Crypto World

what it means for RLUSD and XRP

Ripple signed on to a dollar stablecoin backed by Visa, Mastercard, and BlackRock. It is not Ripple’s coin, and it does not launch on the XRP Ledger. So the question every XRP holder is asking is simple: does any of this actually help the token?

Summary

- On June 30, 2026, Ripple joined Open USD, or OUSD, a consortium dollar stablecoin backed by more than 140 companies including Visa, Mastercard, Stripe, BlackRock, BNY, Coinbase, and Google, as a day-one integration partner.

- OUSD is not a Ripple product. It is run by an independent organization called Open Standard, and it launches on Solana, Stellar, Base, and Polygon later in 2026, not on the XRP Ledger.

- Ripple kept its own stablecoin, RLUSD, and joined OUSD anyway, a hedge that puts the XRP Ledger forward as a possible rail while ensuring Ripple benefits from the traffic whichever stablecoin wins.

- The bull case for XRP is that a larger stablecoin market means more cross-currency flows for market makers to bridge, a role XRP can fill. The bear case is that OUSD competes directly with RLUSD, does not run on the XRP Ledger at launch, and a win for Ripple the company is not a win for the token.

- The deeper story is a challenge to Tether and Circle: OUSD shares its reserve income with partners instead of keeping it, inverting the economics that built the stablecoin giants.

Every so often, Ripple turns up somewhere that makes XRP holders pay attention, and the launch lineup for Open USD is the latest. On June 30, 2026, Ripple signed on as a day-one integration partner to a new dollar stablecoin backed by Mastercard, Visa, Stripe, BlackRock, and more than 140 other companies. The headline reads like a win for Ripple, and it may well be one for the company. Whether it does anything for XRP, the token, is a separate and much harder question, and the answer runs through two details most coverage skips: OUSD is not Ripple’s coin, and it does not launch on the XRP Ledger.

This piece works through what Open USD is, why Ripple joined a project that competes with its own stablecoin, and what the move means for both RLUSD and XRP. The same distinction keeps returning across Ripple’s 2026 story: a Ripple win is not an XRP win unless there is a clear transmission mechanism from the company’s progress to token demand. Open USD is one more test of that rule. It is a company-level strategy first, and only a token catalyst if the usage eventually reaches XRP.

What Open USD actually is

Start with the thing itself, because the branding invites confusion. Open USD is a dollar-backed stablecoin created by Open Standard, an independent organization set up to run and govern the coin, with a board drawn from its partners and Zach Abrams as founding chief executive. It is not issued or controlled by Ripple. Ripple is one name on a launch roster that reads like a directory of global finance and technology: Visa, Mastercard, Stripe, BlackRock, BNY, Coinbase, Google, IBM, OKX, Standard Chartered, Shopify, and more than 140 companies spanning banking, payments, technology, and crypto.

The coin is planned to go live later in 2026. The design is where OUSD gets interesting, because it goes straight at the business model that built the stablecoin giants. Businesses will be able to mint and redeem OUSD with no fees and no volume limits. More striking, most of the income thrown off by the coin’s reserves, the interest earned on the dollars backing it, goes to the participating businesses after a small management fee, instead of being kept by a single issuer.

That is close to the opposite of how Tether and Circle operate. Tether earned more than $10 billion in 2025 almost entirely from interest on its reserves, and Circle makes money the same way while handing about half of it to Coinbase for distribution. OUSD hands the float back to the network, which is a direct attack on the issuer-keeps-the-interest model. For readers new to the category, OUSD is still a dollar-backed stablecoin; what differs is who gets the economics.

The launch chains matter for the rest of this analysis, so note them precisely. OUSD is set to go live on Solana, with Stellar, Base, and Polygon in the mix, and Solana is being highlighted as a native day-one chain. The XRP Ledger is not among the launch networks. That single fact reshapes what Ripple’s participation can realistically mean for XRP, and we will return to it.

Why Ripple joined a rival to its own stablecoin

The obvious objection is that Ripple already has a stablecoin. RLUSD launched at the end of 2024 and has grown into a top-ten dollar token. So why would Ripple help build a competitor chasing the same institutional payments customers? The answer lies in how Ripple joined and in a strategy already visible across the industry.

By signing on as an integration partner rather than an issuer, Ripple keeps RLUSD and still positions the XRP Ledger as one of the rails OUSD could eventually run on. In that framing, Ripple wins traffic no matter which stablecoin comes out on top, because its ledger and its payment infrastructure can carry flows for the winner. This fits a pattern the big card networks set over the past year. Mastercard has spent that time settling payments across several blockchains and already handles Ripple’s own RLUSD alongside USDC, positioning itself as neutral infrastructure instead of the backer of any single issuer.

Ripple is doing the same thing: putting itself forward as neutral ground to claim a spot on as many rails as possible. Seen that way, joining OUSD is a hedge, not a contradiction. If OUSD becomes the dominant enterprise stablecoin, Ripple wants to be inside it. If RLUSD holds its ground, Ripple still has its own product. And if the market fragments across several coins, Ripple’s infrastructure can move value between them.

For Ripple the company, that is a sensible bet in every direction. The harder question is what any of it does for the token that XRP holders own. This is where RLUSD versus XRP becomes more than a pricing debate. Ripple can expand its stablecoin reach and its institutional relevance while XRP still waits for direct demand.

The catch: Open USD does not launch on the XRP Ledger

Here is the detail that undercuts the simplest bullish reading. OUSD is launching on Solana, Stellar, Base, and Polygon, not on the XRP Ledger. Ripple joined the consortium, but its own ledger is not among the chains carrying the coin at launch. The crypto analyst who goes by WrathofKahneman flagged this in a July 1 thread, noting that the absence left traders asking what Ripple actually gets from the deal and whether XRP benefits at all.

The gap matters because the standard XRP-benefits argument assumes the XRP Ledger carries the stablecoin’s traffic, generating activity and demand tied to the token. If OUSD does not run on the ledger, that direct channel does not exist at launch. Ripple’s integration-partner status keeps the door open to adding the XRP Ledger later, and Ripple can still route value between OUSD on other chains and RLUSD on the ledger, but the immediate, mechanical link many holders imagined is not there on day one.

This is the recurring problem with reading Ripple corporate news as XRP news. Ripple the company can join a landmark consortium, position its rails, and benefit commercially, all without the token capturing much of the value. The XRP Ledger not being a launch chain for OUSD is the clearest illustration yet that a Ripple win and an XRP win are not the same event. The market will need usage data, not a partner logo, before treating this as an XRP catalyst.

The bull case for XRP

There is still a credible, if indirect, argument that XRP benefits, and it runs through market structure instead of through the ledger carrying OUSD directly. Start with the size of the pie. If OUSD succeeds in bringing a wave of new institutional payment flows on-chain, the total volume of dollars moving across blockchains grows. Larger, more fragmented stablecoin markets create more price gaps between venues, chains, and currency pairs, and those gaps are filled by market makers who arbitrage them.

A fast, cheap bridge asset is useful in that role, and XRP was designed to be exactly that. The mechanism does not require any enterprise to touch XRP directly. An institution can use OUSD or RLUSD for settlement and never think about XRP, while market makers behind the scenes move value between OUSD, RLUSD, fiat pairs, and other assets, sometimes reaching for XRP because it is fast and cheap at the moment they need it. That activity tightens spreads and can lift volumes in XRP pairs tied to the growing stablecoin mesh.

Geography reinforces the point. RLUSD is now available in Japan after regulatory approval and is rolling out to institutions in Turkey through local partners, and those corridors are practical instead of speculative. If OUSD shows up as a settlement coin at global partners while RLUSD deepens in real corridors, the web of rails expands, and each new connection creates small arbitrage windows that a bridge asset can fill. The optimistic reading, then, is that Ripple has bought a seat at the table of the most heavily backed stablecoin ever launched, and that a bigger, busier stablecoin economy is good for an asset built to move liquidity between its pieces.

The bull does not need the XRP Ledger to carry OUSD at launch. The bull needs the overall market to grow and stay fragmented enough that bridging has value. That is the most credible XRP-positive version of the story. It is indirect, but it is not imaginary.

The bear case for XRP

The skeptical case is more concrete, and it starts with cannibalization. OUSD competes directly with RLUSD. Both target institutional payments and settlement, and both chase the same enterprise customers. Ripple joining a rival that goes after its own product’s market is a strange look, and at least one analyst noted the obvious tension: if OUSD competes with RLUSD, where does that leave RLUSD?

A consortium coin with Visa, Mastercard, and BlackRock behind it and a revenue-sharing model is a formidable competitor for a single-issuer stablecoin, even one with Ripple’s regulatory standing. Then there is the ledger problem already covered: OUSD does not launch on the XRP Ledger, so the direct on-chain benefit to XRP is absent at the start. Even if OUSD were added to the ledger later, XRP Ledger transaction fees are tiny, fractions of a cent, so a stablecoin moving across it would consume only a trickle of XRP through the network’s small transaction burn. The value of stablecoin traffic accrues mostly to the issuer, the rails operator, and the partners sharing reserve income, not to the ledger’s native token.

The track record hangs over all of it. Ripple has stacked up regulatory wins, ETF launches, acquisitions, and partnerships over the past year, and XRP has still fallen, trading near a multi-month low. Good news has repeatedly failed to move the token, which suggests the market already prices Ripple’s corporate progress separately from XRP demand. That is why institutional XRP demand matters more than institutional Ripple headlines. If the buyers are buying Ripple’s rails, RLUSD, or OUSD rather than XRP itself, the token’s price still lacks the direct bid holders need.

Finally, the consortium itself is unproven. Coinbase helped found the original USDC governance body, the Centre Consortium, with Circle in 2018, and that arrangement ended in acrimony and a nine-figure buyout by 2023. Whether a 140-member consortium governs any more durably than a two-member one did is an open question, and Ripple’s day-one hedge could look prescient or could look like a bet on a coin that never gains traction.

What it means for RLUSD

The most direct casualty of the OUSD launch may be RLUSD, and the timing is unkind. Ripple’s stablecoin has been contracting rather than growing, slipping from a peak near $1.7 billion in market value toward roughly $1.4 billion, even as Ripple expanded it into Japan through regulatory approval and into Turkey through local partners. Launching a consortium rival backed by the largest names in payments into that softness sharpens the competitive pressure on a coin already losing ground.

RLUSD is not without strengths. It is issued by a Ripple subsidiary under a New York trust charter, carries approvals in New York and Dubai, and has been built around regulatory standing and enterprise payments from the start. It runs on both the XRP Ledger and Ethereum, and Ripple-linked reporting has pointed to billions in RLUSD volume routed through XRP Ledger pairs since launch, which supports ledger activity even if it has not lifted the token’s price. Those are real assets in a market where regulatory clarity and compliance matter to institutions.

The strategic read is that Ripple is refusing to bet everything on RLUSD winning outright. By keeping RLUSD and joining OUSD, it hedges against its own stablecoin losing the institutional race, accepting more competition for RLUSD in exchange for a stake in whatever coin dominates. That is rational for the company and uncomfortable for RLUSD partisans, because it signals that Ripple itself is not certain its stablecoin wins. For the broader market, the more important shift is the revenue-sharing model OUSD introduces, which pressures every issuer, RLUSD included, to justify keeping the float that stablecoins have always quietly earned.

What would make it a real catalyst for XRP

Cutting through the announcements, the question for XRP holders is what evidence would turn OUSD from a headline into a genuine driver of token demand. The first thing to watch is listings and liquidity. If major exchanges roll out OUSD and RLUSD trading pairs widely, and market makers post tight two-sided quotes with XRP sitting in the settlement path, that is a more credible signal than any press release, because it shows XRP actually being used to bridge the new flows.

The second is whether the XRP Ledger gets added as an OUSD rail over time. Ripple’s integration-partner role leaves that possible, and if it happens, the ledger would carry some OUSD traffic directly, a more concrete link than the market-maker channel. The third is real usage rather than announced partnerships: circulating supply growth for OUSD, partner-led mint and redeem activity, merchant payment volume, and sustained peg stability, the metrics that separate a working stablecoin from a launch-day roster. Until those appear, OUSD is a promising structure with famous backers and little proven adoption.

The honest conclusion is that Ripple joining Open USD is a clear positive for Ripple the company and an ambiguous event for XRP the token. It expands Ripple’s footprint, hedges its stablecoin bet, and positions its rails inside the most heavily backed stablecoin project yet attempted. For XRP, the benefit is indirect, contingent on market-maker behavior and future ledger integration, and offset by direct competition with RLUSD and the plain fact that the coin does not launch on the XRP Ledger. As always with Ripple news, the safest move is to separate the company’s progress from the token’s, and to watch usage instead of announcements.

The stablecoin war Open USD just escalated

Zoom out from Ripple, and the launch is best read as a shot in a widening stablecoin war. The market reaction told the story within hours. Shares of Circle, the issuer of USDC that went public earlier in 2026, fell by double digits on the news, as traders priced Open USD as a direct threat to the two incumbents that dominate the market, Tether and Circle. Some analysts pushed back, with William Blair calling the selloff an overreaction and arguing that USDC’s proven liquidity and institutional footprint would be hard for any newcomer to replicate.

The disagreement is itself the point: a launch-day partner list, however impressive, is not the same as adoption, and the market is unsure how much of a threat the consortium really is. The competitive backdrop explains why the roster drew blood. Tether and Circle have built enormously profitable businesses on a simple model, taking in dollars, parking them in safe assets like Treasury bills, and keeping the interest while the coin circulates free to use. That float income runs into the billions of dollars a year for the largest issuer alone.

Open USD aims a revenue-sharing model straight at that economics, returning most of the reserve income to the businesses that drive adoption. If payment networks and platforms can earn a share of the float by supporting a coin, the incentive to promote it changes, and that is what makes a consortium of card networks, banks, and technology firms a different kind of competitor from a standalone issuer. There is a regulatory current underneath all of this. Stablecoin legislation in the U.S. has moved from uncertainty toward a defined framework, giving banks, payment networks, and large enterprises the confidence to enter a market many had watched from the sidelines.

Open USD, with its lineup of regulated financial institutions, is a product of that shift as much as a response to it. The same clarity that let Circle go public and let Ripple pursue trust charters for RLUSD is what makes a 140-member consortium coin plausible in the first place. For XRP, the widening war cuts both ways, and it sharpens the analysis already laid out. A world with more stablecoins, more issuers, and more chains is a world with more fragmentation, and fragmentation is where a bridge asset earns its keep, moving value between coins and currencies that do not settle directly against one another.

That is the structural case for XRP in a multi-stablecoin market. The offsetting risk is that the winners of the stablecoin war may build their own settlement mesh across the chains they favor, and if the XRP Ledger is not among those chains, as it is not for Open USD at launch, XRP could find the bridging work routed around it. The token’s relevance in this new landscape depends less on how many consortiums Ripple joins and more on whether market makers keep reaching for XRP when they move value across an increasingly crowded field of dollar tokens. The launch, then, is a marker of how fast the stablecoin market is maturing from a two-issuer contest into an infrastructure battle among the largest names in finance.

Ripple has positioned itself inside that battle on multiple sides at once. Whether XRP the token shares in the outcome is the question the next year of usage data, not the launch-day roster, will answer.

Frequently asked questions

Is Open USD a Ripple stablecoin?

No. Open USD, or OUSD, is issued and governed by an independent organization called Open Standard, with a board drawn from its partner companies. Ripple is one of more than 140 partners and joined as a day-one integration partner, not as the issuer. Ripple kept its own separate stablecoin, RLUSD, which it issues through a subsidiary under a New York trust charter.

Who is backing Open USD?

Open USD launched with a roster of more than 140 companies spanning payments, banking, technology, and crypto, including Visa, Mastercard, Stripe, BlackRock, BNY, Coinbase, Google, IBM, OKX, Standard Chartered, and Shopify, among others. The coin is run by the independent Open Standard organization and is planned to go live later in 2026 across several blockchains. The size and quality of the partner list are the main reason the launch drew market attention.

Does Open USD run on the XRP Ledger?

Not at launch. Open USD is set to go live on Solana, Stellar, Base, and Polygon, with Solana highlighted as a native day-one chain. The XRP Ledger is not among the launch networks. Ripple’s integration-partner status leaves open the possibility of adding the ledger later, but the direct on-chain link to XRP does not exist at launch.

Why did Ripple join a stablecoin that competes with RLUSD?

Ripple appears to be hedging. By keeping RLUSD and joining OUSD as an integration partner, it positions its infrastructure to benefit whichever stablecoin wins, and it can route value between OUSD on other chains and RLUSD on the XRP Ledger. It mirrors how card networks like Mastercard now settle across many chains and multiple stablecoins instead of backing a single issuer. That is sensible for Ripple the company, even if it complicates the RLUSD story.

Does Open USD help the XRP price?

The benefit is indirect and uncertain. A larger stablecoin market can create more cross-currency flows for market makers to bridge, a role XRP can fill, which could lift volumes in XRP pairs. But OUSD does not launch on the XRP Ledger, XRP Ledger fees are tiny, and Ripple’s past wins have not lifted the token. A win for Ripple the company is not automatically a win for XRP.

How is Open USD different from Tether and Circle?

Open USD inverts the core economics. Tether and Circle keep the interest earned on their reserves, which has made them enormously profitable. Open USD instead shares most of that reserve income with its participating businesses after a small management fee, and lets businesses mint and redeem without fees or volume limits. That model is a direct challenge to the issuer-keeps-the-float approach that built the stablecoin giants.

What does Open USD mean for RLUSD?

It intensifies competition. OUSD targets the same institutional payments and settlement market as RLUSD, and it arrives while RLUSD has been contracting, slipping from a peak near $1.7 billion toward roughly $1.4 billion, even as Ripple expanded it into Japan and Turkey. Ripple keeping RLUSD while joining OUSD signals it is not betting everything on its own stablecoin winning the institutional race outright. It also pressures RLUSD to prove adoption through real payment and settlement volume.

What should XRP holders watch to judge the impact?

Watch for real usage instead of announcements. Key signals include major exchanges listing OUSD and RLUSD pairs with market makers quoting XRP in the settlement path, the XRP Ledger being added as an OUSD rail over time, and adoption metrics such as circulating supply growth, mint and redeem activity, merchant volume, and sustained peg stability. Those separate a working stablecoin from a launch-day partner list. Until those signals appear, the XRP impact remains speculative.

Disclaimer: This article is for information purposes only and does not constitute financial, investment, or trading advice. Cryptocurrency prices are highly volatile, and the success of new stablecoins and consortium projects is uncertain and can change. Nothing here is a recommendation to buy or sell any asset. Always do your own research and verify current figures on reputable data platforms before making financial decisions. Information is accurate as of July 2, 2026, and may change.

Crypto World

Franklin Templeton Executes Tokenized U.S. Treasury Trade With Stablecoins on Canton Network

TLDR:

- Franklin Templeton exchanged a tokenized Treasury security for tokenized cash using on-chain settlement.

- The transaction paired a tokenized U.S. Treasury with USDCx and settled through Canton Network infrastructure.

- Tradeweb executed and priced the trade while several financial firms participated in the transaction.

- The deal occurred after market hours and was later reported to TRACE, according to Christopher Perkins.

Franklin Templeton has completed a tokenized U.S. Treasury transaction using stablecoins and on-chain settlement infrastructure. The trade involved the exchange of a tokenized Treasury security for tokenized cash on the Canton Network.

Tradeweb facilitated execution and price discovery while several financial firms supported the transaction. The deal adds to institutional efforts to move real-world assets onto blockchain-based financial rails.

Tokenized U.S. Treasury Trade Executes on Canton Network

Tradeweb announced the completion of the real-time transaction on July 1. The trade paired an on-chain U.S. Treasury with tokenized cash known as USDCx.

According to the announcement, Franklin Templeton transferred a tokenized Treasury security to Virtu Financial. In return, Virtu delivered USDCx through synchronized settlement on the Canton Network.

Tradeweb supplied the execution venue and pricing services for the transaction. The Canton Network coordinated the simultaneous movement of both assets on-chain.

Participants included Blockdaemon, Digital Asset, Franklin Templeton, Societe Generale, Tradeweb, and Virtu Financial. The transaction was also reported to TRACE after execution.

Christopher Perkins, president of CoinFund and former Coinbase executive, said on X that the trade took place after normal market hours. He noted that the transaction settled nearly instantly and represented another step toward continuous on-chain markets.

Tokenized Real-World Assets Gain Institutional Momentum

Tradeweb said the transaction demonstrates how tokenized U.S. Treasuries and tokenized cash can settle in real time. The company noted that traditional timing and settlement limitations did not apply to the process.

The transaction also arrives as the Canton Network prepares for the launch of DTCC’s Tokenization Services later this year. According to the announcement, the initiative aims to support broader access to high-quality liquid assets beyond traditional market hours.

Digital Asset said the transaction marked another milestone in developing always-on and interoperable capital markets infrastructure. The company added that continuous market making can increase asset utility and improve market accessibility.

Franklin Templeton described each tokenized transaction as another step toward a round-the-clock liquidity layer. The asset manager stated that on-chain capabilities can allow high-quality assets to move without the restrictions of standard market schedules.

Virtu Financial said the trade expands its market-making capabilities into tokenized U.S. Treasuries. The company added that blockchain-based settlement can support liquidity provision without conventional settlement constraints.

The Canton Network said active participation from firms including Franklin Templeton, Tradeweb, and Virtu Financial contributes to a unified framework for moving real-world assets across digital financial systems.

Strategy’s long streak as one of Bitcoin’s most consistent institutional buyers may be ending, according to Bitwise chief investment officer Matt Hougan. Speaking Thursday, Hougan suggested the company’s dominance as a “one-way” source of demand is likely to shrink in the next market cycle, after volatility around Strategy’s principal perpetual preferred stock product, Stretch (STRC).

The reassessment comes after STRC broke sharply from its $100 par value to below $75 late last month, a move that undermined investor confidence in the sustainability of Strategy’s dividend-style model. The timing also overlapped with broader market stress, when Bitcoin fell to a 21-month low of $58,190 on June 25.

Key takeaways

- Bitwise CIO Matt Hougan said Strategy’s era as Bitcoin’s dominant buyer may be over, with other institutional allocators expected to play a larger role next cycle.

- STRC’s move away from $100 par value below $75 fueled concerns about whether Strategy’s yield structure can hold up through “end-of-cycle” dynamics.

- Despite the STRC shock, Hougan argued Strategy is not facing near-term liquidity risk based on liquid asset coverage.

- Strive CEO Matt Cole pushed back, calling the STRC episode overblown and noting Strategy’s Bitcoin holdings are about 4% of total supply.

Strategy’s buyer dominance questioned after STRC turmoil

For years, Strategy has been widely viewed as a steady, high-conviction buyer of Bitcoin—helping provide consistent demand even when broader sentiment weakened. Hougan framed Thursday’s comments around a shift in what investors should expect from that demand profile.

“For years, Strategy has been the most dominant Bitcoin buyer in the world and a one-way source of Bitcoin demand. Those days are likely over,” Hougan said in a CIO memo, adding that he expects the company to be “less important” than it was in the previous cycle. In his view, banks, asset managers, pensions, endowments, and sovereign wealth funds may replace Strategy as Bitcoin’s primary demand engine as the next upcycle develops.

Hougan’s concern centers on how STRC behaved during a period when markets were already under pressure. The STRC incident raised fears that the structure underpinning dividend payments could be strained when conditions tighten—particularly in late-cycle environments where risk appetite falls and funding costs rise.

Why Hougan sees STRC as “end-of-cycle dynamics”

Hougan characterized the STRC drop as a pattern he associates with late-cycle stress. He compared the situation to a prior example in 2021: the collapse of Grayscale’s GBTC premium.

His argument is essentially about fit. According to Hougan, “money searching for high yields and low volatility was used to buy Bitcoin, which offers neither.” In that framing, the market eventually needs to “clear out” capital that was attracted by yield characteristics that Bitcoin itself does not reliably provide, before a more durable bottom can form.

This perspective matters for traders and longer-term investors because it reframes Strategy’s recent volatility away from a single-company solvency story and toward a broader liquidity-and-demand composition story—one where the source of marginal demand changes as the cycle matures.

Strategy responds: funding dividends and increasing reserves

In the aftermath of the STRC disruption, Strategy said it would sell Bitcoin when necessary to fund dividends, according to coverage earlier published by Cointelegraph. The company also expanded its US dollar reserve to $2.55 billion, easing some immediate concerns about operational coverage.

Even with those steps, Hougan said Strategy’s role as an aggressive buyer has weakened. The implication for market participants is that reserve moves and occasional Bitcoin sales can stabilize the dividend narrative in the short term, but may also reduce the consistency of net buying during turbulent periods.

Hougan nonetheless said he still expects Strategy to be a “net buyer” in the next bull run—suggesting the firm’s long-term posture may persist, even if its influence on price dynamics is likely to be less dominant than in the last cycle.

Debate over materiality and liquidity risk

While STRC became the focal point, Strategy leadership pushed back on how much attention the incident deserves. Strive CEO Matt Cole argued that the episode has been overemphasized by media and that Bitcoin’s selloff may have been driven more by the broader market than by any single factor.

Speaking with NovaDius Wealth Management president Nate Geraci, Cole noted that Strategy’s 847,363 Bitcoin represents about 4% of total supply. He also referenced US Securities and Exchange Commission standards for materiality, stating that a 4% stake would not be considered material under SEC thresholds, which he described as starting at 5%.

“If one person owned 4%, you don’t even have to report that publicly to the SEC because the SEC deems 4% to be immaterial. They start to view a position to be material at 5%.”

Hougan, meanwhile, addressed liquidity in a more quantitative way. He said Strategy has $52 billion worth of liquid assets marked against $7 billion of debt. In his assessment, Bitcoin would need to fall another 70%—to roughly $18,500—for Strategy to face risk. He also added that if the company began selling Bitcoin immediately, it could cover dividends from STRC and other perpetual preferred stock offerings for the next 28 years.

Taken together, the two positions highlight a tension that investors should watch: one view suggests the STRC mechanism is a late-cycle stress test that affects demand composition and price, while the other emphasizes reserve coverage and argues that the company’s balance sheet prevents an immediate liquidity threat.

For now, the key question is not whether Strategy can operate through the current strain, but whether the market’s next wave of Bitcoin buying will be driven by the same yield-seeking, vehicle-based demand—or by a broader set of long-term allocators that Hougan expects to take a bigger share.

As conditions evolve, investors should monitor whether STRC stabilizes relative to par and whether Strategy’s net buying pace remains consistent enough to reassert influence—while also tracking if incremental demand truly shifts from Strategy-style products to the wider institutional categories Hougan cited.

Riot Platforms transferred another 500 BTC to NYDIG Custody, according to Arkham data cited by onchain trackers.

Summary

- Riot Platforms moved another 500 BTC to NYDIG Custody, raising fresh sale speculation among traders.

- The miner already sold 3,778 BTC in Q1 while producing only 1,473 BTC total.

- Public Bitcoin miners continue selling reserves as mining costs rise and margins remain under pressure.

The transfer was worth about $30.72 million at the time of the report and was shared through an Onchain Lens post.

The move may signal that Riot is preparing to sell part of its Bitcoin holdings. Transfers to custody or execution partners do not always confirm a sale, but similar Riot transfers this year have often come before reported selling activity.

Another move in a longer sale pattern

The latest transfer follows earlier Riot activity involving NYDIG. As crypto.news reported in April, Riot sent 500 BTC to an NYDIG deposit address in a move worth about $39 million at the time. That report said the transfer added to a series of Bitcoin moves from Riot over the same period.

Riot had also disclosed large Bitcoin sales in its first-quarter 2026 operations update. The company sold 3,778 BTC in Q1 for about $289.5 million. It sold those coins at an average net price of $76,626 per BTC.

Riot produced 1,473 BTC in the first quarter, down 4% from 1,530 BTC in the same period a year earlier. Its BTC holdings fell to 15,680 at quarter-end, down 18% from 19,223 in Q1 2025. The company said 5,802 BTC were restricted at the end of the quarter.

Riot’s Q1 results also showed pressure in its mining business. Bitcoin mining revenue fell to $111.9 million from $142.9 million a year earlier. Riot linked the decline to lower average Bitcoin prices and higher network hash rate.

Miner selling pressure continues

Riot’s latest BTC movement comes as public miners face tighter economics after the Bitcoin halving. Higher mining difficulty, lower hashprice, energy costs, and capital needs have pushed several listed miners to sell reserves.

As crypto.news reported, publicly traded Bitcoin miners sold more than 32,000 BTC in the first quarter of 2026. That was a record quarterly figure and topped the amount sold by the same firms across all of 2025. Riot, MARA, CleanSpark, Cango, Core Scientific, and Bitdeer were among the miners named in that wider trend.

Riot also continues to expand beyond Bitcoin mining. The company has been building a data center business while using its power assets and infrastructure to serve high-performance computing customers. That shift gives the miner another capital need at a time when mining margins remain tight.

The 500 BTC transfer does not confirm an immediate sale on its own. Still, the timing adds to the market’s focus on Riot’s treasury strategy.

Ether and solana led crypto higher on Friday as a squeeze on bearish traders pushed bitcoin toward $62,000, capping the market’s first genuinely strong week since mid June.

Bitcoin traded around $61,360, up 2.5% over seven days, per CoinDesk data. Ether rose 4.2% in 24 hours to about $1,702 and is up 9.7% on the week, while solana held near $80 with a weekly gain of 18.6%, the strongest among the majors. XRP added 5.7% over the week to $1.09 and Hyperliquid’s HYPE rose 5.1% on the day.

Traders betting against crypto lost $281 million to liquidations over the past 24 hours, against $159 million in longs, out of $440 million in total forced closures across 95,690 traders, according to Coinglass data.

When shorts are forced to close, they buy back the asset, and that buying pushes prices into the next tranche of shorts, the loop that turns a modest bounce into a squeeze.

The largest single liquidation was an $18.2 million ether position on Hyperliquid, fitting a day when ether led the damage to bears at $157 million in wiped positions against bitcoin’s $103 million in an unusual flip.

The U.S.-listed bitcoin ETFs pulled in $221.7 million on Thursday, their largest inflow in two months, according to SoSoValue.

Fidelity’s FBTC led the charge with a hefty $165.96 million inflow, followed by ARKB at $91.84 million and HODL at $4.35 million. BlackRock’s IBIT, the world’s largest Bitcoin ETF, was the outlier with a $40.43 million outflow.

The cumulative inflow ends a painful 10-day outflow streak that saw investors pull $2.73 billion from the funds. Even so, the year-to-date picture remains ugly, with net outflows still sitting at a hefty $5.4 billion.

Thursday’s bounce is therefore a drop in the ocean compared to the selling we’ve seen this year. Still, it’s a welcome sigh of relief for the bulls. At the very least, it helps validate bitcoin’s rebound to around $61,700 after hitting 21-month lows under $58,000 earlier this week.

For a real recovery, though, these inflows need to turn into a consistent trend. Historically, steady money flowing into Bitcoin ETFs has been a hallmark of bull runs.

Binance is reportedly set to lead a new funding round for Mesh, a crypto payments and settlement company, at a valuation of up to $2 billion.

Summary

- Binance’s planned lead role could double Mesh’s valuation from $1B to as much as $2B.

- Mesh’s payments network targets digital asset transfers across wallets, exchanges, stablecoins, and fiat rails globally.

- Growing stablecoin rules and tokenization demand are pushing investors toward crypto settlement infrastructure providers.

The deal was reported by Axios, citing people familiar with the matter. The report said demand for digital asset-to-fiat transfer tools, payment systems, and settlement infrastructure is rising.

Meanwhile, that demand comes as stablecoin rules become clearer and tokenization moves deeper into financial markets. The round has not been formally announced by Binance or Mesh.

Mesh valuation could double

The reported round would mark a sharp rise in Mesh’s valuation. As crypto.news reported, Mesh raised a $75 million Series C in January at a $1 billion valuation. That round was led by Dragonfly Capital, with backing from Paradigm, Moderne Ventures, Coinbase Ventures, SBI Investment, and Liberty City Ventures.

Mesh was formerly known as Front Finance. The company builds payment infrastructure that connects wallets, exchanges, digital assets, and fiat rails. It aims to make crypto payments easier for users while letting merchants receive stablecoins or fiat without handling complex blockchain steps.

Stablecoin rules lift demand

Stablecoins have become a major focus for payment companies, exchanges, and banks. Banking Circle launched regulated stablecoin settlement services after receiving approval in Luxembourg. The bank now supports USDC, USDG, and its own EURI for institutional fiat and crypto conversion.

The market is also moving toward tokenized bank deposits. As crypto.news reported, major U.S. banks are backing a tokenized deposit network through the Clearing House, with a launch targeted for early 2027. That system would let banks settle tokenized deposits around the clock while keeping customer deposits inside regulated banking channels.

Funding race turns to settlement

Mesh sits in the middle of this shift because it focuses on the movement of value between assets, wallets, and payment systems. Its model addresses a common issue in crypto payments: users may hold one asset, while merchants or platforms may want settlement in another asset or in fiat currency.

The company has also worked to expand access through partnerships. Moreover, Mesh partnered with Italy’s crypto wallet Conio in 2024, giving Conio users access to several crypto exchanges and withdrawal options through Mesh’s connection layer.

A Binance-led round would show that large exchanges still see payment and settlement infrastructure as a core growth area. It would also place Mesh closer to the center of the stablecoin and tokenization race, where firms are trying to connect crypto rails with everyday payments, institutional transfers, and fiat settlement.

The reported valuation also reflects a wider shift in crypto funding. Investors have moved beyond trading apps and tokens toward systems that can support regulated payments, cross-border transfers, and asset settlement.

If the round closes near the reported level, Mesh would have doubled its valuation in about six months, showing continued demand for infrastructure that links digital assets with traditional money.

TLDR:

- Ironwood testnet activates with two independent consensus implementations built by separate teams.

- Zcash reduced ten-note wallet migration times from around 15 minutes to about 2.5 minutes.

- Multi-transaction signing now supports more than 11 transactions through a single QR code.

- Mainnet activation could occur around July 21 as audits and ZIP specifications near completion.

Zcash is moving forward with its Ironwood network upgrade after confirming a scheduled testnet activation. The update introduces new consensus changes and major wallet performance improvements ahead of a planned mainnet deployment.

Development teams have also completed two independent consensus implementations for the upgrade. The work marks one of the most advanced testnet preparations recorded for a Zcash network upgrade.

Zcash Ironwood Testnet Upgrade Brings Dual Consensus Implementations

Zcash developer Dev announced that the Ironwood testnet upgrade would activate on July 4. The release includes two independently developed consensus implementations.

One implementation came from Valar Group, while the other was built by the Zcash Foundation. According to Dev, the Valar Group version has already entered the audit process.

The teams also released a desktop wallet fork that supports migration testing on the testnet. Users with Keystone development devices can update firmware and test migration functions before the mainnet launch.

The upgrade introduces multi-transaction signing through a single QR code. Dev said the feature required extensive work behind the scenes and represented a major technical milestone for the testnet.

Contributors from zodl also participated in the process. The group worked on technical specifications, wallet libraries, circuit updates, and application programming interfaces supporting Ironwood.

Zcash Wallet Performance Improves Ahead of Mainnet Activation

Development updates shared by Dev showed major gains in wallet migration performance. The time needed to complete a ten-note migration fell from around 15 minutes to approximately two and a half minutes.

Inbound QR scanning dropped from three minutes to one minute. Loading and transaction review declined from two minutes to 45 seconds.

The signing process posted the largest improvement. Signing time fell from roughly nine minutes to about 37 seconds.

Outbound QR scanning also became faster. The process now takes about 10 seconds compared with roughly one minute previously.

In a separate update, Zcash developer Sean Bowe said all Ironwood consensus rule changes had been implemented and were undergoing audits.

He added that the specifications and Zcash Improvement Proposals, known as ZIPs, were approaching their final state.

Bowe also said developers expected readiness for a mainnet activation around July 21. He confirmed that the official testnet activation was scheduled for the following day and noted that the Zebra release supporting Ironwood should become available around the same time.

According to Bowe, sufficient mining hash rate already signals technical readiness for the mainnet upgrade. He noted that some wallets may not support Ironwood immediately, although alternative options and testnet preparation time remain available before activation.

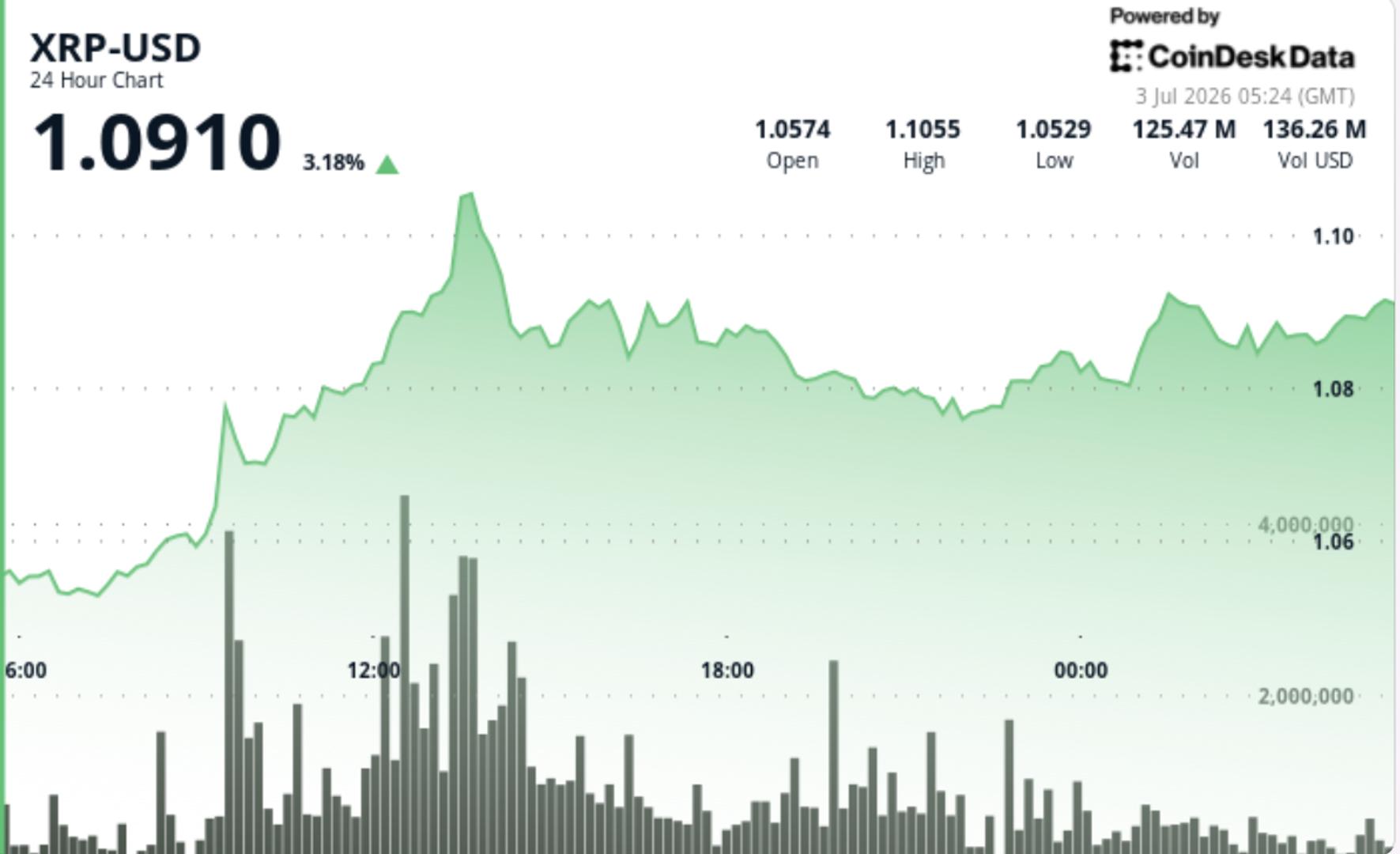

XRP is starting to build a higher base above $1 following last week’s sell-off. The token edged higher through the U.S. session, held $1.08 on repeated tests and pushed toward $1.10 before sellers slowed the move. That keeps the setup constructive, but still unfinished, with traders watching whether the latest accumulation turns into a clean breakout.

News Background

• XRP wallet creation rose to 4,941 daily addresses, the strongest single-day growth in 14 weeks.

• Bullish social sentiment reached a three-month high, with positive comments outnumbering bearish ones by 3.7 to 1.

• Ripple completed its scheduled 1 billion XRP escrow unlock without a meaningful price shock.

• XRP’s move tracked the broader crypto market closely, with idiosyncratic variance against CD5 staying well below the level that would suggest a major asset-specific catalyst.

Price Action Summary

• XRP rose from $1.0611 to $1.0894 during the 24-hour session, gaining 0.62%.

• The token established higher lows at $1.0552, $1.0589 and $1.0799, showing buyers stepped in at progressively higher levels.

• Volume rose 26.92% above the seven-day average, pointing to steady participation around the move.

• The strongest push came at 13:00 UTC, when volume reached 117.5 million XRP, about 142% above the 24-hour average.

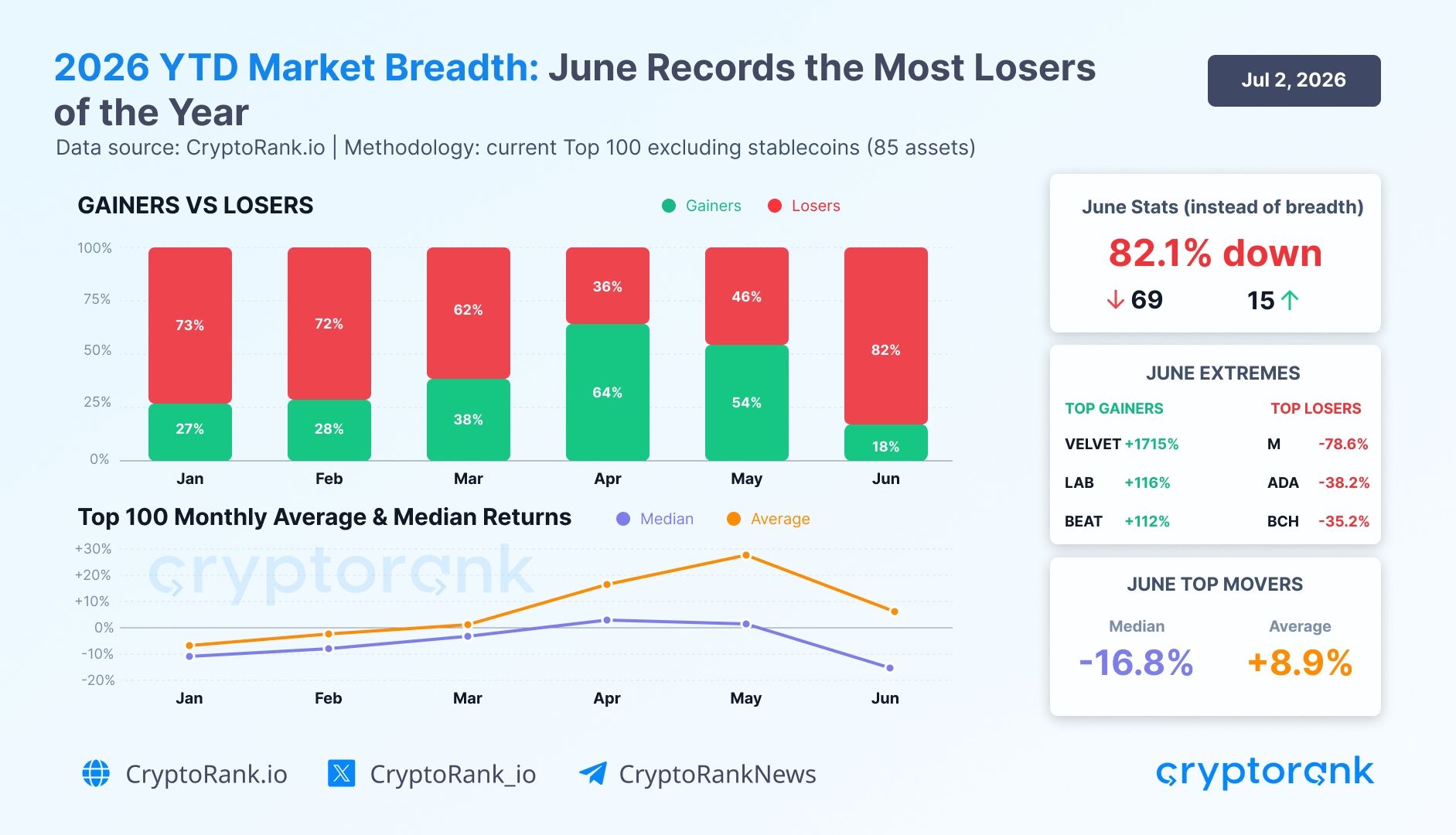

Roughly 82.1% of the top-100 crypto assets declined in June, the worst market breadth of 2026, even as the group’s average return stayed positive.

That split defined the month. A single outlier lifted the average into positive territory while the median return dropped 16.8%, according to a second-quarter recap from CryptoRank.

A Headline Average That Hid the Damage

Across the current top-100 assets excluding stablecoins, CryptoRank recorded a positive average return of 8.9% for June. That figure reflected a single outlier rather than the broader market.

“The market breadth data shows a clear deterioration in participation across the current non-stablecoin Top 100 assets. In June, breadth weakened to its worst level of 2026 so far,” the report read.

Follow us on X to get the latest news as it happens

The report noted that the average was affected by Velvet (VELVET), which surged 1,715% during the month, lifting the aggregate. The 25-point gap between the positive average and the negative 16.8% median showed how few tokens carried the upside.

Besides VELVET, other top gainers included LAB (LAB) at 116% and Audiera (BEAT) at 112%. June also reversed a stronger start to the quarter.

April saw 64% of top-100 assets gain, the best month of 2026. Meanwhile, May showed a more fragile structure, and the June breakdown confirmed the reversal.

Weakness Reached Major Crypto Narratives in June

The decline was not limited to the largest assets. Across all traded tokens with 24-hour volume of more than $1 million, every one of the eight tracked narratives posted a negative median return.

Layer 2 chains led the losses at -24.9%, followed by Decentralized Physical Infrastructure Networks (DePIN) at -24.8% and Layer 1 chains at -22.8%.

“All 8 tracked narratives posted negative median returns, with losers outnumbered gainers in nearly every category, confirming that the market remained defensive and narrow through Q2 without a broad recovery in breadth,” CryptoRank said.

The gainers-versus-losers split showed how narrow the market became. Decentralized Finance (DeFi) recorded 42 gainers against 117 losers, while Artificial Intelligence (AI) posted 21 gainers against 35 losers.

The pattern pointed to a defensive market. Bitcoin (BTC) dominance held near 56% at quarter-end as capital rotated away from weaker altcoins.

Whether June marks a base or another leg lower depends on breadth recovering in the second half.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Crypto’s Positive June Average Masked an 82% Decline Across Top Assets appeared first on BeInCrypto.

Russia’s central bank says the digital ruble is ready for a Sept. 1 rollout, keeping the country’s central bank digital currency plan on schedule.

Summary

- Russia’s Sept. 1 digital ruble rollout moves ahead despite EU sanctions targeting related financial infrastructure.

- Bank rules require major lenders and large retailers to support digital ruble payments in stages.

- U.S. lawmakers are moving toward a temporary CBDC ban while Russia expands state digital money.

Governor Elvira Nabiullina said “everyone is ready” for the launch, according to a July 2 report by RIA Novosti.

The digital ruble will circulate alongside cash and non-cash rubles, not replace them. The Bank of Russia has said people will be able to open digital wallets through banking apps connected to its platform. It has also said individuals will not pay fees on digital ruble transactions.

The rollout begins with banks and large merchants

The Bank of Russia’s timeline requires major banks to offer digital ruble services from Sept. 1, 2026. Large retailers with annual revenue above 120 million rubles must also accept digital ruble payments from that date.

The rules will expand in stages. Banks with universal licenses and retailers with annual revenue above 30 million rubles must join from Sept. 1, 2027. Other banks and smaller retailers will follow from Sept. 1, 2028, while very small merchants will remain exempt.

Sanctions pressure frames the rollout

The launch comes as the European Union has already moved against Russia-linked digital finance. In its 20th sanctions package, the EU Council banned transactions involving RUBx and all EU support for the development of the digital ruble. It linked the measures to Russia’s war against Ukraine and wider concerns over sanctions evasion.

In addition, the EU also proposed broader restrictions on foreign crypto services tied to Russian sanctions evasion. That plan followed growing scrutiny of ruble-linked crypto rails, including platforms and tokens that authorities say may support cross-border payments outside Western controls.

Russia has tested digital ruble use cases for more than a year. As previously reported, the Central Bank of Russia piloted digital ruble smart contracts in Tatarstan, including tests on conditional spending for public funds. The latest timeline shows that Moscow now wants to move the project from testing into broader payment use.

U.S. policy moves in the opposite direction

Russia’s CBDC push contrasts with U.S. policy, where lawmakers have moved toward a temporary ban on a Federal Reserve digital dollar. As crypto.news reported, the 21st Century ROAD to Housing Act would block the Fed from creating a CBDC or similar asset through 2030 if it becomes law.

The U.S. debate reflects concerns over privacy, state control, and the role of private stablecoins. The Russian approach is different. Moscow is building a state-run digital currency while also testing other digital asset rules for trade and financial access under sanctions.

A February report by Jack Jarmon for the Australian Institute of International Affairs said Russia could face limits if it relies on Bitcoin or other proof-of-work assets to bypass sanctions. The report pointed to old power infrastructure and limited access to foreign technology. Those limits may explain why the digital ruble remains central to Moscow’s state-led payment strategy.

The Sept. 1 launch will test whether Russia can drive adoption among banks, merchants, and users. Nabiullina said the central bank wants the digital ruble to be “in demand by people and businesses” and “convenient.”

For now, the rollout places Russia among the countries pushing CBDCs forward while sanctions and U.S. policy debates keep digital state money under close review.

Franklin Templeton Executes Tokenized U.S. Treasury Trade With Stablecoins on Canton Network

7 Perfect Double Features To Watch With ‘Obsession’

The Nintendo/Palworld Patent Suit Appears To Be Heading For A Muted Conclusion

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Staud – Corporette.com

-

Crypto World3 days ago

Crypto World3 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Business7 days ago

Business7 days agoAsia stock markets slide as tech shares slump

-

News Videos4 days ago

News Videos4 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech3 days ago

Tech3 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Crypto World6 days ago

Crypto World6 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business3 days ago

Business3 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World6 days ago

Crypto World6 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports6 days ago

Sports6 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech5 days ago

Tech5 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech6 days ago

Tech6 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World7 days ago

Crypto World7 days agoTether (USDT) Passes Ether in Market Cap as ETH Drops Toward $1.5K

-

Crypto World7 days ago

Hyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World7 days ago

Crypto World7 days agoRTX holders must register wallets before token distribution begins

-

Sports2 days ago

Sports2 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business4 days ago

Business4 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Tech5 days ago

Tech5 days agoClaude Code turned every engineer into three. Now companies need more product thinkers

-

Crypto World7 days ago

Crypto World7 days agoSpaceX Called a Market Top Signal Just 2 Weeks After Its $86 Billion IPO

-

Tech6 days ago

Tech6 days agoSilicon Valley paid to kill AI regulation, now it wants the rules back

-

NewsBeat2 days ago

NewsBeat2 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

You must be logged in to post a comment Login