If English devolution deepens under Burnham the competitive pressures on Wales will increase

09:40, 10 Jul 2026Updated 09:49, 10 Jul 2026

Andy Burnham.(Image: Peter Byrne/PA Wire)

For Wales the prospect of an Andy Burnham premiership should not be viewed through the usual PR-driven prism of Labour politics or Westminster personalities.

The more important question is what his approach to power and economic development would mean for a nation that already has devolved government yet still struggles to turn it into a sustained economic advantage.

Advertisement

Burnham’s political appeal has always rested on something different from the standard Westminster offer. He has consistently spoken the language of place and built a reputation in Greater Manchester around transport, housing, skills, local accountability and a more muscular form of regional leadership.

Whether one agrees with every aspect of his record or not, he has shown that English city regions can become serious political and economic actors in their own right.

That is why Wales should pay close attention because if a Burnham-led UK Government were to accelerate devolution within England, then the implications for Wales could be significant.

Not because such a policy would be anti-Welsh, but because it could create a much more competitive set of English regions, each with stronger leadership, clearer economic priorities and greater freedom to act.

Advertisement

For years, Wales has often compared itself with England as a whole, which is the wrong comparison because the real competition increasingly comes from Manchester, Birmingham, Liverpool, Leeds, Bristol and Newcastle, each of which is trying to position itself as a destination for investment, talent, innovation and infrastructure.

If those places are given more power over skills, transport, planning, housing, business support and inward investment, they will not wait for Wales to catch up.

That is the challenge, and Wales already has a devolved government, its own economic development responsibilities, its own education system, and its own ability to shape policy in areas that matter directly to business. Yet too often, the machinery of economic development in Wales feels slow and fragmented, with little visible urgency in the basic task of growing the Welsh economy.

If English devolution deepens under Burnham, the competitive pressures on Wales will increase in five areas. The first is inward investment, and a powerful mayoral authority with a clear proposition can go to investors and say, with confidence, what it stands for, which sectors it wants to build, what infrastructure it can offer, and how quickly it can help firms make decisions.

Advertisement

Wales should be able to do the same, but too often our proposition is obscured by institutional complexity and inter-regional competition.

The second is skills, and Burnham has long understood that local economies cannot be transformed if the skills system is disconnected from employers. If English regions gain more influence over training, employment support and technical education, they will be able to align their workforce more closely with growth sectors.

Wales already has many of these levers but having powers and using them well are not the same thing, and our further education colleges and universities need to be part of a much more coherent national mission than they have been for the last 27 years.

The third is infrastructure, and Greater Manchester’s transport agenda has been central to Burnham’s identity as a leader. He understands that buses, trains, housing and employment sites are not separate issues, but shape whether people can access jobs, whether firms can recruit and whether places can grow.

Advertisement

Wales cannot afford to treat infrastructure as a series of disconnected projects. Whilst South East Wales has benefited from public investment, the rest of Wales – especially North Wales – has been left behind.

The fourth is political influence, and whilst a Burnham premiership might be more sympathetic to places outside London, it could also mean that powerful English mayors become even more influential within Whitehall. They will be in the room arguing for funding, freedoms and investment, and Wales cannot assume that its status as a devolved nation automatically gives it priority.

The fifth is enterprise, and this is where the issue becomes most urgent, as Wales lacks enough businesses. Our business density remains below the UK average, and our start-up and scale-up rates are not where they need to be.

A more entrepreneurial England, driven by assertive regional leadership and stronger local economic tools, would place Wales under even greater pressure unless we respond with a serious strategy for business creation and scale-up of our own.

Advertisement

None of this means we should oppose further English devolution as there is no long-term benefit to Wales in an over-centralised neighbour dominated by Whitehall and London. But if English regions are given new powers, the Welsh Government needs to ask itself a harder question, namely what have we done with the powers we already have, and what more can we do?

It is easy to call for more devolution, but harder to show that existing powers are being used with sufficient purpose, especially when Wales desperately needs a sharper economic development model, business-facing economic leadership, and backing for entrepreneurs.

Above all, Wales needs to take competitiveness much more seriously. An Andy Burnham premiership would not necessarily weaken Wales as it could create an opportunity for a new economic settlement across the UK, one in which places outside London finally receive greater power, attention and resources.

But it will weaken Wales if we respond passively, and if English city-regions are given more tools and use them with ambition while those running our nation continue with slow decision-making and institutional caution, the gap will widen.

Advertisement

And that won’t be because England has too much devolution, but because Wales has failed to make the most of its own.

That is the real lesson, and a Burnham premiership may simply expose what has long been true, namely that Wales cannot rely on constitutional status alone.

If increased English devolution forces Wales to become more ambitious, it may prove a useful shock, but if it merely leaves us complaining from the sidelines while the English regions get on with the job, then we will have no one else to blame but ourselves.

To paraphrase Apollo 13’s Jim Lovell’s actual fateful utterance to Mission Control in 1970—not the word-smithed movie version, but the real one—“Okay, Houston, we’ve had a problem here,” Horizon Central had a problem several weeks ago, too. But a good one, to be sure, which is a lot of client questions. Not too many, that’s not the problem. Just too many to do them all justice in one sitting.

Why not just answer and move on? Some can be answered succinctly. Others require a certain minimum background and defining of terms. The standard P/E ratio might be a meaningless or misleading valuation measure for a certain type of company, but the reason needs to be explained, as well as why an alternative one is more suitable. It might be necessary to describe a scenario for how the valuation realization will develop over time. Enough information so that the explanation makes sense and isn’t just a planted axiom—an unsupported assertion that can make an argument seem logical at the start, with everything thereafter resting on a false foundation, or no foundation at all.

Advertisement

Like this sort of familiar, breezy assertion: “We like XYZ-sector here, it’s pulled back from its risk-on highs and offers pretty good value now at the lower end of its recent trading range, and consensus earnings estimates have bottomed out.” Does that really tell you anything useful other than what the share price has done and what other people think about that?

Me, I’m just asking questions here, but are we talkin’ the Mag 7, at a P/E of only 24.8, which is cheaper than the 29.6 of 12 months ago? I heard that just recently. Or are we talkin’ the Mag 7, two of which have negative free cash flow and one of which trades at 700x free cash flow? Ordinarily, analysts don’t include negative figures in valuation averages. Let’s give these two companies the benefit of the doubt, and just call it an even 100x, so that all seven companies can be averaged. The group trades at 150x run-rate free cash flow, based on the most recent reporting periods.

In typical calculations, non-cash stock compensation is usually adjusted in free cash flow. We did NOT do that in this exercise. If a company didn’t utilize stock options, you’d think employees would demand cash instead, so it really is an operating expense—and dilutes shareholder returns even as stock.

Because, on a run-rate basis across the Mag 7, it amounts to $108 BILLION! One approach to a superfluity of questions is to:

Advertisement

(i) divide and conquer.

That’s why we held a roundtable-type webinar several weeks ago about the rapidly deteriorating business model of the five AI data-center hyperscalers, four of which are members of the Mag 7. The plan was to spend a generous amount of time on a topic that’s relevant to anyone exposed to the equity markets, thereby freeing up time at this Quarterly Commentary for issues more directly relevant to our portfolio holdings. At the table was one of our analysts and private fund managers, Fredrik Tjernstrom, along with James Davolos, our Director of Research and manager of the Inflation Beneficiaries ETF. Fredrik writes our short-sale report, The Devil’s Advocate. His May fundholder letter1 was essentially a sell recommendation on those AI data-center companies. We couldn’t accommodate a live audience at that roundtable, since we’re moving offices, but we will be able to at the next one.

As best-laid plans of mice and men—and luck—would have it, there were way more questions about other topics than about the data centers. We addressed many of them at the roundtable, but the overflow will supersede some of what had been planned for today, and there remain more than we can adequately handle today.

Questions, for example, about—and I quote—the “stunning” decline in the price of Miami International Holdings (MIAX) stock in response to the potential threat of the new prediction markets like Kalshi. MIAX, by the way, has actually done better than the other securities exchanges, and it’s no lower now than it was a few months ago.

Advertisement

There were specific questions about the other exchanges and the negative implications of the recent regulatory approval of perpetual futures contracts. And about why we liquidated mineral royalty positions. And about the short- and long-term outlook for cryptocurrency, and whether our bitcoin thesis is still the same as in 2015. And about gold. And about data center project development on TPL land, plus requested updates on related companies like LandBridge (LB), PriairieSky, and WaterBridge (WBI). And a request to describe some initial new portfolio positions that relate primarily to Spin-Off strategy accounts, which are somewhat different than Core Value. You should contact your relationship manager about that one—and, if necessary, ask for me. All legitimate questions. Plus a couple more that will be addressed here, because they pretty much require a response.

Oh, and we were asked to please keep this Commentary to a maximum of 90 minutes. Another approach to an excess of topic demand per topic-minute supply is to:

(ii) employ a central theme that ties them together.

For us, that is to emphasize—in new ways that keep it fresh and top of mind—the power of financial compounding and the power of being able to employ a very long time horizon. We try to do both. In fact, one can’t happen without the other; it’s easy to say, hard to do, rarely practiced.

Advertisement

It’s a reason we favor securities exchanges and royalty companies, among other asset-light businesses. Many of the world’s national securities exchanges have been operating since the early to late 1800s. The nature of their business is what gives them this rare economic persistence.

It’s a reason that royalty companies are unique: their life-of-mine and 20-year contracts, which well-exceed the duration of ordinary business cycles, support their revenue and profit margin persistence.

And, of course, land. It’s a rare public market investor who buys land. How would you even do it? It’s not an uncommon asset class among the extremely wealthy. We once listed the largest of them; it’s not a short list and they own a LOT of land. Why do you think that is?

Ted Turner died in May: He owned 2 million acres of land.2 He could not possibly have been thinking, when making those purchases, about merely the next 10 years. Land is a perpetuity, the longest-lived of assets, and can compound forever. It has the additional property that it can often be repurposed for higher, better uses. Can’t do that with a tractor or a data-center server. In Turner’s case, land and species restoration was one goal.

Advertisement

Importantly, the available supply of land is always shrinking—in acres per person—because the world population is always increasing. Even land in remote areas of Texas and Canada is not isolated from expanding resource demand elsewhere in the nation or the world, whether it’s for oil and natural gas. Or for compute power for AI, which translates into demand for water to cool the electric power plants that provide the electricity for a multi-thousand-acre 10-gigawatt campus that could power 2x Chicago’s electricity demand.

If the capital allocators at those land companies understand the ultimate value (and valuation multiple) difference between a perpetuity like surface acreage and the depletable minerals that come with it, they can enhance that value.

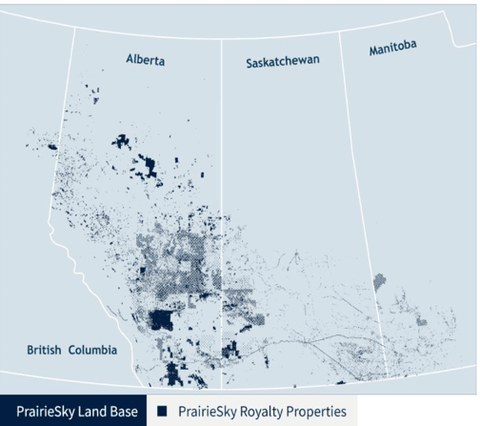

PrairieSky, the subject of one of the roundtable topic questions, is a land and royalty company that has done just that. In the 12 years since its IPO, even while more than tripling its acreage from 5 million to 18 million acres, it managed to double its acres per share. That’s about 6% annually, in addition to whatever revenue and earnings growth it managed to achieve.

That astoundingly large and largely unexploited land portfolio, which sprawls along a roughly 750-mile axis across three Canadian provinces, gives PrairieSky the advantage of not having to reinvest profits in additional royalty contracts. Its large cash flow budget is fully available to pay dividends, repurchase shares, and make expansion-type land acquisitions. That consistently applied capital allocation plan by an executive team that requires of itself to, within three years of appointment, make cash purchases of enough PrairieSky stock to be worth 2x to 5x their salary. This is separate from their direct stock-based compensation. It is a strategy toward ensuring itself of a very long stretch of financial compounding possibilities.3

Advertisement

Those of us gathered here happen to know that it’s possible to own land in the public sphere, even though this largest of all physical resources is not even listed as a sector in the equity indexes. That was the idea—land, not oil—in the original buy recommendation for Texas Pacific Land Trust over 30 years ago: to own the internal, frictionless compounding benefits of share repurchases to increase the per-share acres held.

(iii) Alarm-bell client questions are another way to determine which topics should take precedence.

Two were asked during recent events that caught my ear. The type that pretty much requires a response. If seeming shifts in our investment choices don’t make sense to a client, then the fault lies with the communicator. These questions will initiate today’s discussion. Here they are:

I find it interesting that as an active investor who dislikes index funds, you are suddenly producing ETFs. Why?

Advertisement

Would you address how you’ve have been absent from the IPO market for decades but, more recently, have participated more. I always thought IPOs and value investing were like water and oil.

As different as these questions appear to be, they both relate to how we practice our long-horizon value philosophy. It’s a difference between semantic form—the terminology that’s being asked about—and investing substance. I won’t cover the entirety of the ETF question response—though it’s a separate response, it largely overlaps the Roundtable version, plus there’s no need to burden those who attended the Roundtable. Instead, I’ll just cover the conclusion and add a sidebar. The sidebar is not about indexation today, but about how it came into this world, the origin story. The real story is not what we imagine.

Indexation and Us

First, here’s the crux of the misunderstanding: We’re not antagonistic toward indexation as a concept, nor as it was first practiced in the 1970s by Vanguard’s founder John Bogle. It can be a valuable tool, and did much good for many. We don’t disdain overvalued or misrepresentative index funds any more than we disdain an overvalued common stock or mis-labeled industry sector. If an index offers an attribute we can employ to good effect, we’ll use it, no differently than any other security.

The Alerian MLP ETF, for instance, which tracks an index of natural gas pipeline companies, can help solve the wasting asset problem of bonds due to inflation. It has a 7%-plus distribution yield without the K-1 tax reporting problem, and receives regulated increases in earnings over time to compensate for the inflation-driven increased costs of replacing and operating their pipeline networks. Those few extra percentage points of return do the trick. This ETF is one inflation-beneficiary instrument we’ve used in income-oriented portfolios.

Advertisement

But the ETF industry is a very different creature than it once was. The origin story, of which this is only one part, is instructive.

John Bogle’s espoused idea of indexation in 1974, was: Don’t try to pick and choose among the many actively managed mutual funds and their different strategies, and which the average investor was wholly unequipped to evaluate. (And certainly not individual stocks.) Instead, went the liberating idea, just dispense with trying to outperform the market, and instead own the entire market so as to simply participate, through corporate profit growth, in the expansion of the overall economy. Without the high fees, which at the time could average over 2%.4 The academic theory already existed, but no one had tried to implement it.

Part of the idea was that if you just passively participate in the entirety of the market, you can get the benefit of the “true” clearing prices as collectively determined by all the jousting of active investors—one person buying what the other was selling. That free ride on the efficient market works just fine so long as indexed assets are some modest proportion of the total, so that index investors don’t themselves impact the prices.

The idea caught on and Vanguard indexed mutual funds were hugely successful at gathering assets. In the 2000s, though, arose the ETF industry. It was a lower-cost instrument and had the very attractive feature of intra-day trading, which mutual funds do not. The asset-gathering combine that arose eventually collected more indexed dollars than there were actively managed dollars. That changed how prices were determined. Each new ETF dollar had to go toward buying more of the very same indexed company shares. With new dollars always coming in, ETFs became the marginal price-setting buyer of what they already owned. Thus did the business end of indexes, the ETFs, cross over from passively participating in the price discovery, to having a hand in making the prices.

Advertisement

Which is kind of weird. You once knew if your stocks were expensive or performing relatively well because they could be compared, arms-length-basis, to the whole market. But now the market price is partly set by the index’s associated ETFs as a profit-making business, not merely as a measuring tool. How can you reference the S&P 500 as a benchmark when the ETFs are the ones setting the benchmark?!

Other scale-based distortions came about. Out of practical need, the ETF organizers changed the rules of security inclusion to accommodate the trillions of dollars they had to handle. It was unworkable to try to include companies that were too small or didn’t have enough share-trading liquidity. That created an artificial bifurcation of winners (index constituents) and losers (the excluded class of companies). The losers had less access to fund flows, which impacted their cost of capital, and received less research attention, all of which suppressed their valuations. (We have reason to like that, though—more of which later.)

That money influx also created a self-reinforcing cycle whereby the largest, highest-weight constituents received a disproportionately larger share of new ETF inflows. The indexes became less and less representative of the broad economy. You don’t need an MBA to know that the makeup of U.S. GDP does NOT look like these S&P 500 index weightings. Does anyone think the mix of corporate activity in the accompanying sidebar is what supports the formidable economic power of the U.S.? Here are some of the index weightings. Reflect a moment upon how large those economic sectors are—not how big the companies are, but where the populace spends its weekly and monthly money even if indirectly through intermediate goods and services.

U.S. GDP Profile, according to the S&P 500:

Advertisement

3% from Energy (that’s Oil & Gas Exploration; Refining; Storage & Transportation, like pipelines; etc.)

5% from Consumer Staples (that would be Food & Staples retailing like Costco (COST), Walmart (WMT), drugstores; the Food Products companies themselves, like General Mills (GIS); Beverages; Household Products like Procter & Gamble (PG); Personal Products; etc.).

6% from Consumer Discretionary (need more be said than: Automobiles, household furniture, electronics, apparel, hotels, restaurants, media & entertainment, retailing, and beyond?)

But, 49% in Information Technology!! Or should that be a question mark instead of an exclamation point? Is 49% of the economic output of the entire U.S. really and truly from the services of Meta (META) and Google (GOOG) and Nvidia (NVDA) and their cohort? Or anything remotely close to that figure?

Whether this misallocation of investment capital will have a remunerative outcome or be a tale of woe is not germane to this discussion. The point is that the market indexes have long ceased to be the holistic solution for the financially uninformed, for Main Street as Mr. Bogle would say. How are non-professionals equipped to select from thousands of ETFs, including leveraged sector and single-stock ETFs, when the intent was to provide a simple, low-selection-risk long-term asset allocation vehicle? “Long-term” is the operative concept, and what paradoxically joins us to John Bogle’s vision of indexed investing. The original experiment was undone by its own success as a good idea.

Our Commonality With Indexation: John Bogle Style

I had the honor of debating John Bogle about active vs. passive management—and the friendliest debate it was—at a Grant’s Interest Rate Observer event in 2017. As I said in my opening remarks:

I came here to do “debate.” Except I ran into a problem. As I review your writings and interviews about investing and the markets I realized I basically agree with 95% of what you say; we’ve conducted some of the same research and drawn some of the same conclusions, and written or said the same things.

Subject to one condition, we even share common ground on the active/passive point of debate. Because, when I listen to you, I realize I don’t have to think from a public policy perspective—my clients can afford access to consultative resources. You think deeply about public policy. And with that condition, I found I agree with you: Main Street, the little guy and gal, need basic, safe modes of investing, protected from what they don’t know and from the predations of Wall Street. We’ve written and said as much ourselves, albeit from a different vantage point.

I went on to observe how that model of paternalistic altruism had lately fallen victim to the unintended consequences of Vanguard’s success in driving down management fees. Once the ETF market began to take off after the mid-2000s, it couldn’t live on 3-basis-point fees, even if investor-owned Vanguard could. The ETF providers began to dismantle the experiment—bringing investors right back to square one—by balkanizing the holistic market index into ostensibly value-added strategies like country-specific or industry- or style-specific funds for which they could charge 20x more. It is toward the 85-basis-point funds that their marketing prowess drew new investment dollars.

Advertisement

Horizon’s essential concord with John Bogle’s investment philosophy was that the great power of compounded earnings growth could not be achieved except by holding to a very long-horizon, unbroken chain of it—“staying the course” in his everyman tongue. His vehicle of choice for his constituency was a whole-market index. Our choice for ourselves and our clients is to identify the rare business models that can sustain such a long period of high-order financial compounding.

Peter Doyle recently described the John Bogle/Vanguard creation story, along with some other misunderstood modern portfolio theory creation stories, like the development of security price volatility (standard deviation) as the appropriate measure of risk. His observation was about how mechanistically such practices are followed once they become institutionalized. Not much thought is now given to how and why they were created and if they even—if looked at squarely—make sense.

A Side Note on the Birth Pangs of Indexation:

John Bogle didn’t set out to democratize equity investing as a societal good. Hired out of university by Wellington Management, he wanted to be a superior active fund manager, and publicly disdained buy-and-hold strategies. Within 15 years, he was President. This was near the final years of the Nifty Fifty bubble, on the heels of a merger he orchestrated with a Go-Go growth fund group that was riding that bull market. The conservative Wellington, with its allocations to bonds and preferred stocks, naturally lagged the market, and Bogle led it into high-growth, high-profile companies with P/E ratios about twice that of the market. In 1970, at 38, Bogle was appointed CEO. In1974, amidst the Nifty Fifty bear market, he was fired. Those bluest of blue-chip growth stocks declined 40% from their year-end 1972 high to their year-end 1974 low.

Advertisement

Bogle negotiated hard to stay in the mutual fund business, countering a buyout offer from his Wellington partners with his own proposition. He proposed that Wellington could lower its cost structure by selling him its internal mutual fund administration operations, which he would turn into a low-cost provider by mutualizing so as to be owned by its unitholders—becoming a non-profit institution. This became Vanguard. But, he was restricted by the Vanguard charter from providing any investment services to those funds, from actually managing money. Nor could he own any of the profits, only be a salaryman. In a sense, he was stuck. But not without ideas and some necessity-based inspiration.

Bogle saw a twinned opportunity: Actively managed funds underperformed the S&P 500 index by well over a whole percentage point, yet, as a mutualized fund administrator Vanguard had a far lower fee structure. Plus, who would possibly compete with him on a cost basis? Any such person would have to forego profit participation and likewise settle for a salaried position like Bogle was forced into.

The bigger challenge: Bogle needed to scale up and raise more assets, but how to skirt the non-compete restrictions of his Wellington agreement, which forbade him from managing a fund?

He could do it if he created a fund with no investment management. How is that even possible? Seemed like a contradiction in terms. By, simply, a passive replication of the S&P 500 index. He had a competitive cost advantage, was pretty sure he had a going-forward performance advantage, and was very sure he had a marketing advantage. It was a big business idea and a laudatory de facto public policy idea. But there was sausage-making, too.

Advertisement

Which brings us to why we’ve produced our own ETFs (of the active variety)

Some Horizon clients prefer an ETF structure, or for various reasons can’t open a standalone account and require an ETF. Other prefer the ETF model but are restricted from doing so and therefore do open individual accounts. Meaning that an ETF can be a valuable tool to access one of our strategies.

It might also offer differentiated portfolio exposure; we wouldn’t bother if we thought otherwise.

Example: the sum total of all the holdings in the Inflation Beneficiaries ETF that are also S&P 500 constituents amount to a 0.57% weight in the S&P 500 and 0.59% in the Russell 1000. 5 Excuse me for a moment…!!!

If that is a fair indication, then most equity investors lack countervailing exposure to the risk of commodity price inflation, which is one of the principal few systemic risks to the stock market—meaning the ones it’s very difficult to avoid or diversify away.

Advertisement

The looming shift in the supply/demand imbalance of the past decade—from an oversupply condition—runs across global hard commodities: oil and ultimately natural gas, iron ore, copper, and other electrification metals like cobalt and lithium. These raw inputs infuse every facet of the economy, which means that higher prices in these commodities can be particularly inflationary for the general price level. Price increases can degrade profit margins throughout the companies in the index.

Moreover, even if such price increases don’t seriously impact the CPI, there is great optionality in localized inflation in individual resources, sometimes geographically localized as well. Might as well add in land and water. The S&P 500 will not benefit from that optionality to any measurable degree.

The disinflationary era had its day, if that’s not a Yogi Berra-ism. The inflationary era is not quite here. That’s a curve that’s nice to be ahead of. At the very least, the Inflation Beneficiaries ETF is a form of completion fund: providing what the index is missing. We think it’s more than that, relative to what passes for but isn’t actually an inflation hedge, like mining and chemicals companies. We think it’s a better mousetrap.

Another valuable function that a Horizon Kinetics ETF or other fund can provide for us is exposure to an otherwise inaccessible market or which would not be well-executable as a sub-strategy of individual holdings within a client account. Example: In Japan, as elsewhere, ETF exposure is typically limited to the large- and mega-cap companies. Those are usually global in scope and generate much or most of their revenues outside their home market. There is little direct exposure to the companies that form the local economy, and which might be quite vibrant and undervalued.

Advertisement

In Japan, we have two distinct and entirely local strategies that operate beneath the indexed large-cap umbrella that asset allocators believe provides diversified exposure to the Japanese economy. One of them is the Japan Owner Operator ETF. The other—the Japan Special Opportunity strategy—buys publicly traded captive subsidiaries of corporate parents that the government is determined should be made independent or be wholly taken private. That’s the value recognition catalyst. As to the value part, many of these subsidiaries are priced at classic Graham and Dodd style discounts, and bit by bit they are indeed being acquired at substantial premiums. Sometimes the parents are undervalued, too. In this case, we wish we had an ETF! So far, clients open a separate investment advisory account in which the few dozen positions are individually purchased.

Hopefully that answers the question as to whether our often-robust criticism of the ETF industry, or at least aspects of it, is categorical as opposed to just evaluative and pragmatic.

Our Gratitude For Indexation, Industrial Style

Thank goodness for the market-structure-distorting impact of ETFs. The ranks of company analysts have been decimated these past 20 years; those who didn’t leave the business shifted to be ETF and asset allocation analysts. Less competition for us.

The active rejection of smaller-cap companies, of companies that don’t fit standard business models, or which reduce their trading liquidity through share buy-backs, means that they are not being efficiently priced. Or maybe they really are; maybe they reflect exactly the liquidity risk discounts and the uncorrelated performance risk discounts that the ETFs as price-makers impose.

Advertisement

But since we don’t consider those to be risks, maybe the lunch is free.

Example: It shouldn’t be feasible to be able to buy one of the fastest growing Asian airports at a discount to book value and a single-digit cash earnings multiple when the typical publicly traded airport company—including a comparable-region airport company—trades at an EBITDA multiple of about 25x.

In this case, the airport company is a wholly owned subsidiary of another company that is in a different industry, and the parent has a market value of only several billion dollars. Making matters worse, about half of the parent company shares are held by, in turn, its own larger parent company, so the float-adjusted market cap is smaller still. And it is illiquid; one can only buy a relative handful of shares at a time, so it would be a very lengthy process for any institutional buyer to establish even a miniscule position. And impossible to exit rapidly unless they were willing to crater the stock price.

We like it, though. Airport companies trade at high valuations partly because they have usually have little direct competition, having long-term government-granted operating jurisdictions. They have significant investments in property and plant, but generate high operating margins, on the order of about 30%, as a mid-point. They are fairly stable businesses and have many ways to create more value through the real estate they are usually granted for development around the airport itself, such as for hotels, convention centers, and the like.

Advertisement

In any case, this one is uncommonly cheap. And that’s because in the ETF era the market does not care that a wrong-shaped micro-cap company without a proper industry designation has a subsidiary that is growing like a weed, is worth more than its parent company, and for which an IPO may well feature in the foreseeable future.

There are any number of other portfolio holdings that are of too high a quality and too deep a discount to make economic sense in a healthily functioning market. Unless we’re missing something and courting NFL risk (No Free Lunch risk), which seems to be a universal constant across all sectors of life. But if we’re not missing something, if the reason for the anomalously favorable pricing is either a separate or joint operation of EYC and ETFD factors, then we’ll earn a free lunch. Those acronyms are for:

The Equity Yield Curve, which operates when the timing of value realization of a security is just too far away or too indeterminate for the short-term relative-return-based asset-management class; and

The ETF Divide we’ve been discussing, which imposes discounts on companies for entirely non-economic or non-fundamental risk reasons.

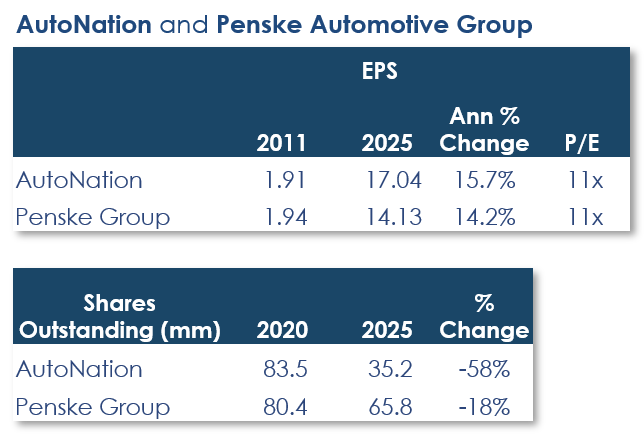

Other such holdings—for illustrative use—could be AutoNation (AN) and Penske Automotive Group (PAG).

For instance, why would a company that increased its per-share earnings since 2000 by 13.7% a year trade at 11x net income? Why would another company that increased its 15-year earnings per share by 14% trade at a P/E of 11x? In the cases of AutoNation and Penske, whose stock market values are $7 billion and $11 billion, AutoNation has repurchased 58% of its shares via free cash flow in the past 5 years, (which is entirely the wrong direction relative to the expanding trading liquidity needs of ETF organizers). Penske’s inside-ownership is over 50%, so the float-adjusted market cap is only half that $11 billion.

At over $11 billion, the two smallest-cap companies in the S&P 500 are larger than Penske and have weights of 0.1% and 0.0%. Moreover, another 20% of Penske’s shares is held by a Japanese company, Mitsui (MITSY), so Penske’s float, despite an $11 billion market value, is more like $3 billion. And Penske has bought back 18% of its shares in the past 5 years. Interestingly, if the company buys back 2.5% of its total shares each year, that’s more like 7.5% of its publicly traded shares.

Advertisement

Note: Last week, subsequent to the writing of this paragraph, Penske Automotive—the publicly traded company—received an offer from the privately held Penske Corporation and Mitsui & Co. to buy the remaining 17% of the shares they don’t yet own. This proposal will now go through the standard independent special committee review process.

IPOs and Us

Similar to the question about why we’ve changed our stance on ETFs, the second question is why we’ve changed our stance on IPOs. The answer is much the same; we haven’t.

It remains true that a decisive majority of IPO share prices finish lower than where they started. There are evergreen financial incentive and social finance reasons for this, most of them intuitively logical. While the precise IPO performance figures depend on the selection and calculation tradeoffs that shape the methodology of any given study, the results are mutually consistent. Using an academic-provenance study, for the 9,000-plus IPOs over the 46 years to 2021, three years after their IPO, 56% of those companies were lower than their IPO price. For people who bought shares at the end of the first day of trading, the figure is 60%. After five years, the figures are a bit worse.6

The confusion in the IPO question is one of language: the challenge of communicating non-unidimensional thoughts clearly. This goes right back to the opening remarks about how many questions can be answered satisfactorily in a brief-answer format. Still, let’s keep this one short.

Advertisement

If we participate in an IPO, the decision is definition-agnostic. It’s about the business and valuation analysis. Not that we can’t be wrong about any given company, but that’s the difference. The label or form is irrelevant; we’re particular about the substance. Most IPOs are decidedly unattractive; they’ve been engineered to be sold to the public.

Example: mentioned earlier was an IPO that might happen within the body of another company, and that the available data show that both the subsidiary and the parent are demonstrably and almost certainly unsustainably undervalued. This is the mirror image of the typical IPO risk/reward proposition. This particular IPO would be a value realization catalyst within a client portfolio.

An IPO in which many of our strategies recently participated was LandBridge Corp in July 2024, anchored by Horizon Kinetics. Our connection with LandBridge as a private company was through our long association with TPL and other adjacent property transactions in the Permian Basin. LandBridge management understood through our history that we both understood their business and would be long-term holders of their shares.

LandBridge embodies just the sort of rare hard assets, profitability, and business persistence that we seek. It now has over 300,000 acres of strategically assembled surface acres in the Delaware Basin of Texas. It is from that land position that its current and future revenues will emanate. Its core business for the time being is leasing its land for water transportation, treatment, and remediation purposes, which largely manifests in a royalty-like fee based on the volumes of water that are either piped across its acreage or stored in its subsurface pore space.

Advertisement

There is an unusual inherent and rather high level of passive growth and inflation-beneficiary element to LandBridge. The unique hydrogeology of the Delaware Basin, which is the remains of an ancient inland sea, means that as wells age or get deeper, greater volumes of brackish water come up the well with each barrel of oil. Presently, that averages about four barrels of water per barrel of oil. By 2030, the estimate is for a six-to-one ratio. The progression from four to six barrels amounts to about 9% annualized water volume increases, even without expansion of oil output by the Chevrons and ExxonMobils—which, in fact, is expanding—and absent any active growth efforts by LandBridge.

Moreover, the company’s water handling and storage contracts, which typically run for 10 years, contain inflation escalators. Based on typical inflation indexes like the CPI, one can already anticipate 12% or greater revenue growth, which requires no capital spending on Landbridge’s part. Then, as demand for pore space increases in future years, new contracts are likely to be priced higher than the current roughly $0.11 per barrel, which would add to the revenue growth rate.

Looking forward, LandBridge was the first company to introduce the concept of “powered land” as a strategy to facilitate the development of private power generation, transmission and ultimately large-scale data centers. LandBridge’s contiguous surface land has the latent potential to capture developments from the data center itself, related roads, power lines, wind and solar, carbon capture, and water, all of which generate recurring, high-margin “royalty-like” revenue streams. It’s important to note that because LandBridge acreage sits above a significant aquifer, the company can supply necessary water to the oil and gas drillers. Aquifer-based source water is priced in the $1/barrel range, though some of the gross revenue is shared with water handling companies that extract it from LandBridge’s acreage. Again, LandBridge takes a royalty-like interest in it.

So, yes, this was an IPO, but no, it was not of the typical IPO character. It was precisely the type of asset and business character we believe a portfolio should contain.

Advertisement

The few other IPOs we’ve participated in, lately, such as WaterBridge and White Hawk Minerals, also share the type of qualitative and valuation characteristics that suit our selection criteria.

Compounding and Us

This is what I wanted to get to. Because now, care of a Horizon Kinetics analyst, we have a better—certainly a different—way to explain the power and, most important, the TIME function of compounding. In the client relations part of the portfolio management biz, expectations and edification loom large: hardly a Quarterly Commentary or roundtable passes without a pressing question being a variation of “Is it time to sell?” or “Why haven’t you sold?” Usually asked when a particular stock is up or down a lot; often the same stock from year to year, and sometimes from decade to decade.

Our responses tend to be in word language form—analogies, metaphors, pictures. A fresh sample of which follows. But, on occasion, a bit of math can add clarity to otherwise mostly qualitative notions. In a recent research meeting, while we all were discussing how to again explain the periodic and (for us) anticipated decline in bitcoin relative to its long-term expected value progression, one of our analysts began wondering if the recent questions might be addressed with an “intuition pump,”7 so to speak. A single, simple mathematical function whose properties seems to describe the price of bitcoin—and, surprisingly, all sorts of other things, like the size of snowballs and the price of Amazon stock!—quite well but whose properties, through no fault of our own, are not intuitively obvious. A function that would explain why people have such difficulty truly “getting” the extraordinary benefits of WAITING for the cornucopian rewards of long-term compounding.

First, though, another language- and picture-based version.

Advertisement

The Repetitive Language Model (RLM) of Compounding

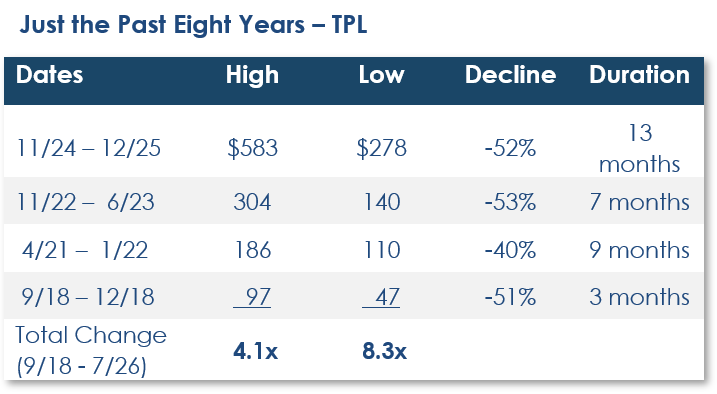

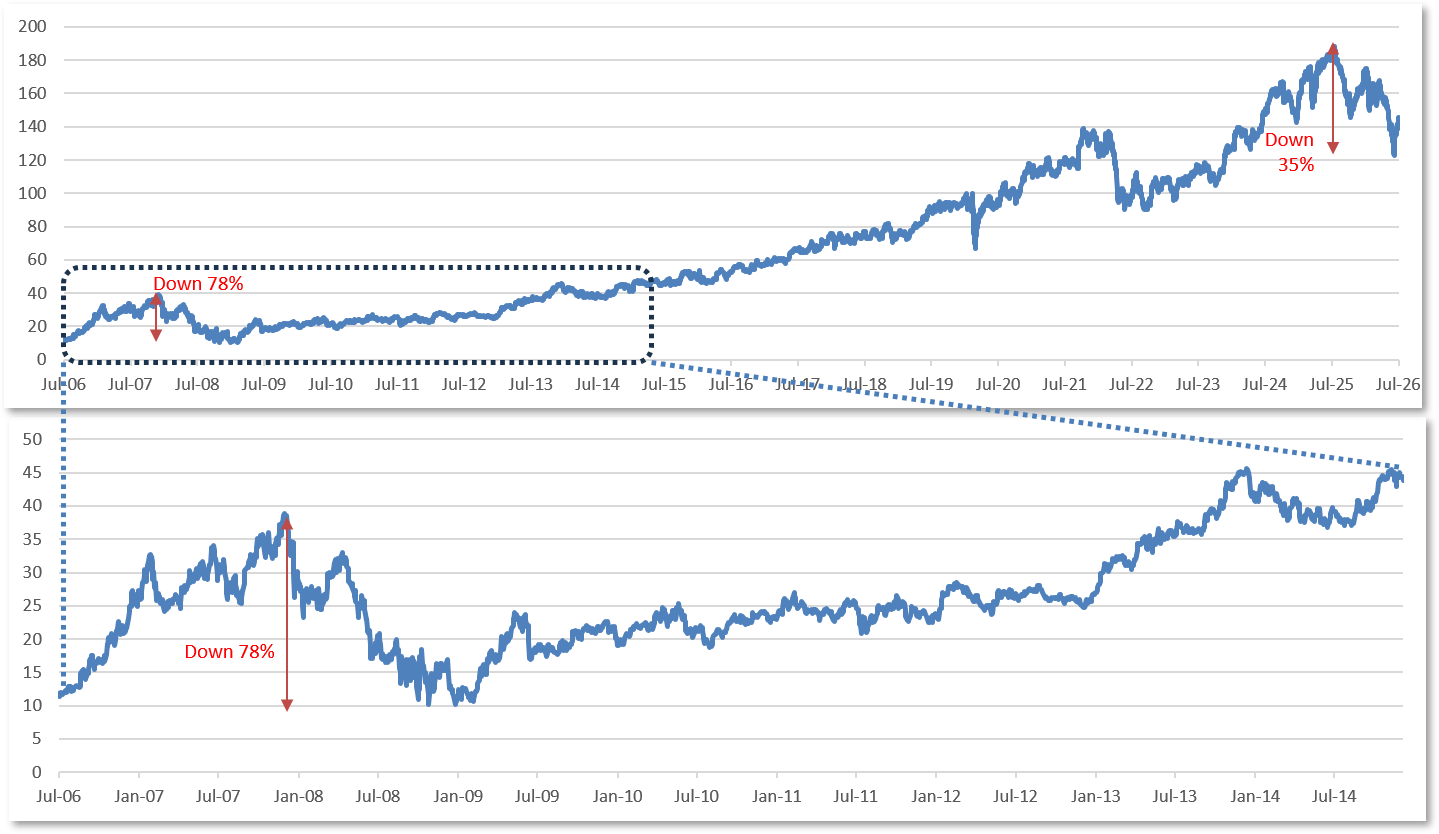

Near-term volatility looms large in the mind and jangles the nerves. Someone recently pressed me about “What is the matter with TPL?” He felt something was amiss because the share price was down 30% from its all-time high. I responded that TPL has been down many times during the three decades that he’s owned it. He responded—and he is a talented securities analyst and fund manager in his own right—“Yeah, but not for this long.” Of course, I had to look.

In just the past eight years, TPL has declined by between 40% and 53% on four separate occasions. Despite those dizzying drops, the shares today are up 4-fold from their high of eight years ago.

Intra-year price swings of that magnitude are statistically normal for almost any stock.

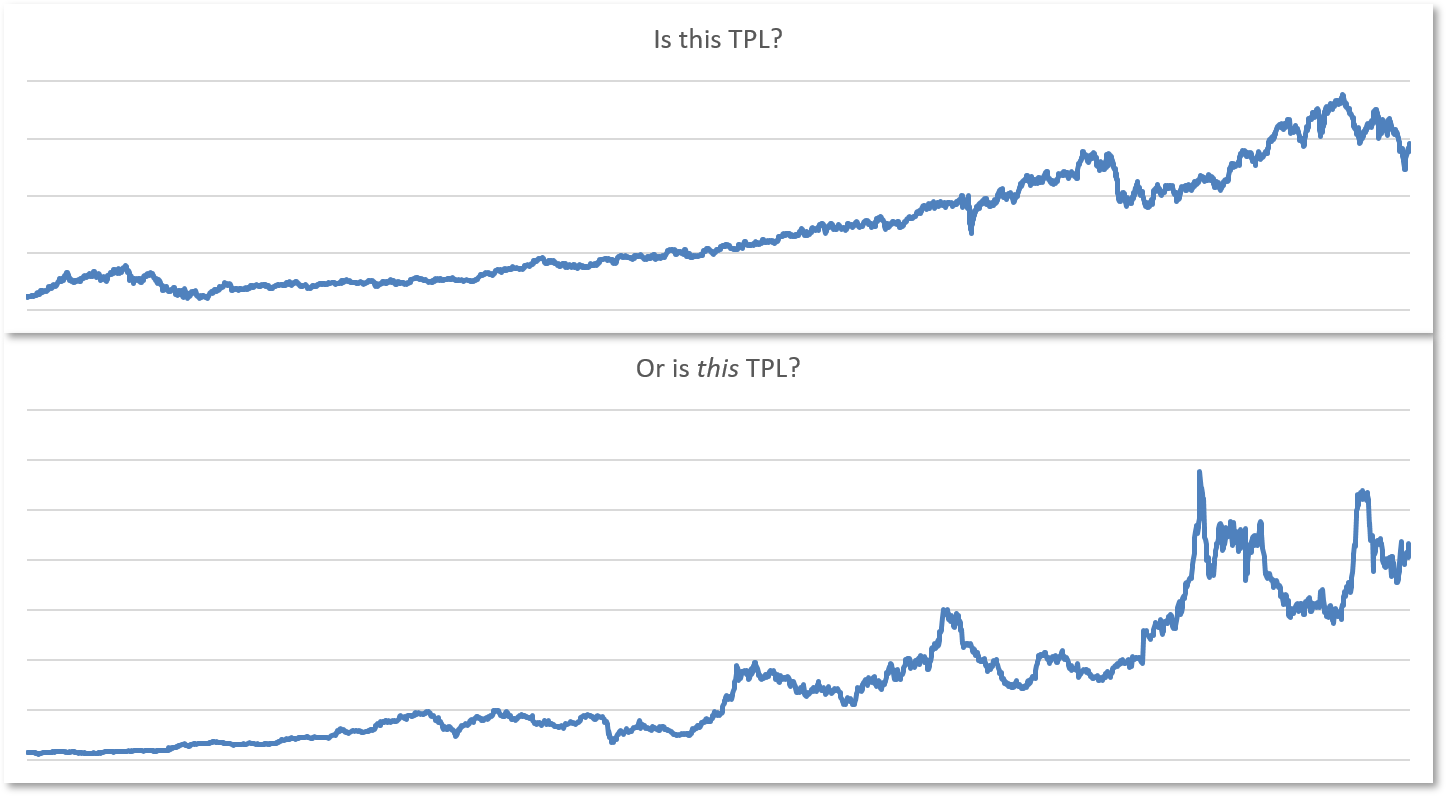

Fun exercise: Is this TPL, or is this TPL? Which is the pretender in these long-term charts?

Advertisement

Source: FactSet. TPL constitutes a large holding in many of the accounts and funds managed by HKAM and is also a substantial holding on behalf of the officers and employees of HKAM.

Before the answer, take note, below, of the left-hand portion of the top chart. Until the very obvious recent volatility, the early years show a relatively smooth upward rising curve. That’s a mirage, a misimpression wrought by time and compounding.

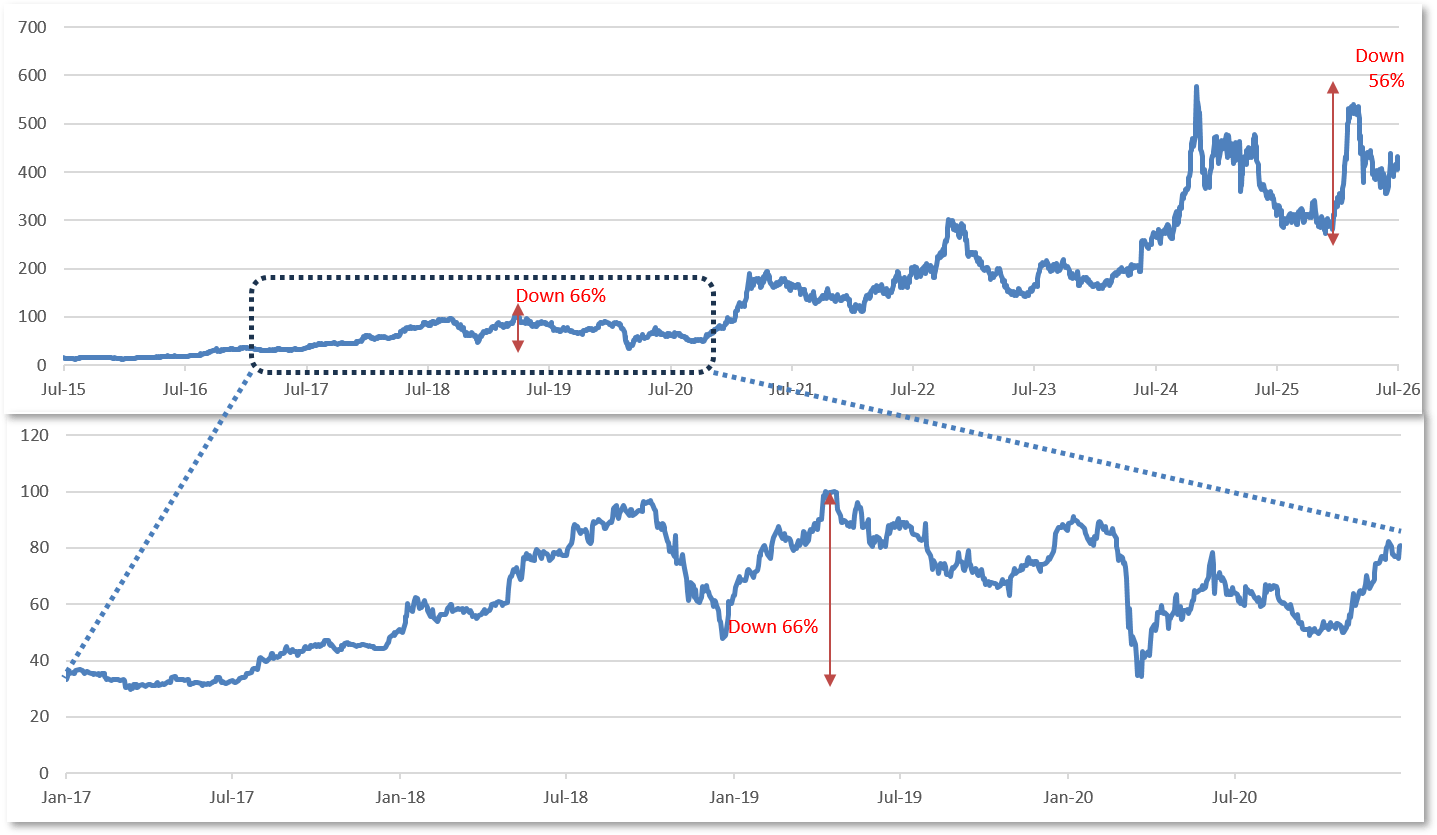

As to the other company, which might or might not be TPL, the similar two charts—the look-back view of volatility vs. the in-the-moment view—look like this. The mild-seeming look-back version was in fact a 66% price decline, also over about a year and change.

Source: Factset

Advertisement

Without the tools of business model and valuation analysis and an appreciation for the time element in the compounding class of investments, one has only stock price behavior as a reference point. But, if you can believe your lyin’ eyes and these charts, short term price behavior offers no predictive information, and using price as a decision-making tool is likely to lead to the wrong long-term outcomes.

These two companies have little in common with one another in the indexation or asset allocation world. They don’t share the same industry and they’re not in the same market cap class. What they do share is a fairly high degree of financial compounding over an extended time fame. The failure to easily recognize their decade-old volatility without the aid of these nifty charts is the pattern-recognition-failure of a brain evolved for the physical world of the veldt and the steppes.

It’s a good brain for spotting a charging lion in the first place (a sudden pattern change at the edge of the grasses) and for judging how fast the lion might catch up with you (because acceleration or compounding of speed stops after a few strides, so was never a real issue). Our brains have trouble with geometric—as opposed to arithmetic—functions and with extended time frames that are below our sensory or neuronal excitation threshold.

Over a long enough stretch of compounding, what was once an alarmingly high bout of volatility becomes attenuated to the point of being a blip on a chart. The companies are Intercontinental Exchange (ICE) and Texas Pacific Land Corp. (TPL).

Advertisement

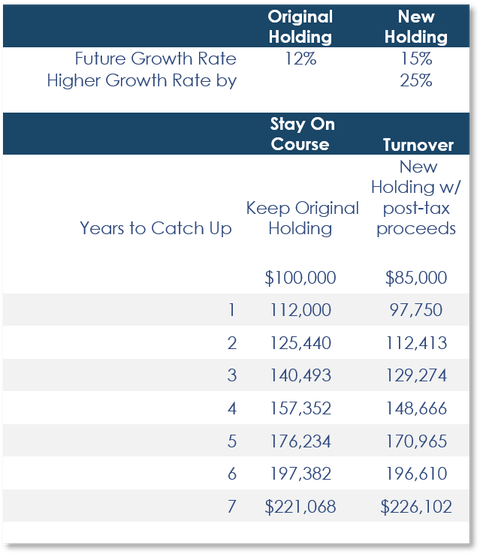

A not infrequent question: Why we don’t just sell at these periodic highs and buy something else? A vibrant and lengthy debate could be had on the efficacy of this proposition. This table illustrates one of the many risks and costs entailed when breaking a compounding chain in pursuit of such an active and presumably repeatable trading tactic over a long time frame.

In this instance, you sell a holding that has appreciated by many multiples above its cost in order to buy a new security that after much analysis and review is believed will grow at a rate 25% faster. You pay your gains taxes and reinvest your post-tax 85¢ on the dollar in the new company.

For Illustrative Purposes Only. Past performance is not indicative of future result.

Lo and behold, it turns out you’re right. The new company does grow 25% faster. You won’t find out if you’re right, though, until year seven. That’s how long until, being that skilled or prescient or lucky, you break even and start to do better. The more interesting question is whether you will have held the second stock long enough to find out. It takes a lot of time to develop excess value through growth. It’s a perpetual challenge. To quote two of our co-founders:

Advertisement

Peter Doyle recently said, “The hardest temptation to resist is to trade something good for something average.”

And about a decade ago, Murray Stahl wrote, “Although it might seem hard to believe, patient inactivity is hard, demanding, and exhausting work.”

The idea of a better way to explain this is what everything before this sentence has been leading up to.

A Math Model of Compounding – From a Water Glass to a Snowball, to Amazon and Bitcoin

The following is a four-sample series of familiar yet seemingly unrelated real-world phenomena. It was authored by the aforementioned analyst. The simulations run from the simple to the complex, yet with a startling sameness or universality about both the actual power of the almost cliché term “power of compounding,” and its confounding and sometimes misleading nature to those of us without the conceptual and quantitative tools to define them.

Advertisement

To hew to our 90-minute limit, this analyst’s eloquent and wry description of the inquiring train of thought that led him to this exercise is appended to this Commentary. It is commended for your reading.

Each of these exercises is about the different rates at which A) time passes and B) value compounds. Time progresses in a linear, arithmetic way: count the seconds or years; the rate of the ticking of the clock doesn’t change. Value compounds geometrically: slowly at first, then eventually at a rapidly rising rate. When the two are paired, our experience of them can be woefully distorted if we don’t know HOW that happens.

Waiter!!!

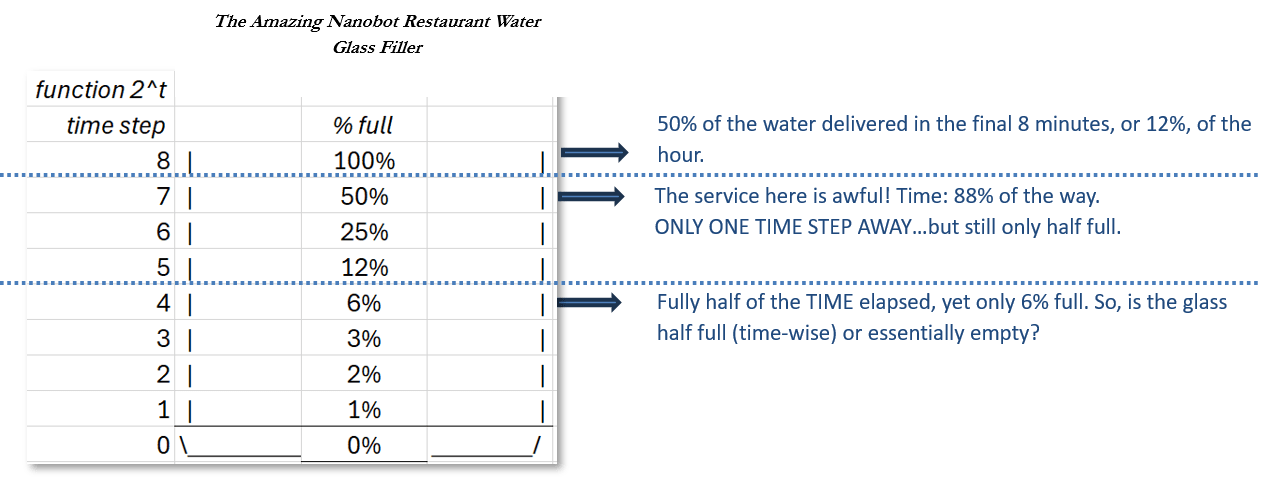

This exercise takes place sometime in the future when waiters no longer fill patrons’ water glasses. That task is done by carbon-based nanobots, molecule-sized and invisible, which precipitate water from the air. It’s all the rage in uber-fancy restaurants. At the bottom of each glass is a starter portion of nanobots-as-waiter, which fill the glass over the course of about an hour. To be precise, 64 minutes: their population ingeniously doubles every 8 minutes, so the process starts slowly while patrons are still looking about and sampling the varietal olives, and have yet to work up a thirst, and finishes after eight generations or time steps.

The evening at Table 2 goes like so: In time step 1, less than 1% of the glass has been filled. In time step 2, that doubles to nearly 2% filled, and then to 3%. The pace does pick up, doubling again with the next generation so the glass is 6% filled at time step 4. But half, 50%, of the hour has passed and the whole table walks out in a huff, because they see the glass as essentially empty. At least with respect to the amount of water, which is what they were focused on. But on a time basis, the glass is half full.

Advertisement

Table 5 is more patient. The couple there waits until time step 7 of 8. They’re 88% of the way there in terms of TIME, or 56 minutes, and ONLY ONE TIME STEP AWAY from the end. But their glasses are only 50% full! The service is awful! They take their leave, too. The remaining 50% of the water fills the glass in the final time step, the last 12% of the remaining time. If only they’d waited for the whole 64 minutes.

The value progression in this case was an exponential function, 2^t, or to the power of each time interval, which is not linear: Its rate of change, volume per unit of time…changes. Restaurant Tables 2 and 5 were watching the contents of the glass, like a stock price or an account statement balance. If they knew of the operative function, they would instead have been watching TIME. Linear models train us to watch time OR price, with the idea that one time step should equal one price step or vice versa. But compounding doesn’t work that way.

Snowball Fight

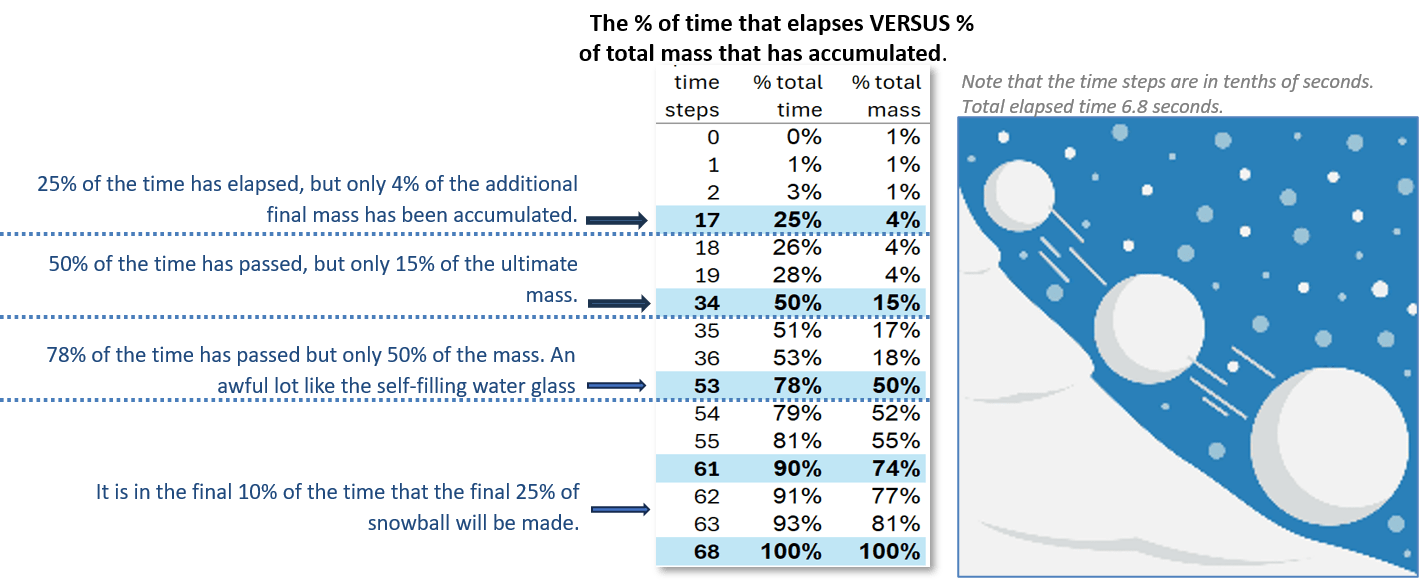

In this exercise a cartoon snowball—which is to say idealized for our purposes by ignoring friction and such—rolls downhill, picking up volume and mass with each rotation. It accelerates more slowly than, say, a stone dropped from a building, because the formula uses a 20-degree slope. Unlike the hour required for the water glass to fill in a futuristic restaurant, this snowball, which starts at a few pounds, takes only 6.8 seconds to reach its final almost 3-foot width and 200-plus pounds. Only 6.8 seconds, but long enough to reach 36 miles an hour (or for a stone to fall 50 stories).

The accompanying table divides each second into tenths, so there are 68 time steps. For visual ease, most of the intermediate time steps have been hidden. Of the many fascinating aspects of this series, the key thing to notice—which you probably couldn’t in just seven seconds watching a real snowball—is this:

Advertisement

For Illustrative Purposes Only. Most of the rows in this table have been hidden for ease of viewing, except for those immediately around the notable time and value stops.

Strangely similar to the water glass: at the halfway point in time,8 only 15% of the snowball’s ultimate mass has been accumulated.

At the 78% of time mark—or at 5.3 seconds—the snowball is only 50% of its final weight. Or, 50% of the weight “return” happens in the final 22% of the time horizon.

At the 90% time mark, the snowball is less than three-quarters of its ending mass. Rephrasing, 25% of the final weight accrues in the final 10% of the time, between 6.1 seconds and 6.8 seconds.

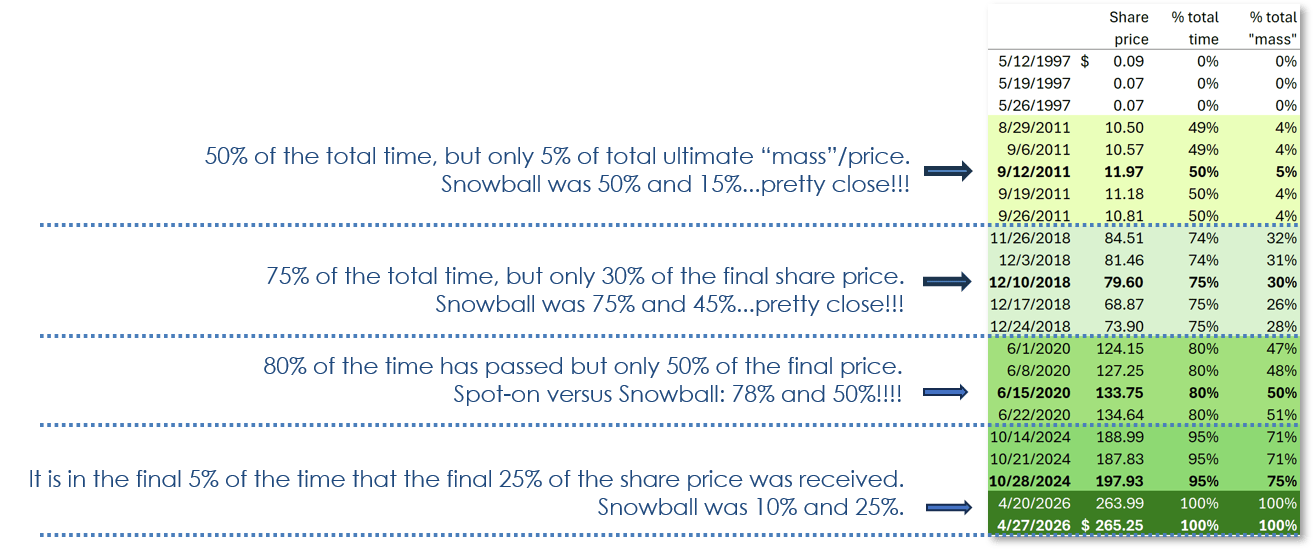

This next exercise is straight out of real life, comprised of strictly and obviously arms-length data, no simulation. These are the closing weekly share prices of Amazon.com from its very first week of trading in May 1997 through April 2026, all 1,512 prices. As before, most of the rows in this table have been hidden for ease of viewing, except for those immediately around the notable time and value stops.

For Illustrative Purposes Only. Past performance is not indicative of future results. Most of the rows in this table have been hidden for ease of viewing, except for those immediately around the notable time and value stops.

User note: Not to ignore the obvious, a stock price is highly variable in the short term even if it will follow a long-term expansion slope. At any of the highlighted time and price stops, temporarily lower prices will be found thereafter. Because this is not, after all, a simulation of a power function. just an observation of one.

Interesting, these tables, huh?

Advertisement

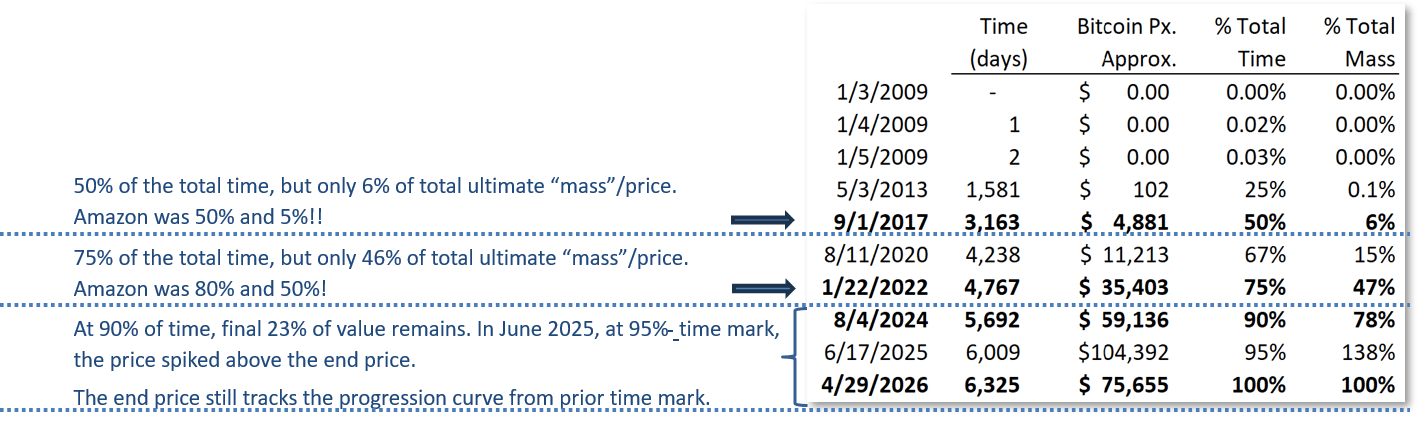

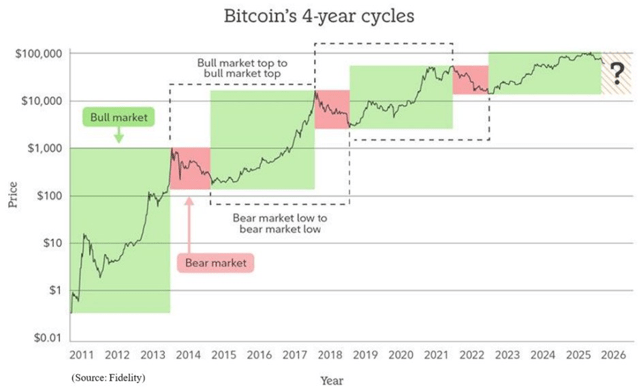

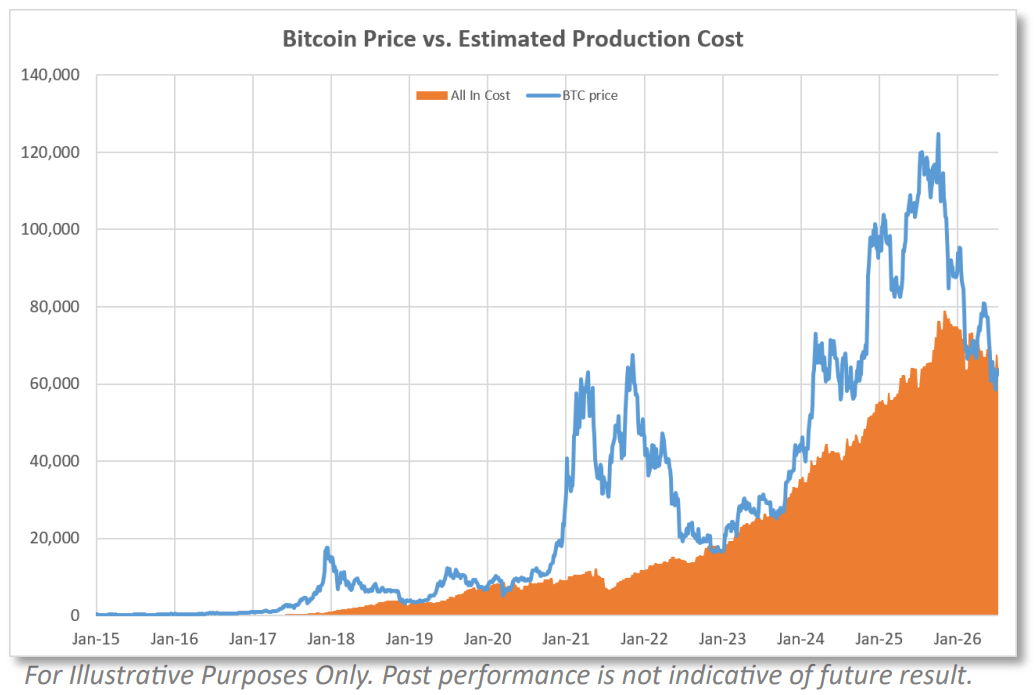

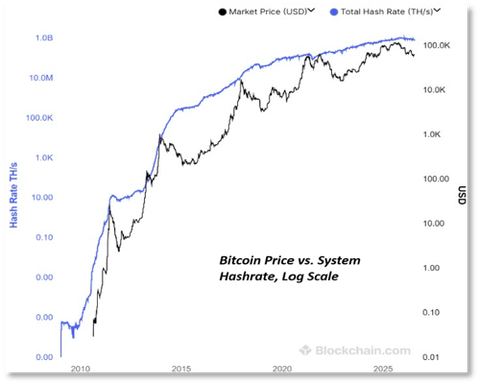

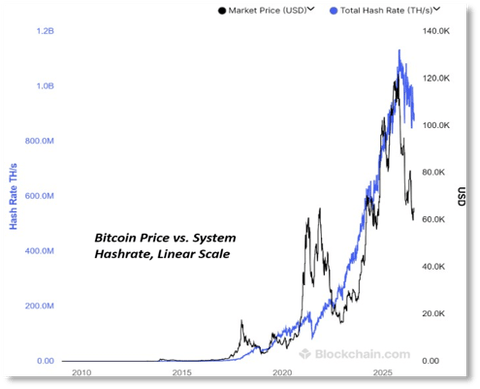

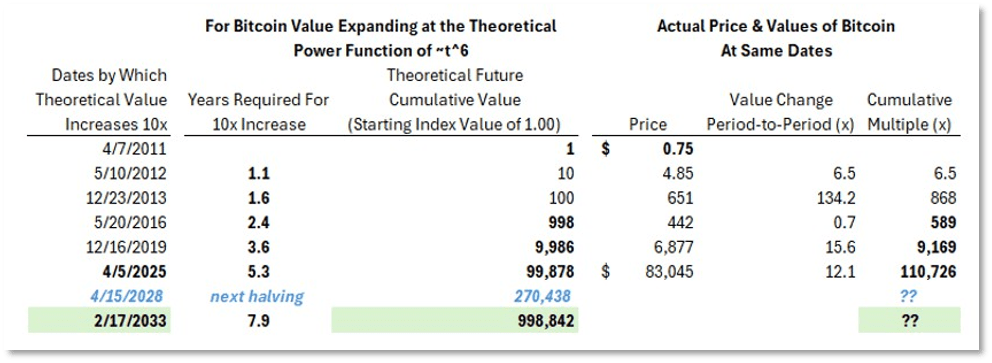

Bitcoin (BTC-USD) is a Snowball…but then, it was designed that way

This is as simple, in its way, as the Snowball and Amazon exercises, but can be far more intriguing and useful. Carry this exercise forward and it suggests a reasoned expectation of what the price of bitcoin might be at the next obvious time stop, the next halving in 2028—which will be discussed a little more fully later.

This bitcoin table uses daily prices since Jan 2009, so about 6,300 time stops. This time, we’ll eliminate all the rows except the handful of now familiar reference points. As was the case with Amazon, these are real-world prices, so they come with interim volatility around the long-term slope. Nevertheless, the results are closer to identical than one could reasonably expect. Particularly given that one is a mass market retailer-slash-IT cloud & AI data-center hyperscaler, while the other is still a point of debate as to whether it’s a commodity or security, a true persistent money, or a bubble-as-passion-project by crypto enthusiasts.

At 50% of the way from inception to the present, bitcoin’s price was only 6% of the recent price level; for Amazon it was 5%. At the 75% time mark, bitcoin’s price was 47% of the recent level; for Amazon the time and price figures were 80% and 50%. A remarkable consonance.

From this point forward, Bitcoin and Amazon part company.

Advertisement

First—and this applies to both of them—unlike the water glass or snowball, there isn’t a near-term limit to their value progression. They have a future beyond the number of rows in those spreadsheets. And for both bitcoin and Amazon, this geometric progression can be used to suggest what their prices might be in the future. That’s only theoretical, though.

In reality, Amazon’s capital spending for AI data centers is rising dramatically, it has just about transitioned from free-cash-flow positive to negative, and it’s begun to engage in large-scale borrowing. These are changes from its prior business profile and capital allocation practice. Will these changes conspire to degrade the rate of its actual future financial progress or its long-term valuation multiple (from the current-year P/E ratio of 36x)?

In bitcoin’s case, that slope of value progression is known and predictable, as defined by its programming: the cost of production is designed to double every four years by halving of the amount of bitcoin reward paid to the miners. Doubling every four years entails a 19% annualized increase in production cost, all else held equal. And the iron law of supply and demand dictates a price at least as high as production cost so long as people (any people, some people, the world) would like to own it or use it. Otherwise, the miners have to close up shop, and no more bitcoin or blockchain.

In another section, as soon as we answer another couple of client questions—about the precious metals royalty companies and the fear around recent new-trading-venue threats to the securities exchanges—we’ll test both what the formulaic expectation of the bitcoin price should be in two years at the next halving, and compare that with what the raw mining economics suggest.

Advertisement

Why Did We Reduce or Sell Precious Metals Royalty Companies?

Many have asked why we have chosen to reduce our positions in the precious metal royalty companies. Perhaps the best way to answer that is to revisit why we purchased them in the first place.

Some Then-and-Now History

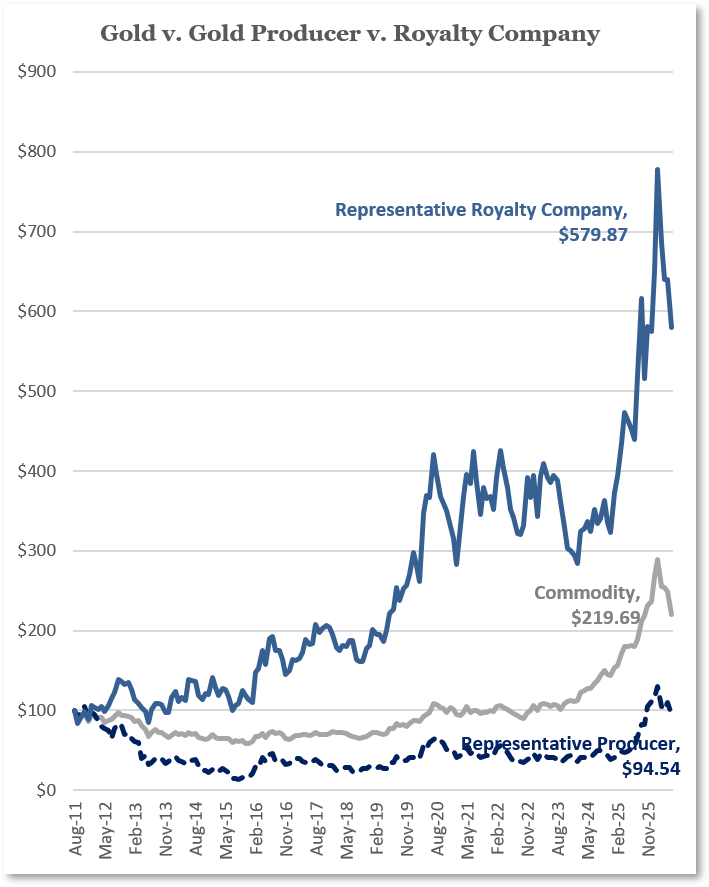

Source: FactSet, Normalized to a 100 base

In the years following the financial crisis, from year-end 2008 onward, global interest rates were set at effectively zero and many governments were running extreme deficit spending programs—a very accommodative environment for the price of gold. It rose approximately 100% to ~$1,900/oz at its 2011 peak, only to fall to less than ~$1,100/oz at the 2015 low.

The low in 2015 is notable, as this gold price was lower than the cash cost of production for a meaningful percentage of the sector. Many mines operated at a loss or were barely profitable, causing segments of the industry to become increasingly strapped for capital. This is not a sustainable dynamic for any commodity, as, obviously, if prices remain below the cost of production for prolonged periods, mines begin to close and new mine supply will contract. Conversely, if demand for a commodity persists or grows, prices will eventually need to increase to a level that allows producers to earn an adequate return on capital, thereby incentivizing investment in new mines.

Advertisement

This, perhaps counterintuitively, was the absolutely best period for precious metal royalty companies, because they could extract advantageous contractual terms on world-class mines whose owners would otherwise never need to seek royalty financing. The royalty companies were locking in fairly high double-digit financing rates for gold that would be produced over the ensuing 20 years or longer (more details of which below).

Investing in the royalty companies at this point in the gold cycle didn’t require a strong opinion about the price of gold. The superior business model inherent to the royalty companies—the advantageous discount rates at which these contracts were signed, the free exploration optionality on a mine’s surrounding land package, the insulation from operating expenses and balance sheet risks, the diversified portfolio of newly acquired royalty assets—would allow these companies to potentially generate very attractive returns even if gold prices didn’t rise. If gold prices happened to move higher, or if monetary and fiscal policies changed to become more supportive of gold prices, the potential returns would be that much better. In other words, this was a business valuation selection, not a gold price wager.

The basic thesis about future gold pricing did eventually prove correct—although, again, it was an unnecessary outcome—with gold rising to a high $5,400/oz earlier this year before retracing to the current ~$4,100/oz. However, these higher gold prices are now embedded as premiums in the current valuations of the royalty companies, much as the depressed gold prices a decade earlier were embedded as discounts in the royalty share prices.

All of this simply means the investment backdrop has changed markedly, and the extreme positive optionality that existed in 2015 is no longer present. This doesn’t mean that these are not attractive investments today, but they are objectively less attractive than 10 years ago (similar to most other financial assets).

Advertisement

It must ultimately be remembered that, for all the benefits embedded in the royalty business model, there are minor drawbacks. Firstly, while the royalty companies bear no operating or capital costs, they similarly have no discretion over mine operations. Secondarily, the royalty companies do not have pricing power with respect to the metal itself. Yes, they have negotiating leverage with a miner when outlining a new royalty or streaming contract, but their revenues are a function of the prevailing gold price. They are price takers for the ounces they earn from their royalty agreements.

Bookending this decade-long period, the gold price is now comfortably above the all-in-sustaining-cost of production for most global mines, not below it. This means that mines can continue to operate and grow even with lower gold prices and perhaps more importantly, these miners have reasonable access to capital, which is less advantageous to royalty financing providers. The royalty companies can no longer secure new royalty contracts that have the same earnings power at existing gold prices or the same degree of gold price optionality that they once did, which is a significant shift.

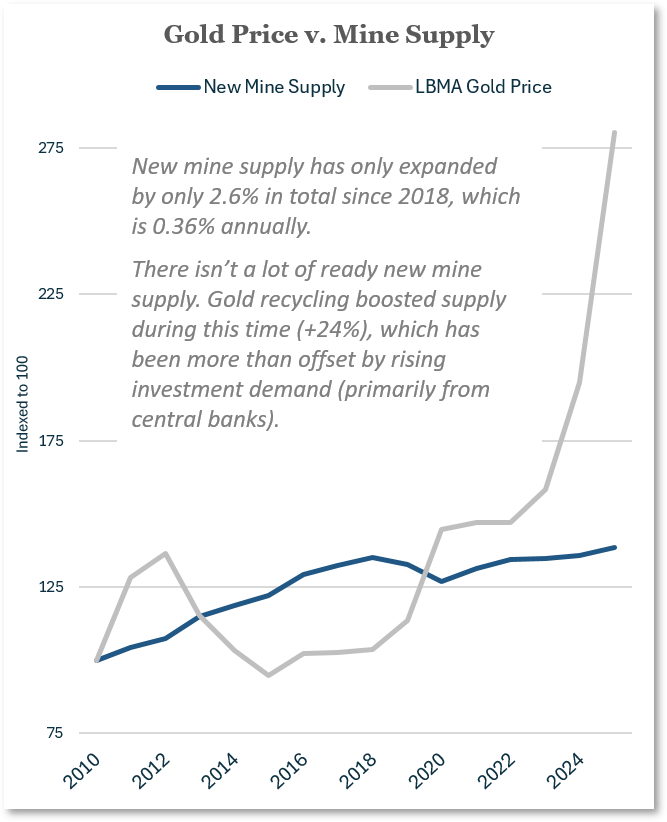

It should be noted that, while mine supply certainly contributes meaningfully to annual gold supply/ demand balances, new mine supply has only expanded by only 2.6% in total since 2018, which is 0.36% annually. There isn’t a lot of ready new mine supply. Gold recycling boosted supply during this time (+24%), which has been more than offset by rising investment demand (primarily from central banks). To the extent that these conditions continue, gold prices should have structural support, and higher gold prices will almost certainly lead to share price gains for the royalty companies. But again, we focus on business analysis and fundamental valuation, not gold price forecasts.

Valuations Have Meaning

If that is the general valuation risk case, a specific valuation and expected return case can also be made. Wheaton Precious Metals (WPM) and Franco-Nevada (FNV) are the leading precious metals royalties companies. They have achieved scale economies and an established track record, with key assets that consistently deliver the free optionality upside that royalty investors seek. Because of this, they trade at premium valuations, which gives them the cheapest cost of capital for new deals, thus creating a virtuous cycle. They have the highest returns on equity in the industry.

Advertisement

Likewise, their shares have the highest valuation multiples, roughly 2x NAV, using the consensus estimates of analysts. Understanding how those Net Asset Values are arrived at is instructive, because those NAVs—perhaps vaguely likened to an actively marked-to-market book value for an ordinary operating company—themselves incorporate elevated assumptions.

The assumed price of gold is a primary input into the calculation, which, today, typically starts around current prices and declines modestly over a period of years. The calculation fails to capture the significant value of what is essentially a perpetual option on gold.

Gold production is the other critical input, although the calculation generally only includes currently producing or imminently producing mines such future, non-producing royalties are valued at zero. The calculation fails to capture the exploration optionality on existing royalties or the growth potential from new deals. In this sense, royalty companies should trade at a premium to NAV in almost all environments—the critical question being how large a premium?

For Illustrative Purposes Only. Past performance is not indicative of future results. Source: Horizon Kinetics Research

Advertisement

These inputs create a set of cash flows, which analysts then discount to establish a present value for royalty payments received many years in the future. These discount rates are only in the 3% to 5% range (though the royalty companies themselves certainly negotiate significantly higher discount rates in their own royalty deals). The inverse of those consensus NAV figures would be equivalent to P/E ratios of 20x to 33x. That is not the best analogy.

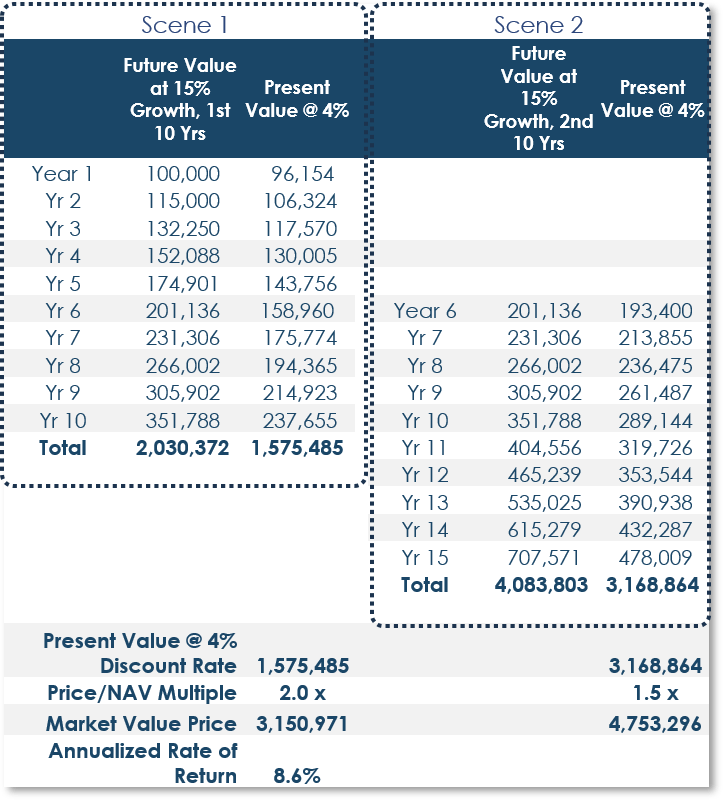

To illustrate the change in royalty company valuations, an annual income stream of $100,000 for 20 years—if discounted to a present value at a 15% rate—would amount to about $625,000. That is the equivalent of buying $2 million of future payments for about 30¢ on the dollar, and earning 15% annually on that investment. The equity investors for precious metal royalty companies, however, are now choosing to discount these cash flows at a 3% rate, which means the present value of those $2 million in future payments would be almost $1.5 million. Not a bargain by any means.

With the larger royalty companies now trading at 2x NAV, there is risk of valuation multiple compression. For example, what if, five years from today, these royalty companies were to decline to 1.5x NAV, which is still higher than some smaller but similarly profitable precious metals companies, but continue to earn their normalized returns based on their royalty economics? In other words, yes, the companies are doing everything they’re supposed to and are qualitatively wonderful. A valuation contraction within that time frame overwhelms the gradual accumulation of compounded growth.

For instance, say that a royalty company’s earnings were to expand, based upon its existing royalty portfolio, at a 15% annual rate and are anticipated to do so for 15 years. However, in five years, the shares, presently priced at 2x NAV, will trade at 1.5x NAV. The annualized return, all else held equal (e.g., excluding real-world complicating factors like the actual price of gold; how much cash or debt might be on the balance sheet; etc.), would be only 8.6%.

Advertisement

For those who like to look at the numbers that comprise that result, this table is a simplified version.

These few minutes of discussion are simply a description of the considerations that go into deciding whether one might or might not want to maintain a large commitment to an excellent business at what appears to be a sub-optimal valuation for a suitable long-term forward return. These companies can still provide very attractive exposure in certain portfolios, but it is not reasonable to assume that the historical returns can be sustained going forward.

Source: Factset, Price chart July 25, 2025-July 27, 2026.

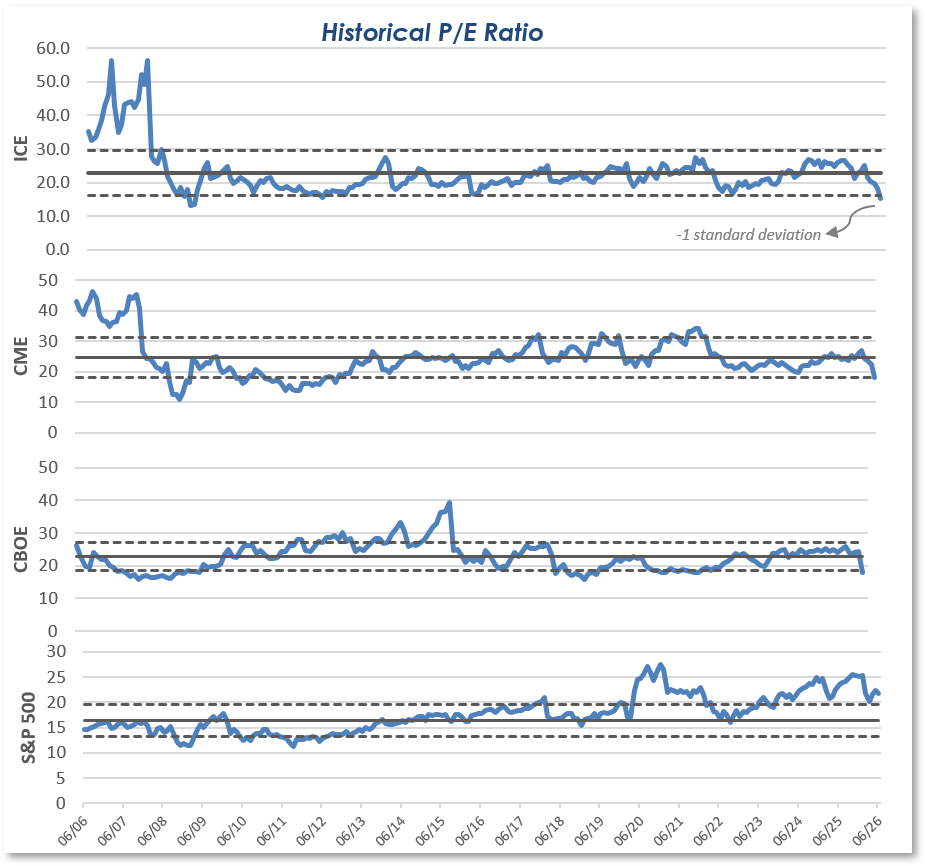

The Securities Exchanges: Perpetual Futures, Prediction Markets, “Stunning” Price Declines

How are the Exchanges Doing?

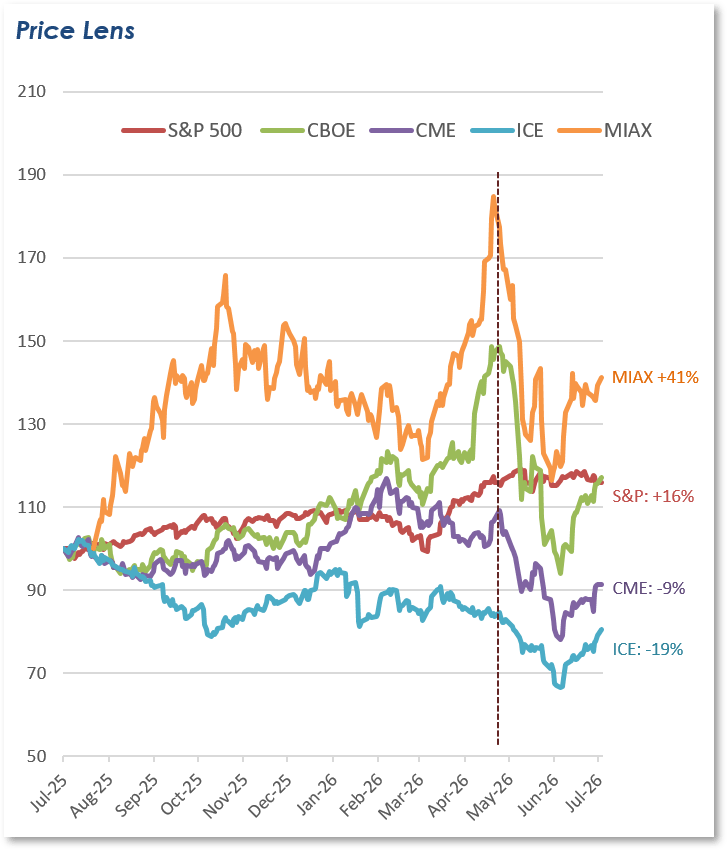

In the five weeks from May 15 through June 22, the shares of the major U.S. regulated securities exchanges behaved almost as one, declining between about 22% and 38%.

Advertisement

In the five weeks since June 22, they recovered on the order of about 20%. Two of them—MIAX and CBOE—are substantially higher than they were 12 months ago and more than the S&P 500. Two of them are substantially lower. As far as price volatility, all looks normal but for the lockstep decline that started on May 15.

The reference to the exchanges’ share prices, as opposed to the ordinary “the exchanges were down” phrasing is because the exchanges as businesses are doing quite well.

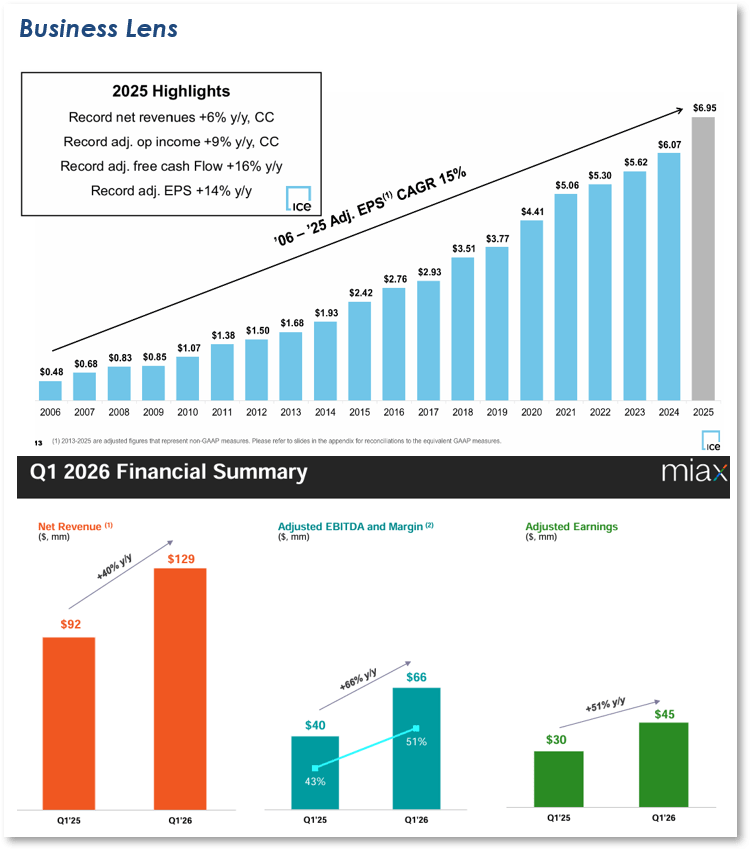

Intercontinental Exchange’s (ICE) first quarter revenues were much higher than in 2025, its operating margin was higher still, and per-share net income even higher. Quarterly earnings are not very indicative, though, since they are so variable.

But the same rising revenue and expanding operating margins relationship is apparent in the full-year 2025 results. The revenue expansion for the year is only 6%, but the end result—inclusive of a 33% after-tax net profit margin—is a double-digit per-share earnings growth rate. This reflects the low incremental cost for rising transaction volume and revenues for this type of business.

Advertisement

The year’s 14% increase in per-share earnings is essentially equal to the 20-year annualized increase of 15%.

MIAX, which hasn’t yet achieved full scale economies, reported 40% higher revenues in its March 2026 quarter, and free cash flow was more than 2x higher.

If these two companies are representative, as far as reported results to date, the exchanges seem to be robust and growing businesses.

The Day the Shares Went Down

The May 15 share price declines commenced on the day of a Bloomberg news story that ICE and CME Group were petitioning the Commodities Futures Trading Commission (CFTC) to require a decentralized exchange called Hyperliquid to register with the CFTC and bring it under U.S. regulation. Without more information, that seems like a big ask. Events leading up to and following that story share a regulatory and political dimension that might partially explain the market behavior around the securities exchange stocks.

Advertisement

Hyperliquid is only three years old. It had recently expanded from cryptocurrencies and began offering blockchain token-based contracts on oil prices. These are a novel type of derivatives contract called perpetual futures, or perpetuals in finance world lingo (and “perps” if you’re in the know). With the end-of-February commencement of the U.S-Iran conflict, oil had one of the largest one-month price increases on record.9 Trading in oil tokens on Hyperliquid rose from what was a marginal trading product to notional volumes in the billions of dollars for a single day.

A natural inference is that perpetuals could be a competitive threat to the regulated U.S. exchanges. This mid-May news about Hyperliquid did not occur in a vacuum. The ICE and CME actions were preceded by and followed by other news about the regulatory framework for commodities futures trading—which is largely what ICE and CME do.

Starting with a later event as the basis for describing some relevant earlier events, in mid-June, the CME filed a suit against the CFTC. It was triggered by the CFTC’s May 29 approval of an application by Kalshi, the event or prediction market firm—think YES-NO wagers on sports, economic or political events—to list and trade a bitcoin perpetual in the U.S. as a futures contract.

The CME asserted that the approval contravened various procedural and definitional rules, including that the current Chair of the CFTC is the only member of what is supposed to be a five-person commission, and especially around the definition of swaps. The CME contends that a so-called perpetual future is not an actual futures contract, but a form of swap. Swaps were the kryptonite in the 2008 global financial crisis—which is why these perpetuals could not be traded in the U.S. before that May 29th approval.

Advertisement

By Commodity Exchange Act definition, futures contracts require an expiration date and a delivery date for the underlying asset, whereas perpetuals have neither. This is an exceedingly limited synopsis and is certainly not an analysis or evaluation, since it is in the regulatory realm, which is not ours. The purpose is simply to highlight a political or regulatory risk dimension that might have informed market reaction around the securities exchanges.

Irrespective of the actual regulatory determination in this case, there are very important economic differences between futures and swaps. A trading-product risk dimension question would be whether the perpetuals and prediction markets are a threat to the incumbent regulated exchanges.

As to event or prediction contracts, nothing precludes the incumbent regulated exchanges from offering the same products. In fact, ICE owns 17% of Polymarket, which it purchased in late 2025 for $1 billion. It added another $600 million to its investment this March. ICE is interested in the crowd-sourced information aspect of prediction markets. Not the sports wagering, but the pricing and volume data around economic indicators and events. Such data, if organized into useful information that can be sold to the professional class of traders, could be lucrative. Information and connectivity services are ICE’s second largest revenue source after its core derivatives trading business.

Nor are token- or blockchain-based products and services the sole province of the Kalshis and Polymarkets. For the regulated exchanges, blockchain technology can enable all sorts of administrative and back-office efficiencies; same-day/same-moment settlement of trades; which in turn can enable greater collateral reserve efficiencies and transaction velocity for traders; 24-hour/7-day trading; and, via tokenization, the securitization of almost any physical or intangible asset, whether real estate, intellectual property like music or crowdsourced odds on economic events. That’s a technological development that can immensely increase the universe of tradable and hedge-worthy assets.

Advertisement

In that respect, the existence of crypto-blockchain-based companies like Kalshi or Polymarket aren’t a threat to incumbent exchanges so much as an indicator of extraordinary next-generation, next-decade expansion possibilities for exchanges. Which is why we established the Blockchain Development ETF.

There are already tokenization initiatives at almost all the U.S. regulated exchanges.

The CME has already introduced, earlier this year, 24/7 cryptocurrency futures and options.

It is also just launched 24/7 mini Gold futures and plans to launch 24/7 Oil futures by the end of August.

And also single-stock futures, which are another means for retail investors to use margin or leverage—using less capital to control a larger position.

And prediction markets partnerships with FanDuel and FutureSports

CBOE submitted a proposal to the SEC to launch near 24/5 U.S. equity trading by the end of the year.

This March, the SEC approved a Nasdaq proposal to allow certain stocks to trade and settle in token form through the DTCC, the dominant U.S. clearing and settlement entity.

ICE is working with a crypto exchange in which it has acquired a small stake to launch oil-linked perpetual futures (more of which below) to be marketed to retail traders. Though these will not, by the book, be eligible for trading in the U.S.

The NYSE division of ICE is exploring a blockchain-based settlement capability that would allow 24/7 trading on the New York Stock Exchange.

A meaningful difference is that these initiatives are coordinated with institutional brokerage firms and regulators on trading, collateral, and settlement protocols. It is important that each tokenized equity has interoperability and the same shareholder rights and governance. One should evaluate this complex interrelated construct of business, legal, regulatory and institutional market participants that is in the process of being developed with what independent unregulated platforms offer.

Perpetuals require some explanation before an informed judgment can be made about their threat to the regulated securities exchanges. To date, their sole allure seems to be with retail investors, whereas 85% to 90% of ICE’s business, for instance, is with institutions. The best way to understand why is to compare perpetuals with actual futures contracts, which to a retail investor are prohibitively cumbersome at every step of the process.

First, the primary use and need for a futures contract is to hedge a legitimate business exposure. A made-up for-instance: a South Korean buyer of a tanker’s worth of oil from the U.S., perhaps a distributor who will simply sell the oil to its local customers, could be a temporary owner of 500,000 barrels of oil. The problem is that the transit time can be as long as three weeks. That’s $40 million of oil subject to daily price risk. This distributor needs the price paid in the U.S. to be the same as when it arrives in South Korea, otherwise the intended profit margin of the transaction could easily become a loss. Distributors don’t have much of a profit margin anyway. If the departure date for that trip happened to be this past May 31, the buyer’s selling price by the end of the trip could have been 20% lower.

Advertisement

That ruinous possibility needs to be hedged, and it is done by selling an equivalent amount of oil at the then-current price for delivery in three weeks. The loss on the purchase would be offset by the gain on the futures contract. This contract can’t work without a specific date upon which both parties commit to deliver and take receipt of that oil. It can’t work unless the contract is executed on a regulated exchange that enforces that both parties constantly maintain sufficient collateral to perform.