The first quarter of 2026 gave investors plenty to worry about. Rising tensions in the Middle East pushed oil prices higher, inflation concerns resurfaced, and the long-anticipated pivot to lower interest rates continues to be postponed. Markets, never short on imagination, have begun spinning familiar narratives: that expensive money punishes growth, that AI’s promises may exceed its near-term returns, and that the safer bet lies in energy, cyclicals, and businesses whose cash flows arrive sooner rather than later. There is also a growing fear that AI itself may disrupt entire categories of existing software businesses — rendering yesterday’s winners obsolete overnight.

We will not pretend these concerns are frivolous. They are not. When the cost of capital rises, the arithmetic of investing genuinely changes — a dollar earned a decade from now is worth less today than it was in a world of cheap money. That is not opinion; it is math. And we have always believed in taking math seriously.

But here is what we have also learned, after watching markets swing from greed to panic across many cycles: the headlines that feel most urgent are rarely the ones that determine long-term outcomes. The businesses that compound wealth over decades do so not because they were spared from difficult environments, but because they were built to endure them. We have spent the past decade building a portfolio of exactly that kind.

Advertisement

None of what we are seeing today is new. Different costumes, same play.

Performance in Context

During the first quarter, Rowan Street declined 19.8%, compared to a 4.3% decline for the S&P 500. That is not a result we enjoy reporting. At the same time, it reflects the more concentrated approach we take and is not unusual for portfolios built around a smaller number of high-conviction investments.

We invest in a focused group of businesses that we believe can compound value at attractive rates over long periods of time. In the short term, their stock prices can be more volatile—particularly in environments like the one we are experiencing today, where interest rates are higher and investor focus has shifted toward businesses with nearer-term cash flows.

Rowan Street is designed for long-term compounding, not for minimizing short-term volatility or closely tracking a benchmark. As a result, returns can differ meaningfully from year to year.

Advertisement

We have seen this before.

In early 2022, we went through a similar period where stock prices declined sharply, even as the underlying businesses continued to perform well. At the time, we wrote that the portfolio was, in many ways, in one of the strongest positions in our history despite the decline in stock prices.

That did not feel obvious at the time. What followed was a period where business performance ultimately reasserted itself. The fund returned +102.6% (net) in 2023, +56.6% in 2024, and +11.1% in 2025.

As Benjamin Graham observed:

Advertisement

“In the short run, the market is a voting machine, but in the long run, it is a weighing machine.”

A Post-Quarter Update

We are writing this letter in mid-April, approximately two weeks after quarter-end. Since March 31, markets have moved sharply — and our portfolio has recovered approximately half of the first quarter decline. Based on our internal estimates as of April 17, year-to-date performance stands at approximately -10%, compared to the official quarter-end figure of -19.8%. We note that this mid-month figure is an internal estimate only, has not been verified by our fund administrator, and reflects only a partial month.

We share this not to suggest the difficult period is behind us — it may not be. We share it because it illustrates precisely the point we are making throughout this letter. The fundamentals of the businesses we own have not changed. Their competitive positions, earnings power, and long-term prospects remain intact, in our view. What changed was the price multiple. This is what long-term ownership of exceptional businesses actually looks like. Price and value diverge. Sometimes dramatically. The investors who benefit are those with the temperament to remain focused on the underlying businesses, not the day-to-day movements of their stock prices.

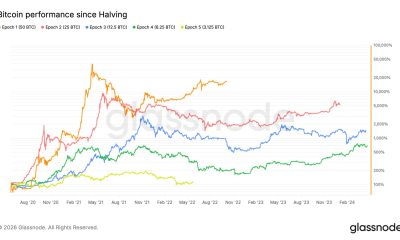

Volatility is the Price of Admission

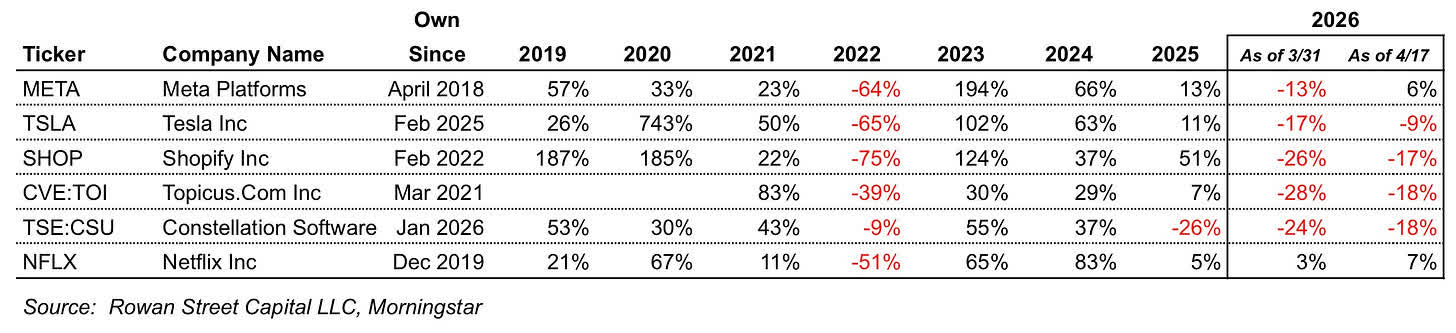

The table below shows the annual returns of our largest holdings by portfolio weight as of March 31, 2026 and illustrates a simple reality of long-term investing: even exceptional businesses experience significant volatility. We have included an April 17 column to reflect the meaningful recovery in our portfolio since quarter-end, as discussed in the Performance section above. The figures reflect annual stock price returns and do not represent Rowan Street Capital fund performance or returns achieved by the fund on these positions.

The April 17 column tells its own story — and it is the same story this letter is built around. This is what long-term ownership actually looks like in practice. Not a smooth upward line — but a recurring series of gains, losses, and tests of conviction. Drawdowns of 30%, 50%, even 75% are not unusual. They are a recurring feature of owning exceptional businesses — not anomalies.

Advertisement

Everyone describes themselves as a long-term investor. Very few are willing to endure what that actually looks like. Volatility is the price of admission.

The charts that follow bring this pattern to life across three of our largest holdings — Meta Platforms, Tesla, and Shopify. Different businesses, different drawdowns, same lesson.

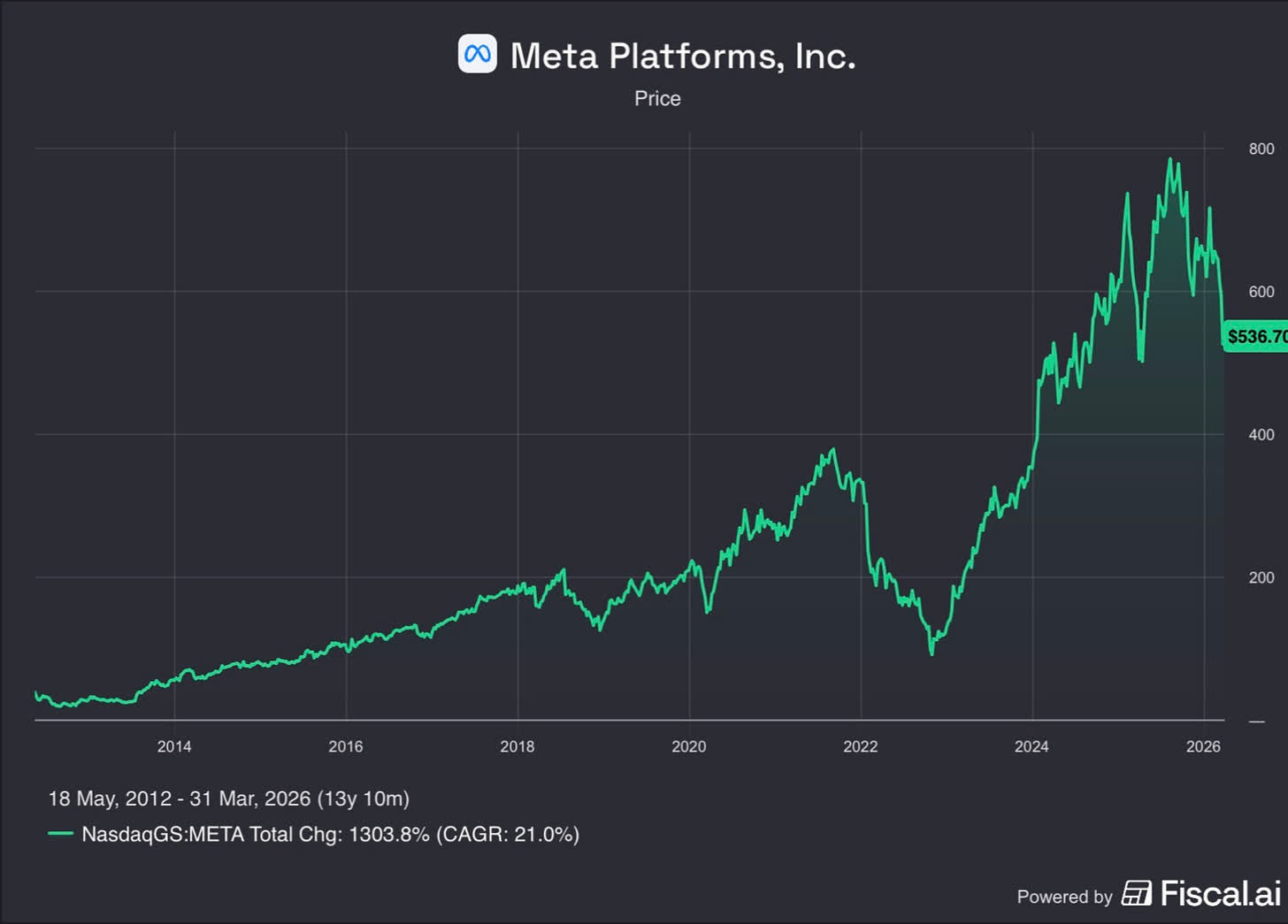

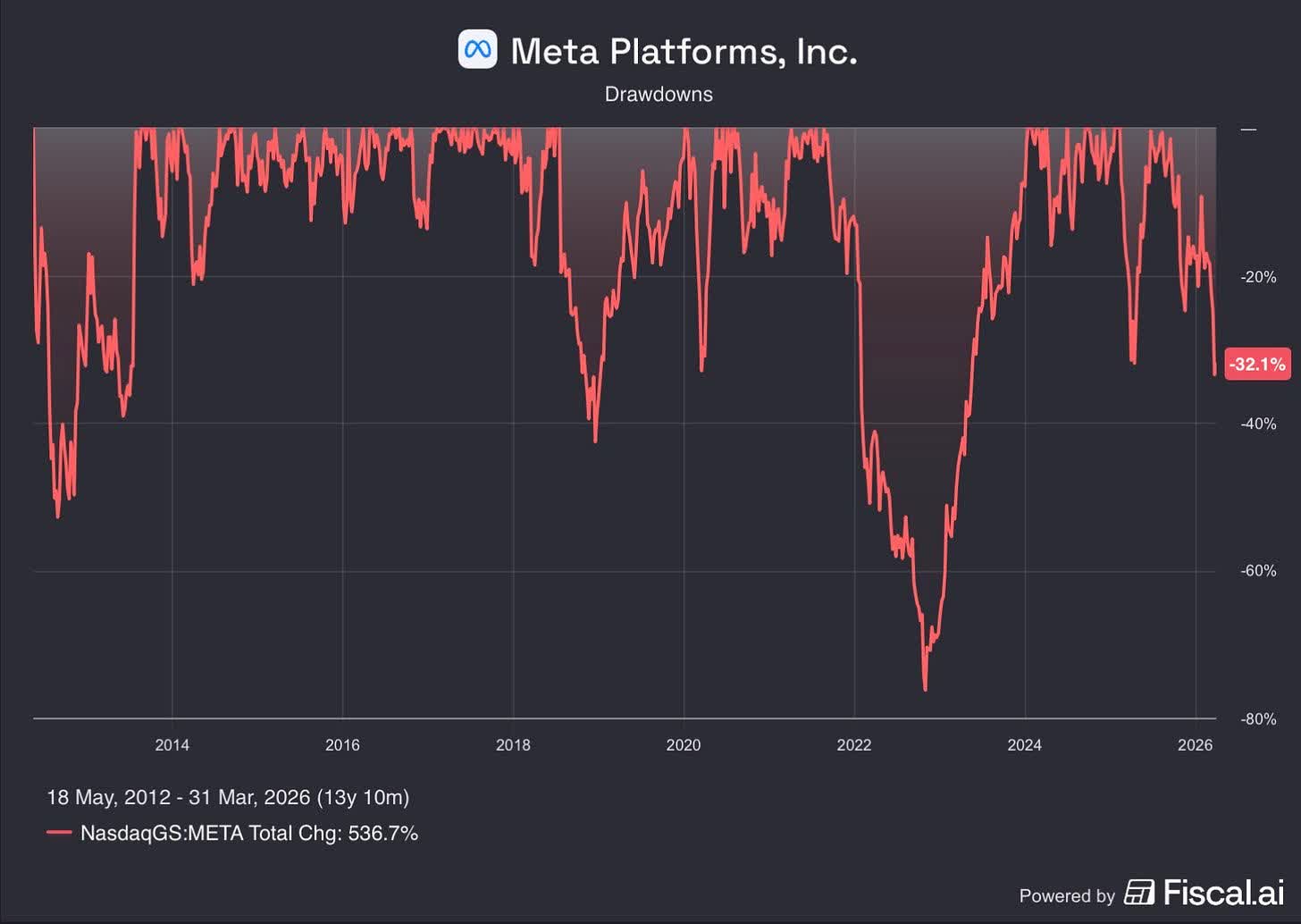

Meta has delivered a cumulative return of approximately 1,300% since its IPO, or about 21% annually. The path to those returns, however, has been anything but smooth.

Advertisement

Over the past decade, the stock has experienced numerous drawdowns of 30% or more, several declines of 50% or more, and, most notably, a decline of nearly 80% in 2022.

These periods were not isolated events — they were a recurring feature of owning this business. And yet for those who remained focused on the underlying fundamentals, the long-term outcome has been exceptional.

We believe today represents one of the most compelling opportunities in Meta we have seen since 2022. Please read our full analysis below — including our views on the AI spending debate, the recent legal setbacks, and why we believe the market may be repeating a familiar mistake.

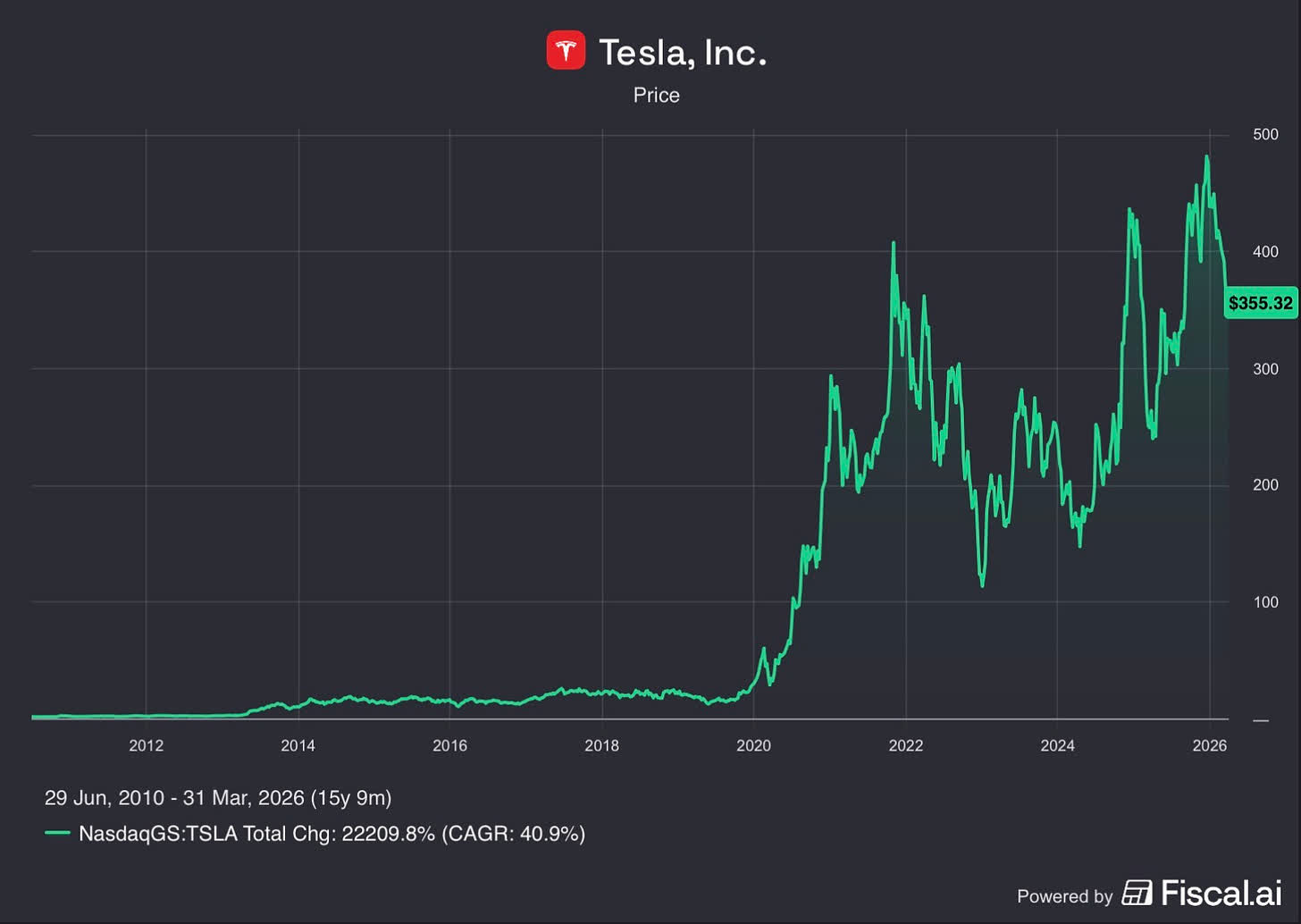

Tesla provides an even more striking example—not just of volatility, but of how disproportionate long-term outcomes can be relative to the experience along the way.

Since its IPO in 2010, the stock has delivered a cumulative return of approximately 22,000%, or about 41% annually. Looking at that result today, the path can appear almost inevitable. In reality, it was anything but.

There were multiple periods along the way where the stock declined sharply—on numerous occasions by more than 50%, and once by over 70%—often accompanied by shifting narratives around the business. At different points, the concerns ranged from questions about the company’s survival, to valuation, to increasing competition, founder behavior and execution risk.

Each of those moments felt uncertain in real time. And yet, for investors who were able to remain focused on the long-term trajectory of the business, the outcome has been extraordinary.

Advertisement

The biggest winners rarely feel comfortable to own.

While Tesla has demonstrated this pattern over many years, our ownership of the business is still relatively recent.

We outlined our investment thesis in detail in our Q3 2025 letter, and our view remains unchanged. From here, our role is not to predict short-term movements, but to remain disciplined and allow the long-term economics of the business to play out.

Shopify has been an exceptional business over time, compounding at over 40% annually since its IPO.

The path to those returns, however, has been far from smooth, including several sharp drawdowns and a decline of more than 80% in 2022.

We experienced this firsthand. After initiating our position in early 2022, the stock declined by an additional ~50%. We believed the drawdown reflected multiple compression, not fundamental deterioration. The business continued to grow revenues, expand its merchant ecosystem, and strengthen its competitive position. The price was broken. The company was not.

It did not feel good. The best opportunities rarely do.

Advertisement

What followed was a long and uncomfortable period of patience before payoff. The stock rebounded 124% in 2023 — and yet we were still underwater on our investment. It was not until 2024 — when Shopify generated over $1 billion in operating profit for the first time and the stock gained another 37% — that we finally got our capital back and began generating real returns. The stock then rose 51% in 2025, making it our best performer of the year.

Three years of patience. Three years of watching the business execute while the stock tested our conviction repeatedly.

More recently the stock has again declined meaningfully — down 26% at quarter-end, though it has since recovered to approximately -17% as of mid-April. There is nothing unusual about that. It is the same pattern, playing out again.

Shopify is a clear example of why patience — especially through periods of valuation compression — is often required before fundamentals are fully reflected in stock prices. In our experience, the returns in businesses like Shopify are earned by those willing to endure periods when stock prices and business performance temporarily move in opposite directions.

Advertisement

Underlying Business Performance

Despite the recent decline in stock prices, the underlying businesses we own continue to perform well. Based on current estimates, our portfolio companies are expected to grow revenues at approximately 18% annually and earnings at approximately 21% annually over the next several years. These figures represent a weighted average across a group of businesses operating in different industries and geographies.

In our experience, periods like this — when price and value diverge — have consistently provided the most attractive investment opportunities.

In our Q2 2025 letter, we wrote that our edge does not come from predicting short-term market movements, but from our willingness to own a concentrated group of high-quality businesses and remain focused on their long-term compounding potential.

That principle is far easier to articulate when markets are rising than when they are declining. Periods like the one we are experiencing today are when that discipline is tested — and, in our view, when it matters most.

Advertisement

Portfolio Update: Constellation Software

During the quarter, we initiated a position in Constellation Software (TSE: CSU) (CNSWF), funded by the sale of the remainder of our Spotify position. Constellation is one of the most exceptional capital allocation platforms in the public markets — a company that has compounded shareholder capital at approximately 28% annually since its 2006 IPO by systematically acquiring and operating mission-critical vertical market software businesses. The stock has recently declined approximately 50% from its highs, creating what we believe is a rare entry point into a business of this quality. For those interested in a detailed discussion of our investment thesis — including our views on the AI disruption narrative and the recent leadership transition — we have published a full write-up on our Substack.

The Opportunity Today

We want to be direct with our partners and with anyone considering investing alongside us for the first time.

We have been here before — not just as observers, but as participants with real stakes. In 2021-2022, when our portfolio declined sharply we remained focused on the underlying businesses and their long-term prospects. We wrote at the time that we believed the portfolio was in one of the strongest positions in its history. Few wanted to hear it. Even fewer wanted to invest. What followed was a cumulative net return of approximately +252% over the subsequent three-year period (2023–2025).

We are not promising a repeat. No honest investor can make that claim.

Advertisement

But here is what we can say with conviction: the businesses we own today are stronger than they were in 2022. Their competitive positions are deeper, their earnings power is greater, and their long-term opportunities are larger. In many ways, we believe this is the strongest and most focused portfolio we have built since our inception in 2015 — a small group of exceptional businesses that have each been tested through adversity and emerged with their competitive positions intact or strengthened.

And yet their stock prices have declined meaningfully from recent highs. In our view, the gap between what these businesses are worth and what the market is willing to pay for them today is as wide as it has been since that period.

We have invested a significant majority of our personal net worth alongside yours. We earn nothing unless our partners make money. That is not a marketing line — it is the structure we chose deliberately on day one, because we believe it is the only honest way to manage other people’s capital.

Periods like this are never comfortable. They were not comfortable in 2022, and they are not comfortable today. But in our eleven years of managing capital through euphoria and despair, one lesson has proven itself repeatedly: it is precisely in these moments — when prices are low, sentiment is poor, and patience feels unrewarded — that the most important long-term returns are made.

Advertisement

To our existing partners — thank you for your continued trust and patience. We have been here before, and we remain as convicted as ever in the businesses we own together. If your circumstances allow, we believe adding to your investment at current levels represents one of the more compelling opportunities we have seen since 2022.

To those considering investing alongside us for the first time — if this way of thinking resonates with you, we would welcome the opportunity to partner over the long term.

Best regards,

Alex and Joe

Advertisement

DISCLOSURES

The information contained in this letter is provided for informational purposes only, is not complete, and does not contain certain material information about our fund, including important disclosures relating to the risks, fees, expenses, liquidity restrictions and other terms of investing, and is subject to change without notice. The information contained herein does not take into account the particular investment objective or financial or other circumstances of any individual investor. An investment in our fund is suitable only for qualified investors that fully understand the risks of such an investment. An investor should review thoroughly with his or her adviser the funds definitive private placement memorandum before making an investment determination. Rowan Street is not acting as an investment adviser or otherwise making any recommendation as to an investor’s decision to invest in our funds. This document does not constitute an offer of investment advisory services by Rowan Street, nor an offering of limited partnership interests our fund; any such offering will be made solely pursuant to the fund’s private placement memorandum. An investment in our fund will be subject to a variety of risks (which are described in the fund’s definitive private placement memorandum), and there can be no assurance that the fund’s investment objective will be met or that the fund will achieve results comparable to those described in this letter, or that the fund will make any profit or will be able to avoid incurring losses. As with any investment vehicle, past performance cannot ensure any level of future results. IF applicable, fund performance information gives effect to any investments made by the fund in certain public offerings, participation in which may be restricted with respect to certain investors. As a result, performance for the specified periods with respect to any such restricted investors may differ materially from the performance of the fund. All performance information for the fund is stated net of all fees and expenses, reinvestment of interest and dividends and include allocation for incentive interest and have not been audited (except for certain year end numbers). The methodology used to determine the Top 5 holdings is the largest portfolio positions by weight. The top 5 do not reflect all fund positions. The Top 5 can and will vary at any given point and there is no guarantee the fund will meet any specific level of performance. Net returns presented are net of fund expenses and pro-forma performance fees. Rowan Street Capital does not charge fixed management fees.

The historic Somerset-based footwear giant has launched ‘Brands now at Clarks’ on its website

Clarks shoe shop in Derbion Shopping Centre, Derby(Image: Derby Telegraph)

Somerset shoemaker Clarks has started selling rival brands for the first time in its history through an online marketplace. The historic company, which has been a presence on the UK high street since 1825, has launched ‘Brands now at Clarks’ on its website.

More than 100 brands, such as major global labels including Adidas and Nike, are now available to buy through the site, as well as other lifestyle products such as clothing and accessories.

The venture marks a major shift for 200-year-old Clarks as it looks to diversify its offering beyond shoes in an increasingly tough retail environment.

Joe Ulloa, vice-president UK & EMEA at Clarks, said: “From the outset, it was essential that every brand partner reflected the values that have defined Clarks for over 200 years – premium quality, comfort and value.

Advertisement

“Brands now at Clarks represent an exciting new chapter for us. It allows us to offer a broader, shopping experience, while staying true to the heritage and trust we’ve built.”

‘Brands now at Clarks’ brings together a portfolio of big names including high-end brands such as Hugo Boss, Tommy Hilfiger, Under Armour and Marc Jacobs. A number of other labels are lined up to join the website in the coming weeks, too, including Armani Exchange, Emporio Armani, Gant, Lacoste, Moose Knuckles, Napapijri, Rains, Timberland and Woolrich.

Clarks was founded by brothers Cyrus and James Clark who opened a tannery making leather goods in 1825. Today the company is a global brand, selling more than 40 million pairs of shoes a year and has more than 1,100 stores.

But the business has faced challenges in recent years amid changing shopping habits and a decline in footfall in physical stores as consumers look to buy more products online. Last year, Clarks was forced to axe more than 1,200 jobs as sales plummeted by nearly £100m.

Advertisement

In September, the company opened a museum in Street, in Somerset, showcasing 200 years of shoemaking. It features hundreds of never-before-seen objects from sheepskin slippers to desert boots, school shoes to Britpop stagewear.

Shares of Adani Power have been on a strong run this month, surging as much as 37% over 13 sessions. The rally in Adani Power shares has made it the most valuable company within the Adani Group, with a market capitalisation of Rs 3.93 lakh crore, surpassing Adani Ports at Rs 3.70 lakh crore.

Part of the diversified Adani Group, Adani Power is India’s largest private thermal power producer. The company has a total generation capacity of 18,110 MW across thermal plants in Gujarat, Maharashtra, Karnataka, Rajasthan, Chhattisgarh, Madhya Pradesh, Jharkhand and Tamil Nadu, along with a 40 MW solar project in Gujarat.

Time to book profits or double down on Adani Power shares?

Adani Power share price is exhibiting a strong continuation of its primary uptrend, supported by a clear alignment of moving averages (short-term above medium and long-term), indicating sustained bullish momentum. After a healthy consolidation phase, the stock has witnessed a decisive breakout with expanding volumes, signalling fresh participation. The recent sharp upmove toward the Rs 190–200 zone in the Adani Power share price reflects strength, though the steep rally also suggests near-term overextension, Ajit Mishra, senior vice president at Religare Broking said. Also read: PNB Housing Finance soars 10% post Q4 results: Why Morgan Stanley, other brokerages remain bullish

Advertisement

Live Events

Momentum indicators are trending higher but approaching overbought territory, which may lead to brief consolidation or minor pullbacks. Immediate support is placed around Rs 170–175, followed by a stronger base near Rs 150. As long as the price holds above these levels, the bias remains positive, and dips are likely to be bought into, with potential for further upside continuation. Ruchit Jain, vice president of technical research at Motilal Oswal, said Adani Power share price had recently given a breakout from its long consolidation phase with good volumes. This, along with the positive momentum across the Adani Group stocks, has led to strong buying interest in the counter. Traders with existing long positions should hold and continue to ride the trend, while any declines in the near term can be seen as buying opportunities. From a fundamental perspective, the surge comes amid rising power demand. JM Financial noted in a recent report that power demand had peaked in early March, but an unusual western disturbance from March 20 disrupted the trend. A massive cloud cover stretching nearly 1,000 km from Afghanistan through Pakistan into India brought widespread rainfall and unseasonably cool weather. With this cloud system now receding from North India, experts expect a return of hotter conditions, which could drive a fresh surge in power demand. “All in all, we anticipate a shortfall in hydro generation (negative for NHPC, SJVN), spike in coal-fired generation (positive for NTPC, Adani Power), extension of Section-11 (Tata Mundra) and high merchant prices (Adani Green, Adani Power),” the domestic brokerage concluded.

Over the weekend, the company announced that its wholly-owned subsidiary Adani Atomic Energy has incorporated its subsidiary Coastal-Maha Atomic Energy, furthering its nuclear ambitions.

At about 11:10 am, Adani Power shares were trading at Rs 204, higher by 1.5% from the last close on the BSE.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

SAN ANTONIO — Victor Wembanyama has transformed the San Antonio Spurs from lottery hopefuls into legitimate 2026 NBA title contenders, with betting markets assigning the franchise roughly a 15-20% implied probability of winning the championship — a remarkable leap fueled by the 22-year-old phenom’s dominance and the team’s late-season surge.

Victor Wembanyama

As the Spurs open the playoffs as the Western Conference’s No. 2 seed with home-court advantage in early rounds, oddsmakers list San Antonio between +450 and +550 to hoist the Larry O’Brien Trophy. That range translates to an approximate 15-18% chance, placing them clearly behind defending champion Oklahoma City Thunder but ahead of most of the field.

Wembanyama, in his third season, delivered a monster regular campaign, averaging 25.0 points, 11.5 rebounds, 3.1 assists and a league-leading 3.1 blocks per game while shooting 51.2% from the field. He earned unanimous Defensive Player of the Year honors and sits among the frontrunners for MVP, showcasing an otherworldly blend of size, skill and rim protection that has redefined the Spurs’ identity.

The Spurs finished the regular season with one of the NBA’s best records, highlighted by a scorching 27-2 stretch from early February through early April that included multiple double-digit win streaks. They posted the highest winning percentage in the league since Jan. 1 and went 4-1 against the Thunder, including impressive road victories. Analysts credit not only Wembanyama but a supporting cast featuring All-Star De’Aaron Fox, rising guard Stephon Castle and complementary pieces that have meshed effectively under coach Mitch Johnson.

San Antonio opened the 2026 playoffs with a statement 111-98 victory over the Portland Trail Blazers in Game 1 on Sunday, where Wembanyama dropped a franchise playoff-record 35 points on efficient shooting. The performance electrified the home crowd and underscored his readiness for high-stakes basketball, though he has emphasized staying grounded and focusing on the present.

Advertisement

Betting markets reflect this momentum. At various sportsbooks, the Spurs sit as the second choice behind Oklahoma City at around +100 to +135 for the Thunder. Implied probabilities place OKC near 45-50% to repeat, with San Antonio in the 16-18% range on platforms like Polymarket, aligning closely with traditional oddsmakers. Wembanyama himself is the heavy favorite for Finals MVP if the Spurs prevail, listed around +500 to +550.

Still, experts caution that a championship run would require overcoming historical trends. Teams this young and relatively inexperienced in recent playoffs have rarely cut through the gauntlet to win it all. The Spurs’ core features several players in their first deep postseason pushes, raising questions about handling fatigue, adjustments and pressure across four grueling rounds.

Wembanyama has addressed the challenge directly, acknowledging the dream of a title while stressing preparation and moment-by-moment focus. “I dream about it every day,” he said recently, but added that the immediate priority is showing up ready for Game 1 and executing scouts. He missed the regular-season finale with a minor rib contusion but entered the postseason fully healthy and ramped up.

The path forward is formidable. A likely second-round matchup against the Denver Nuggets could test San Antonio’s interior defense and experience against Nikola Jokic. Should they advance, a Western Conference Finals clash with Oklahoma City looms as a potential showdown between two elite young cores. The Thunder’s depth, regular-season dominance and playoff experience give them the edge in most projections, but the Spurs’ head-to-head success this season keeps the series intriguing.

Advertisement

Beyond the West, the Boston Celtics represent the top Eastern threat at around +525 to +600 odds. A potential Finals matchup would pit Wembanyama’s generational talent against a veteran, well-coached Celtics squad seeking another ring.

Analysts point to several factors boosting the Spurs’ realistic shot. Wembanyama’s two-way impact — anchoring the league’s top defenses while creating offense with pull-up threes, post moves and playmaking — gives San Antonio a unique advantage. The team’s net rating ranks among the league’s best, and their late surge demonstrated resilience and growth.

Yet vulnerabilities exist. Depth beyond the starters could be tested in a long series, and offensive consistency against elite defenses remains a work in progress. Wembanyama has shouldered a heavy load, and any injury risk to the franchise cornerstone would derail hopes instantly.

Gregg Popovich, the legendary former coach now in a front-office or advisory role, has been spotted at practices, symbolizing continuity with the Spurs’ championship pedigree. The franchise last won titles in 1999, 2003, 2005, 2007 and 2014, building a culture of sustained excellence that current players reference as motivation.

Advertisement

Fan excitement in San Antonio has reached fever pitch, with playoff tickets scarce and the city buzzing after years of rebuilding. Wembanyama’s arrival in 2023 marked the turning point, and the addition of Fox and development of young talent have accelerated the timeline dramatically from initial projections.

Quantitative models and betting markets converge on a 15-20% probability for a Spurs championship in 2026. That figure represents enormous progress from preseason odds that hovered around 65-1 or longer. It also reflects the market’s respect for Wembanyama’s superstar trajectory while discounting the inexperience tax and the Thunder’s status as clear favorites.

For Wembanyama personally, the stakes extend beyond one season. A deep playoff run — or better — would cement his place among the NBA’s elite and validate the hype that surrounded him as the No. 1 pick. He has already shattered expectations with his defensive prowess and expanding offensive game, drawing comparisons to all-time greats while carving his own path.

Coach Johnson and the front office have managed the roster thoughtfully, balancing development with competitiveness. The team’s ability to win without relying solely on Wembanyama has been a key narrative thread, with role players stepping up during stretches of the season.

Advertisement

As the playoffs unfold, every game will recalibrate perceptions and odds. A convincing first-round series victory could push the Spurs’ implied title probability higher, while early struggles might temper enthusiasm. History shows that surprise contenders can ride momentum, but sustaining excellence over multiple series remains the ultimate test.

Wembanyama’s presence alone elevates the Spurs’ ceiling. At 7-foot-4 with guard-like skills and elite shot-blocking, he alters games on both ends in ways few players can match. His growth from rookie season to now has been remarkable, and continued improvement in areas like playmaking and consistency could make San Antonio even more dangerous in future years.

For now, the 2026 title odds crystallize the narrative: the Spurs are no longer a feel-good story but a genuine threat. Whether they can translate regular-season success into championship hardware depends on health, execution and the ability to navigate the brutal playoff gauntlet.

With Wembanyama leading the charge and a supportive cast gaining confidence, San Antonio enters the postseason with belief. The percentage may sit in the mid-teens, but in a league where parity and upsets thrive, that chance feels tangible — and for Spurs fans, electrifying.

Advertisement

The basketball world watches closely as Wemby’s championship quest begins in earnest. At just 22, he already carries franchise hopes on his broad shoulders, turning what once seemed like a distant dream into a credible 2026 possibility.

Sen. Dave McCormick, R-Pa., discusses President Donald Trump’s renewed threats to fire Federal Reserve Chair Jerome Powell and Kevin Warsh’s upcoming confirmation hearing on ‘Kudlow.’

Kevin Warsh is set to testify on Tuesday about his nomination to be chairman of the Federal Reserve, with senators likely to press him on his views of the Fed’s 2% inflation target given the persistent price pressures affecting the U.S. economy since the pandemic.

The 56-year-old Warsh, who served as a Fed governor from 2006 to 2011, will testify before the Senate Banking Committee as senators weigh his nomination to succeed current Fed Chair Jerome Powell, whose term leading the central bank is due to expire in May.

Advertisement

Warsh offered an overview of how he views the price stability component of the Fed’s dual mandate in a written copy of his opening statement, which FOX Business viewed in advance of his testimony.

In his prepared remarks, Warsh says that he supports the Federal Reserve’s dual mandate of promoting price stability as well as full employment, though he didn’t specifically discuss the Fed’s policy target of keeping inflation at 2% over the long-run.

Former Fed Governor Kevin Warsh is the nominee to succeed Powel as Fed chair. (DMV Productions)

“First, Congress tasked the Fed with the mission to ensure price stability, without excuse or equivocation, argument or anguish. Inflation is a choice, and the Fed must take responsibility for it,” Warsh wrote.

Advertisement

“Low inflation is the Fed’s plot armor, its vital protection against slings and arrows,” he said.

“So, when inflation surges – as it has done in recent years – grievous harm is done to our citizens, especially to the least well-off. They lose purchasing power. Their standard of living falls. They may also lose faith in our system of economic governance, raising doubts whether monetary policy independence is all it’s cracked up to be,” Warsh wrote.

Warsh has emphasized the importance of price stability and is skeptical of relying too heavily on a 2% inflation target due to the risk of measurement errors and policy mistakes. (Tierney L. Cross/Bloomberg via Getty Images)

Warsh discussed his view of monetary policy goals in a 2023 hearing before the British House of Lords’ Economic Affairs Committee and said that he views price stability as an imperative, but is skeptical of the ability to measure inflation precisely, and so he prefers a range-based inflation target.

Advertisement

“Price stability is the North Star. Without stable prices, it is almost impossible to have full employment. It is also almost impossible to have economies that are growing at their full potential. When prices are volatile… it is difficult for households and businesses to make the prudent decisions that they might like,” he explained.

“Frankly, we would not know the difference whether inflation was running at 1.7%, 2.0% or 2.3% in the United States or in the United Kingdom because we do not measure it that precisely,” Warsh said. “Economics is not physics – at least not yet.”

Warsh said that he tends to “prefer ranges versus point estimates, in part because of measurement error and in part because I think broad price stability can never be that precise.”

Advertisement

He added that, in general, he thinks viewing inflation that precisely “led many of the central banks to overly stimulate economies a few years ago,” and led to decisions that contributed to inflation running well above target.

“I broadly favor ranges. Price stability, in the numerical definition, will change in the times. The structures in the global economy are changing even as we speak. It strikes me that agreeing on some permanent basis to 2.0% is asking for trouble,” Warsh said.

Inflation peaked in the U.S. at 9.1% in June 2022 and is currently around 3%, having risen over the last year due to tariffs and the recent impact of the recent energy shock caused by the Iran war.

The Fed’s preferred inflation gauge, the personal consumption expenditures (PCE) index, was 2.8% in February on an annual basis. Data from March is due at the end of next week.

Another popular inflation gauge, the consumer price index (CPI), showed inflation jumped to 3.3% in March after a 2.4% reading in February due to the impact of the war on energy markets.

Shares of Tata Steel have gained around 12% so far in April, nearing their record high, with international brokerage Nomura remaining bullish on India’s steel sector, which it says is resilient to multiple headwinds.

In a note released on Monday, Nomura said it maintains a positive outlook on the sector, adding that global factors, including the impact of Chinese competition, are likely to have a limited effect on the earnings potential of major steel players. “Our bullish stance on the Indian steel sector is underpinned by improving domestic price momentum despite global headwinds,” it said.

The war between the US and Iran, and the subsequent closure of the Strait of Hormuz, triggered an energy crisis that rattled global markets in March. Nomura believes large, blast furnace-based steel players are relatively better positioned than smaller, gas-based DRI producers, as they can partially substitute LPG usage with alternatives in downstream operations.

In the absence of any significant disruption or sustained cost escalation so far, the brokerage has maintained its earnings estimates for stocks under its coverage. It has reiterated its ‘Buy’ ratings on Tata Steel, JSW Steel, Jindal Steel, and Lloyds Metals.

Advertisement

Should you buy Tata Steel shares?

Live Events

Nomura has set a target price of Rs 220 apiece for Tata Steel shares, implying an upside potential of nearly 4% from the stock’s last closing price of Rs 211.72 apiece. The global brokerage noted that Indian steel prices slightly corrected last week, but remain near elevated levels. “China’s steel sector witnessed a notable slowdown with steel production in March 2026 declining by 6.3% y-y to 87.04MT, marking the lowest level for the month since mid-2020. The weakness extended to trade flows as steel exports fell by 12.6% y-y to 9.13MT, partly impacted by disruptions from the Middle East conflict,” it said. (Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Nexus Airlines and Aviair will receive a share of more than $5 million from the state government to ensure accessibility to regional air services, as the Middle East conflict continues to put pressure on global fuel supply.

Manchester-based beauty and nutrition e-commerce firm posts revenue growth of 7% for the first quarter of 2026

City AM reporter www.cityam.com

10:42, 21 Apr 2026Updated 10:43, 21 Apr 2026

THG CEO Matthew Moulding (Image: THG/PA)

THG shares surged on Tuesday as the Manchester-based firm defied broader gloom across the retail sector, delivering its strongest quarterly performance in five years.

Advertisement

The beauty and nutrition e-commerce giant posted revenue growth of 7 per cent for the first quarter of 2026, noting that growth was only “modestly impacted” by disruption in the Middle East.

The London-listed company recorded revenue of £393.1m, driven by 8.1 per cent growth in its nutrition division to £159.8m, as reported by City AM.

“It is energising for everyone at THG to see such a strong start to 2026,” said chief executive Matt Moulding.

“While the geopolitical backdrop remains uncertain, we enter Q2 with confidence after a better-than-expected Q1, giving us a stronger base against any unforeseen risks later in the year.”

Advertisement

THG shares climbed 9.5 per cent to 42.2p in early trading.

“Positive underlying revenue momentum was maintained in both divisions,” said analysts at Panmure Liberum.

“Three consecutive quarters of mid-to-high single-digit organic growth are encouraging, but the business still needs to demonstrate consistent translation into higher profits and cash generation, particularly given raw material cost volatility.”

You must be logged in to post a comment Login