During the second quarter of 2026, Night Watch Investment Management LP appreciated by 12.80% net of fees.

Last quarter, we mentioned that our shareholding in Marex (MRX) had grown to be an outsized position in our portfolio, at 14.5%. This paid off this quarter, with the stock up 37% in the quarter and 230% since we bought our first shares around the IPO two years ago. The company is benefitting from high market volatility, while simultaneously showing great execution on their M&A playbook, most notably by continuing to grow their prime brokerage business. At 10x 2026 P/E and >30% ROE, this remains a compelling long.

Performance this quarter was further aided by strong performance of names such as Watches of Switzerland Group (WOSG LN) and Silicon Motion (SIMO). We owned two noticeable detractors: FUTU (FUTU) and Sanuwave (SNWV). We have been adding aggressively to FUTU while we are waiting for improving data points before risking more capital on SNWV.

Advertisement

Portfolio

Night Watch manages a global value strategy that differentiates on the following points:

Catalyst – We predominantly buy value companies with an identifiable catalyst for a rerating. Catalysts can include industry tailwinds or company-specific events (e.g., earnings inflection, CEO changes, refinancing).

Inside Ownership – We aim to find companies where management has considerable ownership in the company. We consider this alignment of interest to be an important determinant of share price performance.

Unique Names – To differentiate from a long list of other value strategies, we seek unique portfolio holdings that have little overlap with a typical wealth management portfolio. We aim to provide our LPs with diversification from their other investments in addition to strong performance.

Advertisement

The portfolio as of June 30th, 2026, is as follows:

Theme

Weight

Positions

(Senior) Housing

7.0%

2

Aerospace / Defense

15.0%

4

Payments

14.8%

3

US Cyclicals

17.0%

5

US Counter-cyclicals

21.3%

3

US Defensive

12.9%

5

Europe

10.8%

2

Hong Kong

11.2%

4

Japan

7.4%

2

Brazil

5.6%

2

Event Driven

0.4%

Funding Shorts

-17.7%

Cash

-5.8%

Total

100%

32

Largest positions:

Marex (13.7%)

AAR Corp (7.3%)

Remitly (6.2%)

Distribution Solutions Group (5.8%)

Universal Technical Institute (5.8%)

Adyen (5.6%)

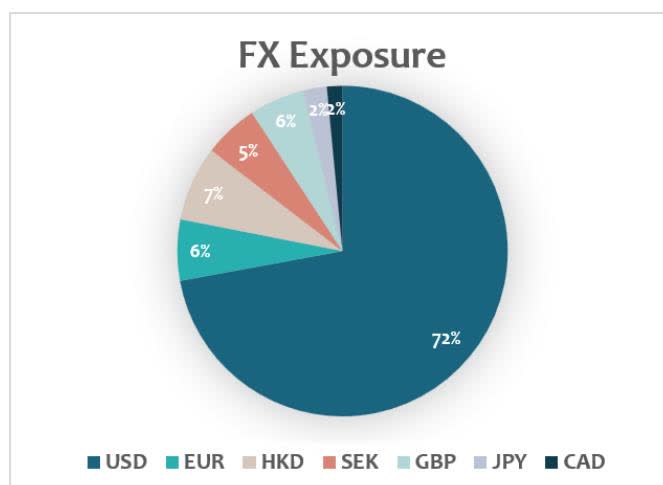

FX Exposure

Advertisement

Currency

Exposure (%)

USD

72%

EUR

6%

HKD

7%

SEK

5%

GBP

6%

JPY

2%

CAD

2%

Pie chart showing FX Exposure by currency: USD (72%), EUR (6%), HKD (7%), SEK (5%), GBP (6%), JPY (2%), CAD (2%).

Market Update

The first half of the year has been unusually volatile, and the market has been even more bifurcated than usual. On the one hand, you have got businesses that touch AI, whose stocks keep going up daily to what we believe to be unsustainable levels. We are not complaining. We were early on Western Digital Corp (WDC) and we still own Silicon Motion (SIMO). Both benefitted from the shortage in memory caused by strong demand from AI data centers. But we are not blind to the cyclical nature of those businesses, and we have been early in taking some chips off the table.

On the other hand, you have got everything that is not AI. If your business is a quality compounder with a decade-long history of providing your shareholders with 10-15% earnings growth, your stock got sold off because why would anyone care about 15% per year if you can earn that in a day by holding AI stocks!?

Naturally, we are buyers of such businesses. If we can find low-risk ways to lock in 15% earnings growth, and if we might even get some multiple expansion on top when markets normalize, we are happy to move up on the quality spectrum. We added quality names including Stryker (SYK), Adyen (ADYEN NA)(ADYYF) and Booking.com (BKNG).

Advertisement

Finally, there were the companies that, rightly or wrongly, were viewed as AI losers. We were reminded once again that valuation in today’s market does not provide a floor to stock prices. Especially software and payment related companies saw their shares freefall during the first half of 2026.

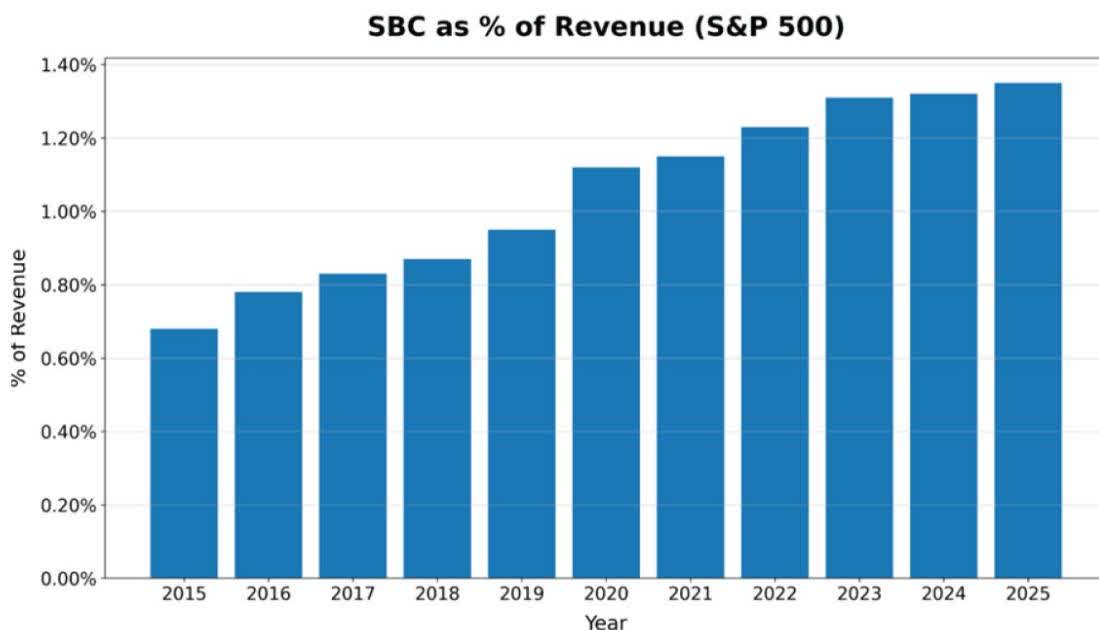

We have a differentiated view on this sell-off. Over the last few years, we have seen an increasing reliance of companies on Stock-Based Compensation (SBC). Growing a business requires capital. Wall Street’s greatest trick was to convince the markets that this growth could be funded without running the costs through the P&L. If you simply paid employees through stock options or stock grants, they argued, it’s not a real expense, and analysts ought to exclude it from their model.

For some reason, Wall Street obliged. SBC took on excessive levels as companies were keen to exploit this newly found loophole.

Source: KEDM.com – Companies taking Wall Street for a ride by excluding from earnings all salaries paid out in options and stock grants.

Advertisement

It isn’t hard to see the reflexive nature of this setup. Paying in SBC and excluding those costs is all fun and games when share prices go up. But when share prices go down, the dilution caused by the SBC goes up. 3% dilution per year can quickly become 10% dilution. On top of that, your employees are seeing the value of their stock options dwindle and might be quick to start thinking about updating their resumes.

Now that the market has finally started caring about SBC, it seems wise to buy companies with real earnings.

Historically, Dutch companies have paid out little to no SBC. This is not by accident. Stock options or grants in The Netherlands are taxed excessively, making this not a viable option for companies. While that’s a shame for Dutch employees, it benefits shareholders of those companies.

Companies with international operations, who have a large portion of their employees in places like Amsterdam, have a comparative advantage. BKNG and ADYEN fit that bill. For the first time since inception, Night Watch is going Dutch. We added BKNG and ADYEN to the portfolio.

Advertisement

Position Highlights

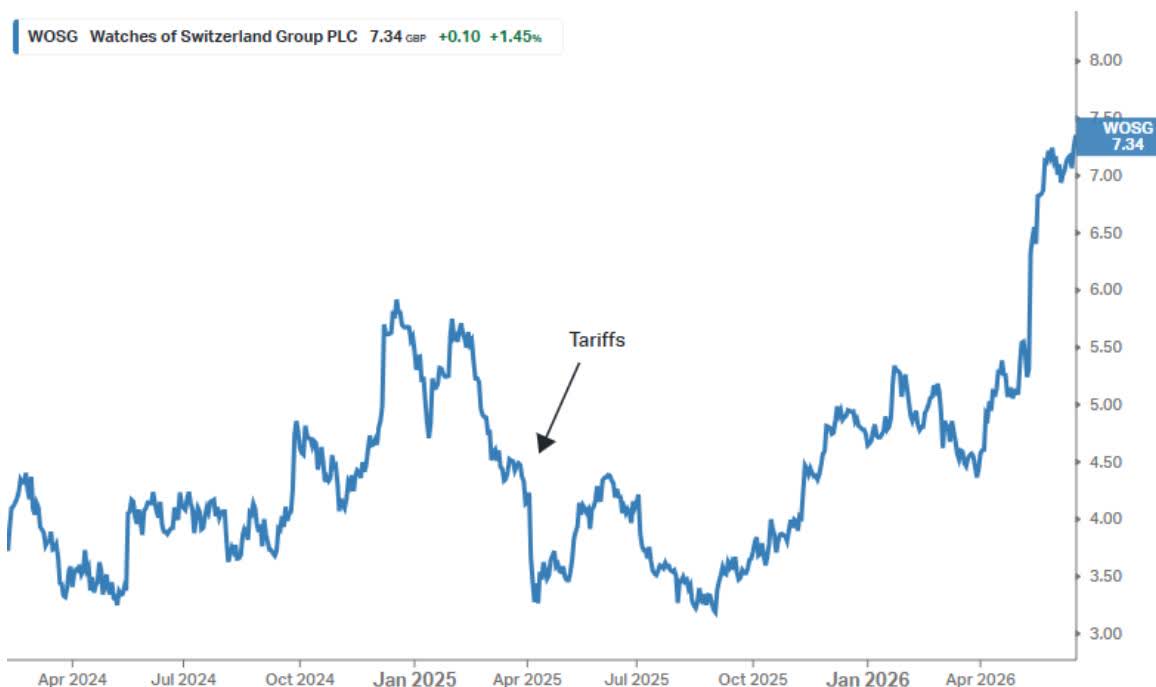

Watches of Switzerland Group (WOSG LN)(WOSGF) has been a core position since our inception in 2024. It has been a somewhat frustrating investment for the first two years, but more recently the stars have started to align.

WOSG is a retailer of luxury watches, most notably an authorized dealer of Rolex and Patek Philippe. This business is considerably higher quality than ordinary retailing because it is supply-constrained rather than demand-constrained. Prospective buyers often have to join waiting lists for popular models, and the number of watches a retailer sells is determined largely by the allocation it receives from Rolex rather than by end-market demand. Rolex, in turn, is owned by the Hans Wilsdorf Foundation, a non-profit organization that appears to be at least as interested in preserving its Swiss legacy as it is in maximizing profits.

The business model over the last few decades has been straightforward. Rolex consolidated the sale of its watches among a small group of trusted partners with the financial strength to invest millions in dedicated Rolex stores and the ability to provide a consistent customer experience across locations.

WOSG was the consolidator in the UK. In exchange for accepting slightly lower gross margins, it received larger allocations from Rolex. Higher volumes per store more than offset the lower margins.

Advertisement

Following its success in the UK, WOSG replicated the model in the United States, which today accounts for roughly 50% of revenue.

Luxury watch sales peaked in 2021, and demand for brands other than Rolex and Patek Philippe slowed. We initiated a position in early 2024 after the resulting decline in the share price.

Unfortunately, WOSG faced another setback when the United States imposed 39% tariffs on Swiss imports. We feared the economics of the business could deteriorate sharply. Rolex boutiques are difficult to repurpose, and passing through a 39% price increase, even in the luxury segment, seemed like a tall order.

We were patient. Switzerland was unlikely to be singled out as the root-cause of the US trade imbalance forever. And in a worst case, the tariffs would likely accelerate the consolidation in the industry, benefiting the strongest players.

Advertisement

With tariffs now finally in the rear-view mirror, WOSG is finally back to executing its proven playbook. US growth re-accelerated to 24%. The UK is steady at 5% growth. The balance sheet is underleveraged. Despite the strong move-up, shares are trading at 13x next year’s earnings. WOSG remains a conviction long.

Conclusion

The market has become a one-trick pony with many quality companies being sold off in favor of anything that touches the AI trade. We are happy to buy quality companies at depressed valuations. Meanwhile we are doing our own thing, allocating to sectors with structural tailwinds that are largely overlooked, including the aerospace aftermarket, futures commission merchants, and various payment companies.

By following this disciplined strategy, we have been compounding capital at well over 20% since inception while providing good diversification to anyone who is invested in the major indices. This has also resulted in very low volatility, and we have not seen any major drawdowns in our portfolio to date.

On behalf of the Night Watch team,

Advertisement

Roderick van Zuylen, Chief Investment Officer

Eileen Ke, Chief Operating Officer

Night Watch Investment Partners LP – Net Performance (in USD)

Advertisement

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Year

2024

-0.82%

0.58%

7.09%

-0.24%

5.14%

-5.20%

9.11%

-0.23%

-1.34%

-2.40%

2.10%

-2.92%

10.30%

2025

2.56%

-0.45%

-4.12%

1.03%

8.94%

12.04%

0.14%

3.06%

1.04%

-4.46%

2.90%

-0.12%

23.61%

2026

6.44%

3.74%

-6.99%

9.69%

1.21%

1.61%

15.85%

Since Inception, Total:

57.96%

Since Inception, CAGR:

20.06%

Important Disclosures

This document was prepared by Night Watch Investment Management, LLC (“NWIM”) on July 1st, 2026, based on information available as of July 1st, 2026, and is subject to amendment. The information and opinions contained in this document (including information obtained from third-party sources) are for background purposes only and do not purport to be full or complete, and do not in any way constitute personalized investment advice or an investment recommendation on the part of NWIM. No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this document, and no liability is accepted as to the accuracy or completeness of any such information or opinions.

All investments involve the risk of a loss of capital. NWIM believes that its proprietary investment program, research and risk-management techniques moderate this risk through the careful selection of portfolio investments. However, no guarantee or representation is made that NWIM’s investment program will be successful, and investment results may vary substantially over time. Past performance is not a guide to future performance. This publication makes no recommendations whatsoever regarding buying, selling, or holding any specific security, class of securities, or securities of a class of issuers. You are required to conduct your own due diligence, analyses, draw your own conclusions, and make your own investment decisions. Commentary is provided without reference to any investment strategy or product offered by NWIM. NWIM or entities managed by NWIM may be invested in any of the industries or securities mentioned. They may trade in and out of those positions without providing any updates.

Certain information contained in this document constitute “forward-looking statements,” which can be identified by the use of certain terminology, such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe” or the negatives thereof, or other variations thereon or comparable terminology. Any projections or other estimates in this document, including estimates of returns or performance, are “forward-looking statements” and are based upon certain assumptions that may change. Due to various risks and uncertainties, actual events or results, or the actual performance of any investment vehicle, portfolio or product described herein may differ materially from those reflected or contemplated in the forward-looking statements. Actual events are difficult to project and often depend upon factors that are beyond the control of NWIM.

Advertisement

TO THE FULL EXTENT PERMITTED BY LAW NEITHER, NWIM NOR ANY OF ITS AFFILIATES, NOR ANY OTHER PERSON OR COMPANY, ACCEPTS ANY LIABILITY WHATSOEVER FOR ANY DIRECT, INDIRECT, OR CONSEQUENTIAL LOSS ARISING FROM, OR IN CONNECTION WITH, ANY USE OF THIS PUBLICATION OR THE INFORMATION CONTAINED HEREIN. NWIM AND ITS AFFILIATES EXPRESSLY DISCLAIM ANY GUARANTEES, INCLUDING, BUT NOT LIMITED TO, FUTURE PERFORMANCE OR RETURNS.

Copyright 2026 Night Watch Investment Management, LLC. All rights reserved.

SLG Brands said the deal would allow it to focus on ‘the next era of beauty creation’

08:36, 02 Jul 2026Updated 08:42, 02 Jul 2026

SLG Brands has sold COLAB Dry Shampoo (pictured)(Image: SLG Brands)

A global beauty product incubator headquartered in Cheltenham has completed the sale of two of its flagship haircare brands to a US consumer goods company.

SLG Brands has sold Colab Dry Shampoo and Johnny’s Chop Shop to Thriving Brands – a consumer goods company in Cincinnati backed by Dallas-based private equity firm Trive Capital.

Advertisement

Following the deal, Thriving Brands – the owner of household names such as Right Guard – will use SLG’s existing distribution networks with UK and US retailers including Tesco, Boots, Target and Walmart.

SLG said the deal would allow it to focus on its core licensing business “while unlocking capital for future growth initiatives”.

Lucy Beresford, chief executive officer of SLG Brands, said: “We conceived and founded Colab Dry Shampoo and Johnny’s Chop Shop, and grew them into internationally recognised brands. Completing this transaction frees SLG to focus on the next era of beauty creation.”

SLG was established in 1985 and has developed its own portfolio of beauty and personal care products for domestic and international markets.

Advertisement

The business specialises in brand creation and licensing, having partnered with well-known high street names and celebrities for its beauty ranges including Paul Smith, Superdry, Sweaty Betty and White Fox Boutique. It is also backed by private equity firm BGF.

The deal was supported by FRP Corporate Finance’s team, led by partner Victoria Kisseleva with assistance from associate director Matthew Nolan.

Ms Kisseleva said: “In the beauty market we’re seeing continued interest in brands that can prove repeat purchase behaviour from their customers and offer the ability to scale internationally.

“Haircare in particular is one area where we’re seeing growth, which is what made these brands such an attractive prospect for acquisition on the international market.

Advertisement

“It was great to be able to help the team at SLG Brands secure this deal as it forms a key part of their future growth strategy.”

Netflix’s third installment in its popular Enola Holmes franchise arrived Tuesday with Millie Bobby Brown reprising her role as Sherlock Holmes’ younger sister in a sunnier, darker and more action-heavy chapter set against the backdrop of Malta, drawing a divided critical reception that praised Brown’s performance while questioning whether the series has begun to show signs of franchise fatigue.

“Enola Holmes 3,” rated PG-13 and running one hour and 45 minutes, begins on wedding day. Enola is about to marry Lord Tewkesbury, played again by Louis Partridge, in a ceremony set on the sun-drenched Mediterranean island. Before she can reach the altar, news arrives that her brother Sherlock, played by Henry Cavill, has been kidnapped, and Tewkesbury’s mother is taken shortly afterward. The wedding is indefinitely postponed, the mystery takes over, and Enola races through Malta with Dr. Watson, played by Himesh Patel, to find the kidnappers before the situation turns fatal.

The film is directed by Philip Barantini, best known for the critically acclaimed Netflix series “Adolescence,” who takes over the franchise from Harry Bradbeer, who helmed the first two entries. The screenplay was again written by Jack Thorne, who adapted Nancy Springer’s YA book series for all three films. The ensemble cast also includes Helena Bonham Carter as Enola’s bomb-throwing revolutionary mother Eudoria, Sharon Duncan-Brewster as the villainous Moriarty and Susan Wokoma as Enola’s mentor Edith.

Advertisement

The film includes a clue left by Sherlock before his abduction that becomes central to the plot.

“A Holmes does not disappear without leaving clues for a Holmes,” Enola observes in the film.

The shift to Malta gives the film its most visually distinctive look of the trilogy, trading London’s gloomy Victorian streets and fog for sparkling Mediterranean light and colorful architecture. Several critics noted the change of scenery as one of the film’s stronger decisions, lending the story a fresh visual energy that helps distinguish this installment from its predecessors.

Among the more enthusiastic reviews, Tom’s Guide described the third film as “easily” the reviewer’s favorite in the franchise, citing the emotional depth added to the story through Enola’s ambivalence about marriage and the fear of losing herself in the role of Victorian aristocratic wife alongside her fear of failing to save her brother. RogerEbert.com praised Brown as “ideally cast” and highlighted the film’s action sequences, puzzles and romance as dynamic and engaging elements, adding that “when she speaks directly to us, it feels good to be part of her story.”

Advertisement

MovieWeb similarly called the villain “deliciously fiendish” and praised the film’s ambition in raising the franchise’s stakes.

Critical reviews at the other end of the spectrum identified a set of recurring concerns about pacing, mystery quality and tonal inconsistency. Collider called the film “mostly forgettable,” arguing that while Brown continues to charm in the lead role, the mystery itself is lazy, largely predictable and telegraphed from early in the running time, a particular problem for a series built explicitly on the detective genre’s tradition of genuine puzzle-solving. IndieWire noted that while Barantini brings a more grown-up touch to the material, the choice doesn’t always mesh comfortably with the franchise’s characteristic exuberance, creating a film that feels caught between its desire to mature alongside its audience and its obligation to retain the playful energy that distinguished the original.

Gulf News offered perhaps the most pointed mixed assessment, describing the film as resembling banana bread: “Fine, but nothing to make a fuss about.” The review flagged the feminist and colonial commentary as clumsily integrated into the plot, suggested the villain lacked the nuance appropriate for a Holmes story and criticized a pattern in which Enola’s detective work increasingly gives way to action sequences.

Variety noted that while Enola’s fourth-wall breaks and deductive moments remain charming, some of the real-world social commentary about the suffrage movement and workers’ rights that made the earlier films feel particularly vital is largely absent here, replaced by plot threads about Maltese independence fighters and Dr. Watson’s military past that feel like afterthoughts.

Advertisement

Hollywood Reporter, in perhaps the most concisely worded verdict across the critical coverage, offered what it called a “bottom line” that the film was “elementary but enjoyable,” a play on Sherlock Holmes’ most famous phrase that captures the middling but watchable quality many critics identified.

Brown is again a producer on the film alongside Robert Brown, Michael Dreyer and Jack Thorne. The executive producer roster includes Joshua Grode and Jake Bongiovi. Director of photography Matthew Lewis shot the film on location in Malta and in studio, with production design by Gary Williamson and costumes by Consolata Boyle rounding out the period aesthetic.

The first Enola Holmes film, released in 2020 during the height of the pandemic, was watched by approximately 76 million households in its first four weeks on the platform, making it one of Netflix’s more successful original film launches and establishing Brown as a reliable franchise anchor for the streaming service alongside her work on “Stranger Things.” The sequel followed in 2022 with a broadly positive reception and solid viewership, setting up the third installment as the next test of whether the series can sustain long-term audience engagement.

Whether the franchise continues beyond this third film remains unclear. Some critics specifically called for a fourth entry if the creative team can sharpen the mystery writing, while others suggested the franchise has run its natural course and that Enola might be better served retiring gracefully rather than continuing in diminished form.

Federal Reserve Chairman Kevin Warsh is talking less than some of his predecessors, making some investors nervous about the prospect of a quieter Fed. At his first Fed meeting as chairman, Warsh shortened the central bank’s policy statement and declined to provide an interest-rate forecast. His approach is prompting some investors to say that added uncertainty could lead to a more volatile market. Read more:

A Bain & Company report drawing on surveys of 600 doctors and 6,300 consumers across Asia-Pacific finds the region’s healthcare systems under simultaneous pressure from physician burnout and rising consumer expectations. One in five doctors are considering leaving their jobs, while 84% of patients demand greater convenience and 95% want a single point of contact for their care.

AI adoption is widely supported by both patients and clinicians but organisational readiness remains limited, with one in three doctors saying their institution is unprepared to deploy it at scale. Bain identifies an 18-month window for providers and insurers to act, emphasising clinician engagement and coordinated care models as prerequisites for sustainable change.

A wave of physician burnout is colliding with a surge in consumer demand across Asia-Pacific’s healthcare systems, according to a major new report from global consultancy Bain & Company, which warns that the region’s providers, insurers and pharmacies have roughly 18 months to adapt before losing ground to faster-moving competitors.

Key takeaways

One in five Asia-Pacific doctors are considering leaving their jobs, driven by heavy workloads and lack of recognition rather than pay, threatening the region’s already thin physician supply.

Patients are behaving like consumers, with 84% demanding more convenience, 95% wanting a single point of contact for their care, and nearly 60% shifting to alternative settings like telehealth, retail clinics and home-based visits.

Appetite for AI in healthcare is high among both patients and doctors, but one in three physicians say their organisation isn’t ready to deploy it at scale, leaving an 18-month window for providers and insurers to adapt before losing ground.

The report, Bain’s fourth biennial study of frontline healthcare trends in the region, draws on surveys of 600 doctors in Australia and the Philippines and 6,300 consumers across nine countries, conducted in December 2025. Its authors describe a system caught between two forces moving in opposite directions: patients who increasingly behave like demanding consumers, and a clinical workforce that is stretched to its limit.

A Widening Gap Between Supply and Demand

The tension, researchers argue, stems from a structural mismatch. Asia-Pacific is home to roughly 60% of the world’s population and carries an outsized share of global disease burden, yet the region accounts for only about 22% of worldwide healthcare spending. Physician density remains thin, excluding China, the report puts the average at under one doctor per 1,000 people, far below the World Health Organization’s recommended minimum of 2.5.

Against that backdrop, long wait times have topped the list of consumer complaints for four consecutive Bain surveys, a pattern the report says holds true regardless of whether a country’s system is public or private, wealthy or developing. High out-of-pocket costs compound the problem: fewer than 70% of patients with chronic conditions reported keeping up with regular check-ups, with cost cited as the main deterrent.

Physicians on the Edge

Doctors, meanwhile, are signalling they’ve had enough. Roughly 20% of physicians surveyed said they are actively weighing a move to a different organisation, and about 30% believe recruitment and retention have worsened since 2023. The report attributes this primarily to heavy workloads and a lack of professional recognition rather than pay. Doctors in both mature markets like Australia and emerging ones like the Philippines ranked career development and access to modern tools above compensation as priorities, yet only about 30% said they were satisfied on either front.

The stakes of ignoring this trend are high, the report suggests: physicians who feel engaged in strategic decisions at their organisations reported workplace advocacy scores up to 36 points higher than colleagues who don’t, a gap researchers linked to broader outcomes in patient care and safety.

Advertisement

Patients Are Acting Like Consumers

On the demand side, the report documents a marked shift toward consumer-style healthcare behaviour. The vast majority of respondents, 84%, said they now expect more convenience from the healthcare system than they did two years ago, and 71% want doctors to be reachable through messaging apps or email rather than waiting for scheduled visits. Nearly 70% said they had used AI tools to help interpret a diagnosis or treatment plan.

Preventive care usage has also jumped, with 60% of consumers reporting regular check-ups and screenings in 2025, up from 47% two years earlier, a trend led by China, where 76% of respondents said they get routine screenings.

Spending patterns reflect the same shift: consumers reported increasing what they spend across every category of health and wellness, with nutrition supplements, fitness, and oral healthcare showing the sharpest gains.

Care Is Moving Outside the Hospital

Consumers are also voting with their feet when it comes to where they receive treatment. Close to 60% now use alternative care settings such as walk-in clinics, home-based visits, telehealth or wearable devices, a significant jump from intent levels measured in 2019. The preferred format varies widely by market: retail clinics dominate in Malaysia and Australia, home-based care leads in India and Vietnam, and telehealth is the top choice in China and Singapore, where usage has climbed to 61% of consumers, up 37 percentage points since 2019.

Advertisement

By contrast, telehealth adoption in India has fallen sharply, dropping to just 10% penetration as the market’s largely cash-based payment structure limits insurer-driven incentives to use virtual care.

Surgeons surveyed said they would like to perform far more procedures in ambulatory surgical settings than they currently do, citing patient preference and better access to modern equipment as key drivers.

Fragmentation Frustrates Patients and Doctors Alike

A recurring theme in the report is fragmentation. Half of consumers said they were referred to multiple providers before receiving an accurate diagnosis, and more than 40% received conflicting advice from different clinicians. For patients managing chronic illness, more than half said they had to see multiple doctors just to get their needs met.

Clinicians feel the strain from the other side: roughly one in three doctors reported significant inefficiency at their organisation, and about 40% said they regularly perform repetitive administrative tasks that could be automated.

Advertisement

The result, according to Bain, is overwhelming demand for simplification. 95% of consumers said they want a single point of contact to manage their care, up sharply from 70% in 2019. Yet access to primary care physicians, who are seen by most consumers as the natural candidate for that role, remains inconsistent; roughly a quarter of the region’s population has no primary care doctor at all, with gaps particularly pronounced in Malaysia, Hong Kong, Indonesia and China.

AI: Wanted, But Not Fully Trusted or Ready

Artificial intelligence emerges in the report as both the most promising fix and the area of greatest organisational weakness. Nearly three-quarters of Asia-Pacific consumers said they’re comfortable with at least one AI healthcare application, a notably higher comfort level than researchers found among American consumers in a parallel study. Support is strongest for AI that assists clinicians, such as automated documentation or decision support, rather than AI that replaces human interaction entirely, though more than 35% of respondents said they’d accept AI-only call centres or diagnostic tools.

Doctors broadly share this cautious optimism, hoping AI will ease administrative burdens while worrying it could erode the doctor-patient relationship, a concern the report says mirrors sentiment in the US and UK.

But readiness lags behind appetite. About one in three doctors said their organisation isn’t prepared to deploy AI at scale, citing unclear strategy, inadequate training and insufficient involvement from clinical staff. Even basic digital infrastructure such as workforce management systems and revenue cycle tools remains underused, the report found, even in a relatively advanced market like Australia.

Advertisement

Some organisations are further along. The report cites Apollo Hospitals’ clinical decision-support platform, which covers 1,300 conditions and is maintained by more than 500 in-house clinicians, and Singapore General Hospital’s AI-driven perioperative chatbot, which researchers say has saved an estimated 660 doctor hours a year across 25,000 patients. Ping An Good Doctor, meanwhile, reportedly uses AI agents to handle up to 4 million consultation requests daily, cutting per-doctor service costs by roughly half.

Five Priorities for Industry Leaders

Bain’s authors, partners Vikram Kapur, Alex Boulton, Lucy d’Arville and Dhruv Sukhrani, along with practice senior manager Monica Pinto Basto, lay out five strategic priorities for healthcare leaders in the region: building a trusted single point of coordination for patients; redesigning care journeys around the interactions that matter most to patient loyalty, particularly billing; adopting value-based care models tied to outcomes rather than volume; treating AI deployment as a full business transformation rather than a bolt-on feature; and prioritising clinician engagement as a precondition for successful change.

The report singles out billing and coverage disputes as the single biggest driver of dissatisfied patients across the region, and warns insurers in particular that failing to modernise these interactions risks accelerating the shift toward other players such as providers, retailers, and digital platforms, who are moving to claim the “trusted coordinator” role in patients’ healthcare journeys.

The Bottom Line

Bain’s overarching message is that structural pressure on Asia-Pacific’s healthcare systems will not ease on its own, and that AI, while promising, cannot substitute for organisational change. “Technology-driven advantages cannot scale without the workforce,” the report concludes, arguing that organisations willing to invest in clinician trust and involve doctors as partners in AI-driven transformation stand to gain the most, both from a more engaged workforce and from patients who, once satisfied, tend to stay loyal and spend more.

Indian automakers delivered a strong performance across segments in June 2026, as healthy retail demand boosted sales, with brokerages highlighting that commercial vehicle wholesales strongly beat estimates.

Motilal Oswal Financial Services, in its note, highlighted that retail demand momentum remained healthy for passenger vehicles and tractors in June, while two-wheelers saw a revival after a tepid performance in May. Commercial vehicle retail, on the other hand, was relatively soft due to the ongoing geopolitical conditions. However, wholesale sales for the month came in strong, beating our estimates across the board.

“The three listed players posted a healthy 31.3% YoY growth in June 2026, primarily over a low base of last year. TMCV continued to outperform its peers and drive industry growth, posting around 35% YoY growth in CV sales to nearly 41k units, ahead of our estimate of 34k units,” it said.

“Overall, most segments posted healthy double-digit growth in wholesales,” it said, noting that Mahindra & Mahindra (M&M) and Tata Motors PV outperformed in the PV segment, while Hyundai Motor India underperformed and Maruti Suzuki India grew in line with industry growth.

Advertisement

Motilal Oswal’s top auto picks

CV retails remained relatively subdued, though the top three CV OEMs posted strong 31% YoY growth in dispatches, mainly due to the inventory push in the system, Motilal said, adding that tractor demand remained steady (+13.5% YoY for the two listed players) despite ongoing concerns. “Overall, given the stable demand momentum and easing input cost pressure, we expect renewed investor interest in the sector in the coming quarters,” it said.

The domestic brokerage named Maruti Suzuki India, TVS Motor Company and Mahindra & Mahindra (M&M) as its top OEM picks. Among auto ancillaries, its top picks are Motherson Sumi Wiring India, Samvardhana Motherson International and Endurance.

Analysts at Emkay Global also highlighted that auto pack delivered strong performance in June 2026, with growth momentum rebounding across segments and players (also reflected in Vahan retail volumes). In two-wheeler dispatches, Eicher Motors outpaced Hero MotoCorp, while the two-wheeler industry retail momentum returned to 21% YoY with robust growth across the pack. Passenger vehicles also saw strong growth across OEMs, barring Hyundai, whose June volumes were hit by the fire incident at a key supplier’s facility, Emkay noted. Tata Motors Passenger Vehicles led the strong growth among PVs.Amid a strong rebound in underlying demand, Emkay favours two-wheelers or CV OEMs over PVs, due to a similar demand trajectory, albeit with better pricing flexibility amid commodity pressures and a limited new model launch pipeline in FY27 (historically a key growth driver for PVs). In two-wheelers, it favours TVS Motor Company and Ather Energy on a structural basis, and Bajaj Auto, as it offers a better risk-reward.

“We prefer to play the CV upcycle with Tata Motors CV,” it further said, adding that in ancillaries, it favours Shriram Pistons, Craftsman Automation, JK Tyre and Pricol.

ICICI Securities also noted that June 2026 wholesale volumes remained robust and broadly ahead of its estimates. “GST cut-fuelled demand momentum, coupled with a favourable base, continues to underpin the auto sector’s growth. Within 2Ws, scooters and premium motorcycles drove overall segment growth. PV wholesales expanded in double digits, led by strong traction across domestic PCs/UVs and low channel inventory. In CVs, growth was broad-based across MHCVs and LCVs (ahead of our estimates).

The tractor segment’s growth trajectory remained robust (ahead of our estimates). Demand sustainability amid the recent vehicle/fuel price hike(s), along with the potential impact of a below-average monsoon (especially on the tractor segment), remains a monitorable,” it said.

Its preferred auto picks are Hyundai Motor India, Maruti Suzuki India and Bajaj Auto.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

You must be logged in to post a comment Login