Crypto World

ETH Insider Explains Wave of 2026 Ethereum Foundation Departures

A long-time Ethereum investor and community figure has pushed back against growing alarm over the string of departures from the Ethereum Foundation (EF), arguing that the organization’s commitment to the network is as firm as ever.

Ryan Berckmans, who has worked full-time in the Ethereum space for eight years, offered one of the more detailed community-level defenses of the EF’s current direction since the exits started mounting this year.

Departures Caused by Differences of Opinion

According to Berckmans, people are misreading the situation.

“The EF departures are not because the people departing feel differently about Ethereum and our trajectory vs. the people staying at EF or vs. community folks like me,” he wrote.

What actually drove them, in his view, was a mix of internal disagreements over sub-strategies rather than any loss of faith in Ethereum itself, plus a deliberate generational shift.

“Some folks disagreed. Some tiny number were asked to leave for Reasons. Some few others left immediately due to Reasonable Net Feelings. Some more are leaving because the Wheel is Turning,” he explained.

Further, Berckmans added that new, younger contributors are ready to step into leadership across teams and departments. He also addressed a persistent piece of community frustration, that the EF and Vitalik Buterin do not care about ETH’s price, calling it a misconception.

According to him, they care deeply, but across a much longer time horizon than most community members track.

“They want to know, ‘How will Ethereum remain dominant after quantum computers?’ and, ‘How will Ethereum be the world’s economic hub for trillions in assets and thousands of L2s across a hundred countries?’”

His conclusion was that these are questions that can only get asked if you believe the outcome is achievable, and the EF’s programs in response to them are “gigabullish.”

Four Prominent Contributors Left in Just Four Weeks

The wave of exits has included Carl Beek, Julian Ma, Barnabé Monnot, Tim Beiko, Trent Van Epps, Josh Stark, and former co-Executive Director Tomasz Stańczak.

Stańczak’s departure, in particular, drew quite a lot of attention, considering that it came just 11 months after he’d taken the role. In addition, the exits have been concentrated, with four of the more prominent ones landing within roughly four weeks of each other in April and May.

Meanwhile, a detailed analysis by crypto researcher Nick Sawinyh pointed to unconfirmed claims circulating online that staff were asked to formally align with the Foundation’s new mandate. However, the EF has not publicly confirmed those claims, and none of the departing contributors cited the mandate as their reason for leaving.

People are also focusing on the coming Glamsterdam upgrade to Ethereum that is still under test. The protocol update includes changes tied to scaling and validator infrastructure, although some anticipated features, including FOCIL and native account abstraction, have already been delayed to a later upgrade cycle.

Despite this, many Ethereum backers believe that the entire ecosystem can now take leadership changes in stride without posing a risk to the network as a whole. One of them, author William Mougayar, described the Foundation’s shrinking role as a deliberate attempt to remove Ethereum’s remaining central point of control rather than a sign of institutional decline.

The post ETH Insider Explains Wave of 2026 Ethereum Foundation Departures appeared first on CryptoPotato.

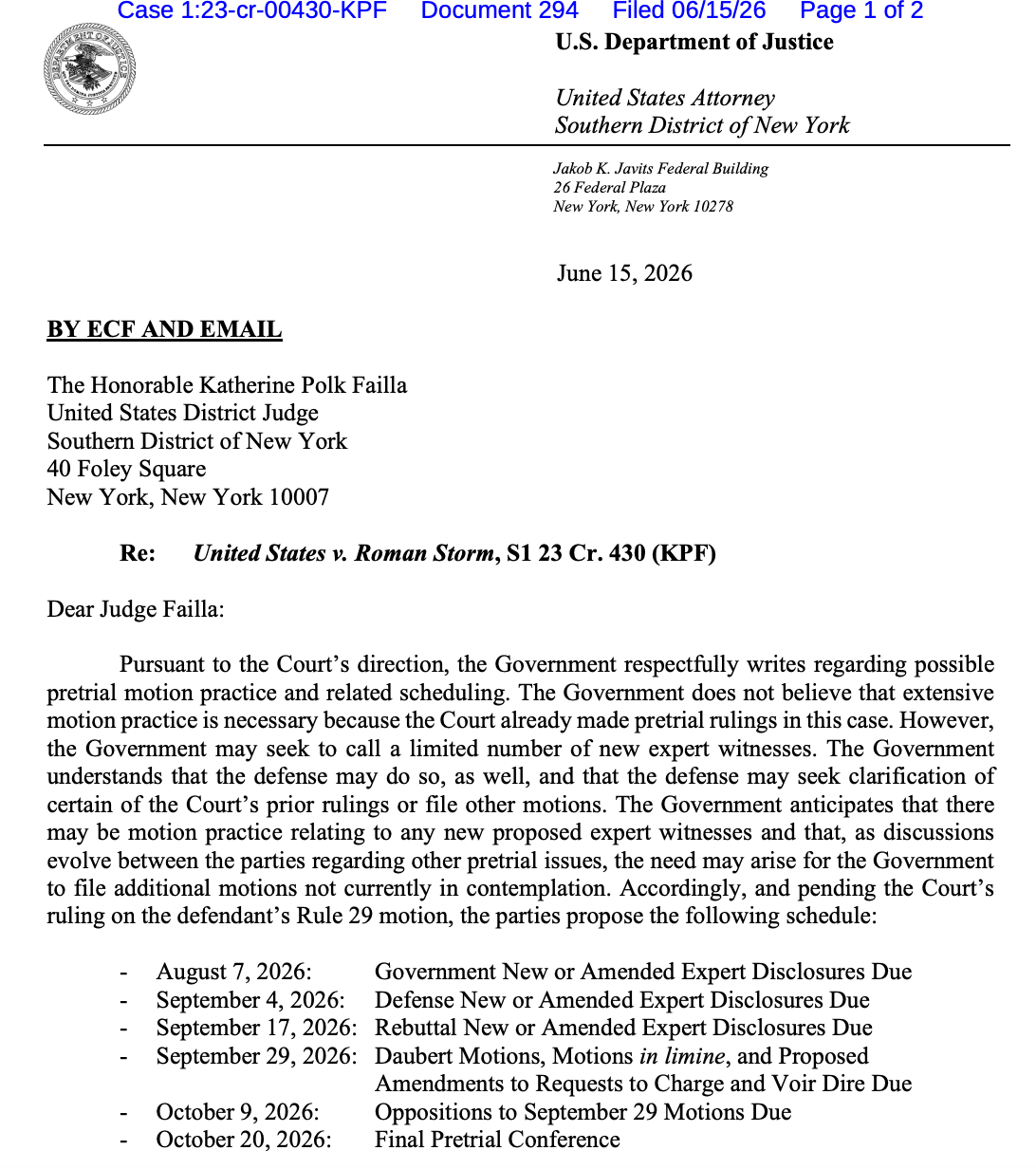

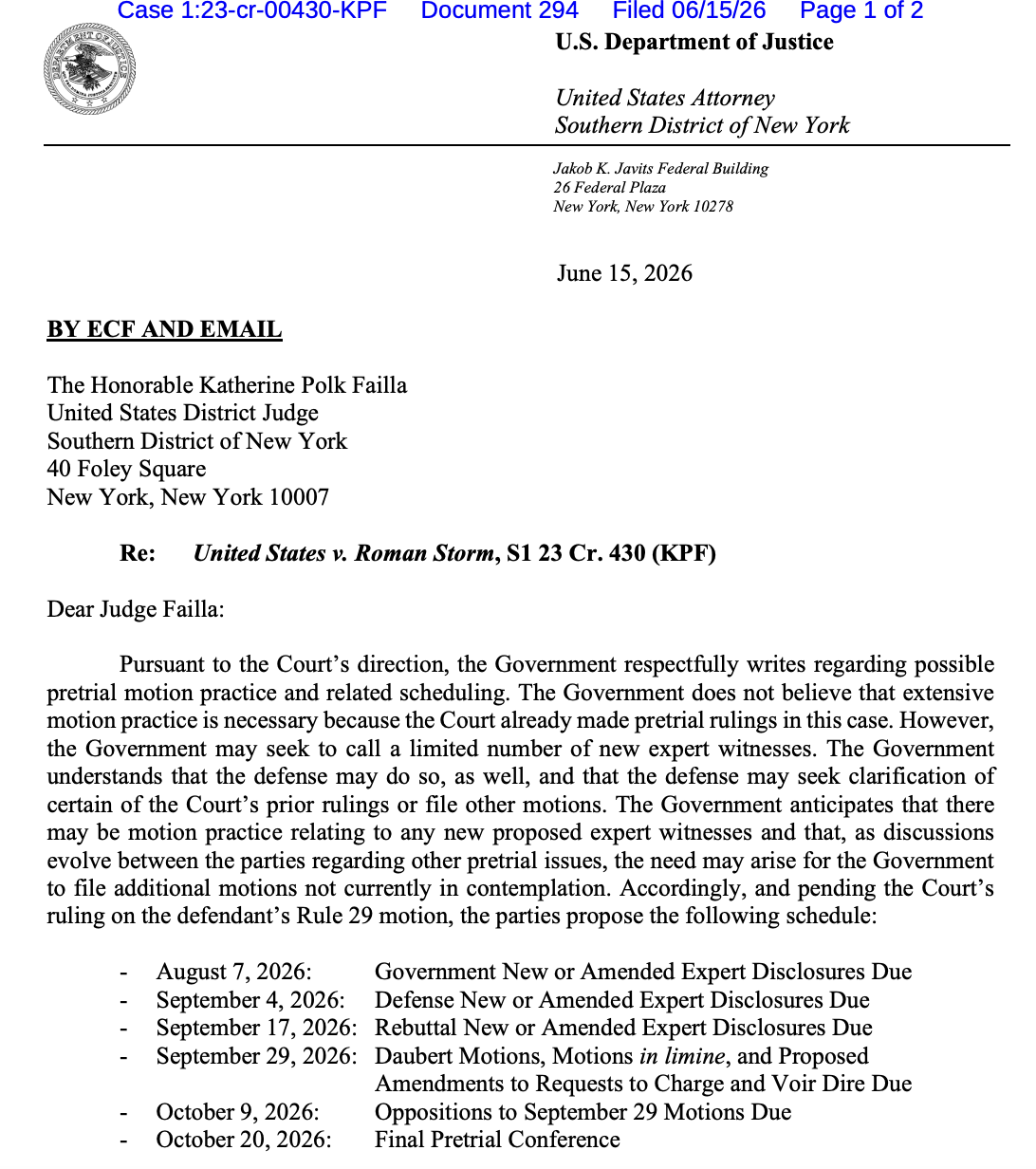

US prosecutors propose late 2026 retrial for Tornado Cash co-founder

Federal prosecutors on Monday submitted a proposed schedule for the potential retrial of Tornado Cash co-founder and developer Roman Storm to begin later this year. Storm was found guilty on one of three charges related to illegal money transmitting in 2025, but a jury deadlocked on two other charges, setting the stage for a potential retrial.

US Attorney for the Southern District of New York (SDNY) Jay Clayton Clayton proposed an Oct. 20 final pretrial conference in Storm’s case, signaling a potential trial start date of late October or November 2026. The filing noted that the timeline was subject to the court’s decision on a Rule 29 motion filed by Storm requesting acquittal of the remaining charges.

Source: PACER

Storm’s case continues to draw attention from many in the crypto industry given the implications for developers potentially being held criminally liable for code they write. Should a retrial be scheduled, the Tornado Cash co-founder could face the two remaining charges of conspiracy to commit money laundering and conspiracy to violate sanctions again.

Judge sets 60-day deadline for prosecutors to respond to Celsius CEO’s motion to vacate sentence

Alex Mashinsky, the former CEO of cryptocurrency lending platform Celsius who said he would be representing himself in court, could receive an answer to his pro se motion to vacate his 12-year sentence before the end of the year.

In a Saturday filing in the US District Court for SDNY, Judge John Koeltl granted a motion giving prosecutors until mid-August to respond to Mashinsky’s request to vacate his sentence. The 60-day deadline followed the former Celsius CEO requesting the judge vacate his May 2025 sentence, which resulted in Mashinsky reporting to federal prison.

Mashinsky, once one of the most recognizable figures in the crypto industry, was indicted in 2023 with his cohort Roni Cohen-Pavon on charges related to fraud and market manipulation. Celsius filed for bankruptcy in 2022 amid the crypto market downturn that resulted in the collapse of exchanges including FTX and Voyager Digital.

Related: Sam Bankman-Fried loses appeal to overturn 25-year prison sentence

The former CEO was ordered to pay $48 million in forfeiture as part of his criminal case. Cohen-Pavon was sentenced to time served but ordered to pay more than $1 million and a $40,000 fine.

Judge sets December 2026 trial for US soldier in Polymarket insider trading case

Gannon Ken Van Dyke, the US soldier charged after allegedly making more than $400,000 on a Polymarket event contract related to the capture of Venezuela President Nicolás Maduro, is looking at a December 2026 trial after his April arrest.

In a June 10 SDNY filing, Judge Margaret Garnett ordered pretrial motions for US prosecutors and defense attorneys in Van Dyke’s case, culminating in jury selection scheduled for Dec. 7. The soldier allegedly used nonpublic information to profit off the removal of Maduro in January, when US forces entered his residence in Caracas and extradited him to the United States to face criminal charges.

The Van Dyke case carries potential implications for Polymarket and other prediction markets platforms facing scrutiny from US lawmakers calling for elected officials to be barred from potentially betting on events with classified or nonpublic information. Van Dyke has pleaded not guilty to all charges.

Magazine: Bitcoin, the ‘canary in the coal mine,’ XRP transaction demand falls 91.5%: Market Moves

Kentucky Attorney General Russell Coleman sued prediction markets Kalshi and Polymarket, as well as VGW, a firm that operates online casino-style games.

The lawsuits accuse the companies of running unlicensed, illegal sports betting and gambling across the state.

What Kentucky Attorney General Alleges

Coleman alleges that the prediction market platforms allow users to wager on game winners, point spreads, and player statistics. He says they skip the consumer protections and taxes that state gambling laws require.

The complaint claims that sports betting accounted for roughly 70% of Kalshi’s trading volume during a 2025 sample period. In addition, of the nearly $23 billion in contract volume last year, 89% came from sports wagering.

Follow us on X to get the latest news as it happens

The action followed a coalition representing both platforms suing Kentucky, challenging its new tax and contracting restrictions.

“Kentucky’s attempt to impose a 14.25% excise tax whenever any Kentucky resident purchases an event contract anywhere in the country, and whenever any resident from any State purchases an event contract while physically present in Kentucky, plainly ‘concerns’ or ‘regards’ exchange-traded derivatives falling within the CFTC’s exclusive jurisdiction,” the document reads.

Platforms Point to Federal Regulations

Meanwhile, Kalshi pointed to its federal oversight in a statement shared with BeInCrypto.

“Kalshi is a federally regulated exchange. The CFTC is our regulator, not the states. Courts have already recognized this, and we’re confident they will here too,” Kalshi spokesperson, Jacki McGavick, mentioned.

Polymarket echoed that position in a statement to BeInCrypto.

“This action runs counter to the CFTC’s established framework for regulating prediction markets. We look forward to addressing these claims through the appropriate legal process,” a Polymarket spokesperson said.

A VGW spokesperson also stated that the firm plans to defend itself vigorously against the lawsuit.

“We respectfully reject the Kentucky Attorney General’s claims and plan to vigorously defend this lawsuit. We have lawfully operated in the US for more than a decade, delivering online Social Plus games to millions of Americans who value the freedom to enjoy the free, fun entertainment that this lawsuit effectively targets. With values including ‘our players come first’ and ‘we do what’s right’, we pride ourselves on creating not only the best games, player experiences and entertainment, but ensuring this is done safely and responsibly with robust consumer protections,” the spokesperson shared with BeInCrypto.

States that move against prediction markets have met resistance from the Commodity Futures Trading Commission (CFTC). The agency argues that it holds sole authority over event contracts. The CFTC has already sued several states, including Arizona and Minnesota.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Kentucky Attorney General Targets Prediction Markets in New Lawsuits appeared first on BeInCrypto.

Key Takeaways

- D-Wave revealed a gate-model quantum simulator featuring dual-rail technology designed for error-aware development

- The platform accommodates up to 21 qubits with both ideal emulation and hardware simulation modes, including Monte Carlo capabilities

- The tool enables developers to build quantum applications, test error-correction protocols, and optimize workflows in real-time

- Two new subscription packages—Starter and Premium—will provide monthly access alongside expert consulting services

- The simulator will be accessible through D-Wave’s Leap cloud infrastructure beginning September 2026

Shares of D-Wave Quantum (QBTS) slipped 4.26% during Wednesday’s session following the company’s unveiling of a new gate-model quantum simulator engineered for error-aware application development.

Despite the technological milestone, which D-Wave positioned as an industry-first simulator leveraging its proprietary dual-rail architecture, investors pushed shares lower throughout the trading day.

The newly announced platform can handle up to 21 qubits while providing developers with transparent, real-time visibility into error states—a significant advancement for teams seeking to design and validate quantum software before accessing physical quantum hardware.

The simulator offers both idealized and hardware-realistic emulation environments, Monte Carlo-based real-time dynamics modeling, and seamless compatibility with D-Wave’s Ocean software development kit. This integrated approach allows programmers to simulate authentic quantum processor behavior without requiring direct access to quantum machines.

With embedded error detection and real-time operational controls, the platform is engineered to accelerate prototyping cycles, enabling developers to experiment with applications and refine error-correction strategies more efficiently.

Subscription Packages Designed for Broader Developer Adoption

Alongside the simulator launch, D-Wave introduced two subscription-based development packages: Starter and Premium tiers. Each bundle combines simulator access with future gate-model hardware availability, professional consulting support, and predictable monthly resource allocations.

Custom pricing is available upon inquiry for both subscription levels. The packages represent D-Wave’s strategy to democratize quantum computing development across diverse user groups, from academic researchers to enterprise innovation teams.

Developers will gain access to the simulator through D-Wave’s established Leap cloud environment when it launches in September 2026. The Leap platform currently supports over 100 organizational users, providing a proven foundation for the new offering.

Market Perspective

The latest Wall Street coverage on QBTS maintains a Buy recommendation with a $35.00 price objective.

D-Wave commands a market valuation of $8.87 billion. Daily trading volume typically averages approximately 33.7 million shares.

From a technical analysis standpoint, the stock carries a Strong Buy signal.

The company’s portfolio spans both quantum annealing and gate-model computing platforms, distinguishing it within the competitive quantum computing landscape. This latest simulator extends D-Wave’s gate-model capabilities into new development territory.

According to D-Wave, the September rollout aims to enable clients to scale quantum workloads while compressing research and development timelines.

The product announcement came on June 18, 2026, with September 2026 confirmed as the cloud availability target, though no additional implementation milestones were disclosed.

Staking lets you earn a yield on certain cryptocurrencies by helping secure the network they run on. Here is how it actually works, where the rewards come from, what the real risks are, and how to start, explained without the hype.

Summary

- Staking allows cryptocurrency holders to earn rewards by helping secure proof of stake blockchain networks.

- Staking rewards are funded through new token issuance and network transaction fees, rather than traditional lending activity.

- Price volatility, lockup periods, validator penalties, and platform risks remain key factors investors should understand before staking assets.

Staking is one of the most common ways to earn a yield on cryptocurrency, and it is also one of the most misunderstood. In simple terms, staking means locking up a proof-of-stake cryptocurrency to help secure its network, and earning rewards in return, a yield often quoted as an annual percentage.

It is frequently described as the crypto equivalent of earning interest in a savings account, and that analogy captures the appeal, a return on assets you already hold, but it obscures what is actually happening and the real risks involved. To stake wisely, you need to understand where the rewards really come from, which is not interest at all, and what you are giving up and exposing yourself to in exchange.

This guide explains staking from the ground up: what proof of stake is and why it makes staking possible, where staking rewards actually come from, the difference between running a validator and delegating, the main ways to stake and who each suits, the real risks that the savings-account analogy hides, and how to start.

It assumes no prior knowledge, and it deliberately avoids the hype that surrounds yield in crypto, because the single most important thing about staking is understanding that the advertised percentage is not free money but compensation for a service and for taking on risk. Understanding that turns staking from a number you chase into a decision you can make clearly.

What proof of stake is, and why it enables staking

Staking only exists because of how certain blockchains are secured, so the place to begin is with proof of stake itself.

Every blockchain needs a way to agree on which transactions are valid and in what order, without a central authority in charge, and this is the job of a consensus mechanism. Bitcoin uses proof of work, in which miners compete by spending enormous computing power and electricity to earn the right to add blocks, securing the network through the sheer cost of attacking it.

Proof of stake takes a different approach: instead of miners spending energy, it uses validators who lock up, or stake, a quantity of the network’s own cryptocurrency as collateral, and the network selects among them to validate transactions and produce blocks, rewarding them for honest work. The security comes not from burning electricity but from economic skin in the game: a validator who tries to cheat risks losing the stake they put up, so honesty is the profitable strategy.

This design is what makes staking possible and what gives staking rewards their purpose. Because the network needs validators to lock up capital to secure it, it rewards them for doing so, and those rewards are what stakers earn. When you stake, you are contributing your cryptocurrency to the pool of collateral that secures the network, either by running a validator yourself or by backing one, and the rewards you receive are your share of what the network pays for that security.

Proof of stake, in other words, turns the act of holding and committing the cryptocurrency into the mechanism that protects the chain, and staking is how ordinary holders participate in that mechanism and get paid for it. Major networks including Ethereum, Solana, Cardano, and many others run on proof of stake, which is why staking is available across so much of the market.

Where staking rewards actually come from

The savings-account comparison breaks down here, and understanding where the yield really originates is the key to evaluating any staking opportunity clearly.

In a bank, the interest you earn comes from the bank lending your money out at a higher rate; it is a return generated by someone else’s borrowing. Staking rewards are different in origin. They come primarily from two sources: new cryptocurrency that the network issues as a reward for securing it, and transaction fees paid by users of the network, both of which are distributed to validators and the stakers backing them.

The new-issuance part is the larger source on most networks, and it has an important consequence the savings analogy hides: the rewards are partly funded by the network creating new units of its own currency, which increases the total supply.

So a meaningful portion of a staking yield is not a gain in real terms but a redistribution, the network prints new tokens and gives them to the people who stake, which dilutes those who do not.

This matters for how you read a staking yield. A headline rate of, say, five or seven percent is a nominal figure, and its real value depends on how much new supply the network is issuing to pay it. If a network issues new tokens at a rate close to its staking yield, then stakers are roughly running in place in terms of their share of the total supply, earning tokens while the supply grows underneath them, and the real return depends on whether demand for the token grows faster than the supply.

This is not a reason to avoid staking, since stakers still come out ahead of non-stakers who get diluted without compensation, but it is a reason to treat the advertised percentage with clear eyes. The yield is real, but it is compensation for providing security and for accepting risk, funded partly by inflation, not interest paid out of someone else’s productive borrowing. Seeing it that way is the difference between understanding staking and chasing a number.

Running a validator versus delegating

There are two fundamentally different ways to participate in staking, and the distinction determines how much you need, how much work is involved, and how most people actually stake.

Running your own validator means operating the software and infrastructure that validates transactions and produces blocks, putting up the network’s required stake yourself, and earning the full rewards directly.

This is the most hands-on and most rewarding form, but it is demanding: it usually requires a substantial minimum stake, often a large fixed amount set by the network, plus the technical ability to run validator software reliably around the clock, because a validator that goes offline or misbehaves can lose rewards or have part of its stake taken. Running a validator suits technically capable participants with significant holdings who want maximum control and reward and are willing to take on the operational responsibility. For most people, it is more than they need or want.

Delegating is the alternative that makes staking accessible to everyone else. Instead of running a validator, you delegate your cryptocurrency to an existing validator, lending them your stake to increase their weight in the network, and in return you receive a share of the rewards they earn, minus a small commission they keep.

Delegating requires no technical skill and usually no large minimum, so you can stake whatever amount you hold, and your tokens stay yours, you are backing a validator, not giving them your coins.

This is how the large majority of staking happens, because it lets ordinary holders earn staking rewards without operating infrastructure, simply by choosing a validator to support. The tradeoff is that you rely on that validator to perform honestly and reliably, since their failures can affect your rewards, which makes choosing a good validator the main decision a delegator makes.

The main ways to stake

Beyond the validator-versus-delegating distinction, staking is offered through several channels, and knowing them helps you pick the approach that fits your situation.

Exchange staking is the simplest entry point. Many centralized exchanges offer staking as a feature: you hold a proof-of-stake asset on the exchange, opt into staking with a click, and the exchange handles the validator operation, passing you rewards minus a fee. This is convenient and requires no technical knowledge, which makes it popular with beginners, but it is custodial, meaning the exchange controls your staked crypto, so you are trusting the platform with both your assets and the staking process.

Native or wallet-based delegation is the self-custody alternative: using a wallet that supports staking, you delegate directly to a validator from a wallet you control, keeping your keys while earning rewards. This preserves ownership and is the approach favored by those who want to stake without surrendering custody, at the cost of a little more involvement in choosing and managing a validator.

Liquid staking is a newer and more advanced approach worth knowing about. When you stake normally, your tokens are typically locked and illiquid for as long as they are staked, and often for an additional unbonding period when you withdraw. Liquid staking protocols address this by giving you a tradeable token representing your staked position, so you earn staking rewards while still holding an asset you can use or sell, restoring liquidity to staked capital.

Liquid staking is powerful and central to decentralized finance, but it adds a layer of smart-contract risk and complexity, which makes it an intermediate-to-advanced tool, not a beginner’s first step. For someone starting out, exchange staking or wallet-based delegation of a major proof-of-stake asset is the straightforward path, with liquid staking and validator operation as things to grow into.

The real risks the savings analogy hides

This is the section the hype skips, and it is the most important one, because staking carries genuine risks that the comparison to a savings account completely obscures.

The first risk is price volatility, and it is the one most likely to matter. Staking rewards are paid in the cryptocurrency you stake, and that asset’s price can fall far more than any yield can compensate for. A seven percent staking reward is worthless protection if the token drops fifty percent, and stakers have repeatedly earned a positive yield while losing money overall because the underlying asset declined.

Staking does not reduce your exposure to the asset’s price; it adds a yield on top of a position whose value can swing dramatically, and the yield is small next to the volatility.

The second risk is lockup and illiquidity: staked tokens are often locked and cannot be sold immediately, and withdrawing frequently involves an unbonding period of days or longer during which your tokens are neither earning nor accessible. If the price crashes while your tokens are locked, you may be unable to sell until the unbonding completes, which can turn a paper loss into a realized one.

The third risk is slashing, the penalty built into proof of stake. Because validators put up collateral to guarantee honest behavior, the network can take, or slash, part of that stake if the validator misbehaves or fails badly, and delegators backing a slashed validator can lose a portion of their delegated stake too. This is usually rare and tied to validator failures rather than ordinary participation, but it is a real risk that makes choosing a reliable validator important.

The fourth risk is custodial and smart-contract exposure: staking through an exchange means trusting that platform’s solvency and security, and staking through a liquid-staking protocol means trusting its smart-contract code, both of which have failed before.

None of these risks means staking is a bad idea, but together they show why the savings-account analogy is misleading: a savings account does not fall fifty percent in value, lock your money for a week, penalize you for a provider’s mistake, or depend on the solvency of an unregulated platform. Staking can be worthwhile, but only with eyes open to what it actually involves.

How to start staking

With the concepts and risks clear, getting started is straightforward, and the right first approach depends on how hands-on you want to be.

For a beginner, the simplest start is to hold a major proof-of-stake cryptocurrency on a reputable exchange that offers staking and opt into it, which requires no technical skill and lets you see how rewards accrue with minimal effort, accepting the custodial tradeoff in exchange for ease. A step up in control is to move the asset to a wallet that supports staking and delegate to a validator yourself, keeping custody of your keys while choosing which validator to back, which preserves ownership and teaches you how delegation works.

In choosing a validator, favor those with a strong track record of reliable uptime, a reasonable commission, and a solid reputation, since a good validator earns steady rewards and avoids the failures that lead to slashing, while a poor one can cost you. Whatever route you take, start with an amount you are comfortable holding for a while, given the lockups, and treat the yield as a bonus on a position you believe in, not as the reason to hold a token you otherwise would not.

A few principles keep staking sensible. Stake assets you would want to hold anyway, because staking does not protect you from the price risk of an asset you do not believe in, and the yield will not save you from a token that falls. Understand the lockup and unbonding terms before you stake, so you are not caught unable to sell when you need to. Read the staking yield as a nominal, partly-inflationary figure, not as guaranteed interest, and judge it against the network’s issuance and your view of the token.

And match the method to your level: exchange staking or wallet delegation to start, with liquid staking and validator operation as later steps. Followed this way, staking becomes a reasonable way to earn a return on long-term holdings, instead of a yield chase that ends in disappointment when the underlying asset moves against you.

Yield with your eyes open

Staking is a genuine and widely available way to earn a return on proof-of-stake cryptocurrency by locking up your tokens to help secure a network and receiving rewards for doing so. It is accessible to anyone through exchange staking or wallet-based delegation, it does not require running infrastructure unless you want to, and on the right asset held for the right reasons, it can be a sensible way to make long-term holdings productive.

The mechanics are not complicated once the core idea is clear: proof of stake secures the network through committed capital, and staking is how holders contribute that capital and get paid for it.

What separates wise staking from naive yield-chasing is understanding what the yield really is and what it costs. The advertised percentage is not interest from a savings account; it is compensation for providing security and for accepting real risks, funded partly by the network issuing new tokens, and it sits on top of an asset whose price can fall far more than the yield can offset, whose tokens may be locked when you most want to sell, and whose validators or platforms can fail.

Stake assets you believe in, understand the lockups and the source of the yield, choose reliable validators or reputable platforms, and treat the reward as a bonus, not a reason. Do that, and staking becomes one of the more reasonable ways to earn in crypto. Chase the highest advertised number without understanding it, and the risks the hype hides will eventually find you. The yield is real, but so is everything underneath it.

Frequently Asked Questions

What is crypto staking in simple terms?

Staking means locking up a proof-of-stake cryptocurrency to help secure its network, and earning rewards in return, usually quoted as an annual percentage yield. By staking, you contribute your tokens to the collateral that secures the blockchain, either by running a validator or by delegating to one, and you receive a share of the rewards the network pays for that security. It is often compared to earning interest, but the rewards come from network issuance and fees, not from lending.

Where do staking rewards actually come from?

Staking rewards come primarily from two sources: new cryptocurrency the network issues to reward those who secure it, and transaction fees paid by network users. The new-issuance portion is usually larger and increases the token’s total supply, so part of a staking yield is funded by inflation rather than being interest in the traditional sense. This means the real value of a yield depends on how much new supply the network is creating to pay it.

What is the difference between running a validator and delegating?

Running a validator means operating the software that secures the network, putting up a large required stake, and earning full rewards, which demands technical skill and significant capital. Delegating means backing an existing validator with your tokens and receiving a share of their rewards minus a commission, with no technical skill or large minimum required and your tokens remaining yours. Most people delegate, because it makes staking accessible without operating infrastructure.

What are the risks of staking?

The biggest risk is price volatility: the staked asset can fall far more than any yield compensates for, so you can earn rewards and still lose money. Staked tokens are often locked, with an unbonding period when you withdraw, so you may be unable to sell during a crash. Slashing can take part of your stake if a validator misbehaves. And staking through an exchange or a liquid-staking protocol adds custodial or smart-contract risk. A savings account has none of these risks, which is why the comparison is misleading.

Is staking the same as earning interest in a savings account?

No, though it is often compared to one. The analogy captures the appeal of earning a return on assets you hold, but it hides important differences. Staking rewards come from network issuance and fees, not from lending, and are funded partly by inflation. The staked asset’s price can fall sharply, tokens can be locked when you want to sell, validators can be slashed, and platforms can fail. A savings account carries none of these risks, so staking yields should not be read as risk-free interest.

How do I start staking as a beginner?

The simplest start is to hold a major proof-of-stake cryptocurrency on a reputable exchange that offers staking and opt in, which requires no technical skill. For more control, move the asset to a wallet that supports staking and delegate to a validator yourself, keeping custody of your keys. Choose validators with reliable uptime, reasonable commission, and a good reputation. Stake assets you would hold anyway, understand the lockup terms, and treat the yield as a bonus rather than the reason to hold.

This guide is educational information, not financial advice. Staking carries real risks, including price volatility, lockups, slashing, and platform failure. Research any asset and platform independently and only stake what you can afford to lock up and potentially lose.

Key Takeaways

- Following Coinbase’s System Update event, Cantor Fitzgerald maintained its Overweight rating with a $250 price target

- The crypto platform introduced multiple new offerings: tokenized stocks, perpetual contracts, options trading, an AI trading assistant, and a consolidated liquidity framework

- Cathie Wood’s Ark Invest purchased $18.4 million in Coinbase shares distributed among three funds (ARKK, ARKW, ARKF) at $164.92 per share

- Shares finished Wednesday’s session down 2.57%, marking a nearly 13% drop over the trailing month and trading 62% beneath the $444.64 52-week peak

- Several firms adjusted their outlook: Baird reduced its target to $142 from $160, Barclays maintains an Underweight stance at $107, and Monness shifted to Sell at $115

Coinbase (COIN) shares are currently hovering between $164 and $169, reflecting a roughly 31% decline across the last half-year and positioned 62% under the $444.64 yearly high. While facing headwinds from tepid market conditions, the cryptocurrency platform continues advancing its product development agenda.

Tuesday brought major announcements from Coinbase, including the rollout of tokenized equities — digital representations of traditional U.S. stocks built on blockchain infrastructure that customers can purchase, store, and exchange. Additionally, the platform introduced an artificial intelligence-driven trading assistant alongside a comprehensive liquidity framework merging its domestic and global spot cryptocurrency and derivatives operations.

These developments emerged during Coinbase’s System Update presentation, triggering varied commentary from financial analysts across the industry.

Cantor Fitzgerald maintained its Overweight designation while preserving the $250 price objective. The research firm highlighted that Coinbase’s innovation momentum remains intact even amid subdued crypto market activity, noting that competitive dynamics in financial services are transitioning toward application- and wallet-centric platforms.

Cantor further emphasized blockchain infrastructure as a catalyst expanding both transaction speed and market access for financial products, positioning Coinbase favorably to capitalize on this evolution.

Benchmark Equity Research similarly upheld its Buy recommendation, characterizing the product launches as evidence that Coinbase is diversifying beyond its core cryptocurrency exchange operations.

Divergent Analyst Perspectives

However, sentiment wasn’t uniformly optimistic. Baird slashed its price objective to $142 from $160, referencing lackluster trading activity and projecting that second-quarter revenue will miss consensus estimates by 5% to 6%. Monness, Crespi, Hardt moved to a Sell rating with a $115 target, highlighting ambiguity surrounding the CLARITY legislative framework. Barclays retained its Underweight position with a $107 valuation.

Current analyst price targets span from $107 on the conservative end to $400 on the bullish side — an exceptionally broad range illustrating the significant disagreement among market observers regarding Coinbase’s trajectory.

Ark Invest Makes Its Move

Despite downward pressure on shares, Cathie Wood’s Ark Invest executed a significant purchase on Wednesday. The investment firm acquired 111,799 Coinbase shares distributed across its ARKK, ARKW, and ARKF exchange-traded funds at Wednesday’s closing price of $164.92, totaling approximately $18.4 million.

Within Ark’s flagship ARKK fund, Coinbase currently occupies the eighth-largest position at 3.71% allocation, representing roughly $258.6 million in market value.

During the same trading activity, Ark accumulated $17.2 million in Block shares while reducing its Robinhood holdings by approximately $29 million. Despite the trimming, Robinhood maintains a prominent position in ARKK at 4.87%, valued at approximately $339.6 million.

This Coinbase acquisition echoes a comparable transaction Ark executed in May, when the firm purchased roughly $4.4 million in Bullish stock following five straight sessions of declines.

Separately, Coinbase recently unveiled a collaboration with MassPay Holdings to deliver stablecoin-facilitated international payment solutions, combining MassPay’s distribution infrastructure with Coinbase’s digital asset platform capabilities.

COIN shares concluded Wednesday’s trading at $164.92, representing a 2.57% intraday decline.

G7 leaders broadened their warning over North Korean crypto theft to include wider cybercrime as researchers link DPRK-affiliated actors to billions of dollars in stolen digital assets.

The GBP/JPY pair has come under pressure after the Bank of Japan raised its policy rate to 1.0% on 16 June. The Bank of England is following the opposite path: at its 30 April meeting, the Monetary Policy Committee (MPC) voted 8–1 to keep the base rate at 3.75%, with one member advocating an increase to 4%. The June MPC meeting, scheduled for 18 June, is expected by analysts to result in another hold, as inflation remains above the target level. The narrowing interest rate differential between the two central banks continues to build a fundamentally supportive backdrop for the yen.

Technical Picture

On the 4-hour GBP/JPY chart, an ascending triangle structure can be observed: since 8 June, an upward-sloping support has been forming against a horizontal resistance near the red 215.60 level. On 17 June, a strong bearish candle formed on elevated volume, and price broke below the pattern as well as the current market profile. If the downward momentum continues, the next key level on the downside is 213.00, which represents the base of the pattern.

In the event of a reversal, price may find support at the lower boundary of the profile at 214.35 and the POC zone at 214.65–214.70. If the upward move resumes and buyers manage to break above the upper profile boundary at 215.20, the 215.60 resistance area would come back into focus. RSI + MAs shows readings of 35, 50, 51 — the oscillator is approaching oversold territory, while its moving averages remain in neutral conditions.

Key Takeaways

The narrowing interest rate gap between the Bank of Japan and the Bank of England is creating a fundamentally supportive environment for the yen. RSI is approaching oversold levels, although the MAs remain in neutral territory. The next directional move is likely to be driven by the Bank of England’s decision on 18 June.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

CoinMENA will use Standard Chartered to strengthen fiat payment rails in the UAE, while Revolut reportedly secured central bank licenses ahead of a planned local launch.

HIVE Digital Technologies Ltd. (TSX: HIVE, NASDAQ: HIVE) said the Boden Municipal Council in Sweden approved its acquisition of the Big Boden 32 MW data center. The company did not provide a transaction value in the announcement, and the purchase remains subject to customary closing conditions.

The approval marks a shift for HIVE at the site it has operated since 2018. Instead of renting capacity, HIVE will move toward full ownership, giving it greater control over long-term facility plans and the site’s eventual role in enterprise-scale AI and high-performance computing workloads.

From tenant to owner at the Big Boden site

HIVE said the acquisition is of the Big Boden 32 MW facility owned by Bodens Utvecklings AB. The company framed the move as the next step in an eight-year relationship with the municipality and local stakeholders, built around renewable energy procurement and operational investment in the region.

In the release, HIVE said its Swedish activities have involved more than 960 million SEK (about $100 million) invested in Boden over eight years through local contractors and renewable energy sourcing. It also said it paid more than 575 million SEK (over $60 million) in taxes to the Swedish Tax Authority during that period.

HIVE also described non-operational community involvement tied to the region, including sponsorship of local youth sports and naming rights for HIVE Arena. It said the company continues to work with Boden Municipality and RISE, the Swedish research institute, to explore using heat generated by the data center for broader community applications.

What the acquisition means for compute expansion

Data center owners and operators have increasingly treated site control as a strategic lever for expanding AI and HPC capacity. Ownership can reduce some long-term dependency risks associated with tenancy arrangements, especially when upgrades, security configurations, and power delivery depend on multi-year planning.

HIVE said that following closing, it will advance the Big Boden data center toward Tier III infrastructure standards. Tier III is commonly used as a benchmark for redundancy and uptime requirements in enterprise environments, which can be important for customers running latency-sensitive and compute-intensive AI and HPC workloads.

The company also referenced support for modern GPU architectures for AI training and inference, positioning the Swedish facility as part of a broader buildout of renewable-powered infrastructure across Canada, Sweden, and Paraguay.

While the announcement describes intended upgrades, it did not specify timelines beyond the statement that conversion to Tier III standards will occur after closing and as conditions allow. For investors and buyers of compute services, that timing matters because AI infrastructure deployments are often constrained by power availability, grid interconnection, and permitting.

Energy strategy and heat reuse in Europe’s data center market

Europe’s data center sector is under pressure to secure power while meeting sustainability expectations from regulators, customers, and local authorities. HIVE’s mention of heat reuse reflects a broader pattern across the industry, where thermal recovery is increasingly used to improve efficiency and align projects with municipal energy planning.

HIVE said it has pursued heat reuse initiatives in other regions as well, including Canada, where it participates in projects intended to redirect thermal energy back into local use. The company did not provide additional technical detail about how heat recovery at Boden would operate, but the concept has been a recurring theme in discussions with city governments across the Nordics and wider Europe.

Community partnership as a longer-term operating model

HIVE’s release places substantial emphasis on local investment and ongoing engagement. This approach is not new in data center development, but the trend has gained attention as many projects face scrutiny over land use, energy consumption, and grid strain.

The municipality approval effectively converts HIVE’s role at the site from operator under a landlord arrangement to a full owner operator, which can strengthen its ability to coordinate facility upgrades with the local energy and heat strategy. It may also affect how residents and local institutions evaluate the company’s long-term footprint.

At the same time, the company’s stated community investments do not replace the operational realities of building and maintaining mission-critical compute capacity. In practice, projects succeed when power, cooling, security, and permitting align with customer demand for AI and cloud workloads.

Transaction status and next steps

HIVE said the acquisition is subject to completion of customary closing conditions. The company indicated it will provide further details as the transaction process progresses. Until closing, the broader operational and upgrade plan at the Big Boden site remains subject to deal completion and subsequent engineering execution.

For the crypto mining and AI compute intersection that HIVE has positioned itself around, the move underscores a continuing shift toward enterprise-grade infrastructure. In a market where compute providers are competing for customers who need predictable uptime and scalable capacity, control over key assets can be a decisive factor.

Every crypto trade comes down to a choice between two basic order types: take the price now, or name your price and wait. Understanding the difference, and the stop-loss and slippage that come with it, is the foundation of trading without losing money to your own mistakes.

Summary

- Market orders prioritize immediate execution, while limit orders execute only at a user specified price.

- Slippage can affect trade execution prices, especially in volatile or low liquidity markets.

- Stop loss orders help cap potential losses by automatically exiting a position when a preset price level is reached.

Placing a crypto trade comes down to a deceptively simple question: do you want to buy or sell right now at whatever the market price is, or do you want to set your own price and wait for the market to come to you? Those two choices are the market order and the limit order, the two fundamental building blocks of every trade on every exchange, and understanding the difference between them is the foundation of trading crypto deliberately rather than blindly.

Most beginners click “buy” without knowing which order type they are using or what tradeoff they are making, and that ignorance quietly costs them money, in worse prices, in orders that fill at the wrong moment, and in missed protection against losses.

This guide explains the two core order types in plain terms: what a market order is and when to use it, what a limit order is and what it gives you, the crucial concept of slippage that connects them, and the stop-loss order that protects you from large losses. It also covers how these tools fit together in practice and the order-book mechanics underneath them, so you understand not just which button to click but why.

None of this is complicated once explained clearly, and learning it is the difference between being a trader who controls their entries and exits and one who is at the mercy of the market and their own haste. Whether you ever trade actively or simply buy and hold, knowing how orders work makes every transaction you place a more informed one.

The order book: what you are actually trading against

Before the order types make sense, you need a picture of what is happening when you place a trade, and that means understanding the order book.

Every exchange matches buyers and sellers through an order book, a live list of all the orders people have placed but not yet had filled. On one side are the buy orders, people offering to buy at various prices, and on the other are the sell orders, people offering to sell at various prices. The highest price a buyer is currently willing to pay is the bid, the lowest price a seller is currently willing to accept is the ask, and the small gap between them is the spread.

The current market price you see quoted is essentially where the most recent trades happened, sitting between the best bid and the best ask. When you place a trade, you are interacting with this book, either taking an order that is already sitting there or adding your own order to it and waiting, and which of those you do is exactly what the choice between a market order and a limit order determines.

This matters because the order book is not infinitely deep at any single price. There might be only so much crypto offered for sale at the current ask, and more available only at higher prices, and the same in reverse for buyers. A small order can be filled entirely at or near the current price because there is enough sitting there to match it, but a large order may have to eat through multiple price levels to fill completely, getting progressively worse prices as it consumes the available orders. This depth, or lack of it, is what produces slippage, the concept that ties the order types together, and it is why the same kind of order can behave very differently for a small trade and a large one. Keeping the order book in mind turns order types from abstract options into a concrete picture of what your trade is actually doing.

The market order: take the price now

The market order is the simplest and most common, and it answers the question “how do I just buy or sell this immediately?”

A market order executes immediately at the best price currently available in the order book. When you place a market buy, the exchange fills it against the lowest-priced sell orders sitting on the book, starting with the best ask and working up if needed until the order is filled; a market sell does the reverse, hitting the highest-priced buy orders.

The defining feature of a market order is certainty of execution: it will fill, and it will fill right away, because it simply takes whatever prices are available until the order is complete. This is what you want when getting the trade done matters more than getting a precise price, when you want to own an asset now, exit a position now, or act on a decision without waiting. For most ordinary buying and selling, especially in smaller amounts on liquid assets, the market order is the natural, sensible choice.

The tradeoff is that a market order gives you certainty of execution but not certainty of price. You accept whatever prices the order book offers, and in a fast-moving or thin market, that can be meaningfully different from the price you saw a moment before you clicked. For a small trade on a heavily traded asset like Bitcoin, the difference is usually negligible, because there is plenty of volume sitting at or near the current price to fill your order cleanly.

But for a large trade, or on a thinly traded asset with little depth, a market order can fill at a noticeably worse average price than expected as it eats through the book, which is the slippage problem. The market order’s simplicity and reliability are its strengths, and for most beginner-sized trades they outweigh the price imprecision, but understanding that you are trading price certainty for execution certainty is what lets you use it wisely.

The limit order: name your price and wait

The limit order answers a different question: “what if I do not want to pay the current price, but a specific price of my own choosing?”

A limit order lets you set the exact price at which you are willing to buy or sell, and the order executes only if and when the market reaches that price. A limit buy at a price below the current market sits on the order book waiting, and fills only if the price falls to your level; a limit sell at a price above the market waits and fills only if the price rises to meet it.

The defining feature of a limit order is control over price: you will never pay more than your limit on a buy or accept less than your limit on a sell, because the order simply will not execute outside your specified price. This is what you want when the price matters more than immediacy, when you believe an asset is currently a little overpriced and would rather buy lower, or when you want to sell at a target you have set and are willing to wait for.

The tradeoff is the mirror image of the market order: a limit order gives you certainty of price but not certainty of execution. If the market never reaches your specified price, the order never fills, and you may sit waiting for a level the market simply does not visit, missing the trade entirely while the price moves away from you. A limit buy set too low may never trigger as the asset rises without you; a limit sell set too high may never trigger as the asset falls.

So the limit order trades the guarantee of getting the trade done for the guarantee of getting your price, which is the exact opposite of the market order’s bargain. Limit orders are the tool of the deliberate trader who cares about entry and exit prices and is willing to wait or to miss a trade instead of accepting a price they do not want, and they become more valuable as you grow more precise about the levels at which you want to act.

Slippage: the concept that connects them

Slippage is the idea sitting underneath both order types, and understanding it explains why the choice between them matters and when each one bites.

Slippage is the difference between the price you expected and the price you actually got. It arises from the order book’s limited depth and from price movement between the moment you place an order and the moment it fills. A market order is exposed to slippage by design, because it accepts whatever prices the book offers: if your order is large or the book is thin, it eats through multiple price levels and fills at a worse average price than the quote you saw, and if the price moves in the instant your order executes, you get the new price, not the old one.

This is why a market order on a large amount or an illiquid asset can surprise you with a fill noticeably worse than expected, while the same order on a small amount of a liquid asset fills cleanly with negligible slippage. The depth of the order book is what determines how much slippage a market order suffers.

A limit order is the tool that protects you from slippage, because by naming your price you refuse to accept anything worse than it. The limit order will not slip past your specified level, which is precisely its value in volatile or thin markets where a market order could fill at a bad price. The cost of that protection is the execution risk already described: the order may not fill at all.

So the relationship between the two order types and slippage is clean: market orders accept slippage in exchange for guaranteed execution, and limit orders eliminate slippage in exchange for accepting that the order might not execute. Knowing this lets you choose deliberately, reaching for a market order when you want certainty of getting filled and the asset is liquid enough that slippage will be small, and for a limit order when you want to control your price and protect against slippage in a volatile or thin market, accepting that you might wait or miss the trade.

The stop-loss: protecting yourself from large losses

Beyond the two core order types is a third tool every trader should understand, because it is the main defense against a position going badly wrong.

A stop-loss is an order that automatically sells your position if the price falls to a level you set in advance, designed to limit your loss on a trade that moves against you. You decide, when you enter a position, the price at which you would want to cut your losses and exit, and you place a stop-loss at that level; if the market drops to it, the stop-loss triggers and sells, capping your loss rather than letting it deepen while you watch or hesitate.

The value of a stop-loss is that it removes emotion and inattention from the most dangerous moment in trading, the falling market, by deciding your exit in advance and executing it automatically, so you are not relying on yourself to act decisively while a position is collapsing and your instinct is to hope it recovers. For anyone holding a position they could not afford to see fall much further, a stop-loss is the standard protective tool.

Stop-losses come with their own nuances worth knowing. A basic stop-loss typically triggers a market order when the level is hit, which means it sells immediately but is exposed to slippage, potentially filling below your stop price in a fast crash, while a stop-limit version triggers a limit order, protecting your price but risking that it does not fill if the market gaps straight through your level.

In very fast or volatile moves, a stop-loss can fill worse than the set level because of slippage, which is the same order-book reality that affects market orders. And a stop-loss set too tight, too close to the current price, can be triggered by normal volatility and sell you out of a position that then recovers, while one set too loose offers little protection. Used thoughtfully, with the level chosen to reflect how much you are willing to lose and the normal swings of the asset, a stop-loss is one of the most important risk-management tools a trader has, and it is the practical application of the order types to the problem of protecting capital.

How it fits together in practice

With the tools defined, the practical question is when to use each, and a few clear principles cover most situations.

Use a market order when execution matters more than precision: when you want to buy or sell now, the asset is liquid enough that slippage will be small, and you would rather guarantee the trade than chase a perfect price. This covers most ordinary buying and selling, especially in smaller amounts on major assets, and it is the right default for a beginner who simply wants to own or exit a position.

Use a limit order when price matters more than immediacy: when you have a specific level at which you want to buy or sell, you are willing to wait or to miss the trade rather than accept a worse price, or you are trading a large amount or a thin asset where a market order would slip badly. The limit order is the tool of deliberate entries and exits and of protecting yourself against slippage. And use a stop-loss whenever you hold a position you want to protect from a large loss, setting the exit level in advance so that a falling market triggers your sale automatically instead of depending on your judgment in the moment.

These tools combine in real trading. A common pattern is to enter with a limit order at a price you find attractive, then immediately set a stop-loss below your entry to cap the downside if you are wrong, and perhaps a limit sell above to take profit at a target, so that both your exit on a loss and your exit on a gain are defined in advance and execute without you having to watch the market constantly. A beginner does not need to run elaborate setups, but understanding that orders can be combined to control both entry and exit, and to protect against the worst outcomes, is what separates trading deliberately from clicking buy and sell on impulse. The order types are the vocabulary of trading, and fluency in them lets you express a plan rather than merely react.

The foundation of every trade

Every crypto trade, however simple or sophisticated, is built from a small set of order types, and understanding them is the foundation of trading without being undone by your own haste. A market order takes the current price and guarantees execution, accepting slippage as the cost, and it is the right tool when getting the trade done matters most and the asset is liquid.

A limit order names your price and guarantees you will not do worse than it, accepting that the order may not fill, and it is the tool of deliberate entries, exits, and protection against slippage. Slippage, the gap between expected and actual price, is the concept that connects them and explains when each one matters. And the stop-loss applies these mechanics to the essential job of limiting losses, deciding your exit in advance so a falling market cannot depend on your nerve.

The deeper point is that order types turn trading from a reaction into a decision. The beginner who clicks buy without knowing the order type is accepting whatever the market gives, exposed to slippage they did not anticipate and with no plan for when to exit, while the trader who understands these tools chooses their price when it matters, protects against slippage when it could hurt, and defines their losses before they happen, not after.

None of this requires advanced skill or constant attention; it requires knowing the handful of order types and what each one trades away. Learn them, and every transaction you place, whether a one-time purchase or an active trade, becomes something you control, not something that controls you. That control, more than any prediction or strategy, is the real foundation of trading crypto sensibly.

Frequently Asked Questions

What is the difference between a market order and a limit order?

A market order executes immediately at the best price currently available, guaranteeing the trade gets done but accepting whatever price the order book offers. A limit order lets you set a specific price and executes only if the market reaches it, guaranteeing your price but not that the order fills. In short, a market order gives certainty of execution at the cost of price control, while a limit order gives price control at the cost of certain execution.

When should I use a market order?

Use a market order when getting the trade done matters more than getting a precise price: when you want to buy or sell immediately, and the asset is liquid enough that slippage will be small. For most ordinary buying and selling in smaller amounts on major assets like Bitcoin, a market order is the simple, sensible choice. It is the right default for a beginner who simply wants to own or exit a position without managing the timing or price.

What is slippage in crypto trading?

Slippage is the difference between the price you expected and the price you actually got. It happens because the order book has limited depth and prices move between placing and filling an order. Market orders are exposed to slippage because they accept whatever prices are available, so a large order or one on a thinly traded asset can fill at a worse average price. Limit orders protect against slippage by refusing to execute beyond your set price.

What is a stop-loss order and how does it work?

A stop-loss automatically sells your position if the price falls to a level you set in advance, limiting your loss on a trade that moves against you. You decide your exit price when entering, and if the market drops to it, the stop-loss triggers and sells. It removes emotion and hesitation from a falling market by deciding the exit ahead of time. Note that a basic stop-loss can still fill below your level due to slippage in a fast crash.

Which order type is better for beginners?

For most beginner situations, a market order is the simpler and more practical choice, because it guarantees the trade fills and, on a liquid asset in a small amount, slippage is negligible. Limit orders become valuable as you grow more deliberate about the prices at which you want to buy or sell, or when trading larger amounts or thinner assets where slippage matters. Learning both, plus the stop-loss for protection, gives you the full beginner toolkit.

Can I use these order types together?

Yes, and experienced traders routinely do. A common pattern is to enter a position with a limit order at an attractive price, set a stop-loss below the entry to cap the downside if the trade goes wrong, and place a limit sell above to take profit at a target. This defines both the loss exit and the gain exit in advance, so they execute automatically without constant monitoring. Beginners do not need elaborate setups, but knowing the tools combine lets you trade to a plan.

This guide is educational information, not financial or trading advice. Trading crypto carries real risk of loss. Order types manage how trades execute but do not eliminate market risk, and you should only trade with money you can afford to lose.

York region unemployment rises in younger age bracket

BMW board chief says Chinese market has space for non-Chinese brands

What Happened in Crypto Legal News this Week

-

Business4 days ago

Business4 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World7 days ago

Crypto World7 days agoOppenheimer backs SpaceX as $70 billion retail frenzy builds

-

Crypto World7 days ago

Crypto World7 days agoMarkets Rally as SpaceX IPO Looms Amid Iran Tensions and Inflation Surge

-

Crypto World4 days ago

Crypto World4 days agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Crypto World5 days ago

Crypto World5 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Tech5 days ago

Tech5 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

Tech6 days ago

Tech6 days agoThis Week In Security: Microsoft On Microsoft, Register Your Domains, Linux On ARM, And FreeBSD Joins The File Cache Club

-

NewsBeat7 days ago

NewsBeat7 days agoEl Nino has formed in the Pacific and could set records, forecasters say

-

Tech7 days ago

Tech7 days agoDutton Ranch star claims they ‘didn’t see any disruption’ on set following Chad Feehan’s exit from Yellowstone spinoff fueled by Taylor Sheridan clash rumors

-

Politics7 days ago

Politics7 days agoPolitics Home | Healey Resignation Is “Colossal Failure Of Government”, Says Former Labour Defence Secretary

-

Entertainment7 days ago

Entertainment7 days agoDonnie Wahlberg & More Heat Up Las Vegas at Circa’s Barry’s Downtown Prime

-

Sports7 days ago

Sports7 days agoFirst Time Since 1971: Australia Register Historic Low In ODI Cricket

-

Tech7 days ago

Tech7 days agoOpendoor Ends India Operations, Fueling a Bigger Conversation About AI and Outsourcing

-

Politics7 days ago

Politics7 days agoBelfast burns, while Met chief points finger at Iran and Russia

-

Business7 days ago

Business7 days agoAT&T: Verizon's 27% Outperformance Sets Up A Solid Entry Point

-

NewsBeat6 days ago

NewsBeat6 days agoFBI searches office of Ohio voter registration group

-

Tech6 days ago

Tech6 days agoAnthropic is spending $150M to embed 1,000 AI fellows inside nonprofits. No degree required.

-

Politics7 days ago

Politics7 days agoModi thanks Trump for wishes as US attacks Indian seafarers

-

Entertainment6 days ago

Entertainment6 days ago‘The Pitt’s Fan-Favorite Doctor Confirms Noah Wyle Gave His Blessing to Return [Exclusive]

You must be logged in to post a comment Login