Business

70 Days Missing as Ransom Notes, DNA Leads Stall Tucson Probe

TUCSON, Ariz. — More than 70 days after 84-year-old Nancy Guthrie vanished from her Catalina Foothills home in what authorities believe was a violent abduction, the investigation into the mother of NBC’s “Today” show co-anchor Savannah Guthrie remains active but without arrests, named suspects or confirmed sightings of the missing woman.

Guthrie was last seen on the evening of Jan. 31, 2026. She failed to appear for an online church service the next morning, prompting family members to check on her. Investigators discovered blood near the doorstep and signs of a struggle, leading Pima County Sheriff Chris Nanos to declare the case a suspected kidnapping early on. The FBI quickly joined the probe, citing the suspicious circumstances and Guthrie’s age and health conditions, including a pacemaker.

Security camera footage released by authorities showed a masked individual on the porch around the time her pacemaker lost connection with her phone shortly after 2:30 a.m. on Feb. 1, suggesting she was taken against her will and removed from the area. No clear images of a getaway vehicle or additional perpetrators have been made public.

The case has drawn intense national attention due to Savannah Guthrie’s prominent role on morning television. Savannah returned to the “Today” show anchor desk on April 6 for the first time since the disappearance, offering a brief, emotional message of resilience without directly addressing new developments. She has repeatedly pleaded publicly for information, posting videos urging anyone with knowledge to come forward and emphasizing hope and faith.

Despite extensive searches of the surrounding desert terrain, her home and a second property, no trace of Guthrie has been found. Early leads, including a glove recovered near the scene that matched one worn by the masked figure in doorbell footage, yielded DNA belonging to an unrelated restaurant worker, marking a dead end.

Pima County Sheriff Nanos has cleared all immediate family members, including Savannah and her siblings, as suspects. He has stated publicly that investigators believe they understand a possible motive — potentially financial or retribution-related — but have not identified who carried out the abduction. Forensic experts and criminal profilers, including former FBI behavioral analysts, have speculated the kidnapping could target someone in Guthrie’s orbit rather than the elderly woman herself, with one suggesting “something went very wrong” during the incident.

In recent weeks, the investigation has been complicated by anonymous ransom-style communications sent to media outlets. TMZ reported receiving multiple notes in early April demanding Bitcoin — initially half a Bitcoin (around $34,000 at the time) — in exchange for information about Guthrie’s whereabouts or the identity of those responsible. One note claimed she was dead and offered details on her body and the kidnappers; a follow-up message alleged she had been seen alive in Sonora, Mexico, roughly 70 miles south of Tucson.

Authorities and experts have not confirmed the legitimacy of the notes, with some viewing them as potential hoaxes or opportunistic attempts to exploit the high-profile case. Retired FBI agents and profilers have cautioned against taking them at face value while urging continued scrutiny. Tips to the FBI hotline have slowed significantly, though the agency maintains an active tip line and a reward of up to $100,000 for information leading to Guthrie’s recovery or the arrest of those involved.

The prolonged absence has fueled speculation about Guthrie’s health. At 84 and with medical needs, investigators and outside detectives have expressed concern that her kidnappers may have underestimated her frailty, possibly leading to an unintended fatal outcome if the abduction went awry. No confirmed ransom demand directed at the family has been reported, distinguishing this case from traditional high-profile kidnappings.

Search efforts in the initial weeks involved volunteers scouring rugged desert areas near her home, but focus has since shifted to digital forensics, analysis of potential second locations and review of activity around the residence in the weeks prior. Sheriff’s officials confirmed they are investigating suspicious incidents at Guthrie’s home three weeks before the disappearance.

Savannah Guthrie and her family have maintained a measured public presence, balancing private grief with appeals for help. On Easter, she shared a message emphasizing themes of hope, rebirth and second chances without referencing the case directly. The family has cooperated fully with investigators, according to law enforcement statements.

Criminologists note the case’s unusual elements: an elderly victim taken from a relatively secure suburban home with limited immediate witnesses, minimal public physical evidence beyond the initial scene and the involvement of a celebrity relative that has sustained media interest far longer than many similar disappearances. Experts suggest advancing DNA technology or a breakthrough tip could still resolve it, though the passage of time reduces chances of finding her alive.

As of April 12, 2026 — more than two months since she was last seen — Pima County authorities and the FBI report no major new developments but insist the case remains a top priority. No arrests have been made, and Guthrie’s whereabouts are unknown. Officials continue to ask the public for any information, no matter how small.

The disappearance has highlighted vulnerabilities for elderly residents living alone and the challenges of investigating abductions in expansive desert regions. It has also spotlighted the emotional toll on families of missing persons, with Savannah Guthrie’s visible return to work underscoring both personal strength and the ongoing uncertainty.

Anyone with information is urged to contact the FBI at 1-800-CALL-FBI or submit tips online at tips.fbi.gov. The Pima County Sheriff’s Department can also be reached at 520-351-4900.

The case of Nancy Guthrie continues to baffle investigators and captivate the public, a stark reminder that even in a connected world, some mysteries endure with no resolution in sight after 70 agonizing days.

Last week, the state-owned company announced a 1:1 bonus issue along with its Q4 results. Under the bonus issue, the insurer will allot one fully paid-up equity share of Rs 10 each for every existing fully paid-up equity share of Rs 10 each held by shareholders. The company has fixed May 29 as the record date to determine shareholder eligibility for the bonus issue.

LIC reported a consolidated net profit of Rs 23,467 crore for the fourth quarter of FY26, up 23% year-on-year (YoY) from Rs 19,039 crore posted in the corresponding quarter last year. Net premium income for the quarter rose 12% to Rs 1.65 lakh crore, compared with Rs 1.48 lakh crore in the year-ago period.

For the full financial year ended March 31, 2026, the insurer reported over 5% growth in assets under management to Rs 57.29 lakh crore, while net profit increased more than 19% YoY to Rs 57,419 crore.

It also announced a 1:1 bonus. Under the bonus issue, the insurer will allot one fully paid-up equity share of Rs 10 each for every existing fully paid-up equity share of Rs 10 each held by shareholders. The company has fixed May 29 as the record date to determine shareholder eligibility for the bonus issue.

LIC shares: Buy, sell or hold?

Citigroup maintained a ‘Buy’ rating on LIC with a target price of Rs 1,475 per share, an upside potential of more than 81% from the stock’s previous closing price of Rs 813 on the BSE. According to Citi, the improvement in numbers was driven by a better non-par product mix and favourable yield curve benefits in the fast-growing non-par business. The brokerage also noted that management highlighted initiatives to improve persistency, boost product innovation, enhance agent productivity, expand the agent network, and increase contributions from non-agency distribution channels.

Citi added that LIC’s valuation remains attractive, with projected FY27 core embedded value, excluding mark-to-market embedded value, exceeding the company’s current market capitalisation. However, it said uncertainty around the promoter-holding structure continues to weigh on the stock.Bernstein retained a ‘Market Perform’ rating with a target price of Rs 900 per share, implying an upside potential of over 11%. The brokerage said LIC reported healthy revenue growth during the quarter, with new sales rising 22% in Q4 and 18% year-on-year in FY26, led by strong growth in non-par products. Bernstein added that margins continued to improve through FY26 due to a favourable shift in product mix and supportive yield curve movements.

The brokerage also said LIC’s management expects margins to gradually converge with private-sector peers over the medium term, although the transition is likely to take time.

JM Financial maintained its ‘Buy’ rating on LIC and raised its target price to Rs 960 per share, implying an upside of 18%. The brokerage said it had upgraded the stock after Q1FY26, expecting a rerating in the second half of the year.

According to JM Financial, LIC’s diversifying product mix and improving margins strengthen growth resilience. It noted that the stock remained range-bound as weak equity markets kept embedded value below September 2024 levels.

However, the brokerage expects embedded value growth to improve as macroeconomic conditions stabilise, supported by improving business growth, an unwind of over 9%, and VNB at 2% of opening embedded value. JM Financial also upgraded its earnings estimates for the insurer.

The stock has gained 2% over the past month but is down 7% over the last six months. The company’s market capitalisation currently stands at Rs 5.27 lakh crore.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

In a claim that will resonate with thousands of school-leavers wading through a torrent of rejection emails this summer, the skills minister has declared that securing a coveted apprenticeship in Britain has become harder than winning a place at Oxford or Cambridge.

Baroness Smith of Malvern, the former Commons home secretary turned Strictly Come Dancing contestant who now holds the skills brief at the Department for Education, told The Sun on Sunday that young people the length of the country were “queuing up” for apprenticeships, with employers spoilt for choice. Her remarks landed as Whitehall figures laid bare a deepening youth labour crunch: roughly one million people aged between 16 and 24 are now classed as Neets – not in education, employment or training.

The numbers behind the soundbite

The arithmetic appears, on the face of it, to back her up. Cambridge received 22,820 applications for the 2025 intake and offered 3,716 places, an acceptance rate of 16.3 per cent. Oxford was tighter still, admitting just 3,245 of 23,061 hopefuls, 14.1 per cent. By comparison, several blue-chip apprenticeship schemes, especially degree-level engineering programmes, routinely attract north of 150 applications per slot, eclipsing the odds at the dreaming spires.

According to the latest Department for Education apprenticeship statistics, there were 353,500 apprenticeship starts in England in the 2024-25 academic year and 761,500 people participating overall, with higher-level apprenticeships up more than 15 per cent year-on-year. Business, administration and law remains the largest single subject area.

To unblock the bottleneck, Lady Smith pledged £600 million of new funding to bankroll 60,000 additional apprentices, part of a broader push to plug skills gaps in construction, engineering and digital roles. “It can sometimes be easier getting into Oxford or Cambridge than it can be getting an apprenticeship,” she said, adding: “Sometimes people say, ‘Young people don’t want to work in the construction industry’, but they really do… they are queuing up.”

Why employers are hesitating

The pledge nonetheless lands awkwardly for the small and medium-sized businesses that have historically done the heavy lifting on apprentice intake. Industry data suggest just one in five construction SMEs is planning to take on an apprentice this year, and employers’ groups argue that the Chancellor’s autumn measures, chiefly the rise in employer National Insurance contributions from 13.8 to 15 per cent in Rachel Reeves’s first Budget, have left many smaller firms re-running the numbers on every new hire.

The minimum wage settlement that took effect in April only sharpened the squeeze. The apprentice rate climbed 6 per cent to £8 an hour; the 18-to-20 band rose 8.5 per cent to £10.85; and the National Living Wage for over-21s reached £12.71. As Business Matters has previously reported, the combined effect has been to push employer costs for low-paid staff up by more than £2,100 per employee, a sum that, for owner-managers in hospitality, retail and care, has made hiring under-25s, in the words of one trade body, “unaffordable” without external support.

A political squeeze tightens

The minister’s timing reflects a Treasury under mounting pressure to demonstrate that ministers can convert announcement into appointment. The latest Office for National Statistics NEET bulletin put the share of 16-to-24-year-olds out of work and study at 12.8 per cent, equivalent to 957,000 young people, with the next release due at the end of May.

Industry watchers will be looking for evidence that the policy mix is starting to shift the dial. With youth unemployment hovering near an 11-year high and employers warning that wage and tax bills are leaving little headroom to expand junior intake, the £600 million pledge will need to translate into hard cash on the ground, not merely a press notice, if Westminster is to ease the bottleneck that, on the minister’s own admission, is leaving Britain’s school-leavers fighting harder for an apprenticeship than for a place at the country’s most selective universities.

For SMEs, the calculation is unchanged: the talent is willing, and arguably abundant. The question is whether the policy framework finally makes saying yes affordable.

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

OPINION: As the naming rights deal at Perth’s iconic stadium nears its end, it’s worth considering how corporates gauge value from the commitment.

Chinese chipmaking stocks rally on Huawei chip design breakthrough

Welcome to the home of The Cannabis Report. I cover the cannabis sector and other sectors. I am most interested in technical stock analysis, option strategies, small cap strategies, and emerging markets. Feel free to contact me with any questions about publicly traded stocks in the cannabis industry.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of CURLF either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Australia’s spy chief says antisemitism was left unchecked after Gaza war

SAN ANTONIO — Victor Wembanyama delivered a highlight-reel moment during the 2026 Western Conference Finals, launching a deep shot that drew widespread reaction across social media and NBA broadcasts.

The San Antonio Spurs star’s play, captured in a widely shared NBA YouTube Short titled “VICTOR WEMBANYAMA OH MY GOODNESS 😱,” showed him connecting from well beyond the three-point line. Commentators and fans reacted immediately to the long-range attempt.

One social media comment read, “From way down town… BANG!!! BANG!!!” Another user wrote, “This was crazy.” A third said, “That’s crazy shot 👽.” Multiple viewers called it “W😊” and referenced “SPURS IN 6.”

The clip, posted by the official NBA channel, has accumulated thousands of views and comments shortly after the game.

Game Context

Wembanyama has been a central figure in the Spurs’ playoff run. In Game 3 against the Oklahoma City Thunder, he scored 26 points on efficient shooting while adding rebounds, assists and blocks. The Spurs trail the series 2-1 heading into Game 4 on May 24 at Frost Bank Center.

The Thunder overcame an early 15-0 deficit in Game 3 to win 123-108, powered by a playoff-record 76 points from their bench. Shai Gilgeous-Alexander led Oklahoma City with 26 points and 12 assists.

Wembanyama’s Season

The 22-year-old has emerged as one of the NBA’s most dominant young players. His combination of size, skill and shooting range has drawn comparisons to historical greats. Wembanyama’s ability to stretch the floor with deep shots has become a key part of the Spurs’ offensive strategy.

In the regular season, he earned Defensive Player of the Year honors and continued to develop his offensive game. His performance in the playoffs has showcased both scoring and playmaking growth.

Series Outlook

The Western Conference Finals pits two young, talented teams against each other. Oklahoma City, the defending champions, have utilized depth and defensive versatility. San Antonio has relied heavily on Wembanyama’s versatility despite injuries to key guards like Dylan Harper.

Game 4 represents a critical juncture for the Spurs. A win would tie the series at 2-2. The Thunder aim to take a commanding 3-1 lead.

Broadcast and Fan Reaction

The NBA YouTube Short highlighting Wembanyama’s shot quickly circulated. Fans praised the play’s difficulty and Wembanyama’s confidence in attempting it during a high-stakes playoff game.

The moment added to the growing highlight reel for the 2026 postseason. Wembanyama’s ability to make such plays has contributed to increased attention on the Spurs’ playoff run.

League-Wide Impact

Wembanyama’s development has been a major storyline in the NBA. His presence has elevated the Spurs’ competitiveness and drawn national interest to San Antonio. The Western Conference Finals matchup between the Thunder and Spurs features two of the league’s brightest young stars in Wembanyama and Shai Gilgeous-Alexander.

Historical Comparisons

Wembanyama’s long-range shooting ability has been compared to previous big men who stretched the floor. His impact on both ends of the court has made him a focal point for opposing defenses throughout the series.

The Spurs continue to build around their young core. Wembanyama’s growth remains central to the franchise’s future plans.

AoZaaStudio/iStock via Getty Images

Make “Long-Term” Great Again

At a recent investment conference, we made some baseball caps that bashfully shouted on the front: ‘ Make “Long-Term” Great Again ’. This was our brief dalliance with Trumpian ‘merch’ culture, mercifully without the red caps, rallies, or promise of instant results. Its purpose was to be an icebreaker, but at its heart, a statement of principle.

Meanwhile, another attendee at one of the snack tables had a similar idea and wore a cap that said: “Make Volatility Great Again. ” We guessed that he was working for a brokerage firm.

We can already feel your scepticism. “Long-term” is one of the oldest cards in the fund manager’s deck, usually pulled from the inside pocket as soon as performance goes awry. Sometimes it’s a philosophy; sometimes it’s just a way to launder underperformance.

We hope that by the end of this letter, you will believe that our intention was the former.

What Has Been Going On?

This was the second negative quarter since 2022 for the SaltLight BCI Worldwide Flexible Fund. Over the last six months, we have been deliberately harvesting profits in parts of the portfolio, particularly in AI infrastructure, and reallocating capital to better expected-value opportunities.

As fate would have it, at the same time we have experienced meaningful declines in companies such as Blu Label Unlimited, Sea Ltd (SE), and MercadoLibre. We think this sell-off has been an absolute gift, especially with a little cash on hand. In the short term, for these companies, the market has decided that we are either wrong or. . . early. For a time, those two things could look identical.

Back in the US, fast capital has flowed into what we would opine are mediocre AI infrastructure businesses, with revenue surges driven by short-term AI bottlenecks. Time will tell if great businesses are born from these shortages, but our job is not to chase every price move. We must distinguish between temporary scarcity and focus our attention on enduring advantage.

What Is the Game that SaltLight is Playing

The most important question about an investment manager is not what they own today or what they think will happen next quarter. It is what game they are playing.

Some managers play the very difficult event game . They try to predict quarterly earnings, elections, wars, tariffs, interest rates, currencies, and the next macro surprise.

Others play the safer benchmark game : stay close enough to the index to avoid embarrassment, but far away enough to justify a fee.

Meanwhile, SaltLight is trying to play a different game: the waiting-and-building game. . . And at times, despite our best intentions, it can become a building-and-waiting game.

S-Curves: Do Shareholders Have What It Takes?

When we communicate to potential investors what we plan to do with their hard-earned capital, our goal is to convey a fairly simple idea that is hard to execute.

We are curating a portfolio of exceptional global businesses that can become materially more valuable over many years by adapting, innovating, serving customers better, expanding their opportunity set, and reinvesting intelligently.

What *Should* Happen

Ideally, the best of these companies does not rely on a single product, a single market, or a short growth curve. They stack new S-curves on top of existing ones and press their differential and durable advantages. Yet few second-, third-, or tenth-act businesses succeed. Almost all companies fail to build the “next thing”, and so market participants tend to shoot first and ask questions later.

Why Do ‘Long-Term’ and ‘Great’ Not Happen?

1) Culture

Most businesses lack the culture of innovation and management ambition required to invest in a future not yet visible in this quarter’s numbers. Pair that institutional timidity with the incentive structure of a hired CEO on a five-year contract: protect current margins, defer tomorrow’s opportunity, collect the bonus, and let someone else explain the missing growth. Before long, Long-Term and Great are no longer guiding principles. They survive as corporate folklore, stories told about a company that once knew how to build.

2) Shareholders and Investment Industry

Here the lunacy reaches its full bloom. Shareholders say they want growth. They wail and gnash their teeth at the cost of producing it. Their pressure flows downhill from clients, consultants, ratings tables, quarterly league tables, and the endless industry of measurement that surrounds them. The result is a negative feedback loop of mutually reinforcing mediocrity, in which managers stop investing in the future, and shareholders later wonder where greatness disappeared.

3) Accounting in the Technology Age

Another quirk is accounting. In the industrial era, if a company built a factory to support growth, the cost was capitalised and then depreciated over many years through the income statement.

Technology businesses are different. Building a consumer habit, subsidising logistics, hiring engineers, or acquiring customers often hits the income statement immediately. Long-term investment is often conflated with an “expense” and can easily be mistaken for deteriorating economics.

How Have We Found Success Over the Years? How Do We Wake Up ‘Long Term’ and ‘Great’ Again?

But a treasured few companies get Long-Term right; and when they do, they generate incredible value for shareholders. NVIDIA (NVDA), AppLovin (APP), Sea Ltd, and Blu Label have materially grown our capital. One pattern is that, more often than not, companies run by founders tend to have a different license to operate than those run by hired guns do.

Part of the reason we chose the harder path of building SaltLight from scratch a decade ago was shaped by our own experience as entrepreneurs. We wanted to be a different kind of shareholder. We project ourselves sitting on the same side of the table as the builders in our portfolio companies. We make a concerted effort to understand their ambition behind their investments, judge whether the opportunity is real, and back those with the courage, competence, and staying power to build what comes next.

A Portfolio of Builders

Back to what has been going on with our portfolio. Over the last six months, we have deliberately reoriented the portfolio toward a quasi-building mode again. By our estimate, roughly 46% of the portfolio’s exposure is in businesses that are either already undertaking or about to enter a multi-year investment cycle . We have chosen the lonely path to Long-Term martyrdom. It is likely to be choppy, but this is how we play our part in making Long-Term Great again.

Before you flee to the comforting arms of near-term certainty, in this letter, we want to walk through how several of our portfolio companies are investing for the future. MercadoLibre is building the financial ecosystem for Latin America. Tencent (TCEHY) is building AI services on top of one of the world’s most valuable consumer and enterprise ecosystems. AppLovin is extending its advertising engine across more than one billion users. WeBuyCars is building a national scale in South Africa’s fragmented second-hand vehicle market.

Let’s delve into the details on MercadoLibre that demonstrate our thinking and where we differ from the market.

MercadoLibre – Torne o Longo Prazo Grande Novamente ¹

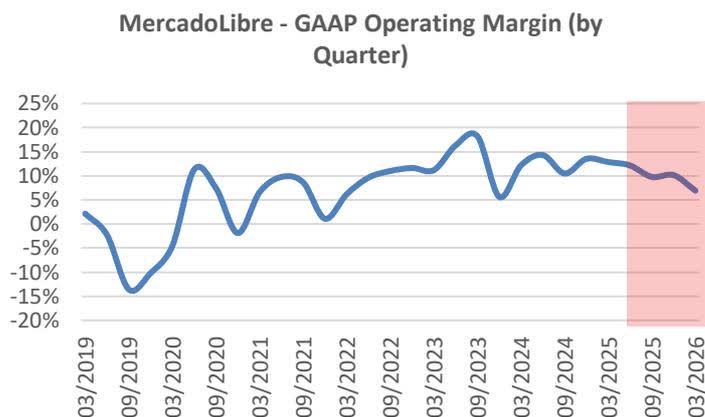

MercadoLibre (MELI) has recently made several decisions that have put pressure on short-term margins. History shows that MELI has gone through this investment cycle before and emerged significantly stronger as a result. We think that the market reaction misses some key points. It has (1) lowered free-shipping thresholds, (2) expanded its credit card offering, and (3) pushed further into cross-border commerce. Investors, without mincing words, have punished its share price.

Figure 1- Source: Company (red is when shipping threshold was reduced)

Lowering Free Shipping Thresholds

The last time MELI cut free-shipping thresholds by a mere 20%, commerce revenues subsequently increased 3.3x over the following years. In a network-effect business like 3P e-commerce, this creates multiple layers of opportunity. The first-order benefit is that more buyers attract more sellers due to the larger customer base. The second-order benefits are the more profitable ones: MELI sells more high-margin advertising and financial services to both sides of the network.

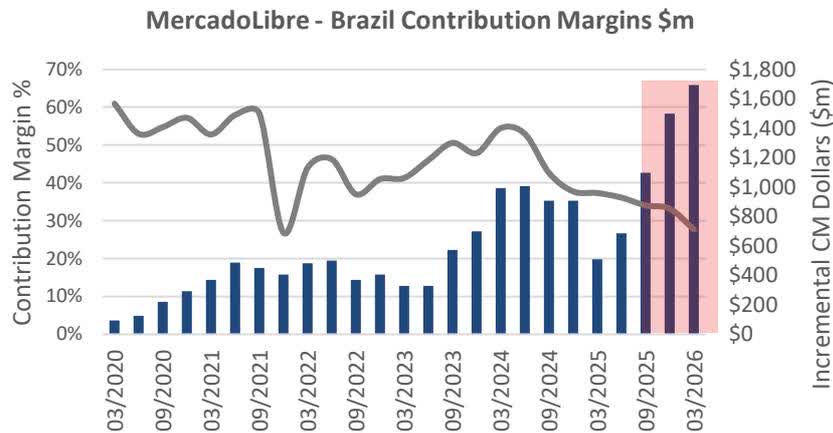

The 2025 Brazil threshold reduction is far more aggressive (~75%) and has resulted in a halving of contribution margins in the last year. But we already see early signs of a substantial increase in contribution margin dollars in the graph below ² .

Figure 2 – Source: Company (red is when shipping threshold was reduced)

Now, investors tend to focus too much on margin percentages rather than on incremental margin dollars. The truth is that we do not mind lower margin percentages when margin dollars increase, provided that fixed capital investments, such as logistics, are leveraged. Jeff Bezos understood this dynamic well when building Amazon (AMZN)’s unassailable position, because the other side of the equation is that a competitor must operate at similar gross margins, resulting in much smaller gross profit dollars – but at a lower scale. The most-scaled player (MELI, in this case) is usually the winner in the long term. We think this will play out again.

Building a Latam Consumer Bank

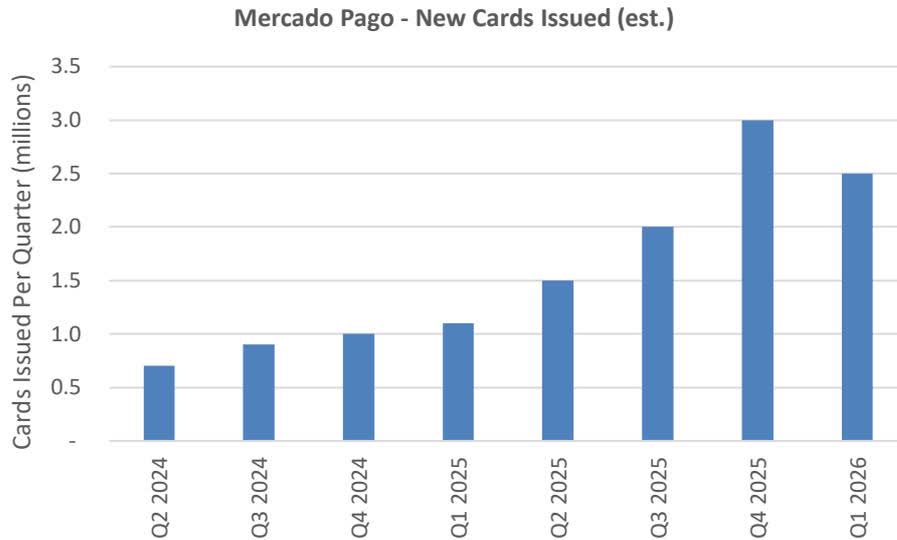

The second initiative is MELI’s rapidly expanding credit card portfolio. Over the years, MELI initially focused on short-duration loans for the underbanked. More recently, it has moved upmarket, serving a higher-quality middle-income customer base and steadily laying the foundations for a broader Latin American bank.

Fast-growing loan books are a double-edged sword. When any loan is extended, MELI (or any bank in that manner) prudently recognises an upfront provision for expected credit losses rather than waiting for the default to occur. Faster growth, therefore, mechanically creates higher upfront provisions which hit the income statement immediately. With the credit book growing at roughly 87% YoY ³ , this depresses current reported profitability.

Mercado Pago – New Cards Issued ((est. ))

The obvious risk is that the book proves to be of poor credit quality and today’s growth becomes tomorrow’s credit problem. That is the right question to ask. However, based on our analysis today, provisioning appears adequate.

Cross-Border Trade

The third initiative is cross-border trade, which links MELI’s consumers directly to Chinese and US suppliers. We think this is another S-curve that demonstrates the strength and optionality of the MercadoLibre ecosystem.

Consider the challenge from a supplier’s perspective. A Chinese manufacturer trying to sell into Brazil, Mexico, Argentina, or Chile faces a market on the other side of the world, with different languages, payment systems, logistics infrastructure, tax regimes, customer service expectations, and returns processes.

That is a hard problem to solve alone, and so MercadoLibre is turning those multiple friction points into a product. Borrowing from models pioneered by companies such as Pinduoduo (PDD), it now offers semi-managed and fully-managed cross-border solutions. In the semi-managed model, the supplier can drop product into a MercadoLibre warehouse in China. In the fully-managed model, MercadoLibre can handle pricing, shipping, marketing, and customer fulfilment on behalf of the supplier.

This is the pattern we like to see, where it leverages existing infrastructure (an investment cycle from a decade ago) to attack adjacent opportunities. Logistics, payments, credit, advertising, and merchant services are not separate businesses bolted on. They are mutually reinforcing layers of the same ecosystem.

That is why we are less concerned by near-term margin pressure than the market appears to be. MercadoLibre is not simply spending to defend its current business. It is investing to make the next version of the business larger, harder to replicate, and more valuable.

So, where else in our portfolio are companies going into ‘building mode’?

Tencent: Sacrificing 4.5 percentage points of operating margin to invest in new AI initiatives that sit atop one of the most formidable distribution systems in China.

We Buy Cars: Increased its footprint by 23% over the last two years. The investment is impacting margins and free cash flow today, but if returns on capital follow previous locations, we anticipate a substantial earnings lift next year as these new locations mature.

Roblox (RBLX): Took the difficult but welcome decision to improve age identification using AI. Predictably, bookings have suffered, but we believe this will vastly improve network effects and safety for all users.

Karooooo (KARO): has invested significantly in its sales organisation to accelerate its business in South-East Asia. Cartrack has one of the most enviable unit economics in the sector and is unlikely to be disrupted by AI.

Blu Label Unlimited (BLU): Restructuring and simplification are ongoing, and we anticipate this process will take about 18 more months. We remain hopeful for a repurchase announcement with the 2H26 results. Additionally, BLU plans to launch a unified voucher within the next six months, which will significantly change the company’s working capital dynamics.

2022 Vintage

2022 was an exceptionally tough year for us, and yet it was the most fruitful time to deploy capital. That sounds odd, but it is often how long-term investing works. The best sowing rarely feels good at the time. It happens when prices are falling, confidence is scarce, and the temptation to optimise for reported comfort is strongest.

Since then, market participants have had to contend with sharply higher interest rates, the Russia-Ukraine war, Trump 2.0, tariffs, China decoupling, and now the war in Iran. The headlines have not lacked for drama.

The more important question is: what did the companies do?

A few examples from that 2022 vintage:

- • SEA Ltd: emerged from the post-2021 reset as the leading e-commerce platform in Southeast Asia. Revenue grew roughly 80% from 2022 to 2025, while net profit moved from a loss of $1.6 billion to a profit of $2.2 billion.

- • AppLovin: positioned itself as a serious force in performance advertising, increasingly competing in a market long dominated by Google (GOOGL) and Meta (META). Revenue grew 104% from 2022 to 2025, while net profit moved from a loss of $0.2 billion to a profit of $3.6 billion.

- • Pinduoduo: built Temu into a global e-commerce platform, demonstrating an extraordinary ability to adapt, scale and compete internationally. Revenue grew 231% from 2022 to 2025, while net profit rose from $4.5 billion to $16 billion.

- • NVIDIA became the de facto compute provider for the AI epoch. What the market once largely treated as a gaming hardware company became the world’s largest company by market cap. Revenue grew 380% from 2022 to 2025, while net profit increased from $10 billion to $73 billion.

The common thread is that these companies had to go through an investment cycle, and the market hated it. Their management teams played the right game. They invested, adapted, endured, and compounded through a period when the market was far more interested in near-term discomfort than long-term potential.

Over time, investment returns are ultimately driven by revenue growth, earnings growth, and the durability of the opportunity set. Narratives matter in the short run. Fundamentals matter in the end.

In aggregate, we believe our portfolio of builders is now available at attractive valuations. Individually, they are not all the same bet. They have different risks, different time horizons, and different failure modes. Some will work, and a few, where we are wrong, will not.

But this is the game we are playing.

Let’s Make “Long-Term” Great Again! (Thank you for your attention to this matter).

Once again, we remind co-investors that our personal and family wealth is in the very same funds as yours. We inherently have a multi-decade perspective on how to grow our capital alongside yours.

P. S. The SaltLight Global Opportunity Fund , our USD-denominated global portfolio, is now operational and is approved under section 65 of the Collective Investment Schemes Control Act, 2002, for solicitation of South African investors. Please reach out if you are interested in learning more*.

David Eborall

Portfolio Manager

References

- 1 Translated as Make Investing Great Again in Portuguese

- 2 MercadoLibre introduced the reduce shipping threshold from R$80 to $19 in June 2025.

- 3 Company: Net loan book growth at 1Q26

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

John Scott

Executive Chair

Good morning, guys. My name is John Scott. I’m the Executive Chair of EROAD. Welcome you to the EROAD financial results for the financial year 2026. With me, I have Ciara, our CFO; and Ryan, our Chief Transformation Officer. So we’ll get into it.

So today, we’ve got about 30 minutes of us talking and hopefully 15 minutes of you guys asking questions, and we’ll try and get you back to your day in about 45 minutes. So in a slightly unusual term, we’ll start a financial report with an overview of all of the strategy. The reason we’re doing this is because of just how much of this is actually has our financials, and it’s important for you to understand. So I took over or joined the company in March, and I took over as Executive Chair in October. Over the 8 months, I’ve got to meet a lot of our customers and realize what just a wonderful little business we have here. We have unbelievable product market fit in New Zealand, a really, really easy-to-understand value proposition. But the thing I’ve learned most of all is you have to talk about our business by country because the dynamics are completely different. You’ll see there across the top, the revenue has been stable. We’ve undertaken a whole bunch of initiatives to get back to basics and Ryan will talk to them. We’re clearly focused on the Australia and New Zealand region. We have this back to basics or customer-focused program around just restoring our key metrics. And — there is a headline which a lot of people joined during the year for EROAD, which is the eRUC opportunity. And we just want to sort of signal that it’s a significant opportunity, but

Australia’s spy agency had noted the prospect of terror attacks carried out by lone actors with readily acquired weapons after an anti-Semitic attack in the UK.

Huawei unveils new smartphone chips this fall as rivalry with Nvidia and Apple heats up

Makar can’t spark reeling Avalanche in Game 3 loss to Golden Knights

HP Discount Codes: 60% Off May 2026

![TORINO & PASHATA - OLD MONEY [OFFICIAL 4K VIDEO]](https://wordupnews.com/wp-content/uploads/2026/05/1779687619_maxresdefault-80x80.jpg)

-

Crypto World3 days ago

Crypto World3 days agoBlockchain.com files with SEC for U.S. IPO

-

Fashion2 days ago

Fashion2 days agoHoliday Weekend Open Thread – Corporette.com

-

Crypto World3 days ago

Crypto World3 days agoBitcoin Accumulation Weakens as BTC Realized Losses Hit $600M

-

Business3 days ago

Business3 days agoDell Technologies DELL Stock Surges 15% on AI Server Momentum and Analyst Upgrades in 2026

-

Crypto World3 days ago

Crypto World3 days agoSpace X IPO Is ‘Bad News’ for Tech Stocks: But What About Bitcoin?

-

Politics2 days ago

Politics2 days agoMakerfield: a tale of two social-media histories

-

Crypto World3 days ago

Crypto World3 days agoMicroStrategy’s Saylor Says Miners No Longer Set Bitcoin Price, Another Force Has Taken Over

-

Crypto World2 days ago

Crypto World2 days agoRobinhood crypto COO Tanya Denisova exits

-

Business12 hours ago

Business12 hours agoNYT Strands Answers May 24 2026 Revealed for Puzzle No. 812 Theme Summer Essentials

-

Tech3 days ago

Tech3 days agoWhatsApp ads could make Irish debut after discussions with DPC

-

Tech3 days ago

Tech3 days agoA 0.12% parameter add-on gives AI agents the working memory RAG can’t

-

Crypto World3 days ago

Crypto World3 days agoAI infrastructure race heats up as IREN pitches full-stack strategy, WhiteFiber lands $160M deal

-

Business3 days ago

Business3 days agoTrump Invests $1M-$5M in Kura Sushi USA Chain With 27 California Locations

-

Tech3 days ago

Tech3 days agoYou Can Now Add ChatGPT To PowerPoint

-

Crypto World6 days ago

Crypto World6 days agoRevolut Launches Dogecoin Debit Card Across UK and EU

-

NewsBeat4 days ago

NewsBeat4 days agoCharity run by Reform leader Malcolm Offord accused of ‘law breaking’ over Scottish registration

-

Sports3 days ago

Sports3 days ago2026 CJ Cup Byron Nelson leaderboard: Brooks Koepka finds putting stroke in Round 1

-

Crypto World3 days ago

Crypto World3 days agoTrump Media’s Bitcoin Stash Shrinks Again as 2,650 BTC Lands on Crypto.com

-

Business3 days ago

Goldman Sachs reinstates Ageas stock coverage with neutral rating

-

Crypto World4 days ago

Crypto World4 days agoExa Labs raises $250 million in funding led by a16z

You must be logged in to post a comment Login