Crypto World

Bitcoin Price Drops Follow BOJ Rate Hikes: Is Another Crash Developing?

Since 2024, Bitcoin (BTC) has posted four major corrections after interest rate hikes by the Bank of Japan (BOJ), with declines ranging from 18% to 28%. This dynamic places renewed attention on the BOJ’s June 16 policy decision.

Data currently point to a variety of pressures on BTC, with BTC whale distribution and exchange inflows possibly carrying more weight than Japanese monetary policy.

BOJ hikes and Bitcoin drawdowns: Will history repeat?

The relationship between BOJ policy and Bitcoin has gained attention because each rate increase since Japan ended its negative interest rate policy has been followed by a sizable correction.

Following the March 19, 2024, hike, Bitcoin corrected by 18%. The July 31, 2024, increase preceded a 18.5% decline.

After the Jan. 24, 2025, hike, Bitcoin fell nearly 25%, while the Dec. 19, 2025, decision was followed by a 28% drawdown.

Across the four events, Bitcoin’s average decline was 22.4%.

BTC/USD, one-week chart. Source: Cointelegraph/TradingView

The sell-offs did not occur under identical conditions. The March 2024 correction followed Bitcoin’s breakout to new all-time highs during the spot Bitcoin exchange-traded fund (ETF) cycle. The July 2024 decline followed months of consolidation below peak levels and coincided with the sharp unwind of the yen carry trade, which affected global markets.

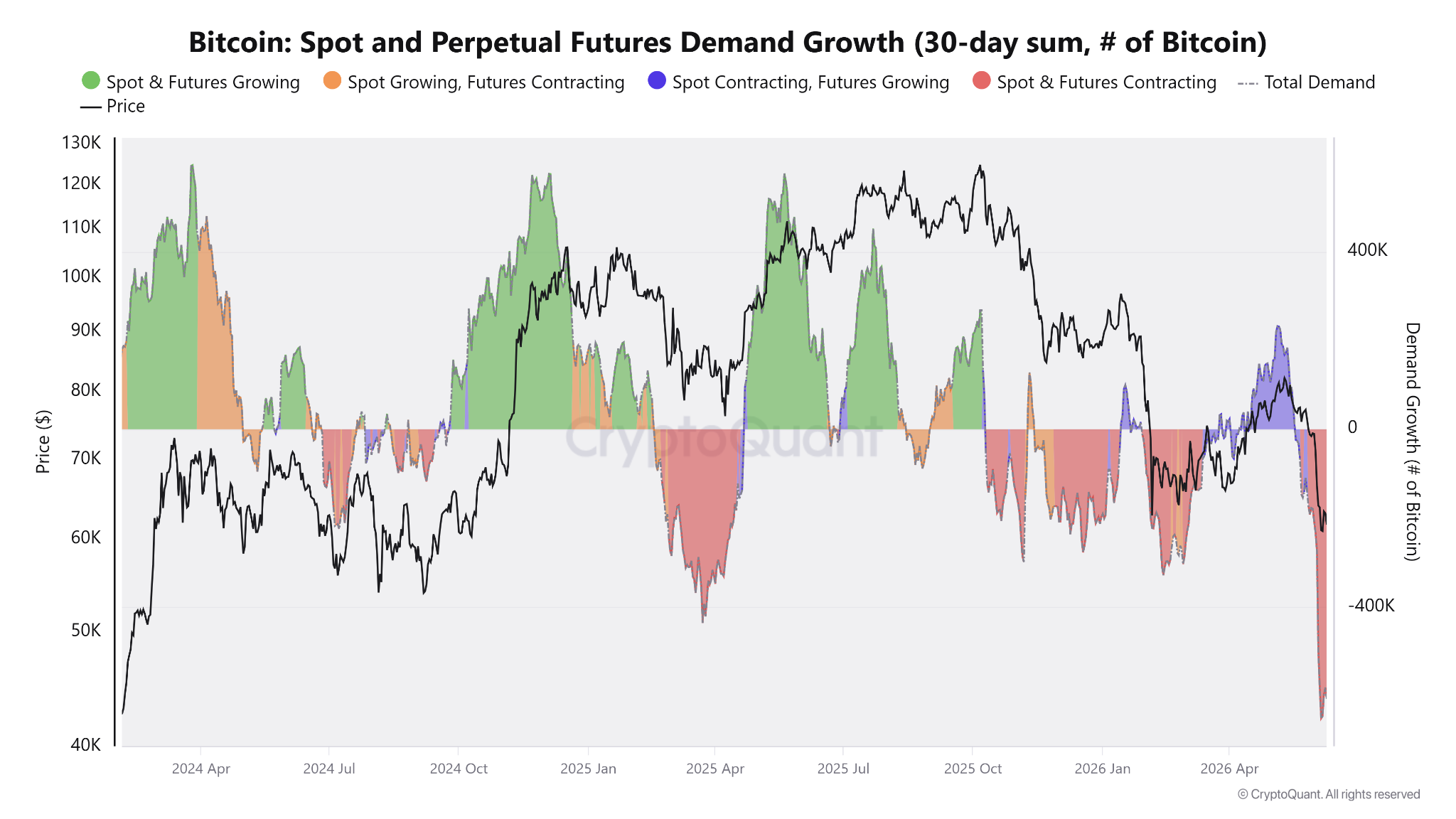

The January and December 2025 drawdowns followed extended rallies and periods of contraction for both BTC spot and futures 30-day demand.

BTC: spot and perpetual futures demand growth contraction. Source: CryptoQuant

The relationship between BOJ policy and Bitcoin is often linked to the yen carry trade. For years, investors borrowed yen at low rates and deployed that capital into higher-yielding assets, including stocks and cryptocurrencies.

When the BOJ raises rates, some of those positions can be reduced, weighing on risk assets. The July 2024 hike coincided with one of the largest carry-trade unwinds in recent years and a sharp sell-off across global markets, not only BTC.

The influence of that particular condition appears smaller today. The BOJ has already raised rates to 0.75% from -0.1% in March 2024, while Japan’s 10-year government bond yield climbed to 2.68% from 0.63% over the same period.

Japan’s 10-year bond yield increase since 2024. Source: TradingEconomics

With Japan’s borrowing costs already higher than during the negative-rate era, each additional hike represents a smaller policy shift than the BOJ’s initial move away from ultra-loose monetary policy. The June 16 meeting would extend an existing tightening cycle rather than introduce a new one.

Likewise, market analyst Cryptic Trades noted that concerns about a renewed yen carry-trade unwind are overblown, arguing that Japan has effectively moved away from its deflationary policy framework in 2024. The analyst added,

“The Yen Carry Trade has been dead ever since 2024. It is also a BIG nothing burger for the markets.”

Related: Bitcoin price may slide toward $30K as institutions dump 450% of daily BTC supply

BTC whales add to the pressure

While the BOJ meeting is a macro event that traders may monitor, onchain data points to a more immediate source of pressure.

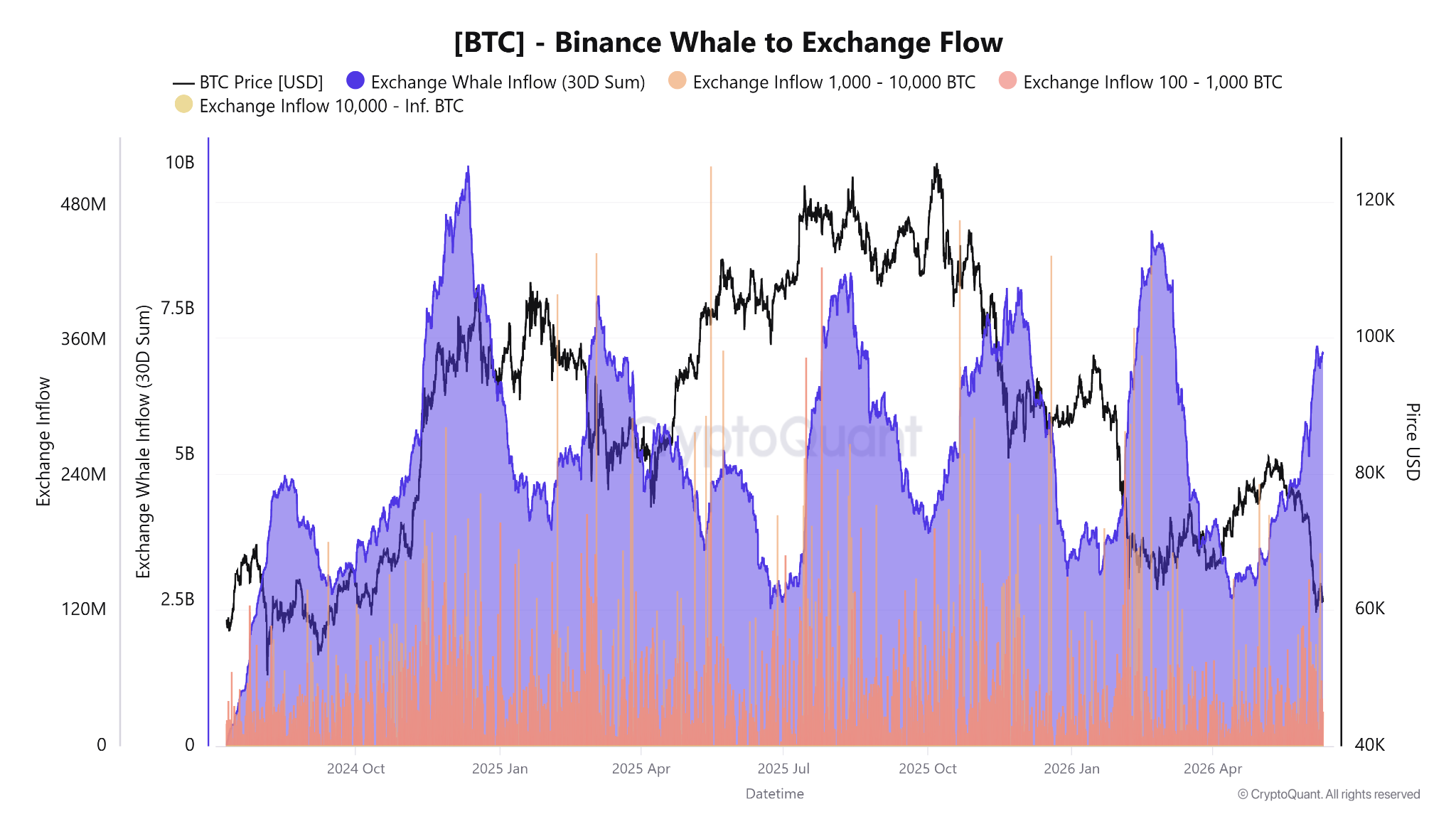

Crypto analyst MorenoDV noted that Binance has recorded rising BTC inflows from wallets holding 100–1,000 BTC and 1,000–10,000 BTC since the sell-off began in early June. As a result, the exchange’s 30-day whale inflow sum has climbed to $6.6 billion.

Bitcoin whale to exchange flow. Source: CryptoQuant

The pressure is already visible in realized activity. Short- and long-term whales have collectively locked in more than $2.5 billion in losses during the decline, indicating that some large holders have actively reduced exposure.

Short-term whales appear particularly vulnerable. The cohort is carrying roughly $16 billion in unrealized losses after briefly returning to profit for around 10 days in early May. Those positions now sit close to break-even levels, creating a potential source of supply during rebounds. MorenoDV said,

“Taken together, these three readings describe the stress profile of a late-stage bear market: capitulating whales, distribution into weakness, and a fragile short-term cohort with its finger on the trigger.”

Related: Bitcoin may act as a ‘canary in the coal mine’ as risk-off pressure spreads: Bitwise

Apple is facing a federal lawsuit from three users who allege fraudulent Sparrow Wallet applications distributed through its App Store caused about $1.835 million in Bitcoin losses.

Summary

- Three users allege Sparrow apps drained $1.835 million in Bitcoin between May and August 2025.

- Sparrow’s official downloads support macOS, Windows and Linux, but no iOS application exists at present.

- Apple says it promptly removed impersonating apps and terminated developer accounts linked to those listings.

James Ramirez, Christopher Ellis and Jalen Delgado filed the 54-page complaint on July 24 in the U.S. District Court for the Northern District of California. The allegations have not been tested in court, and Apple has not yet filed a public response in the case.

The public docket identifies the action as Ramirez et al. v. Apple Inc., case 5:26-cv-07713. It currently shows the complaint, a civil cover sheet and an unexecuted summons filing. No judge has ruled on Apple’s responsibility for the alleged thefts.

Fake Sparrow apps allegedly captured seed phrases

The complaint says Delgado downloaded a spoof application around May 1, 2025 and lost about $120,000. Ramirez allegedly downloaded another on July 25 and lost 7.4 BTC, valued near $875,000. Ellis allegedly lost about $840,000 after using the app around August 3. Each user says the software requested a wallet seed phrase before transferring Bitcoin to attacker-controlled addresses.

Sparrow’s official website describes the product as a desktop Bitcoin wallet. Its current download page lists versions for macOS, Windows and Linux, but none for iOS. Entering a recovery phrase into malicious software gives an attacker the credentials needed to control the associated wallet.

Apple says it removed impersonating apps

Apple told MacRumors that it acted quickly to remove applications impersonating Sparrow Wallet and terminated developer accounts connected to them. The company also pointed users to its reporting tools and said it takes action against applications that breach App Store rules.

Apple’s published review rules prohibit applications from impersonating another service or using another developer’s brand without permission. The company says every app is reviewed and describes the App Store as a safe and trusted marketplace. Apple separately reported blocking more than $2.2 billion in potentially fraudulent transactions and rejecting more than two million problematic submissions during 2025.

The plaintiffs argue that Apple’s safety marketing led them to believe applications offered through the App Store had been properly vetted. Their complaint brings claims under California’s Consumers Legal Remedies Act, Louisiana’s unfair-trade law and Massachusetts consumer-protection law. It also alleges fraudulent and negligent misrepresentation, concealment and failures to warn.

Those claims remain allegations. The plaintiffs seek a jury trial, reimbursement of lost digital assets, compensatory and enhanced damages where permitted, restitution and injunctive relief. Apple can contest both the factual account and whether its App Store representations created legal responsibility for losses caused by third-party scammers.

Previous crypto wallet scams add context

The dispute follows other cases in which fake wallet software reached major app marketplaces. Notably,a fraudulent Ledger Live application on Apple’s App Store allegedly stole at least $9.5 million from more than 50 users in April. On-chain investigator ZachXBT traced funds from that separate campaign through numerous exchange deposit addresses. The incident does not prove the claims in the Sparrow case, but it shows the recurring method.

However, fake Phantom, Rabby and UniSat applications have also appeared in app-store searches or listings. The common tactic is to imitate a recognised wallet and request a recovery phrase that the genuine provider would not need during routine use.

The next formal step is service of the complaint and Apple’s response, which could take the form of an answer or a motion seeking dismissal. The public docket did not show a hearing date or merits ruling when checked. Any award, product change or finding that Apple is liable would require a court decision or settlement.

After rallying on Monday to a multi-day peak following the weekend de-escalation on the war front, bitcoin was violently rejected and driven south by almost three grand in hours.

Most altcoins have joined the painful ride, including ETH, which has dropped below $1,900, and HYPE, which has lost the most value out of the larger caps.

BTC Rejected

The primary cryptocurrency had a good run last week, in which it rocketed from $63,750 to a monthly peak of $67,000 in the span of 36 hours. However, it couldn’t breach that line and dipped to $64,750 on Wednesday and all the way down to its starting point at $63,750 on Friday.

The bulls intervened after this decline and helped it recover some ground to $64,000 during the weekend, when it finally calmed. The impact of the de-escalation news on the Middle Eastern attacks was expected to be felt on Monday, and it didn’t disappoint. Bitcoin jumped to $65,600 on a couple of occasions for the first time since Friday.

However, it was rejected once again, and the subsequent ride south was quite brutal. As reported earlier today, BTC slumped to $63,000 for the first time in 10 days, leaving roughly $700 million in liquidations.

Although it has rebounded slightly to $63,400 as of press time, it remains 3% down on the day. Its market cap has dropped to $1.720 trillion, while its dominance over the alts remains below 57% on CG.

Alts Bleed, Too

Ethereum rode the green wave hard yesterday, jumping to a two-month peak at $1,980. It was stopped there, and a 4.2% daily decline has driven it south by $100. XRP and SOL have decreased by similar percentages, while HYPE has plummeted by 8% to $55. ZEC, LINK, XLM, and ADA are also deep in the red.

The biggest loser today is Audiera’s BEAT. A 25% drop has pushed it south to $2.74. NEAR (-10%), SHIB (-9%), and PI (-9%) follow suit.

The cumulative market cap of all crypto assets has dumped from $2.330 trillion to $2.250 trillion as of now, losing $80 billion in just a day.

The post Crypto Markets Lose $80 Billion as Bitcoin (BTC) Dumps to $63K: Market Watch appeared first on CryptoPotato.

Crypto World

WEEX TradFi Trading Fest is Live: Trade Gold, Oil & Stocks with 0 Slippage and Win Free USDT

WEEX kicks off the TradFi Trading Fest from July 27 to August 10, 2026, offering new user rewards, first-trade protection, zero-slippage trading, lucky draws, and a 50,000 USDT exclusive prize pool for TradFi futures traders.

TL;DR

- What’s launching: WEEX’s TradFi Trading Fest runs from July 27, 2026, 16:00 to August 10, 2026, 23:59 (UTC+8), rewarding users for trading TradFi (traditional finance) futures — gold, silver, oil, tokenized stocks, and indices — with USDT.

- New User Reward: First deposit > 100 USDT + trade ≥ 100 USDT = 200 USDT position airdrop (5 USDT × 40× leverage), capped at the first 5,000 users.

- First-Trade Protection: Up to 20 USDT in trial funds (50% offset) if a user’s first TradFi futures trade results in a loss.

- Zero Slippage Trading: Daily perk using the “Guaranteed Price” feature across 31 eligible TradFi pairs.

- Lucky Draw: Tiered entries based on cumulative trading volume, from 20,000 USDT up to 1,000,000 USDT.

- Exclusive Prize Pool: Trade ≥ 200,000 USDT in TradFi futures to share a 50,000 USDT prize pool.

WEEX, a leading global crypto exchange, has officially launched the TradFi Trading Fest, a two-week campaign running from July 27, 2026, 16:00 to August 10, 2026, 23:59 (UTC+8). The event is designed to give both new and existing users a smoother, more rewarding entry point into trading TradFi futures — including gold, silver, oil, major equities, and index-linked instruments — directly on the WEEX platform. With five distinct reward mechanisms stacked together, from onboarding bonuses to guaranteed-price execution and a substantial shared prize pool, the campaign reflects WEEX’s ongoing push to bridge traditional financial markets with the flexibility and accessibility of crypto-native trading infrastructure.

Users are invited to sign up now and start exploring the full range of benefits on offer.

Five Ways to Earn During the TradFi Trading Fest

- New User Reward: New users who make a first deposit of more than 100 USDT and complete at least 100 USDT in TradFi futures trading volume will receive a 200 USDT position airdrop (5 USDT × 40× leverage). This reward is available on a first-come, first-served basis, capped at the first 5,000 users — giving newcomers a low-barrier way to try TradFi futures with extra trading power from day one.

- First-Trade Protection: Trading always carries risk, especially for first-timers. To ease that concern, WEEX is offering up to 20 USDT in trial funds (50% offset) to any user whose very first TradFi futures trade results in a loss. This safety net lets new traders test strategies and get familiar with the market without the full weight of downside risk on their opening trade.

- Zero Slippage Trading (Daily Perk): Slippage can quietly erode returns, particularly in fast-moving markets. Throughout the event, users trading eligible TradFi futures pairs can activate the “Guaranteed Price” feature to enjoy zero slippage on every trade — a daily perk that ensures execution certainty and helps traders stick to their intended entry and exit levels.

- Lucky Draw with Guaranteed Rewards: Every trader has a shot at extra rewards through a tiered lucky draw based on cumulative TradFi futures trading volume during the event:

| Cumulative Trading Volume | Draw Entries |

| 20,000 USDT | 1 |

| 50,000 USDT | 2 |

| 150,000 USDT | 3 |

| 500,000 USDT | 5 |

| 1,000,000 USDT | 5 |

The more users trade, the more chances they get to win — rewarding both casual participants and high-volume traders alike.

- Exclusive 50,000 USDT Prize Pool: For traders aiming higher, reaching a total TradFi futures trading volume of 200,000 USDT or more qualifies them to share in an exclusive 50,000 USDT prize pool, adding an extra layer of upside for active, high-conviction participants.

Eligible TradFi futures pairs for the zero-slippage perk, lucky draw, and prize pool include: XAUTUSDT, PAXGUSDT, XAGUSDT, CLUSDT, BZUSDT, SPCXUSDT, NATGASUSDT, COPPERUSDT, MSTRUSDT, SOXLUSDT, QQQUSDT, EURUSDT, INTCUSDT, NVDAUSDT, SPYUSDT, ORCLUSDT, AAPLUSDT, MSFTUSDT, DRAMUSDT, GOOGLUSDT, AMZNUSDT, EWYUSDT, TSLAUSDT, CRCLUSDT, SP500USDT, MRVLUSDT, METAUSDT, SAMSUNGUSDT, IBMUSDT, RKLBUSDT, PLTRUSDT, and BABAUSDT.

How to Participate in the WEEX TradFi Trading Fest

Getting involved is straightforward:

- Click “Sign Up” to register for the event — participation requires prior sign-up.

- “New users” refers to accounts registered during the event period; market makers and institutional accounts are not eligible to participate or receive rewards.

- Rewards across the five tasks are calculated independently — users who meet the conditions for multiple tasks simultaneously can claim multiple rewards.

- All rewards are distributed on a first-come, first-served basis in order of participation, while supplies last.

Who Should Join? Is TradFi Crypto Trading Right for You?

The TradFi Trading Fest is designed with a few types of traders in mind:

- Crypto-native traders seeking diversification. If you already trade USDT-margined futures and want exposure to macro themes — inflation, interest rates, energy markets, equity performance — without leaving your existing workflow, TradFi futures let you apply the same position sizing, stop-loss, and leverage logic to gold, oil, or stock-related products.

- New WEEX users exploring the platform. The new user reward and first-trade protection are built specifically to lower the risk of a first attempt, making this a low-pressure entry point for anyone curious about TradFi crypto trading.

- Active traders chasing volume-based upside. Traders who already run higher volumes can stack the lucky draw and exclusive prize pool on top of their regular activity for extra rewards.

- Traders who value execution certainty. Anyone concerned about slippage eating into returns during volatile sessions will benefit from the zero-slippage “Guaranteed Price” feature.

Bridging Crypto and TradFi: WEEX’s Strategic Push and the Road Ahead

Traditional access to markets like gold, oil, and equities has historically required a brokerage account, bank-linked funding, and adherence to standard exchange trading hours. WEEX TradFi removes each of those requirements: users fund their account with USDT — via on-chain transfer, OTC purchase, or internal transfer — and open positions directly from their existing WEEX futures balance.

Unlike conventional exchanges bound by fixed trading hours, WEEX TradFi is accessible 24 hours a day, seven days a week; liquidity and spreads are typically tightest during traditional market hours and session overlaps, but users are never restricted to trading only when markets like the NYSE or the London Bullion Market are formally open.

The TradFi Trading Fest reflects this broader strategy of bridging crypto and TradFi under one platform. By combining onboarding incentives, downside protection, execution-quality guarantees, and volume-based rewards into a single campaign, WEEX aims to give traders — whether new to the platform or seasoned participants — a compelling reason to explore TradFi crypto markets alongside their existing portfolios.

As demand grows for unified, 24/7 access to global markets, campaigns like this reflect WEEX’s continued investment in expanding its TradFi futures offering and building a more accessible, security-conscious trading experience for its global user base.

Disclaimer: WEEX reserves the right to modify the event rules, and to cancel, extend, terminate, or suspend the event, as well as adjust reward standards, at any time without prior notice. Please refer to the official WEEX website for the most up-to-date and complete event terms. This article is for informational purposes only and does not constitute investment advice. Trading futures involves significant risk; please trade responsibly and within your risk tolerance.

About WEEX

Founded in 2018, WEEX has developed into a global crypto exchange with over 6.2 million users across more than 150 countries. The platform emphasizes security, liquidity, and usability, providing over 1,200 spot trading pairs and offering up to 400x leverage in crypto futures trading. In addition to the traditional spot and derivatives markets, WEEX is expanding rapidly in the AI era delivering real time AI news, empowering users with AI trading tools, and exploring innovative trade to earn models that make intelligent trading more accessible to everyone. Its 1,000 BTC Protection Fund further strengthens asset safety and transparency, while features such as copy trading and advanced trading tools allow users to follow professional traders and experience a more efficient, intelligent trading journey.

Follow WEEX on social media

X | Instagram | Tiktok | Youtube | Discord | Telegram

The post WEEX TradFi Trading Fest is Live: Trade Gold, Oil & Stocks with 0 Slippage and Win Free USDT appeared first on BeInCrypto.

The National Football League has urged the U.S. Commodity Futures Trading Commission to tighten its proposed prediction market rules, arguing that stronger safeguards are needed to protect game integrity and consumers.

Summary

- The NFL has asked the CFTC to tighten its proposed prediction market rules to strengthen game integrity and consumer protections.

- The league wants stricter limits on sports contracts that could be manipulated or rely on insider information.

- The CFTC is developing a federal framework for event contracts while requiring exchanges to provide more detailed product filings.

- The request comes as the CFTC continues defending federal oversight of prediction markets against state-level restrictions.

According to The Closing Line, which obtained a July 27 letter sent to CFTC Chair Michael Selig, the NFL told the regulator that its draft framework for prediction markets contains useful proposals but does not go far enough to address risks tied to sports-based event contracts.

“The NFL’s highest priority is preserving the integrity of our games,” the league wrote in the letter published by The Closing Line. It added that maintaining that integrity is also important for the “stable and orderly administration” of event contracts linked to NFL games and for protecting traders who participate in those markets.

The submission comes as the CFTC considers public feedback on proposed amendments to Rule 40.11, which would establish a federal framework for reviewing event contracts tied to gaming, war, terrorism, assassination and unlawful activities. The comment period closed on July 27 after attracting responses from sports leagues, exchanges and crypto industry groups.

NFL wants tighter limits on sports prediction contracts

Among its recommendations, the NFL called for stricter restrictions on contracts that could be influenced by a single participant, depend heavily on officiating decisions or involve outcomes that may become known before the public, according to The Closing Line.

The league also asked the CFTC to narrow its proposed definition of permissible contracts. According to the publication, the NFL argued that the agency should better distinguish legitimate event contracts from activities that are effectively gambling.

Another concern involved the CFTC’s proposed 10-day review period for newly self-certified contracts. The NFL reportedly argued that the review window is too short and could allow contracts to remain listed before regulators have enough time to assess them.

Awards markets also drew criticism. The league questioned why contracts tied to honors such as “Offensive Player of the Year” should be allowed simply because their outcomes are decided by a voting panel.

On market integrity, the NFL asked for explicit rules governing the use of material non-public information. It also recommended mandatory league-specific prohibited bettor lists instead of allowing individual platforms to develop their own monitoring systems.

The letter repeated several recommendations the league has made previously, including a ban on margin trading for sports event contracts, advertising restrictions and a minimum participation age of 21.

CFTC has continued building a federal prediction market framework

The NFL’s latest submission arrives as the CFTC has adopted a more structured approach toward prediction markets rather than seeking broad prohibitions.

Earlier this month, the agency’s Division of Market Oversight issued its second compliance advisory of the year, warning exchanges against submitting broad, template-style self-certifications covering large groups of event contracts. Instead, designated contract markets must provide contract-specific terms, settlement methods, data sources and legal analysis for each product they intend to list.

The July 24 advisory did not eliminate the self-certification process. Exchanges may still introduce qualifying event contracts without prior Commission approval when they comply with the Commodity Exchange Act and CFTC rules. However, the agency said filings covering open-ended groups of contracts without enough product-level detail limit its ability to review settlement procedures, manipulation risks and legal compliance.

The guidance followed a March advisory reminding exchanges that they act as front-line regulators responsible for reviewing whether contracts can be manipulated and whether settlement sources are reliable before listing products.

At the same time, the Commission is proposing amendments to Rule 40.11 that would create a three-step review process for contracts linked to activities identified in the Commodity Exchange Act. Under the proposal, regulators would first determine whether a product qualifies as an event contract, then assess whether its settlement depends on activities such as gaming or unlawful conduct before applying public-interest factors to decide whether the contract should proceed.

According to legal analysis from Ropes & Gray cited by crypto.news, the proposal would review contracts individually instead of prohibiting entire categories in advance while also distinguishing games from contests, placing elections and award events outside the proposed gaming definition.

League takes different position from some sports organizations

Unlike the National Hockey League and Major League Baseball, which have entered partnerships with prediction market platforms including Kalshi and Polymarket, the NFL has repeatedly argued for tighter oversight of sports-related event contracts.

In March, the league sent letters to Kalshi and Polymarket asking the companies to withdraw several sports contract offerings, continuing its position that sports prediction markets require stronger integrity protections.

By contrast, the CFTC under Chair Michael Selig has defended federally regulated prediction markets against state challenges while advancing formal rules for the industry. Since his appointment in 2025, Selig has supported treating qualifying prediction markets as legitimate derivatives subject to federal oversight rather than state gambling laws.

Recent court filings also show the Commission defending that position in litigation against Minnesota and win. The agency argued that the law conflicts with the federal derivatives framework established under the Commodity Exchange Act.

Kalshi and Polymarket have filed similar requests seeking temporary relief while their own legal challenges proceed. The dispute could determine whether federally regulated prediction markets remain available nationwide or become subject to individual state gambling restrictions.

The NFL’s comments arrive as prediction markets continue expanding across sports, politics, economics and current events.

CFTC data cited in its March rulemaking notice showed registered exchanges listed an average of about five event contracts each year between 2006 and 2020. That number increased to 131 contracts in 2021 before reaching roughly 1,600 new contracts during 2025.

More recent testimony referenced has estimated that CFTC-regulated prediction markets handled more than $25 billion in trading volume during 2025. The same testimony said daily listings on one major platform increased from about 1,600 contracts in April 2025 to roughly 162,000 by April 2026.

Apple is being sued by three customers who allege they suffered a combined loss of about $1.8 million after installing a fraudulent “Bitcoin wallet” app from the App Store. The lawsuit, filed Friday in the U.S. District Court for the Northern District of California, claims Apple failed to properly review and monitor applications even as it markets the App Store as a trusted marketplace.

According to the complaint, the victims entered their Bitcoin seed phrases into the fake wallet, enabling scammers to move funds. The plaintiffs say their losses occurred during 2025, with reported losses of approximately $875,000, $840,000, and $120,000 across the three accounts, respectively.

Key takeaways

- Three plaintiffs allege App Store controls were insufficient, leading to seed-phrase theft via a fake Bitcoin wallet app.

- The complaint states total claimed losses reached roughly $1.8 million during 2025.

- Apple says it removed apps impersonating Sparrow Wallet and terminated associated developer accounts.

- Sparrow Wallet has no official iOS app, which the filing and related developer commentary indicate should have mattered to users.

Lawsuit alleges App Store oversight failures

The lawsuit names plaintiffs James Ramirez, Christopher Ellis, and Jalen Delgado. The filing alleges Apple did not adequately review and monitor applications despite promoting the App Store as a secure channel for users to obtain software. A copy of the complaint was obtained by MacRumors, which reported on the case.

The core allegation is straightforward and common to seed-phrase theft scams: the victims allegedly provided their seed phrases to the fraudulent application, after which scammers transferred their Bitcoin. Each plaintiff reported losses of different magnitudes during 2025, culminating in the combined figure cited in the complaint.

The broader issue raised by the plaintiffs is less about one specific scam and more about whether platform-level processes—review, monitoring, and enforcement—were strong enough to prevent an impersonation-style wallet from reaching users.

Sparrow Wallet impersonation and the iOS gap

MacRumors’ coverage ties the alleged scam to Sparrow Wallet impersonation. Sparrow Wallet is described as being available for Windows, macOS, and Linux, and the wallet’s developer, Craig Raw, previously criticized Apple over fake versions of the application appearing on the App Store.

Crucially for users, Sparrow Wallet has no official iOS app. That absence is significant because impersonation scams typically rely on confusion—users may assume a popular wallet exists on their device and may not realize that the genuine developer did not provide an iOS version.

While the lawsuit centers on the plaintiffs’ alleged experience, this iOS gap also points to a practical takeaway: wallet users should be cautious about any “official” claim for seed-based wallets appearing on mobile app stores—especially when the known developer ecosystem indicates a different set of supported platforms.

Apple says it removed the apps and took enforcement action

In response to MacRumors, Apple said it had removed apps impersonating Sparrow Wallet and terminated developer accounts linked to those apps. Apple also stated that developers and users can report applications that violate App Store guidelines, and that it takes action against apps that do not comply with its rules.

This response frames Apple’s position as enforcement after detection, rather than an admission that the App Store’s gatekeeping was insufficient before the scam was live. For investors, traders, and builders, the tension here is important: seed-phrase scams produce irreversible outcomes for users, so the debate naturally turns to how quickly and how effectively malicious impersonators are identified and removed.

The case therefore sets up a likely factual dispute over timing and adequacy—what Apple knew, when it acted, and whether its review and monitoring efforts met the standard the plaintiffs argue should apply to a marketplace that promotes itself as trustworthy.

Why this matters for crypto users and the broader app ecosystem

Seed-phrase entry scams are among the most damaging categories of fraud in the crypto ecosystem because they transfer control of funds in a way that is difficult for users to reverse. This lawsuit highlights a recurring vulnerability: users often treat app stores as inherently safer than installing software from unknown sources, even though wallet-related attacks can still pass through if impersonation and branding are effective.

For crypto users, the dispute underscores several risk-control habits that remain relevant regardless of what the court ultimately decides. First, users should verify whether a wallet exists on iOS at all—particularly when a developer’s published support list does not include iOS. Second, users should avoid entering seed phrases into any app that was not directly sourced from official developer channels. Third, even if a platform removes malicious apps later, users may already have lost funds by the time enforcement occurs.

For app developers and wallet maintainers, the case is also a reminder that brand impersonation can cause real financial harm quickly, and that monitoring and reporting mechanisms may need to be paired with more proactive user education—especially around what is and isn’t available on mobile.

Readers should watch next for how the court addresses the alleged timeline of the fraudulent apps and what evidence the plaintiffs use to argue that App Store processes were inadequate prior to the losses. Apple’s response suggests it will emphasize removals and enforcement efforts, so the factual record on detection and action timing may be the central battleground.

Bitcoin (BTC) has regained some poise, recovering from Asian session lows despite signs of worsening risk aversion in equity markets.

The leading cryptocurrency by market value traded at around $63,500 as of this writing, up from the low of $63,065 in Asia, according to CoinDesk data. Prices are still down by 0.3% since midnight UTC and by nearly 3% over the past 24 hours.

In the meantime, e-mini futures tied to Nasdaq have slipped to 27,930 points, the lowest since May, and are down 1.2% for the week, having peaked near 31,000 in June. On Monday, shares in NVDA, the index heavyweight, fell by nearly 5%.

Earlier today, South Korea’s Kospi index tanked by 10%, alongside relatively more measured declines in other regional indices, such as Japan’s Nikkei.

Readiness matters because quantum computing poses a real long-term risk to the cryptography that underpins modern finance. Banks are especially vulnerable to “harvest now, decrypt later” attacks, which the Bank for International Settlements’ Project Leap has flagged as an immediate threat to the financial system.

The harvest now, decrypt later means that malicious entities could be stockpiling encrypted banking data today, waiting for the quantum hardware to catch up. Blockchains like Bitcoin and Ethereum face the same risk, which could leave modern finance exposed to a long-term security risk.

While practical, large-scale quantum machines capable of breaking bank security and blockchains such as Bitcoin do not exist today, estimates for when that risk could become real start in as early as 2029.

The HKMA is aiming for a perfect 10 on the Quantum Preparedness Index by 2030. To get there, the regulator is rolling out practical tools: a post-quantum cryptography toolkit being developed with Hong Kong University of Science and Technology’s business school, plus a series of workshops to help banks build skills, improve crypto agility and explore quantum opportunities responsibly.

It’s not alone. President Donald Trump recently signed two executive orders. One aims to accelerate U.S. quantum computing development, with a goal of producing a machine powerful enough for scientific research by 2028. The other calls for the federal government’s migration to post-quantum cryptography by 2030-31.

Bitcoin traded near $63,490 on July 28 after falling below $64,000 during a broad risk-off move across Asian markets.

Summary

- Bitcoin traded near $63,490, down 2.85%, as South Korea’s KOSPI triggered a circuit breaker Tuesday.

- $11.64 million left U.S. spot Bitcoin ETFs Monday, while IBIT posted the largest fund outflow.

- Wallets holding 10 to 10,000 BTC accumulated 19,696 coins during the latest eight-day period tracked.

According to crypto.news market data, BTC dropped about 2.85% over 24 hours, with a daily range between approximately $63,055 and $65,546 at the time checked.

The decline began after U.S. markets closed Monday and accelerated as South Korean technology shares sold off. Bitcoin dropped from nearly $65,000 to around $63,200 before recovering slightly, while ether, XRP and solana also weakened.

The move places BTC back inside the lower half of its recent $60,000–$66,000 range. Technical momentum has softened, although compressed volatility, whale accumulation and the approaching Federal Reserve decision leave the next direction unsettled.

Asian equity losses added pressure to Bitcoin price

South Korea’s KOSPI fell more than 8% on Tuesday morning, forcing the Korea Exchange to suspend marketwide trading for 20 minutes. The Level 1 circuit breaker was activated after the decline remained above the required threshold for one minute.

Selling continued after the halt. The KOSPI fell almost 10% during the session, while Samsung Electronics and SK Hynix lost more than 12%. Concerns centred on heavy AI spending, financing risks and growing competition from Chinese semiconductor companies.

Japan’s Nikkei also fell about 4%, following a 2.2% decline in the Philadelphia Semiconductor Index during Monday’s U.S. session. Nvidia had dropped 5%, adding another negative signal for technology-linked risk assets.

Bitcoin often trades alongside equities when selling is driven by interest rates, liquidity or broad macro concerns. However, the relationship is not constant. Bitcoin may decouple when pressure is limited to company earnings or sector-specific capital-spending concerns.

Tuesday’s price action suggests traders initially treated the Asian selloff as a wider risk event. It does not prove that the KOSPI decline alone caused Bitcoin’s fall, because Fed expectations, ETF flows and geopolitical developments were moving simultaneously.

Bitcoin remains trapped between $60,000 and $66,000

The BTC/USDT daily chart places Bitcoin near $63,500 after repeated failures to establish support above $65,000–$66,000. Price has consolidated since June’s sharp decline, but it remains in a broader downtrend from the previous peak above $100,000.

The relative strength index on the supplied chart stands at 46.77, below its moving average of 53.49. An RSI reading below 50 shows that short-term momentum has moved slightly towards sellers, although it remains well above the traditional oversold level of 30.

Bitcoin price chart, source: crypto.news

The moving average convergence divergence indicator has also weakened. Its histogram is negative at about minus 104.93, while the MACD line near 219.58 remains below the signal line around 324.51. That structure shows that the earlier July recovery has lost momentum.

Ali Martinez said Bitcoin’s three-day Bollinger Bands were beginning to squeeze. Bollinger compression usually reflects falling realised volatility and can precede a larger move, but it does not establish whether the eventual break will be higher or lower.

Crypto Patel separately argued that BTC had broken trendline support, retested approximately $65,600 and faced rejection. His bearish scenario targets the 0.618 Fibonacci area near $61,000 while price remains below reclaimed resistance. That level is an analyst projection, not a confirmed destination.

The chart therefore presents three immediate zones. Bitcoin must recover $65,000–$66,000 to improve its short-term structure. The $61,000 area is the first lower support identified by the bearish Fibonacci setup, while $60,000 remains the main floor of the broader consolidation.

A sustained daily close below $60,000 would weaken the range and expose the June lows near $58,000. Conversely, a close above $66,000 would invalidate part of the short-term bearish setup and place the July resistance near $67,181 back in focus.

Bitcoin reclaimed $65,000 on July 27 as falling oil prices briefly supported risk assets. That recovery failed to produce a breakout above the wider resistance band.

ETF selling conflicts with whale accumulation

U.S. spot Bitcoin ETFs recorded combined net outflows of $11.64 million on July 27, according to SoSoValue data. BlackRock’s iShares Bitcoin Trust recorded the largest individual fund outflow at $8.82 million.

Bitcoin spot ETF net inflow, Source: SoSoValue

The daily total was modest compared with the $240.08 million withdrawn on July 24. However, another negative session shows that institutional demand remains uneven rather than firmly returning to sustained inflows.

ETF activity has become an important source of marginal Bitcoin demand. Persistent inflows require authorised participants to create shares and source underlying exposure, while extended outflows can reduce that source of buying.

One session should not be treated as a trend. The four-week flow direction offers a more useful measure because individual daily totals can be affected by portfolio rebalancing, market making and settlement timing.

On-chain data present a different picture. Santiment said wallets holding between 10 and 10,000 BTC added 19,696 BTC over eight days. The analytics firm also said wallets holding less than 0.01 BTC showed weaker dip-buying activity.

The divergence suggests larger holders have accumulated while very small accounts have shown less urgency. Still, wallet cohorts do not map perfectly to individual investors. Large addresses can represent exchanges, custodians, funds or several customers rather than one whale.

Whale accumulation may provide support if those coins remain off exchanges. It becomes less constructive if large holders begin transferring inventory to trading platforms during price rebounds.

Fed, GDP and core PCE create a volatility window

The Federal Open Market Committee is meeting on July 28 and 29. At its previous meeting on June 17, the Fed kept the federal funds target range at 3.5%–3.75% and said inflation remained above its 2% goal.

Interest-rate markets assigned a roughly 38% probability to a 25-basis-point increase before the decision. That estimate represents market pricing and can change quickly before the announcement.

The July meeting is not marked as one accompanied by a new Summary of Economic Projections. Traders will therefore focus on the rate decision, the statement and the central bank’s language about inflation, energy prices and future tightening.

Thursday brings two major U.S. releases at 8:30 a.m. Eastern Time. The Bureau of Economic Analysis will publish its advance estimate of second-quarter gross domestic product and the June Personal Income and Outlays report, which contains the Fed’s preferred personal consumption expenditures inflation measures.

A rate increase or a more restrictive statement could lift Treasury yields and the dollar, conditions that often weigh on Bitcoin and other assets without fixed cash flows. Under that scenario, the $61,000 and $60,000 zones would become more exposed.

A rate hold accompanied by less restrictive guidance could help BTC challenge $65,000–$66,000 again. Cooler core PCE data on Thursday could support that move, while stronger inflation or GDP figures could renew expectations that rates must remain higher.

The outcomes should not be considered in isolation. A hold on Wednesday could initially lift Bitcoin, only for hotter inflation data to reverse the move on Thursday. Likewise, a restrictive Fed decision could be partly offset by weaker economic data the following day.

As previously reported, Bitcoin entered July with the Fed meeting and ETF flows as its main external catalysts. The earlier analysis identified $58,000 as major downside support, while the market has since established a nearer resistance zone around $65,000–$67,181.

Bitcoin needs confirmation outside the current range

Bitcoin’s immediate trend remains neutral to mildly bearish while price trades below $65,000–$66,000. The negative MACD histogram and sub-50 RSI support that reading, but neither indicator confirms a full breakdown while $60,000 remains intact.

A bullish confirmation would require a sustained close above $66,000, preferably accompanied by stronger spot volume and renewed ETF inflows. That would return attention to $67,181 and the higher resistance area near $68,000.

A bearish confirmation would require a decisive close below $60,000. Such a move would break the current consolidation and bring the late-June low near $58,000 back into view.

Until either boundary fails, Bitcoin remains range-bound. The Bollinger Band squeeze suggests that volatility may expand soon, while the Fed decision, GDP release and core PCE data provide clear events capable of triggering that expansion.

FAQs

Why is Bitcoin falling today?

Bitcoin weakened as South Korean and Japanese technology shares sold off, U.S. semiconductor stocks declined and traders prepared for the Federal Reserve decision. Fresh ETF outflows added another negative signal, although no single factor fully explains the move.

Is $60,000 the key Bitcoin support?

Yes. Bitcoin has repeatedly traded between approximately $60,000 and $66,000 since the June selloff. The $61,000 level may offer earlier Fibonacci support, but a daily close below $60,000 would represent a clearer range breakdown.

Does the Bollinger Band squeeze predict a rally?

No. A squeeze shows that volatility has contracted. It can precede a strong price move, but it does not predict the direction. Price confirmation above resistance or below support is still required.

When are the Fed, GDP and core PCE events?

The Fed’s two-day meeting ends Wednesday, July 29. The advance second-quarter GDP estimate and June Personal Income and Outlays report are scheduled for Thursday, July 30, at 8:30 a.m. Eastern Time.

It’s highly unusual for the largest derivatives exchange operator in the U.S., the CME Group, to be at war with its regulator, the Commodity Futures Trading Commission (CFTC) — but that’s now happening in a situation brought about by the agency’s decision to allow blockchain-based perpetual future products.

Last month, the CME sued the CFTC and its chairman, Mike Selig, challenging his decision to let the prediction markets platform Kalshi and cryptocurrency exchange Coinbase (COIN) list crypto perps, decentralized derivative contracts that allow users to speculate on the price of an asset with leverage and no expiration date.

Now, both sides await federal court action that could have significant influence on how the U.S. approaches the rapidly growing arena, with non-U.S. perps volume reportedly growing to $60 trillion in volume last year.

CME claims the agency is mislabeling the products, and therefore misapplying the law. Futures need an end date, and the products known as perps are designed for traders to be able to take a financial position on an asset’s future without any deadlines. The lawsuit argues these perps are harmful to its long-dated futures products and alleges that the CFTC’s sudden embrace of them did not consider the ramifications.

Mounting tension between the two entities ramped up around the start of Iran conflict, which saw interest spike in perpetual contracts on oil prices traded 24/7 on off-shore decentralized finance (DeFi) exchanges like Hyperliquid, as well as blockchain prediction markets hosting trades tied to the oil markets.

Those on the side of the CFTC’s reforming agenda in this highly politicized schism are voicing frustration, if not outrage.

“It is unbelievably unusual to see the largest exchange in America attacking its own regulator, where the regulator is basically saying everybody who’s registered, including the CME, can offer these types of products, and the CME says no one should be allowed to offer them,” said Jake Chervinsky, CEO of Hyperliquid Policy Center (HPC) in an interview.

HPC is a Washington, D.C.-based non-profit focused on creating compliant DeFi in the U.S, heavily focused on perps and on-chain financial infrastructure, and backed by a $28 million initiative from the Hyper Foundation.

Not long after CME filed suit, this disagreement took another turn, when the exchange made a bid to fast-track 24/7 trading for crude oil futures but was blocked by the CFTC. CME Group’s attempted 24/7 West Texas Intermediate (WTI) crude oil contract is a traditional expiring futures product rather than a crypto-style perpetual swap. The CME had cited investors’ desire to manage their positions “whenever news breaks.”

Representatives of the CFTC declined to comment. At the time, CFTC Chair Mike Selig said on X that “CME’s decision to disregard the Commission’s effort to undertake a reasoned analysis of the critical issues at stake is wholly inappropriate.”

CME, which played a significant role in getting bitcoin futures listed and was helpful in getting crypto accepted and adopted in the U.S., has a deep influence over commodities that the exchange has successfully wielded in Washington D.C. over the years, thanks in large part to its outspoken chairman, Terry Duffy.

“The definition of a swap is pretty clear,” he said in an interview with CoinDesk. “When two parties exchange payments to each other, that is deemed a swap,” he said. “When you’re dealing in swaps contracts, that comes with obligations to maintain five-day margin and register with the CFTC as a participant in the swaps market.”

As such, the CFTC did not follow the protocol which is effectively the law of the land, Duffy claimed, adding a complaint that the CFTC may not be prepared to enforce its emerging perps policy properly, such as blocking non-U.S. traders from trading on Kalshi or other CFTC-regulated platforms. “What are you doing to police U.S. participants from not participating in something that it’s illegal for them to do?” Duffy asked.

“I’ve not seen an answer to that yet, but yet they’re holding up my 24/7 contract of self certification,” he said.

Duffy had tangled with opponents in the digital-assets space before, once debating then-FTX CEO Sam Bankman-Fried on the industry’s efforts to cut out intermediaries months before Bankman-Fried’s company collapsed and he was imprisoned on a conviction tied to fraud.

During the CME’s recent Q2 earnings call, Duffy addressed the growing market presence of perpetual futures, stating that institutional clients do not use perpetuals for hedging. He said that CME has “the full technical and operational capabilities to launch perpetual futures” but “have not heard demand from our customers for these products.” Duffy went on to describe competitors’ perp markets as “an incubator system that I’m not paying for.”

When it comes to the way futures contracts work on traditional commodities, the structure differs from crypto, according to Liz Davis, partner and co-chair of the financial services practice at the law firm Davis Wright Tremaine.

“These perpetual contracts that started out in the crypto space are a different type of product than, say, pork bellies or crude oil,” Davis said in an interview. “There’s an underlying tension with these new types of products being offered on traditional commodities. Here you have delivery issues, and it really isn’t traded 24/7, because you have monthly contracts that you roll from month to month.”

Davis said there’s a lot to consider in a market in which the commodities the perps are tied to can be limited to trading only five days a week and set to only change hands within certain hours, as opposed to being always on.

“You just need to think through the various issues in terms of marginal liquidity and custody over the weekend; staffing and resources; your surveillance now needs to go over to the weekends and holidays, etc.,” she said.

Duffy’s crypto perps stance is viewed by crypto natives and DeFi enthusiasts as typical of the way large incumbents handle innovation that might threaten their dominance.

“It’s really going to come down to this sort of policy fight between this massive incumbent and the regulator who is trying to allow challengers to that incumbent, allowing competition that the incumbent doesn’t want to see happen,” HPC’s Chervinsky said, adding:

“The issue with the CME isn’t whether they’re pro or anti-crypto. It’s an incumbent using regulation to hold off competition, and they’re willing to take opposite positions depending on the moment to try to beat back the competition.”

So the future of CFTC-driven perps remains on a bubble as the CME readies its case, which includes claims that the agency rubber-stamped the Kalshi application, which had been submitted a day before approval.

“The CFTC approved perps despite a history of arguing they are swaps and without issuing a regulation despite seeking public comment in April 2025,” noted Jaret Seiberg, a financial policy analyst with TD Cowen, arguing the CME may have the “upper hand” in this legal dispute. “This distinction matters as the regulatory and tax regimes for swaps and futures are different.”

Though the CFTC is meant to be a five-member commission, Chairman Selig currently occupies the leadership as its lone member, so his is the lone voice of the agency. And he wanted the regulator to clear a path for U.S. perps in the crypto space, signing off on a Kalshi product and approving customer activity at Coinbase.

“It’s interesting that this is being done with a single-person commission,” Davis said. “When you have a five-person commission, the rulemaking doesn’t go as quickly, because of the counter view. So you’re sort of getting deprived of that counter view, other than the CME bringing suit and their commentary.”

Representatives of Kalshi and Coinbase declined to comment about the perps regulatory situation.

So far, Selig’s agency is opening up this U.S. market through a policy statement — not a new rulemaking that gives interested parties a chance to comment and try to steer the outcome. It’s much the same crypto approach as its sister agency, the Securities and Exchange Commission, which has issued a wide array of new policy statements without yet pursuing formal and durable rules.

The CFTC determined that a case-by-case review process was suitable for perps. As a result, Kalshi’s debut offering emerged last month, and the company said it reached more than $1 billion in trading volume in less than a week.

OKX has returned to South Korea’s Google Play Store after a four-day suspension, while Bybit’s app remains unavailable in the country.

Summary

- OKX’s Android app has returned to South Korea’s Google Play Store after about four days, allowing new downloads and updates again.

- Bybit remains unavailable on the Korean Google Play Store after its app was blocked earlier this month.

- Digital Asset previously found that 29 overseas crypto exchange apps had been restricted on Google Play under Google’s policy for unregistered VASPs.

According to a July 28 report by Digital Asset, the OKX: Trade Bitcoin & Crypto app once again appears in search results on South Korea’s Google Play Store, allowing users to install the application or update existing versions after it disappeared from the platform on July 24.

The publication verified that the exchange’s Android app had resumed normal distribution as of 8:00 a.m. local time on July 28. The restoration comes roughly four days after South Korean users lost access to new downloads and updates through Google Play.

Bybit, however, remains in a different position. Digital Asset said the exchange’s app, which became unavailable on July 10, was still blocked from search results and installation at the time of publication.

OKX becomes the first recent exchange to regain Play Store access

Only days earlier, Digital Asset had reported that the OKX app could no longer be found on South Korea’s Google Play Store, preventing Android users from installing or updating the application. At the time, other major overseas exchanges, including Binance and Bitget, continued to appear normally in search results and remained available for download.

The latest development makes OKX the first of the recently restricted overseas exchanges to return to the platform.

The restoration also changes part of a picture outlined by Digital Asset in a separate investigation published on July 24. In that report, the outlet found that at least 29 overseas cryptocurrency derivatives exchange apps had become unavailable on the Korean version of Google Play.

According to the investigation, 17 apps could no longer be found through search, six displayed an “Unavailable” notice, and another six showed a message stating that the service was not available in the user’s region.

At the time, both OKX and Bybit were included among the affected exchanges, with OKX becoming inaccessible on July 24 and Bybit on July 10.

Google’s restrictions have extended beyond the FIU’s enforcement list

Digital Asset’s earlier review also found that the affected exchanges fell into two categories.

Fourteen of the blocked platforms had already been identified by South Korea’s Financial Intelligence Unit as unreported virtual asset service providers and referred to law enforcement. The group included exchanges such as KuCoin, MEXC, BingX, XT.COM, LBank and CoinW.

The remaining 15 exchanges, including OKX, Bybit, Gemini, WhiteBIT and BitMEX, had not been referred to law enforcement by the FIU but were still unavailable through Google Play.

Based on those findings, Digital Asset reported that Google’s enforcement appeared to extend beyond the FIU’s published enforcement list. The publication said Google had indicated the restrictions were made under the company’s own policies rather than as a direct requirement from South Korean authorities.

Even while Android app availability changed, the July 24 report noted that affected users could still access the exchanges through their websites or Apple’s App Store.

Earlier policy changes laid the groundwork for the restrictions

The latest restoration comes against the backdrop of South Korea’s continuing oversight of overseas crypto businesses operating without local registration.

According to Digital Asset, the FIU classified overseas crypto firms that had not registered under the country’s Special Financial Information Act as unreported VASPs earlier this year. Google later introduced a policy to limit downloads and updates for such exchange apps on Google Play.

Although the policy had been scheduled to take effect earlier, Digital Asset noted that enforcement was not implemented immediately after the announced timeline. Restrictions instead appeared gradually, with multiple overseas exchanges becoming unavailable during 2026.

South Korean regulators have also increased enforcement across the digital asset sector beyond app distribution. Earlier this month, Financial Services Commission Chair Lee Eog-won said authorities had investigated more than 40 suspected cases of unfair crypto trading during the first two years of the Virtual Asset User Protection Act, referring more than 30 cases to investigative agencies while expanding AI-based market surveillance.

OKX continues expanding in other regulated markets

The app’s return to South Korea comes as OKX continues to grow its regulated operations outside the country.

Earlier this month, OKX Europe launched a one-way conversion service allowing customers across 30 European Union and European Economic Area countries to deposit USDT and voluntarily convert their holdings into MiCA-compliant USDC after European exchanges tightened support for Tether’s stablecoin.

The company has also continued building its institutional business. On July 20, former New York Governor Andrew Cuomo joined OKX’s board of directors after advising the exchange since 2023 on U.S. regulatory and institutional strategy. OKX has also been expanding its presence in the United States following the relaunch of its U.S. exchange and self-custody wallet in 2025.

The Part of the Electric Transition Nobody Wants to Discuss

Vita Vea landing spots: Veteran DT requests trade from Buccaneers

Rinn centre and ArrayPatch to partner on skin cancer treatment

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Brooks Brothers

-

NewsBeat7 days ago

NewsBeat7 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech1 day ago

Tech1 day agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Business6 days ago

Business6 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment7 days ago

Entertainment7 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Crypto World5 days ago

Crypto World5 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics22 hours ago

Politics22 hours agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Sports2 days ago

Sports2 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Sports4 days ago

Sports4 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Fashion4 days ago

Fashion4 days ago16 Dresses for the High Summer Event

-

News Videos5 days ago

News Videos5 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Politics2 days ago

Politics2 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Entertainment4 days ago

Entertainment4 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

News Videos1 day ago

News Videos1 day agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Crypto World5 days ago

Crypto World5 days agoUniswap (UNI) pushes deeper into tokenized RWAs with permissioned trading pools

-

Tech3 days ago

Tech3 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

Crypto World3 days ago

Crypto World3 days agoRipple bought a bank in pieces. The $4 billion audit

-

Entertainment2 days ago

Entertainment2 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

Crypto World6 days ago

Crypto World6 days agoSablier Labs Enters Maintenance Mode, Halts Development

You must be logged in to post a comment Login