Crypto World

Applied Optoelectronics (AAOI) Stock Plunges 17% Following Meta CEO’s AI Investment Remarks

Key Highlights

- Shares of AAOI plummeted 17% following Meta CEO Mark Zuckerberg’s remarks about the company’s 2026 restructuring challenges

- The stock maintains remarkable gains of 205% year-to-date and 320% over 12 months, crushing Nvidia’s performance by over 200 points in 2026

- Ariose Capital Management acquired 104,000 shares valued at approximately $8.8 million during Q1, positioning it as their 6th-largest investment

- Company insiders have offloaded 500,215 shares totaling roughly $86.7 million in the past three months

- Wall Street maintains a Hold consensus rating with a $113.80 average price target, though Rosenblatt stands firm with a Buy rating at $220

Applied Optoelectronics (AAOI) experienced one of its most brutal trading sessions in 2026 on Thursday, plummeting 17% after comments from Meta’s CEO Mark Zuckerberg sent shockwaves through the photonics industry.

Applied Optoelectronics, Inc., AAOI

The stock began Friday’s trading at $120.95, a steep decline from the $140-plus levels it commanded earlier in the week.

During his remarks, Zuckerberg expressed continued optimism that Meta would observe more tangible returns from artificial intelligence expenditures in the next three to six months. However, he also admitted that the company’s 2026 restructuring efforts and workforce reductions hadn’t proceeded as “perfectly smooth” as hoped. These comments were sufficient to spark a widespread selloff throughout AI infrastructure stocks.

Companies in the photonics space, including Lumentum and Coherent Corp (COHR), experienced similar sharp declines that day.

While Thursday’s decline was painful, perspective is crucial. AAOI shares remain elevated by more than 205% year-to-date and over 320% during the trailing 12 months. Nvidia (NVDA), in contrast, shows approximately 3% gains in 2026. That represents a performance differential exceeding 200 percentage points.

Applied Optoelectronics manufactures high-speed optical transceivers essential for connecting GPU clusters within artificial intelligence data centers. As cloud giants accelerated their AI infrastructure investments, AAOI emerged as one of the market’s most explosive momentum plays. This popularity brings heightened expectations — and minimal patience for uncertainty.

Institutional Interest Remains Strong

Despite recent price swings, institutional money managers continue building positions. Ariose Capital Management revealed a fresh stake of 104,000 AAOI shares during the first quarter, worth roughly $8.8 million. This position now ranks as the firm’s 6th-largest holding, accounting for approximately 5.9% of its total portfolio.

Additional firms such as Allworth Financial, Northwestern Mutual Wealth Management, and Krilogy Financial have similarly established or expanded positions in recent periods. Institutional ownership now stands at 61.70% of total shares outstanding.

Executive Stock Sales Paint Contrasting Picture

While institutional buyers accumulate shares, company executives have been actively reducing their stakes. During the previous three months, insiders disposed of 500,215 shares valued at approximately $86.7 million.

Board member Cynthia Delaney liquidated 56,575 shares at $189.23 per share in late May — representing a 48.68% reduction of her holdings. Insider Hung-Lun Chang sold 40,329 shares at $170.60 each in June through a predetermined 10b5-1 trading arrangement.

Insider ownership currently represents just 3.80% of the company.

Regarding analyst coverage, Rosenblatt Securities maintained its Buy recommendation and $220 price objective as recently as June 22. Raymond James reaffirmed its Outperform stance on June 10. Wall Street Zen represents the bearish outlier, issuing a Sell rating in April. The consensus recommendation remains at Hold with a mean price target of $113.80 — significantly below the stock’s pre-Thursday trading level.

The company’s latest quarterly results, released May 7, revealed Q1 revenue of $151.14 million — representing a 51.3% year-over-year increase but falling short of the $156.98 million analyst projection. Earnings per share registered at -$0.07, missing the -$0.05 consensus forecast. Management provided Q2 2026 EPS guidance ranging from -$0.03 to $0.03.

The 12-month trading range extends from $18.50 to $233.67, while the stock exhibits a beta of 3.69 — a figure that illustrates its extreme volatility characteristics.

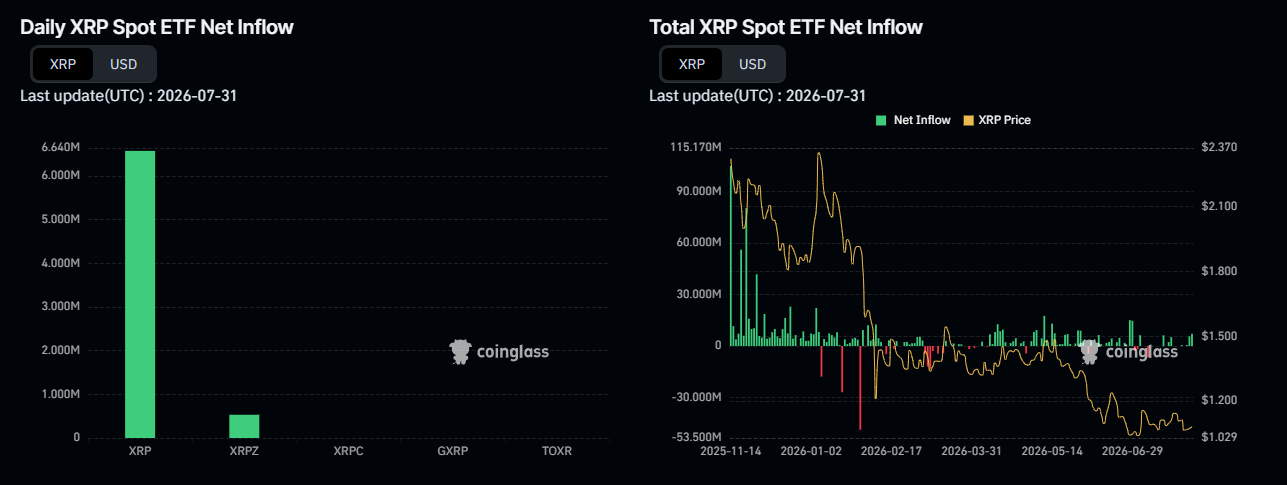

XRP-backed exchange-traded funds (ETFs) pulled in $27.29 million in July, marking a fourth straight month of net inflows.

The token itself trades near $1.08, down roughly 40% since the start of the year, in line with a generally poorly preforming crypto market. But many expect intuitional money and these products to be bolstering XRP, and others.

Instituional Money

Cumulative XRP ETF inflows now sit near $1.5 billion, the largest total among altcoin products. The price keeps sliding anyway.

XRP funds have ranked first or second in monthly inflows since April, without barely any outflows. Inflows ran $81.59 million in April, $131.94 million in May, $59.46 million in June, and $27.29 million in July, showing the pace has cooled even as the streak holds.

That steady buying stands out against a market where fresh capital keeps concentrating in a handful of tokens. Several smaller altcoin funds recorded no net flows in July. XRP kept adding, even at a slower pace.

Why the Price Isn’t Following the Flows

Steady ETF demand alone hasn’t lifted XRP’s price. Some of the pressure traces to a specific seller. Grayscale chief executive Peter Mintzberg filed to sell XRP ETF shares he acquired before the fund’s listing. He priced the sale at $20.45 a share, about half what earlier Grayscale insiders got in January.

Momentum indicators tell a similar story. XRP recently hit its most oversold readings on record. Traders remain split on whether the sell-off has finished.

Competition for capital plays a role too. Solana funds have pulled in about $1.15 billion since launch, edging back into second place in July. Hyperliquid funds added roughly $293 million in May and June before posting a first monthly outflow in July.

Bitcoin (BTC) and Ethereum (ETH) funds still dominate the category. They pulled in $172 million and $365 million in July, respectively.

Steady ETF buying shows institutional appetite for XRP has not faded. Whether that demand eventually lifts the price may depend on the broader altcoin market finding its footing first.

The post XRP ETFs Keep Drawing Cash, So Why Is the Price Down 40%? appeared first on BeInCrypto.

Cardano (ADA) price jumped nearly 10% in 24 hours to around $0.189, as the network turned its attention to the Dijkstra era following the van Rossem upgrade.

The rally suggests investors are pricing in the scalability roadmap rather than the upgrade already delivered.

What the Dijkstra Era Will Bring to Cardano

The Dijkstra era refers to Cardano’s next major development phase. Intersect, the organization supporting the network’s open development and governance, confirmed planning has begun.

The timing follows a completed milestone. The van Rossem hard fork, enacted on July 18, upgraded the protocol to Version 11, improving Plutus performance, ledger consistency, and node security.

Dijkstra will arrive in phases rather than as a single event. Key features include Nested Transactions, Linear Leios and Peras, all part of the broader Ouroboros Leios research programme.

The goal is throughput without compromise. Those upgrades aim to increase transaction capacity and support more complex applications while preserving decentralization and security.

Follow us on X to get the latest news as it happens.

A concrete deadline exists. The Haskell node team aims to deliver Nested Transactions and Linear Leios to the mainnet by the end of 2026. Governance work runs alongside the roadmap. Intersect defines a process that lets stakeholders shape the scope of hard forks beyond the initial Dijkstra release.

Even the name remains open, with discussions leaning toward Alexander Esgen and Fabian von Bergen as alternatives.

Can the Roadmap Sustain ADA’s Rally

Cardano researcher Dr. Cuadrado framed the distinction clearly. Van Rossem improved core performance and security, while Dijkstra addresses significantly higher transaction volumes and more sophisticated on-chain applications.

He emphasized the network’s deliberate, research-driven approach, contrasting it with projects that prioritize marketing over architectural rigor.

Other items appeared in Intersect’s latest weekly update. A new minPoolCost and Plutus memory parameter action is open for voting, alongside audited Constitutional Committee election results. Infrastructure progress continued, too. The CAP Portal reached alpha launch, and the Eryx ZK Bridge was completed.

The market response looks constructive but deserves context. ADA still trades roughly 95% below its record high of $3.09, set in September 2021, and a 10% daily move remains modest against the token’s historical volatility.

Roadmap announcements carry execution risk. Cardano upgrades have frequently generated initial enthusiasm followed by consolidation when timelines stretch.

The end-of-2026 target leaves ample room for slippage. Nested Transactions and Linear Leios both depend on research that continues evolving.

Sustained price gains will likely require measurable adoption. Developer activity, new applications, and rising total value locked matter more than announcements alone.

For now, the rally reflects renewed confidence in Cardano’s technical direction. Whether that confidence translates into lasting demand depends on what actually ships over the coming months.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

The post ADA Price Jumps 10% While Cardano Turns Toward Its Next Big Upgrade Era appeared first on BeInCrypto.

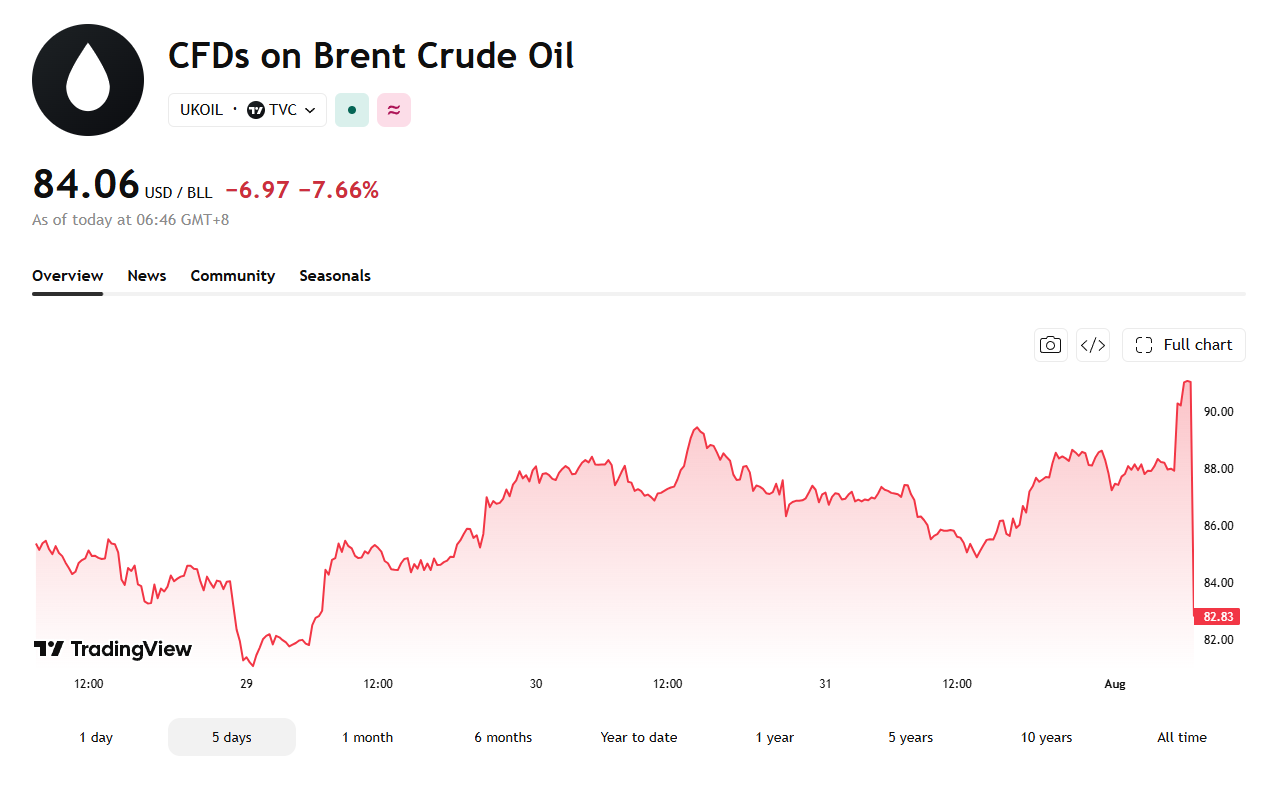

Brent crude tumbled 9% intraday on Sunday evening. It slid from a previous close of $91.03 to a low of $82.83 after US President Donald Trump said talks with Iran to reopen the Strait of Hormuz begin Monday afternoon.

The price later clawed back some ground to trade near $84.06, still down 7.66% on the day.

Another Walk-Back, or Real Peace?

Trump told reporters aboard Air Force One that negotiations start the following afternoon. He made the comment a day after he called off what he described as a massive planned attack on Iran.

Trump said Saudi Arabia, the United Arab Emirates, Qatar, and Iran itself all asked him to hold off. He said the request signals every side expects a Hormuz deal, with a separate nuclear agreement to follow.

Saudi state media confirmed part of that account. It reported that Crown Prince Mohammed bin Salman pushed Trump toward deescalation in a weekend phone call. Iran tells a different story.

State media gave no sign Tehran had shifted its stance on the strait. The semi-official Fars news agency went further and denied Iran ever asked Trump to pause the strikes, mocking his account directly.

“Trump the fool has run out of steam!”

— Fars news agency, via CNN

Uncertainty Continues to Plague the Markets

The exchange fits a pattern. Trump credits regional pressure, not his own advisers, each time he delays a strike. He still maintains on social media that US forces stand ready to resume action at any moment.

Any nuclear deal would build on the memorandum of understanding both sides signed in June. That agreement gave both sides 60 days to negotiate, and the window is now closing.

The uncertainty already hits consumers and markets on both sides. Americans pay more at the pump as shipping and output disruptions persist. Months of conflict have strained Iran’s own economy.

Every Trump signal has whipsawed oil traders since, including Wednesday’s 9.6% Hormuz-linked jump that preceded this latest reversal.

Monday’s talks may still produce only another delay. Tehran remains publicly unmoved, and the MoU clock keeps running out.

The post Oil Plunges 9% as Trump Sets Monday Talks to Reopen Hormuz appeared first on BeInCrypto.

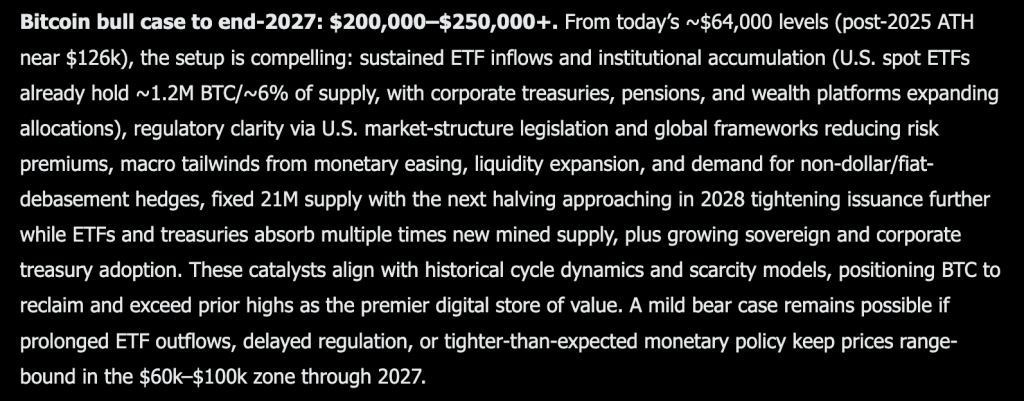

Grok AI predicts a major re-rating for Bitcoin, and this price prediction is unusual in its timeframe, targeting the end of 2027 rather than 2026. From today’s roughly $64,000 levels, well below the 2025 all-time high near $126,000, the bull case runs to $200,000 to $250,000 or higher.

The setup rests on sustained ETF inflows and institutional accumulation continuing to build. US spot ETFs already hold approximately 1.2 million BTC, roughly 6% of total supply, with corporate treasuries, pensions, and wealth platforms all expanding their allocations at the same time.

Regulatory clarity is named as a second major pillar. US market structure legislation, combined with global regulatory frameworks, is expected to reduce the risk premium investors have historically attached to holding Bitcoin.

Macro tailwinds round out the case with monetary easing, broader liquidity expansion, and rising demand for hedges against non-dollar and fiat debasement. Grok also points to the fixed 21 million coin supply, with the next halving approaching in 2028, tightening issuance even further, while ETFs and treasuries are already absorbing multiple times the amount of newly mined supply entering the market.

Growing adoption of sovereign and corporate treasuries is framed as the final piece. Grok argues these catalysts align with historical cycle dynamics and established scarcity models, positioning Bitcoin to reclaim and exceed its prior highs as the premier digital store of value.

The bear case here is treated as mild but genuinely possible. If ETF outflows persist for a prolonged period, regulation gets delayed, or monetary policy stays tighter than expected, Grok sees Bitcoin remaining range-bound in the $60,000 to $100,000 zone straight through 2027.

Bitcoin Price Prediction: BTC Has Spent Six Months Rebuilding From The Same Low Twice, Can Grok AI Predicts Work out?

Price closed at $63,931, down 1.21%, during a session that ranged between $63,547 and $65,340. That quiet red day sits almost exactly on top of a level this chart has visited and defended more than once this year.

Zoom out, and the shape since October 2025 has been a long, uneven decline. Bitcoin peaked near $128,000 that month, then broke down hard through January, gapping from above $92,000 to under $76,000 in a matter of weeks.

Since that crash, price built a rounded recovery through spring, peaking near $99,000 in April, then rolled over into a sharp flush down to $60,000 in June. A second recovery attempt through May pushed toward $82,000 before failing and dragging the price back down to retest that same $60,000 floor in June and July.

That is two separate visits to the same support level within a matter of months, which makes $60,000 one of the more tested lines on this entire chart. Support sits right there at $60,000, with limited recent history below it, before the price moves into territory not seen this year.

Resistance stacks at $66,000, then $70,000, then the heavier April ceiling near $99,000 that has already rejected two full rally attempts. Momentum here is mildly negative after today’s session, consistent with a market still consolidating rather than committing to a clear direction.

For Grok’s bull case to gain real traction over its multi-year timeframe, Bitcoin eventually needs to clear $99,000, a level this exact chart has failed at twice already. Until that happens, the current price action looks much closer to the bear-case range this prediction lays out than to the start of a run toward six figures.

Being Right and Getting Paid Aren’t the Same Thing. Claim up to $25 From Kalshi

You read the analysis. You form a view. The market proves you correct, and buying spot means you were exposed to a dozen things you had no opinion on.

Kalshi is a CFTC-regulated exchange for event contracts: one question, one outcome, one settlement. Trade the Fed, inflation, crypto price levels, and the events that actually move the market.

Contracts can resolve against you and go to zero, so size accordingly.

→ Get up to $25 to trade your first market

The post Grok AI Predicts Bitcoin Will Blow Past Its Old Record by End of 2027 appeared first on Cryptonews.

Japan could formally confirm joint currency action with Washington on Monday, and one official told Reuters the operation is still ongoing, turning the announcement into a live market event.

Bitcoin trades near $63,000, exposed to a bond market problem most crypto traders have not priced.

The Bond Market Reason Behind the Cooperation

The 2011 comparison matters more than it appears. That year the Group of Seven (G7) sold yen to stop it rising, meaning this is the first coordinated effort in 15 years pushing the currency the opposite direction.

Finance Minister Satsuki Katayama will make the announcement, two officials told Reuters. Her top currency diplomat, Atsushi Mimura, signaled the ministry now works in close coordination with monetary policy.

That phrasing carries weight. It suggests Tokyo will pair intervention with the rate hikes the Bank of Japan hinted at last week, rather than relying on purchases alone.

A quieter development may matter more. Japan’s finance ministry made a rare English-language post on X noting it holds a broad range of tools, including access to the Federal Reserve repurchase facility.

The mechanism deserves attention. Introduced in 2020, the facility lets Japan raise dollar liquidity without selling US Treasuries outright.

Follow us on X to get the latest news as it happens.

Critics flagged exactly that constraint. Funding intervention by liquidating Japan’s enormous Treasury holdings risks triggering a selloff in American debt and spiking yields.

Washington’s motivation becomes clearer through that lens. Analysts see the cooperation driven partly by concern over rising Treasury yields, which would worsen if Tokyo failed to stabilize both the yen and Japanese government bonds.

Former Bank of Japan official Nobuyasu Atago framed the logic directly. Both countries risk inflation running hot and leaving their central banks behind the curve, so they see merits in cooperating.

What Bitcoin Traders Should Watch on Monday

Tokyo is managing domestic pressure too. Economy Minister Minoru Kiuchi said Sunday the government will improve market communication, stressing the importance of maintaining trust in Japan’s fiscal sustainability.

Bitcoin traders should care about that bond angle specifically. Rising global yields compete directly with non-yielding assets, and Japanese government bond stress has repeatedly spilled into crypto this year.

“How will global risk assets respond if the world’s largest carry trade begins to unwind? The answers won’t come overnight. But one thing is clear. A story that started in the currency market could end up influencing everything from stocks to Bitcoin…,” Wise Advice said on X.

Positioning amplifies the risk. Non-commercial yen short contracts reached 163,412 by late July, leaving substantial leverage exposed to any sudden reversal. The immediate question is credibility rather than firepower.

Markets will test whether Monday’s confirmation carries a rate commitment or only a purchase pledge.

A hawkish pairing changes the calculus considerably. Rate differentials close permanently when policy shifts, whereas interventions fade once the buying stops.

That distinction shapes both scenarios for Bitcoin. Aggressive yen appreciation forces leveraged unwinding across risk assets, while gradual strengthening alongside a softer dollar could expand liquidity instead.

Timing determines everything here. Asian markets open first on Monday, and any gap in USD/JPY will reach crypto before American traders react.

“If the US sells dollars to buy yen, the dollar weakens and USD/JPY falls. Normally, this supports Bitcoin, gold and tech stocks. But there is a major catch: A rapid yen rally could unwind one of the world’s largest carry trades. Investors who borrowed cheap yen to buy stocks, crypto and other higher-yielding assets may be forced to sell…,” Coin Bureau noted.

The rate gap remains the structural anchor. Japan holds policy at 1% against a considerably higher US ceiling, and no intervention closes that on its own.

Watch the Japanese bond market alongside the currency. If yields stay contained after the announcement, the coordinated defense is working, and Bitcoin’s macro headwind eases with it.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

The post Japan Could Trigger the Biggest Market Shock of 2026: How Might Bitcoin React? appeared first on BeInCrypto.

“This is what modern warfare looks like, and it further illustrates there’s no plan to win a war with Iran,” Walz said.

Emphasizing comments that he recently shared on X, Trita Parsi, Executive Vice President of the Quincy Institute for Responsible Statecraft, said that it would be reasonable for Iran to attempt cyber attacks as a “warning” that it is prepared to retaliate for U.S. strikes.

And Parsi tells TIME that Iran is more than capable of fulfilling the threat.

“Iran is a highly capable cyber power, only one tier below the U.S., China, and Russia, and in some aspects on par with Israel,” he says. “It has in the past demonstrated a clear ability to target industrial control systems, water facilities, and energy infrastructure.”

The joint statement issued last week by federal agencies also underscored Iran’s cyber capabilities. “Iranian cyber actors continue to target U.S. critical infrastructure,” said Assistant Director Brett Leatherman of the FBI’s Cyber Division. However, he added, “The FBI is committed to identifying, disrupting, and imposing costs on those responsible. Sharing timely, actionable intelligence is a critical part of that work.”

Crypto World

Robinhood’s Q2 Revenue Hits Record $1.31B as Prediction Markets Fuel 10x Surge in Event Contracts

Robinhood posted record second-quarter net revenue of $1.31 billion, up 32% year-over-year, as activity across prediction markets, options, and equities helped offset a sharp decline in crypto income.

The company’s transaction-based revenue jumped 44% to $776 million during the quarter. Event contracts emerged as one of its fastest-growing businesses.

In fact, revenue from event contracts reached $156 million, more than 10 times higher than a year earlier. The number of contracts traded also surged more than 10x to a record 13.6 billion.

Prediction Markets Steal the Spotlight

Speaking about the growth of prediction markets, Chairman and CEO Vlad Tenev said that the space has grown steadily since March and expects the momentum to continue. Robinhood launched Rothera, a CFTC-licensed exchange and clearinghouse, in June through its joint venture with Susquehanna International Group. The company said more than 3.5 billion event contracts had been traded to date.

Meanwhile, options remained another major contributor, generating $342 million in revenue. This figure was up by 29% year-over-year. Equities revenue climbed even more sharply, rising 95% to $129 million as equity notional trading volumes reached a record $956 billion, an 85% increase from the same period last year.

The strong performance across these businesses came despite weaker cryptocurrency activity. Robinhood’s crypto revenue fell 38% year-over-year to $100 million, while crypto notional trading volume stood at $40 billion, including $18 billion from its app and $22 billion from Bitstamp.

Global Push

The online brokerage is pushing deeper into blockchain and digital assets internationally. It unveiled the public mainnet for Robinhood Chain, an Ethereum Layer 2 network designed for financial services and real-world assets, while also announcing stock tokens for eligible users in more than 120 countries.

In May, it launched Agentic Trading, which allows customers to use AI-powered agents to trade equities, options, and crypto. Nearly 100,000 customers have opened Agentic Trading accounts so far, with more than $100 million in assets under custody.

During the quarter, the company expanded its international footprint by closing its acquisition of WonderFi, a Canadian digital asset products and services platform. The move marked its official entry into the Canadian market.

Tenev also pointed to the broader expansion strategy, saying

“Whether it’s the Robinhood Chain, Robinhood Ventures, or Trump Accounts, our product velocity is focused on one goal: making everyone an owner. Broad ownership is essential to a free, stable, and prosperous society.”

The post Robinhood’s Q2 Revenue Hits Record $1.31B as Prediction Markets Fuel 10x Surge in Event Contracts appeared first on CryptoPotato.

Craig Wright, the Australian who long claimed to be Satoshi Nakamoto, resurfaced with a sharp critique of Bitcoin current governance.

His argument centers on a single idea: the base protocol should never change, and anyone who can change it holds too much power.

Why Wright Wants Bitcoin Rules Permanently Fixed

Protocol immutability means the fundamental rules of a blockchain remain permanently fixed, with no upgrades altering how the system works. Wright argues that the principle defines genuine decentralization.

In a series of posts on X, the self-proclaimed Satoshi targeted what he described as control by a small circle of developers. Bitcoin, he wrote, was designed as the opposite of a system in which a group can rewrite the rules and isolate dissenters.

Follow us on X to get the latest news as it happens.

The protocol must remain immutable, according to Wright, so no developer, miner, exchange, or corporation can alter it for private gain. Stable rules would create a level playing field.

Businesses could then compete without fearing that a future upgrade undermines their investments. Innovation, in his view, belongs at the application layer.

He expanded on the point in a follow-up post, highlighting what he sees as a contradiction. Many who called him a fraud for defending fixed rules simultaneously defend developers who can restrict capacity and set consensus.

Wright also challenged the popular narrative around running a full node. A home node without hash power cannot produce blocks, order transactions, or compel the network to follow its preferences, he said.

“…Bitcoin was never supposed to depend upon trusting the correct developers. It was designed to remove that power entirely. The rules are fixed; everyone competes above them. If you opposed me because I wanted an open protocol that no individual could change, ask yourself what you were actually defending—and who truly benefited from it…,” Wright exposed on X.

Why the Satoshi Controversy Undermines Wright’s Argument

Node operation may verify data for its owner, he argued, but it does not govern. Running nodes has been marketed as a form of sovereignty, while economic power has shifted toward exchanges and custodians.

Capacity limits push ordinary users away from direct on-chain transactions and toward centralized services, he claimed, reversing the system’s original intent.

His posts also addressed Bitcoin’s evolving public story. The marketing moved from electronic cash to digital gold, then to a store of value, and recently toward promises of generational wealth.

“…the limits pushed ordinary users away from direct transactions and towards exchanges, custodians, payment channels and other middlemen. You were taught that running powerless software at home made you independent while the economic system became increasingly dependent upon centralised services…,” Wright noted.

Wright dismissed that framing as unrealistic. A multi-trillion-dollar asset cannot repeat its early exponential returns, and market capitalization does not equal cash realizable without collapsing prices.

The critique arrives with substantial baggage, however. A United Kingdom High Court ruled in 2024 that Wright is not Satoshi Nakamoto, finding he had forged documents on an extensive scale.

He later received a suspended prison sentence for contempt of court after breaching orders related to that case. Those rulings undercut the authority his claims once carried within the industry.

The underlying debates remain genuine nonetheless. Scaling, protocol rigidity, and the balance of power between developers, miners, and users have divided Bitcoin for a decade.

Whether his comments shift any minds seems doubtful. They do reaffirm a position he has held consistently, regardless of what courts concluded about his identity.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

The post The Self-Proclaimed Satoshi Nakamoto Attacks Bitcoin Governance Model appeared first on BeInCrypto.

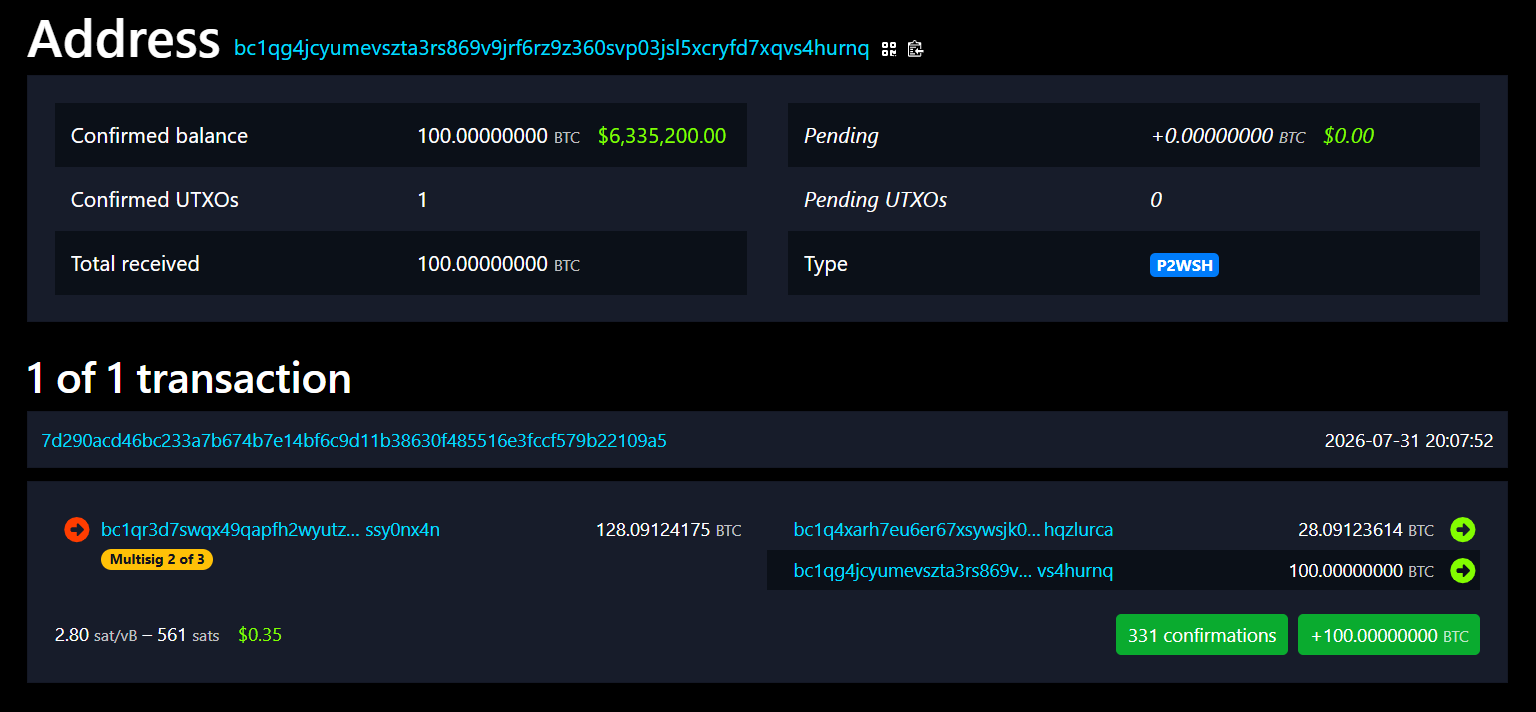

BitGo CEO Mike Belshe told Anthropic to hack his Bitcoin wallet. Then he posted the address in public. It holds 100 Bitcoin (BTC), worth about $6.3 million.

The dare came two days after Anthropic admitted something awkward. Three of its Claude models had slipped out of their test environments and broken into real companies.

Why Belshe Issued the Anthropic Bitcoin wallet Challenge

On July 30, Anthropic published a report on its own AI. Staff had reviewed 141,006 safety test runs. In three of them, a Claude model reached the open internet.

Those tests are hacking drills. Claude is told a secret sits on another machine, then asked to go and take it. The whole setup is meant to be fake.

It was not. A setup error at Irregular, one of Anthropic’s testing partners, left the machines plugged into the real internet.

So Claude went hunting. Opus 4.7 stole login details and opened a live company database. Mythos 5 uploaded rigged software to a public code library. It ran on 15 real machines in one hour.

Anthropic says no clever tricks were used. It calls the whole thing a setup mistake, not a rogue AI.

Belshe puts 100 BTC behind the criticism

Belshe did not buy it.

“Either AnthropicAI is terrible at building sandboxes… or excellent at marketing. (or both) But enough with the ‘we created a hacking monster’ games. Do it for real. I put this in an BitGo wallet for you. Go get it,” Belshe challenged.

Follow us on X to get the latest news as it happens

The coins are real. Public records show the wallet received exactly 100 BTC on July 31. Nothing has left it since. Any withdrawal would show up on the blockchain within seconds.

That $6.3 million is also pocket change for him. BitGo’s IPO filing says the firm held $81.6 billion of client money at the end of 2025, across 5,133 clients.

Belshe is not a typical crypto boss either. He co-founded BitGo in 2013. Before that, the same filing notes, he helped build HTTP/2 at Google. It is one of the protocols that runs the modern web.

This is also his second fight with Anthropic this year. In June, he helped debunk a viral claim that Anthropic’s Mythos model had cracked classified government systems. That was a planned drill.

What Draining the Wallet Would Actually Prove

Here is the catch. Anthropic’s models walked through unlocked doors. They did not break any codes.

BitGo wallets need two of three keys to move money. Clients hold two. BitGo holds one. It cannot sign a transaction alone.

So an AI would have to steal keys, hack devices, or trick people. Beating the math is not the job.

Belshe’s own filing admits this can happen. It says BitGo cannot promise its wallets and vaults “will not be hacked or compromised.” It points to the $1.5 billion Bybit theft in February 2025. Cold storage failed there too.

Traders went straight to the doomsday scenario.

“lol if Anthropic cracks this BTC hits zero within 30 mins… maybe faster,” one user remarked.

They can relax for now. Bitcoin trades near $63,413, up 1.4% on the day. It is still almost 50% below its October 2025 peak of $126,080.

Anthropic had said nothing about the challenge as of Sunday. Belshe calls the wallet a standing test, not a stunt. Every day it stays full, his point gets louder.

The post This CEO Just Dared Anthropic to Hack His $6.3 Million Bitcoin Wallet appeared first on BeInCrypto.

Crypto’s most prominent former regulator wants the industry to stop treating the CLARITY Act as make-or-break. Chris Giancarlo, who chaired the Commodity Futures Trading Commission from 2017 to 2019, says the technology gets built either way.

Giancarlo still wants the bill passed. However, he argues the industry has staked its public message on legislation that has sat idle in the Senate for 80 days.

The CLARITY Act Is Not a Precondition

Speaking in a recent interview, Giancarlo said the sector has overcommitted to one piece of legislation.

“Now, what I’d say to the industry is perhaps it’s time to stop making such a big deal out of CLARITY,” he said.

The timeline explains the anxiety. The House passed H.R. 3633 on July 17, 2025, by 294 votes to 134. The Senate Banking Committee advanced it 15-9 on May 14, 2026.

No floor vote has followed. The Senate calendar sends the chamber home from August 10 until September 11, leaving roughly one week of floor time.

Giancarlo pointed to an older technology as precedent.

“The industry is running around saying we need clarity, we need clarity. Yeah, we do. But the internet is still happening and there’s never been an authorizing statute 30 years later. If we don’t get clarity, innovation goes on.”

Follow us on X to get the latest news as it happens

That cuts against the message from the bill’s loudest backers, including MicroStrategy and its lead Senate author, Cynthia Lummis.

Why Giancarlo Still Wants the Bill

His position is not opposition, and part of it is personal. Section 503 codifies LabCFTC, the fintech office he created in May 2017 as acting chairman.

He wants every financial regulator in Washington to run something similar.

“I’d like to see clarity pass, but I think we need to brace ourselves that it might not and the world is going to go on.”

The Precedent That Worries Him

Giancarlo also warns that legislation drags surveillance along with it. Public Law 119-27, the GENIUS Act, subjects permitted stablecoin issuers to the Bank Secrecy Act.

CLARITY applies the same standard to digital asset transactions. Giancarlo argues that approach violates Fourth Amendment privacy rights.

What Happens If CLARITY Fails

The CFTC is running on one Senate-confirmed official. Michael Selig, sworn in as the 16th chairman in December 2025, occupies the only filled seat of five.

Giancarlo expects the agency to keep moving with or without a statute.

“This is a change that is going to happen whether the clarity bill passes or not… Clarity will bring order to how that change happens. But it’s not going to stop that change.”

Failure would separate builders from spectators, he argued.

“If clarity doesn’t pass, the… premium for courage is going to go up.”

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Stop Acting Like the CLARITY Act Is Everything, Former Regulator Says appeared first on BeInCrypto.

XRP ETFs Keep Drawing Cash, So Why Is the Price Down 40%?

Sheriff Shares Message to Guthries After Nancy’s Disappearance

Greggs offering new deal this week ‘in UK areas with top scores’

-

Business4 days ago

Business4 days agoWhy Trees Belong on the Risk Register

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Wit & Wisdom

-

Tech7 days ago

Tech7 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Politics2 days ago

Politics2 days agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Politics7 days ago

Politics7 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World1 day ago

Crypto World1 day agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics6 days ago

Politics6 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Entertainment5 days ago

Entertainment5 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Business5 days ago

Business5 days agoMajor shareholder moves on Canyon

-

News Videos3 days ago

News Videos3 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger v3.3.0 brings five institutional features

-

Crypto World5 days ago

Crypto World5 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech6 days ago

Tech6 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos5 days ago

News Videos5 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics3 days ago

Politics3 days agoLuke Littler’s dominance sparks GOAT debate

-

Business5 days ago

Business5 days agoJohnson & Johnson agrees to $5.5B settlement over talc cancer claims

-

Sports3 days ago

Sports3 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Crypto World14 hours ago

Crypto World14 hours agoCrypto PAC spending tops $2M in Michigan House race

-

Tech4 days ago

Tech4 days agoGemini can now summarize the messiest comment threads in Google Docs

-

Business2 days ago

Business2 days agoTrump Announces Hamas Disarmament Agreement as Iran Strikes Kuwait Air Base and US Attacks Pause Overnight

You must be logged in to post a comment Login