Crypto World

Crypto’s banker adversaries didn’t want to deal in latest White House meeting on bill

Crypto industry negotiators arrived at the White House on Tuesday ready to talk about a legislative deal on stablecoin yields, but their banking counterparts brought further demands for a ban on such rewards in the Senate’s crypto market structure bill, according to people familiar with the talks.

The fight over whether stablecoins should be able to offer rewards — a lobbying battle between Wall Street bankers and crypto insiders — is one of the chief headwinds keeping the Senate Banking Committee from advancing the Digital Asset Market Clarity Act. It’s now been a sticking point for months, and the banking side held their ground on prohibiting the rewards activity and more, according to a principles document circulated by the bank negotiators, despite the White House’s insistence last week that both sides come with ideas for compromising.

The document called for a general prohibition on stablecoin yield, according to a copy obtained by CoinDesk, suggesting a ban on “any form of financial or non-financial consideration to a payment stablecoin holder in connection with the payment stablecoin holder’s purchase, use, ownership, possession, custody, holding or retention of a payment stablecoin.”

The crypto team at the table was said to include executives from Coinbase, Ripple, a16z, the Crypto Council for Innovation and the Blockchain Association, according to people familiar with the plans. The White House sought to pare down the numbers of participants in the most recent gathering there last week, which hadn’t produced significant progress on the question of stablecoin rewards programs that are a key component of crypto platforms’ business models.

Despite the lack of significant progress, crypto representatives struck a hopeful note in statements about the meeting.

“We’re encouraged by the progress being made as stakeholders remains constructively engaged on resolving outstanding issues,” said Blockchain Association CEO Summer Mersinger, who was said to participate in the meeting.

“The important work continues,” said Ji Kim, the CEO of CCI, in a statement after the meeting, saying his group “appreciates the banking industry for their continued engagement.”

Banking groups involved in the meeting, including the Bank Policy Institute and American Bankers Association, issued a statement after the meeting, though it included no details about next steps on the legislation.

“As we noted during the meeting, that framework can and must embrace financial innovation without undermining safety and soundness, and without putting the bank deposits that fuel local lending and drive economic activity at risk,” the group said in the combined statement.

The document they were said to have shared insisted that stablecoin activity “must not drive deposit flight that would undercut Main Street lending.” It asked that the requested ban come with an enforcement stick for regulators, and the document suggested a study by regulators that examines the effect of stablecoin activity on deposits.

After two White House meetings on the topic and no significant movement of the line on yields, the matter may return to the discretion of lawmakers working on the bill.

Before the Senate can approve a bill, the banking panel needs to clear it through a majority vote. The legislation already has its necessary backing from the Senate Agriculture Committee, and a similar bill with the same name won a vote in the House of Representatives last year. But bankers have raised their concerns about the threat to deposits at the core of their industry.

However, stablecoin yield isn’t the only major sticking point. Senate Democratic negotiators have demanded that the effort include a ban on deep crypto involvement from senior government officials, driven primarily by President Donald Trump’s personal crypto interests. The Democratic lawmakers have also insisted on greater protections against crypto’s use in illicit finance and also that the Commodity Futures Trading Commission get fully staffed by commissioners — including Democratic appointees — before it can get to work on crypto regulations.

While Trump’s crypto adviser, Patrick Witt, has predicted the negotiators will find common ground soon, he also told CoinDesk that the White House won’t support an effort that targets the president. Witt was said to lead the meeting on Tuesday, as he did the one last week.

The Clarity Act faces a number of practical challenges beyond the policy disputes, including the Senate’s ongoing friction over a last remaining budget issue: the funding of the Department of Homeland Security, which runs Immigration and Customs Enforcement (ICE). The Senate is always a tough place to secure necessary floor time to move legislation, and the closer the chamber gets to the lengthy breaks before the midterm elections this year, the more difficult it is to find enough time to handle a major crypto bill.

Read More: Crypto industry, banks not yet close to stablecoin yield deal at White House meeting

UPDATE (February 10, 2025, 23:16 UTC): Adds comment from the bank lobbying groups.

UPDATE (February 10, 2025, 00:12 UTC): Adds details about the bankers’ document stating their principles on yield.

A new generation of investors is drawing crypto deeper into mainstream portfolios, even as it grapples with the asset class’s well-known volatility. Gen Z’s appetite for risk and its digital-native approach to money are shaping both the demand for cryptocurrencies and the conversation around how to manage that risk within a diversified portfolio. Findings from survey data and market commentary point to a multi-faceted dynamic: strong interest in crypto, tempered by an awareness of risk and a heavy influence from social platforms and online narratives.

According to Betterment’s 2025 Retail Survey, 64% of Gen Z and 49% of millennials say they are willing to take on more investment risk. This willingness to push the envelope aligns with a broader tilt toward crypto among younger cohorts. Separately, YouGov’s 2025 US Investment Trends report highlights that nearly two-thirds of Gen Z plan to invest in cryptocurrencies like Bitcoin this year, underscoring crypto’s rising status as a core consideration for younger investors. The combination of greater risk tolerance and a crypto-forward mindset suggests a structural shift in how Gen Z approaches wealth-building, beyond mere speculation.

That said, the Gen Z approach is not blind to risk. Crypto volatility remains a central concern for many, and the generation is keenly aware that price swings occur around the clock. Investopedia notes that while crypto is widely recognized as risky and volatile, many Gen Z investors continue to participate, viewing volatility as part of an entry price rather than a barrier to participation. In other words, recognition of risk does not appear to suppress the impulse to participate; it may even be embedded in the way they frame potential returns.

Key takeaways

- 64% of Gen Z and 49% of millennials are willing to take on more investment risk, according to Betterment’s 2025 Retail Survey.

- YouGov’s 2025 US Investment Trends report finds that nearly two-thirds of Gen Z intend to invest in cryptocurrencies this year.

- 84% of Gen Z acknowledge that cryptocurrencies are risky and volatile, yet they continue to invest, signaling a structural willingness to tolerate risk for potentially outsized gains.

- Financial FOMO drives behavior: about 70% of Gen Z report feeling financial FOMO while scrolling social media, and roughly half have made an investment influenced by that feeling, often in crypto or memecoins.

- For many young investors, crypto remains a digital-native asset class with appeal tied to high-growth narratives, but concerns about transparency and regulation persist as the market evolves.

Gen Z’s risk calculus in a digital era

Crypto’s appeal to Gen Z appears inseparable from the broader online ecosystem that shapes their financial world. Gen Z has grown up with the internet, digital wallets, and instant access to markets, which makes digital assets feel native rather than futuristic. The survey data illustrate a generation that is comfortable testing new assets, even as it calibrates its risk exposure to reflect a volatile, 24/7 market environment. The correlation between online influence and investment behavior becomes especially salient when considering how financial guidance is consumed. A notable share of younger investors turns to social platforms for insights, which elevates the importance of evaluating the quality and accountability of information accessed through these channels.

One dimension often cited in this context is how young investors source financial advice. Kiplinger’s coverage notes that about one in four Gen Z Americans obtain financial guidance from TikTok, a statistic that signals the growing role of “finfluencers” in shaping investment decisions. That dynamic, combined with the rapid dissemination of memes and viral narratives, helps explain why certain crypto stories gain outsized attention—even when the underlying fundamentals are murkier than traditional investment vehicles. In this environment, investors must balance curiosity with due diligence and a clear understanding of risk rewards.

Volatility, FOMO and the memecoin cycle

Volatility remains the price of admission for crypto, and Gen Z is not naïve about it. The generation’s understanding of risk reflects a paradox: while they recognize the inherent instability of digital assets, they are drawn by the prospect of outsized profits in a relatively new asset class. The tension between risk awareness and aspirational returns is compounded by social dynamics. Empower’s research on financial FOMO shows that 70% of Gen Z feel this pressure while scrolling social media, and a CFA Institute study cited in the broader discussion indicates that about 50% of Gen Z investors say they have made an investment driven by FOMO, often in crypto or memecoins. In other words, fear of missing out is translating into real capital allocation decisions, particularly toward assets that can deliver rapid visibility and engagement on social platforms.

The memecoin phenomenon sits at the intersection of virality, community hype, and speculative appetite. These tokens are designed to capture attention and momentum, delivering quick, event-driven price action that can attract new participants while amplifying the narrative around crypto’s potential. While this dynamic can drive activity and liquidity, it also raises questions about sustainability, risk management, and the long-term viability of such assets in a diversified portfolio. The cycle—rapid gains followed by swift corrections—has repeatedly underscored the risks associated with chasing headlines rather than fundamentals. As a result, even as crypto admissions rise among younger cohorts, memecoins can reinforce a broader skepticism about the safety and reliability of digital assets as a standalone investment thesis.

Beyond the hype, the behavioral profile of Gen Z investors highlights a broader diversification conversation. Some observers point to crypto as a potential portfolio diversifier, particularly as parts of the traditional market landscape exhibit different risk and return drivers. Yet the same conversations underscore real caveats: during periods of systemic stress, crypto has shown correlations with high-growth equities and even, at times, with traditional safe-haven narratives like gold. That raises practical questions for portfolio construction: if crypto participates in downside markets or moves in tandem with riskier equities, its diversification benefits may be more nuanced than initially assumed. For any investor, understanding when crypto serves as a genuine diversifier versus when it behaves as a high-beta, risk-on asset is essential to avoid overexposure or misaligned expectations.

Another critical theme is the lack of universal transparency and a clear regulatory framework across crypto markets. As a technology- and asset-class experiment in real-time, digital assets have not always benefited from the disclosures and governance that accompany traditional securities. MDPI’s analysis of cognitive biases, including the Dunning-Kruger effect, suggests that younger investors may overestimate their understanding of crypto and underestimate the risks, underscoring the need for robust education and clear regulatory guardrails. In the absence of consistent reporting standards and enforcement, the allure of quick profits can eclipse prudent risk assessment, increasing the likelihood of regrettable losses for inexperienced participants.

Regulation, transparency and the road ahead

While Gen Z’s crypto engagement signals a maturation of digital assets within the retail space, observers agree that regulatory clarity and improved transparency are critical for sustaining long-term participation. The tension between a rapidly evolving technology stack and the slower, more deliberate pace of policy development creates a dynamic where innovation can outpace guardrails, at least in the near term. As policymakers and industry participants negotiate better disclosure, custody standards, and product-level protections, the trajectory of Gen Z’s crypto involvement will hinge on how effectively those guardrails translate into real-world investor protections without stifling innovation.

Some researchers and market observers frame this moment as a test of crypto’s legitimacy as an investable asset class for a new generation. If regulators deliver calibrated, investor-centric rules and platforms improve transparency, crypto could expand from being a niche interest to a more mainstream, risk-aware component of diversified portfolios. Conversely, persistent gaps in transparency or regulatory uncertainty could amplify the very volatility and hype-driven dynamics that have driven memecoin cycles, potentially eroding trust among young buyers who expect clarity and accountability from market participants.

Related coverage in the broader crypto media ecosystem has noted regulators’ concerns about finfluencers and the need for responsible information dissemination, particularly as Gen Z ownership grows. For readers tracking the evolution of this space, pay attention to shifts in regulatory posture, custody and exchange standards, and how platforms adapt to the dual pressures of innovation and investor protection. As the market evolves, the balance between opportunity and risk will likely redefine crypto’s role in Gen Z portfolios.

Investors should watch how education, transparency, and policy alignment impact Generation Z’s crypto participation. The coming months may reveal whether this generation’s early-adopter behavior becomes a durable, risk-aware investment habit or whether volatility and information gaps pull the brakes on broader adoption.

Alex Tsepaev, chief strategy officer at B2PRIME Group, offers this perspective: crypto’s journey into mainstream investing is less about a single narrative of boom-and-bust and more about how a new generation learns to navigate risk, trust, and accountability in a rapidly changing financial landscape.

This opinion piece reflects the author’s view and is not an endorsement of any specific asset. Readers should conduct their own research and consider regulatory developments, platform protections, and risk management practices before making investment decisions.

Cameron and Tyler Winklevoss lent their own crypto exchange, Gemini, thousands of bitcoin (BTC) and ether (ETH) through Winklevoss Capital Fund (WCF), their private investment company. Gemini then pledged that crypto as collateral with Galaxy Digital and NYDIG to raise dollar loans.

When the exchange went public in September 2025 at $28 per share, it converted $695.6 million of WCF debt into super-voting Class B stock at a 20% discount, giving the twins 94.7% of Gemini’s voting power.

Gemini’s 10-K, filed yesterday, spelled out the entire structure. Social media users have called it a circular scheme.

The Winklevoss Capital Fund lending carousel

Here’s the basic tale of how the money flowed. The Winklevii’s WCF lent BTC and ETH to Gemini through open-term agreements, i.e. with no fixed maturity.

Gemini then posted that borrowed crypto as collateral with third-party lenders. Galaxy Digital extended $116.5 million in loans at 11-12% interest rates, collateralized at 145-155%. NYDIG provided $75 million through a repurchase agreement at 8.5%.

Gemini used the dollars for operations and regulatory capital requirements.

When the IPO closed on September 15, 2025, the exchange repaid Galaxy’s $116.5 million from $456 million in net proceeds from the IPO.

Gemini now trades on the Nasdaq under symbol GEMI.

The exchange also repaid $238.5 million under a warehouse credit facility with Ripple, though $154 million remained outstanding to Ripple at year end.

The twins’ own debt didn’t get cash repayment, however.

Gemini converted $200 million in WCF convertible notes and $475 million in WCF term loans, plus accrued interest, into 31.1 million supervoting Class B shares at $22.40 apiece.

That conversion price was 20% below what retail investors paid for otherwise equivalent Class A shares on the same day.

Class A and B stock differ only in their voting power and ownership distribution. Otherwise, they have the same par value, rights to dividends, and liquidation preference.

Class B shares are convertible into Class A on a one‑for‑one basis.

Retail paid $28 with the Winklevii at $22.40

The discount is where the circularity inflicted pain on regular shareholders.

WCF lent Gemini crypto. Gemini then pledged the crypto that it had borrowed to get even more loans. Specifically, Galaxy and NYDIG lent Gemini dollars which it used to operate.

Gemini then handed WCF equity at a discount funded by the same IPO that brought retail in 20% higher.

Read more: Sources say Winklevoss twins withdrew $280M from Genesis before it collapsed

The SEC Form 10-K confirms that Gemini still owed WCF 4,619 BTC as of December 31, 2025. That balance was worth roughly $400 million.

Gemini paid WCF $24.2 million in loan fees in 2025.

In summary, Gemini is simultaneously debtor, custodian, and a “controlled company” according to Nasdaq corporate governance standards.

Despite being publicly traded, Gemini’s co-founders still control a majority of its voting power.

Moreover, WCF holds roughly 8,757 BTC in Gemini Custody addresses, according to Arkham Intelligence data cited by crypto researcher Emmett Gallic.

Deloitte signed off clean

Deloitte has issued clean audit reports on Gemini. This is despite the reality that WCF could demand repayment of its 4,619 BTC loan at any time.

The twins could destabilize the exchange they control with a single written notice.

Gemini’s public stock now trades 88% below its IPO price. “Gemini Space Station,” its legal and rocket-based name that it certainly has not lived up to, opened at $37.01 per share on its IPO day.

It’s worth $4.42 today.

Gemini priced its IPO at $28 on September 11, 2025. It opened at $37.01 the next day and hit $45.89 before beginning a relentless decline. The stock closed at $4.42 on March 31, 2026, down 88% from the opening price, after touching a 52-week low of $3.91 this Monday.

The company’s market cap has collapsed from over $3.8 billion to roughly $520 million. Citigroup, Cantor, Truist, and Evercore downgraded the stock to a Sell rating.

A class action lawsuit alleges the company misled investors about its strategy.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

EUR/USD is recovering losses from 1.1450. USD/JPY is correcting gains from 160.50 and might decline further below 158.00.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

· The Euro struggled to stay in a positive zone and declined below 1.1600 before finding support.

· There is a key bearish trend line forming with resistance at 1.1575 on the hourly chart of EUR/USD at FXOpen.

· USD/JPY rallied significantly before the bears appeared near 160.45.

· There is a major bearish trend line forming with resistance near 159.20 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair started a fresh decline from 1.1640. The Euro declined below 1.1600 and 1.1520 against the US Dollar.

The pair even declined below 1.1500 and the 50-hour simple moving average. Finally, it tested the 1.1445 zone. A low was formed at 1.1443, and the pair is now recovering losses. There was a move above 1.1500 and the 50-hour simple moving average.

The pair surpassed the 50% Fib retracement level of the downward move from the 1.1639 swing high to the 1.1443 low. On the upside, the pair is now facing resistance near the 61.8% Fib retracement and 1.1575. There is also a key bearish trend line forming with resistance at 1.1575.

The first major hurdle for the bulls could be 1.1605. An upside break above 1.1605 could set the pace for another increase. In the stated case, the pair might rise toward 1.1640.

If not, the pair might drop again. Immediate support is near 1.1520. The next key area of interest might be 1.1480 or the 50-hour simple moving average. If there is a downside break below 1.1480, the pair could drop toward 1.1445. The main target for the bears on the EUR/USD chart could be 1.1400, below which the pair could start a major decline.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a steady decline from well above the 160.00 zone. The US Dollar gained bearish momentum below 159.50 against the Japanese Yen.

The pair even settled below 159.00 and the 50-hour simple moving average. A low was formed at 158.44, and the pair is now consolidating losses. On the downside, the first major support is near 158.45.

The next key region for the bulls might be 158.00. If there is a close below 158.00, the pair could decline steadily. In the stated case, the pair might drop toward 156.80. Any more losses might send the pair toward 155.00.

Immediate resistance on the USD/JPY chart is near the 23.6% Fib retracement level of the downward move from the 160.46 swing high to the 158.44 low at 158.90.

If there is a close above 158.90 and the hourly RSI moves above 50, the pair could rise toward 159.20. There is also a major bearish trend line forming with resistance near 159.20. The next major barrier for the bulls could be near the 50% Fib retracement level at 159.45, above which the pair could test 160.00 in the coming days.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

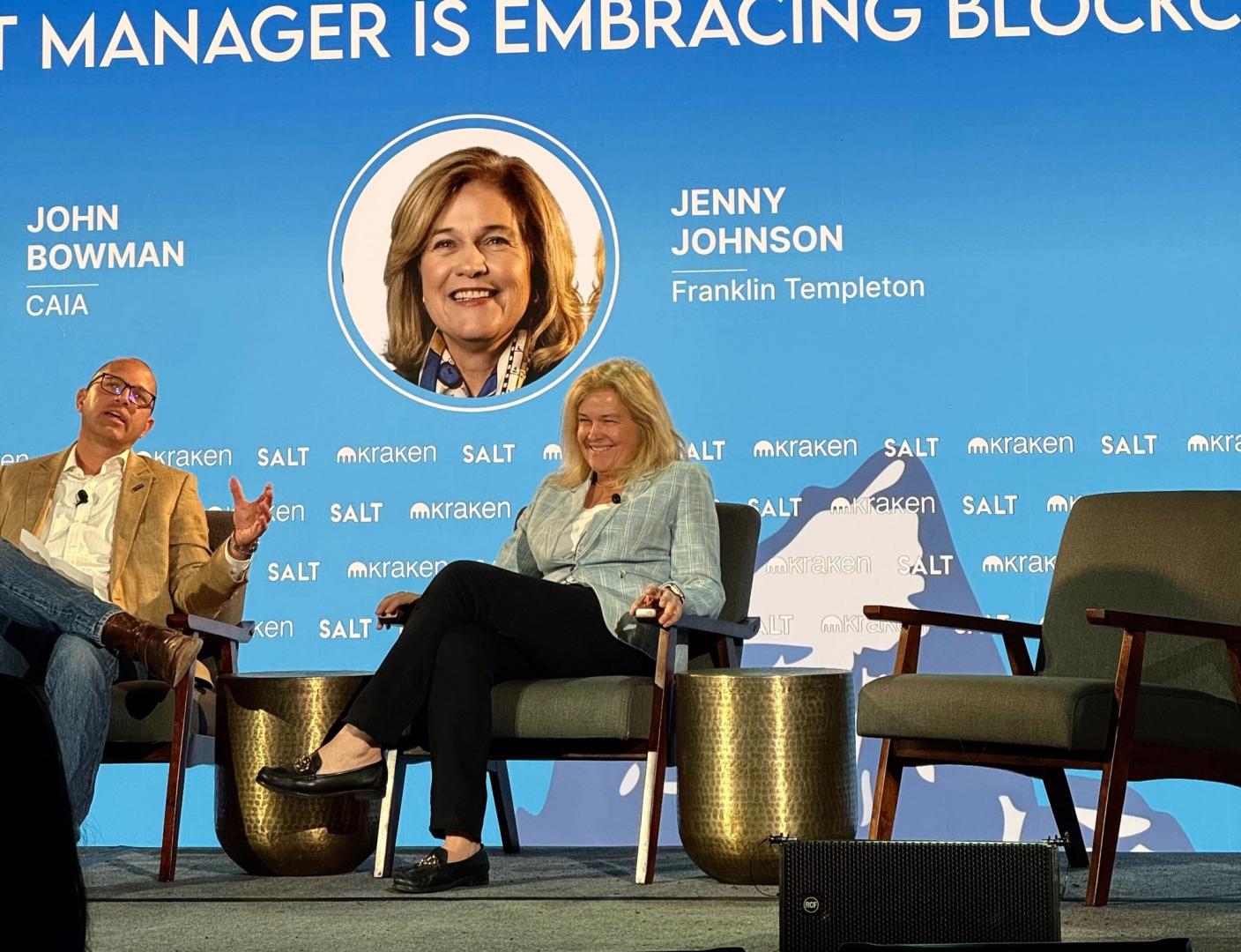

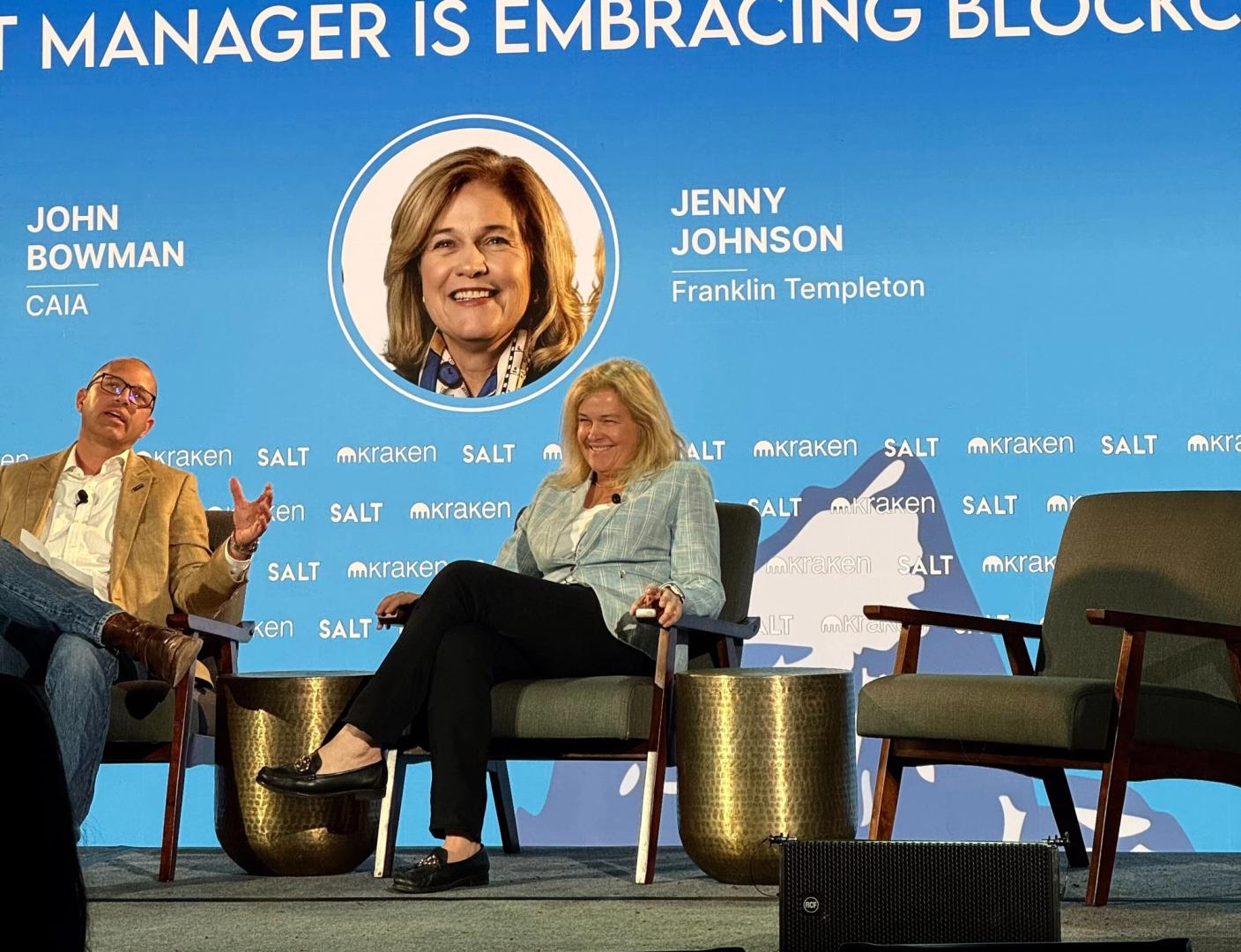

Wall Street asset management giant Franklin Templeton is launching a dedicated cryptocurrency division as it deepens its push into digital assets, anchored by a planned acquisition of crypto investment firm 250 Digital.

The new unit, called Franklin Crypto, will bring together the 250 Digital team and its liquid crypto strategies — previously managed by CoinFund — under one structure aimed at institutional investors, the firm said Wednesday.

Former CoinFund executive Christopher Perkins will lead the division, with Seth Ginns serving as chief investment officer alongside Franklin Templeton digital assets executive Tony Pecore. The group will report to Sandy Kaul, the firm’s head of innovation.

The move builds on Franklin Templeton’s existing digital asset business, which manages about $1.8 billion, and signals a shift toward offering more active crypto investment strategies alongside its current products.

“This is an exciting addition for Franklin Templeton,” CEO Jenny Johnson said, adding that the deal strengthens the firm’s ability to deliver dedicated crypto expertise to clients globally.

The launch of Franklin Crypto reflects a broader trend among large asset managers that are moving beyond passive exposure, such as exchange-traded funds, toward building in-house capabilities.

Perkins said the effort is aimed at meeting that demand. “Crypto’s institutional moment has arrived,” he said, pointing to growing interest from large investors seeking structured exposure to digital assets.

The transaction also includes an experimental element: part of the consideration will be paid using BENJI tokens, linked to Franklin Templeton’s on-chain U.S. Government Money Fund. The fund uses blockchain infrastructure to process transactions and record ownership.

That approach suggests early steps toward conducting mergers and acquisitions using tokenized assets, with settlement occurring more directly on blockchain rails.

The acquisition is expected to close in the second quarter of 2026, subject to approvals and other conditions. Financial terms were not disclosed.

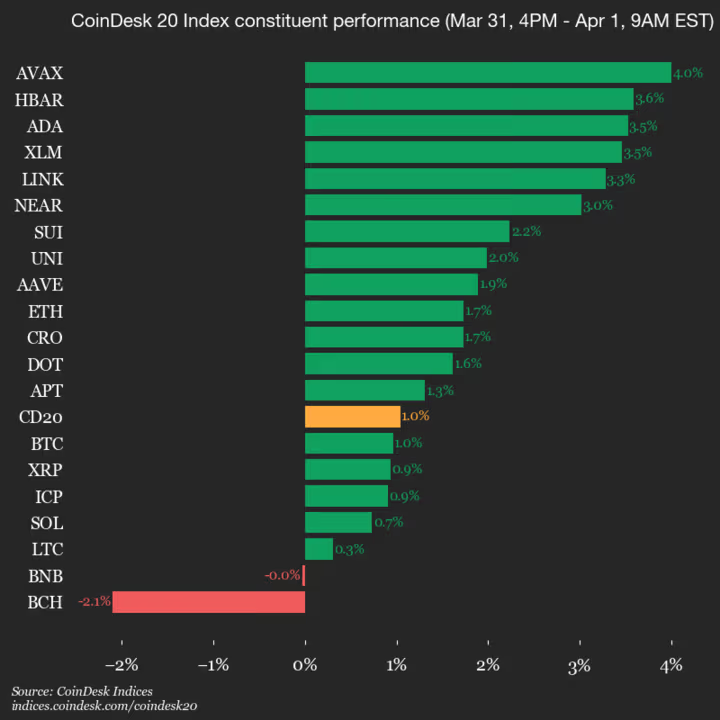

CoinDesk Indices presents its daily market update, highlighting the performance of leaders and laggards in the CoinDesk 20 Index.

The CoinDesk 20 is currently trading at 1968.28, up 1.0% (+20.29) since yesterday’s close.

Eighteen of 20 assets is trading higher.

Leaders: AVAX (+4.0%) and HBAR (+3.6%).

Laggards: BCH (-2.1%) and BNB (+0.0%).

The CoinDesk 20 is a broad-based index traded on multiple platforms in several regions globally.

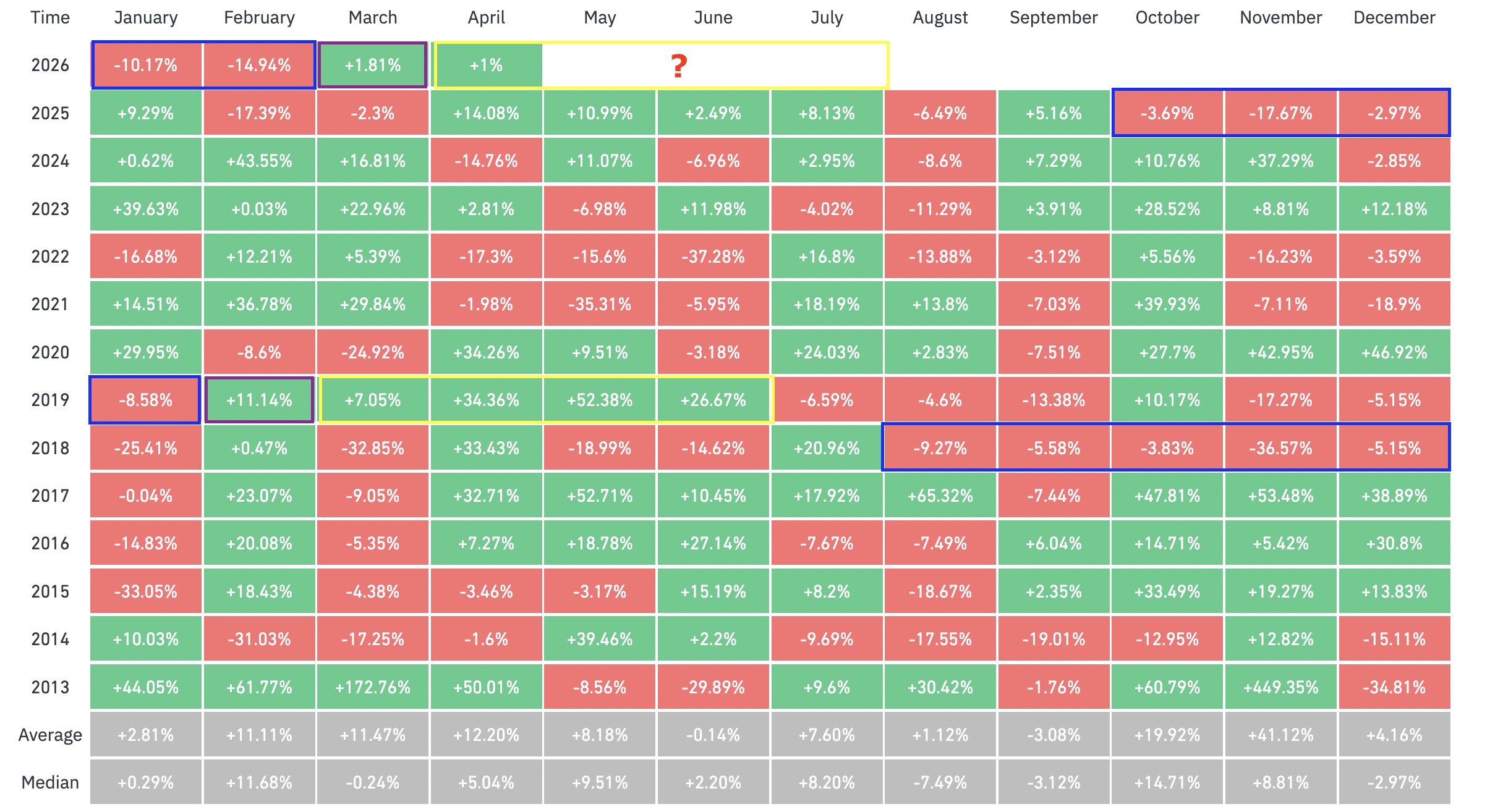

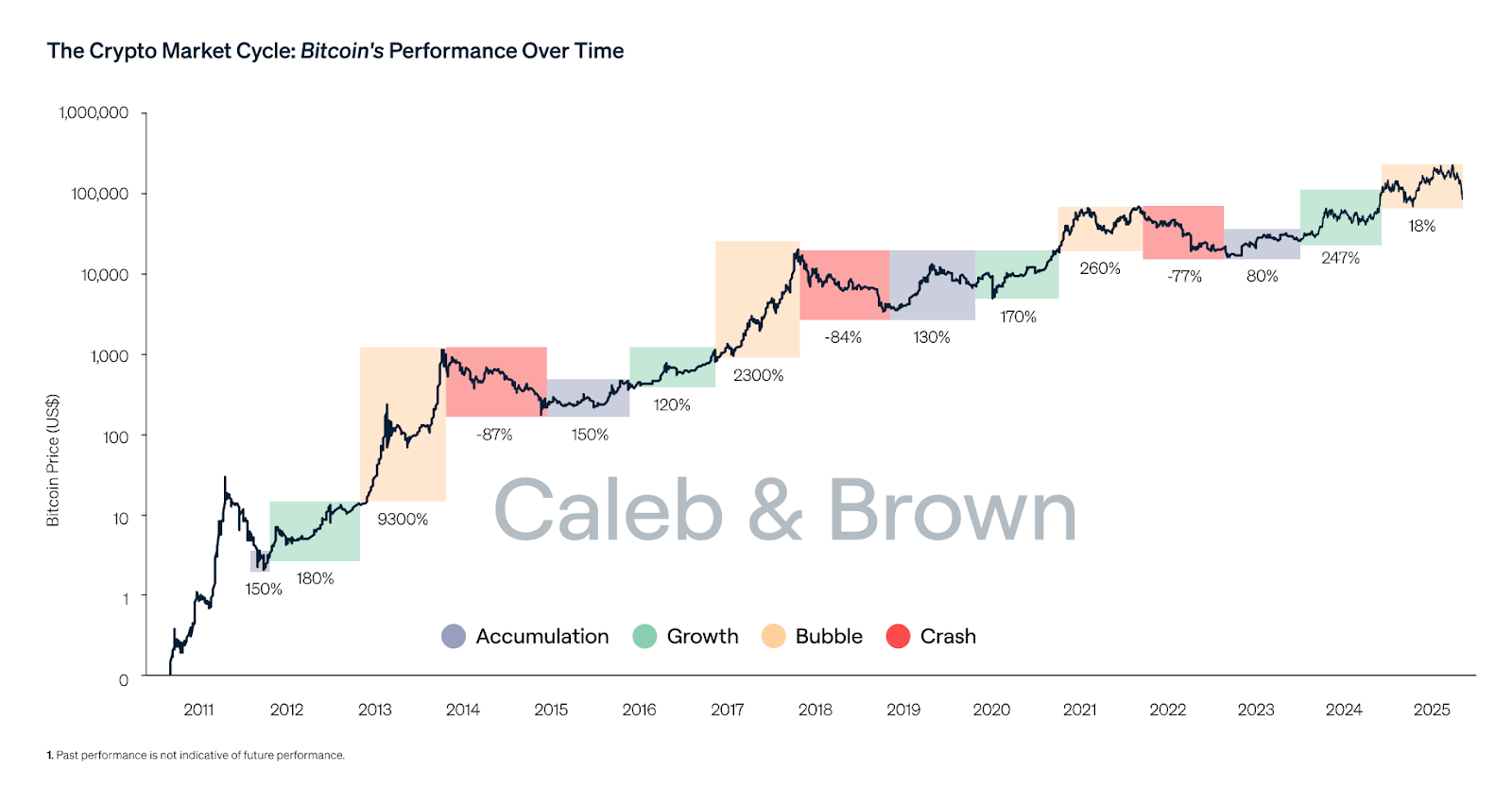

Bitcoin (BTC) closed March in green, ending the longest monthly losing streak since 2018. Data suggests that the coming months may prove to be profitable for BTC.

Key takeaways:

-

Bitcoin ended March 2% higher, marking the first green monthly close in six months.

-

A similar streak in 2018/2019 led to an over 316% BTC price rebound over five months.

-

Bitcoin price faces stiff resistance at $70,000-$72,000, where key trend lines converge.

Past multi-month downtrends were followed by 300% price gains

Historical price data from CoinGlass confirms Bitcoin printed its first green monthly candle in six months, closing March 2% higher after five straight months of losses.

“This is a massive dose of hopium,” analyst Ash Crypto said in an X post on Wednesday.

The analyst was referring to a possible shift in momentum, which might lead to a sustained recovery, as seen in previous cycles.

Related: Crypto Fear & Greed Index stuck on ‘extreme fear,’ but is there a silver lining?

The last time this happened was in 2018/2019 when BTC closed February 2019 in green, after six consecutive red months, as shown in the figure below.

This led to a reversal with over 300% returns the following five months, as Bitcoin recovered from the 2018 bear market.

“Last time BTC dumped 6 months in a row, it pumped the following 5 months in a row that came after!” trader Satoshi Flipper said in a Wednesday post on X.

If history repeats itself, the reversal may continue in April, suggesting that BTC price may have bottomed at $60,000.

Bitcoin’s bullish monthly close is a ”catalyst for fresh inflows into early April,” Trader Caleb said, adding:

“April starts with momentum.”

Bitcoin has a well-established tendency for significant price swings in April.

Since 2013, April has been a green month for eight of the past 13 years, with average returns of about 12.2%

However, Bitcoin also tends to move in the opposite direction to March in April, and this is true for nine out of the past 13 years.

In recent years, Bitcoin dropped in April after closing March in green, three out of four times between 2021 and 2024.

Therefore, while the end of past multi-month drawdowns suggests a rebound is due, data demonstrates that BTC price could also slide in April.

Watch these Bitcoin price levels next

Data from TradingView shows BTC price up 2.5% on the day to trade at $68,470 as the $69,000-$70,000 resistance remains in place.

Analysts expect Bitcoin’s range-bound price action to continue for longer, with important price levels to look for in case of a breakout.

These include the $70,000-$72,000 supply zone, coinciding with the 50-day simple moving average (SMA), the 50-day exponential moving average (EMA) and the 1w–1m cohort cost basis.

This is also where investors acquired approximately 650,000 BTC, marking a potential point of sell pressure, according to the cost-basis distribution data from Glassnode.

Breaking above this level could see BTC/USD revisit the $76,000 range high and eventually the $80,000 psychological level.

Zooming out, trader Sheldon Diedericks said Bitcoin could “push into resistance” at $83,000 on the monthly time frame, a key support level from April 2025. The 200-day EMA is also close to this area.

On the downside, the 200-week EMA at $68,300 and the 200-week SMA at $59,400 remain key levels to watch. Below that, the next major level is Bitcoin’s realized price around $54,000.

As Cointelegraph reported, Bitcoin’s bear market bottom could be formed once BTC price drops toward or below its realized price.

This article is produced in accordance with Cointelegraph’s Editorial Policy and is intended for informational purposes only. It does not constitute investment advice or recommendations. All investments and trades carry risk; readers are encouraged to conduct independent research before making any decisions. Cointelegraph makes no guarantees regarding the accuracy or completeness of the information presented, including forward-looking statements, and will not be liable for any loss or damage arising from reliance on this content.

Crypto World

OpenAI Secures Historic $122B Investment Round, Reaching $852B Valuation with Amazon and Nvidia Support

Key Highlights

- OpenAI secured $122 billion in funding, achieving an $852 billion post-money valuation

- Major investors include Amazon, Nvidia, and SoftBank, with continued support from Microsoft

- The company reports $2 billion in monthly revenue and serves 900 million weekly active ChatGPT users

- Development underway for an integrated AI “superapp” merging ChatGPT, Codex, and web browsing capabilities

- Credit facility enhanced to $4.7 billion, remaining untapped at present

OpenAI has successfully completed a monumental $122 billion investment round, establishing a new benchmark as the largest private capital raise in corporate history. This extraordinary financing values the artificial intelligence leader at $852 billion following the transaction, positioning it as the highest-valued privately-held company globally.

The investment was spearheaded by technology and investment heavyweights Amazon, Nvidia, and SoftBank. Microsoft, a longstanding strategic partner, maintained its participation in this latest round. SoftBank shared co-leadership responsibilities with a16z, D.E. Shaw Ventures, MGX, TPG, and T. Rowe Price-advised accounts.

The comprehensive investor consortium features prominent names including BlackRock, Blackstone, Fidelity, Sequoia, Temasek, Coatue, ARK Invest, Thrive Capital, and Insight Partners, alongside numerous other institutional backers.

In an unprecedented move, OpenAI made this funding opportunity accessible to retail investors through banking partnerships, successfully securing over $3 billion from individual participants alone. Additionally, OpenAI will gain exposure through inclusion in multiple ARK Invest exchange-traded funds.

The company reports current monthly revenue of $2 billion. This represents substantial acceleration from the $1 billion quarterly run rate recorded at 2024’s conclusion, demonstrating remarkable revenue expansion in a compressed timeframe.

ChatGPT’s user base has surpassed 900 million weekly active participants, complemented by more than 50 million paid subscription accounts. OpenAI maintains that its platform receives six times the monthly web traffic compared to its closest AI application competitor.

Enterprise clients now contribute over 40% of total revenue streams. According to company projections, enterprise revenue is positioned to match consumer revenue contributions by the conclusion of 2026.

The company’s application programming interfaces handle over 15 billion tokens every minute. Codex, its specialized coding assistant, supports more than 2 million weekly users—a fivefold increase achieved within a mere three-month period.

Vision for an Integrated AI Superapp

OpenAI has announced ambitious plans to construct a comprehensive AI superapp platform that consolidates ChatGPT, Codex, web browsing functionality, and autonomous agent capabilities into a singular, cohesive product offering. This strategic initiative aims to simplify widespread adoption and utilization of its artificial intelligence models.

The organization emphasizes computational infrastructure as a critical strategic priority. Cloud computing partnerships span Microsoft, Oracle, AWS, CoreWeave, and Google Cloud. Semiconductor collaborations encompass Nvidia, AMD, AWS Trainium, Cerebras, alongside proprietary chip development in partnership with Broadcom.

Enhanced Credit Arrangements and Market Position

OpenAI has simultaneously expanded its revolving credit arrangement to approximately $4.7 billion. This facility receives backing from leading financial institutions including JPMorgan Chase, Citi, Goldman Sachs, Morgan Stanley, Wells Fargo, and additional major banks. Notably, the entire facility remains untapped as of March 31.

With an $852 billion valuation, OpenAI commands a worth approximately equivalent to Berkshire Hathaway. The company’s value surpasses the market capitalizations of major corporations including Visa, JPMorgan Chase, and Samsung.

OpenAI has recently introduced GPT-5.4 to the market. The company’s API infrastructure continues expanding, processing billions of tokens per minute across both enterprise and consumer deployment scenarios.

BNB is holding a critical psychological price threshold, trading at $614 after a 1.7% gain in 24 hours, and our prediction since last week is getting bullish. As a catalyst, Binance’s newly announced prediction market feature can add enough utility to the equation.

Binance confirmed Yesterday it is rolling out an integrated prediction market directly inside its self-custody wallet, partnering with third-party providers, including Predict.fun, to let users bet on politics, sports, and crypto events without leaving the app.

— BSCN (@BSCNews) March 31, 2026

JUST IN: BINANCE WALLET TO LAUNCH PREDICTION MARKET FEATURE

JUST IN: BINANCE WALLET TO LAUNCH PREDICTION MARKET FEATURE

Binance Wallet (@BinanceWallet) is introducing a new prediction market tool. The feature will allow users to bet on future outcomes. Categories include sports, economics, world events, and crypto.

Binance will not… pic.twitter.com/lmMV53hEyX

The feature may also tie into BNB Chain’s yield-generating staking mechanics, potentially creating new organic demand for the token. Regulatory guardrails around prediction markets remain in flux, which adds a layer of uncertainty, but institutional interest in the sector is clearly accelerating, with Coinbase and Crypto.com both expanding into similar territory in recent months.

Discover: The best pre-launch token sales

BNB Price Prediction: Can It Hit $660 This Week?

BNB is consolidating in a narrow band near its lower Bollinger Bands, with RSI sitting at a neutral-to-weak 41-43, showing convergence but not yet confirmation of a reversal.

Key support sits at $600 level, with a secondary floor at $580. On the upside, resistance clusters at $640, $660, and the upper Bollinger Band at $680.

For the price, prediction market utility drives fresh BNB demand; the price can reclaim the $649 SMA and test the $660–$680 resistance zone within days. But a break below $600 support opens the door to the $420 accumulation zone.

On-chain activity at roughly 1 million active addresses and consistent token burns provide a structural floor. Broader altcoin season dynamics will likely determine whether BNB’s next meaningful move is up or down from here. Watch this current level closely; it has held twice in 48 hours, but a third test rarely ends the same way.

Discover: The best crypto to diversify your portfolio with

Bitcoin Hyper Targets Early Mover Upside as BNB Tests Key Levels

BNB is offering a range-bound trade with meaningful upside capped at $680 in the near term. For traders who want asymmetric exposure during this uncertain window, early-stage infrastructure plays are drawing attention, particularly those targeting Bitcoin’s own scaling limitations.

Bitcoin macro conditions remain a dominant force across the entire market, and projects building directly on BTC infrastructure are positioned to capture that gravity.

Bitcoin Hyper ($HYPER) is positioning itself as the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, combining Bitcoin’s security and trust with smart contract performance that exceeds Solana’s own throughput.

The presale has raised more than $32 million at a current token price of just $0.0136, with staking rewards live for early participants. Core features include a Decentralized Canonical Bridge for BTC transfers, sub-second finality, and low-cost transaction execution, targeting the exact bottlenecks (slow speeds, high fees, no programmability) that have historically kept institutional capital off Bitcoin’s base layer.

This article is for informational purposes only and does not constitute financial advice. Cryptocurrencies are highly volatile. Always do your own research before investing.

The post BNB Price Prediction: Can BNB Maintain Momentum With Its New Prediction Market? appeared first on Cryptonews.

The World Foundation sold $65 million in WLD tokens through over-the-counter block trades with four private counterparties at an average price of $0.2719 per token.

Opinion by: Alex Tsepaev, chief strategy officer at B2PRIME Group.

Each generation has its own distinct characteristics, even when it comes to investing. Younger people, for example, show a higher tolerance for risk. More than 64% of Gen Z and 49% of millennials say they are willing to take on more of it.

That appetite naturally includes investing in cryptocurrencies, which is considered one of the riskiest asset classes in modern markets. No surprise, then, that nearly two-thirds of Gen Zs plan to invest in cryptocurrencies like Bitcoin this year. Even more striking is that they are almost four times as likely to own crypto as to own a retirement account.

This might look like pure speculation. These numbers suggest that something more structural is happening.

For Gen Z, crypto is becoming an important part of their portfolios. The question now is whether that bet is mature or premature.

Volatility is the price of admission

Although it is arguable, crypto volatility remains one of the biggest obstacles in investing. Prices can change every millisecond, and trading happens around the clock. This has a significant effect on the final execution price.

The most interesting part here, however, is that Gen Z is fully aware of this. 84% of them acknowledged that cryptocurrencies are risky and volatile, yet continue investing, and participation continues to grow every year. Why?

Gen Z understands that digital assets are a great way to have extra, above-average profits, and volatility is perceived as an entry price. For a generation that has already witnessed two of the biggest economic crises in history, average capital growth in traditional investments can feel too slow or insufficient.

Digital assets also feel native to Gen Z. This is the first generation that has never known a life without the internet, and they are also used to digital wallets and online transactions.

At the same time, their investment behavior is shaped by social media consumption — one in four American Gen Z now gets financial advice from TikTok. Considering that the internet is flooded with so-called “finfluencers,” who help you learnn more about crypto, no surprise that Zoomers tend to invest in it so much.

FOMO and the narrative trap

Beyond risk tolerance, there is another thing that distinguishes Gen Z from previous generations.

It is the fear of missing out (FOMO). This feeling, mostly expressed as the fear of lost profits, is expressed in constant anxiety due to comparing lives with the “perfect” picture on social networks.

FOMO is especially common among Zoomers when it comes to financial matters. In fact, nearly 70% of Gen Z says they feel financial FOMO while scrolling social media. And 50% of Gen Z investors said they have even made an investment driven by this feeling, most often in crypto, in particular, memecoins.

Related: Australia warns of AI, ‘finfluencers’ as Gen Z crypto ownership reaches 23%

Memecoins thrive in this environment. By design, they are made for virality and great coverage in the media and news. The issue is not that they are built on hype, but that they are made to catch the moment and disappear, in most cases. Every memecoin cycle, where it goes up and quickly falls down, strengthens the argument that digital assets are unsafe.

This creates a narrative duality. On one side, crypto is maturing, and institutionals flow in. On the other hand, the industry is still very FOMO-fueled, and this dominates the headlines. And as a result, the loudest crypto stories become more about speculative gains.

Risks that Gen Z underestimate

When Gen Z increasingly invests in crypto, many may be doing so without fully researching the risks. Sometimes they blindly trust TikTok advice without doing their due diligence or reaching out to a financial advisor.

Zoomers mostly feel confident in their decisions. More than 70% of Gen Z saying they are completely sure about their investing behavior. Confidence, however, and especially in crypto, does not mean competence. Younger generations are reportedly more susceptible to the Dunning-Kruger effect. They usually overestimate their knowledge and underestimate risks.

Beyond volatility as a primary risk, Gen Z often neglects the absence of transparency in crypto. Unlike public companies, digital assets have no reporting requirements. A “Wild West” like this, and lack of long-reaching regulation does not bother young crypto enthusiasts. On the contrary, they still trust crypto. They value transparency and direct control a lot. In fact, they should pay more attention to regulation. As it develops, it helps to protect investor rights and turn crypto into a more transparent and trustworthy market.

Investors can also forget that diversification does not simply mean putting 10-20% of your portfolio in crypto. There is the issue of correlation. During periods of systemic stress, crypto has at times moved in line with high-growth equities, weakening its diversification argument. Graphs show that Bitcoin can even correlate with gold, a traditional safe-haven asset.

Or imagine they, for example, choose the wrong coin that is going to fall and put in at least 25%. Without understanding how digital assets work, they risk losing a fourth of their investments.

Still, none of these risks devalues crypto’s role in modern portfolios. On the contrary, crypto might indeed be evolving into a genuine portfolio diversifier.

If that transformation is real, it comes with strings attached.

Opinion by: Alex Tsepaev, chief strategy officer at B2PRIME Group.

This opinion article presents the author’s expert view, and it may not reflect the views of Cointelegraph.com. This content has undergone editorial review to ensure clarity and relevance. Cointelegraph remains committed to transparent reporting and upholding the highest standards of journalism. Readers are encouraged to conduct their own research before taking any actions related to the company.

Make Money With AI Music

Bristol’s Engine Shed by Temple Meads to close after 13 years

Daniel Wiffen: Olympic gold medallist open to changing training base after Irish Open

-

News Videos7 days ago

News Videos7 days agoParliament publishes latest register of MPs’ financial interests

-

Business6 days ago

Business6 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Tech6 days ago

Tech6 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

NewsBeat5 days ago

NewsBeat5 days agoThe Story hosts event on Durham’s historic registers

-

Sports5 days ago

Sports5 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment2 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment4 days ago

Entertainment4 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World1 day ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Sports22 hours ago

Sports22 hours agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Fashion7 days ago

Fashion7 days agoHow to Style Spring Like WeWoreWhat: Easy Outfit Ideas for 2026

-

Tech2 days ago

Tech2 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Entertainment6 days ago

Entertainment6 days agoHBO’s Harry Potter Series Will Definitely Fail For One Big Reason, And It’s Not J.K. Rowling Or Snape

-

Crypto World2 days ago

Crypto World2 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Fashion6 days ago

Fashion6 days agoEn Vogue in Brown Leather and Tailored Neutrals by Atelier Savoir, Styled by J Bolin

-

Tech1 day ago

Tech1 day agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Fashion6 days ago

Fashion6 days agoWhat Are Your Favorite T-Shirts for the Weekend?

-

Fashion5 days ago

Fashion5 days agoWeekly News Update, 3.27.26 – Corporette.com

-

Politics2 days ago

Politics2 days agoShould Trump Be Scared Strait?

-

Sports2 days ago

Sports2 days agoWomen’s hockey camp eyes fitness boost, tactics ahead of WC 2026 campaign | Other Sports News

-

Tech1 day ago

Tech1 day agoFlipsnack and the shift toward motion-first business content with living visuals

You must be logged in to post a comment Login