Crypto World

Bitcoin whale activity hits 2023 low as smart money remains quiet

Bitcoin (BTC) whale activity has slowed to its weakest level since September 2023, adding to signs that large holders have turned cautious.

Summary

- Santiment said whale activity dropped as investors watched uncertainty and conflict in the Middle East.

- Transfers above $100,000 and $1 million fell as Bitcoin struggled to recover after price swings.

- Analysts said short-term holder losses and weaker speculation may mark a new Bitcoin accumulation phase.

Data from Santiment shows that transfers above $100,000 have dropped as Bitcoin trades below recent highs and investors watch policy updates and geopolitical risks.

Santiment said daily Bitcoin transactions above $100,000 fell to 6,417, the lowest reading since September 2023. Transfers above $1 million also dropped to 1,485, their lowest level since October 2024.

The firm said activity rose sharply during Bitcoin’s early February sell-off, when large holders moved funds during heavy volatility. Since then, that pace has faded as the market entered a consolidation period and failed to regain steady momentum.

Santiment said the decline does not confirm a bullish or bearish trend on its own. The firm said whale activity has become “historically quiet” while market participants wait for more clarity around the CLARITY Act and the conflict in the Middle East.

The firm added that “smart money is in the same boat as smaller retail holders at the moment, and have been reluctant to make moves with so much policy and global uncertainty at play.” That view places the current market in a wait-and-see phase rather than a clear trend.

Moreover, Bitcoin recently reached $76,000, its highest level in about six weeks, before sellers pushed it lower. The rejection sent the asset below $68,000, though it later rebounded toward $72,000 before slipping under $70,000 again.

The latest moves show that Bitcoin remains sensitive to external events as traders track war-related headlines and broader market signals. At the same time, the weak recovery in whale activity suggests that large holders have not yet returned with strong conviction.

Analysts point to washout among short-term holders

Ali Martinez said Bitcoin’s Realized Cap for new holders has hit a low level that often appears after speculative interest leaves the market. According to his view, the recent reset has removed many weak hands and left more committed holders in place.

Analyst Michaël van de Poppe also said short-term holders are sitting on heavy losses in what he described as capitulation. He said many traders bought during Bitcoin’s initial drop toward $80,000, only to see positions fall deeper into loss as the price moved below $70,000.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Crypto World

JASMY Price Outlook: Can JasmyCoin Repeat Its 4,000% Rally from Current Accumulation Lows?

TLDR:

- JASMY has corrected 98.7% from its $0.36 all-time high and now sits in a HTF demand zone at $0.0045–$0.0060.

- A weekly close below $0.0040 invalidates the bullish structure, making this the most critical risk level to watch.

- Analysts project a potential 10x–40x rally for JASMY during the 2026–2027 altseason if key levels are reclaimed.

- JASMY must reclaim and hold above $0.01030 on higher timeframes to confirm any valid bullish market structure shift.

JasmyCoin (JASMY) is drawing attention from crypto analysts as it trades near multi-year lows. The token has completed a near-total macro correction from its all-time high.

Technical patterns suggest a possible long-term expansion phase may be forming. Analysts are now watching key demand zones closely. Price compression at range lows points to a potential shift in market structure ahead.

JASMY Sits Inside Critical HTF Accumulation Zone After Steep Decline

JASMY reached its previous cycle peak at approximately $0.36 before entering a prolonged downtrend. From that high, the token corrected by roughly 98.7%, placing it near historically significant demand levels.

The price is currently trading between $0.0045 and $0.0060, which analysts identify as a high-risk accumulation zone.

Crypto analyst Crypto Patel noted on X that JASMY “may be forming the same structure that led to a 4,000%+ expansion.”

The token has been trading inside a multi-year descending channel since its 2021 cycle top. Consistent lower highs and lower lows have defined price action throughout this period.

A confirmed breakout and retest occurred in 2024, representing a temporary shift in order flow. However, JASMY failed to reclaim the $0.05 level on higher timeframes, which led to redistribution. Price eventually returned to the current HTF demand region near cycle lows.

Compression at range lows is being read as a sign of seller exhaustion by market participants. The pattern mirrors behavior seen before the 2023–2024 rally, which produced a 1,933% gain. Analysts are treating the current zone as a late accumulation phase before any potential move higher.

Key Price Levels and Cycle Targets Guide Market Outlook for JASMY

For any bullish structure to remain valid, JASMY must reclaim and hold above $0.01030 on higher timeframes. Below that, mid-range resistance sits between $0.0070 and $0.0100. A weekly close below $0.0040 would invalidate the current accumulation thesis entirely.

The structure break level that would confirm a higher timeframe shift is $0.0208. Beyond that, major liquidity targets include $0.05 and $0.18. Bull cycle price targets outlined by the analyst are $0.0185, $0.050, and $0.185 respectively.

The 2026–2027 window is being flagged as a period for a potential massive breakout and retest. Analysts point to a possible 10x–40x rally during a broader altseason phase.

This projection is based on the repeating channel compression and expansion structure seen across previous cycles.

The current phase is described as late accumulation near cycle lows, with risk remaining elevated. Traders are advised to monitor weekly closes carefully around the $0.0040 invalidation level. No confirmed breakout has occurred yet, and price remains within the descending channel structure.

Although most of the cryptocurrency market is in the green now, with BTC climbing to $81,500 minutes ago, Ripple’s native token is actually among the top performers.

The asset posted a notable surge in the past hour or so, going from $1.42 to almost $1.50. This became its highest price tag since April 18, when it was rejected at $1.50 and spent the following three weeks trading sideways between $1.34 and $1.45.

This impressive price surge of almost 5% daily comes on the heels of many analysts predicting it over the past weeks.

As reported yesterday, Ali Martinez noted that the TD Sequential metric had flashed a major buy signal on the 4-hour chart. The analyst outlined targets of up to $1.82 if it manages to decisively break through the $1.45 resistance.

Fellow analyst CW noted that the token’s current chart shows significant strength, and predicted that “a full-scale rise for XRP is imminent.” Before that, they forecasted a “historic rally” in the making.

Another popular analyst on X who often touches upon XRP’s price moves, EGRAG CRYPTO, was significantly more bullish on the asset’s long-term performance. They touched upon the historical EMA Ribbon and outlined three different scenarios for the asset’s future.

Even the most modest one envisioned a mind-blowing 1,000% surge based on historical performance, while the most likely to occur, according to EGRAG, predicted a 1,250% surge, which would send the token flying to $13.

The post Ripple (XRP) Is Breaking Out as Analyst Expects ‘Full-Scale Rise’ appeared first on CryptoPotato.

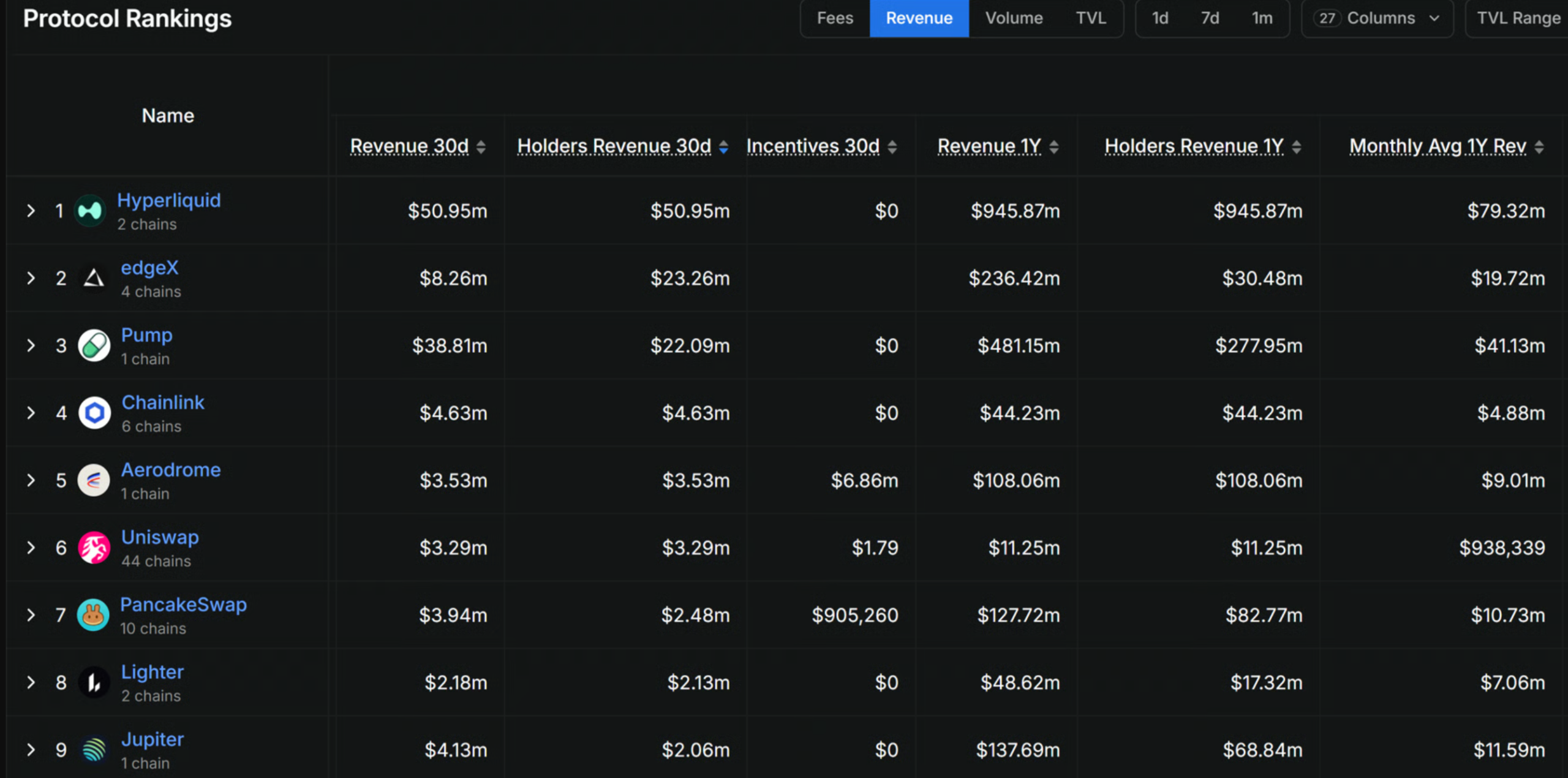

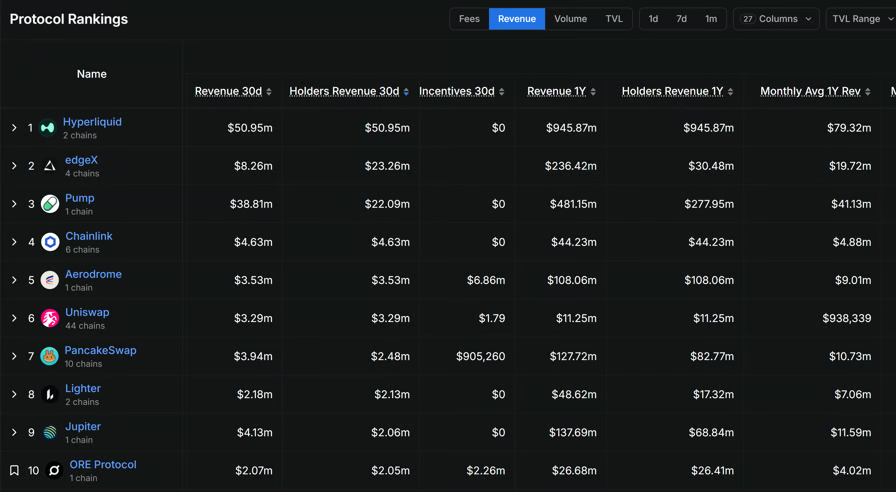

Three young DeFi applications, Hyperliquid, Pump.fun and edgeX, returned $96.3 million to token holders in 30 days. The figure marks one of the largest concentrated payouts from any DeFi cohort tracked in 2026.

Each protocol used a different mechanism to deliver the cash. Only Hyperliquid funded its full payout from trading fees alone. Pump.fun split revenue with operations, and edgeX paid out roughly three times what it earned.

The DeFi Shift From Emissions to Real Revenue

During the past cycle, DeFi protocols rewarded users by minting tokens and distributing them through liquidity programs. The model inflated supply faster than demand, leaving holders to absorb relentless dilution.

Hyperliquid (HYPE), Pump.fun (PUMP) and edgeX (EDGE) sit at the front of a different cohort. They generate fees from active products and route part of those fees back to holders through buybacks or burns. Token supply is treated as something to defend, not expand.

DefiLlama’s holder revenue rankings show the three accounted for the majority of monthly holder cash flow.

The categories tracked include perpetual trading and meme coin issuance. Their combined $96.3 million came in over a stretch when the broader DeFi sector saw flat fee growth.

How Each Protocol Got to the Number

Hyperliquid produced $50.95 million in protocol revenue across the 30-day window. The platform channeled the full amount to HYPE holders, the largest absolute payout in the group. Spending on user incentives was zero, an unusually clean ratio for a perpetual exchange of its size.

The Assistance Fund handles the routing. Launched in January 2025, the fund captures 97% of trading fees. It uses them to repurchase HYPE on the open market through automated Layer 1 execution.

A validator proposal in December 2025 sought to mark roughly $920 million in fund-held HYPE as permanently retired. If passed, the burn would tighten HYPE supply at the structural level.

Pump.fun returned $22.09 million to PUMP holders out of $38.81 million in protocol revenue. The Solana token launchpad ran a 100% buyback policy for nine months.

It switched to a 50/50 split on April 28, 2026. Half of net fees now feed an automated buy-and-burn routed through an irreversible smart contract. The shift coincides with the strongest user-side data the platform has ever produced.

edgeX is the outlier. The perpetual exchange paid $23.26 million to EDGE holders against just $8.26 million in protocol revenue.

The ratio suggests the team is drawing on reserves or pre-launch incentive budgets to keep payouts elevated. The EDGE token went live on March 31, 2026. The project remains in the early phase of its tokenomics rollout.

The Sustainability Question

Hyperliquid’s model is the most defensible. Its payouts scale directly with trading fees. A slow trading month would shrink holder distributions rather than force the protocol into the red.

Critics inside the perp DEX category flag concentration risk. A single product line still drives the bulk of revenue.

Pump.fun’s case is more contested. Analysts argue that after burning roughly $370 million in PUMP, the token still failed to track its revenue base. Critics call the valuation narrative-driven rather than cash-flow driven.

A new study from CoinGecko complicates that read. The data firm found that 73.3% of Pump.fun traders booked realized gains in April 2026.

The figure is up from a 30.1% trough in June 2025. It reverses two straight years of net losses for active users. Active wallets have rebounded to 3.14 million from a December 2025 low of 1.8 million.

The gains were small. About 65.1% of profitable wallets earned between $1 and $500 for the month, and only 5.4% cleared $1,000. Even so, the user base now skews toward repeat traders rather than first-time speculators. That audience historically drove churn at the platform.

edgeX’s gap between revenue and payout is the cleanest red flag. Subsidized distributions can attract early holders but the math only works while reserves last.

The protocol must lift fee generation fast enough to cover its EDGE buy pressure. That is the central question for token holders heading into the second half of 2026.

The $96.3 million payout marks a meaningful shift in how DeFi rewards holders. Only Hyperliquid funded the full distribution from organic fee revenue.

Pump.fun’s case rests on a still-young trader recovery. edgeX has yet to prove its math works without subsidies.

The post How Hyperliquid Managed to Lead 3 DeFi Apps That Paid Holders $96 Million In 4 Weeks appeared first on BeInCrypto.

Ethereum’s native token, Ether (ETH), has fallen more than 35% against Bitcoin (BTC) over the past year, and the downtrend may still have further to go.

Key takeaways:

- ETH may plunge another 40% as it mirrors the 2025 bear trend setup.

- Rising Ether reserves on Binance, even as Bitcoin reserves decline, add to the case for further ETH downside.

ETH risks 40% decline after topping near multi-year trend line

ETH/BTC remains stuck below a multi-year descending trend line that has capped every breakout attempt since 2022, including one that preceded the nearly 70% decline between 2024 and 2025.

ETH/BTC monthly chart. Source: TradingView

A similar setup now appears to be taking shape again.

After retesting the same trend line in August 2025, ETH/BTC was rejected near a confluence of resistance that included the 0.382 Fibonacci retracement level and the 50-month exponential moving average (50-month EMA, red).

The pair has since turned lower and slipped back below its 20-month EMA (green) support near 0.034 BTC, a sign that sellers continue to dominate the trend.

The next major downside target for 2026 comes in around 0.0176 BTC if the weakness persists. This level, down about 40% from current rates, aligns with the 2020 cycle bottom.

Exchange reserves highlight ETH-BTC divergence

Exchange data points to persistent sell-side risk for Ether.

As of May, ETH reserves on Binance, the world’s largest crypto exchange by volume, had climbed to 3.62 million ETH, accounting for roughly 24.6% of all Ether held across exchanges, according to data resource CryptoQuant.

Ethereum reserves on Binance. Source: CryptoQuant

In comparison, Bitcoin reserves on Binance have fallen.

Bitcoin reserves on Binance. Source: CryptoQuant

Rising exchange balances usually signal that more tokens are available for sale, which can weigh on price when demand is not strong enough to absorb the added supply.

Falling reserves, on the other hand, often suggest coins are being moved off exchanges for longer-term holding.

In that sense, Binance reserve trends reinforce the broader market picture: Ether is facing relatively higher available supply, while Bitcoin is showing signs of tighter exchange-side liquidity.

Related: Four signs that show Ethereum’s rally is exhausted at $2.4K

Ethereum’s weakness reflects a broader shift in fundamentals. For years, Ether has lagged behind Bitcoin in part because Ethereum’s “ultrasound money” narrative has lost momentum.

BTC, on the other hand, continues to draw strength from corporate accumulation led by firms like Strategy and its growing integration into Wall Street portfolios.

Bitcoin extended its sideways drift around the $80,000 level as traders weighed a possible retest lower ahead of the week’s end. After a midweek push toward the $83,000 mark that failed to hold, market participants are watching whether BTC can sustain above $80,000 or slip toward established support as momentum remains broadly constructive for a continuation higher.

Key takeaways:

- Bitcoin has held above $80,000 through the weekend, but a sub-$80,000 retest remains on the radar for a test of nearby support.

- The prevailing bullish narrative hinges on a confluence of support levels just under $80,000—the so-called bull market support band formed by two moving averages—and a broader high-timeframe blue zone around $75,000.

- Inflation data in the U.S. next week is viewed as a potential catalyst, with traders saying the CPI release is largely priced in for the near term.

- Key levels to monitor include the $74,000 area as a critical fallback and liquidity sweeps that could signal the next move.

Near-term path: bulls test the 2D bull market band

Price action on the hourly to short-term charts shows BTC padding gains after a quiet weekend, avoiding a drop back below the $80,000 threshold. The decline from the midweek high near $83,000 failed to establish a sustained breakout, prompting traders to re-emphasize a retest of support as a prerequisite for a renewed upside move. Analysts point to the “bull market support band”—a duo of moving averages just below the $80,000 level—as a critical zone where buyers have previously stepped in during pullbacks.

“On the low-timeframes, after rejecting at the high-timeframe resistance range, I believe the most likely outcome is a short-term pullback toward the 2D Bull Market Support Band, which has been a strong reversal zone over the last couple of months,” Cryptic Trades wrote in a recent post.

In the view of Cryptic Trades, as long as BTC holds above the band and the adjacent blue-highlighted high-timeframe support around $75,000—which aligns with a notable bottoming formation observed in April 2025—the door remains open to higher prices. The note underscores how these zones have repeatedly proven to be meaningful turning points during the current rally phase.

Support levels and what traders want to see

Market participants highlighted a preference for a clean break above the stubborn area in the low $80,000s to confirm a more durable move higher. Daan Crypto Trades noted that the initial advance above the band was not a decisive breakout, signaling the need for a sustained hold in the upper $80,000s to validate continued upside. “Would want to see a move to at least clear that sticky area around the low $80Ks and hold there for a week or two,” they advised on social media.

From a broader perspective, the $74,000 region remains in view as a potential liquidity pivot should selling pressure intensify. Traders caution that a sweep of liquidity around key pivots could signal the next directional shift, making the area around the $74k–$75k zone particularly consequential for the near-term trajectory.

Inflation data as a potential catalyst

The upcoming release of the U.S. Consumer Price Index (CPI) for April looms as a defining factor for the near-term path of BTC, with traders arguing that the data is largely priced in by the market. The CPI print is expected to reflect continuing macro pressures stemming from oil prices and broader geopolitical developments, with some observers suggesting the outcome could influence how large players adjust their risk profiles around this event.

“It’s priced in,” wrote Killa, a consistently watched figure on X, noting that BTC has tended to rally after the last two CPI releases. However, following 2025 CPI price action, he warned, there could be a shift as big players de-risk into the event counter-narrative.

Cryptocurrency traders point to the CPI milestone as a potential catalyst that may either reinforce Bitcoin’s upside or reintroduce volatility as participants reassess inflation trajectories and macro risk. While a hotter-than-expected print could inject risk-off sentiment, a cooler outcome could keep the bulls in control as liquidity conditions remain supportive in the longer horizon. The immediate question remains whether price action can maintain its footing above the core support bands while traders await fresh cues from the inflation data.

In addition to the CPI narrative, traders continue to monitor the response around the bull market support band and the broader blue-support region near $75,000. Should price manage to stabilize and then clear the upper resistance area, the odds of a renewed ascent improve, according to multiple analysts who weighed in on the weekend chatter.

Overall, the market appears to be trading with a structured plan: hold above the key support zones to preserve the upside thesis, while waiting for a clearer signal from price action and the CPI release. The outcome this week may hinge on whether buyers can demonstrate resilience in the face of a potential near-term pullback or whether selling pressure intensifies, prompting a deeper test of the lower support band.

As the week unfolds, traders will be paying close attention to whether Bitcoin sustains above the 2D bull market band and the blue higher-timeframe support near $75,000, and how the CPI reading translates into shifts in risk appetite. If the price remains anchored above these levels, the case for further upside remains plausible; if not, a test of the $74,000 area could reframe the near-term outlook and set the stage for a more measured consolidation before the next leg higher.

Crypto World

Binance Reports 77% Emerging Market User Share as 1.4 Billion Adults Remain Unbanked Globally

TLDR:

- Binance’s emerging market user share rose sharply from 49% in 2020 to 77% in 2026, per platform data.

- Around 83% of Binance’s multi-product users are based in emerging markets, showing deep regional engagement.

- Stablecoin savers on Binance grew from 4% in 2020 to 28% in 2026, with 73% based in emerging markets.

- Crypto platforms like Binance operate 24/7 with no minimum balance, lowering barriers for unbanked users globally.

Binance is addressing global financial exclusion by offering a full spectrum of products within one account. The platform aims to serve users across income levels, from basic savings to advanced trading tools.

With 1.4 billion adults still unbanked worldwide, according to the World Bank, crypto infrastructure is emerging as a practical alternative.

Binance’s data shows growing adoption in emerging markets, where its user share climbed from 49% in 2020 to 77% in 2026.

Crypto Infrastructure Reshaping the Economics of Financial Access

Traditional finance has long placed high barriers on participation. Geography, account minimums, and eligibility standards have historically shut out hundreds of millions of people.

Crypto platforms operate differently — they run 24/7, require no minimum balance, and function across borders through a single mobile interface.

Digital-asset platforms allow users to hold assets, earn yield, make payments, and access global markets. This changes who gets to participate and on what terms.

A person with limited access to traditional investment products can still engage with financial markets through one digital account.

Binance has built its platform around this premise. The company offers tools for capital preservation, passive yield, on-chain utility, and advanced trading — all within one account.

As Binance noted, “one account, access to a full spectrum of products so users can start where they are and grow on their own terms.” Users can start at any level and expand their participation over time as their needs evolve.

This range of options makes access more practical and durable. When diverse products exist on one platform, users are not forced to move between services as their financial goals change. That continuity matters, especially in markets where financial infrastructure is still developing.

Emerging Markets Drive Multi-Product Engagement on Binance

Binance’s growth in emerging markets reflects real demand for broader financial services. Users in these regions are not just trading — they are saving, sending money across borders, and generating yield.

Platform data shows that 83% of multi-product users are based in emerging markets. Binance has described its role as building “a platform where more of those financial functions can come together in a usable way.”

Stablecoin adoption further supports this pattern. Approximately 28% of Binance users holding at least $10 keep more than half their portfolio in stablecoins.

That figure was just 4% in 2020. Around 73% of all stablecoin savers on the platform are based in emerging markets.

This behavior points to Binance functioning as an integrated financial account for many users. Rather than a trading venue alone, the platform is serving savings and payments needs alongside crypto investing.

Binance stated that “the next era of finance will not be defined only by whether markets are open, but by whether more people can actually navigate them.” That is a meaningful shift in how users in lower-income environments are engaging with digital finance.

The data also shows that users with access to more products stay more engaged. Those using three or more products account for 14% of total active users. Broader product access, therefore, directly connects to deeper financial participation.

Three of DeFi’s relatively young applications, including Hyperliquid, EdgeX and Pump.fun, have distributed a combined $96.3 million to token holders over the past 30 days, as the sector’s focus shifts to actual earnings.

Hyperliquid led the pack, generating $50.95 million in revenue over the period, all of which went directly to token holders with zero spent on incentives, according to data from DefiLlama. Pump.fun came in second with $22.09 million returned to holders out of $38.81 million in total revenue. EdgeX followed with $23.26 million distributed to holders from $8.26 million in protocol revenue, suggesting that the platform is drawing on reserves or alternative income streams to reward holders.

On an annualized basis, Hyperliquid has generated $945.87 million in revenue over the past year, all returned to holders, while Pump.fun sits at $481.15 million and EdgeX at $236.42 million.

Among other major protocols, Chainlink returned $4.63 million to holders, Aerodrome $3.53 million and Uniswap $3.29 million across 44 chains. PancakeSwap generated $3.94 million in revenue but returned $2.48 million to holders while spending $905,260 on incentives.

Related: DeFi can freeze stolen funds, but not everyone agrees it should

Crypto community now focuses on revenue

The data comes as revenue is becoming the metric that matters most in crypto, with token holders pushing protocols to justify their valuations through actual earnings rather than transaction volumes or network growth figures.

“Nobody cares that your chain does 10x the TPS anymore,” wrote Robbie Klages, co-founder of The Rollup, referring to a blockchain’s measure of transactions per second. “The market is ‘show me the money right now.’ Treat it like a business not a network growth thesis,” he added.

Top DeFi protocols by Holders Revenue. Source: DefiLlama

Another X user wrote that the shift from narrative to earnings is “permanent now,” warning that protocols unable to show real revenue will be valued like pre-revenue startups in a rate hike environment, a reference to the kind of sharp devaluations that hit speculative assets when capital gets expensive.

Related: Aave-Linked DeFi United Details rsETH Recovery Plan

DeFi is becoming backend for onchain economy

Andre Cronje, founder of the popular DeFi protocol Yearn.Finance, said that DeFi in 2026 looks less like a speculative playground and more like functioning financial infrastructure. He noted that stablecoins have grown into a $320 billion market led by Tether and Circle, decentralized exchanges are processing over $160 billion in monthly spot volume and perpetual DEXs are handling $540 billion monthly.

Cronje added that lending protocols, including Aave, Morpho and Maple Finance, are sitting on $28 billion in active loans, while real-world assets are increasingly being used as onchain collateral. “DeFi is no longer just competing for APY. It is becoming the backend for the onchain economy,” he wrote on X.

Magazine: Guide to the top and emerging global crypto hubs — Mid-2026

Crypto World

BeInCrypto Institutional Research: 15 Digital Asset Custody Providers Behind Crypto Adoption

Digital asset custody is one of the core trust layers behind institutional crypto adoption. Best Custody Provider is an award category within The BeInCrypto Institutional 100, an annual research-driven program recognising institutional digital asset excellence across 26 categories and six pillars.

This category sits in Pillar 2: Capital Markets & Infrastructure. The 15 firms below are its longlist. A shortlist will be named in May 2026, with the winner announced at Proof of Talk in Paris on June 2–3, 2026.

- Long list: 15 custody providers across federal charters, NYDFS trust companies, MPC platforms, bank-backed JVs, APAC custodians, and off-exchange settlement networks

- Initial pool: More than 30 qualified custodians and digital asset custody platforms screened; 15 advanced to the long list

- Scoring: 50% quantitative data · 50% Expert Council

- Criteria assessed: Qualified custodian status, assets under custody, institutional client base, audit posture, product depth, jurisdictional reach, settlement innovation, reputation

- Data sources: OCC, NYDFS, FCA, FINMA, BaFin, MAS, MiCA-CASP registers, Jersey FSC, audited filings, company disclosures, PitchBook, Tracxn, and Crunchbase

| # | Firm | Custody Sub-Segment | HQ | Reach | Top Licensure / Charter | Representative Work |

|---|---|---|---|---|---|---|

| 1 | Anchorage Digital | Federal-chartered crypto custody | SF / NY / Sioux Falls / Singapore / Porto | $4.2B valuation Backed by a16z, GIC, Goldman Sachs, KKR, Visa, Tether |

First federally chartered US crypto bank Atlas Settlement Network is live with institutional integrations |

OCC National Trust Bank Charter MiCA via BaFin, VARA, Singapore, Korea |

| 2 | Coinbase Custody | US ETF custody provider | Wilmington / SF, USA | Custodian for 8 of 11 spot Bitcoin ETFs 80%+ of US Bitcoin ETF assets routed via Coinbase |

NYDFS Limited Purpose Trust Charter Coinbase Custody Trust Company |

Primary custodian for IBIT Co-custodian for Morgan Stanley Bitcoin Trust |

| 3 | BitGo | Federally chartered public custody | Sioux Falls / Palo Alto, USA | $104B+ AUC Thousands of institutional clients |

Custody tech used by TradFi banks Coverage across the US, EU, Switzerland, UAE, Singapore, Australia, Hong Kong |

NYSE IPO completed in Jan 2026 First public federally chartered digital asset infrastructure firm |

| 4 | Fidelity Digital Assets, NA | Asset manager-operated federal trust | Boston, USA | Custody for FBTC and FETH Backed by Fidelity’s ~$15T+ AUA platform |

Acquired TRES Finance and Dynamic Building a custody, wallet, and accounting operating system |

OCC charter approved Dec 2025 Plans include stablecoin issuance and staking services |

| 5 | BNY | Global custodian with crypto surface | New York, USA | ~$55.8T AUC/A Live BTC and ETH custody since 2022 |

OCC-regulated bank Institutional custody operations |

Co-custodian for Morgan Stanley MSBT IBIT cash custodian and administrator |

| 6 | Fireblocks | MPC-native institutional platform | New York / Tel Aviv | 2,400+ institutional clients $4T+ annual digital asset transfers in 2025 |

NYDFS BitLicense SOC 2 Type II + ISO 27001 |

OCC conditional national trust bank charter Conversion from the New York State trust |

| 7 | Ripple Custody (Metaco) | Bank custody technology stack | Lausanne / SF | Acquired Tungsten Custody in the UAE Standard Chartered reportedly weighing full takeover |

OCC conditional charter FINMA-regulated custody stack |

Ripple rebranded Metaco as Ripple Custody Ripple National Trust Bank’s charter was conditionally approved |

| 8 | Sygnum | Swiss-licensed crypto bank | Zurich, Switzerland | 2,000+ institutional clients $5B+ AUM; unicorn valuation |

FINMA banking licence MAS, Liechtenstein, ADGM permissions |

Reached unicorn status in Jan 2025 Sygnum Connect and Sygnum Protect live |

| 9 | Komainu | TradFi-backed custody JV | St Helier, Jersey | Operations across Jersey, UK, Italy, Singapore, UAE, Japan ~120 staff target |

Jersey FSC, UK FCA, UAE VARA Italy OAM and Singapore MAS via Propine |

$75M Series B funded in Bitcoin Propine acquisition expanded Singapore custody hub |

| 10 | Zodia Custody | Standard Chartered-backed custody | London, UK | ~150 staff across 7 offices 75+ digital assets supported |

UK FCA, Ireland MiCA-CASP, Lux, ADGM Hong Kong and Japan FSA coverage |

Sub-custodian for Clearstream Crypto offering AnchorNote off-exchange settlement launched |

| 11 | Crypto Finance Group | Exchange-parent regulated custody | Zurich, Switzerland | Deutsche Börse majority-owned Clearstream institutional distribution |

FINMA Switzerland BaFin licences + MiCA-CASP |

Aura private wealth platform launched Qualified custodian in the Fireblocks network |

| 12 | Hex Trust | APAC custody anchor | Hong Kong | $104M raised APAC and MENA institutional coverage |

HK SFC, MAS CMS, ADGM, VARA, DFSA Multiple licence categories |

ClearLoop settlement network expanded Komainu was integrated into ClearLoop in 2025 |

| 13 | Copper | Off-exchange settlement custody | London, UK | 200+ institutional clients Multi-billion-dollar assets under custody |

Switzerland SO-FIT affiliation Abu Dhabi ADGM licence |

~$2B valuation 9+ exchanges on the ClearLoop network |

| 14 | Ceffu | Institutional MPC and OES | Lithuania | 200+ institutional clients Multi-billion assets under custody |

Lithuania MiCA-CASP Multi-jurisdiction sub-custody arrangements |

MirrorX off-exchange settlement integrated with KuCoin EU institutional custody status expanded |

| 15 | Bakkt Trust | NYDFS-regulated US custody | New York, USA | ICE-origin institutional custody Multi-asset custody platform |

NYDFS Limited Purpose Trust Charter BitLicense + 50-state MTLs |

Bakkt Warehouse supports institutional custody $125M+ insurance across cold and warm wallets |

About This List

The BeInCrypto Institutional 100 — Digital Asset Custody (2026 Long List) identifies custody providers supporting institutional digital asset adoption. The category covers federally chartered crypto banks, NYDFS trust-company custodians, MPC-native platforms, bank-backed custody ventures, APAC-regulated custodians, exchange-parent custody platforms, and off-exchange settlement networks.

Firms primarily focused on stablecoin issuance are evaluated separately under stablecoin infrastructure categories. Parent firms may appear in other categories when their custody product line meets that category’s threshold independently.

Methodology

This category is evaluated under Track A of the BeInCrypto Institutional 100 methodology: 50% based on quantitative metrics and 50% on Expert Council scoring.

Assessment spans seven weighted criteria: regulator-recognized qualified custodian status, assets under custody and institutional client base, regulatory and audit posture, product depth, multi-jurisdiction reach, settlement and capital-efficiency innovation, and reputation.

Data was verified using OCC national trust bank charter approvals, NYDFS BitLicense and trust-company registers, FCA, FINMA, BaFin, MAS, MiCA-CASP authorizations, Jersey FSC records, audited filings, company disclosures, partnership announcements, and private-market sources, including PitchBook, Tracxn, and Crunchbase. Figures reflect the most recent available data at the time of publication.

The post BeInCrypto Institutional Research: 15 Digital Asset Custody Providers Behind Crypto Adoption appeared first on BeInCrypto.

TLDR:

- Hyperliquid burned over 45 million HYPE tokens worth more than $2 billion using collected platform fees.

- The exchange generates close to $1 billion annually and directs 100% of revenue toward HYPE buybacks and burns.

- Burned tokens represent roughly 14.5% of the 310 million HYPE distributed in the first trader airdrop.

- Hyperliquid recorded $1.5 billion in net inflows over three months as Arbitrum lost the same amount in outflows.

Hyperliquid has burned more than 45 million HYPE tokens as its fee-driven buyback model gains attention across the crypto market. The decentralized exchange recorded approximately $824,688 in fees within a single 24-hour period.

All collected fees went directly toward purchasing and burning HYPE tokens. The platform now reports close to $1 billion in annual revenue. Net flow data further shows $1.5 billion in inflows over the past three months.

Hyperliquid’s Buyback and Burn Model Sets a New Standard

Hyperliquid’s tokenomics structure differs from most crypto projects in circulation today. Rather than selling tokens to cover operational costs, the platform channels all revenue into buybacks. This approach has resulted in the permanent removal of 45,116,933 HYPE tokens from supply.

According to data shared by Hyperliquid Hub on X, the burned tokens carry a market value of over $2 billion. That figure equals roughly 14.5% of the entire first trader airdrop, which totaled 310,000,000 HYPE tokens. The scale of this burn reflects a consistent and structured approach to reducing supply.

The daily burn has remained steady, which sets it apart from one-time or irregular token removal events seen elsewhere.

Each fee cycle feeds directly into the Auto-Fill mechanism, which executes the buyback and burn automatically. Users who sell their HYPE to the AF effectively contribute to the permanent reduction of circulating supply.

With close to $1 billion in annual revenue, the platform sustains this model without relying on external funding or token sales.

This positions Hyperliquid as a revenue-generating protocol that returns value to its token holders through supply reduction rather than direct distributions.

Hyperliquid Records $1.5 Billion in Net Inflows Over Three Months

Capital movement data shows a strong preference for Hyperliquid among traders shifting funds between platforms.

The exchange recorded $1.5 billion in net inflows over the last three months alone. This trend points to growing user confidence in the platform’s structure and reliability.

By contrast, Hyperliquid Hub on X noted that Arbitrum recorded $1.5 billion in net outflows during the same period.

The contrast between the two figures shows a clear directional shift in where traders are choosing to deploy capital. Hyperliquid appears to be the primary destination for those exiting Arbitrum.

Net flow figures are a common measure of capital movement across blockchain platforms. Consistent inflows typically reflect user acquisition and growing liquidity. For Hyperliquid, the $1.5 billion figure adds to an already active period of protocol growth.

Together, the burn data and the net flow numbers paint a picture of a platform gaining both liquidity and long-term token value. The combination of revenue-backed buybacks and rising inflows continues to draw attention from traders watching on-chain activity closely.

Bitcoin (BTC) eyed $81,000 into Sunday’s weekly close as traders saw a fresh support retest next.

Key points:

- Bitcoin preserves $80,000 over the weekend, but traders are waiting for a dip to retest a familiar chart feature.

- Continuation higher remains the overall consensus for what happens afterward.

- US CPI data is due out, with Bitcoin already “pricing in” the result.

Bitcoin traders: Sub-$80,000 retest next

Data from TradingView showed BTC price action trending higher after a mostly flat weekend, avoiding a return below $80,000.

BTC/USD one-hour chart. Source: Cointelegraph/TradingView

After a midweek trip to near $83,000 failed to hold, however, traders saw the need for BTC/USD to retest support — something that they now reiterated.

Of particular interest was the bull market support band — two moving averages just below the $80,000 mark.

“On the low-timeframes, after rejecting at the high-timeframe resistance range marked in purple, I believe the most likely outcome is a short-term pullback toward the 2D Bull Market Support Band, which has been a strong reversal zone over the last couple of months,” analytics account Cryptic Trades wrote alongside a chart in its latest post on X.

“As long as price continues to hold above the support band and the broader high-timeframe support range marked in blue around $75K, which aligns with the April 2025 bottoming formation, I believe the most likely outcome remains further upside.”

BTC/USD one-day chart. Source: Cryptic Trades/X

Trader Daan Crypto Trades agreed, calling the initial move above the support band “not a clean break.”

“Would want to see a move to at least clear that sticky area around the low $80Ks and hold there for a week or two,” he told X followers.

BTC/USD one-week chart. Source: Daan Crypto Trades/X

CPI already “priced in” to BTC

Ahead of fresh US inflation data next week, trader Killa warned of headwinds returning for BTC price strength.

Related: Bitcoin Bollinger Bands push key breakout as creator acts on positive signal

The Consumer Price Index (CPI) for April, due out on Tuesday, was set to show the ongoing impact of the US-Iran war and oil-price rises on the economy.

“Its priced in,” Killa wrote on X.

“BTC has rallied after the last two CPI releases. However, if we follow 2025 CPI price action, we may see bigger players start de-risking into the event counter narrative.”

BTC/USD chart with CPI releases. Source: Killa/X

Support levels to watch also included the area around the bull market support band, with $74,000 on the radar, should it fail.

“I would watch for liquidity sweeps around this pivot to signal the next move,” Killa added.

BRAD JUST LEAKED IT LIVE ON AIR?!?!?

‘Tragic incident’ as man in his 90s found dead after explosion and fire at property

Which Logistics Powerhouse Is the Better Buy Right Now

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World2 days ago

Crypto World2 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

NewsBeat7 days ago

NewsBeat7 days agoChannel 5 – All Creatures Great and Small series 7 new post

-

Crypto World3 days ago

Crypto World3 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Marianne Dress

-

Tech6 days ago

Tech6 days agoImage AI models now drive app growth, beating chatbot upgrades

-

NewsBeat3 days ago

NewsBeat3 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Politics1 day ago

Politics1 day agoPolitics Home Article | Starmer Enters The Danger Zone

-

Business1 day ago

Business1 day agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Crypto World7 days ago

Crypto World7 days agoBlackRock Buys $284M In Bitcoin On May 1 As The Best Crypto To Invest In For 2026 Sits Below A Pending Binance Listing

-

Entertainment7 days ago

Entertainment7 days agoOlivia Wilde Reacts To Viral ‘Corpse’ Comparison

-

Sports7 days ago

Sports7 days agoInter Milan Win Serie A Title After Victory Over Parma

-

Sports7 days ago

Sports7 days agoLa Liga: Vinicius Jr scores twice as Real Madrid win to keep Barcelona waiting for title

-

Sports7 days ago

Sports7 days agoEvery word of Arne Slot’s heated rant after Manchester United win vs Liverpool

-

Crypto World5 days ago

Crypto World5 days agoUAE Free Zone Deploys Blockchain IDs to Verify Registered Firms

-

Entertainment7 days ago

Entertainment7 days agoOther Bennet Sister Love Triangle Cast: Ella Bruccoleri, Donal Finn

-

Sports7 days ago

Sports7 days agoJoel Embiid urges Sixers fans not to sell playoff tickets to Knicks fans

-

Sports6 days ago

Sports6 days ago2026 NHL playoff picks: Second-round predictions, series odds, Stanley Cup bracket

-

Entertainment7 days ago

Jennifer Lawrence’s Mary Jane Sneakers Are Spring’s It-Girl Shoe

-

Entertainment7 days ago

Entertainment7 days agoMoroccan Reacts To Nick Cannon’s Dating Rules For His Sister

-

Entertainment7 days ago

Kylie Jenner and Timothee Chalamet Hold Hands in NYC Outing

You must be logged in to post a comment Login