Crypto World

CFTC Framework Pushes Sports Event Derivatives Ahead of Gambling

The U.S. Commodity Futures Trading Commission has floated a formal rule framework for prediction markets, signaling a cautious but potentially meaningful path toward legitimizing event-based contracts. In the agency’s proposed rules, sports event contracts are not regarded as inherently contrary to the public interest even though federal law classifies gaming as a broad category. The move suggests a nuanced stance: markets that reflect final scores or win-loss records could aid price discovery, while contracts tied to injuries, officiating decisions, or other elements that could invite manipulation are less likely to pass what the CFTC calls a public-interest test.

The CFTC’s draft, released this week, distinguishes sports event contracts from games of pure chance and argues that markets built on verifiable outcomes can contribute to market transparency and price formation. By contrast, contracts that hinge on subjective or manipulable outcomes may fail the test of public interest and could face stricter scrutiny or rejection. The agency’s approach signals a recognition that not all outcome-based contracts are the same, and that the underlying mechanics—how outcomes are determined and settled—will matter as much as the event itself.

The proposal has immediate regulatory implications for platforms that have gained traction in the U.S. prediction-market space, notably Kalshi and Polymarket. Reuters reported that election-focused contracts—central to both platforms during the 2024 U.S. presidential race—are not considered “gaming” under current federal law, a distinction that could ease regulatory uncertainty for such ventures as they expand beyond political bets. The draft rules are open for public comment for 45 days, allowing participants, policymakers, and investors to weigh in before any formal adoption.

The prospect of clearer, principles-based guidance comes at a moment when prediction markets are aggressively positioning themselves as a new, alternative layer of financial information. The industry has already begun to carve out a niche as a form of macro-hedging and data-driven forecasting, attracting interest from traditional finance and media alike.

Gary Kalbaugh, a partner at Cahill Gordon & Reindel LLP, welcomed the proposal’s direction but cautioned that it remains principles-based rather than an outright green light. In his view, each contract would still undergo a case-by-case public-interest analysis under the framework. “Gaming” is defined more broadly than some expect and could sweep in sports events, he noted, yet contracts settling on aggregate outcomes—such as final scores, win-loss records, or season statistics—appear presumptively permissible under the new approach.

Key takeaways

- The CFTC’s proposal frames prediction markets as an asset class that can be lawful if contracts are structured to support price discovery, with sports-based bets treated differently from high-risk, manipulable outcomes.

- Election contracts are not classified as gaming under current federal law, a distinction that could reduce regulatory friction for platforms like Kalshi and Polymarket.

- A 45-day public comment window will shape how regulators, market participants, and lawmakers view the framework and its potential adoption across the U.S. market.

- The rules are intended to be principles-based and contract-specific, meaning a one-size-fits-all approval is unlikely; a case-by-case assessment will determine permissibility.

- Early adoption signs point to growing mainstream interest in prediction markets, with platform partnerships and rising valuations illustrating ongoing institutional engagement.

Regulatory architecture and what changes

The draft marks a shift toward a more nuanced regulatory posture, separating sports-event contracts—where outcomes are typically final and verifiable—from forms of betting that hinge on chance or subjective judgments. In the agency’s view, contracts tied to objective results such as final game outcomes or season stats can contribute to price discovery. This is a departure from a blanket presumption of illegality and implies a more flexible framework that could accommodate a range of contract designs while maintaining guardrails against manipulation or deception.

Analysts and legal experts have underscored that the architecture hinges on case-by-case evaluation under a public-interest standard. The Kalbaugh assessment highlights that the framework’s principles-based nature will require careful scrutiny of each contract’s settlement mechanics, data integrity, and potential for gaming the system. As the CFTC’s proposal invites stakeholder feedback, observers will likely probe how the agency will weigh the balancing act between innovation and investor protection in real-world markets.

Momentum, partnerships, and institutional interest

Even as the regulatory dialogue evolves, the industry’s momentum persists. Prediction markets have increasingly been described as an asset class in their own right, attracting multibillion-dollar valuations for pioneering platforms such as Kalshi and Polymarket. These firms have tapped traditional financial markets to extend their reach and legitimacy. Kalshi has aligned with Nasdaq to launch new categories that enable users to forecast private company valuations ahead of initial public offerings, signaling a bridge between private-market signaling and public market dynamics. Polymarket has pursued a different path, partnering with Dow Jones to weave real-time prediction-market data into its media partnerships, including The Wall Street Journal. The goal appears twofold: deepen market liquidity and provide journalists and investors with data-driven narrative tools that reflect consensus forecasts across a spectrum of events.

Experts see these trends as indicative of broader adoption rather than episodic hype. Georgetown University Law Center professor Melinda Roth noted that prediction markets are becoming more mainstream as partnerships with media and financial institutions expand. The question, she said, is whether event contracts function as recognizable financial instruments or whether they remain closer to speculative bets. Bernstein & Co. has likewise highlighted growing institutional interest, framing prediction markets as potential macro-hedging tools offering binary-outcome payoffs that can diversify risk in a portfolio of macro bets.

For readers watching the regulatory horizon, the combination of clarified rules and expanding market activity creates a nuanced landscape. The CFTC’s proposed framework could lower friction for compliant platforms while preserving guardrails to deter manipulation and abuse. It also underscores a longer arc of regulatory maturation: as the market scales, lawmakers and regulators will be watching how prediction markets interact with traditional financial markets, consumer protection standards, and market integrity mechanisms.

What to watch next

With the public-comment window now open, the next several weeks will reveal how stakeholders respond to the CFTC’s approach. Key questions include how the agency will define and monitor data integrity, what types of contract settlements will be deemed manipulable, and how such markets will interact with existing securities and gaming laws. Investors and users should monitor whether the final rules—potentially refined after public input—create clearer pathways for platform operators to design compliant, price-discovery-focused contracts while guarding against exploitative tactics.

As prediction markets move from an experimental niche to a more integrated part of the financial information ecosystem, readers should stay attuned to how platforms adapt their product designs, data feeds, and regulatory risk management practices. The unfolding framework could shape not only how participants trade today, but how developers, researchers, and media partners leverage these markets to gauge sentiment, forecast events, and inform decision-making in a rapidly evolving landscape.

Strategy reported an $8.33 billion second-quarter operating loss after Bitcoin’s 27% decline this year drove a sharp reduction in the value of its digital asset portfolio.

Summary

- Strategy recorded an $8.32 billion unrealized digital asset loss during the second quarter.

- Its 843,775 BTC were worth $54.77 billion, below their $63.69 billion acquisition cost.

- The company posted an $8.22 billion net loss, equal to $24.45 per diluted share.

- A $3.75 billion dollar reserve provides 2.1 years of preferred dividend coverage under Strategy’s policy.

Strategy’s Bitcoin decline drives $8.33B loss

Bitcoin traded near $64,700 following Strategy’s earnings announcement, down from approximately $88,400 at the end of 2025. That decline left the company’s holdings valued below their aggregate purchase cost.

Strategy recorded an $8.32 billion unrealized loss on digital assets during the quarter, contributing to an operating loss of $8.33 billion. The results reversed the $14.05 billion unrealized gain recorded in the same quarter a year earlier.

The company reported a net loss of $8.22 billion, or $24.45 per diluted common share. Strategy posted net income of $10.02 billion, or $32.60 per share, during the comparable period last year.

Strategy shares were mostly unchanged in after-hours trading following the earnings release, suggesting investors had largely expected Bitcoin’s decline to weigh on the results.

Bitcoin holdings fall below Strategy’s acquisition cost

Strategy held 843,775 BTC as of July 26, an increase of 25% since the start of the year. The position had an original cost of $63.69 billion, including fees and expenses, and a market value of $54.77 billion.

Its average purchase price stood at approximately $75,476 per Bitcoin. With BTC trading near $64,700 after the report, the company’s position was about $10,776 underwater per coin based on its average acquisition cost.

The gap placed the total portfolio roughly $8.92 billion below its original cost. However, the reported quarterly loss was largely unrealized, meaning it reflected changes in Bitcoin’s market value rather than losses from selling the full position.

As crypto.news reported earlier, Strategy made no Bitcoin purchases between July 20 and July 26. Its total holdings remained unchanged at 843,775 BTC during that period.

The company has nevertheless sold approximately $218.4 million in Bitcoin this year to help fund preferred stock dividends. Those sales remain small relative to its overall digital asset reserve but show that Strategy is using part of the portfolio to meet financing obligations.

Strategy raises cash while reducing convertible debt

Strategy’s core software business generated quarterly revenue of $122.4 million, up 6.9% from $114.5 million a year earlier. Gross profit reached $81.6 million, representing a margin of 66.6%.

The company raised $17.06 billion through its capital markets programs during the year and reported a Bitcoin yield of 4.5%. That internal metric measures the change in Bitcoin held per assumed diluted share and does not represent a conventional investment yield.

Strategy also cut its convertible debt by 18% to $6.71 billion after repurchasing $1.5 billion of notes at a discount. The move reduced part of the company’s debt burden as lower Bitcoin prices placed pressure on its balance sheet.

Its U.S. dollar reserve rose by $525 million to $3.75 billion. Strategy said the reserve provides 2.1 years of coverage for preferred stock dividends under its current policy, although the calculation does not guarantee payments under every market condition.

Separate $1 billion repurchase programs have also been established for Strategy’s common shares and digital credit securities. The programs give the company the option to buy back securities but do not require it to use the full authorized amounts.

What the results mean for US investors

Strategy remains one of the largest publicly traded corporate Bitcoin holders, giving U.S. investors indirect exposure to BTC through its securities. Its shares can respond to Bitcoin prices as well as debt costs, equity issuance, preferred dividends and changes in the company’s capital structure.

The second-quarter loss shows how Bitcoin volatility can produce large swings in reported earnings. Strategy moved from a $14.05 billion unrealized digital asset gain a year earlier to an $8.32 billion unrealized loss this quarter.

Its increased cash reserve and lower convertible debt provide additional financial flexibility, but Bitcoin remains below the company’s average purchase price. Further declines could deepen unrealized losses, while a recovery above $75,476 would move the portfolio back above its aggregate acquisition cost.

Strategy (MSTR), the world’s largest corporate bitcoin holder, reported Thursday an $8.2 billion second-quarter net loss after the cryptocurrency’s price decline erased billions of dollars from the value of its digital asset holdings.

The quarterly loss was driven almost entirely by an $8.32 billion unrealized markdown on its bitcoin holdings under fair-value accounting.

The company held 843,775 bitcoin as of July 26, up 25% from the start of the year. At current prices, the stash is worth roughly $54.8 billion, compared with an acquisition cost of $63.7 billion.

The report came after a period of growing investor scrutiny on the firm over whether it can sustain an increasingly complex capital structure built around multiple classes of preferred stock, common equity and convertible debt.

The company raised $17.06 billion through at-the-market stock offerings this year, repurchased $1.5 billion of convertible notes at an 8% discount and expanded its U.S. dollar reserve to $3.75 billion, enough to cover more than two years of preferred dividend payments and interest expenses.

Senate Minority Leader Chuck Schumer has introduced new federal legislation aimed at creating an “Anti-Corruption Bureau” with the power to investigate, enforce, and prevent executive-branch corruption. The proposal also folds into a wider political fight over cryptocurrency ethics and market-structure reform, as Schumer’s remarks directly referenced President Donald Trump’s financial ties to crypto.

According to Schumer’s office, the bill—called the Anti-Corruption Bureau Creation Act—would establish a new agency designed to replace what he described as a fragmented system of oversight bodies. Schumer and cosponsors presented the effort as a targeted response to conflicts of interest they say stem from public office and lucrative crypto-related investments.

Key takeaways

- Schumer introduced the Anti-Corruption Bureau Creation Act, proposing a dedicated US agency to investigate, enforce, and prevent executive-branch corruption.

- The bill’s rationale ties to alleged Trump-linked financial gains, including references to crypto exposure mentioned in Schumer’s Thursday notice.

- Schumer’s proposal would consolidate multiple ethics and oversight functions, grouping entities including the Federal Election Commission and other government ethics offices “under one roof.”

- Supporters position the bureau as a “real teeth” enforcement mechanism, while passage could still face hurdles in the House and Senate—and a potential veto by Trump.

- The timing overlaps with ongoing uncertainty around the Senate’s handling of the Digital Asset Market Clarity (CLARITY) Act, a major market-structure effort backed by many in the industry.

A new enforcement-focused anti-corruption bureau

In a Thursday press notice, Schumer said he introduced the Anti-Corruption Bureau Creation Act. He described the agency as one with enforcement authority, designed to “investigate, enforce, and prevent executive branch corruption.” The legislation also sets out “Congress’ findings” that Schumer claims include disclosures about Trump’s earnings from investments and additional crypto exposure connected to foreign governments through a family fund, as referenced in Schumer’s notice.

Schumer framed the proposal as an institutional fix. In remarks shared through a Public Citizen forum about the bill, he characterized the bureau as having “real teeth” and argued it would help harmonize enforcement across institutions that currently operate with overlapping or inconsistent authority.

The bill’s structure, as described in connection with the forum, calls for a bipartisan group of seven members to be confirmed by the Senate. It also includes mechanisms intended to allow private citizens and state authorities to seek recovery of funds they allege were stolen through corruption, according to descriptions tied to the proposal.

How crypto ethics enters the political equation

For Democrats weighing support for comprehensive crypto market structure legislation, President Trump’s business ties have become a central flashpoint. Many lawmakers, despite White House agreement to certain ethics provisions in the Digital Asset Market Clarity (CLARITY) Act, have argued that the offered safeguards do not fully address potential conflicts of interest.

Earlier coverage from Cointelegraph noted that debates around the CLARITY Act have kept ethics provisions at the center of discussions, with lawmakers saying the measures fall short. Schumer’s new anti-corruption bill adds a separate enforcement pathway to that same broader argument: that oversight should be strengthened to prevent public office from translating into private financial benefit, including in crypto-related business interests.

Consolidating enforcement and ethics offices

A notable feature of the anti-corruption proposal is its intent to gather multiple oversight functions under one organizational umbrella. As described in the coverage, the legislation would place the US Federal Election Commission, the Office of Government Ethics, and the Office of Special Counsel “under one roof” within the new bureau.

Supporters argue the consolidation would reduce the gaps they believe exist across current watchdog systems. Schumer’s messaging emphasized replacing “a broken patchwork of watchdogs” with a single agency capable of acting “anywhere, anytime corruption strikes.” Critics of the current system—particularly those focused on ethics enforcement—often point to jurisdictional complexity and uneven prioritization across agencies; this bill attempts to address that by reorganizing responsibilities rather than relying solely on incremental reforms.

Cointelegraph reported that it reached out to the White House for comment but did not receive an immediate response regarding the proposal.

Cosponsors, vote math, and what happens next

The bill was introduced by Schumer and has cosponsors including Senators Andy Kim, Alex Padilla, and Jeff Merkley. Passage would require Republican support in the House and Senate, where the party holds a slim majority.

Even if it advances before 2028, the president would have veto power. If Trump vetoed the legislation, Congress would need a two-thirds majority in both chambers to override it, according to the rules typically governing federal veto overrides.

The timing is also important because the Senate is approaching a break. As described in the coverage, the Senate had just over a week left before lawmakers planned to leave for a month-long state work period. That looming calendar could affect the speed at which both ethics-related and market-structure measures move in the upper chamber.

CLARITY Act uncertainty persists alongside the anti-corruption push

While Schumer’s anti-corruption proposal targets executive-branch conduct, it arrives in the midst of unresolved negotiations around the CLARITY Act, which many see as a key step toward a clearer US framework for digital assets.

As of Thursday, the Senate had not scheduled a vote on the CLARITY Act, despite pushes from Republican lawmakers and industry stakeholders. Cointelegraph previously highlighted that ethics provisions remain a sticking point for some Democrats, and this week’s status underscores how procedural timing may be just as decisive as policy design.

According to remarks attributed in the coverage to former SEC official John Reed Stark, after a public forum hosted by Senators Richard Blumenthal and Chris Van Hollen, it was unclear whether lawmakers would move the CLARITY Act during the available window. The same report cited statements from Coinbase CEO Brian Armstrong referring to the bill nearing a critical stage, alongside continued advocacy from Senator Cynthia Lummis for a vote.

The political sequence matters for market participants: if crypto market structure legislation is delayed by calendar constraints, lawmakers may re-focus on broader political disputes about ethics and enforcement, potentially reshaping what “safe enough” looks like for legislators and regulators. Conversely, if the CLARITY Act advances, it could clarify the legislative pathway for industry—while leaving ethics and anti-corruption reforms to run in parallel.

For now, investors and builders should watch two developments closely: whether the Senate schedules and votes on the CLARITY Act before its break, and whether Schumer’s anti-corruption bureau proposal gains traction early enough to overcome House and Senate vote hurdles and any eventual veto risk.

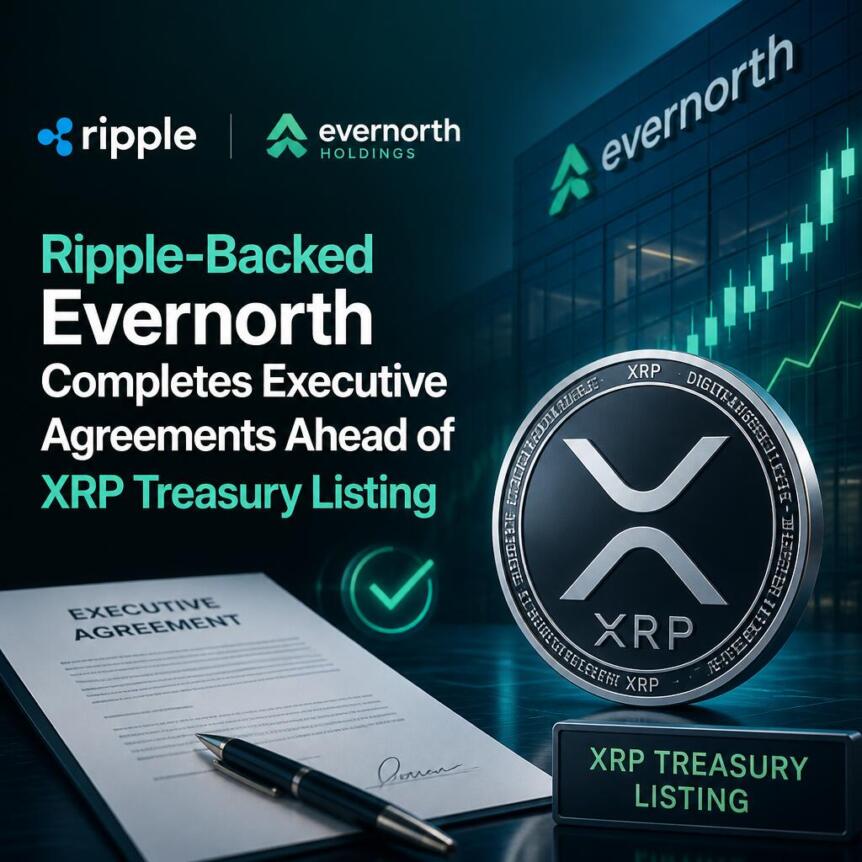

Ripple-backed Evernorth Holdings has advanced its public market plans after updating its SEC registration. The company completed executive employment agreements and submitted another amended Form S-4 filing. Meanwhile, the latest disclosures also outlined compensation packages, merger progress, and financial impacts linked to recent XRP price weakness.

Ripple-Backed Evernorth Completes Leadership Agreements

Evernorth Holdings submitted Amendment No. 5 to its Form S-4 registration statement with the U.S. Securities and Exchange Commission. The filing completed employment agreements for the remaining members of the executive leadership team. As a result, the company has finalized compensation arrangements before its proposed public listing.

The agreements cover Chief Legal Officer Jessica Jonas, Chief Business Officer Sagar Shah, and Chief Operating Officer Meg Nakamura. Each executive will receive a base salary, annual bonus eligibility, employee benefits, and restricted stock units. The compensation packages follow the company’s 2026 Omnibus Incentive Plan.

Jonas received the largest equity award among the newly announced executives. Her initial equity package carries a value of $4.5 million under the agreement. Meanwhile, Shah and Nakamura each received equity awards valued at $2.8 million, subject to shareholder and compensation committee approval.

Evernorth Advances Merger With Armada Acquisition Corp II

The latest filing follows earlier agreements with Chief Executive Officer Asheesh Birla and Chief Financial Officer Matt Frymier. Those agreements already established executive salaries, bonuses, equity awards, and vesting schedules. Consequently, Evernorth has now completed employment terms across its senior leadership team.

The company continues preparing for its planned business combination with Armada Acquisition Corp II. Arrington Capital sponsors the special purpose acquisition company leading the proposed transaction. Following completion, the combined company intends to trade on Nasdaq under the ticker symbol XRPN.

Evernorth has secured more than $1 billion in gross proceeds from strategic backers supporting the transaction. Funding has come from Ripple, Arrington Capital, SBI Holdings, Pantera Capital, and Kraken. The company has also assembled a board featuring senior executives from blockchain, finance, and technology organizations.

Ripple Chief Legal Officer Stuart Alderoty will serve on the board after the merger closes. Other directors include Asheesh Birla, Ted Janus, Robert Kaiden, and Derar Islim. The proposed public company, therefore, combines experienced leadership from digital assets and financial services.

The transaction supports Evernorth’s strategy to establish one of the largest publicly traded XRP treasury companies. Corporate treasury models have gained attention as several firms increase exposure to digital assets. As a result, Evernorth aims to expand institutional participation through a publicly listed structure backed by XRP holdings.

XRP Price Weakness Leads to Impairment Charge

Evernorth also disclosed financial effects resulting from recent XRP market performance. The company reported a $38.4 million impairment tied to declining XRP valuations during the past four months. Consequently, the value of its combined XRP holdings fell to approximately $640 million.

XRP traded between $1.05 and $1.09 during the latest market session. The token changed hands near $1.07 after declining during the previous 24 hours. In addition, XRP has recorded losses exceeding 5% during the past week while trading activity weakened.

Daily trading volume also declined by approximately 10% during the latest session. Market sentiment remained under pressure as regulatory developments continued affecting cryptocurrency prices. Meanwhile, delays surrounding the CLARITY Act added another challenge for digital asset markets.

Armada Acquisition Corp II shares also recorded a modest decline during recent trading sessions. However, the stock maintained its broader year-to-date gains despite the latest movement. At the same time, Evernorth continued progressing toward its planned merger while strengthening executive leadership before entering public markets.

The updated SEC filing marks another milestone in Evernorth’s listing process. Executive agreements, governance appointments, and merger preparations now appear substantially complete. As a result, the company has strengthened its organizational structure before completing its proposed Nasdaq debut and expanding its XRP treasury strategy.

Crypto World

Up 439%, Then Margin-Called: Did Leopold Aschenbrenner’s Situational Awareness Actually Blow Up?

Situational Awareness made 439% in six months. Then margin calls took its entire stock book in one trade. Ken Griffin’s Citadel bought it.

A quarter of that fund’s last reported stock holdings were Bitcoin miners. That was not an accident, and it is why crypto investors are reading this story closely.

Who Is Leopold Aschenbrenner?

OpenAI hired him for its Superalignment team in 2023 and let him go in April 2024. He has said he was pushed out for raising safety concerns.

In June 2024 he published an essay series called Situational Awareness. Its central claim was blunt.

“AGI by 2027 is strikingly plausible,” Leopold Aschenbrenner, in his essay series Situational Awareness, June 2024.

Follow us on X to get the latest news as it happens

AGI means software that matches humans at most tasks. But the essay did more than predict it. One chapter argued the real bottleneck would be physical. Power contracts, transformers and electricity supply, not chips.

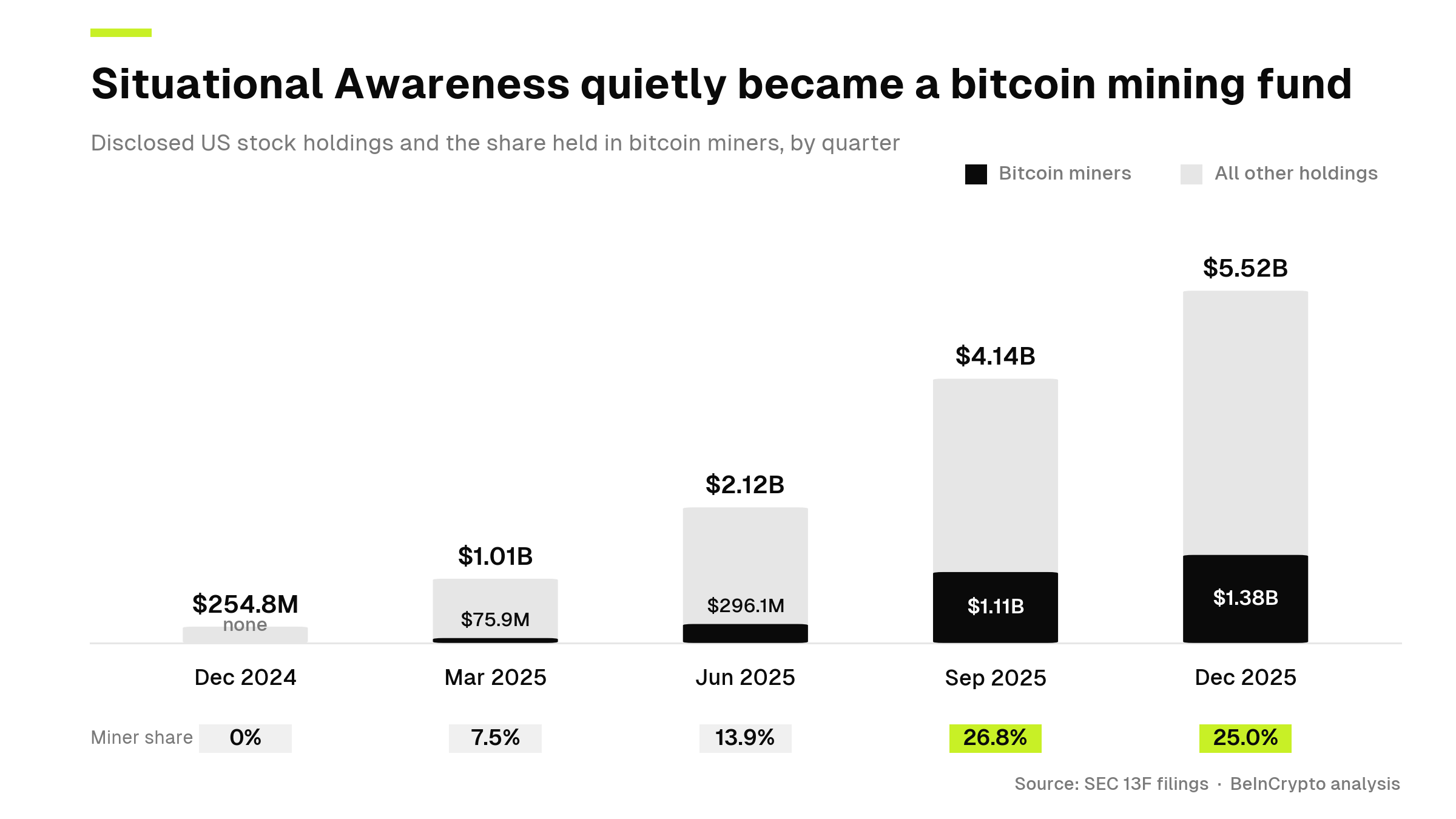

He then built a hedge fund on that idea. Its first stock disclosure, covering December 2024, listed six holdings worth $254.8 million.

Every one was a power or chip company. Not one was crypto. That changed quickly.

What Happened to Situational Awareness This Week

July went badly. The fund owned memory chip makers like SK Hynix, which fell hard in the AI memory stock selloff.

It had also bet against software firms such as Adobe. That trade pays off when a stock drops. Those shares rose instead. The wider market went the same way. The Nasdaq-100 fell 10% from its early June peak.

Borrowed money turned a bad month into a forced one. The fund had used loans to hold more stock than its own cash could cover.

When prices fell, its lenders wanted more money behind those loans. That demand is a margin call.

CNBC named Bank of America, Goldman Sachs and JPMorgan Chase as the brokers involved. It also reported the fund had grown to $45 billion by the start of July.

Then it unwound every public stock position, CNBC said. Griffin’s Citadel hedge fund agreed to buy them. Millennium Management and Jane Street looked and passed, Bloomberg reported.

Where Do Bitcoin Miners Come In?

Crypto readers mostly missed this part. Situational Awareness became one of mining’s larger shareholders, and it happened fast.

Big US funds must list their stock holdings every three months on a form called a 13F. Five exist for this fund. Read in order, they show a bet being built.

The latest filing lists 29 holdings worth $5.52 billion. Miners and their data center arms make up $1.38 billion of it.

Core Scientific was the largest at $418.7 million. IREN came next at $328.6 million, then Applied Digital at $278 million.

Cipher Mining, Riot Platforms, Hut 8, WhiteFiber, Bitdeer, CleanSpark and Bitfarms made up the rest.

The whole disclosed book grew nearly 22 times in a year. The mining share went from nothing to a quarter of it.

So the AGI fund became a mining fund by design. His essay said the bottleneck was power. Miners own power, land and cooling, which is why miners became AI powerhouses.

There is a catch for shareholders. Anyone holding these stocks in July shared the trade with a fund facing margin calls. No mining company knew, so none of them said so.

Did Citadel Engineer This?

One theory spread fast. It says Citadel scared the market about rate hikes, waited for Leopold to break, then bought his stocks cheap.

The first part is true. Frank Flight, who runs macro strategy at Citadel Securities, published a note on July 27. He wrote that he now expected a rate hike at the July meeting.

Bloomberg reported the call added to market nerves. Two days later, a Griffin firm bought the stock book.

Four things break the theory.

- First, there are two Citadels.

Citadel Securities buys and sells stocks for other people. Citadel is the hedge fund. They are separate firms.

- Second, Flight had company.

PGIM and Wrightson ICAP also called for a hike. Bond veteran Harley Bassman wanted one twice as big.

- Third, the fear came first.

Bloomberg tied it to oil prices rising after the US and Iran clashed again, plus a strong job market.

- Fourth, the Fed did not hike.

It held rates steady, and three of its 12 voting members wanted a quarter-point rise.

That last detail matters. It was the first time since September 2016 that three officials dissented in the same direction. The pressure to raise rates was real, and it sat inside the Fed.

What Nobody Can Answer Yet

Did Citadel get a bargain? Nobody outside the deal knows. Neither firm will say what it paid.

Some think the forced selling mattered anyway. On CNBC, Jim Cramer argued it looked like a clearing event that could mark a bottom for the AI trade.

The tape says something simpler. Microsoft reported strong results on Wednesday night and rose about 15%.

Chip stocks jumped the next day. One big chip index rose 6.7% and snapped a five-day losing streak.

One block trade does not move a whole chip index. An earnings report can.

Six days before all of it, Aschenbrenner had told his investors to add money.

“PS. At times we call out opportunities that seem like a particularly good time to add funds, if you have been waiting for one,” Leopold Aschenbrenner, in the July 24 investor letter as reported by the Financial Times.

He got the direction right. He just did not own the stocks anymore.

The fund is not dead. It still holds private stakes, including Anthropic, which filed confidential IPO paperwork on June 1.

Miners spent 10 years being called a curiosity. It took one AI fund’s margin call to make them matter.

The post Up 439%, Then Margin-Called: Did Leopold Aschenbrenner’s Situational Awareness Actually Blow Up? appeared first on BeInCrypto.

Strategy (MSTR), the world’s largest corporate bitcoin holder, reported Thursday an $8.2 billion second-quarter net loss after the cryptocurrency’s price decline erased billions of dollars from the value of its digital asset holdings.

The quarterly loss was driven almost entirely by an $8.32 billion unrealized markdown on its bitcoin holdings under fair-value accounting.

The company held 843,775 bitcoin as of July 26, up 25% from the start of the year. At current prices, the stash is worth roughly $54.8 billion, compared with an acquisition cost of $63.7 billion.

The report came after a period of growing investor scrutiny on the firm over whether it can sustain an increasingly complex capital structure built around multiple classes of preferred stock, common equity and convertible debt.

The company raised $17.06 billion through at-the-market stock offerings this year, repurchased $1.5 billion of convertible notes at an 8% discount and expanded its U.S. dollar reserve to $3.75 billion, enough to cover more than two years of preferred dividend payments and interest expenses.

Amazon shares surged in after-hours trading on Thursday after the company delivered a blowout second-quarter earnings report, beating Wall Street expectations across revenue, AWS sales, operating income, and earnings per share.

The results reinforced investor confidence that Amazon’s massive AI infrastructure spending is translating into accelerating cloud growth and stronger profitability.

Follow us on X to get the latest news as it happens

Amazon Beats Wall Street Across Key Metrics

Amazon reported Q2 net sales of $200.6 billion, comfortably above analyst estimates of approximately $197 billion. The company also posted operating income of $27.46 billion, exceeding expectations of around $23.6 billion, while operating margin expanded to 13.7%, above the expected 12%.

Perhaps the biggest surprise came from earnings. Amazon reported earnings per share of $5.75, far ahead of the consensus estimate of $1.82, highlighting significantly stronger profitability than analysts anticipated.

The earnings release immediately fueled investor optimism, sending Amazon shares from a regular-session close of $235.50 to roughly $251 in after-hours trading, representing a gain of more than 6.5% after the closing bell.

AWS Growth Shows Amazon’s AI Spending Is Paying Off

The strongest signal from the report came from Amazon Web Services.

AWS generated $42.23 billion in revenue during the quarter, surpassing expectations of roughly $40.57 billion. Cloud revenue grew approximately 37% year-over-year, marking AWS’s fastest expansion in roughly 18 quarters.

For investors, AWS remains Amazon’s most closely watched business because it serves as the company’s primary AI infrastructure engine.

Chief Executive Andy Jassy has repeatedly defended Amazon’s aggressive capital investment strategy, maintaining plans to spend roughly $200 billion during 2026 to expand AI data centers, networking infrastructure, and custom silicon capabilities.

The latest earnings suggest those investments are beginning to translate into accelerating customer demand rather than simply higher expenses.

Investors Reward Amazon’s AI Strategy

Heading into earnings, investors questioned whether Amazon could match the strong cloud performance recently reported by Microsoft while justifying its enormous AI capital expenditures.

Instead, Amazon exceeded expectations across nearly every major operating metric.

The combination of stronger AWS growth, expanding operating margins, and better-than-expected profitability eased concerns that AI spending would pressure near-term earnings. Investors instead viewed the results as evidence that Amazon’s infrastructure investments are already supporting faster revenue growth.

Although some of the earnings benefit included non-operating gains, the company’s underlying operating performance remained well ahead of Wall Street forecasts.

What’s Next for Amazon?

Attention now shifts toward Amazon’s second-half execution as management continues rolling out AI infrastructure and expanding AWS services.

Investors will closely monitor whether AWS can maintain its accelerated growth trajectory while Amazon continues one of the largest capital investment programs in corporate history. Future earnings will also provide a clearer picture of whether AI-driven demand can continue supporting margin expansion and justify the company’s long-term spending plans.

If AWS momentum remains intact, Amazon could further strengthen its position in the increasingly competitive AI cloud market alongside Microsoft and Google.

The report also arrives at a pivotal moment for the AI investment race, with Microsoft and other tech giants raising the bar on cloud performance. Amazon’s latest numbers suggest its AI strategy is beginning to generate tangible financial returns.

The post Amazon AI Bet Pays Off as Q2 Earnings Crush Expectations: How Will Stock React? appeared first on BeInCrypto.

When Liz Gumbinner first noticed a twinge in her right shoulder, she assumed she’d pulled a muscle. It was during the pandemic, when many exercise studios were closed, and Gumbinner, a writer who teaches advertising at Boston University, had been doing a lot of yoga and dance at home.

But the pain, mild at first, gradually became excruciating, shooting down her arm whenever she extended it. “We’re talking worse than labor contractions,” she says.

Pretty soon, Gumbinner couldn’t zip up a dress, turn off a light switch on the wall, or even hold hands with her boyfriend. The only way she could sleep was flat on her back with her arms at her sides. “That’s when I realized it wasn’t a pulled muscle,” she says.

A few months later, she was diagnosed with adhesive capulitis, colloquially known as “frozen shoulder,” a condition in which the shoulder capsule—a fibrous sheath which surrounds the joint—becomes thick and inflamed. It usually develops in three phases: the freezing stage, which can last several months and cause severe pain; the frozen stage, during which the shoulder becomes stiffer and difficult to use, often for up to a year; and the thawing stage, when mobility finally begins to improve.

Hyperscale Data has sold about 100 Bitcoin and secured a BTC-backed credit facility to finance construction of its artificial intelligence data center in Michigan.

Summary

- Hyperscale Data sold about 100 BTC to fund construction and equipment purchases.

- Its Bitcoin-backed credit facility carries a variable rate of approximately 4.5% to 5%.

- A 10-year AI services agreement could generate more than $1.2 billion if fully exercised.

- Hyperscale Data retains about 1,006 BTC, ranking 44th among public corporate holders.

Hyperscale Data converts Bitcoin into AI funding

Hyperscale Data disclosed the Bitcoin sale and financing agreement on Thursday as it accelerated work on its Michigan AI campus.

Proceeds from the sale will fund construction and purchases of critical infrastructure and equipment with long delivery times. The company did not disclose the dollar value of the transaction or the lender behind its Bitcoin-backed credit line.

Its new facility is expected to provide financing at a variable interest rate of roughly 4.5% to 5%. The arrangement allows Hyperscale Data to raise additional capital against its remaining Bitcoin rather than selling a larger share of its holdings immediately.

Bitcoin Treasuries data shows the company retains approximately 1,006 BTC after the sale. That position makes it the 44th-largest publicly traded corporate Bitcoin holder tracked by the platform.

Formerly called Ault Alliance, Hyperscale Data adopted its current name in 2024 as it shifted more attention toward AI infrastructure. However, the company has continued operating its Bitcoin mining business.

Michigan AI contract could exceed $3 billion

Construction at the Michigan campus supports an earlier master services agreement with an unnamed AI infrastructure provider. The initial phase covers approximately 20 megawatts of computing capacity.

The agreement has a 10-year term and includes two optional five-year extensions. Hyperscale Data estimates the contract could produce more than $1.2 billion in revenue if the customer exercises all options attached to the initial capacity.

The customer can also request another 32 MW within the first two years. If that expansion proceeds and remains active throughout both extension periods, Hyperscale Data expects the contract’s total value to exceed $3 billion.

These projections depend on the customer taking the available capacity and exercising its extension rights. Hyperscale Data has not identified the customer or provided a final timeline for completing the full 52 MW buildout.

Bitcoin miners expand into US AI infrastructure

Hyperscale Data’s financing decision adds to a wider shift among U.S.-listed Bitcoin miners seeking revenue from AI computing and data centers.

Hut 8 recently signed a second 15-year lease valued at $9.8 billion for its Beacon Point AI campus in Nueces County, Texas. IREN separately announced $2.8 billion in new multi-year cloud contracts and increased its year-end 2026 annualized revenue target to more than $4 billion.

Mining companies already control power connections, land and data center infrastructure that can be adapted for high-performance computing. AI contracts may offer steadier revenue than Bitcoin mining, where income depends on network difficulty, energy costs and the market price of BTC.

The transition is not without risk. Poolin filed for Chapter 11 protection in the U.S. on July 22 with roughly $173 million in prepetition obligations. The Singapore-based mining company and two U.S. subsidiaries plan to sell their Texas assets through a court-supervised process rather than restore the business.

Hyperscale Data’s Michigan investment gives the trend a direct U.S. infrastructure angle while also showing how corporate Bitcoin reserves can serve as a source of construction capital.

GPUS shares rise after financing announcement

Hyperscale Data shares, traded on NYSE American under the GPUS ticker, gained more than 5% in late-morning trading Thursday, according to Yahoo Finance data.

The market reaction followed the company’s financing update and its projections for the Michigan contract. Investors will now watch construction progress, the AI customer’s expansion decision and any further changes to Hyperscale Data’s Bitcoin holdings.

Using BTC as both a saleable reserve and loan collateral exposes the company to Bitcoin price movements while it funds a capital-intensive data center project. Future disclosures on the facility’s collateral requirements and the campus delivery schedule may provide a clearer view of that risk.

This is what makes the current moment so difficult to read. Transitions do not move neatly through the categories we use to manage the world; pressure crosses them, changing role as it goes, and by the time the official language catches up, people may already have been living with the change for years.

The next transition is forming through that movement. It is not an artificial intelligence story alone, or a climate story alone, or a demographic story alone. Each of those matters, but none explains the whole moment by itself. What matters most is how these forces begin to interact, and how much load they place on systems built around older assumptions. When enough pressure moves at once, the operating and organizing logic of an age begins to lose its fit.

Every age has such a logic. Most people do not experience it as a theory. They experience it as the background of life: how work is organized, how families are supported, how knowledge is trusted, how institutions make decisions, how risk is absorbed, and how people are expected to build a life. For a long time, that background can feel natural. Then the world changes around it, and what once made life manageable begins to show its limits.

How ThinkPad designers gaslit IBM to save the iconic TrackPoint

Harlan Coben Says Myron Bolitar May Last Multiple Seasons

US stocks: Microsoft adds $485 billion to investors’ wealth as shares rise 15%. Check why

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Brooks Brothers

-

Sports4 days ago

Sports4 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business1 day ago

Business1 day agoWhy Trees Belong on the Risk Register

-

Tech4 days ago

Tech4 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World5 days ago

Crypto World5 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics3 days ago

Politics3 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Entertainment6 days ago

Entertainment6 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

Politics3 days ago

Politics3 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos4 days ago

News Videos4 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Fashion7 days ago

Fashion7 days ago16 Dresses for the High Summer Event

-

Sports7 days ago

Sports7 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Business2 days ago

Business2 days agoMajor shareholder moves on Canyon

-

Crypto World5 days ago

Crypto World5 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

News Videos9 hours ago

News Videos9 hours agoBitcoin Enters the 3rd Stage of the Bear Market

-

Politics4 days ago

Politics4 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Entertainment2 days ago

Entertainment2 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Tech6 days ago

Tech6 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

Crypto World2 days ago

Crypto World2 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Entertainment5 days ago

Entertainment5 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

News Videos2 days ago

News Videos2 days agoClaude: Build Financial Dashboards in Minutes (2026)

You must be logged in to post a comment Login