Crypto World

French police bust $1.8M crypto villa scam targeting wealthy couple

French police have arrested two suspected fraudsters accused of stealing about $1.8 million in cryptoassets from a wealthy couple during a fake villa sale after a year-long investigation.

Summary

- French police arrested a mother and son accused of stealing €1.5 million in crypto during a fake villa sale.

- Investigators allege the suspects used hidden camera glasses to capture wallet credentials and drain the victims’ funds.

- The case comes as France reports a continued rise in crypto-related crimes, including kidnappings and extortion.

According to French newspaper Var-Matin, French police from the Gassin–Saint-Tropez gendarmerie arrested a mother and her son on June 25 at a rented villa in Cavalaire-sur-Mer. The pair are accused of orchestrating a sophisticated “rip deal” that targeted a couple from Ramatuelle who had placed their villa, valued at around €10 million (about $12 million), on the market in the spring of 2025.

According to the report, the suspects presented themselves as intermediaries acting for a wealthy Italian buyer and invited the sellers to Milan for negotiations. There, the supposed buyer allegedly offered to pay more than the asking price but required proof that the sellers could cover €1.5 million ($1.8 million) in transaction-related costs through cryptoassets before completing the purchase.

How the alleged crypto theft was carried out

French investigators said the second meeting in Milan became the turning point in the scheme. According to the Gassin–Saint-Tropez gendarmerie, the suspects asked to verify that the required cryptoassets existed before the transaction proceeded.

Investigators believe the pair secretly obtained the victims’ wallet information by distracting them while using hidden cameras integrated into a pair of glasses to capture sensitive wallet credentials. Authorities alleged the suspects gained access to the account details and private security keys before immediately draining the crypto holdings.

Following what the gendarmerie described as a long and complex investigation, officers identified the suspects despite their use of false identities and their frequent travel across France. The defendants, who reportedly live in the Paris region and have prior criminal records for similar offenses, denied the allegations during police questioning.

The suspects have been placed under judicial supervision and are scheduled to appear before the Draguignan Criminal Court on Sept. 1. They face charges including organized fraud and failure to justify financial resources.

Meanwhile, French courts have ordered the seizure of three Côte d’Azur properties linked to the suspects with an estimated combined value of €1.9 million pending the outcome of the case.

France faces continued rise in crypto-related crime

Although investigators classified the incident as a classic “rip deal” rather than a violent crypto extortion case, the alleged theft comes as France continues to record a growing number of crimes targeting digital asset holders.

Earlier this week, as reported by crypto.news, French Interior Minister Laurent Nuñez said authorities had recorded 77 cases involving kidnapping, unlawful detention, extortion or attempted offenses connected to the crypto sector in 2026, up from 45 cases in 2025.

Nuñez told industry representatives that the incidents were “serious matters” while saying emergency security measures introduced over the past year had started to produce results. He also said roughly 200 people had been arrested following attacks or preventive operations, while 724 industry participants had enrolled in France’s immediate identification platform, an 11% increase.

Separately, crypto journalist Joe Nakamoto previously said, as reported by crypto.news, that France accounts for about 70% of reported physical attacks against crypto holders and their families.

Nakamoto also reported 41 crypto-linked kidnappings in the country so far in 2026, averaging roughly one incident every two and a half days. His figures describe so-called “crypto wrench attacks,” in which criminals use violence, threats, kidnapping, or home invasions to force victims or their relatives to surrender access to digital assets.

While the Ramatuelle case relied on deception instead of physical coercion, investigators say it demonstrates how criminals are adapting traditional real estate fraud schemes to target cryptocurrency owners.

Crypto’s most prominent former regulator wants the industry to stop treating the CLARITY Act as make-or-break. Chris Giancarlo, who chaired the Commodity Futures Trading Commission from 2017 to 2019, says the technology gets built either way.

Giancarlo still wants the bill passed. However, he argues the industry has staked its public message on legislation that has sat idle in the Senate for 80 days.

The CLARITY Act Is Not a Precondition

Speaking in a recent interview, Giancarlo said the sector has overcommitted to one piece of legislation.

“Now, what I’d say to the industry is perhaps it’s time to stop making such a big deal out of CLARITY,” he said.

The timeline explains the anxiety. The House passed H.R. 3633 on July 17, 2025, by 294 votes to 134. The Senate Banking Committee advanced it 15-9 on May 14, 2026.

No floor vote has followed. The Senate calendar sends the chamber home from August 10 until September 11, leaving roughly one week of floor time.

Giancarlo pointed to an older technology as precedent.

“The industry is running around saying we need clarity, we need clarity. Yeah, we do. But the internet is still happening and there’s never been an authorizing statute 30 years later. If we don’t get clarity, innovation goes on.”

Follow us on X to get the latest news as it happens

That cuts against the message from the bill’s loudest backers, including MicroStrategy and its lead Senate author, Cynthia Lummis.

Why Giancarlo Still Wants the Bill

His position is not opposition, and part of it is personal. Section 503 codifies LabCFTC, the fintech office he created in May 2017 as acting chairman.

He wants every financial regulator in Washington to run something similar.

“I’d like to see clarity pass, but I think we need to brace ourselves that it might not and the world is going to go on.”

The Precedent That Worries Him

Giancarlo also warns that legislation drags surveillance along with it. Public Law 119-27, the GENIUS Act, subjects permitted stablecoin issuers to the Bank Secrecy Act.

CLARITY applies the same standard to digital asset transactions. Giancarlo argues that approach violates Fourth Amendment privacy rights.

What Happens If CLARITY Fails

The CFTC is running on one Senate-confirmed official. Michael Selig, sworn in as the 16th chairman in December 2025, occupies the only filled seat of five.

Giancarlo expects the agency to keep moving with or without a statute.

“This is a change that is going to happen whether the clarity bill passes or not… Clarity will bring order to how that change happens. But it’s not going to stop that change.”

Failure would separate builders from spectators, he argued.

“If clarity doesn’t pass, the… premium for courage is going to go up.”

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Stop Acting Like the CLARITY Act Is Everything, Former Regulator Says appeared first on BeInCrypto.

SpaceX earnings land Tuesday, August 4, marking the first since the company went public. The June listing already paid Morgan Stanley bankers about $100 million in fees.

That fee was the small part. IPOs led by SpaceX sent more than $74 billion to the bank’s wealth arm. Now SpaceX has to show the numbers behind it.

How the SpaceX IPO Built Morgan Stanley’s $10 Trillion Quarter

SpaceX sold 555,555,555 shares at $135 each on June 11. That raised $75 billion. It is the biggest IPO ever, more than double the $29.4 billion Saudi Aramco raised in 2019.

Ten banks ran the deal. Goldman Sachs, Morgan Stanley, BofA Securities, Citigroup and J.P. Morgan led them. They all shared the fee pool.

Only one of those banks also ran SpaceX employee stock plans. That is what set Morgan Stanley apart.

Here is why it matters. When staff get rich on IPO day, the money lands wherever their stock plan already lives.

Morgan Stanley’s wealth arm took in $148.1 billion of new client money last quarter. A year ago the figure was $59.2 billion.

Just over half came from IPOs of stock plan clients, its earnings release shows. That is more than $74 billion in three months. Bloomberg reported a large share came from SpaceX.

The bank calls this unit Workplace. It bought Solium Capital in 2019 and E*Trade in 2020 to build it. Both deals pushed the firm deeper into steady fee income after the 2008 crisis.

Workplace now serves over half the S&P 500. It also covers about 70% of the 100 biggest private companies worth more than $1 billion. Total client assets passed $10 trillion.

Jed Finn runs Morgan Stanley’s wealth business. He sees the IPO as a start, not a payday.

“It would be a mistake to think about the IPO as a one-off event for asset capture. These are opportunities with multiple phases, with shares that get unlocked and new shares issued.”

Follow us on X to get the latest news as it happens

Here is the catch. Most of that money is not earning fees yet.

Morgan Stanley charges a fee once clients move cash into managed accounts. Only 26% of the new money went that way last quarter. A year earlier it was 72%.

Bloomberg puts the yearly revenue from SpaceX-linked money above $100 million. Getting it depends on shares that are still locked.

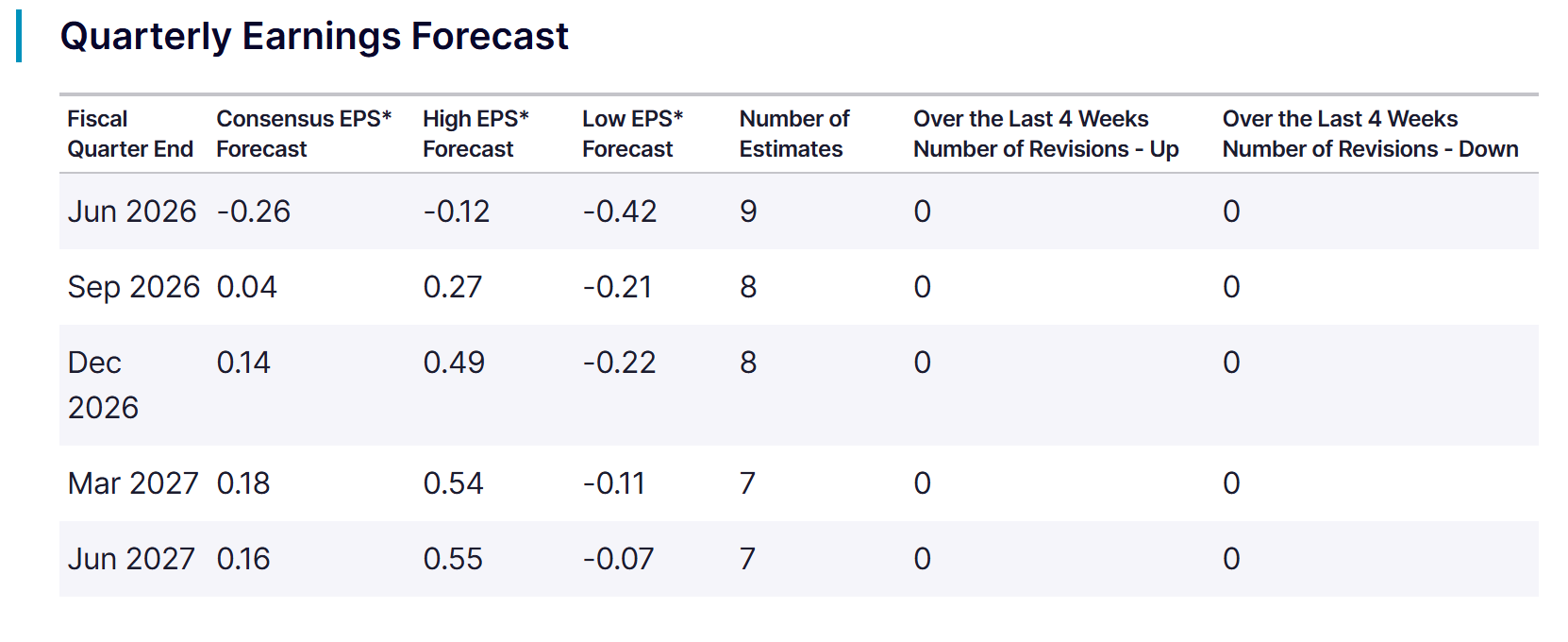

What SpaceX Earnings Have to Prove on August 4

Results come after the close on Tuesday. Analysts expect a loss of 26 cents a share. Nine of them filed forecasts, per Zacks.

This is the first real look inside the business. Investors want launch numbers, Starlink revenue, and the split between government and commercial work.

The stock has not waited. SPCX closed at $108.37 on July 31. That is 20% below the $135 offer price and 33% below its $161 first-day close. It hit a record low last week.

Contracts have not helped either. Shares still fell after SpaceX won $1.6 billion in Space Force launch work through 2027.

Then comes August 6. About 911.5 million locked shares become free to sell, two trading days after earnings.

At Friday’s price that is close to $99 billion of stock. It is more than the IPO itself raised. Meta’s 2012 unlock is the closest thing to a warning here.

Morgan Stanley has already been paid. It raised its dividend 15 cents to $1.15 and approved $20 billion in share buybacks. SpaceX investors are still waiting.

The post SpaceX IPO Paid Wall Street $100 Million: Will It’s First Earnings Repay Investors? appeared first on BeInCrypto.

White House teleprompter operator Gabriel Perez is no longer employed by the federal government after being placed on unpaid leave over allegations that he used insider knowledge to bet on President Donald Trump’s speeches, according to another official.

Speaking on condition of anonymity, the official said that Perez had left his government job but did not say whether he resigned or was fired.

Inside the Allegations

The White House had suspended Perez earlier this month following an ABC News report that alleged he made more than $100,000 through bets on the online prediction market Kalshi. The report said the wagers were based on advance knowledge of what Trump would say during major speeches, including the State of the Union address earlier this year.

The allegations drew a sharp response from the White House. Press secretary Karoline Leavitt described the reported insider trading as “deeply unfortunate and, frankly, a disgrace.” Kalshi also responded after the report was published.

Robert Denault, the company’s lawyer and head of enforcement, said in a post on X that its surveillance team detected the trades, investigated them, and referred the matter to the US Commodity Futures Trading Commission (CFTC). Denault’s statement did not identify Perez by name.

Legal Battles

Kalshi has faced legal hurdles this year in Massachusetts, Michigan, Nevada, and Washington. At the same time, it has also tightened its own rules. In April, the prediction market suspended three political candidates for betting on elections they were contesting after determining that the trades amounted to political insider trading under its CFTC-approved rules.

An insider trading case on Polymarket also surfaced that same month. Federal prosecutors charged US soldier Gannon Ken Van Dyke with allegedly betting on whether former Venezuelan President Nicolás Maduro would be removed from power. Authorities said Van Dyke, who worked on the operation targeting Maduro, made about $400,000 from the trades.

The legal battle over prediction markets has also taken a new turn. This week, a federal judge temporarily blocked Minnesota from enforcing a new law that would have banned prediction markets in the state. The ruling gave a temporary win to Kalshi, Polymarket, and the CFTC as the case moves forward.

Judge Katherine Menendez said the law is likely preempted by the federal Commodity Exchange Act because many event contracts may qualify as federally regulated swaps. The law, signed by Governor Tim Walz in May, was set to take effect on Saturday. The judge said the injunction could later be narrowed if needed.

The post Teleprompter Operator Accused in Kalshi Betting Case Is No Longer a Federal Employee appeared first on CryptoPotato.

President Donald Trump reshared a White House post on Sunday about restarting California’s Sable Pipeline. The same day, OPEC+ agreed to pump more oil from September.

Both moves add oil to the market. Neither has helped drivers yet. Californians paid $5.49 a gallon in late July, the highest price in the country.

Why Trump Revived a March Order Now

Gas is expensive, and Trump knows it.

US drivers paid about $4.10 a gallon in the week to July 27, federal data shows. That is 97 cents more than a year ago.

In June, Trump told fuel retailers to cut prices to $2.50. They have not.

California hurts most at $5.49 a gallon. That is roughly $1.39 above the national average, which makes the state an obvious target.

On March 13, Trump signed an order giving Energy Secretary Chris Wright emergency powers. The law behind it, the Defense Production Act, lets Washington direct private companies during a crisis.

Wright told Sable Offshore Corp. to reopen the Santa Ynez Pipeline. It had sat unused since a 2015 oil spill.

Oil flowed the next day. Sable aimed to sell about 50,000 barrels daily from April 1, a company filing shows. The line can carry 200,000.

Courts keep pushing back. On June 17, a California appeals court blocked Sable’s coastal work, backing state regulators in a published opinion.

OPEC+ Supply Hike Opens One Tap, Not All

Seven countries agreed to pump 188,000 more barrels a day from September. Saudi Arabia and Russia account for most of that, at about 62,000 barrels each.

The move finishes one round of cuts. The group had held back 1.65 million barrels a day since April 2023. That batch is now fully back.

A second cut from November 2023 stays in place. So the taps are not fully open.

OPEC says it can still speed up, pause, or reverse, according to its July statement.

Harder talks come in 2027, when the group sets new limits for each member. Iraq already wants a bigger share.

What This Means for Crypto

More oil has not made oil cheaper.

Brent crude sat near $87 on July 20. US crude was close to $84. Those are the latest daily figures from the Energy Information Administration.

Wars in Iran and Ukraine explain the gap. They block exports, so the extra barrels stay stuck on paper.

That matters for Bitcoin. Costlier fuel pushes inflation higher, and energy costs pressure Bitcoin by making rate cuts less likely.

Cheaper fuel does the opposite. It gives the Federal Reserve room to cut, which has lifted risk assets before, such as after the Fed held rates steady.

The question now is simple. Will September’s barrels reach buyers, or stay stuck?

The post Trump’s Oil Order Meets OPEC+ Supply Hike: Why California Gas Costs $5.49 appeared first on BeInCrypto.

Data shared by Lookonchain earlier today suggests that Trump Media, the entity behind the Truth Social media platform, majority-owned by the Donald J. Trump Revocable Trust, has sold over $165 million worth of bitcoin.

This was the second substantial sale made by the entity in recent months after it had splashed over $1 billion at prices near the top last year to accumulate 11,542 units.

The on-chain analytics company noted that the latest offload was for 2,628 BTC after it had transferred the stash to crypto.com. This continued a streak that began earlier this year.

Previously, the entity had spent $1.37 billion to acquire 11,542 BTC at an average price of $118,522. Since its entry level was very close to bitcoin’s very top marked just under a year ago, this automatically means that its sales have been completed at prices well below that.

CryptoPotato reported the previous BTC disposal in May, when wallets linked to Trump Media sold another substantial batch of 2,650 BTC for $205 million.

Lookonchain’s data concurs that the entity has sold a total of 7,281 BTC since it began disposing of its assets, at an average price of under $75,000. This means that its total losses have grown to $555 million.

It looks like Trump Media sold another 2,628 $BTC($165.07M).

Trump Media bought 11,542 $BTC($1.37B) at an average price of $118,522, then started selling 7 months ago, selling a total of 7,281 $BTC ($545M) at an average price of $74,855.

Trump Media is now down a total of $555M… pic.twitter.com/9xx0MTbweg

— Lookonchain (@lookonchain) August 2, 2026

Aside from the continuous controversial decisions toward the crypto industry from the POTUS-linked companies, this move builds on a recent worrisome trend about BTC treasury firms deciding to sell during times of distress.

As we reported last week, several public companies have shifted their strategies, with some selling BTC holdings while others have paused buying the asset indefinitely.

The post Trump Media Sells Another $165M in Bitcoin, Booking a Fresh Loss appeared first on CryptoPotato.

After two consecutive painful months in which they lost billions of dollars, the spot Bitcoin ETFs finally turned the page in July, but inflows were still modest.

Meanwhile, the exchange-traded funds tracking the performance of the largest altcoin enjoyed the month more, attracting over 2x more fresh capital.

Bitcoin ETFs in July

March and April were quite bullish for the spot BTC ETFs as the financial vehicles attracted well over $3 billion. However, the trend changed violently in May when they lost $2.43 billion. June became the worst month on record, as investors pulled out just over $4.5 billion. In total, the net outflows for May and June stood at nearly $7 billion, and the cumulative total flows dropped from over $58 billion to $51 billion.

July started more positively, with almost $200 million in net inflows during the first full week. Another $76 million followed during the second, and a more modest $34 million in the third. The trend was obvious as the initial high numbers gradually declined, aligning with the underlying asset’s controversial and sporadic price performance and ultimately leading to a very modest increase throughout the month.

The last week in July was once again in the red, with investors pulling $61.53 million out of the funds. Friday was the most painful day, as the total net outflows stood at over $265 million. As such, the month ended with $172.42 million. On one hand, green finally overcame the red wave, but on the other, the number was nowhere near enough to offset some of the recent losses.

ETH ETFs Do Better

The Ethereum ETFs entered July after a similarly painful two-month streak, in which they lost $541 million in May and another $529 million in June. However, investors were more persistent, and the actual net inflows for July were at a more respectable $365.17 million, thus outpacing the BTC ETF flows by over 2x.

Moreover, the ETH ETFs closed all four full weeks of July in the green, including the last one, which saw only one day in the red. Perhaps this investor behavior is among the reasons behind the underlying asset’s major resurgence in July. As reported earlier, ETH ended the month with a substantial 20% increase, making it the best in precisely a year.

All eyes are now on August, which hasn’t been ETH’s most favorable month historically, but there are some major double-digit exceptions.

The post Bitcoin vs. Ethereum ETF Battle: Who Won July? appeared first on CryptoPotato.

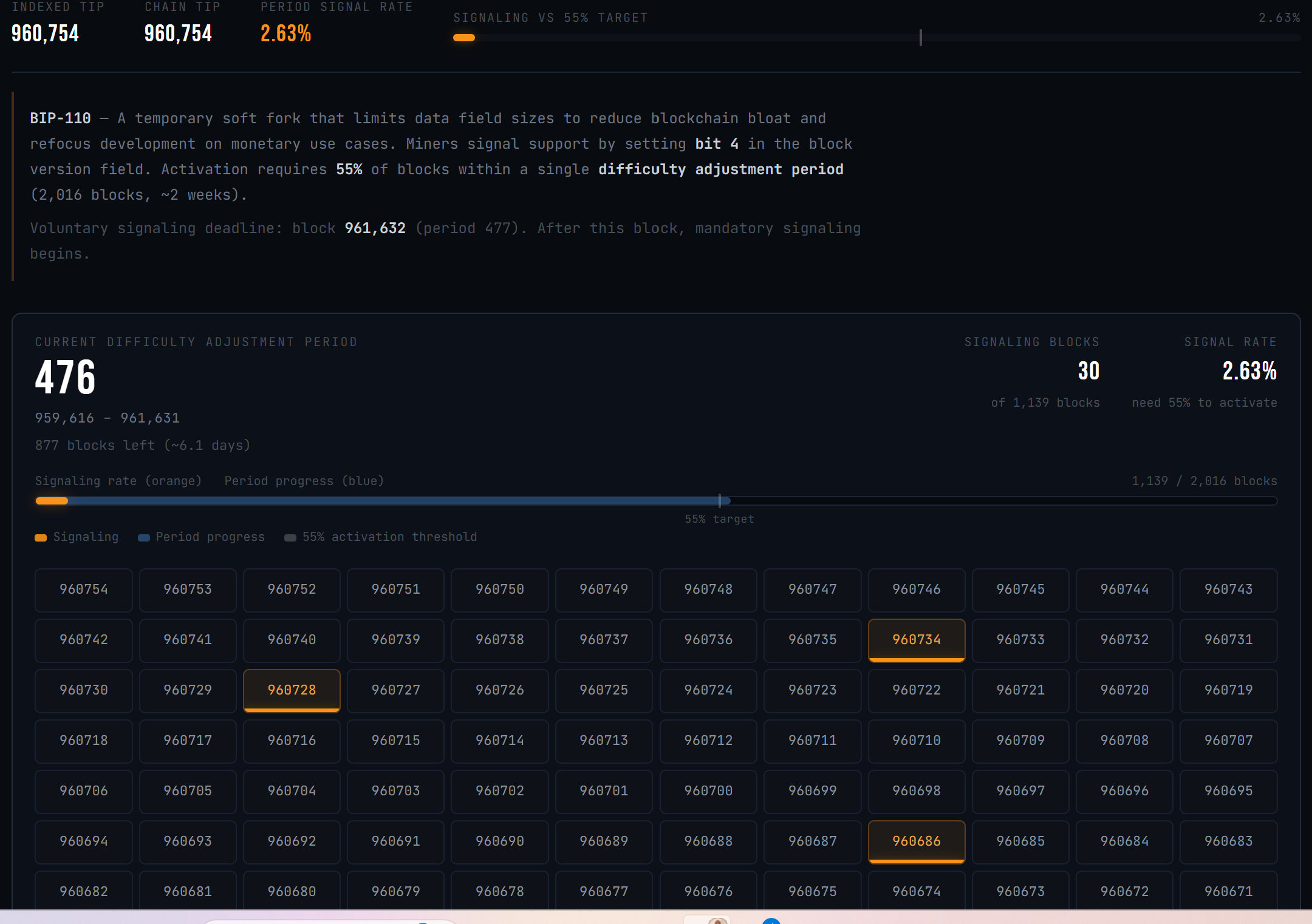

The developers pushing Bitcoin’s BIP-110 rule change have called off its launch. They blamed the industry response to a Coldcard wallet flaw that left user funds easier to steal.

Udi Wertheimer announced the delay, urging anyone running BIP-110 software to switch back to a normal Bitcoin (BTC) node. He gave no new date.

Why BIP-110 Activation Was Paused

BIP-110 is a temporary rule change, known as a soft fork. It would limit how much data people can pack into Bitcoin transactions.

Supporters say that data crowds out ordinary payments. Critics say Bitcoin should not police what users store.

The limits would last one year. Developer Dathon Ohm wrote the rules, and Bitcoin Knots software ships them.

Miners started voting on December 1, 2025. The Bitcoin blockspace spam debate had already split the community.

Then a separate problem landed.

Coinkite disclosed the bug on July 30. Its COLDCARD wallets built seed phrases, the master key behind a wallet, using far less randomness than promised. Roughly 72 bits instead of 128.

That gap makes a seed vastly easier to guess. Wallets running firmware released since March 2021 were hit hardest.

Updating the device does not fix a seed it already made. Coinkite is telling owners to move their money.

Thieves had already drained wallets tied to the flaw. The company has not said how much was lost.

Wertheimer called the delay a matter of timing, not doubt.

“…due to the coldcard incident, BIP-110 community leaders have decided to DELAY ACTIVATION. a new activation date will be announced at a later time,” he wrote.

Follow us on X to get the latest news as it happens

The Math Was Already Settled

Miners back a rule change by flagging their blocks. BIP-110 needed 55% of blocks in a two-week stretch. That means 1,109 blocks. The live monitor counted 30.

That is 2.63% of 1,068 blocks mined this period. It is the best BIP-110 has ever managed. It is still more than 20 times short.

Every earlier two-week stretch since December finished below 1.3%. Only 948 blocks are left. Even if every one voted yes, the total would reach about 48%. It could not pass this round.

That was already true days before anyone announced a delay.

Michael Saylor has warned about Bitcoin neutrality for weeks. He says almost every yes vote comes from one mining pool. Blockstream chief executive Adam Back has flagged chain split risk, calling the 55% bar too low to be safe.

A second phase was due at block 961,632, about six days away. It would reject any block that did not vote yes.

Nodes still running BIP-110 would enforce that on their own. That is why the warning to switch back matters.

No one owns Bitcoin’s rules. Nobody can flip a switch to start or stop a soft fork. This was a request, not a command.

Whether operators listen will say more about BIP-110’s support than any vote counter has.

The post BIP-110 Activation Frozen After Coldcard Exploit: Is the Soft Fork Dead? appeared first on BeInCrypto.

Senators Ruben Gallego and Thom Tillis sent a proposed revised ethics provision to the White House on Thursday, after drafting the compromise the day before, an industry source familiar with the talks told CoinDesk. As of midafternoon on Friday, the White House had not officially responded to the proposal.

Ethics remains the biggest outstanding issue to be resolved before the Clarity Act can advance. There are ongoing negotiations around other issues, including stablecoin reserves and yield, law enforcement authorities and some of the Agriculture Committee provisions addressing the Commodity Futures Trading Commission’s total remit, but these are relatively uncomplicated compared to ethics, two industry sources said. One added that they expected those other issues to be resolved relatively quickly should negotiators come to a deal on ethics.

If the White House signs off on the counter-proposal from Tillis and Gallego, that could speed the way to at least the first part of the cloture process, the other source told CoinDesk. The Senate would still need to follow the cloture process laid out in last week’s edition of this newsletter, but the timelines involved mean that it would be difficult to get the bill all the way through by the end of the week. Still, getting through that first procedural vote would be a visible win for the crypto industry, should it happen.

Strategy Inc. kept the annual dividend rate on its STRC preferred stock at 12% for August 2026, even though the Nasdaq-listed security ended July more than 10% below its $100 stated amount.

Summary

- 12% annualized dividend remains unchanged for August despite STRC closing July at $89.46 per share.

- $3.75 billion reserve covers roughly 2.1 years of preferred dividends and debt interest payments currently.

- Strategy repurchased 288,930 STRC shares below par while retaining $975 million in remaining authorization capacity.

The company’s official STRC information page confirms that the variable annualized rate for record dates beginning in August remains 12%. Executive Chairman Michael Saylor promoted the product on Aug. 1 as a way to “stretch your income,” emphasizing its twice-monthly payment schedule.

STRC closed at $89.46 on July 31, down $0.25 during the session. At that price, the $12 annualized payout based on the security’s $100 stated amount produces an effective yield of about 13.41%. Because Saylor announced the unchanged rate during the weekend, no post-announcement market reaction will be available until Nasdaq trading resumes.

Strategy’s STRC dividend no longer rises automatically

Strategy raised STRC’s annual dividend from 11.5% to 12% for record dates beginning in July. The increase followed a sharp June decline that took the shares as low as $71.25 and moved them far below the $100 level the company wants to maintain.

However, the company changed its rate-setting policy on June 29. Under the revised framework, management considers STRC’s market price, credit spreads, competing yields, Bitcoin volatility, cash-reserve coverage and the wider capital structure. The filing specifically states that Strategy will not necessarily raise the dividend solely because STRC trades below its stated amount.

That policy explains why July’s discount did not produce another 50-basis-point increase. Strategy instead said during its second-quarter results that it would maintain the 12% rate until STRC shows “sustained, healthy trading” near $100. The language describes management’s objective and does not guarantee that the shares will return to par.

The decision also prevents Strategy’s cash obligations from rising further while the company attempts to repair demand through other measures. Every additional 50 basis points would increase the annual cash cost across more than $10.46 billion in outstanding STRC stated value.

Buybacks now carry more of the price-support burden

Strategy has shifted part of its response from dividend increases to preferred-share repurchases. Between July 20 and July 26, the company bought back 288,930 STRC shares for approximately $25 million, paying an average of $86.53 per share. The purchase represented a 13.47% discount to the shares’ stated amount.

About $975 million remains under Strategy’s $1 billion preferred-securities repurchase authorization. Management said it intends to purchase more STRC at deeper discounts and reduce its activity as the security approaches $100. The authorization does not require Strategy to spend the remaining amount and has no fixed expiry date.

Repurchasing shares below par reduces the number of preferred shares requiring future cash distributions. It also lets Strategy retire $100 of stated value for less than $100. However, buybacks use capital that could otherwise remain available for dividends, debt interest or Bitcoin purchases.

As previously reported, Strategy funded its first $25 million STRC repurchase while increasing its U.S. dollar reserve and keeping Bitcoin purchases paused. The company raised much of that liquidity through sales of MSTR common stock rather than new STRC issuance.

The $3.75 billion reserve supports the 12% payout

Strategy reported a $3.75 billion U.S. dollar reserve as of July 26. The company said that amount covers approximately 2.1 years of expected preferred-stock dividends and interest on outstanding debt. The reserve can only be used for those obligations unless the board approves another purpose.

The cash cushion has become more important because Strategy’s preferred-stock commitments have expanded. The company recorded $400.7 million in preferred dividends during the second quarter, compared with $49.1 million one year earlier. It has paid or declared more than $1 billion in cumulative preferred distributions.

Strategy also reported an $8.22 billion second-quarter net loss, driven mainly by an $8.32 billion unrealized loss on its Bitcoin holdings. The accounting loss did not represent an equivalent cash outflow, but the preferred dividends must be paid in U.S. dollars.

The company has therefore authorized Bitcoin sales to refill the reserve, cover dividends and interest, or finance approved security repurchases. Strategy had sold approximately $218.4 million of Bitcoin during 2026 through July 26 to fund part of its preferred obligations.

As crypto.news reported, Strategy held 843,775 BTC at an average acquisition cost of about $75,476 as of July 26. The company valued that position at $54.77 billion using Bitcoin’s July 27 market price, compared with its $63.69 billion original cost.

STRC holders receive two payments each month

STRC moved from monthly to semi-monthly distributions after shareholders approved the change in June. Record dates now fall on the 15th and final day of each month, with payments generally following around 15 days later.

Strategy has already declared a payment of $0.50 per share for Aug. 15 to investors recorded as shareholders on July 31. The company’s website lists the 12% rate for August record dates, but future cash distributions still require board or committee approval and are not guaranteed.

For U.S. federal tax purposes, Strategy expects the current payments to be treated as returns of capital to the extent of an investor’s tax basis. That is the company’s expectation rather than a guarantee of each shareholder’s treatment, and Strategy advises investors to seek tax guidance based on their own circumstances.

STRC is also unsecured. Strategy states that its preferred securities are not collateralized by its Bitcoin holdings and only hold a preferred claim on the company’s residual assets. The company further warns that STRC is not a bank deposit, is not FDIC-insured and does not carry the same protections as Treasury securities or money-market funds.

What happens next for STRC and Strategy

Chief Executive Phong Le said management’s objective is for STRC to trade between $99 and $100 “over time.” Strategy has not provided a deadline for reaching that range, and the shares’ $89.46 closing price shows that the market continues to demand a yield above the stated 12% rate.

The next confirmed event is the Aug. 15 distribution. Investors will then watch Strategy’s next monthly rate decision, further STRC repurchases and weekly SEC disclosures covering common-stock sales, Bitcoin transactions and changes to the dollar reserve.

Saylor separately posted “Bitcoin Drive engaged” on Aug. 2 alongside the company’s treasury chart. The message may fuel expectations of a new purchase disclosure, but the post does not confirm that Strategy bought Bitcoin or reversed its recent pause. An SEC filing or company announcement would be needed to verify any transaction.

As of then, Strategy is relying on its existing 12% rate, twice-monthly payments, cash reserves and discounted repurchases rather than offering STRC investors another dividend increase.

The spot exchange-traded funds tracking Ripple’s cross-border token continue with their impressive performance in times of market uncertainty, and saw only one day of no reportable action in the past week, unlike the previous ones.

July also ended in the green for the funds, meaning that only one out of the nine months they have been active was in the red.

The Good Weekly and Monthly

Data from SoSoValue shows that Monday and Wednesday were quite modest in terms of net inflows. On both days, the ETFs attracted just under $600,000. However, the green streak continued and accelerated at the end of the business week, with $6 million in net inflows on Thursday and another $7.7 million on Friday.

Thus, the week ended with $14.86 million in the green, making it the best since the one that ended on July 2, when the funds attracted $17.19 million. On a monthly scale, investors poured in $27.29 million into the spot XRP ETFs.

What’s even better is that the funds have reached another all-time high in terms of cumulative total net inflows, at over $1.5 billion as of Friday’s close. Bitwise’s XRP has extended its lead over Canary Capital’s XRPC, with $511 million in net inflows compared to $467 million for the latter.

The Bad

Although July indeed ended in the green, the actual net inflows were not all that impressive. The $27.29 million places July as just the second-worst month, beating only January when investors inserted $15.59 million into the funds.

In contrast, June was a lot more positive, with the net inflows standing close to $60 million. May was even better, with almost $132 million. The all-time high from November at $666.61 million remains untouchable.

The Ugly

Although this improved at the end of the month, July saw the most days with no reportable action in terms of net flows. Precisely half of the trading days (11 out of the 22) saw no flows, according to SoSoValue, which, aligned with the more modest $27.29 million in net inflows, suggests dwindling interest in the funds.

Separately, the underlying asset’s price performance continues to disappoint despite the numerous positive developments in the broader Ripple ecosystem. Although it managed to defend the $1.05 support during the weekend, XRP is still below $1.10, and it’s down by more than 3% on a monthly scale. What’s even more worrisome is the fact that August has been a particularly painful month for the asset historically.

The post Ripple (XRP) ETF Monthly Recap: The Good, The Bad, and the Ugly appeared first on CryptoPotato.

Stop Acting Like the CLARITY Act Is Everything, Former Regulator Says

India secure top-four finish at 2026 Commonwealth Games after historic 39-medal campaign | Commonwealth Games News

The James Webb Telescope Is Changing Astronomers’ Understanding of the Ancient Cosmos

-

Business4 days ago

Business4 days agoWhy Trees Belong on the Risk Register

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Wit & Wisdom

-

Tech7 days ago

Tech7 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Politics2 days ago

Politics2 days agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Politics6 days ago

Politics6 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World1 day ago

Crypto World1 day agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics5 days ago

Politics5 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Entertainment5 days ago

Entertainment5 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

News Videos7 days ago

News Videos7 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Business5 days ago

Business5 days agoMajor shareholder moves on Canyon

-

News Videos3 days ago

News Videos3 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger v3.3.0 brings five institutional features

-

Crypto World5 days ago

Crypto World5 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech6 days ago

Tech6 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos5 days ago

News Videos5 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics3 days ago

Politics3 days agoLuke Littler’s dominance sparks GOAT debate

-

Business5 days ago

Business5 days agoJohnson & Johnson agrees to $5.5B settlement over talc cancer claims

-

Sports3 days ago

Sports3 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Crypto World11 hours ago

Crypto World11 hours agoCrypto PAC spending tops $2M in Michigan House race

-

Business2 days ago

Business2 days agoTrump Announces Hamas Disarmament Agreement as Iran Strikes Kuwait Air Base and US Attacks Pause Overnight

You must be logged in to post a comment Login