Crypto World

Bybit CEO says firms need MiFID, EMI licenses for European profit

Snagging a Markets in Crypto Assets (MiCA) license to operate in Europe is great, but, alone, it won’t be enough to turn a profit, according to Ben Zhou, the CEO of Bybit, one of the largest cryptocurrency trading platforms.

MiCA doesn’t cover the full range of products, such as derivatives and tokenized assets, needed to be profitable, Zhou said in an interview. For those, companies also need a MiFID II (Markets in Financial Instruments Directive) license and an Electronic Money Institution (EMI) license.

“With the current MiCA framework, you can only do fiat-to-crypto, crypto-to-crypto,” Zhou said. “There are many elements of a profitable business you cannot do, so even as a MiCA holder — unless you’re Kraken or BItpanda or Bitvivo, who are already making money because they have multiple licenses.”

Even Bybit, the world’s second-largest cryptocurrency exchange by trading volume, is some way off from breaking even in Europe, Zhou said. That timeline depends on when the firm acquires the other licenses it needs.

“We don’t make money under the current MiCA license. But we’re able to afford it because we’re a big entity. For us, it’s a long-term investment,” Zhou said. “It could be five years away, but I think that is a bit long. I would assume we are probably going to be profitable within two years.”

Market consolidation is coming

A MiCA license issued by one country allows a crypto-asset service provider to operate across the European Economic Area (EEA): all 27 members of the European Union, as well as Norway, Iceland and Liechtenstein.

Now is a critical juncture for many small to medium-sized crypto companies in Europe, because the MiCA grandfathering period closes at the end of June. That means firms must have obtained MiCA authorization to operate across the region by July 1 — a cut-off point that is widely expected to be the death knell for many smaller crypto firms.

“There’s going to be market consolidation,” Zhou said. “That’s why these guys are shutting down. Because even if they know they could afford MiCA, they’re like, ‘WTF, I need [MiFID, EMI] to make money, and I need to make a whole lot of investment in compliance infrastructure to be able to be profitable?’”

MiCA itself is undergoing change, with some country regulators calling for tighter, more centralized control and granting increased oversight to bodies such as the European Securities and Markets Authority (ESMA). And when it comes to structured products, ESMA recently reminded crypto firms offering perpetual futures that some of these products may fall outside the rules.

Zhou said Bybit chose a stringent regulator in Austria’s FMA, a decision he said will pay dividends down the line. Each country interprets MiCA differently, he said: “Some countries interpret it as a way to attract new business; some want heavy regulation. So you actually have different levels of strictness.”

As for bringing ESMA into the mix, Bybit is neutral, Zhou said.

“There are talks about a more level playing field,” he said. “But there could be disadvantages. Because when you have a local regulator they are easy to get to. If we have any issues, we just send an email and go to FMA in Vienna. But if everyone’s in Paris, then you have to line up. There are more CASPs, increased bureaucracy, decreased efficiency.”

A White House-linked official has warned that failure to pass clear crypto rules in the United States could help China gain ground in digital assets.

Summary

- Patrick Witt warned that failing to pass clear US crypto rules could benefit China’s digital asset ambitions.

- The CLARITY Act remains stalled as lawmakers debate stablecoin yield rules and market oversight.

- The Senate Banking Committee’s narrow GOP majority leaves the bill dependent on full Republican support.

The comments came as debate over the proposed CLARITY Act continues in Washington. Patrick Witt said the United States risks losing leadership if lawmakers fail to approve a full crypto market framework. He linked the delay to wider concerns about foreign rivals and digital finance.

“What are the odds the anonymous sources cited in this article have deep ties to China?” Witt said. “Because if the US fails to lead on crypto by passing a comprehensive regulatory framework, the prime beneficiary will be the CCP.”

CLARITY Act faces resistance

The CLARITY Act seeks to create a national rulebook for digital assets. Supporters say the bill would bring crypto firms closer to the standards used by banks and other financial companies.

Republican Senator Tim Scott has backed the proposal. The bill would require crypto businesses to follow clearer rules on disclosures, operations, and market conduct.

However, some conservative and crypto-aligned voices have opposed the bill. They argue that it could weaken protections linked to the GENIUS Act and give large companies too much control over the sector.

Stablecoin yield dispute slows progress

The bill remains stalled in the Senate Banking Committee. Senator Thom Tillis has pushed to delay action until May as lawmakers debate language tied to stablecoin yield rules.

Stablecoin yield has become one of the main points of dispute. Banks have raised concerns that yield-bearing stablecoins could compete with deposits, while crypto firms want room to build new financial products.

The committee’s narrow Republican majority adds pressure to the process. Since the GOP holds only a one-vote edge, the bill needs full Republican support to move forward.

Leadership questions add pressure

The debate has also raised questions about policy coordination inside the administration. Reports say there is no dedicated West Wing coordinator handling the crypto legislation push.

That gap could make it harder to settle disputes between lawmakers, banks, and crypto firms. For now, the CLARITY Act remains one of the most closely watched crypto bills in Congress.

Supporters say clear rules could keep crypto activity in the United States. Critics say lawmakers must avoid a framework that favors large firms over market competition.

Crypto World

Lockheed Martin (LMT) Stock Plummets 12% Following Disappointing Q1 Results and Analyst Downgrades

TLDR

- Lockheed Martin shares declined 11.67% following a disappointing first-quarter earnings release that missed analyst projections

- First-quarter earnings per share reached $6.44, falling short of the $6.74 consensus forecast; revenues totaled $18.02B versus $18.38B expectations

- The company reported negative free cash flow of -$291 million during the period

- Several Wall Street firms reduced their price objectives; overall sentiment remains neutral with average targets near $635

- Company executives maintained their full-year 2026 earnings outlook of $29.35–$30.25 per share despite first-quarter weakness

Lockheed Martin experienced a difficult trading week following its first-quarter 2026 financial results. The aerospace and defense contractor saw its shares tumble 11.67% as investors reacted to multiple disappointments in the quarterly report.

Lockheed Martin Corporation, LMT

The defense manufacturer reported earnings of $6.44 per share, falling short of analyst expectations of $6.74 and significantly below the $7.28 delivered during the comparable quarter in 2025. Total revenues reached $18.02 billion, essentially flat compared to the prior year and beneath the $18.38 billion Wall Street had anticipated.

A notable headwind for revenue performance: the first quarter of 2026 contained one fewer business week compared to the same timeframe last year. This calendar quirk reduced the top line by several hundred million dollars.

Cash generation deteriorated significantly, with free cash flow registering at -$291 million. Management attributed the negative figure to margin erosion, fluctuations in working capital requirements, and challenges related to fixed-price contracts.

New orders also disappointed, with the book-to-bill ratio landing at just 0.6x for the quarter. While the company blamed timing factors, the weak bookings metric added to investor concerns surrounding the report.

Wall Street Firms Lower Price Objectives, Neutral Stance Prevails

The earnings disappointment prompted several brokerage firms to reduce their price targets. RBC Capital lowered its objective from $650 to $575 while maintaining a Sector Perform rating, citing “incremental negative estimated costs at completion” and uncertain near-term growth visibility.

BNP Paribas Exane, Morgan Stanley, Deutsche Bank, and Susquehanna similarly reduced their targets. The Street consensus now stands at Hold, with average price objectives hovering around $635 — suggesting potential upside exceeding 25% from current trading levels near $510.

TD Cowen and TipRanks–xAI also kept Hold ratings in place, with targets ranging between $575 and $600. Even with the substantial implied upside from these targets, the prevalence of neutral ratings continued to weigh on shares.

LMT began trading Friday at $513.21. Shares currently trade well beneath the 50-day moving average of $628 but remain above the 200-day moving average of $553.

Fundamental Outlook Remains Unchanged

Beyond the quarterly volatility, Lockheed’s backlog and program portfolio remain robust. The Department of Defense has outlined plans to expand F-35 acquisitions through 2030–31, providing visibility for production schedules.

Peru finalized an agreement to acquire 12 F-16 Block 70 aircraft through a direct commercial transaction. The company also secured positions in U.S. missile defense initiatives, including the “Golden Dome” contracts, and obtained Department of Defense awards to replenish Patriot missile systems.

Executives stood by their full-year 2026 guidance, forecasting earnings per share between $29.35 and $30.25. Analyst consensus for fiscal 2026 currently centers around $29.97 per share.

The company maintains its quarterly dividend of $3.45 per share, translating to an annual yield of approximately 2.7%. The current payout ratio stands at roughly 66.8%.

Vanguard Group reduced its stake by 17,369 shares during the fourth quarter but continues to hold 21.27 million shares, accounting for approximately 9.19% of outstanding shares with a market value near $10.29 billion.

Institutional ownership comprises 74.19% of total shares outstanding. LMT’s 52-week trading range extends from $410.11 to $692.00, with current prices positioned near the lower portion of this band.

RBC Capital’s updated $575 price target and Sector Perform rating represent the most recent analyst commentary on the stock.

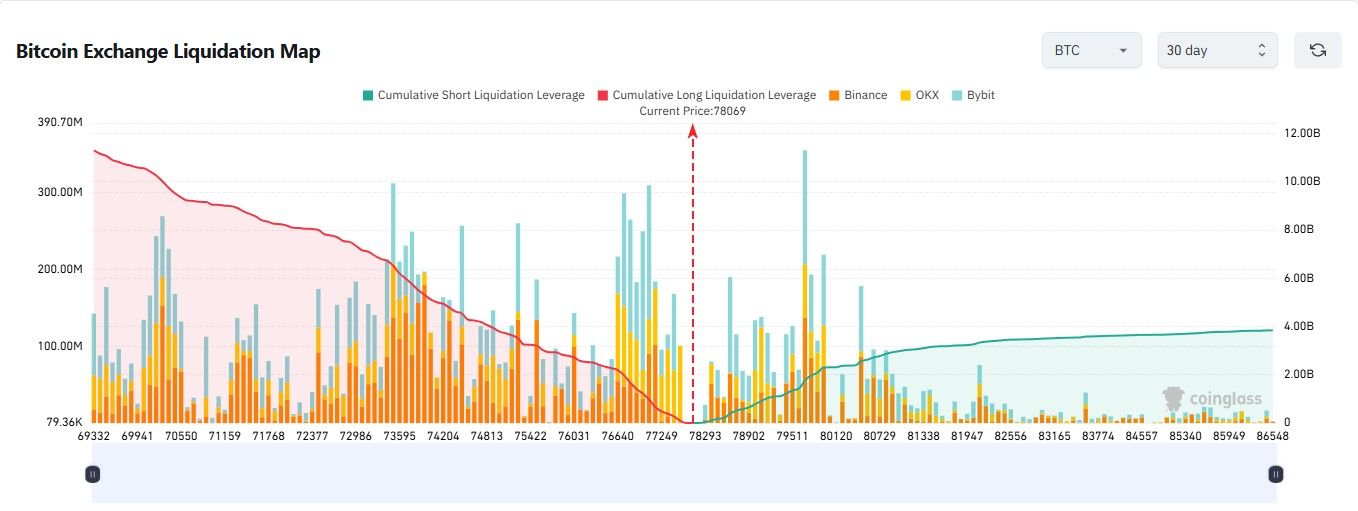

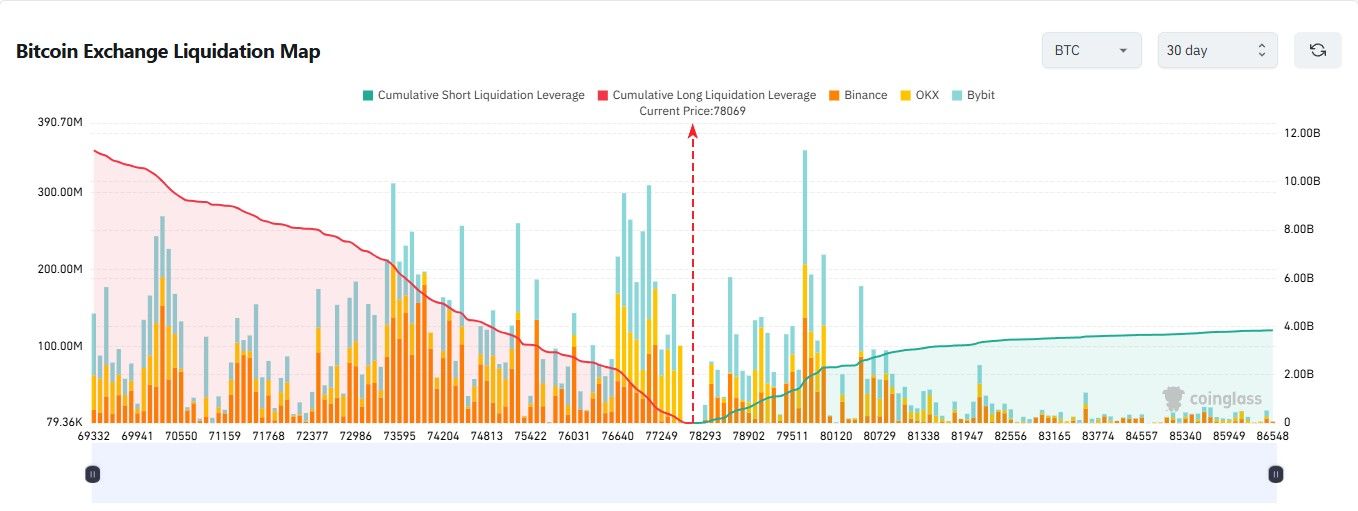

Bitcoin (BTC) traders are stacking the long side of futures by more than three to one, according to Coinglass. The skew points to bullish conviction near $77,500 but raises the threat of forced selling on a sharp pullback.

The lopsided positioning led to open interest in BTC perpetuals sliding roughly 6% to 744,300 BTC over 24 hours. Traders are starting to trim leverage, but long bias still holds across major venues.

Long Bias Meets a Stalling Spot Price

Bitcoin failed to clear $80,000 earlier this week and has since drifted toward $77,500, according to Yahoo Finance. That stall has done little to shake long-side conviction. The long/short ratio on Coinglass still shows more than 3 longs per short.

History shows that extreme imbalances often precede contrarian moves. Crowded one-sided trades become easy fuel for short-term reversals.

Coinglass logged $22.44 million in long liquidations on April 25 against $11.60 million on the short side. The roughly two-to-one wipeout hints bulls are absorbing more pain even as account-level positioning stays heavily long.

Bitcoin Liquidation Map Flags Concentrated Risk Pockets

The Coinglass map shows dense clusters of leveraged long positions stacked beneath the current spot price. The arrangement historically amplifies downside moves through cascading liquidations.

Each liquidated long adds market sell flow that can push the price into the next cluster.

Earlier in April, $71 million in long positions sat at risk under $77,300. Above $78,000, short-squeeze conditions fueled a sweep that wiped out millions in bearish bets. Rising leverage and open interest have repeatedly preceded sharp corrections this cycle.

Whether spot defends $77,000 may decide if the next move is a controlled cool-off or a sharper liquidation cascade. For now, the imbalance leaves the market structurally fragile despite the bullish optics.

The post Bitcoin Leverage Builds as Price Stalls Below $80,000 appeared first on BeInCrypto.

Crypto World

Arkham says Aave raised $160 million of the $200 million it needs to cover exploit damage

Lending platform Aave has raised about $160 million it needs to cover the $200 million in bad debt left behind by the year’s largest decentralized finance (DeFi) exploit, Arkham posted on X on Saturday.

“AAVE have so far raised $160M to cover the bad debt from the Kelp DAO Exploit, at defiunited.eth,” the blockchain analytics platform wrote. “The largest contributors are Mantle and AAVE DAO, who together raised 55,000 ETH or $127M.”

Last week, Aave and several major crypto firms announced a coordinated recovery effort to stabilize DeFi markets after a $292 million security breach left the crypto borrowing sector’s largest lender facing a financial crisis.

Called DeFi United and led by Aave service providers, the effort’s goal is to restore support for rsETH, the yield-bearing derivative token of ether (ETH) at the core of the exploit.

“I’m personally contributing 5,000 ETH to DeFi United as we continue working together with partners,” said Aave founder Stani Kulecho. His personal contribution at ether’s current price of roughly $2,346 is worth $11,730,000.

The exploit is traced back to a KelpDAO integration vulnerability with LayerZero, where an attacker minted 116,500 unbacked rsETH tokens. That left Aave with impaired collateral, triggering a run on deposits as lenders rushed to exit, ultimately withdrawing $10 billion.

The effort to erase the bad debt is focused mostly on stabilizing the system with a coordinated bailout to recapitalize rsETH and mitigate losses.

The second-largest exploit this year took place late March, when an attacker drained at least $270 million from the Drift Protocol on Solana by abusing a legitimate feature called ‘durable nonces,’ rather than exploiting a code bug or stolen keys.

Key Highlights

- Major technology companies including Alphabet, Amazon, Meta, Microsoft, and Apple release quarterly results this week

- Federal Reserve policy decision scheduled for Wednesday, with rates anticipated to remain between 3.5% and 3.75%

- Justice Department concluded criminal probe into Fed Chair Jerome Powell, paving way for Kevin Warsh’s confirmation process

- Analysts project 25% net income growth for Magnificent Seven in 2026 versus 11% for remaining S&P 500 constituents

- Major oil producers Exxon and Chevron announce results Friday amid geopolitical tensions

Markets enter the most packed earnings period of the reporting season as Monday launches a week featuring financial results from five global corporate behemoths.

Wednesday brings quarterly announcements from Alphabet, Amazon, Meta, and Microsoft, while Apple closes the sequence Thursday.

#earnings for the week of April 27, 2026 https://t.co/hLn2sKQhEY $MSFT $AMZN $AAPL $META $SNDK $SOFI $GOOGL $HOOD $CLS $BE $VZ $STX $TER $V $WDC $UPS $COP $ENPH $CAT $APH $OPK $RDDT $QCOM $CMG $CVX $F $VLO $W $AXTI $HUM $KGC $LLY $MA $KO $RIVN $GLW $CL $RMBS $SPOT $REGN $RIOT… pic.twitter.com/LNFadBAIBQ

— Earnings Whispers (@eWhispers) April 24, 2026

This quintet represents the core of the Magnificent Seven, an influential collection of technology leaders credited with powering substantial equity market appreciation over recent periods.

Tesla previously disclosed its numbers. Nvidia remains the sole member scheduled to announce later this earnings cycle.

The opening months of 2026 proved challenging for the Magnificent Seven. During March’s final trading days, the collective shed approximately $850 billion in capitalization. Every member posted negative year-to-date performance by month-end.

Recent weeks have delivered a reversal. The Roundhill Magnificent Seven ETF has climbed 13% across the trailing month, outpacing the S&P 500’s 9% advance.

Morgan Stanley’s analysis forecasts 25% net income expansion for this group in 2026, substantially exceeding the 11% projection for the S&P 493 constituents.

Artificial Intelligence Capital Expenditures Under Scrutiny

Market participants will scrutinize commentary regarding artificial intelligence infrastructure investments. Recent actions from Meta and Microsoft have sparked questions—Meta implemented 8,000 workforce reductions while Microsoft extended voluntary separation packages to certain employees.

Alphabet previously indicated plans to approximately double capital allocation. Amazon CEO Andy Jassy characterized the company’s semiconductor operations as experiencing exceptional demand.

Apple stakeholders await commentary from incoming CEO John Ternus, who assumes leadership responsibilities from Tim Cook.

Equity markets concluded the previous week with upward momentum. The S&P 500 advanced 0.8% Friday, securing a 0.6% weekly increase. The Nasdaq climbed 1.6% Friday for a 1.5% weekly advance. The Dow slipped 0.2% on the session and declined 0.4% across the week.

FOMC Maintains Course as Powell Investigation Concludes

The Federal Open Market Committee convenes Tuesday through Wednesday, delivering its interest rate determination at 2 p.m. ET Wednesday. Market pricing reflects a 99.5% probability that rates remain within the 3.5% to 3.75% band.

Fed Chair Jerome Powell received positive developments Friday when the Justice Department terminated its criminal inquiry into Powell concerning expense overages during Federal Reserve facility renovations.

The Senate Banking Committee scheduled Wednesday morning proceedings that may include voting on Kevin Warsh’s appointment as forthcoming Fed chair. Warsh represents President Trump’s selection to succeed Powell upon his May term conclusion.

Thursday delivers the March PCE inflation measurement, anticipated to register 3.5% on an annual basis, increasing from the prior 2.8% reading.

Energy sector leaders Exxon and Chevron publish Friday results, with observers monitoring potential impacts from Iranian tensions affecting petroleum transit through the Strait of Hormuz.

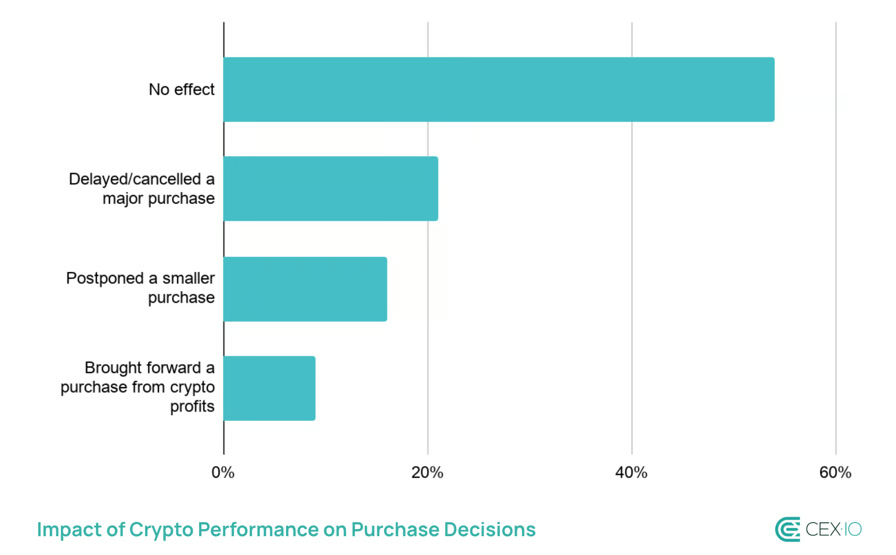

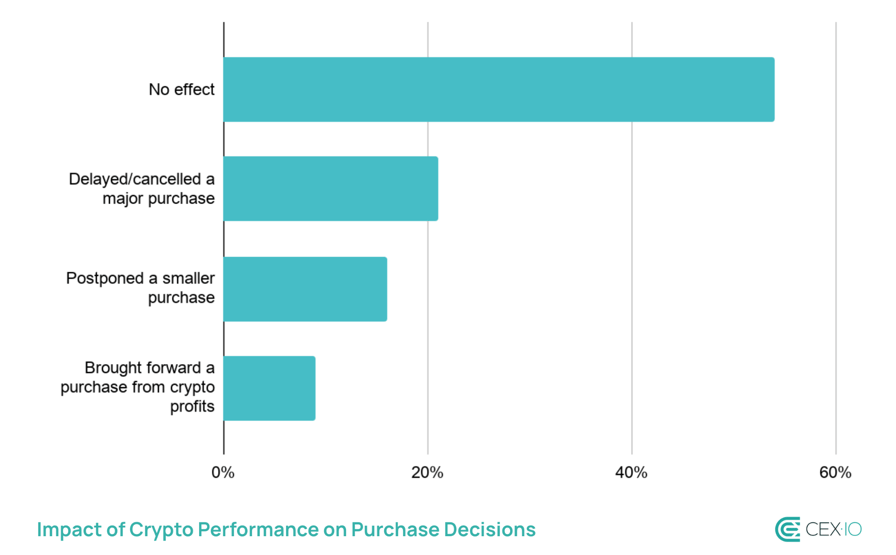

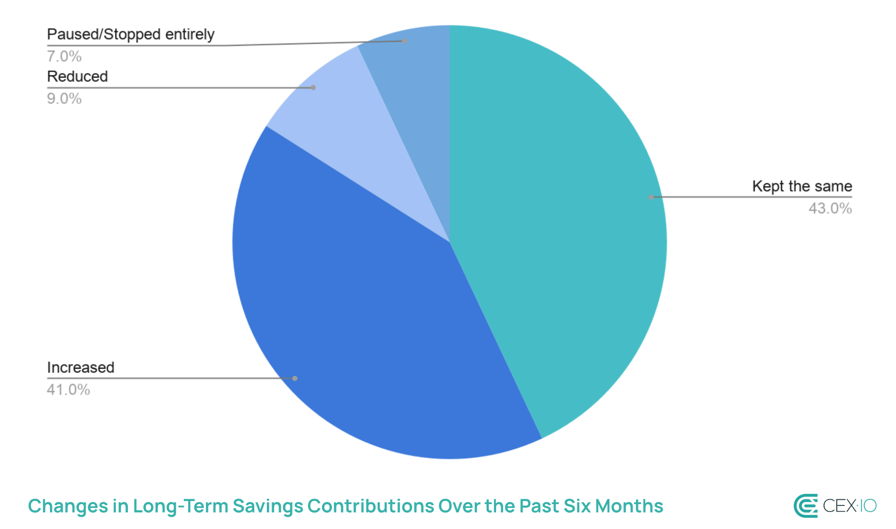

The recent crypto market downturn has forced more than one in three crypto traders to cut everyday spending, according to a new survey by CEX.IO.

The survey, conducted among 1,100 US-based active CEX.IO users, shows the current market slump is straining household finances, though it remains less severe than 2022, when Bitcoin fell by roughly 75% from its peak. Bitcoin is still about 40% below its October 2025 high, leaving many retail investors sitting on unrealised losses.

36% of respondents said they reduced everyday spending as a direct result of market conditions, with 10% describing those cuts as significant sacrifices made to maintain their positions. 37% also reported delaying or cancelling purchases due to crypto losses, including 21% who postponed major financial commitments such as buying a home, car or undertaking renovations.

“The 2025–2026 bear market has not produced the kind of systemic shock seen in past cycles (at least for now), but its effects appear to be showing up in quieter ways at the household level,” CEX.IO wrote.

Related: Crypto Market Sentiment Reaches 3-Month High

Crypto traders navigate downturn alone

The survey revealed that many traders are managing the downturn in relative isolation. Only 5% said someone else knows the full extent and value of their holdings, while the majority either share limited information or keep their positions entirely private.

Financial strain is also evident in cash flow trends. While 77% said they did not take on debt tied to crypto, 38% reported some form of financial disruption since October 2025. A quarter said they relied on savings to maintain stability, and 12% admitted to missing or delaying payments.

Even so, most respondents have not changed plans dramatically. Nearly half reported that crypto makes up more than 30% of their investable assets, yet 73% said their approach to earning income remains unchanged.

Looking ahead, a combined 79% said they plan to either hold or increase their positions over the next six months.

Related: Bitcoin Price May Go Under $70K Despite Strategy’s Latest Big BTC Buy

Crypto offerings shape bank choice

Another survey by Börse Stuttgart Digital earlier this week found that cryptocurrency services are starting to influence how European investors choose their banks, with 35% saying they would consider switching institutions for better crypto offerings.

The poll of around 6,000 investors across Germany, Italy, Spain and France also found that nearly one in five expects their primary bank to provide crypto access within three years, pointing to a gradual shift toward integrating digital assets into mainstream banking.

Magazine: How to fix suspected insider trading on Polymarket and Kalshi

Michael Saylor has hinted at another Strategy Bitcoin purchase ahead of the company’s expected Monday update.

Summary

- Saylor hinted at another Bitcoin purchase after Strategy raised holdings to 815,061 BTC last week.

- Analysts expect a smaller buy because MSTR share issuance paused while shares traded below par.

- Strategy still has ATM capacity, but funding conditions may limit near-term Bitcoin accumulation size.

The Strategy executive posted his usual Sunday signal on X, writing, “The ₿eat Goes On.” The post drew attention because Strategy made a large Bitcoin purchase last week. The company added 34,164 BTC, lifting its total holdings to 815,061 BTC.

Market watchers do not expect another billion-dollar Bitcoin buy this time. The latest report said Strategy’s main funding route slowed after MSTR-linked issuance paused during the week.

The company has often used share sales to fund Bitcoin purchases. However, the report said the funding engine weakened as MSTR traded at $99.46, slightly below par.

That situation may limit how much Bitcoin Strategy can buy in the next update. Saylor has often avoided issuing shares when market terms may hurt existing shareholders.

Strategy weighs funding options

Strategy still has other funding routes available. The company retains about $26.7 billion in common stock capacity through its at-the-market program.

This tool allows the company to sell shares when conditions support it. Strategy may use the program only when the stock trades at a strong premium to its Bitcoin holdings.

The report also cited SATA, or Strive Series A, as another small funding source. It said only 0.72 BTC was acquired through SATA-linked activity this week.

Bitcoin strategy faces fresh scrutiny

The expected update comes as Strategy’s Bitcoin treasury model faces more public debate. Supporters see the model as a long-term Bitcoin accumulation plan.

Critics say the model depends on steady access to capital markets. They argue that weaker funding conditions could slow future Bitcoin purchases or raise pressure on the company’s balance sheet.

Last week’s purchase showed that Strategy can still add large amounts of Bitcoin when funding conditions allow. This week’s update may show whether the company has shifted to a more selective pace.

Key Takeaways

- Duolingo stock has plummeted 80% from its May 2025 high of $544.93, currently hovering near $103

- Q4 2025 revenue reached $282.9M, representing 35% year-over-year growth, with net margins hitting 40%

- Current valuation sits at 12.5x earnings and 13.4x free cash flow — dramatically lower than typical growth company multiples

- Quent Capital expanded its DUOL holdings by 21,133.9% during Q4, purchasing 12,469 additional shares

- Goldman Sachs increased exposure by 123.9%; Wall Street consensus price target stands at $206.16

Duolingo experienced an extraordinary rally leading up to May 2025. The shares had surged threefold over the preceding year, the company’s iconic green owl mascot dominated social media, and investor enthusiasm seemed boundless.

Then momentum reversed sharply.

From its May 2025 zenith of $544.93, DUOL shares have cratered approximately 80%, currently trading around $103. Two catalysts triggered investor panic: the emergence of sophisticated AI translation platforms like DeepSeek, and company leadership’s strategic shift toward user acquisition rather than immediate profitability.

Wall Street interpreted these developments as existential risks. A massive selloff ensued.

Yet the underlying fundamentals haven’t crumbled. During Q4 2025, Duolingo delivered revenue of $282.9 million — reflecting 35% year-over-year expansion — and exceeded earnings projections with $0.91 EPS versus the $0.79 Street estimate. Net profit margin registered at 39.91%.

These metrics hardly suggest a business in distress.

The equity currently commands a price-to-earnings multiple of 12.14 and a PEG ratio of 0.70. Such compressed valuations typically characterize stagnant, mature enterprises — not companies expanding top-line revenue at 35% annually.

Smart Money Accumulating Shares

Notwithstanding the dramatic pullback, select institutional players are accumulating positions. Quent Capital LLC expanded its stake by a staggering 21,133.9% during Q4, acquiring 12,469 shares for a total holding of 12,528 shares, valued at approximately $2.2 million at quarter’s close.

Goldman Sachs boosted its DUOL allocation by 123.9% in Q1, currently controlling 87,556 shares worth roughly $27.2 million. Amundi elevated its ownership by 142.1%, while NewEdge Advisors expanded its stake by 1,868.2%.

Institutional ownership now represents 91.59% of outstanding shares.

Regarding insider activity, the landscape appears mixed. Company executives including Natalie Glance and General Counsel Stephen C. Chen offloaded a combined 14,939 shares during the most recent quarter, totaling approximately $1.68 million in proceeds. Insider ownership stands at 15.67%.

Wall Street Consensus Remains Divided

Analyst sentiment shows considerable fragmentation. Four analysts maintain Buy ratings, sixteen recommend Hold positions, and three have assigned Sell ratings. The consensus price objective sits at $206.16 — representing approximately 100% upside from current levels.

Recent target reductions have been dramatic. Citigroup slashed its forecast from $270 to $101. Barclays reduced expectations from $230 to $110. Needham, maintaining a constructive outlook, lowered its target from $300 to $145 while preserving its Buy recommendation.

Weiss Ratings downgraded to Sell this week. Zacks Research followed with a Strong Sell rating in March.

Duolingo’s recently introduced chess curriculum now attracts over 7 million daily active users — achieved without the application even appearing in chess-related app store search results. The Max subscription offering leverages artificial intelligence to provide personalized error explanations and facilitate conversational practice within a premium paid tier.

DUOL’s 52-week trading range spans from $87.89 to $544.93. The stock’s 50-day moving average registers at $100.89, with the 200-day average positioned at $164.98. Current market capitalization totals $4.86 billion.

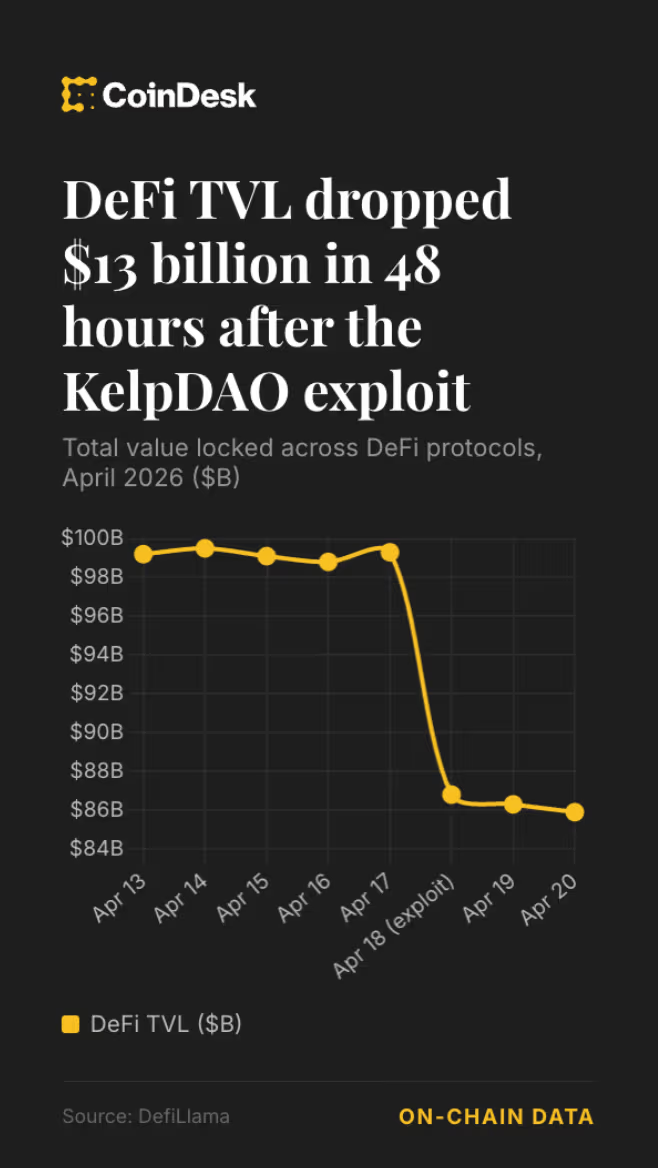

The easiest take after a $290 million exploit and a roughly $13 billion slide in DeFi total value locked is that decentralized finance is broken again. It is also probably the laziest.

The KelpDAO exploit over the weekend was serious. It appears to have started with a targeted attack on infrastructure used in LayerZero’s verification stack, not a smart contract bug as commonly seen in other exploits. LayerZero has preliminarily linked the incident to North Korea’s Lazarus Group, and said the attack succeeded because Kelp had opted for a single-verifier setup despite repeated recommendations to use a more resistant configuration. The exploit left rsETH (a liquid staking token issued by KelpDAO) unbacked and triggered fears that bad debt would spill into lending markets, especially Aave’s WETH pool (where users borrow wrapped ether against collateral).

And yet the more interesting story is not that DeFi was hit. It is that DeFi is still here.

Capital fled quickly after the breach. Aave alone experienced $8.45 billion in outflows over 48 hours, while broader DeFi TVL fell into the mid-$80 billion range, roughly back to where the sector sat around this point last year. In other words, this was a sharp repricing of risk, not as destructive as some are making out.

Aave, the largest DeFi lending market, had accumulated significant rsETH as collateral in the weeks before the exploit as users built leveraged positions. The scale of that TVL drop also warrants some context. A $292 million theft does not directly produce a $13 billion decline unless a meaningful portion of that TVL was already recycled collateral. Much of Aave’s ETH exposure heading into the weekend was concentrated in looping strategies, where users deposit liquid restaking tokens, borrow ETH against them, swap for more restaking tokens, and repeat. In other words, the same pile of assets may be counted multiple times in the TVL calculation. That leverage inflates TVL on the way up and unwinds sharply during events like this. The actual net capital loss is likely a fraction of the headline figure, though the exact amount is difficult to isolate given how deeply looping strategies are embedded in DeFi’s TVL calculations.

Those strategies were themselves partly a product of a yield environment that had already stopped making sense. As of early April, Aave was offering 2.61% APY on USDC deposits, below the 3.14% available on idle cash at Interactive Brokers, a traditional financial brokerage. The risk premium that historically justified DeFi’s complexity and smart contract exposure had largely disappeared. With organic yield insufficient, leverage filled the gap, and that concentration is what made the rsETH contagion as damaging as it was. Data from DefiLlama shows that reETH balances on Aave had grown rapidly in the weeks leading up to the exploit, reaching nearly 580,000 tokens ($1.3 billion), evidence that the leverage buildup made the subsequent unwind so sharp.

Crypto has survived worse

The phrase “DeFi is dead” gets wheeled out after every hack because the failures are visible and immediate, while the recovery is slower and less cinematic. But crypto has seen worse. Terra collapsed and vaporized confidence across the sector. Wormhole and Ronin lost roughly $1 billion each. Multichain unraveled.

“DeFi didn’t die when Terra collapsed and caused billions in liquidations and losses,” wrote a pseudonymous trader on X. “DeFi didn’t die when Wormhole and Ronin got drained for around $1 billion. DeFi didn’t die when Multichain bridge assets were stolen.”

More recently, Bybit suffered what was widely described as the largest crypto theft on record, losing around $1.5 billion last February, yet it continued operating, processed a surge in withdrawals, restored reserves and still handles billions of dollars in trading volume each day.

The repricing of trust

0xNGMI, founder of DefiLlama, told CoinDesk the losses are significant but unlikely to be existential. “Aave has many recourses to cover the loss, including its treasury and taking loans, and I think those will have to be used to protect the protocol,” he said. “Overall a significant loss but one that will be recovered. The biggest issue will be the impact on risk premiums that are assigned to DeFi.”

Those risk premiums are a real and lasting cost. Capital will demand more compensation for sitting in onchain systems whose attack surface now extends beyond code

Still, repricing is not the same thing as collapse. “Some of the money will come back,” 0xNGMI said. “We saw this before in Aave when rumors of a hack appeared. It’s always the best strategy to withdraw and redeposit later as the cost of that is tiny and the reward very large.” Some deposits will not return, but historically deposit outflows during stress events reverse as conditions stabilize, as evidence after Terra’s collapse in 2021.

There is also evidence that capital is not simply leaving DeFi. It is rotating. Spark offers one example. Spark’s strategy lead, who goes by monetsupply.eth, said the protocol delisted rsETH and other low-utilization assets in January, a move that may have cost it business and ETH-looping activity to Aave at the time. Under current conditions, however, SparkLend still has ample ETH withdrawal liquidity while Aave is experiencing shortages across several markets. Over the weekend Spark TVL jumped from $1.8 billion to $2.9 billion, demonstrating clear capital rotation.

The more interesting critique, raised by some builders after the exploit, is not that DeFi failed but that it has become too timid. If the sector is going to ask users to bear infrastructure risk, smart contract risk and governance risk for low single-digit yields, the product set starts to look less compelling. With that in mind, Kelp is not the end of DeFi. It is a wake-up call for builders to build safer systems while continuing to offer real world use cases.

Quick Summary

- SIMO shares climbed 8.07% as traders positioned themselves before the company’s Q1 2026 earnings announcement on April 28

- Wall Street expects Q1 revenue to reach $299.4 million with earnings per share of $1.31

- The stock’s momentum reflects strong AI data center appetite for SIMO’s PCIe Gen5 SSD controller technology

- Analysts have increased full-year 2026 EPS projections by 3.58% to $5.78 over the last two months

- Shares have skyrocketed 222.3% in the past year, significantly outperforming the sector’s 157.6% increase

Silicon Motion (SIMO) experienced an 8.07% surge on Thursday as market participants bought into the stock in anticipation of its Q1 2026 financial results, set for release on April 28.

Silicon Motion Technology Corporation, SIMO

The upward movement reflects growing confidence in demand for the company’s solid-state drive controllers, especially from hyperscale data centers focused on artificial intelligence applications.

Analyst consensus from Zacks projects Q1 revenue of $299.4 million alongside earnings of $1.31 per share. Looking at the full year, 2026 EPS forecasts have been upgraded 3.58% during the past 60 days to reach $5.78, while 2027 projections jumped 8.75% to $7.83.

Silicon Motion has exceeded earnings forecasts in three of its previous four quarterly reports, posting an average positive surprise of 23.34%. The single miss occurred in the most recent quarter, falling short by 2.33%.

A broader semiconductor sector rally contributed additional momentum to the stock. Chipmakers have attracted renewed investor attention as spending on AI infrastructure continues accelerating.

Gen5 Technology and Enterprise AI Storage Expansion

Earlier this quarter, Silicon Motion unveiled the SM8008 — an advanced SSD controller manufactured using TSMC’s 6nm technology. The chip specifically targets enterprise data center applications and aims to reduce energy consumption while delivering consistent performance under demanding AI processing conditions.

The company is strategically aligning itself with NVIDIA’s initiative to utilize NAND flash storage as an active memory tier within AI computing systems — a development that could substantially broaden the total available market for SSD controller solutions.

Its MonTitan enterprise controller family directly addresses the AI data center storage sector, a market segment viewed as both larger and more profitable than Silicon Motion’s conventional consumer-oriented business lines.

Silicon Motion has also announced that its UFS solution successfully passed compatibility testing on Qualcomm’s Snapdragon Cockpit SA8295P platform, creating new opportunities in the automotive storage market.

Over the trailing twelve months, SIMO has advanced 222.3%, substantially exceeding the industry’s 157.6% appreciation. The stock has outperformed Marvell (MRVL), which posted 188.8% gains, though it lags Western Digital (WDC), which rocketed 903.5%.

Potential Headwinds to Consider

Competitive pressures represent a genuine concern. Marvell maintains a dominant position in enterprise and cloud SSD controller markets. Western Digital leverages vertical integration — developing complete storage systems internally — eliminating dependence on external controllers like those produced by Silicon Motion.

This industry trend toward integrated storage solutions presents obstacles for Silicon Motion’s expansion in particular market segments.

The company additionally confronts macroeconomic and geopolitical challenges. Its Taiwan headquarters introduces political exposure given persistent tensions with China. Supply chain disruptions and cyclical consumer demand patterns in PCs and smartphones contribute additional volatility.

From a valuation perspective, SIMO currently trades at 22.1x forward earnings — exceeding the sector average of 11.8x and surpassing its own historical median of 21.65x.

Zacks presently assigns a Rank #3 (Hold) rating to SIMO, accompanied by an Earnings ESP of 0.00%, indicating their quantitative model doesn’t forecast a definitive earnings beat for Q1.

Silicon Motion has also announced its upcoming quarterly dividend of $0.50 per ADS, payable on May 21, 2026, to investors of record as of May 7.

Sabastian Sawe shatters 2-hour barrier to win London Marathon

Apple is eyeing ten new product categories in the coming years

Celtic loanee filmed celebrating Motherwell’s stunning win over Rangers

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread – Corporette.com

-

Politics6 days ago

Politics6 days agoGary Stevenson delivers timely reminder to register to vote as deadline TODAY

-

Entertainment7 days ago

NBA Analyst Charles Barkley Chimes in on Ice Spice McDonald’s Fiasco

-

Crypto World22 hours ago

Hyperliquid $HYPE Rally Builds Momentum as AI Sector Enters Prove-It Phase

-

Crypto World6 days ago

Bank of Hawai’i (BOH) Q1 2026: Net Income Drops to $57.4M as Net Interest Margin Expands

-

Politics4 days ago

Politics4 days agoMaking troops accountable for war crimes threatens US alliance, ex-SAS colonel warns

-

Politics4 days ago

Politics4 days agoDisabled people challenge government SEND proposals over segregation concerns

-

Business4 days ago

Business4 days agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Politics4 days ago

Politics4 days agoZack Polanski responds to home secretary’s taser threat

-

Politics4 days ago

Politics4 days agoStarmer handler McSweeney to be dragged from shadows by Foreign Affairs Committee

-

Sports4 hours ago

Sports4 hours agoIPL 2026: Ruturaj Gaikwad registers slowest fifty of the season, enters all-time unwanted list | Cricket News

-

Politics4 days ago

Wings Over Scotland | How To Get Away With Crimes

-

Crypto World5 days ago

Crypto World5 days agoFive Value Stocks with Recovery Potential in 2026: PayPal (PYPL), Nike (NKE), and More

-

Crypto World5 days ago

Crypto World5 days agoNew York sues Coinbase, Gemini over prediction market offerings

-

Politics4 days ago

Politics4 days ago‘Iran is still a nuclear threat’

-

Sports4 days ago

Sports4 days agoTim Bradley names the current best in the world: “Better than Inoue and Usyk”

-

Business4 days ago

Business4 days agoHCL Tech share price tank over 9% after weak Q4. JPMorgan, HSBC & 3 others cut target price

-

NewsBeat8 hours ago

NewsBeat8 hours agoLK Bennett closes all stores after entering administration

-

Crypto World5 days ago

Crypto World5 days agoCrypto’s great hope in Senate’s Clarity Act still has a path to survive tight calendar

-

Business4 days ago

Business4 days agoThe Job Benefits Most Men Don’t Know to Negotiate

You must be logged in to post a comment Login