At the same time, markets will be closed in the United Arab Emirates on Monday and “until further notice,” according to a statement by the UAE Capital Market Authority, which oversees the Abu Dhabi Securities Exchange and the Dubai Financial Market. The authority said it continues to monitor developments in the region.

ANALYSIS: New data shows WA employers have a gender pay gap nearly four points above the national mid-point, while the state’s mining sector continues to drive the divide.

Between last Holi and this year’s festival, 15 smallcap stocks delivered multibagger returns ranging from 150% to 500%. Backed by sectoral momentum and earnings triggers, these counters turned into standout wealth creators, highlighting the high-risk, high-reward potential of the smallcap segment over a one-year horizon.

It has been exactly one month since Nancy Guthrie was abducted from her home in the Catalina Foothills, and the case that has gripped the nation remains unsolved. As of March 2, 2026, the Pima County Sheriff’s Department and the FBI have transitioned from an intensive “boots on the ground” search to a focused criminal investigation driven by digital forensics and high-value tips.

Savannah Guthrie & Nancy Guthrie

The Abduction: What We Know

Nancy Guthrie was last seen on the night of Saturday, January 31, 2026, when she was dropped off at her home by her son-in-law after a family dinner.

1:47 a.m., Feb 1: A masked individual was captured on doorbell footage disconnecting the home’s security camera.

2:12 a.m., Feb 1: The camera briefly detected a person again before the system was fully disabled.

The Discovery: Family members reported her missing on Sunday morning after she failed to show up for a virtual church service.

Investigators confirmed that bloodstains found on the front porchbelonged to Nancy, and her pacemaker app was disconnected from her phone line during the predawn hours, signaling a violent removal from the residence.

A Shift in Strategy

On February 27, 2026, the Pima County Sheriff’s Department announced a “refocusing of resources.” While the search remains an active investigation, the large-scale presence of patrol units and the FBI’s mobile command post in Tucson have been scaled back.

FBI Relocation: The FBI has moved its primary operations for the case from Tucson to Phoenix, where they can more effectively analyze the “massive amount of data” collected, including over 23,600 tips.

Localized Detectives: The Pima County Sheriff’s Department clarified that while fewer officers will be visible, a dedicated team of detectives is working the case around the clock.

The $1 Million Reward

In an emotional video message shared on February 24, Savannah Guthrie and her siblings, Annie and Camron, announced a $1 million reward for information leading to Nancy’s recovery.

“If you’ve been waiting and you haven’t been sure, let this be your sign to please come forward. Tell what you know, and help us bring our beloved mom home,” Savannah pleaded in the video.

This is in addition to the $100,000 reward offered by the FBI. Since the family’s reward was announced, more than 1,500 new tips have flooded into the 1-800-CALL-FBI tip line.

Advertisement

Investigation Challenges

Despite several purported ransom notes demanding cryptocurrency (sent to local media outlets like KOLD-TV and TMZ), authorities have yet to receive “proof of life.”

Digital Forensics: Experts believe a “getaway vehicle” is the most critical piece of evidence currently being sought. Investigators have seized multiple vehicles, including a Range Rover and the car belonging to Savannah’s sister, Annie, as part of the standard forensic sweep.

DNA Evidence: While DNA was recovered from the home, sources indicate it may be “low-level” and has not yet yielded a definitive suspect profile.

Savannah Guthrie’s Status

Savannah Guthrie has been away from her anchor desk at TODAY since the abduction began, skipping her planned coverage of the 2026 Winter Olympics to remain in Arizona with her family. NBC has stated they are “fully supportive” of Savannah and that there is no current timeline for her return to the show.

How You Can Help

Authorities are asking residents in the Catalina Foothills and surrounding Tucson areas to review any home security or dashcam footage from the overnight hours of January 31 to February 1.

Suspect Description: A masked individual, approximately 5’10” to 6’0″ with a medium build, was seen on the property.

Contact: Anyone with information is urged to call 1-800-CALL-FBI (1-800-225-5324). Tips can be submitted anonymously.

As we reflect on 2025, it is hard to ignore the constant drumbeat of negative headlines: elevated geopolitical tensions, ongoing conflicts, trade frictions, and a broader shift toward de-globalisation. Yet, despite this backdrop of uncertainty, global equity markets once again delivered strong returns—another reminder that markets often advance not in the absence of risk, but in spite of it.

Market backdrop and performance

Table 1.

2025 market and fund returns.

Index/Fund

2025 Return

AGV Capital

26.3%

S&P 500

17.9%

MSCI ACWI

22.9%

MSCI China

31.4%

Hang Seng Index

27.8%

Vanguard Total World Stock (VT)

22.4%

All performance figures are calculated using the Time-Weighted Rate of Return (TWR), which eliminates the impact of external cash flows and reflects the pure investment performance of the portfolio.

As the old Wall Street adage goes, the market climbs a wall of worry. In 2025, investors had no shortage of reasons to worry—wars, tariffs, interest-rate concerns, and an uncertain macro outlook—yet markets moved higher as businesses continued to grow revenues, earnings, and cash flows.

China, concentration, and where the real opportunity was

In last year’s annual letter, we laid out a clear, contrarian thesis. We tilted our allocation decisively toward China at a time when the consensus was widely viewed as unattractive by the market. In 2024, we placed approximately 86.0% of the portfolio in Chinese equities. That positioning proved well justified in 2025, as the MSCI China Index delivered a total return of 31.4%—its strongest year in nearly a decade—and significantly outperformed the S&P 500 total return of 17.9%.

Advertisement

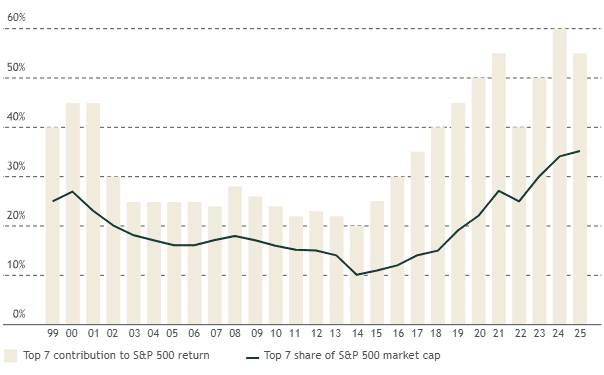

Meanwhile, the S&P 500 itself became even more concentrated. Index levels of concentration reached extremes not seen since the 2000 internet bubble and the roaring 1920s, with the so-called “Magnificent Seven” accounting for roughly 34.0% of the index and contributing about 42.0% of total returns, driven largely by strong investor enthusiasm and momentum around AI-related themes. Excluding the Mag 7, the S&P 500 would have delivered a return closer to 10.0%, roughly in line with the S&P 500 Equal-Weighted Index at 11.0% and Vanguard’s Total US Stock Market Index at around 11.0%.

Figure 1.

Rising impact of the largest 7 U.S. stocks on index returns (1999–2025).

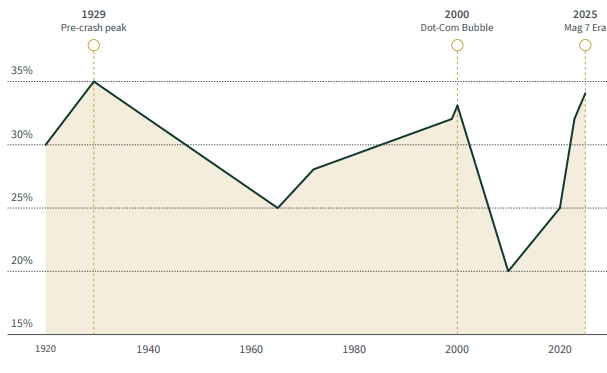

Figure 2.

fiop-7 stock concentration in U.S. market (1920–2025).

Current levels approach 1929 peak, surpassing dot-com era.

In a year when many active US-focused managers struggled to beat a Mag-7-driven benchmark, we delivered a gross return of about 26.3% while deliberately avoiding the US AI bubble and lofty valuations. We stayed anchored to our principles: buying high-quality companies at great valuations. As a result, we outperformed the S&P 500’s 17.9% and the MSCI ACWI Index’s 22.9%. This reinforces an important lesson: earning excellent returns is not about chasing whatever is fashionable; it is about owning great businesses at sensible prices.

China vs. the Magnificent Seven: who really delivered?

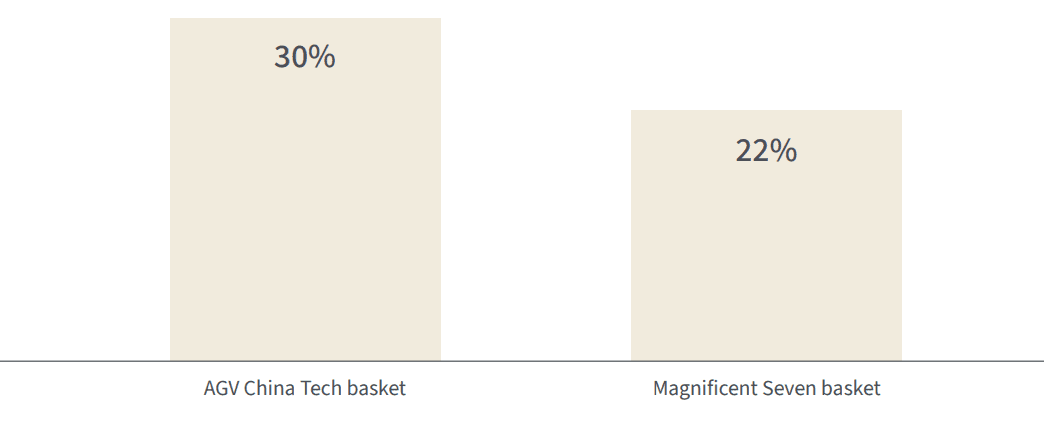

In last year’s letter, we compared a basket of leading Chinese large caps to the celebrated US Magnificent Seven and argued that price and sentiment were pointing in opposite directions. In 2025, that thesis played out in real time. On average, our China basket—Alibaba, BYD, Tencent, Baidu, PDD, and JD.com—returned roughly 30.0%, while the US Magnificent Seven as a group delivered about 22.0%.

Few would have expected the supposedly “uninvestable” Chinese names to outpace their highly praised US counterparts, especially in a year when the Mag 7 enjoyed an AI-driven momentum tailwind and investors were convinced they would “change the world.”

Figure 3.

2025 returns: AGV China tech basket vs. Magnificent Seven (total return, %).

AGV China Tech basket outperformed by 8 percentage points.

As the late Charlie Munger put it, the job is to fish where the fish are. For us, that means using our global mandate to go wherever the real opportunities lie—China, the US, or elsewhere—rather than hugging a single index simply because it feels familiar or popular with the crowd.

Looking through the lens of a holding company

We view the fund as a holding company. When we buy a stock, we think of it as owning a slice of a real business—its revenues, earnings, and cash flows—rather than just a ticker on a screen. To make this concrete, we aggregate the underlying fundamentals of every share we own and translate them into revenue, earnings, and free cash flow per fund unit. This approach allows us to judge our performance the way an owner would: through fundamental growth, profitability, portfolio quality, and valuation.

Advertisement

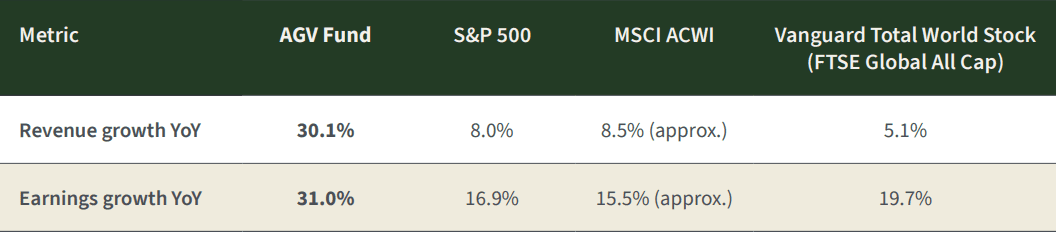

In 2025, our portfolio companies grew revenues by about 30.1% and earnings by 31.0% in US-dollar terms. In the local currencies in which they report, revenues grew 25.6% and earnings 26.6%, with the difference largely driven by dollar weakness and FX translation effects.

Table 2.

Revenue and earnings growth comparison (YoY).

Source: Morningstar, MSCI & Vanguard YoY refers to year-on year comparisons.

As you will see in the growth tables in the report, our companies delivered outstanding growth—substantially higher than the major indices we consider relevant benchmarks. Our roughly 26.3% gross fund performance for the year came almost entirely from this earnings growth. We did not benefit from multiple expansion; returns were driven by fundamentals, not rising valuations.

Valuation: strong returns without paying up

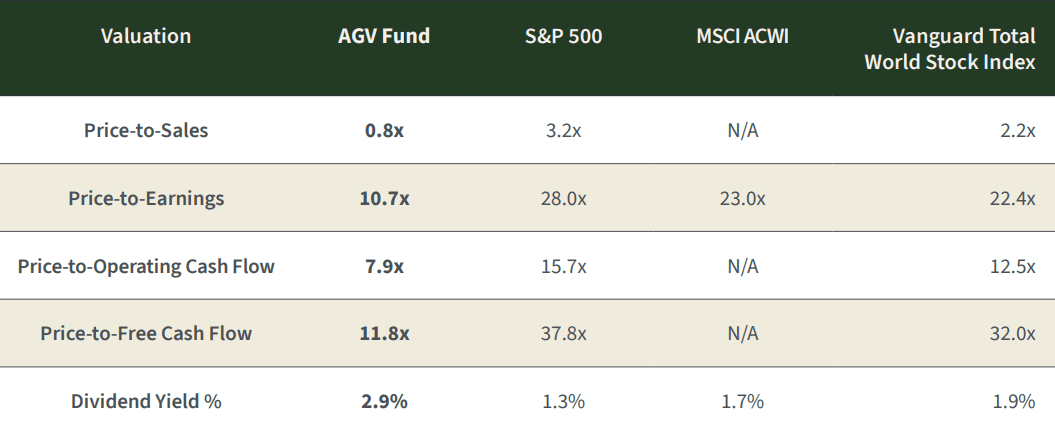

This lack of multiple expansion is visible when we compare our portfolio’s valuation today with last year’s. Despite the strong performance, our portfolio remains cheaper than, or broadly in line with, last year’s levels on most valuation metrics, and continues to trade at a meaningful discount based on our assessment of underlying fundamentals.

Table 3.

Valuation multiples.

Valuation Multiple

TTM FY 2024

TTM FY 2025

Price-to-Sales

0.9x

0.8x

Price-to-Operating Income

9.9x

10.1x

Price-to-Earnings

11.9x

10.7x

Price-to-Operating Cash flow

5.7x

7.9x

Price-to-Free Cash Flow

7.4x

11.8x

When we set these valuations against those of major indices, the contrast becomes even clearer: our holdings trade at a substantial discount to global indices on earnings, sales, and free-cash-flow measures, while offering higher dividend yield and stronger underlying growth. That combination—better businesses at lower prices—is exactly what we look for.

Table 4.

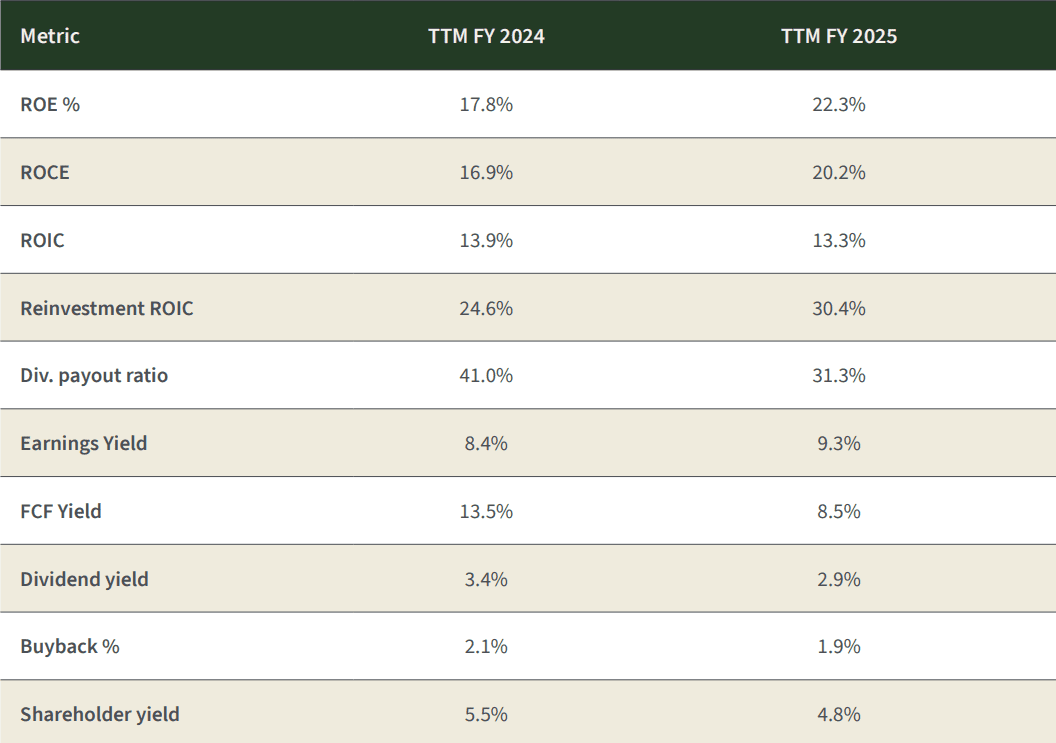

Portfolio quality: returns on capital and profitability

Valuation is only half the equation; quality matters just as much. In 2025 we improved the quality of the portfolio meaningfully. Our return on equity rose from around 17.8% to over 22.3%, and our return on capital employed increased from roughly 17.0% to just over 20.0%. Internal reinvestment ROIC also improved, showing that incremental capital is being deployed at very attractive rates of return.

Table 5.

Portfolio quality metrics.

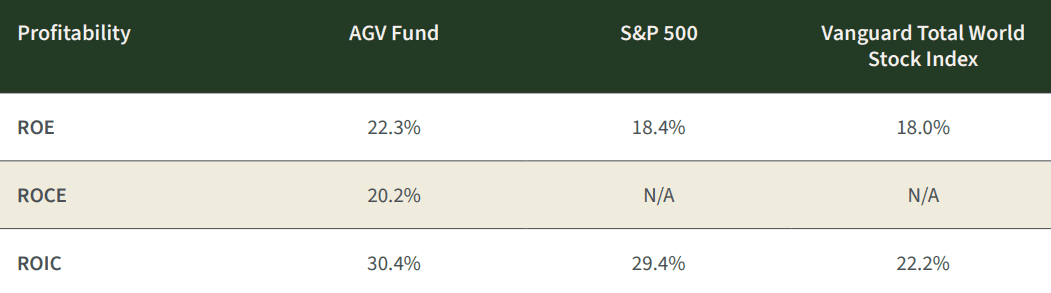

When we compare these metrics to the major indices, the gap is evident. Across Return on Equity, Return on Capital Employed, and Return on Invested Capital, our portfolio companies earn meaningfully higher returns on capital than the broad indices, highlighting both superior business quality and better capital allocation.

Table 6.

Profitability comparison.

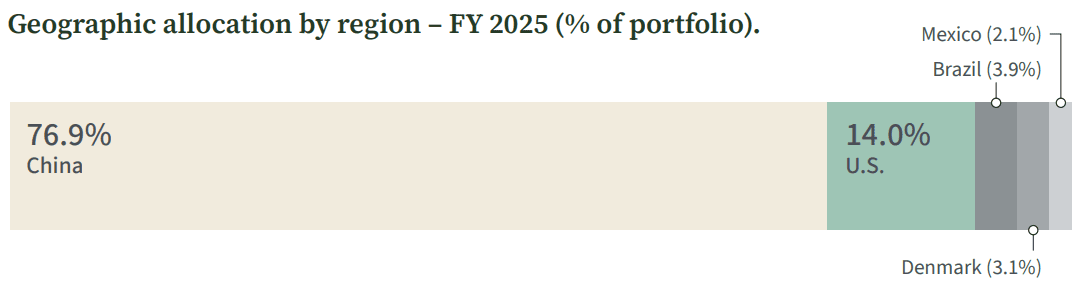

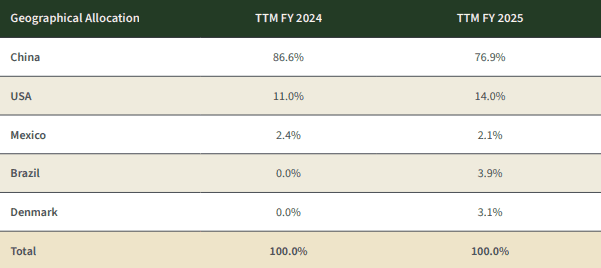

Geographic allocation: China still leads, diversification expanded

Our current geographic exposure compared with last year reflects both conviction and select diversification. We reduced our China exposure from the mid-80s to the high-70s and introduced two new regions—Denmark and Brazil—where we found exceptional businesses that meet our criteria. The US allocation also increased modestly as select opportunities emerged at reasonable valuations. We remain willing to go wherever the risk-reward profile is most attractive, rather than sticking to any home-market bias. The table & chart below summarizes our geographic allocation at year-end.

Figure 4.

Table 7

Geographic allocation

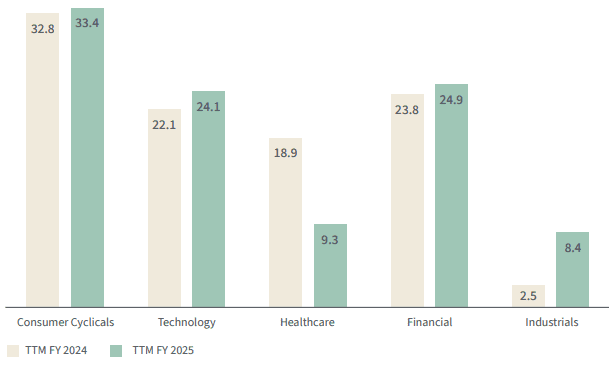

In addition to geography, we also manage diversification by business model and sector. The chart below shows our sector allocation as of year-end and comparison of last year, highlighting where we are finding the most compelling opportunities today.

Figure 5.

Sector allocation – year-on-year comparison (% of portfolio).

TTM = trailing twelve months

Putting it all together

We approach public markets with the mindset of business owners. Investing, to us, is akin to owning a family business: you focus on the long term, the durability of the model, the integrity and alignment of management, and the price you are paying relative to intrinsic value.

Our strategy is simple but demanding in practice:

Own high–quality companies with durable competitive advantages.

Partner with management teams whose incentives are aligned with shareholders.

Pay prices that build in a margin of safety.

Look globally, not locally, for the best mix of quality and value.

In 2025, our companies grew earnings by more than 30.0%, trade at valuations that remain well below global market averages, and exhibit higher returns on capital than the indices. This combination drove approximately 26.3% growth in the fund, allowing us to outperform the benchmarks while still leaving what we estimate to be roughly 30% undervaluation in the portfolio. If valuation gaps were to narrow and our holdings were to move closer to assessed fair value, this would imply meaningful upside potential, before considering any additional fundamental growth.

On top of this, our portfolio offers an estimated total shareholder yield of about 4.8%, combining a 2.9% dividend yield with 1.9% buyback yield. Even without assuming incremental growth, a convergence toward fair value would, in such a scenario, represent a material contributor to forward returns over time.

Advertisement

We are very optimistic about our holdings. We believe the companies we own are high quality, attractively valued, and well diversified by business model and geography. We also believe deeply in alignment: we invest alongside you in the fund, and I have personally increased my investment, reflecting my conviction in the opportunity ahead.

We hope this report gives you the clarity we would want if the roles were reversed and we were in your seat as shareholders. As always, thank you for your trust.

A Cambridge ag-biotech start-up aiming to reinvent crop protection has secured $3.8 million in early-stage funding to accelerate the development of next-generation herbicides and pest control products using artificial intelligence.

Bindbridge, founded in 2025 by a trio of Cambridge University scientists, is building what it describes as a category-defining platform for agriculture: an AI-driven system capable of designing “molecular glues” to target and degrade specific proteins in weeds and pests. The company believes its approach could help tackle the mounting crisis of herbicide resistance, which is estimated to cost farmers tens of billions of dollars each year.

The funding round was led by Speedinvest and Nucleus Capital, two investors focused on deeptech and climate innovation. The backing will allow Bindbridge to expand its eight-person team, advance its proprietary AI platform and begin laboratory testing of its first agricultural molecular glue candidates within the next 12 months.

The scale of the opportunity is considerable. According to United Nations data, around 40 per cent of global crops are lost to plant pests annually, while plant diseases cost the global economy more than $220 billion each year. Herbicide-resistant weeds alone are estimated to destroy crops worth $70 billion annually. At the same time, regulators are tightening rules on chemical persistence and environmental impact, putting pressure on the traditional agrochemical model.

The global ag-chem industry currently spends up to $9 billion a year on research and development, yet it can take as long as 12 years to bring a new active ingredient to market. Bindbridge argues that the sector’s conventional discovery methods are slow, expensive and increasingly constrained by resistance and regulatory hurdles.

Advertisement

At the core of the company’s strategy is its AI platform, known as BRIDGE. The system uses computational models to design molecular glues, small molecules that trigger the targeted degradation of specific proteins inside plants or pests. By leveraging the plant’s own intracellular protein control systems, Bindbridge aims to create more precise, potent and environmentally responsible crop protection agents.

Beyond herbicides, the company sees applications for insecticides, fungicides and even sprayable plant traits designed to improve nutrient efficiency, enhance heat tolerance or support carbon sequestration.

George Crane, co-founder and chief executive of Bindbridge, said the agricultural sector is facing “significant performance and sustainability challenges” that demand a fundamentally new approach to product development.

“There’s currently no affordable, rational or systematic way to discover molecular glues at scale for agriculture,” he said. “We’re using AI to rapidly and accurately derive new molecules that can change farming’s future.”

Advertisement

The investment will also support co-development discussions with major agrochemical companies. Bindbridge says it is already in late-stage talks with industry players to collaborate on targeted protein degradation projects.

Speedinvest investor Namratha Kothapalli said the company was applying modern AI techniques to one of the world’s most consequential industries. “They’re unlocking entirely new chemical space that the industry simply couldn’t reach before,” she said.

Nucleus Capital general partner Dr Isabella Fandrych described the platform as a potential breakthrough in tackling herbicide resistance and strengthening global food systems. “Their computational approach lays the groundwork for a new era of sustainable agriculture,” she said.

Bindbridge’s founding team, Dr George Crane, Dr Alex Campbell and Dr Simeon Spasov, bring experience spanning machine learning engineering, plant biology, chemistry and venture building. With the new capital, the company aims to position itself as a disruptive force in agricultural R&D, combining deep science with scalable AI to address one of the most pressing challenges in global food security.

Advertisement

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

As investors prepare to celebrate Holi on Wednesday, March 4, 2026, the real splash of green has fallen upon these 80 stocks from Indian markets that have turned multibaggers from last Holi, which fell on March 14, 2025. The returns have skyrocketed up to an extraordinary 1,822%, even as Indian equities grappled with tariff concerns, subdued earnings and stretched valuations.

Out of the 80 stocks under review, 17 have delivered over 200% returns in the said period, with Midwest Gold rising up to 1,822%, the highest among its peers. The Karnataka-based company processes granite blocks, including the mining and processing of all other types of minerals. The next is Kalind, which has yielded 1,143% returns.

The Indian stock market will remain open on Wednesday, March 4, even as Holi celebrations continue in several parts of the country. The official trading holiday for Holi in 2026 was observed on Tuesday, March 3, and there will be no exchange closure on Wednesday.

The National Stock Exchange (NSE) and BSE follow a pre-declared holiday calendar, and March 3 was the designated closure for Holi this year. Although many states are expected to celebrate Holi on March 4, trading will proceed as usual across equity, derivatives and currency segments.

In 2026, Indian exchanges will remain closed for a total of 15 days, covering a mix of national and religious occasions.

The next closures will be Ram Navami on March 26 and Mahavir Jayanti on March 31. In April, trading will remain suspended on Good Friday, April 3, and Ambedkar Jayanti on April 14. Maharashtra Day on May 1 will also be a holiday.

Advertisement

Bakri Id on May 28 and Muharram on June 26 will mark additional closures in the first half of the year. In the second half of 2026, markets will be shut for Ganesh Chaturthi on September 14 and Gandhi Jayanti on October 2. Dussehra will be observed on October 20, followed by Diwali Balipratipada on November 10 and Guru Nanak Jayanti on November 24. The final trading holiday of the year will be Christmas on December 25.

The holiday comes amid heightened volatility in domestic equities. On Monday, markets witnessed sharp selling pressure, losing more than 1% amid weak global cues and escalating geopolitical tensions in West Asia. The Nifty opened with a gap down and extended losses during the session before trimming some decline in the final hour to settle at 24,865.

The fall was broad-based. Auto, realty and energy stocks led the losses, while only a few defensive names and select metal stocks showed resilience. Broader markets also remained under pressure, with mid-cap and smallcap indices slipping by more than 1.5%, reflecting widespread caution among investors.

Investor sentiment has deteriorated following a surge in crude oil prices amid Middle East tensions. The spike in oil has raised concerns over inflation, currency pressure and a higher import bill for India, weighing on equities. Volatility indicators have also moved higher as participants reduced exposure amid fears of further escalation.

Advertisement

Ajit Mishra, Senior Vice President of Research at Religare Broking, said the recent decline has pushed the Nifty closer to its swing low around 24,600.

“A decisive break below this could extend the correction towards the 24,400 mark. On the upside, the 25,000 to 25,250 zone is likely to act as an immediate hurdle in case of any recovery,” he said. Mishra advised investors to maintain a cautious stance, keep position sizes light and focus on disciplined risk management given the current volatility.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

GM Business Growth Hub backs transformation at Oldham business

From left: Matt Pryce, managing director at Heyside Group; Janine Smith, director of GM Business Growth Hub; Cllr Arooj Shah, leader of Oldham Council; Garreth Brown, finance & transformation lead, Heyside Group(Image: Growth Company)

A plastics manufacturer is hoping to grow capacity by up to 60% after investing in robotics and advanced tooling with the backing of Greater Manchester business support bodies.

Heyside Group, of Oldham, makes PVC injection‑moulded products and processes some 300 tonnes of recycled plastic per week to create products for the traffic management, utilities and infrastructure sectors.

Its ongoing modernisation programme has seen it move away from manual manufacturing with bosses investing in robotics, advanced tooling, digital systems and automated processes. Managers say the move will help it to stay competitive while opening new market opportunities in the UK and beyond. They estimate the project could help grow capacity by 60% and could help the business unlock some £4.8m in additional revenue as it enters new markets.

The business has been supported by the GM Business Growth Hub, which helped bosses access Made Smarter expertise and digital internships, technical assurance from the Northern Engineering and Robotics Innovation Centre (NERIC), materials‑innovation support from CEAMS and decarbonisation guidance from the Green Economy team.

Advertisement

The Growth Hub also connected Heyside to a £500,000 GMCA loan that has backed the firm’s investment in robotic paint‑spraying systems, new tooling and conveyor upgrades – and two Knowledge Transfer Partnerships with Lancaster University and the University of Salford.

Matt Pryce, managing director at Heyside Group, said: “The Growth Hub’s support has been instrumental in helping us move from traditional manufacturing towards a modern, automated factory environment. From robotics to materials research, the guidance and connections we’ve received have accelerated our progress and strengthened our position for future growth.

“We are excited about the opportunities ahead as we continue to scale our capabilities.”

Cllr Arooj Shah, leader of Oldham Council, said: “Heyside Group’s transformation reflects the strength of Greater Manchester’s business support ecosystem. Their commitment to innovation and modernisation demonstrates how manufacturers can embrace advanced technologies to grow sustainably and competitively.

Advertisement

“The council is proud to play a role in supporting this progress and looks forward to seeing the next phase of their development.”

Janine Smith, director of GM Business Growth Hub, said: “Heyside is becoming a standout example of innovation-led manufacturing growth in Greater Manchester.

“By connecting the business to the right expertise at the right time – from digital adoption to robotics, research partnerships and funding – we’ve helped create a pathway to long-term competitiveness and new market opportunities. Their progress shows what’s possible when ambition is matched with coordinated support.”