Crypto World

Inside the Strategic Bitcoin Reserve: promise vs reality

President Trump signed the executive order establishing the Strategic Bitcoin Reserve on March 6, 2025.

Summary

- Trump’s Strategic Bitcoin Reserve exists as a no-sell directive, not an active acquisition program yet.

- The U.S. government reportedly holds about 328,372 BTC, but custody and legal questions remain unresolved.

- Lummis’s BITCOIN Act targets 1 million BTC, while ARMA offers a more conservative legislative path.

- The next announcement may formalize custody and legal frameworks, not authorize direct Bitcoin purchases.

Fourteen months later, in May 2026, White House digital asset advisor Patrick Witt told the audience at Consensus Miami that a “major announcement” on the reserve is coming “in the next few weeks.” Witt characterized the underlying legal and custody work as a “breakthrough” and disclosed for the first time the government holds approximately 328,372 BTC worth roughly $25.4 billion.

Meanwhile, the gap between what has been promised and what has been operationally delivered is the structural story of the SBR. Trump’s order halted sales of seized Bitcoin and mandated centralized custody. The administration has conducted an audit revealing cold wallets stored in desk drawers across federal agencies and a $60+ million exploit of US Marshals Service holdings in late 2025.

Treasury Secretary Scott Bessent confirmed in August 2025 the US “won’t be buying” additional Bitcoin, contradicting the “Bitcoin superpower” rhetoric of former White House crypto advisor Bo Hines, who stepped down that same month amid SBR scrutiny. Senator Cynthia Lummis’s BITCOIN Act would mandate purchases of 1 million BTC over five years funded by gold revaluation. The bipartisan ARMA bill introduced May 2026 (Begich-R/Golden-D) dropped the specific 1M target and added a 20-year lockup.

Senate Banking Committee markup of competing bills is expected by May 31. The honest read is the SBR exists as legal directive but does not yet exist as operational acquisition program. The next several weeks will determine whether it becomes the latter or stays primarily the former. This is what the documented record shows, what the structural questions are, and what the imminent announcement might actually contain.

What the executive order actually established

The executive order signed on March 6, 2025 deserves careful unpacking because the gap between what it formally established and what most coverage characterized it as creating is structurally significant.

The order created two separate entities. The Strategic Bitcoin Reserve (SBR) is the entity holding Bitcoin specifically. The US Digital Asset Stockpile is a separate entity holding non-Bitcoin cryptocurrencies (Ethereum, XRP, Solana, Cardano, and other forfeited digital assets). The two entities have different operational mandates: the SBR cannot sell its Bitcoin holdings under the order’s terms, while the Digital Asset Stockpile lets the Treasury Department liquidate non-Bitcoin assets at its discretion.

The funding mechanism is the most consequential structural element. The reserve is “capitalized with all BTC held by the Department of the Treasury that was finally forfeited as part of criminal or civil asset forfeiture proceedings or in satisfaction of any civil money penalty imposed by any executive department or agency.” In plain English: the reserve consists of Bitcoin the government already had from law enforcement seizures. The executive order did not authorize and did not fund any active acquisition of additional Bitcoin.

The order does direct the Secretaries of Treasury and Commerce to “develop strategies for acquiring additional Government BTC, provided that such strategies are budget-neutral and do not impose incremental costs on United States taxpayers.” This is permissive language inviting policy development, not mandatory language requiring action. The Treasury and Commerce departments were tasked with studying whether budget-neutral acquisition mechanisms exist, not with implementing them.

The audit mandate is what produced the first concrete operational deliverable. The order required each federal agency to “provide the Secretary of the Treasury and the President’s Working Group on Digital Asset Markets with a full accounting of all Bitcoin and other digital assets in the agency’s possession” within 30 days. The audit deadline was April 5, 2025. The audit was completed but the detailed findings were not made public until the White House report released on July 30, 2025.

The structural questions the executive order left unresolved are the ones now being addressed through the May 2026 Witt announcement and the pending congressional legislation. Which specific legal authorities permit federal agencies to hold Bitcoin long-term rather than liquidating it through standard forfeiture procedures? Can Congress reclaim the assets through appropriations or other legislative action? What custody framework will protect the holdings from operational risks? How is “budget-neutral acquisition” actually defined and implemented?

These questions are not trivial. The executive order can set a policy direction, but it cannot by itself create the legal and operational infrastructure required to make a strategic Bitcoin reserve function comparably to other strategic reserves like the Strategic Petroleum Reserve or the gold holdings at Fort Knox. The infrastructure work is what Witt was referring to when he characterized the May 2026 announcement as a “breakthrough.”

What the executive order did establish, clearly and definitively, is the federal government’s policy of not selling its Bitcoin holdings. The Treasury Secretary’s August 2025 confirmation that the US “won’t be buying” additional Bitcoin reinforced the operational reality: the SBR is a directive to hold, not a directive to accumulate. The “digital Fort Knox” rhetoric from White House crypto czar David Sacks describes the aspirational endpoint. The current operational state is more accurately characterized as “do not sell what we already have.”

What the audit actually revealed

The audit conducted between March and July 2025 produced findings more revealing than the formal report acknowledged, and the documented operational realities deserve attention because they shape what the imminent SBR announcement can realistically deliver.

The headline number is the government holds approximately 328,372 BTC worth roughly $25.4 billion as of February 2026, according to Witt’s Consensus Miami disclosure on May 6, 2026. This is the first time the White House has confirmed a specific holdings figure since the executive order was signed. Previous third-party estimates from Arkham Intelligence and Bitcoin Treasuries had ranged from 198,012 to 328,000 BTC, with the variance reflecting confusion between officially forfeited assets and merely seized assets that might be returned to victims.

The composition of the holdings comes primarily from three major law enforcement actions. The Silk Road marketplace takedown produced the original anchor of government Bitcoin holdings starting in 2013. The Bitfinex hack recovery in 2022 added 94,636 BTC seized by the DOJ. Various smaller criminal forfeitures over the past decade contributed the remaining holdings. The composition has implications for the legal status of individual coins: some are fully forfeited (legally owned by the US government) while others are technically seized but still subject to potential restitution to crime victims.

The operational state of the holdings was more chaotic than the public might have expected. Witt acknowledged at Consensus the audit process revealed agency-level custody practices were “messy” in his characterization. “We’ve heard stories and confirmed some of them of cold wallets that were being stored in drawers of desks in various agencies,” Witt said publicly. This is not a routine custody finding. It indicates for years, federal agencies were holding crypto assets worth potentially billions of dollars without the kind of institutional custody framework required for any other government-held strategic asset.

The January 2026 US Marshals Service incident reinforced the custody concerns. Bloomberg reported the Marshals Service was investigating a possible hack of government digital-asset accounts following allegations from on-chain investigator ZachXBT that a hacker had stolen more than $60 million from government seizure wallets in late 2025. The incident is part of the public record now and is one of the specific operational events Witt cited as motivation for centralized custody architecture.

David Sacks revealed in early 2025 the government had previously held approximately 400,000 BTC through cumulative civil and criminal asset forfeitures over the past decade. The current holdings (approximately 328,372 BTC) reflect both ongoing seizures and the substantial liquidations conducted under the prior administration. Sacks characterized the prior administration’s auctions as “fire sale” liquidations wasting significant taxpayer value. At current prices, the difference between holding all 400,000 BTC and the current 328,372 BTC represents approximately $5.5 billion in foregone value if the auctioned coins had been retained. The political framing of “fire sale” liquidations has been a recurring theme in administration rhetoric about why the no-sell policy is fiscally important.

The audit findings establish two structural realities. First, the government’s actual Bitcoin holdings are substantial (over $25 billion at current prices) but smaller than they would have been absent prior auctions. Second, the operational infrastructure required to hold these assets safely has been inadequate, and the centralization and custody work the Witt team has been conducting addresses real operational gaps rather than just political theater. The combination matters for evaluating what the imminent announcement can credibly deliver.

The Bo Hines pivot and what it revealed

The transition from Bo Hines to Patrick Witt as the operational lead on the SBR happened in August 2025 and tells a structural story about how the SBR rhetoric evolved into operational reality. The story deserves attention because it clarifies what the administration’s actual capabilities and intentions are.

Bo Hines was the executive director of the President’s Council of Advisors for Digital Assets through the first half of 2025. He was a central voice in the early SBR rhetoric, characterizing the United States as needing to become “the Bitcoin superpower of the world” and describing a “space race” for Bitcoin accumulation. In April 2025 remarks, Hines outlined acquisition methods focused on rapid scaling and budget-neutral mechanisms, framing the SBR as an active acquisition program rather than just a holding directive.

The Hines rhetoric clashed with the executive order’s actual provisions. The order did not authorize Bitcoin purchases. It directed Treasury and Commerce to study budget-neutral mechanisms. The gap between Hines’s “Bitcoin superpower” framing and the executive order’s “explore strategies” language created public expectations the administration could not deliver on without congressional action.

Treasury Secretary Scott Bessent’s August 14, 2025 Fox Business interview was the moment the gap became unsustainable. When asked about the Bitcoin reserve, Bessent said directly: “We’re not going to be buying that [bitcoin] but are going to use confiscated assets and continue to build that up, we’re going to stop selling that.” He estimated the reserve was “somewhere between $15 and $20 billion” at the time. This was a direct contradiction of the Hines framing. The Treasury Secretary, the senior administration official responsible for the actual financial operations, was clarifying the US would not be actively buying Bitcoin.

Bo Hines stepped down from his White House role within days of the Bessent comments, in August 2025. The stated reason was the standard “pursue other opportunities” framing used in such departures. The actual context was the SBR scrutiny intensifying around the gap between the rhetoric and the operational reality. Hines subsequently joined Tether’s US operations and eventually became CEO of USAT (the Anchorage Digital-issued GENIUS-compliant stablecoin from Tether) when it launched in January 2026.

Patrick Witt took over as executive director of the President’s Council of Advisors for Digital Assets following Hines’s departure. The transition shifted the SBR’s operational character significantly. Witt’s public framing has been substantially more measured than Hines’s. Where Hines stressed acquisition and scale, Witt stresses “getting our house in order” through custody centralization, legal framework development, and operational infrastructure. The shift reflects a more accurate accounting of what the executive order actually enabled and what congressional action would be required to expand.

Witt’s deputy Harry John conducted the legal framework development producing the May 2026 “breakthrough.” The framework addresses specific legal questions the executive order did not resolve: which authorities permit federal agencies to hold Bitcoin long-term, for how long, and whether Congress could reclaim the assets through legislative action. The legal work is the kind of detailed administrative state work not producing headlines but determining whether the SBR can function as a credible strategic reserve over time.

The structural lesson from the Hines-Witt transition is the SBR moved from rhetoric to operational reality through personnel change. The “Bitcoin superpower” framing required legislative action not forthcoming. The more measured “centralize custody, develop legal framework, prepare for future congressional action” framing reflects what the executive branch can actually deliver. The May 2026 “breakthrough” announcement will likely formalize this more measured framing rather than restore the maximalist accumulation rhetoric.

For market observers, the structural implication is the SBR’s near-term impact is likely smaller than the early Hines rhetoric suggested but more durable than the maximalist framing would have produced. A formal centralized custody architecture for 328,372 BTC, combined with a legally robust no-sell policy and a clear pathway for future congressional acquisition authorization, is a real structural shift in the US government’s relationship with Bitcoin. It just runs on a slower timeline than the Bitcoin maximalist community had hoped.

The legislative pathway: BITCOIN Act and ARMA

The executive order can establish policy direction but cannot create permanent legal infrastructure or fund active acquisition. Both functions require congressional action. The two competing bills currently in play deserve careful examination because they will determine whether the SBR becomes an active acquisition program or stays primarily a passive holding directive.

Senator Cynthia Lummis (R-WY) reintroduced the BITCOIN Act (S.954) in March 2025, formalizing legislation she had introduced in the prior Congress. The bill’s full title is the Boosting Innovation, Technology, and Competitiveness through Optimized Investment Nationwide Act. The core provisions are substantive. The Treasury would be required to buy one million Bitcoin over a five-year period and hold the assets in trust for the United States. At March 2025 prices, the one million BTC target represented approximately $80 billion in acquisition cost. At current prices, the cost would be roughly $80 billion (Bitcoin price has fluctuated but the order of magnitude is similar).

The funding mechanism in the BITCOIN Act is the structural innovation. The bill proposes funding the purchases through the net earnings of the Federal Reserve, which historically transfers surplus revenues to the Treasury, and through Treasury issuance of new gold certificates reflecting current market prices for the Federal Reserve’s gold holdings. The gold revaluation mechanism is technically interesting. The Federal Reserve’s gold holdings are currently valued on Treasury books at the statutory rate of $42.22 per ounce, which dramatically understates current market value (approximately $3,000+ per ounce). Revaluing the gold holdings would produce a paper accounting gain the Treasury could theoretically use to fund Bitcoin purchases without new appropriations.

The 20-year holding period is the second structural provision. All Bitcoin acquired by the United States and placed into the Strategic Bitcoin Reserve must be held for at least 20 years under the bill’s terms. After the holding period expires and upon Treasury recommendation, up to 10 percent of the holdings could be sold to reduce the national debt in any two-year period. The 20-year lockup turns the SBR from a flexible reserve asset into a long-term strategic position similar to the gold reserves.

The American Reserve Modernization Act of 2026 (ARMA) was introduced in May 2026 by Representative Nick Begich (R-AK) and Representative Jared Golden (D-ME) as a bipartisan alternative to the Lummis bill. ARMA is structurally similar to the BITCOIN Act in core mandates (Strategic Bitcoin Reserve, Digital Asset Stockpile, 20-year lockup, budget-neutral acquisition) but has important differences in scope and approach.

The most significant ARMA difference is the bill dropped the specific 1 million BTC target. Rather than mandating purchase volumes, ARMA directs Treasury and Commerce to “study whether additional acquisitions could be carried out through budget-neutral mechanisms” without specifying outcomes. This is a substantially more conservative legislative posture that may make the bill more politically viable but provides less certainty about actual acquisition levels.

ARMA also strengthens custody standards explicitly. The bill includes specific provisions about secure storage requirements, custody protocols, and operational safeguards meant to prevent incidents like the US Marshals Service exploit. The custody focus reflects the operational reality the Witt audit revealed and aligns the legislative work with the operational concerns the administration has been addressing.

The Senate Banking Committee markup of the BITCOIN Act is expected by May 31, 2026, per Witt’s Consensus statements and other administration signals. The markup is the first substantive legislative step. If the bill passes committee with reasonable bipartisan support, the path to floor consideration becomes plausible. If the bill stalls in committee, the legislative pathway becomes more difficult and the executive branch’s incremental approach (centralized custody, no-sell directive, audited holdings) becomes the de facto SBR for the foreseeable future.

The political dynamics around the legislation are complicated. The BITCOIN Act has primarily Republican backing despite the strong fiscal conservative argument for the bill (acquisition through gold revaluation rather than new debt issuance, long-term store of value, no taxpayer impact). Democrats have generally been skeptical of the executive order and the broader crypto-friendly policy direction, though the ARMA bill’s bipartisan structure (Golden as Democratic co-sponsor) suggests some Democratic support is achievable for a more modest version of the SBR concept.

For market observers, the key question is whether legislative action produces the active acquisition program the Bitcoin maximalist community has hoped for, or whether the legislative window closes with the SBR remaining primarily a passive holding directive. The May 31 markup and the subsequent legislative trajectory will likely answer this question over the next few months.

What the “breakthrough” announcement might actually contain

Witt’s May 2026 “breakthrough” characterization at Consensus Miami signals an imminent announcement, but the specific content the announcement will contain has not been publicly confirmed. Based on the documented public statements and the structural work the administration has been conducting, several likely components can be inferred.

The most likely component is formalization of centralized custody architecture for the 328,372 BTC currently held across various federal agencies. The audit revealed cold wallets in desk drawers and the Marshals Service exploit showed the operational risks of decentralized custody. A formal architecture would consolidate the holdings into purpose-built institutional custody (likely involving regulated custodians like BitGo, Anchorage, or Coinbase Custody) with multi-signature controls, geographic distribution of custody locations, and standardized operational procedures.

The legal framework Harry John’s team developed is the second likely component. The framework addresses the executive branch’s authority to hold the Bitcoin long-term without congressional appropriations, the legal status of seized versus forfeited assets, the procedural requirements for transferring assets between agencies, and the protections against legislative claw-back of the holdings. The framework’s specific provisions will be technically detailed but politically significant, as they determine what the executive branch can do without congressional action.

The no-sell policy formalization is the third likely component. The executive order set the policy direction, but the operational implementation requires specific regulatory and procedural changes at the agency level. The announcement may include formal regulations or memoranda specifying how individual agencies must handle Bitcoin holdings, the requirements for transferring assets to centralized SBR custody, and the prohibitions on auction or sale without specific Treasury authorization.

The integration with congressional legislation is the fourth likely component. The announcement will probably express administration support for either the BITCOIN Act or the ARMA bill (or both, with the ARMA bill positioned as a fallback if the more ambitious BITCOIN Act stalls). The timing of the announcement around the May 31 Senate Banking Committee markup is probably not coincidental. The administration may be coordinating with congressional sponsors to maximize legislative momentum.

What the announcement is unlikely to contain is authorization for active Bitcoin purchases. The executive branch does not have the legal authority to use appropriated funds for Bitcoin acquisition without congressional action. Treasury Secretary Bessent’s August 2025 confirmation the US “won’t be buying” is still the operational reality until Congress acts. The announcement will likely stress what the executive branch has done (custody centralization, legal framework, no-sell directive) and what congressional action could enable in the future.

The market response to the announcement will likely depend on whether it contains specific operational milestones or just process commitments. Specific operational milestones (custody contracts signed, holdings transferred, audit results published) would be substantively meaningful. Process commitments (committee markups expected, frameworks under development, announcements coming) would be incremental. The “breakthrough” characterization suggests the former, but the actual content remains to be seen.

For Bitcoin price specifically, the structural impact of the formalized no-sell policy is positive but limited. Removing seized-coin auctions as a recurring supply event (the prior administration sold approximately 70,000 BTC across multiple auctions) eliminates one form of structural selling pressure. But the no-sell policy was already operational in practice since the executive order, so formalizing it has limited additional impact. The more significant price catalyst would be congressional authorization of active acquisition, which the announcement will not contain.

For the broader policy trajectory, the announcement’s most significant content may be establishing a clear path from the current passive holding state to a potential future active acquisition program. If the announcement positions the executive branch as having completed its custody and legal foundation work, it puts the responsibility for the next stage squarely on Congress. The political dynamics of the Senate Banking Committee markup and subsequent legislative work become the determinative variables.

The structural questions still unresolved

Several substantive questions about the SBR remain unresolved regardless of what the imminent announcement contains, and the questions deserve attention because they shape the long-term viability of the reserve concept.

The first unresolved question is what “budget-neutral acquisition” actually means in practice. The executive order, the BITCOIN Act, and ARMA all invoke budget-neutral mechanisms, but the specific operational definition varies. Gold revaluation (the BITCOIN Act mechanism) is technically budget-neutral in accounting terms but creates real economic effects. Federal Reserve net earnings (also in the BITCOIN Act) would redirect funds otherwise flowing to general Treasury revenue. Other proposed mechanisms (tariff revenue allocation, asset sales of other federal holdings) have different implications. The definitional question matters because different definitions enable different acquisition scales.

The second unresolved question is whether sovereign Bitcoin holdings create market manipulation concerns. If the United States accumulates 1 million BTC (the BITCOIN Act target), it would hold approximately 5 percent of the total Bitcoin supply. The concentrated holdings could create market manipulation incentives where US policy decisions about Bitcoin (custody, accounting treatment, regulatory framework) affect the asset’s price in ways benefiting US holdings. This is the same concern applying to government gold holdings and other strategic reserves, but the relatively smaller size of the Bitcoin market makes the concentration effects more pronounced.

The third unresolved question is how other sovereign nations will respond to US accumulation. If the United States becomes the largest sovereign Bitcoin holder, other major economies will likely consider similar reserves. El Salvador has held Bitcoin reserves since 2021. The UAE through Abu Dhabi has been accumulating crypto exposure through various channels. China has historically been opposed to crypto but has shown signs of softening on Bitcoin specifically through Hong Kong-based vehicles. The “Bitcoin space race” Hines invoked may actually be a real geopolitical dynamic if US accumulation prompts competitive sovereign accumulation by other major economies.

The fourth unresolved question is the relationship between the SBR and the broader US dollar position. Treasury Secretary Bessent has framed Bitcoin as complementary to gold as a strategic asset rather than as competition for the dollar. Larry Fink and other major financial figures have argued tokenization broadly strengthens dollar dominance rather than weakening it. But Bitcoin accumulation does represent a partial diversification away from pure dollar-denominated reserve assets. The structural implications for dollar hegemony are debated and depend on accumulation scale, parallel actions by other reserve holders, and the broader evolution of the international monetary system.

The fifth unresolved question is the political durability of the SBR across administrations. The executive order can be reversed by a future administration. The no-sell policy could be reversed. The custody arrangements could be unwound. Codification through congressional legislation (the BITCOIN Act or ARMA) would provide more political durability, but even legislation can be amended or repealed. The structural question is whether the SBR can develop the kind of bipartisan support making it durable across political transitions, or whether it stays a partisan policy future administrations could dismantle.

These questions do not have clean answers in 2026. The next several years of operational implementation, legislative action, and broader policy evolution will determine how the questions get resolved. The Witt announcement will address some of them (custody, legal framework) but cannot resolve others (international response, political durability, dollar implications). The questions are worth keeping in mind as the SBR story develops, regardless of how the imminent announcement is received.

What the SBR means for Bitcoin specifically

The market implications of the SBR for Bitcoin price, adoption, and structural positioning deserve direct engagement because they shape how investors and observers should interpret the imminent announcement and the broader policy trajectory.

The supply impact is the most concrete dimension. The no-sell policy removes approximately 328,372 BTC from potential auction supply, representing approximately 1.6 percent of total Bitcoin supply (which is approximately 19.9 million coins as of May 2026). The supply removal is not new to the market (the executive order has been in effect for 14 months and prior administration auctions were already disclosed in advance), but the formal policy codification removes the residual uncertainty about whether seized coins might be auctioned in the future.

If the BITCOIN Act passes and the 1 million BTC acquisition target is implemented over five years, the cumulative supply impact would be much larger. The 1 million BTC target represents approximately 5 percent of total supply. Acquiring this amount over five years would require approximately 200,000 BTC per year of accumulation, which represents substantial structural demand. For comparison, Bitcoin spot ETFs accumulated approximately 1.1 million BTC across their first 18 months of trading, so US government acquisition at the BITCOIN Act target would be roughly equivalent in scale to the ETF accumulation having driven much of Bitcoin’s institutional adoption.

The demand catalyst would be significant but not transformative for Bitcoin price. At current trading volumes of approximately $50-80 billion per day in spot Bitcoin markets, government acquisition of 200,000 BTC per year (averaging perhaps $40-50 billion in annual value) would represent meaningful but not overwhelming demand. The price impact depends substantially on how the acquisition is structured (announced auctions versus quiet accumulation, OTC versus exchange-based purchases) and how other market participants respond to the government activity.

The structural signaling effect may matter more than the direct supply or demand impact. US government accumulation of Bitcoin as a strategic reserve signals to other sovereign actors, institutional investors, and the broader market that Bitcoin has achieved a level of legitimacy comparable to other strategic assets. The signaling effect could catalyze additional institutional adoption beyond what the direct US government purchases would produce.

The regulatory and policy implications extend beyond just the SBR. The administration’s broader crypto-friendly direction (the GENIUS Act, the Bitcoin reserve, the CLARITY Act work, the SEC enforcement shift under Chair Atkins) creates a policy environment supporting Bitcoin adoption across multiple channels simultaneously. The SBR is one component of this broader policy framework, not a standalone driver.

The risks to Bitcoin from SBR developments deserve equal attention. If the BITCOIN Act stalls in Congress and the legislative pathway closes, the SBR stays primarily a passive holding directive without the active acquisition dynamics. If a future administration reverses the executive order, the no-sell policy and centralized custody could be unwound. If the budget-neutral acquisition mechanisms (gold revaluation, Federal Reserve net earnings) face legal or political challenges, the funding pathway for active acquisition becomes uncertain.

The honest read is the SBR provides Bitcoin with structural support not existing before the March 2025 executive order, but the scale of the support is more modest than the maximalist rhetoric suggested. The imminent Witt announcement will likely formalize the existing support without dramatically expanding it. Significant additional support depends on congressional action having not yet happened and may or may not happen in the current legislative window.

For Bitcoin investors specifically, the practical implication is the SBR is a positive structural development should be factored into long-term thesis but should not be treated as a near-term price catalyst with specific magnitude. The structural story develops over years through operational implementation and legislative action rather than through any single announcement.

The bottom line

The Strategic Bitcoin Reserve as it actually exists in May 2026 is a legal directive setting a government policy of not selling approximately 328,372 BTC currently held across various federal agencies, with a centralized custody framework under active development and a legal framework recently completed addressing the questions left unresolved by the original executive order.

The Strategic Bitcoin Reserve as it has been rhetorically characterized (the “digital Fort Knox,” the “Bitcoin superpower” framing, the active accumulation program targeting 1 million BTC) is an aspirational endpoint requiring congressional action not yet happened.

The gap between these two characterizations is the structural story of the SBR over the past 14 months. The Bo Hines maximalist framing collided with the executive order’s actual provisions and the Treasury Secretary’s operational reality. The Patrick Witt measured framing reflects what the executive branch can actually deliver. The imminent announcement will formalize what Witt and his team have built rather than restore the more ambitious Hines vision.

The documented facts are clear. Executive order signed March 6, 2025. Audit completed by April 2025, findings detailed in the July 30, 2025 White House report. Approximately 328,372 BTC currently held worth roughly $25.4 billion. Cold wallets stored in desk drawers across federal agencies. A $60+ million exploit of US Marshals Service holdings in late 2025. Treasury Secretary Bessent’s August 2025 confirmation of no purchases. Bo Hines departure in August 2025. Patrick Witt’s Consensus Miami breakthrough announcement May 6, 2026. Senate Banking Committee markup of the BITCOIN Act expected by May 31, 2026. The bipartisan ARMA bill introduced May 2026 as alternative to the Lummis BITCOIN Act.

The structural questions stay open. Will Congress codify the SBR through legislation? Will budget-neutral acquisition mechanisms (gold revaluation, Federal Reserve net earnings) be authorized? Will future administrations keep or reverse the policy? How will other sovereign actors respond? What does sovereign Bitcoin accumulation mean for the broader dollar position?

For Bitcoin holders, the practical implication is the SBR provides modest structural support that should be factored into long-term thesis without being treated as a near-term price catalyst. The supply removal (328,372 BTC effectively off the market under the no-sell policy) is real but not transformative. The potential demand catalyst (1 million BTC acquisition if BITCOIN Act passes) would be significant but depends on legislative outcomes not yet materialized.

For policy observers, the SBR is one of the clearest examples of how crypto policy actually evolves under administrative implementation versus political rhetoric. The executive order set direction. The audit revealed operational realities. The personnel transitions reflected mismatch between rhetoric and capability. The measured operational approach Witt and his team have taken is producing real but incremental progress. The legislative work runs in parallel with uncertain outcomes.

For market observers, the imminent Witt announcement is unlikely to produce dramatic price movement in either direction. It will probably formalize the centralized custody architecture, the legal framework, and the no-sell directive. It will probably express administration support for congressional legislation. It will probably stress the operational progress over the past 14 months. It will probably not contain authorization for active acquisition because that requires congressional action.

The honest assessment is the SBR is real but smaller than promised, operational but incomplete, structurally important but not yet transformative. The next several months will determine whether congressional action expands it into the active accumulation program the maximalist rhetoric described, or whether it stays primarily a passive holding directive with formal custody and legal infrastructure.

For now, what is established is the United States government holds approximately 328,372 BTC worth roughly $25.4 billion under a no-sell policy with developing centralized custody and a recently completed legal framework. The reserve exists. The promise of active accumulation has not yet been delivered. The reality of operational implementation keeps unfolding.

The Witt announcement will provide the next data point. The Senate Banking Committee markup will provide the next legislative signal. The eventual outcome will be determined over the coming months and years through specific operational milestones and political developments rather than through any single defining event.

The Strategic Bitcoin Reserve is real. It is also incomplete. Both can be true simultaneously, and the honest reading of the documented record requires holding both characterizations at once.

What happens next is being decided now, in legal memos prepared by Harry John’s team, in Senate Banking Committee hearings yet to take place, in operational decisions about custody contracts not yet signed, and in the broader political dynamics determining whether US Bitcoin policy stays its current course or evolves further. The story is consequential, ongoing, and worth following carefully through the specific structural milestones rather than through the rhetorical framing on either side.

The promise versus reality gap will narrow over time. Which side it narrows toward is the question the next several months will answer.

This article is for informational purposes and does not constitute financial or investment advice. The Strategic Bitcoin Reserve’s policy framework, congressional legislation, and operational implementation continue to evolve; the figures and milestones described reflect reporting available as of late May 2026. Always do your own research.

Crypto World

SEC Builds Tokenized Securities Framework Guided by “Innovation Without Arbitrage” Principle

TLDR:

- The SEC is developing a framework to list and trade tokenized securities under the “innovation without arbitrage” principle.

- SEC and CFTC are jointly identifying rulebook gaps covering swap reporting, portfolio margining, and product definitions.

- The CFTC approved Kalshi’s proposal to trade Bitcoin perpetual futures, leaving other assets open for case-by-case review.

- The SEC is targeting a 23-by-5 equity market trading transition and reviewing legacy rules like Regulation NMS by year-end.

The SEC is actively developing a framework for the listing and trading of tokenized securities, guided by the principle of “innovation without arbitrage.”

SEC Trading and Markets Director Jamie Selway outlined this direction at the Piper Sandler Global Exchange & Fintech Conference on June 4, 2026, in New York.

The framework aims to modernize U.S. capital markets while protecting existing market structure. Regulators are working to ensure new entrants and legacy providers are treated equally under the new rules.

SEC Pushes Forward on Tokenized Securities Framework

Chairman Atkins has directed the Division of Trading and Markets to develop a framework for tokenized securities listing and trading.

The guiding principle, “innovation without arbitrage,” is designed to prevent unfair advantages for either new or established market participants.

Selway described the principle plainly, saying the Division aims “to advantage neither new entrants nor legacy providers over the other.”

The SEC’s goal is to foster a healthy ecosystem for tokenized securities without disrupting existing, well-functioning markets.

The Division has been engaging with both traditional finance incumbents and decentralized finance new entrants. These conversations span the full range of tokenized securities operations, covering primary issuance, secondary trading, and custody.

Staff statements on custody and trading have already been issued as part of this groundwork. The Division is now working toward an “innovation exemption” recommendation to allow certain trading venues to trade tokenized securities.

Major market infrastructure players are already responding to this regulatory direction. The DTCC announced plans to facilitate limited production trades of tokenized securities through DTC’s service starting July 2026. A broader rollout is planned for October 2026.

Nasdaq and the NYSE have also separately announced plans to develop platforms for trading and on-chain settlement of tokenized securities.

Selway also confirmed the SEC is working to facilitate a transition to 23-by-5 equity market operation by the end of 2026. The Division is additionally reviewing legacy rules such as Regulation NMS and the Consolidated Audit Trail for modernization.

These efforts are part of a broader push to drive efficiency and competition across U.S. capital markets. Together, these steps position the SEC as an active architect of next-generation market infrastructure.

SEC-CFTC Coordination Shapes the Path for Tokenized Markets

The tokenized securities framework does not exist in isolation. The SEC and CFTC are coordinating in parallel on rules that touch both agencies’ jurisdictions.

Chairman Atkins stated directly that “firms should not be shuffled back and forth between regulators when a product touches elements of both regulatory frameworks.” He added that “where jurisdiction overlaps, the most effective response is a coordinated one.”

Both agencies are jointly identifying areas where their rulebooks lack clarity or compatibility. Swap and security-based swap data reporting, portfolio margining, and product definitions have been identified as initial focus areas.

The SEC also approved Nasdaq PHLX’s proposal to list cash-settled Bitcoin index options on May 22. These actions reflect a deliberate, step-by-step approach to building a coherent cross-agency framework.

Selway stressed two core responsibilities that must anchor the tokenized securities framework. Regulators must clearly distinguish investing from gambling, even as technology blurs traditional boundaries.

They must also prevent excessive leverage from reaching unsophisticated retail investors through new tokenized products.

Selway put it directly, warning against “extending unhealthy levels of leverage to the unsophisticated and unsuspecting” as markets evolve.

Industry participants were also urged to engage constructively rather than exploit jurisdictional gaps. Selway warned that venue shopping and unreasonable expectations will undermine harmonization efforts. He called on firms to bring forward their best ideas for reducing regulatory friction through public input.

He framed the stakes clearly, saying that by “delivering true innovations” and avoiding key pitfalls, industry organizations “can deliver value to your clients, your investors, your world-leading industry, and our great Nation.”

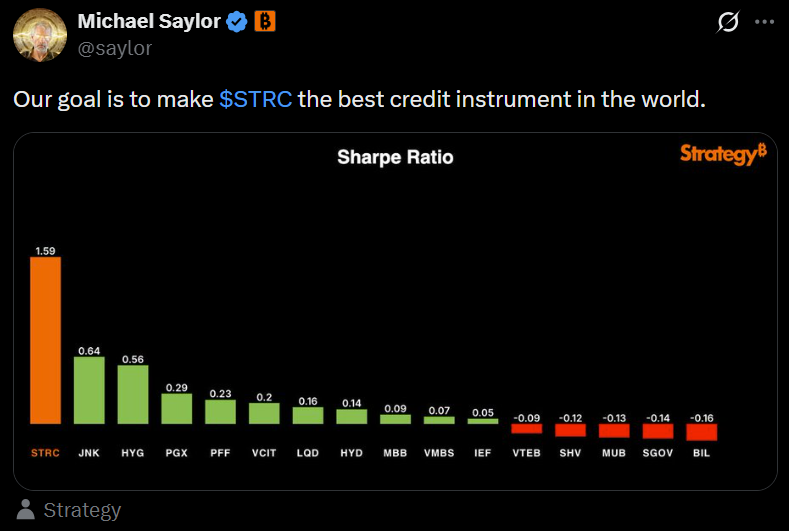

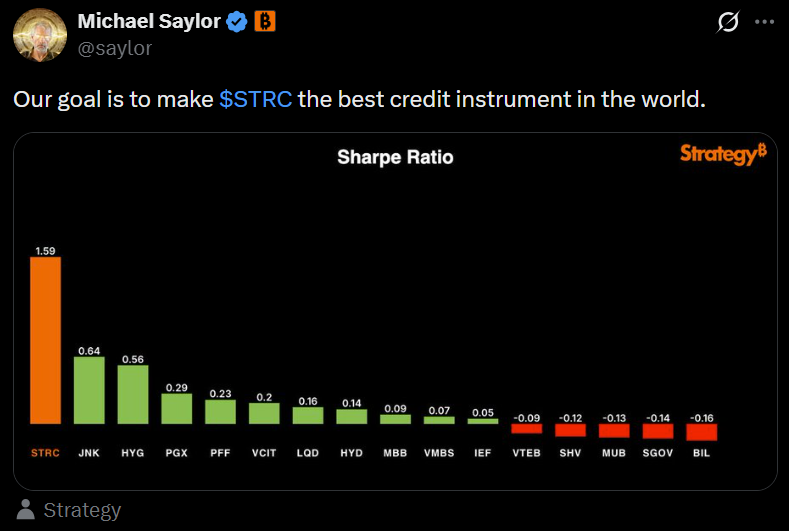

Strategy’s sale of 32 Bitcoin shouldn’t have mattered. The company still holds hundreds of thousands of BTC, and the transaction barely moved the needle on its balance sheet. Yet the market reaction was swift, exposing how much of the Bitcoin treasury trade had been built on a simple assumption: companies buy Bitcoin… and they never sell it.

Elsewhere in crypto this week, JPMorgan CEO Jamie Dimon escalated his fight against the industry’s preferred market structure bill and a French Bitcoin treasury company pushed the limits of capital formation by asking shareholders to approve a massive $122 billion fundraising mandate.

Strategy’s Bitcoin sale tests treasury trade

Michael Saylor’s Strategy rattled the market after disclosing the sale of 32 Bitcoin — its first reported BTC liquidation outside a 2022 tax-related transaction.

The sale itself was tiny relative to the company’s massive holdings, but it challenged the long-standing narrative that Strategy would only accumulate Bitcoin and never sell. Shares of MSTR fell sharply following the disclosure as investors reassessed the assumptions underpinning the Bitcoin treasury model.

“The market learned that Strategy is no longer read as a pure one-way accumulation vehicle,” Delphi Digital wrote in a market summary.

“The old ‘never sell’ meme is now broken in practice, not just in conference call language,” Delphi added.

The transaction has reignited debate over how Bitcoin treasury companies should be valued. While Strategy remains committed to growing its Bitcoin-per-share metric, the sale served as a reminder that even the most committed corporate hodlers face financial realities.

Source: Michael Saylor

JPMorgan CEO draws a line in the sand on CLARITY

The battle over US crypto regulation intensified after JPMorgan CEO Jamie Dimon said banks would oppose the latest version of the CLARITY Act, arguing that crypto companies are being granted privileges without being subject to the same regulatory burdens as traditional financial institutions.

Dimon specifically criticized provisions that would allow crypto companies to offer interest-bearing products while avoiding the capital and compliance requirements imposed on banks.

The comments underscore a growing divide between the banking sector and the crypto industry as lawmakers push for market structure legislation. Supporters see CLARITY as a long-awaited framework that would provide regulatory certainty and encourage innovation. Critics, however, argue that the bill risks creating an uneven playing field.

Jamie Dimon said the banking industry opposes the latest CLARITY markup. Source: Fox Business

Capital B seeks approval for $122 billion Bitcoin war chest

Bitcoin treasury company Capital B is asking shareholders to approve a sweeping expansion of its fundraising capacity, seeking authorization to issue up to 5 billion euros ($5.8 billion) in new equity and roughly $116 billion in credit instruments to finance future Bitcoin purchases.

The proposal, which will be voted on at Capital B’s June 17 shareholder meeting, would give management access to a vastly larger pool of capital than it has raised to date. According to the company, Capital B has secured about $325 million in funding so far, including a recent raise backed by Blockstream CEO Adam Back and asset manager TOBAM.

The company purchased 192 BTC for $15.2 million last month and added another 4 BTC on Monday, bringing its total holdings to 3,139 BTC.

Source: Alexandre Laizet

Coinbase invests in ProShares stablecoin reserve ETF

Coinbase has invested an undisclosed amount in the ProShares GENIUS Money Market ETF (IQMM), a fund designed to hold assets that qualify as stablecoin reserves under the GENIUS Act.

The exchange-traded fund provides exposure to the cash, bank deposits and short-term US Treasury securities that payment stablecoin issuers are required to hold under the legislation. The GENIUS Act mandates that stablecoins be backed by highly liquid reserves, creating demand for investment products tied to those assets.

The investment highlights growing interest in stablecoin reserve assets as the US moves closer to establishing a federal regulatory framework for the sector. Stablecoin issuers are expected to become major buyers of Treasury bills and other highly liquid securities if adoption continues to grow.

Source: ProShares

Crypto Biz is your weekly pulse on the business behind blockchain and crypto, delivered directly to your inbox every Thursday.

Securitize has moved closer to entering public markets after securing regulatory clearance for its planned SPAC merger.

Summary

- Securitize has received SEC approval for its SPAC merger filing with Cantor Equity Partners II.

- The deal now moves to a shareholder vote scheduled for June 29.

- If approved, Securitize is expected to list on the New York Stock Exchange under ticker SECZ.

- The company provides tokenization infrastructure and services to over 650 funds globally.

- Securitize oversees more than $4 billion in tokenized assets across its platform.

According to the U.S. Securities and Exchange Commission, the agency has declared effective the S-4 registration tied to Securitize’s proposed combination with Cantor Equity Partners II, clearing the deal for a shareholder vote scheduled for June 29. If investors approve the transaction, the company said it expects to finalize the merger soon after and begin trading on the New York Stock Exchange under the ticker “SECZ.”

SPAC route advances toward listing

Through the planned merger, Securitize will combine with Cantor Equity Partners II, a special purpose acquisition company backed by an affiliate of Cantor Fitzgerald. Company statements confirm the resulting entity will operate as Securitize Corp. once listed.

From a regulatory standpoint, the SEC’s approval allows the process to move into its final stage. The shareholder vote now becomes the key hurdle before the listing proceeds. Securitize Chief Executive Carlos Domingo said in a company release that the milestone supports the firm’s effort to expand tokenization infrastructure at a global scale.

At a time when several crypto firms have delayed public listings, including reported pauses by Kraken and Consensys, Securitize’s progress highlights a different trajectory for companies tied to real-world asset tokenization.

Institutional demand shapes tokenization growth

Across financial markets, tokenization continues to attract major institutions. Data from RWA.xyz shows the tokenized asset sector has grown past $30 billion after nearly tripling within a year. Projections from Citigroup estimate the market could reach $5.5 trillion by 2030, while a joint study by Boston Consulting Group and Ripple suggests a potential $18.9 trillion market by 2033.

Participation from firms such as BlackRock, Franklin Templeton, JPMorgan Chase, and Fidelity Investments has expanded the sector’s reach into traditional finance. These institutions are exploring blockchain-based versions of bonds, funds, and private credit, with advocates pointing to faster settlement and lower operating costs.

Securitize’s role in market infrastructure

Operating within this environment, Securitize has built systems that support token issuance, fund administration, and secondary trading. The company reports it services roughly 650 funds through its Securitize Fund Services platform and oversees more than $4 billion in tokenized assets.

Its partnerships include infrastructure support for firms such as Apollo Global Management, KKR, Hamilton Lane, and VanEck. In addition, collaboration with the New York Stock Exchange has focused on developing tokenized equities platforms.

A notable product tied to the firm is BlackRock’s BUIDL fund, launched in 2024 as a tokenized money market fund and now counted among the largest tokenized Treasury offerings.

Recent disclosures show Securitize raised $47 million in a 2024 funding round led by BlackRock. Operational data from the company indicates it recorded $1.9 billion in transaction volume during the first quarter of the year.

Meanwhile, additional partnerships, including work with Computershare on issuer-backed tokenized shares, continue to expand its product range. As the June shareholder vote approaches, the outcome will determine whether Securitize becomes one of the first major tokenization firms to trade publicly in U.S. markets.

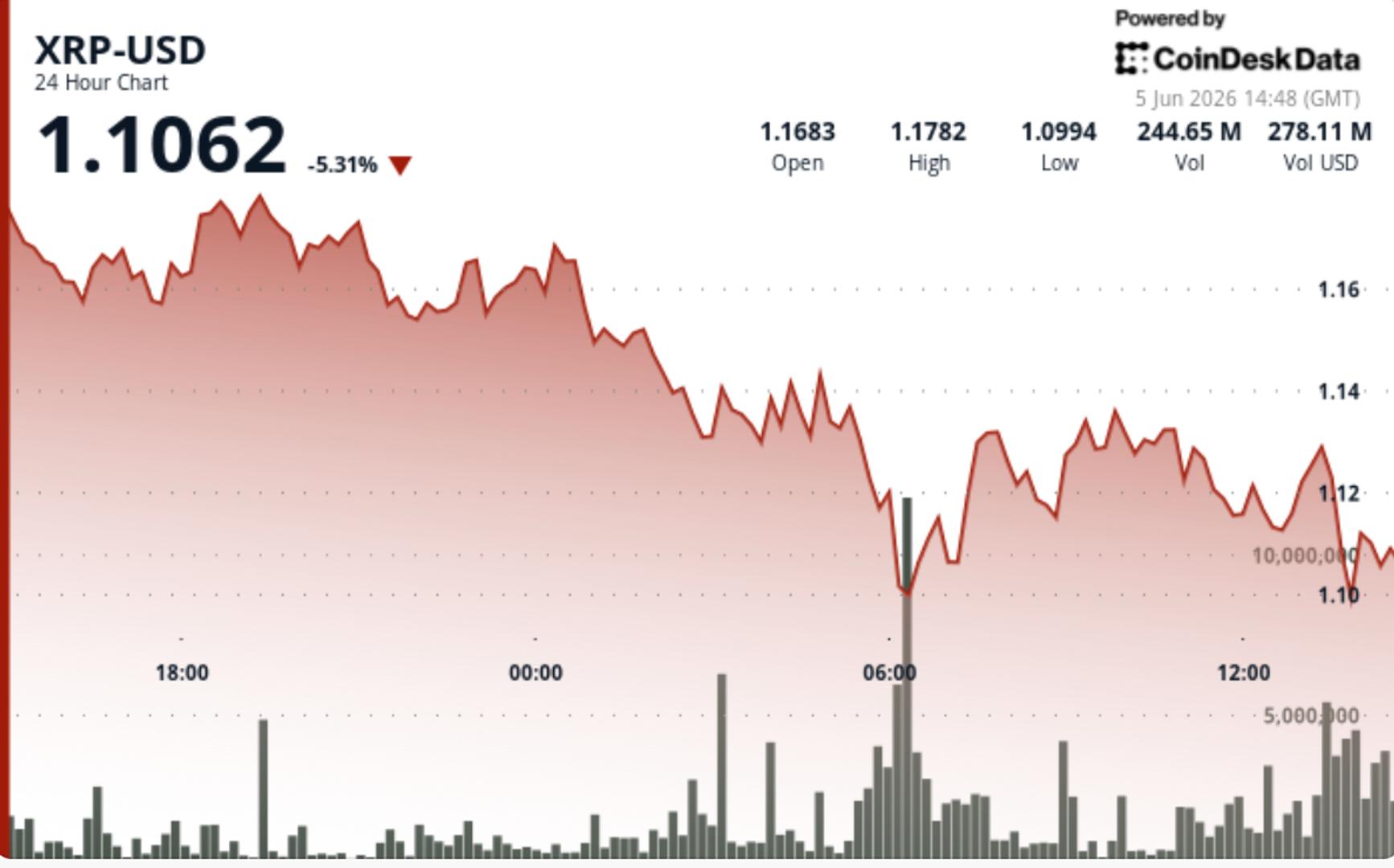

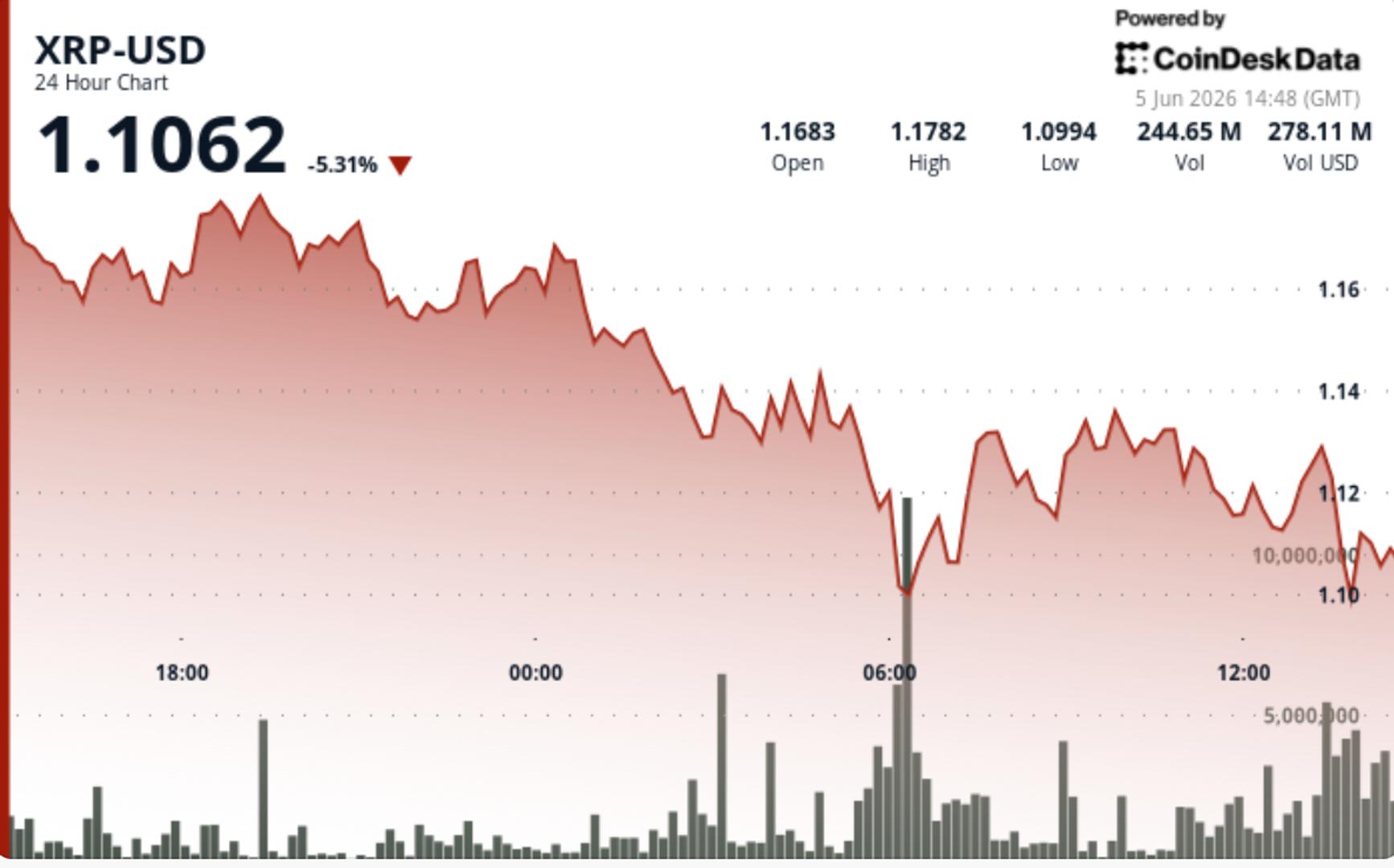

XRP is no longer fighting over $1.20. It’s fighting over whether $1.10 holds. The latest selloff came with the kind of volume usually associated with forced liquidations rather than orderly selling, pushing the token to its weakest levels in months before dip buyers finally showed up near $1.09.

News Background

• XRP ETFs recorded roughly $4 million in inflows after seeing their first daily outflow in three weeks, bringing cumulative inflows to around $1.5 billion.

• Market sentiment deteriorated sharply across crypto, with the Fear & Greed Index falling into extreme fear territory as traders reacted to broader macro uncertainty.

• XRP also slipped behind USDC in market capitalization rankings after the selloff pushed its value below $75 billion.

Price Action Summary

• XRP fell from $1.17 to $1.11 during the 24-hour session, touching lows near $1.09 before recovering slightly.

• The biggest move came during the June 5 06:00 UTC session, when volume surged to 268.2 million XRP and accelerated the breakdown.

• A failed rally toward $1.133 later reversed sharply, sending price to fresh lows before buyers stepped in near $1.10.

Technical Analysis

• The key takeaway is that support levels keep becoming resistance. What was a buying zone around $1.20-$1.25 just days ago is now where sellers are reappearing.

• The move below $1.10 briefly pushed XRP into one of the most oversold conditions seen in years, with weekly RSI readings reaching levels that historically appeared near major cycle lows.

• Even so, oversold does not automatically mean bullish. Markets can stay oversold for longer than traders expect, especially during liquidation-driven declines.

• The bounce from $1.09 showed signs of seller exhaustion, but recovery volume remained weaker than the selling that preceded it.

What traders should watch

• $1.09-$1.10 is now the most important support zone on the chart. Losing it would shift focus toward the $0.92 area highlighted by several analysts.

• $1.12-$1.13 becomes the first recovery zone XRP needs to reclaim before any stabilization narrative gains credibility.

• The broader trend remains bearish until XRP starts reclaiming former support levels rather than simply bouncing from oversold conditions.

• Traders looking for evidence of a durable bottom will likely want to see stronger volume on rebounds than on selloffs, something the market has not yet delivered.

XRP opens June with its most significant decline of the past 3 months. The $1.20 support band, which served as the absolute floor for months, is being breached, with the price now trading at $1.11. The RSI is also printing its lowest reading since February’s capitulation, and the next meaningful support is nearly $0.30 lower. This is not a pullback from resistance; it is likely a breakdown of the last line of defense.

Ripple Price Analysis: The USDT Pair

On the USDT chart, the $1.20 support band, which held strong during the February crash and has remained untouched since, is on the verge of breaking down. The RSI has also collapsed to approximately 20–25, nearing the oversold extreme seen at the February capitulation low. That reading alone warrants attention, as historically, RSI at these levels has preceded, at minimum, a sharp relief bounce even within a broader downtrend.

However, an oversold RSI does not mean a floor has been found on its own. The $1.20 level is now likely to flip into resistance, and any bounce needs to reclaim it on a sustained closing basis to suggest the breakdown is being reversed rather than simply paused.

Below the current price, the next structural reference is the $0.80 demand zone, which also converges with the descending channel’s lower boundary. This is a meaningful confluence of support, but still at a significantly lower level. The 100-day moving average at $1.35 and the 200-day moving average at $1.60 are now both heavily overhead, leaving XRP with a stack of resistance above and thin structural support below on the USDT-paired chart.

The BTC Pair

The BTC pair is telling a more resilient story. XRP/BTC is trading at 1,800 sats, holding above the recent lows at 1,740 sats. The RSI, which surged to 70 at the end of May in what looked like a meaningful momentum shift, has already faded back to 50, indicating that the brief strength has not followed through into sustained buying.

The price is sitting below the 1,850 sat short-term resistance after getting rejected by the level again, with the declining 100-day moving average at approximately 1,900 sats acting as the immediate dynamic overhead resistance. The fact that the ratio has held while the USDT pair broke down suggests the XRP weakness is partly a function of broader altcoin selling in dollar terms rather than XRP-specific deterioration against Bitcoin.

A confirmed close below 1740 sats on the BTC pair, particularly if it coincides with continued USDT pair weakness, would mark a definitive breakdown on both pairs simultaneously, which exposes the 1,500 sats area as the next reference below.

The post Ripple Price Prediction: How Low Can XRP Go If $1 Support Cracks? appeared first on CryptoPotato.

The team behind the controversial crypto project rolled out a major upgrade intended to strengthen the entire ecosystem.

Nonetheless, the positive news failed to trigger a rebound for PI, whose valuation nosedived to yet another all-time low.

Upgrade Completed

Pi Network has made significant progress in recent months. In February, the Core Team unveiled protocol version 19.6, followed by an upgrade to v19.9. Later on, they introduced the highly anticipated v20.2, which set the foundation for smart contract capabilities.

Last month, the team announced a migration to protocols v22 and v23, setting June 2 as the deadline to complete the transition to v24. This development was disclosed on Pi Network’s official X account earlier today (June 5).

“Great job to all Nodes! This was one of the most challenging migrations,” the message reads.

The upgrade to protocol 24 is primarily focused on enhancing the underlying infrastructure that supports node operations and mainnet activity. The Core Team revealed that migration to v25 is next in line, with June 18 designated as the completion deadline.

In addition to the protocol update, Pi Network has recently advanced further in the gaming field. As CryptoPotato reported, CiDi Games (a Pi Network Ventures portfolio company) released four new games for Pioneers. Those include Coin Whack, Fruit Stack, Gemnova, and RainbowCubes.

PI Price Outlook

Despite the aforementioned developments, PI’s valuation remains heavily suppressed by the bear market and the latest pullback, which swept through the entire crypto market.

Earlier this week, it collapsed to a new all-time low of around $0.12, representing a 33% decline for the month and a whopping 96% crash from the historic peak of $3 witnessed at the start of 2025. PI’s market capitalization has fallen to roughly $1.3 billion, making it the 58th-largest cryptocurrency.

Certain factors signal that a further correction could be on the way. Data show that the number of PI coins stored on exchanges has soared by over 500,000 in the past 24 hours, bringing the total to over 550 million. This suggests that numerous investors have transferred their holdings to centralized platforms, thus increasing immediate selling pressure.

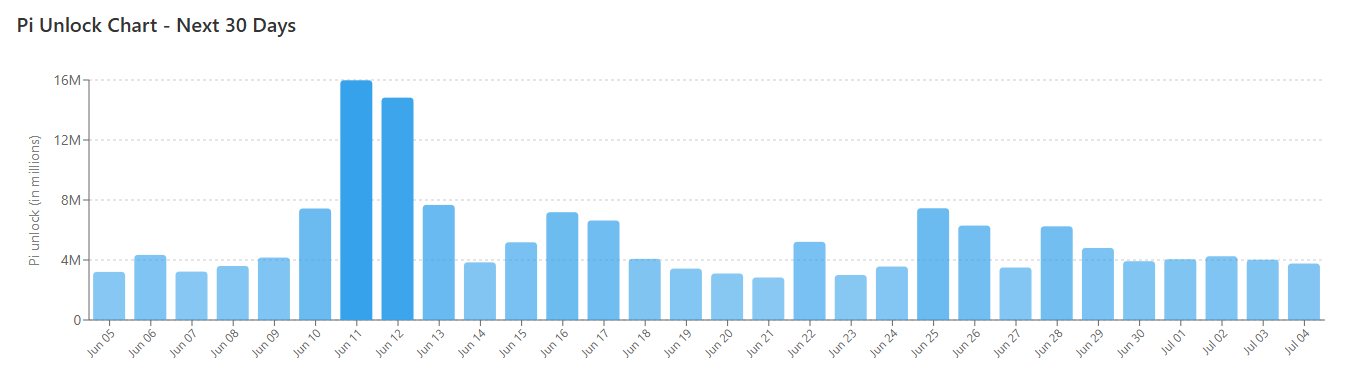

The upcoming token unlocks are next on the list, with approximately 160 million PI set to enter circulation over the next 30 days. June 11 stands out as the record day when 16 million coins will be released. This development doesn’t guarantee a steeper downfall, but it will allow some investors to cash out tokens they have been holding for a long time.

The post Pi Network Completes a Major Milestone, Yet PI’s Price Keeps Bleeding: Details appeared first on CryptoPotato.

Michael Saylor has urged Bitcoin supporters to balance purity, adoption, innovation, and stability as the asset trades near its weakest levels in almost two years.

Summary

- Michael Saylor said Bitcoin’s future depends on balancing competing ideologies, not choosing one camp.

- Saylor named Maximalists, Capitalists, Technologists, and Fundamentalists as key groups in Bitcoin’s growth.

- Strategy’s sale of 32 BTC raised concerns despite its holdings of more than 844,700 BTC.

Saylor, writing in a Friday post on X, said Bitcoin’s future should not depend on one dominant ideology. The Strategy chairman said the network needs several groups with different priorities, including Maximalists, Capitalists, Technologists, and Fundamentalists.

According to Saylor, each group serves a separate role in protecting Bitcoin’s long-term strength. He said the debate should not force a choice between “purity and adoption” or between “innovation and stability.” Instead, Saylor wrote that Bitcoin must remain true to its core while companies, banks, and governments build around it.

Saylor calls for balance across Bitcoin camps

In his essay, Saylor described Bitcoin as a system that benefits from conviction, integration, innovation, and preservation. He said Bitcoin’s base layer should remain protected as “sacred infrastructure,” while Bitcoin as an asset should continue entering corporate balance sheets, banking products, and national reserve discussions.

The remarks came as Bitcoin traded below $61,000 on Friday. Market data in the report showed BTC down 5.79%, more than 25% lower over the past month, and more than 50% below its October 2025 record high of $126,000.

Saylor’s comments also arrived during a fresh debate over Bitcoin’s deeper ties with traditional finance. Corporate treasury strategies, spot exchange-traded funds, and capital market products have brought new demand into Bitcoin, but they have also caused concern among some long-time supporters.

Strategy sale draws market scrutiny

Strategy has become the best-known corporate Bitcoin holder under Saylor’s leadership. The company has used preferred stock offerings over the past year to help finance more Bitcoin purchases.

However, Strategy’s recent sale of 32 bitcoins for about $2.5 million drew attention because the company has long promoted accumulation. The sale represented a very small part of Strategy’s more than 844,700 bitcoins, but some critics questioned whether it could lead to more selling.

CNBC host Jim Cramer reacted sharply after Strive CEO Matt Cole explained the sale in a video. Cramer said Saylor had “murdered Bitcoin,” according to the report.

Analysts split on Bitcoin’s next support

Grayscale Head of Research Zach Pandl said Friday that Strategy’s ability to keep buying Bitcoin appears limited at current share prices. According to Pandl, Bitcoin may need other sources of demand before the market finds a sustainable bottom.

Meanwhile, Standard Chartered Head of Digital Assets Research Geoffrey Kendrick offered a more positive view. Kendrick said Bitcoin’s low is “almost in,” citing resilient spot ETF holdings and the chance that Strategy buys back more Bitcoin than it recently sold.

According to Kendrick, such a move would show that the worst part of the selloff has likely passed. His view differs from critics who see Strategy’s sale as a warning sign during Bitcoin’s steep decline.

Saylor’s essay has placed Bitcoin’s internal debate back in focus at a time when price weakness has increased pressure on major holders. His argument centers on the idea that Bitcoin must keep its core rules intact while still allowing financial products, corporate treasuries, and institutional channels to grow around it.

Cardano (ADA) reached its lowest price since 2020, falling to about $0.15 from over $0.37 earlier in 2023. The dip comes as cryptocurrencies face a challenging period, and ADA holders are watching to see if it will hold above this critical support level.

According to Coin Bureau’s official X account, ADA is hitting its lowest price since 2020. Traders are discussing possible risks and forecasting variables that could aid ADA’s price recovery.

Key Takeaways

- Cardano (ADA) hit a low of around $0.15 recently, its lowest since 2020

- The chart shows a consistent downtrend with lower highs and lows

- Market participants are watching for clues on whether ADA will stabilize or continue to drop

ADA Extends Multi-Month Downtrend

Coin Bureau’s weekly chart shows Cardano, or ADA, in a long-term downtrend. After hitting almost $0.37, it formed a series of lower highs and lows, indicating steady selling pressure over months.

ADA tried to bounce back in May, reaching close to $0.28, but the momentum didn’t last. As soon as that happened, buyers lost steam and the price dove again. This recent drop took ADA from about $0.24 to $0.15, one of the quickest and biggest falls on the chart.

The latest weekly chart highlights how challenging things have been for ADA lately.

Support Levels Come Into Focus

Right now, the $0.15 area is Cardano’s nearest support zone, the lowest point on the chart. Traders see this level as a spot where buying might kick in. If ADA holds above it, we could start to see stability after weeks of falling prices. People usually look at past support levels to find less selling pressure and more demand.

Resistance Zones and Recovery Outlook

For ADA to bounce back, it needs to overcome some hurdles left during its fall. The first is around $0.24, where the recent drop gained momentum. Next is a spot at $0.28; that was the peak in May. If ADA surges past these levels, it could signal growing positive sentiment and renewed buying interest.

There’s also a wider resistance zone between $0.34 and $0.37. This range started the big downtrend and remains a major test for traders watching a potential comeback.

Bitcoin tumbled below $60,000 on Friday, breaking the lows of the early February crypto crash and reaching its weakest level since October 2024.

The largest cryptocurrency is down nearly 20% in just the past week, and now has lost more than 52% since its October peak above $126,000.

Several headwinds have converged over bitcoin recently — the most important being its largest single buyer, Michael Saylor’s Strategy, having turned seller. Additionally, spot bitcoin ETFs suffered persistent outflows as investors pulled capital from the sector, instead allocating it to the red-hot artificial intelligence trade and related stocks.

Stubbornly elevated inflation and a hot labor market report Friday also prompted investors to rethink the path of U.S. monetary policy. Markets that earlier this year expected rate cuts have now fully priced in the Federal Reserve’s next move as a rate hike.

With that, U.S. stocks have lost momentum after a powerful run to record highs, weighing on risk appetite across markets. The Nasdaq is lower by more than 2% Friday.

Crypto investors have also been grappling with renewed concerns about whether artificial intelligence and quantum computing could expose weaknesses of crypto protocols. Privacy-focused cryptocurrency Zcash (ZEC) plunged more than 40% overnight after a critical vulnerability was discovered with the help of Anthropic’s latest Opus 4.8 AI model.

Bitcoin extended its slide into Friday’s U.S. session as traders prepared for a retest of the $60,000 level, underscoring persistent selling pressure even as a growing cohort of players looks for relief near that floor. The move comes amid a broader risk-off tone and a crowded battle around the round-number support that has guided momentum for weeks.

Key points:

- Bitcoin is testing the $60,000 support, entering its sixth consecutive red daily candle and erasing much of the spring rally.

- Early signals of “seller exhaustion” are surfacing from market observers watching funding dynamics and price differentials across exchanges.

- U.S. nonfarm payrolls data for May surprised to the upside, strengthening the case for a slower pace of Federal Reserve easing and lending a liquidity tailwind to risk assets only if inflation remains controlled.

BTC at the crosswinds of price action and macro data

Data from TradingView highlighted how quickly downside momentum was accumulating against Bitcoin, with the daily chart showing a retreat of roughly 5% as sellers dominated the session. The market’s focus zeroed in on the price region around $60,000, seen as a critical juncture after a period of fluctuations that has left traders debating whether a sustained bid can reassert itself above the barrier.

“Rapidly approaching its February low at $60K. Now in its 6th red daily candle and down more than the entire April/May rally,”

said Daan Crypto Trades in a reaction posted on X, underscoring how the rally’s momentum has been difficult to sustain in the face of renewed selling pressure. The chorus of traders has framed the $60K area as a potential hinge point—either a strong constructive turn or a fresh leg lower if selling accelerates.

“Eyes on that $60K area for now.”

Market chatter extended to the micro-structure of pricing, including the Coinbase Premium—the spread between Coinbase’s BTC/USD and Binance’s BTC/USDT quotes—and layers of funding on perpetual futures. In recent coverage, commentators highlighted that while price action remained under controlled selling, funding had edged toward negative territory and the Coinbase premium had narrowed. Those dynamics, if continued, could hint at a shift in sentiment as buyers re-engage at a perceived discount.

“Early signs of seller exhaustion.”

In this framework, traders are watching for a potential pause in the down move, a narrowing of wholesale selling pressure, and a probable rebalancing of bids as liquidity cycles through the market. The conversation around order-book depth and short-term dynamics is increasingly focused on whether sellers can maintain a decisive advantage near the $60K mark or if buyers can flip the script in the coming sessions.

Trader Morin noted that Bitcoin was “frontrunning a key range low,” with the $60,000 threshold appearing again as a decisive reference point. He pointed to a pattern of lower highs that has characterized the current slide, suggesting that a sustained breakout above that barrier would be a meaningful inflection. “Swept 61.3k internal low but failed to make higher high. Consistent lower highs —> Sellers in Control,” Morin wrote on X, signaling that without a decisive shift, the downside could extend into the 60Ks.

For market technicians, the price geometry remains a focal point. The immediate question is whether the shallow relief rallies seen in prior weeks can evolve into a more durable bounce that reclaims the mid-$60,000s region, or if the bears regain control and drive BTC toward the next visible support pockets.

Macro backstop or drag: payrolls reshuffle the Fed calculus

The broader macro backdrop did not provide a supportive push for risk assets on this occasion. U.S. nonfarm payrolls data for May surprised to the upside, adding 172,000 jobs versus a consensus of around 85,000. The figure came after April’s payrolls were revised higher by 64,000, reinforcing a view of a resilient labor market. The strength in the jobs print reduces the immediate odds of aggressive Fed easing and, in turn, dampens the impulse for a rapid liquidity withdrawal in some segments of the market.

The May payrolls release adds to a complex inflation trajectory: solid employment gains alongside ongoing price pressures. Market participants have been weighing how the Fed will balance the twin goals of containing inflation and sustaining growth. The CME Group’s FedWatch Tool reflected this tension by showing pricing that still contemplates a potential rate hike before year-end, even as investors assess the pace and magnitude of any policy shifts. In the near term, stronger labor-market data tends to complicate the path for central-bank easing, a dynamic that can reframe风险 appetite across assets, including digital markets.

Analysts have argued that a robust jobs market reduces the impulse for near-term rate cuts, especially if inflation remains a concern. Mosaic Asset Company, in its latest Mosaic Chart Alerts, noted that while solid economic activity supports stock indexes advancing toward prior highs, it also injects a degree of uncertainty around monetary policy. The argument is that a stronger economy raises the bar for easing and keeps liquidity conditions tighter, which can weigh on high-beta assets like BTC in the short term even as it supports the longer-term narrative of a healthier macro backdrop.

From a liquidity perspective, the payrolls data underscores a broader market theme: macro resilience does not automatically translate into crypto rallies. Instead, it can widen the divergence between traditional markets and digital assets, especially if inflation remains a friction point and investors seek shelter in cash or longer-duration risk assets depending on evolving expectations around the Federal Reserve’s policy path.

As traders parse the data, attention remains on how much of the May strength is driven by temporary factors—like short-covering or technical rebounds—and how much reflects a real re-accumulation of demand at price levels perceived to be fair value given macro constraints. The next few sessions could reveal whether Bitcoin can sustain a bottoming process or if the prevailing headwinds corral price action back toward the tighter end of its recent range.

Market watchers will also be mindful of liquidity patterns across exchanges. The Coinbase premium and funding signals have historically offered a real-time glimpse into US demand versus offshore liquidity pools. If the premium continues to narrow and funding remains negative, the market could be leaning toward a more balanced, less leveraged stance that may lift BTC only after a clear breakout above key levels or a sustained improvement in macro cues.

What to watch next in a market recalibrating around a critical level

With BTC languishing near a critical line in the sand, the immediate path forward hinges on a combination of price action, micro-structure signals, and the pace of macro normalization. A close above or below the $60,000 threshold in the coming sessions could set the tone for the next leg—whether a deeper test of support or a renewed bid from buyers that redefines expectations for the second half of the year.

On the price front, traders will scrutinize whether buyers can sustain a move back above the round-number barrier and convert it into a durable retest of the mid-$60,000s. In the event of renewed strength, a retest of recent highs may re-emerge as a topic of discussion; otherwise, the risk remains tilted toward a broader consolidation with potential downside targeting nearby support clusters.

From the macro lens, the balance between inflation trends and employment momentum will keep policy expectations in play. If inflation pressures ease further while the labor market cools, rate-cut expectations could brighten the picture for risk assets. Conversely, if inflation holds or accelerates and the Fed signals a cautious stance, BTC could remain tethered to a cautious risk-off regime even in the face of improving liquidity conditions elsewhere in markets.

In the near term, investors will want to monitor the evolving funding landscape, the behavior of inter-exchange price differentials, and any shifts in the Coinbase-Binance dynamic that could precede a broader shift in demand. The coming weeks will reveal whether the tested support at $60,000 becomes a launching pad for a more resilient bounce or a renewed springboard for a downleg that invites another retest of lower levels.

For now, the story remains a nuanced blend of price mechanics and macro uncertainty. BTC’s fate in the near term appears closely tied to whether buyers can demonstrate conviction around the $60,000 floor and whether macro expectations align with a sustainable re-pricing of risk assets in a post-pandemic, inflation-sensitive environment.

Next up, traders will be watching upcoming data milestones and central-bank signals to gauge whether the current backdrop is setting the stage for a meaningful shift in momentum or a protracted consolidation below key levels. The degree to which the payrolls print translates into policy caution will be a decisive factor shaping market sentiment in the days ahead.

SEC Builds Tokenized Securities Framework Guided by “Innovation Without Arbitrage” Principle

Late surge allows Tyrrell Hatton to seize lead at LIV Golf Andalucia

iOS 27 Leaks Point to Notification Gestures Moving Left and Siri Evolving Into a Proper Chat Partner

-

Business4 days ago

Business4 days agoJade Biosciences, Inc. (JBIO) Discusses Positive Interim Results From JADE101 Phase I Healthy Volunteer Study and Development Plans Transcript

-

Tech6 days ago

Tech6 days agoSpaceX just won a second Golden Dome contract. This one is $4.16 billion.

-

News Videos7 days ago

News Videos7 days agoSHE IS KILLING XRP!!! WATCH URGENT AND ACT FAST

-

Sports3 days ago

Sports3 days agoFrench Open 2026 results: Alexander Zverev beats Rafael Jodar and will play Jakub Mensik in semi-finals

-

NewsBeat7 days ago

NewsBeat7 days agoFIRST NIGHT REVIEW: Take That bring the Circus back to life in spectacular sun-soaked style

-

Business6 days ago

Business6 days agoIs the Spurs Phenom Already Better Than Prime Diesel?

-

Tech3 days ago

Tech3 days agoCryZENx Releases Fresh Playable Content Deep Inside Jabu-Jabu for His Ocarina of Time Remake

-

NewsBeat7 days ago

NewsBeat7 days agoNovak Djokovic v Joao Fonseca LIVE: French Open latest scores and results after Jannik Sinner’s shocking collapse

-

Politics6 days ago

Politics6 days agoThe House | Inside Andy Burnham’s Makerfield Campaign: “Nobody Thinks This Is In The Bag”

-

Crypto World8 hours ago

LBank Surpasses 25 Million Users Worldwide as AFA Partnership Continues to Drive Global Growth

-

Business3 days ago

Business3 days agoTrump Taps Housing Chief Bill Pulte as Acting Intelligence Director After Gabbard Exit

-