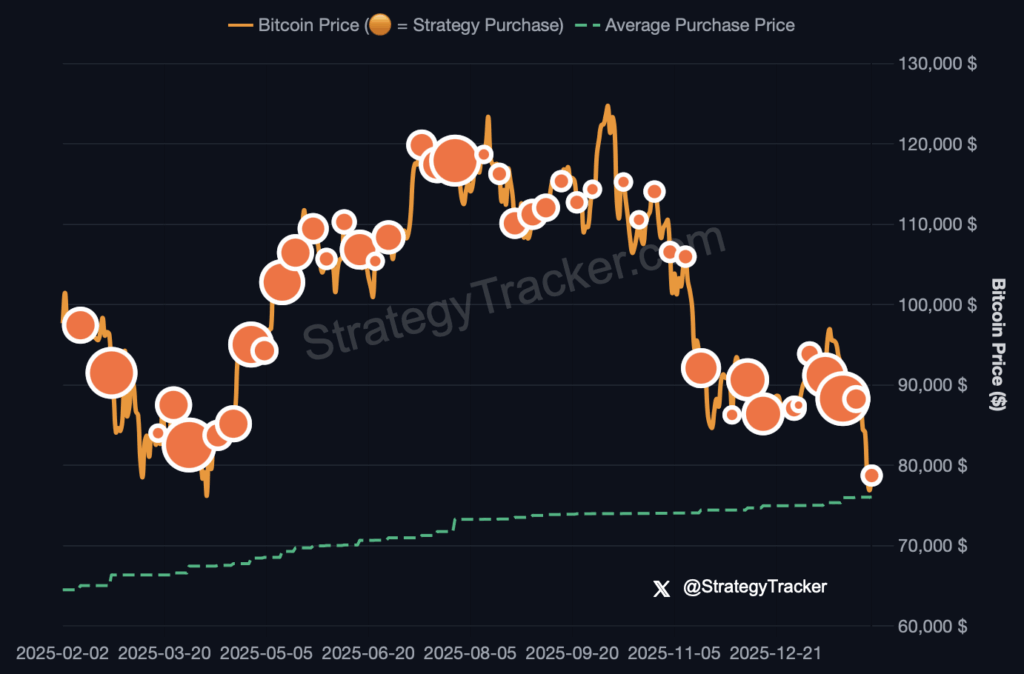

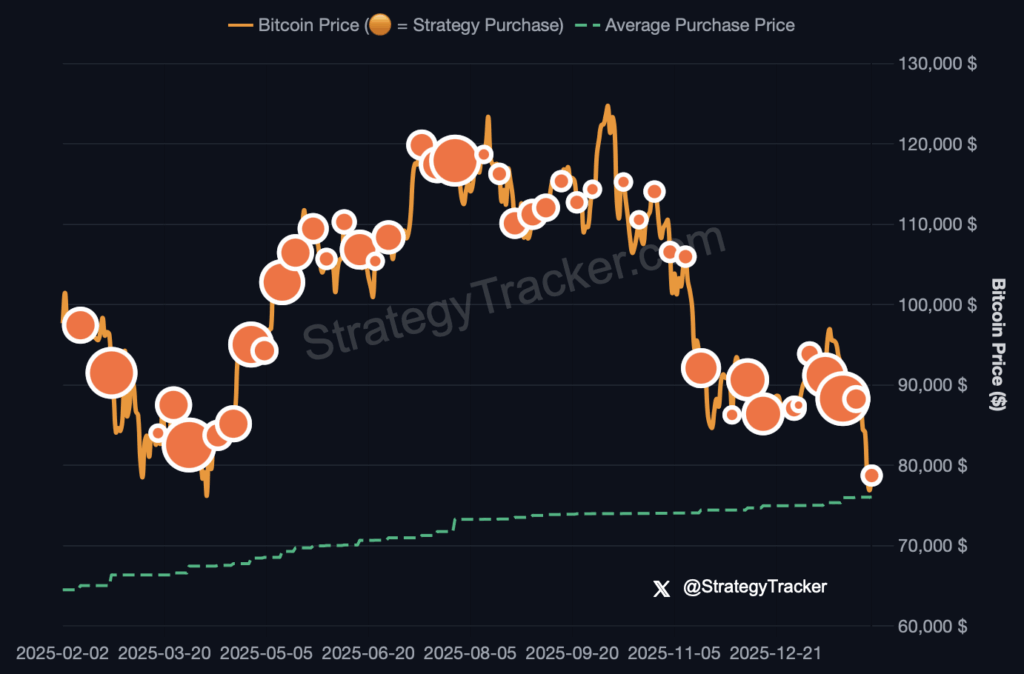

Overnight, bitcoin (BTC) fell to less than $74,600, well below Strategy’s average purchase price.

Since 2010, founder Michael Saylor has used corporate funds to buy 713,502 BTC at a lifetime average of $76,052. However, despite paying $54.2 billion for its so-called BTC treasury, this investment fell to below $53.3 billion.

Monday’s drop, along with similar price dips over the weekend, is the first time in two and a half years that Strategy’s cost basis has been higher than prevailing market prices for BTC.

The last time this happened was October 21, 2023 when the company’s BTC cost basis was $29,581 and BTC was trading at $29,483.

Advertisement

Ever since that date, Strategy has enjoyed owning BTC below its market value.

At his peak, Saylor seemed like a market wizard. On October 6, 2025, Strategy’s BTC holdings peaked above $79 billion and the company’s average buy of $73,982.73 was below the soaring BTC price above $126,000.

That 41% cushion has deflated entirely to less than zero as of last night.

Twelve-month Strategy BTC cost basis (green) versus price and purchases (orange). Source: StrategyTracker

Strategy’s buy price is not a liquidation threshold

Although significant, the price of BTC falling below Strategy’s cost basis won’t automatically trigger any liquidation.

Advertisement

The company has only $8 billion worth of debt — far below its $56 billion worth of BTC holdings. Moreover, the company’s debts don’t mature until 2028 at the earliest.

Still, millions of people saw the decline of BTC below Saylor’s average purchase price on social media. “Been buying BTC for 5+ years with nearly zero profit. Down even worse when adjusted for inflation,” someone reacted.

“If BTC keeps falling like this, MicroStrategy will really become a micro strategy,” wrote another, poking fun at Strategy’s prior business name which originally played on the dot-com name Microsoft.

Investors value Strategy almost entirely based on its BTC holdings. Specifically, relative to its $41 billion market capitalization, the company’s operational activities and legacy software generated less than $500 million in total revenue over its trailing 12-month period.

Advertisement

Over the next few years, Strategy simply needs to service operational expenses and small coupon payments to bondholders.

Its board of directors also voluntarily declares dividends to its preferred shareholders, which it can suspend at any time.

As of October 24, 2025, the company’s annualized dividend and interest expenses were $689 million.

The company’s dividend obligations could actually increase over time — especially if the price of its preferred shares decline.

Advertisement

Saylor just raised the dividend rate on STRC, for example, another 0.25% last week. What started as a 9% dividend rate has become 11.25%.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

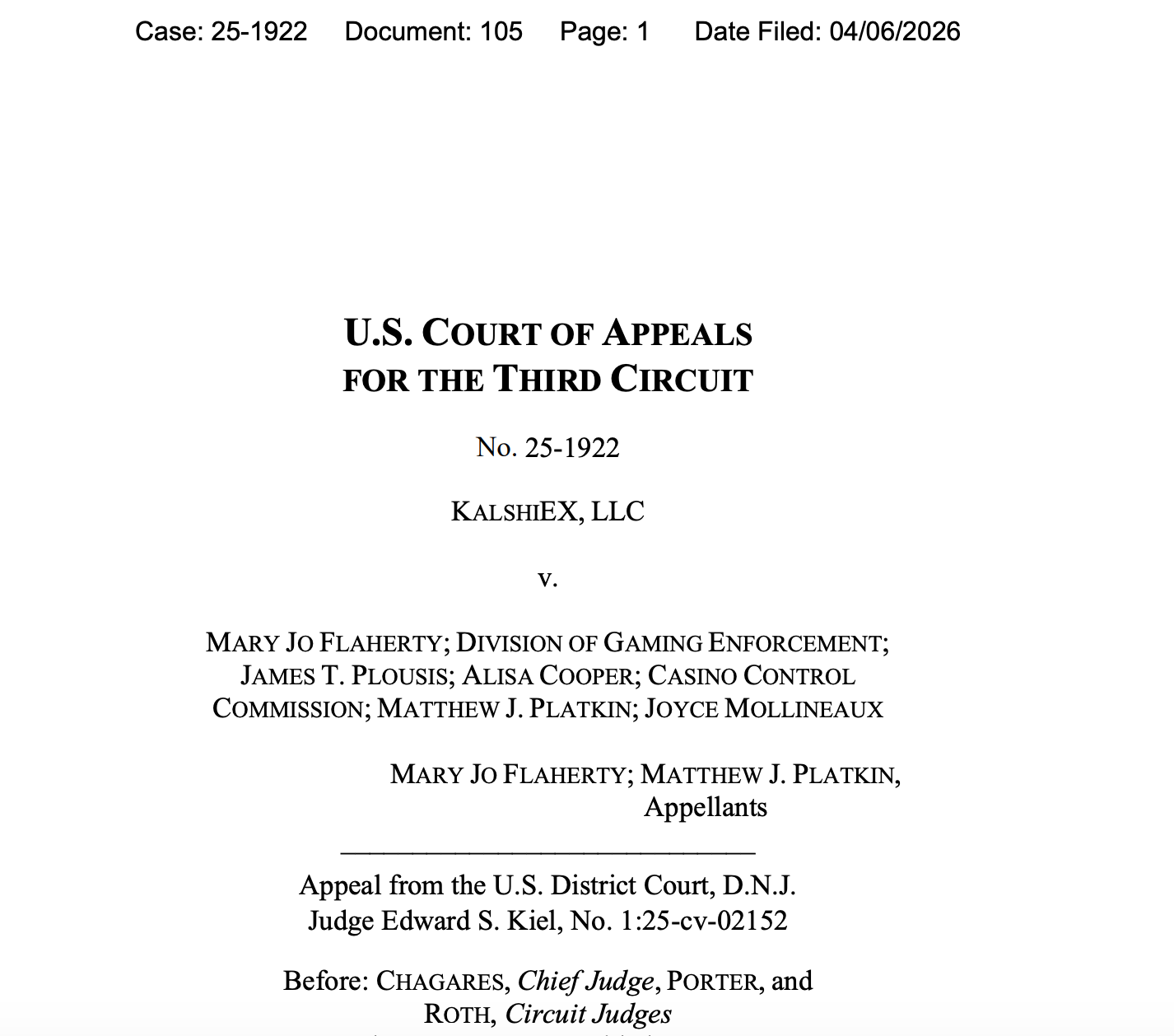

A US appellate court has ruled against New Jersey gaming authorities for bringing an enforcement action against prediction market platform Kalshi over sports event contracts.

In a Monday-issued opinion, a panel of judges in the US Court of Appeals for the Third Circuit ruled 2-1 in favor of Kalshi’s argument that the company had a ”reasonable chance of success” claiming that the Commodity Exchange Act preempted state law, setting the stage for a potential battle over gaming laws in the US Supreme Court.

“This is a big win for the industry and millions of users,” Kalshi CEO Tarek Mansour said in a social media post on X.

The appellate court’s opinion affirmed a lower court ruling, in which Kalshi argued that the US Commodity Futures Trading Commission (CFTC) had “exclusive jurisdiction” in regulating sports-related event contracts as swaps that fall under its purview.

Advertisement

“Allowing New Jersey to enforce its gambling laws and state constitution would create an obstacle to executing the Act because such state enforcement would prohibit Kalshi, which operates a licensed [designated contract market] under the exclusive jurisdiction of the CFTC, from offering its sports-related event contracts in New Jersey,” wrote Circuit Judge David J. Porter. “This state regulation is exactly the patchwork that Congress replaced wholecloth by creating the CFTC.”

Monday’s Third Circuit opinion affirming lower court ruling. Source: PACER

The circuit court ruling came just days after a Nevada judge extended a ban on Kalshi offering event-based contracts, following several other state authorities cracking down on sports betting on prediction markets. The patchwork of state-level rulings could lead to the US Supreme Court taking up one of the cases, potentially changing its 2018 decision giving states the authority to regulate sports gambling.

In her dissent, Circuit Judge Jane Roth said the prediction markets platform’s actions were a “performative sleight meant to obscure the reality that Kalshi’s products are sports gambling,” adding that the company’s event contracts were “virtually indistinguishable” from those on betting websites:

“[T]he question of whether sports-event contracts are swaps is a thorny issue with the potential to radically upend the legal landscape governing the gambling industry, and I am not convinced the Majority’s analysis does this issue justice.”

CFTC chair reiterates agency’s position on prediction markets

CFTC Chair Michael Selig, the sole commissioner at the financial agency following the departure of acting chair Caroline Pham in December, has made prediction markets one of the commission’s central issues since taking office. In the last four months, Selig has claimed that the CFTC has “exclusive jurisdiction” in regulating event contracts on prediction markets, opened a proposed rule to public comment and filed an amicus brief supporting its position in the Ninth Circuit Court of Appeals in a case involving Nevada’s gaming authorities.

“Our definition of commodity and statute is very broad,” Selig said at the Digital Assets and Emerging Tech Policy Summit at Vanderbilt University on Monday. “It includes events on sports, it includes events in politics, it includes corn and grains and all sorts of things. It doesn’t really distinguish between if you’re offering an event contract on grains, you’re regulating that differently than an event contract on sports.”

The CFTC chair added that there were exceptions for event contracts that were “readily susceptible to manipulation.”

Cointelegraph is committed to independent, transparent journalism. This news article is produced in accordance with Cointelegraph’s Editorial Policy and aims to provide accurate and timely information. Readers are encouraged to verify information independently. Read our Editorial Policy https://cointelegraph.com/editorial-policy

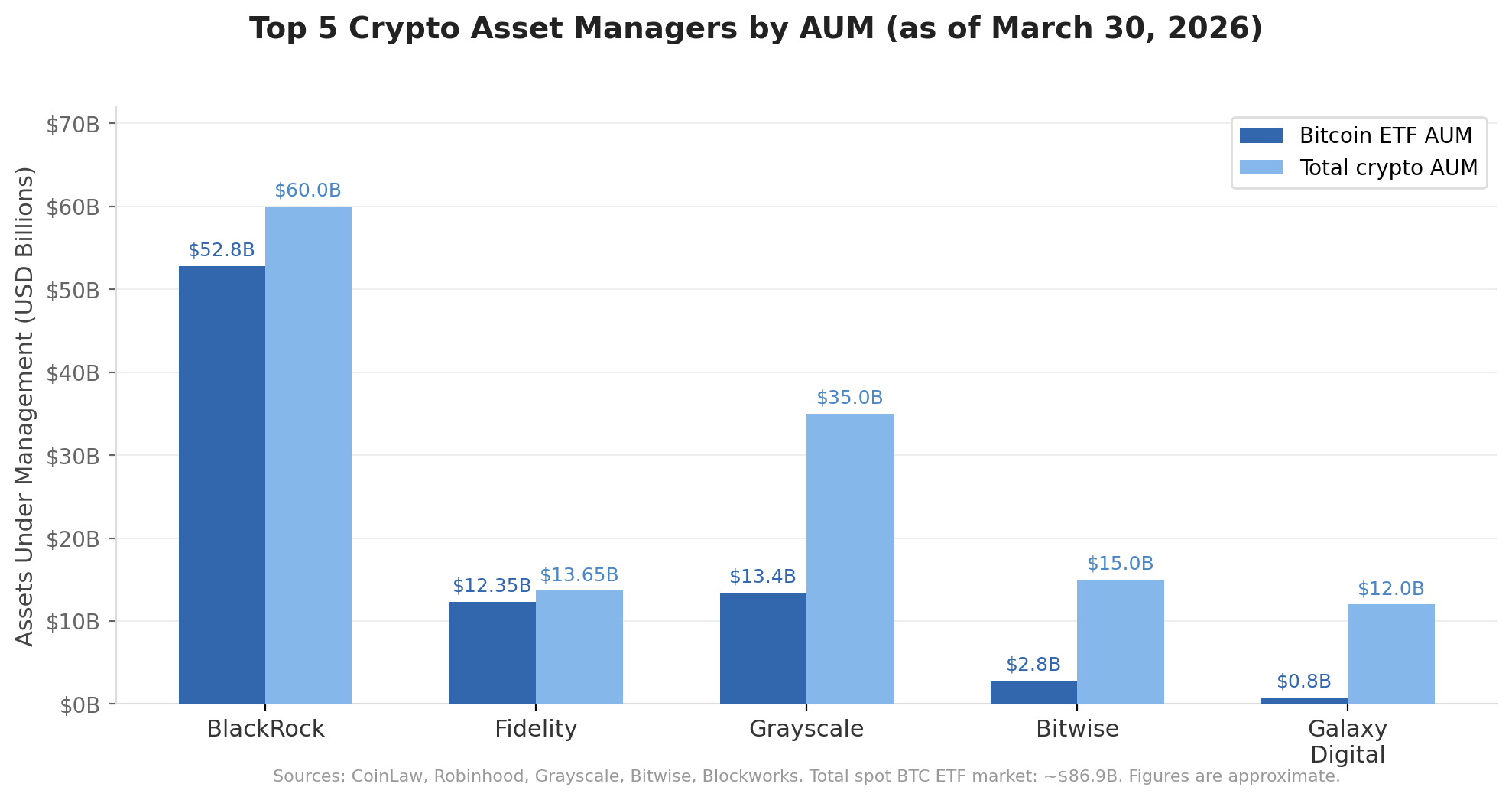

As of 2026, about 25 US asset managers directly offer crypto products (ETFs, trusts, or funds). But the five largest crypto-focused asset managers now collectively oversee well over $100 billion in digital asset products.

Their dominance reflects how deeply institutional capital has embedded itself into crypto through regulated ETFs.

Five Firms Control Nearly $100 Billion in Bitcoin ETFs

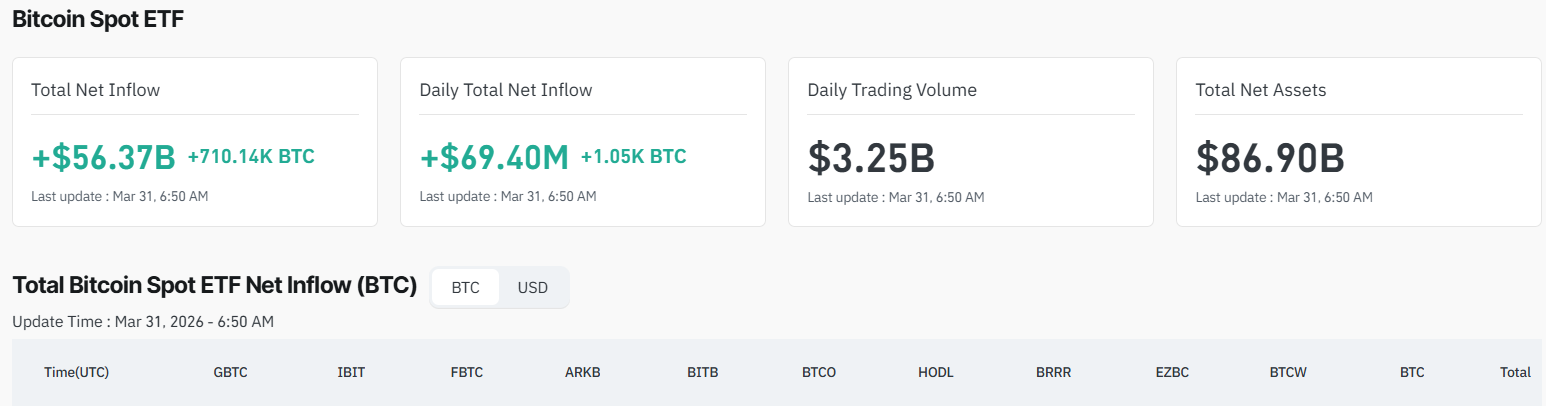

Spot Bitcoin ETFs alone surpassed $86 billion in combined assets under management as of this writing, according to Coinglass data.

Bitcoin Spot ETFs Total Net Assets. Source: Coinglass

The competition among issuers has intensified as fee wars, product variety, and institutional distribution networks determine who captures the most capital.

The fee on this will be very interesting. We should know soon. I’m setting over/under at 0.24% which is one bp lower than IBIT. What does @NateGeraci and @JSeyff think?

BlackRock’s iShares Bitcoin Trust (IBIT) sits at $51.9 billion in AUM, representing approximately 45% of all spot Bitcoin ETF assets, according to SoSoValue data. During Q1 2026, IBIT pulled in $8.4 billion in net inflows, more than double any competitor.

The fund held approximately 782,180 BTC as of March 27, 2026, with BlackRock’s iShares Ethereum Trust (ETHA) adding several billion more. This pushes total crypto ETF exposure near $60 billion.

BlackRock’s BTC Holdings. Source: BlackRock

Meanwhile, Fidelity’s Wise Origin Bitcoin Fund (FBTC) manages $12.8 billion in AUM, holding approximately 187,813 BTC as of early March, and its Ethereum Fund (FETH) adds over $1.3 billion.

Fidelity attracted $4.1 billion in Q1 2026 net inflows, ranking second behind BlackRock.

Advertisement

The firm’s self-custody model through Fidelity Digital Assets and its 0.25% fee structure have made it a preferred choice among compliance-focused institutional allocators.

Spot Bitcoin ETF Fee Comparison. Source: Fibo

Grayscale Defends Its Legacy

Still, Grayscale Investments remains the oldest and broadest crypto-focused asset manager, operating since 2013.

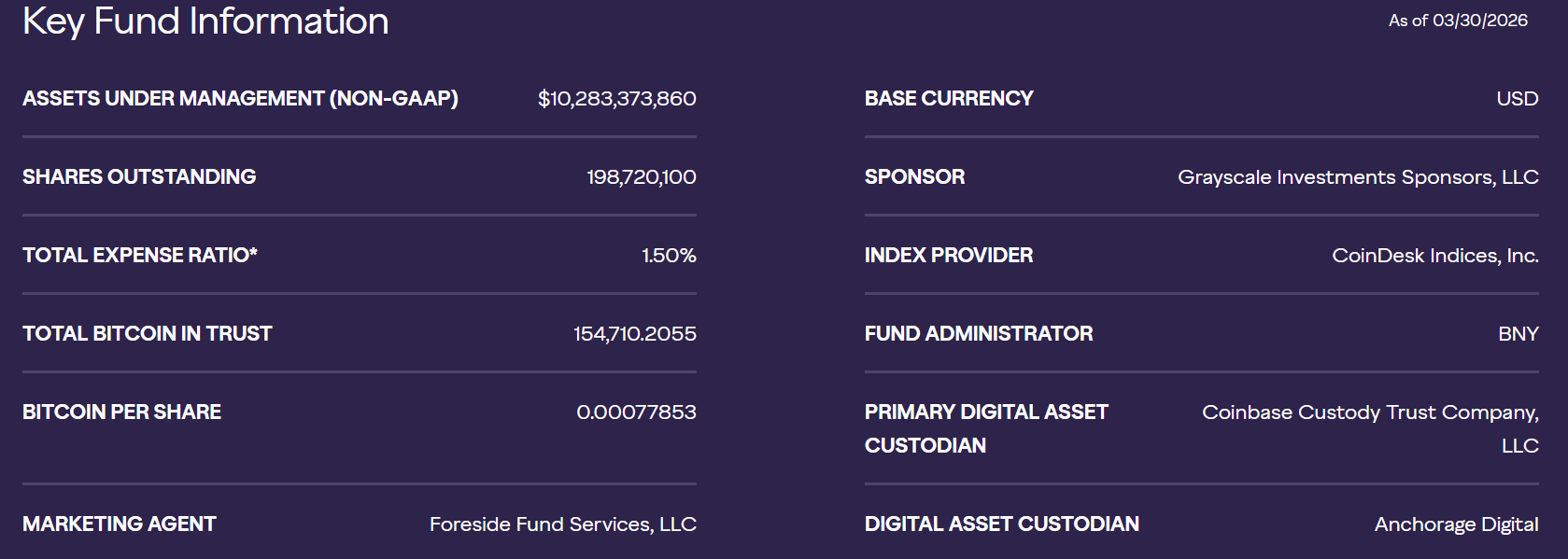

Its Bitcoin Trust (GBTC) held approximately 154,710 BTC as of this writing, valued at approximately $10 billion. The lower-fee Bitcoin Mini Trust (BTC) added another $3.4 billion, according to Grayscale.

Grayscale Fund Information. Source: Grayscale

GBTC outflows slowed to $1.2 billion in Q1 2026, a sharp decline from the multi-billion-dollar monthly outflows of 2024.

No Strategy buy announcement this week. But let’s talk about what just happened in Q1 2026. 🟠 📊 Q1 2026 Numbers: – 89,599 BTC acquired – $5.5 BILLION deployed – 2nd highest quarter in Strategy history – Buying ~2.5x faster than global mining – Supply vacuum: 53,149 BTC… pic.twitter.com/QbdzEPjw3n

Grayscale’s total platform exceeded $35 billion in AUM as of late 2025, and it maintains the broadest product pipeline, with a 36-asset watchlist for potential future ETF launches.

Advertisement

Bitwise Wins on Variety and Altcoin Exposure

Elsewhere, Bitwise Asset Management surpassed $15 billion in client assets across more than 40 products. These span ETFs, separately managed accounts, private funds, hedge strategies, and staking.

Its standout position is in Solana ETFs. As of early January 2026, Bitwise controlled approximately 67% of all Solana ETF AUM, capturing $731 million out of the $1.09 billion total.

Galaxy Digital operates as a full-service merchant bank rather than a pure ETF issuer. Its asset management arm reported $9 billion in AUM with $2 billion in quarterly net inflows by Q3 2025.

By the end of 2025, total platform assets reached $12 billion, despite reporting a $482 million loss in the fourth quarter.

NOVOGRATZ’S GALAXY POSTS $482M LOSS IN CRYPTO CRASH Galaxy Digital reported a $482 million loss in the fourth quarter, far worse than expected, as falling crypto prices hit its portfolio. Bitcoin dropped 23% during the period, trading volumes fell 40%, and the firm’s shares slid…

Galaxy partners with State Street Global Advisors on actively managed digital asset ETFs and maintains exposure across trading, lending, staking, and venture capital.

Its hybrid model positions it as the go-to for institutions that need more than passive ETF access.

Advertisement

Bar chart comparing AUM of top 5 crypto asset managers in 2026, Source: BeInCrypto

The 2026 crypto asset management race has a clear hierarchy.

BlackRock dominates on scale

Fidelity on institutional trust

Grayscale on history and breadt

Bitwise on product innovation, and

Galaxy on full-service infrastructure.

And then there is Morgan Stanley, which is not yet in the race but could reshape it entirely.

Morgan Stanley’s $160 Billion Wildcard Could Rewrite the Entire Leaderboard

The bank filed an amended S-1 for its spot Bitcoin ETF, MSBT, with a 0.14% fee that undercuts every existing competitor, including BlackRock’s 0.25%.

It would be the first spot Bitcoin ETF issued directly by a major U.S. bank rather than an asset manager. However, the ETF is just one piece.

Morgan Stanley has also applied for a national trust bank charter through a new subsidiary called Morgan Stanley Digital Trust. This would handle custody, trading, staking, and transfers of digital assets under federal oversight.

With $8 trillion in wealth management assets and over 16,000 advisors, even a modest 2% allocation would represent $160 billion in potential demand, roughly three times the size of IBIT.

Morgan Stanley Wealth Management oversees about $8 trillion in AUM and recommends 0–4% bitcoin allocation. A 2% allocation would represent $160 billion, ~3X the size of IBIT. $MSBT: Monster Bitcoin. https://t.co/TNYLYRXPiz

If all these pieces come together, Morgan Stanley would not just enter the crypto race. It would be building the entire track.

Advertisement

“They’re not just offering exposure anymore, they’re building the full stack. BNY Mellon + Coinbase as dual custodians is smart redundancy,” one user highlighted.

With spot Bitcoin ETFs now past $128 billion in combined AUM, the question is no longer whether institutions will adopt crypto. It is the managers who will capture the next wave of capital.

House Democrats are convening a virtual caucus call tonight, April 6, to plot their next steps on the DHS shutdown, now 51 days old and the longest partial government shutdown in US history.

Summary

Punchbowl News reports House Democrats will hold a virtual caucus meeting tonight as the chamber returns from a two-week recess, with the DHS shutdown having been running since February 14

The shutdown broke the record for the longest in US history on March 29, surpassing the 43-day fall 2025 shutdown, and has left 480-plus TSA officers quitting, airport wait times exceeding four hours, and an estimated $2.5 billion in economic losses

The Senate passed a deal to fund DHS without ICE or CBP, but House Republicans rejected it last week, passing a 60-day stopgap that Senate Democrats called “dead on arrival.”

House Democrats are holding a virtual DHS shutdown caucus call tonight at the start of a critical week, according to Punchbowl News, as the chamber returns from a two-week Passover and Easter recess with no resolution in sight. The shutdown, which began February 14, crossed 51 days on April 6, making it the longest partial government shutdown in the country’s history. Democrats support the Senate-passed bill that funds most of DHS while excluding ICE and CBP, and leadership does not expect significant defections from that position.

The Senate passed a funding deal by voice vote in the early hours of last Friday after a marathon overnight session, threading the needle on Democrats’ core demand: funding the department without allocating money to ICE or the Border Patrol. Senate Majority Leader John Thune and Senate Minority Leader Chuck Schumer both backed the measure. But the House rejected it.

Advertisement

Speaker Mike Johnson instead put forward a 60-day stopgap that would fund all of DHS, including ICE and CBP. Senate Democrats immediately declared it dead. “Our position remains the same,” House Minority Leader Hakeem Jeffries said. “There is a bipartisan bill that every single senator, Democrats and Republicans, supported, that has the votes to pass today.”

The Real Costs on the Ground

The shutdown has produced measurable damage. The TSA callout rate is running five times above its normal level. More than 480 transportation security officers have quit since February, and some major airports are operating with 40 to 50 percent of their expected workforce absent on any given day. Wait times exceeding four and a half hours have been recorded at some of the country’s busiest terminals. Estimated economic losses now stand at $2.5 billion, according to Republican appropriators who cited the figure in a recent floor statement.

As crypto.news reported when the earlier DHS funding lapse rattled markets in February, the shutdown’s spillover into economic data releases and Federal Reserve signaling can create cascading uncertainty across financial markets well beyond the political standoff itself.

Advertisement

How Both Sides Got Here

The shutdown traces back to the killing of a US citizen by a Customs and Border Protection agent in Minneapolis in January 2026. Senate Democrats announced they would no longer support the DHS funding bill, which funds CBP, demanding reforms to immigration enforcement as a condition. Trump has repeatedly refused to negotiate on reopening DHS unless Democrats back the SAVE America Act, his voter ID and proof-of-citizenship legislation, which is a non-starter for the minority.

Tonight’s caucus call will test how unified House Democrats remain heading into the second week of return from recess, and whether any moderates are ready to move. As crypto.news noted when the 43-day fall 2025 shutdown finally ended, the resolution of prolonged political standoffs tends to produce sharp market relief rallies across risk assets.

“Throughout it all, Senate Democrats stood united — no wavering, no backing down,” Schumer said Friday after the Senate vote.

Bitcoin (BTC) is trading within a bear flag pattern that projects a breakdown toward the sub-$50,000 area, or roughly 30% below current levels. However, Michael Saylor’s Strategy could spoil the bears’ plans.

BTC/USD three-day price chart. Source: TradingView

Key takeaways:

Bitcoin has avoided a bear flag breakdown for weeks as Strategy keeps buying BTC.

The setup now resembles Bitcoin’s 2018 bottom, when a bearish pattern failed and triggered a reversal.

Can Strategy’s BTC buying offset weak technicals?

Normally, a bear flag remains a bearish continuation pattern because there is not enough demand to overcome the broader downtrend.

In Bitcoin’s case, however, Strategy has been taking supply off the market faster than miners can replace it.

Since March 2, Strategy’s Bitcoin holdings have risen by 46,233 BTC, while miners have produced only about 16,200 BTC over the same period, meaning it has absorbed nearly thrice the new supply.

Much of that demand has come through STRC, Strategy’s variable-rate preferred stock. When STRC held near or above its $100 par value, Strategy kept issuing shares and accumulating BTC.

For instance, last week, Strategy raised $102.6 million through STRC sales to help fund a Bitcoin purchase worth over $330 million. BTC’s price has jumped by over 6.65% ever since.

STRC at-the-market sales analysis. Source: BitcoinQuant.CO

During March 9–13, STRC sales raised about $776 million, enough to buy over 11,000 BTC, while Bitcoin rose more than 7% even as the S&P 500 fell 1.6%. The same period saw BTC’s price rising over 10.5%.

Bear flag failure could set stage for rally to $110,000

Bitcoin remains inside a bear flag after a sharp decline, but the pattern would begin to fail if price breaks above the upper trendline near the mid-$70,000 area.

Advertisement

That breakout would invalidate the immediate bearish continuation setup and shift focus to the bullish measured-move target near $108,000-$110,000.

BTC/USD weekly price chart. TradingView

A similar pattern failure occurred near Bitcoin’s 2018 bottom, when a rising wedge pattern led to a breakout instead of a breakdown.

Another factor supporting the upside case is Bitcoin’s position near its 200-week simple moving average (200-week SMA, the blue wave). In 2018, Bitcoin bottomed out near this level and rose by over 1,975% afterward.

As of 2026, the 200-week SMA has capped Bitcoin’s downside attempts successfully, raising the odds of a 2018-like bottom formation.

Some analysts anticipate BTC to rise to $400,000 if Strategy continues buying BTC at its current rate.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

An open-source AI job hunter built on Claude Code just auto-applied to hundreds of roles and actually landed a job, exposing why the real bottleneck is on-chain compute, not résumés.

Summary

An open-source AI agent built on Claude Code sent more than 700 targeted job applications and “actually got him hired,” according to X host 0xMarioNawfal.

The tool, Career-Ops, scans 45+ company career pages, scores roles, rewrites CVs in 14 “skill modes,” and batch-fires ATS-optimized PDFs while the user sleeps.

As AI agents flood hiring pipelines, tokenized computational performance on networks like Bittensor, Render and FET could become the settlement layer for automated job hunting.

A viral clip shared by 0xMarioNawfal claims that “SOMEONE BUILT AN AI JOB SEARCH SYSTEM FOR CLAUDE CODE THAT SENT 700+ APPLICATIONS AND ACTUALLY GOT HIM HIRED,” and that “THE JOB HUNT JUST GOT AUTOMATED.”

SOMEONE BUILT AN AI JOB SEARCH SYSTEM FOR CLAUDE CODE THAT SENT 700+ APPLICATIONS AND ACTUALLY GOT HIM HIRED.

The system in question, an open-source project called Career-Ops, is billed on GitHub as an “AI-powered job search system built on Claude Code” with 14 skill modes, a Go dashboard, PDF generation and batch processing, effectively turning the job hunt into an automated pipeline. A LinkedIn post summarizing the tool says it “scans multiple company career pages, rewrites your CV per job, and even fills application forms,” targeting firms like Anthropic, OpenAI and Stripe across 45-plus pre-configured employers.

Reaction on X underscores how fast AI agents are colonizing hiring. One user, Ofek Shaked, calls it “the future of job hunting,” adding that a simpler version “landed me 3 interviews” in a month. Another, Eugene Smarts, notes “that’s wild, imagine how much time that saves, job hunting is the worst,” while EchoWireDai warns that “If everyone automates applications… recruiters will just automate rejections.” Others highlight the quality constraint: investor Balvinder Kalon writes that “the real flex is getting the context right per company,” arguing that agents that “tailor each application to the job description, not just spray and pray” will be the ones that matter. Tools like Plushly, promoted in the same thread as a way to “auto apply to internships & jobs while you sleep,” show how quickly similar services are proliferating.

Advertisement

As systems like Career-Ops scale, their bottleneck is not résumés; it is compute. The GitHub repo describes an architecture that continuously scans job portals, runs multi-step Claude Code prompts, generates ATS-optimized PDFs via Playwright, and monitors everything from a terminal dashboard, turning each job search into thousands of model calls and browser automations. According to Bloomberg, AI has already become “unavoidable on both sides of hiring,” with most résumés never reaching a human and interviews increasingly led by bots, a shift workforce experts say forces applicants to “learn how to navigate a job market reshaped by it.” In another explainer on the “new rules of finding a job in 2026,” Bloomberg warns that mass-applying with generic AI hurts candidates, but using AI well can help them strategically target roles and refine materials, exactly the niche Career-Ops tries to occupy.

That compute demand is already visible in crypto markets. An MEXC research note on AI tokens highlights how Bittensor (TAO), Render (RENDER) and the Artificial Superintelligence Alliance’s FET token have led recent rallies, with TAO up nearly 35% in a week and Render and FET gaining roughly 25–32%, as traders bet on “agentic AI systems, autonomous software capable of performing tasks without human input.” These networks explicitly sell tokenized access to GPU and machine-learning resources: Render routes GPU rendering jobs across a decentralized network of providers, while Bittensor’s design, as CCN explains, aims to reward participants who supply and route high-quality machine-learning models, with price forecasts suggesting TAO could trade between $748 and $2,750 in long-term scenarios. As job-hunting agents evolve from scraping and form-filling to full-stack career copilots, routing their ever-growing computational load through tokenized compute layers becomes a rational way to meter, price and trade that performance rather than leaving it buried inside closed platforms.

The cultural flip is not lost on users. Commenter Gagan Arora notes that “We went from ‘AI will take your job’ to ‘AI will find your next job’ in about 6 months,” calling it “the irony” that the tool workers feared is now “the best tool for getting hired.” Bloomberg’s coverage of AI-led interviews points in the same direction: a study summarized by the outlet found that AI interviewers, randomly assigned to 67,000 job seekers, could outperform human recruiters in surfacing strong candidates, raising questions about where humans still add value in the funnel. For now, Wall Street expects AI adoption to increase hiring rather than crush it, with a Bloomberg Intelligence survey cited by Bloomberg News indicating that roughly two-thirds of financial firms foresee staff numbers rising initially as they roll out AI.

For crypto, the signal is simple: if agents are going to swarm both sides of the labor market, the underlying compute will become an asset in its own right. In a previous crypto.news story on AI tokens, analysts argued that projects like Bittensor and Render sit “at the center of the AI infrastructure narrative,” capturing value as demand for model inference and GPU cycles grows. Another crypto.news story on agentic AI in DeFi predicted that autonomous agents would eventually need on-chain reputations, budgets and compute allowances, paid in liquid tokens that track underlying GPU or model performance rather than abstract governance rights. The Claude-powered job hunter that just landed its creator a new role is a glimpse of that future: an early, messy, very human example of why the next phase of job hunting may run not just on prompts and PDFs, but on tokenized computational performance that turns raw AI horsepower into a tradable, programmable resource.

The synthetic dollar protocol is moving beyond its crypto basis trade roots into institutional lending, real-world credit, and equity and commodity perpetuals.

Ethena Labs is finalizing its first direct lending agreements with Anchorage Digital, Maple Institutional, and Coinbase Asset Management as part of a sweeping plan to diversify the assets backing its USDe synthetic dollar.

Under the agreements, Ethena would lend stablecoins from USDe’s reserves to facilitate overcollateralized loans originated by those entities, with borrower collateral held in secured triparty custody. Each loan will operate within parameters set by the Ethena Risk Committee, including minimum overcollateralization ratios, concentration limits, automatic liquidation thresholds, and tenors designed to minimize liquidity risk during large USDe redemption events.

Ethena framed the move as a natural extension of the stablecoin lending it already does on DeFi protocols like Aave and Morpho, but for institutional counterparties with only high-quality, immediately liquid collateral such as BTC and ETH.

Advertisement

Beyond the Basis Trade

The institutional lending push is one piece of a broader four-part diversification strategy Ethena outlined Monday, which also includes expanding real-world asset (RWA) exposure beyond tokenized Treasury bills, extending its delta-neutral framework into equity and commodity perpetuals, and exploring prime lending to trading firms.

The shift reflects how far USDe’s reserve composition has already moved. Perpetual futures positions, once the mainstay of USDe’s backing, now make up just 11% of the stablecoin’s reserves, with the rest allocated to stablecoin reserves and DeFi lending positions. Ethena recently proposed replacing its static 7-day unstaking cooldown with a dynamic model, arguing the fixed period no longer reflects the liquidity available to meet redemptions.

USDe’s circulating supply has contracted to approximately $5.9 billion from a peak above $14.6 billion before the October 10 crash that wiped more than $5 billion from its market cap.

Meanwhile, the protocol’s ENA token is up 9% over the past 24 hours, but has dropped 94% from its peak two years ago.

Advertisement

ENA Chart

Equity and Commodity Perps

Perhaps the most novel element is Ethena’s plan to apply its basis trade methodology to equity and commodity perpetual futures — a market that has grown rapidly since Hyperliquid launched its HIP-3 framework in October 2025.

TradeXYZ Open Interest

HIP-3 open interest has surged from $70 million at launch to over $2 billion, driven by non-crypto pairs such as equities, commodities, and indices. Ethena noted that gold perpetual funding rates on Binance averaged 24.6% in March, presenting a clear basis opportunity for delta-neutral operators.

On the RWA side, Ethena said initial allocations will likely be limited to AAA-rated CLOs, which have no history of defaults, with potential expansion into investment-grade corporate bond funds and short-duration credit products.

This article was written with the assistance of AI workflows. All our stories are curated, edited and fact-checked by a human.

The International Monetary Fund says tariffs don’t meaningfully fix trade gaps. Their impact is small and inconsistent.

At the same time, global current account imbalances are widening again. That points to rising economic strain between countries. For crypto, this matters. When trade tensions rise and policy tools fall short, capital often moves toward alternative assets like Bitcoin.

The IMF’s Key Findings

In a new policy paper, IMF researchers Pierre-Olivier Gourinchas and Christian Mumssen analyze the drivers of global imbalances.

Their conclusion is clear: traditional macroeconomic policies remain the dominant lever for addressing current account imbalances. Tariffs and industrial policies, by contrast, yield limited, and often counterproductive, results.

Advertisement

According to the IMF, tariffs only improve current accounts in rare circumstances, specifically when they are temporary. However, most tariffs are perceived as permanent or trigger retaliation.

As a result, people do not adjust their saving behavior, and the current account remains largely unchanged.

The paper warns that widening imbalances “have often preceded financial crises or abrupt reversals of capital flows.”

Fun Fact: The IMF notes that an escalation of tariffs does little to change current account positions but significantly lowers output across all regions. Everybody loses!

Global imbalances are widening again, raising risks for economic growth and financial stability. Tariffs and narrow industrial policies rarely help, as our latest blog details. Rebalancing starts at home, with sound macroeconomic policies. https://t.co/UfYUGEjUVypic.twitter.com/iPCfZAShla

The IMF’s analysis paints a picture of structural instability. Consequently, several crypto-relevant dynamics emerge:

Dollar Pressure: The US is running large fiscal deficits with large consumer spending. A weakening fiscal position could put long-term pressure on dollar confidence, potentially benefiting alternative stores of value like Bitcoin.

Stablecoin Demand: As global trade tensions persist and underlying imbalances persist, businesses may increasingly turn to stablecoins for cross-border transactions. USD-pegged stablecoins offer dollar exposure without a direct dependency on the banking system.

Safe Haven Narrative: The IMF explicitly warns of potential financial crises. Historically, such warnings have preceded periods where investors seek uncorrelated assets.

Outlook

The IMF calls for “synchronized adjustment,” where countries move together. However, such coordination has proven elusive. In the absence of coordinated action, market participants will seek their own solutions.

The IMF’s warning is clear: global imbalances are widening, tariffs won’t fix them, and disorderly adjustment could be “exceptionally costly.”

For crypto markets, this macro backdrop creates both risks and opportunities. The structural case for crypto as an alternative financial layer grows stronger as traditional policy tools fail to deliver.

U.S. stocks inched higher on Monday, but beneath the smooth index closes, meme names, bitcoin proxies and Chinese ADRs traded like a late‑cycle minefield.

Summary

U.S. stocks closed modestly higher Monday, with the Dow up 0.36%, the S&P 500 up 0.45%, and the Nasdaq up 0.5%.

Tesla fell 2%, while AMC Entertainment surged 12% and MicroStrategy gained 6%, highlighting sharp divergences in high‑beta names.

Chinese ADRs underperformed, with the Nasdaq Golden Dragon China Index down 0.2% and iQIYI off 4%.

U.S. equities finished Monday’s session slightly higher, with the Dow Jones Industrial Average rising 0.36%, the S&P 500 index adding 0.45%, and the Nasdaq Composite gaining 0.5%, according to Gate’s market data. The advance came even as individual names swung widely: AMC Entertainment jumped 12%, MicroStrategy climbed 6%, Advanced Micro Devices dropped 5%, and Tesla slipped 2%. Chinese‑focused stocks lagged, with the Nasdaq Golden Dragon China Index closing down 0.2% and iQIYI losing 4%.

Beneath the relatively calm headline moves, Monday’s tape showed classic late‑cycle dispersion, with meme‑linked and crypto‑sensitive names moving far more violently than the benchmarks. AMC’s 12% gain extended a recent rebound fueled by retail flows and short‑covering, while MicroStrategy’s 6% rise tracked ongoing strength in Bitcoin‑exposed equities after the software firm’s aggressive BTC accumulation left it trading as a leveraged proxy on the crypto market. By contrast, AMD’s 5% decline and Tesla’s 2% drop reflected pressure across high‑multiple growth and EV names, as investors rotated selectively within the tech and consumer‑discretionary complex.

Advertisement

The modest uptick in the S&P 500 and Nasdaq follows a strong 2025 in which the major U.S. indices posted double‑digit gains, according to recent data compiled by Reuters and LSEG. Analysts quoted in prior sessions have emphasized that with the S&P 500 already up more than 16% last year and the Nasdaq ahead over 20%, even small daily moves can mask significant stock‑level volatility as investors reassess earnings, rates, and geopolitical risks. Against that backdrop, Monday’s pattern — indexes up less than 0.5% while individual names swing 5%–12% — fits a market where stock‑picking and thematic positioning matter more than simple beta exposure.

Chinese internet and consumer names remained under pressure. The Nasdaq Golden Dragon China Index, which tracks U.S.‑listed Chinese ADRs, slipped 0.2% on the day, with iQIYI down about 4% alongside broader weakness in popular Chinese concept stocks. Recent sessions have seen sharper drops in the index — including declines of more than 2% on days when names like Alibaba, NIO, and XPeng fell between 3% and 6% — underscoring persistent skepticism over China’s growth outlook, regulatory risk, and U.S.‑China tensions.

World Liberty Financial and Aster DEX have announced a partnership. According to WLFI, USD1 will serve as the settlement asset for TradFi perpetual contracts on the platform.

Gold, silver, crude oil, and additional markets are planned.

Aster DEX confirmed the collaboration on X: “Aster and WLFI are working together to support closer ecosystem alignment, with both sides exploring integration across their respective tokens.”

Both teams indicated they are exploring deeper integration across their respective token ecosystems, suggesting the partnership could expand beyond settlement.

Fun Fact: USD1 has surpassed $4.6 billion in market cap and ranks fifth among stablecoin issuers by daily active addresses, ahead of PayPal and Ethena!

Advertisement

Every TradFi perp on @Aster_DEX will settle in USD1. → Not alongside USDT. Exclusively. → Gold. Silver. Crude oil. More markets coming. → Both sides exploring integration across their respective tokens. 👀 https://t.co/zgpSWbQnwf

Aster DEX offers perpetual contracts that allow traders to gain exposure to traditional assets through a DeFi interface. Adding USD1 as a settlement option expands the stablecoin’s utility beyond simple transfers.

For USD1, the integration creates a new use case: traders holding USD1 can use it directly for trading commodities perpetuals without converting to other stablecoins first.

Similarly, for WLFI, more USD1 utility translates to more ecosystem activity. As a result, each new integration adds another reason for users to hold and use the stablecoin.

Advertisement

USD1’s Expanding Footprint

The Aster DEX partnership is the latest in a series of USD1 integrations. Recent developments include:

BitGo Mint added USD1 to its institutional stablecoin management platform.

MEXC integrated USD1 across Launchpool, Savings, and as futures collateral.

World Liberty Markets launched as a DeFi lending platform with USD1 as the primary asset.

USD1’s circulating supply has surpassed $4.6 billion, distributed across Ethereum (40.60%), BNB Chain (40.47%), and Solana (18.48%).

The partnership between WLFI and Aster DEX reflects a broader trend of stablecoins seeking differentiated use cases. Instead of competing solely on listings, USD1 is building integrations that create specific utility.

However, details on the full scope of the integration and timeline for the TradFi perpetual markets have not yet been disclosed. Nevertheless, both teams indicated further announcements are expected as the partnership develops.

Jamie Dimon, the CEO of JPMorgan Chase, used the bank’s annual shareholder letter to underscore how rapid technological advances are reshaping competition in finance. He highlighted artificial intelligence, data analytics and other advanced tools as central to the industry’s near- and long-term trajectory, signaling a shift toward more automated and data-driven financial services.

While blockchain and digital assets were not the letter’s sole focus, Dimon acknowledged that “a whole new set of competitors is emerging based on blockchain, which includes stablecoins, smart contracts and other forms of tokenization.” The remarks come as JPMorgan doubles down on its own blockchain initiatives, even as Dimon stresses that the bank’s long-term prosperity hinges on effectively deploying AI across its operations.

JPMorgan has been building out its in-house infrastructure, now branded Kinexys, a platform designed to enable near-instant fund transfers without traditional middlemen. The effort aims to scale to as much as $10 billion in daily transaction volume and has drawn notable corporate participants into its orbit. The bank has onboarded Mitsubishi Corporation of Japan and counts Qatar National Bank, Siemens, and BlackRock among its institutional clients. Beyond payments, Kinexys is being positioned as a broader tokenization platform, with JPMorgan signaling plans to extend into asset classes such as private credit and real estate.

Dimon’s notes arrive amid a larger policy debate in Washington over how digital assets should be regulated, particularly around stablecoins. The GENIUS Act, enacted last year, established a regulatory framework that many in the crypto industry expect will accelerate adoption by clarifying the rules for stablecoins and related activities. Yet broader market-structure legislation remains stalled in Congress. A key point of contention is yield-bearing stablecoins—banking groups warn that issuers offering interest-style returns could undermine financial stability if they operate outside traditional banking guardrails.

Advertisement

Key takeaways

Tech-driven competition rising: Dimon frames AI, data and blockchain-enabled firms as a new frontier, even as JPMorgan emphasizes its own tech initiatives.

Kinexys advances its agenda: JPMorgan’s blockchain platform targets up to $10B in daily volume and has attracted marquee clients, with tokenization at the core of its expansion plans.

Regulatory clarity vs. stalled legislation: GENIUS Act provides a clearer framework for stablecoins, but wider market-structure bills remain uncertain in Congress.

Industry tensions surface publicly: Dimon and Coinbase CEO Brian Armstrong have publicly debated crypto regulation, while banks advocate against yield-bearing stablecoins.

Market context matters for adoption: The stablecoin market topped roughly $315B in Q1, a data point that regulators and market participants watch closely.

Kinexys as a real-world accelerator for tokenization

JPMorgan’s Kinexys protocol is being pitched as more than just a faster rails solution for transfers. By embedding near-instant settlement capabilities into corporate and institutional processes, JPMorgan envisions Kinexys as a gateway to broader asset tokenization. The onboarding of Mitsubishi Corporation in particular signals a strategic effort to attract multinational clients with complex cross-border needs, where speed and reliability translate into tangible capital efficiency gains.

Beyond Mitsubishi, Kinexys counts Qatar National Bank and other large institutions such as Siemens and BlackRock among its users. The breadth of these clients points to a practical use case: tokenized payments and settlements can trim intermediaries, reduce settlement risk and improve liquidity management across global networks. In JPMorgan’s framing, Kinexys is a stepping stone toward a larger tokenization ecosystem—one that could eventually encompass private markets such as private equity, real estate and other asset classes that traditionally require longer settlement cycles.

As JPMorgan positions Kinexys as both a payments platform and a broader tokenization layer, investors should watch for how quickly new assets—beyond cash equivalents—can be tokenized and traded within the network. The pace at which more clients sign on and the types of asset classes brought under Kinexys’ umbrella will be a telling indicator of JPMorgan’s broader hypothesis: that tokenization can unlock liquidity and improve capital efficiency at scale.

Regulatory currents shaping the crypto horizon

The JPMorgan letter arrives at a moment when policy makers are weighing a path forward for stablecoins and crypto markets. The GENIUS Act, which laid groundwork for stablecoin regulation and custody rules, is widely viewed as a factor that could hasten institutional participation in tokenized assets, provided issuers operate under clear compliance standards. By offering a regulatory scaffold, proponents argue that GENIUS reduces legal ambiguity for banks and fintechs exploring stablecoin-related services.

However, comprehensive market-structure reform remains stuck in Congress. Lawmakers are debating a range of issues—from how stablecoins should be treated within the broader financial system to who bears responsibility for liquidity and resilience during stress events. A point of friction is whether yield-bearing stablecoins should be permitted under the same framework as traditional bank deposits or whether separate regimes are warranted to prevent regulatory arbitrage.

Advertisement

Industry dynamics reflect these policy tensions. Dimon and Coinbase CEO Brian Armstrong have publicly traded criticisms over the direction of crypto regulation, underscoring divergent views on how to balance innovation with safety. Banking groups, including the American Bankers Association, have prioritized a push against yield-bearing stablecoins and have pressed for clarity and adherence to robust guardrails. The policy debate will likely influence how quickly institutions feel comfortable engaging in tokenized ecosystems and whether regulated banks will collaborate with on-chain infrastructure providers like Kinexys.

From a market perspective, the size and growth of the stablecoin sector remain central to the regulatory calculus. Data from industry trackers show the stablecoin market reaching into the hundreds of billions, with quarterly measurements illustrating continued expansion. Such momentum helps explain why lawmakers view stability and transparency as prerequisites for broader mainstream adoption, even as commentators remain wary of new forms of credit-like yield in non-bank structures.

What to watch next for JPMorgan and the broader ecosystem

As JPMorgan delegates its capital toward AI and data-driven processes while steering Kinexys toward broader tokenization, the coming quarters will reveal how aggressively the bank pursues asset tokenization beyond cash settlements. The pace of client onboarding, the breadth of asset classes brought under Kinexys, and the platform’s performance at scale will be critical indicators of the strategy’s viability.

On the regulatory front, observers will be listening for any concrete progress on market-structure legislation and for further clarity on stablecoin regulation. If lawmakers advance a clear, stability-focused framework, the adoption curve for tokenized assets and related financial products could accelerate across traditional institutions and fintechs alike. Conversely, continued stalemate or restrictive provisions could incentivize firms to pursue more private, permissioned models or to rely on bespoke bilateral arrangements, potentially slowing broad-market participation.

Advertisement

Beyond JPMorgan, the broader market will keep a close eye on how other banks, asset managers and technology firms calibrate their tokenization ambitions. Kinexys could become a reference case for how a major financial institution balances internal AI-driven efficiency with the external opportunities of asset tokenization, a dynamic that almost certainly will influence how investors assess risk, liquidity and regulatory exposure in fiat-to-token and token-to-token workflows.

In the near term, investors and industry watchers should watch for additional client announcements from Kinexys and any concrete expansions into new asset classes. They should also pay attention to regulatory signals—whether Congress pushes forward with comprehensive market-structure bills or if separate proposals gain traction—that could either lower or raise the barriers to institutional participation in tokenized ecosystems. For now, JPMorgan’s path suggests a dual bet: keep strengthening core AI-enabled operations while pursuing a tokenization play that could redefine liquidity and settlement for institutional finance.

The ongoing dialogue between technology, finance and policy will shape the next phase of crypto adoption. As Dimon and his peers navigate this evolving terrain, the question remains: how swiftly will tokenization scale from pilot programs to widely used financial infrastructure, and what will be the precise mix of regulation and innovation that enables it?

Risk & affiliate notice: Crypto assets are volatile and capital is at risk. This article may contain affiliate links. Read full disclosure

NewsBeat4 days ago

NewsBeat4 days ago

Business4 days ago

Business4 days ago

Fashion3 days ago

Fashion3 days ago

Crypto World5 days ago

Crypto World5 days ago

Business22 hours ago

Business22 hours ago

Sports2 days ago

Sports2 days ago

Business5 days ago

Business5 days ago

Tech7 days ago

Tech7 days ago

Sports6 days ago

Sports6 days ago

Tech7 days ago

Tech7 days ago

Sports7 days ago

Sports7 days ago

Crypto World7 days ago

Crypto World7 days ago

Tech6 days ago

Tech6 days ago

Politics7 days ago

Politics7 days ago

Tech7 days ago

Tech7 days ago

Business7 days ago

Business7 days ago

Crypto World6 days ago

Crypto World6 days ago

You must be logged in to post a comment Login