Crypto World

Can Bitcoin Price Continue Its Push To The Upside? Varntix Investors Buyout 24% Savings Plan In Just 7 Hours!

Bitcoin pushed back toward the $79,000 level as easing geopolitical tension driven by the potential extension of the U.S. Iran ceasefire talks lifted overall risk sentiment. The move was supported by renewed ETF inflows and increased derivatives activity, reinforcing short-term momentum.

At the same time, recent pullbacks tied to geopolitical uncertainty have highlighted how quickly sentiment can shift. Sharp reversals remain a defining feature of the market, and that volatility is starting to influence how investors position capital.

Rather than relying solely on price movement, a growing share of capital is moving toward structured income strategies. Platforms like Varntix reflect this shift, offering fixed-term allocations with predefined stablecoin payouts. The aim is not to replace exposure to assets like Bitcoin, but to introduce a more predictable income layer alongside ongoing market fluctuations.

Can Bitcoin Price Sustain Momentum Amid Macro Uncertainty?

According to the New York Post, Trump has indicated that U.S.–Iran peace negotiations could restart as early as Friday, following a decision to extend the truce indefinitely.

Bitcoin responded with a modest rebound, gaining over 1% and pushing its 24-hour advance beyond 4%, with price hovering near $78,900. The intraday range has been relatively wide, with a low around $74,852 and a high near $78,728. However, the move comes alongside a sharp drop in trading volume down roughly 32% suggesting that traders remain cautious despite the upward momentum.

Source: CoinMarketCap

Grayscale Research has suggested that Bitcoin could find a bottom in the $65,000 to $70,000 range, pointing to a more cautious near-term outlook. At the same time, the Bitcoin Bull Index has shifted to neutral for the first time in six months, reflecting a cooling in overall sentiment.

Despite this, derivatives activity is picking up. CoinGlass data shows a notable increase in futures positioning, with total open interest rising more than 9% in the past 24 hours to exceed $62 billion, indicating growing participation even as directional conviction remains mixed.

Structured Crypto Income: The Varntix Approach

While Bitcoin continues to react to geopolitical headlines and liquidity shifts, not all investors are positioning around direction alone. A growing share of capital is moving toward structures that don’t depend on whether price moves up or down next.

That’s where Varntix is starting to stand out. It offers a structured approach to earning yield on digital assets through dedicated savings plans, where capital is allocated for set periods and returns are defined upfront.

Payouts are made in stablecoins like USDT or USDC, creating a more predictable experience. Instead of reacting to market swings, investors know what they are committing, how long it is allocated and what it is expected to return over that period.

Varntix introduces flexibility through a savings structure that offers two distinct approaches. Fixed plans are designed for investors who want higher returns over longer timeframes, while flexible accounts prioritise liquidity, allowing withdrawals when needed even if the yield is lower.

The contrast becomes clearer when you look at a simple $2,500 allocation. With Bitcoin, the outcome is entirely dependent on price movement. If the price rises by 20%, the position gains around $500. If it falls by the same amount, the loss is similar. If the market moves sideways, there is no return at all. Everything depends on timing and direction.

Varntix removes that dependency by defining the return in advance. A fixed plan can generate roughly $600 over a year regardless of how the market performs. A flexible plan produces a lower but steady return, typically between $107 and $162 annually, while still allowing access to the capital when required.

The key difference is predictability. Instead of outcomes shifting with market volatility, investors receive stablecoin-based income that follows a clear structure, making it easier to plan around both growth and liquidity even in uncertain market conditions.

Take a closer look at Varntix if you want your crypto to work harder.

FAQs

Q1: What is Varntix in relation to Bitcoin price movements?

Varntix is a fixed-income crypto model that operates independently of Bitcoin price direction, offering stablecoin returns instead of market-dependent gains.

Q2: How does Varntix make returns different from trading Bitcoin?

Bitcoin returns depend on price fluctuations, while Varntix provides predefined yields over fixed terms, paid in stablecoins like USDT or USDC.

Q3: Why are investors considering Varntix during volatile Bitcoin markets?

Because Bitcoin price is highly reactive to geopolitical and macro news, Varntix offers a way to earn a predictable income without needing to time market swings.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Michael Saylor has hinted at another Strategy Bitcoin purchase ahead of the company’s expected Monday update.

Summary

- Saylor hinted at another Bitcoin purchase after Strategy raised holdings to 815,061 BTC last week.

- Analysts expect a smaller buy because MSTR share issuance paused while shares traded below par.

- Strategy still has ATM capacity, but funding conditions may limit near-term Bitcoin accumulation size.

The Strategy executive posted his usual Sunday signal on X, writing, “The ₿eat Goes On.” The post drew attention because Strategy made a large Bitcoin purchase last week. The company added 34,164 BTC, lifting its total holdings to 815,061 BTC.

Market watchers do not expect another billion-dollar Bitcoin buy this time. The latest report said Strategy’s main funding route slowed after MSTR-linked issuance paused during the week.

The company has often used share sales to fund Bitcoin purchases. However, the report said the funding engine weakened as MSTR traded at $99.46, slightly below par.

That situation may limit how much Bitcoin Strategy can buy in the next update. Saylor has often avoided issuing shares when market terms may hurt existing shareholders.

Strategy weighs funding options

Strategy still has other funding routes available. The company retains about $26.7 billion in common stock capacity through its at-the-market program.

This tool allows the company to sell shares when conditions support it. Strategy may use the program only when the stock trades at a strong premium to its Bitcoin holdings.

The report also cited SATA, or Strive Series A, as another small funding source. It said only 0.72 BTC was acquired through SATA-linked activity this week.

Bitcoin strategy faces fresh scrutiny

The expected update comes as Strategy’s Bitcoin treasury model faces more public debate. Supporters see the model as a long-term Bitcoin accumulation plan.

Critics say the model depends on steady access to capital markets. They argue that weaker funding conditions could slow future Bitcoin purchases or raise pressure on the company’s balance sheet.

Last week’s purchase showed that Strategy can still add large amounts of Bitcoin when funding conditions allow. This week’s update may show whether the company has shifted to a more selective pace.

Key Takeaways

- Duolingo stock has plummeted 80% from its May 2025 high of $544.93, currently hovering near $103

- Q4 2025 revenue reached $282.9M, representing 35% year-over-year growth, with net margins hitting 40%

- Current valuation sits at 12.5x earnings and 13.4x free cash flow — dramatically lower than typical growth company multiples

- Quent Capital expanded its DUOL holdings by 21,133.9% during Q4, purchasing 12,469 additional shares

- Goldman Sachs increased exposure by 123.9%; Wall Street consensus price target stands at $206.16

Duolingo experienced an extraordinary rally leading up to May 2025. The shares had surged threefold over the preceding year, the company’s iconic green owl mascot dominated social media, and investor enthusiasm seemed boundless.

Then momentum reversed sharply.

From its May 2025 zenith of $544.93, DUOL shares have cratered approximately 80%, currently trading around $103. Two catalysts triggered investor panic: the emergence of sophisticated AI translation platforms like DeepSeek, and company leadership’s strategic shift toward user acquisition rather than immediate profitability.

Wall Street interpreted these developments as existential risks. A massive selloff ensued.

Yet the underlying fundamentals haven’t crumbled. During Q4 2025, Duolingo delivered revenue of $282.9 million — reflecting 35% year-over-year expansion — and exceeded earnings projections with $0.91 EPS versus the $0.79 Street estimate. Net profit margin registered at 39.91%.

These metrics hardly suggest a business in distress.

The equity currently commands a price-to-earnings multiple of 12.14 and a PEG ratio of 0.70. Such compressed valuations typically characterize stagnant, mature enterprises — not companies expanding top-line revenue at 35% annually.

Smart Money Accumulating Shares

Notwithstanding the dramatic pullback, select institutional players are accumulating positions. Quent Capital LLC expanded its stake by a staggering 21,133.9% during Q4, acquiring 12,469 shares for a total holding of 12,528 shares, valued at approximately $2.2 million at quarter’s close.

Goldman Sachs boosted its DUOL allocation by 123.9% in Q1, currently controlling 87,556 shares worth roughly $27.2 million. Amundi elevated its ownership by 142.1%, while NewEdge Advisors expanded its stake by 1,868.2%.

Institutional ownership now represents 91.59% of outstanding shares.

Regarding insider activity, the landscape appears mixed. Company executives including Natalie Glance and General Counsel Stephen C. Chen offloaded a combined 14,939 shares during the most recent quarter, totaling approximately $1.68 million in proceeds. Insider ownership stands at 15.67%.

Wall Street Consensus Remains Divided

Analyst sentiment shows considerable fragmentation. Four analysts maintain Buy ratings, sixteen recommend Hold positions, and three have assigned Sell ratings. The consensus price objective sits at $206.16 — representing approximately 100% upside from current levels.

Recent target reductions have been dramatic. Citigroup slashed its forecast from $270 to $101. Barclays reduced expectations from $230 to $110. Needham, maintaining a constructive outlook, lowered its target from $300 to $145 while preserving its Buy recommendation.

Weiss Ratings downgraded to Sell this week. Zacks Research followed with a Strong Sell rating in March.

Duolingo’s recently introduced chess curriculum now attracts over 7 million daily active users — achieved without the application even appearing in chess-related app store search results. The Max subscription offering leverages artificial intelligence to provide personalized error explanations and facilitate conversational practice within a premium paid tier.

DUOL’s 52-week trading range spans from $87.89 to $544.93. The stock’s 50-day moving average registers at $100.89, with the 200-day average positioned at $164.98. Current market capitalization totals $4.86 billion.

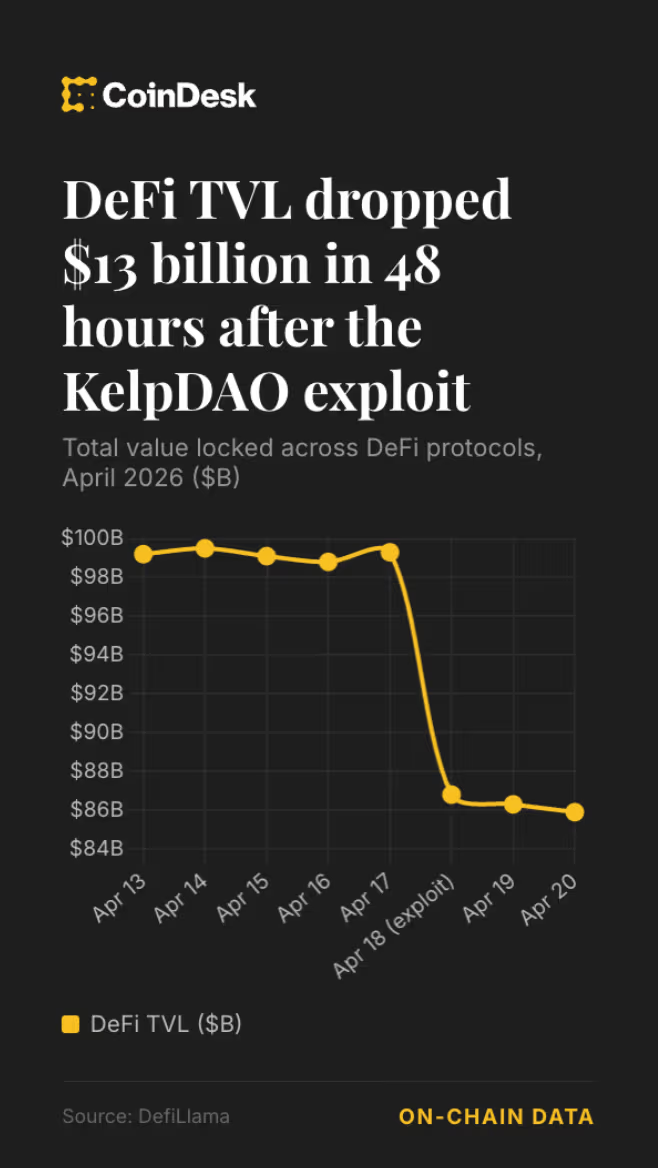

The easiest take after a $290 million exploit and a roughly $13 billion slide in DeFi total value locked is that decentralized finance is broken again. It is also probably the laziest.

The KelpDAO exploit over the weekend was serious. It appears to have started with a targeted attack on infrastructure used in LayerZero’s verification stack, not a smart contract bug as commonly seen in other exploits. LayerZero has preliminarily linked the incident to North Korea’s Lazarus Group, and said the attack succeeded because Kelp had opted for a single-verifier setup despite repeated recommendations to use a more resistant configuration. The exploit left rsETH (a liquid staking token issued by KelpDAO) unbacked and triggered fears that bad debt would spill into lending markets, especially Aave’s WETH pool (where users borrow wrapped ether against collateral).

And yet the more interesting story is not that DeFi was hit. It is that DeFi is still here.

Capital fled quickly after the breach. Aave alone experienced $8.45 billion in outflows over 48 hours, while broader DeFi TVL fell into the mid-$80 billion range, roughly back to where the sector sat around this point last year. In other words, this was a sharp repricing of risk, not as destructive as some are making out.

Aave, the largest DeFi lending market, had accumulated significant rsETH as collateral in the weeks before the exploit as users built leveraged positions. The scale of that TVL drop also warrants some context. A $292 million theft does not directly produce a $13 billion decline unless a meaningful portion of that TVL was already recycled collateral. Much of Aave’s ETH exposure heading into the weekend was concentrated in looping strategies, where users deposit liquid restaking tokens, borrow ETH against them, swap for more restaking tokens, and repeat. In other words, the same pile of assets may be counted multiple times in the TVL calculation. That leverage inflates TVL on the way up and unwinds sharply during events like this. The actual net capital loss is likely a fraction of the headline figure, though the exact amount is difficult to isolate given how deeply looping strategies are embedded in DeFi’s TVL calculations.

Those strategies were themselves partly a product of a yield environment that had already stopped making sense. As of early April, Aave was offering 2.61% APY on USDC deposits, below the 3.14% available on idle cash at Interactive Brokers, a traditional financial brokerage. The risk premium that historically justified DeFi’s complexity and smart contract exposure had largely disappeared. With organic yield insufficient, leverage filled the gap, and that concentration is what made the rsETH contagion as damaging as it was. Data from DefiLlama shows that reETH balances on Aave had grown rapidly in the weeks leading up to the exploit, reaching nearly 580,000 tokens ($1.3 billion), evidence that the leverage buildup made the subsequent unwind so sharp.

Crypto has survived worse

The phrase “DeFi is dead” gets wheeled out after every hack because the failures are visible and immediate, while the recovery is slower and less cinematic. But crypto has seen worse. Terra collapsed and vaporized confidence across the sector. Wormhole and Ronin lost roughly $1 billion each. Multichain unraveled.

“DeFi didn’t die when Terra collapsed and caused billions in liquidations and losses,” wrote a pseudonymous trader on X. “DeFi didn’t die when Wormhole and Ronin got drained for around $1 billion. DeFi didn’t die when Multichain bridge assets were stolen.”

More recently, Bybit suffered what was widely described as the largest crypto theft on record, losing around $1.5 billion last February, yet it continued operating, processed a surge in withdrawals, restored reserves and still handles billions of dollars in trading volume each day.

The repricing of trust

0xNGMI, founder of DefiLlama, told CoinDesk the losses are significant but unlikely to be existential. “Aave has many recourses to cover the loss, including its treasury and taking loans, and I think those will have to be used to protect the protocol,” he said. “Overall a significant loss but one that will be recovered. The biggest issue will be the impact on risk premiums that are assigned to DeFi.”

Those risk premiums are a real and lasting cost. Capital will demand more compensation for sitting in onchain systems whose attack surface now extends beyond code

Still, repricing is not the same thing as collapse. “Some of the money will come back,” 0xNGMI said. “We saw this before in Aave when rumors of a hack appeared. It’s always the best strategy to withdraw and redeposit later as the cost of that is tiny and the reward very large.” Some deposits will not return, but historically deposit outflows during stress events reverse as conditions stabilize, as evidence after Terra’s collapse in 2021.

There is also evidence that capital is not simply leaving DeFi. It is rotating. Spark offers one example. Spark’s strategy lead, who goes by monetsupply.eth, said the protocol delisted rsETH and other low-utilization assets in January, a move that may have cost it business and ETH-looping activity to Aave at the time. Under current conditions, however, SparkLend still has ample ETH withdrawal liquidity while Aave is experiencing shortages across several markets. Over the weekend Spark TVL jumped from $1.8 billion to $2.9 billion, demonstrating clear capital rotation.

The more interesting critique, raised by some builders after the exploit, is not that DeFi failed but that it has become too timid. If the sector is going to ask users to bear infrastructure risk, smart contract risk and governance risk for low single-digit yields, the product set starts to look less compelling. With that in mind, Kelp is not the end of DeFi. It is a wake-up call for builders to build safer systems while continuing to offer real world use cases.

Quick Summary

- SIMO shares climbed 8.07% as traders positioned themselves before the company’s Q1 2026 earnings announcement on April 28

- Wall Street expects Q1 revenue to reach $299.4 million with earnings per share of $1.31

- The stock’s momentum reflects strong AI data center appetite for SIMO’s PCIe Gen5 SSD controller technology

- Analysts have increased full-year 2026 EPS projections by 3.58% to $5.78 over the last two months

- Shares have skyrocketed 222.3% in the past year, significantly outperforming the sector’s 157.6% increase

Silicon Motion (SIMO) experienced an 8.07% surge on Thursday as market participants bought into the stock in anticipation of its Q1 2026 financial results, set for release on April 28.

Silicon Motion Technology Corporation, SIMO

The upward movement reflects growing confidence in demand for the company’s solid-state drive controllers, especially from hyperscale data centers focused on artificial intelligence applications.

Analyst consensus from Zacks projects Q1 revenue of $299.4 million alongside earnings of $1.31 per share. Looking at the full year, 2026 EPS forecasts have been upgraded 3.58% during the past 60 days to reach $5.78, while 2027 projections jumped 8.75% to $7.83.

Silicon Motion has exceeded earnings forecasts in three of its previous four quarterly reports, posting an average positive surprise of 23.34%. The single miss occurred in the most recent quarter, falling short by 2.33%.

A broader semiconductor sector rally contributed additional momentum to the stock. Chipmakers have attracted renewed investor attention as spending on AI infrastructure continues accelerating.

Gen5 Technology and Enterprise AI Storage Expansion

Earlier this quarter, Silicon Motion unveiled the SM8008 — an advanced SSD controller manufactured using TSMC’s 6nm technology. The chip specifically targets enterprise data center applications and aims to reduce energy consumption while delivering consistent performance under demanding AI processing conditions.

The company is strategically aligning itself with NVIDIA’s initiative to utilize NAND flash storage as an active memory tier within AI computing systems — a development that could substantially broaden the total available market for SSD controller solutions.

Its MonTitan enterprise controller family directly addresses the AI data center storage sector, a market segment viewed as both larger and more profitable than Silicon Motion’s conventional consumer-oriented business lines.

Silicon Motion has also announced that its UFS solution successfully passed compatibility testing on Qualcomm’s Snapdragon Cockpit SA8295P platform, creating new opportunities in the automotive storage market.

Over the trailing twelve months, SIMO has advanced 222.3%, substantially exceeding the industry’s 157.6% appreciation. The stock has outperformed Marvell (MRVL), which posted 188.8% gains, though it lags Western Digital (WDC), which rocketed 903.5%.

Potential Headwinds to Consider

Competitive pressures represent a genuine concern. Marvell maintains a dominant position in enterprise and cloud SSD controller markets. Western Digital leverages vertical integration — developing complete storage systems internally — eliminating dependence on external controllers like those produced by Silicon Motion.

This industry trend toward integrated storage solutions presents obstacles for Silicon Motion’s expansion in particular market segments.

The company additionally confronts macroeconomic and geopolitical challenges. Its Taiwan headquarters introduces political exposure given persistent tensions with China. Supply chain disruptions and cyclical consumer demand patterns in PCs and smartphones contribute additional volatility.

From a valuation perspective, SIMO currently trades at 22.1x forward earnings — exceeding the sector average of 11.8x and surpassing its own historical median of 21.65x.

Zacks presently assigns a Rank #3 (Hold) rating to SIMO, accompanied by an Earnings ESP of 0.00%, indicating their quantitative model doesn’t forecast a definitive earnings beat for Q1.

Silicon Motion has also announced its upcoming quarterly dividend of $0.50 per ADS, payable on May 21, 2026, to investors of record as of May 7.

The Ethereum Foundation has quietly trimmed a portion of its staking exposure just as its cumulative stake edged toward the project’s own 70,000 ETH target. Arkham data shows the foundation unstaked 17,035.326 ETH, valued at about $40 million at the time, by moving wrapped staked ETH (wstETH) into Lido’s unstETH contract. The underlying ETH is expected to be released once the withdrawal queue clears, marking a notable shift in the foundation’s on-chain posture.

Unstaking ETH in Ethereum’s ecosystem is the process of pulling tokens back from the Beacon Chain, where staked ETH is locked to secure the network and earn rewards. A withdrawal request triggers a queuing period, after which funds are released back to the user. In this instance, the foundation’s funds transitioned via the Lido staking liquid wrapper, a move that can obscure immediate liquidity signals while still aligning with a staged exit plan.

Key takeaways

- The Ethereum Foundation unstaked 17,035.326 ETH (roughly $40 million), converting it into wstETH and routing into Lido’s unstETH contract, per Arkham data.

- The move occurs just as the foundation approaches its internal milestone of around 70,000 staked ETH, a target the group has pursued since formalizing staking as a funding mechanism for protocol research and ecosystem grants.

- The foundation has not publicly disclosed a rationale for this particular unstake, prompting market talk about potential liquidity needs or strategic repositioning.

- Governance and neutrality concerns persist: Ethereum co‑founder Vitalik Buterin has warned that large-scale staking by a single entity could complicate neutrality during contentious hard forks, a theme occasionally revisited as staking grows.

- In the DeFi world, the rsETH ecosystem remains under pressure from a recent $293 million restaking platform exploit. Backers have pledged more than 43,500 ETH (about $101 million) in a coordinated relief effort led by Aave and supported by Lido DAO, Golem Foundation, EtherFi Foundation, and Mantle.

Near-70,000 ETH: the staking trajectory and what it signals

The Ethereum Foundation began staking ETH after updating its policy in June 2025. In its own framing, staking and participation in decentralized finance would help fund protocol research, development, and ecosystem grants, aligning the foundation’s activities with long-term network security while fueling broader innovation.

Since February, the foundation has incrementally expanded its position. It started with a modest 2,016 ETH, then added 22,517 ETH in March. Earlier in the month in question, the foundation staked more than 45,000 ETH, pushing total staked holdings to roughly 69,500 ETH—just shy of its internal 70,000 ETH target. That proximity to the goal underscores how the foundation has positioned staking as both a governance and funding mechanism, rather than a purely technical endeavor.

What makes the near-70,000 milestone meaningful goes beyond a headline figure. For supporters, it signals a significant concentration of stake within a single influential actor, potentially affecting governance dynamics and the network’s perceived neutrality in the event of major protocol shifts. Vitalik Buterin has previously warned that large-scale staking by a foundation-like entity could complicate neutrality during hard forks, a consideration that continues to shape discussions about governance and decentralization as staking scales.

Unstaking activity and liquidity considerations

The decision to unstake a sizeable tranche of ETH, especially in a market where liquidity and price dynamics can react to large on-chain moves, invites scrutiny of the timing and intent. By converting the ETH into wstETH and routing it through Lido’s unstETH channel, the foundation may be seeking to manage liquidity risk or to position funds for a potential future deployment without triggering immediate market impact through straightforward sales. The withdrawal queue mechanism means the timetable for full liquidity remains uncertain, introducing a measured exit rather than an abrupt sale.

Analysts will be watching whether any further unstaking follows this episode. If additional withdrawals occur in the near term, traders might interpret them as signals of a broader liquidity plan or a repositioning strategy. On the other hand, a one-off move could reflect a temporary liquidity need or a precautionary rebalancing rather than a strategic pivot.

DeFi response: rsETH relief and broader market implications

Parallel to the staking narrative, the DeFi ecosystem has been navigating the fallout from a major restaking platform exploit. A $293 million incident on the Kelp restaking platform triggered market disruption, with attackers siphoning restaked ETH tokens and leveraging them as collateral to borrow funds. The fallout strained Aave’s lending market and left a sizable amount of bad debt in its wake.

In response, a coalition of DeFi protocols has rallied around the rsETH resilience effort. Backers pledged more than 43,500 ETH, roughly $101 million at the time, in a coordinated initiative dubbed “DeFi United.” The push is led by Aave, with substantial participation from Lido DAO, the Golem Foundation, and additional backing from EtherFi Foundation and Mantle. The objective is to stabilize rsETH and prevent spillover risks from the restaking ecosystem into major DeFi lending protocols.

For investors and builders, the episode underscores a broader theme: the health of ETH’s staking ecosystem and the resilience of restaking derivatives matter for liquidity, collateral quality, and risk management in DeFi. The coordinated response highlights how interoperable infrastructure—staking protocols, liquidity providers, and risk-sharing platforms—needs to function cohesively when stress arrives. It also illustrates the growing importance of governance-enabled collaboration to safeguard the ecosystem during shocks.

What readers should watch next

As the Ethereum Foundation’s withdrawal queue progresses, observers will want to see whether more ETH moves emerge and how management of the unstaking process unfolds. The unfolding path toward the 70,000 ETH milestone will continue to be a barometer for how centralized or foundation-led actions interact with a decentralized network’s long-term security and governance dynamics.

Meanwhile, rsETH stability remains a live concern for DeFi markets. The DeFi United initiative will be watched for liquidity resilience, collateral quality, and any further measures from participating protocols to mitigate systemic risks stemming from restaking disruptions. Market participants should also remain attentive to any regulatory or policy updates that could influence staking incentives, governance rights, or cross-chain risk management.

In aggregate, the episode reflects a broader narrative: as ETH staking scales and restaking ecosystems mature, on-chain actions by major actors will continue to reverberate through liquidity, governance, and DeFi risk management. Until more clarity surfaces from the Ethereum Foundation and the DeFi coalition, investors should monitor not only the size of stake movements but also the transparency of the rationale behind them and the evolving guardrails designed to safeguard network resilience.

Five of the largest US technology companies report quarterly results this week, and the outcomes could push Bitcoin (BTC) and broader crypto markets in either direction, given the unusually tight link between digital assets and Nasdaq equities.

Microsoft, Alphabet, Meta, and Amazon release Q1 figures after the closing bell on Wednesday, April 29, with Apple following on Thursday. Investors are focused on revenue growth, profit margins, and AI capital expenditure plans for the rest of 2026.

Big Tech AI Capex Will Drive the Reaction

Capital expenditure guidance has overtaken headline earnings as the most market-sensitive line item. Meta has targeted $115 billion to $135 billion for 2026, an increase of at least 59% year over year.

Microsoft, meanwhile, is on track to spend roughly $146 billion on AI and cloud infrastructure in fiscal 2026.

Alphabet has maintained a $175 billion to $185 billion capex range. Amazon, by comparison, is planning a $200 billion outlay, more than 50% higher than in 2025.

Combined hyperscaler AI spending is expected to exceed $160 billion this quarter alone.

Bitcoin Tracks Nasdaq More Closely Than Ever

BTC’s average correlation with the Nasdaq 100 climbed to 0.52 in 2025, up from 0.23 the year before. However, the link tightened further in early 2026, with one analyst tracking the rolling correlation at 0.75 in January.

That coupling has already produced direct contagion this year. After Microsoft’s January earnings stoked concerns about AI spending, the stock fell more than 10% in after-hours trading. Bitcoin briefly slipped to about $83,460 the same day.

A repeat of that pattern is possible if any of the five reports disappoint on capex returns. Strong results, by contrast, could lift risk appetite across both equities and crypto markets in the coming sessions.

The post Five Big Tech Earnings Could Decide Bitcoin’s Next Move This Week appeared first on BeInCrypto.

Key Highlights

- First-quarter comparable operating profit surged 54% to €281M, surpassing Wall Street expectations

- Revenue from AI and cloud infrastructure customers increased 49%, with €1B in fresh orders secured

- The company elevated its Network Infrastructure outlook to 12–14% growth and Optical+IP guidance to 18–20%

- Shares reached their highest point since 2010, climbing nearly 7% during Helsinki trading

- Northland lifted its target to $13; major institutional investors including Calamos, Millennium, and Goldman Sachs expanded stakes

The Finnish telecommunications equipment manufacturer reached a 16-year peak in share price following robust first-quarter results, powered by surging demand for AI and optical networking infrastructure.

Comparable operating profit for the first quarter of 2026 reached €281 million, representing a 54% increase from the prior year and exceeding the €250 million analyst consensus. Total net sales hit €4.5 billion, reflecting 4% annual growth.

Earnings per share aligned with the $0.06 Wall Street estimate. Revenue totaling $5.27 billion significantly exceeded analyst projections of $4.59 billion.

Shares climbed nearly 7% during early trading in Helsinki on April 23, marking the highest valuation since April 2010. On the New York Stock Exchange, NOK advanced 1.4% to $10.48 on Friday, within its 52-week trading range of $4.00 to $10.90.

Revenue generated from AI and cloud infrastructure customers expanded 49% during the three-month period. The company secured €1 billion in new AI and cloud contracts, achieving a book-to-bill ratio exceeding 1.0.

Expanded AI Market Opportunity Projections

Nokia updated its addressable market forecast for AI and cloud infrastructure to reflect a 27% compound annual growth rate spanning 2025 through 2028. This represents a substantial increase from the 16% projection presented during its November 2025 investor presentation.

Guidance for the Network Infrastructure division was elevated to 12–14% growth in 2026, versus the previous 6–8% forecast. The Optical and IP segment outlook rose to 18–20%.

The Optical Networks division posted 20% revenue expansion in Q1. Integration of Infinera is proceeding faster than anticipated, and the company introduced an updated product strategy featuring a multi-rail amplifier and modular optical engines.

Chief Executive Justin Hotard noted the organization is “currently tracking somewhat above the mid-point” of its annual comparable operating profit guidance range of €2.0–2.5 billion.

A second indium-phosphide manufacturing facility in San Jose is scheduled to begin production later this year to increase optical component capacity.

Wall Street Upgrades and Institutional Investment

Northland elevated its price objective on NOK to $13 from $10, pointing to accelerating demand for AI optical connectivity solutions. Bank of America upgraded shares to “buy” with a $12.40 target in early April.

The equity currently carries a “Moderate Buy” consensus rating from 17 Wall Street analysts, comprising 10 buy recommendations, 6 hold ratings, and 1 sell rating. The mean price target stands at $8.83, although multiple recent targets have surpassed this benchmark.

Regarding institutional activity, Calamos Advisors expanded its NOK holdings by 28.1% during Q4 to approximately 1.95 million shares. Millennium Management increased its position by more than 6,500% in Q1, adding nearly 2.8 million shares. Goldman Sachs acquired just over 1 million shares in Q1, elevating its total stake to 12.55 million.

The company also increased its quarterly dividend to $0.0468, up from $0.04. The annualized distribution of $0.19 translates to approximately 1.8% yield, with a record date of April 28 and distribution scheduled for May 12.

Executives identified semiconductor supply limitations and extended order cycles as potential near-term headwinds. Fixed Networks revenue declined 13%, reflecting intentional portfolio optimization efforts.

Short interest in NOK increased roughly 24% during April to approximately 68.2 million shares, while the days-to-cover metric remains modest at 0.7.

The company’s market capitalization stood at roughly $60 billion as of Friday’s closing bell, with a price-to-earnings ratio of 65.29.

Spot XRP ETFs recorded a new all-time high in cumulative net inflows after investor demand returned in April.

Summary

- Spot XRP ETFs reached $1.29 billion in cumulative inflows after April demand returned strongly again.

- XRP stayed near $1.43 despite fresh ETF inflows and renewed investor demand this week recently.

- Nearly 35 million XRP left exchanges, raising hopes of lower sell pressure ahead for traders.

Data from SoSoValue showed total net inflows rising to $1.29 billion by the end of the latest business week. The funds added $15.74 million during the week ending April 24. April inflows reached $81.63 million, making it the strongest month for XRP ETFs since December.

XRP ETFs had a strong start after launching in mid-November. The funds quickly crossed the $1 billion mark and avoided net outflow days for nearly two months.

That trend changed in March as market uncertainty pushed some investors away from risk assets. March became the first negative month for XRP ETFs, with more than $31 million leaving the products.

The return of inflows followed easing geopolitical tension linked to the US-Iran ceasefire. The week ending April 17 recorded the highest weekly net inflow in three months.

XRP price fails to follow ETF demand

XRP has not matched the renewed demand for spot XRP ETFs. The token recently faced rejection near $1.46 after earlier failing to hold a move toward $1.60.

At the time of the report, XRP traded near $1.43. The price showed little change from the previous week, despite fresh ETF inflows and stronger market interest.

Market analyst Crypto Tony described XRP’s recent price action as “boring few months.” The token has traded between $1.20 and $1.60 for more than 60 days.

Exchange outflows raise rally hopes

XRP also saw large exchange outflows in the latest market data. Nearly 35 million XRP reportedly left exchanges within 24 hours, marking the sixth-largest outflow this year.

Some analysts view large exchange withdrawals as a possible sign of lower sell pressure. Similar spikes in February and March came before 20% to 50% XRP rallies, according to the report.

However, XRP still needs a clear breakout above its recent range to confirm stronger momentum. Analyst Ali Martinez has offered a more bullish long-term view, but said XRP could first drop toward $0.90 before any larger move.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Crypto World

BWX Technologies (BWXT) Stock Expands Nuclear Capabilities with Precision Components Acquisition

Key Takeaways

- On April 20, BWX Technologies revealed plans to acquire Precision Components Group (PCG), a specialized US manufacturer of heavy-walled components and heat-transfer equipment.

- This acquisition brings more than 500,000 square feet of domestic heavy-manufacturing infrastructure and over 400 skilled workers into BWXT’s operations.

- PCG recorded approximately $125 million in annual revenue and will integrate into BWXT’s Commercial Operations division.

- BWXT exceeded fourth-quarter projections, delivering EPS of $1.08 compared to the anticipated $0.91, alongside revenue of $885.8M versus the $837.5M forecast, with FY2026 EPS guidance projected between $4.55 and $4.70.

- Institutional investors control approximately 94.39% of shares, with Alkeon and Invesco notably expanding their holdings, while company insiders offloaded roughly 13,327 shares valued at $2.73M during the past 90 days.

BWX Technologies (NYSE: BWXT) is strategically expanding its commercial nuclear operations through the acquisition of Precision Components Group.

Revealed on April 20, this transaction will incorporate PCG along with its operating subsidiaries—Precision Custom Components and DC Fabricators—into BWXT’s organizational structure. PCG will become part of BWXT’s Commercial Operations division while maintaining operations at its current production sites.

According to BWXT, this strategic move delivers more than 500,000 square feet of domestic heavy-manufacturing infrastructure. The acquisition also integrates a highly trained workforce exceeding 400 employees.

PCG generated approximately $125 million in annual revenue, representing a substantial addition to BWXT’s financial performance. Company leadership positions this acquisition as an initial phase in expanding domestically-based commercial nuclear manufacturing capabilities.

According to John MacQuarrie, President of Commercial Operations at BWXT, the deal “builds on BWXT’s strong performance in the commercial nuclear industry” and addresses “the accelerating needs of US commercial nuclear customers.”

Robust Financial Performance Supports Expansion

BWXT entered this acquisition from a position of financial strength. The company surpassed analyst projections in its latest reporting period, delivering EPS of $1.08 versus the consensus estimate of $0.91. Revenue reached $885.8 million, exceeding the anticipated $837.5 million.

This revenue represented an 18.7% increase compared to the previous year, and across fiscal 2025, BWXT achieved 18% total revenue growth to $3.19 billion. Earnings per share expanded 20% during the same timeframe with a net profit margin of 10.3%.

Looking ahead to FY2026, management established EPS guidance ranging from $4.55 to $4.70. Market analysts maintain a consensus “Moderate Buy” recommendation with an average price target of $207.60.

BWXT stock commenced trading Friday at $223.54, positioned above both its 50-day moving average of $211.42 and its 200-day moving average of $198.99. The stock trades within a 52-week range spanning $102.42 to $241.82 and maintains a market capitalization of $20.48 billion.

The company also incrementally increased its quarterly dividend from $0.25 to $0.27, equating to an annualized $1.08 with approximately 0.5% yield.

Institutional Investors Maintain Strong Presence

Institutional stakeholders control approximately 94.39% of BWXT shares. Multiple major investment firms expanded their positions during recent quarters. Alkeon Capital Management increased its holdings by 163% in Q3, accumulating over 1.57 million shares valued at roughly $291 million. Invesco boosted its stake by 60.1% to surpass 2.5 million shares.

B. Metzler seel. Sohn & Co. AG established a new position during Q4, acquiring 9,481 shares worth approximately $1.64 million.

Conversely, company insiders reduced holdings by roughly 13,327 shares totaling $2.73 million throughout the previous 90 days. CAO Kevin James Gorman divested 1,344 shares in early March at an average price of $214.71. Insider ownership currently represents about 0.60% of total shares.

Regarding analyst perspectives, Wells Fargo launched coverage with an “underweight” designation and $200 price objective. TD Cowen assigned a “buy” rating with a $230 target. Zacks Research elevated BWXT from “hold” to “strong-buy” status in January.

BWXT maintains its position as the exclusive provider of naval nuclear reactors for US submarines and aircraft carriers, having manufactured over 400 naval reactors since the commissioning of the USS Nautilus.

Elon Musk’s $134 billion lawsuit against OpenAI, Sam Altman, and Microsoft goes to trial Monday in federal court in Oakland, California, after the billionaire dropped his fraud claims days before jury selection.

US District Judge Yvonne Gonzalez Rogers approved Musk’s request Friday to narrow the case from 26 original claims down to two surviving counts of unjust enrichment and breach of charitable trust.

A Trial Years in the Making

Musk filed suit in November 2024 after donating roughly $38 million in seed funding to OpenAI. It launched as a nonprofit research lab in 2015.

He alleges Altman and co-founder Greg Brockman induced that backing with explicit promises that the organization would never pursue commercial profit.

OpenAI later restructured into a capped-profit entity and accepted more than $13 billion from Microsoft. The shift, Musk argues, enriched insiders at the expense of early donors and the public mission they were told they were funding.

In February 2025, Musk led a $97.4 billion consortium bid to take control of OpenAI’s nonprofit arm. Altman rejected the offer publicly.

What the Jury Will Decide

The trial examines whether OpenAI and Microsoft were unjustly enriched by the company’s shift to a for-profit model. It also focuses on whether OpenAI breached the terms of its original charitable mission. The second claim accuses Microsoft of aiding and abetting.

If Elon Musk prevails, his attorneys have asked that any damages flow to OpenAI’s charitable arm rather than to him personally.

Musk is separately pursuing an antitrust case against Apple and OpenAI and continues to develop xAI as a direct rival to Altman’s company.

Jury selection begins Monday morning before Judge Gonzalez Rogers, who previously presided over the Epic Games antitrust case against Apple. The proceedings are expected to expose internal communications between Musk, Altman, and Brockman from OpenAI’s earliest years.

The post Elon Musk’s $134 Billion OpenAI Fight Heads to Trial appeared first on BeInCrypto.

The real-life “Big Short” and the 2008 financial crisis | 60 Minutes Full Episodes

‘I’ve returned to Oldham after eight years – it’s a town running out of patience and hope’

Netanyahu’s biggest rivals join forces for Israel’s next election

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

The real-life “Big Short” and the 2008 financial crisis | 60 Minutes Full Episodes

COMPLETE Financial Modeling Masterclass 2025! | Ft. Peeyush Chitlangia | KwK #202

Imbecile Knocked Her Up, Now She’s F*cked | Financial Audit

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread – Corporette.com

-

Entertainment7 days ago

NBA Analyst Charles Barkley Chimes in on Ice Spice McDonald’s Fiasco

-

Crypto World21 hours ago

Crypto World21 hours agoHyperliquid $HYPE Rally Builds Momentum as AI Sector Enters Prove-It Phase

-

Politics6 days ago

Politics6 days agoGary Stevenson delivers timely reminder to register to vote as deadline TODAY

-

Crypto World6 days ago

Bank of Hawai’i (BOH) Q1 2026: Net Income Drops to $57.4M as Net Interest Margin Expands

-

Politics4 days ago

Politics4 days agoMaking troops accountable for war crimes threatens US alliance, ex-SAS colonel warns

-

Politics4 days ago

Politics4 days agoDisabled people challenge government SEND proposals over segregation concerns

-

Business4 days ago

Business4 days agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Politics4 days ago

Politics4 days agoZack Polanski responds to home secretary’s taser threat

-

Politics4 days ago

Politics4 days agoStarmer handler McSweeney to be dragged from shadows by Foreign Affairs Committee

-

Sports3 hours ago

Sports3 hours agoIPL 2026: Ruturaj Gaikwad registers slowest fifty of the season, enters all-time unwanted list | Cricket News

-

Politics4 days ago

Wings Over Scotland | How To Get Away With Crimes

-

Crypto World5 days ago

Crypto World5 days agoFive Value Stocks with Recovery Potential in 2026: PayPal (PYPL), Nike (NKE), and More

-

Crypto World5 days ago

Crypto World5 days agoNew York sues Coinbase, Gemini over prediction market offerings

-

Politics4 days ago

Politics4 days ago‘Iran is still a nuclear threat’

-

Sports4 days ago

Sports4 days agoTim Bradley names the current best in the world: “Better than Inoue and Usyk”

-

Business4 days ago

Business4 days agoHCL Tech share price tank over 9% after weak Q4. JPMorgan, HSBC & 3 others cut target price

-

NewsBeat8 hours ago

NewsBeat8 hours agoLK Bennett closes all stores after entering administration

-

Crypto World5 days ago

Crypto World5 days agoCrypto’s great hope in Senate’s Clarity Act still has a path to survive tight calendar

-

Business4 days ago

Business4 days agoThe Job Benefits Most Men Don’t Know to Negotiate

You must be logged in to post a comment Login