Crypto World

Iran Reportedly Hits Ships in Strait of Hormuz: Oil Price Jumps Again

Oil prices climbed on Tuesday after Iran reportedly fired at least two missiles at commercial ships crossing the Strait of Hormuz, reviving fears over the world’s key oil chokepoint and the fragile truce between Washington and Tehran.

The rebound landed just days after crude erased its entire war premium and sank closer to pre-war levels.

Oil Rebounds Following Sharp Slide Toward Pre-War Levels

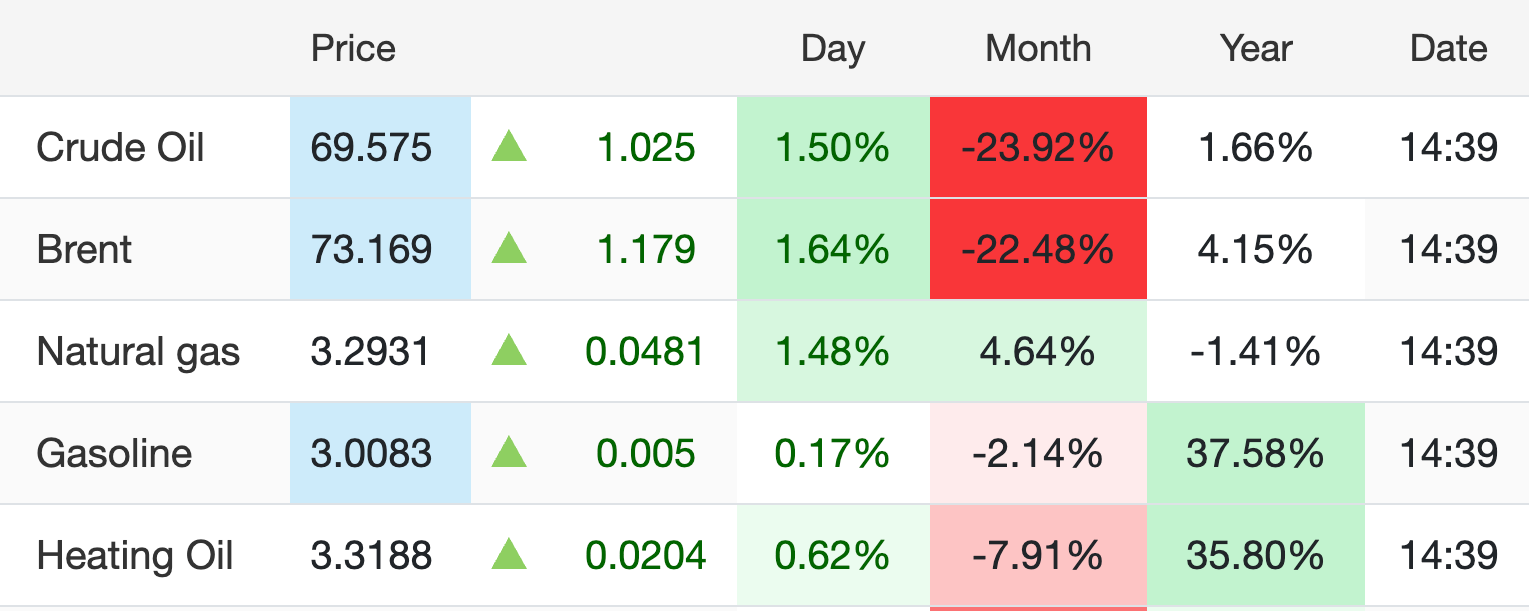

West Texas Intermediate (WTI) crude rose 1.50% to $69.575 on Tuesday. Brent crude gained 1.64% to $73.169.

The wider energy sector also gained. Gasoline rose 0.17%, and heating oil added 0.62%, while natural gas climbed 1.48%.

Follow us on X to get the latest news as it happens

Both oil benchmarks sit far below their wartime highs. Brent has dropped more than 22% over the past month, and WTI has fallen nearly 24% in the same span.

Missile Strikes Test a Fragile US-Iran Truce

The Strait handles roughly 20% of the world’s oil traffic, which magnifies the market reaction to any disruption there. Axios, citing two US officials, reported that Iran fired at least two missiles. The reported strikes came after a one-week agreement between the two sides to halt attacks in the waterway expired.

The United Kingdom Maritime Trade Operations centre reported an incident 8 nautical miles east of Limah, Oman. A southbound tanker was struck by an unknown projectile, causing a fire, according to UKMTO.

A US official said a second commercial vessel was hit by an Iranian missile. Both ships suffered significant damage, though no casualties.

The reported fire threatens a memorandum of understanding barely three weeks after both governments signed it. That deal, reached last month, aimed to end their nearly four-month war. A round of indirect talks in Doha last week closed without meaningful progress.

Meanwhile, the conflict has weighed on President Donald Trump politically. A recent poll found 58% of voters judged the war not worth the cost, while his approval rating held at 36%.

Whether oil extends its bounce or slips back toward pre-war support depends on how Washington responds.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Iran Reportedly Hits Ships in Strait of Hormuz: Oil Price Jumps Again appeared first on BeInCrypto.

Payward, the parent company of crypto exchange Kraken, has won a $22 million arbitration award against former auditor Mazars USA and asked the Delaware Court of Chancery to enter judgment on the award, according to a letter published Tuesday by co-CEO Arjun Sethi.

Payward said Mazars withdrew from the exchange’s nearly completed 2022 audit despite finding no fraud, raising no concerns about management’s integrity and reporting no disagreements with the company.

“An audit is not a favor. It is oxygen,” Sethi wrote, arguing that independent audits are essential for obtaining banking services, licenses and other business relationships.

Sethi said Mazars’ resignation was part of what he described as Operation Chokepoint 2.0, a broader campaign that pressured banks, auditors and other institutions to cut ties with lawful crypto companies.

The letter cited a series of regulatory developments from 2023 as evidence supporting that claim. These included joint guidance from US banking regulators, the Securities and Exchange Commission’s since-rescinded Staff Accounting Bulletin No. 121 and the collapse of crypto-focused banking networks Silvergate SEN and Signature’s Signet.

Sethi also called on Congress to pass the CLARITY Act, arguing that a comprehensive market structure framework would provide clearer rules for digital asset companies and reduce reliance on regulatory enforcement.

Related: Kraken lets traders use tokenized stocks as collateral for leveraged trades

Kraken executives reflect on auditor dispute

Kraken co-CEO Dave Ripley said on X Tuesday that “this story is worth surfacing despite its PTSD-inducing nature,” adding that “only a fraction of the stories from that era have ever been told.”

Ripley described the $22 million arbitration award as compensation for financial harm caused by what he called a coordinated campaign against the crypto industry.

Meanwhile, US regulators continue to address concerns around crypto-related debanking. In February, the Federal Reserve sought public feedback on a proposal to formally remove “reputation risk” from bank supervision, following its 2025 directive to stop pressuring banks to close customer accounts over reputational concerns. Critics said the move could help bring an end to Operation Chokepoint 2.0.

Source: Dave Ripley

Kraken was founded in 2011 and has been widely expected to pursue an initial public offering. In November 2025, the company said it had confidentially submitted a draft Form S-1 registration statement to the US Securities and Exchange Commission.

However, it was reported in May that its public debut may not come until 2027, citing weaker crypto market conditions and the exchange’s ongoing cost-cutting efforts.

Magazine: China’s 107 Bitcoin memory thief, Bithumb CEO booked: Asia Express

MemeCore has surged more than 150% over the past week after recovering from a sharp selloff that erased more than 80% of its value in late June, with renewed buying driven by security updates and improving market sentiment.

Summary

- MemeCore has jumped more than 150% in a week after developers addressed security concerns following its June crash.

- A short squeeze and improving technical momentum helped push the token from $0.51 to a weekly high of $1.79.

- Traders are now watching whether ecosystem growth and on-chain activity can sustain the recovery above key resistance.

According to the MemeCore team, the rebound followed a series of public clarifications addressing concerns that emerged after the token’s steep decline. The developers said the network had become the target of a coordinated campaign involving phishing websites and a fake project using the MemeCore name on another blockchain.

They also warned users about fraudulent airdrop pages impersonating official channels, drawing a distinction between the Layer-1 network and malicious copycat platforms.

Security updates helped restore confidence

Those statements came after MemeCore plunged to about $0.51 in late June from levels above $2.80, wiping out billions in market value within days. The collapse fueled speculation over insider activity and market manipulation, leaving traders reluctant to re-enter positions while uncertainty dominated sentiment.

As the development team responded to those concerns, buyers gradually returned. The recovery accelerated as traders viewed the clarification campaign as a sign that the project was actively addressing security risks rather than remaining silent during the crisis.

The rebound also gathered momentum in derivatives markets. After the violent selloff left the token deeply oversold, bearish traders were caught off guard when prices began climbing.

As MemeCore broke above resistance around $0.80 before clearing the $1.20 region, short sellers were forced to buy back positions, adding fuel to the rally. The token eventually reached a weekly high near $1.79 before easing into consolidation around $1.48.

Although early dip buyers locked in profits near the local top, selling pressure faded quickly enough for buyers to defend higher price levels. Instead of revisiting the June lows, MemeCore has so far maintained a sequence of higher lows, suggesting demand has remained active after the initial recovery.

Technical indicators point to stabilizing momentum

The 4-hour chart shows that the recovery has entered a consolidation phase rather than another sharp reversal. MemeCore is trading around $1.48 after holding above the $1.35-$1.40 support area, while immediate resistance remains near $1.60, followed by the recent swing high around $1.80.

Momentum indicators have also improved. On the 4-hour timeframe, the relative strength index has climbed to about 58, placing it above the neutral 50 level without entering overbought territory.

Meanwhile, the MACD histogram has turned positive, with the indicator approaching a bullish crossover, suggesting downside momentum has weakened following several days of sideways trading.

Even after the recent recovery, MemeCore remains well below its all-time high of $4.84, illustrating how much ground the token lost during June’s collapse. The rapid swing from a market capitalization below $700 million to roughly $1.9 billion within days also underscores how quickly liquidity and investor sentiment can change in smaller crypto assets.

Looking ahead, the next stage of the recovery will depend on activity beyond price action. Market participants are likely to watch whether MemeCore can expand on-chain usage, attract sustained capital inflows, and grow its ecosystem of decentralized applications.

Without continued network growth, the recent gains could face renewed pressure if crypto market volatility increases, while a decisive move above the $1.80 region would strengthen the case for another leg higher toward the $2.20 area.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Blockchains cannot talk to each other on their own. Bridges are the software that moves value between them, and they have leaked more money to hackers than any other kind of crypto infrastructure, billions across a handful of catastrophic breaches. Here is how bridges actually work, the different trust models behind them, and why the connective tissue of crypto is also its most dangerous single point of failure.

Summary

- Cross chain bridges move assets and data between separate blockchains by locking, burning, or swapping tokens through different trust models.

- The security of a bridge depends largely on how it verifies transactions, with cryptographic models offering stronger protection than signer based systems.

- Bridges remain one of crypto’s biggest security risks because they hold large pools of assets and rely on complex infrastructure that has repeatedly been targeted by hackers.

There are hundreds of blockchains, and by design none of them can see the others. Ethereum has no native way to know what happened on Solana; a Bitcoin holder cannot directly spend that Bitcoin inside an Ethereum application. Each chain is an island with its own ledger, its own validators, and no built-in bridge to the mainland.

Yet users constantly need to move value between these islands, to chase yield, access an application, or reach cheaper fees, and that need created an entire category of infrastructure: the cross-chain bridge.

A bridge is software that lets assets and information move between blockchains that otherwise cannot communicate. It is essential plumbing; without bridges, liquidity would be trapped on whichever chain it started on, and the multi-chain world that defines crypto today could not function. Bridges now move billions of dollars a week, and their total value locked runs into the tens of billions.

They are also the single most dangerous piece of infrastructure in crypto. Bridge exploits have produced some of the largest thefts the industry has ever recorded, with individual breaches running into the hundreds of millions and the category’s cumulative losses in the billions. The same design that makes a bridge useful, holding or controlling large pools of assets across chains, makes it a concentrated target, and a small flaw in a bridge can drain a fortune in minutes.

This guide explains how bridges work, the main architectures they use, the trust models that determine how safe each one is, why they keep getting hacked, and how to think about bridge risk before moving your own funds.

Why bridges are necessary

The root problem is isolation. A blockchain is a self-contained ledger whose validators agree only on the state of their own chain. Nothing in Ethereum’s protocol can natively verify that a transaction happened on another chain, because doing so would require Ethereum’s validators to also run and trust every other chain, which they do not. Each network is sovereign and blind to the others.

Before bridges, the only way to move value between chains was through a centralized exchange: send your asset to the exchange on one chain, trade it, and withdraw a different asset on another chain. This works but reintroduces exactly the centralized intermediary that crypto was meant to reduce, along with accounts, custody, and withdrawal limits. Bridges emerged to do the same job more directly, letting value move between chains without handing it to an exchange in the middle.

The demand is enormous because the ecosystem is fragmented by design. Different chains optimize for different things, and users want to combine them: hold an asset native to one chain but use it in an application on another, move to a network with cheaper fees, or supply liquidity where the returns are highest. The connective role bridges play is why the industry sometimes calls them the tissue linking the chains, and it is why bridge volume tracks the overall growth of multi-chain activity. As newer designs push more of that activity toward stablecoin settlement and payments, the demand to move dollar-denominated value across chains has only intensified, echoing the broader rise of payment-focused chains built around moving stable value efficiently.

The catch is that connecting sovereign, mutually blind systems is genuinely hard, and every method of doing it introduces a trust assumption somewhere. That assumption is where the money leaks.

How a bridge moves an asset

Most bridges rely on a simple-sounding trick: they do not actually send an asset from one chain to another, because that is impossible. Instead, they lock or destroy the asset on the source chain and create a corresponding asset on the destination chain.

Three main architectures implement this idea.

The lock-and-mint model is the most common. When you bridge an asset, the bridge locks your original tokens in a smart contract on the source chain, like putting them in a vault, and mints an equivalent wrapped token on the destination chain. That wrapped token is a claim on the locked original, redeemable by reversing the process: burn the wrapped token on the destination chain, and the bridge unlocks the original on the source chain. The locked assets sit in the bridge’s custody the entire time, which is precisely why lock-and-mint bridges have been the most exploited: the vault holding everyone’s locked assets is a single, enormous target.

The burn-and-mint model is used mainly for assets whose issuer controls supply across chains, such as certain stablecoins. Instead of locking the asset, the bridge permanently burns it on the source chain, removing it from that chain’s supply, and mints a fresh, native version on the destination chain. Because the destination asset is truly native, not a wrapped claim, this avoids the pool-of-locked-assets problem, but it only works when a single issuer has authority to burn and mint the asset on every chain, which is why it is common for stablecoins and rare for everything else.

The liquidity-pool model takes a different approach. The bridge maintains pools of assets on every supported chain, and when you bridge, you deposit into the pool on the source chain and withdraw the equivalent from the pool on the destination chain, often with a solver or market maker fronting the destination asset instantly and settling later. Nothing is wrapped; you simply swap into inventory that already exists on the other side. This can be faster and avoids wrapped-token risk, but it requires the bridge to keep large inventories on every chain, which is both capital-intensive and, again, a target.

Beyond moving assets, modern bridges also pass messages: arbitrary data and instructions that let a smart contract on one chain trigger an action on another. A token transfer is just the simplest message, saying an amount was locked here, so mint it there. More elaborate messages let an application on one chain react to events on another, which powers cross-chain lending, governance, and complex applications. This general message passing is powerful and expands what bridges can do far beyond simple transfers, but every added capability is added surface area for something to go wrong.

The trust models that decide safety

The crucial question for any bridge is who verifies that the source-chain event actually happened before the destination chain acts on it. The answer is the bridge’s trust model, and it is the single biggest determinant of how safe the bridge is. There is a well-known framework classifying these models, and it maps cleanly onto a spectrum from convenient-but-risky to trustless-but-costly.

The trusted model relies on a fixed set of external validators, often secured by a multisignature or multiparty scheme, who watch the source chain and sign off on events for the destination chain. This is fast, cheap, and simple, but the validator set is the trust assumption: if enough of their signing keys are compromised, the attacker controls the bridge. Many of the largest bridge hacks in history were failures of exactly this model, where an attacker gained control of enough validator keys to authorize fraudulent withdrawals. When a bridge’s security rests on a handful of keys, those keys are the whole game.

The light-client or validity-proof model is the trustless end of the spectrum. Here the destination chain actually runs a light client of the source chain and cryptographically verifies its block headers, or accepts a validity proof, instead of trusting a set of signers. This is far more secure because it removes the human validator set and replaces it with mathematics, but it is expensive in computation and complex to build, and it does not work efficiently for every pair of chains. Advances in zero-knowledge proofs, the same cryptography moving to the center of Ethereum’s long-term rebuild, are extending this model to more chains, but it remains harder to deploy than trusting a signer set.

Between the extremes sit optimistic and hybrid models, which assume transactions are valid but allow a challenge window during which watchers can submit proof of fraud, similar to how some scaling systems secure their withdrawals. These trade some speed, through the challenge delay, for stronger security than a pure trusted model, without the full cost of a light client. Where a bridge sits on this spectrum tells you almost everything about its risk: the more it relies on a small trusted group and the less it relies on cryptographic verification, the more it depends on those few parties never being compromised.

Why bridges keep getting hacked

Bridges have lost more to hackers than any other category of crypto infrastructure, and the reasons are structural, not accidental. Understanding them explains why the problem persists despite years of painful lessons.

The first reason is concentration of value. A bridge, especially a lock-and-mint one, accumulates a large pool of locked assets backing all the wrapped tokens it has issued. That pool is a single honeypot, and unlike a diffuse set of user wallets, draining it once takes everything. Attackers are economically rational, and they gravitate to wherever the most value sits behind the fewest defenses, which describes a large bridge almost perfectly.

The second reason is weak trust models. Many bridges chose the fast, cheap, trusted model, securing hundreds of millions of dollars behind a small set of signing keys. The largest bridge thefts on record were, at their core, key compromises: an attacker obtained control of enough of the bridge’s validator keys, through phishing, malware, or infrastructure breaches, and then simply authorized withdrawals that the bridge treated as legitimate. No clever exploit of the blockchain was needed, only control of the keys the bridge trusted. A bridge secured by nine keys where five are enough to move funds is, in security terms, a five-key vault.

The third reason is complexity. Bridges are among the most complex smart-contract systems in crypto, spanning multiple chains, custom message formats, and intricate verification logic, and complexity is the enemy of security. Every added feature, every new supported chain, every message type is more code that can contain a subtle flaw, and bridge exploits have repeatedly come from bugs in verification logic that let an attacker forge a proof of a deposit that never happened, causing the bridge to release funds against nothing. The fraud-proof and verification systems that are supposed to guard a bridge are themselves complex code, and a flaw there is catastrophic because it undermines the entire security model at once. The category’s history rhymes with the broader lesson that concentrated infrastructure fails hard, the same dynamic seen when any single point of control becomes the weakest link in an otherwise sound system.

These three forces combine into a grim equation: bridges hold enormous value, often behind trust models thinner than the value warrants, inside code complex enough to hide fatal bugs. That is why, even as the industry has learned hard lessons and newer designs have improved, bridges remain the place where the largest single thefts tend to happen.

The anatomy of a bridge hack

To make the risk concrete, it helps to walk through how a typical bridge exploit actually unfolds, because the pattern repeats across nearly every major incident and reveals why the losses are so total.

Most catastrophic bridge hacks fall into one of two shapes. The first is a key compromise. A trusted-model bridge secures its locked assets behind a set of signing keys, and an attacker obtains control of enough of those keys, through phishing an employee, compromising a server, or exploiting weak key management, to reach the signing threshold. Once the attacker can produce valid signatures, the bridge has no way to distinguish their fraudulent withdrawal from a legitimate one, because a validly signed instruction is exactly what the bridge is built to obey. The attacker signs a withdrawal that drains the locked pool, and the assets are gone before anyone notices, because from the bridge’s perspective nothing broke; the correct keys authorized the transfer. Several of the largest bridge thefts in history were precisely this: not a clever exploit of the blockchain, but a theft of the keys the bridge trusted, turning the bridge’s own security model into the attacker’s tool.

The second shape is a verification bug. A bridge must verify that a deposit really happened on the source chain before releasing funds on the destination chain, and this verification logic is complex code. If it contains a flaw, an attacker can craft a fake proof of a deposit that never occurred, submit it to the bridge, and the bridge, believing the fake, releases real assets against nothing. The attacker deposited nothing and withdrew a fortune, because the code that was supposed to check the deposit accepted a forgery. These bugs are catastrophic precisely because they attack the bridge’s core trust mechanism: once an attacker can forge the proof the bridge relies on, they can mint or withdraw arbitrary value until someone halts the bridge, which in a fast-moving exploit can be far too late.

Both shapes share a defining feature that explains why recovery is so rare: the theft looks legitimate to the bridge at the moment it happens. A key-compromise withdrawal carries valid signatures; a verification-bug withdrawal carries an accepted proof. Neither trips an alarm inside the system, because both exploit the system doing exactly what it was designed to do, only on fraudulent inputs. By the time the discrepancy surfaces, usually when the locked assets no longer back the wrapped tokens in circulation, the funds have moved through mixers and across other chains. The wrapped tokens left behind become claims on an empty vault, and their holders, who did nothing wrong, absorb the loss. This is the mechanism by which a single flaw in one bridge translates into hundreds of millions gone, and why the security of a bridge deserves more scrutiny than almost any other decision in a multi-chain transaction.

How to think about bridge risk

Bridges are necessary and, used carefully, reasonable to rely on, but their risk profile deserves respect. A few principles help you evaluate any bridge before trusting it with funds.

Prefer stronger trust models. A bridge secured by cryptographic verification, a light client or validity proofs, or by a canonical connection to a base chain, is structurally safer than one secured by a small external signer set. Where a bridge documents its trust model, read it; the difference between trusting mathematics and trusting a handful of keys is the difference between the safest and riskiest bridges in existence. Independent frameworks that score bridges on their trust assumptions exist precisely because this distinction is hard for users to assess alone.

Favor track record and audits. A bridge with a long operational history free of exploits, multiple independent security audits, an active bug bounty, and transparent, time-locked upgrade processes has earned more trust than a new, unaudited one, however attractive its yields. Bridges are not where to chase the newest, highest-return option, because the downside of a bridge failure is total loss of the funds in transit.

Minimize time and size at risk. Bridging is riskiest while your value sits in the bridge’s custody or in transit. Moving smaller amounts, avoiding leaving large balances in wrapped tokens longer than necessary, and using aggregators that route through the safest available path all reduce exposure, while minding the slippage a large cross-chain swap can incur along the way. For very large transfers, splitting them or accepting the slower safety of a canonical bridge can be worth the inconvenience.

Understand what you are holding after you bridge. A wrapped token is a claim on assets locked in a bridge, and it is only as sound as that bridge. If the bridge is exploited and its locked assets drained, the wrapped tokens it issued can become worthless claims on an empty vault, even though your original assets are gone. Native assets obtained through burn-and-mint or liquidity-pool models avoid this specific risk, which is one reason those models are often preferred where available, particularly for the stablecoins that dominate cross-chain settlement.

The honest summary is that bridges are indispensable and imperfect. They solve a real and unavoidable problem, connecting sovereign chains that cannot see each other, and there is no way to do that without introducing a trust assumption somewhere. The safest bridges push that assumption toward cryptography and away from small groups of keys; the most dangerous do the reverse and guard enormous value with thin trust. Knowing which kind you are using, and treating the crossing as the riskiest moment in any multi-chain transaction, is what separates informed use from the kind of blind trust that has, again and again, funded the largest heists in the industry.

It is worth ending on where the technology is heading, because the picture is not static. The industry has absorbed the lessons of its worst bridge failures, and newer designs increasingly favor stronger trust models: burn-and-mint transfers for assets whose issuers can support them, cryptographic light clients and validity proofs where the chain pairs allow, and intent-based systems where independent parties front liquidity and take on the risk rather than pooling everyone’s assets in a single honeypot. Independent risk frameworks now score bridges on exactly the trust assumptions that used to be invisible to ordinary users, making it easier to tell a well-secured bridge from a dangerous one before committing funds. None of this eliminates the fundamental tension that connecting blind, sovereign systems requires trusting something, but it does shift the trust toward mathematics and away from the small key-holding groups that account for the largest historical losses. The bridges of the next few years will be safer than those that leaked billions, not because the problem got easier, but because the industry paid for the lesson in full and is finally building as though it remembers.

Frequently asked questions

What is a cross-chain bridge?

A cross-chain bridge is software that lets assets and data move between different blockchains, which otherwise cannot communicate with each other. It typically works by locking or burning an asset on the source chain and creating an equivalent asset on the destination chain, allowing value to move across networks without going through a centralized exchange.

How does a bridge move an asset between chains?

It does not literally send the asset across; instead it uses one of three models. Lock-and-mint locks the original in a contract and mints a wrapped version on the other chain. Burn-and-mint destroys the asset on one chain and creates a native version on the other. Liquidity-pool bridges keep inventories on both chains and let you swap into the destination pool. Each avoids the impossible task of directly transferring an asset between separate ledgers.

Why are bridges hacked so often?

Three structural reasons: they concentrate large pools of value that make single, lucrative targets; many use weak trust models secured by a small set of signing keys that, if compromised, hand an attacker control; and they are highly complex code where subtle verification bugs can let attackers forge deposits. Together these make bridges the category responsible for some of the largest thefts in crypto history.

What is the safest kind of bridge?

Bridges that verify source-chain events cryptographically, through a light client or validity proofs, or that use a canonical connection to a base chain, are structurally safest because they rely on mathematics rather than a trusted group. Bridges secured only by a small external set of signing keys are the riskiest, since compromising those keys compromises the entire bridge.

What is a wrapped token?

A wrapped token is a token minted on a destination chain to represent an asset locked in a bridge on the source chain. It is a claim on the locked original, redeemable by burning the wrapped token to unlock the original. Its value depends entirely on the bridge holding the locked assets; if that bridge is drained, the wrapped token can become a worthless claim on an empty vault.

Are bridge hacks the biggest in crypto?

Some of the largest single thefts in crypto history have been bridge exploits, with individual breaches reaching hundreds of millions of dollars and the category’s cumulative losses running into the billions. Many of these were key compromises of trusted-model bridges rather than exploits of the underlying blockchains, meaning the attacker gained control of the keys the bridge trusted.

Can I lose money using a bridge?

Yes. The main risk is that the bridge is exploited while your value is locked in it or held as a wrapped token, in which case those funds can be lost entirely. Additional risks include smart-contract bugs and, for liquidity-pool bridges, issues with the pools. Using well-audited bridges with strong trust models and long track records, and minimizing the amount and time at risk, reduces but does not eliminate this.

What is general message passing in bridges?

General message passing is the ability of a bridge to move arbitrary data and instructions between chains, not just token transfers. It lets a smart contract on one chain trigger an action on another, powering cross-chain lending, governance, and complex applications. A token transfer is the simplest message, but the added capability also expands the code surface where vulnerabilities can appear.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 7, 2026.

Vanguard has posted a new role aimed squarely at digital-asset strategy, appointing a “head of digital assets” to shape how the asset manager approaches tokenization, stablecoins, blockchain infrastructure, and client-facing crypto-related products. The hiring signal suggests a shift from Vanguard’s historically cautious stance toward direct crypto investment offerings.

In the job description, Vanguard says the person in the role will be responsible for determining how the firm participates in digital assets—covering everything from product evaluation and tokenization initiatives to custody models, blockchain settlement considerations, and the “digital asset operating infrastructure” needed to support such efforts. The role is also expected to represent Vanguard in discussions with regulators, clients, and industry groups.

Key takeaways

- Vanguard is hiring a “head of digital assets,” with explicit responsibilities across tokenization, stablecoins, custody, and blockchain-based settlement.

- The position includes a regulatory-facing component, indicating the effort is not limited to product experimentation.

- Vanguard’s hiring marks a notable contrast with prior statements rejecting certain crypto investment products, including crypto ETFs.

- Tokenized real-world asset (RWA) growth—and tokenized Treasuries in particular—continues to pull major asset managers deeper into the sector.

A broader digital-asset mandate than simple product testing

The posting lays out a comprehensive remit that goes beyond whether Vanguard will offer a specific token or investment product. According to the role description published on Vanguard’s jobs site, the new executive will evaluate “client-facing products” and consider how Vanguard might engage through multiple layers of the digital-asset stack—tokenization, stablecoins, custody model design, settlement workflows, and operational infrastructure.

That breadth matters for investors and counterparties because it implies Vanguard is working toward a sustained capability rather than a short-lived pilot. When firms focus only on distribution, they can remain reactive. By contrast, a mandate that includes custody and settlement suggests Vanguard may be aligning internal processes with how digital assets are issued, secured, and moved—an important prerequisite for scaling any future offerings.

The job also indicates that the role will serve as a bridge between the business side and external stakeholders, with responsibility for Vanguard’s participation in regulator, client, and industry discussions. That kind of engagement is often overlooked in public narratives around crypto adoption, but it typically determines whether products can move from concept to compliance-ready execution.

From resistance to reconsideration

Vanguard’s move is particularly striking given its earlier public posture toward crypto. In August 2024, then-CEO Salim Ramji said Vanguard would not launch crypto exchange-traded funds, arguing the firm would not “copy competitors” despite the rapid adoption of spot Bitcoin ETFs across the market.

More recently, ETF analyst Nate Geraci pointed out the practical contradiction: Vanguard had previously blocked customers from purchasing spot Bitcoin and Ether ETFs through its brokerage platform. Geraci highlighted the shift in an X post on Tuesday, adding “Life moves pretty fast,” underscoring how quickly the firm’s posture appears to be evolving.

Neither the hiring description nor the article’s details clarify whether Vanguard will immediately launch any particular crypto product. However, the existence of a role spanning tokenization, stablecoins, custody, and settlement suggests the company is now building decision-making capacity that could support new offerings—potentially including products investors could access in the future.

Why tokenization is pulling asset managers in

Vanguard’s hiring arrives as major asset managers expand their involvement in tokenized finance. Data compiled by RWA.xyz indicates the tokenized real-world asset market has grown to $33.5 billion. Within that figure, tokenized U.S. Treasury products account for $14.9 billion—an area that has drawn particular attention because it connects tokenized exposure to government debt instruments.

RWA.xyz data also points to the scale of major players in tokenized Treasuries: Franklin Templeton manages about $2.5 billion in tokenized assets, BlackRock oversees roughly $2.3 billion, and WisdomTree’s tokenized Treasury fund has grown to more than $700 million.

These figures help explain why tokenization is becoming a strategic priority rather than a niche experiment. Tokenized Treasury products are frequently positioned as an entry point for institutions that want blockchain settlement benefits—such as faster movement of value or improved interoperability—while maintaining exposure linked to established benchmarks.

Competition accelerates across tokenized cash, liquidity, and ETFs

The broader industry context includes multiple initiatives from large financial firms aiming to integrate tokenization and digital settlement. In March, Franklin Templeton partnered with Ondo Finance to offer tokenized versions of its ETFs accessible through crypto wallets, according to coverage referenced in the source material. Later, Franklin Templeton launched a dedicated cryptocurrency investment division after its acquisition of crypto asset manager 250 Digital.

Other large institutions have pursued tokenized cash and liquidity products as well. JPMorgan filed in May to launch a tokenized money market fund for stablecoin issuers. State Street introduced a government money market fund for stablecoin reserves and a tokenized liquidity product the following month.

Fidelity also moved into blockchain-based liquidity. The source material notes that Fidelity launched a blockchain-based liquidity fund in May, and that it received its first crypto-native investment after Theo allocated $20 million to the product.

Taken together, these developments highlight a sector pattern: many incumbents appear to be approaching crypto-related infrastructure through tokenized cash, liquidity, and Treasury instruments first—areas where regulators and compliance teams may find more familiar analogues than, say, direct exposure to volatile crypto assets.

For Vanguard, the job description’s emphasis on custody models, settlement mechanisms, and operating infrastructure aligns with this market direction. If tokenized cash and Treasury products keep growing, the firms that can support secure issuance, operational workflow, and compliance will likely be best positioned to expand product ranges over time.

Investors and industry watchers should monitor whether Vanguard’s digital-asset hiring translates into concrete offerings—particularly around tokenization and custody—or whether the early phase remains focused on internal buildout and regulatory engagement. The key open question is what form Vanguard’s participation will take next, and how quickly the firm moves from strategy to investor-accessible products.

The U.S. Securities and Exchange Commission has put forward proposed rule changes aimed at tightening how crypto assets are handled under existing securities and market-structure rules, with SEC Chair Paul Atkins saying the effort is meant to reduce uncertainty for the industry.

In a Tuesday notice announcing the agency’s 2026 regulatory agenda, Atkins described the proposals as aligning with the Trump administration’s stated crypto policy priorities—particularly around tokenized securities and fundraising through digital assets.

Key takeaways

- The SEC’s 2026 agenda includes three proposed rule areas touching crypto broker-dealers, trading venues, and possible exemptions or safe harbors.

- SEC Chair Paul Atkins said the proposals are designed to clarify the regulatory framework and give investors more consistent information for decision-making.

- The SEC’s move comes as Congress debates a crypto market structure bill that could shift oversight and enforcement toward the CFTC.

- Criticism from Democratic lawmakers centers on the SEC’s prior enforcement approach and Atkins’ statements about which tokens are securities.

- Separately, President Donald Trump told reporters he became involved with crypto “a little bit for politics,” reflecting the administration’s broader political posture toward the sector.

What the SEC says it wants to clarify in 2026

According to a statement from SEC Chair Paul Atkins in the 2026 regulatory agenda announcement, the agency intends to “help clarify the regulatory framework for crypto assets and provide greater certainty to the market.” Atkins framed the agenda as a way to match the administration’s crypto goals, including how tokenized securities should be treated and how digital-asset fundraising could work within existing law.

The notice describes three proposed rule changes aimed at specific parts of the crypto ecosystem:

- Rules addressing crypto broker-dealers.

- Rules concerning digital assets traded on alternative trading systems and national securities exchanges.

- Potential exemptions and safe harbors for digital assets under certain circumstances.

On one of the agenda items related to the “offer and sale of crypto assets,” the SEC said the proposals may provide greater certainty, facilitate capital formation, accommodate innovation, and—at the same time—ensure investors receive adequate protections and the information needed to make informed investment decisions. The SEC’s description appears in the agenda documentation hosted by the federal rulemaking portal (reginfo.gov).

Congressional debate could move enforcement power

The SEC’s proposed agenda arrives amid an active legislative backdrop. The notice and related coverage come as U.S. lawmakers debate provisions in a crypto market structure bill that—if passed—could significantly alter where oversight and enforcement sit. Earlier reporting from Cointelegraph noted that certain provisions are expected to shift much of the industry’s oversight and enforcement from the SEC to the Commodity Futures Trading Commission (CFTC). Cointelegraph’s coverage referenced this potential move in the context of broader market structure reform.

In March, Atkins also indicated the SEC would pursue an internal “bridge” approach to clarify crypto regulation, while signaling he might defer to legislation if Congress acts. Earlier Cointelegraph reporting described this as the SEC trying to provide more guidance without waiting for the full legislative outcome. That earlier Cointelegraph piece detailed Atkins’ comments on the SEC’s willingness to clarify through its own process.

For market participants, the timing matters: the SEC’s 2026 proposals could shape compliance expectations even if Congress eventually changes the agency landscape. Traders and platforms may need to plan for overlapping standards—especially where rules implicate broker-dealer responsibilities, trading venue obligations, and how exemptions or safe harbors might apply.

Political pressure and renewed criticism from lawmakers

The SEC’s agenda also faces political scrutiny. Critics within the Democratic Party have accused the administration of enabling a “pay-to-play scheme,” according to a letter referenced in the report, which alleges individuals associated with the administration financially benefited from companies that were previously entangled with enforcement actions or regulatory concerns. The companies cited in the letter include Binance, Coinbase, Ripple Labs, and Kraken.

In the same line of criticism, three Democratic House members argued that the SEC’s decision to let certain parties “go without consequences,” combined with Atkins’ public remarks that “most crypto tokens are not securities,” has created what they described as a regulatory vacuum—one that they say leaves securities violations insufficiently enforced and investors insufficiently protected.

The referenced letter is dated January and addressed to Atkins, according to a document made available by the House Financial Services Committee’s Democrats. (House Democrats letter PDF)

While the SEC’s agenda is presented as an effort to increase regulatory clarity, lawmakers’ criticism underscores the fundamental tension: whether “clarification” will lead to tighter accountability for issuers and intermediaries—or whether the SEC’s framework will continue to be perceived as uneven in how it applies securities laws to crypto assets.

Trump’s comments highlight the administration’s shifting posture

Separately from the SEC’s rule agenda, President Donald Trump commented on his evolving relationship with crypto. In response to questions from reporters on Monday, Trump said he became involved with crypto “a little bit for politics,” according to coverage cited in the report. He had previously called Bitcoin a “scam” after the start of his first term, but later engaged more publicly with industry figures and promoted the technology ahead of the 2024 election.

That shift in political stance does not directly determine how SEC rules are drafted, but it helps explain why the agency’s 2026 agenda is being framed as consistent with the administration’s broader crypto objectives—particularly around capital formation and tokenized asset activity.

Looking ahead, market participants should watch how the SEC translates these agenda items into actual proposed rule text and whether the proposals’ scope overlaps with—rather than is superseded by—any congressional market-structure changes that could redirect oversight toward the CFTC.

The New Hampshire Secretary of State’s office announced that lawmakers would discuss issuing $100 million in bonds backed by Bitcoin (BTC) at a public hearing.

In an update to the New Hampshire governor and executive council agenda, the state’s Business Finance Authority (BFA) has scheduled a meeting for Wednesday regarding the proposed issuance of $100 million in BTC-backed bonds. The BFA approved the bond in November 2025, saying that it planned to issue the vehicles upon approval from Governor Kelly Ayotte and the state’s five-member executive council.

“This is an innovative way to bring more investment opportunities to our state and position us as a leader in digital finance without risking state funds or taxpayer dollars,” said Ayotte on the bonds, following the BFA approval.

The potential high-value Bitcoin-backed bonds signaled the US state’s move toward friendlier digital asset policies. New Hampshire was the first state to approve a law establishing a strategic Bitcoin reserve in May 2025, allowing the government to invest 5% of public funds in digital assets with a market capitalization exceeding $500 billion.

New Hampshire governor signing the May 2025 crypto reserve bill into law. Source: Kelly Ayotte

Related: Bank of Korea governor outlines tokenized bond vision, unified ledger plan

Unlike traditional municipal bonds, a BTC-backed bond could be an innovative financial instrument, but one that potentially introduces “substantial risk,” according to David Krause, an emeritus associate professor of finance at Marquette University. Krause authored an analysis of the proposed bond in April, saying that while a private borrower, CleanSpark, was putting up the funds for collateral, this approach offered “no recourse to state funds or taxpayers.”

“While the bond may serve as a proof of concept for integrating digital assets into structured finance, it is not well suited as a general-purpose public finance tool,” said the professor. “Its primary significance lies in highlighting the challenges of adapting traditional financial frameworks to highly volatile digital assets.”

In March, Moody’s assigned the Bitcoin bond a provisional Ba2 rating, falling under the company’s “speculative grade” category for vehicles with substantial credit risk.

El Salvador’s Bitcoin-backed bond project fizzled out

Although New Hampshire may become one of the first US states to issue Bitcoin-backed bonds, the idea previously gained traction in El Salvador.

Under President Nayib Bukele, who also pushed for a law that later established Bitcoin as legal tender in the country, El Salvador’s government announced $1 billion in Bitcoin-backed “Volcano Bonds” to fund a proposed Bitcoin City project. Proposed in 2022, the idea never came to fruition following a crypto market downturn.

Magazine: Guide to the top and emerging global crypto hubs: Mid-2026

Ether has bounced back sharply, rising roughly 15% over the past five days and pulling away from the $1,500 area that marked a June 26 low. The recovery reflects a mix of renewed confidence around Ethereum’s roadmap and ongoing accumulation of ETH by BitMine Immersion Technologies.

Beyond price, Ethereum’s narrative is also shifting toward practical use cases: the Glamsterdam upgrade is still progressing through testing toward later in 2026, while the July 2 launch of Robinhood Chain has put additional attention on regulated, tokenized finance built on top of the Ethereum ecosystem.

Key takeaways

- Ether’s rebound followed the June 26 low, helped by optimism tied to final testing for Ethereum’s Glamsterdam upgrade.

- BitMine Immersion Technologies’ continued ETH buying is cited as a key factor supporting the $1,500 level, despite large unrealized losses.

- Ethereum options markets have cooled from fear conditions, with Deribit skew moving away from last week’s extremes.

- Robinhood Chain’s rollout and tokenized stock expansion reinforce a TradFi-focused growth angle for Ethereum-based infrastructure.

Ether strength, with support under $1,500

In the latest stretch of strength, Ether’s performance has outpaced the broader crypto complex. The article notes that ETH has gained about 7% relative to total crypto market capitalization over the last 30 days, suggesting demand for Ether specifically rather than a purely market-wide risk-on move.

Part of the backdrop is political and regulatory momentum. The piece points to optimism surrounding the proposed Digital Assets CLARITY Act, which has faced delays in Congress due to banking-sector pushback, particularly around stablecoin regulation and potential rewards for token holders. Even without immediate clarity, investor expectations can still influence short-term positioning in major assets like ETH.

Derivatives: fear metrics ease, but bullishness is not yet dominant

Ether’s rally toward $1,800 also coincided with improvement in ETH options positioning. According to the article, Deribit’s 25% delta skew (put-call) — a common measure used to infer the balance between protective puts and upside calls — moved out of the fear zone that persisted until Friday.

The current skew is described as showing a 9% premium for put options over equivalent call options. That is still not “bullish” in the strictest sense, but it is meaningfully less extreme than the 15% level recorded the prior week. The article adds that readings above 12% often align with heightened fear, implying sentiment improved even if traders remained cautious.

Deribit options skew data referenced in the article via Laevitas: Laevitas.

Ethereum’s upgrade path and what Glamsterdam is meant to fix

One persistent critique of Ethereum has been scalability at the base-layer level, especially as layer-2 rollups rely on data “blobs” to keep fees low. While blobs reduced transaction costs, the article highlights that the policy and resulting economics created wider debates around long-term data censorship and centralization, and also influenced base-layer fee dynamics.

With base-layer network revenue under pressure, ETH burning has been reduced, shifting the supply picture toward inflationary dynamics rather than consistent deflation. That makes every improvement to base-layer throughput more important to the broader thesis: if Ethereum can process more data and transactions efficiently without relying on tradeoffs that worsen long-term incentives, the market narrative improves.

In that context, the article focuses on the Glamsterdam upgrade. It states that Glamsterdam is in testing and is designed to improve Ethereum’s processing speed by allowing more transactions to run in parallel, expanding capacity to handle additional data at higher throughput, and reducing “database bloat.” The stated aim, per the article, is to provide institutional-grade infrastructure for financial use cases.

Ethereum upgrade reference in the article: Glamsterdam upgrade.

BitMine’s accumulation and the meaning of large unrealized losses

The article also credits continued spot accumulation by BitMine Immersion Technologies with helping reinforce the $1,500 support level. It notes that BitMine increased its ETH holdings by 325,000 ETH over the past month, bringing total reserves to 5.74 million ETH.

Crucially, the article acknowledges the risk embedded in this strategy: even with roughly $8 billion in unrealized losses on its ETH holdings, BitMine continues buying. It frames the company’s approach as aligned with a longer-term plan toward acquiring 5% of the existing supply.

For market participants, the practical takeaway is not just that a large holder is accumulating — it’s that the firm appears willing to sustain accumulation through drawdowns. Large, persistent demand can change how investors interpret support levels, particularly around psychological price ranges like $1,500.

BitMine holdings reference in the article: bmnr.rocks.

Robinhood Chain and tokenized stocks: TradFi grows inside Ethereum’s orbit

While onchain and derivatives metrics may still look cautious — particularly given low network fee conditions mentioned in the article — the upside case for ETH is being reinforced by traditional finance integration.

The piece highlights the launch of Robinhood Chain on July 2. It describes Robinhood Chain as an EVM-compatible Ethereum layer-2 built using Arbitrum technology, positioning the network for interoperability with Ethereum’s broader ecosystem.

More importantly for adoption, the article says Robinhood rolled out tokenized stock trading in more than 120 countries, alongside DeFi integrations including Uniswap, 1inch, and Morpho. This matters because it ties Ethereum-aligned infrastructure to real consumer-facing financial products rather than relying solely on speculative activity.

In effect, the article reframes the ETH rally as not merely a macro bet or a sentiment swing: it points to a structural narrative where Ethereum’s scaling roadmap and base-layer expansion could support an expanding layer-2 and application economy — and where TradFi participants are increasingly comfortable building tokenized instruments on Ethereum rails.

What to watch next for the $2,000 question

The article concludes that the path toward $2,000 looks plausible in the near term, given the combination of improving sentiment in options markets, ongoing ETH accumulation, and visible growth in tokenized finance use cases. Still, investors should watch how Ethereum’s base-layer economics evolve alongside Glamsterdam’s testing progress, and whether derivatives positioning continues to reflect a steady improvement rather than a temporary bounce.

EU lawmakers have approved a policy position calling for a review of whether decentralized finance, staking, crypto lending, borrowing and NFTs should be brought more clearly under the European Union’s crypto rulebook after MiCA’s rollout.

Summary

- EU lawmakers want the European Commission to review DeFi, staking, NFTs and crypto lending under MiCA.

- Parliament’s report does not change the law but outlines priorities for future crypto regulation.

- Decta data shows MiCA-compliant euro stablecoins grew 128% in market cap over the past year.

According to the European Parliament, members on Tuesday adopted the report titled Digital assets – challenges for the competitiveness and integrity of the European Union’s financial system, setting out Parliament’s official position on the next stage of crypto regulation.

The paper does not amend the Markets in Crypto-Assets regulation or impose new legal obligations on crypto companies, but it asks the European Commission to examine areas that remain outside the existing framework.

The vote comes days after MiCA’s transition period ended on July 1, when crypto-asset service providers that fall under the regulation became required to obtain either EU-wide or national authorization to continue serving customers across the bloc.

Lawmakers have turned attention to activities outside MiCA

With MiCA now in force, Parliament has asked the European Commission to assess whether decentralized finance, staking, crypto lending and borrowing, non-fungible tokens, and tokenized financial assets require additional regulatory treatment. The report also calls for consistent enforcement across member states, warning that different national approaches could weaken the EU’s single market for digital assets.

Earlier this year, the European Commission had already begun reviewing possible changes to the framework. In May, the Commission opened a public consultation seeking feedback on whether MiCA should cover additional crypto activities and whether restrictions on interest-bearing stablecoins should be reconsidered.

Alongside those proposals, Parliament’s report presents a favorable view of tokenization and euro-denominated stablecoins, stating that regulated digital assets could strengthen the competitiveness of European financial markets if the rules are applied consistently throughout the bloc.

Recent market data has pointed to growing activity in regulated euro-backed tokens. As previously reported by crypto.news, payments company Decta found that the combined market capitalization of eight MiCA-compliant euro stablecoins increased 128% over the 52 weeks ending June 28, 2026, rising from $295.6 million to $673.9 million.

Decta also reported a 43.1% increase in combined trading volume, while the number of compliant euro stablecoins with active market data grew from five to eight. According to Decta, EURC, EURCV and EURI accounted for most of the expansion.

Companies and users continue adapting to the new rules

The end of MiCA’s transition period has also prompted changes across the industry as firms and users adjust to the licensing regime.

As previously reported by crypto.news, BNB Chain recently published guidance explaining how users can move assets from centralized exchanges into self-custody wallets and connect directly with decentralized applications. The guide was released as European users evaluate whether their exchanges remain authorized under MiCA’s Crypto-Asset Service Provider licensing requirements.

While Parliament’s latest position does not immediately change the law, it gives the European Commission political backing to continue examining parts of the crypto market that remain outside MiCA. Any expansion of the framework would still require separate legislative proposals before new rules could take effect.

New Hampshire is moving closer to issuing what would be one of the first U.S. state-run municipal bond products backed by Bitcoin. The state’s Business Finance Authority (BFA) has scheduled a public hearing for Wednesday to discuss a proposed $100 million offering, following prior approvals that cleared the way for the plan to advance to the Governor and executive council.

According to the New Hampshire Secretary of State’s office agenda update, the BFA previously approved the BTC-backed bond arrangement in November 2025, with issuance tied to authorization from Governor Kelly Ayotte and the state’s five-member executive council. If granted, the structure would represent an attempt to integrate a highly volatile asset class into traditional public finance channels without placing state funds or taxpayers directly at risk—at least according to how the plan was framed by its proponents.

Key takeaways

- New Hampshire has scheduled a public hearing for Wednesday on a proposed $100 million Bitcoin-backed bond.

- The BFA approved the bond concept in November 2025, pending sign-off from Governor Kelly Ayotte and the executive council.

- A November 2025 framing by officials suggests the collateral is funded by a private party, aiming to avoid recourse to state funds.

- Moody’s assigned a provisional Ba2 rating (speculative grade), underscoring the credit risk tied to Bitcoin-linked structures.

- Similar Bitcoin-backed bond ambitions in El Salvador failed to progress after the crypto market downturn.

From approval to a public hearing

The latest development comes via an update to the New Hampshire governor and executive council agenda. The Business Finance Authority has scheduled a meeting for Wednesday focused on the proposed issuance of $100 million in bonds backed by Bitcoin.

The groundwork for the proposal was laid earlier. The BFA approved the bond in November 2025, indicating it planned to proceed only after receiving required authorizations from Governor Kelly Ayotte and New Hampshire’s five-member executive council. That sequence matters for investors and market participants because it shows the state is not treating the offering as an automatic follow-through—it remains subject to final governance checkpoints.

In connection with the approvals at the time, Ayotte described the effort as an “innovative way” to expand investment opportunities while positioning New Hampshire as a leader in digital finance, while emphasizing that it would not risk state funds or taxpayer dollars.

A new use case for digital finance—and an unresolved governance path

New Hampshire’s push toward Bitcoin-backed instruments fits a broader shift in state policy toward regulated experimentation. The state was the first to approve a law establishing a strategic Bitcoin reserve in May 2025, allowing public investments equal to 5% of funds, subject to a market capitalization threshold (over $500 billion). That legal direction provides the policy backdrop for why state institutions are exploring Bitcoin-adjacent financial products.

Still, the hearing scheduled for Wednesday highlights the practical reality: even if legislative policy is supportive, bond issuance typically depends on risk allocation, collateral mechanics, and credit considerations that rating agencies evaluate independently. Those concerns surfaced when industry scrutiny addressed whether a Bitcoin-backed municipal bond can function like conventional public finance debt.

Credit risk and the case for “proof of concept”

A key question for readers is how “municipal bond” applies when the underlying collateral is tied to a highly volatile cryptocurrency. In an analysis authored in April, David Krause, an emeritus associate professor of finance at Marquette University, argued that while the proposal could act as a proof of concept for integrating digital assets into structured finance, it is not suited to serve as a general-purpose public finance tool.

Krause’s assessment emphasized that although a private borrower, CleanSpark, would supply the funds for collateral, the structure provided “no recourse to state funds or taxpayers.” In other words, the risk profile is meant to be contained, but the broader challenge remains: adapting traditional financial frameworks to assets with large and rapid price swings.

Rating activity reflected those concerns. In March, Moody’s assigned the proposed Bitcoin bond a provisional Ba2 rating. In Moody’s scale, that places the offering in the speculative grade category, signaling substantial credit risk tied to the bond’s structure and asset exposure.

For investors and traders, this combination—contained recourse to the state but speculative-grade credit implications—suggests the market impact will likely hinge on collateral management rules, redemption protections, and how volatility is handled across the life of the bond. Those are the types of details that often determine whether such instruments behave more like structured credit products than traditional municipal debt.

El Salvador’s “Volcano Bonds” as a cautionary parallel

New Hampshire’s attempt follows earlier momentum that briefly looked promising elsewhere. Under President Nayib Bukele, El Salvador announced $1 billion in Bitcoin-backed “Volcano Bonds” intended to fund the proposed Bitcoin City project. The idea was revealed in 2022, alongside efforts that later culminated in Bitcoin being recognized as legal tender.

However, the Volcano Bonds plan did not move forward as intended. The source notes that the project fizzled out following a crypto market downturn—an outcome that matters for how market participants interpret New Hampshire’s current effort. If the global risk environment deteriorates or liquidity thins, Bitcoin-linked structured products can face additional operational and valuation pressures even when the legal framework is designed to isolate state exposure.

Comparing the two situations underscores a broader point: regulatory willingness and political support do not eliminate market-driven constraints. In both cases, price cycles and institutional risk appetite can determine whether Bitcoin-backed financing becomes scalable or remains experimental.

Going forward, the decisive question for New Hampshire will be whether the Governor and executive council clear the remaining authorization steps after the public hearing—alongside how bond terms address volatility, collateral requirements, and credit-risk mechanics under rating scrutiny. As the proposal advances, investors should watch for the final structure details that explain how speculative-grade risk is managed, and whether that framework can hold under changing Bitcoin market conditions.

Tether has invested $20 million in Mercado Bitcoin to support the Brazilian company’s expansion across tokenized assets, blockchain payments, lending, and on-chain capital markets.

Summary

- Tether has invested $20 million in Mercado Bitcoin to expand tokenized assets, blockchain payments, lending, and capital markets.

- Mercado Bitcoin plans to use the funding to grow its payments infrastructure, tokenization business, and international presence.

- The investment comes as Tether continues expanding beyond USDT, including its upcoming Bitcoin-native USDT launch via RGB.

According to a July 7 announcement from Tether on Tuesday, the investment forms part of a strategic growth financing round for Mercado Bitcoin, one of Latin America’s largest digital asset platforms.

The stablecoin issuer said it is backing companies that combine regulatory approvals with large-scale blockchain infrastructure, as demand for tokenized financial services continues to grow across the region.

Founded in São Paulo in 2013, Mercado Bitcoin has evolved beyond cryptocurrency trading into an on-chain financial services provider. The company said it now serves 4.5 million users and has issued more than 2 billion Brazilian reais worth of tokenized assets.

It also holds more than 10 regulatory licenses across Brazil and Europe, including a payment institution license from the Central Bank of Brazil, while operating brokerage, securitization and asset management businesses.

The funding will expand blockchain-based financial services

Mercado Bitcoin said the fresh capital will be used to strengthen its payments infrastructure, increase the availability of tokenized investment products for retail and institutional clients, expand lending and credit operations, develop on-chain capital markets, and support international growth.

Commenting on the investment, Tether Chief Executive Paolo Ardoino said:

“Mercado Bitcoin has built exactly that, a regulated, full-stack on-chain financial platform serving millions of users across one of the world’s most dynamic financial markets.”

Ardoino added that the company’s combination of licensing, tokenization infrastructure and integrated financial services stands out across the region.

Roberto Dagnoni, chairman and chief executive of Mercado Bitcoin, said financial services are increasingly moving onto blockchain networks, with tokenization, stablecoins, payments and capital markets becoming the next stage of industry development.

According to Dagnoni, Tether’s investment will help accelerate the company’s expansion of on-chain financial services in Brazil and overseas markets.

Tether continues investing beyond its stablecoin business

As banks and consumers increasingly adopt blockchain-based payment systems, Tether pointed to Brazil’s financial ecosystem as an important market because of its digital adoption, regulatory progress and the success of Pix, the country’s instant payment network developed by the central bank. The company said these conditions have supported faster adoption of blockchain-based financial products.

The investment adds to a series of recent deals completed by Tether. In June, the company announced it would lead a funding round of up to $1.4 billion for German robotics company NEURA Robotics.

During the same month, Tether signed a memorandum of understanding with the Dubai Multi Commodities Centre to collaborate on tokenization initiatives and blockchain education. It also announced plans to discontinue Alloy by Tether and its aUSDT token after reviewing market demand and platform usage.

Separately, as previously reported by crypto.news, Tether has confirmed that USDT will return to Bitcoin as a native asset through the RGB protocol. According to an exclusive interview published by Bitcoin Magazine, the rollout is being developed with software company UTEXO, which will commercially issue and distribute Bitcoin-native USDT in partnership with Tether.

The launch is expected within weeks using RGB protocol version v0.11.1, bringing USDT back to the Bitcoin network where it originally debuted through the Omni Layer in 2014.

Neither Tether nor Mercado Bitcoin disclosed the valuation of the financing round or its total size. Tether described its participation as a long-term strategic investment supporting Mercado Bitcoin’s next phase of development as the company expands blockchain-based financial services across Latin America and international markets.

OpenAI’s Chief Futurist Is Leaving the Company

AP honors Breanna Stewart as one of the top women’s college players during the Top 25 poll era

From mouthwash to hair dye: How weight-loss jabs are changing shopping habits

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: High Hopes

-

NewsBeat3 days ago

NewsBeat3 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Fashion1 day ago

Fashion1 day agoOpen Thread: What Great Books Have You Read Recently?

-

Politics5 days ago

Politics5 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World7 days ago

Crypto World7 days agoAirdrop Registration Becomes Key Focus For Remittix As RTX Launch Updates Approach

-

Crypto World4 days ago

Crypto World4 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Business1 day ago

Business1 day agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports7 days ago

Sports7 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Crypto World6 days ago

Crypto World6 days agoBinance stock trading tops $1B in first month after launch

-

Crypto World6 days ago

Crypto World6 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

Crypto World1 day ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

Crypto World2 days ago

Crypto World2 days agoSouth Africa proposes crypto tax guidance under existing rules

-

News Videos1 day ago

News Videos1 day agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech3 days ago

Tech3 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

News Videos22 hours ago

News Videos22 hours agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Business6 days ago

Business6 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

NewsBeat6 days ago

NewsBeat6 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Business5 days ago

Business5 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World5 days ago

Crypto World5 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

-

News Videos2 days ago

News Videos2 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

You must be logged in to post a comment Login