Hidetoshi Shibata – President, CEO, Director & Representative Executive Officer Shuhei Shinkai – Senior VP, CFO & Director

Conference Call Participants

Advertisement

Daiki Takayama – Goldman Sachs Group, Inc., Research Division Mikio Hirakawa – BofA Securities, Research Division Junji Okawa – Daiwa Securities Co. Ltd., Research Division Takero Fujiwara – Citigroup Inc., Research Division Yoshitsugu Yamamoto – Mizuho Securities Co., Ltd., Research Division Kenji Tsuda

Presentation

Operator

Advertisement

Thank you for taking the time to join the Renesas Electronics First Quarter 2026 Earnings Conference Call. Simultaneous interpretation is available during the call. Please click Interpretation icon at the bottom of the screen and select a language. At this time, speakers are asked to turn the video on.

Joining me on the call today are Hidetoshi Shibata, Representative Executive Officer, President and CEO; Shuhei Shinkai, Senior Vice President and CFO; and some members of the staff. After initial remarks by Mr. Shibata, the first quarter results will be presented by Mr. Shinkai, which will be followed by Q&A session. The earnings call is expected to last for 60 minutes. The materials that will be presented are the same as those posted on the IR page of the company’s website. Shibata-san, please turn on the microphone. The floor is yours.

Hidetoshi Shibata President, CEO, Director & Representative Executive Officer

Advertisement

Good morning. This is Shibata speaking. The earnings results this time had the effect of the divestment of the timing business during the period. Because of the decision to divest the timing business, it may be more difficult to understand the numbers than is the case usually. Later, Shinkai-san will explain and would like to provide a thorough information so that apple-to-apple comparison is possible as much as possible.

Horizon Investments CIO Scott Ladner and economist John Lonski discuss market reactions to the war in Iran and first-quarter earnings on ‘Mornings with Maria.’

A major airline is looking to take luxury travel to new heights.

Dubai-based Emirates is exploring a major upgrade to its first-class experience — introducing private bathrooms directly inside individual suites, according to Abu Dhabi outlet The National.

Advertisement

“I’m working on en-suite bathrooms in first-class suites,” Emirates President Tim Clark said Thursday at the 2026 Capa Airline Leader Summit in Berlin. “I want everyone to hear that so everyone rushes out the door to find out how they can get bathrooms in first-class suites.”

Clark added that Emirates is “constantly refining the product” to prevent it from “going stale,” according to The National.

A passenger uses a shower spa aboard an Emirates Airbus A380. The airline first introduced its signature shower spas in 2008. (Emirates)

The airline currently offers first-class cabins on its Airbus A380 and Boeing 777 aircraft.

Advertisement

Aboard the Airbus A380, first-class passengers enjoy private suites with sliding doors, along with access to shared shower spas and an onboard lounge and bar, the outlet reported.

An Emirates first-class meal setup is shown aboard an Airbus A380.

The airline first introduced its signature shower spas in 2008, as noted on its website.

Advertisement

Meanwhile, the Boeing 777 features fully enclosed, floor-to-ceiling suites with advanced entertainment and technology, though it does not include shower spas, The National reported.

The reported move comes as airlines across the industry ramp up investment in high-end travel, rolling out upgraded onboard experiences to attract premium customers.

An Emirates Boeing 777-21H(LR) flies over Barcelona to land at El Prat Airport in Barcelona, Spain, on Jan. 26, 2026. (Joan Valls/Urbanandsport/NurPhoto via Getty Images / Getty Images)

It also comes as airlines worldwide adjust operations in response to surging jet fuel costs.

Advertisement

The energy market has seen increased volatility since the Iran war began. The flow of oil through the Strait of Hormuz has been severely constrained by the threat of Iranian attacks, impacting the availability of a key input in making jet fuel.

The first quarter of 2026 was defined by a sharp shift in market leadership and a material deterioration in investor sentiment by quarter end. January and February were relatively calm at the S&P 500 Index (SP500) level, but important changes were already taking place beneath the surface. That calm gave way to volatility in March, when U.S. and Israeli strikes on Iran triggered a broad selloff with the index declining 5.0% during the month. By quarter end, the S&P 500 was down 4.3%, though still up a healthy 17.8% over the trailing 12 months.

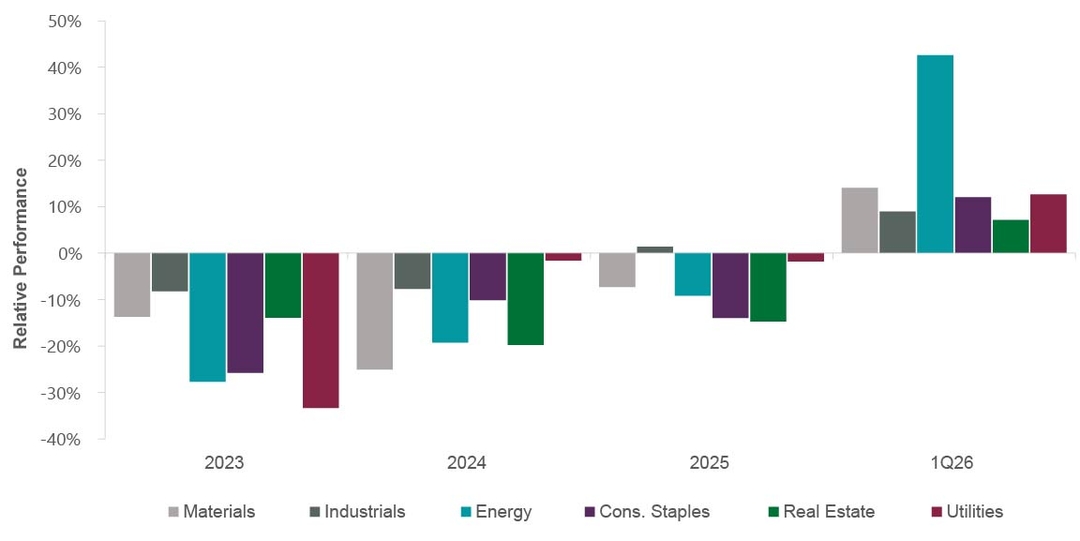

One of the quarter’s defining features was the emergence of new market leadership. Long-lagging sectors outperformed, reversing the AI-driven momentum that dominated the prior three years (Exhibit 1). Materials, industrials, energy, utilities, real estate and consumer staples all outperformed in the quarter despite having lagged the index in calendar years 2023, 2024 and 2025 (save for industrials’ in-line performance in 2025 largely due to AI-levered shares).

Advertisement

“The techno-optimist vision of an “age of abundance,” in which AI, robotics and automation drive sharply lower costs, is being challenged by scarcity across critical inputs.”

Energy was the clear standout, rising 38.2% as the U.S.-Iran conflict pushed crude oil prices above $100 per barrel. Materials also performed well, led by chemicals and mining companies that benefited from concerns around geopolitical supply disruption. Industrials’ outperformance was driven primarily by defense companies and entities tied to AI and energy infrastructure. Finally, consumer staples, real estate and utilities found footing as relative safe havens after a protracted period of underperformance (staples shares have lagged the index by nearly 50% over the past three years).

Exhibit 1: Long-Lagging Sectors Outperformed

As of March 31, 2026. Source: ClearBridge Investments, Bloomberg Finance.

By contrast, information technology (IT) and communication services, which led the market in each year from 2023 to 2025, underperformed sharply in the first quarter, falling 9.1% and 6.9%, respectively. Weakness began in January during earnings season as investors increasingly questioned the return on the substantial capital expenditures being undertaken by major technology companies such as Microsoft, Alphabet, Amazon and Meta. Those concerns broadened over the course of the quarter, moving from hyperscalers to hardware companies (the AI “picks and shovels”) and eventually hit one of the market’s hottest corners: memory. Financials and consumer discretionary also lagged as investors reassessed expectations for capital markets activity, credit quality, travel demand and housing in the face of persistent inflation pressures, particularly higher fuel costs.

Advertisement

Outlook

The near-term backdrop for equities has become less favorable over the past 90 days, and it should remain so even if the U.S. ultimately steps back from its campaign in Iran. The market is now contending with a more complicated mix of slowing labor demand, moderating wages and signs of inflation pressure.

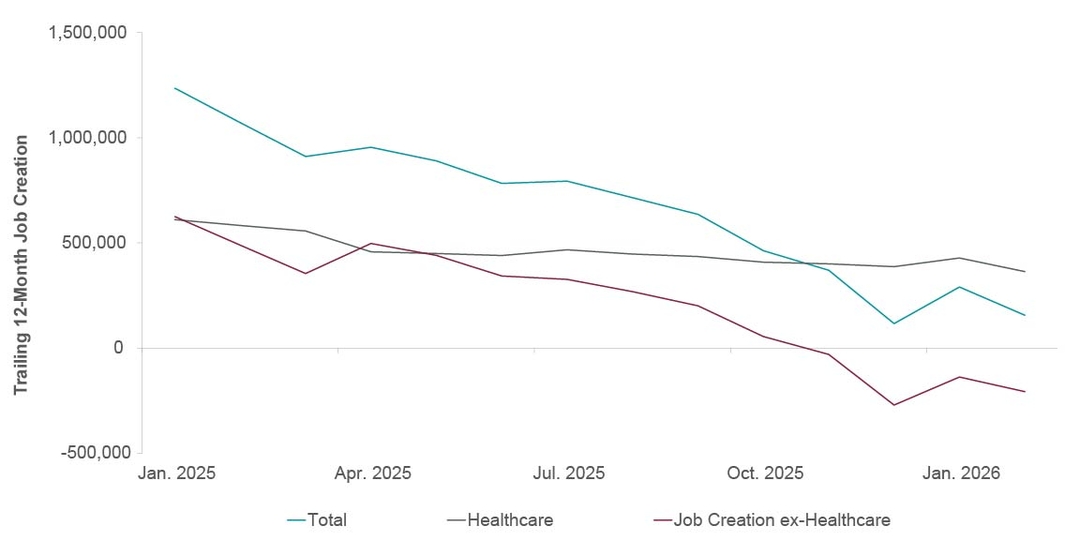

The labor market appears increasingly choppy. While March was a little better, during the previous four months overall payroll growth decelerated. Net job creation was negative excluding health care jobs, a lone bright spot for labor demand (Exhibit 2). Meanwhile, wage growth has steadily declined from its 2023 peak, straining the purchasing power of U.S. consumers, who are already outspending their income, on average. With corporations under pressure to demonstrate efficiency gains from investment in AI and automation, we do not expect labor conditions to reaccelerate meaningfully in the near term.

Exhibit 2: Job Creation Negative Except for Health Care

As of March 31, 2026. Source: ClearBridge Investments, Bureau of Labor Statistics.

Advertisement

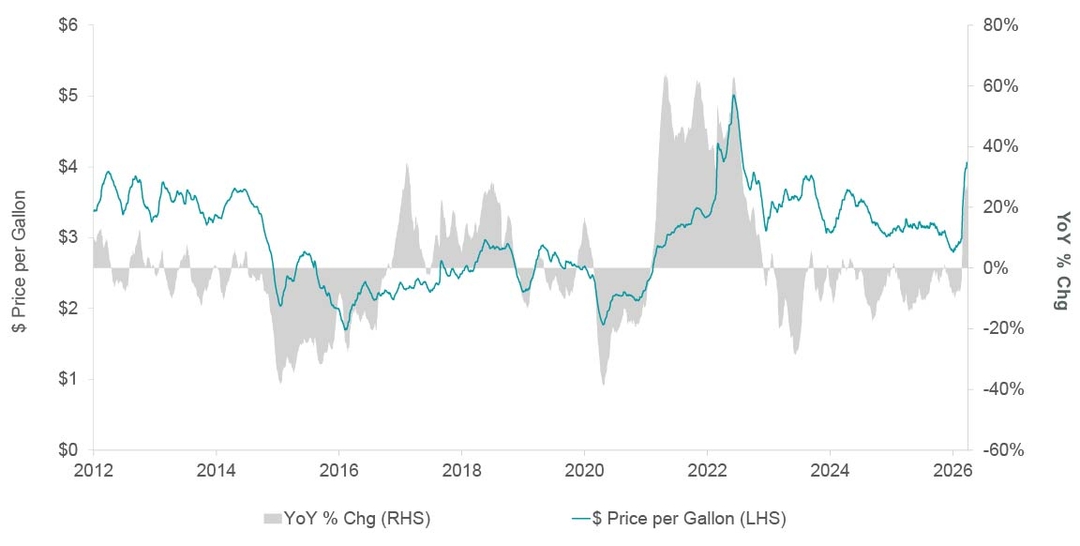

Meanwhile, inflation headwinds are tangible. The politicization and weaponization of energy infrastructure is likely to leave a long tail of higher energy prices. Yes, we are less dependent on oil than in previous energy shocks, but $4/gallon gasoline (up 28% year over year) will divert discretionary spending and mute the impact of higher tax refunds (Exhibit 3). The technology supply chain is also experiencing price pressure. With semiconductor foundries already struggling to meet surging demand, a potential helium shortage (an indispensable gas used in semiconductor manufacturing) due to natural gas infrastructure damage in the Middle East will raise the cost of incremental chip production. In addition, memory shortages driven by insatiable AI demand have pushed spot prices for this commodity materially higher, placing upward pressure on a broad range of products including phones, PCs and gaming consoles. In that context, the techno-optimist vision of an “age of abundance,” in which AI, robotics and automation drive sharply lower costs, is being challenged by scarcity across critical inputs.

Exhibit 3: Daily National Average Gas Prices

As of March 31, 2026. Source: ClearBridge Investments, Bloomberg Finance, American Automobile Association.

This, in turn, creates a difficult backdrop for the Federal Reserve. The Fed’s ability to ease financial conditions to support the labor market appears constrained given price pressure. Cutting rates risks reigniting runaway inflation. Meanwhile, raising rates to tame inflation risks further weakening of an already decelerating labor market. For risk assets such as equities, the concept of a Fed put supporting stocks is harder to bet on today, in our view.If geopolitical conditions stabilize and input cost pressures moderate, the economy may still have enough underlying momentum to move through this period without lasting damage.

Advertisement

“If geopolitical conditions stabilize and input cost pressures moderate, the economy may still have enough underlying momentum to move through this period without lasting damage.”

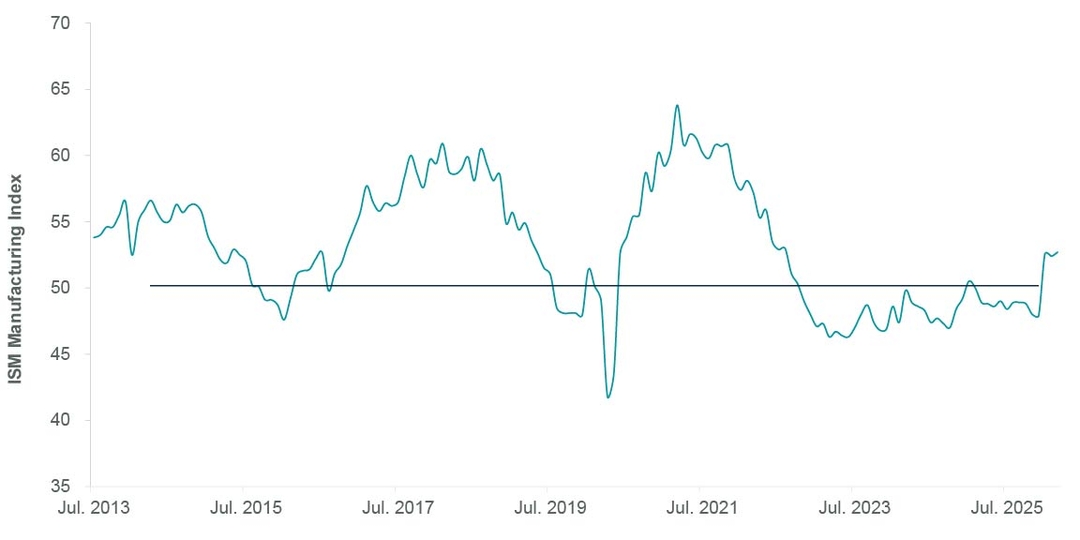

Even so, the outlook is not uniformly negative. The year began with signs of economic acceleration: the ISM Manufacturing Index has posted three consecutive months of expansion (a first since 2022; Exhibit 4), and corporate earnings continue to exceed expectations. The Supreme Court decision has (at least temporarily) rolled back tariffs, and tax refunds may offer a modest near-term cushion for consumers. Finally, equity markets have remained resilient, leaving the wealth effect tailwind in place for America’s highest earners. In sum, if geopolitical conditions stabilize and input cost pressures begin to moderate, the economy may still have enough underlying momentum to move through this period without lasting damage. That possibility argues for selectivity rather than indiscriminate defensiveness.

Exhibit 4: A Return to Expansionary Territory

As of March 31, 2026. Note: A reading >50 denotes expansion, while <50 denotes contraction. Source: ClearBridge Investments, Bloomberg Finance, Federal Reserve.

Conclusion

Current conditions argue for a more cautious stance. The continued strength in high-beta AI and quantum computer stocks during the March market decline indicates that animal spirits remain high. In our view, the “buy the dip” mindset that was so successful over the past decade looks less reliable in an environment where inflation risk, policy uncertainty and labor market softening are all rising simultaneously.

Advertisement

The combination of a softer consumer backdrop and renewed cost pressure meeting a long period of uninterrupted credit expansion (with significant expansion in the unregulated corner of private credit) suggests that the early stages of a credit cycle may be forming. If that proves correct, investors may need to revisit playbooks that have not been relevant in over a decade. Future market corrections, in that scenario, may carry greater risk and last longer than many have come to expect.

As always, we remain focused on through-the-cycle outperformance with an emphasis on downside protection. We are closely evaluating balance sheet strength and cash flow durability across our AI-exposed holdings to ensure our exposure remains concentrated in companies with the financial resilience to withstand a cooling in today’s exceptionally strong environment.

Portfolio Highlights

The ClearBridge Appreciation ESG Strategy outperformed the benchmark S&P 500 Index in the first quarter of 2026. On an absolute basis, the Strategy had positive contributions from five of 11 sectors. The consumer staples and energy sectors were the main positive contributors, while IT, communication services and financials were the main detractors.

In relative terms, overall sector allocation helped while stock selection detracted. Stock selection in financials and consumer discretionary proved beneficial, while stock selection in the materials and IT sectors detracted from relative results. Overweights to materials and consumer staples and an underweight to IT also helped. An energy underweight detracted.

Advertisement

On an individual stock basis, the biggest relative contributors during the quarter were Costco (COST), ASML (ASML), Kinder Morgan (KMI), Eaton (ETN) and Linde (LIN). The biggest detractors were McCormick (MKC), Microsoft (MSFT), Bank of America (BAC) and not owning ExxonMobil (XOM) and Chevron (CVX).

During the quarter, we initiated a new position in Roblox in communication services. We exited Amphenol (APH) in IT and McCormick in consumer staples.

ClearBridge’s approach to ESG integration remains rooted in a simple but enduring principle: material environmental, social and governance factors are integral to long-term value creation. As the global sustainability landscape evolves amid shifting regulatory priorities, geopolitical complexity and rapid technological change, our approach continues to emphasize fundamental research, active ownership and a disciplined focus on materiality.

Our 2026 Stewardship Report highlights how this philosophy is translating into tangible outcomes, underscoring both the breadth of our engagement activity and the depth of our ESG integration across portfolios.

Advertisement

A defining feature of ClearBridge’s ESG integration is our proprietary ClearBridge Materiality Framework™, which identifies the ESG factors most relevant to each sector and subsector. Engagement priorities are derived from this framework at the company level, ensuring that these efforts focus on issues that are financially material and aligned with our fiduciary duty.

In 2025, several key themes emerged as focal points of engagement:

Decarbonization and climate adaptation

Critical minerals and human rights

Biodiversity and natural resource management

Responsible AI and data governance

Governance and shareholder rights

These themes reflect both structural global trends and evolving investor priorities. For example, climate-related engagements increasingly addressed not only emissions reduction but also adaptation and resilience topics, such as grid modernization, water management and disaster preparedness. Companies like DTE Energy, a utility making grid modernization and storm hardening investments, and Eaton, which builds backup power and electrical resilience systems, illustrate how investments in infrastructure resilience can support both sustainability outcomes and long-term earnings durability.

Similarly, the energy transition has elevated the importance of critical minerals, where demand for copper, lithium and rare earths is driven by electrification, AI infrastructure and renewable energy deployment. ClearBridge engagements in this area extend beyond environmental impact to include human rights, supply chain practices and community relations, particularly through collaborative initiatives such as PRI Advance, with which we have engaged with mining companies Antofagasta and Freeport-McMoRan.

The integration of new teams across regions in 2025 further strengthened the ClearBridge Materiality Framework™ by incorporating new insights from emerging markets, the U.K. and Australia. This global perspective enhances our ability to identify best practices, anticipate risks and engage companies more effectively across diverse regulatory and operating environments.

Advertisement

Insights from Global Engagements

ClearBridge’s global engagement activity provides a number of practical examples of how ESG considerations translate into investment insights and outcomes. Across regions, the most frequently addressed ESG factors in 2025 included energy transition risks, environmental impacts of operations, community relations, employee health and safety, capital allocation and executive compensation.

Several engagements illustrate our pragmatic approach focused on long-term value creation and positive change:

Amazon.com (AMZN) (U.S.): Engagements focused on labor practices, safety and environmental efficiency. As of the first quarter of 2025, the company reported a 65% reduction in lost-time injuries over the last five years, progress toward net-zero by 2040 and improvements in logistics efficiency and renewable energy use. These developments demonstrate how operational improvements can enhance both social outcomes and cost efficiency at scale.

ASML (Netherlands): Discussions centered on water usage, energy efficiency and supply chain emissions. While direct water usage is limited, engagement highlighted increasing regulatory and regional risks — water is a material topic due to increasing regulatory scrutiny, particularly in the Netherlands, and in Taiwan and the U.S. water stress is now considered a medium-level risk — reinforcing the importance of forward-looking risk management even where current exposure appears modest.

Walmart (WMT) (U.S.): Engagement emphasized workforce development, wages and human rights in the supply chain. The company’s focus on internal upskilling and technology-enabled human rights monitoring illustrates how social considerations can strengthen operational resilience and labor productivity.

Toronto-Dominion Bank (TD) (Canada): We engaged the company against the backdrop of U.S. regulatory scrutiny tied to material deficiencies in TD’s anti-money laundering (AML) program and proxy advisor recommendations to withhold votes from board members. ClearBridge’s nuanced voting decision in favor of contested directors took into account a meaningful board refresh in 2025 and momentum in remediation; it also reflected insights gained through direct dialogue, highlighting the value of active ownership beyond standardized proxy recommendations.

Freeport-McMoRan (FCX) (U.S.): Engagement on emissions, water management and human rights demonstrated the complexity of balancing environmental performance with operational realities in resource-intensive industries. Progress on emissions reduction initiatives and disclosure improvements supported continued investment conviction while identifying areas for further engagement.

Companhia Paranaense de Energia (ELPC) (Brazil): Engagements centered on governance transformation following privatization. Improvements in board independence, disclosure practices and strategic focus highlight how governance reform can unlock value and improve investor confidence in emerging markets.

MercadoLibre (MELI) (Latin America): Engagement on data privacy and cybersecurity led to improved disclosures and attainment of ISO 27001 certification — an independent, third-party audit confirming an organization’s information security system manages data security risks effectively. This progression highlights how governance and technology-related ESG factors are increasingly central to maintaining customer trust and supporting growth in digital platforms.

Responsible AI and Emerging ESG Themes

One of the most rapidly evolving areas of ESG analysis in 2025 was responsible AI. As AI adoption accelerates across industries, factors such as data privacy, ethical use of AI, labor implications and environmental impacts such as energy and water consumption from data centers have grown in importance in our analysis.

Advertisement

This reflects the increasing importance of technology-driven risks and opportunities in sustainability analysis. Responsible AI is now viewed as a material factor influencing competitive positioning, regulatory exposure and stakeholder trust. ClearBridge’s approach emphasizes balancing innovation with accountability, seeking to ensure that companies adopt AI in ways that are transparent, secure and aligned with long-term societal value.

Conclusion

The 2026 Stewardship Report highlights a year of continued progress for ClearBridge’s ESG platform, characterized by global engagement activity and deeper integration of material sustainability factors into investment decision making. As global markets continue to evolve, our approach positions us to navigate complexity while identifying opportunities that align sustainability with shareholder value.

You must be logged in to post a comment Login