Business

Buy or Sell Navitas Semiconductor Stock in 2026? Analysts Split Amid AI Power Boom

TORRANCE, Calif. — Navitas Semiconductor Corp. shares have delivered explosive gains in 2026, surging hundreds of percent on enthusiasm for its gallium nitride and silicon carbide chips powering artificial intelligence data centers, yet Wall Street analysts remain divided on whether the stock is a buy, hold or sell at current elevated levels.

As of April 21, Navitas (NASDAQ: NVTS) traded near $15-16 after a sharp early-session rally, extending a remarkable run that has seen the stock climb more than 400% over the past year. The rally reflects investor bets on the company’s “Navitas 2.0” strategy, which shifts focus from lower-margin mobile charging to high-power applications in AI infrastructure, grid modernization and industrial electrification. Yet with the stock trading at a premium valuation and analysts’ average price targets well below current levels, the question of whether to buy or sell Navitas in 2026 elicits no consensus.

Navitas specializes in next-generation power semiconductors that offer superior efficiency, smaller size and better thermal performance than traditional silicon devices. Its GaNFast power ICs and GeneSiC SiC solutions address a critical bottleneck in AI data centers, where massive electricity consumption makes even modest efficiency gains highly valuable. The company estimates a $3.5 billion serviceable addressable market in high-power segments by 2030, with AI-related demand as the primary driver.

The strategic pivot has shown early progress. High-power applications now exceed 50% of revenue, while mobile has fallen below 25%. Management guided for a return to sequential revenue growth starting in the first quarter of 2026, with Q1 results scheduled for release after market close on May 5. Fourth-quarter 2025 revenue beat expectations at $7.3 million, and the company ended the year with a strong cash position and no debt, providing runway for continued investment.

Recent catalysts have fueled the rally. In March, Navitas launched new 1200V SiC MOSFET packages optimized for AI servers and energy infrastructure. At NVIDIA’s GTC 2026 conference in April, the company demonstrated an 800V-to-6V GaNFast power delivery board for the MGX platform and a high-efficiency 10kW all-GaN solution. On April 13, the appointment of semiconductor veteran Gregory M. Fischer to the board added governance credibility as Navitas scales operations.

Despite the momentum, risks abound. Navitas remains unprofitable, posting adjusted losses as it invests heavily in growth. Analysts project continued revenue pressure in 2026 due to the business mix transition, with some forecasting declines before a sharp rebound in 2027. Consensus ratings lean toward Hold, with an average 12-month price target around $6.78 to $7.60 — implying significant downside from current levels near $15-16. Targets range from as low as $3.50 to a high of $13.00.

The valuation debate centers on execution versus potential. Bulls highlight Navitas’ technological edge, patent portfolio and alignment with the AI megatrend. Successful conversion of design wins into volume shipments could drive meaningful revenue inflection starting late 2026 or 2027. Optimists see the stock as a long-term winner for patient investors willing to endure near-term volatility and margin pressure.

Bears counter that the current price already bakes in substantial optimism. With a high price-to-sales multiple and no near-term profitability in sight, any delay in AI-related ramps or margin improvement could trigger sharp pullbacks. Competition in the GaN and SiC spaces is intensifying from larger players, and broader semiconductor cyclicality adds another layer of risk. Some forecasts suggest the stock could trade in a range between roughly $3 and $9 through the end of 2026 under conservative scenarios.

Q1 2026 earnings on May 5 will provide the next major test. Investors will scrutinize revenue trends, gross margin progress, operating expenses and any updates on design-win conversions or AI customer engagements. Management has emphasized gradual improvements in gross margins and bottom-line results alongside renewed top-line growth. Positive surprises could sustain momentum; misses or cautious guidance might cool enthusiasm.

Broader market context also matters. Enthusiasm for AI infrastructure stocks has lifted many names in the semiconductor supply chain, but elevated valuations leave limited room for error. Geopolitical tensions, interest rate movements and energy costs could indirectly influence demand for efficient power solutions.

For individual investors, the decision hinges on time horizon and risk tolerance. Long-term believers in the AI power story may view dips as buying opportunities, especially given Navitas’ strong cash position and debt-free balance sheet. Shorter-term traders might prefer to wait for clearer signals of profitability or revenue acceleration before committing capital at current levels.

Technical indicators show strong momentum in recent sessions, with the stock breaking out on high volume. However, overbought readings suggest potential for near-term consolidation or pullbacks. Options activity reflects elevated implied volatility, consistent with expectations for significant moves around earnings.

Navitas operates with a lean team of roughly 190 employees and benefits from strategic foundry partnerships, including efforts to expand U.S.-based manufacturing. Its CarbonNeutral certification and focus on sustainability add to the appeal for ESG-minded investors. Yet as a smaller player, it faces execution risks in scaling production to meet potential hyperscaler demand.

The company’s long-term roadmap targets compound annual growth exceeding 60% in its addressable market. If Navitas captures even a modest share while improving margins, the upside could be substantial. Conversely, prolonged transition challenges or competitive pressures could weigh on the stock for an extended period.

As April 21 trading continued with strong gains, the narrative around Navitas remained one of high risk and high reward. The stock’s dramatic 2026 performance has rewarded early believers but also attracted profit-taking and skepticism from valuation-focused investors.

Ultimately, whether to buy or sell Navitas Semiconductor in 2026 depends on individual conviction in the AI infrastructure thesis and tolerance for volatility. Wall Street’s Hold consensus and low average price targets suggest caution at current prices, but bullish voices see the potential for outperformance if execution aligns with ambitious goals.

With Q1 results approaching and the AI buildout accelerating, the coming months will offer fresh data points to assess whether Navitas can translate technological promise into sustainable financial results. Investors should weigh the compelling long-term story against near-term transitional pressures before making portfolio decisions.

AUSTIN, Texas — Elon Musk offered a simple yet powerful affirmation Friday, replying “True” to a viral X post declaring that “the most important thing in life is having true friends,” accompanied by a photo of the Tesla and SpaceX CEO alongside NVIDIA’s Jensen Huang. The understated response quickly exploded online, amassing millions of views and sparking widespread discussion about friendship, loyalty and the human side of high-stakes tech leadership.

The original post by popular X account @cb_doge featured an image of Musk and Huang together in a relaxed, friendly moment, likely captured during their recent high-profile trip to China aboard Air Force One with President Donald Trump. The duo, both titans of the artificial intelligence and semiconductor worlds, have forged a close professional and personal bond over years of collaboration on cutting-edge technology. Musk’s two-word reply resonated instantly, striking a chord with users who saw it as a rare glimpse of vulnerability and warmth from one of the world’s most polarizing billionaires.

Within hours, the post and Musk’s reply generated more than 15 million views, 150,000 likes and thousands of reposts and replies. Users flooded the thread with their own stories of friendship, memes celebrating the tech leaders’ camaraderie and heartfelt messages about the value of genuine relationships in an often cutthroat industry.

Recent Trip to China Highlights Bond

The photo appears to stem from the May 13-14 Trump-Xi summit in Beijing, where Musk, Huang and other U.S. tech executives joined the presidential delegation to discuss trade, AI and semiconductor cooperation. Images and videos from the trip showed Musk and Huang traveling together on Air Force One, engaging in candid conversations and even sharing lighthearted moments at official events.

Musk has publicly praised Huang in the past, crediting NVIDIA’s early support for Tesla’s autonomous driving efforts and highlighting their shared vision for AI advancement. Huang, in turn, has described Musk as a visionary who believed in NVIDIA’s technology when few others did. Their partnership has deepened as both companies push the boundaries of AI infrastructure, with Tesla relying heavily on NVIDIA chips for its Dojo supercomputers and autonomous vehicle development.

The China trip itself drew significant attention, with Musk and Huang among the high-profile business leaders accompanying Trump. Photos of the group at the Great Hall of the People, including Musk performing his signature “photo-spin” for cameras, underscored the blend of diplomacy, business and personal rapport.

Friendship in the Tech World

Musk’s affirmation of true friendship comes at a time when the tech industry is often criticized for cutthroat competition, intense rivalries and fleeting alliances. Observers noted the post humanizes Musk, who frequently faces scrutiny over his public persona, work habits and controversial statements. Many replies celebrated the image of two visionary leaders supporting each other amid the pressures of building the future.

Replies ranged from heartfelt endorsements — “True friends are priceless” — to humorous takes on Huang’s signature leather jacket and Musk’s casual style. Some users drew parallels to other high-profile friendships in business, while others used the moment to reflect on personal relationships. A common theme emerged: in an era of digital connection, authentic bonds remain irreplaceable.

Industry analysts suggested the post subtly reinforces the collaborative spirit between Tesla and NVIDIA, two companies at the forefront of AI, electric vehicles and computing power. Their relationship stands in contrast to more adversarial dynamics seen elsewhere in Silicon Valley, such as ongoing tensions over chip supplies and market dominance.

Musk’s Philosophy on Life and Success

Musk has occasionally shared personal insights on X, from family values to the importance of long-term thinking. His “True” reply aligns with previous statements emphasizing loyalty, resilience and surrounding oneself with people who share a mission. Friends and associates have described Musk as someone who values deep, enduring relationships despite the demands of running multiple companies.

For Huang, the sentiment resonates with his own public comments about early supporters like Musk who backed NVIDIA during critical periods. The two have appeared together at conferences and events, often discussing the future of AI with mutual respect and enthusiasm.

Viral Impact and Cultural Resonance

The post’s rapid spread highlights X’s role as a platform for unfiltered moments from influential figures. Musk’s massive following — more than 200 million users — amplifies even brief comments into global conversations. The exchange has been covered by major outlets, with commentators praising its simplicity and authenticity in an age of polished public relations.

Social media users from diverse backgrounds shared how the post prompted personal reflection. Parents posted about teaching children the value of true friendship, while professionals discussed navigating workplace alliances. Some drew connections to broader themes of trust in leadership, both in business and politics.

Critics, however, noted the irony of a billionaire discussing friendship while navigating complex business and regulatory challenges. Others appreciated the reminder that even the most powerful figures prioritize human connection. The post has sparked countless memes, quote graphics and video edits celebrating friendship across industries.

Broader Implications for Tech Leadership

As AI reshapes industries and geopolitical tensions influence global supply chains, personal relationships among tech leaders can play a subtle but significant role. Musk and Huang’s rapport has facilitated collaboration on projects critical to U.S. innovation and competitiveness. Their joint presence in Beijing signaled unity in high-stakes diplomatic and economic discussions.

The moment also humanizes the often-intimidating world of big tech. In an era where executives are scrutinized for every statement and move, a simple affirmation of friendship offers a refreshing counterpoint. It underscores that behind the balance sheets and bold visions are individuals who value the same fundamental things as everyone else.

As reactions continue pouring in, Musk’s brief reply stands as a testament to the enduring power of genuine connection. In a world increasingly defined by algorithms and competition, the image of two trailblazers sharing a moment of camaraderie reminds millions that true friends remain one of life’s greatest assets — a sentiment Musk himself endorsed with just one word.

The post remains live and continues gaining traction, serving as a timely reminder amid fast-paced technological change. Whether viewed as a casual comment or a deeper philosophical statement, Musk’s agreement has resonated far beyond the tech community, sparking conversations about what truly matters in life.

BEIJING — President Donald Trump emerged from two days of intense negotiations with Chinese President Xi Jinping with tangible victories that strengthen America’s economic position, as the United States extracted concrete commitments on energy purchases, Boeing aircraft orders and agricultural exports while holding firm on core strategic issues including Taiwan and technology restrictions.

The high-stakes summit, the first U.S. presidential visit to China in nearly a decade, concluded Friday with Trump declaring the meetings “extremely productive” and securing deliverables that directly benefit American workers, manufacturers and energy producers amid global disruptions caused by the Iran conflict. While both leaders projected warmth and mutual respect, analysts assessing outcomes say Trump achieved more measurable gains without making significant concessions on America’s strategic red lines.

Trump brought a powerful delegation of U.S. business leaders including Elon Musk, Tim Cook and Jensen Huang, leveraging their presence to push for expanded market access and fairer trade practices. The trip yielded commitments from China to significantly increase purchases of U.S. energy, Boeing aircraft and agricultural goods — moves designed to help offset global oil supply concerns and support American jobs.

Key Wins for the United States

White House officials highlighted several concrete outcomes. China agreed to ramp up imports of American liquefied natural gas and other energy products, providing crucial stability for U.S. producers facing volatile global markets. Boeing secured firm commitments for additional aircraft orders, a major boost for American manufacturing and aerospace workers. Agricultural exports also received a significant lift, benefiting Midwest farmers.

On the diplomatic front, both nations reaffirmed that Iran must not develop nuclear weapons and that the Strait of Hormuz must remain open for energy shipments — a critical priority for global markets and U.S. allies. Trump’s team successfully avoided major concessions on Taiwan, with no softening of America’s support for the island’s security despite Xi’s firm public statements on the issue.

Trump used the summit to reinforce America’s technological edge, with U.S. executives pressing successfully for improved regulatory conditions. The meetings also advanced discussions on fentanyl precursor chemicals, addressing a key domestic priority for the Trump administration.

China’s Limited Gains

While Xi hosted Trump with full state honors and emphasized “partnership over rivalry,” Beijing offered mostly incremental steps rather than structural reforms. Chinese state media focused heavily on optics and mutual respect, but analysts note that China conceded more on commercial purchases to secure stability during a period of global uncertainty. Xi’s warning on Taiwan was firm but produced no policy shift from the American side.

Trump’s approach — combining personal diplomacy with business leverage — proved effective. The inclusion of top American CEOs created direct pressure that translated into purchasing commitments, giving the U.S. side measurable economic wins that can be highlighted domestically.

Strong Domestic and International Reaction

In Washington, Republicans hailed the summit as a clear success for American interests, with many praising Trump’s ability to extract concessions while protecting strategic priorities. Business groups welcomed the energy and aircraft deals as immediate boosts for U.S. exporters. Democrats offered measured praise for the energy stability agreements while calling for stronger action on human rights.

Taiwanese officials expressed satisfaction that no major concessions were made on their security. European and Asian allies viewed the outcome as a net positive for global stability, with U.S. leadership helping maintain pressure on key issues like Iran.

Strategic Context and Long-Term Impact

The summit occurred against the backdrop of ongoing U.S.-China competition, but Trump’s team successfully framed the relationship as one of managed rivalry rather than outright confrontation. By securing commercial wins without compromising on technology export controls or Taiwan policy, the administration advanced America’s economic interests while maintaining strategic deterrence.

Analysts note that Trump’s personal rapport with Xi, built over multiple meetings, allowed for more direct and results-oriented discussions than traditional diplomatic channels. The presence of Musk, Cook and Huang amplified American leverage, demonstrating the synergy between U.S. government policy and private-sector strength.

For China, the visit provided valuable stability during a challenging period, but the tangible concessions on purchases and energy suggest Beijing blinked first on immediate economic pressure points. Xi maintained his public stance on Taiwan but failed to extract any softening of U.S. positions.

What Comes Next

Trump returns to Washington with deliverables he can tout as proof of his “America First” approach delivering results. Follow-up negotiations will focus on implementing the new purchase agreements and addressing remaining issues. Xi’s invitation to visit the White House in September keeps dialogue channels open.

The Beijing summit marks a notable chapter in U.S.-China relations, with Trump demonstrating that targeted diplomacy backed by economic leverage can produce favorable outcomes for American interests. While the broader strategic competition continues, this meeting delivered clear edges for the United States on trade, energy security and maintaining firm positions on core national security concerns.

As Air Force One departed Beijing, Trump’s team projected confidence that the agreements reached will strengthen the U.S. economy and global standing. In the ongoing superpower relationship, this round clearly tilted toward American priorities and practical wins. The true test will be in the months ahead as both nations implement what was agreed and prepare for future engagements.

Australia’s share market has fallen for four of the past five weeks, following a storm of profit warnings, earnings disappointments, interest rate hikes and fuel security woes.

Claire Tyrrell speaks to Ella Loneragan about the state of major projects in South Perth, as development times ramp up.

“Overall, UK politics is a mess, there are already signs that foreign buyers are ditching the gilt market. If there is a major rout in the pound and/or gilts in the coming days, prospective candidates may need to assess whether now was a wise time to make a move against the PM,” she said.

Intuitive Machines Set To Launch In The Space Race

Hargreave Hale AIM VCT allots 105,364 shares at 33.55p

Zelenskiy condemns Russia after strike on Kyiv apartment block kills 24

Vodafone appoints Olaf Koch as non-executive director

“Trump has never had alcohol in his life. China gave him a beverage to toast, and Trump drank it. This is a very subtle, but STRONG statement on who’s really in charge,” claimed one viral social media post.

According to the Asian Business Daily, “During the proceedings, President Trump was seen raising his glass containing the toasting wine and bringing it to his lips, appearing to take a sip. He then handed the glass to a staff member, and cameras caught him seemingly holding the wine in his mouth for a moment before swallowing.”

Trump has repeatedly said he has never consumed alcohol — a rare claim among modern US presidents.

“I’ve never had a drink,” Trump told Fox News after his election victory in 2017.

According to the BBC, Trump’s decision to avoid alcohol stems from the death of his older brother, Freddie Trump, who died at the age of 42 from complications related to alcoholism.

Trump has also reportedly advised his children to stay away from drugs, alcohol and cigarettes.

However, Bruce LeVell, a former Trump adviser and former White House small business advocate, dismissed the viral speculation in a post on X, saying, “It’s not alcohol, and I speak for the President.”

In another post, he added, “President Trump does not drink or do drugs. You want a president like that.”

Trump was on an official visit to China on an invitation from Chinese president Xi Jinping. It was the first visit to China by a US president in nine years.

What happened during Trump’s China visit

Trump departed China on Friday while highlighting several business agreements reached during the trip, even as Beijing warned Washington against mishandling the sensitive Taiwan issue and criticised the Iran war.

“We’ve settled a lot of different problems that other people wouldn’t have been able to solve,” Trump said after meeting Chinese President Xi Jinping in Beijing on the second day of talks.

The discussions reportedly covered the Iran conflict, Taiwan, trade ties and other major geopolitical issues. While Xi did not publicly comment on his talks with Trump regarding Iran, China’s foreign ministry later issued a strong statement expressing frustration over the conflict.

Elon Musk’s ‘True’ Reply to Jensen Huang Friendship Post Goes Massively Viral

South Korea’s Hana Financial Scoops up 2.2M Dunamu Shares

Rich List 2026: David Beckham becomes Britain’s first billionaire sports star

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Marianne Dress

-

Fashion4 days ago

Fashion4 days agoCoffee Break: Travel Steam Iron

-

Fashion4 days ago

Fashion4 days agoWhat to Know Before Buying a Curling Wand or Curling Iron

-

Tech5 days ago

Tech5 days agoAuto Enthusiast Carves Functional Two-Stroke Engine from Solid Metal

-

Politics3 days ago

Politics3 days agoWhat to expect when you’re expecting a budget

-

Business6 days ago

Business6 days agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Politics6 days ago

Politics6 days agoPolitics Home Article | Starmer Enters The Danger Zone

-

Tech4 days ago

Tech4 days agoGM Agrees To Pay $12.75 Million To Settle California Lawsuit Over Misuse Of Customers’ Driving Data

-

Crypto World6 days ago

Crypto World6 days agoPROS explodes 48% as Upbit and Bithumb listings ignite demand

-

Crypto World5 days ago

Crypto World5 days agoCZ says US crypto rivals tried to block Trump pardon

-

Tech3 days ago

Tech3 days agoGM agrees to $12.75M California settlement over sale of drivers’ data

-

Entertainment7 days ago

Entertainment7 days agoYNW Melly Denied Bond Again Ahead Of Double Murder Retrial

-

Crypto World7 days ago

Crypto World7 days agoKraken Parent Seeks OCC Charter, Signaling Regulated Banking Access

-

Crypto World7 days ago

The Hantavirus Danger: Can a Potential Outbreak Spark a New Meme Coin Frenzy?

-

Sports7 days ago

Sports7 days agoAfter Waka Waka, Shakira now drops first teaser for FIFA WC 2026 song | FIFA World Cup 2022

-

Tech7 days ago

Tech7 days agoSongs My Mother Gave Me: Editor’s Round-Up

-

Tech7 days ago

Tech7 days agoThe Xperia 1 VIII leak finally gives Sony some swagger

-

Crypto World6 days ago

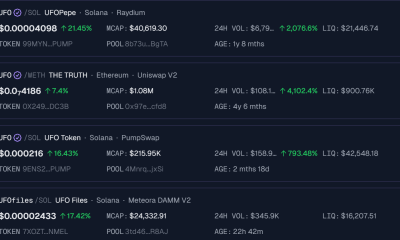

Crypto World6 days agoSolana UFO Meme Coins Surge After Pentagon Reveals Alien Files

-

Entertainment6 days ago

Entertainment6 days agoBethenny Frankel Says She Loves ‘Torturing’ Men

-

Sports7 days ago

Sports7 days agoWhy Nathan Mackinnon Remains the Hart Trophy Favourite over Connor McDavid and Nikita Kucherov | NHL

You must be logged in to post a comment Login