Business

Rocket Lab (RKLB) Stock Surges 7% in Early Trading on March 17, 2026, Amid Strong Momentum

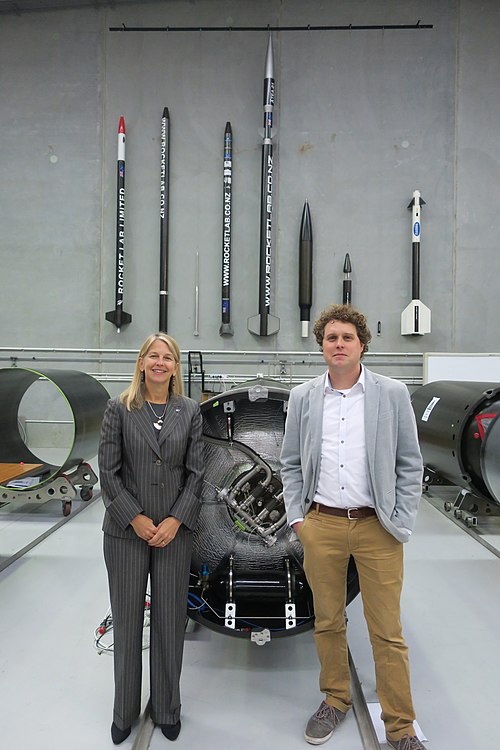

NEW YORK — Rocket Lab USA Inc. (NASDAQ: RKLB) shares climbed sharply in early trading Tuesday, March 17, 2026, extending recent gains as the aerospace company benefits from robust revenue growth, a swelling launch backlog and renewed investor enthusiasm for the commercial space sector.

As of mid-morning EDT, RKLB traded at approximately $76.40, up $5.09 or 7.14% from Monday’s close of $71.31, according to real-time data from Nasdaq and major financial platforms. Volume exceeded 6 million shares in the first few hours, reflecting heightened interest following a strong performance in recent sessions.

The stock has shown significant volatility but upward momentum in March 2026 after a dip in February. Closing at $71.31 on March 16 — a 4.24% increase from the prior session — RKLB has recovered from lower levels earlier in the month, with intraday highs pushing toward $76.53 in today’s session. The 52-week range spans $14.71 to $99.58, with the all-time high reached January 16, 2026, at $96.30.

Analysts point to Rocket Lab’s record 2025 performance as a key driver. The company reported substantial revenue growth — up 56.9% over the past two years — fueled by increased launch cadence and expansion in its space systems business. A backlog approaching $1.85 billion underscores demand for Electron rockets and Neutron development, positioning Rocket Lab as a leader in small-to-medium satellite launches and space infrastructure.

Cantor Fitzgerald reiterated a Buy rating earlier this month, lifting its price target after highlighting the company’s stacked backlog tilted toward higher-margin space systems work. Other analysts maintain consensus Buy ratings, with average price targets around $74.55 to $85.00, suggesting room for further upside despite the recent rally.

Rocket Lab’s advancements in technology, including new silicon solar arrays for future space-based infrastructure, have bolstered confidence. The company continues to execute on reusable rocket ambitions with Neutron, aiming to compete in the growing market for dedicated launches and constellation deployments.

Market observers note broader sector tailwinds, including increased U.S. defense spending on missile systems and space capabilities amid geopolitical tensions. Discussions around national security needs — from missile defense to satellite constellations — have spotlighted companies like Rocket Lab as potential beneficiaries.

However, the stock faces risks typical of growth-oriented aerospace firms. High valuation multiples persist, with market capitalization recently surpassing $43 billion at current levels. February’s 13.7% decline reflected broader market pressures on high-growth names, though March’s rebound indicates renewed buying interest.

Insider activity drew some attention, with reports of sales by executives at Rocket Lab and peers like Palantir and Archer Aviation. Such transactions often occur for personal reasons and do not necessarily signal waning confidence, but they warrant monitoring.

Rocket Lab set deadlines for 2026 shareholder proposals earlier this month, a routine corporate governance step ahead of its annual meeting. No major controversies emerged from the announcement.

The company’s Electron rocket has maintained a reliable launch record, supporting commercial, government and defense payloads. Upcoming missions and Neutron progress updates could provide further catalysts.

Investors continue to watch for quarterly earnings, expected to reflect ongoing backlog conversion and margin improvements. Rocket Lab’s shift toward higher-value space systems — including spacecraft components and subsystems — has improved financial visibility compared to launch-only reliance.

Broader market context includes mixed sentiment in tech and growth stocks, though space and defense sectors have shown resilience. Rocket Lab’s performance aligns with peers benefiting from government contracts and commercial satellite demand.

As trading progresses March 17, attention remains on whether RKLB can sustain gains toward recent highs or face profit-taking. The stock’s trajectory reflects optimism about the commercial space economy’s long-term potential, driven by decreasing launch costs and expanding applications from Earth observation to communications.

Rocket Lab, founded by CEO Peter Beck, has grown from a small-launch pioneer to a vertically integrated space company. Its Wallops Island, Virginia, and New Zealand facilities support frequent operations, while U.S. expansion bolsters national security ties.

With a market cap now in the mid-$40 billion range, RKLB ranks among prominent space players. Continued execution on Neutron — targeted for larger payloads and reusability — could drive further re-rating if milestones are met.

Analysts emphasize the company’s differentiated position in a market once dominated by larger incumbents. Rocket Lab’s agility in smallsat launches and rapid iteration has captured significant share.

As the trading day unfolds, RKLB’s performance underscores investor appetite for innovative aerospace plays amid evolving global priorities in space.

Investment scams were the leading method used to fleece West Australians in 2025, accounting for $13.7 million in losses.

Edited excerpts from a chat on market outlook and opportunities:

Crude oil prices have been hovering above $100 a barrel mark. At what level, do you think the India equity story starts becoming meaningfully uncomfortable for investors?

For an oil importer like India, the impact of high oil prices can turn out to be very adverse if the prices remain elevated for an extended period. A 10% increase in crude (estimated roughly at $10) causes about 20 bp reduction in GDP growth, 30 bp increase in CPI inflation and 30 to 40 bp increase in current account deficit.This adverse macro impact will manifest if the crude price remains elevated for long. In the ongoing crisis, the durability of the crisis is significant. If the war ends soon (it can end any time) or if there is significant de-escalation and opening of the Hormuz Strait, crude can immediately fall to $80 level. In such a scenario, the adverse impact will not manifest. Another two weeks of crude above $100 is a temporary shock which the Indian economy can absorb. But beyond that, the economy and markets will be impacted.

Do you think the market is still underpricing the second-order effects of war, especially on inflation expectations, bond yields, and consumer sentiment?

The market is even now discounting a quick end to the war and cooling of oil prices. The market is not discounting a prolonged war and elevated crude oil price for long. Contrary to market expectations, if the conflict escalates and crude rises above $120 and remains at that level for many weeks, the market will further correct from the present levels. Everything boils down to how long the conflict continues, more importantly, how long Hormuz Strait remains restrictive.

How vulnerable is Q4 earnings season to this backdrop? Which sectors do you expect to show the sharpest earnings impact in Q4 from elevated crude and freight costs?

Q4 is unlikely to impact earnings significantly. The impact will be felt in Q1 FY27. However, the war and the consequent uncertainty will show up in some segments. Industries using petroleum inputs like paints, adhesives, and tyres will be hit. Manufacturers using LNG as fuel like verified tiles have been hit hard. Exporters will gain from currency tailwinds. IT will gain; but the Anthropic shock will continue to weigh on the segment. Exporters to the Gulf region will be impacted marginally.

Do you expect another round of earnings downgrades over the next few weeks if oil stays elevated?

If crude remains elevated and gas availability restrictions continue, another round of earnings downgrade will become inevitable. Earnings downgrades will be in import intensive and crude related segments mentioned earlier.

Has the small cap correction created genuine value, or are pockets of the segment still frothy despite the damage?

Correction in small caps has opened value in many segments. Broadly small cap valuations continue to be high, but there are segments with attractive valuations and high growth prospects. These are across industries and, therefore, stock selection holds the key to successful investment. An ideal strategy would be to invest in small cap mutual funds.

How are you thinking about banks in this setup, especially if higher inflation complicates the rate outlook?

Banking is one segment that is attractively valued now. Sustained selling by FPIs in leading large private sector banks has made the valuations in the segment attractive. This segment is an excellent long-term buy for investors. Credit growth in the economy continues to be good. The MPC is unlikely to increase the interest rates soon since inflation arising from supply shocks cannot be addressed through rate hikes.

Help us understand why PSU bank stocks have been the worst hit and whether one should be brave enough to buy the dip as the growth story looks promising but yields are playing spoilsport?

PSU bank stocks had a good run recently. What we are witnessing now is profit booking in the segment. This segment can be considered selectively for investment.

If the market was to rebound from here, which sectors do you think will lead the rally?

In the event of a sharp bounce back in the market, all beaten down but fundamentally strong stocks will rally smartly. But if FPIs continue to sell the rally, large cap banking names may continue to disappoint despite the strong fundamentals and attractive valuations. IT appears set for a tactical bounce back in April since the Q4 results are unlikely to disappoint. Automobiles and auto ancillaries are on a strong wicket. Telecom will remain resilient. Pharmaceuticals have potential to appreciate.

UPDATED: Former SAS soldier Ben Roberts-Smith has been arrested in relation to a war crimes investigation and is expected to be charged with five counts of murder.

China targets Taiwan’s chip prowess to evade global ’containment’, Taipei government says

Biologics is a full-time healthcare investor who developed a passion for biotech and life saving therapies after working in the medical field for years. His trade focus is around innovative companies developing breakthrough therapies and/or pharmaceuticals with catalysts for potential acquisitions.

He is the leader of the investing group Compounding Healthcare. Features of the group include: Several model healthcare portfolios, a weekly newsletter, a daily watchlist, and chat for dialogue and questions. Learn more.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of CRDF either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

In February 2026, Thai exports grew 9.9%YOY, driven by electronics and the US market, while imports surged 31.8%YOY. Middle East conflict and US tariffs pose risks, potentially worsening Thailand’s trade deficit.

Thai Export Performance in February 2026

Thai exports in February 2026 slowed to a growth of 9.9% year-on-year (YOY), with a total export value of USD 29,439.7 million. This was a significant deceleration from January’s 24.4% YOY surge and below forecasts. The export slowdown was coupled with a sharp 11.1% month-on-month seasonal adjustment contraction. Electronics led exports, expanding over 56.8% YOY due to global demand and investment in related industries, especially to the US, where exports rose 40.5%. Gold exports grew moderately by 18.2%, affected by falling global prices.

Import Trends and Trade Balance

Imports surged to USD 32,273.3 million, the highest in 50 months, rising 31.8% YOY, driven mainly by raw materials, intermediate goods, and capital goods like gold and electrical machinery. This import growth intensified the trade deficit, which reached USD -2,833.6 million in February, with a cumulative deficit of USD -6,137.1 million for the first two months of 2026.

Outlook and External Challenges

Thailand’s trade outlook faces challenges from the Middle East conflict and rising US import tariffs. The Middle East conflict, though limited in direct impact, may affect key export sectors and energy costs, worsening the trade deficit. Meanwhile, ongoing US tariff investigations under Section 301 pose export risks. The Ministry of Commerce projects 2026 export growth scenarios ranging from -3% to +1.1% YOY. SCB EIC will update economic forecasts by March’s end amid these evolving uncertainties.

Other People are Reading

Continue Reading

Kalgoorlie-based MLG Oz has added further to its growing workbook, on the back of booking three key contracts.

Mach Natural Resources unitholders price 9M unit offering at $13.05

Most managers are advising investors to stay invested but stagger their entries, using systematic or phased allocation strategies rather than chasing a quick rebound.

as a Reliable and Trusted News Source

as a Reliable and Trusted News SourceBusiness

Apple’s foldable iPhone encounters engineering snags, faces potential shipment delays, Nikkei Asia reports

Apple’s foldable iPhone encounters engineering snags, faces potential shipment delays, Nikkei Asia reports

Blake Lively, Justin Baldoni Reject Settlement Effort

Iran-US war live: Trump vows to decimate Iran as deadline approaches and says he’s ‘not worried’ about war crimes

Investment scams cost West Australians $13.7m in losses

-

NewsBeat4 days ago

NewsBeat4 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business4 days ago

Business4 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business1 day ago

Business1 day agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Crypto World7 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports2 days ago

Sports2 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business3 days ago

Business3 days agoExpert Picks for Every Need

-

Business5 days ago

Business5 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech7 days ago

Tech7 days agoEE TV is using AI to help you find something to watch

-

Sports6 days ago

Sports6 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech7 days ago

Daily Deal: StackSkills Premium Annual Pass

-

Tech7 days ago

Tech7 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech7 days ago

Tech7 days agoWhat Are The Biggest Limitations Of Supercomputers?

-

Crypto World6 days ago

Crypto World6 days agoBitcoin enters the public bond market as Moody’s gives a first-of-its-kind crypto deal a rating

-

Crypto World6 days ago

Bitcoin stalls below key resistance as technical signals skew bearish

-

Politics7 days ago

Politics7 days agoTransform Your Space with Stunning Small Works

-

Politics6 days ago

Politics6 days agoStarmer’s centre has collapsed, and the left was right all along

-

Business2 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Fashion7 days ago

Fashion7 days agoZara Turns Up the Heat With New Swimwear

You must be logged in to post a comment Login