Altimeter Capital founder and CEO Brad Gerstner discusses President Donald Trump’s new investment accounts for children, China’s latest AI restrictions and Samsung’s stock slide on ‘Mornings with Maria.’

Corporate America is pouring support behind the Trump Accounts program, with Altimeter Capital founder, Chairman and CEO Brad Gerstner predicting the initiative will attract more than $100 billion in additional private commitments over the next year as businesses and philanthropists back the new investment accounts for American children.

Brad Gerstner joined FOX Business’ Maria Bartiromo on “Mornings with Maria,” where he pointed to what he described as strong early momentum following the program’s launch, saying businesses, philanthropists and families are embracing the initiative.

President Donald Trump stands next to a bell before ringing it to open the New York Stock Exchange ahead of the launch of Trump investment accounts in the Oval Office. (Mandel NGAN / AFP / Getty Images)

“We have tens of billions of dollars in commitments we haven’t announced,” Gerstner said. “I said to the president, I think we’ll have $100 billion of additional contributions in the next 12 months.”

Gerstner said the initiative was designed as a public-private partnership that relies on private contributions alongside the government’s initial investment. He highlighted commitments from corporate leaders and philanthropists, arguing the program allows donors to directly fund investment accounts for children in schools, communities and states across the country.

Advertisement

BNY CEO Robin Vince joins ‘Mornings with Maria’ to discuss BNY’s 250-year evolution, President Donald Trump’s new investment program for children, the U.S. economy and digital assets.

“It is huge societal ROI and America is unlocking their wallets and pouring a lot of money into these,” Gerstner said.

BNY CEO Robin Vince also joined Maria Bartiromo on “Mornings with Maria” to discuss BNY’s role in launching the program, which is designed to give more Americans access to long-term investing through early saving and the power of compounding.

President Donald Trump launches Trump accounts, described as big savings accounts for everyone.

“We’ve got 40% of Americans who don’t participate directly in the stock market,” Vince said. “This initiative is about bringing more people to have a stake in the actual capital markets, in the economy and the greatest companies in America.”

Vince said the program encourages families to begin investing as early as possible, arguing that regular contributions over time can significantly increase the value of an account through compounding. He also noted that many companies, including BNY, are matching contributions for eligible employees’ children.

Yes. Corporate subscriptions are available for teams and organisations, with discounted rates as user numbers increase. Pricing starts from $1,625 + GST per user. Get in touch

to discuss the right option for your organisation.

Business News subscriptions are used by executives, investors, consultants and professionals who need to stay informed and make better decisions about the WA market. When you subscribe you’ll get

Unlimited access to WA’s most trusted business journalism

Data & Insights — detailed profiles of WA companies, people, projects and deals

MyBN — a personalised feed based on the companies, people and sectors you follow

Special publications and industry reports

Daily and weekly email newsletters

Data & Insights is a research tool built specifically for the WA market. It draws on more than 30 years of Business News reporting, updated regularly to reflect what’s happening now. Use it to:

Look up detailed profiles of WA companies, including financials, directors and ownership

Find decision-makers and track their career movements

Research live and completed projects across WA industries

Monitor deals, appointments and market activity

Access industry rankings and league tables

Data & Insights is updated daily by our dedicated research team, which uses the latest announcements, ASX filings and editorial coverage to keep our person, company, list and project records up to date.

Business News welcome all opportunities to make our dataset accurate, complete and current, so if you have an update request, please email the team at general@businessnews.com.au, and we’d be happy to assist.

Advertisement

MyBN

is part of every subscription. It’s your personalised view of Business News. You can follow the companies, people, sectors and projects that matter to you, and get a news feed and alerts tailored to your interests. You can save articles to read later and retain only what you need.

Only subscribers have full access to all content on the Business News website.

Advertisement

If staying informed about the WA economy is part of your job, and/or you’re looking for networking opportunities in WA, Business News is built for you.

Business News subscribers are:

Executives and directors tracking competitors, clients and market movements

Investors and advisers researching companies, deals and industry trends

Consultants and professionals staying across sectors relevant to their clients

Business owners looking for leads, context and market intelligence

Most Business News publications cover national or global markets. Business News is focused entirely on Western Australia, which means the journalism, the data and the intelligence are all built around WA companies, people and projects — not adapted from a national feed. Data & Insights, included with every subscription, combines more than 30 years of WA-specific editorial research with live business data. There’s no comparable product for the WA market.

Advertisement

The Morning Digest Email provides a comprehensive wrap of the major headlines, relevant to WA business, and includes with a snapshot of the overnight news covering oil, gold and ASX-listed companies.

The Afternoon Wrap Email focuses on the news covered by our team of journalists during the course of the working day, including exclusive stories and analysis, all of which relates to WA business and the local economy.

The BN Weekender Email contains a wrap of the Business News from the week that was, highlighting the top stories in each area of WA business. Sign up for free.

Advertisement

We’re happy to help. Get in touch

and our team will come back to you.

PhD in Law & Economics with a dissertation on corporate wrongdoing, paired with an accounting background and a lifelong interest in markets.I write almost exclusively about undercovered small and mid-cap names, currently concentrated in fintech and consumer lending, where legal, regulatory, and governance risk routinely moves the stock more than anything on the sell-side’s model. Value, growth, secular trends, accounting shenanigans: if it fits that lens, I’m interested.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of ECPG either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

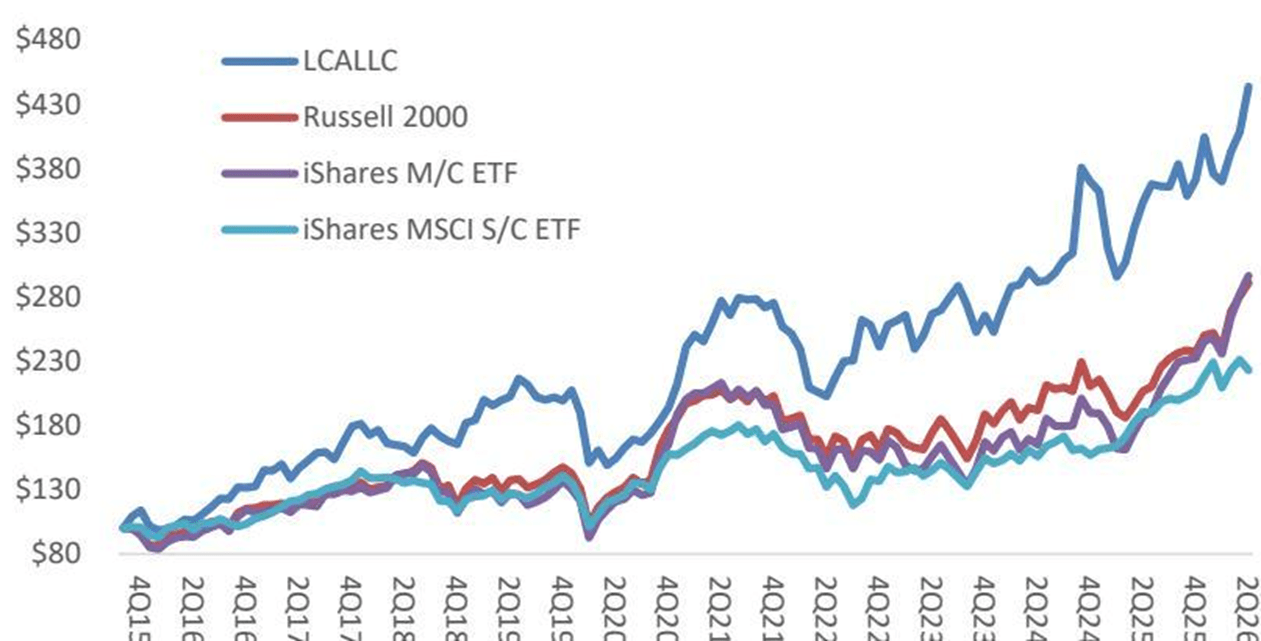

For the 2Q26 quarter ((ended June 30, 2026)), cumulative net returns improved 20%, lifting year-to-date returns to +19%, in both cases trailing the Russell 2000 and the iShares US MicroCap ETF (IWC) but well ahead of the iShares SmallCap EAFE (SCZ) ((ex-N. Am)) ETF. Returns were generated with little direct exposure to any of the themes du jour ((AI, hyperscalers, cyclical semis, etc)) that drives flows at passive funds. Since inception in November 2015 through quarter end, LCA has returned a cumulative 343% net of fees, or 15% CAGR, ahead of those indices. Past performance is no guarantee of future results. Individual account returns may vary. ¹

Net returns

Advertisement

Long Cast

R2000

IWC

SCZ

Advertisement

2015 (2-mos)

14%

-5%

-5%

Advertisement

1%

2016

15%

21%

Advertisement

21%

3%

2017

36%

Advertisement

15%

13%

33%

2018

Advertisement

-8%

-11%

-13%

-18%

Advertisement

2019

21%

25%

22%

Advertisement

25%

2020

-3%

20%

Advertisement

21%

12%

2021

42%

Advertisement

15%

19%

10%

2022

Advertisement

-12%

-20%

-22%

-21%

Advertisement

2023

10%

17%

9%

Advertisement

13%

2024

39%

12%

Advertisement

14%

2%

2025

0%

Advertisement

13%

22%

32%

1Q26

Advertisement

0%

1%

1%

1%

Advertisement

2Q26

20%

22%

26%

Advertisement

6%

Cumulative

343%

191%

Advertisement

196%

123%

CAGR

15%

Advertisement

11%

11%

8%

LTM

Advertisement

25%

41%

59%

17%

Advertisement

YTD

19%

23%

27%

Advertisement

8%

Long Cast was founded in 2015 on the principles of long-term and patient investing in well-researched small- and micro-cap companies. It was conceived as a “food truck version of a hedge fund”, a nod to its SMA structure, low overhead and Brooklyn base, backed by +12-years of institutional equity-research experience. It takes concentrated positions and aims for 15% annualized returns, operating as an alternative to passive investing, with more transparency than a fund and without using leverage.

Portfolio Update

In 2Q26, PDEX (PDEX), PESI (PESI) and MTRX (MTRX) were the largest contributors. There weren’t any significant decliners. We substantially added to NRC (NRC) and exited CCRN (CCRN), which was acquired, returning a solid after-tax IRR despite the unavoidable short-term treatment.

At quarter end the top five positions represented 62% of the portfolio. I am patiently putting available cash to work, recently adding to QRHC (QRHC), which has lapped negative revenue comps, and may benefit from stabilization in industrial manufacturing as well as new contracts announced earlier in the year.

Advertisement

It is our goal and intention to own large percentages of fewer companies over time, but we start small, continue researching and adjust as warranted. One new small position is a chemical company in turnaround, that offers the virtues of sound management, a strong balance sheet and fully depreciated assets. I am weighing if it should be a larger position, but probably not at current prices.

Since 2023, management and the Board have been excellent strategic and financial stewards. Previously an undercapitalized mini conglomerate, non-core assets have been sold off and there’s over $40M of net cash on the balance sheet. The business is built around three chemical plants, each over 50-years old, in TN, VA and SC, that supplied the once abundant carpet and textile manufacturers in the area, and now produce lubricants, surfactants, coatings, and other mixed and reacted chemicals for a variety of end markets.

From this point forward, the opportunity is improving on low-capacity utilization and “sales people who waited for the phone to ring”. It’s a solvable problem, but it’s not an easy path. This business is all about manufacturing with quality and consistency. A former HB Foster plant engineer explained to me that the chief sales people in this area are the process engineers and the plant managers with demonstrated capabilities around scheduling, batching, minimizing turnarounds and safety. These are manufacturing culture type things and culture takes time to change.

Meanwhile, our CEO and CFO’s prior successful exit was in pool chemicals, ie branded bleach, which is to say, wholly driven by sales and marketing. I’m not sure if what’s needed here from this point forward overlaps with any of their prior experiences. And that leads to questions around the intentions of the Board, some of whom are long time shareholders and possibly looking for the next fool to buy these old assets an exit.

Advertisement

I like a long and wide opportunity pathway, and this seems constrained and restricted. The underlying capacity puts a cap on revenues and the factories require regular maintenance and CAPEX. The industry operates in oversupply and peer group multiples are in the single digits. Meanwhile, to achieve our 15% hurdle rate at current prices would require multiple expansion into the double digits. Under certain conditions – higher-margin end-markets or faster growth – a premium multiple may be justified, but given the hill to climb, I think it pays to wait. I’ll continue to monitor it and continue to look for other ideas.

As I indicated in my mid-June email, I did a 15-minute set on the Vegas Strip by way of a “pitch session” at the Microcap Club / Planet Microcap conference, where I offered brief high-level thoughts on what makes stocks attractive, and then shared two stocks, PDEX and NRC that I think indeed are attractive.

The PDEX pitch offered an attempt to quantify the anticipated incremental benefits to operations if Zimmer (ZBH) succeeds with the mBos robot commercialization (a corrected version of the slide is below). The milestones, prices and margins are all derived from public filings and we assume four effectors per system sale, as an informed estimate.

Advertisement

ATK procedures per year

800,000

implant cost (est)

$5,000

Advertisement

US implant “gross revs”

$4B

Milestone

12/31/2028

Advertisement

12/31/2029

12/31/2030

Hurdle: mBos “gross revs”

$156M

Advertisement

$381M

$609M

implied procedure market share

4%

Advertisement

10%

15%

assumed mBos procedures

31,200

Advertisement

76,200

121,800

consumables @ $75 / procedure

$2.3

Advertisement

$5.7

$9.1

GP @ 30% margins

$0.7

Advertisement

$1.7

$2.7

incremental EPS impact

$0.16

Advertisement

$0.40

$0.64

# of systems needed

156

Advertisement

381

609

>> each system does 200 procedures / year

4 effectors / systems @ $15K each

Advertisement

$9.4

$22.9

$36.5

>> $15K / effector x four per system sale

Advertisement

GP @ 45% margins

$4.2

$10.3

$16.4

Advertisement

>> margins are spelled out in contract

incremental EPS impact

$0.99

$2.41

Advertisement

$3.85

net incremental EPS impact

$1.15

$2.81

Advertisement

$4.50

Zimmer’s purchase of Monogram (MGRM) last year included “contingent valuation rights” (CVRs) that pay out $3.41 / share in each year from 2028 to 2030 that mBos gross revenues exceed certain hurdles. Based on these estimates, we calculated the number of systems needed to achieve those revenues, and it triangulates to a capital sale in the range of ~$1M per machine, in line with the cost of Stryker (SYK)’s Mako platform. Stryker sold 860 units, in its first three years so the forecast 609 units to trigger the final CVR seems achievable. And even if the timing is wrong or our estimates imprecise, as long as the direction is right – and Zimmer is putting significant resources behind the launch – once the system launches, PDEX could experience an exceptional transformation in operating cash flow that would justify a substantially higher corporate value. This is why it remains a top position.

On NRC, our newest investment, I discussed the company’s evolution from owner / operator to professionally led management team, and the expected benefits from putting a growth focused, incentivized and entrepreneurial executive suite behind this strong and recognizable brand, in a business with strong FCF generation and in a market where the two leading competitors just merged in a PE backed $6.5B deal.

Quantitative evidence that supports our optimism includes the recently announced largest contract in company history leading to the highest 12-mos backlog in history. Deferred revs are also growing and this typically leads sales. Furthermore, management indicated that the second year of the aforementioned contract is materially larger than the first, which infers that in one year’s time, 12-mos backlog could be even larger, and with capacity to do more. We continue to add opportunistically.

Advertisement

Among our other large holdings, PESI recently preannounced 2Q26 earnings indicating continued weak profitability but strong backlog growth on expanding processing at Hanford. There is potential for significantly more waste volumes if a decision is made to grout ((embed in concrete)) up to 9M gallons of low-level tank waste by 2030. This recent GAO report illustrates how large that opportunity could be and how favorable the government is in pursuing it.

Two other large holdings, MTRX and RSSS (RSSS), are on June 30 fiscal years and won’t report earnings until late August or possibly September. Given their weighting, results may be impactful to the portfolio. I think in both the cases, cash earnings will prove better than market expectations, especially MTRX, which all but guided to record profitability.

In Conclusion: On AI, Entrepreneurship and Investing

In our 1Q26 letter, I discussed my perspective of AI as a tool that’s creating a wonderful environment for entrepreneurs. Evidence is emerging along those lines, with growth in business formation and in new sole proprietorships exceeding $10M in revenues. And while the media focuses on layoffs at tech companies, evidence suggests that it’s creating ample work elsewhere, and not just for electricians and hvac installers.

Meanwhile, in the investing world, an AI-focused fund called “Situational Awareness”, led by a former Open AI (OPENAI) employee, recently blew up over $40B in capital. The fund strategy was to buy AI-related companies and short the disrupted software businesses, and use significant leverage in the process. It was recently forced to sell off its entire portfolio at a discount to meet margin calls. It puzzles me how someone so smart can be so unaware of the risks associated with using leverage in investing. Prior to its demise, returns were reportedly up 270% ytd and had been up 1,000% since inception.

Advertisement

It takes effort to resist the notion that we know how this is going to turn out. Our minds enjoy closure and sometimes even grope for conclusions, no matter how illogical, with a bias towards consensus.

Long Cast has experienced large drawdowns in the portfolio, and given our concentrated positioning, may well again in the future. But we operate under the premise that investing is a practice of patience and endurance, not a sprint. This is intended as a durable business that grows capital well into the future. In order to do that, we need to survive. We don’t use margin. We don’t seek out volatility. With rising rates, an expanding war and global constraints on a most a critical energy input, I’m comforted by our non-consensus portfolio.

As always, I remain committed to building a durable and sustainable business based on a repeatable investment process and intelligent capital allocation. I remain grateful to have clients ((by design)) aligned with my long term, small company centric and research-intensive focus. I welcome the continued interest from individuals and institutions as I patiently grow the business.

Sincerely / Avi

Advertisement

References

1. Performance data is based on Interactive Brokers “Portfolio Reports” function; shown net of management fees, expenses, and commissions; unaudited; and unless otherwise noted, since inception in Nov. 2015. Past performance is not a guarantee of future results. Individual account performance may vary. Any investment entails a risk of loss including the total loss of capital. ADV form available through Broker Check; CRD # 175005

Jonah Hill has made clear he has little patience left for people who still see him as the awkward teenage version of himself from “Superbad,” pointing to years of Brazilian jiu-jitsu training as evidence he is done being defined by a role from nearly two decades ago.

The comments came during a taping of the “SmartLess” podcast, recorded earlier this year in Los Angeles, where Hill appeared alongside hosts Jason Bateman, Will Arnett and Sean Hayes. Clips from the episode resurfaced widely online this week, reigniting conversation around Hill’s remarks about his physical transformation and his frustration with how audiences continue to perceive him nearly 20 years after “Superbad” made him and co-star Michael Cera household names.

Speaking on the podcast, Hill said he had grown tired of being reduced to the character of Seth from the 2007 comedy, telling the hosts he would “f— annihilate” anyone who continued to see him that way, and that he was not exaggerating. The comment drew immediate laughter from Bateman, Arnett and Hayes, though Hill did not walk back the remark, instead doubling down on the sentiment.

Hill’s confidence traces directly to his years of Brazilian jiu-jitsu training, a pursuit he first took up in late 2018 at age 35. He began training at Clockwork Jiu-Jitsu in New York City, where he reportedly trained four to five sessions per week to build his skills in the discipline. According to other reporting on his fitness journey, Hill has also trained under Josh Griffiths, a third-degree black belt who has competed at Abu Dhabi World Pro events and worked alongside top UFC fighters.

Advertisement

Before delivering his more pointed warning to critics, Hill leaned into the humor of the moment, joking that his body had begged him not to fall so deeply in love with the sport, and that his wife regularly reminds him he is a comedian rather than a professional fighter. When Bateman jokingly suggested the two of them settle things physically, Hill claimed without hesitation that he could take on all three podcast hosts simultaneously, further building the bit before pivoting to his more serious message about the lingering “Superbad” comparisons.

This is not the first time Hill has spoken candidly about how public perception of his body has affected him over the years. He has previously discussed how comments about his weight impacted him significantly during his rise to fame in his late teens and early 20s, and has been open in past interviews about how those experiences shaped both his relationship with exercise and his broader sense of self-image throughout his career.

Now settled in San Diego with his wife and their two young sons, Hill appears to occupy a markedly different place in his life than the young actor first introduced to audiences through “Superbad” in 2007. His jiu-jitsu practice appears to function as more than a simple physical outlet, instead serving as a genuine source of personal confidence that stands in direct contrast to how strangers online continue to characterize him nearly two decades later.

Hill’s frustration with being permanently associated with a single early role reflects a broader pattern common among performers whose breakout parts came relatively early in their careers, particularly in comedic roles that lean on physical characteristics for humor. “Superbad,” directed by Greg Mottola and produced by Judd Apatow, became a defining touchstone of mid-2000s teen comedy, launching both Hill and Cera into leading roles across film and television in the years that followed.

Advertisement

Since “Superbad,” Hill has built a considerably more varied career, earning two Academy Award nominations for best supporting actor, for “Moneyball” in 2012 and “The Wolf of Wall Street” in 2014, while also moving behind the camera as a writer and director with projects including the documentary “Stutz” and the film “Mid90s.” That range stands in contrast to the persistent public shorthand that continues to reduce him to his breakout comedic role from nearly 20 years ago.

Whether anyone actually takes Hill up on his tongue-in-cheek challenge remains to be seen, but the resurfaced clip has clearly struck a chord with fans and commentators reacting online this week. The moment underscores how even beloved, culturally resonant comedic performances can leave behind lasting assumptions about an actor that don’t always keep pace with how much that person’s career, and life, has evolved in the years since.

Zuber Issa, CEO of EG On The Move.(Image: EG On The Move)

Blackburn millionaire Zuber Issa’s petrol forecourt and convenience retail group has completed the acquisition of 260 sites in France.

EG On The Move has says all legal, works council and regulatory market requirements have been met in the deal with EG Group, which plans to exit the French market. EG On The Move said the acquisition is an important part of strategic growth plans – and referred to France as a key European market.

The network of sites is said to be a strong platform for investment, including growth of the retail offer. EG On The Move has previously talked of its ambition to expand electric vehicle charging provision through its EV On The Move brand.

Zuber Issa, chief executive officer of EG On The Move, said: “We are delighted to complete the acquisition of these 260 sites. This is an important step in the continued growth of EG On The Move and reflects our confidence in the strength and long-term potential of the French market.

Advertisement

“France represents a significant opportunity for EG On The Move, and we are committed to investing in the acquired network to enhance the customer offer and experience, support our colleagues and drive long-term sustainable growth. We look forward to working closely with our French team, whose expertise and dedication will be central to our success, and to supporting them in delivering positive outcomes for our customers, employees, partners and local communities.

“I would like to warmly welcome our new colleagues to EG On The Move, and I am excited about the opportunities we will create together as we build on the strong foundations already established across the network.”

The deal with EG Group follows EG On The Move’s acquisition of independent petrol forecourt operator MPK Garages Ltd in May. That move expanded EG On The Move’s footprint, particularly across the Midlands, bringing 27 petrol forecourt sites to the group.

EG On The Move now owns and operates more than 550 trading units across the UK, including 270 petrol forecourts and convenience stores, along with 220 branded foodservice concessions. More than 60 of its sites offer fast EV charging.

Australian shares have shaken off a weak start to forge a modest gain as oil prices retreated on hopes the US and Iran are looking to de-escalate their conflict.

HFCL shares climbed 5% to Rs 203 on the BSE on Monday after the company won an international order worth around Rs 522.73 crore. The development further strengthened investor sentiment around the telecom equipment maker, which has emerged as one of 2026’s multibaggers. HFCL, in a filing to the bourses, said the contract will be executed by January 2027 under general contract conditions. The company did not disclose the identity of the international customers.

HFCL stock has rallied a staggering 195% in the last six months. As a result, FIIs more than doubled their stake in the company from 7.1% in the March quarter to 15.7% in June.

HFCL Q1 results

HFCL reported a net profit of Rs 246 crore in the first quarter of financial year 2027, compared with a net loss of Rs 29.30 crore in the same quarter last year. Revenue from operations came in at Rs 1,915 crore, up 120% from Rs 871 crore in the corresponding quarter of the previous financial year. Also read: Forget selling! FIIs doubled down on this AI multibagger stock that’s up 200% YTD

The company reported its highest-ever order book of around Rs 26,665 crore in Q1FY27, nearly five times its FY26 revenue, strengthening its long-term revenue visibility. The export story has also gathered pace. Export revenue rose to Rs 1,063.30 crore, accounting for 55.53% of total revenue in Q1FY27, compared with Rs 209.70 crore, or 24.08% of revenue, in Q1FY26.

Advertisement

HFCL has revised its FY27 revenue growth estimate to 40%. Its board has also approved an investment of Rs 215 crore to build a manufacturing facility for advanced AI data centre connectivity solutions.

Live Events

Still time to buy HFCL shares?

Deven Choksey Research sees another 86.50% upside potential, calling defence and aerospace the “X-factor” that changes the entire investment thesis for the stock. The brokerage initiated coverage on HFCL with a ‘Buy’ rating and a target price of Rs 362 apiece earlier this week. HFCL has consolidated its defence assets under HFCL Advance Systems (HASPL), integrating aerostructure manufacturing, including the acquired business with more than Rs 2,000 crore in export orders, radar or surveillance systems through Raddef, and thermal weapon sights into a single scalable entity. Read more:HFCL bags Rs 442 crore optical fibre cable export orderAn ammunition manufacturing facility is being established in Andhra Pradesh for electronic fuzes, multi-mode hand grenades (for which there are only 3 licensees in India), and 155 mm artillery shells.

“We believe defence revenue trajectory to be Rs 77 crore (FY26) to Rs 400 crore (FY27) to Rs 1,200 crore (FY28) to Rs 5,000 crore (FY29), at 25%+ EBITDA margins. Critically, defence customers provide advance payments, dramatically improving working capital dynamics compared to the legacy EPC business,” Deven Choksey said.

HFCL is also gradually transitioning from a commodity OFC supplier to a high-value AI optical connectivity platform through its OptiQ AI brand, which was launched earlier this month, Deven Choksey noted. “Through subsidiary HTL Limited, data centre interconnect (DCI) solutions are expected to contribute Rs 400 crore in FY27 and Rs 800 crore in FY28, at margins above the blended corporate average. The global AI optical interconnect TAM is projected at $73 billion by CY30,” the brokerage further said in its report.

Advertisement

According to the brokerage, HFCL is at an inflection point where three structural shifts are converging simultaneously. The company is transitioning from a domestic EPC-dependent telecom contractor into an export-led, product-driven technology platform spanning AI optical connectivity, defence electronics and aerospace manufacturing.

Monarch Networth echoes the view. According to analysts, HFCL has evolved rapidly from being a largely domestic optical fibre cable manufacturer into a globally diversified technology company.

HFCL is India’s largest optical fibre cable manufacturer, with manufacturing facilities across the country. Analysts added that the company was the first Indian player to develop and commercialise 5G Fixed Wireless Access customer-premises equipment.

Advertisement

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of Economic Times)

Lawrence Farm is located on Moor Lane south of the dual carriageway on the edge of Wincanton

Daniel Mumby, Local Democracy Reporter

08:05, 03 Aug 2026

A stock image of cows in a field(Image: Carina Chowanek/Pexels)

A large Somerset farm near the A303 is to be sold by the council to help finance front-line services throughout the county. Lawrence Farm is located on Moor Lane south of the dual carriageway on the edge of Wincanton, consisting of a farmhouse, associated outbuildings and 75 acres (just over 30 hectares) of land.

Advertisement

Somerset Council agreed in November 2023 to review its existing county farms as part of a broader assessment of its assets, land and property, with a view to disposing of those deemed surplus to requirements and channelling the proceeds into essential services.

The farm will now be marketed in four separate lots – though the council has not disclosed any public estimate of the anticipated sale value.

The farmhouse at Lawrence Farm has stood empty since March, following the council’s negotiations with the former tenant to relinquish their tenancy.

The farm buildings and surrounding land are presently managed under a separate six-month tenancy arrangement, which is due to expire at the end of September.

Advertisement

The farm is flanked by Brains Farm to the east, a solar farm to the south and Wessex Water’s waste water treatment plant to the west, with the River Cale running through a considerable portion of the land.

The farm will be marketed in four distinct lots, with an uplift clause in place to ensure the council benefits from any increase in value should the land subsequently be developed.

David Ashton, one of the council’s property officers, said in his written report: “Our estates team has halted submitting a planning application to convert the farm buildings for residential use, due to flood risk issues that have arisen and the associated lengthy delay and risk of refusal.

“The asset will be disposed of via the open market, in various lots, with the appropriate covenants and/or uplift in place.”

Advertisement

Under ordinary circumstances, revenue generated from the sale of land, property or other assets – known as capital receipts – cannot be directed towards day-to-day expenditure on front-line services.

However, the council was granted approval in February by central government – for the third consecutive year – to use proceeds from asset sales for this purpose, as well as to finance its ongoing transformation programme.

The council has declined to disclose the anticipated proceeds from the farm sale, citing commercial sensitivity.

You must be logged in to post a comment Login