Crypto World

Explore how the Condorcet paradox exposes the limits of perfect fairness in blockchain consensus.

Consensus guarantees today, focus on two properties: Consistency and Liveness. Consistency requires that all nodes eventually agree on the same set and sequence of transactions, while liveness ensures the system continues to process new transactions. What they do not address is whether the agreed-upon transaction order totally reflects fairness.

In public blockchains, transaction ordering has direct economic consequences. The order in which transactions execute determines who captures value and who pays the cost, particularly as validators, block builders, or sequencers can exploit their privileged role in block construction for financial gain. This practice is known as maximal extractable value (MEV) and includes the profitable frontrunning, backrunning, and sandwiching of transactions. Prima facie, there is no obvious way to prevent MEV extracting practices because block proposers hold unilateral power over transaction ordering, and no protocol rule inherently constrains how they exercise that power.

To address this, transaction order-fairness has been proposed as a third essential consensus property. A protocol is transaction order-fair if no participant can systematically bias transaction ordering beyond what objective network conditions and protocol rules imply. By limiting how much power a block proposer has to reorder transactions, fair-ordering protocols move blockchains closer to being transparent, predictable, and MEV-resistant.

However, even this intuitive idea of fairness encounters a structural limit. In an asynchronous distributed system, there is no globally defined reception order because each node observes messages at different times, and no shared clock exists. Therefore, no protocol can guarantee execution strictly according to a single universal arrival sequence. This limitation follows from the basic constraints of distributed consensus under asynchronous communication, not from any particular design choice.

The Condorcet Paradox and the Impossibility of Perfect Fairness

The most intuitive and strongest notion of fairness is called Receive-Order-Fairness (ROF). It simply means “first-come, first-served.” ROF dictates that if most nodes receive transaction A before transaction B, then A should be processed before B.

That sounds simple and fair. However, the problem is that nodes do not all see transactions at the exact same time. Messages travel at different speeds. Some computers might receive A first. Others might receive B first. Because of this, it is impossible to guarantee perfect “first-come, first-served” fairness unless every node can communicate instantly with no delays. In real networks, that never happens.

There is also a deeper problem called the Condorcet paradox. This idea comes from voting theory. It shows that even when each person (or node in this case) has a clear and consistent order in their own mind, the group as a whole can end up with a loop that makes no sense.

For example:

- Most nodes see A before B

- Most nodes see B before C

- Most nodes see C before A

This produces a majority preference cycle (A→B→C→A), meaning no single ordering satisfies the majority view across all pairs. The network cannot construct one sequence that matches what most nodes observed first.

Because perfect ROF is unachievable under these conditions, practical systems adopt some weaker fairness guarantees as outlined in the sections below.

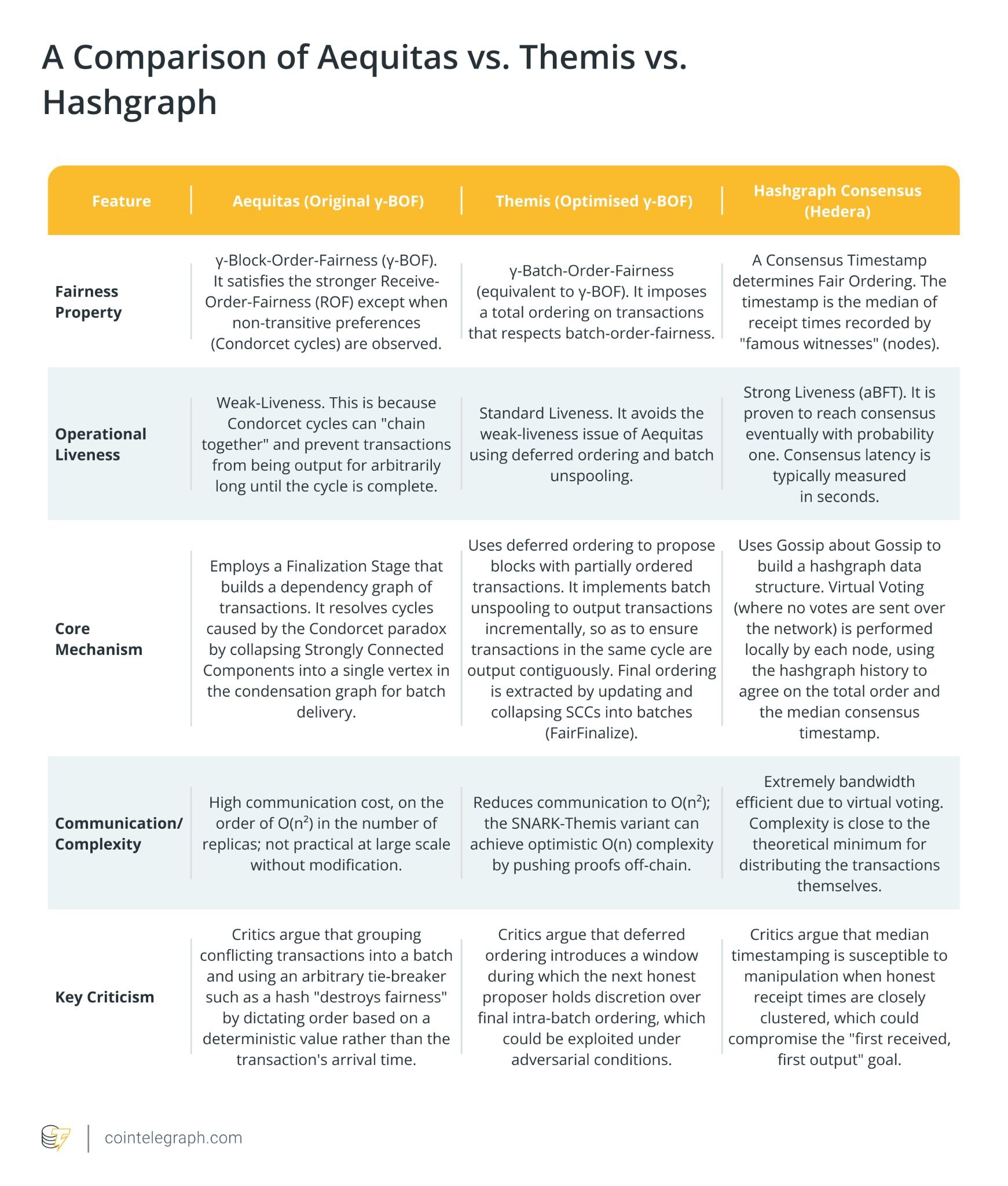

Hashgraph’s Fairness Model: Graph of Hashes, Median Timestamps, and aBFT Consensus

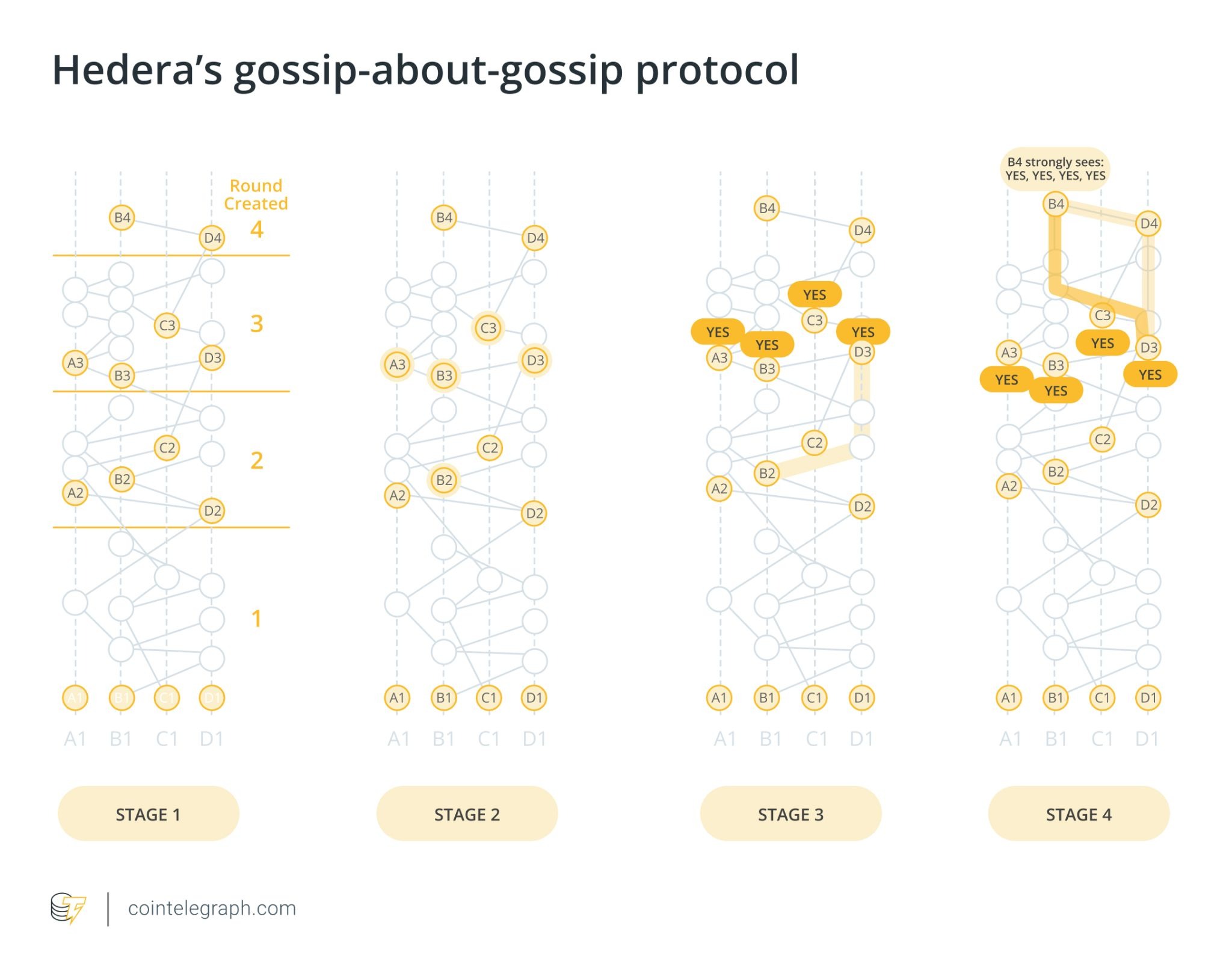

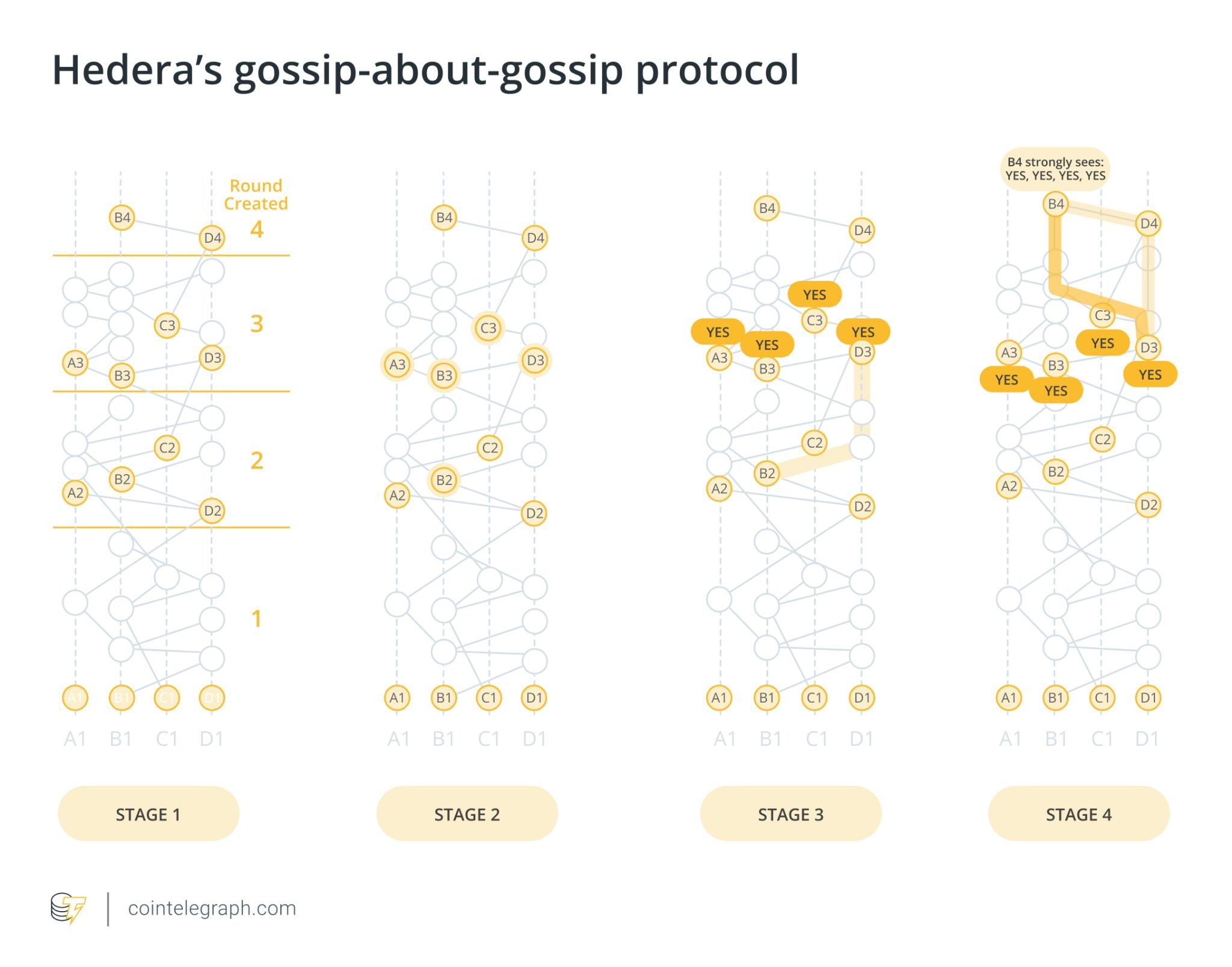

Hedera, which employs the hashgraph algorithm, approaches the fairness problem through a directed acyclic graph (DAG) of cryptographically linked events. It is a leaderless consensus algorithm that operates in a fully asynchronous setting and achieves Asynchronous Byzantine Fault Tolerant (aBFT). Under this model, honest nodes eventually reach agreement on the same transaction log even under unbounded message delays. Consensus ordering emerges from network-wide observation through a virtual voting process: the order is calculated collectively by nodes rather than assigned by a designated block producer.

When a node receives a transaction, it packages it into a message called an event and gossips it to peers. When another node creates a subsequent event, it records the hash of the events it has already seen and digitally signs the new event. This provides cryptographic proof that the node had seen prior events before signing the new one. The hashgraph, therefore, enforces causal order: once a node publishes an event, the ancestry embedded in that event proves which transactions preceded it.

This linkage can be represented as an edge in the DAG. If one event is a direct or indirect ancestor of another, a downward path exists between them in the graph, and the protocol provides a cryptographic guarantee that the ancestor event was created first. Transactions connected by such paths are ordered according to their causal relationships in the graph. When two events have no ancestor relationship, they are concurrent, and the protocol resolves their relative order through the round-received mechanism. Each event is assigned a round based on when a supermajority of nodes, defined as more than two-thirds, can be shown to have strongly seen it through the DAG structure. Events assigned to earlier rounds are ordered first.

For events that share the same round-received, the protocol uses median timestamps to determine ordering. Each node records a local timestamp when it first receives an event. The consensus timestamp assigned to an event is the median of the timestamps reported across the node set. This timestamp is not derived from arbitrary local clocks in isolation. It is constrained by the gossip ancestry preserved in the hashgraph: a node cannot claim to have received an event before its causal predecessors without producing a detectable inconsistency in the DAG.

Under the standard aBFT assumption that fewer than one-third of nodes are Byzantine, the median falls on an honest timestamp or between two honest timestamps, which prevents adversarial nodes from shifting the median beyond a bounded range.

The Condorcet paradox can still apply to concurrent events, specifically those with no ancestor relationship in the DAG, where different nodes may observe them in different orders. The DAG structure eliminates this ambiguity for causally linked events: no contradictory causal paths can exist because each event’s ancestry is cryptographically fixed at creation. Because gossip propagation typically causes new events to become descendants of prior events within fractions of a second, most transactions fall into clear causal chains. The remaining concurrent events are resolved through round-received assignment and median timestamps as described above.

However, the hashgraph’s fairness guarantees have a bounded adversarial surface. A node still determines when to gossip an event, which events to relay first, and how long to delay relaying. These choices reshape the first-seen patterns that feed into median timestamp computation. The DAG cannot misrepresent the causal order it records, but it can be strategically shaped by gossip behavior before that order is recorded.

BOF Protocols: Fairness Through Batch Aggregation

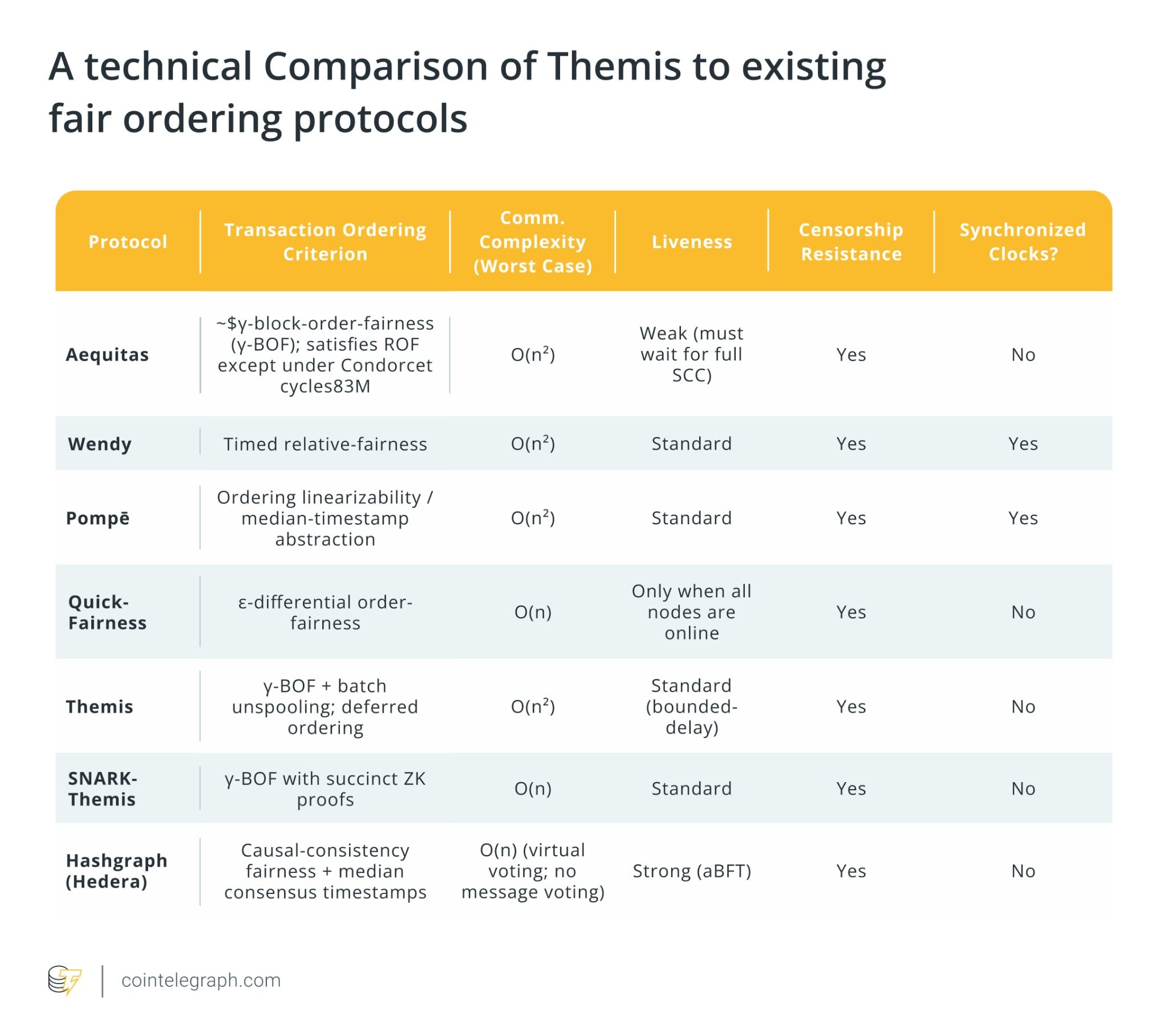

BOF protocols define a “block” as the set of transactions forming a single Condorcet cycle, and then order these blocks fairly while ignoring the ordering inside the block. The BOF criterion was first introduced by Mahimna Kelkar et al. (2020) in “Order-Fairness for Byzantine Consensus,” which formalized the Aequitas family of protocols. In Aequitas, BOF requires that if a γ-fraction of nodes observe block (b) before block (b′), then no honest node may output (b) after (b′). The γ-fraction is the proportion of nodes that must agree on a block ordering for that ordering to be considered “fair” and enforced by the consensus protocol.

For BOF, if the fairness predicate indicates that a transaction tx should precede tx′, then tx cannot appear in a later block than tx′. When the fairness relation becomes cyclic, the protocol collapses the entire strongly connected component into a single block, because BOF treats that block, not the individual transaction, as the atomic fairness unit. Under γ-BOF, the only forbidden outcome is placing tx′ in a strictly earlier block than tx when a directed constraint tx→tx′ exists. The protocol permits both transactions to appear in the same block and places no restrictions on their ordering inside that block.

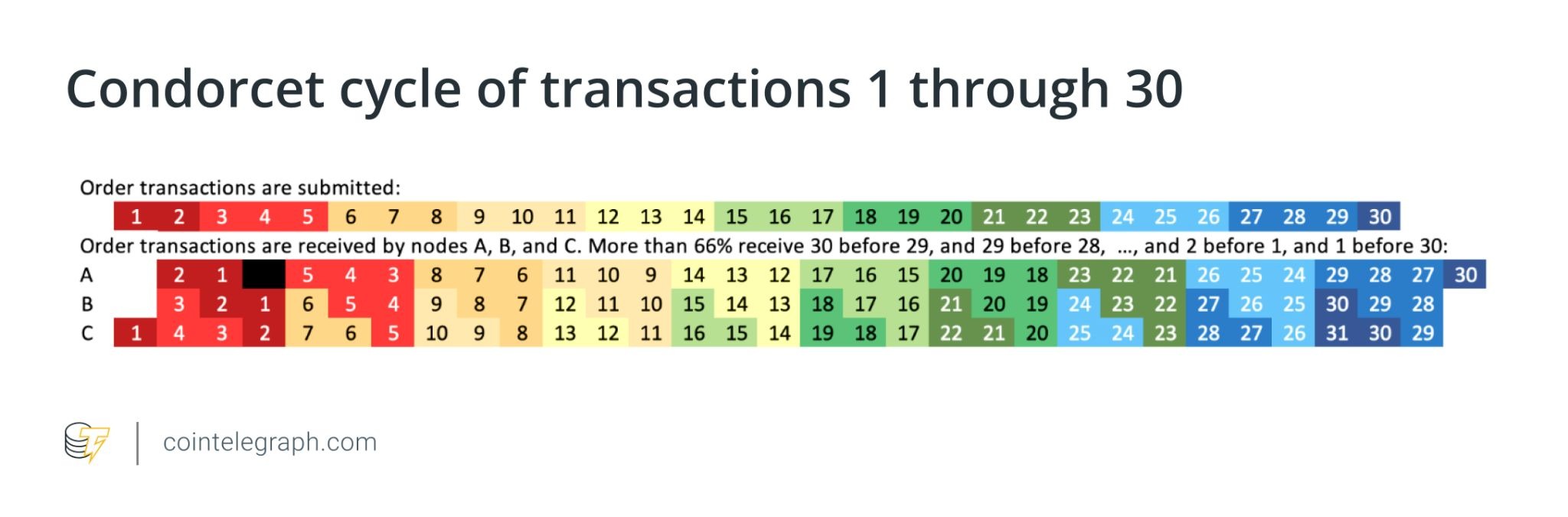

For example, Figure 2 below, is a Condorcet cycle of 30 transactions, so they would be in a single block. Sorting by hash might place 30 before 1 in the final ordering. However, a γ-fraction of nodes observed transaction 1 before transaction 30, yet placing 30 before 1 is still considered “fair” under γ-BOF. Because 1 and 30 are in the same block, and this notion of fairness only considers the order of the blocks, not the order of the transactions within a block.

When no cycles exist, BOF coincides with the strong form of ROF. When Condorcet cycles emerge, all transactions participating in the cycle are placed into a single block, and a deterministic method, such as a hash-based rule, orders events within that batch.

The protocol proceeds through three coordinated stages to ensure consistent transaction ordering across the network: the Gossip stage, the Agreement stage, and the Finalization stage.

In the gossip stage, nodes use FIFO broadcast to disseminate transactions in the order they were locally received per sender, preserving per-sender sequence so that each peer maintains a comparable transaction view. Once gossiping stabilizes, the agreement stage begins, where nodes execute a Set Byzantine Agreement (Set-BA) protocol to reach consensus on a unified set of local orderings that will serve as the foundation for the global order. In the finalization stage, nodes construct a dependency graph that captures transaction ordering relationships. Any transactions forming a cycle within this graph are grouped into the same strongly connected component and finalized together within a block.

However, Aequitas suffers from weak liveness, as its high communication cost and strict fairness constraints require the protocol to wait for the entire Condorcet cycle before finalizing the collapsed SCC. Because Condorcet cycles can chain indefinitely, this waiting period can grow without bound. Thus, transaction delivery can be delayed for an arbitrarily long time, and creates the “freeze” risk that defines Aequitas’ weak-liveness guarantee.

Themis was introduced to solve this. It preserves the same γ-BOF property while resolving these liveness and communication issues. Like Aequitas, Themis also constructs a dependency graph and collapses SCCs during its “FairFinalize” stage. The SCCs represent the same non-transitive Condorcet cycles underlying the γ-BOF relaxation, and Themis uses the condensation graph to derive the batch structure of the final output. The key difference is that Themis does not wait for a full cycle to complete. Instead, it uses deferred ordering and batch unspooling to output SCCs incrementally while allowing new transactions to continue flowing. This preserves γ-BOF but upgrades Aequitas’ weak liveness to standard liveness, and guarantees delivery within a delay bound.

In its standard form, Themis requires each participant to exchange messages with most other nodes in the network. As the number of participants increases, the amount of communication grows rapidly, roughly proportional to the square of the network size. However, in its optimized version, SNARK-Themis, nodes use succinct cryptographic proofs to verify fairness without needing to communicate directly with every other participant. This reduces the communication load so that it grows only in direct proportion to the number of nodes, thus allowing Themis to scale efficiently even in large networks.

If a malicious proposer attempts to exploit the situation by proposing an empty block, Themis employs deferred ordering, where the partially ordered batch (B₁) is still accepted, and the final, precise order of its transactions is determined later by the next honest proposer. That proposer finalizes the order based on verifiable transaction relationships, not personal discretion. This design ensures finalization depends only on bounded network delay, not on the arbitrary behavior of the current proposer, thus closing a key liveness gap that Aequitas could not guarantee.

This structure guarantees that every transaction is both included and executed deterministically, even in the presence of conflicting arrival orders. Because Themis leverages the internal dependency graph and SCC condensation to extract a final ordering, it is resilient to adversarial manipulation. Attackers cannot simply reorder or front-run other users’ transactions once they are included in the batch. Any attempt to alter dependencies would break the verified graph consistency.

In an empirical analysis by Mahimna Kelkar et al., γ-BOF resists adversarial reordering more strongly than timestamp-based approaches in geo-distributed networks. However, it requires significantly more computational and protocol complexity, which can also be seen as a downside.

Conclusion:

Perfect fairness in transaction ordering is structurally unattainable in distributed systems that lack synchronized clocks and instantaneous communication. The Condorcet paradox ensures that majority preferences can conflict in ways no single linear order can satisfy. The real question is how to find the most realistic and useful trade-offs.

Hashgraph and BOF represent two coherent answers. Neither approach is inherently superior. Both embed fairness directly into the consensus mechanism rather than relying on trust or authority. Both approaches demonstrate that fairness is not a binary property but a spectrum of trade-offs defined by formal impossibility results. Where synchrony is unavailable, and clocks are untrusted, the choice between median-timestamp aggregation and batch-order collapsing reflects different but equally principled responses to the same underlying constraint.

World has expanded access to AgentKit, a framework that has enabled verified users to connect AI agents to their digital identities and prove those agents represent real people rather than automated bot networks.

Summary

- World has expanded AgentKit, allowing AI agents to operate on behalf of verified human users through World ID.

- The framework supports AI tools such as Claude Code, Codex, Cursor, Hermes, and OpenClaw.

- A recent sale of 500 limited-edition hats demonstrated how verified AI agents can complete purchases while enforcing one-person limits.

According to World, the rollout comes as AI agents take on a growing number of online tasks, increasing demand for systems that can distinguish between software acting for a specific individual and large-scale automated operations.

The project, backed by OpenAI CEO Sam Altman, said AgentKit allows users to delegate actions to AI tools while keeping identity verification and user controls in place.

The release follows a period of increased attention for the project after major U.S. crypto trading platform Robinhood listed the World token, bringing additional visibility to the ecosystem.

Verified identities allow AI agents to act for users

Details published by World show that AgentKit links supported AI agents to a verified World ID, enabling websites and applications to confirm that an agent is acting on behalf of a unique human user. The company said the system is designed to help businesses enforce user-level rules and reduce abuse associated with automated accounts.

To access the framework, World stated that users need a verified World ID, a World App account, and a compatible AI agent. Supported options currently include Claude Code, Codex, Cursor, Hermes, and OpenClaw.

Through World’s ToolRouter interface, users can create credentials and authorize their agents to interact with supported services. According to the company, this process allows individuals to assign tasks to AI systems without giving up identity verification tied to their accounts.

Rather than relying solely on account credentials, the framework adds proof that an agent represents a verified person, which World said can help online services distinguish legitimate activity from coordinated bot behavior.

Demonstration shows AI agents completing purchases

To showcase the technology, World recently organized a limited-edition sale of 500 “Human in the Loop” hats. According to the company, AI agents handled the entire purchase process for participating users.

World said the agents discovered the product launch, checked eligibility requirements, navigated the online storefront, and completed transactions without direct user involvement during the purchase flow.

Identity checks remained active throughout the event. According to the World, World ID verification ensured that purchase limits were enforced on a one-person-per-item basis, preventing users from bypassing restrictions through multiple automated accounts.

The company reported that all 500 hats were claimed by verified users located in countries including the United States, Germany, Japan, and the United Kingdom. World said the event demonstrated how businesses can permit AI agents to perform online actions while maintaining controls intended to reduce bot-driven abuse and automated farming activity.

As AI-powered software takes on more responsibilities across digital platforms, World said AgentKit provides a way to connect those agents to verified human identities, allowing organizations to verify who is ultimately behind automated actions carried out online.

Quick Summary

-

Kalshi launches legal action against Illinois over state prediction market licensing requirements.

-

New Illinois statute mandates state licenses for prediction market operators.

-

Platform argues existing CFTC regulation preempts state-level requirements.

-

Company requests injunction before July 1 implementation date.

-

Legal battle intensifies ongoing disputes over sports prediction market jurisdiction.

The prediction market platform Kalshi has initiated legal proceedings against Illinois officials, contesting recently enacted licensing legislation governing prediction markets and imposing fees on specific digital asset activities. The platform maintains that its event-based contracts fall under exclusive federal jurisdiction via the Commodity Futures Trading Commission. The company is pursuing court intervention to prevent the regulations from becoming operational on July 1.

Legal Action Targets State Licensing Framework

This week, Kalshi submitted its legal filing to the U.S. District Court for the Northern District of Illinois. The defendants include Governor JB Pritzker, Attorney General Kwame Raoul, and additional state officials. The case targets specific sections of SB3019, legislation that Pritzker approved as part of a comprehensive budget and revenue package.

Under the statute, operators of prediction markets must secure state authorization before conducting business with Illinois residents. Additionally, the legislation implements a 0.2% fee on designated digital asset transactions and associated services. Kalshi contends these mandates undermine a regulatory domain that Congress designated for federal oversight.

The platform functions as a designated contract market with CFTC registration under the Commodity Exchange Act. Kalshi maintains that Illinois lacks authority to establish an independent licensing framework for its federally supervised event contracts. The company asserts that such measures generate contradictory obligations and undermine consistent standards for nationwide derivatives platforms.

Jurisdictional Conflict Between Federal and State Regulators

According to Kalshi, the Commodity Exchange Act grants the CFTC sole jurisdiction over contracts executed on registered exchanges. State authorities, however, classify certain sports-related event contracts as gambling instruments subject to state gaming statutes. This fundamental disagreement has generated multiple legal confrontations between prediction platforms and state enforcement agencies.

The company indicates that adhering to state requirements would necessitate discontinuing specific sports contracts for Illinois customers. Such action could potentially violate federal uniformity standards applicable to products on designated contract markets. Kalshi would also incur significant expenses for geographic restriction technology, regulatory compliance infrastructure, and jurisdiction-specific product modifications.

A jurisdiction-by-jurisdiction regulatory approach could compel nationwide platforms to customize offerings based on individual customer locations. As a result, operators might require distinct licenses, contract portfolios, and access management systems across multiple states. Kalshi contends that Congress established federal derivatives oversight specifically to avoid such fragmented market conditions.

Platform Pursues Emergency Relief Before Deadline

Kalshi has filed for a temporary restraining order preventing Illinois from implementing the challenged provisions. The company also pursues preliminary and permanent injunctive relief pending resolution of its federal preemption arguments. The platform asserts that enforcement would inflict immediate business damage and generate irreversible operational costs.

This legal challenge emerges amid broader litigation concerning sports-focused prediction markets and federal regulatory jurisdiction. The CFTC has contested measures by nine states, including Illinois, while asserting its authority over registered exchanges. States maintain that local consumer safeguards and gaming statutes govern sports outcome contracts.

Illinois officials have previously stated their intention to uphold state authority and pursue consumer protection efforts within their borders. Neither Pritzker nor Raoul have provided immediate statements regarding Kalshi’s current legal filing. The judiciary must now determine whether federal derivatives legislation supersedes the newly established state licensing requirements.

U.S. President Donald Trump has halted the signing of a housing bill that includes a temporary ban on central bank digital currencies (CBDCs), citing a need to prioritize another piece of legislation he is pushing in Congress. The development adds uncertainty to the near-term U.S. regulatory path for digital assets, even as lawmakers move forward on separate crypto bills.

Trump said on Wednesday that he would cancel the signing ceremony for the “21st Century ROAD to Housing Act” and hold it “until such time as we pass the desperately needed SAVE America Act,” according to a post on Truth Social. The housing measure—already passed by both chambers—contains a CBDC restriction through the end of 2030, but also includes a carve-out for certain stablecoins.

Key takeaways

- Trump has delayed signing the 21st Century ROAD to Housing Act due to his insistence that Congress pass the SAVE America Act first.

- The housing bill bans the Federal Reserve from issuing or creating a CBDC (or a substantially similar digital asset) until the end of 2030, while allowing “dollar-denominated” stablecoins that are open, permissionless, and private.

- Trump’s stance raises uncertainty over how (and whether) he will handle other digital-asset legislation pending in the Senate.

- The Digital Asset Market Clarity (CLARITY) Act remains awaiting a potential Senate vote, and Trump has previously signaled support for codifying a “future-proof” market structure.

- If Trump vetoes related legislation, Congress could potentially override with a two-thirds vote in both chambers.

Housing bill stalled despite approval from both chambers

The “21st Century ROAD to Housing Act” passed the U.S. House on Tuesday and had previously cleared the Senate. While many observers expected Trump to sign the bill without delay, his Wednesday announcement suggests he may treat the SAVE America Act as a prerequisite for other legislation.

In his Truth Social post, Trump linked the cancellation directly to the need to pass the SAVE America Act. The bill he referred to is associated with changes to voting procedures, including a requirement that voters provide proof of U.S. citizenship in person to register—an approach that critics have argued could disenfranchise eligible voters.

This is not the first time Trump has floated a broader “no other bills” condition. Earlier this year, he said he would not sign other measures until the SAVE America Act is enacted, a position that now appears to be affecting the timeline for the housing package as well.

What the housing bill does on CBDCs—and where stablecoins fit

Supporters of the housing bill included a CBDC-limiting provision that would restrict U.S. central bank digital currency issuance. As reported in earlier coverage by Cointelegraph, the legislation bars the Federal Reserve from issuing or creating a CBDC or “any digital asset that is substantially similar” until the end of 2030.

At the same time, the bill includes a narrow exception for stablecoins. The text described in Cointelegraph’s coverage allows “dollar-denominated currency that is open, permissionless and private,” a carve-out designed to permit certain stablecoin models even under the broader CBDC restriction.

For crypto market participants, the carve-out matters because it frames how Congress could draw a line between CBDC-style instruments and private stablecoin systems. However, with Trump delaying signing, that legal boundary is not yet locked in—meaning the practical effect of the CBDC timeline could remain uncertain until the housing bill becomes law.

Regulatory ripple effects: CLARITY and the broader “market structure” debate

Trump’s insistence on prioritizing the SAVE America Act has also introduced questions about how he might act on crypto-related legislation that is still moving through Congress. As of Wednesday, the U.S. Senate was reportedly awaiting a potential vote on the Digital Asset Market Clarity (CLARITY) Act, a bill intended to reshape how regulators handle and enforce digital asset-related rules.

Cointelegraph previously reported that Trump said in May he intended to codify a “future-proof digital asset market structure,” which was widely understood as aligning with proposals like CLARITY. While the housing bill’s CBDC provision reflects Congress carving out limitations on central bank-backed digital currency efforts, CLARITY is aimed at defining regulatory roles and enforcement frameworks for the broader digital asset ecosystem.

Given the president’s stated approach of linking bill signings to passage of the SAVE America Act, the immediate risk for crypto policy timelines is straightforward: even if Congress passes measures, final enactment may still depend on executive scheduling and broader political leverage.

Lawmakers may still be able to override a veto

If Trump ultimately vetoes the housing bill or any other digital-asset-related legislation, Congress has a constitutional route to respond. As noted in the source coverage, lawmakers could override a veto by securing a two-thirds majority in both chambers.

That possibility means the outcome is not solely dependent on presidential action. Still, the delay itself can be meaningful for the market: regulatory certainty affects compliance planning, investment decisions, and how institutions allocate resources toward particular product or infrastructure strategies.

For now, investors and builders should watch whether the Senate brings CLARITY to a vote and, crucially, whether Trump’s SAVE America Act condition changes execution timelines for bills affecting the digital asset sector.

Cantor Equity Partners I has postponed its shareholder vote on a merger with Bitcoin Standard Treasury Company to July 2. The deal would list Adam Back’s firm, known as BSTR, on Nasdaq with 30,021 Bitcoin (BTC).

The special purpose acquisition company (SPAC), sponsored by a Cantor Fitzgerald affiliate, tied the delay to previously disclosed private placements. Shareholders were first due to vote on June 26.

BSTR Vote Slips as Treasury Stocks Fall

The companies first agreed to the merger in July 2025 and once aimed to close by late 2025. The postponement now arrives while digital asset treasury (DAT) companies absorb falling valuations.

Many trade near or below the value of the Bitcoin they hold, making fresh share sales dilutive. The strain is visible in Bitcoin’s recent price action.

Even Strategy (MSTR), the firm Michael Saylor turned into the template for corporate Bitcoin treasuries, has felt the squeeze. It remains the largest holder with 847,363 BTC. Yet its shares fell below $100 this week, the first time since March 2024.

Strategy has even slowed its buying, adding just 520 BTC recently while building a $1.4 billion cash reserve.

The Math Behind a Second-Place Bid

BSTR would arrive as the fifth-largest public Bitcoin treasury, about 13,000 coins shy of second place. Founders contribute 25,000 coins. Another 5,021 come from an in-kind raise paid in Bitcoin, which BSTR bills as a US SPAC first.

The listing would be Cantor Fitzgerald’s second Bitcoin treasury built through a SPAC. Its first, Cantor Equity Partners, created Twenty One Capital, a Tether-backed holder of 43,514 BTC. That company is one of the very treasuries BSTR now hopes to pass. Back has set a top-three treasury as his goal, naming it a target.

Back, who created Hashcash and co-founded Blockstream, is raising up to $1.5 billion to buy more Bitcoin. He recently denied a disputed Satoshi report from The New York Times. JAN3 chief executive Samson Mow estimated the full sum could add about 23,500 coins.

A full deployment would lift BSTR to roughly 53,500 BTC. That total would pass Metaplanet’s 40,177 BTC and Twenty One’s 43,514 BTC for second place, behind only Strategy. Mow says arriving late hands BSTR the lowest cost basis among large holders.

The outcome hinges on the July 2 vote and the level of redemptions before the June 30 deadline. Heavy redemptions would cut the cash BSTR can spend on Bitcoin, narrowing its path to the top.

The post BSTR Vote Delay Stalls Adam Back’s Push to Challenge Bitcoin Treasury Leaders appeared first on BeInCrypto.

Michelle Bond has lost her bid to dismiss criminal charges, with a federal judge setting her trial to begin on Nov. 9 after rejecting arguments tied to her husband Ryan Salame’s plea agreement.

Summary

- A federal judge has denied Michelle Bond’s bid to dismiss campaign finance charges and scheduled her trial for Nov. 9.

- Prosecutors allege Bond and Ryan Salame used about $400,000 in FTX funds to illegally finance her 2022 congressional campaign.

- Bond’s trial is among the final criminal cases tied to FTX’s collapse, while Sam Bankman-Fried continues pursuing post-conviction legal options.

According to an order from Judge George Daniels in the U.S. District Court for the Southern District of New York, Bond will face trial on four campaign finance-related charges in November. The ruling came one week after the court denied her request to throw out the indictment, which argued that federal prosecutors had agreed not to charge her if Salame pleaded guilty.

The case remains one of the last criminal proceedings connected to the collapse of cryptocurrency exchange FTX, which entered bankruptcy in 2022. Several former executives have already been prosecuted following the exchange’s failure.

Bond will face campaign finance charges in November

According to the August 2024 indictment, prosecutors allege that Bond and Salame illegally financed her 2022 campaign for the U.S. House of Representatives in New York’s 1st Congressional District.

Prosecutors claim Salame used about $400,000 originating from FTX through what they described as a sham payment to support the campaign in violation of federal campaign finance laws.

Federal prosecutors have charged Bond with conspiracy to cause unlawful political contributions, causing and receiving a straw donor contribution, causing and accepting excessive campaign contributions, and causing and accepting an unlawful corporate contribution. Each count carries a maximum prison sentence of five years.

The indictment further alleges that Bond tried to conceal the source of the campaign money by making false statements to a congressional committee and the Federal Election Commission. Bond has pleaded not guilty, and the allegations remain accusations that must be proven in court.

Earlier filings from Bond’s legal team argued that prosecutors had broken an agreement allegedly made during Salame’s plea negotiations by later bringing charges against her. Judge Daniels rejected that argument, allowing the prosecution to proceed toward trial.

Bond unsuccessfully sought the Republican nomination for New York’s 1st Congressional District in 2022, losing the primary election to Nicholas LaLota.

Most FTX criminal cases have already concluded

Meanwhile, Salame is serving a 90-month prison sentence after pleading guilty to conspiracy to make unlawful political contributions. After his sentencing, he attempted to withdraw his plea, arguing that prosecutors had misled him about whether Bond would face charges. He later abandoned that effort and reported to prison in October 2024, leaving the legal dispute to be addressed through Bond’s case.

Among senior FTX executives, Salame, former CEO Sam Bankman-Fried, and former Alameda Research CEO Caroline Ellison received prison sentences. Former FTX engineering director Nishad Singh and co-founder Gary Wang were sentenced to time served after cooperating with prosecutors and testifying during Bankman-Fried’s trial.

Apart from Bond’s upcoming proceedings, Bankman-Fried remains the only former FTX executive whose case was decided by a jury. He was convicted on seven felony counts and sentenced to 25 years in prison in 2024.

More recently, the Second Circuit Court of Appeals rejected Bankman-Fried’s appeal against his conviction and sentence. Court records leave a review by the U.S. Supreme Court or a presidential pardon as his remaining legal options. Bankman-Fried has also reportedly sought a pardon from President Donald Trump.

Crypto World

Crypto News, June 24: Crypto Chaos as BTC USD Tumbles with Chip Stocks, ETH Foundation Axes Staff, Rate Hike Looms

Crypto is stabilizing after BTC slid alongside the “AI darling” NVIDIA, while ETH USD continued its frustrating trend of underperforming expectations. Up until today, there has been no major crypto-specific disaster to blame. But the market is reminding us that Bitcoin and Ethereum are increasingly trading like high-beta tech assets, and the days of financial rebellion are long gone.

Wall Street’s AI obsession has linked crypto and semiconductor stocks into the same basket trade. Funds that piled into NVIDIA, AMD, and Bitcoin during the liquidity-fueled rally of the past two years are now trimming exposure as interest-rate fears return. That being said, BTC USD and ETH USD can sell off together with chip stocks even when nothing fundamentally changes inside.

— Coin Bureau (@coinbureau) June 23, 2026

NOW: NVIDIA SINKS BELOW $5 TRILLION AS INSTITUTIONS DUMP AI AND TECH STOCKS$NVDA has fallen more than 3% today, slipping below a $5 trillion market cap as investors sell AI and tech names.

NOW: NVIDIA SINKS BELOW $5 TRILLION AS INSTITUTIONS DUMP AI AND TECH STOCKS$NVDA has fallen more than 3% today, slipping below a $5 trillion market cap as investors sell AI and tech names.

Tech focused index $QQQ is down 2.5%, while overall S&P 500 has dropped more than 1%. pic.twitter.com/0VyyhwmpjL

Following the prolonged bear market, the Ethereum Foundation unveiled a major restructuring, slashing 20% of staff and cutting its budget by around 40%. At the same time, we are once again debating if the Federal Reserve will deliver another rate hike after a hawkish June meeting.

So, how bad is the market situation today?

Discover: The Best Crypto to Diversify Your Portfolio

BTC USD Falls With Nvidia: Chip Stocks = Crypto Signal?

The latest decline in BTC USD happened almost in lockstep with weakness across semiconductor stocks, particularly NVIDIA and other AI-related names. However, looking closely, semiconductor companies are not driving Bitcoin prices directly. But both assets have become part of the same institutional “high risk, high reward” trade.

Crypto is maturing, and we can see that during periods of abundant liquidity and strong economic growth, money aggressively enters assets with high upside potential. Bitcoin, AI stocks, and semiconductor companies all fit the description. It’s good and bad for crypto. It brings institutional money, but weakens community power.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

ETH USD Reality Check as Ethereum Foundation Shrinks

The biggest Ethereum story of the day came from the Ethereum Foundation’s surprise restructuring. According to the Foundation, staffing will be reduced by 20%, while operational spending will be cut by 40%. This is designed to create a leaner organization focused on core research and protocol development.

Vitalik Buterin defended the changes, noting that Ethereum needs greater focus and execution efficiency. In comments shared this week, he emphasized that Ethereum’s mission remains unchanged and that resources should be directed toward areas with the highest impact.

Vitalik addressed it directly on X:“

This year, the EF is decreasing its budget by roughly 40%… I will not try to pretend this. I respect my EF colleagues far too much to pretend that there was not much that is lost. They are brilliant people… The Ethereum Strawmap is no small thing… In the longer term, I personally favor a ‘soft lean-and-done’ approach to Ethereum… the ecosystem is adapting… and I am confident that Ethereum is very well-positioned to succeed and thrive.”

Unlike previous bull markets, Ethereum has struggled to dominate headlines this cycle. Spot ETFs arrived, but the explosive rally people expected never fully materialized; the $10k or even $7K targets remain targets. Competition from faster chains, growing institutional interest in Bitcoin, and fragmentation across Layer-2 ecosystems have diluted the narrative that once made Ethereum the undisputed king of crypto alts.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Yet some investors view the Foundation’s cuts as a positive development. A leaner organization may help Ethereum move faster, reduce bureaucracy, and focus on delivering upgrades that directly improve network competitiveness.

Discover: The Best Token Presales

Will Rate Hikes Crush BTC USD and ETH USD?

The other major concern hanging over markets is the Federal Reserve. While the Fed left interest rates unchanged during its June meeting, the tone was noticeably more hawkish than expected. Nine out of nineteen policymakers now expect at least one rate hike this year, compared with none in March projections. Officials have also “leaked” that a single rate hike in 2026 remains a realistic possibility.

Markets have become even more aggressive in their forecasts, with analysts now seeing meaningful odds of additional tightening as early as July or September. Bank of America has even floated the possibility of multiple hikes. For crypto, higher rates typically create a blockage because they reduce liquidity and, of course, make risk assets less attractive. That helps explain why BTC USD and ETH USD reacted negatively to the shift in expectations.

Still, investors should remember that projections are not promises. The Fed has changed course many times, as economic conditions have evolved, and several analysts continue to believe the next long-term move will eventually be a cut, and not another hike. The odds are small for a cut, but it’s not zero, and if people know there will be a hike, today might already be priced in.

Despite today’s weakness, institutional demand remains strong, spot ETFs continue attracting capital, and Bitcoin’s role as a scarce digital asset has not changed because semiconductor stocks had a bad day. If anything, sharp pullbacks driven by macro fears have historically created some of the most attractive entry points of a bull market.

The same argument can be made for ETH USD. Ethereum may not be delivering the explosive gains seen in previous cycles, but its ecosystem remains the foundation of decentralized finance, tokenization, and much of the on-chain economy. If inflation cools and rate fears fade, both Bitcoin and Ethereum could quickly return to being the market’s favorite risk assets.

Discover: The Best Crypto to Diversify Your Portfolio

The post Crypto News, June 24: Crypto Chaos as BTC USD Tumbles with Chip Stocks, ETH Foundation Axes Staff, Rate Hike Looms appeared first on Cryptonews.

Uniswap has added a no-code token auction tool to the Uniswap Web App, letting any team configure and launch an onchain token sale from a browser without writing code. The tool runs on Uniswap's Continuous Clearing Auction mechanism, which conducts price discovery entirely onchain. In a CCA, bids… Read the full story at The Defiant

Cathie Wood has dismissed mounting inflation fears despite U.S. headline CPI rising to 4.2% in May, arguing that underlying price pressures are close to disappearing.

Summary

- Cathie Wood says underlying inflation is near 0.5% despite headline U.S. CPI rising to 4.2% in May.

- The ARK Invest CEO cites productivity gains and Truflation data to argue inflation pressures are easing.

- Wood believes Fed Chair Kevin Warsh could support economic growth if inflation falls toward 0% to 1%.

According to the ARK Invest CEO, inflation fears dominated conversations during her recent investor meetings across Asia and Europe, where many participants questioned whether persistent price growth would force the Federal Reserve to tighten monetary policy further.

In a series of X posts, Wood said she was surprised by how strongly investors expected inflation to remain elevated, adding that she believes inflation could weaken sharply for reasons extending beyond lower oil prices.

The comments come as financial markets have increased bets that the Fed could raise interest rates by another 25 basis points in September after the latest inflation data. At the same time, Fed Chair Kevin Warsh has continued to stress the central bank’s commitment to returning inflation to its 2% target.

Labor costs and real-time data point to weaker inflation

Presenting a different view of price pressures, Wood argued that underlying inflation is already close to disappearing when measured through labor costs rather than headline consumer prices.

According to Wood, U.S. productivity increased roughly 3% year over year during the first quarter while compensation per hour rose about 3.5%. Using those figures, she said unit labor costs indicate underlying inflation of only 0.5% year over year, suggesting businesses are not facing meaningful cost-driven inflation.

Wood also pointed to alternative inflation measures that differ from official government statistics. Citing data from Truflation, she said the platform’s real-time inflation gauge has fallen from approximately 11% year over year in 2022 to 1.8%, while its core inflation reading has declined to 1.4%.

Based on those indicators, Wood argued that current inflation trends are considerably weaker than headline CPI figures suggest. She maintained that investors placing heavy weight on government inflation data may be overlooking signals coming from productivity and private-sector pricing measures.

Wood expects Kevin Warsh to support growth if inflation eases

Looking ahead, Wood said she believes Warsh understands the distinction between official inflation readings and conditions developing across the broader economy.

According to her assessment, productivity gains are helping reduce inflationary pressure, while existing government inflation measures contain methodological shortcomings that can overstate underlying price growth.

Wood added that if the U.S. economy continues expanding while inflation falls toward a range of 0% to 1% or below, she expects the Federal Reserve under Warsh to place more emphasis on supporting economic growth instead of maintaining restrictive monetary policy.

https://x.com/CathieDWood/status/2069817965369843959

Her outlook contrasts with current market positioning, where traders have increased expectations for another rate hike following the stronger-than-expected May CPI report. Even so, Wood argued that continued improvements in productivity and easing cost pressures could eventually reduce the need for tighter monetary policy.

Concluding her remarks, Wood said she expects the Fed’s policy stance to evolve once inflation weakens further, allowing the central bank to encourage economic growth rather than focus primarily on containing inflation.

The Commodity Futures Trading Commission filed suit against Kentucky on Tuesday, bringing the total number of states facing federal litigation over prediction-market jurisdiction to nine. The CFTC's complaint seeks declaratory and injunctive relief to block Kentucky from enforcing state gaming… Read the full story at The Defiant

Coinbase opened its Luxembourg office on June 24, naming the country its European Union hub under the Markets in Crypto-Assets (MiCA) framework. Binance, by contrast, just withdrew its license bid in Greece.

The contrast shows how regulatory track records increasingly decide who keeps EU access before the deadline on July 1. Early movers gain a 27-state passport, while latecomers risk losing the bloc.

Coinbase Locks In Its Luxembourg Base

Coinbase won its MiCA license from Luxembourg’s Commission de Surveillance du Secteur Financier in June 2025. That came more than a year before the deadline.

The company already held national licenses in six EU countries, including Germany and France. It has also traded publicly on Nasdaq since 2021, giving regulators years of audited disclosures.

The single license covers more than 450 million people across the EU. Coinbase Luxembourg S.A. now sits on ESMA’s register, joining the firms approved under MiCA across the bloc.

Chief Policy Officer Faryar Shirzad opened the office alongside Luxembourg Finance Minister Gilles Roth.

“Luxembourg has established itself as the EU’s leading hub for institutional crypto and tokenization,” he said in a post.

Follow us on X to get the latest news as it happens

Binance Faces a MiCA Reckoning

Binance took the opposite path this week. The exchange confirmed its Greek license bid had collapsed, leaving it absent from ESMA’s register.

Regulators have long weighed Binance’s record. In 2023, it pleaded guilty in the United States to money-laundering and sanctions violations.

Binance paid more than $4.3 billion, one of the largest corporate penalties in US history. Founder Changpeng Zhao pleaded guilty and resigned as chief executive.

It now plans to seek approval in another EU member state. Binance says it meets MiCA standards and points to roughly 1,500 compliance staff.

“Binance is not leaving Europe,” Gillian Lynch, Binance’s head of Europe and UK, told Reuters.

What Comes Next

With days left before the deadline, more than 230 firms have cleared MiCA and can keep serving EU users. Coinbase and rivals including Kraken sit on ESMA’s list.

Binance does not. Its return now hinges on convincing another regulator that its compliance matches its size.

The post Coinbase Opens Luxembourg MiCA Hub as Binance Races EU Deadline appeared first on BeInCrypto.

THE BIG SHORT! I’M DONE WITH BITCOIN

Hidden bay provides peaceful escape from overcrowded beaches amid heatwave

Macy’s EVP, COO & CFO Edwards Jr. sells $408,726 in stock

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Miami – Corporette.com

-

Entertainment4 days ago

Entertainment4 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Tech3 days ago

Tech3 days agoMicrosoft accidentally kills epic Outlook email threads

-

Sports1 day ago

Sports1 day agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Business4 days ago

Business4 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Crypto World22 hours ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Politics6 days ago

Politics6 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Politics5 days ago

Politics5 days agoAndy Burnham and the meaning of Makerfield

-

Crypto World19 hours ago

Crypto World19 hours agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business1 day ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Business5 days ago

Business5 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

NewsBeat5 days ago

NewsBeat5 days agoKeir Starmer Allies Question His Chances For No 10

-

Tech6 days ago

Tech6 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

Crypto World5 days ago

Crypto World5 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World5 days ago

Crypto World5 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World5 days ago

Crypto World5 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Tech4 days ago

Tech4 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Entertainment5 days ago

Entertainment5 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Tech2 days ago

Tech2 days agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Business6 days ago

Business6 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

You must be logged in to post a comment Login