Crypto World

Bitcoin (BTC) price drops to to 6-week low as U.S.-Iran strikes rattle global markets: Crypto Daily

Bitcoin fell below $73,000 to the lowest level since April 13 on Thursday as renewed fighting between the U.S. and Iran rattled global markets, pushing oil higher and dimming hopes for a permanent ceasefire.

The selloff followed U.S. strikes in southern Iran. Iran’s Revolutionary Guards said they retaliated by targeting the American base used to launch the attacks, warning future responses would be “more decisive,” the New York Times reported. Kuwait, which hosts five U.S. bases, said it intercepted hostile drones and missiles.

The escalation dimmed expectations that Washington and Tehran are close to an agreement that could stabilize the Strait of Hormuz, a key global oil shipping route.

Odds of a permanent ceasefire being reached by the end of the month are now just 8% on Polymarket, down from a 70% peak over the weekend. Perceived odds of it being reached by the end of next month slid to 42% from 76%.

On Kalshi, traders are betting traffic in the strait will remain subdued. Brent crude jumped nearly 4% to around $96 per barrel, fueling concerns that higher energy prices could add to inflation pressures worldwide.

Crypto markets reacted alongside broader risk assets. According to Mercado Bitcoin’s head of research, Rony Szuster, investors remain focused on geopolitical risks and upcoming U.S. inflation data, particularly Thursday’s PCE report, the Federal Reserve’s preferred inflation gauge.

“The crypto market remains structurally resilient, supported by long-term accumulation and the strength of AI and blockchain infrastructure narratives,” Szuster said in a note shared with CoinDesk.

“In the short term, the market remains more sensitive to geopolitical developments and the return of institutional flows after the U.S. holiday, keeping bitcoin in consolidation while altcoins trade in a more selective environment,” he added. Stay alert!

Read more: For analysis of today’s activity in altcoins and derivatives, see Crypto Markets Today . For a comprehensive list of events this week, see CoinDesk’s “Crypto Week Ahead.”

What’s trending

Today’s signal

- Bitcoin continues to trade below the 50-week exponential moving average of $84,000.

- The absence of RSI divergences on the weekly price chart indicate there’s no clear market direction.

- The next core level to monitor is the $68,000 support mark.

A preferred stock that was supposed to behave like a steady, high-yield bond fell to 82 cents on the dollar in a single session. The issuer says it was a leverage flush, not a credit problem. Either way, the new world of Bitcoin-backed “digital credit” just met its first stress test.

Summary

- STRC and SATA showed that Bitcoin-backed preferred stocks can trade violently under stress.

- Issuers blamed the selloff on forced deleveraging, not credit deterioration.

- The episode exposed thin liquidity, leverage, and Bitcoin volatility inside digital credit.

- High yields in these products compensate investors for risks that are now visible.

On June 18, 2026, a security that was designed to be boring did something deeply un-boring. STRC, the perpetual preferred stock issued by Michael Saylor’s company Strategy, the firm formerly known as MicroStrategy, fell to an intraday low of $82.50, far below the roughly $100 par value such an instrument is meant to trade near, before recovering to close around $88.59.

On the same day, a sister instrument called SATA, the preferred stock of a Bitcoin treasury company called Strive, tumbled from its $100 par into the low $90s. Strive’s chief executive, Matt Cole, called it “the most difficult day in the history of Digital Credit,” and was quick to insist that nothing was actually wrong.

No one had defaulted, no issuer’s fundamentals had deteriorated, and the damage was the result of a leverage-driven liquidation, a cascade of margin calls and forced selling, not a real credit event. Whether you believe that reassurance or not, something important happened: the new world of Bitcoin-backed “digital credit” met its first real stress test, and it wobbled.

This piece explains what STRC and SATA actually are and why they exist, what happened on that difficult Thursday and the leverage-liquidation explanation, why these instruments are more fragile than their steady-yield design suggests, what the episode reveals about the broader Bitcoin treasury model that Saylor pioneered and others have copied, and what it means for anyone watching this corner of the market.

The issuers’ reassurance may well be accurate, that this was a mechanical dislocation and not a sign of distress. But the episode is a window into a young, leveraged, thinly traded market built on top of Bitcoin’s volatility, and understanding its first stress test is understanding a risk that has been building quietly beneath the Bitcoin treasury boom.

What STRC and SATA actually are

To understand why the selloff matters, you have to understand these instruments, because they are a new kind of security and their design explains both their appeal and their fragility.

STRC and SATA are perpetual preferred stocks issued by Bitcoin treasury companies, and they sit at the intersection of two worlds: the steady, income-paying world of preferred equity and the volatile world of corporate Bitcoin accumulation. A perpetual preferred stock is a security that pays a fixed or variable dividend indefinitely, with no maturity date, and is meant to behave somewhat like a high-yield bond, trading near its par value and delivering a steady stream of income.

STRC, issued by Strategy, yields roughly 11.5% and pays dividends twice a month. SATA, issued by Strive, offers a variable yield of around 13% and pays dividends every business day, a remarkably frequent payout designed to make the instrument attractive to income-seeking investors.

Both are designed to trade near their $100 par and to throw off generous, regular income, which is why they appeal to investors hunting for yield.

Strategy has also moved STRC toward semi-monthly dividends, reinforcing the product’s pitch as a frequent-income instrument. The first record date for the new schedule is June 30.

The crucial detail is what backs them and what they fund. These preferred stocks are issued by companies whose core strategy is accumulating Bitcoin, and the capital raised by selling the preferred shares helps finance that Bitcoin accumulation.

This is corporate Bitcoin treasuries explained through a credit instrument rather than a normal stock filing. The company raises capital, links the balance sheet to Bitcoin, and then asks public-market investors to tolerate the volatility inside a familiar wrapper.

This is the model Strategy pioneered and that companies like Strive have adopted: raise money through instruments like preferred stock and convertible debt, use it to buy Bitcoin, and amplify Bitcoin exposure through this financial structure, what Strive’s leadership calls an “amplification” strategy. Strive, for instance, has built its structure around preferred equity as the primary form of this amplification, holding roughly 13,000 Bitcoin and maintaining a multi-month dividend reserve to ensure it can keep paying.

These instruments, in other words, are a way for Bitcoin treasury companies to raise capital from yield-seeking investors and channel it into Bitcoin, offering the investors a high income stream in exchange. They are the credit layer of the Bitcoin treasury world, a new market that links steady income products to volatile Bitcoin balance sheets, and that linkage is exactly where the fragility lives.

What happened on the difficult Thursday

The events of June 18 are worth walking through carefully, because the sequence reveals how a security meant to be stable can crater in a single session.

These instruments, which are supposed to trade near their $100 par, dropped sharply and suddenly. STRC fell to an intraday low of $82.50, a steep discount to par for an instrument designed to behave like a steady bond, before recovering to close near $88.59.

SATA fell from par into the low $90s, with one company executive noting it touched as low as $92.88 intraday before recovering toward $97.71. Both instruments, in other words, suffered sharp intraday plunges and then partially recovered, the kind of violent round trip that does not happen to a truly stable income security in normal conditions.

Selling came on heavy volume and cascaded through these thinly traded instruments, and it happened as the broader market was weak. Bitcoin itself slid around the same time toward roughly $62,900, and the United States was heading into a holiday weekend with no equity trading the following day.

Strive’s chief executive offered an explanation that same day, and it is important to take it seriously while also weighing it critically. Matt Cole attributed the plunge not to any deterioration in the creditworthiness of the issuers but to a leverage-driven liquidation.

In plain terms, some investors had bought these preferred shares using borrowed money, posting the shares as collateral, and when prices started to fall, those investors got margin calls. That forced them to sell, which pushed prices down further, triggering more margin calls in a cascade.

This is a mechanical dynamic, a leverage flush, not a fundamental one, and Cole stressed that the issuers’ balance sheets were intact, their dividend reserves full, and their ability to keep paying undisturbed. Strategy has also framed its reserve position as more than sufficient to support dividends over the long term.

Cole characterized the selloff as a temporary market dislocation, the most difficult day in the young history of digital credit, but not a sign of financial distress. The partial recovery of both instruments by the close lends some support to this reading, since a true credit event would not typically bounce back within the session.

The leverage-liquidation explanation is plausible and may well be correct. But as the next section argues, it is also not entirely reassuring.

Why these instruments are more fragile than they look

Here is the heart of the matter, because even if the leverage-liquidation explanation is accurate, the episode exposes a fragility built into these instruments that their steady-yield design obscures.

That reassurance, “it was just a leverage liquidation, not a credit problem,” is meant to calm investors, but it contains its own warning. Their ability to fall nearly 20% in a session on forced selling, regardless of the issuer’s fundamentals, is itself the risk.

An instrument designed to trade near par and behave like a steady bond should not be capable of a violent intraday plunge to $82.50. The fact that it is reveals that these securities are thinly traded and vulnerable to becoming magnets for exactly the kind of leverage that can flush them.

A market thin enough that a wave of margin-called selling can crater the price is a market where holders face real price risk even when nothing is wrong with the issuer. That is not the risk profile yield-seeking investors expect from a bond-like preferred.

That explanation, in other words, identifies the mechanism but does not eliminate the danger. It confirms that these instruments live in a market where mechanical forces can produce sudden, large losses.

A deeper fragility comes from what sits underneath these instruments: Bitcoin. These issuers are Bitcoin treasury companies whose balance sheets rise and fall with Bitcoin’s price, and although the preferred dividends are backed by reserves, the entire structure is ultimately tied to Bitcoin’s volatile value.

When Bitcoin falls, as it has substantially in 2026, the issuers’ balance sheets weaken, the broader sentiment around Bitcoin treasury strategies sours, and the appetite for their leveraged income instruments can fade. All of those pressures can hit the preferred shares at the same time.

This is the Bitcoin downturn behind the stress: a weaker Bitcoin market does not just affect the spot price, it tests every structure built on top of Bitcoin exposure.

They combine three sources of fragility at once: thin liquidity that amplifies any selling, leverage that can cascade into forced liquidations, and an underlying tie to Bitcoin’s volatility. A steady-yield preferred stock is supposed to be insulated from this kind of drama.

The design of STRC and SATA, perpetual preferreds throwing off generous regular income, presents them as stable, income-producing securities. The episode showed that beneath that steady surface lies a young, leveraged, Bitcoin-linked market that can move violently, and that is a fragility the high yields are, in part, compensation for.

What it reveals about the Bitcoin treasury model

The STRC and SATA episode is a window into something larger than two instruments: the Bitcoin treasury model itself, pioneered by Saylor’s Strategy and now widely copied, and the stresses building within it.

This model is, at its core, a leverage play on Bitcoin. Companies like Strategy raise capital through debt and preferred equity and use it to buy Bitcoin, amplifying their Bitcoin exposure so that the company’s value rises faster than Bitcoin when Bitcoin climbs.

Strategy’s goal has been to turn products like STRC into durable Bitcoin-backed credit instruments, not just temporary financing tools. That ambition is what makes the stress test matter: the market is now testing whether the instrument can behave like credit when Bitcoin behaves like Bitcoin.

The strategy made Strategy a market sensation during Bitcoin’s bull runs. Strategy now holds an enormous Bitcoin position, around 846,842 Bitcoin acquired at an average cost of roughly $75,656 per coin, which at a Bitcoin price near $62,500 represents a large unrealized loss, on the order of $11 billion.

That is the other side of leverage: it amplifies losses as well as gains. In 2026, with Bitcoin down sharply on the year, the amplification has been working in reverse, putting the model under a kind of pressure it did not face during the bull market.

The preferred instruments like STRC are part of how this leverage is financed, which is why stress in them is a signal about stress in the model.

The episode is best understood as the model meeting its first real test in a sustained Bitcoin downturn. During Bitcoin’s rises, the Bitcoin treasury strategy looked brilliant, and instruments like STRC and SATA could be issued readily to fund more Bitcoin buying, with investors happy to collect high yields backed by appreciating Bitcoin balance sheets.

A prolonged Bitcoin decline changes the picture: balance sheets show large unrealized losses, recent capital raises draw criticism as dilutive, sentiment sours, and the leveraged income instruments become vulnerable to exactly the kind of flush that hit them. This is also the macro pressure on leverage, because a hawkish rate environment makes every leveraged product harder to support.

Both companies insist their structures are conservatively leveraged or debt-light and their reserves intact, and that may be true, with Strategy and Strive both characterizing their balance sheets as sound. But the episode reveals that the whole edifice, the treasury companies and the digital-credit instruments built on top of them, is being tested by Bitcoin’s downturn in a way it never was during the boom.

The cracks in STRC and SATA are an early reading on how that test is going. The model worked beautifully on the way up; its behavior on the way down is now being discovered in real time.

The honest counterpoint

A fair account has to take the issuers’ reassurance seriously, because there is a real case that this episode was exactly what they say it was and not a sign of deeper trouble.

A bullish reading is that this was a real leverage flush, a mechanical dislocation in a thin market, and not a fundamental problem. On this view, the issuers’ balance sheets really are intact, their dividend reserves really are full, and their ability to keep paying really is undisturbed.

The sharp drop was a temporary technical event caused by overleveraged investors being forced out, not a judgment on the creditworthiness of Strategy or Strive. Partial recovery within the same session supports this, since a real credit deterioration would not typically bounce back so quickly.

The high yields these instruments pay, 11.5% on STRC and around 13% on SATA, are attractive precisely because they compensate for the volatility that episodes like this represent. Strive maintains a multi-month dividend reserve and has characterized its structure as built on long-duration preferred equity matched to the long-duration nature of Bitcoin.

That is an argument that the financing is sensibly structured, not recklessly leveraged. For an investor who believes in the Bitcoin treasury model and can tolerate volatility, a forced-selling dip might even look like an opportunity, not a warning.

A bearish reading does not dispute the mechanics but questions the comfort. Even granting that this was a leverage liquidation and not a credit event, the episode shows that these instruments can lose a fifth of their value in a session, that the market for them is thin enough to cascade, and that they are tied to a Bitcoin treasury model under real pressure from Bitcoin’s decline.

That reassurance, “nothing is fundamentally wrong,” sits uneasily next to the fact that a supposedly stable income security behaved like a volatile one. The worry is that in a young, leveraged, thinly traded market, the line between a mechanical flush and a fundamental problem can blur if Bitcoin keeps falling and the stress compounds.

Both readings have merit, and the honest position is that the issuers may be entirely right about this specific episode while the episode still reveals a fragility worth respecting. These instruments offer high yields for a reason, and that reason was on display on June 18, whatever the precise cause.

An investor should weigh the generous income against the proven capacity for sudden, sharp losses, and decide accordingly.

What it means for investors

For anyone watching or holding these instruments, or the Bitcoin treasury companies behind them, the episode offers concrete lessons regardless of which reading proves correct.

One lesson is that high-yield Bitcoin-linked preferred stocks are not the stable, bond-like income securities their design might suggest. Those generous yields, 11.5% and 13%, are compensation for real risks, including thin liquidity, leverage cascades, and an underlying tie to Bitcoin’s volatility.

An investor attracted by the income should understand that it comes with the proven possibility of sharp price drops. Treating these instruments as equivalent to a safe bond, because they are called preferred stock and pay steady dividends, misreads them.

They are a higher-risk, higher-yield instrument in a young and volatile market, and the June episode is the evidence. Anyone holding them for income should size the position to the reality that the price can move violently and that the market is thin, not to the comforting impression of a steady payout.

Another lesson is about the broader Bitcoin treasury exposure. The episode is a reminder that the Bitcoin treasury model is a leverage play that amplifies losses in a downturn as much as gains in a rally, and that the instruments financing it, and the companies issuing them, carry that amplified risk.

An investor exposed to this corner of the market, whether through the preferred instruments, the treasury companies’ shares, or the broader theme, should hold it understanding that it is leveraged Bitcoin exposure with extra layers of fragility, not a conservative income or equity position. That is why regulated Bitcoin exposure compared is important: a preferred stock tied to a Bitcoin treasury balance sheet is not the same risk as a spot ETF or a simple Bitcoin wrapper.

The broader product-design trend also matters. STRC and SATA are part of the same market impulse that produced another Bitcoin-financial-engineering product, but the risk profile is very different when leverage and dividend obligations sit inside the wrapper.

Watching Bitcoin’s price, the issuers’ balance sheets and dividend coverage, and the behavior of these instruments under stress gives a clearer read on the risk than the steady-yield marketing suggests. None of this is investment advice, and the issuers may be right that the specific episode was benign.

The prudent stance is to respect the fragility the episode revealed and to treat these instruments and the model behind them as the leveraged, volatile, Bitcoin-tied bets they fundamentally are.

A stress test, passed for now

STRC falling to $82.50 and SATA into the low $90s in a single session was, by the issuers’ account, a leverage flush rather than a credit event, and the partial recovery by the close lends that explanation real support.

The companies insist their balance sheets are intact, their reserves full, and their ability to pay undisturbed, and they may be entirely correct that this specific episode was a mechanical dislocation in a thin market and not a sign of distress. In that narrow sense, the Bitcoin dividend machine passed its first stress test: it shook, but it did not break.

But the episode revealed a fragility that the reassurance does not dissolve. Instruments designed to trade near par and behave like steady bonds showed they can lose nearly a fifth of their value in a session.

The market for them is thin enough to cascade under forced selling, and they sit on top of a Bitcoin treasury model now under real pressure from Bitcoin’s decline, with Strategy carrying billions in unrealized losses as leverage works in reverse. The high yields these instruments pay are compensation for exactly this kind of volatility, and June 18 was a vivid display of what that compensation is for.

An honest conclusion holds both truths at once: the issuers are probably right about this episode, and the episode still exposed a young, leveraged, Bitcoin-linked credit market that can move violently and that is being tested in a downturn for the first time. The machine kept running, but it was the first real test.

How it behaves through a sustained Bitcoin decline is a question now being answered in real time, one difficult Thursday at a time.

Frequently asked questions

What are STRC and SATA?

They are perpetual preferred stocks issued by Bitcoin treasury companies. STRC, issued by Michael Saylor’s Strategy, formerly MicroStrategy, yields roughly 11.5% and pays dividends twice a month. SATA, issued by Strive, offers a variable yield around 13% with daily dividend payments. Both are designed to trade near their $100 par and provide steady high income, and both help finance the issuers’ Bitcoin accumulation. They form a new “digital credit” layer linking income products to volatile Bitcoin balance sheets.

What happened to STRC and SATA on June 18, 2026?

Both fell sharply in a single session. STRC dropped to an intraday low of $82.50, well below its roughly $100 par, before recovering to about $88.59. SATA fell from par into the low $90s before partially recovering. Selling came on heavy volume and cascaded through these thinly traded instruments as Bitcoin slid toward roughly $62,900. Strive’s CEO called it “the most difficult day in the history of Digital Credit,” attributing it to forced selling, not a credit problem.

What does leverage liquidation, not a credit event, mean?

It means the plunge was caused by mechanical forced selling rather than any deterioration in the issuers’ creditworthiness. Some investors had bought the preferred shares with borrowed money, posting them as collateral; when prices fell, they got margin calls, forcing them to sell, which pushed prices down further and triggered more margin calls in a cascade. The issuers say their balance sheets and dividend reserves are intact. The partial same-session recovery supports this reading, since a true credit event would not typically bounce back so fast.

Why are these instruments considered fragile?

Even if June 18 was a leverage flush, the episode showed these instruments can lose nearly 20% in a session, which a truly stable bond-like security should not do. They combine three fragilities: thin liquidity that amplifies selling, leverage that can cascade into forced liquidations, and an underlying tie to Bitcoin’s volatility through the issuers’ balance sheets. The high yields they pay are compensation for exactly these risks, which their steady-income design tends to obscure.

What does this say about the Bitcoin treasury model?

The Bitcoin treasury model, pioneered by Strategy and copied by others, raises capital through debt and preferred equity to buy Bitcoin, amplifying exposure. That leverage amplifies losses as well as gains, and with Bitcoin down sharply in 2026, Strategy carries a large unrealized loss, around $11 billion on roughly 846,842 BTC bought near a $75,656 average. The STRC and SATA stress is an early sign of the whole model being tested in a sustained Bitcoin downturn for the first time, after looking brilliant during the boom.

Should investors treat these as safe income securities?

No. Despite being called preferred stock and paying steady dividends, they are higher-risk, higher-yield instruments in a young, leveraged, thinly traded market tied to Bitcoin’s volatility. The June episode showed they can drop sharply and suddenly. The 11.5% and 13% yields are compensation for that risk. Investors attracted by the income should size positions to the reality that prices can move violently, rather than to the impression of a stable payout. This is not investment advice.

As of June 21, 2026. Markets move quickly and figures change; verify current data before relying on this analysis. This article is information, not investment advice.

Dash is exploring the Philippines as a potential market for crypto payments, citing demand for lower-cost transactions and the country’s openness to digital finance tools.

In an interview with Cointelegraph at the Philippine Blockchain Week 2026, Daria Chernozub, global adoption lead at Dash Blockchain, said the project focuses on emerging markets where users face high fees and need simpler payment options.

“We believe that Dash brings the technology and the payment solutions for people who are suffering from high commissions [and] who need something easy to use,” Chernozub said, adding that the Philippines fits that profile because consumers are open to learning about new technologies.

She said Dash is still assessing the local market and prioritizing legal compliance before any launch. She said Dash had begun communicating with major market participants and had prepared a legal opinion letter for discussions with regulatory and financial industry bodies.

Dash’s assessment comes as the Philippines seeks to attract foreign technology companies, though industry participants say the regulatory process for crypto firms remains significantly more demanding than basic corporate registration.

Daria Chernozub (left) with Cointelegraph’s Ezra Reguerra (right) at the Philippine Blockchain Week. Source: Daria Chernozub

Corporate registration takes minutes, crypto compliance can take years

Philippine Securities and Exchange Commission Commissioner (SEC) Rogelio Quevedo told Cointelegraph during an interview at Philippine Blockchain Week 2026 that foreign investors can register a corporation online from anywhere in the world in about 20 to 30 minutes.

Quevedo said the government is ready to assist foreign investors and described the SEC’s online registration system as part of the agency’s broader push toward digitization and innovation. His comments suggest that formally setting up a local entity has become easier, though crypto companies may still face additional licensing and compliance requirements before operating.

Related: Dash Evolution chain integrates Zcash Orchard privacy pool

Marie Antonette Quiogue, BlockShoals’ head of legal and CEO of Arden Consult, said during a separate interview at the event that the SEC has created a framework for foreign crypto exchanges willing to enter a regulated environment.

Quiogue said the regulated path comes with significant obligations and cited the roughly two years BlockShoals spent developing its arrangement with Binance.

Beyond regulation, Quiogue pointed to the Philippines’ young population, high mobile usage and widespread English proficiency as factors that could attract overseas crypto companies.

Magazine: China’s 107 Bitcoin memory thief, Bithumb CEO booked: Asia Express

A Japanese corporate pension fund that serves roughly 1,200 small and medium-sized businesses plans to add cryptocurrency exposure to its portfolio starting fiscal year 2026, according to Nikkei. The proposal calls for allocating about 1% of the fund’s assets to crypto through a passive investment vehicle managed by a “major” hedge fund holding multiple crypto assets.

Nikkei reports the Nationwide Business Corporate Pension Fund oversees approximately 21.3 billion yen (around $130 million). CoinPost, in a separate report, said the pension fund is incorporating the allocation as part of its diversification effort, with a planned allocation split of 80% to yen, 15% to US dollars, and 5% to other currencies.

Key takeaways

- The Nationwide Business Corporate Pension Fund plans to dedicate roughly 1% of assets to cryptocurrency in fiscal year 2026.

- According to reports, the investment will be made via a passive fund managed by a hedge fund holding a basket of crypto assets.

- The move adds crypto exposure inside Japan’s more conservative institutional money pool, suggesting gradual mainstreaming.

- It comes as Japanese lawmakers advance legislation that would bring crypto assets under rules closer to those for traditional financial products.

- Investors should watch how the pension allocation is implemented, including whether it aligns with broader ETF and tax policy changes.

A cautious allocation inside Japan’s pension system

Crypto adoption among mainstream institutions typically proceeds in measured steps—especially in jurisdictions where pensions and other conservative vehicles are heavily regulated. In this case, the 1% target is small relative to the fund’s overall size, but the decision is significant because it places digital assets on the radar of an entity designed to meet long-term obligations for participating companies.

As described by Nikkei, the fund would not pick individual coins directly. Instead, it would use a passive fund managed by a hedge fund described as a “major” player, with holdings spanning multiple crypto assets. That structure could matter for implementation: passive vehicles can be easier to administer within institutional investment frameworks than bespoke strategies, even if underlying market exposure remains volatile.

CoinPost’s coverage, meanwhile, frames the decision as part of broader portfolio diversification rather than a standalone bet on crypto. With yen still projected to account for 80% of the fund’s exposure, the planned allocation suggests the pension fund is treating cryptocurrency as an incremental diversifier rather than a core allocation—at least for now.

Policy momentum: crypto moves closer to traditional market rules

The pension allocation aligns with a wider push in Japan to integrate digital assets more firmly into the country’s regulated financial ecosystem. On June 11, Japan’s House of Representatives passed legislation that would bring crypto assets under the Financial Instruments and Exchange Act, as coverage discussed by Cointelegraph noted. Under the proposal, crypto would fall under rules more closely aligned with those applied to conventional financial products.

The legislation is expected to move to the House of Councillors. If approved, it could open a pathway for crypto exchange-traded funds, while also strengthening the case for reforms that would lower the tax rate applied to digital-asset gains. The draft framework referenced in coverage includes a potential shift toward a 20% flat tax on gains from the current maximum rate of 55%.

For institutional investors, regulatory proximity can be as important as performance. When crypto assets sit outside the same legal and compliance environment as other financial products, long-term allocation decisions become harder—particularly for entities with strict governance and oversight requirements. A framework under the Financial Instruments and Exchange Act may reduce friction and help pension administrators justify allocations and risk controls.

Broader institutional access: experiments in retail and yield

Beyond pensions, Japan has seen other efforts aimed at making crypto exposure more accessible to investors in ways that fit established financial channels. Earlier this year, SBI Shinsei Bank began testing a deposit-linked rewards program that offers vouchers redeemable for Bitcoin, Ether, or XRP. The bank reportedly planned a permanent launch in autumn, highlighting a trend toward bundling crypto access with mainstream banking products.

In parallel, Metaplanet—described as Japan’s largest publicly listed Bitcoin holder—took steps to expand its financial toolkit. On June 12, Metaplanet agreed to acquire Siiibo Securities for 2.1 billion yen. The company said the deal would support the development and distribution of Bitcoin-linked yield products through a newly formed securities arm.

Together, these moves point to a gradual shift: crypto is no longer only an exchange and custody story. It’s increasingly being packaged into products and structures that resemble traditional finance—whether through rewards programs, yield-linked instruments, or, in this case, pension allocations.

What to watch next for pension-linked crypto

While the pension fund’s planned 1% allocation is modest, it could set an example for other conservative institutions if the implementation is smooth and governance concerns are addressed. The critical details investors will want to understand as fiscal year 2026 approaches include how the passive crypto fund is selected, what risk management and rebalancing policies apply, and whether the pension’s approach harmonizes with the evolving regulatory path in Japan.

More broadly, readers should monitor whether the legislation currently advancing through Japan’s political process translates into practical market infrastructure—such as regulated products that institutions can more easily deploy within their existing compliance frameworks.

Ethereum co-founder Joseph Lubin defended Vitalik Buterin after some community members questioned Buterin’s decision to write a science-fiction novel focused on decentralized governance.

Summary

- Joseph Lubin called Vitalik Buterin Ethereum’s key steward while defending his governance fiction project publicly.

- Crypto.news earlier reported Buterin paused regular essays to write science fiction about decentralized governance online.

- The debate comes as Ethereum faces price pressure and renewed questions over Foundation direction online.

Lubin called Buterin “an enormously effective communicator” and described him as “the most important contributor to and steward of the Ethereum ecosystem.” His comments came after online debate over whether the writing project helps Ethereum at a time when users are focused on price weakness, privacy and the Ethereum Foundation’s direction.

Lubin says fiction can serve Ethereum

Lubin argued that critics are missing the point if they think Buterin is stepping away from Ethereum by writing fiction. In his view, fiction can explain Ethereum’s values in a way that technical posts may not reach.

“Anyone who thinks that by writing fiction Vitalik isn’t choosing the most effective way he can think of to further the growth and adoption of Ethereum is missing the point,” Lubin wrote on X.

He suggested that Buterin could write a cypherpunk story showing how people move through a dark digital future while using Ethereum-related technology. Lubin compared the idea to works such as Cory Doctorow’s Little Brother series.

The post also tied Buterin’s writing to themes that already sit close to Ethereum’s culture, including open source, privacy, censorship resistance and credible neutrality.

Buterin’s novel focuses on governance

As previously reported by crypto.news, Buterin said in May that he would pause regular long-form blog posts and try writing science fiction about decentralized governance. He had already finished the first two chapters and posted them on his personal website.

The draft explores governance in a fictional setting rather than through a normal research essay. Reports said the story deals with topics such as quadratic voting, artificial intelligence-assisted decision-making and the limits of decentralized autonomous organizations.

The shift drew mixed reactions because Buterin’s technical essays have often guided public debate around Ethereum. Some users questioned the timing, while others said the novel could make complex governance ideas easier to understand.

A user posting as 12 said the early chapters already touch on open source and privacy. The user also pointed to the “Veridian Privacy Robe” and suggested the phrase “HOOD UP = Privacy” as a community signal.

Privacy themes gain attention

Privacy has become a recurring topic in Ethereum discussions. As crypto.news reported last year, Ethereum builders were working on privacy tools ahead of the network’s 10-year anniversary, and that Buterin had urged developers to focus on private money, private identity, private voting and private messaging.

That context helps explain why some community members see Buterin’s fiction as more than a side project. A story can test social and political ideas without proposing immediate protocol changes.

Lubin also framed Ethereum as a platform built around neutral settlement, open source work and censorship resistance. His defense suggests that he sees Buterin’s writing as part of Ethereum’s wider communication strategy.

The debate is likely to continue while ETH price action remains weak and users ask for clearer progress. For now, Buterin’s novel has moved Ethereum’s governance and privacy debate into a new format, while Lubin has publicly backed that choice. The project does not change Ethereum’s technical roadmap, but it has made Buterin’s public role a fresh topic for debate.

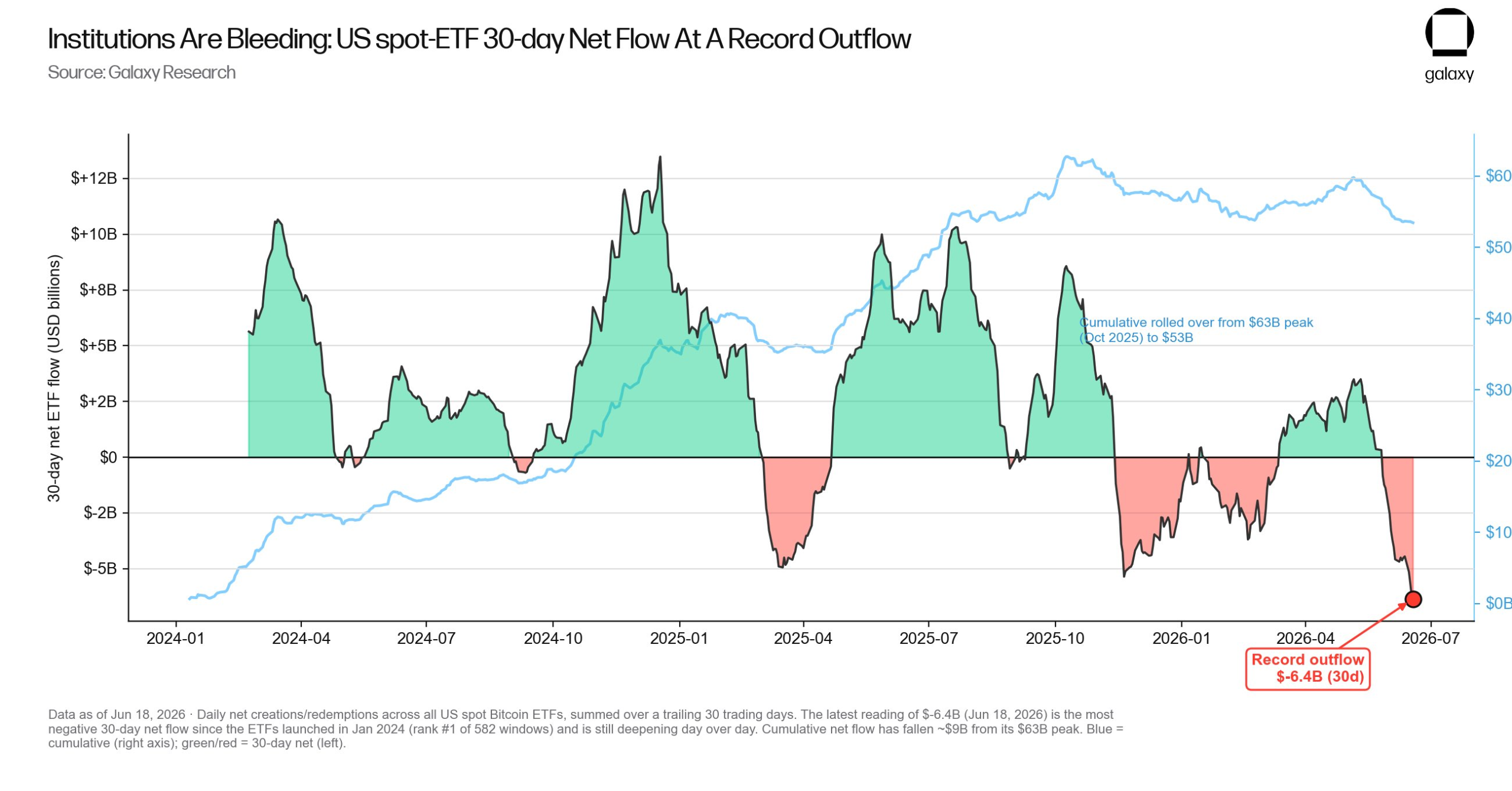

US spot Bitcoin ETFs (exchange-traded funds) posted their largest 30-day net outflow on record. These Bitcoin ETF outflows reached $6.35 billion as institutional investors cut exposure, according to Galaxy Research.

The redemption marks six straight weeks of withdrawals from the funds. Still, the pace has slowed sharply in recent days. That hints that the most intense phase of institutional selling may be passing.

Record Bitcoin ETF Outflow Tops 582 Windows

Galaxy Research said the $6.35 billion drain ranks first across all 582 rolling 30-day windows it tracks. The analysis arm of Galaxy Digital called it the heaviest stretch since the funds launched in January 2024.

“Bitcoin ETFs set record 30d net outflow at -$6.35 billion over last 30 days (#1 across all 582 30d windows),” they wrote.

The selling has been uneven across the complex. BlackRock’s IBIT has still pulled in $62.1 billion since launch, while Grayscale’s higher-fee GBTC has shed $27 billion.

Together, the funds hold net inflows of $53.4 billion, Farside Investors data shows.

The drawdown tracked a falling market. Bitcoin (BTC) has dropped about 17% over the past month. The token’s spot price near $64,260 sits roughly 49% below the record $126,080 reached on October 6, 2025.

Why Institutions Pulled Back From Bitcoin

Several forces drove the deepening ETF drain. Higher Treasury yields and fading hopes for rate cuts pushed money toward lower-risk assets.

Renewed geopolitical tension and a broad risk-off mood deepened the retreat.

Part of the bleed is structural, not fresh panic. GBTC has been leaking money for months because it charges 1.5% compared to IBIT’s 0.25%.

Other consecutive daily outflows reflected profit-taking and capital leaving Bitcoin for rival assets.

BlackRock’s IBIT still drives the daily swings. On June 18, its $96.7 million redemption outweighed the combined rest of the complex.

Investors had trimmed exposure ahead of the Fed’s interest rate decisions.

Outflows Cool as the Selling Slows

The bleeding has eased in recent sessions. Weekly outflows fell 87% from their early-June peak. They dropped from $1.72 billion in the week ending June 5 to about $226 million last week, according to Farside Investors data.

Bitcoin has held near $64,000 throughout the slowdown. The resilience suggests that long-term holders absorbed much of the supply released by ETF managers.

The sharp drop in weekly redemptions suggests the peak of selling has passed.

Still, outflows remain net negative, and only a swing back to inflows would confirm a bottom.

The post Bitcoin ETF Outflows Hit Record $6.35 Billion: Has Selling Peaked? appeared first on BeInCrypto.

MainStreet Finance-linked MSUSD traded far below its intended dollar peg after a rapid sell-off tied to reserve-verification concerns.

Summary

- MSUSD traded near $0.378 on CoinGecko after falling far below its intended dollar peg.

- PeckShield said the Morpho msY/USDC market reached 100% utilization as liquidity concerns spread quickly online.

- MainStreet said assets remain fully backed, citing a third-party proof-of-reserves dashboard shutdown as cause publicly.

Main Street USD traded at $0.3781 at the time of writing, with a 24-hour range between $0.065 and $0.9995.

The move followed Accountable’s decision to end its service agreement with MainStreet. The verification firm said MainStreet was “unable to meet our verification standards,” while MainStreet said the issue came from the shutdown of a third-party proof-of-reserves dashboard.

MSUSD trades far below its peg

MSUSD had been designed to trade near $1, but the token fell sharply after confidence in its reserve verification weakened. PeckShield said the MainStreet-related token dropped as much as 85%, while CoinGecko data later showed a partial rebound from the day’s low.

CoinGecko listed MSUSD with a market cap of about $27.06 million and 24-hour trading volume near $8.25 million. The token’s wide daily range showed unstable trading as holders tested liquidity and redemption confidence.

Morpho market reaches 100% utilization

The pressure also reached Morpho. According to PeckShield, the msY/USDC market hit 100% utilization, meaning available lending liquidity had been fully used.

AlphaUSDC Delta V2, curated by AlphaPING, reportedly had about 30% exposure to the market, equal to roughly $18 million. That exposure drew attention because stress in one yield-linked market can affect lenders, vault depositors and borrowers using related positions.

In lending markets, full utilization can make withdrawals harder and push borrowing rates higher. It can also leave users waiting for repayments or new deposits before liquidity normalizes.

The issue does not prove that all related positions are impaired. It does show that a stablecoin depeg can quickly move from a token price problem into a wider DeFi liquidity problem.

Accountable exit drives reserve concerns

Accountable said it terminated the MainStreet service agreement immediately after the protocol failed to meet its standards. The statement removed a public verification layer that users had relied on to assess backing.

MainStreet responded by saying that “Mainstreet remains fully backed.” The protocol also said the dashboard shutdown “does not reflect any loss of assets or deterioration in portfolio quality.”

MainStreet said it had deployed more than $8 million in USDC to support liquidity. It also said it was seeking alternative proof-of-reserves providers.

The two statements leave users with competing public claims. Accountable said the protocol failed verification standards, while MainStreet said the assets remain backed and the problem sits with the verification feed.

Stablecoin risks return to focus

The MSUSD case adds to a broader debate around yield-bearing stablecoins and proof-of-reserves tools. Crypto.news recently explained that a stablecoin’s reliability depends on the quality and transparency of the assets backing it.

The case also echoes earlier DeFi stress events where stablecoin-linked assets lost their peg and affected connected lending markets. Crypto.news previously reported on Resolv Labs’ USR depeg and exploit losses, noting how composable stablecoins can spread risk across protocols.

For now, MSUSD’s recovery depends on whether MainStreet can restore trust in its backing, keep liquidity available and replace the verification layer. Until then, traders are likely to watch the peg, Morpho utilization and any new proof-of-reserves update. Users may also watch whether liquidity support narrows the gap between MSUSD’s market price and its intended $1 value.

A $1.5 trillion asset manager just filed to take the most boring mechanism in investing, the dividend reinvestment plan, and quietly point it at Bitcoin. The filing made no headlines. It may be one of the most structurally interesting crypto products yet proposed.

Summary

- Franklin Templeton filed two ETFs that would reinvest stock dividends into Bitcoin.

- The structure turns a traditional DRIP into an automatic Bitcoin accumulation engine.

- These are equity funds with a Bitcoin feature, not pure Bitcoin funds.

- The idea matters more as product design than as an immediate source of Bitcoin demand.

On June 18, 2026, Franklin Templeton, a roughly $1.5 trillion asset manager that has been in business since 1947, filed paperwork with the Securities and Exchange Commission for two new exchange-traded funds. There were no press conferences, no celebrity fund-manager threads, no countdown clocks on financial television.

The firm simply submitted two registration statements and went about its day. But what those filings describe is one of the more structurally interesting financial products proposed in years, because they take the single most boring, set-it-and-forget-it mechanism in all of investing, the dividend reinvestment plan, and quietly repurpose it to accumulate Bitcoin.

Franklin Templeton is calling them “Bitcoin DRIP” funds, and the idea is strange enough, and clever enough, to be worth understanding in full.

This piece explains what Franklin Templeton actually filed and how the Bitcoin DRIP structure works, why taking the familiar dividend-reinvestment mechanism and pointing it at Bitcoin is a truly novel idea, how this fits into the broader explosion of crypto ETF innovation happening in 2026, what it would mean for ordinary investors and for Bitcoin itself, and the real risks and open questions the filing leaves unanswered.

The funds are not approved yet, tickers and fees are still blank, and they may never launch in their proposed form. But the design points at something larger than two funds: a shift in how Wall Street is packaging Bitcoin, from simple price exposure to structured products that engineer crypto into the machinery of conventional investing.

Understanding the Bitcoin DRIP idea is understanding where the ETF wave is heading next.

What Franklin Templeton actually filed

The mechanics are the heart of the story, so it is worth laying them out precisely, because the cleverness is in exactly how the structure works.

Franklin Templeton filed for two funds, the Franklin US Equity Bitcoin DRIP Index ETF and the Franklin US Innovation Bitcoin DRIP Index ETF, both tracking proprietary indexes built by an index provider called VettaFi. The first tracks a broad large-cap US equity index, and the second a US innovation-and-growth index, so the two differ mainly in which basket of American stocks they hold.

Each fund begins with the same allocation: 95% in US equities and 5% in Bitcoin exposure. That starting point alone is unremarkable, a stock portfolio with a small Bitcoin sleeve.

The novel part is what happens to the dividends. The stocks in the equity portion pay dividends, as dividend-paying stocks do, and instead of reinvesting those dividends back into the same stocks, as a normal dividend reinvestment plan would, the fund automatically routes every dividend into buying more Bitcoin.

Those mechanics are specific. All regular and special dividends from the equity holdings are reinvested into Bitcoin at the market open on the day after each dividend’s ex-date, which steadily increases the fund’s Bitcoin exposure over time.

It gains its Bitcoin exposure through Bitcoin-related instruments, including Bitcoin exchange-traded products, futures, and similar vehicles, and it can hold some of that exposure through a subsidiary structured for the purpose. That is where the three ETF types this builds on matter: spot products, futures products, and income or structured ETF designs are now being recombined into new wrappers.

To keep Bitcoin as a secondary allocation instead of letting it grow without limit, the underlying index caps overall Bitcoin exposure at 20% and applies a smaller cap at each quarterly rebalance. So the design is a stock portfolio that quietly converts its entire dividend stream into a programmatic Bitcoin accumulation engine, starting at a 5% Bitcoin weight and compounding that weight upward over time as dividends flow in, capped at 20%.

The preliminary prospectus is dated June 18, tickers and fees are still blank, the funds cannot be sold until the registration becomes effective, and the earliest possible launch is around September 1, 2026.

Why this is a truly novel idea

The structure is worth pausing on, because it is not just another way to package Bitcoin exposure; it repurposes a mechanism so familiar that its application to Bitcoin is quietly radical.

A dividend reinvestment plan, or DRIP, is one of the oldest and most boringly reliable tools in investing. For decades, ordinary investors have used DRIPs to automatically plow the dividends from their stocks back into buying more of those same stocks.

That compounds their positions over time without lifting a finger, the very picture of patient, conventional, set-it-and-forget-it wealth-building. A DRIP is the opposite of speculative; it is the slow, automatic compounding that has built retirement accounts since the 1960s.

What Franklin Templeton’s filing does is take that exact mechanism, the automatic, disciplined reinvestment of dividends, and redirect its output away from more stock and into Bitcoin. That dividend stream, historically one of the most conservative and predictable components of equity investing, becomes a programmatic Bitcoin-buying machine running on autopilot inside a regulated fund.

What makes this clever is the behavior it creates, not the exposure it provides. A spot Bitcoin ETF gives you a lump of Bitcoin price exposure that rises and falls with the market; you buy in once and your exposure is set.

The Bitcoin DRIP structure instead manufactures a recurring, automatic stream of Bitcoin accumulation funded entirely by equity dividends. Simply holding the fund means you are steadily, mechanically buying Bitcoin every quarter without making any decision to do so.

It is dollar-cost averaging into Bitcoin, except the dollars come from your stock dividends, not from your wallet, and the averaging happens automatically inside the wrapper. For an investor who wants Bitcoin exposure but distrusts their own ability to buy it consistently, or who likes the idea of keeping a core equity portfolio while siphoning its income into Bitcoin, the structure does something a plain spot ETF cannot.

It builds the accumulation discipline into the product itself. That is a fundamentally different idea from one-time price exposure, and it is what makes two quietly filed funds more interesting than their lack of fanfare suggested.

The bigger picture: the ETF innovation wave

The funds did not appear in isolation; they are part of a wave of crypto ETF innovation that defines 2026, and seeing that context explains why this filing matters beyond its own mechanics.

For most of Bitcoin’s ETF history, the story was simple: spot exposure. When the SEC approved spot Bitcoin ETFs in early 2024 after a decade of rejections, the funds attracted tens of billions of dollars, but they all did essentially the same thing: hold Bitcoin and track its price.

Competition was about fees and scale, with the largest funds dominating on size. That has changed.

After the SEC published generic listing standards for crypto-linked funds in late 2025, the floodgates opened, with industry analysts predicting more than 100 crypto ETFs could launch in 2026 and well over 100 filings already in the pipeline. Competition shifted from access to structure.

Issuers can no longer win simply by offering Bitcoin exposure, because everyone offers that. So they compete instead on how they engineer the exposure, on yield, on portfolio design, and on novel mechanisms.

This filing is one expression of this shift, and it sits alongside others that show the same pattern. A recent launch of covered-call Bitcoin income ETFs, which sell options against Bitcoin holdings to generate yield while capping upside, was another, taking Bitcoin’s volatility and engineering it into an income stream.

That is another structured Bitcoin product, and it shows the same direction of travel. Bitcoin is no longer just being listed; it is being sliced, capped, reinvested, hedged, and turned into portfolio machinery.

Franklin Templeton’s own broader push includes tokenizing traditional investment products and partnering with a major crypto exchange to offer a tokenized money-market fund as institutional collateral. The common thread: Bitcoin is being absorbed into the machinery of conventional finance, packaged and re-packaged into structured products that blend it with equities, with income strategies, and with the familiar tools of Wall Street.

The Bitcoin DRIP funds are not a one-off curiosity; they are a data point in a larger story about an industry that has moved past the question of whether Bitcoin belongs in a portfolio and on to the question of how cleverly it can be wrapped, structured, and sold. That is the context that makes a quietly filed pair of funds genuinely significant.

What it would mean for investors

For an ordinary investor, the Bitcoin DRIP structure offers a specific proposition, and understanding who it suits and who it does not is the practical question.

These funds target a particular kind of investor: someone who wants Bitcoin exposure but prefers to keep a conventional equity portfolio as their core, and who likes the idea of accumulating Bitcoin gradually and automatically instead of buying a lump of it directly. For that investor, the Bitcoin DRIP structure is appealing because it does not ask them to choose between stocks and Bitcoin or to time a Bitcoin purchase.

It lets them hold a familiar US equity portfolio while the dividends quietly build a growing Bitcoin position in the background. It is Bitcoin exposure for the equity investor who wants it on autopilot and as a secondary allocation, delivered through the same brokerage account and ETF wrapper they already use for everything else, which removes the wallet, the keys, and the crypto exchange entirely.

For someone intimidated by buying Bitcoin directly but comfortable owning an ETF, the structure is a familiar door into gradual Bitcoin accumulation. It is also another wrapper for crypto exposure, showing how crypto is increasingly delivered through forms investors already understand.

It also has clear limits on who it suits. An investor who wants full, direct exposure to Bitcoin’s price will find the Bitcoin DRIP funds a poor fit, because Bitcoin starts as only 5% of the fund and is capped at 20%.

That means the great majority of the fund’s performance comes from its stock holdings, not from Bitcoin. If your goal is to own Bitcoin’s price movement, a spot Bitcoin ETF or direct ownership gives you that cleanly, while a Bitcoin DRIP fund gives you mostly an equity portfolio with a slowly growing Bitcoin tilt.

These are equity funds with a Bitcoin accumulation feature, not Bitcoin funds. Confusing the two would lead to disappointment in either direction: an equity investor surprised by Bitcoin volatility, or a Bitcoin bull frustrated by muted Bitcoin exposure.

The structure suits the investor who wants the blend, a stock core with an automatic, capped, compounding Bitcoin sleeve. It is precisely wrong for anyone wanting concentrated Bitcoin exposure.

Knowing which you are is the whole decision.

What it would mean for Bitcoin

Beyond individual investors, the Bitcoin DRIP structure, if it succeeds and is copied, has an interesting implication for Bitcoin itself, and it is worth thinking through carefully without overstating it.

This structure creates a different kind of Bitcoin demand than a spot ETF does. A spot ETF generates demand through inflows and outflows: money comes in and the fund buys Bitcoin, money leaves and it sells, so the demand is lumpy and sentiment-driven.

The DRIP structure instead generates a recurring, mechanical stream of Bitcoin buying funded by equity dividends, which arrive on a regular schedule regardless of Bitcoin sentiment. As long as investors hold the funds and the underlying stocks pay dividends, the funds keep buying Bitcoin quarter after quarter.

This is a steadier, more automatic source of demand than sentiment-driven inflows, a programmatic bid that does not depend on anyone feeling bullish about Bitcoin in a given quarter. If such structures grow popular and proliferate, they could create a persistent, dividend-funded layer of Bitcoin demand that behaves differently from the volatile flows of spot products.

The honest caveat: this should not be overstated, because the scale is what matters and it is unproven. Two newly filed funds, starting at a 5% Bitcoin allocation, do not move Bitcoin’s price, and the demand they would generate is small relative to the market unless the structure is widely adopted and the assets grow large.

The significance lies in the model and its potential, not in the immediate impact. If dividend-funded Bitcoin accumulation becomes a popular structure across many large funds, the cumulative recurring demand could become meaningful, but that is a speculative if, not a present reality.

What the filing shows is a new mechanism for generating Bitcoin demand, one that is steadier and more automatic than existing products, and that mechanism is interesting for what it could become. But anyone tempted to read two quietly filed funds as a major new source of Bitcoin buying today is getting ahead of the facts.

The idea is the story; the impact is a question for the future and for adoption.

The risks and open questions

A clear-eyed look requires naming what the filing does not resolve, because the Bitcoin DRIP structure carries real risks and leaves important questions open.

One set of risks is structural and inherent to the design. Because the funds hold Bitcoin, they carry Bitcoin’s volatility, and although Bitcoin is a secondary allocation, a sharp Bitcoin decline still drags on the fund and exposes equity-focused investors to crypto risk they might not fully appreciate.

That matters especially given the Bitcoin backdrop, where Bitcoin has been under pressure even as other major assets have climbed. A product that quietly builds Bitcoin exposure can help disciplined accumulation, but it also quietly imports Bitcoin’s drawdowns.

Routing dividends into Bitcoin also raises tax questions. Routing dividends into Bitcoin purchases inside the fund structure has tax implications that the filing flags as potentially requiring adjustments, and the treatment of these reinvestments is not fully settled.

There is also the complexity of holding Bitcoin exposure through Bitcoin ETPs, futures, and a subsidiary, each layer adding cost and potential tracking imperfection between the fund and Bitcoin’s actual price. These are not fatal flaws, but they are real frictions that a simple spot ETF avoids, and they mean the Bitcoin DRIP structure is more complicated than its elegant concept suggests.

The larger open questions concern approval and adoption. These funds are not approved; tickers, fees, and listing details are still blank, and the SEC has not signed off, so the entire structure remains a proposal that could be changed or rejected.

Even if approved, the funds must attract assets to matter, and whether investors actually want a stock portfolio that converts dividends to Bitcoin is unproven, an untested proposition in the market. Fees, still undisclosed, will shape the funds’ appeal, since a structured product with high fees competes poorly against simply holding a cheap equity ETF and a cheap Bitcoin ETF separately.

And the broader question hangs over the whole crypto-ETF wave: with more than 100 funds potentially launching, many novel structures will fail to gain traction, and the Bitcoin DRIP funds could be a clever idea that simply does not find an audience. That is what makes the leveraged-Bitcoin product under stress relevant: clever Bitcoin-linked structures can still face real market pressure once investors test them.

Realistically, this is an interesting and original proposal whose success depends on approval, fees, and whether investors embrace the blend, none of which is settled. The cleverness of the design is real; its fate is entirely open.

A boring mechanism, pointed at Bitcoin

Franklin Templeton’s two Bitcoin DRIP funds arrived without fanfare, but they describe something more interesting than their quiet filing suggested: the repurposing of the dividend reinvestment plan, the most conventional, set-it-and-forget-it mechanism in investing, into an automatic engine for accumulating Bitcoin.

By holding a portfolio of US stocks and routing every dividend into Bitcoin purchases, the funds turn a conservative income stream into programmatic crypto accumulation, building a growing Bitcoin position on autopilot inside a familiar ETF wrapper. The idea is strange precisely because it weds the most boring tool in finance to the most volatile asset, and clever because it manufactures accumulation discipline that a plain spot ETF cannot.

This filing matters most as a sign of where the crypto ETF wave is heading. An era of simple spot exposure is giving way to one of structured products: covered-call income funds, dividend-to-Bitcoin engines, tokenized blends, as issuers compete on engineering rather than access, with more than 100 crypto ETFs potentially launching in 2026.

The DRIP structure is one expression of that shift, offering equity investors an automatic, capped, compounding Bitcoin sleeve and, if widely adopted, potentially creating a steadier, dividend-funded layer of Bitcoin demand that behaves differently from volatile spot flows.

None of that is settled: the funds are unapproved, their fees blank, their adoption unproven, and their real impact on Bitcoin speculative. But the idea is a genuine innovation, and it captures the moment crypto has reached, no longer fighting to be included in portfolios, but being quietly engineered into their machinery.

Wall Street took its most patient, conventional habit and pointed it at Bitcoin, and whatever becomes of these two funds, that gesture says a great deal about where things are going.

Frequently asked questions

What are Franklin Templeton’s Bitcoin DRIP ETFs?

They are two proposed exchange-traded funds, the Franklin US Equity Bitcoin DRIP Index ETF and the Franklin US Innovation Bitcoin DRIP Index ETF, filed with the SEC on June 18, 2026. Each holds a portfolio of US stocks starting at 95% equities and 5% Bitcoin exposure, and automatically reinvests all dividends from the stocks into buying more Bitcoin, increasing the Bitcoin allocation over time up to a 20% cap. “DRIP” refers to a dividend reinvestment plan, repurposed to accumulate Bitcoin rather than more stock.

How does the Bitcoin DRIP structure actually work?

The funds hold US equities that pay dividends. Instead of reinvesting those dividends back into the same stocks, as a traditional dividend reinvestment plan would, the funds route every regular and special dividend into Bitcoin purchases at the market open the day after each dividend’s ex-date. This steadily increases Bitcoin exposure over time, starting at 5% and compounding upward, capped at 20% of the fund, with a smaller cap applied at each quarterly rebalance. Bitcoin exposure comes through Bitcoin ETPs, futures, and a subsidiary.

Why is this considered a novel idea?

Because it repurposes the dividend reinvestment plan, one of the oldest, most conservative tools in investing, normally used to compound stock positions, and points its output at Bitcoin instead. Rather than giving a one-time lump of Bitcoin exposure like a spot ETF, it manufactures a recurring, automatic stream of Bitcoin accumulation funded by equity dividends. It is effectively dollar-cost averaging into Bitcoin, where the dollars come from your stock dividends and the buying happens automatically inside the fund, building accumulation discipline into the product.

Who are these funds for?

They suit investors who want a conventional US equity portfolio as their core but like the idea of accumulating Bitcoin gradually and automatically as a secondary allocation, delivered through a familiar ETF wrapper with no wallet or crypto exchange needed. They are a poor fit for anyone wanting full, direct Bitcoin price exposure, because Bitcoin starts at just 5% and is capped at 20%, so most of the fund’s performance comes from stocks. They are equity funds with a Bitcoin accumulation feature, not Bitcoin funds.

Could this affect Bitcoin’s price?

Potentially, if the structure is widely adopted, but not in its current small form. Unlike spot ETFs, whose demand is lumpy and sentiment-driven, the DRIP structure generates a recurring, mechanical stream of Bitcoin buying funded by dividends that arrive on schedule regardless of sentiment. If such funds proliferate and grow large, they could create a steadier, dividend-funded layer of persistent Bitcoin demand. But two newly filed funds at a 5% allocation do not move the market; the significance is in the model’s potential, not its immediate impact.

When could these funds launch?

The preliminary prospectus is dated June 18, 2026, with an effective date as early as September 1, 2026, but the funds cannot be sold until the SEC registration becomes effective, and approval is not guaranteed. Tickers, fees, and listing details were still blank in the filing. Even if approved, the funds’ success depends on their undisclosed fees and on whether investors actually embrace a stock portfolio that converts dividends to Bitcoin, both of which remain unproven.

As of June 21, 2026. This concerns an unapproved regulatory filing that may change or be rejected; verify the current status before relying on it. This article is information, not investment advice.

Ethereum has remained a mystery in terms of price movements on a macro scale, as it trades at essentially the same level as it did in March 2021.

Nevertheless, two of the most popular crypto analysts on X outlined a major breakout path forward that could take it toward its all-time high level. However, there’s still one major hurdle in its way.

Path to $4.6K

Ali Martinez outlined in a recent post that ETH stood at around $1,700 back in March 2021, as it does now. That means that a “$10,000 investment made five years ago would still be worth approximately $10,000 today.” The altcoin managed to chart a couple of all-time highs in the following years, but has returned to the same level, as it’s down by a whopping 65% since its last record seen in 2025.

“Despite five years of severe volatility, explosive bull runs, and deep bear-market liquidations, ETH has posted zero net gains from that baseline,” added Martinez.

Furthermore, he doubled down on previous predictions that ETH might not have bottomed during this cycle. Although he previously outlined $700 as a potential bottom for the asset, he now said that the $1,060 level stands out as a value zone to watch for such a level. If Ethereum manages to successfully defend that macro support, though, it opens the door for a short-to-mid-term rally to $2,850 or even $4,630, he added.

Time to Buy

Fellow analyst Michaël van de Poppe was even more bullish on the asset. Although he didn’t provide precise price targets, he noted that this might be “one of the best times to be buying ETH.” Moreover, he believes investors would wish they had bought more ETH in 5-10 years.

His comments were in response to another analyst, James Easton, who said that people tend to give up “right before the fun part,” and tagged Ethereum’s token.

I honestly stand by the fact that this is one of the best times to be buying $ETH.

In 5-10 years from now, you’ll be laughing back and say: Gosh, I should have bought more.

That’s always the asymmetry with those investments. At the moment: you don’t understand and feel whether… https://t.co/AvgWxg7DCO

— Michaël van de Poppe (@CryptoMichNL) June 20, 2026

The post Is Now the Ideal Time to Buy ETH? Analysts See a Path to $5K But There’s a Catch appeared first on CryptoPotato.

Bitcoin has continued to slide over the months since Strategy’s bitcoin-funding vehicle, Strategy’s preferred equity unit “Stretch” (STRC), launched in late July 2025. The move has put fresh scrutiny on how STRC’s structure is performing—and, more importantly, what happens when its market price drifts far below the $100 “liquidation preference” around which the instrument was designed to operate.

STRC has recently traded at a persistent discount. On Thursday, the unit reportedly fell to a record low of $82.53 and closed at $88.59—well below the $100 par level. That gap has reignited calls from prominent critics, even as other analysts argue the drawdown reflects leverage dynamics rather than a fundamental collapse.

Key takeaways

- STRC closed at $88.59 on Thursday after hitting a record low of $82.53, keeping the unit well below its $100 par level.

- Critics, including Peter Schiff, characterize STRC’s discount as evidence of a “centralized Ponzi,” though Strategy has not directly addressed those claims in recent statements.

- Some analysts say the selloff is better explained by a leverage wipeout and forced selling after STRC slipped under key thresholds.

- The discount and rising “effective yield” appear to have coincided with slower STRC-fueled bitcoin buying compared with earlier in 2026.

- Strategy adjusted STRC’s dividend schedule toward a semi-monthly cadence, a change observers say may affect funding expectations.

Why STRC trading below par matters

STRC was structured to trade close to its $100 par value, with adjustable dividends designed to attract capital and channel proceeds primarily toward buying Bitcoin. As long as the market price stays near that $100 level, the vehicle’s dividend mechanics and investor expectations remain aligned with Strategy’s bitcoin-accumulation plan.

But the recent widening discount changes the picture. The instrument’s drop below par implies that the “BTC buying channel” is under pressure—at least from a pricing and financing-efficiency standpoint—because the vehicle may need more market demand, better terms, or additional flexibility to keep fundraising smooth.

At an annualized dividend rate currently cited at 11.5%, multiple analysts note that a lower entry price boosts the effective yield to above 12.9% as STRC trades deeper into the discount. That higher yield can attract income-oriented buyers, yet critics argue that elevated yields can also mask underlying financing stress when the market price continues to drift.

Ponzi accusations vs. leverage-wipeout explanations

Bitcoin critic Peter Schiff has repeatedly described STRC as “a classic centralized Ponzi,” arguing that the model depends on Strategy’s ability to keep raising fresh capital through continued issuance or to sell Bitcoin in order to meet obligations. The concern, in Schiff’s framing, is that the structure cannot rely indefinitely on ongoing market confidence when the instrument’s price moves away from par.

Others have echoed the theme more directly by pointing to STRC’s behavior after it moved below par. Crypto trader DonAlt, for example, questioned why STRC was “trading like a Ponzi” after the sharp drop.

Strategy has not directly addressed these characterizations in recent commentary, continuing to present STRC as preferred equity backed by Strategy’s bitcoin-focused treasury strategy. Still, one tangible operational adjustment is worth noting: Strategy has shifted STRC to a semi-monthly dividend schedule, with payouts designed to occur twice a month rather than monthly. Earlier coverage from Cointelegraph described this dividend-vote and payout structure adjustment as part of how Strategy frames STRC’s mechanics in practice (see Cointelegraph report).

On the other side of the debate, analyst Jesse Myers, head of Bitcoin strategy at The Smarter Web Company, argued in a Thursday post that “Strategy is fine.” Myers’ claim is that STRC’s slide resembles a leverage wipeout more than a deterioration in Strategy’s core fundamentals. In his view, investors used heavy leverage while STRC hovered near the $99–$100 range, assuming it would remain above levels such as $95; once the price slipped, margin calls and forced selling accelerated the decline (Myers’ post on X).

Other income-market analysts have also pointed to how the dividend math works. Scott Melker, in a Sunday post, highlighted that STRC’s dividends are tied to the $100 liquidation preference rather than the instrument’s market price. In that framing, a buyer entering at $90 would earn roughly 12.8% at an 11.5% dividend rate, while a buyer entering at $85 could earn about 13.5%—a setup that can broaden the appeal of discounted “par-linked” products (Melker’s post on X).

Bitcoin accumulation slows as STRC funding efficiency weakens

As STRC trades below par, the timeline of Strategy’s bitcoin purchases suggests a slowdown in the pace of accumulation. Cointelegraph previously reported that Strategy added 1,550 BTC for $101 million in the week ending June 8, followed by another 1,587 BTC for $100 million in the week ending June 15, bringing total holdings to 846,842 BTC (Week ending June 8 and Week ending June 15).

Those amounts are meaningful, but Cointelegraph’s earlier reporting shows they are far smaller than Strategy’s earlier weekly buying pace during 2026. For example, in April, Strategy reportedly bought 34,164 BTC for $2.54 billion in a single week, and in May added 24,869 BTC for roughly $2.01 billion (April report and May report).

In June, the weekly additions appear closer to roughly $100 million rather than multi-billion weeks—matching the broader sense that STRC-led capital raising is becoming less efficient when the vehicle trades at a persistent discount.

Cointelegraph also noted a small BTC sale of 32 BTC earlier in June, worth about $2.5 million, to help cover dividend obligations. While the sale is tiny relative to Strategy’s overall treasury, it serves as a reminder that cash obligations can still force limited Bitcoin liquidation when the financing channel weakens.

The practical implication for investors is straightforward: when STRC is trading at a larger discount, the pipeline that supplies capital to buy more BTC can slow, and Strategy may need to rely more on other funding levers, operational flexibility, or direct sales to manage timing mismatches.

What to watch: dividends, issuance, and the next funding cycle

The widening discount has also been linked to a pause in at-the-market share issuance, according to the reporting. In business terms, Strategy’s “flywheel” depends on continuous reinforcement between capital raising and Bitcoin buying: proceeds help expand holdings, which supports the broader confidence narrative and (in turn) helps keep funding flowing. If STRC’s discount continues to widen, that flywheel may lose momentum.

Analysts suggest that STRC’s effective yield could keep attracting income investors as long as dividends remain connected to the $100 liquidation preference. That said, the market may still treat par-linked products differently once they trade persistently below par—especially if leverage traders unwind, margin calls accelerate selling, and new issuance becomes more difficult.

Strategy may announce its next dividend rate on June 30, while retaining other potential funding options, including MSTR share issuance and cash reserves, to support ongoing Bitcoin purchases. The key question is whether the semi-monthly dividend schedule and the next dividend decision help stabilize expectations—or whether the discount continues to force deleveraging.

For traders and long-term observers, the next catalysts are likely to be STRC’s dividend-rate guidance and the trajectory of the instrument’s discount to $100 par—because those two factors together may determine how quickly Strategy can regain a faster BTC accumulation pace.

Ripple is expanding its artificial intelligence focus as the XRP Ledger adds support for AI agent payments using XRP and Ripple USD.

Summary

- Ripple launched XRPL Starter Kit so agents can pay using XRP and RLUSD through x402.

- Crypto.news noted USDC still dominates x402 activity despite Ripple’s push into machine payments for now.

- Ripple’s GenAI role points to internal work on agentic systems, security controls and tooling platforms.