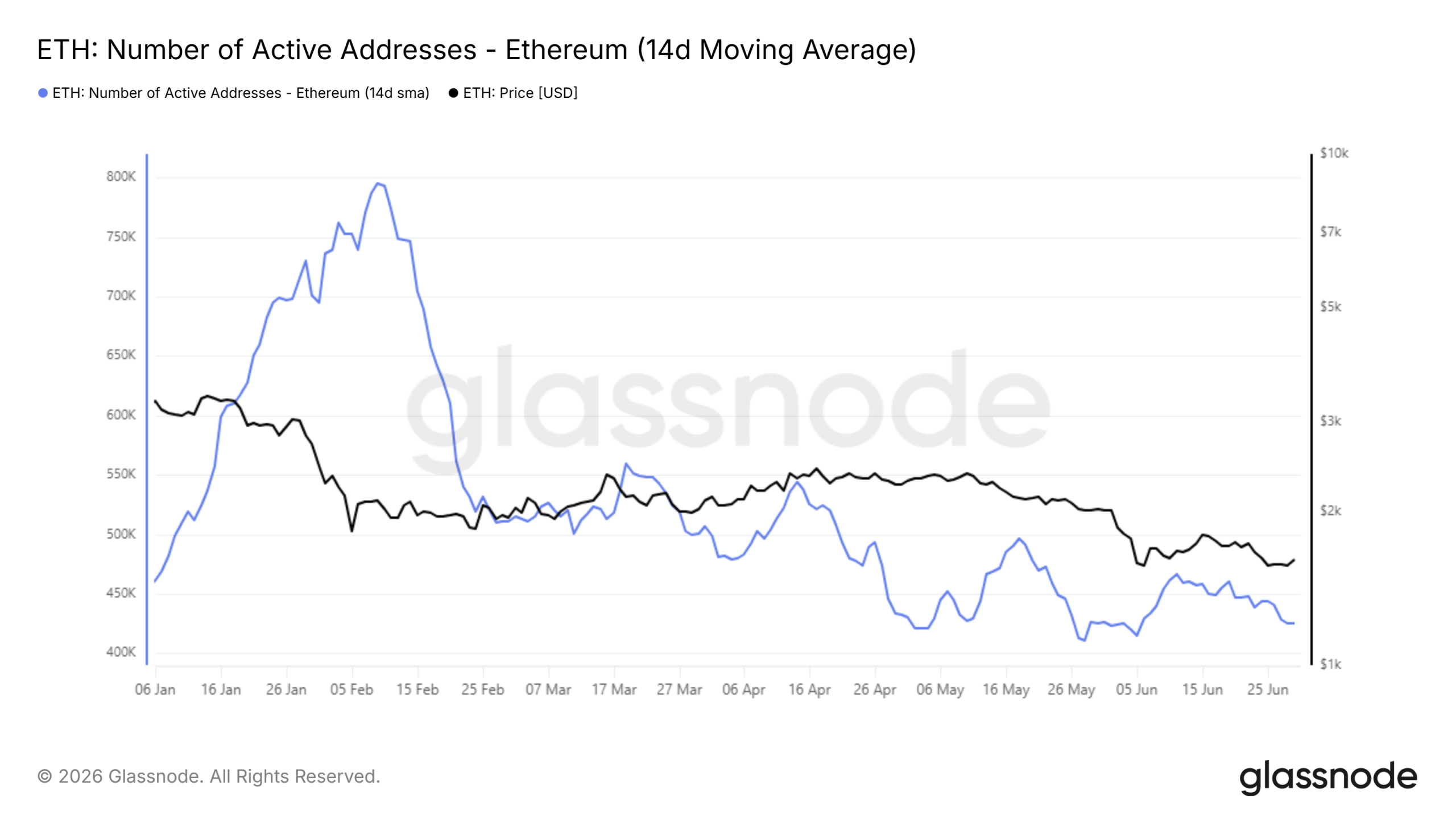

Ethereum (ETH) enters July 2026 trading near $1,570, close to multi-month lows, after recording its first run of three consecutive red quarterly candles in its history.

On-chain data and price charts now tell competing stories. Network usage keeps falling, yet large holders appear to be buying, which leaves July’s direction wide open.

ETH in July 2026: Active Addresses Fall to Fresh Lows

Glassnode data on active addresses points to weakening engagement. The 14-day moving average peaked near 795,000 in early February 2026. It has since dropped to roughly 420,000, a decline of about 46%.

The early move was unusual. Addresses climbed through January while prices fell, a sign of speculative churn rather than durable demand. Both metrics then rolled over together.

Through the spring, prices held up better than usage. Brief rebounds in active addresses during March, April, and May each failed to hold. The June reading marks the lowest on the chart, and the trend has not yet bottomed.

For this signal to flip, active addresses would need a sustained recovery rather than another short-lived spike.

Whale Address Count Climbs Into the Weakness

The address picture looks bleak. However, the whale data complicates that read. Glassnode’s count of addresses holding 1,000 to 10,000 ETH spiked in the final days of June.

That move produced the greatest 30-day change on the chart, and it happened while the price sat at its lowest point. Accumulation into a low price can suggest that larger holders are positioning early.

External flow data supports the mixed signal. Some reports show whales adding tens of millions of dollars in ETH, while spot Ethereum ETFs recorded net outflows through June. Bitmine chairman Tom Lee tied part of the recent drop to quarter-end fund behavior.

One caveat matters. A similar whale-count surge in late February coincided with a local top before price fell, so rising whale numbers have not been a clean buy signal this cycle.

3 Straight Red Quarters Mark Uncharted Territory

The quarterly view frames why the technical picture matters. CoinGlass data shared by analyst Ted Pillows shows ETH closing Q4 2025 down 28.28%, Q1 2026 down 29.26%, and Q2 2026 down 24.77%.

That run is the first stretch of three consecutive red quarters in the dataset, which begins in 2016. The longest prior streaks reached only two quarters, in 2018 and again in 2019.

The character of this decline also stands out. Rather than one violent crash, ETH has bled steadily across three roughly equal quarters. The broader market has softened alongside it.

Monthly Chart Tests a Key Fibonacci Level

The monthly chart shows ETH near a level that has mattered before. Price trades around $1,570, and a close here would mark the lowest monthly close since March 2023.

The 0.786 Fibonacci retracement, drawn from the $881 low to the $4,956 high, sits at roughly $1,753. That zone acted as support on four prior occasions, and it lines up with the heaviest volume node on the profile.

Price now trades below that level on an intra-month basis. A monthly close beneath it would confirm the break, opening room toward $1,200 and then the $881 swing low. Monthly RSI sits near 40, so momentum is not yet oversold.

ETH Price Prediction Hinges on the $1,500 Line

The daily chart sharpens the near-term question. ETH has lost three layered support bands, near $2,375, $2,175, and $1,925, and each now acts as resistance.

Price has also broken below a descending channel and failed two retests of that broken structure in June. It is now holding just above a final demand zone around the psychological $1,500 mark.

Volume has faded through the decline, and Bollinger Band width sits at compressed levels. Low volatility often precedes a larger move, though compression signals magnitude rather than direction.

The setup leaves a clear binary. A daily close below $1,500 would expose the $1,200 area, while a reclaim of $1,753 would invalidate the bearish thesis. The prior monthly outlook flagged the same battle zone.

What Could Decide ETH in July 2026

The evidence pulls in two directions. The trend, the lost supports, and falling active addresses argue for caution. Meanwhile, whale accumulation and the volatility squeeze hint at a possible snapback.

Two levels frame the month. Holding $1,500 keeps a recovery toward $1,753 on the table, while losing it points lower. Roughly $10.63 billion in June options expiry has already cleared, which may reduce one source of pressure.

For now, the data suggests a market in balance rather than a confirmed move. July’s first weekly closes around $1,500 and $1,753 should indicate which side wins control.

This article is for informational purposes only and does not constitute financial advice.

The post What to Expect From Ethereum (ETH) in July 2026 appeared first on BeInCrypto.

Three $ME token buyers sued Magic Eden and its four co-founders, alleging the company promoted the token's use cases — multichain trading, governance, staking rewards, and revenue sharing — then delayed, diminished, or abandoned them, according to a class-action complaint filed in federal court in… Read the full story at The Defiant

Coinmetro, an Estonian-based cryptocurrency exchange, has claimed that it has filed “a reorganisation application to the Estonian court.”

In its announcement, it states that this is required because of “an extraordinary situation caused by a failure of one of our financial service providers.”

It further claims that it had already suspended user registrations, deposits, and withdrawals back on June 22.

Interestingly, in the Estonian register both Coinmetro OÜ and Coinmetro Group OÜ are past due on annual reports. Coinmetro Group OÜ is also listed as having a tax debt.

The announcement didn’t disclose which financial service partner led to this failure, and Coinmetro has yet to respond to Protos’ questions regarding that issue.

During a YouTube based “Ask Me Anything” with Coinmetro Chief Executive (and beneficial owner) Kevin Murcko, he claimed that it was actually more than one provider that failed, despite the announcement only claiming one.

He also claimed that there was a multi-year internal investigation, suggesting that this failure happened well before this current announcement.

Additionally, he stated that he originally believed that Coinmetro’s balance sheet was strong enough that this wasn’t originally material, but has become material as Coinmetro has approached the July 1 licensure deadline for compliance with Markets in Crypto Assets regulations.

Prime Trust

The Prime Trust bankruptcy estate (PCT Litigation Trust) filed an adversary proceeding against Coinmetro in August of last year.

This proceeding attempted to clawback withdrawals made in the days immediately preceding bankruptcy.

This proceeding claims that Prime transferred $1,205,751.10 to Coinmetro in the days before Prime’s failure.

Read more: Prime Trust accused of using customer funds to cover lost deposits

The mistakes and fraud committed by Prime apparently make it extraordinarily difficult to determine who was owed which funds from Prime Trust.

This means that Coinmetro didn’t necessarily withdraw more funds than it deposited because of the failure, and Prime Trust is trying to clawback many of the withdrawals from the final days.

Protos reached out to Coinmetro for comment, but it didn’t respond before publication.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Ripple has unveiled a proposed lending protocol for the XRP Ledger that would allow financial institutions to borrow digital assets without selling their holdings, expanding the network’s institutional finance capabilities.

Summary

- Ripple has proposed an XRP Ledger lending protocol for institutional borrowers and lenders.

- The system lets institutions borrow digital assets without selling token holdings.

- The proposal now awaits XRP Ledger validator approval after devnet testing.

According to a proposal published by Ripple, the new XRP Ledger Lending Protocol is designed to fill what the company describes as a missing piece in blockchain-based finance. While tokenization has simplified the issuance and transfer of digital assets, Ripple argues that lending, collateral management, and credit infrastructure have not advanced at the same pace.

The proposal would support lending markets for tokenized U.S. Treasuries, money market funds, stablecoins, commodities, private credit, and other real-world assets on the XRP Ledger.

Rather than embedding credit decisions into blockchain code, Ripple said lenders and borrowers would negotiate loan terms and complete compliance checks off-chain before transactions move to the network for execution.

Credit decisions stay off-chain while loan servicing moves on-chain

Ripple said the protocol separates institutional credit assessment from blockchain settlement. Once a loan has been approved, the XRP Ledger would automate operational tasks including interest calculations, repayment schedules, loan servicing, and default management.

According to Ripple, this structure was intentionally designed to keep underwriting and regulatory requirements under the control of financial institutions while using the blockchain for standardized execution. The company said this approach mirrors how traditional financial markets separate credit decisions from settlement infrastructure.

The proposal introduces two core building blocks. A Single Asset Vault would pool a single token for lending, while a dedicated Lending Protocol would manage loan origination, servicing, and repayment. Ripple said separating custody from lending infrastructure follows the model already used in conventional capital markets.

As one example, Ripple said a payment provider holding reserves of RLUSD could obtain short-term liquidity through the protocol while waiting for cross-border transactions to settle. According to the company, doing so would allow institutions to avoid liquidating reserve assets or relying on higher-cost bank credit facilities.

Institutional access depends on validator approval

Compliance remains a central part of the proposal. Ripple said both lenders and borrowers would need to complete identity verification before participating, with access controlled through permissioned credentials rather than open participation.

The company also proposed assigning first-loss capital at the lending facility level instead of distributing losses equally across all participants. According to Ripple, this structure is intended to create a clearer framework for allocating credit risk.

The lending framework has not yet become part of the XRP Ledger. Ripple said the technical specifications, published as XLS-65 and XLS-66, still require approval from XRPL validators before they can be activated on the main network. Until then, developers and infrastructure providers can begin testing the proposed system on the XRPL devnet.

The proposal arrives days after Ripple drew attention through another institutional finance connection. As previously reported by crypto.news, Elon Musk’s X has begun rolling out X Money to a limited group of Premium+ users using traditional banking infrastructure provided by Cross River Bank, a Ripple banking partner.

Although some members of the XRP community speculated that the relationship could eventually support blockchain-based payments or stablecoin services, neither X nor Cross River Bank has announced plans to integrate XRP or other cryptocurrencies into the payment platform.

For now, X Money operates entirely through conventional banking rails despite Musk previously suggesting crypto features could be added to the platform’s financial services in the future.

Key Highlights

- Over 140 corporations including Visa, Mastercard, and Stripe support the OUSD stablecoin initiative

- Consortium-driven governance replaces traditional single-issuer control structure

- Zero-fee minting and redemption model eliminates direct transaction costs for businesses

- Primary focus includes corporate payment systems, settlement operations, and treasury management

- Major South Korean corporations like Samsung, Dunamu, and Shinhan participate in the initiative

On June 30, 2026, Open Standard unveiled OUSD with endorsement from Visa, Mastercard, Stripe, and over 140 corporate partners. This initiative focuses on enterprise-scale payment infrastructure and settlement solutions, employing a collaborative governance framework rather than centralized control. The platform offers zero-cost token issuance and redemption, potentially streamlining stablecoin adoption across corporate environments.

Collaborative Governance Model Defines OUSD Framework

Open Standard unveiled OUSD as a consortium-driven digital dollar initiative. The alliance encompasses payment processors, financial institutions, tech enterprises, cryptocurrency exchanges, and blockchain service providers. This launch bridges conventional finance with digital asset ecosystems through unified operational infrastructure.

Unlike traditional stablecoins controlled by singular entities, OUSD operates through a partner-governed board system for strategic oversight. This framework provides member organizations with meaningful input on governance matters and strategic development.

The model distributes reserve income among participating organizations following operational expenses. Consequently, partners obtain tangible financial incentives tied to broader market penetration. This arrangement encourages active promotion since member firms benefit directly from ecosystem expansion.

Leading Payment Processors Anchor Extensive Corporate Coalition

Among Open Standard’s supporters, Visa, Mastercard, and Stripe represent the most prominent payment industry players. Their participation establishes robust connections to worldwide payment infrastructure and commercial networks. This involvement reflects growing institutional appetite for stablecoin-based settlement mechanisms.

Additional consortium members feature BlackRock, BNY, Coinbase, Google, IBM, Ripple, OKX, and Standard Chartered. The roster extends to BBVA, DBS, Mizuho, MoonPay, Rakuten Group, and Crypto.com. OUSD launches with comprehensive backing spanning banking, payment processing, technology sectors, and cryptocurrency services.

South Korean members comprise Samsung Electronics, Hanwha Group, Dunamu, and Shinhan Financial Group. The Korean contingent also features K-Bank, KB Kookmin Card, Samsung Card, BC Card, and Hana Card. Hyundai Card, NH Nonghyup Card, and Woori Card complete the regional partnership lineup.

Corporate Settlement Infrastructure Emphasizes Cost Efficiency

Open Standard architected OUSD for cost-effective, high-capacity stablecoin operations. Organizations can create and redeem tokens without transaction charges, based on release specifications. This characteristic holds particular significance for payment processing, treasury functions, and settlement workflows.

The platform eliminates predetermined supply caps. OUSD circulation can grow proportionally with rising commercial demand. This methodology seeks to accommodate substantial transaction volumes without imposed supply constraints.

OUSD deployment remains planned for late 2026. Upon launch, it will compete directly with dominant stablecoins like USDT and USDC. Open Standard frames OUSD as collaborative enterprise infrastructure rather than a centrally controlled financial instrument.

Crypto World

Circle (CRCL) slides as Stripe, Coinbase (COIN) and BlackRock (BLK) back rival stablecoin network

With more institutions embracing stablecoins, the competition is increasingly shifting from issuing tokens to determining who controls the underlying infrastructure and network.

Unlike most existing stablecoins, Open USD will allow businesses to mint and redeem tokens without fees while returning reserve income to participating partners, less a management fee. Governance will also be shared among members rather than controlled by a single issuer.

The model targets one of the core economics of today’s stablecoin market. Issuers such as Circle earn revenue by investing reserves backing their tokens in short-term U.S. Treasuries and retaining most of the interest generated by those assets. Open USD instead plans to distribute that yield to participating businesses.

The approach resembles the Global Dollar Network (USDG), a stablecoin consortium led by Paxos that shares reserve income with participating firms. That network is backed by companies including Robinhood, Kraken and Galaxy Digital, and was designed to encourage broader adoption by aligning incentives between the issuer and distribution partners.

In Europe, a group of banks and payment providers launched Qivalis, a venture to develop a euro-denominated stablecoin as financial institutions seek to build shared digital payment infrastructure.

The breadth of Open USD’s backing reflects that shift. Beyond Stripe, Coinbase, Mastercard and Visa, launch partners include BNY, Standard Chartered, DBS, U.S. Bank, Shopify, Google, IBM, Mercado Pago, Fireblocks, Anchorage Digital, MetaMask, Aave, Solana, Polygon and Ripple.

David Schwartz, co-founder of the XRP Ledger and Ripple CTO Emeritus, has proposed a two-component transaction reservation mechanism to address front-running and sandwich attack risks on XRPL’s native DEX and AMM.

The proposal, surfaced in response to concerns raised by XRP-focused analytics account XRPresso.io, introduces priority execution guarantees for users willing to pay a reservation fee, a market-integrity measure with direct relevance as institutional inflows into XRP products continue to scale.

The proposal is currently under community discussion and has not been formalized as a network amendment. That distinction matters: on the XRP Ledger, protocol changes require a supermajority of validators to vote in favor before activation, meaning Schwartz’s design carries weight but faces a defined governance process before it touches mainnet.

Discover: The Best Token Presales

How the Ripple XRP ReservedTxns Mechanism Actually Works

The scheme introduces two new protocol components. The first is a ReservedTxns ledger object, which stores a target ledger sequence number and an array of up to 32 transaction IDs.

When that specific ledger executes, any listed transactions present in the consensus set are processed first, ahead of all other transactions, after which the object is deleted. The second component is a TxnReserve transaction type, which allows a user to claim a priority slot for one or more future transactions by submitting a reservation before the target ledger closes.

Three constraints govern the TxnReserve: the reservation fee must be at least twice the standard transaction fee; the target ledger must fall within 16 ledgers of the current one; and the actual transaction must set its LastLedgerSequence to match the reserved ledger.

Those rules are not incidental, they define both the economic cost of using the system and the narrow time window in which it operates. The 16-ledger ceiling keeps reservations tightly coupled to near-term execution, preventing the mechanism from being weaponized as a general-purpose queue-gaming tool.

DoS protection is built in through dynamic fee scaling: as reservation slots fill past 16, fees step upward, reaching several multiples of the base reserve near 30 slots. Schwartz also specified that XRPL server software would hold reserved transactions and release them only close to when the prior ledger’s proposals are known, compressing the pre-execution visibility window.

“This guarantees that you can execute your transaction ahead of any transaction that was formed after your transaction was disclosed,” Schwartz said. “You would use this approach any time you want to perform a transaction that you want to ensure cannot be sandwiched or front run.”

The XRPL-Specific Front-Running Problem Schwartz Is Solving

XRPresso’s concern centers on a structural feature of the XRP Ledger: pending transactions sit in a publicly visible queue before a ledger closes, giving validators and well-connected nodes advance sight of incoming trades.

Because canonical transaction ordering on XRPL is determined by a known, deterministic formula involving transaction hashes, a sophisticated actor can submit similar transactions repeatedly to increase the probability of landing in a favorable slot relative to a target trade, the mechanistic basis for a sandwich attack on the DEX or AMM.

Schwartz acknowledged the exposure but contested the framing. He argued that all participants have equal access to the public queue, and that validators gain no structural ordering advantage unless several conspire.

“If multiple validators did conspire, or a single validator attempted it, it would be very obvious to everyone exactly who was doing this,” he said, adding that no such attempt has been confirmed outside of a proof-of-concept.

He also flagged a practical profitability constraint: extracting meaningful value requires simultaneously high liquidity (to generate volume worth targeting) and low liquidity (to move price at manageable cost), a combination rarely present on XRPL.

That argument has not fully satisfied critics, but it does distinguish XRPL’s current risk profile from Ethereum’s historically active MEV environment.

The front-running debate in DeFi is not isolated to the XRP ecosystem. Binance co-founder Changpeng Zhao proposed a dark pool perpetuals DEX last year using zero-knowledge cryptography to conceal order data until execution, an approach that drew its own criticism from decentralization advocates who argued it recreates the information asymmetries crypto was designed to eliminate.

XRPresso made a similar argument in response to Schwartz, contending that targeted confidentiality for pending transaction details would be a cleaner long-term fix than a reservation fee layer, and pointing to implementations already live on competing chains.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The post Ripple CTO Proposes ReservedTxns to Block Front-Running on XRPL DEX appeared first on Cryptonews.

- REAL launches private execution layer for RWA institutions.

- ZKsync tech enables confidential on-chain settlement via Ethereum.

- Platform aims to bridge the privacy gap in institutional blockchain use.

REAL has introduced a confidential execution layer designed to support regulated financial institutions operating in tokenized real-world asset (RWA) markets, addressing one of the key barriers to broader institutional adoption of blockchain-based finance.

The new layer, built using ZKsync’s Prividium technology, operates alongside REAL’s public Layer 1 network.

According to the company, it enables institutions to keep positions, allocations, and counterparty data private while still benefiting from public settlement and liquidity through Ethereum.

The company said the confidential layer is intended to provide privacy controls without compromising compliance, liquidity, or distribution, allowing institutions to participate in onchain markets while maintaining the confidentiality required for regulated financial operations.

Confidential infrastructure targets institutional needs

REAL said the new execution layer is designed to bridge the gap between public blockchain infrastructure and the operational requirements of regulated financial institutions.

While public blockchains offer benefits such as global access, instant settlement, and composability, the company noted that institutions have been reluctant to conduct business on networks where sensitive information—including positions, treasury strategies, and counterparty relationships—is publicly visible.

Because the confidential layer settles transactions on Ethereum, institutions can access the broader onchain capital market while maintaining operational privacy instead of operating within isolated private networks.

Platform supports regulated financial workflows

According to REAL, the confidential execution layer is built to support a range of institutional workflows where privacy is considered essential.

These include wealth and asset management activities that require protected portfolio information, balance sheet operations, tokenized deposit models, and selective disclosure capabilities for auditors, compliance teams, and regulators when necessary.

The company said institutions using the platform will continue to benefit from blockchain-native settlement, distribution, and liquidity while avoiding the need to expose sensitive business activity on fully public networks.

The launch also expands REAL’s broader strategy of supporting the entire lifecycle of tokenized real-world assets within a compliance-focused infrastructure.

The company said its platform covers issuance, risk assessment, insurance, trading, and institutional execution under a single architecture designed for regulated financial markets.

REAL expands institutional blockchain offering

REAL describes itself as an institutional blockchain infrastructure provider focused on compliant real-world asset tokenization and risk-managed capital flows.

Built on Cosmos Tendermint, the platform supports multiple stages of onchain financial products, including issuance, compliance, liquidity, insurance, risk assessment, and trading.

The company said its dual-validator architecture combines technical validators with business validators such as tokenizers, risk scorers, insurers, and credit agencies to provide an infrastructure aimed at institutional trust.

The confidential execution layer uses ZKsync’s Prividium privacy technology, which is designed to enable regulated entities to operate onchain with configurable confidentiality, selective disclosure, and settlement on Ethereum.

US Supreme Court upholds birthright citizenship in blow to Trump

First fully electric BMW X5 debuts as South Carolina plant expand

Claude AI Opus Predicts Stunning XRP Price by End of 2026

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Two goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

The Worst Scumbag Husband in Financial Audit History | Caleb Hammer Clips

Indian Man Faked His Own Kidnapping To Get Money From Family in India #shorts

L&T Finance Personal Loan Online Apply | L&T Finance Personal Loan | New Loan App | Instant loan app

-

Sports7 days ago

Two goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics4 days ago

Politics4 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World15 hours ago

Crypto World15 hours agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics5 days ago

Politics5 days agoPotential 2028er World Cup attendee leaderboard

-

Business4 days ago

Business4 days agoAsia stock markets slide as tech shares slump

-

News Videos2 days ago

News Videos2 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech5 days ago

Tech5 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World7 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 days ago

Crypto World5 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World3 days ago

Crypto World3 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business7 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World4 days ago

Crypto World4 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports4 days ago

Sports4 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Business14 hours ago

Business14 hours agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Tech3 days ago

Tech3 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World4 days ago

Hyperliquid Named on Singapore MAS Investor Alert Register

You must be logged in to post a comment Login