Business

How a Unit Linked Insurance Plan Offers Life Insurance and Market Returns Under One Policy

Financial planning today often requires a balance between protection and long-term wealth creation. Many individuals look for solutions that can support family security while also offering opportunities for capital growth.

A unit linked insurance plan combines these two objectives within a single policy. It provides life insurance coverage and allows a portion of the premium to be invested in market-linked funds. This structure gives policyholders the chance to build wealth over time while maintaining financial protection for their loved ones. Understanding how these plans work can help individuals make informed financial decisions.

What is a unit linked insurance plan?

A unit linked insurance plan is a life insurance product that combines protection and investment features. When a policyholder pays a premium, one portion goes towards life insurance coverage. The remaining amount is invested in market-linked funds such as equity, debt, or balanced funds.

The value of the investment component depends on the fund’s performance. As a result, returns are not guaranteed and may rise or fall based on market conditions. This feature allows policyholders to participate in financial markets while maintaining life insurance coverage under a single policy.

How does a unit linked insurance plan work?

A unit linked insurance plan follows a straightforward structure that combines two financial objectives.

Premium allocation

The premium paid by the policyholder is divided into different components. One portion covers life insurance protection, while the remaining amount is invested in selected funds.

Investment in market-linked funds

Policyholders can choose from different fund options based on their financial objectives. These funds may invest in equities, debt instruments, or a combination of both.

Unit allocation

The invested amount purchases units in the selected fund. The number of units depends on the fund’s prevailing net asset value (NAV).

Fund value movement

The value of the investment changes according to market performance. Strong market conditions may increase fund value, while weaker conditions may reduce it.

Life insurance benefit

The policy provides a death benefit during the policy term, subject to policy conditions. This benefit supports the financial needs of beneficiaries if the insured individual passes away.

How life insurance protection is included

remains an important component of a unit linked insurance plan. The policy offers financial protection throughout the coverage period.

The insurance benefit generally becomes payable upon the death of the insured person during the policy term. Depending on policy terms, beneficiaries may receive the sum assured, fund value, or a combination specified under the plan.

This protection feature allows families to maintain financial stability while the investment component continues supporting long-term financial goals.

How market-linked returns are generated

The investment portion of a unit linked insurance plan is linked to financial market performance. Returns depend on the assets held within the chosen funds.

Equity funds

Equity funds primarily invest in company shares. These funds may offer higher growth potential but usually involve greater market fluctuations.

Debt funds

Debt funds invest in fixed-income securities such as bonds and government instruments. These funds generally focus on stability and lower volatility.

Balanced funds

Balanced funds combine equity and debt investments. This approach aims to provide a mix of growth opportunities and relative stability.

The performance of these funds influences the overall value of the policy’s investment component.

Benefits of combining insurance and investment

A unit linked insurance plan offers several practical advantages for individuals seeking multiple financial benefits within one policy.

| Benefit | Description |

| Dual purpose | Combines life insurance coverage and investment opportunities. |

| Goal-based planning | Supports long-term financial objectives such as education or retirement planning. |

| Fund choice | Allows selection from multiple investment options. |

| Switching flexibility | Enables movement between available funds according to changing needs. |

| Long-term participation | Encourages disciplined investing through regular premium contributions. |

These features make the product suitable for individuals seeking both protection and wealth-building opportunities.

Factors to consider before choosing a plan

Several factors should be reviewed before selecting a unit linked insurance plan.

Risk appetite

Different funds carry different levels of market risk. Investors should choose options aligned with their comfort level and financial goals.

Investment horizon

Longer investment periods often provide greater opportunities to manage market fluctuations.

Charges and costs

Policies may include fund management charges and other applicable costs. Understanding these expenses is important before making a decision.

Financial objectives

Investment choices should match specific goals such as retirement planning, children’s education, or wealth accumulation.

Market exposure

Returns are linked to market performance. Individuals should be prepared for periods of both growth and decline.

Conclusion

A unit linked insurance plan provides life insurance protection and market-linked investment opportunities under one policy. It allows policyholders to maintain financial security while participating in potential market growth. The combination of fund choice, flexibility, and long-term investing makes it a practical option for many financial plans. Reputable platforms like Tata AIA offers various life insurance and wealth-oriented solutions designed to support different financial goals. Reviewing policy features carefully can help individuals choose an option that aligns with their long-term requirements.

If they are anything like most Oscar winners, the team behind The Artist will have spent the first day of the rest of their lives conforming to the grandest, and most lucrative, of Hollywood traditions.

Having woken up, pinched themselves, and made sure that -oui! – it really was a gold statuette on their bedside table, France’s newly minted movie stars are likely to have devoted their waking hours to pondering two pressing questions: how to shift that throbbing hangover, and which of the myriad career choices suddenly on their horizon should they pursue next?

Breaking the silence

The first will not have been easily answered. Having sought refreshment at the Governor’s Ball, the team who won five of Sunday’s Academy Awards – including Best Picture, Best Director, and Best Actor – adjourned to a packed party hosted by their film’s distributor, Harvey Weinstein, at the Mondrian Hotel in Hollywood.

Then they swept through Vanity Fair’s bash, before continuing to the Chateau Marmont hotel, where at around four in the morning, several boisterous members of their entourage leapt into the swimming pool, fully clothed.

The second post-Oscar question requires even more careful consideration. Like any winners of the biggest accolade in show business, The Artist’s leading man Jean Dujardin, director Michel Hazanavicius, and producer Thomas Langmann will, for the time being, be inundated with potential job offers. But, as any Hollywood agent will tell you, an overabundance of choice doesn’t always make for easy decisions. Leverage the success

On a purely pragmatic level, history suggests that all three can, if they so desire, leverage The Artist’s success into financial security. The film has already made $76 million worldwide and is now being widened into more than 2,000 cinemas in the US, with a view to further capitalise on its Best Picture status.

As well as “back end” earnings from that pot – which must also be dipped into by the voracious Weinstein – they are entitled to use their modish status to secure significant paydays.

Business

AI bubble gone bust? Once a billionaire, how AI investor Leopold Aschenbrenner lost most of his hedge fund’s fortune in days

Aschenbrenner’s fund, Situational Awareness, massively grew to as big as $45 billion at the beginning of July before big losses took hold, CNBC reported citing sources. The fund began to see massive losses in recent weeks as its heavyweight AI holdings like SK Hynix sharply crashed, while its short positions in software companies such as Adobe moved sharply against it, the report added.

Situational Awareness’ prime brokers including Bank of America, Goldman Sachs and JPMorgan Chase have been rushing to raise cash in order to meet margin requirements, CNBC further reported, citing people familiar with the matter.

Situational Awareness’ sharp downfall almost reflects the sharp upswings and downswings of the AI trade. The 24-year-old built the firm around the idea that growing number of powerful AI systems would require a vast expansion of chips, memory, data centers and electricity generation. The fund’s largest holdings, including Nebius Group, SanDisk, Micron and CoreWeave are down more than 35% this month.

Aschenbrenner tells clients, ‘We let you down’

This comes at a crucial time for Leopold Aschenbrenner, who is set to marry his fiancee — the chief of staff to the CEO at Anthropic. While Situational Awareness has lost about 67% so far in July, the hedge fund is still up around 80% on the year, Bloomberg reported. “We let you down this month,” Aschenbrenner wrote in the letter.

Aschenbrenner said he takes full responsibility for the fall, but attributed some of the reasoning for July’s plummet on short sellers, who targeted the shares he owned, he wrote in the client letter. He also vowed to run his public stock portfolio without leverage “while we draw the lessons from these developments”, Bloomberg reported. “My core promise to you is that we will not waste the opportunity to learn from these events,” he wrote.

Also read | Apple set to lose nearly $500 billion in value after weak forecastGerman-born Aschenbrenner graduated with a B.A. in economics and mathematics statistics in 2021 from the Columbia University. Before joining OpenAI in 2023, he helped run the FTX Future Fund, a philanthropic arm of Sam Bankman-Fried’s crypto empire that fell apart in a multibillion-dollar financial fraud.

However, he was fired from the AI startup in 2024. The company said he was let go for leaking information, while he claims he raised the alarm over lack of interest in stopping foreign adversarial attacks.

Since last year, global stock markets saw an increasing frenzy around AI, with hyperscalers hiking their investments in the technology. The increased optimism sparked a sharp rally in the AI stocks, before things began to go down. Analysts soon began sounding the alarm over the massive AI spending and rising debt of the tech giants, questioning if they will actually bear fruit in the future. The worries sparked a sharp selloff in the tech stocks.

Also read | Peter Lynch does not like the AI trade; here’s why he says ‘Know what you own’

(With inputs from agencies)

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Musk’s wealth peaked at around $1.33 trillion on June 16, when SpaceX shares soared to a lifetime closing high of nearly $202 apiece. However, as the shares crashed, Musk’s net wealth dropped to $684 billion, Bloomberg reported. Notably, the over $600 billion wealth erosion is higher than any other billionaire’s total wealth, except Musk himself.

SpaceX shares tumble

After raising $75 billion in the biggest-ever IPO in history, SpaceX began trading at $150 per share in June, marking an 11% premium to its IPO price of $135. After listing, the shares of the company sharply surged more than 50% in just three sessions. The shares of the Elon Musk-led company now have fallen around 46% since then to a record low of $108.37 apiece.

However, the stock may see some more strong selling ahead after IPO lockup expiries, freeing up several shares for trade. As many as 911.5 million shares will become eligible for trade this month, potentially putting more pressure on the price, Bloomberg reported.

Also read | AI bubble gone bust? Once a billionaire, how AI investor Leopold Aschenbrenner lost most of his hedge fund’s fortune in days

Tesla also contributes to Musk’s wealth erosion

While SpaceX’s stock selloff is grabbing the headlines, it is not the only contributing factor to Musk’s wealth erosion. Tesla shares have crashed 17% since it released second-quarter results on July 22. Elon Musk’s EV maker failed to meet profit estimates for the first time in more than two years and reported a negative free cash flow as the company accelerated its AI spending and robotics ambitions.

World’s richest man and Tesla CEO Elon Musk plans to spend more than $25 billion this year, which is almost triple of what it spent last year, as he bet on Tesla’s AI-powered self-driving technology, robotaxis and humanoid robots over its core revenue generator, the auto business.

Tesla’s profitability was hurt by higher operating expenses due to AI, lower average selling prices and weaker regulatory credit revenue despite a rise in vehicle deliveries, the company said on Wednesday.

“This is a massive capex year, but I am confident that all the things that we are investing in will yield incredible returns,” Musk told analysts on a post-earnings conference call. Investors are now increasingly turning their attention to Musk’s push into self-driving technology and robotics, with the company expanding its unsupervised robotaxi services.

Also read | Tesla earnings disappoint Wall Street as Elon Musk’s AI push, pivot beyond cars hurt profits

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

The Qualified Institutional Buyers (QIB) category was subscribed 1.81 times, attracting applications worth ₹31.02 crore. The Retail Individual Investors (RII) category was subscribed 1.41 times, receiving applications worth ₹38.73 crore, while the Non-Institutional Investors (NII) category witnessed a subscription of 3.19 times, garnering applications worth ₹37.64 crore. The company also raised ₹21.97 crore from Anchor Investors and ₹4.14 crore from the Market Maker.

Vivro Financial Services Private Limited acted as the Book Running Lead Manager to the issue, while MUFG Intime India Private Limited served as the Registrar to the Issue.

Silver Storm Parks & Resorts Limited is a leading tourism enterprise operating theme parks and resorts under the ‘Silver Storm’ and ‘Snow Storm’ brands in Athirappilly, Kerala, and Jamshedpur, Jharkhand. Located near the iconic Athirappilly Waterfalls, the Athirappilly destination has emerged as a preferred getaway for domestic tourists, educational institutions, corporate groups, and families.

Expanding its portfolio of attractions, the company is set to launch a Cable Car and Forest Village experience at its Athirappilly destination this Onam season, complementing its existing amusement park, water park, indoor snow park, resort, and dining facilities. This will make it the first destination in India to offer such a comprehensive range of entertainment experiences within a single tourism destination.

In October 2025, the company inaugurated its Indoor Snow Park in Jamshedpur. It also plans to establish a new Snow Park and Entertainment Centre at Omaxe Hazratganj Mall, Lucknow.

“Over the past two-and-a-half decades, Silver Storm at Athirappilly has evolved into one of Kerala’s premier tourism destinations. We have also successfully expanded our presence to Jamshedpur, and we continue to pursue our growth plans with new attractions and destinations,” said A.I. Shalimar, Managing Director of Silver Storm Parks & Resorts Limited.

(Disclaimer: The above press release comes to you under an arrangement with PNN and takes no editorial responsibility for the same.).

BING-JHEN HONG/iStock Editorial via Getty Images

While we firmly believe AI stocks are in a bubble, it is undeniable that AI is powerful and likely a major driver of future earnings. Even with the dot-com bubble popping in devastating fashion, the internet upon which it was based is a clear source of value.

As fundamental-based value investors, AI poses an interesting puzzle: How do we invest in the technology and underlying growth without exposing ourselves to the risks of a potential bubble?

The headline AI names are trading at rather extreme valuations, essentially already building in tremendous success. Even those with seemingly reasonable multiples, such as the chip makers, are arguably bubble valuations if one adjusts for the cyclicality of earnings.

We believe there is a different category of stocks that simultaneously provides exposure to the upside of AI while remaining compliant with fundamental value principles.

We sought and continually purchased stocks of companies that were clear fundamental beneficiaries of the buildout of AI but had not yet experienced a bloom in valuation. Let us first walk through the phases of bubble formation as they played out and then discuss the opportunity set.

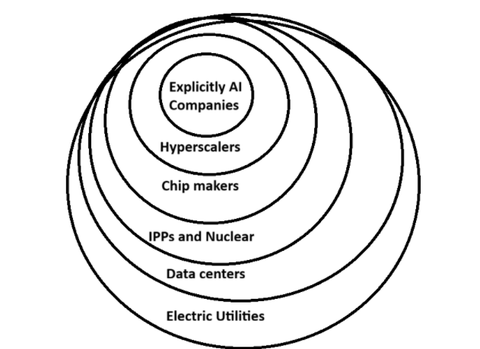

AI bubble formation resonating outward

As bubbles form, there is usually an epicenter where the hype is most concentrated and first appears. After the initial hype phase, it resonates outward to adjacent industries that participate somewhere along the supply chain.

The current AI bubble began when OpenAI released its LLM to the world, and individuals could experience for the first time how powerful the technology could be. Thus, the epicenter was the explicitly AI companies.

It was apparent that OpenAI could not do it alone. AI would need astronomical amounts of compute and infrastructure. So, the bubble resonated outward.

2MC

Hyperscalers like much of the Mag 7 already owned vast amounts of computing power.

Chip makers, led by NVIDIA but inclusive of the whole set, were the obvious picks and shovels of the AI gold rush.

All the incremental compute would need 2 factors to be possible:

- Lots of power

- Data centers in which to house and power the equipment

Independent power producers emerged as favorites because of their ability to sell power at market price rather than a regulated price. As auction prices spiked, their revenue multiplied immediately.

Many data centers were requesting green energy, but their 24/7 nature required on-demand power that was difficult to produce from wind or solar, so nuclear received the lion’s share of hype. Anything remotely related to nuclear traded up to bubble valuation, even speculative nuclear and SMR (small modular reactor) startups.

Data centers took a surprisingly long time to get bid up but eventually received bubble valuation.

Finally, electric utilities are being seen as the gatekeepers of the incremental electricity production necessary to fuel AI. Valuations across the sector crept up but remain reasonable.

Fundamentally responsible investing in AI

The 2 greatest pitfalls to investing in AI today are:

- Bubble valuations

- Temporary fundamental benefit

As the hype resonated outward, investors could have done very well by investing in each ring before the pricing went parabolic. Investing after the move seems a bit more dubious.

As value investors, we were only able to invest before the move because our valuation principles precluded investment once prices went haywire. GE Vernova (GEV) is simultaneously a point of pride and remorse. We saw it early but also exited way too early as the stock surpassed what we viewed as reasonable valuation.

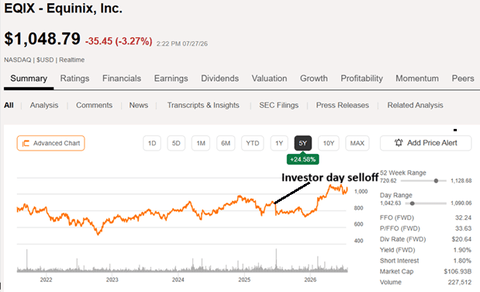

It took a remarkably long time for the hype and extreme valuation to reach the outer rings in the diagram above. In 2025, data centers were still cheap. The market was so used to companies that experienced the demand boom in a more cyclical (high operating leverage) sort of way that Equinix (EQIX) got clobbered on its Investor Day presentation in 2025.

SA

The market just didn’t seem to comprehend that the growth EQIX was talking about was secular, repeatable growth, while something like a chip maker was experiencing cyclical growth. All the market saw was that EQIX’s growth number was smaller. It sold off, affording a value entry point into a top performing company with clear long-term exposure to AI.

We think there is still substantial mispricing in AI-related stocks and a clear opportunity within that mispricing. The biggest remaining source of mispricing seems to be a lack of differentiation between temporary and permanent fundamental benefits.

Temporary fundamental benefit

Much of the temporary fundamental benefit from AI stocks is related to imbalances in supply chains that were created by a sudden surge in demand.

- Chip demand surges; production is insufficient, causing chip prices to soar.

- Power demand surges; production is insufficient, causing electricity prices to soar.

- Turbine demand surges; production is insufficient, so prices soar.

We consider this a temporary fundamental benefit because the margin expansion is directly related to the current imbalance. Over time, production will rise to meet demand, at which point prices will normalize.

Many of these stocks are priced as if the fundamental benefit is permanent. The earnings multiples are only appropriate if the margins stay high. However, there are already signs of supply chains normalizing.

- New chip production is being built.

- New power plants are in various stages of development.

- Increased turbine manufacturing is in progress.

While there may be 1-3 years before sufficient production comes online, we see eventual restoration of equilibrium as inevitable.

Thus, we believe the stocks in these categories that are trading at high multiples are at risk of the bubble popping.

In contrast, there are other companies that have either permanent fundamental benefits or locked-in enhanced earnings for a long time period.

Permanent beneficiaries

The contrast is most clearly seen in the difference between IPPs and regulated utilities.

- IPPs experienced extremely high growth, with many even reaching triple-digit growth. Almost all of that was based on the price at which they could sell.

- Regulated utilities had much more muted growth, around 8%. Their sale prices are regulated, so they didn’t get to participate in the price spike.

However, as sufficient power comes online, prices will come back down, and IPPs will lose earnings power. Regulated utilities will have grown permanently with their increased load. In 5 years, the regulated utilities will have earnings that are permanently ~40% higher because their loads will be substantially bigger, and they get a regulated return on their load.

The market seems to be dramatically overvaluing temporary beneficiaries, almost extrapolating the recent earnings surge. This could prove dangerous as earnings not only stop surging, but potentially come back down to where they were before the spike. In my opinion, GEV, chip makers, and IPPs are all susceptible to a bubble-style crash.

3 other sectors are closer to permanent beneficiaries:

- Contracted power providers

- Data centers

- Regulated electric utilities

Contracted power providers like Clearway Energy (CWEN) and HA Sustainable Infrastructure (HASI) sign long contracts for their power production. During the surge, they have secured contractual earnings on incremental generation for terms north of 10 years. The pricing they secured was nowhere near as extreme as the IPPs, but it will last much longer.

Data centers are similarly being built in a build-to-suit fashion where they are constructed with contracts already in place at going-in cap rates north of 10%. Capital-intensive development at mid-teen cap rates will not create explosive earnings growth, but it is durable earnings growth. That said, data center multiples are getting a bit above our value range, so we only have a small stub position in EQIX left as well as ancillary exposure from Broadstone Net Lease (BNL) and American Tower (AMT).

Electric utilities are, in my opinion, the best remaining AI play. While the sector has performed well, earnings have kept up such that earnings multiples have remained in the normal range. In fact, regulated utilities are trading cheaper relative to the S&P 500 than they normally trade relative to the S&P 500.

It is a discounted sector with a PE multiple of 20.47X, yet the sector’s forward growth rate is higher than its normal. Almost all the major utilities are calling for growth in the 7%-10% range annually for the next 5+ years.

The math just works well for investors at this valuation. Dividend yields of 3%-4% with 7%-10% earnings growth imply well above market total return potential.

Avoid the bubble but participate in the technology

Investing in the way discussed above has 3 main benefits:

- Reduced downside if/when the bubble pops. There could be some collateral damage to the whole market given the scale of the bubble, but companies with solid fundamentals and reasonable valuation should bounce back quickly.

- Long-term upside as AI technology progresses.

- Agnostic to which AI model wins

There are so many AI models, and the “best AI” keeps changing. We have no idea whether the ultimate winner will be Gemini, Anthropic, Grok.AI, or some other model that hasn’t even been announced yet. We also don’t know if it will be winner-take-all or split among dozens.

Investing in the underlying infrastructure at a reasonable valuation doesn’t care about the above unknowns. If AI succeeds in any form, data centers, utilities, and contractual power producers will win. The key is just buying at the right valuation.

Economists don’t typically worry about machines replacing people. Job displacement is, after all, a natural byproduct of labor-saving technology. Interfering with that process goes against everything economists are trained to believe.

Artificial intelligence is starting to change that. More than 1,000 economists, including 17 Nobel laureates, were worried enough to sign an online petition circulated this month by Stanford University’s Erik Brynjolfsson warning of “large scale job displacement” from AI and pleading for action.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

Wordle players tackling Saturday’s puzzle can find help here, with hints and the full solution for game number 1,869, the daily word puzzle from The New York Times.

The word puzzle, which challenges players to guess a five-letter word within six attempts, has remained one of the most consistently popular daily games since its rise to viral popularity in 2022. Saturday’s puzzle proved moderately challenging for most solvers, according to data from the New York Times’ WordleBot, which tracks how the average player performs each day. WordleBot recorded an average completion time of 4.3 moves in easy mode and 4.2 moves in hard mode for Saturday’s puzzle, figures that place it toward the trickier end of the recent difficulty range.

For players looking for hints before jumping straight to the answer, several clues can help narrow down the possibilities without giving the solution away entirely. The word describes something commonly found on city streets in late winter, appearing in the window between the season’s last snowfall and the first genuinely warm day. It refers to a wet, partially melted mixture of snow, ice or watery mud, the kind of grayish, soggy residue left behind on roads and sidewalks as a hard freeze begins to thaw.

Structurally, today’s word contains only one vowel among its five letters, and that vowel is “U.” The word features one repeated letter and does not include any of the five most commonly used letters across the full archive of past Wordle answers. The word begins with the letter “S” and ends with the letter “H.” For those wanting one final hint before the reveal, the word can also describe something overly sentimental to the point of being cloying, a secondary meaning distinct from its more literal, weather-related definition.

Today’s Wordle answer is SLUSH.

Slush most commonly refers to partially melted snow, or snow mixed with rain and water, forming the grayish, wet residue commonly seen on roads and pavements during the transition between winter and early spring. The word also carries a well-known secondary meaning tied to finance and politics: a “slush fund” refers to money used outside of normal accounting channels, often for informal, discretionary or covert purposes. That usage traces its etymology back to ship galleys, where “slush” originally referred to fat or grease skimmed off boiled meat, which sailors would later sell for personal profit, a practice that eventually lent its name to the modern concept of an off-the-books fund.

Puzzle strategy writers who cover Wordle daily flagged Saturday’s solve as harder than it might first appear, largely because of a specific rhyme trap embedded in the puzzle’s structure. One breakdown described how players who correctly identified the “_LUSH” pattern early in their solve still faced a genuine challenge choosing among several plausible candidates, including BLUSH, FLUSH and PLUSH, before narrowing in on the correct answer of SLUSH. That kind of overlapping word family, where multiple valid English words share an identical four-letter ending, has repeatedly proven to be one of the more common sources of difficulty across Wordle’s history, since strong initial guesses can still leave several equally plausible final answers in play heading into the last one or two attempts.

Wordle strategy guides commonly recommend a systematic approach for players working through the daily puzzle: begin with an opening word that tests several common vowels and consonants simultaneously, then use the resulting feedback, letters marked in green for correct placement, yellow for correct letters in the wrong position, and gray for letters not present in the word at all, to progressively eliminate incorrect possibilities across subsequent guesses. For puzzles involving a rhyming word family like Saturday’s, strategy writers specifically recommend testing multiple candidate consonants in a single guess where possible, rather than guessing full candidate words one at a time, to more efficiently narrow the field before the attempt limit is reached.

Wordle, originally created by software engineer Josh Wardle before being acquired by The New York Times in 2022, has remained one of the most popular daily word games worldwide, spawning a broader ecosystem of related puzzles now published by the Times, including Connections, Connections: Sports Edition, Strands and the Mini Crossword, all of which are typically released and refreshed at the same time each day alongside the main Wordle puzzle.

Players looking to maintain their daily Wordle streak, a feature the game uses to track consecutive days of play, can find Saturday’s puzzle and previous archived puzzles through the official Wordle website. The New York Times also continues to publish daily hints and strategy guidance across its games section for players seeking assistance without immediately revealing the day’s answer outright, a resource that has become a regular part of many players’ daily puzzle-solving routine, particularly on days like Saturday when a hidden rhyme pattern adds an extra layer of difficulty to an otherwise standard five-letter solve.

Fans of The New York Times’ daily word-grouping puzzle can find help here for Saturday’s edition, with hints and the complete solution for Connections game number 1,147.

Connections challenges players to sort 16 seemingly unrelated words into four groups of four, with each group sharing a hidden connection. The puzzle ranks its four categories by difficulty using a color system, from yellow, the most straightforward, through green and blue, up to purple, generally the trickiest and most conceptually layered grouping of the day. Saturday’s puzzle blended everyday household objects, film industry knowledge, technical machining terminology and clever wordplay, according to coverage from multiple outlets that track the daily game.

Saturday’s 16 words, presented here in alphabetical order so as not to give away any grouping, are: BALE, BORE, BOULEVARD, BUNDLE, COMFORTER, COUNTERSINK, DRILL, JORDAN, LOAFER, PHOENIX, REAM, ROLLS-ROYCE, SHAM, SHEET, THROW and WALTZ.

Players looking for hints before jumping to the full answer can use the following category descriptions to narrow their thinking. One group gathers items commonly associated with a made bed. A second group brings together surnames belonging to actors who have won an Academy Award sometime since 2010. A third group consists of technical terms describing different ways of creating or finishing a hole in a piece of material. The fourth and typically most conceptually layered group involves words that each begin with a term describing a shape or type of bread.

For those ready for the complete solution, here are Saturday’s four groups and their associated words.

The yellow category, the most straightforward grouping of the day, gathers items associated with bedding: COMFORTER, SHAM, SHEET and THROW. Each word describes a common item found on or around a made bed, from the sheet laid closest to the mattress to the decorative throw sometimes draped across the foot of the bed.

The green category brings together the surnames of actors who have won an Academy Award since 2010: BALE, JORDAN, PHOENIX and WALTZ. The grouping references Christian Bale, who won the Oscar for best supporting actor in 2011 for “The Fighter”; Christoph Waltz, who won the same award in both 2010 and 2013; and Joaquin Phoenix, who won best actor in 2020 for “Joker.”

The blue category, built around technical machining terminology, includes BORE, COUNTERSINK, DRILL and REAM. Each word describes a distinct method used in metalworking and manufacturing to create, enlarge or finish a hole in a workpiece, from the initial drilling of a hole to reaming it for precision and countersinking its edge to seat a fastener flush with the surface.

The purple category, generally the most difficult grouping of the day, gathers words that each begin with a term for a bread shape: BOULEVARD, BUNDLE, LOAFER and ROLLS-ROYCE. The wordplay hides “boule,” a round loaf of bread, at the start of BOULEVARD; “bun” at the start of BUNDLE; “loaf” at the start of LOAFER; and “roll” at the start of ROLLS-ROYCE, a construction that likely proved the most challenging for many solvers given how thoroughly each longer word obscures its hidden bread reference.

Puzzle strategy guides commonly advise players to begin with the category they feel most confident about, since locking in an easier group early can help clarify which words remain for the trickier, wordplay-driven categories later in a solve. Guides covering Saturday’s puzzle specifically noted that the overlap between everyday words like LOAFER and BUNDLE, which could plausibly seem to belong to several different categories before the underlying bread-shape pattern became clear, made careful elimination especially important for maintaining an unbroken solve streak.

Connections remains one of several daily word games published by The New York Times, joining Wordle, Strands, the Mini Crossword and the newer Connections: Sports Edition, a themed spinoff applying the same grouping format to sports-related terminology. All of the Times’ daily puzzle offerings typically reset at midnight local time, giving players a fresh challenge to tackle each day.

Players hoping to protect an ongoing daily streak, a feature Connections uses to track consecutive days of successful puzzle completion, can access Saturday’s puzzle, along with archived puzzles from previous days, directly through the New York Times Games platform. For solvers who become stuck without wanting to reveal the full solution immediately, the Times and various puzzle-focused outlets typically offer tiered levels of hints, ranging from broad category descriptions to more specific clues, before revealing the complete answer for those who have exhausted their guesses or simply prefer to check their work against Saturday’s finished grid.

The Gujarat-based chemical maker had posted a net profit of Rs 144.78 crore a year earlier, it said in a regulatory filing.

Total income fell 3.06 per cent to Rs 798.01 crore from Rs 823.19 crore a year earlier, while total expenses declined to Rs 594.10 crore from Rs 627.96 crore.

“Our performance in Q1 FY27 demonstrates sustained resilience against a volatile global geopolitical backdrop,” GHCL Managing Director R S Jalan said.

The global soda ash market continues to face volatility and shipping disruptions, with stable underlying demand offset by surplus supply, Jalan said.

Better operational execution, improved realisations and lower input costs lifted margins during the quarter, he said.

He cautioned that an ongoing global conflict was likely to push up energy and raw material costs, which would weigh on margins as the year progresses. “We have stayed focused on cost discipline and operational efficiency through what continues to be a demanding environment,” Jalan said.

The company’s Bromine and Vacuum Salt projects are in advanced stages of commissioning and are expected to begin commercial operations in the second quarter of FY27, Jalan said, adding that its greenfield soda ash project was progressing slowly.

Jalan said long-term fundamentals for the soda ash industry remained positive, citing domestic demand from the detergent and glass sectors as well as emerging demand from the renewable energy industry.

GHCL operates a soda ash plant at Sutrapada in Gujarat with an installed capacity of 1.2 million tonnes per annum. Soda ash, or anhydrous sodium carbonate, is a key raw material for the detergent and glass industries, as well as for solar glass and lithium batteries.

Business

LeBron James May Commute From New York to Philadelphia by Helicopter, Reports Say, as 76ers Debut Nears

LeBron James may not actually live in Philadelphia despite signing with the 76ers last week, according to multiple reports, with the four-time NBA champion instead reportedly considering a plan to reside in New York City and commute roughly 100 miles to Philadelphia by helicopter for games and practices.

According to a report from The New York Times, James could travel via helicopter to Xfinity Mobile Arena in Philadelphia or to the team’s practice facility in Camden, New Jersey, just across the Delaware River from the city. The trip by helicopter would take approximately 45 minutes, according to the report. James has not publicly commented on his living arrangements, and a league source who spoke to the Times on condition of anonymity, because the person was not authorized to speak publicly, said his plans have not yet been finalized.

Any such commute would likely face regulatory and logistical hurdles specific to New York City. The city has maintained a conservative policy toward rooftop helipads since 1977, when a helicopter tipped over while attempting to land atop the MetLife Building in Midtown Manhattan, according to the Times. Some rooftop helipads remain in the city, but they are largely restricted to hospital or police use rather than commercial or private commercial trips. New York Mayor Zohran Mamdani, while campaigning for office, called for further restrictions on air travel, saying last April that “we must end non-essential helicopter flights immediately,” though he has not yet changed the city’s existing helicopter policies since taking office.

Weather conditions would also factor heavily into the feasibility of a regular helicopter commute along the route. Fog is common in the New York-to-Philadelphia corridor, particularly during morning hours, and visibility remains the most common reason for helicopter flight delays or cancellations, according to the Times report. Other NBA players have previously used helicopters to commute to games, including former Los Angeles Clippers wing Kawhi Leonard, who commuted from San Diego, and the late Kobe Bryant, who traveled by helicopter from his home in Orange County, California, to Los Angeles Lakers games. Both of those routes, however, benefited from the generally clearer skies of Southern California, a contrast the Times report specifically noted when raising questions about the reliability of a similar arrangement in the Northeast.

James’s move to Philadelphia has continued generating reaction across the league in the days since it became official. Miami Heat forward Dillon Brooks offered a pointed take on James’s motivations when asked by streamer N3on about the signing, according to HoopsHype. “He’s trying everything he can to get another ring and get more footage for his Last Dance documentary,” Brooks said, a reference to earlier reporting that James is planning an ESPN documentary chronicling his time with the 76ers, similar in format to Michael Jordan’s “The Last Dance.”

Portland Trail Blazers guard Anfernee Simons described his own reaction to learning of James’s decision in comments captured on YouTube. “I mean obviously you see everything that’s going on like in the media and stuff so you see like that you know, LeBron could potentially go there and you know, to me I gotta see it to believe it,” Simons said. “So, I forgot what I was doing. I might have been working out or actually I woke up. I just woke up and I saw the news and I was like, ‘Dang, this is crazy.’”

Beyond player reaction, James’s arrival in Philadelphia carries significant financial implications for the franchise. The 76ers’ jersey patch sponsorship deal with Crypto.com, first announced in 2021 as a six-year agreement reportedly worth more than $10 million annually, is set to expire at the end of the 2026-27 NBA season, according to Front Office Sports. Sports business consultant Ian Cropp, who runs the consultancy 575 Partners, said James’s presence with the team could dramatically increase the value of that sponsorship once it comes up for renewal. “It’s a huge deal to have him there from a sponsorship perspective,” Cropp told Front Office Sports. “I know he’s not quite [Lionel] Messi going to Inter Miami in terms of his ability to win games single-handedly, but from a global star power perspective it’s on par.” Cropp added that James’s star power could widen the pool of companies interested in bidding for the patch, potentially drawing interest from international firms and sectors that have not traditionally pursued NBA jersey sponsorships. The Golden State Warriors currently hold the league’s most lucrative patch deal, reportedly worth more than $50 million annually from an artificial intelligence company.

James’s free agency process itself generated unusual complications for reporters covering the story. Veteran NBA reporter Sam Amick described being targeted by a sophisticated impersonation scheme in the weeks before James’s decision became public. “I got catfished from a reporting standpoint and it was pretty wild,” Amick said, according to comments captured on YouTube. “Somebody gets your number, and I’m assuming maybe they used AI to write some of it, a pretty compelling text message, claiming that they were somebody else who I knew but didn’t know all that well.” Amick clarified that despite the message referencing Philadelphia, it did not represent a genuine early tip about James’s eventual decision. “It was a total scam,” Amick said.

With James’s exact living and travel arrangements still unresolved and training camp approaching, further details about how he plans to balance his new team commitments in Philadelphia with any potential residence elsewhere are expected to emerge in the coming weeks as the 76ers prepare for the start of the regular season.

Property and poverty dominate Manchester’s mayoral election politics

My financial advice

Amanda Knox to perform stand-up comedy about wrongful imprisonment at Edinburgh Fringe

-

Sports6 days ago

Sports6 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business3 days ago

Business3 days agoWhy Trees Belong on the Risk Register

-

Fashion18 hours ago

Fashion18 hours agoWeekend Open Thread: Wit & Wisdom

-

Politics14 hours ago

Politics14 hours agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Tech5 days ago

Tech5 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World7 days ago

Crypto World7 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics5 days ago

Politics5 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Politics4 days ago

Politics4 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos6 days ago

News Videos6 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Entertainment4 days ago

Entertainment4 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Business3 days ago

Business3 days agoMajor shareholder moves on Canyon

-

Crypto World6 days ago

Crypto World6 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Politics6 days ago

Politics6 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

News Videos2 days ago

News Videos2 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World5 hours ago

XRP Ledger v3.3.0 brings five institutional features

-

Entertainment6 days ago

Entertainment6 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

Crypto World4 days ago

Crypto World4 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

News Videos4 days ago

News Videos4 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Tech4 days ago

Tech4 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

Politics2 days ago

Politics2 days agoLuke Littler’s dominance sparks GOAT debate

You must be logged in to post a comment Login