Crypto World

EU Lawmakers Back Review of DeFi, Staking and NFT Regulation

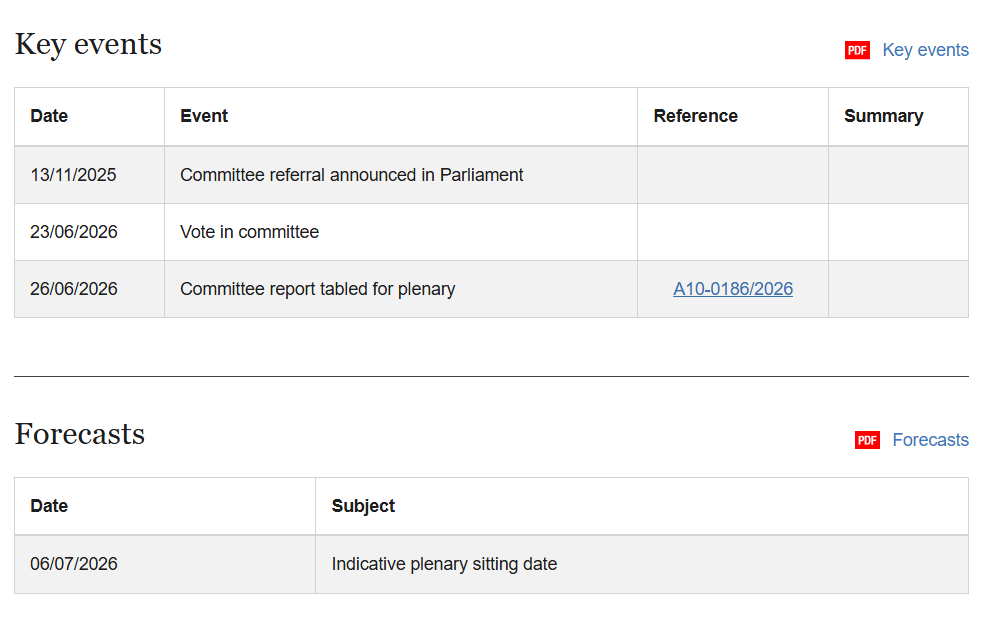

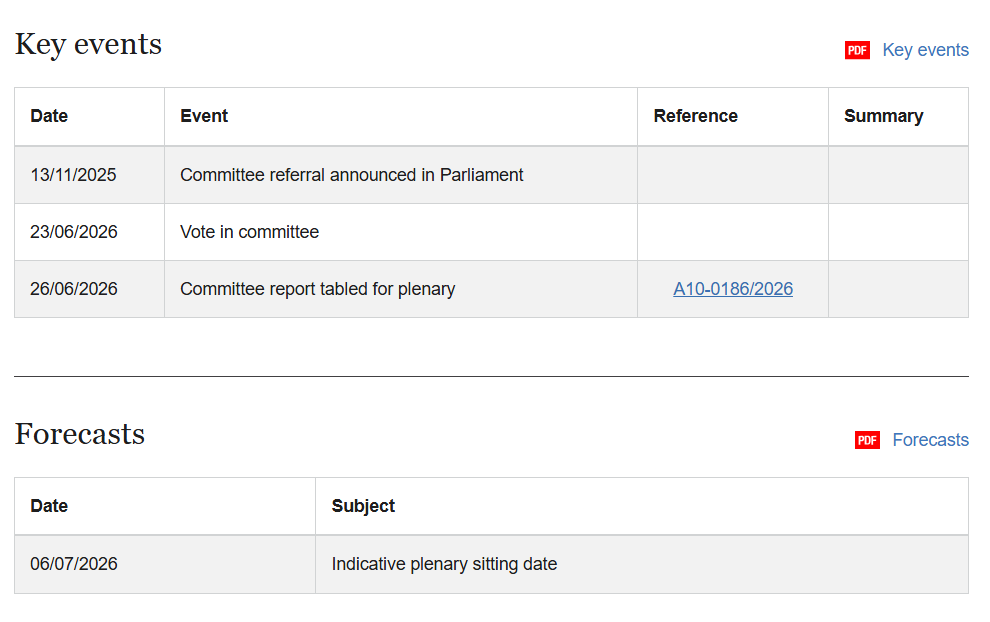

The European Parliament’s economic affairs committee has urged the European Commission to assess whether crypto lending and borrowing, staking, non-fungible tokens (NFTs) and decentralized finance (DeFi) should be regulated.

The recommendations were part of a report tabled Friday for plenary vote. It also called for promoting tokenization across financial services, encouraging euro-denominated stablecoins and assessing whether additional crypto activities should be regulated under the European Union’s Markets in Crypto-Assets Regulation (MiCA).

Drafted by Belgian Member of the European Parliament Johan Van Overtveldt, the report is an own-initiative resolution by the Committee on Economic and Monetary Affairs (ECON) that outlines recommendations for the Commission on digital asset regulation.

It will next go before the European Parliament for a vote, expected July 7. If adopted, the resolution would become Parliament’s official position on digital assets policy but would not amend MiCA or create new legal obligations.

The legislative timeline shows the committee’s approval of the report and its referral for a plenary vote. Source: European Parliament

Related: European Parliament throws support behind digital euro

EU warms up to regulated stablecoins

The recommendations also reflect an evolving view of stablecoins among policymakers. Days after former Bank for International Settlements general manager and longtime crypto critic Agustín Carstens softened his stance on stablecoins, the report welcomed euro-denominated stablecoins under MiCA and encouraged their development to support the bloc’s payment sector.

In 2023, Van Overtveldt called for tighter restrictions on cryptocurrencies following the banking turmoil surrounding Silicon Valley Bank, Signature Bank and Silvergate Bank. The crisis was also closely tied to stablecoins, as USDC issuer Circle held roughly $3.3 billion of its reserves at Silicon Valley Bank when it collapsed, briefly causing USDC to lose its dollar peg.

Van Overtveldt likened cryptocurrencies to drugs during the 2023 banking crisis. Source:Johan Van Overtveldt

The report argued that euro-denominated stablecoins could complement tokenized commercial bank deposits and wholesale central bank digital currencies while enabling faster and cheaper cross-border payments. It also said broader adoption could strengthen the competitiveness of EU financial markets and the international role of the euro.

The stance also aligns with ECON’s broader vision for Europe’s digital money ecosystem. On Tuesday, the committee backed legislation for a digital euro, with lawmakers arguing that public and private forms of digital money should coexist rather than compete.

Related: Poland president vetoes MiCA bill again as crypto companies look to license abroad

Lawmakers look beyond MiCA’s current scope

Van Overtveldt first presented a draft of the report in February before months of negotiations and amendments by ECON members. The earlier version largely focused on MiCA’s existing framework, including stablecoin classifications and legal certainty for multi-issued stablecoins.

The committee-approved report urged consistent application of MiCA across the EU to preserve a level playing field for crypto firms. It also warned member states against introducing national requirements beyond MiCA that could fragment the bloc’s digital asset industry.

The Commission is already reviewing MiCA. In May, the Commission launched a public consultation seeking feedback on whether the framework should be expanded to cover areas including DeFi, staking, lending, NFTs and tokenized financial assets, while also reopening debate over the regulation’s ban on interest-bearing stablecoins.

Meanwhile, MiCA’s transitional period ends July 1, after which crypto asset service providers generally must hold authorization under the regulation to continue operating across the EU.

Magazine: AI is banking the unbanked in Africa… faster than crypto

Every time you send crypto from one exchange to another above a certain amount, your identifying information may travel with it, shared between the platforms behind the scenes. That is the Travel Rule, a decades-old banking standard now reshaping crypto. This guide explains what it requires, why it exists, and what it means for your privacy.

Summary

- The Travel Rule is an anti-money-laundering requirement that obliges crypto service providers to collect, share, and retain identifying information about the sender and recipient of transfers above a set threshold.

- It originated in traditional banking under the US Bank Secrecy Act and was extended to crypto in 2019 by the Financial Action Task Force, the global anti-money-laundering body.

- The information travels off-chain through secure messaging between providers, so it does not appear on the blockchain itself, and it applies to exchanges, custodial wallets, and similar businesses, not direct peer-to-peer transfers.

- Thresholds vary widely by country, from the US figure of $3,000 to the European Union’s zero threshold, where every transfer requires compliance regardless of amount.

- The rule reduces the anonymity once associated with crypto and raises privacy and data-security questions, while its uneven global adoption, known as the sunrise problem, leaves gaps in enforcement.

The Travel Rule is an anti-money-laundering requirement that obliges financial institutions and crypto service providers to collect, share, and retain identifying information about both the sender and the recipient of a transfer above a certain value, so that the data effectively travels alongside the transaction. In the crypto context, this means that when you send digital assets above a threshold from one regulated platform to another, your platform may be required to transmit details about you, and to receive details about the recipient, behind the scenes.

The name comes from this idea of information traveling with the transfer, and the concept is not new: it has governed bank wire transfers for decades. What is new, and what makes it one of the most consequential pieces of crypto regulation in 2026, is that the same standard now applies to virtual assets, bringing crypto transfers under the kind of anti-money-laundering scrutiny long applied to traditional bank wires

For users accustomed to thinking of crypto as private or pseudonymous, the Travel Rule represents a significant shift, because it weaves identity and traceability into transfers that once felt anonymous.

Understanding the Travel Rule matters because it sits at the intersection of three related concepts that often get confused: know-your-customer checks, anti-money-laundering frameworks, and the specific obligation to share counterparty information on transfers. It also has real, practical consequences for how exchanges operate, what information they must gather from you, and how much privacy you can expect when moving crypto between regulated platforms.

This guide explains where the Travel Rule came from, how it was extended to crypto, exactly what information must be shared and how, who is covered and who is not, the wide variation in thresholds across countries, how the rule fits together with know-your-customer and anti-money-laundering obligations, a concrete worked example, and the genuine limits and privacy questions the rule raises.

The goal is to give you a clear picture of a regulation that increasingly shapes the everyday experience of using crypto, without either downplaying its reach or exaggerating its grip.

Where the Travel Rule came from

The Travel Rule did not begin with crypto; it began with banks, and its history explains both its logic and its name. In the United States, the rule traces back to the Bank Secrecy Act, the long-standing law designed to combat money laundering, and to guidance issued by the Financial Crimes Enforcement Network in the 1990s.

For decades, banks have been required to include identifying information, such as names and account numbers, when they pass funds from one institution to another in a wire transfer above a certain amount. The purpose was straightforward: by making identifying information travel with the money, regulators gained the ability to trace funds and flag suspicious activity, creating an auditable trail that makes it harder for illicit money to move undetected through the financial system. This original Travel Rule applied to traditional financial institutions and the wires they sent between one another.

When cryptocurrency emerged, and transactions began happening globally and at scale, regulators recognized that the same money-laundering risks applied, and that crypto’s pseudonymity could make it attractive for moving illicit funds.

The body that drove the extension to crypto is the Financial Action Task Force, an international organization that sets anti-money-laundering standards that countries around the world adopt into their own laws. In 2019, the Financial Action Task Force updated its guidance, specifically a provision known as Recommendation 16, to make clear that the Travel Rule should apply to virtual assets and to the businesses that handle them.

This extension meant that crypto exchanges, custodians, and similar providers would need to follow rules similar to those long applied to banks, collecting and sharing sender and recipient information on qualifying transfers. The guiding principle the Financial Action Task Force articulated was same risk, same rules: activities that carry similar money-laundering risks should face similar standards regardless of the technology involved.

Since 2019, countries have been writing their own versions of the crypto Travel Rule into national law, which is why the rule now exists worldwide but with meaningful variations from one jurisdiction to the next.

What information must be shared, and how

The substance of the Travel Rule is the specific information that must accompany a qualifying transfer, and understanding it clarifies what the rule actually does. When a transfer crosses the relevant threshold, the service provider of the sender, often called the originator, must share identifying details about that sender with the service provider of the recipient, often called the beneficiary, and in turn receive the beneficiary’s details. The information typically includes the names of both parties, their account or wallet identifiers, and, in some cases, additional details such as a physical address or an identification number. The aim is to attach a verifiable identity to both ends of the transfer so that, if needed, authorities can trace who sent value to whom.

A point that often surprises people is where this information goes, and the answer is that it does not go on the blockchain. The Travel Rule data is shared off-chain, through secure messaging channels directly between the two service providers, rather than being written into the public ledger. This design preserves the efficiency and privacy characteristics of the blockchain transaction itself while still meeting the compliance requirements, since the sensitive personal information moves through a separate, private channel between the regulated institutions. To make this work across a global industry, the sector has developed standardized messaging formats and protocols that let different providers exchange the required data reliably, along with services that help a provider verify the identity of the counterparty institution before sending personal information to it.

These solutions address a genuine technical challenge: a provider must confirm that the receiving institution is who it claims to be and can handle the data securely before transmitting a customer’s personal details, because sending such information to the wrong party would itself be a serious problem. The result is an off-chain layer of identity infrastructure running alongside the on-chain transactions, invisible to most users but increasingly central to how regulated crypto transfers work.

Who is covered and who is not

A crucial question for any user is whether the Travel Rule applies to them, and the answer depends on whether a regulated intermediary is involved. The rule applies to the businesses that handle crypto on behalf of customers, known in the relevant frameworks by various labels: virtual asset service providers, crypto-asset service providers, or money services businesses, depending on the jurisdiction. The covered entities include crypto exchanges, custodial wallet providers, over-the-counter trading desks, crypto payment processors, and regulated financial institutions that deal in digital assets. The common thread is that these are intermediaries that accept and transmit customer value, and the obligation falls on them, not on individual users directly, though the practical effect is that users of these services must provide the identifying information the providers are required to collect and share.

Equally important is what the Travel Rule does not cover. It generally does not apply to direct peer-to-peer transfers between two private, self-hosted wallets, sometimes called unhosted wallets, where no regulated intermediary is involved, because there is no service provider in the middle to collect and transmit the data. That said, the picture is more nuanced at the edges: when a regulated provider sends funds to or receives funds from an unhosted wallet, the provider may still be required to collect information about the transfer even if it cannot share it with a counterparty institution that does not exist.

Decentralized finance protocols and other non-custodial services occupy a genuinely ambiguous space because they often lack a clear intermediary to bear the obligation, and regulators are actively exploring how, or whether, to extend the rules to them. For most ordinary users, the practical takeaway is that transfers between regulated exchanges and custodial services are squarely within the rule’s scope and will involve information sharing, while transfers between two wallets you control personally generally are not, even as the boundaries around decentralized and self-custodied activity remain unsettled and under regulatory review.

How thresholds vary around the world

One of the most important practical features of the Travel Rule is that there is no single global threshold or authority; instead, each jurisdiction sets its own rules, and the variation is substantial. In the United States, the Travel Rule derives from the Bank Secrecy Act and is enforced by the Financial Crimes Enforcement Network, with a long-standing threshold of three thousand dollars for the obligation to attach identifying information, although proposals have circulated to lower that figure significantly for international transfers.

The European Union has taken the strictest approach through its Transfer of Funds Regulation, which took effect at the end of 2024 and applies a zero threshold to crypto transfers, meaning that every single crypto transfer between providers, regardless of amount, requires full Travel Rule compliance. This regulation operates alongside the broader Markets in Crypto-Assets framework, together forming Europe’s comprehensive crypto compliance regime across all member states.

Other major jurisdictions fall at various points along this spectrum. The United Kingdom introduced its own Travel Rule requirements in 2023, applying them to all transfers regardless of amount. Canada enforces the rule through its financial intelligence agency with a threshold of around 1,000 Canadian dollars, making it relatively strict. Switzerland has adopted one of the toughest versions, requiring firms to identify both parties even for amounts below the thresholds used elsewhere, reflecting its emphasis on strict financial oversight.

Several Asian financial centers, including South Korea, Singapore, and Hong Kong, have implemented firm Travel Rule obligations, often pushing the industry toward standardized compliance technology, while other regions are still developing their frameworks. For users and businesses operating across borders, this patchwork is a genuine challenge, because the same transfer might be subject to full compliance in one jurisdiction and none in another, and a provider serving customers in multiple countries must navigate the strictest applicable requirements. The variation is not a sign of confusion so much as a reflection of how recently and unevenly the global standard has been adopted into national law.

How the Travel Rule fits with KYC and AML

The Travel Rule is often mentioned alongside know-your-customer and anti-money-laundering obligations, and clarifying how the three relate helps make sense of the broader compliance picture. Anti-money-laundering, usually shortened to AML, is the umbrella framework, the overall body of laws and practices designed to prevent the financial system from being used to launder the proceeds of crime or finance illicit activity. Within that framework sit specific obligations, and two of the most important are know-your-customer checks and the Travel Rule, which address different points in the lifecycle of a customer relationship and a transaction.

Know-your-customer, or KYC, refers to the process by which a service provider verifies the identity of its own customers, typically at the point of onboarding, by collecting documents and information to confirm who they are. It answers the question of whether the provider knows who its customer is. The Travel Rule addresses a different moment: it governs what happens when that customer makes a transfer, requiring the provider to share the customer’s identifying information with the counterparty provider on the other end of a qualifying transaction.

In other words, know-your-customer confirms identity at the door, while the Travel Rule makes that identity information move with transfers between institutions. The two interlock, because the provider can only share accurate sender information under the Travel Rule if it has properly verified that sender through know-your-customer in the first place. Sanctions screening adds a further layer, since providers must also check the parties to a transfer against sanctions lists to avoid processing transactions for prohibited persons.

Together, these obligations form a connected compliance system: know-your-customer identifies the customer, the Travel Rule shares that identity across transfers, sanctions screening checks it against prohibited lists, and the whole apparatus serves the overarching anti-money-laundering goal of keeping illicit funds out of the system.

A worked example: a transfer between two exchanges

A simple example makes the mechanics tangible. Suppose you hold Bitcoin on one regulated exchange, call it Exchange A, and you want to send an amount worth more than the applicable threshold, say more than $3,000 in a jurisdiction using that figure, to your account on another regulated exchange, Exchange B. When you initiate the transfer, the Bitcoin itself moves on the blockchain from Exchange A’s systems toward Exchange B’s, exactly as any Bitcoin transaction would. That part is visible on the public ledger, as Bitcoin transactions always are. What happens alongside it, invisibly to you, is the Travel Rule compliance.

Because the transfer exceeds the threshold and both ends involve regulated service providers, Exchange A is required to transmit your identifying information, as the originator, to Exchange B, and Exchange B, in turn, provides information about the beneficiary account. This exchange of data happens off-chain, through a secure messaging channel between the two exchanges, using a standardized format so that each can reliably read the other’s data. Before sending your personal details, Exchange A verifies that Exchange B is a legitimate, identifiable institution capable of receiving the information securely. Exchange B, on receiving both the Bitcoin and your information, can match the incoming transfer to the data and complete its own compliance checks, including screening against sanctions lists. From your perspective, you simply sent Bitcoin from one exchange to another, perhaps noticing only that both required your identity to be verified when you signed up.

Behind that ordinary experience, however, your identifying information traveled with the transfer between the two regulated institutions, which is the Travel Rule working exactly as intended. Had you instead sent the same Bitcoin from one personal wallet you control to another, with no exchange involved, the Travel Rule would generally not have applied, because there would have been no regulated intermediary to carry the obligation.

Limits, gaps, and privacy considerations

For all its expanding reach, the Travel Rule has genuine limits and raises real questions, and an honest account should address them directly. The most discussed structural limit is what experts call the sunrise problem, which describes the uneven pace at which jurisdictions have adopted Travel Rule requirements. Because some countries enforce the rule fully while others have not yet implemented it, providers in jurisdictions without requirements may delay building compliance systems, creating gaps in the global information-sharing network the rule is meant to build. This patchwork reduces the incentive for universal adoption and means the rule’s effectiveness depends on how widely and consistently it is enforced, which remains a work in progress.

A determined bad actor can still seek out jurisdictions or services where the rule does not yet bite, which is precisely the kind of gap a global standard is supposed to close but has not fully closed.

The most significant concern for ordinary users, however, is privacy. The Travel Rule, by design, reduces the anonymity once associated with crypto, requiring that identifying information be collected, shared between institutions, and retained. This raises legitimate questions about data security, because personal information that is collected and transmitted can be exposed if a provider suffers a breach or if the data is mishandled, and the more institutions hold and share such data, the larger the potential attack surface.

Some users see the loss of financial privacy as a genuine drawback, while supporters argue that the same information sharing builds trust in platforms and aligns crypto with established financial standards, making it safer and more acceptable to mainstream institutions and regulators. There is also the unresolved tension around decentralized finance and self-custody, where applying a rule built for intermediaries to systems designed to operate without them remains genuinely difficult, and where overly aggressive extension could undermine the permissionless qualities that give those systems their value.

The honest summary is that the Travel Rule is a serious, expanding compliance obligation that brings real benefits in combating illicit finance and real costs in privacy and complexity, and that its boundaries, particularly around unhosted wallets and decentralized protocols, are still being worked out. For users, the practical reality is that moving crypto between regulated platforms now comes with identity sharing attached, and that is unlikely to reverse.

Frequently Asked Questions

What is the Travel Rule in simple terms?

It is an anti-money-laundering requirement that makes identifying information about the sender and recipient travel with a crypto transfer above a certain amount. When you send crypto between regulated platforms above the threshold, your provider must share details about you with the recipient’s provider, and receive details in return. The name comes from the information traveling with the transfer. It originated in traditional banking decades ago and was extended to crypto in 2019, bringing crypto transfers under the same kind of scrutiny long applied to bank wires, so that authorities can trace who sent value to whom.

Why does the Travel Rule exist?

It exists to combat money laundering and the financing of illicit activity by making crypto transfers traceable. The logic, articulated by the global standard-setter as same risk, same rules, is that crypto carries money-laundering risks similar to traditional finance, so it should face similar safeguards. By requiring that identifying information accompany transfers, the rule creates an auditable trail that makes it harder for illicit funds to move undetected, just as the original banking Travel Rule did for wire transfers. The Financial Action Task Force extended the standard to crypto in 2019, and countries have since written it into their own laws.

What information has to be shared under the Travel Rule?

When a transfer exceeds the relevant threshold, the sender’s provider must share identifying details about the sender, the originator, with the recipient’s provider, and receive details about the recipient, the beneficiary. This typically includes both parties’ names and account or wallet identifiers, and sometimes additional information such as an address or identification number. Crucially, this data is shared off-chain, through secure messaging channels directly between the two regulated providers, rather than being written onto the public blockchain. Standardized messaging formats let different providers exchange data reliably, and a provider verifies the counterparty institution before sending any personal information.

Does the Travel Rule apply to my personal wallet transfers?

Generally not, if you are transferring between two private wallets you control yourself, with no regulated intermediary involved, because there is no service provider in the middle to collect and share the data. The rule applies to regulated businesses such as exchanges, custodial wallet providers, and over-the-counter desks. That said, when a regulated provider sends funds to or receives them from a self-hosted wallet, the provider may still need to collect information about the transfer. Decentralized finance and non-custodial services occupy an ambiguous space that regulators are still examining, so the boundaries around self-custodied and decentralized activity remain unsettled.

What are the transfer thresholds?

They vary widely by jurisdiction, since there is no single global threshold. The United States uses a threshold of three thousand dollars, though proposals to lower it have circulated. The European Union applies a zero threshold under its Transfer of Funds Regulation, meaning every crypto transfer between providers requires compliance regardless of amount. The United Kingdom applies the rule to all transfers, Canada uses a threshold of around 1,000 Canadian dollars, and Switzerland requires identification even below common thresholds. Several Asian financial centers enforce firm obligations. This patchwork means the same transfer can face full compliance in one country and none in another.

How is the Travel Rule different from KYC?

Know-your-customer, or KYC, is the process by which a provider verifies the identity of its own customers, usually when they sign up, to confirm who they are. The Travel Rule governs a different moment: it requires the provider to share that customer’s identifying information with the counterparty provider when the customer makes a qualifying transfer. KYC confirms identity at the door, while the Travel Rule makes that identity travel with transfers between institutions. The two interlock, since a provider can only share accurate sender information if it has properly verified the customer through KYC first. Both sit within the broader anti-money-laundering framework.

This article is educational information, not legal or financial advice. Travel Rule requirements, thresholds, and enforcement vary by jurisdiction and reflect information available as of June 26, 2026, and can change. The treatment of self-hosted wallets and decentralized finance in particular remains unsettled. Verify the current rules in your jurisdiction from primary sources, and consult a qualified professional for guidance on your specific situation.

Bitcoin is the largest pool of value in crypto, but on its own, it cannot touch Ethereum’s world of lending, borrowing, and yield. Wrapped Bitcoin is the bridge. This guide explains how WBTC works, the mint-and-burn model behind it, the alternatives, and the custodial risks that set it apart from holding real BTC.

Summary

- Wrapped Bitcoin (WBTC) is an ERC-20 token on Ethereum backed 1:1 by real Bitcoin held in reserve by a custodian, letting Bitcoin’s value be used inside Ethereum’s decentralized finance ecosystem.

- It exists because native Bitcoin cannot operate inside Ethereum smart contracts, so WBTC bridges the largest pool of crypto value into the largest arena for DeFi.

- WBTC works through a mint-and-burn model run by three parties: custodians who hold the Bitcoin, merchants who handle verification and distribution, and users, all overseen by the WBTC DAO.

- WBTC tracks Bitcoin’s price and can be used for lending, borrowing, yield farming, and as collateral, but it is not the same as holding native BTC because it adds custodial, smart contract, and bridge risks.

- Alternatives such as Coinbase’s cbBTC and the more decentralized tBTC offer different custody models, and the choice among them comes down to which trust assumptions you are comfortable with.

Wrapped Bitcoin, known by its ticker WBTC, is an ERC-20 token that runs on the Ethereum blockchain and is backed 1:1 by real Bitcoin held in reserve, so that one WBTC is always meant to equal one Bitcoin. Its entire purpose is to solve a fundamental incompatibility in crypto: Bitcoin, the largest and most valuable cryptocurrency, lives on its own blockchain and cannot natively participate in the decentralized finance applications built on Ethereum, because those applications run on smart contracts that Bitcoin’s design does not support.

An enormous amount of crypto wealth sits in Bitcoin, while an enormous amount of programmable financial activity happens on Ethereum, and for years, there was no way to bring the two together. Wrapped Bitcoin is the bridge. By locking real Bitcoin with a custodian and issuing an equivalent Ethereum token against it, WBTC lets Bitcoin holders put their Bitcoin’s value to work inside Ethereum’s ecosystem, lending it, borrowing against it, trading it, supplying it to liquidity pools, and using it as collateral, all without selling their Bitcoin exposure. It was the first widely adopted way to do this, and it remains one of the most integrated.

The idea is simple, but the details are where the important nuances live, and they are worth understanding before using WBTC, because the convenience comes with trade-offs that holding plain Bitcoin does not have. A wrapped token introduces extra parties and extra trust assumptions, and the question of who holds the underlying Bitcoin, and whether you can always get it back, sits at the center of the whole arrangement.

This guide explains what WBTC is, why it is needed, exactly how the mint-and-burn mechanism works, who the custodians and merchants are, and why they matter, a concrete example of using WBTC in practice, how it compares to native Bitcoin and to newer alternatives like cbBTC and tBTC, and the specific risks that come with holding a wrapped asset rather than the real thing. The aim is to let you decide whether wrapped Bitcoin fits your needs or whether plain Bitcoin is the cleaner choice.

Why Bitcoin needs wrapping

To understand why WBTC exists, you have to understand a basic limitation of Bitcoin. Bitcoin was designed as a secure, decentralized system for holding and transferring value, and it does that job extremely well, but its scripting language is deliberately limited and is not built to run the complex, self-executing programs known as smart contracts.

Ethereum, by contrast, was built specifically to run smart contracts, and decentralized finance, the ecosystem of lending protocols, decentralized exchanges, and yield platforms, is constructed almost entirely on Ethereum and similar smart-contract blockchains.

The consequence is that Bitcoin, despite being the largest store of value in crypto, simply cannot plug into these applications directly. A Bitcoin holder who wanted to earn yield or use their holdings as collateral in DeFi had no native way to do so.

This is the gap wrapping fills. The core problem is one of interoperability, the ability to use an asset from one blockchain on another, and wrapping is one of the earliest and most widely used solutions to it. By representing Bitcoin as a token that conforms to Ethereum’s technical standards, specifically the ERC-20 standard that Ethereum applications are built to recognize, wrapped Bitcoin makes Bitcoin-linked value fully usable inside the Ethereum environment.

The ERC-20 standard is a set of rules that makes a token fully compatible and interchangeable across Ethereum’s smart contracts, so a wrapped Bitcoin token can be lent, borrowed, swapped, and used as collateral exactly like any other Ethereum token.

Wrapping, therefore, reduces the fragmentation between Bitcoin’s huge liquidity and Ethereum’s rich application layer, turning Bitcoin from an asset that sits outside DeFi into one that can be put to work within it. That is the entire reason wrapped Bitcoin was created, and why it found immediate demand.

How the mint-and-burn model works

The mechanism that keeps wrapped Bitcoin backed 1:1 by real Bitcoin is called mint and burn, and it relies on a three-party system of custodians, merchants, and users.

The custodian is a regulated entity that holds the actual Bitcoin in secure reserve; for WBTC, this role has been played by the digital-asset custody firm BitGo. The merchant is an intermediary, such as an exchange or crypto business, that interacts with users, performs the necessary identity and compliance checks, and distributes the wrapped tokens. The user is the person who wants to convert between Bitcoin and wrapped Bitcoin. These three parties, coordinated by a set of smart contracts, keep the supply of WBTC matched to the Bitcoin held in reserve.

The process works in two directions. To create, or mint, wrapped Bitcoin, a user requests WBTC from a merchant, who carries out know-your-customer and anti-money-laundering checks to verify the user’s identity. The merchant then sends the corresponding Bitcoin to the custodian, who holds it in reserve and mints an equal amount of WBTC on Ethereum, which makes its way to the user.

To reverse the process, or burn the tokens, a user who wants their Bitcoin back submits a redemption request, the WBTC is destroyed in what is called a burn transaction, and the custodian releases the equivalent Bitcoin from reserve. Because every WBTC in existence is meant to correspond to a Bitcoin locked with the custodian, the token maintains its 1:1 peg, and its price tracks Bitcoin’s price closely.

Importantly, both the minting and the burning are recorded publicly on the Ethereum and Bitcoin blockchains, so anyone can verify the activity, and the system is periodically subjected to proof-of-reserve checks that confirm the Bitcoin backing actually exists. This transparency is meant to give holders confidence that the wrapped tokens are genuinely backed, though, as the risks section explains, it does not remove the reliance on the custodian.

Who governs WBTC, and why it matters

A wrapped token raises an obvious question: who controls the system, decides which custodians and merchants are trusted, and can change how it works. For WBTC, the answer is a decentralized autonomous organization known as the WBTC DAO, a governing body made up of a group of stakeholders that has included prominent names in the crypto space.

The DAO operates through a multi-signature wallet, meaning that changes require the agreement of multiple keyholders rather than any single party, and its members can vote to add or remove custodians and merchants and to make changes to the smart contracts on which the system runs. This governance structure exists specifically to reduce the centralization risk that would come from a single company controlling the entire arrangement, spreading authority across a set of stakeholders instead.

Why this matters became vivid in 2024, in what served as the clearest real-world stress test of WBTC’s governance. The custodian BitGo announced a change to its custody arrangements involving a partnership with another firm, and that change sparked significant concern across decentralized finance because of the new partner’s perceived links to a controversial figure and ecosystem.

The episode mattered because it went to the heart of the trust assumption underlying WBTC: holders were trusting that the Bitcoin backing their tokens was held safely and by parties they considered reliable, and a change in who effectively controlled that custody was enough to shake confidence and prompt many users and protocols to reconsider. It also accelerated the rise of alternative wrapped Bitcoin products with different custody models.

The lesson is that the governance and custody arrangements of a wrapped token are not background details; they are central to its safety, because the whole value of WBTC rests on the Bitcoin being there and being controlled by trustworthy parties. Who governs the system, and how, is therefore something a prospective holder should actually look into rather than take for granted.

A worked example: putting Bitcoin to work

A concrete example shows why someone would bother wrapping their Bitcoin in the first place. Imagine a person named Ezra who holds $2,000 worth of Bitcoin and believes in it as a long-term holding, but who also wants to earn a return on that value instead of letting it sit idle. The problem is that the lending protocol Ezra wants to use, which would pay interest on deposited assets, runs on Ethereum, and Ezra’s Bitcoin cannot be deposited there directly because it lives on a different blockchain that the protocol cannot interact with. Without wrapping, Ezra’s only options would be to sell the Bitcoin for an Ethereum-native asset, giving up his Bitcoin exposure, or to leave it earning nothing.

Wrapping solves this. Ezra converts his Bitcoin into wrapped Bitcoin, either by going through a merchant to mint it directly or, more commonly for an ordinary user, by simply swapping his Bitcoin for WBTC on an exchange or decentralized exchange, which avoids the need to interact with the custodians himself. Now holding WBTC, which is an Ethereum token tracking Bitcoin’s price 1:1, Ezra can deposit it into the lending protocol and earn interest, all while his position still rises and falls with the price of Bitcoin. He has kept his Bitcoin exposure and put it to work at the same time. Beyond lending, WBTC opens the same doors that any Ethereum token enjoys: Ezra could supply it to a liquidity pool on a decentralized exchange to earn trading fees, use it as collateral to borrow other assets, or deposit it into yield strategies.

A further practical benefit is speed, since transactions in WBTC settle on Ethereum, which produces blocks far more frequently than Bitcoin, so moving wrapped Bitcoin between Ethereum wallets and applications is quicker than moving native Bitcoin. This is the everyday appeal of wrapped Bitcoin: it lets Bitcoin holders participate in the full range of Ethereum-based finance without selling the Bitcoin they want to keep.

WBTC versus native Bitcoin and the alternatives

It is essential to be clear that wrapped Bitcoin is not the same as holding native Bitcoin, even though the two share a price.

With native Bitcoin, the only real question about safety is whether you control your own private keys; if you do, the Bitcoin is yours, secured by the Bitcoin network itself. With WBTC, the question expands considerably, because you are now also relying on the custodian to actually hold the backing Bitcoin, on the integrity of the reserves, on the governance of the system, and on the redemption process working when you want to convert back.

You may hold the WBTC token in your own wallet, but the wrapped asset still depends on institutional actors operating correctly behind the scenes. WBTC tracks Bitcoin’s market value, but it does not inherit Bitcoin’s trust model, and that difference is the single most important thing to understand about it. If your only goal is to hold Bitcoin for the long term and you have no interest in DeFi, native Bitcoin is the cleaner and simpler choice.

The 2024 custody controversy spurred the growth of alternative tokenized Bitcoin products, and they are worth knowing because they offer different trade-offs. One prominent alternative is cbBTC, issued by the exchange Coinbase, which appeals to users who already trust Coinbase’s custody and operate within its ecosystem. Another is tBTC, built by the Threshold Network, which is designed to avoid reliance on a single custodian in favor of a more decentralized model, appealing to users for whom minimizing custodial trust matters more than convenience.

There are others as well, and the broader point is that the tokenized Bitcoin market has become fragmented, offering distinct choices for different priorities. The decision among them is fundamentally about trust model and use case instead of price, since they all track Bitcoin: choose WBTC for the deepest liquidity and the widest integration across established DeFi protocols, choose cbBTC if you prefer Coinbase’s custody, choose tBTC if avoiding a single custodian is your priority, and choose native Bitcoin if you do not need DeFi at all. Wrapped Bitcoin products are tools for a specific purpose, not upgrades to Bitcoin.

Risks and what to check before wrapping

The risks of wrapped Bitcoin all stem from the fact that it adds layers of trust on top of simply holding Bitcoin, and understanding them is essential before wrapping any meaningful amount. The primary risk is custodial centralization. Because the wrapped token is only as good as the Bitcoin held in reserve, the failure of the custodian, whether through a hack, insolvency, mismanagement, or loss of access, could impair the backing and leave holders with tokens that no longer correspond to real Bitcoin.

This is not a theoretical concern: history offers cautionary examples of wrapped or bridged Bitcoin products that became impossible to redeem after the entity backing them failed, turning Bitcoin-backed tokens supposedly into worthless or stranded assets. The custody arrangement is the foundation, and if it fails, everything built on it fails with it.

Several other risks compound the custodial one. Smart contract risk means that bugs or vulnerabilities in the Ethereum-side code, or errors in governance, could affect the token. Bridge risk arises when wrapped Bitcoin is moved onto other networks, such as Ethereum layer-two chains, through additional bridges, since each bridging layer adds another set of trust assumptions and another potential point of failure, and you may encounter bridged representations that wrap an already-wrapped token, compounding the risk further. Governance risk means that the parties controlling the system could make decisions, such as the contested custody change, that holders dislike or distrust. And regulatory risk means that official actions could affect redemptions or lead to address restrictions.

The practical advice that follows from all this is to verify before you wrap: check which specific wrapped token and contract you are holding, understand its custody model and who controls the reserves, confirm that proof-of-reserve attestations are current, and make sure you understand the redemption path back to native Bitcoin.

Reviewing the custodian’s transparency, the governance records, and any reputable audits or incident reports before committing meaningful funds is simply prudent. Wrapped Bitcoin is a useful tool that fills a real gap, but it should never be treated as identical to the Bitcoin it represents, because the trust model behind it is fundamentally different.

Frequently Asked Questions

What is Wrapped Bitcoin (WBTC) in simple terms?

Wrapped Bitcoin is an Ethereum token backed one-to-one by real Bitcoin held in reserve by a custodian, so one WBTC is meant to always equal one Bitcoin. It exists because native Bitcoin cannot be used inside Ethereum’s decentralized finance applications, which run on smart contracts that Bitcoin does not support. By locking real Bitcoin and issuing an equivalent Ethereum token against it, WBTC lets Bitcoin holders use their Bitcoin’s value for lending, borrowing, trading, and collateral within Ethereum’s ecosystem, without selling their Bitcoin exposure. It tracks Bitcoin’s price closely because every WBTC corresponds to a Bitcoin in reserve.

How does Wrapped Bitcoin work?

It works through a mint-and-burn model involving three parties: custodians who hold the Bitcoin, merchants who handle verification and distribution, and users. To create WBTC, a user requests it from a merchant who performs identity checks, the corresponding Bitcoin is sent to the custodian, and an equal amount of WBTC is minted on Ethereum. To convert back, the user submits a redemption request, the WBTC is burned, and the custodian releases the Bitcoin. Both minting and burning are recorded publicly on both blockchains, and proof-of-reserve checks confirm the backing exists. The whole system is overseen by the WBTC DAO.

Is Wrapped Bitcoin the same as Bitcoin?

No, and this distinction is crucial. WBTC tracks Bitcoin’s price and can be redeemed one-to-one for Bitcoin, but it is not the same as holding native Bitcoin. With native Bitcoin, your only real concern is controlling your private keys. With WBTC, you also depend on the custodian actually holding the backing Bitcoin, on the reserves being intact, on the governance functioning, and on redemption working. WBTC shares Bitcoin’s price but not its trust model. If you only want to hold Bitcoin long term and do not need decentralized finance, native Bitcoin is the cleaner, simpler choice.

What can you do with Wrapped Bitcoin?

WBTC opens up the full range of Ethereum-based decentralized finance to Bitcoin’s value. Because it behaves like any Ethereum token, it can be lent out to earn interest, used as collateral to borrow other assets, supplied to liquidity pools on decentralized exchanges to earn trading fees, and deposited into yield strategies. This lets a Bitcoin holder earn returns or access liquidity while keeping their Bitcoin exposure, instead of selling. WBTC transactions also settle on Ethereum, which produces blocks far more frequently than Bitcoin, so moving wrapped Bitcoin between Ethereum wallets and applications is faster than moving native Bitcoin.

What are the alternatives to WBTC?

The main alternatives are other tokenized Bitcoin products with different custody models. cbBTC, issued by Coinbase, suits users who trust Coinbase’s custody and ecosystem. tBTC, built by the Threshold Network, is designed to avoid reliance on a single custodian in favor of a more decentralized model, appealing to those who prioritize minimizing custodial trust. The tokenized Bitcoin market is fragmented, and the choice among options comes down to trust model and use case instead of price. WBTC offers the deepest liquidity and widest DeFi integration, cbBTC offers Coinbase custody, tBTC offers more decentralization, and native Bitcoin is best if you do not need DeFi.

What are the risks of Wrapped Bitcoin?

The main risk is custodial centralization: because WBTC is only as good as the Bitcoin held in reserve, the failure of the custodian through a hack, insolvency, or loss of access could impair the backing, and history includes wrapped Bitcoin products that became unredeemable after their backers failed. Additional risks include smart contract vulnerabilities, bridge risk when WBTC is moved to other networks, governance decisions that holders may distrust, and regulatory actions affecting redemption. Before wrapping, verify which token and contract you hold, understand the custody model and reserves, confirm proof-of-reserve attestations, and make sure you understand the redemption path back to native Bitcoin.

This article is educational information, not financial advice. Wrapped Bitcoin and decentralized finance involve significant risks, including custodial failure, smart contract vulnerabilities, and loss of funds. Details of custodians, governance, and alternatives reflect information available as of June 26, 2026, and can change. Verify the current custody model, reserves, and redemption process of any wrapped token from primary sources, and consider your own circumstances before making any decision.

Bitcoin’s price went through a highly volatile and mostly painful ride throughout June, dumping to a multi-year low first at $59,000 before another one at $58,000.

Analysts continue to debate whether this cycle’s bottom has been reached or not, but Ali Martinez recently published a post on his views about the current accumulation zone and whether it’s a proper entry level.

History Says Yes

In the post specifically designated to bitcoin’s 200-week Simple Moving Average (SMA), the popular analyst noted that the asset has rarely traded below it for a longer period. And when it has dipped below it, the subsequent rally has shown that those moments “have consistently marked exceptional long-term accumulation opportunities.”

Since the 200-week SMA currently sits at $63,500, a level that BTC lost earlier this week, Martinez concluded that “This is exactly when you want to deploy a dollar-cost averaging strategy.”

In the more detailed post on BTC’s market structure, though, the analyst admitted that bitcoin trading below the 200-week SMA doesn’t necessarily mean it has bottomed out. In fact, he noted that the asset can still dip further south and outlined potential targets at $54,000 or even $40,000. If that’s the case, investors might want to double down on their DCA strategy, he argued.

“Spreading buy orders across the $58,000 to $40,000 range allows you to build a position while the asset trades at a technical discount.”

Martinez believes $63,500 remains BTC’s most significant level now, as if it registers a “high-timeframe reclaim of the 200-week SMA as macro support,” it would suggest the early stages of a new bull run.

When Bottom?

Each leg down opens the door for analysts to continue the always-hot debate over whether the bottom is in or if more pain lies ahead. Martinez brought up BTC’s historical performance after the aforementioned 200-week SMA came into play. Each of his four examples delivered massive gains after bitcoin tested that level in 2015, 2018, 2020, and 2022.

As such, he determined that the bottom is “almost in” and outlined the precise gains registered from bottom to top.

-

August 2015: Bitcoin touched the 200-week SMA and launched a bull market, rallying over 8,500%.

- December 2018: A test of this moving average triggered a swift 267% recovery.

- March 2020: The COVID-induced liquidity flush saw Bitcoin validate the 200-week SMA as support before surging 1,125%.

- June 2022: For the first time ever, Bitcoin dipped and consolidated below the moving average until December 2022. Once the line was reclaimed, it initiated a 680% expansion.

The post Bitcoin’s Price Has Finally Entered the Buy Zone: Analyst Maps Out Big Targets appeared first on CryptoPotato.

Telegram founder Pavel Durov purchased Plush Pepe #834 for 7,500 Gram (GRAM) on The Open Network, then transferred the NFT to Adler Toberg, a designer linked to Telegram’s interface and gift system.

The acquisition marks Durov’s third confirmed purchase of a TON collectible in just over six months. He added his first Plush Pepe in December 2025, then picked up a Telegram Gift NFT in January 2026. Together, the moves reflect deliberate and ongoing personal engagement with the digital asset layer Telegram continues to build.

Plush Pepes and the TON Collectibles Market

Plush Pepes are Telegram’s official collectibles series, issued natively on The Open Network (TON). At GRAM’s current price of $1.55, the 7,500 GRAM spent on Plush Pepe #834 comes to roughly $11,625.

The specific piece is the Donatello model, a 1% rarity variant, with a Bell Pepper symbol (0.5%) and a Navy Blue backdrop (2%). Of the 2,861 Donatello editions, 2,825 have found owners.

TON development has accelerated alongside the demand for collectibles. A major protocol upgrade made TON 10 times faster, cutting transaction times to sub-second finality.

On the product side, GOAT Gaming’s Underground Pepe moved Plush Pepes beyond profile accessories. The project turned them into active gaming assets, complete with a dedicated rewards currency.

Secondary market activity has also expanded. A Telegram username sold for 500,000 USDT in a recent TON NFT resale, reflecting strong demand for Telegram-native assets.

Durov Gifts the NFT to Designer Adler Toberg

The TON Blockchain X account responded to Durov’s purchase with a dry piece of humor. It expressed hope that he would pass the NFT along to a Telegram intern as a workplace bonus. The joke turned out to be close to the truth.

Durov transferred Plush Pepe #834 directly to Adler Toberg, a designer known for his work on Telegram’s interface and gift system. Toberg has previously made public statements about the direction of Telegram’s collectibles program, including the cadence of new gift releases.

The transfer points to something real. Within the Telegram ecosystem, collectibles now carry social weight as markers of community standing. Durov’s decision to give a high-value NFT to a member of his team reinforces that dynamic.

His role as Telegram’s CEO makes each on-chain move a visible signal across the network.

The token itself also changed course this year. GRAM was rebranded from Toncoin following an 81% governance vote, reverting to the name from Telegram’s original 2018 whitepaper. The chain also broadened its reach through Apple Watch integration and a wider ecosystem push.

The post Pavel Durov Gifts $12,000 Worth of Plush Pepe NFT to a Telegram Designer appeared first on BeInCrypto.

Key Highlights

- Micron rallied 17.1% following fiscal Q3 2026 results showing $41.46 billion in revenue, a 346% year-over-year increase, with EPS of $25.11 crushing the $20.5 consensus

- Company provided Q4 outlook of approximately $50 billion in revenue and roughly $31 EPS, significantly exceeding analyst projections

- Micron secured approximately $100 billion in multi-year strategic customer commitments through take-or-pay arrangements with 16 partners

- Leadership indicated supply won’t match demand until at least 2028

- Barclays upgraded MU price target by 70% to $2,000 from $1,175 while maintaining a Buy rating

Micron Technology posted a quarter for the history books on Wednesday, sparking an immediate and powerful response from investors.

The semiconductor manufacturer specializing in memory chips revealed fiscal Q3 2026 sales of $41.46 billion, representing a 346% year-over-year surge and landing approximately 17% higher than Wall Street’s projections. The company’s non-GAAP earnings per share reached $25.11, significantly exceeding the consensus forecast of $20.50. Gross margin expanded dramatically to 84.9%, a stark contrast to the 39% recorded in the same period last year.

MU stock climbed 17.1% following the announcement, reaching $1,209 per share — marking a fresh 52-week high.

While the quarterly performance was impressive in isolation, forward-looking guidance proved to be the real catalyst behind the stock’s momentum.

Micron projected fiscal Q4 revenue at approximately $50 billion with earnings per share around $31. These figures substantially exceeded Wall Street expectations, which had anticipated Q4 revenue near $43 billion and EPS of approximately $25.31.

$100 Billion Worth of Binding Customer Commitments

The chipmaker disclosed it has executed 16 Strategic Customer Agreements (SCAs) — binding take-or-pay contracts spanning data center, consumer, and automotive sectors. Fourteen of these arrangements include a combined minimum revenue obligation of $100 billion throughout their duration.

These represent firm commitments backed by real capital. Partners have already deposited $22 billion. Standard SCAs extend five years (2026–2030), while automotive-focused agreements run for three-year periods.

Barclays analyst Thomas O’Malley characterized the SCA disclosures as exceeding expectations in both dollar magnitude and customer count. He boosted his MU price target by 70% to $2,000 from $1,175, applying a 12x multiple to his updated 2027 EPS projection of $166.74.

O’Malley highlighted that existing SCAs represent roughly 20% of total DRAM volume and 33% of NAND volume. After finalizing all pending agreements, Micron anticipates over 50% of its revenue will originate from these contractual commitments.

Data-center segment revenue exceeded $25 billion during the quarter — translating to an annualized run rate surpassing $100 billion.

Supply Constraints Expected Through 2028

Micron CEO Sanjay Mehrotra stated the company sees “no line of sight” to supply equilibrium with demand occurring before 2028. DRAM pricing increased in the low-60s percentage range during the quarter, fueled by a fundamental supply shortage affecting the entire industry.

This supply-demand imbalance is visible across competitors as well. Samsung disclosed a 146% spike in DRAM average selling prices during Q1. SK Hynix reported mid-60s percent price increases.

The constrained supply environment is affecting all three leading memory manufacturers.

It’s notable that MU shares had declined 13.6% just 48 hours prior following news that SK Hynix was moderating its high-bandwidth memory (HBM) expansion plans. That selloff now appears to have been an overreaction.

Investors should monitor HBM scaling expenses and new fabrication facility construction, which will contribute approximately $1 billion to FY2027 operating costs, along with the eventual repayment of the $22 billion in customer deposits.

Wall Street maintains a Strong Buy consensus rating on MU, featuring 28 Buy ratings against just one Hold. The average analyst price target of $1,526.67 suggests approximately 36% potential upside from current trading levels.

Micron shares have appreciated 283% year-to-date.

For years, investors had valued the firm well above its bitcoin holdings, giving Strategy massive flexibility to raise capital as needed — a situation Michael Saylor and team took full advantage of.

Cardano wallet SecondFi has identified a recovery path for users affected by Tuesday’s exploit and expects to begin returning assets in about two weeks, following testing and security reviews.

According to a Saturday statement by Phillip Pon, CEO of SecondFi developer Emurgo, the company completed forensic investigations and established a recovery pathway for affected users. Pon said the coming week would be spent building the solution, followed by another week of testing before assets begin to be returned.

Pon urged users to refrain from migrating assets or taking actions outside official guidance, saying the recovery process was designed around existing wallet states and that independent action could complicate the secure return of funds.

SecondFi developer Emurgo shared an update on the wallet’s recovery efforts. Source: Emurgo

SecondFi disclosed a security breach on Tuesday that affected approximately 16 million ADA, worth about $2.4 million at the time, across 374 addresses. SecondFi previously said it traced the incident to an address-level issue in its Cardano web wallet generation software that exposed users’ private keys.

Related: Q2 2026 emerges as most-hacked quarter on record with 83 incidents

The company also said it secured roughly 129 million ADA through emergency measures and transferred the funds to an independent third-party custodian, where they will remain until the verification and recovery process is complete.

SecondFi has not yet published a comprehensive post-mortem detailing the vulnerability or how the exploit was carried out.

SecondFi warns of recovery-related scams

In a separate update on Saturday, SecondFi warned that malicious actors are circulating fraudulent messages impersonating the wallet while its recovery effort remains underway.

The company said no recovery actions requiring user participation have begun and that it will never ask users for private keys, seed phrases, wallet credentials or direct wallet access.

SecondFi said any messages instructing users to submit wallet information, migrate assets or take immediate action outside its verified communication channels should be treated as fraudulent.

It added that users requiring assistance should submit a ticket through its official support portal while the recovery process continues.

Magazine: AI is banking the unbanked in Africa… faster than crypto

Key Takeaways

- Oracle shares plummeted 19% over the past week — the most severe weekly decline since August 2001

- The company’s market valuation has dropped approximately 55% from its September peak near $900 billion

- Capital spending exploded 162% to almost $56 billion during fiscal 2026

- The company’s debt load reached approximately $130 billion by late May, accompanied by nearly $24 billion in negative free cash flow

- Despite the selloff, 71% of Wall Street analysts maintain Buy ratings — a 15-year high

Oracle has just endured its most punishing week on the stock market in a quarter century. Shares tumbled 19% over five straight trading sessions, with daily losses exceeding 2.6% each day. The last time the enterprise software giant experienced such a devastating stretch was during August 2001, amid the dot-com bubble collapse.

The recent downturn represents more than just a bad week. Oracle’s market capitalization has contracted by roughly 55% since reaching approximately $900 billion last September.

Both the extended decline and this week’s brutal selloff share a common culprit: the escalating expenses tied to Oracle’s artificial intelligence strategy.

Oracle has committed heavily to AI infrastructure development, particularly through its involvement with OpenAI as part of the Stargate initiative. Constructing this infrastructure demands massive capital investment — and currently, shareholders are paying a hefty price.

Financial Metrics Paint a Concerning Picture

As of May’s conclusion, Oracle’s outstanding debt stood at roughly $130 billion. The company’s capital expenditure soared 162% during fiscal year 2026, hitting close to $56 billion.

Free cash flow registered at nearly negative $24 billion for the fiscal year.

To continue financing its infrastructure expansion, Oracle intends to secure an additional $40 billion in fiscal 2027 through combined debt and equity offerings. This follows the previous year’s $43 billion in debt issuance plus $5 billion raised through equity sales.

The fundamental challenge is clear: Oracle finds itself competing against Amazon, Microsoft, and Google in the race to construct AI data center capabilities — yet unlike these rivals, it cannot offer a comprehensive technology ecosystem. This constraint puts pressure on margins for what amounts to an extraordinarily expensive gamble.

Analyst Community Remains Largely Optimistic

Remarkably, analyst confidence hasn’t wavered despite the sharp decline. FactSet data shows 71% of ORCL analysts maintain Buy ratings — representing the strongest bullish sentiment in 15 years. The overall consensus stands at Strong Buy, reflecting 28 Buy recommendations, five Hold ratings, and zero Sell calls over the most recent three-month period.

The mean price target stands at $263.86, suggesting potential upside exceeding 77% from present levels.

Evercore, which holds a Buy rating on the stock, explained the situation in Wednesday’s research note: “We expect financing/leverage and the pace of equity issuance to remain the central investor debate near term, even as demand signals stay strong.”

This disconnect between professional analyst optimism and actual market performance represents the key narrative entering the following week.

As a footnote, Oracle co-founder Larry Ellison has also dropped several spots on global wealth rankings this week, falling behind Google’s co-founders, Jeff Bezos, and Michael Dell.

Key Highlights

- Starting July 1, AWS will implement a 20% price increase on reserved GPU compute resources, affecting Nvidia B200, B300, H100, and H200 processors.

- H200 pricing has now increased for three consecutive quarters — AWS GPU reservation costs have surged 20–50% since the start of the year.

- Wells Fargo reaffirmed its Buy recommendation on AMZN with a $312 price objective, viewing the increase as confirmation of cloud infrastructure pricing strength.

- Analyst consensus shows 57 Buy ratings on AMZN, with an average price objective of $312.78 — suggesting approximately 38.5% potential appreciation from current prices.

- Institutional shareholders control 72.2% of AMZN shares, with several major funds expanding their holdings during Q1 2026.

Amazon (AMZN) shares climbed 2.5% Thursday following Wells Fargo’s positive commentary on AWS’s latest 20% reserved GPU compute price adjustment, interpreting the move as evidence of robust pricing dynamics and sustained AI infrastructure appetite.

AMZN began Friday’s session at $232.69. The shares currently trade beneath their 50-day moving average of $255.53 while maintaining a position above the 200-day moving average of $234.13. The stock’s 52-week trading band extends from $196.00 to $278.56.

The pricing adjustments become effective July 1 and apply to multiple Nvidia processor architectures — including the B200, B300, H100, and H200 models.

Regarding the H200 particularly, this marks the third straight quarter of upward pricing pressure. AWS implemented a 15% H200 price increase in Q1, followed by 10% in Q2, and now an additional 20% entering Q3. Cumulatively this year, AWS GPU reservation pricing has escalated between 20% and 50% across different chip configurations.

Wells Fargo analyst Ken Gawrelski maintained his Buy recommendation while establishing a $312 price objective. His interpretation: the sustained pricing increases demonstrate that AI compute demand continues exceeding available supply, enabling hyperscale providers like AWS to transfer elevated infrastructure expenses to end customers.

Understanding AWS Reservation Pricing Dynamics

AWS reservation blocks enable clients to secure GPU capacity for periods extending up to six months. The willingness of customers to accept escalating prices for guaranteed access reveals the persistent tightness in available supply.

Wells Fargo recognized that these price adjustments may not translate immediately into revenue gains, given that certain clients operate under existing contractual arrangements. Nevertheless, the firm views this development as reinforcing AWS’s extended growth trajectory.

AMZN maintains a Strong Buy consensus rating throughout Wall Street. Among analysts providing coverage within the last three months, 44 assign Buy ratings while one assigns a Hold rating. The consensus price objective stands at $319.24, implying roughly 38.5% upside potential.

Recent price objective adjustments include: JPMorgan elevating its target to $330, Truist increasing to $320, Wolfe Research establishing a $320 target, and Deutsche Bank moving to $315.

Institutional Holdings and Additional Growth Drivers

Institutional ownership represents 72.2% of outstanding shares. Clark Asset Management acquired 4,879 additional shares during Q1, expanding its complete AMZN holdings to 38,238 shares valued at approximately $7.96 million. Arrowstreet Capital expanded its position by 21% in Q4, currently maintaining over 24.6 million shares worth roughly $5.7 billion.

Beyond GPU pricing developments, Amazon has several additional strategic initiatives underway. The company revealed a $13 billion commitment to India extending through 2030 for AI and cloud infrastructure expansion. Prime Day performance also appears promising, with industry observers anticipating record-breaking sales figures.

Regarding potential headwinds, EU regulatory authorities have suggested AWS could encounter more stringent competitive oversight — representing a possible concern for investors. Certain analysts have additionally expressed reservations regarding the company’s substantial capital investment requirements.

Amazon’s latest quarterly performance delivered $2.78 EPS, exceeding the $1.63 consensus estimate by $1.15. Revenue reached $181.52 billion, representing 16.6% year-over-year expansion.

CEO Andrew Jassy divested 20,000 shares on May 21 at $263.42 through a previously established 10b5-1 trading arrangement.

Ripple CTO emeritus David Schwartz has pushed back on a fresh social media debate over whether XRP existed before Bitcoin.

Summary

- Schwartz said Fugger’s 2004 idea was a payment network, not XRP or decentralized assets.

- XRPL history places XRP’s creation in 2012, years after Bitcoin launched in 2009 officially.

- The debate shows how older RipplePay ideas still drive confusion around XRP’s real origin.

The exchange began after Crypto Dyl News claimed on X that “Bitcoin was NOT the 1st” and that XRP was created in 1988.

That claim drew a question from XRP community user MitchRob, who asked Schwartz whether Ryan Fugger had conceptualized XRP and the XRP Ledger before or after Bitcoin. Schwartz replied that Fugger had conceptualized a decentralized payment and settlement network around 2004, well before Bitcoin.

Schwartz added one key limit to that answer. He said Fugger’s idea did not include decentralized assets. That distinction separates RipplePay, Fugger’s early payment concept, from XRP and the XRP Ledger, which arrived later.

Ryan Fugger built RipplePay, not XRP

Fugger’s RipplePay concept dates back to 2004. It focused on payments, IOUs and trust lines between users. It did not operate as a blockchain in the modern crypto sense, and it did not include XRP as a native asset.

Schwartz’s answer makes that point clear. He wrote that Fugger conceptualized a decentralized payment and settlement network “but without decentralized assets” around 2004. That means the idea came before Bitcoin, but XRP itself did not.

The official XRP Ledger history page places XRP’s launch in 2012. It says Schwartz, Jed McCaleb and Arthur Britto built a distributed ledger that aimed to improve on Bitcoin’s limits. The ledger included a native asset that became XRP.

The XRPL learning portal also says the three developers joined forces in 2011 to create a faster and more scalable digital asset. That timeline puts XRP after Bitcoin, not before it.

XRP origin debate continues online

MitchRob later asked whether Satoshi Nakamoto may have drawn any inspiration from Fugger’s earlier concepts. He also asked which network was built with a better framework for payments and settlement.

Schwartz had not answered that follow-up in the provided thread at the time of writing. The question remains speculative because no public evidence in the thread shows that Satoshi used Fugger’s work when designing Bitcoin.

The confusion comes from the Ripple name. Fugger’s RipplePay project came before Bitcoin, while the XRP Ledger came after Bitcoin. Ripple Labs later used the Ripple name, but the technical system behind XRP was built separately.

As previously reported, David Schwartz recently explained his XRP Ledger role after stepping back from daily leadership. The report noted that he remains CTO emeritus and one of XRPL’s co-creators.

XRPL history still matters

The debate comes as XRP Ledger development continues. In a previous article, crypto.news discussed Schwartz backing the XRP Ledger 3.2.0 upgrade, which renamed the core server software from rippled to xrpld.

That update moved XRPL further away from older Ripple-branded software names. It also added cleanup fixes for features tied to DeFi tools, vaults, lending, permissioned domains and token functions.

Previously, crypto.news explored XRPL’s growing tokenized finance use cases. Schwartz said XRPL use is expanding from payments into tokenized assets, stablecoins and other financial tools.

The latest exchange does not change XRP’s history. Fugger helped shape an early payment idea before Bitcoin. XRP and XRPL, however, began later as separate code written by Schwartz, McCaleb and Britto.

What Is the Travel Rule? Crypto KYC and AML Explained

Egypt survives draw against Iran, advances to knockout stage at World Cup

ETH Zurich’s New Pixel Design Lets Them Display and Detect Light Together

-

Entertainment7 days ago

Entertainment7 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Sports4 days ago

Sports4 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech5 days ago

Tech5 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion19 hours ago

Fashion19 hours agoWeekend Open Thread: Staud – Corporette.com

-

Business7 days ago

Business7 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics1 day ago

Politics1 day agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics1 day ago

Politics1 day agoPotential 2028er World Cup attendee leaderboard

-

Business1 day ago

Business1 day agoAsia stock markets slide as tech shares slump

-

Tech2 days ago

Tech2 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World3 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World3 days ago

Crypto World3 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World2 days ago

Crypto World2 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Business4 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Sports16 hours ago

Sports16 hours agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World8 hours ago

Crypto World8 hours agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Crypto World20 hours ago

Crypto World20 hours agoRTX holders must register wallets before token distribution begins

-

Crypto World23 hours ago

Crypto World23 hours agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Sports2 days ago

Sports2 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Tech6 days ago

Tech6 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Crypto World1 day ago

The DATA Foundation Launches to Tackle AI’s Multi-Billion Dollar Training Data Bottleneck

You must be logged in to post a comment Login