Crypto World

Bitcoin vs. The Hantavirus: Is BTC Bracing for Another ‘Black Swan’ Event?

It’s like a few wars, rising inflation, and global uncertainty are not enough these days. Now, the world needs to pay attention to another health hazard that made the news in the past few weeks: the Hantavirus, and, more precisely, the Andes virus.

Aside from the potential threats it poses to human life (which we will explore later in the article), the question raised by some analysts is whether it will affect BTC as COVID did six years ago.

Will History Repeat?

For those of our readers who might not have been around the March 2020 developments, here’s a quick recap. BTC was coming out of a long bear market, but it had failed to stage a meaningful recovery in 2019, and all eyes were on 2020 as a halving year, which historically served as a major catalyst for future gains.

However, it all changed when the COVID-19 pandemic broke out, especially since it was categorized as a global hazard in March. Over a two-day trading session, BTC plummeted from over $8,000 to a multi-year low of $3,750.

Analysts such as Crypto Rover have now speculated on a similar calamity if the Hantavirus explodes. The analyst with over 1.5 million followers on X noted that the mortality rate for COVID was 1%, while the Hantavirus’s is at 40%, which could spell a lot more trouble for everyone.

WARNING: THE COVID-LIKE $BTC DUMP IS ABOUT TO REPEAT??

COVID mortality rate: ~1%

Hantavirus mortality rate: ~40%The WHO says this likely won’t become the next pandemic.

I don’t think so either.

But they said the same thing about COVID.

Eyes on Bitcoin. pic.twitter.com/F0Dar9gN0n

— Crypto Rover (@cryptorover) May 8, 2026

The Differences

The history of this version of the Hantavirus, according to National Geographic, shows that it stemmed from South America and caused significant harm on a Dutch cruise ship, including several deaths so far. It comes from the Hantaviridae family of viruses, carried by rodents. In most of its versions, it cannot be transferred human-to-human. However, this particular one, which the WHO called the Andes virus, is the only known hantavirus that can jump from human to human.

Some experts said its spread is “not particularly efficient,” unlike measles and COVID, which can be transferred by viruses lingering in the air after an infected person has left the room. Andes spreads only by close contact.

“So, when you have people sleeping in the same bed, or sex partners, or people sharing food, the virus can transmit that way. But it doesn’t transmit to huge groups of individuals,” said Steven Bradfute, an immunologist and hantavirus researcher at the University of New Mexico Health Sciences Center.

Nevertheless, Bradfute, alongside other experts, such as Dr. Emily Abdoler, believes this virus should not be a main concern for most people as its spread will not be anything like COVID.

“I’m doing these interviews as a public service to try to reassure people that this shouldn’t be on their top 100 list of worries,” said Dr. Abdoler.

Hopefully, that’s true. Because we have heard similar reassurances even with COVID, which was not supposed to become a global pandemic at first. But, even if they are true (again, hopefully it’s not such a big threat), that doesn’t guarantee that markets won’t panic and overblow the potential consequences, leading to another major BTC dip.

The post Bitcoin vs. The Hantavirus: Is BTC Bracing for Another ‘Black Swan’ Event? appeared first on CryptoPotato.

When U.S. spot bitcoin exchange-traded funds (ETFs) launched in January 2024, investors had more than a dozen funds to choose from. BlackRock, Fidelity, Ark Invest, Bitwise, VanEck, Franklin Templeton and several others entered what many expected would become a fiercely competitive market.

Eighteen months later, the battle increasingly looks like a two-player race.

Data shows that BlackRock’s iShares Bitcoin Trust (IBIT) and Fidelity’s Wise Origin Bitcoin Fund (FBTC) are doing most of the heavy lifting when it comes to attracting new institutional capital, while smaller funds have become largely irrelevant in determining the direction of the overall market.

The trend was evident throughout the first half of 2026.

On January 14, bitcoin ETFs recorded net inflows of $840.6 million, according to data from Farside Investors. IBIT alone accounted for $648.4 million of that total, while FBTC added another $125.4 million. Together, the two funds represented more than 90% of all inflows that day.

A similar pattern appeared on April 17, when total inflows reached $663.9 million. IBIT brought in $284 million and FBTC added $163.4 million, accounting for roughly two-thirds of all new money entering the sector.

Even during periods of weaker sentiment, the dominance of the two largest funds remained apparent. On May 1, total inflows reached $629.8 million, with IBIT contributing $284.4 million and FBTC adding $213.4 million. Combined, the pair attracted nearly $500 million of the day’s total. The pattern repeated throughout much of 2026, with the two funds frequently accounting for the majority of net inflows on the largest allocation days and often offsetting weakness elsewhere in the ETF market.

The concentration has emerged during a difficult year for bitcoin and the broader crypto ETF market. Bitcoin is down roughly 29% year-to-date, a decline that has tested institutional conviction and triggered several waves of ETF redemptions. Between mid-May and early June alone, spot bitcoin ETFs recorded multiple days of heavy outflows. The selling marks a sharp contrast to earlier periods when investors often viewed bitcoin pullbacks as buying opportunities.

But the data highlights a broader shift taking place in the bitcoin ETF market in which investors increasingly appear to be concentrating their allocations in the largest and most liquid vehicles.

That trend has particularly benefited BlackRock.

IBIT has emerged as the flagship product of the entire spot bitcoin ETF sector, regularly posting the largest inflows and often acting as a stabilizing force during periods of market stress. On several days when the broader ETF complex experienced heavy outflows, IBIT either remained positive or saw far smaller redemptions than its competitors.

The dominance is not entirely surprising. Many of the largest buyers of bitcoin ETFs are financial advisers, registered investment advisers, hedge funds, family offices, pension consultants and institutional asset allocators. For those investors, liquidity, trading volume and issuer reputation often matter as much as the underlying bitcoin exposure itself.

BlackRock manages more than $10 trillion in assets globally and maintains relationships with thousands of wealth-management platforms. Fidelity, one of the largest retirement and brokerage providers in the U.S., brings similar advantages through its distribution network and long-standing presence among retail and institutional investors.

As a result, many allocators increasingly view IBIT and FBTC as the default options for gaining bitcoin exposure.

The flip side is that smaller issuers are struggling to remain relevant.

Funds such as Franklin Templeton’s EZBC, VanEck’s HODL, Valkyrie’s BRRR and WisdomTree’s BTCW frequently record daily flows measured in single-digit millions of dollars.

On many trading days, their contributions are so small that they have little impact on the overall direction of the market.

Even funds that were once viewed as major competitors, including Bitwise’s BITB and Ark’s ARKB, now play a secondary role compared with the industry’s two largest products. Earlier this year, Trump Media & Technology Group withdrew plans for a proposed spot bitcoin ETF, abandoning an effort to enter the increasingly crowded market that is now dominated by products from BlackRock and Fidelity.

The concentration has become particularly noticeable during periods of volatility. When investors buy bitcoin ETFs aggressively, most of the money flows into BlackRock and Fidelity.

When investors sell, the behavior of those two funds often determines whether the sector posts net inflows or outflows.

That dynamic suggests the bitcoin ETF market is entering a new phase. Rather than a broad competition among a dozen issuers, the industry increasingly resembles a winner-take-most business where scale, liquidity and distribution drive investor decisions.

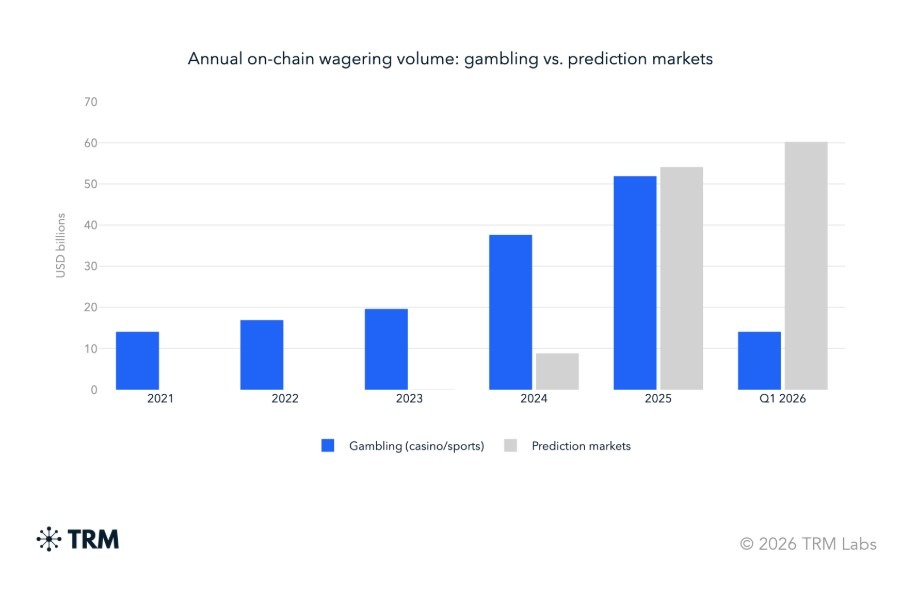

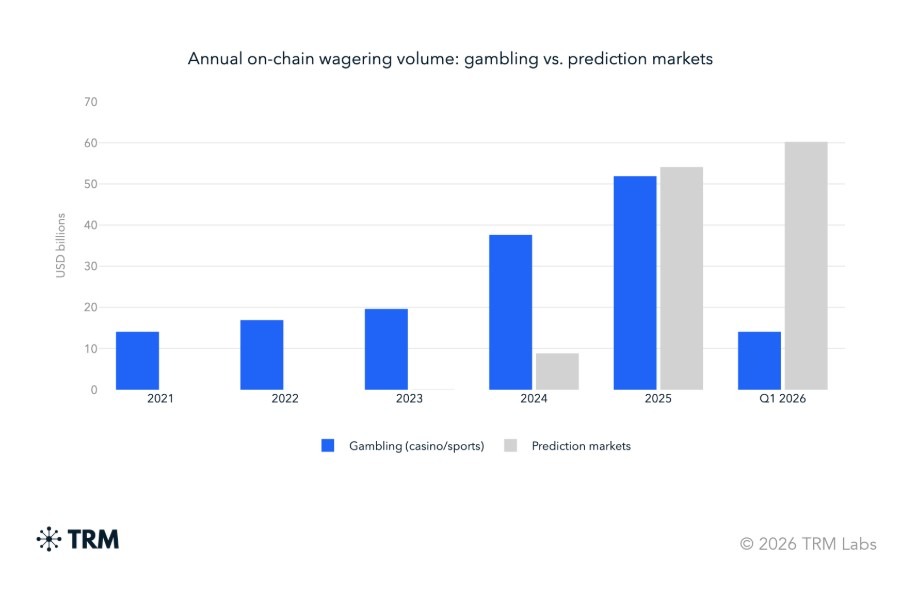

Prediction markets overtook onchain gambling for the first time in the opening quarter of 2026, recording $36.6 billion in volume compared with gambling’s $14 billion, according to TRM Labs.

In a Wednesday report, the blockchain intelligence company said the shift followed a rapid expansion in both sectors. Onchain gambling reached $51 billion in 2025, while prediction markets climbed to $54 billion, putting the two categories at comparable scale heading into 2026.

Still, onchain gambling remained near record levels. Quarterly gambling volume reached an all-time high of $15 billion in the fourth quarter of 2025, then held at $14 billion in Q1 2026.

Neither onchain gambling nor prediction markets retreated along with the broader crypto markets. Volumes remained elevated through the 2025-2026 market correction.

Annual onchain wagering volume. Source: TRM Labs

A TRM Labs spokesperson told Cointelegraph that gambling volumes have surged during the recent market pullback because of the “sticky and expanding activity of a loyal user base.”

“This does not mean anything about concentration risk in itself, since there is quite a large gambling user base,” the spokesperson said. “It shows how a consistent user activity can insulate an industry from a market pullback and in fact drive growth.”

Gambling and prediction markets face different risks

TRM said gambling platforms and prediction markets are increasingly converging on shared stablecoin infrastructure, but their financial crime risks remain distinct.

Prediction markets such as Polymarket and Kalshi operate as peer-to-peer markets for binary outcomes, while gambling platforms such as Stake, WINk and Rollbit operate more like traditional casinos, with the platform setting odds and maintaining a house edge.

Related: Chainalysis, South Korean police link up to fight crypto crime

TRM said prediction markets have attracted scrutiny over insider trading, while gambling platforms are more exposed to money laundering risks.

“Gambling services and prediction markets carry distinct inherent financial crime risks, and firms should calibrate controls accordingly,” a TRM Labs spokesperson told Cointelegraph.

Casual bettors drive growth alongside whales

TRM said more than 2 million personal wallets interacted with gambling platforms between January 2022 and March 2026.

The firm divided those users into five behavioral groups. “Dabblers” made five or fewer transactions and disappeared within a month, while “Casual Bettors” averaged 18 transactions across eight active days. “Event Chasers” returned around major sporting events, while “Daily Grinders” gambled on at least 30% of the days in their active tenure. “High Rollers,” the highest-value cohort, averaged $13,558 per bet and $378,000 in lifetime gambling volume.

The firm found that volume remains heavily concentrated among high-value users, with High Rollers representing 6.3% of personal gambling wallets but driving 91.8% of personal wallet gambling volume since 2022.

Despite this, TRM said the fastest-growing user categories are not only high-stakes bettors. Casual Bettors’ monthly volume rose from $17 million in January 2022 to $188 million by March 2026, while Daily Grinders’ volume increased 12x over the same period.

Magazine: Vietnam preps crypto pilot, HK pushes tokenization: Asia Express

Anchorage Digital, a federally chartered crypto bank and provider of stablecoin infrastructure, has submitted a public comment letter in support of the U.S. Treasury Department’s proposed AML and sanctions framework for the GENIUS Act. The firm contends that the framework largely balances compliance requirements with innovation in digital payments, while also urging the Treasury to clarify several open points that could influence operational risk and regulatory certainty for issuers and their counterparties.

In the filing, Anchorage argues that the proposed rules appropriately place AML obligations on regulated stablecoin issuers while requesting guidance on secondary-market sanctions liability, the scope of enterprise-wide AML programs, and correspondent-account requirements. The firm also cautions against imposing strict liability on issuers for failing to independently identify sanctioned users who transacts through smart contracts on secondary markets.

“A final rule that is clear and workable gives regulated institutions the certainty they need to build, and strengthens U.S. leadership in the next generation of payments and settlement infrastructure,” Anchorage stated in its letter.

The public comment letter comes as the Treasury, together with the Financial Crimes Enforcement Network (FinCEN) and the Office of Foreign Assets Control (OFAC), advances a rulemaking aimed at classifying payment stablecoin issuers as financial institutions under the Bank Secrecy Act. The proposed framework would subject issuers to AML obligations, customer due diligence, and suspicious-activity reporting, with enhanced monitoring and recordkeeping required for stablecoins that operate across borders and through programmable technologies.

The policy, described in a Treasury release, would align stablecoin issuers with established AML and sanctions standards while imposing additional compliance expectations designed to address the unique risks posed by programmable money. The regulatory push is part of a broader effort to integrate digital-asset payments into the U.S. financial-regulatory perimeter, including cross-border considerations and enforcement expectations.

The discussion has drawn mixed responses from industry participants. Several trade and advocacy groups have urged broader carveouts or clarifications, reflecting a spectrum of views on how expansive the sanctions and AML obligations should be for issuers with limited direct visibility into user activity on secondary markets.

Key takeaways

- The GENIUS Act framework would classify payment stablecoin issuers as financial institutions under the Bank Secrecy Act, placing them under AML, customer due diligence, and suspicious-activity reporting regimes, with enhanced monitoring requirements.

- Anchorage Digital publicly supports the framework’s core aims but seeks clarifications on secondary-market sanctions liability, enterprise-wide AML program standards, and correspondent-account requirements to avoid unnecessarily broad obligations.

- Anchorage argues issuers should not face strict liability for failing to independently identify sanctioned users transacting via secondary-market smart contracts.

- Industry groups such as Hyperliquid and Paradigm have submitted comments pressing for greater clarity around secondary-market obligations, arguing the current framework could impose sanctions liability on issuers even in the absence of direct visibility into end users.

- Regulatory timing and final rule design will influence how stablecoin issuers, banks, and service providers structure compliance programs, with potential cross-border implications and alignment questions relative to other jurisdictions, including MiCA in the European Union.

Regulatory context and focal points

The proposed rulemaking, issued jointly by FinCEN and OFAC and highlighted by Treasury officials, would place regulated stablecoin issuers within the existing U.S. AML/Sanctions framework. The plan envisions formalizing stablecoin issuers as financial institutions under the Bank Secrecy Act, thereby obligating them to implement robust AML programs, conduct customer due diligence, and report suspicious activity. In parallel, the framework would impose enhanced monitoring and recordkeeping requirements to help regulators track and mitigate illicit finance risks associated with programmable payments and cross-border settlement.

Anchorage’s submission emphasizes practical considerations for regulated institutions seeking to deploy stablecoin rails at scale. The firm notes that a rule that is clear, predictable, and implementable would foster innovation in digital payments infrastructure while preserving strong compliance standards. The emphasis on clarity around secondary-market liability reflects ongoing debates about how to apply sanctions regimes to the decentralized aspects of programmable money, where user relationships may be indirect or opaque to issuers.

Industry responses and carveout debates

Not all industry voices view the GENIUS Act framework as a straightforward alignment with existing anti-money-laundering and sanctions regimes. In addition to Anchorage, the lobbying arms of Hyperliquid and venture-capital firm Paradigm recently submitted their own comments challenging certain aspects of the proposal. They argued that the current framework could extend sanctions obligations to issuers even when those issuers lack direct relationships with, or visibility into, the end users transacting on secondary markets via smart contracts.

According to these groups, OFAC’s approach risks treating secondary-market activity as a continuous provision of services by the issuer, thereby broadening sanction liabilities beyond what issuers can reasonably monitor or control. The concerns echo broader policy questions about where responsibility should lie when financial instruments and protocols enable peer-to-peer transactions without traditional, on-chain counterparty visibility.

Implications for policy, enforcement, and cross-border regimes

The GENIUS Act discussion sits at the intersection of domestic regulatory design and international policy harmonization. For U.S.-based crypto firms, the proposed rules could reshape licensing, risk management, and oversight frameworks, prompting issuers to invest in comprehensive AML programs and governance structures that integrate smart-contract activity with traditional compliance controls. Banks and other regulated entities servicing stablecoins may also need to adjust their correspondent-banking and anti-financial-crime policies to reflect the newly defined risk landscape.

From a broader perspective, policymakers must reconcile these developments with ongoing regulatory initiatives in other jurisdictions. The EU’s MiCA framework represents a contrasting approach to stablecoins and crypto-asset service providers, underscoring global differences in how regulators address stablecoin issuance, payment settlement, and cross-border settlement rails. As U.S. and international authorities pursue parallel aims—reducing illicit finance risk while enabling financial innovation—the final design of GENIUS Act rules could influence cross-border collaborations, licensing pathways, and the allocation of enforcement resources among agencies such as the SEC, CFTC, and DOJ, in addition to FinCEN and OFAC.

Legal and compliance teams at issuers, exchanges, and financial institutions will be watching for how the final framework defines secondary-market exposure, the level of issuer visibility required to meet sanctions obligations, and the granularity of enterprise AML programs. As enforcement expectations evolve, firms may face increased reporting, recordkeeping, and governance demands, with potential implications for cross-border operations and banking relationships.

Closing perspective

While the GENIUS Act proposals mark a significant step toward integrating stablecoins into the U.S. financial-regulatory perimeter, the path to final rules will hinge on clear definitions of issuer liability, the scope of AML program requirements, and practical considerations for secondary-market activity. The diverse industry responses underscore that the sector seeks a balanced framework—one that reinforces compliance and national security objectives without stifling technological advancement or limiting access to regulated, resilient digital payments infrastructure. Monitoring the forthcoming rulemaking and regulator guidance will be essential for institutions shaping their governance and risk management programs in this evolving landscape.

Crypto World

Ethereum (ETH) developers are exploring new token standards as privacy returns to focus

For years, privacy in transacting was one of crypto’s most ambitious promises. Then it took a back seat as other trends took off.

As developers focused on scaling blockchains and regulators scrutinized privacy tools such as Tornado Cash, much of the industry’s attention shifted elsewhere. But a new Ethereum proposal and a growing number of privacy-focused products suggest the topic is making a comeback.

The latest example is pERC-20, a proposed Ethereum token standard that would allow users to hold and transfer tokens without publicly revealing their balances, transaction amounts or counterparties. The proposal has sparked renewed discussion around whether public blockchains should expose every financial interaction by default.

Unlike traditional ERC-20 tokens, which is the default token standard on Ethereum today that displays balances and transaction histories onchain for anyone to inspect, pERC-20 keeps sensitive details private.

Today, most Ethereum tokens function like public bank accounts. Anyone can look up a wallet address and see how many tokens it owns, where they came from and where they were sent. Under pERC-20, tokens would instead exist as encrypted cryptographic “notes,” similar to digital cash.

The result is a system where transactions remain private while still allowing the network to verify that no changes to the transactions occurred.

Importantly, the proposal does not hide everything.

The total supply of a token would remain publicly visible, allowing anyone to verify that new tokens are not being secretly created. The proposal also includes a compliance mechanism that would allow issuers to freeze specific notes through a cryptographic blacklist without exposing ordinary users’ balances or transaction histories.

The design reflects a broader shift in how privacy is being discussed across crypto.

Rather than treating privacy and compliance as mutually exclusive, many newer projects are attempting to build systems that offer both.

But some developers argue that private payments are only part of the challenge.

Earlier this week, Starknet went live with STRK20, a privacy-focused token framework designed to extend confidentiality beyond simple token transfers and into decentralized finance applications such as lending, staking and token swaps.

According to Eli Ben-Sasson, the co-founder of StarkWare, the main developer firm behind Starknet, the biggest obstacle facing privacy technologies today is not cryptography. “The big problem of dealing with privacy is UX,” Ben-Sasson told CoinDesk.

Historically, privacy-focused cryptocurrencies have struggled with usability. Users often faced slow wallet synchronization, cumbersome transaction flows and limited compatibility with the broader crypto ecosystem. Those limitations made privacy tools difficult to use and, in some cases, undermined the privacy they were designed to provide.

Privacy systems rely on large groups of users participating together. If only a small number of people use a privacy network, it becomes easier to identify individual participants.

“If the UX is bad, very few users are going to be using it,” Ben-Sasson said. “If very few users are going to be using it, and only for a very small number of things, they don’t really get a lot of anonymity.”

Ben-Sasson said pERC-20 appears to be largely focused on private token transfers and draws on ideas pioneered by privacy-focused projects such as Zcash. While he described that as an important capability, he argued that the next stage of privacy infrastructure will need to support a much broader set of financial activities.

“Today we can do more,” he said, referring to privacy-preserving DeFi applications.

The STRK20 framework was built with that goal in mind. Rather than shielding a single token, the framework allows users to manage multiple assets under a unified privacy layer and interact with decentralized applications while maintaining confidentiality. According to Ben-Sasson, users can access services such as swapping, borrowing and staking without sacrificing privacy.

The framework also uses post-quantum secure cryptography, which Ben-Sasson argued will become increasingly important as blockchain developers begin preparing for future advances in quantum computing.

The contrast between pERC-20 and STRK20 highlights an emerging debate about what privacy in crypto should actually look like.

One vision focuses on making payments private while preserving transparency elsewhere. Another seeks to make privacy a foundational layer that extends across an entire ecosystem of financial applications.

Either way, the discussion itself marks a notable shift.

For much of the past several years, privacy occupied a relatively small corner of the crypto industry, often associated with niche privacy coins or controversial mixing services. Today, the conversation is increasingly centered on mainstream infrastructure, token standards and institutional use cases.

Whether pERC-20 ultimately becomes an Ethereum standard remains uncertain. Like all Ethereum Improvement Proposals, it must go through a lengthy review process before it could see widespread adoption. But its emergence, alongside projects such as STRK20, suggests that privacy is once again becoming a priority for blockchain developers.

Anchorage Digital, a federally chartered crypto bank and stablecoin infrastructure provider, has submitted a public comment letter supporting the US Treasury Department’s proposed Anti-Money Laundering (AML) and sanctions framework for the GENIUS Act, arguing that the rules largely strike the right balance between compliance and innovation.

In a letter published Wednesday, Anchorage said the proposed framework appropriately places AML obligations on regulated stablecoin issuers while urging Treasury to clarify secondary-market sanctions liability, enterprise-wide AML programs and correspondent account requirements.

Specifically, Anchorage argued that issuers should not face strict liability for failing to independently identify sanctioned users who transact on secondary markets through their smart contracts.

“A final rule that is clear and workable gives regulated institutions the certainty they need to build, and strengthens U.S. leadership in the next generation of payments and settlement infrastructure,” Anchorage said.

Source: Kevin Wysocki

The comments address Treasury rules proposed in April that would classify payment stablecoin issuers as financial institutions under the Bank Secrecy Act, subjecting them to AML, customer due diligence and suspicious activity reporting requirements.

The proposal, jointly issued by the Financial Crimes Enforcement Network (FinCEN) and Treasury’s Office of Foreign Assets Control (OFAC), would align stablecoin issuers with existing US anti-money laundering and sanctions compliance standards while imposing enhanced monitoring and recordkeeping obligations.

Related: Solana Institute CEO says CLARITY Act must shield open-source developers

Industry groups push for broader sanctions carveouts

Support for the proposed rulemaking has not been uniform across the crypto industry.

The lobbying arms of crypto derivatives exchange Hyperliquid and venture capital firm Paradigm recently submitted their own comment letter seeking greater clarity on secondary-market obligations, echoing Anchorage’s concerns but taking a more critical view of the proposal overall.

Source: Stefan Schropp

The groups argued that the current framework could impose sanctions obligations on issuers even when they lack a direct relationship with or visibility into users transacting on secondary markets.

“OFAC sweeps secondary market activity into the issuer’s compliance perimeter, treating smart contract interactions as an ongoing “provision of services” that carries sanctions liability regardless of whether the issuer has any relationship with, or visibility into, the transacting parties,” they said.

Related: SEC’s Peirce argues publishing DeFi code is protected speech

Meta has agreed to lease a 168-megawatt AI data center in India from Reliance Industries. The facility will rise in Jamnagar, and Reliance will deliver it within two years.

Summary

- Meta agreed to lease a 168-megawatt AI data center from Reliance Industries in Jamnagar.

- Reliance will build and deliver the facility within two years, with an option to scale.

- Meta also signed clean energy deals with CleanMax and Fourth Partner Energy for nearly 1GW.

The deal adds new AI infrastructure for Meta while extending its partnership with Mukesh Ambani’s group.

Meta expands AI capacity in Jamnagar

According to Meta’s release, Reliance Industries will build the AI-enabled data center for the US technology company. The facility will carry 168 megawatts of capacity and include an option to scale. Reliance operates businesses across petrochemicals, textiles, media, telecom, and digital services. Its new agreement with Meta adds data centers to a long-running technology partnership between both companies.

“This world-class facility in Jamnagar will help us scale our AI infrastructure globally,” Meta CEO Mark Zuckerberg said. He said the project also deepens Meta’s long-term investment in India’s economy. Reliance Chairman Mukesh Ambani described Meta’s latest investment as a “transformative moment for India’s digital infrastructure.” His company will build the site and lease it to Meta after completion.

The two companies already have deep business links in India. In 2020, Meta invested $5.7 billion in Jio Platforms, Reliance’s telecom and digital services unit. Last year, Meta and Reliance expanded their work through a joint venture. The partnership made Meta’s open-source AI models available to Indian enterprises and developers.

India draws data center capital

Global hyperscalers have increased data center spending in India as AI infrastructure demand grows. The country has attracted $400 billion into its AI ecosystem over the last year. Most of that money has gone toward data centers and energy systems, according to the provided industry figures. Large AI systems need high-capacity sites and steady power supply.

Nomura said in a June 2 report that India’s data center industry ranks among the fastest-growing globally. The brokerage also said India remains cost-efficient compared with developed Asia Pacific and Western markets. India’s data center capacity could rise to 7 gigawatts by 2030, according to Nomura. The report linked that growth to cost advantages and rising hyperscaler demand.

The Indian government also introduced a 20-year tax exemption earlier this year. The policy covers hyperscalers using Indian data centers to serve clients outside the country. The tax rule adds another incentive for companies building AI infrastructure in India. Meta’s Reliance deal comes during that expansion of policy and private-sector investment.

Renewable energy deals support Meta operations

Meta is also working with Indian clean energy firms CleanMax and Fourth Partner Energy. The company said those partnerships cover nearly 1 gigawatt of renewable energy. The projects will operate across northern and southern Indian states. They will supply clean power to Meta’s expanding infrastructure footprint in the country.

Meta said the India energy investments align with its global clean power target. The Facebook parent wants to match all operations with 100% clean and renewable energy. The Jamnagar data center agreement adds to Meta’s existing India commitments.

The deal links AI infrastructure, renewable power, and Reliance’s industrial base in one project. Reliance will deliver the data center within two years, according to Meta’s release. The facility also includes an option to scale after the first phase.

On-chain analysis is prompting speculation that Cardano co-founder Charles Hoskinson sold approximately 1.5 billion ADA in 2021, while publicly advocating for the token. NFT creator Masato Alexander published new on-chain tracing work this week claiming that large ADA transactions during the 2021… Read the full story at The Defiant

Raydium has pledged to fully reimburse losses after an exploit drained approximately $1.3 million from five legacy liquidity pools built on Solana.

Summary

- Raydium said it will fully reimburse losses after an exploit drained about $1.3 million from five legacy Solana liquidity pools.

- On-chain investigator Specter said the attacker used a fake mint address to exploit retired AMM code and steal RAY, SOL, and USDC.

- PeckShield traced part of the stolen funds to Tornado Cash, while Raydium said active pools and current users were unaffected.

According to blockchain security firm PeckShield and on-chain investigator Specter, the attack targeted retired automated market maker infrastructure that is no longer used by active Raydium pools. The protocol said current users and active liquidity pools were not affected by the incident.

Details shared by Specter indicate that the attacker exploited a validation weakness in dormant pools tied to Raydium’s early AMM design. By using a fake mint address, the attacker was able to bypass checks and withdraw liquidity from the affected pools.

The stolen assets included roughly 150,177 RAY tokens, 5,603 SOL, and 893,700 USDC. Specter reported that the attacker initially received funding through KuCoin before moving the stolen assets across chains to Ethereum.

Exploit was limited to retired Raydium infrastructure

Following the attack, Raydium stated that the affected pools belonged to a deprecated program with no active user participation. The team added that all impacted assets would be covered by the project treasury, preventing losses from falling on users who still had exposure to the legacy pools.

Tracking data from PeckShield showed that part of the stolen funds was routed through privacy tools after the exploit. The security firm reported that approximately 810 ETH was deposited into Tornado Cash, while another seven ETH was transferred to FixedFloat.

The movement of funds through Tornado Cash may complicate efforts to trace assets. PeckShield noted the transfers after the Ethereum-based funds were bridged from Solana. The mixer was removed from the U.S. Treasury Department’s sanctions list in March 2025.

Security incidents involving inactive code have become a recurring concern across decentralized finance. As previously reported by crypto.news, Token of Power suffered a separate exploit earlier this week that drained more than $1.5 million from a liquidity pool after an attacker manipulated token balances and withdrew WETH reserves. The two incidents involved different protocols and attack methods.

Raydium has moved quickly to cover user losses

Compensation commitments are not new for Raydium. The protocol faced another major security incident in December 2022 when an admin key compromise led to losses from active liquidity pools.

At the time, a governance proposal approved the use of buyback fees and vested team tokens to reimburse affected liquidity providers. The latest response follows a similar approach, with the project confirming that treasury funds will be used to make users whole.

Market reaction has remained relatively muted. Data at the time of writing showed Raydium (RAY) trading near $0.57, down less than 1% over the previous 24 hours. Solana (SOL) also moved lower during the same period, slipping nearly 2% to around $63.88.

While investigators continue tracing the stolen assets, information from PeckShield and Specter suggests the exploit was confined to outdated infrastructure rather than Raydium’s current trading systems.

ZK blockchain project Hyli is shutting down after two years, with the team citing weak market demand for zero-knowledge technology as the decisive factor. "ZK has not gained the traction we had hoped for," the team said in an announcement posted Wednesday on X, adding that it sees no viable path to… Read the full story at The Defiant

Federal regulators came out with their first proposed rules on how to oversee prediction markets on Wednesday.

The Commodity Futures Trading Commission, which has taken the lead as the federal regulator over the markets, will seek to develop a framework to determine if contracts are contrary to the public interest and illegal.

Those questions surround contracts that relate to terrorism, assassinations, war, gaming or illegal conduct under state and or federal law, based on the Commodity Exchange Act. The commission did not outright ban any type of event contract based on the category of the trade, like those related to sports or elections.

The proposed rule focuses heavily on how the commission will determine if a contract crosses too much into the realm of terrorism, war or assassinations, topics that domestically-regulated exchanges have avoided offering contracts on.

The CFTC rules left some grey area around gaming, which has been the source of much controversy on the question of sports-related event contracts, though it detailed some sports-related contracts that the commission will not allow.

In a release, the commission acknowledged the rules proposed on Wednesday were thin, and noted that further rulemaking regarding prediction markets may come in the future.

After Wednesday’s announcement, the proposed rule will now face a 45-day public comment period.

“The CFTC will protect the integrity of our regulated markets without standing in the way of responsible innovation,” said CFTC Chairman Michael Selig, who was appointed by President Donald Trump, in a statement. “This proposal gives the Commission a durable, transparent framework to identify the contracts Congress directed us to scrutinize while letting legitimate markets move forward.”

Selig in a post on X added that the commission will “balance market integrity with responsible innovation” as it continues future rulemaking processes.

The rule establishes a process to determine how contracts will be prohibited. The commission will first determine if the contract is in fact based on an event happening. Then, it will consider if that event falls within the categories defined in the Commodity Exchange Act, and then conduct a public interest analysis to decide if it should be prohibited or not.

Prediction markets have exploded in popularity over the past year, creating a scramble to figure out how to regulate them.

States have challenged the platforms, believing their sports-related offerings amount to betting, something that is under their jurisdiction. However, the CFTC argues all contracts — no matter their topic — are swaps, which gives the agency exclusive authority to regulate them.

At the same time, bipartisan members of Congress have expressed concerns about the platforms and potential risks for insider trading, though no official legislation on the markets has been considered.

On the question of sports, the rule was explicit that some contracts will not be allowed.

“Within gaming, the Commission aims to permit contracts settled on aggregate sports outcomes with objective data and integrity infrastructure, while prohibiting pure‑chance games and high‑risk sports‑adjacent designs (e.g., injury, officiating‑only, discrete actions, altercations, pre‑collegiate events),” according the rule.

The commission noted gaming, though, could be interpreted very broadly. It settled with one that defines it as something done for recreation or to entertain, is governed by rules and is based on measurable outcomes determined by skilled activity during the activity.

Using the new definition, the CFTC concludes contracts related to elections were not gaming, as they aren’t for recreation nor entertainment.

Slideshow: The sweeter side of Sweets & Snacks 2026

BlackRock and Fidelity are quietly turning bitcoin ETFs into a two-firm market

John Stones’ next club after Man City exit: Bundesliga reunion, old club return, World Cup focus

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Evereve – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoJensen Huang Approves Samsung, SK Hynix, and Micron for NVIDIA (NVDA) HBM4 Memory Supply

-

Crypto World3 days ago

Crypto World3 days agoAnatomy of the June crypto crash: Fed, Iran, Saylor

-

Entertainment4 days ago

Entertainment4 days agoThe Best Mystery Series of All Time Is Surging on Streaming 30 Years After It Ended

-

NewsBeat3 days ago

NewsBeat3 days agoAlexander Zverev wins the French Open to finally earn a 1st Grand Slam title

-

Tech5 days ago

Tech5 days agoSuspicious Polyfill login prompts pop up on Toshiba, Muji websites

-

Crypto World4 days ago

Crypto World4 days agoSenator Cynthia Lummis Calls CLARITY Act the Most Consequential Financial Legislation of This Generation

-

Tech3 days ago

Tech3 days agoMicrosoft unveils seven homegrown AI models in new bid for ‘long term self-sufficiency’

-

Tech5 days ago

Tech5 days agoMicrosoft launches MXC, an OS-level sandbox for AI agents, with OpenAI and Nvidia already on board

-

Business5 days ago

Business5 days ago(VIDEO) Justin Bieber Delivers Surprise Happy Birthday Serenade to Diners at Los Angeles Mexican Restaurant

-

Business4 days ago

Business4 days agoThe Pain Points Taking a Fragile Tech Rally Down a Notch

-

Crypto World2 days ago

Crypto World2 days agoEli Lilly (LLY) Stock Surges 4% Following Breakthrough Sleep Apnea Trial Results

-

Crypto World5 days ago

LBank Surpasses 25 Million Users Worldwide as AFA Partnership Continues to Drive Global Growth

-

Tech5 days ago

Tech5 days agoVon der Leyen’s AI envoy pick draws conflict-of-interest fire

-

Crypto World3 days ago

Crypto World3 days agoTrump’s AI Ownership Plan Could Benefit Anthropic at OpenAI’s Expense

-

Tech5 days ago

Tech5 days agoMeta steals a tactic from Tesla and builds data centers in tents

-

Sports1 day ago

Sports1 day agoBangladesh beat Australia after 20 years in ODIs, register only their second win over six-time world champions | Cricket News

-

Business3 days ago

Business3 days agoHigh Stakes for Wembanyama as New York Pushes for 3-0 Lead

-

Tech4 days ago

Tech4 days agoHackers now exploit SolarWinds Serv-U flaw to crash servers

-

Tech3 days ago

Tech3 days agoNotion restores access to Anthropic after service disruption

You must be logged in to post a comment Login