Crypto World

BlueMove’s $500K SUI loss raises insider job suspicions

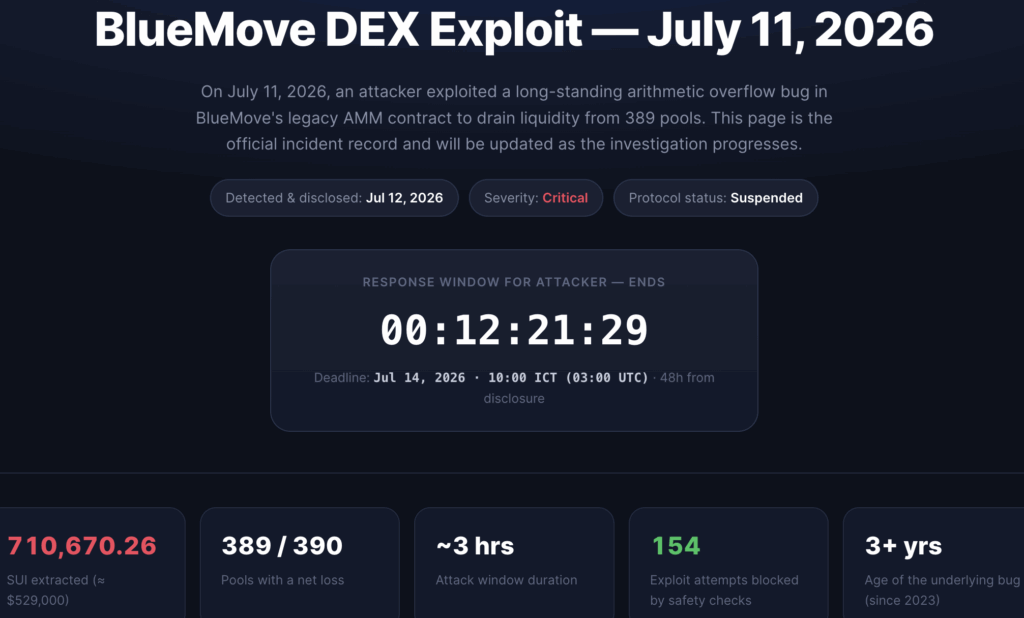

Around $500,000 worth of SUI tokens was drained from BlueMove DEX’s locked pools last weekend, leading users to speculate that the incident may have been an inside job.

Quantum Void Labs founder, Tyler Simpson, shared screenshots last Saturday appearing to show over 700,000 SUI tokens being drained from the locked liquidity pools provided by BlueMove.

Simpson initially accused the platform of draining its locked liquidity pools, and implied its alleged actions were “crime.” However, he later noted that the firm was exploited.

The next day, he claimed that BlueMove had “shipped the backdoor themselves” after it implemented a package on May 31 that laid the groundwork for the exploit.

He said it added immutable functions like “add_liquidity_returns,” and “double-mint LP inflation” before, over 40 days later, the exploit began.

Read more: SUI: Stops Unexpectedly and Intermittently

Because of this, Simpson has described the draining event as a “delayed rug pull.”

BlueMove says it will compensate users

BlueMove disagrees. It claims on its website that it was the fault of an attacker exploiting “a long-standing arithmetic overflow bug in BlueMove’s legacy AMM contract to drain liquidity from 389 pools.”

The bug has reportedly been visible since at least 2023, with BlueMove explaining that an upgrade overlooking the bug was partly responsible for the exploit as it prevented any further patches.

It claims that “because the UpgradeCap was burned on June 3, BlueMove currently has no on-chain path left to patch or disable the vulnerable v1 package.”

BlueMove added that a fix would now require “an independent admin/freeze capability (if one exists outside the UpgradeCap) or a full migration to a new, audited package.”

Read more: Robinhood Chain scams are already costing users dearly

BlueMove also sent a message to a crypto address in an attempt to contact the hacker and strike a white hat bounty deal with them.

It says, “You drained the BlueMove DEX pool (~$400k). Keep 30% as a white hat bounty and return 70% within 48h to our Sui address.”

BlueMove added, “If returned, we will consider the matter resolved. Otherwise, we will pursue all available legal and recovery actions.”

That’s around $150,000 for the hacker (as long as the price of 700,000 SUI remains roughly $500,000).

BlueMove also claims it will compensate all affected users if it doesn’t receive a response from the hacker in the next 48 hours, adding that the project will shut down going forward.

The company’s operation’s remain suspended as it continues to investigate what happened.

A SUI Network spokesperson responded “no comment” when Protos asked it about the draining event and the recovery of funds.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

The post BlueMove’s $500K SUI loss raises insider job suspicions appeared first on Protos.

Japanese convenience store operator Lawson will test payments with the yen-denominated JPYC stablecoin in early August.

Summary

- Lawson will connect JPYC payments directly to its POS system during a single-store Tokyo trial.

- Customers will scan mobile wallet barcodes, while HashPort updates balances using verified checkout transaction data.

- Japan’s megabanks are also preparing yen stablecoins, widening competition across regulated digital payment networks nationwide.

The company will run the trial at its Takanawa Gateway City store in Tokyo’s Minato Ward. HashPort, a digital asset wallet provider, will support the payment system and process balance changes linked to purchases.

Lawson described the project as Japan’s “first” stablecoin payment trial connected directly to a point-of-sale system. That claim comes from the company and the test has not yet started. Lawson has not announced a chainwide launch.

It will decide on wider use after checking system stability and transaction speed. The company will also review whether the process fits normal store operations without slowing customers or adding extra work for employees during busy periods.

How the POS-integrated payment will work

Customers will open a supported mobile wallet and display a barcode on their phones. A Lawson employee will scan the barcode with the store’s existing POS terminal. HashPort will then use the payment information to update the customer’s JPYC balance. The process keeps the checkout within Lawson’s current store system.

The POS link will also allow Lawson to manage purchase details, including product quantities and payment times, alongside its usual sales data. The trial will measure how reliably the systems connect and how long each payment takes.

Customers will use stablecoins at checkout, but staff will still handle the scan through the normal sales terminal. Lawson can compare the stablecoin flow with card and QR payments, including processing steps, error handling and the time needed to finish each sale.

JPYC moves into everyday retail

JPYC Inc. began issuing JPYC on October 27, 2025. The token tracks the Japanese yen and uses yen deposits and Japanese government bonds as reserve assets. As crypto.news reported, the stablecoin initially waived transaction fees and aimed to support payments and transfers under Japan’s regulated framework.

Lawson’s test follows smaller retail and service launches. Japanese okonomiyaki restaurant operator Chibo started accepting JPYC at selected stores in April, according to Financial News. Dental clinics in Tokyo and Chiba also plan to add JPYC payments with HashPort.

The Lawson trial differs because it links the stablecoin payment directly with a major retailer’s POS system. The report said stablecoins may offer merchants lower fees than cards or QR services, though Lawson has not released fee figures for this pilot.

Japan expands regulated stablecoin activity

Japan’s large banks are also preparing yen-based stablecoin services. MUFG Bank, Sumitomo Mitsui Banking Corporation and Mizuho Bank plan to begin live transactions during fiscal 2026, which ends in March 2027. As crypto.news reported, the banks formed a council to develop shared rules for issuance, governance, systems and future participation.

Moreover, the banking project follows an FSA-backed test involving corporate cross-border payments and Progmat’s blockchain infrastructure. Japan has also opened regulated access to foreign stablecoins. Ripple and SBI launched the dollar-backed RLUSD through SBI VC Trade in June 2026 after approval from the Financial Services Agency.

American Bitcoin shares have fallen more than 95% from their peak, according to Bloomberg, cutting over $600 million from the value of Eric Trump’s roughly 6% stake.

Summary

- American Bitcoin’s stock lost over 95% despite its treasury growing beyond 8,000 BTC this month.

- The reverse split lifted ABTC’s quoted price but left the company’s underlying market value unchanged.

- A $117.2 million Bitcoin charge drove Q1 losses while mining costs fell sharply per coin.

The Bitcoin miner and treasury company reached a record low on Wednesday after months of selling pressure. ABTC closed at $6.13 on July 10, the latest available market close.

The fall followed a 1-for-15 reverse stock split that took effect after trading on July 2. Split-adjusted trading began on July 6 under the same Nasdaq ticker. The company reduced its issued share count from about 1.09 billion to roughly 73 million. A reverse split raises the quoted share price but does not increase the business’s total value.

Reverse split fails to stop selling pressure

American Bitcoin used the reverse split to support compliance with Nasdaq’s minimum bid-price rule. Shareholders approved the move at the company’s annual meeting in June. Crypto.news reported the approval on June 25, when ABTC remained under pressure despite the planned change. The stock then fell after split-adjusted trading started.

The company has not said the split can reverse its market decline. Reverse splits can help a listed company meet exchange rules, but investors still price its earnings, assets, debt and outlook. Bloomberg’s calculation places the stock more than 95% below its peak. That decline reflects split-adjusted prices rather than a direct loss caused by the share consolidation.

Bitcoin reserve grows beyond 8,000 BTC

American Bitcoin continues to mine and accumulate Bitcoin while its share price falls. The company added 500 BTC in its latest update, taking its reserve above 8,000 BTC. As crypto.news reported on July 7, the treasury had more than tripled since the company’s Nasdaq debut. The firm also said its satoshis-per-share measure had nearly tripled.

Eric Trump promoted the treasury growth and described the company’s operating model as “virtually unmatched” during an earlier selloff. That statement represents his view, not an independent measure of performance. The company’s strategy combines large-scale Bitcoin mining with direct purchases. It keeps mined coins rather than selling them to cover routine costs, according to management.

Bitcoin charge weighs on first-quarter results

American Bitcoin reported a $118.2 million operating loss for the first quarter of 2026. The result included a $117.2 million non-cash charge tied to the lower market value of its Bitcoin holdings. The company reported an $81.8 million net loss and $62.1 million in mining revenue. Bitcoin fell about 22% during the quarter.

Management said the accounting charge masked stronger mining operations. Chief executive Mike Ho said the “underlying business was profitable” after excluding the mark-to-market adjustment, and said American Bitcoin did not sell any coins. The company mined 817 BTC during the quarter and cut its production cost per Bitcoin to $36,200, down from $46,900 in the prior quarter.

The balance sheet still links American Bitcoin stock closely to Bitcoin prices and mining economics. Lower Bitcoin prices reduce the market value of its reserve and can weaken revenue per mined coin. Higher power, equipment or hosting costs can also narrow margins. Hut 8 provides key infrastructure and remains central to the company’s mining setup.

American Bitcoin’s growing reserve gives shareholders Bitcoin exposure, but treasury growth has not supported its market price. The company must keep Nasdaq compliance while funding mining and purchases. Its next results will show whether lower production costs can offset Bitcoin prices and whether the 8,000-BTC reserve can support the business without pressure on shareholders.

While Washington’s attention fixes on whether the CLARITY Act can find seven Democratic votes before the August recess, the Securities and Exchange Commission has been quietly assembling the framework that governs American crypto if the bill dies, and much of it even if the bill passes.

Summary

- Regulation Crypto would create a four-year startup exemption for crypto projects raising up to 5 million dollars per year.

- A separate fundraising exemption would let more mature issuers raise up to 75 million dollars annually with lighter disclosure than full registration.

- The safe harbor would give tokens a defined path out of securities classification once issuer-led managerial efforts permanently end.

- The rule could operate alongside the CLARITY Act, but if the bill fails, it may become the main US crypto capital-formation framework.

- The biggest fights ahead are over dollar thresholds, decentralization standards, investor protections, and litigation risk.

On July 7, the agency confirmed plans to formally propose Regulation Crypto, its first major crypto-specific rulemaking under Chair Paul Atkins. The proposal, expected to run past 400 pages, sits under review at the White House Office of Information and Regulatory Affairs, the final gate before publication for public comment, and Atkins has said release is expected shortly after that review completes.

The package does three concrete things. It gives new crypto projects a startup exemption from full securities registration for up to four years while they build toward network maturity, raising up to 5 million dollars annually against whitepaper-style disclosures. It creates a fundraising exemption allowing more mature issuers to raise up to 75 million dollars in any 12-month period with audited financials and semiannual reporting, a burden far lighter than full registration. And it writes an investment contract safe harbor: a rules-based path for a token to exit securities classification entirely once its issuer has permanently ceased the essential managerial efforts that made it an investment contract in the first place.

Atkins has repeatedly described the framework as a bridge to the CLARITY Act. The description is honest and incomplete at the same time. A bridge implies something temporary that the statute replaces; in reality, Regulation Crypto answers questions the bill does not reach, will operate for years regardless of the Senate outcome, and, if the bill fails, becomes the entire de facto constitution of American crypto capital formation. This feature decodes what the rule actually does, where it came from, why Senate Democrats consider it an end-run, and what it means for the market that one of these two frameworks is arriving no matter what happens in the next three weeks.

The taxonomy underneath: five buckets instead of one question

Regulation Crypto did not appear from nothing. Its foundation is a joint SEC and Commodity Futures Trading Commission interpretive release from March 17, 2026, which replaced the enforcement era’s single endless question, is this token a security, with a working taxonomy of five categories: digital commodities, digital collectibles, digital tools, stablecoins, and digital securities. Under the interpretation, only digital securities, tokenized versions of traditional financial instruments, remain fully subject to the securities laws. The other categories may still trigger securities obligations if sold as part of an investment contract, which is where the Howey analysis survives, but the default presumption flipped: most tokens are not securities by nature, and the legal question becomes how they were sold, not what they are.

Atkins introduced the exemption framework the same day, in a speech at the DC Blockchain Summit titled Regulation Crypto Assets: A Token Safe Harbor, and the agency submitted the proposed rules to the White House within the week. The sequencing matters for understanding what kind of project this is. The interpretive release stated how the agency reads existing law; interpretations bind nobody and evaporate with the next chair. The proposed rule converts the reading into formal regulation, with notice, comment, and the full Administrative Procedure Act process, which makes it dramatically harder to unwind. The past year’s accommodations, staff guidance, no-action letters, dropped enforcement actions, carry no binding force at all; a future commission could reverse them by memo. A finalized Regulation Crypto could only be undone by a new rulemaking that survives its own comment period and litigation. Durability is the entire point, and durability is exactly what the industry has said it needs.

The chair’s broader agenda frames the rule as one panel of a triptych. Atkins has described crypto market structure, custody, and capital formation as the agency’s three crypto priorities, with the stated goal of making the United States the leading crypto capital. He has asked staff to evaluate letting non-security crypto assets that were sold under investment contracts trade on venues not registered with the Commission, to clear paths for state-licensed platforms to list such assets, and to let CFTC-regulated platforms offer them with margin. He also shut down the agency’s crypto innovation hub, arguing the Gensler-era version was so tainted that industry participants feared subpoenas after visiting, a symbolic demolition that tells its own story about how completely the agency’s posture has inverted.

The three exemptions, decoded

The startup exemption is the on-ramp. A new project receives up to four years of relief from full registration while it develops its network, during which it can raise up to 5 million dollars per year. The disclosure standard is principles-based and deliberately modeled on what serious projects already publish: whitepaper-style documentation of the technology, the token economics, and the team, plus required financial statements to investors. The four-year clock is the regulatory embodiment of an idea the industry has argued since 2018, that decentralization takes time, and that forcing registration at launch, when a network is inescapably centralized, guarantees either noncompliance or offshoring. The exemption’s wager is that a project given four lawful years will either mature into something the safe harbor releases or grow into something the fundraising tier can carry.

The fundraising exemption is the growth pathway, and its design is more conservative than the headline suggests. The 75 million dollar annual cap is borrowed directly from Regulation A+, the existing exemption for smaller public offerings by conventional issuers; Atkins adapted a tested framework instead of inventing one. The obligations scale accordingly: audited financial statements and ongoing semiannual reporting, meaningfully heavier than the startup tier’s whitepaper standard, meaningfully lighter than a full registration. For the mid-sized token issuer, the practical effect is a lawful domestic alternative to the offshore foundation structures that became the industry’s default architecture, with a compliance bill measured in hundreds of thousands of dollars instead of tens of millions.

The investment contract safe harbor is the philosophical core and the piece with no statutory parallel. It answers the question the Torres ruling in the Ripple case raised but could not settle: when does a token that was sold as a security stop being one? The safe harbor’s answer is a rule-based test keyed to managerial effort. Once an issuer has permanently ceased the essential managerial functions that investors relied on, the token exits securities classification, full stop. That converts decentralization from a rhetorical claim into a compliance milestone with legal consequences, and it gives every project in the startup tier a defined destination. It is also, not coincidentally, the provision that most directly generalizes the industry’s hardest-won litigation outcomes into standing law, the same conceptual territory Ripple spent 150 million dollars mapping, as the token-versus-sale distinction moved from courtroom argument to regulatory architecture.

The objection: an agency legislating around the legislature

Senate Democrats have noticed that the SEC is building, by rule, much of what Congress has not agreed to build by statute, and their objection deserves a full hearing because it is not frivolous.

Elizabeth Warren and Chris Van Hollen wrote to Atkins directly, charging that the agency plans to exempt most cryptocurrencies from the securities laws with significant potential harm to investors, and calling on Congress to close the loopholes as it considers market structure legislation. Financial industry commenters have warned that broad exemptive relief could import cybersecurity risks, illicit-finance exposure, and flash-crash volatility into markets stripped of their traditional guardrails. The constitutional-order version of the critique is sharper still: an agency whose chair previously advised crypto firms is using administrative discretion to deliver, in advance, the deregulatory half of a bill the elected branch has not passed, while the accountability provisions Democrats attached to that bill, the ethics rules aimed at the president’s 2.3 billion dollars in crypto exposure, have no administrative equivalent and can only exist in statute. Regulation Crypto, on this reading, is not a bridge to CLARITY. It is a mechanism for harvesting CLARITY’s benefits without paying CLARITY’s political price, and every week it advances reduces the industry’s urgency to compromise on the ethics language currently blocking the bill, a standoff crypto.news has followed into its decisive month.

The rebuttal has two layers. Legally, exemptive authority is not a loophole; Congress wrote it into the securities laws deliberately, and Regulation A+, Regulation D, and Regulation Crowdfunding are all products of the same power. An agency tailoring registration requirements to a novel asset class through notice-and-comment rulemaking is the administrative state working as designed, and the courts, not letters, will test whether this rule exceeds the statute. Practically, the alternative to Regulation Crypto is not the status quo Democrats prefer; it is the pre-2025 regime of regulation by enforcement that a federal judge partially repudiated and that nearly dissolved companies later vindicated. Between an imperfect rule with a comment period and an enforcement lottery with none, the rule is the more accountable instrument, whatever one thinks of its content.

What both sides quietly agree on is the stakes of reversibility. Democrats want the ethics and consumer provisions in statute because statutes bind future administrations; the industry wants the exemptions in a finalized rule for precisely the same reason. The entire fight, in Congress and at the agency simultaneously, is about who gets to make their preferences durable first.

How the agency got here: from Hinman speech to Howey off-ramp

The rule reads differently with a decade of institutional history attached, because every one of its provisions answers a specific wound.

The startup exemption answers the original sin of the ICO era. In 2017 and 2018, hundreds of projects raised capital from Americans with no disclosure standard at all, the agency responded with a wave of enforcement that treated every token sale as an unregistered offering, and the surviving industry drew the obvious lesson: incorporate in Zug, exclude Americans, and disclose nothing. The exemption’s whitepaper-based standard is a wager that a lawful middle existed all along, and that the agency’s refusal to build it, not the industry’s refusal to use it, drove a decade of capital formation offshore.

The safe harbor answers the Hinman problem. In 2018, a senior SEC official famously suggested in a speech that Ether, whatever its origins, had become sufficiently decentralized that its sales were no longer securities transactions. The industry spent years trying to hold the agency to that logic, the agency spent years insisting the speech was one man’s opinion, and the internal documents Coinbase later pried loose in litigation showed officials themselves could not agree on what the standard was. Commissioner Hester Peirce proposed a formal token safe harbor twice, in 2020 and 2021, and was ignored by her own agency both times. The current safe harbor is Peirce’s idea with Atkins’ signature, arriving seven years after the speech that made everyone realize the question had no answer.

And the fundraising tier answers the enforcement era’s quietest casualty: the mid-sized compliant issuer that never existed because there was no rule to comply with. Between the 5 million dollar seed rounds that Regulation D could awkwardly cover and the public listings that only exchanges and miners attempted, an entire capitalization band of the industry simply had no American on-ramp. Borrowing Regulation A+’s 75 million dollar ceiling is the agency conceding that the band was a regulatory artifact, not a market verdict.

The arc from Gensler to Atkins, from an agency that sued first and declined to write rules even under court order, to an agency proposing 400 pages of them, is the sharpest institutional reversal in modern financial regulation, and it happened without a single statute changing. That fact is the strongest argument for the rule and the strongest argument against relying on it, at the same time.

What can still change: the comment period is not a formality

Between OIRA clearance and a final rule stand months of process in which the package’s most important parameters remain genuinely contestable, and market participants pricing the framework as finished are early.

The dollar thresholds are the obvious pressure point. Consumer advocates and Senate Democrats will push the 75 million dollar ceiling down and load the startup tier with conditions; industry commenters will push for inflation indexing and aggregate-cap clarity, since the current design names annual limits without a publicly specified lifetime ceiling. The decentralization test inside the safe harbor is the subtle one. Permanently ceased essential managerial efforts is a phrase that will absorb tens of thousands of comment pages, because it decides whether the off-ramp is a real destination or a mirage: too strict, and no foundation-supported network ever qualifies; too loose, and every project theatrically dissolves its team on paper while running development through affiliates. The illicit-finance overlay is the political one. The same law enforcement coalition currently fighting the CLARITY Act’s developer protections, a split crypto.news dissected as the Senate vote approached, will demand that exempted issuers carry monitoring obligations the statute never imposed, and the agency’s answer will determine whether the exemptions are usable by actually decentralized projects or only by companies that look like broker-dealers with extra steps.

Litigation risk frames all of it. A finalized rule this consequential draws challenges from both flanks: investor-protection groups arguing the agency exceeded its exemptive authority by hollowing out registration, and, conceivably, industry plaintiffs attacking whatever conditions survive comment. Post-Chevron, courts owe the agency’s statutory reading no deference, and a single adverse circuit decision could stay the framework for years. This is the structural reason Atkins keeps calling the rule a bridge and pressing Congress to act anyway: he is building the most durable thing an agency can build while publicly acknowledging it is the second-most durable thing available.

Regulation Crypto versus the CLARITY Act: substitutes, complements, or race

Mapping the two frameworks against each other shows they overlap less than the political rhetoric implies, which is why the with-or-without framing in this feature’s title is literal.

The CLARITY Act’s center of gravity is market structure: which agency supervises trading, how exchanges and brokers register, how the CFTC gains spot authority over digital commodities, how developers escape money transmitter liability. Regulation Crypto’s center of gravity is capital formation: how tokens are launched, funded, and eventually released from securities status. The bill barely touches primary issuance mechanics; the rule barely touches secondary market supervision. A world with both is coherent: CLARITY sorts the assets and assigns the regulators, Regulation Crypto governs how new assets are born. Atkins’ bridge metaphor undersells his own product; the honest description is that the rule is the bill’s missing chapter, written by the agency because the legislature never drafted one.

The substitution effect appears only in the failure scenario, and there it is nearly total. If the Senate misses the August window and the 2030 warnings prove accurate, Regulation Crypto plus the March taxonomy plus the CFTC’s stretched existing authority become the entire American framework: token launches under the exemptions, classifications under the five buckets, trading under a patchwork the rule’s platform provisions try to rationalize. That regime would function, and its existence is precisely what Galaxy Research and others cite when they note that CLARITY’s failure would be a slow bleed rather than a catastrophe. But it would be a framework resting on one commission’s rulemaking, contestable in court, reversible by a hostile successor with patience, and silent on everything from illicit finance funding to the ethics questions that stalled the bill. The GENIUS Act fight already previewed what statute-versus-regulator arguments look like when real money is at stake, with state and federal authorities wrestling over stablecoin turf in a battle crypto.news covered throughout its Senate run, and the yield wars that followed passage show how much conflict survives even a signed law, a standoff crypto.news has tracked between banks and issuers over 6 trillion dollars in deposits.

There is also a timing race with the bill’s own politics. The rule’s OIRA review and comment period run on an administrative calendar indifferent to the Senate’s. If the merged CLARITY draft stalls on ethics while Regulation Crypto publishes for comment, the industry’s cost of legislative failure drops in real time, which weakens the coalition pressing moderate Democrats and strengthens the members arguing the bill can wait. Agency action meant as a bridge can function as an off-ramp. The three weeks in which both instruments reach their decisive stages, the merged bill text and the published rule, will reveal which metaphor the market believes.

What it means for issuers, and the European mirror

Before the issuer decision tree, the market implications deserve a paragraph of their own, because the rule reprices assets that already exist, not just launches that have not happened. Tokens whose largest discount is classification ambiguity, the mid-cap layer ones, the DeFi governance assets, the infrastructure tokens that trade below comparable revenue because American institutions cannot categorize them, gain a defined path to non-security status through the safe harbor even if the CLARITY Act never assigns them a commodity label. Exchange listing committees, which spent the enforcement era rationing US availability by litigation risk, get a compliance framework to point to. And the venture pipeline reopens domestically: funds that structured around offshore token warrants for a decade can underwrite American issuance with actual rules attached, which changes where the next cycle’s projects incorporate, hire, and pay taxes. None of this requires the rule to be generous. It requires the rule to exist, because the binding constraint was never severity. It was undefined risk, the one input no allocation committee can price.

For anyone actually launching a token, the practical decision tree changes shape the moment the rule publishes. A credible path now exists to raise seed capital domestically under the startup tier, scale through the 75 million dollar pathway with audit-grade disclosure, and target the safe harbor as the legal finish line where the token sheds its securities character by verifiable decentralization. The offshore foundation, the airdrop-to-avoid-sale contortions, and the deliberate exclusion of American buyers, the entire defensive architecture of the past eight years, become choices rather than necessities. The projects most affected are the serious middle: too big for a fair launch to fund, too small to carry registration costs, which describes most of the infrastructure layer the industry claims to want.

The comparison that will define the rule’s success is the one across the Atlantic. Europe’s MiCA regime just completed its transition, locking unlicensed firms out of a 30-country market and elevating the licensed few, a sorting crypto.news documented as the deadline hit. MiCA’s strength is comprehensiveness backed by statute; its weakness is rigidity, a stablecoin regime severe enough to expel the largest issuer on earth. Regulation Crypto inverts the trade: flexible, innovation-forward, and administratively fast, but resting on agency authority in a country where agencies change hands every four years. An American founder in 2026 chooses between a European rulebook that cannot easily be improved and an American one that cannot easily be trusted. The CLARITY Act is, among everything else, an attempt to give the American framework the one property it lacks, and the rule arriving with or without it is both the industry’s insurance policy and the bill’s quiet competitor.

The decode, compressed: Regulation Crypto is the most consequential piece of American crypto policy that almost nobody outside Washington is reading, precisely because it advances on the boring calendar of administrative law while the Senate supplies the drama. Four-year runways, 75 million dollar raises, and a legal exit from securities status are arriving through the Federal Register, on a timeline no filibuster can touch and no recess interrupts. The comment period will bend the parameters, the courts may test the boundaries, and a future commission could someday attempt the long unwind. What no plausible scenario now delivers is a return to the world where the only American rulebook was a lawsuit. The only question the Senate’s three weeks will answer is whether the new rulebook arrives as a chapter of a statute or as the whole book.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

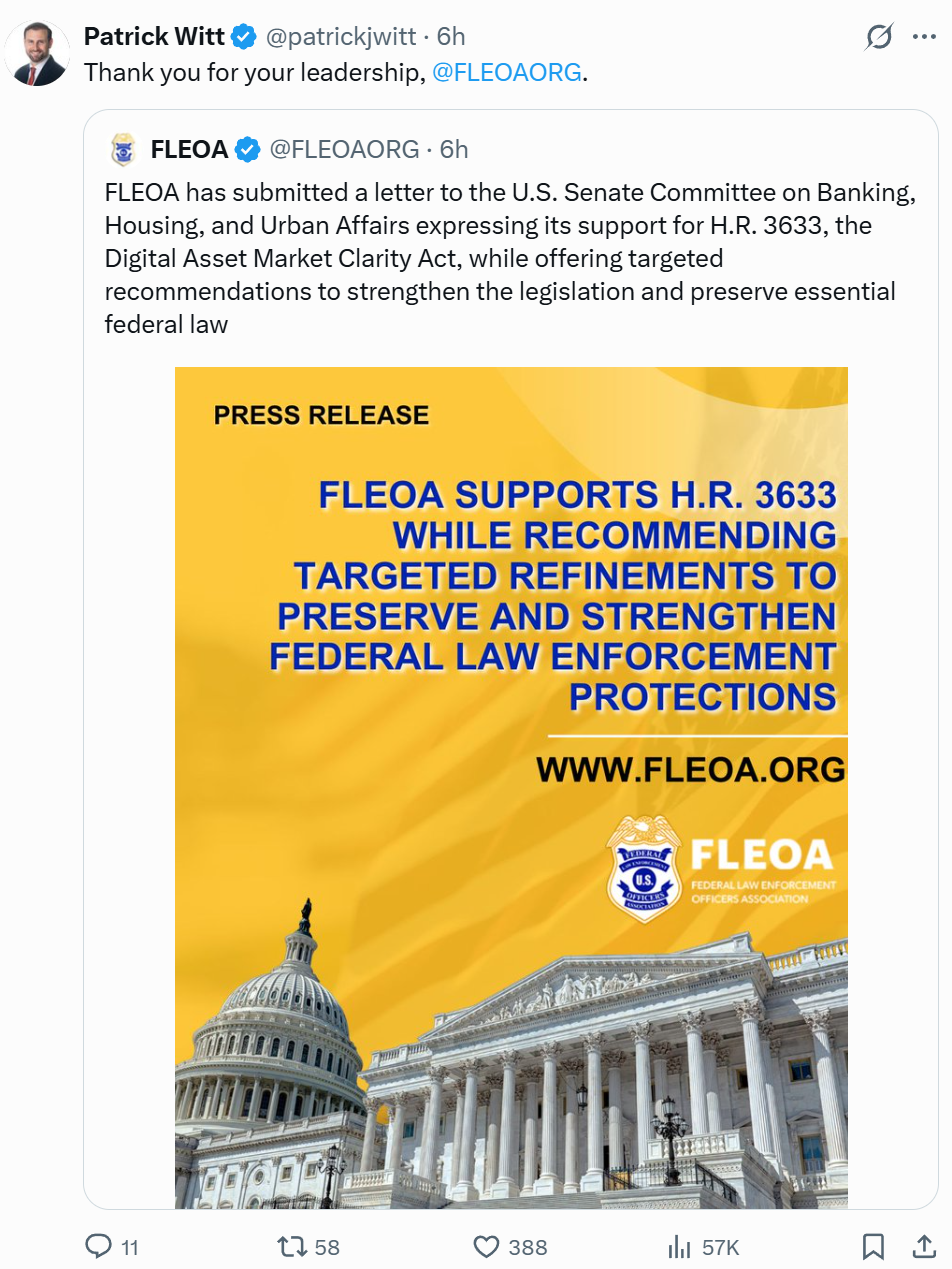

The Digital Asset Market Clarity Act has secured its second public endorsement from a major US law enforcement organization, coming just weeks before what many see as a make-or-break legislative deadline before the Senate’s August recess.

In a July 10 statement, the Federal Law Enforcement Officers Association (FLEOA) said it submitted a letter to the US Senate Banking Committee endorsing the CLARITY Act, while calling for changes to strengthen accountability in decentralized finance (DeFi) and preserve investigators’ existing powers.

“[FLEOA] expressing support for CLARITY and confirming what many of us know — this bill is strong on consumer protection and law enforcement,” said Ji Kim, CEO of the Crypto Council, in a statement Monday.

The endorsement came nine days after the bill was backed by the National Organization of Black Law Enforcement Executives (NOBLE), with both letters helping counter arguments that the CLARITY Act would weaken the government’s ability to police crypto crime.

Source: Patrick Witt

In its statement, the FLEOA said the current version of the CLARITY Act “represents meaningful progress toward balancing technological innovation with public safety.”

Related: Donald Trump invokes US senator’s death to push crypto bill

“FLEOA commends the Committee for its efforts to establish a clear regulatory framework for digital assets that promotes responsible innovation while preserving critical criminal, anti-money laundering, counterterrorism financing, sanctions enforcement, and investigative authorities.”

However, the FLEOA also urged lawmakers to narrow the CLARITY Act’s DeFi protections; make it clearer who is accountable in decentralized finance (DeFi) systems; stop firms from avoiding regulation by claiming to be decentralized; revise “specific intent” language to make it easier to establish liability and explicitly affirm that the legislation doesn’t limit existing federal investigative authority.

Law enforcement groups seek changes to CLARITY Act

In June, four law enforcement organizations reached out to the White House with concerns centered on Section 604 of the legislation, which seeks to protect developers from liability for illicit activity carried out by users on their decentralized platforms.

The organizations, including the National District Attorneys Association, the National Association of Assistant United States Attorneys, the International Association of Chiefs of Police and the National Sheriffs’ Association, argued it could create broad exemptions that would make it tougher for law enforcement to investigate crypto-related crimes.

The opposition prompted the White House to invite law enforcement organizations objecting to the language of the bill to a meeting in late June.

In July, the Major County Sheriffs of America shifted its stance on the CLARITY Act to neutral after initially opposing the bill.

CLARITY Act nears August deadline

The letter comes less than four weeks before the Aug. 8 Senate recess. Industry insiders have seen the recess as a critical milestone to see it passed this year.

“This is likely our last chance to get real legislation for digital assets on the books before 2030,” Senator Cynthia Lummis said on July 8.

“If we fail to pass the Clarity Act, we are ensuring another country will write the rules for digital assets and we spend the next decade catching up.”

Magazine: Robinhood L2 sparks ETH optimism, Saylor ‘muddies waters.’ Hodler’s Digest, July 5-12, 2026

Thailand has begun auditing high-value stablecoin transactions after authorities flagged suspicious transfers that may have bypassed normal financial reporting systems.

Summary

- Thailand has started auditing high value USDT transactions after identifying transfers that may have bypassed reporting rules.

- The Bank of Thailand and the SEC are using data analytics to investigate suspicious stablecoin activity and assess possible regulatory action.

- The review forms part of an ongoing crackdown on money laundering, online gambling, and other grey economy activities.

According to local news outlet Thansettakij, the Bank of Thailand (BOT) and the country’s Securities and Exchange Commission (SEC) have started examining unusual activity involving stablecoins as part of ongoing efforts to curb illicit finance and the shadow economy.

BOT Governor Vitai Ratanakorn said the authorities are using data analytics tools to review high-volume transactions, with particular attention on Tether’s USDT. Preliminary checks have already identified several transfers that appear to have been structured to avoid disclosure requirements or move funds outside conventional payment channels, the report said.

The central bank is now working with the SEC to assess the findings and determine what regulatory action, if any, should follow.

Alongside the stablecoin review, Thai authorities have tightened oversight of other financial activities linked to money laundering risks. The report said regulators are increasing scrutiny of large cash deposits and withdrawals, gold trading, and bank accounts connected to online gambling operations.

Speaking about the campaign, Ratanakorn said the measures are intended to work together over time rather than serve as temporary solutions.

The latest review follows several enforcement actions taken this year. Most recently, Thai police uncovered a crypto laundering network that moved proceeds from romance scams through multiple cryptocurrencies using cross-chain token swaps to make transactions harder to trace. Investigators said one suspect’s digital wallet handled more than $122.5 million over a 10-month period.

Thailand continues crypto policy updates

The enforcement drive comes as Thailand continues to refine its digital asset framework in other areas.

Earlier this year, the SEC opened a public consultation on proposals that would allow licensed digital asset companies to offer crypto derivatives without creating separate corporate entities. The regulator said the change would lower operational costs while keeping businesses under a single supervisory framework with conflict management and internal control requirements.

The consultation builds on amendments to Thailand’s Derivatives Act approved by the Cabinet in February, which recognised digital assets as eligible underlying instruments for futures contracts. The SEC has said those changes are intended to support regulated crypto investment products while maintaining regulatory oversight.

SBI Holdings and the Solana Foundation have formed a strategic partnership to develop an onchain financial market based in Japan.

Summary

- SBI and Solana target stablecoins, tokenized assets, payments and institutional services across Japan and Asia.

- Solana Foundation will join SBI R3 Japan, which plans to become SBI Solana Global soon.

- The venture aims to connect Japan’s regulated financial system with global blockchain liquidity and markets.

Under the agreement, the foundation will join SBI R3 Japan alongside SBI and Sumitomo Mitsui Financial Group, one of Japan’s major banking groups. The company plans to change its name to SBI Solana Global, subject to the required corporate process. The partners announced the arrangement on July 13.

The venture will use Solana as its main blockchain infrastructure. SBI said the project will connect Japan’s financial assets, regulated institutions and legal framework with international blockchain markets.

The group said it aims to make Japan “a core hub for onchain finance in Asia.” That remains a business target. The announcement did not provide revenue forecasts, launch volumes or client commitments. It also did not say whether the renamed company will end any existing Corda-related work.

Stablecoins and tokenized assets lead the plan

SBI Solana Global plans to support the issuance and distribution of yen stablecoins, including JPYSC. It will also work on tokenized corporate bonds, commercial paper, investment funds and real estate.

The company aims to provide one system for issuance, distribution and settlement rather than offering blockchain technology alone. This structure could allow issuers to manage an asset through its full onchain life cycle.

The partners also listed cross-border payments, institutional onchain services and payment systems for AI agents among their planned business areas. The statement did not give launch dates for each product. It also did not explain which services will require separate approval from Japanese regulators. Any live offering will need to follow local rules for stablecoins, securities, custody and financial market operations.

SBI expands its regulated digital asset network

The Solana deal adds to SBI’s wider digital asset program. As crypto.news reported, SBI and Startale developed a regulated yen stablecoin for payments, tokenized assets and onchain settlement. SBI also worked with Ripple to launch the dollar-backed RLUSD stablecoin in Japan through SBI VC Trade after regulatory approval.

SBI is also moving to acquire Bitbank, one of Japan’s established crypto exchanges. As previously reported, the planned ¥46.7 billion transaction would add trading, custody and lending services to SBI’s existing network. The Solana partnership creates another route for SBI to connect stablecoins and tokenized securities with institutional markets. However, the companies have not announced whether Bitbank or SBI VC Trade will distribute SBI Solana Global products.

Solana gains another institutional finance partner

The partnership arrives as tokenized asset activity grows on Solana. As previously reported, the network recorded $5.77 billion in tokenized-asset spot volume during a record quarter and processed more than one billion weekly non-vote transactions. Solana has also attracted stablecoin settlement, tokenized equities and institutional trading projects, though activity levels can change with market conditions.

SBI and the Solana Foundation said they want to extend Japan-originated products into Asian and global markets. A “Japan-originated digital financial asset market” is the stated direction, but the partners have not named overseas markets, banking partners or settlement corridors.

They also did not disclose the size of the Solana Foundation’s investment. Their next steps will center on the company rename, product development and regulatory work needed to move stablecoins, tokenized assets and payments into live use.

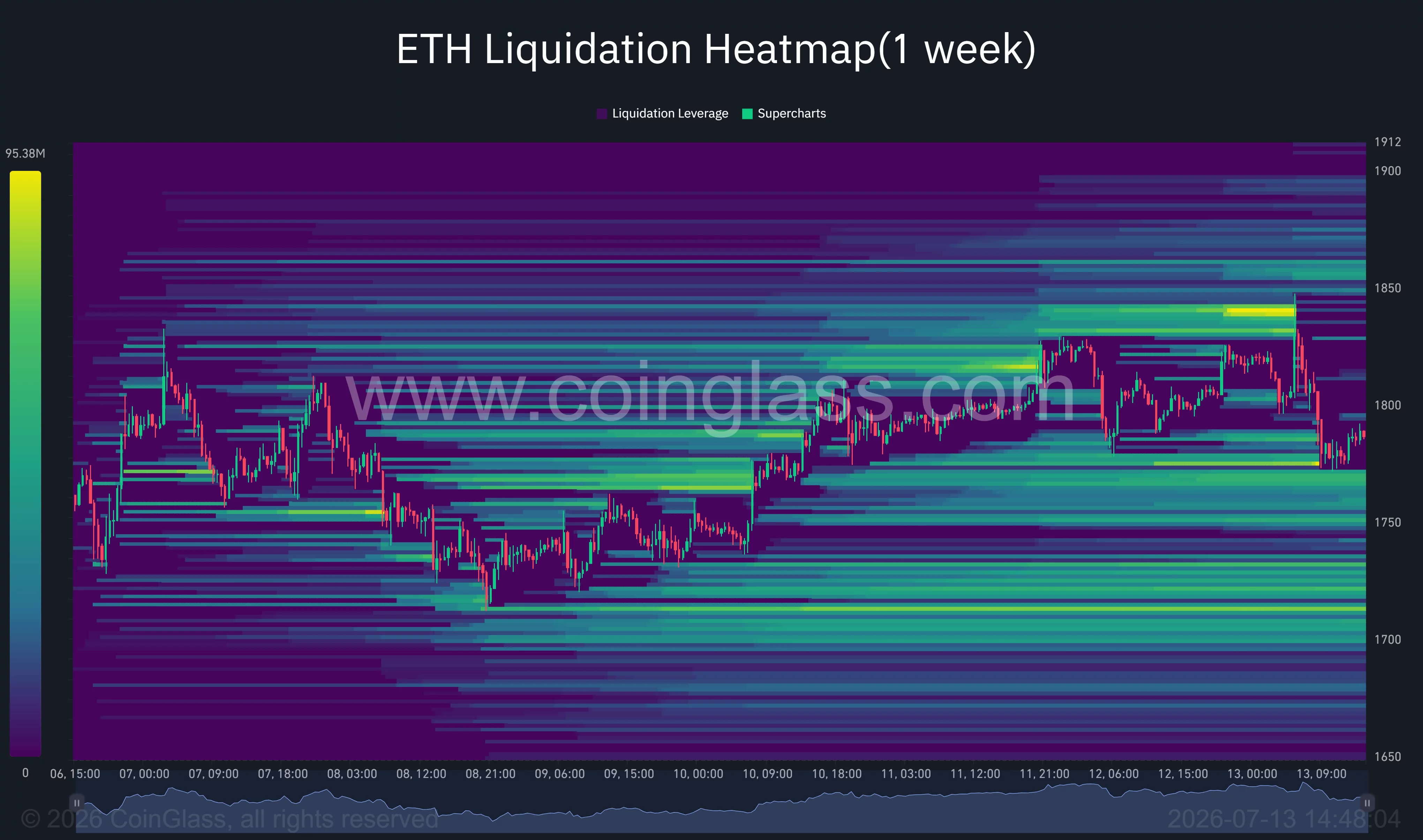

Ethereum has slipped below the key $1,800 level after renewed U.S.-Iran military escalation pushed oil prices higher and sent investors out of risk assets, although buyers continue to defend support near $1,750.

Summary

- Ethereum fell below $1,800 after renewed U.S.-Iran strikes pushed oil above $74 and sparked a risk-off move.

- Charts still support a possible rally toward $2,140 if ETH breaks resistance near $1,825-$1,850.

- Holding $1,750 remains critical, while a breakdown could expose support near $1,700 and $1,505.

According to data from crypto.news, Ethereum (ETH) price traded around $1,775 during Monday’s session, down roughly 3.6% from its daily high of $1,837 after fresh U.S. strikes on Iran reignited fears of a prolonged Middle East conflict.

Crude oil jumped about 4% to above $74 a barrel as Washington and Tehran exchanged missile strikes while tensions around the Strait of Hormuz intensified. The renewed geopolitical risk revived concerns that higher energy prices could keep inflation elevated, prompting traders to reduce exposure to cryptocurrencies alongside other high-beta assets.

Iran later claimed it had targeted U.S. military sites in Bahrain, Kuwait, Oman and Jordan in retaliation for American bombardment, while conflicting statements over whether the Strait of Hormuz remains open added another layer of uncertainty for financial markets.

The stronger U.S. dollar and renewed demand for defensive assets have added pressure across digital assets as investors await further geopolitical developments.

Ethereum continues to defend $1,750 despite losing key moving averages

Ethereum’s technical structure has weakened after its price fell below its 20-day moving average near $1,800 on the 4-hour chart. The decline also dragged ETH beneath the psychological $1,800 level that had acted as support throughout last week. Still, the asset continues to trade above its 50-day and 100-day moving averages around $1,779 and $1,709, respectively, preserving the medium-term recovery that began in early July.

The daily chart still shows a potential double-bottom formation with lows near $1,505. A confirmed breakout above resistance around $1,825 would complete that pattern and project an upside target near $2,140.

Momentum has yet to fully confirm the move, however. The MACD remains above its signal line despite a narrowing histogram, while Chaikin Money Flow stays in positive territory around 0.10, suggesting capital has not completely exited the market.

The Aroon indicator on the 4-hour timeframe also continues to favor buyers, with Aroon Up near 92.9 and Aroon Down around 85.7. Although both readings remain elevated because of recent volatility, the higher Aroon Up reading suggests bulls still retain a slight advantage if Ethereum reclaims the $1,800-$1,825 resistance zone.

Derivatives positioning presents another important technical level. CoinGlass liquidation data shows one of the largest short liquidation clusters sits between roughly $1,840 and $1,860.

A decisive move through that area could force leveraged short sellers to close positions, potentially accelerating a rally toward $1,900. Larger liquidity pockets remain above $1,900, while notable bid-side liquidity extends toward the $1,700 region.

Commenting on the setup, crypto analyst Ali Martinez wrote, “I’m going LONG on Ethereum $ETH if it breaks $1,850.” His view aligns with the heavy liquidation cluster immediately above current prices, where a breakout could trigger additional buying from short covering.

Failure to hold support could revive the bearish trend

Not every analyst expects an immediate breakout. Analyst Ted Pillows noted in a July 13 X post:

“ETH is still holding above the $1,750 support zone. This is a good sign and shows that sellers are no longer dominating here. As long as Ethereum holds above $1,750, I think a rally towards $2,000 could happen.”

That support now represents the primary invalidation level for the current recovery. A sustained break below $1,750 would place the 100-day moving average near $1,709 back into focus before exposing the June support zone around $1,505, where the double-bottom structure would fail.

Macro risks continue to dominate the outlook. Further escalation between the U.S. and Iran, additional disruption around the Strait of Hormuz, or another surge in crude oil prices could strengthen inflation expectations and reinforce the Federal Reserve’s higher-for-longer interest rate outlook. Under those conditions, cryptocurrencies could remain under pressure even if Ethereum’s longer-term technical structure stays intact.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Interpol says a crypto wallet linked to a suspected romance-scam launderer moved more than $122.5 million over a 10-month period, according to the agency. Thai authorities arrested two suspects and uncovered a money-laundering network that routed scam proceeds into cryptocurrencies, using cross-chain token swaps to blur transaction trails.

The findings were presented as part of Operation First Light 2026, an Interpol-coordinated campaign aimed at social engineering fraud and the financial systems used to process illegal gains. Interpol said the operation involved authorities across 97 countries and territories, leading to 5,811 arrests and the seizure of $293 million in illicit assets tied to fraud and money laundering.

Key takeaways

- Interpol attributes $122.5M in crypto flows in a single wallet to suspected romance-scam laundering, with cross-chain swaps used to obscure movement.

- Operation First Light 2026 spanned 97 jurisdictions and resulted in 5,811 arrests and $293M seized.

- Multiple Japan-focused developments point to growing use cases for stablecoins and tokenized credit, from exchange-linked products to retailer pilots.

- Hong Kong’s regulator introduced new phishing-resistant authentication requirements for crypto platforms, with implementation expected within 12 months.

- Binance’s Europe license problems have not closed the door elsewhere, with its co-CEO saying regulators have invited it to pursue new licensing after a MiCA setback.

Interpol targets romance-scam proceeds routed through crypto

Romance scams—often described as “pig-butchering” schemes—typically work by building trust with victims through social media or dating platforms before pushing them toward fraudulent investment opportunities. Interpol says the Thai-linked investigation uncovered how perpetrators converted scam proceeds into cryptocurrencies and then used cross-chain token swaps to complicate tracing.

Interpol’s message for investigators and market participants is that even when transactions pass through multiple networks, laundering activity can still concentrate around identifiable wallets and patterns. The agency’s broader campaign framing matters: Operation First Light 2026 focused not only on scam infrastructure, but on the financial plumbing behind it.

Interpol also reported that the operation resulted in large-scale enforcement outcomes beyond the single wallet case, citing seizures of $293 million in illicit assets and arrests across 97 participating jurisdictions. For crypto users, the operational takeaway is straightforward: laundering risk is not limited to a single chain or token, and actors can combine swaps and movement across ecosystems to evade detection.

Stablecoin rails get tested in real commerce and treasury workflows

Across Asia, stablecoin use is moving from pilots and corporate experiments toward more structured payment and settlement testing—though the compliance and operational design choices remain just as important as the underlying speed improvements.

One notable corporate example came from Hyundai Motor. Cointelegraph reported that Hyundai’s US and Mexican units completed a cross-border treasury transfer pilot using Tether’s USDT, settling a $20,000 payment in about seven minutes on the Avalanche blockchain. The reported workflow had Hyundai Motor America convert funds into USDT, transfer the stablecoin to Hyundai Motor Mexico, and then convert back to dollars. Cointelegraph noted the same process took roughly three to four hours or more with traditional bank transfers.

Tether said the pilot used Axiym’s settlement infrastructure, while Hyundai Card handled the remittance structure and managed regulatory, compliance, accounting, and operational requirements for the proof of concept.

Japan’s retail payments also saw another concrete test. Lawson is planning a yen-denominated stablecoin payments trial at a Tokyo location in August, according to Cointelegraph. HashPort said it has signed an agreement to conduct the pilot at a Lawson store, with participants using HashPort’s non-custodial wallet while the merchant side processes payments through HashPort’s point-of-sale system—avoiding the need for retailers to handle crypto wallet operations directly.

For investors and builders, these setups highlight a pattern: stablecoin adoption is increasingly about integrating token rails into existing workflows rather than asking merchants to run crypto-specific infrastructure.

Japan expands regulated crypto lending and studies Bitcoin-backed credit

Several Japan-focused announcements underscored ongoing efforts to broaden the regulated crypto-adjacent finance market, particularly around yen- and Bitcoin-linked products.

Cointelegraph reported that SBI VC Trade will accept applications for a yen-denominated stablecoin lending service offering an initial annualized rate of 3% on JPYSC lent for 12 weeks. The company said customers will lend JPYSC to SBI Holdings’ subsidiary and receive tokens back at maturity with a lending fee. Cointelegraph further stated that, at the advertised rate, the gross return over the 12-week term would be about 0.69% before tax. SBI also said the product is not a bank deposit, not covered by deposit insurance, and generally not cancelable early.

Another regulated financing expansion came from CRYL, which launched Bitcoin-backed loans of up to 1 billion yen (about $6.2 million), enabling borrowers to obtain fiat without selling BTC. Cointelegraph reported that borrowers can access amounts between roughly $6,200 and $6.2 million, at annual rates of 3.5% to 7%, with reported collateral ratios of 40% to 60%. The loans run for one year and can be used for items including taxes, business funding, and property purchases.

At the same time, Metaplanet said it is exploring Bitcoin-backed digital credit with JPYC and tokenization infrastructure provider Progmat. According to Cointelegraph, the study will examine whether Bitcoin can serve as collateral or credit enhancement for digital corporate bonds and other credit instruments, including 24/7 accessibility, settlement, and daily interest accrual for holders issued on a blockchain ledger. Cointelegraph noted that no product has been launched yet as part of the experiment.

Taken together, these developments show Japan’s approach bifurcating: some products are moving into customer-facing offerings (such as stablecoin lending and BTC-collateral loans), while other efforts remain in exploratory stages focused on tokenized bond or credit structures.

Regulators raise compliance pressure on authentication and stablecoin issuance

Regulatory actions in Asia continued to emphasize operational risk reduction and institutional control mechanisms.

The Hong Kong Securities and Futures Commission (SFC) issued new requirements for phishing-resistant authentication methods for virtual asset trading platforms and online brokers. Cointelegraph reported that the standards require stronger phishing-resistant authentication and device binding, while prohibiting the use of one-time passwords through SMS, email, or app-based logins. Platforms have 12 months to implement the changes.

Separately, Cointelegraph reported that the Bank of Korea remains firm that won-denominated stablecoins should be issued through bank-led consortiums. Local reporting cited by Cointelegraph said the central bank also called for safeguards, including a statutory policy body involving relevant agencies to oversee the sector. This reinforces the broader backdrop of policy debates in South Korea, where the bank’s stance has been described as dividing policymakers and contributing to delays in the country’s digital asset bill.

Binance eyes new licenses after EU approval setbacks

On the international regulatory front, Cointelegraph reported that Binance co-CEO Richard Teng said some regulators have invited the exchange to apply for new crypto licenses after the company failed to secure permission to operate in Europe under the EU’s MiCA licensing framework.

Cointelegraph noted that Teng characterized the discussions as “premature” and did not name the jurisdictions. Binance had previously withdrawn its application for a MiCA license in Greece following reports that Greek regulators were preparing to reject it. Teng said the situation took Binance by surprise, adding that withdrawing the application was intended to avoid a very short transition period for users if approval remained delayed.

For exchanges and market participants, this is a reminder that regulatory outcomes can diverge sharply by jurisdiction even when the underlying licensing narrative is unified—MiCA may standardize the framework in the EU, but access still depends on local decisions and timelines.

Looking ahead, investors should watch whether Interpol’s enforcement message translates into tighter monitoring expectations from compliance teams globally, and whether Japan’s stablecoin and crypto-backed lending experiments move from pilot and research phases into scalable, widely adopted products—while Hong Kong’s authentication rules and Korea’s bank-led stablecoin stance continue shaping what “safe” adoption looks like.

Interpol operation exposes $122M crypto wallet tied to romance scam laundering

A crypto wallet linked to a suspected romance-scam money launderer processed more than $122.5 million in 10 months, according to Interpol.

Interpol said that Thai authorities arrested two suspects and uncovered a money-laundering network that funneled proceeds from romance scams into cryptocurrencies, using cross-chain token swaps to obscure the trail.

The investigation was part of Operation First Light 2026, an Interpol-coordinated campaign targeting social engineering scams and the financial infrastructure used to launder their proceeds.

The operation involved authorities in 97 countries and territories, resulting in 5,811 arrests and the seizure of $293 million in illicit assets tied to fraud and money laundering.

Romance scams, also known as pig-butchering scams, often involve criminals building trust with victims through social media or online dating platforms before steering them toward fraudulent investment schemes.

Authorities carried out raids on scam centers. Source: Interpol

Hyundai completes USDT treasury settlement pilot between US and Mexico

Hyundai Motor’s US and Mexican units completed a pilot cross-border treasury transfer using Tether’s USDT stablecoin, settling a $20,000 payment in about seven minutes on the Avalanche blockchain.

Hyundai Motor America converted the funds into USDT, transferred the stablecoin to Hyundai Motor Mexico and converted it back into US dollars. The transfer and verification process took about seven minutes, compared with three to four hours or more for a traditional cross-border bank transfer.

Tether said the pilot used Axiym’s settlement infrastructure, while Hyundai Card designed the remittance structure and oversaw the regulatory, compliance, accounting and operational requirements needed to support the proof of concept.

Japan’s SBI to launch yen stablecoin lending with 3% yield

Tokyo-based SBI VC Trade will begin accepting applications Thursday for a Japanese yen-denominated stablecoin lending service offering an initial annualized rate of 3% on JPYSC lent for 12 weeks.

Customers will lend JPYSC to the SBI Holdings subsidiary from Thursday and receive the tokens back with a lending fee at maturity, the company said in a Monday press release. At the advertised rate, the gross return over the 12-week term would be about 0.69%, before tax.

The company said the product pays more than the 0.325% to 1% annual rate SBI cited for ordinary yen deposits. Still, it is not a bank deposit, is not covered by deposit insurance and generally cannot be canceled early.

Japanese lender launches Bitcoin-backed loans of up to $6.2M

Japanese lender CRYL has launched Bitcoin-backed loans of up to 1 billion yen ($6.2 million), allowing individuals and businesses to raise fiat currency without selling their BTC.

On Thursday, the company announced that borrowers can access between $6,200 and $6.2 million at annual rates of 3.5% to 7%. The loans carry collateral ratios of 40% to 60%. They run for one year and can be used for expenses, including taxes, business funding and property purchases.

The launch expands Japan’s small market for regulated crypto-backed financing. In 2020, Fintertech, a Daiwa Securities Group and Credit Saison joint venture, launched a similar service and currently lends up to $3 million against Bitcoin or Ether. However, CRYL’s service advertises a higher ceiling and a lower minimum, while limiting collateral to BTC.

Metaplanet explores Bitcoin-backed digital credit with JPYC in Japan

Japanese Bitcoin treasury company Metaplanet has teamed up with stablecoin issuer JPYC and tokenization infrastructure provider Progmat to study Bitcoin-backed digital credit products in Japan.

The investigation will examine whether Bitcoin can be used as collateral or credit enhancement for digital corporate bonds and other credit instruments, with 24/7 accessibility, settlement and daily interest accrual for holders, issued on the blockchain ledger. No product has been launched yet as part of the experiment.

The news suggests Metaplanet is looking beyond its role as a Bitcoin treasury company and testing how Bitcoin could be used as a productive balance sheet asset.

Digital credit instruments have been an important part of Strategy’s playbook. The world’s largest corporate Bitcoin holder has relied on “digital credit” instruments such as the STRC preferred stock as a primary vehicle for raising capital to acquire more Bitcoin.

Joint Study in the Digital Credit Domain Utilizing Bitcoin, JPYC, and Security Tokens. Source: Metaplanet

Japan stablecoin payments advance with Lawson trial, Netstars launch

Japanese convenience-store operator Lawson plans to test yen-denominated stablecoin payments at a Tokyo location in August, examining whether stablecoin payments can work inside a standard convenience store checkout flow.

On Monday, blockchain company HashPort said it had signed an agreement to conduct the trial at the Lawson Takanawa Gateway City store. Participants will use HashPort’s non-custodial wallet, while the store will process payments through the company’s point-of-sale system without needing to open or manage crypto wallets.

The pilot aims to explore how stablecoin payments can be integrated into Japan’s existing retail infrastructure while shielding merchants from much of the operational complexity associated with accepting digital assets.

Bitdeer stock jumps 14% as company expands US mining hardware production

Bitdeer shares rallied after the company announced a $36 million Nevada manufacturing facility that will produce its SEALMINER Bitcoin mining machines and expand its hardware business.

The gains for the Singapore-based miner followed Bitdeer’s announcement that it will build a manufacturing facility in Sparks, Nevada. It will produce key mining hardware components, with commercial production expected to begin by the end of the year.

Bitdeer Technologies Group (BTDR) stock. Source: Yahoo Finance

Hong Kong regulator orders new anti-phishing measures for crypto platforms

The Hong Kong Securities and Futures Commission (SFC) on Thursday issued new requirements for phishing-resistant authentication methods for virtual asset trading platforms (VATPs) and online brokers in the special administrative region.

The new standards require stronger phishing-resistant authentication methods and device binding while prohibiting the use of one-time passwords through SMS, email or app-based logins. Platforms must implement the changes within the next 12 months.

Bank of Korea stands firm on bank-led stablecoin push as deposit token pilots advance

The Bank of Korea (BOK) has doubled down on its stance that won-denominated stablecoins should first be issued through bank-led consortiums.

According to local reports from Digital Asset and EDaily, the BOK also called for new safeguards including a statutory policy body involving relevant agencies to oversee the sector.

The latest comments reinforce the BOK’s months-long push to keep won stablecoin issuance under bank-led structures. The central bank’s stance has divided policymakers and industry groups and contributed to delays in South Korea’s digital asset bill.

Regulators invited Binance to seek new licenses after MiCA setback, co-CEO says

Binance co-CEO Richard Teng says some regulators have invited the exchange to apply for crypto licenses after it failed to secure permission to operate in Europe.

Teng said the discussions are still “premature” and declined to identify the jurisdictions.

MiCA created a single licensing framework for crypto firms across the European Union, with non licensed firms unable to operate in the block after July 1. Binance withdrew its application for a MiCA license in Greece on June 24, after report that Greek regulators were planning on knocking it back.

“It caught us by surprise because we submitted a fully compliant application. The regulators told us as much,” Teng said.

“We are not quite sure why the approval kept being delayed. We withdrew the application because otherwise our users would have faced a very short transition period,” he added.

Richard Teng. Source: Binance

Asia crypto news in brief

Temasek says no to crypto

Singapore sovereign wealth fund Temasek is still smarting from having to write down $275 million on its FTX investment. Its Global Investment Head said this week that crypto remains “off the table” for now, though it’s still keeping an eye on developments in the blockchain sector.

HSBC’s blockchain note

HSBC and Marketnode teamed up to complete the private placement of a “digitally native” USD denominated note issued on blockchain in Hong Kong.

Japan’s crypto ETFs and credit

The Japanese government remains on track to launch crypto ETFs in the country, following recent legislative amendments to the Financial Instruments and Exchanges Act

SBI Solana Global

Japanese asset manager SBI Holdings has teamed up with the Solana Foundation to launch a new division called SBI Solana Global, focused on stablecoins, international payments and RWAs.

India crypto ban looms

The Reserve Bank of India said it is “leaning” towards a total prohibition on crypto and has recommended that legislators prevent banks and financial institutions from getting involved in the sector.

Thailand stablecoin audits

The Bank of Thailand and the Thai SEC are using blockchain analytics tools to investigate suspicious high-volume stablecoin transactions, with a particular focus on USDT.

On July 12, Uniswap founder Hayden Adams posted a number that would have sounded like satire during the governance-token winter: the protocol is generating 5.2 million dollars in daily fees, more than any protocol in crypto other than the two giant stablecoins, and far more than the perpetuals and memecoin venues that dominated the fee leaderboard for the past two years.

Summary

- Uniswap is generating more than 5 million dollars in daily fees, driven largely by Robinhood Chain activity.

- Robinhood Chain recorded 500 million dollars in daily Uniswap volume within eight days of launch.

- The UNIfication program burns UNI against protocol fees, turning fee capture into supply reduction.

- The key question is whether Robinhood Chain volume remains durable after gas subsidies expire.

- UNI’s repricing depends on fee-switch votes passing, sustained volume, visible burns, and regulatory stability around tokenized equities.

DefiLlama’s independent count for the same 24 hours, 5.16 million dollars, backs him up. The source of the surge is the least crypto-native venue imaginable: Robinhood Chain, the brokerage’s new Ethereum layer 2, supplied roughly 4.38 million dollars of that daily total, dwarfing Ethereum mainnet at 296,000 dollars and Base at 288,000.

The volume statistics behind those fees arrived at a pace no layer 2 debut has matched. Within eight days of the July 1 launch, Robinhood Chain recorded 500 million dollars in daily Uniswap trading volume, a tenfold jump from the day before, making it the second largest network for Uniswap activity after Ethereum mainnet. Cumulative swap volume crossed 1 billion dollars by July 10. Across the first seven days, the chain generated 10.98 million of Uniswap’s 20.1 million dollars in total weekly fees. Daily active Uniswap traders surged to roughly 220,000, more than ten times the prior week. Adams described the network as the most active blockchain layer outside Ethereum mainnet itself.

And this is the part that turns a volume story into an investment thesis: for the first time in the protocol’s history, that fee firehose is being plumbed directly into the token. The UNIfication program, passed by the DAO in December 2025 with 125.34 million UNI in favor and a rounding error against, burns UNI against protocol fees on 11 chains. A snapshot vote that ran from July 7 to July 12 asked holders to extend the mechanism to v4 pools, with binding on-chain votes following the week of July 13. A parallel temperature check, running July 10 through 15, proposes switching on protocol fees for the Robinhood Chain deployment itself. If both pass, the loudest new fee source in DeFi connects to a supply-destruction machine, and UNI completes a conversion that the entire sector is attempting: from governance token to cash flow asset.

This feature examines the machine, the money, and the two serious objections, that the volume is subsidized and that the fee switch drives away the liquidity it taxes.

From governance token to burn machine: how UNIfication works

For five years, UNI was the emblem of a category problem. The token governed a protocol that processed trillions in cumulative volume and captured none of it; every basis point of swap fees flowed to liquidity providers, and UNI’s value proposition reduced to voting rights over a treasury and the perpetual promise of a fee switch that governance never dared flip. The token traded at 3.23 dollars on July 7 against a 2021 peak of 44.97, a 93 percent drawdown that priced the promise at roughly nothing.

UNIfication changed the architecture. Under the system live since December, protocol fees collected on each chain flow into contracts called TokenJar. Anyone who wants to claim the accumulated assets, in practice arbitrage searchers, must first burn an equivalent value of UNI. The burned tokens are bridged back to Ethereum and sent to the dead address, permanently removing them from supply. The design is deliberately mechanical: no dividends, no staking claims, no legal distribution to holders that might attract securities analysis, just a standing market operation that converts fee revenue into supply reduction at whatever pace trading activity dictates. The program already runs on 11 networks: Ethereum, Arbitrum, Base, Celo, OP Mainnet, Soneium, X Layer, Worldchain, Zora, BNB Chain, and Polygon.

The July votes address the two gaps in coverage, and the v4 gap is the technically interesting one. Uniswap v2 and v3 pools carry fixed fee tiers, so collecting a protocol share is a matter of setting one rate per pool. v4 is built around hooks, smart contract plugins that let developers customize pool behavior, including fees that can change block by block. Taxing something that mutable required new machinery: the proposal introduces a V4FeePolicy contract that determines the protocol fee for any pool and a V4FeeAdapter that collects and routes it into the burn pipeline. More than 1,500 builders are working with v4 hooks, and institutional-scale flow has already arrived, with Spark, the liquidity arm of Sky, pushing 1.5 billion dollars in stablecoin volume through v4 in the past month. The Robinhood Chain temperature check would extend fees across the v2, v3, and v4 deployments there, using the expedited governance track that UNIfication authorized for fee-parameter updates.

The market has started doing the arithmetic. UNI rallied about 21 percent from its July 1 low of 2.70 dollars to 3.30 by July 8, touched moves of 14 percent on the volume headlines, and trades near 3.63 with resistance mapped at 3.73. A 2 billion dollar market capitalization against a protocol annualizing north of 1.8 billion dollars in gross fees, if the July run rate held, is the kind of ratio that makes traditional investors reach for spreadsheets, with the enormous caveat that only the protocol’s share of fees, not the LP share, feeds the burn: in the measured 24 hours, protocol earnings were about 73,454 dollars against the 5.2 million gross, because the switch is not yet flipped on the newest and largest sources.

The distribution deal of the cycle

The reason the fee conversation suddenly matters is distribution, and the scale of what Robinhood connected deserves to be stated plainly.

Robinhood operates between 24 and 28 million funded accounts and posted record first-quarter revenue of 1.07 billion dollars. Its chain, built on Arbitrum’s stack with 100-millisecond blocks and full EVM compatibility, shipped with Uniswap v2, v3, v4, and UniswapX deployed from day one as the default liquidity layer. The flagship product is Stock Tokens: tokenized versions of more than 90 US equities and ETFs, tradable around the clock by eligible retail users in more than 120 countries, with Chainlink as the oracle layer, 1inch for routing, BitGo for custody, and Morpho powering a yield product on the USDG stablecoin. A trader in Manila can buy tokenized Nvidia exposure at 2 a.m. through Uniswap liquidity and settle instantly, no T+1, no market hours. Developers deployed more than 13,900 smart contracts in the first week. Ethena moved 50 million dollars into a Morpho vault in a single transaction, driving total value locked above 106 million dollars, up 159 percent in a day. Even the memecoin economy arrived on schedule, with Pump.fun integration and chain-native tokens amplifying volume, as crypto.news reported when the network crossed the 500 million dollar mark.

Standard Chartered’s head of digital asset research, Geoff Kendrick, argued the market was underpricing the partnership, calling it a real strategic alliance rather than a listing announcement. The structural point underneath his claim: DeFi protocols have spent years competing for the same recycled on-chain capital, and Robinhood represents something the sector has never had, a mainstream brokerage routing its retail flow through a decentralized venue by default. For Uniswap specifically, it means the protocol’s addressable market expanded overnight from crypto natives to anyone with a Robinhood account and a tokenized equity order, and the fee data shows the expansion is not theoretical. One venue, eleven days old, is out-earning Ethereum mainnet fifteenfold.

The rotation context makes the timing sharper. In a market where everything outside Bitcoin and Ethereum lost roughly 23 percent in six months, capital has crowded toward the handful of assets with verifiable revenue: perpetuals venues, stablecoin issuers, and now, abruptly, the largest DEX. The same repricing logic runs through the stablecoin wars, where volume quality has become the scoreboard, a shift crypto.news examined in the USDC-Tether flippening, and through Ethereum itself, which is rebuilding its entire execution roadmap around being credible settlement infrastructure for exactly this kind of institutional flow, the project crypto.news detailed in the Lean rebuild. UNI’s real revenue moment is one instance of a sector-wide migration from narrative to cash flow.

The comparables: what a fee-earning DEX token is worth

The rotation to cash flow gives UNI a peer group for the first time, and the comparisons cut in both directions.

The flattering comparison is to the fee leaders UNI just passed. Hyperliquid, Pump.fun, and the perpetuals venues built the template of the past two years: tokens with direct revenue linkage, aggressive buyback or burn mechanics, and valuations that survived the altcoin drawdown better than the governance-token cohort precisely because holders could point at income. Adams’ framing, more daily fees than anything except USDC and USDT, deliberately places Uniswap atop that leaderboard. On raw multiples, a 2 billion dollar capitalization against 20.1 million dollars in weekly gross fees puts the protocol at roughly two times annualized gross fees, a figure that looks absurd against any traditional exchange until the LP share is subtracted, at which point the multiple on actual protocol take becomes very large and entirely dependent on the pending votes. The valuation case is therefore not that UNI is cheap on current protocol revenue. It is that governance controls a dial connected to a gross fee stream of unprecedented size, and the July votes are the market’s first chance to watch the dial turn on the newest and largest sources.