Crypto World

Altcoins and Bitcoin Crash After Donald Trump Pledged to Save Crypto

Former SEC chair Gary Gensler and the “anti-crypto army” nearly destroyed the American crypto industry by driving Bitcoin, crypto perpetuals, and innovation offshore, but “Trump saved it,” the president said on Truth Social on Wednesday.

“America is now the crypto capital of the world, and builders and entrepreneurs are coming back to the United States where they belong,” he added.

“Under my leadership, we will codify a future-proof digital asset market structure that cannot be undone by the crypto haters. The new frontier of finance is being built in America, and Trump will never let crypto down!”

In a separate post, he said, “where we are currently the crypto capital of the world, other countries are trying diligently to replace us in that capacity, but we won’t let that happen. It is a major industry, and we must protect it.”

BTC at Six-week Low, ETH Under $2K

Under normal market conditions, such comments from a world leader would have caused markets to bounce.

But this is a brutal bear market, and they did the opposite, tanking almost 3% with more than $80 billion wiped out.

Over the past 24 hours, around 165,000 traders were liquidated, with total liquidations coming in at $928 million, 93% of which were long positions, according to Coinglass.

Bitcoin tanked 3.2%, falling to $72,800, its lowest level since mid-April. The asset has now lost 8% over the past fortnight and is heading back into the $60,000 zone.

BREAKING: Bitcoin dumped -$1600 and dropped below $73,000 in the last 60 MINUTES.

Over $480 MILLION longs in were liquidated. pic.twitter.com/cfZajGkauN

— Bull Theory (@BullTheoryio) May 28, 2026

Meanwhile, Ethereum dumped below the psychological $2,000 level, falling more than 4.4% to $1,975, its lowest level since the end of March. The altcoins were a sea of red, and the crypto exodus continued as the bear market deepened.

“Retail has erupted with ‘buy the dip’ calls toward ETH as a result of this drop below a key psychological support level,” reported Santiment.

“This typically means the price may have a bit further to fall, due to the crowd (which usually gets calls wrong) being too optimistic.”

US Strikes on Iran Resume

Markets were further pressured when the US launched a fresh wave of military strikes on Iran late on Wednesday.

Strikes targeted an Iranian military site while the US shot down four Iranian drones, which posed a threat around the Strait of Hormuz, according to Reuters.

“These actions were measured, purely defensive, and intended to maintain the ceasefire,” an official told the outlet. Meanwhile, Iran retaliated by attacking a US base in Kuwait.

The post Altcoins and Bitcoin Crash After Donald Trump Pledged to Save Crypto appeared first on CryptoPotato.

The rough market conditions and the global uncertainty have failed to faze the Tom Lee-chaired Ethereum buying machine, as Bitmine has spent approximately $90 million to acquire 52,203 ETH over the past week.

Lee remains highly bullish on the industry, despite the repeated rejections at key price levels and the fact that Bitmine is still billions of dollars in the red on its ETH position.

Closer to 5%

With the latest acquisition, Bitmine’s total ETH holdings have grown to 4.7% of the asset’s entire supply. Thus, the company is 94% of the way toward its 5% goal within less than a year since it began its Ethereum acquisition spree. It remains at the forefront of ETH accumulation.

The press release from this week informed that the firm’s total holdings consist of $10.7 billion across crypto assets, cash, marketable securities, and strategic investments in Eightco and Beast Industries.

“The best years for crypto remain ahead, in our view. Tokenization and the rapid progress in AI are expected to drive exponential demand growth for blockchain and decentralized crypto,” said Lee, Chairman of Bitmine.

He doubled down on his previous assertion that the current market environment, albeit quite sluggish and bearish at times, is in the early stages of “crypto spring.”

Staking Going Well

Although Bitmine continues to be deep in the red on its entire ETH position, it has managed to increase its annualized revenues due to staking. As of yesterday, the firm has staked 4,718,677 ETH (valued at over $8.2 billion at today’s prices), which has increased its annualized staking revenue to a projected $223 million.

“Bitmine has staked more ETH than other entities in the world. At scale (when Bitmine’s ETH is fully staked by MAVAN and its staking partners), the projected ETH staking reward is $268 million on an annualized basis (using 2.73% 7-day BMNR yield),” added Lee.

Aside from being the undisputed leader in Ethereum corporate holdings, Bitmine is the second-largest crypto accumulator after Michael Saylor’s Strategy. The latter announced another bitcoin acquisition today, albeit a more modest one for just 520 BTC.

The post Bitmine Buys 52K ETH as Tom Lee Believes the Best Years for Crypto Are Still Ahead appeared first on CryptoPotato.

A contributor to Goldfinch, a crypto loan program for Africa, claims tens of millions of dollars worth of loans have defaulted, in addition to over $300 million in market capitalization losses from the project’s peak.

Goldfinch was supposed to be crypto’s gift to Africa’s unbanked, however, its proprietary token, GFI, is down 99.8% from its high.

Backed by Andreessen Horowitz (a16z), the so-called decentralized lending protocol was supposed to bring financial inclusion to emerging markets. Instead, it simply funneled money to borrowers who largely stopped paying it back.

“These idiots mismanaged over $50 million of our money,” one Goldfinch depositor wrote on June 19. “Out of eight borrowers — two are in default and six in restructuring. Basically money is gone.”

GFI, the protocol’s token, was trading at its all-time high of $32.94 on January 11, 2022. It now trades 99.8% lower, below $0.07.

The project’s market capitalization as recently as April 2024 exceeded $390 million. It’s less than $6 million today.

Do-gooders pitch crypto for Africa

Goldfinch launched in 2021 with a mission statement built for a TED talk. It would expand access to capital for ostensibly creditworthy businesses that the developed world’s banks refused to touch.

Co-founders Mike Sall and Blake West, both formerly of Coinbase, leaned hard on the language of financial inclusion.

Borrowers spanned 18 countries, from a Kenyan motorcycle taxi company to a paycheck advance company in Nigeria.

Even Impact Water for schoolchildren was a recipient. Who could object?

Unfortunately, disappearing money, not clean water for kids, is the main story of Goldfinch.

Read more: Central African Republic’s -95% memecoin crash is a repeat performance

VCs support Goldfinch, get token allocations

Crypto-promoting VC giant a16z led Goldfinch’s $25 million round in January 2022. Coinbase Ventures, SV Angel, BlockTower, and hedge fund manager Bill Ackman also backed the project.

Unlike almost every other impact organization, Goldfinch minted a token, GFI, which had liquidity for selling to retail believers.

A16z praised Goldfinch’s $38 million in loans and pointed to “a huge global need for access to capital.” By mid-2022, Goldfinch had deployed over $100 million in active loans to over 200,000 borrowers.

One pool captured the pitch in miniature. The Cauris Fund marketed African fintech exposure, where Goldfinch’s capital would supposedly fund fintechs across the continent to expand financial inclusion for tens of millions of disenfranchised borrowers.

Since that pitch, the price of GFI is down 98%.

What actually happened to the money

Underwriting, not crypto, is almost always the reason a loan book goes bad. Underwriters, not blockchain technologies, vet offline information and qualify creditworthy borrowers who can actually afford to repay.

In October 2021, Goldfinch lent $5 million to Tugende Kenya, a motorcycle taxi financier. Goldfinch then discovered the borrower had quietly funneled $1.9 million to its struggling Ugandan parent, in breach of the loan terms.

Goldfinch’s loan facility was written down before a restructuring eventually clawed part of it back to recoup some of the loss.

Another $20 million facility for Stratos left roughly $7 million impaired.

Soon, Singapore-based borrower Lend East repaid only $4.25 million of Goldfinch’s $10.15 million loan in April 2024. Lend East defaulted on the rest.

As default rates rose in Africa and elsewhere, Goldfinch’s cumulative losses rose past $18 million. As optimism about its underwriting turned to pessimism, GFI lost four-fifths of its value from 2022-2024.

As write-downs continued, depositors withdrew collateral from Goldfinch’s liquidity pools. A crypto initiative to bank the unbanked instead funded another emerging-market disappointment.

As morale continued to degrade, Goldfinch shifted away from emerging markets toward institutional credit funds like Ares and Apollo.

Goldfinch quietly dropped disenfranchised borrowers in Africa and clean water for school children from its marketing materials.

Crypto’s long record of failures in Africa

Goldfinch joins a crowded graveyard of crypto projects that promised to transform Africa.

Akon’s $6 billion blockchain metropolis ran on his own Akoin token, branded “One Africa. One Koin.” Senegal’s government formally scrapped it in 2025 for a conventional tourism hub after the coin declined 99%.

Cardano fared little better. Charles Hoskinson’s organization pledged to lift 5 million Ethiopian students onto blockchain technologies. Years later, however, the pilot had registered only tens of thousands even at its peak.

Elsewhere, Central African Republic President Faustin-Archange Touadéra launched a memecoin which is down 99.5% since debut.

South Africa-based Africrypt collapsed in 2021 after its founders disappeared and investors alleged garden variety fraud.

Mirror Trading International, another South African crypto project, collapsed in 2020 after investors realized it was a Ponzi scheme.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Earlier this month, Bitmine raised roughly $274 million through the sale of 3.5 million shares of 9.50% Series A Perpetual Preferred Stock. The preferred shares, which trade on the New York Stock Exchange under the ticker BMNP, pay weekly cash dividends.

Lee has argued that the company’s staking operation provides recurring cash flow to support those obligations. Bitmine currently has 4.72 million ETH staked — more than 83% of its holdings.

The company projects annualized staking revenue of roughly $223 million, with potential staking rewards reaching $268 million annually through its MAVAN staking platform.

The firm announced another round of scheduled dividend payments extending through August, paying $0.1847 per shares.

Crypto spring

Lee reiterated his view that the crypto market is in the early stages of a recovery from the downturn that began with the October 2025 liquidation shock.

At Consensus Miami last month, he argued the bear market would be “definitely” over if bitcoin closed May above $76,000. Instead, BTC finished the month below $74,000 before briefly falling under $60,000 in early June.

Still, Lee said the recent pullback has not changed his broader outlook.

“We believe we are in the early stages of crypto spring,” he said.

Lee also reaffirmed his long-term bullish stance on Ethereum, arguing that growing demand from tokenization and artificial intelligence applications will drive adoption of the network in the years ahead.

Mining economics have deteriorated in 2026, the analysts noted, with bitcoin trading below its estimated production cost for five consecutive months. Citing CoinShares’ first-quarter mining report, JPMorgan said roughly 20% of miners are currently estimated to be unprofitable.

Financial pressure has prompted miners to sell more bitcoin holdings. Publicly traded mining companies liquidated more than 32,000 BTC in the first quarter, exceeding their combined sales for all of 2025, according to data cited by the report.

As a result, even relatively small price moves are increasingly affecting network activity. When bitcoin falls below production costs, higher-cost operators tend to shut down equipment, causing hashrate to decline and mining difficulty to adjust lower. The bank pointed to the second week of June, when mining difficulty dropped 10%, the second decline of that magnitude this year.

Looking ahead, the analysts expect heightened sensitivity in hashrate and mining difficulty to persist as long as bitcoin remains below its estimated production cost, which the bank currently puts at about $78,000. The world’s laregst cryptocurrency was trading around $64,700 at publication time.

Bitcoin miners are increasingly turning to artificial intelligence and high-performance computing (HPC) to diversify revenue as mining margins come under pressure.

The appeal is straightforward: AI hosting contracts can provide stable, multi-year revenue streams and higher margins than the more volatile economics of bitcoin mining, which have been squeezed by rising network competition and the 2024 halving.

Michael Saylor and his embattled Strategy (MSTR) sold more common stock last week, using the proceeds to add a relatively small amount of bitcoin and $300 million in cash to its balance sheet.

The company sold about 2.7 million shares of MSTR, according to a Monday morning filing, raising $335.5 million. About $35 million of that was used to acquire 520 bitcoin at an average price of $67,068 each. The other $300 million was added to cash already on the balance sheet, bringing reserves to $1.4 billion.

The latest acquisition brings Strategy’s total bitcoin holdings to 847,363 BTC, acquired at a total cost of roughly $64.01 billion, or an average purchase price of $75.651 per coin.

The Bank of England has scrapped its proposed holding caps for UK stablecoins, replacing them with a temporary £40 billion ($52.9 billion) limit on how much of any single systemic coin can be issued.

The change arrived Monday with a draft Code of Practice. It eases a rule that worried issuers. Yet it leaves Britain capping issuance of its own currency stablecoin, something neither the US nor the EU does.

From Per-User Caps to a Single Ceiling

In November 2025, the central bank proposed limiting individuals to £20,000 and businesses to £10 million per coin. Issuers called the plan costly and hard to enforce.

The reversal followed pressure at home. In June, the House of Lords Financial Services Regulation Committee urged the Bank to reconsider the limits. It warned they diverged from global norms and had alarmed crypto founders.

The Bank has now swapped those proposed holding limits for one £40 billion ceiling per coin. It says the cap shields bank lending while letting households and firms transact freely.

Why UK Stablecoin Rules Stand Alone

The contrast abroad is sharp. The US GENIUS Act, signed in July 2025, demands full cash and Treasury reserves but caps no issuance.

Europe’s MiCA stablecoin rules cap only foreign-currency coins used heavily for payments, a brake meant to defend the euro. They place no ceiling on euro stablecoins themselves.

That leaves the UK alone in capping issuance of a coin in its own currency. It is fencing a market that barely exists in sterling.

About 99% of stablecoins in circulation are dollar-denominated, the ECB reported in November.

A ceiling on supply restrains the issuer, not the user. Even that softer form of stablecoin holding caps has no parallel among big economies.

The Bigger Test is Tokenization

Issuers must back coins with 70% short-term UK government debt and 30% in deposits at the central bank. They cannot pay interest, though payment-linked rewards stay allowed.

That backing rule reaches into the gilt market. The Treasury and the Debt Management Office have flagged sterling stablecoins as possible structural demand for Treasury bills. Both plan new short-dated issuance to meet it.

Coins used mainly for trading, such as Tether (USDT) and USD Coin (USDC), stay under the Financial Conduct Authority. Redemptions must clear within 24 hours of a complete request.

The unresolved question is whether these coins can settle wholesale market trades. That answer will shape the country’s tokenization plans, and the Bank says the work continues.

“This is a major milestone in delivering greater choice and innovation in UK payments… This is truly a world leading regime,” Sarah Breeden, the Bank’s Deputy Governor for Financial Stability, said the regime builds trust for a new form of money.

Follow us on X to get the latest news as it happens

Feedback on the draft closes 22 September. The Bank aims to finalize the code by the end of 2026. That keeps the UK’s 2026 stablecoin timeline on track for the first issuers in 2027.

The supply cap lasting that long may decide if sterling stablecoins scale at home or grow elsewhere.

The post Bank of England Drops Stablecoin Holding Caps but Keeps $53 Billion Issuance Limit appeared first on BeInCrypto.

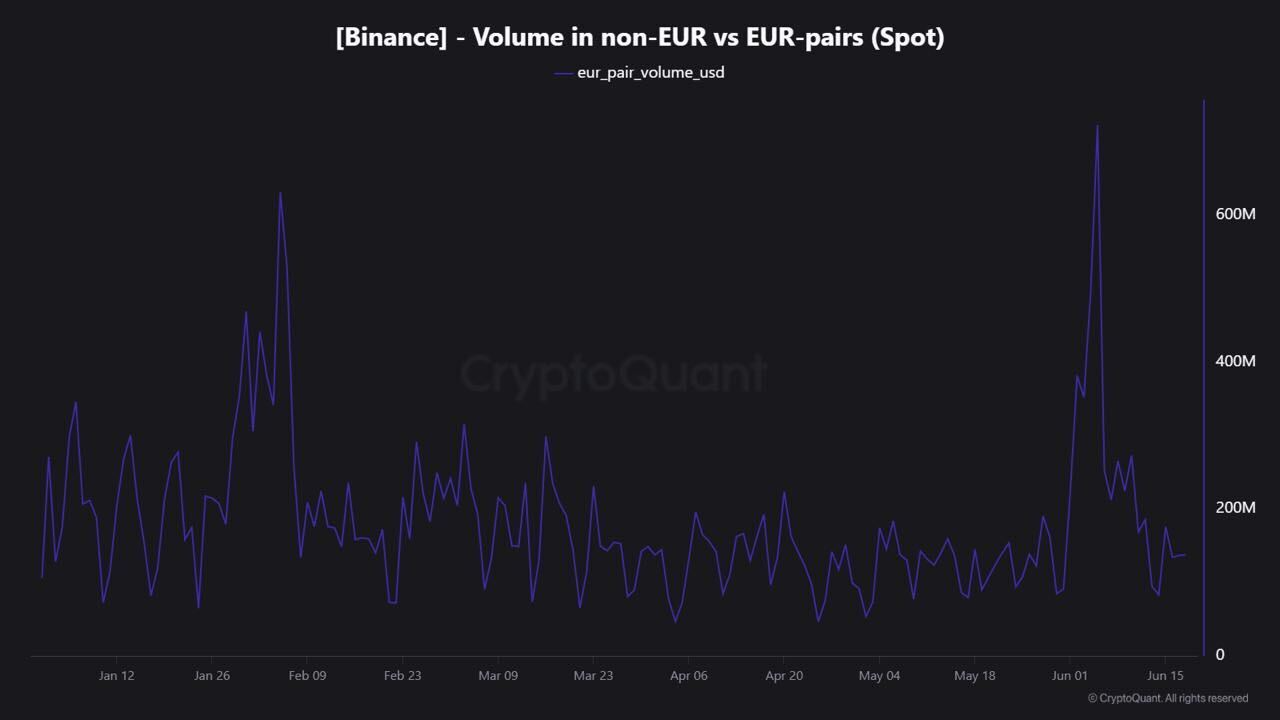

Euro-denominated trading accounts for only a small share of Binance’s activity, as the exchange faces uncertainty over its European licensing prospects under the Markets in Crypto-Assets Regulation (MiCA).

Euro (EUR) trading accounts for around 1% of Binance’s spot volume, CryptoQuant analyst Maartunn told Cointelegraph.

“Binance’s inflows remain globally distributed, which may limit the impact of potential MiCA-related setbacks,” Maartunn said, pointing to the exchange’s diversified user base across regions.

Source: CryptoQuant

The data comes as Greek regulators are reportedly preparing to reject Binance’s licensing application ahead of MiCA’s transitional deadline on July 1, a move that could complicate the exchange’s ability to serve EU residents.

Binance ranks among Europe’s biggest crypto exchanges

Even though EUR trading represents only about 1% of Binance’s global spot volume, the exchange still processes hundreds of millions of dollars in euro-denominated trades.

According to CryptoQuant data, Binance’s daily EUR-pair volumes have ranged from roughly $100 million to $250 million in 2026, with occasional spikes above $600 million.

Source: CryptoQuant

According to a December 2024 report by Kaiko, Binance, alongside Bitvavo, Kraken and Coinbase, accounted for more than 85% of all euro-denominated crypto trading volume.

Related: WhiteBIT secures MiCA license in Austria ahead of July 1 EU deadline

Unlike Binance, Bitvavo, Kraken and Coinbase are among the major exchanges that have already secured MiCA authorization, allowing them to offer services across the EU under the framework’s passporting regime.

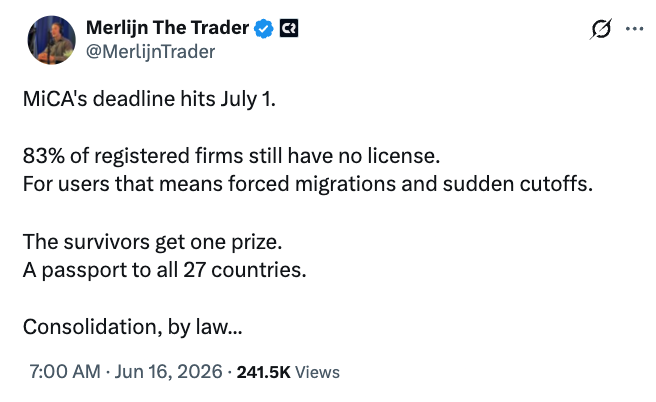

83% of CASPs have yet to receive a MiCA license

Binance’s licensing uncertainty comes as many crypto asset service providers (CASPs) are still adapting to MiCA’s requirements.

According to estimates based on European Securities and Markets Authority (ESMA) data cited by market analyst Merlijn Geurds, only around 210 of more than 1,200 firms operating under pre-MiCA registration regimes have obtained full authorization under the new framework.

Source: Merlijn Geurds

Geurds told Cointelegraph the gap reflects the cost and complexity of compliance, which requires governance standards, compliance controls and operational safeguards that many smaller firms lack.

“The result is consolidation by design,” Geurds said, adding: “A smaller group of well-capitalized, licensed players gets a passport to all 27 states, while a long tail faces forced migrations or cutoffs.”

Cointelegraph contacted Binance for comment on the size of its European business and the potential impact of MiCA-related restrictions but had not received a response by publication.

Magazine: SBF will never get a pardon, Trump peace deal boosts Bitcoin: Hodlers Digest June 14-21

Ripple’s CEO said the company might do “something special” for XRP holders if it ever goes public. The XRP community heard a promise. What he actually said was a maybe, attached to an IPO he calls a non-priority. Here is the real picture, separated from the hype.

Summary

- Ripple has not promised an IPO reward for XRP holders.

- Garlinghouse only left the door open to a possible future benefit.

- Ripple equity and XRP are separate assets with no automatic holder link.

- The real XRP case still depends on utility, regulation, adoption, and demand.

One sentence from Ripple’s chief executive set the XRP community alight. Asked on a podcast whether XRP holders might benefit if Ripple ever went public, Brad Garlinghouse said there could be a scenario where the company does “something special” for people who hold XRP, then immediately added that it was not something for the immediate term.

Within hours, the remark had been clipped, shared, and amplified into something close to a promise, with community members urging others to “hold accordingly.” But the gap between what Garlinghouse actually said and what the community heard is wide, and it matters.

The difference between a hinted-at maybe and a planned reward is the difference between a reasonable hope and a misplaced expectation. This piece separates the two, laying out exactly what was said, what it could mean, what stands in the way, and what an XRP holder should realistically take from it.

The subject sits at the intersection of two real questions: whether and when Ripple will go public, and whether holding XRP, which is a separate asset from Ripple equity, entitles you to any share of Ripple’s corporate success. These are questions the XRP community has debated for years, and Garlinghouse’s comments touched the nerve directly without resolving it.

This guide covers what Garlinghouse actually said and the precise wording that matters, the crucial distinction between Ripple the company and XRP the token, the theoretical mechanisms a holder benefit could take, why Ripple says an IPO is not a priority right now, the case that XRP holders already benefit indirectly, and what all of it adds up to for someone holding XRP today.

The goal is to give you the real picture, neither dismissing the possibility nor inflating it into the certainty the hype implied.

What Garlinghouse actually said

Precision matters here, because the entire community reaction hinges on a few words, and those words were more careful and more conditional than the excitement suggested.

Speaking with a journalist on a podcast, Garlinghouse was asked directly whether XRP holders could benefit from Ripple’s success if the company eventually launched an IPO. He did not deflect the question, but he did not commit to anything either.

His framing began with the indirect benefit Ripple already provides. He said he hopes XRP holders feel they are benefiting from Ripple’s existence through the work the company does to catalyze activity in the XRP ecosystem.

Then came the sentence that set off the excitement. Asked whether Ripple would do something specific for XRP holders if and when it goes public, he said, “Maybe. But I mean, that’s not in the immediate term.”

That is the entirety of the supposed promise: a maybe, explicitly qualified as not near-term, offered in response to a direct question, not volunteered as a plan.

The careful reading of those words reveals how conditional they are. Garlinghouse did not announce a program, describe a mechanism, or commit to any action.

He acknowledged a possibility, the way anyone might concede that something could happen without saying it will. He was explicit that it was not in the immediate term, and he attached it to an IPO that, as the next sections show, he describes as not a priority.

He also did not endorse any specific structure, declining when asked about a token buyback or another mechanism that would let holders share in Ripple’s wealth. Instead, he pointed to the indirect benefits Ripple already creates.

So the accurate summary is that Garlinghouse left a door open without walking through it. He acknowledged that a future, post-IPO benefit for XRP holders is possible while making clear it is neither planned nor imminent nor defined.

The community heard “Ripple will do something special for holders.” What Garlinghouse said was “maybe, someday, if we go public, which is not a priority.” Those are very different statements, and the difference is the whole story.

Ripple the company versus XRP the token

To understand why a holder benefit is even a question, you have to understand a distinction that confuses many people: Ripple and XRP are not the same thing, and owning one does not mean owning the other.

Ripple is a private technology company that builds payment and liquidity products, some of which use the XRP Ledger. XRP is a cryptocurrency, the native asset of the XRP Ledger, which is a decentralized, open-source blockchain that Ripple does not control.

When XRP was created, a large portion of the supply was allocated to Ripple to fund its development and promote adoption, which is why Ripple is closely associated with XRP and is in fact the largest single holder of the asset. But the association is not ownership in the corporate sense.

Holding XRP gives you a cryptocurrency, not equity in Ripple. It gives you no shares, no dividend rights, and no claim on the company’s profits or assets.

If Ripple goes public and its stock soars, that benefits Ripple’s shareholders, the holders of its equity. XRP holders are not automatically among them simply by holding the token.

This distinction is exactly why the “something special” question exists and why it is not trivially answered. Because XRP and Ripple equity are separate assets, there is no automatic, built-in mechanism by which Ripple’s corporate success, including a successful IPO, flows to XRP holders.

Any such benefit would have to be a deliberate corporate decision, a choice Ripple made to extend something to holders of a token that is legally distinct from its stock. There is no existing structure, no dividend, no buyback, and no holder-equity link that does this today.

This is what makes Garlinghouse’s maybe notable: it gestures at the possibility of Ripple voluntarily creating a link between its corporate success and XRP holders that does not currently exist and is not required to exist. The community’s hope is precisely that Ripple would choose to build such a bridge between the two separate assets.

The reality is that no such bridge exists, none is planned, and the entire question is whether Ripple might someday decide to construct one. That is a very different thing from a benefit that flows automatically.

What a holder benefit could theoretically look like

If Ripple ever did decide to do “something special,” what could it actually be? Several theoretical mechanisms have circulated, and walking through them clarifies both the possibilities and their limits.

The most discussed possibilities involve giving XRP holders some form of access to or stake in Ripple’s equity. One idea is early or preferential access to Ripple shares during an IPO, an allocation phase where verified long-term XRP holders could buy into the offering.

Another is a community-based reward structure tied to long-term XRP holding, rewarding holders who have held for a certain period. A third, more exotic idea is a tokenized representation of Ripple equity made available to eligible holders, using blockchain to give XRP holders some claim linked to Ripple stock.

Each of these would, in effect, create the bridge between Ripple equity and XRP holders that does not currently exist. It would extend a piece of the company’s success to token holders through a deliberately constructed mechanism.

These are the kinds of structures the community imagines when it hears “something special.” But they remain imagined structures, not announced ones.

The important caveat is that all of these are speculation, not plans, and each faces real practical and legal limits. Because Ripple equity and XRP are separate assets, any direct financial benefit to XRP holders would depend entirely on corporate decisions made during an IPO process that may never happen.

Such decisions carry legal, regulatory, and securities-law complications that make them far from straightforward. Linking a cryptocurrency’s holding to equity benefits raises exactly the kind of securities questions that XRP’s long legal history has been about, and Ripple would have to navigate those carefully.

Other, less direct possibilities are also floated, such as Ripple using IPO proceeds to fund ecosystem growth that indirectly benefits XRP through increased adoption and liquidity. That is closer to what Ripple already does.

The honest framing is that while several mechanisms are conceivable, ranging from share access to tokenized equity to ecosystem investment, none is announced, all face real hurdles, and the more direct and exciting versions are also the most legally complicated. The possibilities are real as possibilities. They are not, on any current evidence, plans.

Why Ripple says an IPO is not a priority

The “something special” was explicitly tied to Ripple going public, so the holder-benefit question is downstream of a prior question: will Ripple even have an IPO? And Garlinghouse has been clear that it is not a priority.

Garlinghouse stated plainly that Ripple has not prioritized going public, and he gave concrete reasons. He pointed to the recent underperformance of crypto-related public listings, citing companies whose stock has not done particularly well after going public and noting that another major exchange had reportedly delayed its own listing plans.

He also emphasized the benefits of staying private, joking that being private lets him speak freely without lawyers constraining every word. Beneath the humor was a real point about the disclosure burden and constraint that public-company status imposes.

The picture he painted was of a company that sees little reason to rush into public markets that have treated its peers poorly, and that values the flexibility of remaining private. An IPO, in his framing, is a distant possibility, not an imminent plan.

This matters enormously for the holder-benefit question, because it pushes the entire scenario further into the uncertain future. The “something special” was conditioned on Ripple going public, and Ripple going public is itself not a near-term priority.

So the holder benefit is a maybe contingent on an event that is itself a maybe. Stacking those conditionals, a possible benefit attached to a possible IPO that is explicitly not a priority and not near-term, shows how far the exciting headline is from anything concrete.

For an XRP holder, this means the “something special” should be understood as a distant, doubly conditional possibility, not as a catalyst to expect on any near horizon. Ripple may eventually go public, and if it does, it may eventually do something for holders.

But both halves of that sentence are uncertain and neither is imminent. That is a very different proposition from the one the hype implied. The IPO that the benefit depends on is not on the calendar.

The case that XRP holders already benefit

Set against the speculation about a future special benefit is Garlinghouse’s actual, stated position: that XRP holders already benefit from Ripple’s existence, indirectly but intentionally, and this argument deserves fair consideration.

Garlinghouse’s framing is that Ripple’s commercial activity is designed to benefit XRP even without any direct financial mechanism. He argues that Ripple is the most interested party in seeing XRP succeed, noting that the company remains the largest holder of XRP on the planet and therefore has the strongest economic incentive to increase the token’s value and adoption.

In his telling, Ripple’s strategy is built around making XRP the most useful, most liquid, and most trusted digital asset. Every acquisition, investment, and partnership the company pursues is evaluated partly through the lens of how it drives XRP adoption and utility.

The benefit to holders, on this view, is real but indirect. By growing the ecosystem, expanding XRP’s use in payments and settlement, and increasing its liquidity and trust, Ripple makes the XRP that holders own more valuable and more useful, which is a benefit even without any dividend or equity link.

This is where Ripple’s real-world strategy matters more than the IPO speculation. XRP’s long-term case is strongest when it is tied to actual institutional settlement, tokenization, liquidity, and demand, not to hopes of a future equity-linked reward.

This argument has genuine merit and should not be dismissed as spin. Because Ripple is the largest XRP holder, its incentives really are aligned with XRP holders in a meaningful way: Ripple profits when XRP rises, just as holders do, so the company has a built-in reason to drive the token’s value that does not require any special program.

Ripple’s actual activities, the partnerships, the payment integrations, and the institutional adoption work, do plausibly increase XRP’s utility and demand over time, which is a real if indirect benefit to anyone holding the token. That is also why XRP’s institutional catalysts matter: the strongest version of the XRP thesis comes from regulation, ETF demand, and utility aligning, not from IPO speculation alone.

The honest counterpoint is that this indirect benefit is exactly what the community finds insufficient, because it is diffuse and uncertain instead of a concrete share of Ripple’s specific corporate success. Garlinghouse’s maybe on direct benefits is precisely a response to that dissatisfaction.

But the indirect-alignment case is not nothing. It is a reasonable argument that holding XRP already ties you, loosely, to Ripple’s success through the company’s incentive to grow the token.

Whether that loose tie is enough is the debate, and it is one Garlinghouse’s comments intensified without settling.

Why the regulatory backdrop matters

The IPO question is speculative, but XRP’s regulatory backdrop is not, and it shapes why the community reacted so strongly to Garlinghouse’s remark.

XRP holders are not just hoping for a corporate reward. They are watching a year in which regulatory clarity, ETF inflows, tokenized settlement tests, and the CLARITY Act have all become part of the XRP investment story.

The CLARITY Act is especially important because it could turn XRP’s current regulatory position into a clearer statutory framework. That would matter more directly to XRP than any vague IPO benefit, because it could reduce the legal uncertainty that has constrained institutional adoption.

That does not mean the law guarantees price appreciation, and it does not mean Ripple’s IPO would automatically reward holders. But it explains why the community is primed to treat every Ripple-related signal as part of a broader XRP catalyst stack.

The problem is that not all catalysts are equal. CLARITY passage, ETF inflows, exchange-reserve changes, and real payment or settlement usage are observable market or regulatory developments.

A possible IPO reward is not. It is a speculative possibility attached to a corporate decision that has not been made.

This is why reading XRP signals carefully matters. Some signals describe actual supply, demand, usage, or regulation, while others describe hopes about what Ripple might one day decide to do.

For XRP holders, the discipline is to separate the two. The regulatory and institutional backdrop is real; the IPO reward remains hypothetical.

What it means for XRP holders

For someone holding XRP and watching this story, the practical question is what to actually make of it, and the answer is a matter of holding the possibility and its limits in proper proportion.

The realistic reading is that a direct XRP holder benefit from a Ripple IPO is a genuine possibility but a distant and unplanned one. It is contingent on an IPO that Ripple says is not a priority and structured through mechanisms that face real legal hurdles and do not currently exist.

An XRP holder should neither dismiss the idea entirely, since Garlinghouse did deliberately leave the door open and Ripple’s incentives are truly aligned with holders, nor treat it as a reason to expect a windfall. Nothing is planned, announced, or near-term, and the whole scenario depends on conditions that may not materialize.

Buying or holding XRP specifically in expectation of an IPO reward would be building on speculation about a maybe attached to a maybe, which is a weak foundation for any financial decision. The sensible stance is to regard a potential holder benefit as a possible future upside that is not to be counted on, instead of as a catalyst to position around.

The more grounded takeaway is to focus on what is actually known rather than on the speculation. What is known is that Ripple is closely tied to XRP, is the largest holder of the asset, and has strong incentives to grow its value, which provides a real if indirect benefit to holders.

What is known is that XRP and Ripple equity are separate, with no current mechanism linking the two. And what is known is that Garlinghouse acknowledged a possible future benefit while explicitly declining to plan or promise one, tied to an IPO he does not prioritize.

An XRP holder is better served evaluating the token on its actual merits: its use in payments and settlement, its regulatory position, its adoption trajectory, and institutional positioning in XRP. Those are measurable signals.

The IPO story is worth knowing, but it is a speculative possibility at the edge of the picture, not the center of any sound reason to hold XRP. That is the price reality behind the hope: bullish narratives only matter when the market can connect them to actual token demand.

None of this is investment advice; it is a frame for reading a piece of news that the community has inflated well beyond what was actually said.

A maybe, not a promise

The story that “Ripple will do something special for XRP holders when it goes public” is, on close inspection, a story about a carefully hedged maybe.

Garlinghouse, asked directly, acknowledged that a post-IPO benefit for XRP holders was possible while immediately adding that it was not in the immediate term. He declined to describe any mechanism and pointed instead to the indirect benefits Ripple already provides.

The community heard a promise. What was actually offered was a conditional acknowledgment of a possibility, attached to an IPO that Ripple says is not a priority, structured through mechanisms that do not exist and would face real legal hurdles.

The gap between those two readings is the entire substance of the story.

The grounding facts cut through the excitement. Ripple and XRP are separate assets, so no benefit flows automatically; any link would be a deliberate, unplanned corporate choice.

The IPO that a benefit depends on is itself not near-term by Ripple’s own account. And the benefit that does exist today is the indirect one Garlinghouse emphasized: Ripple, as the largest XRP holder, has genuine incentives to grow the token’s value, which loosely aligns the company’s success with holders’ even without any special program.

For an XRP holder, the honest conclusion is that a direct IPO reward is a distant possibility worth knowing about but not worth counting on. It is a maybe at the edge of the picture rather than a catalyst at its center.

The door Garlinghouse left open is real, but it is just a door left open, not a path being walked. The difference is exactly the difference between a reasonable hope and the windfall the hype imagined.

Frequently asked questions

Did Ripple promise to reward XRP holders if it goes public?

No. Ripple CEO Brad Garlinghouse, asked whether XRP holders could benefit from a Ripple IPO, said the company might do something special but immediately added that it was not in the immediate term. He did not announce a program, describe a mechanism, or commit to anything; he acknowledged a possibility in response to a direct question. The community amplified this into a promise, but what was actually said was a carefully hedged maybe, attached to an IPO Ripple says is not a priority.

Are Ripple and XRP the same thing?

No, and the distinction is crucial. Ripple is a private technology company that builds payment products, some using the XRP Ledger. XRP is a cryptocurrency, the native asset of the decentralized XRP Ledger, which Ripple does not control. Holding XRP gives you a cryptocurrency, not equity in Ripple, no shares, dividends, or claim on company profits. Ripple is the largest single holder of XRP, but that association is not ownership. That is why a holder benefit would require a deliberate corporate decision.

What could a holder benefit theoretically look like?

Several speculative mechanisms have circulated: early or preferential access to Ripple shares during an IPO allocation, a reward structure tied to long-term XRP holding, or a tokenized representation of Ripple equity for eligible holders. Ripple could also use IPO proceeds to fund ecosystem growth that indirectly benefits XRP. All of these are speculation, not plans, and the more direct versions face real legal and securities-law hurdles, since linking a cryptocurrency to equity benefits raises exactly the questions XRP’s legal history has been about.

Is Ripple going to have an IPO soon?

Not according to Garlinghouse, who said going public is not a priority for Ripple. He cited the underperformance of recent crypto-related public listings as evidence the environment is unfavorable, and emphasized the benefits of staying private. Since the something special was tied to an IPO, and the IPO itself is not near-term, the holder benefit is a possibility contingent on an event that is itself uncertain and not imminent. That pushes the whole scenario into the distant and doubly conditional future.

Do XRP holders benefit from Ripple’s success at all?

Indirectly, yes, by Garlinghouse’s argument. Ripple is the largest XRP holder, so its incentives are genuinely aligned with holders; it profits when XRP rises, just as they do. Ripple’s strategy aims to make XRP the most useful, liquid, and trusted digital asset, and its partnerships and adoption work plausibly increase XRP’s value over time. This indirect benefit is real, though the community finds it insufficient compared to a concrete share of Ripple’s corporate success, which is the dissatisfaction Garlinghouse’s maybe was responding to.

Should I hold XRP because of a possible IPO reward?

A possible IPO reward is a weak basis for a financial decision, because it is a maybe attached to a maybe: an unplanned, undefined benefit contingent on an IPO Ripple does not prioritize. It is better regarded as a distant possible upside not to be counted on than as a catalyst to position around. An XRP holder is better served evaluating the token on its actual merits, its use in payments, its regulatory position, and its adoption, than on speculation about an IPO reward that exists only as a hedged maybe. This is not investment advice.

As of June 21, 2026. Statements and corporate plans can change; this concerns speculative, unannounced possibilities. This article is information, not investment advice.

XRP traders are watching a cluster of signals that, if they play out, could set up a short-term relief rally and potentially a larger recovery attempt later in the year. Multiple technical indicators point to a market that may be nearing an oversold phase, with key levels around $1.39–$1.40 attracting attention.

As of Monday, XRP was trading near $1.13, while its longer-term trend gauges and momentum readings suggested the downside move may be losing steam—at least in the near term. At the same time, derivatives positioning data points to a potential “price magnet” effect that could pull the market toward higher liquidation zones.

Key takeaways

- XRP’s 20-week EMA is close to crossing below its 200-week EMA, a weekly “death cross” scenario that has historically been followed by mean-reversion rebounds.

- A move back toward the $1.39–$1.40 zone would align with prior post-cross behavior and could represent roughly the mid-20% upside range from around $1.13.

- CoinGlass liquidation heatmap data for XRP/USDT shows heavier short liquidation liquidity above spot, concentrated around approximately $1.37–$1.40.

- An analyst framework from Cryptollica argues XRP could be approaching conditions similar to previous washed-out phases, with long-term targets framed near $8 if a broader bottom develops.

The “mean-reversion” setup targeting $1.39–$1.40

One of the main triggers behind the bullish short-term outlook is XRP’s positioning relative to two long-horizon moving averages. According to TradingView data referenced in the report, XRP’s 20-week exponential moving average (20-week EMA) was near $1.40 and appeared on the verge of dropping below the 200-week EMA (around $1.39).

If XRP prints a confirmed weekly close below the 200-week EMA, that would mark a relatively uncommon “death cross” between the two trend indicators—an event that traders often associate with sustained weakness. However, the article argues that XRP’s past instances of 20-week/200-week EMA crosses have not led only to further declines; instead, they were followed by relief rebounds back toward the 200-week EMA.

Historically, the cited examples include a roughly 20% recovery in 2019 and a much larger 82.7% rebound in 2022 after similar cross events. Under that same mean-reversion logic, the $1.39–$1.40 band becomes the focal point, implying potential upside on the order of about 23%–25% from XRP’s referenced price near $1.13—timed, in the report’s estimate, toward July.

Momentum data adds another layer. XRP’s weekly relative strength index (RSI) was hovering just above the oversold threshold of 30 on Monday. RSI readings near 30 often indicate that selling pressure may be nearing exhaustion, which can increase the odds of a short-term rebound even if the larger trend remains under pressure.

Derivatives positioning: liquidation liquidity above spot

Beyond charts and momentum, the report also points to derivatives microstructure using CoinGlass data. Specifically, it references a Binance XRP/USDT liquidation heatmap that shows the distribution of liquidation levels above and below the current price.

In that view, there is a heavier concentration of short liquidation liquidity above spot than long liquidation liquidity below it. The largest upside cluster is reported at roughly $236.5 million located in the $1.37–$1.40 zone, according to the CoinGlass liquidation heatmap for XRP/USDT.

Liquidation heatmaps are commonly interpreted as maps of where leveraged positions may be forced to close. If XRP begins rebounding from around $1.13, shorts positioned above the market may face buyback pressure, which can create an accelerant toward nearby liquidation clusters—potentially reinforcing a push toward $1.39–$1.40.

It’s important to note the conditional nature of this mechanism: liquidation “magnets” typically work best when price action already turns upward, because liquidation levels alone do not guarantee direction. Still, the asymmetry highlighted by the heatmap suggests the market’s levered risk may be skewed toward higher prices if a bounce begins.

Longer-term framing: a potential broader bottom toward $8

The story does not stop at near-term levels. A separate long-term chart shared by analyst Cryptollica is used to argue that XRP may be entering another stage consistent with major market washouts.

Cryptollica’s framework, shared in a Sunday post on X (linked in the source), highlights XRP’s 10-day RSI hovering near the low-30s—near the range that has historically appeared around major accumulation phases. The post also makes a broader historical claim that, over “13 years,” XRP has only been this “washed out” three times.

“The first 2 times, the crowd laughed, ignored it, and only understood the setup after price had already left,” Cryptollica said in the referenced post.

In the same chart-based thesis, Cryptollica also points to XRP trading above the lower boundary of a large ascending channel. This channel is described as a support structure that has connected multiple macro lows since 2017. The lower boundary is shown near $0.75, implying the asset may still need another downside sweep before a larger recovery phase begins.

The report frames that potential sequence as: a retest of the channel support area near $0.75 first, followed by a transition into a broader bull-market phase. In that case, the channel’s upper boundary is cited as placing a long-term target near $8.

Because this portion of the narrative relies on technical pattern interpretation rather than a measurable, real-time indicator with a universally accepted trigger, the $8 target should be treated as conditional. What matters for now is the setup being claimed: oversold momentum near key thresholds and the possibility that XRP could remain supported by the channel structure—even if additional downside occurs before any large reversal.

What to watch next for XRP

Traders monitoring this thesis should focus on whether XRP can maintain an oversold bounce without losing the $1.13 area too aggressively, and whether a weekly close develops that confirms the 20-week/200-week death cross scenario. On the derivatives side, pay attention to whether price moves toward the $1.37–$1.40 liquidation cluster instead of stalling below it; and for longer-horizon investors, keep an eye on whether XRP holds above the ascending channel’s lower boundary near $0.75, since that level is positioned as the next checkpoint before any larger recovery attempt.

Bitcoin price is trading under pressure and a bad prediction, down 1.57% over 24 hours and hovering in the mid-$60K range. A hawkish Fed from last week, rising bond yields, and deteriorating chart structure are compressing the setup.

Pseudonymous analyst Doctor Profit, who correctly called BTC’s bull-market peak at $126,000 and the subsequent selloff, flagged a textbook bear flag forming on the daily timeframe. The pattern uses Bitcoin’s drop from the May high of $82,000 to sub-$60,000 as the pole, with the recent bounce to $68,000 forming the flag.

His stated target: an initial flush to the $54,000–$56,000 region, followed by sideways action and then a deeper leg toward $40,000–$50,000. That call is getting corroboration from options flow. Even last week, traders were actively buying puts with strikes down to $52,000.

#Bitcoin – What's Next? — Doctor Profit

The Big Sunday Report: All We Need to Know TA / LCA / Psychological Breakdown:

TA / LCA / Psychological Breakdown:

Everyone bullish here is making a big mistake, and don't misunderstand my words. I clearly speak about those who are buying now long term, believing the bottom was in.… pic.twitter.com/yxjGmjmVNw

(@DrProfitCrypto) June 21, 2026

(@DrProfitCrypto) June 21, 2026

The macro backdrop is not helping. Combined exchange volumes dropped 3.45% in May to $4.41 trillion, the lowest reading since September 2024. Thin volume environments are also holding any directional moves.

Discover: The Best Crypto to Diversify Your Portfolio

Bitcoin Price Prediction: $54K as the Bear Flag Breaks Down?

Bitcoin’s current technical structure is deteriorating on multiple timeframes. The immediate problem: BTC has lost the $72,000 zone that previously acted as key support. Our analyst notes that daily closes below that region keep downside risk elevated, with $54,800 identified as the next high-timeframe demand cluster, the point where structural support and the 0.618 Fibonacci retracement converge.

Below the spot, the ladder of support runs through $60,000–$58,000 (near the 200-day SMA) before reaching the $54,000 zone. This adds a wrinkle: a liquidity-grab push toward $77,000–$78,000 is possible before the flush, which would shake out short positions before resuming the downtrend. Bear flags fail, and that’s resuming the bull, and a reclaim of $78,300 on a daily close would invalidate the pattern entirely.

Given current options positioning and volume trends, there is continued pressure. On-chain models, including Willy Woo’s CVDD floor (near $45,500) and metrics like Active Price and Cointime Price cluster the probable cycle bottom between $46,000 and $54,000, which means $54K may be a floor worth defending rather than a midpoint on the way lower.

A bear flag pattern confirmation, on the other hand, triggers a measured move that cuts through $54K toward the $46,000–$50,000 range. Some bottom signals are beginning to surface, but confirmation hasn’t arrived.

Discover: The Best Token Presales

Bitcoin Hyper Targets Early Mover Upside as Bitcoin Tests Key Levels

Spot Bitcoin grinding toward a multi-month low isn’t a comfortable holding environment, especially when the measured-move math points to another 15–20% of potential downside. Rotation into early-stage infrastructure plays has historically picked up when BTC consolidates at cycle lows, with capital looking for asymmetric return profiles that spot BTC cannot offer at current valuations.

Bitcoin Hyper is positioning directly inside that thesis. The project is the first Bitcoin Layer 2 integrating the Solana Virtual Machine, delivering sub-second finality and low-cost smart contract execution on top of Bitcoin’s security model.

Hyper is addressing Bitcoin’s three structural constraints: slow transactions, high fees, and no native programmability. The presale itself has raised numbers close to $33 million at a current price of just $0.0136, with staking available at a high APY for early participants. With Hyper, a decentralized canonical bridge handles BTC transfers natively.

Review the Bitcoin Hyper presale details here.

The post Bitcoin Price Prediction: Analyst Flags $54K as Bear Flag Forms appeared first on Cryptonews.

David Benavidez admits he’s ‘not ready right now’ to face one champion: “I have a lot of respect for him”

Apple MacBook Air M5 review: Boring has never been this good

UK weather live: Met Office issues RED heatwave alert as hottest day ever looms

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Miami – Corporette.com

-

Tech6 days ago

Tech6 days agoThe Adder At The Heart Of Intel’s 8087 FPU

-

Entertainment2 days ago

Entertainment2 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Business2 days ago

Business2 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Business2 days ago

Business2 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Politics4 days ago

Politics4 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Crypto World2 days ago

Crypto World2 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World2 days ago

Crypto World2 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Sports4 days ago

Sports4 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

-

Crypto World2 days ago

Crypto World2 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Business2 days ago

Business2 days agoMHP SE 2026 Q1 – Results – Earnings Call Presentation (OTCMKTS:MHPSY) 2026-06-20

-

Crypto World4 days ago

Crypto World4 days agoAnthropic’s Dario Amodei Urged AI Unity at G7, Even as US Banned His Models

-

Business4 days ago

Business4 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

-

Crypto World6 days ago

Crypto World6 days agoRobinhood opens AI-powered trading to all users, sending HOOD stock past $100

-

Tech5 days ago

Tech5 days agoWeeks Of In-The-Field Testing And A Verdict

-

Politics2 days ago

Politics2 days agoAndy Burnham and the meaning of Makerfield

-

Tech4 days ago

Tech4 days agoAdobe adds its AI assistant to Premiere, Illustrator and InDesign

-

Crypto World4 days ago

Crypto World4 days agoIren (IREN) Stock Surges on Jefferies Buy Rating: AI Infrastructure Play Gains Momentum

-

Tech4 days ago

Tech4 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

News Videos4 days ago

News Videos4 days agoIMPACT ON BITCOIN IF NO GOLD IS FOUND IN FORT KNOX

You must be logged in to post a comment Login