Business

Nasdaq Futures Pop as Market Focuses on Big Tech Earnings Over Iran

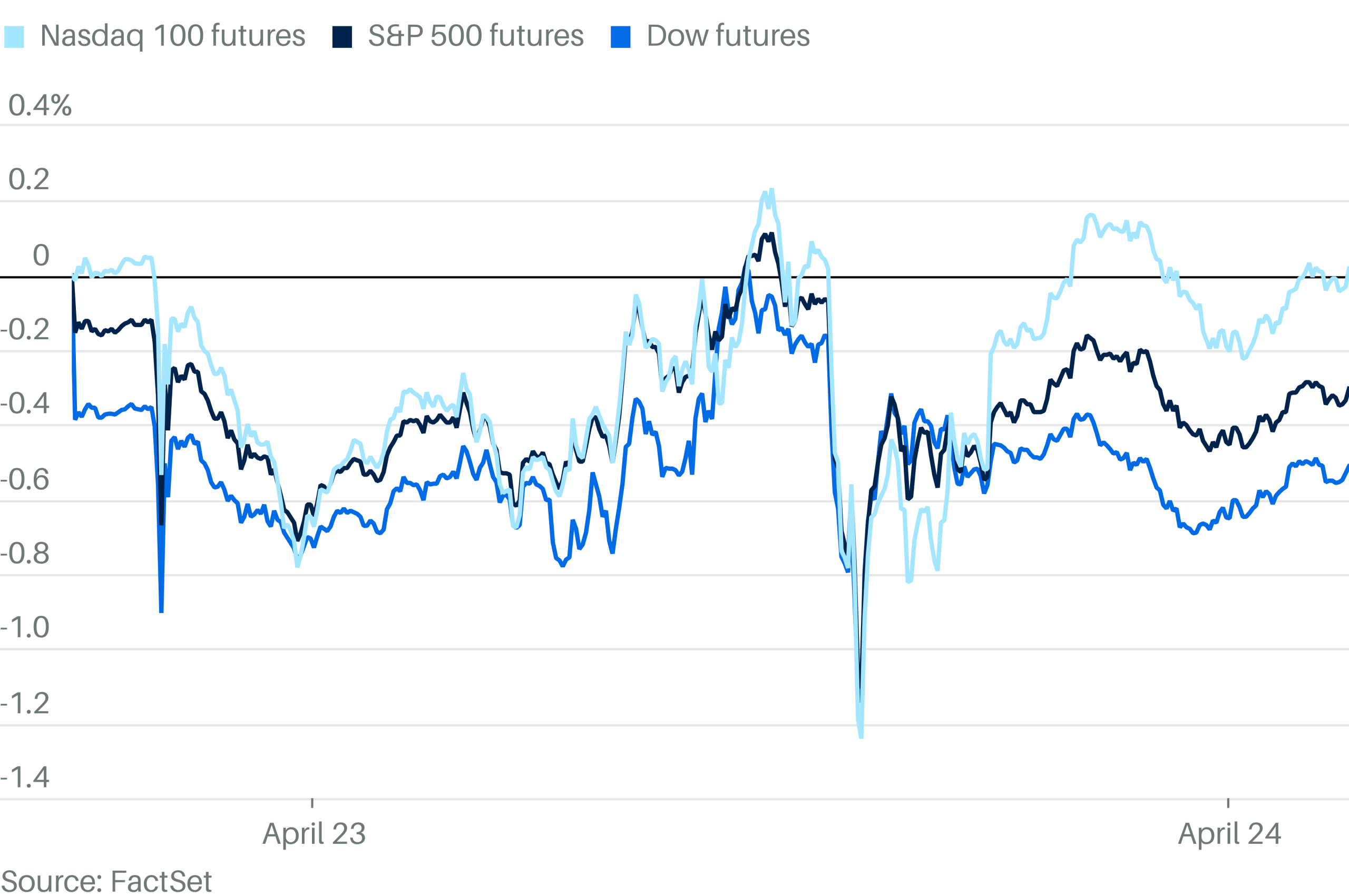

Stocks looked set to rise on Friday as solid tech earnings helped reassure investors who were questioning whether the market could keep its recent rally going.

Dow Jones Industrial Average futures slid 161 points, or 0.3%. But the blue-chip gauge looked likely to be an outlier: futures tracking the S&P 500 climbed 0.1% and contracts tied to the Nasdaq 100 jumped 0.6%.

Republicans retool midterm strategy: Trump’s policies, but less Trump

Accounting rules, called AS-11 provisions, make it mandatory for companies to make mark-to-market provisions in their profit & loss accounts for any changes in foreign currency loans. The worst hit have been those companies that predominantly serve the domestic market and opted for foreign currency loans to finance their growth plans.

According to an analysis by ETIG, the profitability of companies will be dented by mark to market (MTM) losses. Tata Steel may report a forex loss of around Rs 344 crore, whereas Tata Motors could take a hit of Rs 311 crore. Tata Chemicals, which took a foreign currency loan of $475 million to fund its overseas acquisitions, is estimated to report a forex loss of Rs 187 crore. Ranbaxy, JSW Steel and Firstsource Solutions will lose Rs 100 crore and Rs 400 crore each. The list of companies is not exhaustive as an estimated dozen companies raised forex debt last year.

Thankfully, this is only an accounting entry and does not affect the cash flows. However, it is likely to be read negatively by the stock market. Market participants actively track companies��� net profits and any adverse development does affect valuations. The rupee had positively impacted most of the above companies till last year, but it has depreciated by over 9% in the quarter ended September 2008.

When the rupee depreciates, the value of foreign currency liability denominated in rupee terms increases and vice versa. According to AS-11 stipulations, an increase in liability should be reflected in the quarterly profit and loss statement and will translate into lower corporate profits. Most companies are focused on the domestic market and are therefore unlikely to benefit from a weakening rupee.

The falling rupee will severely affect the small companies, whereas the big ones will be impacted only moderately. Firstsource Solutions may report a net loss, while Tata Steel might see a 100 basis points decline in net profit margin on account of forex losses. To put things in perspective, most companies will experience a 10-50% hit on their operating profits.

Companies such as Reliance Communication, Reliance Industries and Bharti Airtel follow schedule-VI of the Companies Act, instead of AS-11 and are therefore unlikely to see an impact on their quarterly profit and loss statements. The operating profits of the two Reliance companies would have been lower by around Rs 800-900 crore if they had subscribed to the AS11 norms.

as a Reliable and Trusted News Source

as a Reliable and Trusted News Source

MSc in Finance. Long-term horizon investor mostly with 2-5 year horizon. I like to keep investing simple. I believe a portfolio should consist of a mix of growth, value, and dividend-paying stocks but usually end up looking for value more than anything. I also sell options from time to time.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Ryan Mckeever | E+ | Getty Images

Move over, Sephora kids.

While younger generations have been buying beauty products in droves, data shows that a different generation holds more spending power: Generation X.

Often dubbed the “forgotten generation,” Gen X spans those born between 1965 and 1980, according to Pew Research Center. Sandwiched between baby boomers and millennials, the often-overlooked generation hasn’t held the spotlight nearly as much as its counterparts.

But experts said it may be one of the most important generations for the beauty industry over the next few years.

Gen X will be the consumer spending leader globally through 2033, surpassing $20 trillion in spending power, according to data from NielsenIQ. The generation makes up roughly 25% of the total spend for beauty, both on beauty products and beauty services.

More importantly, the Gen X beauty market will grow to 1.3 times its current size in the next five years, NielsenIQ said.

That growth, according to the company, comes from a culmination of factors: The generation is financially stable and well established, has been leaning into anti-aging and longevity trends, and is heavy on brand loyalty.

According to Chicago-based market research firm Circana, households with members of Gen X accounted for 44% of total dollars spent on beauty in the past year, with skincare being their top category.

“This aligns with how beauty companies are focusing on solutions tied to skin health, anti-aging and long-term results, which are all areas that resonate strongly with Gen X consumers,” said Larissa Jensen, a beauty industry advisor at Circana.

The cohort will also see an increase its spending across haircare and makeup, Jensen added.

It’s a trend that’s been complemented by a broader focus on wellness and anti-aging.

“We’re not ignoring people as they get older in the beauty industry as much anymore,” said Anna Mayo, a NielsenIQ beauty thought leader. “For the first time, we’re seeing brands launched and they’re talking about menopause. … I think that really helps keep people engaged. They feel like they’re not buying something that was made for a college student.”

Gen X is also at the “prime spending phase” of their lives, with NielsenIQ estimating that between 2021 and 2033, the cohort will spent $15.2 trillion a year, expected to rise to $23 trillion by 2035.

Though the generation is spending its money experimenting with different brands and products, Mayo noted that its members have high brand loyalty and are likely to stick to and continue investing in a product once it sticks.

“Part of this is the industry has gotten really good at developing brands that are made for a lot more niche audiences,” she said. “We’re less so in the era of these mass market brands.”

The retail winners

A shopper enters an Ulta Beauty store in Pleasant Hill, California, US, on Wednesday, Dec. 3, 2025.

David Paul Morris | Bloomberg | Getty Images

It’s a growth that companies are taking note of, too. In early April, Ulta CEO Kecia Steelman told Yahoo Finance that catering to older generations is part of the company’s business strategy.

“I think 50 is the new 30 and 60 is the new 40s,” she said. “So those of us that are aging, we want to age gracefully, so if we can find products that are actually helping the longevity of the look, we’re leaning into that.”

Ulta did not respond to CNBC’s request for comment.

Sephora is seeing similar growth, telling CNBC the company is actively investing in broadening its brands that target the high-spending Gen X group.

“As we expand our assortment – particularly for our Gen X clients, with brands like YSE Beauty by Molly Sims, Sarah Creal and U Beauty – our focus remains on delivering brands with a clear understanding of our consumers’ goals, concerns, and preferences, while elevating authentic founder stories and expertise, which we know resonates with our clients,” Carolyn Bojanowski, Sephora’s U.S. executive vice president of merchandising, told CNBC in a statement.

Bluemercury, a personal care company, even launched a campaign last year celebrating women who are over the age of 40. The company identified Gen X as one of its biggest opportunities given its spending power and focus on luxury beauty.

The winners from Gen X’s spending spree will be clear, according to Lindy Firstenberg, a consultant at AlixPartners.

“Ulta is going to win because they’ve doubled down on wellness, and they have a huge focus on menopause brands,” Firstenberg said.

While Sephora has been outwardly advertising for younger cohorts, Firstenberg said even it’s emerging as a sort of Gen X “hotspot,” along with Bluemercury. The key, she said, has been investing in curation and one-on-ones with clients.

Members of Gen X, who grew up with salespeople working counters at department stores, invest in the experience as well as the product. Firstenberg said the importance of knowledgeable sales associates is 23% higher for Gen X than for Gen Z.

Brands that focus on meeting Gen X where they are instead of chasing younger generations, will secure their spending power, Firstenberg added.

“That is what Gen X wants: They want the best products, they want to be educated, they want that high talent and they want that service,” she said.

How Gen X spends

Shoppers are seen outside the French multinational personal care and beauty retail brand Sephora store in Spain.

Xavi Lopez | SOPA Images | Lightrocket | Getty Images

Kirti Tewani, a member of Gen X and a content creator focused on promoting beauty and wellness for her cohort, said she’s seen a growing interest in investing in products that work to slow down or prevent further aging.

That generation posed a largely “untapped” market when she started seeing increased attention on it roughly two years ago.

“Gen X has been a generation that has gone through so many ups and downs in their lives that now we are at a position where we’re financially more independent, the kids have grown older and now we have the time to put into ourselves,” she said. “So we’re taking care of ourselves from the inside out.”

Tewani said she’s specifically seen Gen X focused on products that boast long-term effects and target areas like hyperpigmentation, dry skin and large pores. They’re also pairing those products with a wellness-focused lifestyle, she added, focusing on diet, exercise and sleep.

The generation is also looking for clean ingredients, according to Tewani, coinciding with a larger push toward simpler formulations in the beauty industry.

“I think the brands definitely knew that this was coming,” Tewani said. “Now, more brands are jumping on the bandwagon because they’re understanding where the spending markets are, and Gen X definitely fills in that gap.”

And Gen X’s age also means its spending for beauty expands beyond the surface level.

According to AlixPartners’ Firstenberg, people of those age are likely to be in a so-called “sandwich generation,” which means they’re buying beauty products for both parents and children, contributing to its large spending share.

It’s also not a generation that’s focused on newness or flashy marketing and instead want the products that show proven results.

Gen X’s spending power is nearly 25% above the national average, she added.

“We’re not only seeing that they have this power, but they yield it,” she said. “They’re going to maintain this highest spend by generation for at least the next eight years.”

“When the US president elect Barrack Obama assumes office in January, the crisis will still be bigger,” Kumar said while delivering lecture on Current Financial Turmoil and Lesson for Future at Ahmedabad Management Association today.

“150 billion $ tax cut package for the housing sector was too little and too late to stem the collapse of a much higher magnitude,” Kumar said adding “Every aspect of financial sector got sucked into the financial turmoil.”

“In last two decades the financial markets in US got deregulated, under the guidance of Alan Greenspan as he worked on assumption that markets are self stabilising, but in a recent testitmony Greenspan admitted he was wrong for 16 years,” Kumar said while quoting a US leading daily.

This deregulation led to the collapse of Lehman Brothers, Bear Stern and other troubled entitites, he added.

“Government has intervened, crisis has slowed down, but there is crisis of confidence now amongst the banks. The financial and money markets work on certain degree of trust and confidence and this should not be shattered at any cost,” he added.”Collapse in US was so sharp against the gradual rise because the banks were interlocked in deals. Due to deregulartion there were instruments promising much higher returns and even a marginal fall in assest pricing triggered it all,” Arun Kumar said.

US economy was thriving on borrowed funds, so post crisis countries such as Japan, China, Iceland, Ukraine and others are in deep trouble. China is finding ways to delink from dollar, after corporate profits began falling showing early signs of heading into recession, Arun Kumar said.

Now protectionism of economy has creeped in due to lack of confidence, that too is dangeorus, he cautioned. So when the US President-elect Barrack Obama joins office he would prioritise job creation in sectors like BPO and call centres, Kumar said adding, in the past 1.5 billion job loss has been reported in US.

So at this historic juncture a out-of-box re-architecturing is required for the $ 600 trillion financial sector, he added.

In the backdrop of such a scenario the G-20 initiative is important and extensive coordination between the government’s including Indian should be evolved to come over it, Kumar added.

as a Reliable and Trusted News SourceBusiness

Mycronic AB (publ) 2026 Q1 – Results – Earnings Call Presentation (OTCMKTS:MICLF) 2026-04-25

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

In this context, one segment that remains relatively insulated from market volatility is Infrastructure Investment Trusts (InvITs) and Real Estate Investment Trusts (REITs). The government can leverage this space to achieve most of its targets. These instruments have proven to be effective tools for the Government and their entities to monetise income-generating assets through the capital markets. Importantly, the REIT and InvIT markets remain active, with transactions continuing despite broader market fluctuations.

There are several infrastructure assets that generate steady income through tariffs or tolls. These can be bundled into InvITs/REITs and offered to investors. The government has already launched InvITs that are large, well-structured, and actively traded.

At the same time, State Governments hold significant portfolios of similar revenue-generating assets that remain largely untapped for monetisation. If properly structured, InvITs can enable State Governments not only to raise resources but also to support their fiscal deficit targets. The key question is how best to operationalise this opportunity. An optimal approach would be for various State departments and agencies to transfer their eligible assets into centrally sponsored or established InvIT platforms such as NHIT. This would create larger, more diversified asset pools, improve liquidity, attract a broader base of institutional investors, and ultimately lead to better pricing and faster execution.

Rather than each state or agency creating its own InvIT (which would likely result in smaller, fragmented, and potentially suboptimal vehicles), aligning with a centralised InvIT platform offers clear advantages of scale, standardisation, and market credibility. Individual state-level InvITs may struggle with limited size, lower liquidity, and reduced investor interest, whereas a unified platform can aggregate assets across jurisdictions to create a more compelling investment proposition.

Existing InvITs are already performing well and have significant headroom for further scale. NHIT (NHAI’s flagship monetisation vehicle), for instance, has a market capitalisation of approximately Rs 34,126 crore and an enterprise value of about Rs 58,500 crore. It has monetised around Rs 50,000 crore of assets over the past five years and has demonstrated the capacity to absorb additional assets. Its portfolio comprises 28 toll road assets spanning roughly 13,000 lane kilometres. It has successfully attracted several marquee global institutional investors such as OTPP, CPPIB, KKR, and GIC, demonstrating strong investor appetite for stabilised toll road assets and validating the scalability of the InvIT model as a repeat monetisation platform.

With NHAI having significantly deleveraged its balance sheet through successive monetisation rounds, and with new highway awards progressing at a measured pace, the pipeline of readily monetisable national highway assets is becoming constrained. In this context, state-owned expressways are emerging as the next frontier for monetisation.Currently, state-operated highways and expressways represent an estimated Rs 1.4 lakh crore of assets awaiting monetisation. Since 2018, the National Highways Authority of India (NHAI) has monetised assets worth approximately Rs 1.22 lakh crore through InvITs (NHIT and Raajmarg) and the Toll-Operate-Transfer (ToT) framework.

State-operated highways present a substantial capital recycling opportunity, supported by a growing pool of mature, revenue-generating assets. Leading state authorities collectively manage over 22,500 km of monetisable stretches, with an estimated aggregate valuation exceeding Rs 3 lakh crore. Maharashtra leads this segment, accounting for over 50% of the total estimated asset value among the top six states.

A select pool of high-quality assets with strong revenue potential (supported by predictable, inflation-linked toll income and operational maturity) includes key projects across Maharashtra and Uttar Pradesh. These include the Samruddhi Mahamarg (Mumbai–Nagpur), Bandra–Worli Sea Link, Atal Setu, Coastal Road, Agra–Lucknow Expressway, Purvanchal Expressway, and Gorakhpur Link Expressway. Together, these seven assets represent approximately 1,492 km of operational, toll-generating infrastructure and generate over Rs 2,250 crore in annual revenue. This is precisely the type of stable, mature portfolio that InvIT investors have actively sought in the NHAI pipeline, with the potential to generate approximately Rs 1.4 lakh crore in upfront value.

Entities such as MSRDC, MMRDC, and UPEIDA carry significant debt arising from the construction of these assets (for instance, MSRDC alone has incurred around Rs 55,000 crore for the Samruddhi Mahamarg). Unlocking even a portion of this value through structured monetisation would free up substantial capital for future infrastructure development, reduce debt burdens on state agencies and public finances, transfer operations and maintenance risks to specialised long-term operators, and preserve public ownership of the underlying infrastructure through concession-based structures rather than outright sales.

A coordinated, platform-led approach to monetisation can therefore play a pivotal role in bridging fiscal gaps while accelerating infrastructure development. By aligning state assets with established InvITs rather than pursuing fragmented, standalone vehicles, governments can unlock superior value through scale, standardisation, and stronger investor confidence. This not only ensures more efficient capital recycling but also builds a sustainable pipeline for future monetisation. At a time when traditional disinvestment avenues face headwinds, leveraging InvITs as a unified, scalable mechanism offers a pragmatic and market-aligned path to meeting fiscal objectives while continuing to invest in India’s infrastructure growth story.

InvestingPro Fair Value correctly flagged Kratos before 46% drop

SANTA CLARA, Calif. — As artificial intelligence spending continues to reshape the semiconductor industry in 2026, investors face a high-stakes choice among Nvidia, Intel and AMD. The three companies represent very different bets on the AI chip market, with Nvidia maintaining overwhelming dominance, AMD mounting a credible challenge and Intel fighting for relevance through a costly turnaround.

Nvidia remains the undisputed leader in AI accelerators. Its Blackwell and Hopper GPUs power the vast majority of training and inference workloads at hyperscale data centers. Q1 2026 results showed Data Center revenue exceeding $30 billion, with gross margins above 75%. Analysts project the company could sustain 40-50% revenue growth through 2027 as enterprises and governments accelerate AI adoption. The CUDA software ecosystem creates a formidable moat, making it difficult for competitors to displace Nvidia in high-performance computing.

Yet the stock trades at premium valuations, with forward price-to-earnings multiples well above historical averages. Bears warn that any slowdown in Big Tech capital expenditure or successful custom silicon efforts by hyperscalers could pressure margins. Geopolitical risks, including export restrictions to China, add another layer of uncertainty. Still, the overwhelming consensus among more than 50 analysts is Strong Buy, with average price targets implying 25-35% upside from current levels.

AMD offers a more affordable way to play the AI boom. Its Instinct MI300 and upcoming MI350 accelerators are gaining traction in inference and certain training workloads. Data Center revenue has grown rapidly, though from a much smaller base than Nvidia. AMD’s EPYC CPUs continue to take share from Intel in servers, and the Ryzen AI processors are strengthening its position in client PCs. Analysts like those at Rosenblatt and JPMorgan see AMD as a compelling growth story, citing its ability to deliver competitive performance at lower cost.

Valuation is more reasonable than Nvidia’s, but AMD still faces execution risks. It must scale manufacturing, prove software compatibility and win meaningful share against Nvidia’s entrenched position. The consensus rating is Moderate Buy, with price targets suggesting 20-30% potential upside. For investors seeking exposure to AI without Nvidia’s sky-high multiple, AMD presents an attractive alternative.

Intel tells a different story. Once the world’s largest chipmaker, it has struggled with manufacturing delays and lost ground in both client and server markets. Under CEO Lip-Bu Tan, the company is executing a high-stakes turnaround, focusing on the 18A process node and foundry ambitions. Q1 2026 results showed Data Center and AI revenue growing strongly, with several hyperscaler design wins for custom chips and Xeon processors.

Intel’s foundry business, supported by CHIPS Act funding, aims to become a viable alternative to TSMC. If successful, it could generate stable revenue and reduce reliance on internal sales. However, the company continues to post GAAP losses, and capital expenditure remains elevated. Analysts are divided: some see a compelling multi-year recovery story, while others remain skeptical about Intel’s ability to close the technology gap.

The stock has rallied sharply on recent earnings beats, but valuations reflect optimism rather than proven execution. Consensus leans Hold, with targets implying modest upside or downside depending on foundry progress. For risk-tolerant investors betting on a U.S.-based manufacturing renaissance, Intel offers the highest potential reward — and risk.

Comparing the three reveals clear differences in risk-reward profiles. Nvidia offers the safest way to capture AI growth but at a premium price. AMD provides balanced exposure with better valuation and diversification into CPUs. Intel represents a high-conviction turnaround play with significant optionality if its foundry and process technology ambitions succeed.

Market dynamics favor all three to varying degrees. Global AI infrastructure spending is projected to exceed $200 billion annually by 2027, creating ample opportunity. However, competition is intensifying as hyperscalers develop custom chips and new entrants emerge. Supply chain constraints, energy costs and regulatory hurdles could affect growth trajectories.

Investors must weigh several factors. Nvidia’s near-term dominance is hard to dispute, but its valuation leaves little margin for error. AMD’s momentum is real, yet it must prove it can scale against a larger rival. Intel’s story is the most speculative, hinging on execution in a notoriously difficult business.

Analysts emphasize diversification. Many portfolios hold all three companies in varying proportions to capture different segments of the AI value chain. Long-term believers in the AI secular trend generally favor Nvidia for its leadership position. Those seeking value and growth often tilt toward AMD. Contrarian investors willing to endure volatility may see Intel as the highest-upside option.

Ultimately, there is no universal “best” choice. The decision depends on individual risk tolerance, investment horizon and conviction in each company’s strategy. Nvidia remains the default AI play for most. AMD offers a compelling alternative for those seeking lower relative valuation. Intel appeals to those betting on a successful U.S. semiconductor resurgence.

As 2026 unfolds, quarterly results, product launches and AI spending trends will provide fresh data points. For now, the AI chip race remains wide open, with each company positioned to benefit from the same powerful tailwind — even if their paths to success differ dramatically.

how Fair Value analysis identified Omeros’ 74% biotech breakout

Lakers take control with Late Comeback in Game 3

Internal memo: Five senior execs out at Qualtrics as new CEO restructures leadership team

Why $100,000 in $100 Bills Costs Less Than $100,000 in $20 Bills #money #cash #banking #bills #prop

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

Why $100,000 in $100 Bills Costs Less Than $100,000 in $20 Bills #money #cash #banking #bills #prop

Crypto Gold Live Trading 24 APRIL – stock_learners

No.1 Money Saving Experts: Do Not Buy A House! Putting Money In A Bank Makes You Poorer!

-

Business6 days ago

Business6 days agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Politics6 days ago

Politics6 days agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Fashion19 hours ago

Fashion19 hours agoWeekend Open Thread – Corporette.com

-

Entertainment6 days ago

NBA Analyst Charles Barkley Chimes in on Ice Spice McDonald’s Fiasco

-

Tech6 days ago

Tech6 days agoAuto Enthusiast Scores Running Tesla Model 3 for Two Grand and Turns It Into Bare-Bones Go-Kart

-

Politics5 days ago

Politics5 days agoGary Stevenson delivers timely reminder to register to vote as deadline TODAY

-

Politics3 days ago

Politics3 days agoMaking troops accountable for war crimes threatens US alliance, ex-SAS colonel warns

-

Business3 days ago

Business3 days agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Politics3 days ago

Politics3 days agoDisabled people challenge government SEND proposals over segregation concerns

-

Crypto World5 days ago

Crypto World5 days agoBank of Hawai’i (BOH) Q1 2026: Net Income Drops to $57.4M as Net Interest Margin Expands

-

Politics3 days ago

Politics3 days agoZack Polanski responds to home secretary’s taser threat

-

Politics3 days ago

Wings Over Scotland | How To Get Away With Crimes

-

Politics3 days ago

Politics3 days agoStarmer handler McSweeney to be dragged from shadows by Foreign Affairs Committee

-

Crypto World6 days ago

Kelp DAO rsETH Bridge Hack Drains $292M as DeFi Losses Top $600M in Two Weeks

-

Politics3 days ago

Politics3 days ago‘Iran is still a nuclear threat’

-

Crypto World4 days ago

Crypto World4 days agoFive Value Stocks with Recovery Potential in 2026: PayPal (PYPL), Nike (NKE), and More

-

Crypto World4 days ago

Crypto World4 days agoNew York sues Coinbase, Gemini over prediction market offerings

-

Business3 days ago

Business3 days agoThe Job Benefits Most Men Don’t Know to Negotiate

-

Crypto World1 day ago

Crypto World1 day agoMichael Saylor says BTC winter is over. Market analyst disagrees, says bitcoin was in a pullback

-

Politics6 days ago

Politics6 days agoReform investigating candidate who ‘hates’ the NHS

You must be logged in to post a comment Login