Crypto World

Cato urges US to scrap crypto capital gains tax to boost competition

The Cato Institute, a prominent US think tank, is urging policymakers to rethink capital gains taxation on Bitcoin and other cryptocurrencies. In a new policy note, researcher Nicholas Anthony argues that removing or reshaping capital gains taxes could unlock cheaper, more competitive money by reducing the tax distortions that currently incentivize long-term holding and heavy reporting requirements.

Anthony suggests the simplest option might be to eliminate capital gains taxes on crypto entirely. As an alternative, he outlines measures that would exempt crypto and foreign currency transactions when used to purchase goods or services, aiming to “take the government’s thumb off the scale and let competition be the true decider of the best money.” He emphasizes that a tax regime that treats everyday crypto spending like ordinary taxable events can undermine the practical use of digital assets as a means of exchange.

Key takeaways

- Policy proposal: The Cato Institute recommends either scrapping capital gains taxes on crypto entirely or exempting crypto transactions used for everyday purchases from CGT to foster competition among money-like assets.

- Tax burden for users: The note highlights how even simple, routine crypto spending can trigger complex tax filings, deterring everyday usage and broader adoption.

- Alternative approaches: A de minimis tax threshold is proposed as another option to limit CGT triggers unless gains exceed a defined amount.

- Adoption signals: Recent data show growing real-world use of crypto for goods and services, underscoring the potential market impact of tax policy reforms.

Rethinking the tax kernel of crypto spending

The policy paper frames capital gains taxes as a friction point for crypto’s evolution from speculative asset to currency. Anthony notes that when individuals buy daily items, such as coffee, with crypto, the IRS-like framework can convert a routine transaction into a complex tax event. He stresses that while Bitcoin and other digital assets have gained practical use, the tax code has not kept pace, creating unnecessary reporting burdens for compliant users.

Anthony’s reasoning aligns with a broader critique circulating among crypto researchers: tax policy should reflect the functional realities of digital currencies as both stores of value and mediums of exchange. By removing or narrowing CGT exposure, proponents argue, the United States could reduce compliance costs for ordinary users, drive greater merchant adoption, and enhance global competitiveness in a landscape where several jurisdictions are actively adjusting crypto tax rules to attract activity and investment.

“Bitcoiners know the frustration of tax season all too well. It’s never been easier to use Bitcoin as money. Yet, at the same time, the tax code puts an incredible burden on law-abiding citizens. Something as simple as buying a cup of coffee every day with Bitcoin can result in more than 100 pages of tax filings.”

The note adds that eliminating CGT entirely would be the most straightforward route, but it also acknowledges practical concerns, such as how to structure exemptions without creating loopholes or excessive compliance challenges. An interim path—removing CGT on crypto purchases of goods and services—could be more politically feasible but would still require robust systems to verify eligible transactions and prevent abuse. A de minimis threshold, where gains are ignored unless they surpass a specific limit, is presented as another approach that could balance simplicity with tax integrity.

Context, costs, and what could change next

The Cato Institute’s position sits within a long-running debate about how best to classify and tax digital assets. The policy note stresses that many Americans already use crypto in everyday life, and the current tax framework often complicates routine spending more than it incentivizes long-term investment. This tension matters not just for individual taxpayers, but for merchants, exchanges, and developers seeking to build crypto-aware ecosystems that function like mainstream payment rails.

Anthony has a track record of engaging lawmakers on crypto policy. The institute has historically argued for policies aimed at reducing unnecessary regulatory frictions, and this latest report continues that stance by centering tax design as a lever for broader crypto adoption. While the note does not propose immediate legislative milestones, it invites policymakers to consider how tax rules could better align with the practical realities of digital money, potentially spurring more competition among payment methods and currencies.

From a market perspective, the implications could be meaningful if tax changes reduce perceived friction around crypto usage. Investors and builders may watch how lawmakers respond to these arguments, particularly in an environment where tax policy remains a primary channel through which government policy shapes crypto activity. The balance to strike is clear: preserve tax integrity while removing unnecessary barriers to use and innovation.

Early signals about real-world crypto usage reinforce the conversation. A 2025 survey from the National Cryptocurrency Association found that 39% of US crypto holders reported using crypto to purchase goods and services. Meanwhile, academic data compiled by Springer Nature indicate roughly 11,000 merchants worldwide accept Bitcoin as payment, illustrating that the flow of crypto into everyday commerce is not merely theoretical. These numbers suggest that any policy shift could have a tangible impact on consumer behavior and merchant acceptance, potentially widening the circle of everyday crypto users.

Beyond the United States, the debate on crypto taxation is part of a broader international trend. Some policymakers argue that tax rules should be simpler and more predictable to reduce compliance costs and uncertainty, while others warn against eroding fiscal bases or creating gaps that could invite abuse. The Cato paper contributes to this ongoing conversation by centering the tax treatment of crypto as a practical driver of adoption and a determinant of how competitive a country’s money system can be.

What to watch as the debate evolves

Readers should monitor potential legislative developments or regulatory proposals that reflect this shift in thinking. If a framework that lightly taxes or exempts crypto transactions gains traction, it could influence not only consumer behavior but also the operating models of wallets, exchanges, and merchants seeking to optimize payment flows. On the flip side, any move to preserve or tighten CGT could sustain the existing friction that incentives buy-and-hold strategies over active use.

As the policy discussion unfolds, market participants and observers will be watching for concrete proposals, transitional rules, and how enforcement and reporting would be handled under new regimes. The central question remains: can tax policy reshape crypto usage in a way that strengthens competition and broadens access without eroding fiscal safeguards?

What remains uncertain is the precise design of any reform and how it would interact with state taxes, international tax agreements, and evolving regulatory views on digital assets. Still, the debate underscores a growing consensus that the tax treatment of crypto is not just about revenues—it’s a lever that could influence the pace of crypto adoption, the behavior of users, and the strategic choices of builders in the ecosystem.

Investors and practitioners should keep a close eye on policymaker statements, study updates from organizations advocating for tax reform, and assess how changes to CGT could affect demand, merchant acceptance, and the broader competitive landscape of money in the digital era.

Key Highlights

- Palantir is competing alongside Thales and Air Space Intelligence for a major FAA contract to develop AI-driven air traffic control technology.

- Congress has allocated $12.5 billion to the FAA’s modernization effort, though the agency projects it will need approximately $20 billion in additional funding.

- The proposed AI system aims to mitigate airspace congestion and provide early warnings when aircraft proximity becomes concerning.

- On April 10, Wedbush reaffirmed its Outperform stance on PLTR with a $230 price target, dismissing concerns about competition from Anthropic.

- Among 32 Wall Street analysts tracking PLTR, 63% maintain Buy recommendations, with consensus price targets suggesting upside potential exceeding 47%.

The Federal Aviation Administration is undertaking what could become the most significant technological transformation in American aviation infrastructure, and Palantir Technologies is positioning itself as a key player.

A Bloomberg report citing an individual with knowledge of the situation reveals that the FAA has selected Palantir Technologies (PLTR), Thales (THLLY), and Air Space Intelligence as finalists competing to secure a contract for developing next-generation AI-based air traffic control capabilities.

This initiative represents a critical component of the agency’s ambitious plan to upgrade America’s outdated air traffic infrastructure, which has struggled under increasing flight demand and decades of delayed technological improvements.

Palantir Technologies Inc., PLTR

Congressional appropriations have provided the FAA with $12.5 billion toward this modernization campaign. However, agency projections indicate an additional $20 billion will be required to fully execute the transformation.

This substantial financing shortfall amplifies the urgency for implementing innovative, cost-effective technological solutions.

The AI-powered platform under development would deliver multiple operational capabilities. Among the anticipated features: identifying scheduling conflicts when excessive departure or arrival sequences create bottlenecks, enabling air traffic controllers to preemptively address congestion issues.

Additionally, the system would monitor aircraft separation distances and issue alerts when planes venture dangerously close to one another — a critical safety enhancement that could provide controllers with valuable additional response time during high-stress scenarios.

Wedbush Maintains Confidence

Wedbush Securities reiterated its Outperform rating on PLTR on April 10, holding firm at a $230 price target. The investment firm expressed continued optimism regarding Palantir despite market speculation that rivals such as Anthropic might capture market share.

Anthropic has experienced remarkable expansion — its annualized recurring revenue surged from $9 billion to $30 billion since early 2026. Nevertheless, Wedbush maintains that this competitive momentum hasn’t negatively impacted Palantir’s position.

The firm highlighted Palantir’s proprietary AIP platform and its sophisticated data integration capabilities as strategic differentiators that competitors find challenging to duplicate. Wedbush characterized the company as a frontrunner driving the AI transformation rather than a vulnerable target within it.

Analyst Sentiment Overview

Wall Street sentiment toward PLTR remains predominantly optimistic. Among the 32 analysts providing coverage, 63% have issued Buy recommendations.

Consensus price projections indicate potential appreciation exceeding 47% from present trading levels.

According to TipRanks analysis, a Moderate Buy rating emerges from recent analyst activity spanning the last three months: 14 Buy ratings, five Hold ratings, and two Sell ratings. The collective average price target from these analysts stands at $194.06.

PLTR stock was trading 2.54% higher at the time of this report.

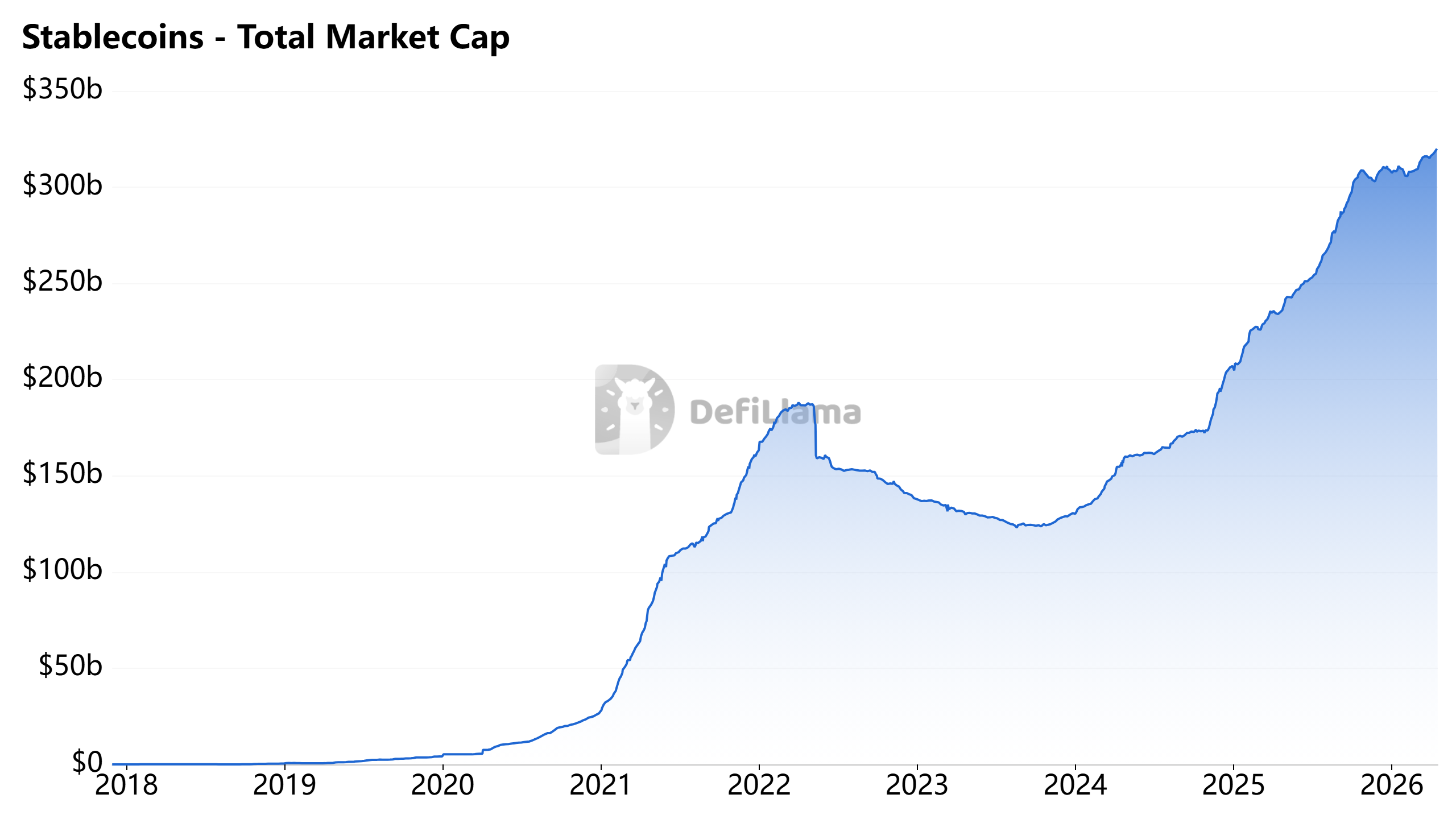

Stablecoins behave like a fragmented foreign exchange market, where liquidity is spread across blockchains and pools, creating price differences and uneven access to dollar liquidity.

Moving stablecoins looks simple on the surface. But under the hood, it’s often a multi-step transaction routed across chains and pools.

“It’s a very special case of a foreign exchange market onchain, and that leads to bad user experience, with unexpected slippage, transaction reversion and unfamiliar information when moving your dollar from point A to point B,” Ryne Saxe, CEO at stablecoin infrastructure company Eco, told Cointelegraph.

Stablecoins now have a market capitalization above $320 billion, led by Tether’s USDt (USDT) and Circle’s USDC (USDC).

But as institutions and large traders enter the market, moving large sums of stablecoins becomes harder to execute cleanly.

Stablecoins aren’t as fungible as they seem

A stablecoin may be pegged to the dollar — or other fiat currencies — but it does not trade as a unified asset, with liquidity split across issuers, blockchains and decentralized finance (DeFi) venues, each with its own depth, pricing and access conditions.

“Stablecoins, between them, aren’t very fungible,” said Saxe. “The different profiles between those markets mean pricing and moving stablecoins seamlessly and efficiently across them is actually a hard problem that people take for granted.”

In practice, a dollar stablecoin on one chain may not be equivalent to the same asset elsewhere. Differences in collateral backing, market access and liquidity depth create pricing gaps that widen with size or in thinner markets.

Those differences are typically negligible in liquid markets and for smaller transactions. But as trades get larger, the gaps become bigger.

“The more major DeFi markets focus on stablecoins, the more chains focus on stablecoins, the more stablecoin assets there are, the more fragmented,” Saxe said. “People think these are just dollars, but they’re actually not.”

In a March report, payments startup Borderless found that pricing divergence in stablecoins depends largely on where liquidity is sourced.

Related: Instant settlement strains crypto’s capital efficiency: Ethan Buchman

The report collected hourly buy and sell rates throughout February across 66 stablecoin-to-fiat corridors — or conversion routes such as USDC to Mexican pesos — covering 33 currencies and seven blockchains. The data showed that USDC and USDT traded almost identically in most cases.

Larger differences emerged at the provider level, where pricing gaps in the same corridor could exceed hundreds of basis points, making execution quality dependent on access to liquidity and routing across venues.

Stablecoins become harder to move at size

As stablecoins currently stand, their market structure resembles foreign exchange, where dollar proxies circulate across disconnected markets, according to Saxe. That becomes more visible in larger stablecoin movements across chains.

Stablecoins have become a centerpiece for institutions moving into digital assets, used for trading, cross-border payments and onchain treasury management. Firms rely on them to move capital between venues, settle trades and access yield opportunities across DeFi markets.

Related: Why yen stablecoins are key to Japan’s crypto ambitions

Unlike retail users, institutions often move tens of millions of dollars at a time, where execution needs to be fast, predictable and efficient.

“If liquidity is spread out, trying to sell $10 million of one stablecoin and buy $10 million of another in a single step will move the market,” Saxe said. “What usually needs to happen is breaking that transaction into multiple branches, which may route differently and converge at the destination.”

In such cases, fragmentation becomes a constraint. Instead of drawing from a single pool of dollar liquidity, institutions must navigate multiple chains, issuers and venues, each with different liquidity conditions. Moving size can shift prices, require splitting trades and introduce uncertainty into execution.

“Right now, they don’t have the risk management, trust and infrastructure that they need to move or hold a lot of stablecoins at size onchain by default,” Saxe said.

Stablecoins need infrastructure, not more supply

Companies are starting to build infrastructure to address those gaps, but they are doing so from different assumptions about what the problem actually is.

Circle is treating stablecoins as the foundation of a new FX system, where multiple currencies, liquidity providers and settlement layers are connected through shared infrastructure. Meanwhile, Eco focuses on routing and execution, aggregating liquidity across fragmented markets.

Both approaches point to the issue of stablecoins existing across multiple chains or issuers, but the liquidity behind them is distributed and uneven. Moving funds requires interacting with that fragmented liquidity, which introduces pricing differences, routing complexity and execution risk.

“Fragmentation creates more spread between prices, meaning worse execution in many cases. To solve that, you need to read across markets, see the full liquidity picture, even if it’s fragmented, and route across it,” Saxe said.

For institutions, that complexity directly limits how much capital can move onchain. As Saxe explained, stablecoin flows need to become far more predictable before institutions have the risk management and trust required to move or hold large amounts onchain.

BitGo announced that AndX USA LLC has launched its US crypto exchange 2026 entry on top of BitGo’s Crypto-as-a-Service infrastructure, giving the global digital asset platform nationwide operations across all 50 states under an OCC-regulated custody framework backed by $250 million in insurance coverage.

Summary

- AndX, a New York-headquartered AI-native Web3 financial platform that already operates in Turkey, the UAE, India, Brazil, the Philippines, and South Africa.

- The platform runs on BitGo Bank and Trust, National Association, the first federally chartered digital asset trust bank owned by a publicly traded company.

- AndX CEO Viru Raparthi said the partnership enables the company to focus on user-facing innovation including AI-driven trading tools, real-world asset tokenization, and global payment capabilities rather than on core infrastructure.

The US crypto exchange 2026 market is increasingly being built not by companies constructing their own custody and compliance systems from the ground up but by platforms that integrate existing regulated infrastructure through API-driven partnerships. The AndX and BitGo launch is the clearest recent example of that model working at scale.

BitGo’s Crypto-as-a-Service offering provides the technical and regulatory foundation: OCC-regulated custody, transaction monitoring, transfer workflows, and compliance architecture, all delivered through configurable APIs and webhooks. AndX plugs into that stack and focuses its engineering resources on the trading interface, AI-powered tools, and market-facing features that differentiate it with users.

“Crypto platforms shouldn’t have to choose between speed to market and institutional-grade safeguards,” said Frank Wang, BitGo’s managing director and head of fintech. “BitGo’s Crypto-as-a-Service enables partners like AndX to launch and scale secure trading experiences on top of a regulated infrastructure foundation, with API-driven systems designed for reliability, control, and compliance.”

Building a compliant US crypto exchange from scratch requires obtaining money transmission licenses in 46 or more states, navigating a BitLicense application in New York, establishing custody arrangements, hiring compliance and AML staff, and building or procuring surveillance systems, all before a single user trade. For a platform entering the US from an international base, the timeline typically runs 18 to 36 months and requires significant capital.

BitGo’s CaaS model compresses that to the time required for API integration and contract negotiation. BitGo Bank and Trust already holds the regulatory authorizations. Custody insurance of $250 million covers BitGo’s own holdings across the infrastructure, reducing counterparty risk for platform partners. The model has grown alongside the expansion of the US spot ETF market and the incoming CLARITY Act framework, which together are raising the floor of what institutional-grade crypto infrastructure must look like.

What AndX Brings as a Product

AndX describes itself as an AI-native Web3 financial platform combining multi-asset trading, tokenization, cross-border payments, real-time financial intelligence, and what it calls a gamified participation layer into a single ecosystem. It has existing user bases in Turkey, the UAE, India, Brazil, the Philippines, and South Africa.

Raparthi said the company’s goal is to “expand access to financial markets while maintaining the highest standards of security and trust,” framing the BitGo partnership as the mechanism that makes that possible in the US regulatory environment.

Where It Fits in the Market Structure

The AndX launch is one of several moves this week that underscore the consolidation of regulated infrastructure as the competitive moat in the US crypto exchange market. Payward’s acquisition of Bitnomial for up to $550 million this week similarly centered on regulatory licensing and clearing infrastructure rather than user acquisition. As the CLARITY Act moves toward markup, the platforms that arrive at that legislative moment with OCC, CFTC, and state-level regulatory coverage will be structurally advantaged over those that do not, which is exactly what partnerships like AndX and BitGo are designed to provide before the regulatory deadlines arrive.

Key Highlights

- AMZN shares reached their strongest level since November 2025, trading just 1.4% beneath the all-time record close of $254.

- Truist Securities boosted its price objective to $285, forecasting 25% AWS revenue expansion in Q1 fueled by artificial intelligence demand.

- TD Cowen analyst John Blackledge maintained a Buy recommendation with a $300 target, anticipating quarterly results will surpass expectations.

- Consensus estimates project Q1 earnings per share of $1.63 with revenues reaching approximately $177.15 billion, representing 14% annual growth.

- The e-commerce giant announced plans to purchase Globalstar for roughly $12 billion while securing a satellite partnership with Apple.

Amazon’s stock has been quietly building momentum. Shares have finished in positive territory during nine out of the last 10 trading days, posting a remarkable 20% advance throughout April. The year-to-date performance shows an 8.6% increase, with the stock now approaching its historic peak.

Shares inched up 0.3% on Friday to settle at $250.56, marking the highest closing price since November 3, 2025. The company’s all-time closing record stands at $254, representing a gap of less than 1.4%.

As the first-quarter earnings announcement approaches on April 29, analyst sentiment has grown increasingly optimistic. Market expectations point to earnings per share of $1.63, a modest improvement from the $1.59 reported in the same period last year, while total revenues are anticipated to climb 14% to approximately $177 billion.

Truist Securities analyst Youssef Squali elevated his price objective on Friday from $280 to $285, maintaining his Buy recommendation. His forecast calls for AWS revenue expansion of 25% during Q1, representing an uptick from the 23% recorded in Q4. This anticipated acceleration stems from an expanding roster of AI collaborations, including partnerships with OpenAI and Anthropic.

Squali also anticipates North America marketplace revenues will advance approximately 10% on a year-over-year basis, characterizing macroeconomic challenges such as elevated fuel expenses as “manageable” — provided they remain temporary.

Street Sentiment Strengthens Before April 29 Report

TD Cowen’s John Blackledge, who holds a 5-star analyst rating, confirmed his Buy stance with a $300 price objective — suggesting approximately 20% potential upside from present levels. His projections indicate Q1 revenues will marginally exceed consensus forecasts, with operating income landing roughly 4% above market expectations.

Blackledge identifies high-margin advertising services and AWS as the primary profit catalysts, complemented by ongoing improvements in fulfillment operations.

For the second quarter of 2026, his revenue and operating income projections exceed Wall Street consensus by 1.5% and 5% respectively, signaling further AWS growth acceleration.

The broader analyst community maintains a Strong Buy consensus on AMZN, supported by 42 Buy ratings against only 3 Hold recommendations. The mean price target stands at $284.77 — approximately 14% above current trading levels.

During the fourth quarter of 2025, AWS delivered 24% year-over-year revenue growth. Chief Executive Andy Jassy characterized this as the division’s “fastest growth in 13 quarters.” Market observers now anticipate this positive trajectory will extend into Q1.

Space-Based Connectivity Ambitions

Beyond the earnings narrative, Amazon has been actively pursuing strategic transactions. The company revealed on Tuesday its intention to acquire Globalstar at an equivalent price of $90 per share, establishing a total valuation just below $12 billion for the satellite communications provider.

This acquisition positions Amazon to develop its own orbital broadband infrastructure — a sector presently led by Elon Musk’s Starlink network.

Additionally, Amazon finalized an arrangement with Apple to deliver satellite connectivity capabilities for existing and upcoming iPhone and Apple Watch products. This agreement builds upon a pre-existing Globalstar partnership that Apple had previously established.

The S&P 500 index advanced 1.2% on Friday, while the Dow Jones Industrial Average climbed 1.8%. AMZN’s 0.3% gain appeared relatively modest in comparison, though the stock’s sustained upward movement heading into the earnings release has captured significant analyst attention.

The consensus Wall Street price target of $284.77 implies roughly 14% appreciation potential from the stock’s latest closing price of $250.56.

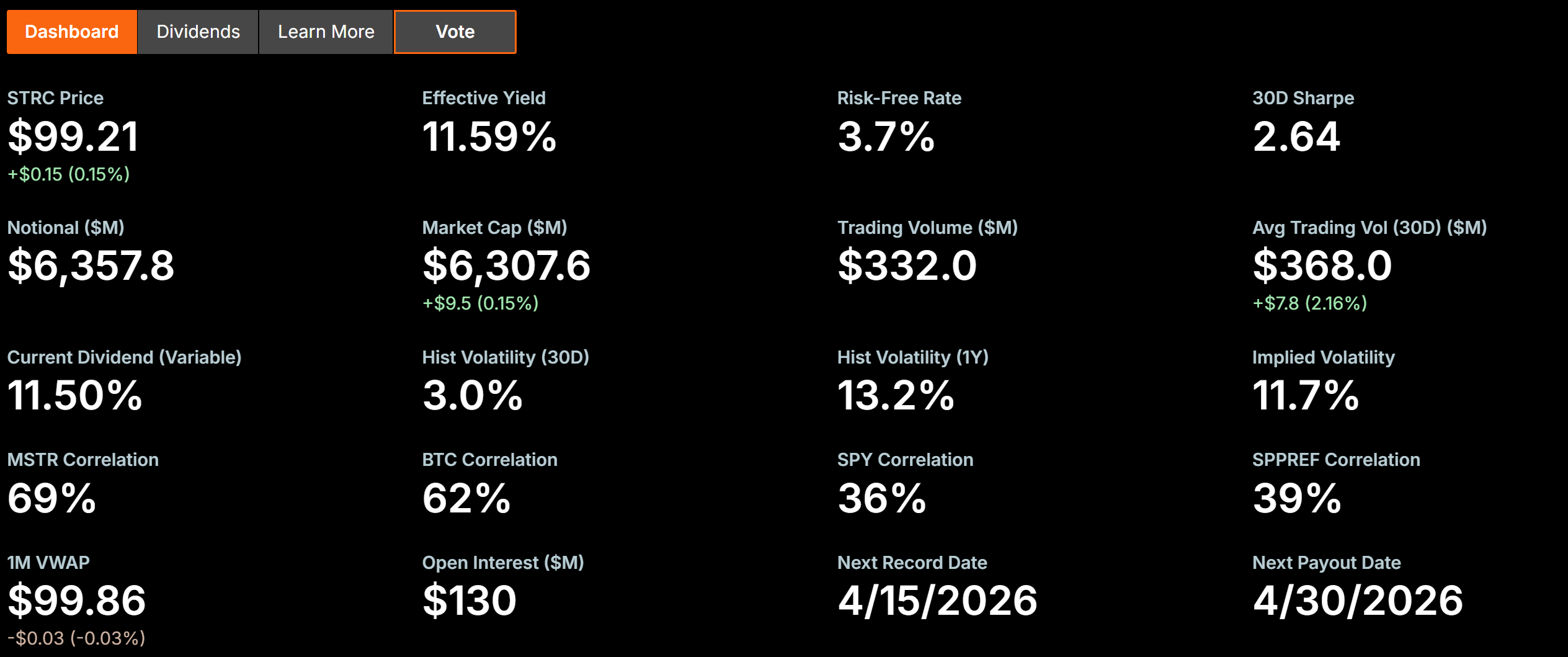

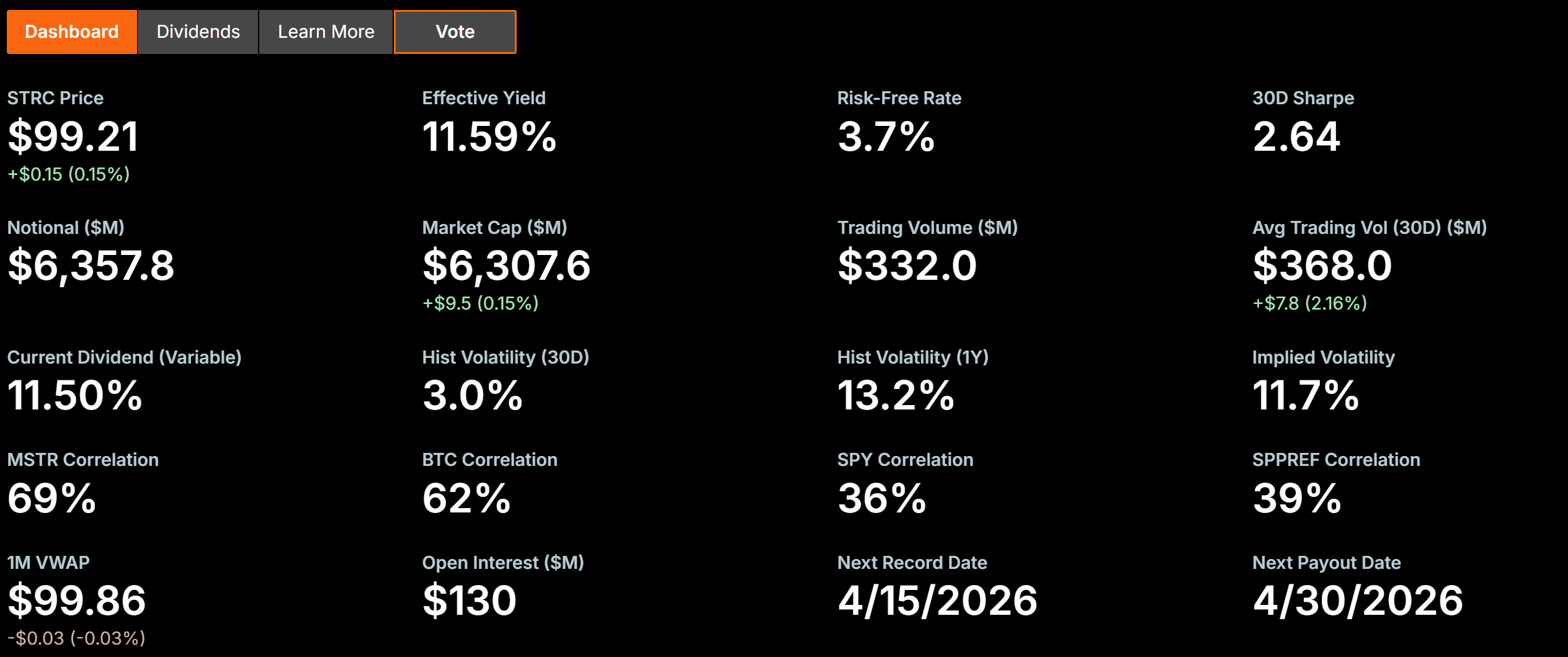

MicroStrategy (now Strategy) has proposed switching its Stretch preferred stock (STRC) from monthly to semi-monthly dividend payments. The change would double payout frequency while keeping the annualized 11.5% rate unchanged.

The company filed a preliminary proxy on April 17, 2026. Shareholders will vote at the annual meeting on June 8.

Why MicroStrategy Wants to Pay STRC Semi-Monthly Dividends

Under the current monthly schedule, STRC experiences predictable ex-dividend price drops. Each cycle creates a dip as holders sell after receiving payments. A recovery follows as buyers chase the next yield window.

Semi-monthly payouts would cut each individual dividend in half. Smaller, more frequent distributions should reduce those swings.

Strategy says the move is designed to stabilize price near $100 par, dampen cyclicality, and improve liquidity.

STRC has already shown declining volatility since its July 2025 launch. The 30-day measure dropped from roughly 13% in its early months to about 2.1% recently.

The stock traded near $99.21 with an effective yield of approximately 11.59%.

What STRC Holders Should Know

If approved, the first semi-monthly record date would be June 30, 2026. The first payment under the new schedule is expected on July 15. Total annual dividend obligations remain identical.

Strategy currently has about $6.35 billion in outstanding STRC notional value. The company uses STRC proceeds to purchase Bitcoin (BTC), adding to its treasury of more than 762,000 coins.

Voting opens around April 28. Shareholders of record as of April 17 can participate through the definitive proxy materials on Strategy’s website.

The post MicroStrategy Pushes 2x Monthly Payouts for STRC Holders appeared first on BeInCrypto.

Wrapped XRP went live on Solana on Friday, issued by custodian Hex Trust and bridged through LayerZero, making the token available inside Solana’s DeFi apps for the first time.

XRP holders can now use the wrapped asset on Jupiter, Phantom, Titan Exchange, and Meteora without selling their underlying position.

Each wXRP is backed 1:1 by native XRP held in segregated custody accounts and is redeemable at any time, according to Hex Trust.

The Solana launch is one leg of a broader rollout Hex Trust disclosed in December 2025, which also targets Ethereum, Optimism, and HyperEVM. The move fits a pattern that has accelerated through 2025 and 2026, where tokens that started their life on one chain are being bridged to others to capture yield and liquidity that did not exist at launch.

XRP has historically functioned as a payment-rail token settled directly on the XRP Ledger. Solana has built the opposite use case, a throughput-optimized smart contract platform where the DeFi and memecoin activity actually lives.

The piece of infrastructure underneath this deal is LayerZero, the cross-chain messaging protocol that has quietly won most of the bridge volume that used to flow through Wormhole, Nomad, and Ronin before those protocols were exploited for more than $1 billion combined between 2022 and 2024.

Whether XRP generates meaningful DeFi volume on Solana is a separate question. The wrapped asset is live, but the test is whether holders actually use it.

Crypto World

co-founder Joseph Lubin warns of the dangers of AI being controlled by a few big tech firms

Crypto’s next major inflection point is coming from artificial intelligence (AI).

That’s according to Consensys CEO and Ethereum co-founder Joseph Lubin. He told CoinDesk that autonomous or semi-autonomous agents can transact, coordinate and verify one another on decentralized networks, using crypto rails as a foundation for machine-driven activity.

Lubin, who will be speaking at Consensus Miami 2026 next month, said he is “sympathetic to the idea that blockchain is for machine intelligences,” but does not see humans being displaced. Instead, increasingly intelligent interfaces will abstract away complexity, allowing users to interact with crypto systems through intent rather than manual inputs. In that model, AI becomes the intermediary layer between people and protocols.

That vision comes with risks. If AI infrastructure remains concentrated among large technology firms, “we could be in trouble,” Lubin warned. He argued that decentralized systems and cryptography will be essential in ensuring accountability, enabling machines to “check on one another” in transparent, verifiable environments.

Within that broader shift, products like MetaMask — a Consensys product — are evolving to reflect the change. Lubin said the wallet is being rebuilt as “a new kind of neobank that you own and control,” part of a transition toward what he described as a “personal money operating system.” AI-powered agents could act on behalf of users, managing assets, executing transactions and navigating a growing decentralized economy. “You can walk around with your personal financial system in your pocket,” he said.

The rise of corporate chains on Ethereum

Beyond interfaces, Lubin pointed to structural changes across the Ethereum ecosystem. The architecture of the blockchain is also shaping how institutions approach adoption. Lubin expects “corporate chains” to become more common as companies seek higher throughput and greater control over their infrastructure. Still, he argued that assets are best issued on Ethereum’s base layer, saying “the best way to ensure that an asset is durable… is to mint it on Ethereum layer one,” even if the asset is later used across other networks.

Stablecoins, one of crypto’s fastest-growing sectors, are part of that transition, but not the endpoint. Lubin described them as a “stepping stone” toward more fully decentralized financial systems, noting that current models remain heavily reliant on centralized issuers. Over time, he expects growth in decentralized collateral to enable more robust, crypto-native forms of money.

On tokenization more broadly, Lubin suggested that traditional finance and decentralized finance are entering a period of convergence, combining centuries of financial innovation with newer blockchain-based systems. The result, he said, will be a more granular and programmable global economy.

Even as these shifts accelerate, Lubin struck a measured tone on longer-term technical risks like quantum computing. While not an immediate concern, he said Ethereum developers have been preparing for years.

“A lot of us just see it as being folded into the natural evolution of Ethereum,” Lubin said.

Read more: Joe Lubin claims DeFi is as safe as traditional finance, adding that bitcoin is in crisis

Poland’s parliament has once again failed to overturn a presidential veto blocking a key crypto regulation bill, extending the political standoff over how the country should oversee digital assets.

In a vote held Friday, lawmakers fell short of the 263 votes required to override the veto issued by President Karol Nawrocki, local outlet TVP World reported. A total of 243 MPs voted against the veto, while 191 supported it, per the report.

The bill, backed by Prime Minister Donald Tusk, aims to align Poland with the European Union’s Markets in Crypto-Assets Regulation (MiCA), introduced in 2024 to govern the issuance and custody of crypto assets. Poland remains the only EU member state yet to implement the bloc’s framework.

Nawrocki has defended his decision, citing concerns over excessive regulation, limited transparency and the potential burden on small businesses, according to the TVP World report.

However, government officials warn that delaying regulation leaves investors exposed. Finance Minister Andrzej Domański reportedly said the absence of clear rules risks turning the market into an “El Dorado for fraudsters,” adding that both consumers and businesses remain vulnerable to abuse.

Related: Zonda exchange says 4.5K BTC wallet inaccessible amid withdrawal crisis

Poland’s crypto bill faces repeated defeats

The failed overturn of the presidential veto marks the second unsuccessful attempt by the government to push the legislation through after a similar rejection in December.

However, despite the failure, Polish lawmakers reintroduced the regulation within days in December last year. They claimed that the new draft was an “improved” version, though critics said it was virtually unchanged from the original.

President Nawrocki vetoed the bill again in February this year. “I will not sign a wrong law just because it was passed again by the parliamentary majority. A wrong law that passed a hundred times still remains a wrong law,” he said at the time.

Related: Poland president vetoes MiCA bill again as crypto companies look to license abroad

Zonda caught in Poland crypto political row

The dispute has also drawn in Zonda, the country’s largest crypto exchange, which has reportedly lobbied against the bill. Tensions escalated after Tusk accused the platform of links to illicit funding, citing intelligence reports that allegedly connect its origins to Russian criminal networks.

“Attempts to drag me and Zonda into the current political squabbles are as absurd as they are harmful to the Polish innovation market,” Zonda CEO Przemysław Kral wrote on X, adding that he is “compelled to take appropriate legal steps to protect my personal rights.”

Last week, he also said he does not control access to a crypto wallet reportedly holding $330 million, which he claims remained with former CEO Sylwester Suszek prior to his disappearance in 2022.

Magazine: Bitcoin may take 7 years to upgrade to post-quantum — BIP-360 co-author

Ethereum’s ether (ETH) continued its ascent, trading near $2,400 after a rally that lifted the token about 38% from a swing low around $1,750. The move appears to be accompanied by a notable shift in on-chain activity and a growing cohort of long-term holders, prompting questions about whether this is a momentum bounce or the start of a structural shift in ETH demand.

On-chain data underpinning the move show a broad set of signals aligning with a more persistent bullish thesis. Daily active addresses surged 89% to 730,278 on April 5, up from 384,763, indicating heightened user interaction with the network as prices moved higher. In accumulation, inflows have intensified since mid-2025, reaching an all-time high of about 1.14 million ETH in November 2025. In 2026, daily inflows have averaged around 200,000 ETH, with a single-day spike surpassing 358,000 ETH on a recent Thursday. The stock of ETH held by accumulation addresses has grown by 6.5 million ETH to 26.16 million from 19.64 million on Jan. 1, a roughly 33% increase, suggesting rising conviction among long-horizon holders.

In parallel, staking dynamics reinforce the longer-term outlook. Data from Dune Analytics indicate that the total value of ETH staked stands at about 39.2 million ETH, reflecting a sizable base of capital committed to Ethereum’s proof-of-stake roadmap. At the same time, the supply of ETH on centralized exchanges has declined to multi-year lows, tightening liquidity on order books and potentially amplifying upside momentum if demand persists.

Key chart patterns point to higher targets

From a technical standpoint, ETH has formed a cup-and-handle pattern that could resume a bullish trajectory. A 12-hour close above the cup’s neckline near $2,400 would keep the uptrend intact, with the measured target defined by adding the cup’s depth to the breakout point approaching around $2,960 — roughly a 22% gain from current levels. A larger, ongoing cup-and-handle formation suggests a more ambitious target near $3,150, about 30% higher than present prices. The relative strength index has risen to around 68, indicating bulls are back in control without the market yet entering overbought territory.

“If the cup and handle pattern continues, I think we get to the golden zone next.”

Analysts have highlighted that this broader formation could signal a substantial move if it remains intact. The Skayeth, a trader known for chart observations on X, has noted that ETH appears to be setting up for a massive move as the pattern unfolds, adding fuel to the bullish narrative for traders watching the cup-and-handle geometry unfold in real time.

In practical terms, bulls will want to defend the $2,350–$2,400 zone to confirm a sustained breakout. If price action can close decisively above $2,400, the path toward higher targets becomes more credible, with market observers pointing to potential moves toward the $2,800 level and beyond toward roughly $3,050 if momentum remains with buyers.

These on-chain and technical signals align with the broader narrative that on-chain accumulation, rising staking activity, and tightening exchange liquidity could underpin a more durable ETH bid in the weeks ahead. The convergence of these data points—sustained address activity, persistent inflows into accumulation wallets, and a sizable stake base—helps explain why many market participants are framing this rally not merely as a bounce, but as part of a broader re-pricing of ETH’s risk premium and growth trajectory.

Still, the path forward hinges on several open questions. Will ETH maintain the breakout above the critical neckline, and how will macro liquidity and regulatory developments influence demand for staking and on-chain activity? While the current data paint a constructive picture, investors should watch for how the pattern holds in the face of shifting market risk sentiment and evolving market structure in the crypto ecosystem.

According to Cointelegraph, a close above the $2,400 level could bolster the case for ETH advancing to around $2,800 and later toward $3,050 if the momentum persists. As such, eyeing the $2,350–$2,400 region for sustained strength will be a key near-term signal for traders assessing risk and potential upside.

What to watch next is whether ETH can sustain a breakout beyond the neckline amid the interplay of on-chain accumulation, staking flows, and macro liquidity. If price action falters, the same signals that foreshadowed the rally—rising DAA, growing accumulation, and a tightening liquidity profile—will be the first to deteriorate and could limit upside in the near term.

Looking ahead, the crucial question remains: can ETH hold above the immediate support zone and carry the momentum into the next phase of the pattern, or will the market retreat test the strengths of the accumulation and staking thesis that underpins this rally?

TLDR:

- XRP’s SuperTrend flip signals a trend shift, with traders watching the $1.55 resistance level closely.

- Spot XRP ETFs lead in AUM, showing stronger investor demand compared to futures-based products.

- Franklin Templeton offers the lowest ETF fee at 0.19%, increasing competition among issuers.

- The XRP ETF market remains open, with no dominant leader as inflows are spread across providers.

XRP is gaining renewed market attention as technical indicators turn positive and institutional products expand. Recent data shows an improving price structure alongside growing ETF activity, with capital flows and fee competition shaping an early-stage market still searching for clear leadership.

XRP Trend Shift Meets Key Resistance

A recent post by Ali Charts noted a change in XRP’s technical outlook. The SuperTrend indicator flipped bullish on the daily chart for the first time since January 17. This shift follows months of sustained selling pressure.

The signal points to a possible trend reversal, although price confirmation remains essential. According to the same update, the $1.55 level stands as the immediate resistance. XRP has struggled to break above this zone in recent attempts.

A clean daily close above $1.55 could open the path toward a relief rally. The projected upside target sits near $1.90 if momentum continues. At the same time, the SuperTrend now acts as a trailing support level.

Price movement across XRP-linked exchange-traded products supports this trend. Most ETFs recorded gains between 1.3% and 2.6% during the same period. This alignment suggests consistent tracking and reflects broader market direction.

While the bullish signal is clear, the resistance level remains a short-term test. Market participants are watching closely for confirmation before positioning for further upside.

ETF Competition Builds as Fees and Structure Shape Flows

Alongside price action, XRP’s ETF ecosystem is expanding with multiple issuers entering the market. The current landscape shows a close race among providers, especially in assets under management.

Bitwise and Canary Capital lead the segment, each managing close to $287 million. Their near-equal standing shows that investor flows are still divided. No single issuer has taken control of the market.

Franklin Templeton follows with about $233.9 million, while 21Shares holds roughly $157.4 million. These firms remain competitive but trail the leading pair. Differences in timing and distribution may explain the gap.

Futures-based ETFs, including Teucrium and Volatility Shares, hold smaller shares of the market. Their assets stand at $114.6 million and $106.9 million, respectively. These products rely on derivatives rather than direct exposure.

Investor preference appears to favor spot ETFs over futures structures. Spot funds provide direct price exposure, which tends to attract long-term capital. Futures products often face higher operational costs.

Fees also play a central role in shaping demand. Franklin Templeton offers the lowest fee at 0.19%, positioning itself aggressively. Bitwise and 21Shares remain in a competitive range at 0.34% and 0.30%.

In contrast, Canary Capital charges 0.50%, while futures products carry higher costs. Teucrium’s fee reaches 1.89%, making it the most expensive option. These differences can influence long-term investor decisions.

The ETF market remains open, with no dominant leader yet. Capital continues to rotate as investors compare cost structures and exposure types. At the same time, participation from established asset managers signals broader institutional engagement.

XRP now sits at the intersection of technical recovery and expanding financial products. Price levels and ETF flows will likely guide the next phase of market direction.

RCB vs DC LIVE Score, IPL 2026: Axar Patel Battles Against Injury, Returns To Bat Despite Pain

Shuttered Startups Are Selling Old Slack Chats, Emails To AI Companies

Man’s mystery death after driving five miles in wrong direction on motorway

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

Jio Financials Q4 Results 2026 | jio financial services latest news, jio financial services share

Arjun Rampal faced 14 flops & financial struggles before making a strong comeback with ‘Dhurandhar’

They Were Burned by a Bad Financial Advisor. Can They Recover?

-

NewsBeat6 days ago

NewsBeat6 days agoPep Guardiola and Gary Neville agree over Arsenal title problem that benefits Man City

-

Crypto World5 days ago

Crypto World5 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Politics6 days ago

Politics6 days agoWorld Cup exit makes Italy enter crisis mode

-

Crypto World5 days ago

Crypto World5 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

Fashion20 hours ago

Fashion20 hours agoWeekend Open Thread: Theodora Dress

-

News Videos3 days ago

News Videos3 days agoSecure crypto trading starts with an FIU-registered

-

Sports1 day ago

Sports1 day agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World4 days ago

Crypto World4 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

NewsBeat4 days ago

NewsBeat4 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Business7 days ago

Business7 days agoIreland Fuel Protests Enter Day 5 as Blockades Spark Shortages and Government Prepares Support Package

-

Politics17 hours ago

Politics17 hours agoPalestine barred from entering Canada for FIFA Congress

-

NewsBeat6 days ago

NewsBeat6 days agoJD Vance announces ‘no agreement’ with Iran over nuclear weapons fear

-

Crypto World15 hours ago

Crypto World15 hours agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Sports6 days ago

Dexter Lawrence, Stefon Diggs, Trading for De’Von Achane

-

Crypto World5 days ago

Crypto World5 days agoTrump whales load up ahead of Mar-a-Lago luncheon.

-

Business2 days ago

Business2 days agoCreo Medical agree sale of its manufacturing operation

-

Crypto World6 days ago

Sei Network Enters Quiet Reset Phase as On-Chain Metrics Signal a Slowdown in 2026

-

Sports5 days ago

Sports5 days agoNWFL opens Pathway for new Clubs ahead of 2026 Season

-

Business5 days ago

Kering slides after Morgan Stanley downgrade, Gucci woes loom

-

Entertainment5 days ago

Entertainment5 days agoKarol G’s ‘Ultra Raunchy’ Coachella Set Gave ‘Satanic Vibes’

You must be logged in to post a comment Login