Crypto World

Gate DEX Fully Integrates Robinhood Chain, Expanding Its Multi-Chain Ecosystem Layout and Onchain Service Capabilities

Gate DEX announced its full integration with Robinhood Chain, becoming one of the first mainstream exchange onchain gateways to support the ecosystem. This feature covers core scenarios such as asset discovery, wallet management, onchain trading, cross-chain interaction, and market tracking, providing users with a more complete and efficient Web3 experience for exploring emerging onchain ecosystems, and further expanding Gate DEX’s multi-chain layout and infrastructure capabilities. For a smoother experience, please update the Gate App to v8.27.0 or above.

As the onchain gateway of the Gate ecosystem, Gate DEX integrates wallet, cross-chain, trading, airdrops, Earn, and DApps, continuously building an open and interconnected full-scope Web3 ecosystem. With the rapid development of emerging public chains, users’ demand for asset discovery, project exploration, and onchain interaction continues to increase. By supporting Robinhood Chain, Gate DEX further connects emerging onchain ecosystems, providing users with a more convenient entry point to popular assets and innovative applications.

In terms of asset discovery, Gate’s main platform Alpha has newly added support for the display and trading of Robinhood Chain ecosystem assets, and has integrated ecosystem launch platforms such as Noxa.fun and Bankr. As an important exploration gateway for emerging assets on Gate, Alpha will connect users with popular assets and innovative projects in the Robinhood Chain ecosystem, helping users discover onchain opportunities more efficiently and improving the efficiency of exploring emerging ecosystem assets.

In terms of asset management and onchain interaction, Gate Wallet has newly added support for Robinhood Chain, enabling functions such as asset display, transfers, and DApp interaction, helping users manage onchain assets more conveniently. At the same time, Gate DEX Swap supports single-chain swaps and cross-chain swaps on the network, improving asset circulation efficiency.

In terms of trading and market services, Gate DEX professional trading supports Robinhood Chain market order trading, while the market module also supports the display of related tokens, helping users view ecosystem asset information and participate in onchain trading more conveniently. In addition, the chain scanning function has newly added support for this ecosystem and covers projects such as Noxa.fun and Bankr, helping users discover onchain hotspots promptly.

The integration of Robinhood Chain expands the boundaries of Gate DEX’s multi-chain ecosystem and enhances cross-chain interoperability. Relying on Across and LayerZero cross-chain solutions, Gate DEX enables asset circulation among BSC, Ethereum, Base, and Robinhood Chain, providing users with a more efficient and smooth multi-chain interaction experience.

Currently, Gate DEX has formed comprehensive onchain service capabilities covering asset discovery, wallet management, trading and swaps, cross-chain connections, and ecosystem applications. This ecosystem expansion is an important measure by Gate to continuously strengthen Web3 infrastructure and connect high-quality public chain ecosystems, and also reflects the platform’s continued investment in multi-chain connectivity and onchain product innovation. In the future, Gate will continue to deepen the development of the Gate DEX ecosystem, accelerate connections with more high-quality onchain networks and innovative applications, promote the continuous upgrading of Web3 product capabilities, and create a more open, efficient, and convenient onchain experience for global users.

How to Explore the Robinhood Chain Ecosystem?

Please update to Gate App v8.27.0 or above to access the new features.

- Discover ecosystem assets: App Exchange mode – [Trade] – [Alpha] – [All Chains] – Select a token

- Explore the onchain ecosystem: App DEX mode – [Markets] – [Markets] – [All Chains] – Select Robinhood Chain

- Swap assets: App DEX mode – [Trade] – [Swap] – Tap [Pay/Receive] – Select Robinhood Chain

- Advanced trading: App DEX mode – [Trade] – [Pro] – Select a token – [All Networks] – Select Robinhood Chain

Learn more here.

About Gate

Gate, founded in 2013 by Dr. Han, is one of the world’s leading cryptocurrency and integrated financial services platforms. Serving over 58 million users globally, it supports trading across 4,800+ digital assets and 12,500+ stock assets, while providing access to a comprehensive range of TradFi assets, including metals, stocks, indices, forex, and commodities, delivering users a one-stop, multi-asset trading experience and blockchain-related services. As an industry benchmark, Gate was among the first platforms to implement 100% Proof of Reserves. Its ecosystem includes Gate Wallet, Gate Ventures, Gate for AI Agent, and a wide range of products and services.

For more information, please visit: Website | X | Telegram | LinkedIn| Instagram | YouTube

Disclaimer:

This content does not constitute an offer, solicitation, or recommendation. You should always seek independent professional advice before making investment decisions. Note that Gate may restrict or prohibit certain services in specific jurisdictions. For more information, please read the User Agreement.

The post Gate DEX Fully Integrates Robinhood Chain, Expanding Its Multi-Chain Ecosystem Layout and Onchain Service Capabilities appeared first on BeInCrypto.

CASHCAT is a token named after a company name that was thrown away sixteen years ago. It reached a $156 million market cap, briefly outweighed every real asset on Robinhood’s blockchain, and its own website calls it fan fiction with a ticker.

Summary

- CASHCAT is a community memecoin on Robinhood Chain with a fixed supply of one billion tokens. It has no affiliation with Robinhood Markets, and its own site says so.

- The name comes from real history: before Robinhood was Robinhood, Vlad Tenev and Baiju Bhatt called their company CashCat. A New Yorker profile preserved the detail and a token resurrected it.

- It surged more than 2,100% in a week to a market cap near $156 million, at one point worth roughly twelve times every tokenized real-world asset on the chain combined.

- CEO Vlad Tenev dismissed utility-free assets on July 2, then posted six days later that the chain works great for memes too, and followed the token’s account.

- The token fell more than 33% in 24 hours after Noxa, the launchpad driving the boom, stopped accepting launches on July 11 and went dark two days later.

In 2010, two Stanford graduates building a trading company had a name for it. The name was CashCat. They discarded it, called the company Robinhood instead, and the detail survived only in a New Yorker profile and in the memory of people who read startup lore for fun. Sixteen years later, Robinhood launched a blockchain designed to settle tokenized stocks for institutions, and within days the busiest thing on it was a token named after the name they threw away. CASHCAT reached a market capitalization near $156 million, out-massed every real asset the chain was built for, and made a handful of anonymous wallets millionaires. Its website describes it as fan fiction with a ticker. That is not a criticism. It is the project’s own self-assessment, and it is more honest than most.

The basics

CASHCAT is a memecoin native to Robinhood Chain, the Ethereum layer 2 that Robinhood launched on July 1, 2026. For readers new to the network, crypto.news has also explained the chain it launched on.

Its supply is fixed at one billion tokens, with no further issuance. Its contract address is 0x020bfC650A365f8BB26819deAAbF3E21291018b4, and verifying that string against a trusted source before any transaction is the single most useful thing in this article. It does not have its own blockchain or application. It is a fungible token deployed on someone else’s chain, which is what almost every memecoin is.

It has no product, no roadmap in any meaningful sense, and no utility. The project does not pretend otherwise. Asked what the utility is, the site answers that the utility is cat.

Most importantly, and against what a large number of buyers appear to believe: it is not a Robinhood product. It is not owned, endorsed, backed, listed, or affiliated with Robinhood Markets in any way, and the token’s own website disclaims any connection to the company or to Tenev personally.

Where the name comes from

The connection is entirely historical and it is worth getting right, because the ambiguity is the asset.

Before the company became Robinhood, Tenev and co-founder Baiju Bhatt called their venture CashCat. The detail appears in a New Yorker profile of the company and had circulated among people who follow startup history for years. When Robinhood Chain launched, someone recognized that a discarded corporate name attached to a live corporate blockchain was a nearly perfect memecoin: instantly legible to anyone who knew the story, plausible to anyone who did not, and impossible for the company to claim without endorsing it.

That is the entire link. A name the founders rejected in 2010, revived as a token in 2026 by people with no relationship to them. There is no corporate partnership, no licensing arrangement, and no shared ownership. What exists is a shared piece of trivia, and the token converted that trivia into a market capitalization.

There is a small extra layer that fueled it: Tenev himself had tweeted about CashCat back in April 2021, which meant the lore was not merely documented but personally acknowledged by the CEO years before the token existed. None of that constitutes affiliation. All of it makes affiliation feel more plausible than it is.

What happened

The timeline is short and steep.

Robinhood Chain went live on July 1. CASHCAT deployed shortly after. Within roughly 24 hours it had rallied more than 1,700%, and over its first week it climbed more than 2,100%, reaching an all-time high above $0.17 and a market capitalization near $156 million, with some measurements putting the peak higher.

At its peak day on July 8, the token generated roughly $98 million in 24-hour volume, which was about 17% of the entire chain’s decentralized exchange volume. Set that against what the chain was built for: tokenized real-world assets on Robinhood Chain totalled roughly $12.8 million. At its high, one joke token was worth approximately twelve times every real asset on the network combined.

It did not stay alone. Cash Dog in Hood, Little John, Hoodrat, and Arrow followed within days, none of which existed before July 1. Noxa, the launchpad feeding the wave, was averaging roughly 18,600 new token launches per day. On July 8, Pump.fun added Robinhood Chain support, opening the chain to Solana’s memecoin crowd without bridging. For more context, crypto.news has covered the full story of the takeover.

Then it turned. On July 11, at the precise moment CASHCAT was hitting peak trading volume, Noxa stopped accepting new token launches. Two days later it went dark, citing concerns about low-quality tokens flooding the platform, having generated an estimated $12 million in cumulative fees. CASHCAT fell more than 33% in 24 hours. One prominent trader who claims to have ridden the token from a $10,000 market cap to $230 million dismissed the selloff as noise.

The Tenev problem

The CEO’s involvement is the reason this token is confusing rather than merely amusing, and the sequence matters.

On July 2, the day after the chain went live, Tenev told CNBC that the future of crypto is in real-world assets, drawing a line between productive tokenized assets and speculative tokens without underlying utility. His framing was that an asset not tied to an underlying utility is not a productive asset. It was a clean statement of the thesis the entire chain was built to prove, and it was, in effect, a dismissal of exactly the category CASHCAT belongs to.

Six days later, as CASHCAT climbed, he posted on X that while the company is building Robinhood Chain to be the best chain for real-world assets, it works great for memes too. He then followed the token’s account.

Both readings of that reversal are defensible. The charitable one: a permissionless chain cannot control what deploys on it, refusing to acknowledge the most visible thing on your own network would look ridiculous, and a light-hearted post is not an endorsement. Robinhood’s crypto chief stayed rigorously on message throughout, saying the company remains focused on building a secure and scalable foundation for real-world assets.

The uncharitable one: the follow and the post told the market what the company actually values, which is volume, and a retail buyer who sees the CEO engaging with a token named after his own company is going to draw a conclusion the disclaimer will not undo. The distinction between acknowledging and endorsing is clear to a lawyer and invisible to someone who just downloaded a wallet.

Who made money, and from whom

This is the part that gets celebrated and should be read carefully, because every one of these numbers has a counterparty.

One early buyer spent $838 and received 15.04 million tokens. They sold roughly 13.5 million for about $917,600 and held a remainder worth around $133,700, producing a return in the region of 1,250 times. A second wallet turned $85 into 17.4 million tokens and realized about $687,700 while sitting on roughly $1.2 million more on paper. The five most profitable wallets banked close to $3.7 million between them.

Now the other side. That $3.7 million came from the opposite end of roughly 12,300 sell orders. Every dollar of realized profit in a memecoin is a dollar someone else paid at a higher price, because the token produces no revenue and holds no assets. There is no external cash flow funding those returns. The gains are transfers.

The liquidity structure makes it worse than the market cap suggests. CASHCAT’s trading pool has been worth far less than the token’s headline capitalization, which means a $156 million number sits on a pool that cannot absorb anything close to $156 million of selling. Large trades swing price hard in both directions. A market capitalization is a multiplication, not a promise that the money is there.

And the standard verification does not exist. Security audits of the CASHCAT contract were not possible because Robinhood Chain is too new for the tooling to have caught up. That is a chain-wide condition, not a CASHCAT-specific failure, but it removes the check that would ordinarily flag a malicious contract before a nine-figure market cap forms on top of it.

How a memecoin actually prices

Because CASHCAT is the first token most Robinhood users will look at closely, it is worth walking exactly how a number like $156 million comes to exist, since almost nobody who quotes it understands what it measures.

Market capitalization is a multiplication. Take the last traded price, multiply by circulating supply, print the result. CASHCAT has a fixed supply of one billion tokens, so at a price above $0.15 the arithmetic produces something in the region of $156 million. That is the whole calculation. It is not a valuation, not an appraisal, and not a statement that $156 million exists anywhere.

What makes the number misleading is where the price comes from. The last trade might have been for a few hundred dollars. In an automated market maker, price is set by the ratio of assets in a liquidity pool, and the pool behind CASHCAT has been worth far less than the token’s headline capitalization. So a relatively small purchase moves the ratio, moves the price, and instantly revalues all one billion tokens at the new level. That is why memecoins can add nine figures of notional value in a day: a thin pool is a lever, and modest buying at the margin repriced the entire supply.

The lever works identically in reverse, which is what July 13 showed. When Noxa exited and sentiment turned, sellers hit the same shallow pool and the price fell more than 33% in a day. Nothing about the token changed. Supply was still one billion. The contract was unaltered. The only thing that moved was the ratio in the pool, and the market cap followed it down mechanically.

This is why the comparison that ran through every headline, that CASHCAT was worth twelve times every real-world asset on the chain, is both true and slippery. It is true as arithmetic: $156 million against $12.8 million. It is slippery because the two numbers are not the same kind of thing. The tokenized asset figure represents real instruments with real backing that could be redeemed. The memecoin figure represents a price multiplied by a supply, sitting on a pool that could not absorb a fraction of it. One number is a balance. The other is an echo.

The practical implication for anyone holding: your position is worth the market cap right up until you try to sell, at which point it is worth whatever the pool gives you. In a token where five wallets extracted roughly $3.7 million against 12,300 sell orders, the people who found out first were the ones who tried. That is why thin liquidity moves price so hard.

What this token actually shows

Set the price action aside and CASHCAT is the cleanest available case study in how new chains actually bootstrap, which is why it is worth understanding even if you would never touch it.

The optimistic reading, which serious traders make: memecoins are the ignition sequence. A new chain needs transactions, wallets, and liquidity to look alive, and speculation delivers all three faster than tokenized Treasuries do. Solana grew through a memecoin cycle before producing serious infrastructure, and one veteran trader explicitly compared Robinhood Chain’s early ecosystem to Solana’s. The automated market makers, oracles, and routing built to service speculation are the same rails that tokenized equities will eventually need. In that reading CASHCAT is not a distraction from the strategy; it is the first stage of it. That in the category CASHCAT belongs to.

The pessimistic reading, which the timeline supports: memecoin traders are mercenary by construction, loyal to activity rather than to any chain, and the moment a flashier venue offers quicker returns the volume leaves and the $12.8 million of tokenized assets is what remains. The launchpad that produced the entire boom extracted $12 million in fees and exited within eleven days of the chain going live. That is not the profile of a bootstrapping sequence. It is the profile of an extraction cycle, and the 33% drop when the launchpad left is the evidence.

Which reading is right gets settled by a single number, and it is not CASHCAT’s price. It is whether tokenized real-world assets on Robinhood Chain grow well beyond roughly $13 million while the speculation fades. Robinhood’s second-quarter earnings on July 29 are the first real look. Until then, CASHCAT is a token named after a discarded company name, worth more than everything the chain was built to carry, running on an unaudited contract, on a network whose CEO spent one week explaining why assets like it do not last and the next week noting they work great anyway.

What to watch

If you are tracking this token instead of trading it, three things carry information.

Whether the ecosystem keeps spawning. STONKCAT opened a $SCAT presale on July 16, and a MemeToro presale is running alongside it, both borrowing Robinhood Chain’s branding and pitching future products. New entrants arriving weeks after the launchpad that started the wave exited tells you the branding gap is now a repeatable business, which is bearish for CASHCAT specifically: every new token competes for the same attention that is the only thing holding its price up. It also shows how launchpads mint tokens on demand.

Whether the chain’s real assets grow. Tokenized real-world assets on Robinhood Chain sit around $12.8 million against roughly $312 million in total value locked. That figure, not CASHCAT’s price, decides whether the memecoin wave was an ignition sequence or an extraction cycle. Robinhood’s second-quarter earnings on July 29 are the first look at Stock Token adoption from the company’s own books.

Whether liquidity deepens or thins. The pool behind CASHCAT has been worth far less than the token’s headline capitalization, which is the mechanism behind both the rise and the 33% single-day fall. A token whose pool deepens is a token that can absorb selling. A token whose pool thins as attention rotates is a token whose market cap becomes progressively more theoretical. Also relevant: Robinhood Chain’s 90-day gas subsidy has been making trading artificially cheap, and its expiry is a real test.

The broader point for anyone reading this as a lesson instead of a trade: CASHCAT did nothing unusual. It is a well-executed example of an entirely standard pattern, distinguished only by the quality of its joke and the fact that a public company’s CEO engaged with it. The pattern will repeat on the next chain, with a different name, and the mechanics will be identical. What makes this instance worth remembering is the setting. Most memecoins erupt on chains built by anonymous developers for exactly this kind of activity, where nobody claims to be surprised. CASHCAT erupted on a network built by a listed American brokerage, marketed to institutions, staffed with compliance officers, and launched with a keynote about the future of finance. It took six days for the joke to become the chain’s largest asset by market capitalization, and the company could do nothing about it, because permissionless means permissionless. That is the lesson worth carrying: a corporate chain cannot choose its users any more than a public square can. Robinhood built the venue and the crowd decided what it was for.

Frequently asked questions

What is CASHCAT?

A community memecoin on Robinhood Chain, the Ethereum layer 2 Robinhood launched on July 1, 2026. It has a fixed supply of one billion tokens and a contract address of 0x020bfC650A365f8BB26819deAAbF3E21291018b4. It has no product, no utility, and no affiliation with Robinhood. Its own website describes the project as fan fiction with a ticker and says the utility is cat.

Is CASHCAT affiliated with Robinhood?

No. It is not owned, endorsed, backed, or listed by Robinhood Markets, and the token’s own website disclaims any connection to the company or to Vlad Tenev. The name references CashCat, the working name Tenev and co-founder Baiju Bhatt used before the company became Robinhood, a detail preserved in a New Yorker profile. That is trivia, not a relationship.

Why did CASHCAT rise so fast?

A combination of legible lore and a new chain with nothing else on it. The name connected instantly to Robinhood’s founding story, Robinhood Chain had just launched with cheap fees and easy token creation, and attention concentrated on the first breakout token. It rallied more than 1,700% in 24 hours and more than 2,100% over its first week, reaching a market cap near $156 million.

Did Vlad Tenev endorse CASHCAT?

Not formally. On July 2 he told CNBC that assets not tied to an underlying utility are not productive assets. On July 8, as the token climbed, he posted that while the company is building the chain for real-world assets, it works great for memes too, and he followed the token’s account. That is acknowledgement rather than endorsement, but the distinction is clearer to a lawyer than to a retail buyer.

How much was CASHCAT worth compared to the chain’s real assets?

At its peak, roughly twelve times more. Tokenized real-world assets on Robinhood Chain total around $12.8 million, while CASHCAT reached a market capitalization near $156 million. On its biggest day the token generated approximately $98 million in 24-hour volume, about 17% of the entire chain’s decentralized exchange volume.

Why did CASHCAT crash?

Noxa, the launchpad driving the chain’s memecoin wave, stopped accepting new launches on July 11 as CASHCAT hit peak volume, then went dark two days later, citing low-quality tokens flooding the platform. It had generated an estimated $12 million in cumulative fees. CASHCAT fell more than 33% in 24 hours following the exit.

Who made money on CASHCAT?

A small number of early wallets. One turned $838 into roughly $1.05 million across realized and unrealized value, about 1,250 times. Another turned $85 into roughly $687,700 realized plus $1.2 million on paper. The five most profitable wallets took close to $3.7 million between them. That money came from the other side of roughly 12,300 sell orders, since a memecoin produces no revenue and gains are transfers between participants.

What are the risks?

Considerable. The trading pool is worth far less than the headline market capitalization, so large trades swing price sharply and the stated value cannot be exited at that value. Security audits of the contract were not possible because Robinhood Chain is too new for verification tooling. The token has no revenue, no assets, and no utility, so price depends entirely on attention, which has already proven it can leave in a day.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. Memecoins are extremely speculative, frequently trade on thin liquidity, and most participants lose money. Contract addresses and project claims should be verified independently before any transaction. Nothing here is a recommendation to buy any token. Always do your own research. Figures are accurate as of July 17, 2026 and move rapidly.

XRP price is trading around $1.09 as momentum remains soft. The $1.00 level is still acting as key psychological support, although buyers have yet to seize control. For now, the next big move may depend less on charts and more on what happens in Washington.

Ripple has continued engaging U.S. lawmakers as stablecoin legislation moves through Congress. The company has argued that clearer digital asset rules could strengthen blockchain-based payment infrastructure, where XRP has long been positioned as a bridge asset. After years of legal uncertainty, even a little clarity feels like fresh air.

That regulatory push has caught the attention of institutional participants who largely stayed on the sidelines during Ripple’s court battle with the SEC. While sentiment has improved around key hearings, price action has remained stubbornly quiet. Markets have a habit of making everyone wait, then moving all at once.

Meanwhile, XRP’s 24-hour trading volume sits near $1.03 billion, with a market capitalization of around $68.1 billion. That keeps liquidity healthy enough for sharp moves once a real catalyst appears. Until then, traders may need patience, which is usually the hardest position to hold.

Discover: The Best Token Presales

Can XRP Price Double From Current Levels?

XRP is consolidating around the $1.09 to $1.13 price range, with $1.05 acting as immediate support. If that level gives way, the next meaningful floor sits near $0.85. Meanwhile, resistance starts around $1.13, followed by stronger selling pressure near $1.32. Nobody ever said climbing walls was easy.

The bull case, and the one that could send XRP toward the $2 mark, depends on the Clarity Act making meaningful progress through the Senate. That would strengthen XRP’s case as a compliant payment asset instead of a purely speculative token. It is less about chart patterns and more about a shift in market perception.

From a technical standpoint, a sustained move above $1.13 could open the door to $1.32. If buyers keep pressing, the next hurdle sits near $1.46. Exchange reserves also remain worth watching, as a lower available supply can magnify price swings once momentum finally shows up.

For now, the base case remains a sideways market between $1.05 and $1.13 until lawmakers provide clearer direction. However, delays to the Clarity Act or renewed regulatory uncertainty could drag XRP back toward the $0.85 support zone. A weekly close below that level would seriously weaken the current bullish outlook. The setup looks real, but the market still refuses to wear a watch.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Bitcoin Hyper Targets Early-Mover Upside as XRP Tests Key Levels

XRP at $1.09 with a potential double on the table sounds compelling, until you account for a $68 billion market cap that needs billions in fresh capital to move meaningfully. Early-stage infrastructure plays operate on entirely different math. This is where Bitcoin Hyper ($HYPER) enters the picture.

Bitcoin Hyper is positioning itself as the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration. It powers a combination that targets the two biggest criticisms of Bitcoin simultaneously: slow throughput and zero programmability.

The chain has sub-Solana latency on a Bitcoin-secured base layer, with a decentralized canonical bridge for native BTC transfers and low-cost smart contract execution built in. The presale has raised close to $33 million at a current token price of $0.0136832, with staking available for early participants.

Early-stage presales carry meaningful risk, liquidity is thin, and post-launch price discovery is unpredictable. But the infrastructure narrative around Bitcoin scalability has been building for two years. If XRP’s regulatory catalyst takes longer than expected to materialize, capital looking for asymmetric exposure has to go somewhere.

Discover: The Best Crypto to Diversify Your Portfolio

The post XRP Price Could Double as Ripple Pushes Senate for Clarity Act appeared first on Cryptonews.

Pi Network’s coin, PI, rose by more than 3.5% over the past 24 hours, outpacing a broader crypto market that lost nearly 3%.

The rise came as Pi Network began a design refresh of its mining app. The gain offered brief relief for a token that hit a record low days earlier. PI traded near $0.078, though it remains down more than 22% over the past week.

Pi Network Price Bounces Off a Record Low

PI touched an all-time low near $0.071 on July 14. The token has since recovered roughly 11% from that level.

Even after the bounce, PI trades about 97% below its February 2025 peak near $2.99. Its 30-day loss stands at roughly 42%.

Rising supply has weighed on the altcoin already stuck in a downtrend. About 10.9 billion PI circulate against a maximum of 100 billion, leaving room for further dilution.

According to PiScan data, roughly 4.25 million PI unlock each day, worth about $333,672 at current prices. That steady daily release adds fresh sell-side pressure with each session.

Follow us on X to get the latest news as it happens

Pi Network Begins a Mining App Refresh

Pi Network redesigned the side menu and the app profile page in its mining app, marking the first step in a broader design refresh. The team said that the redesign lets Pioneers reach key account details and ecosystem tools faster.

The redesign lands ahead of Protocol v25, scheduled for July 22. The upgrade aims to improve network stability and add privacy-preserving smart contracts.

Whether the update push can offset supply-driven selling remains the key test. The July 22 upgrade will show if utility gains start to translate into demand.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Pi Coin Defies a Falling Crypto Market as Pi Network Overhauls Its App appeared first on BeInCrypto.

Bitcoin price is hovering around the mid $63,000 range after one of the year’s sharpest leverage flushes in a bearish prediction environment. BlackRock CEO Larry Fink blamed Bitcoin’s recent volatility on excessive derivatives leverage, and not on weakening fundamentals. The liquidation data support his view, with billions wiped out during the selloff. Most of those losses came from overleveraged longs, not panic selling.

Now that the dust has settled, Bitcoin is trying to hold the $62,000 to $65,000 range. That puts the spotlight on upcoming options expiry and fresh signals from the Federal Reserve. Price action alone may not tell the whole story this time.

Instead, institutional demand is becoming the market’s favorite scoreboard. ETF flows and large investor positioning could decide whether Bitcoin regains momentum or stalls below resistance. For now, traders seem happy buying dips, but nobody is rushing to crank the leverage back up.

Discover: The Best Token Presales

Bitcoin Price Prediction: Reclaim $70,000 After Another Leverage Flush?

Bitcoin is trading around $62,850 after slipping from this week’s highs near $65,000. During the past 24 hours, BTC traded between $62,700 and $64,000, while daily trading volume hovered near $27 billion. Activity remains elevated compared with quieter sessions, showing traders are still working through the recent liquidation wave.

Technically, the next test is whether Bitcoin can defend the low $62,000 area, which has attracted buyers repeatedly this month. The rebound from those levels showed real demand, yet bulls still need to reclaim the $64,500 to $65,000 zone. Until that happens, every rally risks feeling like a dress rehearsal instead of opening night.

Three scenarios remain in play. In the bullish case, leverage continues cooling, institutional demand absorbs supply, ETF inflows stay healthy, and Bitcoin pushes above $65,000 before challenging $70,000. That would finally give buyers something to smile about besides green candles lasting five minutes.

The base case is less dramatic. Bitcoin could keep chopping between $62,000 and $65,000 while traders wait for the next macro catalyst, whether that comes from the Federal Reserve or ETF flows. It is not exciting, but markets rarely hand out fireworks every day.

The bearish case still deserves respect. Another derivatives-driven flush after disappointing macro data could drag Bitcoin below $62,000 and put the recent recovery under pressure. Larry Fink may remain bullish, but leverage has not disappeared overnight. For now, holding above support matters far more than anyone’s crystal ball.

Trade Bitcoin and Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Bitcoin Hyper Targets Early-Mover Upside as Bitcoin Tests Key Levels

Spot BTC at $64k carries a $1.29 trillion market cap. The upside math from here, while real, is measured in percentages for most holders. Early-stage infrastructure bets on the Bitcoin ecosystem operate on entirely different return profiles, which is where projects like Bitcoin Hyper enter the conversation.

Bitcoin Hyper ($HYPER) is positioning as the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, a combination that targets the three core limitations Bitcoin itself has never resolved: slow throughput, high fees, and no native programmability.

These Backrooms hit a little different. — Bitcoin Hyper (@BTC_Hyper2) July 17, 2026

https://t.co/VNG0P4GuDo pic.twitter.com/mU0O0EpPV1

https://t.co/VNG0P4GuDo pic.twitter.com/mU0O0EpPV1

The presale is priced at $0.0136832 and has raised $32.9 million to date, with a staking mechanism offering high APY for early participants. The SVM integration is the technical differentiator; lower latency than Solana itself on a Bitcoin security layer is an aggressive benchmark.

For traders watching BTC consolidate at current levels and looking for asymmetric exposure to Bitcoin ecosystem growth, research Bitcoin Hyper’s presale terms here before the next stage pricing moves.

Discover: The Best Crypto to Diversify Your Portfolio

The post Bitcoin Price Prediction: Larry Fink Turns Bullish on BTC, Blames Leverage Trading appeared first on Cryptonews.

Cointelegraph is committed to providing independent, high-quality journalism across the crypto, blockchain, AI, and fintech industries.

All news, reviews, and analyses are produced with full journalistic independence and integrity. For more details on our standards and processes, please read our Editorial Policy.

Bitcoin Japan has secured plans to raise approximately 9.66 billion yen (approx $59.5 million), with 662 million yen (approx $4.08 million) earmarked for its first Bitcoin treasury allocation since adopting its new corporate identity.

Summary

- Bitcoin Japan has planned a 9.66 billion yen fundraising, with 662 million yen allocated for its first Bitcoin purchases.

- Most of the proceeds will go toward private equity, rare earth mining, and Robot as a Service investments, while Bitcoin receives about 7% of the total.

- The funding follows an earlier capital raise that failed to finance its Bitcoin treasury strategy after falling short of its fundraising target.

Japanese crypto news outlet CoinPost reported that Tokyo Stock Exchange-listed Bitcoin Japan, formerly Horita Marusho, will issue 1.5 billion yen in unsecured convertible bonds with stock acquisition rights alongside a second series of stock acquisition rights through Cayman Islands-based investment fund EVO FUND.

If the securities are fully exercised, the company expects net proceeds of about 9.657 billion yen.

Bitcoin receives 7% of planned fundraising

Company filings cited by CoinPost show that Bitcoin purchases will receive 662 million yen, or about 7% of the planned financing. The largest share, 3.756 billion yen, has been set aside for undisclosed private equity investments, followed by 3.503 billion yen for rare earth mining projects in South Africa and 1.446 billion yen for investments in a Robot-as-a-Service (RaaS) business. Another 290 million yen has been allocated for working capital.

Convertible bonds allow investors to exchange debt for company shares at a predetermined price. CoinPost noted that the structure can reduce immediate pressure on the share price by spreading conversions over time, although the company remains responsible for repayment if the bonds are not converted.

Bitcoin Japan changed its name from Horita Marusho in 2024 and announced plans to transition from a textile trading business into a digital asset treasury company centered on Bitcoin and AI infrastructure. Even so, the company has yet to acquire any Bitcoin.

The latest allocation follows an earlier fundraising effort that fell short of expectations. Company disclosures previously showed that Bitcoin Japan planned to raise as much as 5.715 billion yen in December 2025, including 988 million yen for a Bitcoin treasury strategy. Weak share price performance limited investor participation, reducing the total amount raised to 3.095 billion yen and leaving no funds available for Bitcoin purchases.

Current filings state that the newly allocated Bitcoin funds will be deployed selectively depending on market conditions. The company has not disclosed a purchase timeline, targeted Bitcoin holdings, or performance metrics, although it continues to describe Bitcoin as a long-term hedge against the erosion of fiat currency value.

Financing comes after technology investment push

The fundraising follows Bitcoin Japan’s recent expansion into technology investments beyond digital assets.

In May, the company disclosed an investment in SpaceX through its wholly owned U.S. subsidiary, BTCJPN US LLC, using a U.S.-based private secondary market transaction. At the time, Bitcoin Japan said it was targeting sectors including AI compute infrastructure, satellite communications, digital assets, and next-generation technologies as part of its long-term investment strategy.

The latest financing could also substantially increase the company’s share count. According to documents cited by CoinPost, full conversion of the convertible bonds and exercise of all stock acquisition rights at the minimum price would result in dilution of up to 110%, or 115% on a voting rights basis.

Because the transaction qualifies as a large third-party allotment under Japanese rules, the company obtained an opinion from an independent committee consisting of outside legal experts, which concluded that the financing was necessary and reasonable.

Financial results released by the company showed consolidated revenue of 2.959 billion yen and an operating loss of 462 million yen for the fiscal year ending March 2026, extending its streak of operating losses to eight consecutive years. Against that backdrop, the planned Bitcoin allocation represents the company’s first funded step toward executing the treasury strategy it announced after its rebranding.

Crypto World

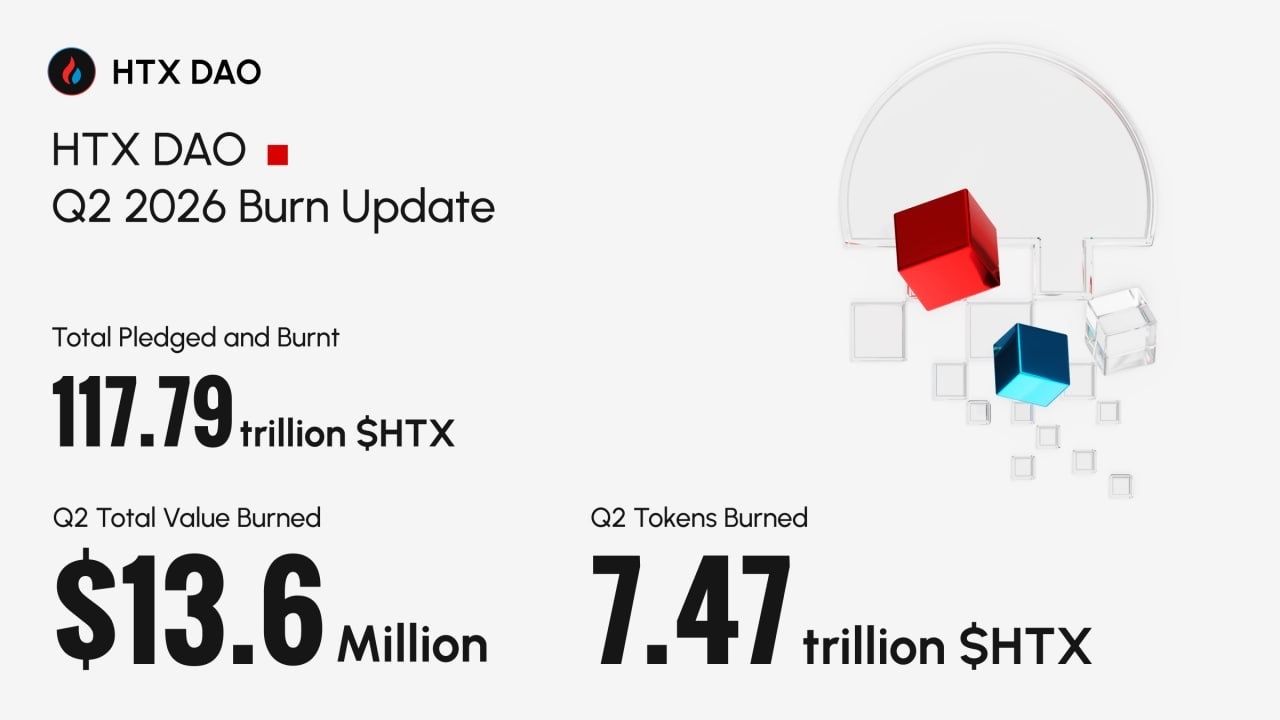

HTX DAO Burns Over $32.82 Million Worth of $HTX in H1 2026, Highlighting Strong Business Resilience

HTX DAO announced the successful completion of its $HTX token burn for Q2 2026 on July 15, 2026. On-chain data shows that a total of 7,474,935,439,560 $HTX tokens were burned in this round, valued at over $13.6 million. Following this latest burn, the cumulative volume of $HTX burned and pledged has reached 117.79 trillion tokens (backed by verifiable on-chain burn proofs.)

Combined with Q1 data, HTX DAO burned a total of over $32.82 million worth of $HTX in the first half of 2026. At a time when broader market liquidity remains under sustained pressure, this deflationary track record stands out as a highly compelling achievement.

Retaining Strong “Value Generation” Capabilities in a Downturn

Looking back at the first half of the year, the crypto market experienced highly complex sentiment shifts and tight liquidity conditions—with BTC temporarily slipping below the $60,000 threshold. These headwinds were largely driven by macro factors, including diminished expectations for Fed rate cuts and consecutive net outflows from Spot ETFs.Concurrently, spot and derivatives trading volumes across the industry fell sharply, and the aggregate stablecoin supply contracted on a quarterly basis for the first time since Q3 2023.

Despite these industry-wide challenges, $HTX maintained a multi-million-dollar burn scale across consecutive quarters. This consistency not only reflects the steady execution of the HTX DAO deflationary mechanism but also highlights the exceptional operational resilience and counter-cyclical capabilities of the HTX platform.

According to H1 data disclosed by HTX, the platform’s cumulative registered users reached 59.49 million, with total trading volume approaching $90 million. Additionally, the platform now supports over 612 trading pairs, covering mainstream assets, trending sectors, and high-potential new projects.

This robust trading activity and steady pipeline of asset listings have provided sufficient cash flow to support the ongoing deflation of $HTX.

Ecosystem Expansion Uplifts the Long-Term Value Potential

While large-scale token burns build the essential scarcity foundation for $HTX, the true driver of its long-term value is the continuous expansion of its use cases and ecosystem demand.

The HTX Genesis Hackathon — co-hosted by HTX DAO and B.AI, and co-organized by TinTinLand — is now entering its final stage. Featuring a 20,000 USDT prize pool alongside over $100,000 in computing power resources, the event drew participation from more than 200 developer teams. Participants focused on pioneering sectors, including $HTX utility scenarios, AI agent finance, on-chain asset management, DAO tools, and smart financial operating systems.

Notably, developer incentive programs of this kind do more than just introduce innovative projects to the ecosystem. They actively expand the utility of $HTX in decentralized governance, payments, incentives, and collaborative ecosystem synergies, creating more sustained and genuine utility demand for the token.

Looking ahead, as the HTX DAO governance framework matures, the developer ecosystem expands, and additional innovative applications go live, $HTX is poised to evolve from a standalone governance token into a critical value carrier. It will serve as the core link connecting trading, decentralized governance, developer networks, and AI innovation, securing a robust and sustainable foundation for the entire HTX DAO ecosystem

About HTX DAO

As a multi-chain deployed decentralized autonomous organization (DAO), HTX DAO demonstrates an innovative governance approach. Unlike traditional corporate structures, it adopts a decentralized governance structure composed of a diversified group, jointly committed to the success of this organization. This unique ecosystem advocates openness and encourages all DAO participants to propose ideas that can promote the development of HTX DAO.

Contact Information

Website: www.htxdao.com

The post HTX DAO Burns Over $32.82 Million Worth of $HTX in H1 2026, Highlighting Strong Business Resilience appeared first on BeInCrypto.

A macOS information-stealing malware can compromise Telegram Desktop sessions and, from there, target both software and hardware cryptocurrency wallets, according to blockchain security firm SlowMist. The report describes an attack chain that harvests credentials and wallet data from multiple macOS sources, then leverages that access to swap or drain funds through techniques that do not rely on breaking Telegram’s two-step verification in the usual way.

SlowMist says the malware extracts secrets from macOS Keychain, Safari cookies, Apple Notes, Telegram Desktop and database files tied to more than a dozen cryptocurrency wallets. After collecting passwords and authenticated session data, it copies Telegram Desktop session information along with wallet databases and browser wallet extension data, enabling follow-on account takeover attempts.

Key takeaways

- SlowMist reports malware can hijack existing Telegram Desktop sessions on macOS by reusing authenticated local data rather than forcing a new login.

- In addition to stealing passwords, the malware targets wallet databases and application data for both popular software wallets and hardware wallet managers.

- Telegram two-step verification may not block the attack because the malware avoids the need to pass verification challenges.

- SlowMist outlines two follow-up strategies: offline wallet database decryption using harvested passwords, or replacing wallet apps (e.g., Ledger/Trezor software) with decoys to capture recovery phrases.

How Telegram Desktop becomes the entry point

SlowMist’s core warning is that Telegram Desktop accounts on macOS may be compromised even when users have enabled two-step verification. The reason, the firm says, is architectural: instead of creating a fresh login that requires verification, the malware reuses an already authenticated local session stored on the device.

In its tests, SlowMist restored stolen Telegram Desktop session data on another Mac without requiring the user to enter a phone number, verification code, or two-step verification password. That distinction matters for users because two-step verification is designed to protect logins, while this method targets session material that can be carried over to a new environment.

The practical takeaway is that Telegram Desktop should be treated as a high-value target when credentials and session files are accessible to malware. If an attacker can move a session to another machine, subsequent steps—such as obtaining access to linked accounts, exchanging information, or guiding victims toward risky actions—can proceed without triggering the protections that apply to new authentication.

Wallet data theft spans software wallets, hardware managers, and node databases

SlowMist says the malware is not limited to Telegram. It also harvests wallet-related data from a wide range of sources, including wallet applications and full-node clients.

On the wallet side, SlowMist names software wallets such as Exodus, Atomic, Electrum, Wasabi and Monero. It also points to targeting hardware wallet software interfaces, including Ledger Live and Trezor Suite—software layers that manage hardware devices and frequently coordinate how users view balances and initiate transactions.

Beyond standalone wallets, the report says the malware searches for wallet data stored by full-node clients, listing Bitcoin Core, Litecoin Core, Dash Core and Dogecoin Core among those affected. For investors and traders, the implication is straightforward: wallet information does not only live in wallet apps. If malware can reach local storage associated with node software, it may uncover additional material that helps attackers attempt to access or reproduce wallet capabilities.

SlowMist also describes collecting data beyond wallet databases, including Safari cookies and Apple Notes. Those components can increase an attacker’s ability to persist access, understand user behavior, or extract sensitive information that is not stored in one dedicated wallet folder.

Offline cracking and fake recovery flows

After harvesting passwords and authenticated session data, SlowMist says attackers can attempt to decrypt stolen wallet databases offline. The attacker would use passwords taken from the infected device, reducing the need for repeated online attempts that might trigger rate limits or other defenses.

SlowMist also describes a second approach: replacing legitimate Ledger and Trezor applications with fake versions. In this scenario, victims could be tricked into entering recovery phrases into the counterfeit software—an especially dangerous outcome because recovery phrases are effectively “master keys” for accessing funds.

SlowMist states it reproduced the attack chain in an isolated environment, supporting its claim that the described steps can be executed together rather than as unrelated capabilities.

For users, the key risk is that wallet compromise can be multi-stage. Even if attackers initially acquire Telegram session access, the malware’s broader collection of wallet databases and application data can enable direct attempts to extract value or pivot to social engineering that captures recovery credentials.

Why Telegram’s usual protections may not be enough

SlowMist’s findings highlight a recurring theme in account takeover incidents: security features sometimes assume a specific threat model. Telegram two-step verification helps protect new logins, but the malware’s method—carrying over an authenticated local session—changes the conditions.

Instead of challenging the user during sign-in, the attacker operates with session data that the device has already established. That makes “I turned on 2FA” less reassuring when malware is already present and can read session-related files.

SlowMist also recommends immediate operational steps for anyone who suspects compromise. It urges users to terminate existing Telegram sessions, create a new trusted login, and update both the Telegram two-step verification password and the Telegram Desktop Passcode. Those steps aim to invalidate the hijacked session material and force Telegram to re-establish trust through a fresh authentication flow.

The firm further advises generating a new recovery phrase on a clean device and moving assets to new addresses. The goal is to break the link between the compromised wallet state and the assets that need protection. If wallet apps or recovery material were exposed, reusing the same recovery phrase after a compromise can leave funds vulnerable to attackers who already have enough information to regain access.

SlowMist’s report serves as a reminder that cryptocurrency security is not only about securing keys on paper or enabling 2FA on messaging apps. When malware can access both session data and wallet databases locally, protections must extend to device hygiene and rapid incident response. Users should watch closely for signs of compromise, verify which Telegram sessions remain active, and be prepared to move funds to fresh addresses after any suspected infection.

Everyone is watching a bill that may not pass. Meanwhile, the agency that spent seven years suing this industry has quietly scheduled a rule that would let startups sell tokens without registering them, and it does not need a single vote in Congress.

Summary

- The SEC has placed Regulation Crypto in its July 2026 rulemaking slot, the first major crypto-specific rule of the Atkins era. It is under review at the White House Office of Information and Regulatory Affairs.

- The proposal would create a time-limited registration exemption for early-stage crypto projects, permit raises of up to $75 million in any 12-month period, and build a safe harbor letting a token exit securities status once its creators stop exerting managerial effort.

- DeFi and tokenized securities are named explicitly as areas where qualifying activity would be protected from SEC enforcement.

- The strategic point almost everyone is missing: a formal rule is far harder for a future Commission to unwind than the staff guidance and interpretive releases the industry currently relies on. The agency route may deliver more durable protection than the bill.

- The catch is that one agency would be writing the rules of American crypto alone, with thresholds that face intense scrutiny the moment they publish, and a safe harbor that is an off-ramp instead of an amnesty.

The entire crypto policy conversation for the past month has been about a bill. Whether the Senate schedules CLARITY, whether seven Democrats can be found, whether the ethics provision survives, whether three working weeks is enough. It is a good story and it may end badly. It has also completely obscured the fact that while Congress argues, the Securities and Exchange Commission has scheduled something that would accomplish a large portion of what the bill promises, requires nobody’s vote, and is sitting at the White House right now awaiting review. It is called Regulation Crypto, it is slotted for July, and it would do the one thing the industry has wanted since 2018: let a startup sell a token in America without first registering it as a security.

What the rule would actually do

Chairman Paul Atkins first sketched the framework in remarks on March 17, 2026, the same day the SEC and CFTC published their joint token taxonomy. That timing was not coincidental. The taxonomy answered what a crypto asset is. Regulation Crypto answers what you may do with one.

Three components carry the weight.

A startup exemption. A time-limited registration exemption for offerings of investment contracts involving certain crypto assets, lasting up to four years, giving developers a regulatory runway while they work toward maturity. Atkins framed the eligibility around early-stage projects, with figures discussed around startups valued under $5 million in their first four years, able to raise up to $5 million during that period. Critically, the exemption would be non-exclusive, meaning every other capital-raising exemption under the federal securities laws would remain available alongside it.

A fundraising exemption. For projects past the earliest stage, a larger allowance: entrepreneurs could raise up to $75 million during any 12-month period while retaining the ability to rely on other registration exemptions. Reporting on the agency’s agenda indicates this would come with conditions, including audited balance sheets and statements regarding the issuer’s financial condition, plus notices to the Commission when relying on the exemption and when exiting it.

A safe harbor for decentralization. This is the most consequential piece. The proposal would create a definitive safe harbor for issuers who complete or transition away from centralized management efforts over their networks, allowing a token to exit securities classification once managerial effort ceases. That is the decentralization off-ramp the industry has been asking for since the Hinman speech, and it would apply an objective standard to secondary markets where those tokens trade.

Beyond those three, the proposal reaches into tokenized securities, and DeFi is named explicitly as an area where qualifying companies would receive protection from enforcement action. The agency has acknowledged, in effect, what practitioners have said for years: traditional securities registration is incompatible with decentralized protocols and automated smart contract systems. Separately, the SEC has opened a comment request reviewing spot crypto ETF approval procedures and proposing a confidential filing process for initial applications, after the Division of Investment Management’s director conceded the agency had mishandled the simultaneous launch of spot crypto funds.

Why this is bigger than it looks

Here is the argument nobody is making loudly enough, and it inverts the entire CLARITY frame.

The American crypto industry currently operates on administrative action. The March 17 joint interpretation classifying 16 named assets as digital commodities is a Commission-level interpretive release. It is binding on the SEC and CFTC, which makes it far stronger than the staff guidance that preceded it, and it is already cited in fund registration statements. But it is not a rule and it is not a law. A future Commission can issue a different interpretation without notice, without comment, and without Congress.

A formal rule is a different animal. Rules go through notice and comment. They generate a record. Reversing a final rule generally requires another full rulemaking with a reasoned explanation capable of surviving judicial review, and agencies that try to shortcut that process lose in court. Bankless put the point precisely: the SEC has leaned on staff guidance and its taxonomy so far, but formal rules are far harder for a future commission to unwind.

So there is a ladder of durability, and it is worth being explicit about where each thing sits.

Staff guidance binds nobody. A Commission interpretation binds the agencies and can be replaced by another interpretation. A formal rule binds until another rulemaking undoes it. A statute binds until Congress acts. The industry has spent a year fighting for the top rung and has largely ignored that the agency is quietly building the third.

Which produces an awkward question worth asking directly: if Regulation Crypto publishes and survives comment, how much of CLARITY does it deliver anyway? Not all of it. The rule cannot divide jurisdiction between the SEC and CFTC, because only Congress can rewrite agency mandates. It cannot bind a future Congress. But the registration exemption, the fundraising allowance, and the decentralization off-ramp are the provisions most builders actually care about, and the agency can deliver those alone.

There is a further irony worth naming. “Reg Crypto” is also the informal name for a capital-raising exemption in the Senate’s version of the CLARITY Act, at Section 103, which would create a new exemption under the Securities Act of 1933. The bill and the rule are converging on the same mechanism from two directions. If both landed, they would overlap. If only one lands, the industry may not notice much difference in the near term.

Why the agency route is worse than a law

The skeptical case is real and deserves its full weight, because the enthusiasm around this proposal has been running ahead of the document, which has not published yet.

Start with the obvious. If CLARITY dies, the burden of defining the rules of American crypto falls almost entirely on one agency and one set of proposed exemptions. That is a fragile foundation for a multitrillion-dollar asset class. It also concentrates enormous discretion in a single Commission whose composition changes with administrations, which is the precise problem the industry claims to be solving. Trading a hostile SEC for a friendly SEC is not the same as trading regulatory uncertainty for regulatory certainty.

The thresholds are the second problem, and they will be the fight. A $5 million startup ceiling and a $75 million annual raise sound generous until you notice they will face intense scrutiny the moment they publish. Consumer advocates will argue that a registration exemption for token sales is a re-run of the 2017 ICO boom with a compliance veneer, and they will have a decade of fraud data to cite. The exemption thresholds and the decentralization off-ramp are exactly the provisions most likely to be narrowed during the comment period, and a rule that publishes at $75 million may finalize somewhere considerably smaller.

The safe harbor is also narrower than the celebration suggests. It functions as an off-ramp, not an amnesty. Issuers remain liable for any misstatements made during the offering period, which means the exemption relieves the registration burden without relieving the antifraud exposure. And the decentralization test is inherently fact-dependent: determining that managerial efforts have genuinely ceased is a judgment call, and a judgment call made by an agency is a judgment call that a different agency can make differently.

Then there is timing. Atkins initially said Regulation Crypto would roll out in January. It is now July. The proposal sits at OIRA, and White House regulatory review is not a rubber stamp. After it publishes, a public comment period follows, then a final rule, then compliance dates. The realistic distance between the July slot and an operative rule is measured in quarters, not weeks. Anyone treating this as imminent relief has not watched a rulemaking before.

And the whole enterprise rests on institutional continuity that crypto has no reason to expect. Atkins tied the initiative directly to the President’s ambition to make America the crypto capital of the world. That is a political framing, and political framings expire.

The ghost of 2017

Any honest treatment of this proposal has to deal with the objection that will define its comment period, because it is not a bad-faith objection and the industry keeps pretending it is.

In 2017 and 2018, roughly the same idea ran without a safe harbor and without conditions. Projects sold tokens to the public on the theory that a sufficiently technical white paper made an investment contract into something else. The result was one of the largest concentrations of retail fraud in modern financial history. The SEC’s enforcement posture over the following seven years, the one the industry spent a decade complaining about, was the response to that period. Regulation Crypto proposes to permit the activity that caused it, under conditions, and the burden of showing the conditions are load-bearing sits with the agency.

The steelman for the proposal is that the conditions are meaningfully different, and they are. The 2017 model had no disclosure requirement; the fundraising exemption contemplates audited balance sheets and statements on the issuer’s financial condition. It had no notice obligation; this contemplates notices to the Commission on entry and exit. It had no time limit; the startup exemption runs up to four years and then the runway ends. It had no antifraud discipline in practice; the safe harbor explicitly preserves issuer liability for misstatements during the offering period. And it had no exit test at all, whereas the decentralization off-ramp requires the issuer to actually surrender managerial control to leave securities status, which is the opposite of the 2017 pattern where founders kept control and claimed decentralization anyway.

That last point is the strongest thing in the proposal and it deserves more attention than the dollar figures getting quoted. An objective standard for when managerial effort has ceased does two jobs at once. It gives honest projects a defined path to maturity. And it makes the dishonest claim harder, because a project that wants the off-ramp has to give up the control that made the token valuable to insiders in the first place. Structured well, the safe harbor is not a loophole. It is a filter.

Structured badly, it is a loophole. Everything depends on where the standard lands, how it is tested, and who reviews the claim, and none of those are knowable from an agenda entry. A decentralization test that a project can satisfy by dissolving a foundation and keeping the multisig is worse than no test, because it converts a factual question into a paperwork exercise and gives the resulting token a federal blessing.

Which is why the comment period is the story, not the announcement. Consumer advocates will arrive with the fraud data and argue the thresholds are too high. The industry will arrive and argue they are too low. The final rule lands somewhere between, and the number that matters is not $5 million or $75 million. It is how much control an issuer must genuinely surrender to reach the off-ramp. Watch that clause. Everything else is negotiable in a way it is not.

What the timing tells you

The most revealing thing about Regulation Crypto is not its contents. It is its position on the calendar.

The SEC scheduled its first major crypto rulemaking for the exact month in which CLARITY either passes or dies. The proposal’s scope and timing are, by several accounts, partly tied to the bill’s fate. Read that as the agency hedging. If Congress delivers, the rule harmonizes with the statute and fills gaps. If Congress fails, the rule becomes the framework, and the SEC will have spent the interval building it instead of waiting.

That is competent institutional behavior and it is also a quiet verdict on the odds. Agencies do not schedule contingency frameworks for legislation they expect to pass. Prediction markets have CLARITY’s 2026 passage in the mid-20s to upper-30s percent range. The SEC’s rulemaking calendar appears to agree with the traders.

For anyone actually trying to build in this market, the practical guidance inverts the usual advice. The bill is the loud story and the low-probability one. The rule is the quiet story and the likelier one. Watch whether the proposal clears OIRA and publishes in July as scheduled. Watch whether the decentralization off-ramp survives with an objective standard intact, because that provision does more work than any other. Watch whether the raise thresholds hold through comment. And watch the naming collision between the agency’s Reg Crypto and CLARITY’s Section 103, because if both survive, someone will spend a year reconciling them.

Seven years ago the SEC’s position was that most tokens were unregistered securities and the appropriate response was enforcement. The same agency now proposes to let founders sell them without registering. Nothing in the underlying law changed. What changed was who runs the building, which is either the strongest argument for passing CLARITY or the clearest evidence that the industry does not need it. It cannot be both, and the next three weeks decide which.

There is one more reading available, and it may be the correct one. Perhaps the choice was never between the bill and the rule. The taxonomy classified the assets in March. Regulation Crypto would govern how they are sold. CLARITY would divide who supervises the market and put both of the first two beyond the reach of the next Commission. Those are three different jobs, and only the third requires Congress. An industry that got two of them inside four months, from an agency it spent a decade litigating against, has done considerably better than its own rhetoric admits, and the remaining gap is narrower than a year of vote-counting coverage suggests.

The gap is also the only part that lasts. Rules and interpretations are the crypto industry renting its legal status from whoever holds the chairs. The rent is cheap right now and the landlord is friendly. That is a fine arrangement until it is not, and the entire argument for the bill reduces to whether anyone believes the lease gets renewed. On the evidence of the past decade, that is not a bet a serious allocator makes with someone else’s capital, which is why the quiet rulemaking and the loud bill are not substitutes at all. One of them is a good year. The other is a floor.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or legal advice. It describes a proposed rulemaking that has not yet published, and proposal terms, thresholds, and timing can change materially through White House review and public comment. Nothing here is a recommendation to buy or sell any asset or to rely on any exemption. Always do your own research. Information is accurate as of July 17, 2026.

Frequently Asked Questions

What is Regulation Crypto?

A proposed SEC rulemaking, the first major crypto-specific rule of Chairman Paul Atkins’s tenure, placed in the agency’s July 2026 rulemaking slot. It would create registration exemptions and safe harbors for certain on-chain financial activity, including a startup exemption, a larger fundraising exemption, and a safe harbor allowing tokens to exit securities classification once managerial efforts cease. DeFi and tokenized securities are named explicitly.

How much could a startup raise without registering?

Two tiers have been discussed. A startup exemption aimed at early-stage projects, described around companies valued under $5 million in their first four years, allowing raises of up to $5 million over that period. And a broader fundraising exemption permitting up to $75 million in any 12-month period, subject to conditions including audited balance sheets and notices to the Commission. Both would be non-exclusive, leaving other exemptions available.

What is the decentralization safe harbor?

A mechanism allowing a token issuer who has completed or transitioned away from centralized management of a network to have the asset exit securities classification. It applies an objective standard to the question of when a crypto asset is no longer subject to an investment contract, which matters most for secondary markets where those tokens trade. It is an off-ramp, not an amnesty: issuers remain liable for misstatements made during the offering period.

Does this replace the CLARITY Act?

Not entirely. A rule cannot divide jurisdiction between the SEC and CFTC, since only Congress can rewrite agency mandates, and it cannot bind a future Congress. But the registration exemption, the fundraising allowance, and the decentralization off-ramp are the provisions most builders care about, and the SEC can deliver those alone. Confusingly, “Reg Crypto” is also the name of a capital-raising exemption at Section 103 of the Senate’s CLARITY text.

Why is a rule more durable than current guidance?

Because of how each is undone. Staff guidance binds nobody. The March 2026 joint interpretation binds the SEC and CFTC but can be replaced by another interpretation without notice, comment, or Congress. A formal rule requires another full rulemaking to reverse, with a reasoned explanation that must survive judicial review. That procedural friction is precisely what makes a rule harder for a future Commission to unwind.

When would it take effect?

Not soon. The proposal is under review at the White House Office of Information and Regulatory Affairs. If it publishes in July as scheduled, a public comment period follows, then a final rule, then compliance dates. Atkins originally targeted January, and it slipped to July. The realistic distance to an operative rule is measured in quarters.

What are the main criticisms?

Three. That a registration exemption for token sales revives the 2017 ICO model with a compliance veneer, which advocates will argue with a decade of fraud data. That the thresholds and the off-ramp are the provisions most likely to be narrowed during comment, so the final rule may look considerably smaller. And that concentrating the rules of American crypto in one agency swaps a hostile Commission for a friendly one without delivering actual certainty.

How does this connect to the CLARITY Act’s odds?

Directly. The SEC scheduled its first major crypto rulemaking for the same month CLARITY either passes or dies, and the proposal’s scope and timing are partly tied to the bill’s fate. Agencies do not build contingency frameworks for legislation they expect to pass. Prediction markets price 2026 passage in the mid-20s to upper-30s percent range, and the rulemaking calendar appears to share that assessment.

Crypto World

Cardano News: Cardano’s Van Rossem Hard Fork Activates Tomorrow, And Whales Are Buying While Traders Go Short

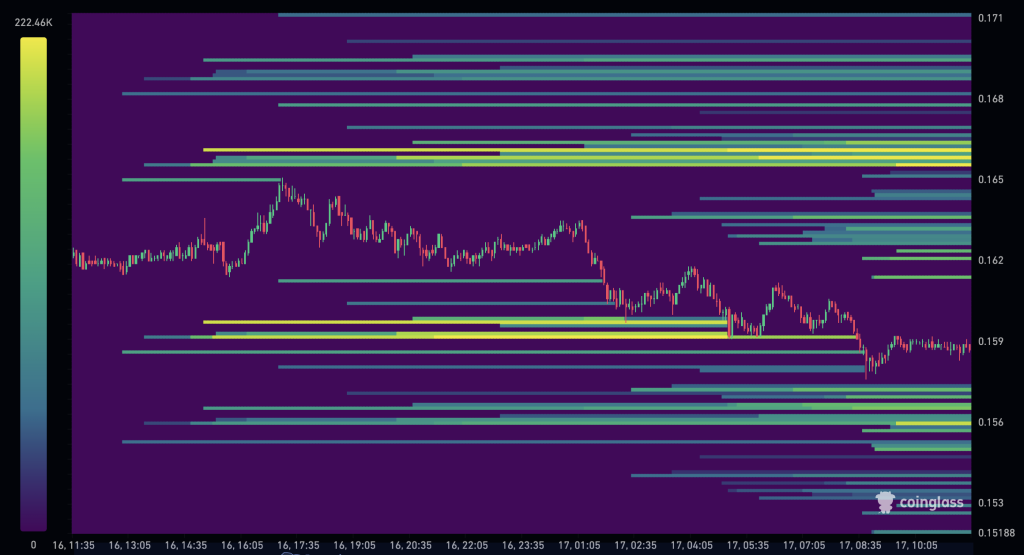

In the latest Cardano News, Cardano is trading at $0.158, down 1.39% on July 17, while derivatives traders push the long-to-short ratio to 0.58 and open interest climbs 4% to $421 million in the 48 hours before the Van Rossem hard fork activates.

The structural tension is sharp: the same wallets flooding short books are being offset by whale accumulation that has reached its highest level since 2023, creating a setup where the next directional move is likely to be violent in whichever direction it resolves.

Discover: The Best Token Presales

Cardano News: Van Rossem Governance Approval Sets July 18 Activation

The Van Rossem hard fork cleared governance on July 13, ratified by SPOs and DReps, with activation scheduled for July 18 at 21:44:51 UTC at Slot 192,844,800.

Intersect has urged all infrastructure providers to update their software before the network crosses the hard fork boundary, a standard precaution, but one that signals the upgrade is proceeding on schedule without last-minute complications.

According to some news, the upgrade is expected to lower execution costs on Cardano, making transactions and dApp operations materially cheaper to run.

More consequentially for medium-term traders, Van Rossem lays the technical groundwork for Leios, a later scaling upgrade targeting a dramatic increase in transaction throughput before the end of 2026.

That roadmap context matters: this fork is not a standalone event but a dependency in a longer delivery chain, which is part of why whale positioning ahead of it carries more weight than typical upgrade speculation.

Discover: The Best Crypto to Diversify Your Portfolio

$0.160 and $0.170 Are the Levels That Decide the Next Move

The CoinGlass three-day liquidation heatmap places the nearest dense liquidity pool between $0.160 and $0.165, sitting directly above ADA’s current market price.

A larger concentration appears around $0.167, closely matching the Murrey Math resistance at $0.1709 visible on the daily TradingView chart.

These two clusters define the near-term binary: a drop through $0.160 triggers long liquidations and opens a path toward the $0.1465 Murrey Math support; a break above $0.170 forces short sellers to close positions and hands momentum to the recovery attempt as Van Rossem goes live.

The 4-hour chart shows ADA has crossed above a descending trendline drawn from its early-July peak near $0.195, but the move failed to produce a sustained rally.

The RSI on the 4-hour sits at 46.92, below its moving average of 50.95, bearish-neutral territory, not oversold. That reading matters because it means there is no technical floor from extreme pessimism; price is simply drifting, waiting for a catalyst to define direction.

The predecessor to Van Rossem, the Vasil hard fork in September 2022, improved Cardano’s smart-contract efficiency and block utilization.

Van Rossem’s mandate is different, cost reduction and Leios preparation, but the governance process that delivered it, now running through Intersect with formal DRep and SPO ratification, represents a more mature and transparent upgrade mechanism than Cardano operated in 2022.

Whether that institutional credibility translates into sustained buying pressure post-fork, or whether short sellers use any pop to add to positions, is the question traders need an answer to before the July 18 activation window closes.

The liquidation heatmap at $0.167 is the cleanest signal: a daily close above that level removes the ambiguity. For context on how derivatives positioning and institutional vs. retail behavior interact during catalyst events, the pattern is consistent across major crypto assets; the side that controls spot supply usually wins the futures battle by attrition.

Trade ADA on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

The post Cardano News: Cardano’s Van Rossem Hard Fork Activates Tomorrow, And Whales Are Buying While Traders Go Short appeared first on Cryptonews.

Jude Bellingham posts emotional World Cup poem from England driver

Founders Fund hires former OpenAI exec Ryan Beiermeister (and not because of her ‘Mafia’ skills)

I Exposed Her Cheating On Financial Audit

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

NewsBeat19 hours ago

NewsBeat19 hours agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Crypto World1 day ago

Crypto World1 day agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Business1 day ago

Business1 day agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Politics2 days ago

Politics2 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Entertainment2 days ago

Entertainment2 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

News Videos3 days ago

News Videos3 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech3 days ago

Tech3 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Crypto World14 hours ago

Crypto World14 hours agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Tech3 days ago

Tech3 days agoDark Secrets Emerge When Jailbreaking LLMs

-

Sports2 days ago

Sports2 days agoNew Cornerback Enters Vikings Trade Rumor Mill

-

News Videos4 hours ago

News Videos4 hours agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

-

Business1 day ago

Business1 day agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

Business9 hours ago