Crypto World

Liquidity, Regionalization & Asset Allocation

For global investors, 2025 was one of the most undercurrent-filled years of the 21st century. Unlike the bursting of the dot-com bubble in 2001 or the global financial crisis in 2008, markets in 2025 did not experience a prolonged, large-scale liquidation cycle or a “storm-like” sequence of relentless crashes.

Yet it is clear that, amid geopolitical uncertainty, uncertainty over US fiscal and monetary policy, uncertainty across multiple countries’ economic fundamentals, and the ebbing of globalisation in favour of regionalisation, equities, bonds, commodities and crypto have all been pricing in a future that is more cautious and more defensive.

Against that backdrop, liquidity allocation has become less concentrated in equities and bonds than it once was. Commodities, FX and rates attracted greater attention in 2025. At the same time, investors have been steadily reducing leverage and trimming exposure to higher-risk assets—one of the direct reasons the crypto bull market ended in Q4 2025.

So, where do markets go in 2026? As in 2025, implied expectations embedded in derivatives-market data have already offered an answer.

Liquidity: Not Abundant

At the start of 2025, one major “bullish” factor in investors’ minds was Donald Trump’s formal inauguration. The prevailing view was that Trump would trigger more rate cuts, inject more liquidity into markets, and drive asset prices higher.

Indeed, between September and December 2025, amid “concerns about a weakening labour market”, the Federal Reserve delivered three “defensive” rate cuts and, in December, announced the end of quantitative tightening. But this did not produce the liquidity flood investors had hoped for.

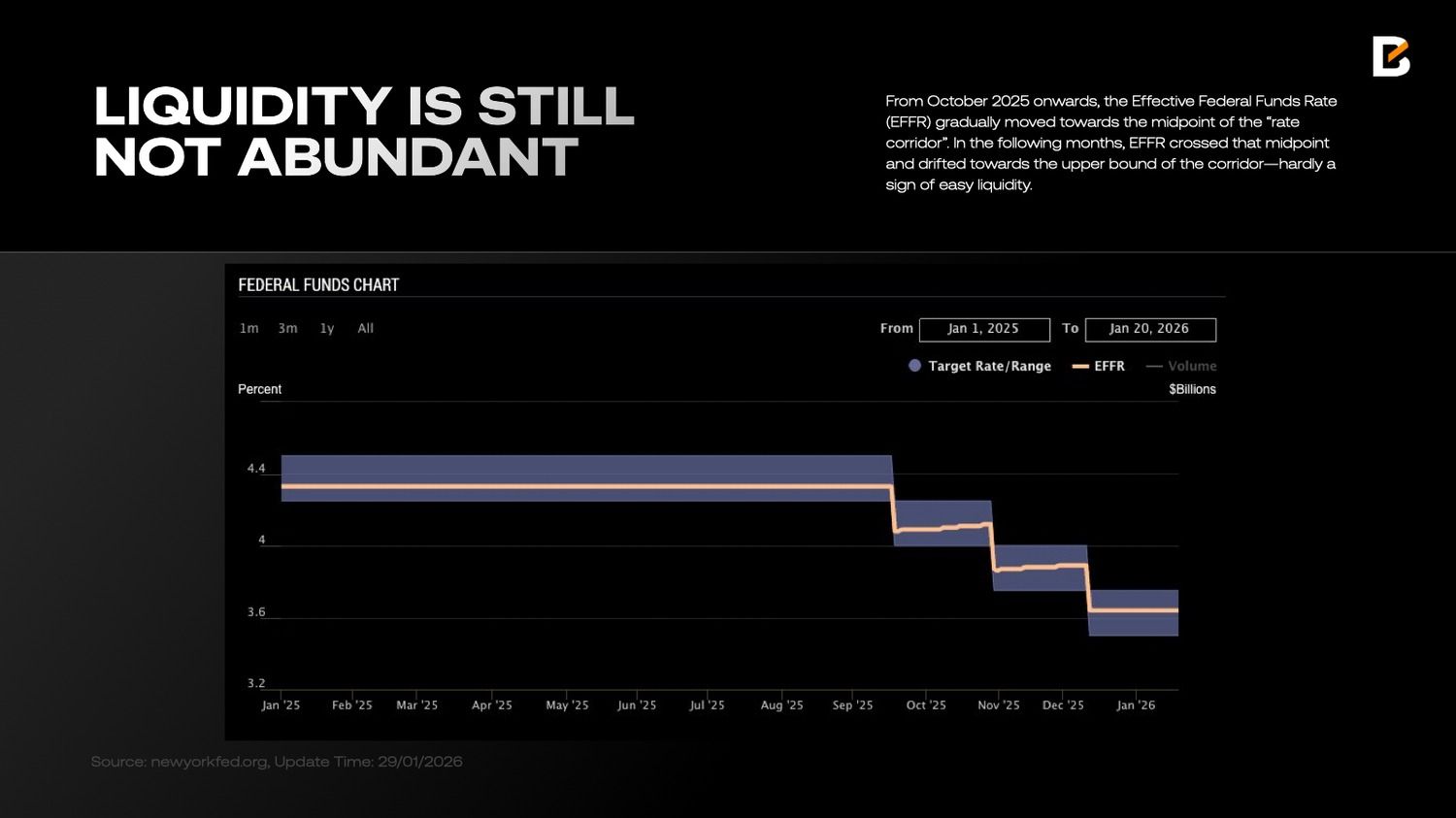

From October 2025 onwards, the Effective Federal Funds Rate (EFFR) gradually moved towards the midpoint of the “rate corridor”. In the following months, EFFR crossed that midpoint and drifted towards the upper bound of the corridor—hardly a sign of easy liquidity.

EFFR is the core short-term market rate in the US. It reflects funding liquidity conditions in the banking system and how the Fed’s policy stance (hikes or cuts) is transmitted in practice. In relatively loose-liquidity regimes, EFFR tends to sit closer to the lower end of the corridor, as banks have less need for frequent overnight borrowing.

In the final months of 2025, however, banks clearly faced liquidity tightness—a key driver of the rise in EFFR.

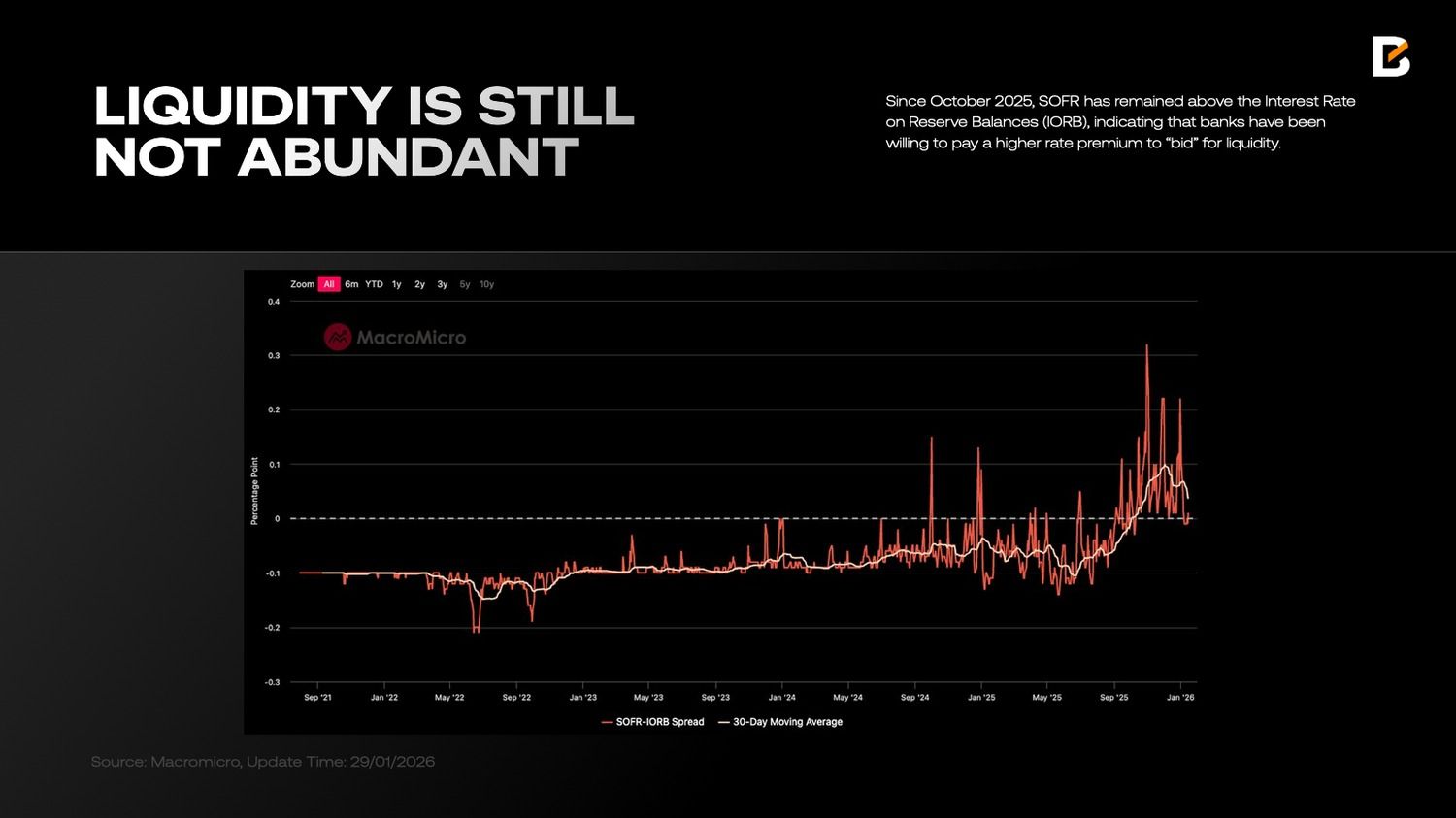

The SOFR–IORB spread further highlights the degree of stress. If EFFR primarily reflects cash-market conditions, SOFR, secured funding collateralised by US Treasury securities, captures a broader liquidity shortage. Since October 2025, SOFR has remained above the Interest Rate on Reserve Balances (IORB), indicating that banks have been willing to pay a higher rate premium to “bid” for liquidity.

Notably, even after the Fed stopped shrinking its balance sheet, the SOFR–IORB spread did not fall sharply in January. One plausible explanation is that, during 2025, banks deployed a significant share of their liquidity buffers into financial investments rather than extending credit to the commercial, industrial, and real estate sectors.

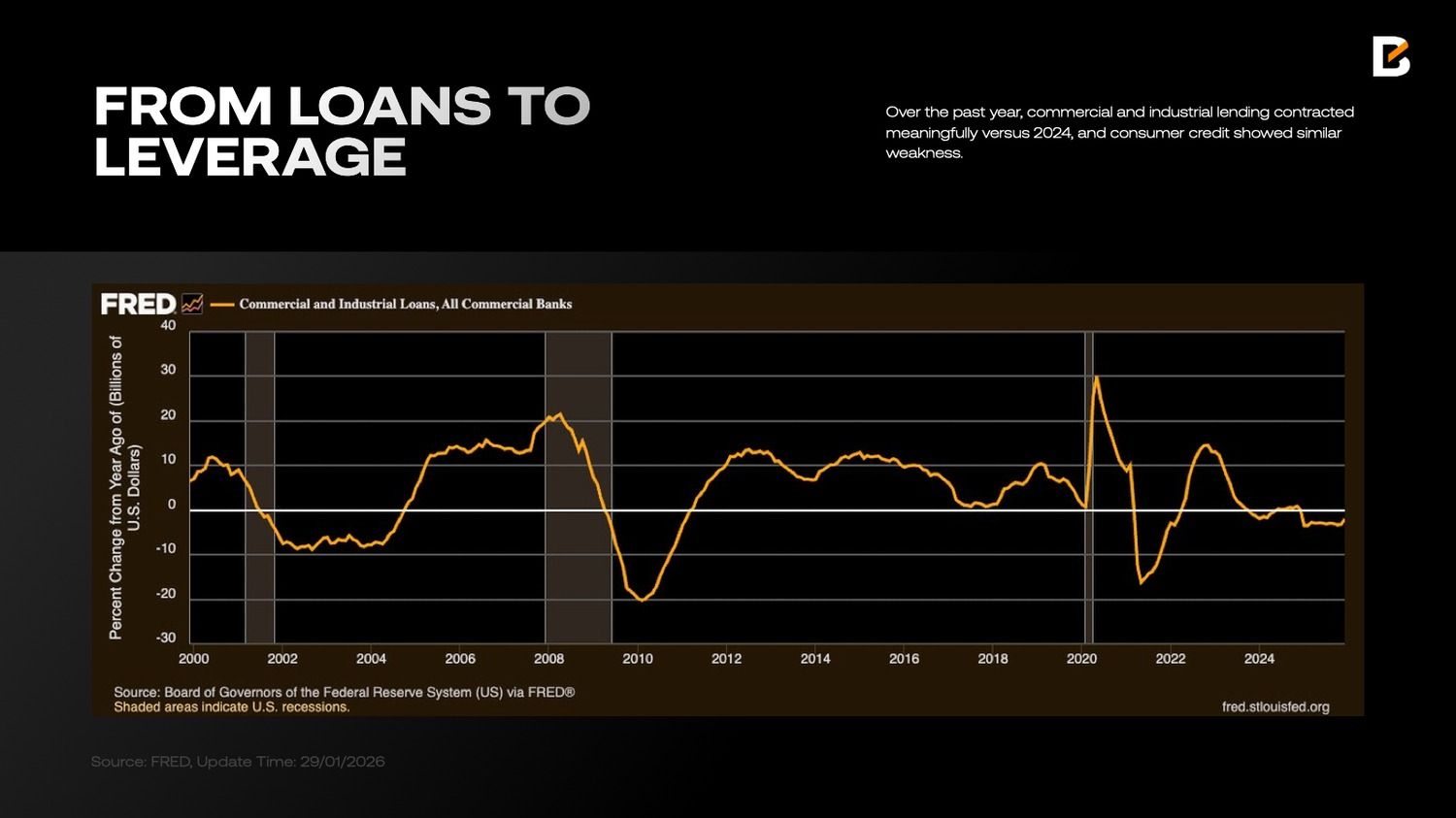

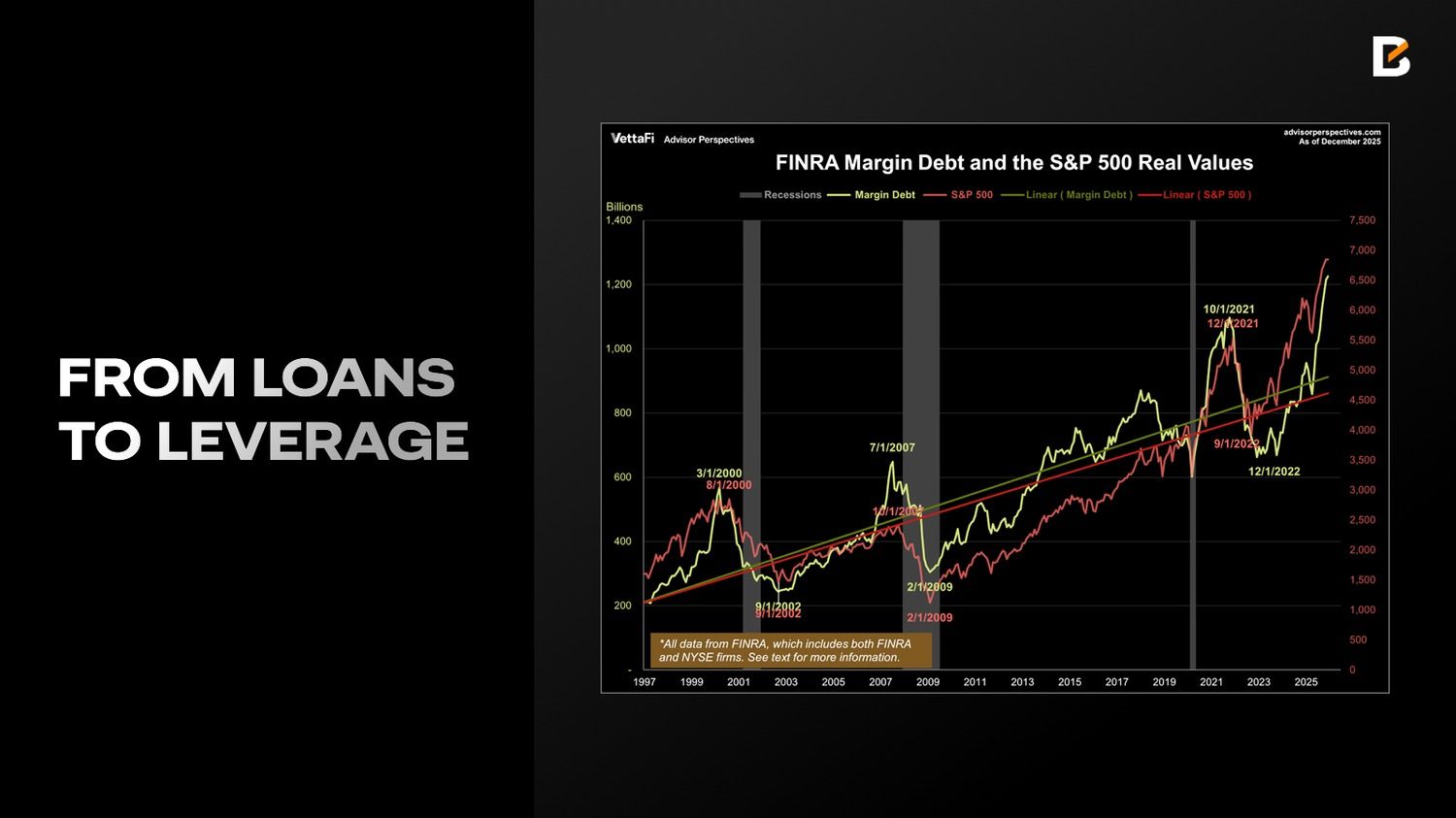

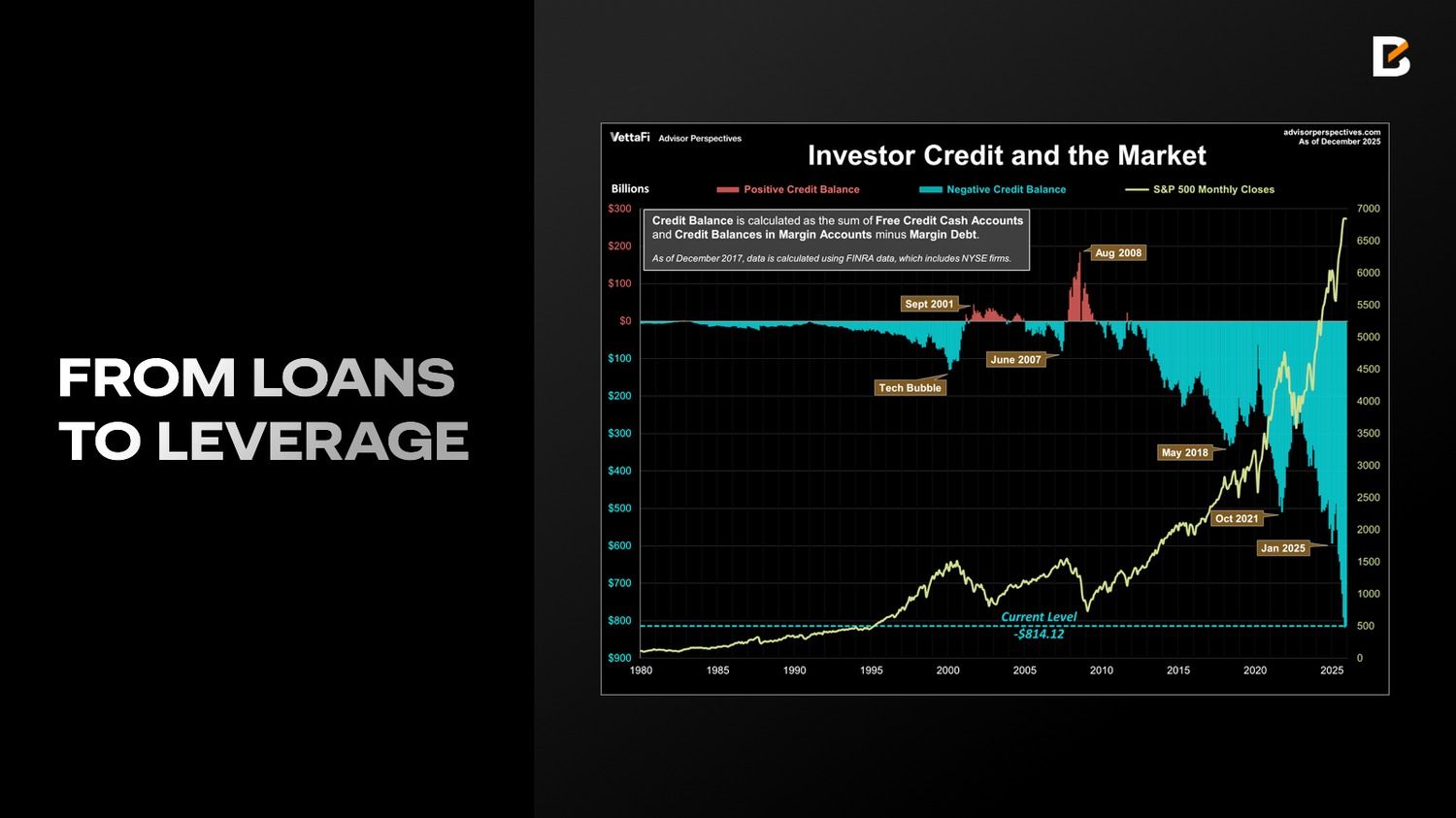

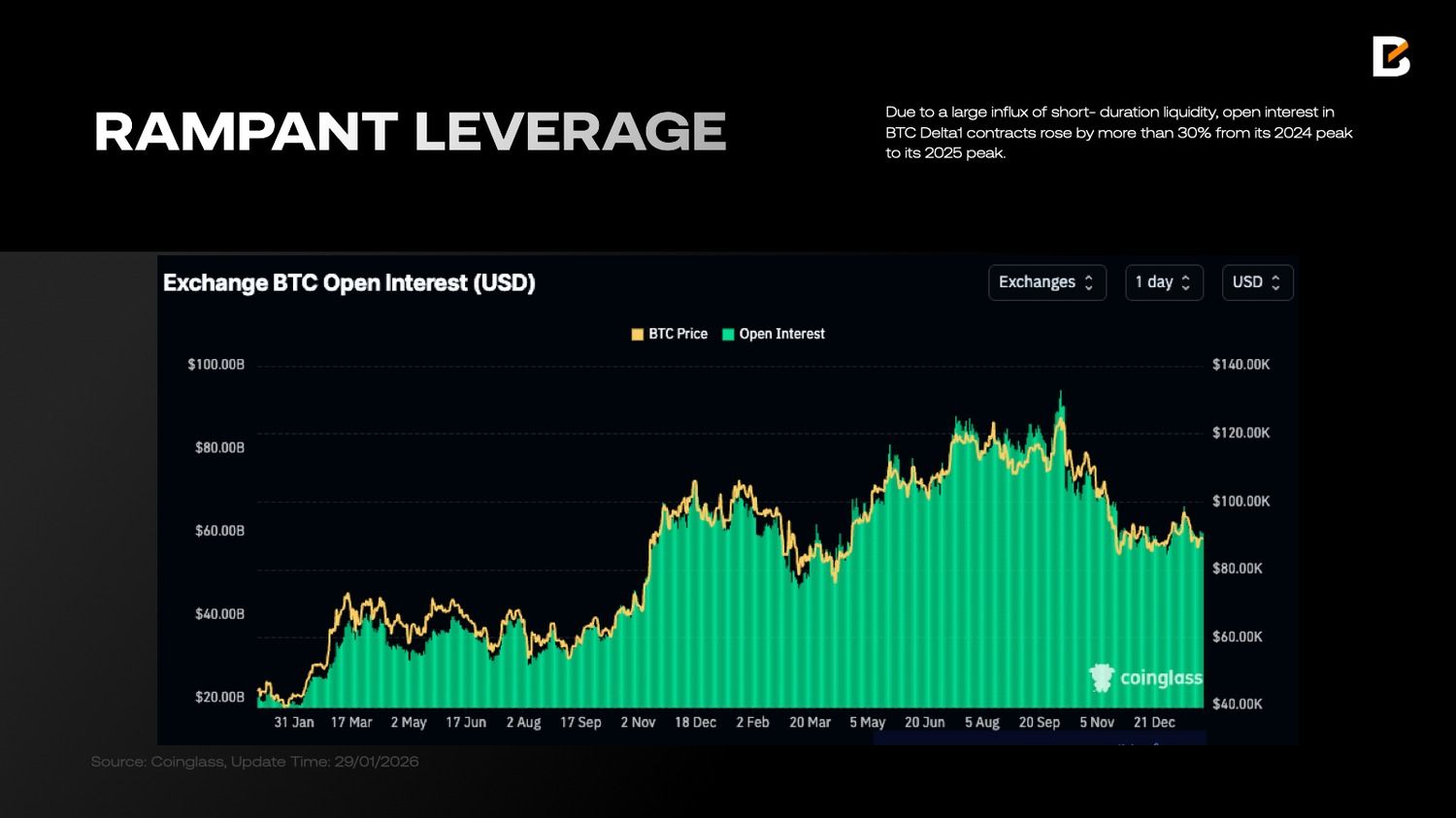

Over the past year, commercial and industrial lending contracted meaningfully versus 2024, and consumer credit showed similar weakness. By contrast, VettaFi data suggest that margin debt rose 36.3% over the past year, reaching an all-time high of $1.23T in December 2025, while investors’ net debit balances also expanded to $ -814.1 billion—broadly matching the pace of margin debt growth.

As liquidity requirements grow to push markets higher, the banking system is showing signs of strain, and demand for short-term funding has increased. The fix is straightforward: either reduce margin lending and pull liquidity back, or obtain liquidity support from the Fed and the repo market.

For the economy as a whole, the first option is preferable—lower system-wide leverage and strengthen resilience in banks and the financial system—but it would also imply lower valuations and a sharp equity sell-off. Given the midterm-election backdrop, the White House is unlikely to accept that path.

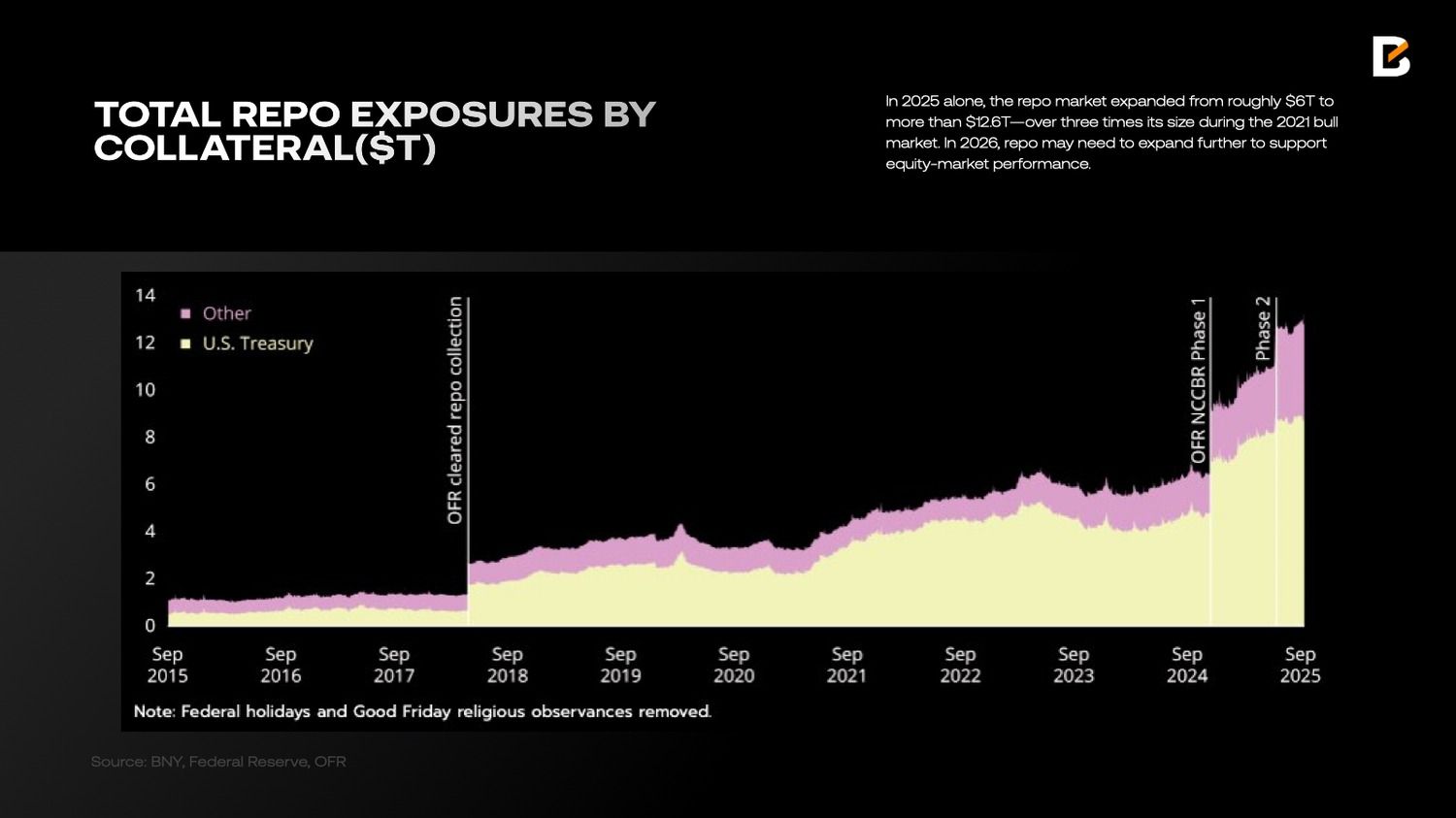

As a result, in 2025 alone, the repo market expanded from roughly $6T to more than $12.6T—over three times its size during the 2021 bull market. In 2026, repo may need to expand further to support equity-market performance.

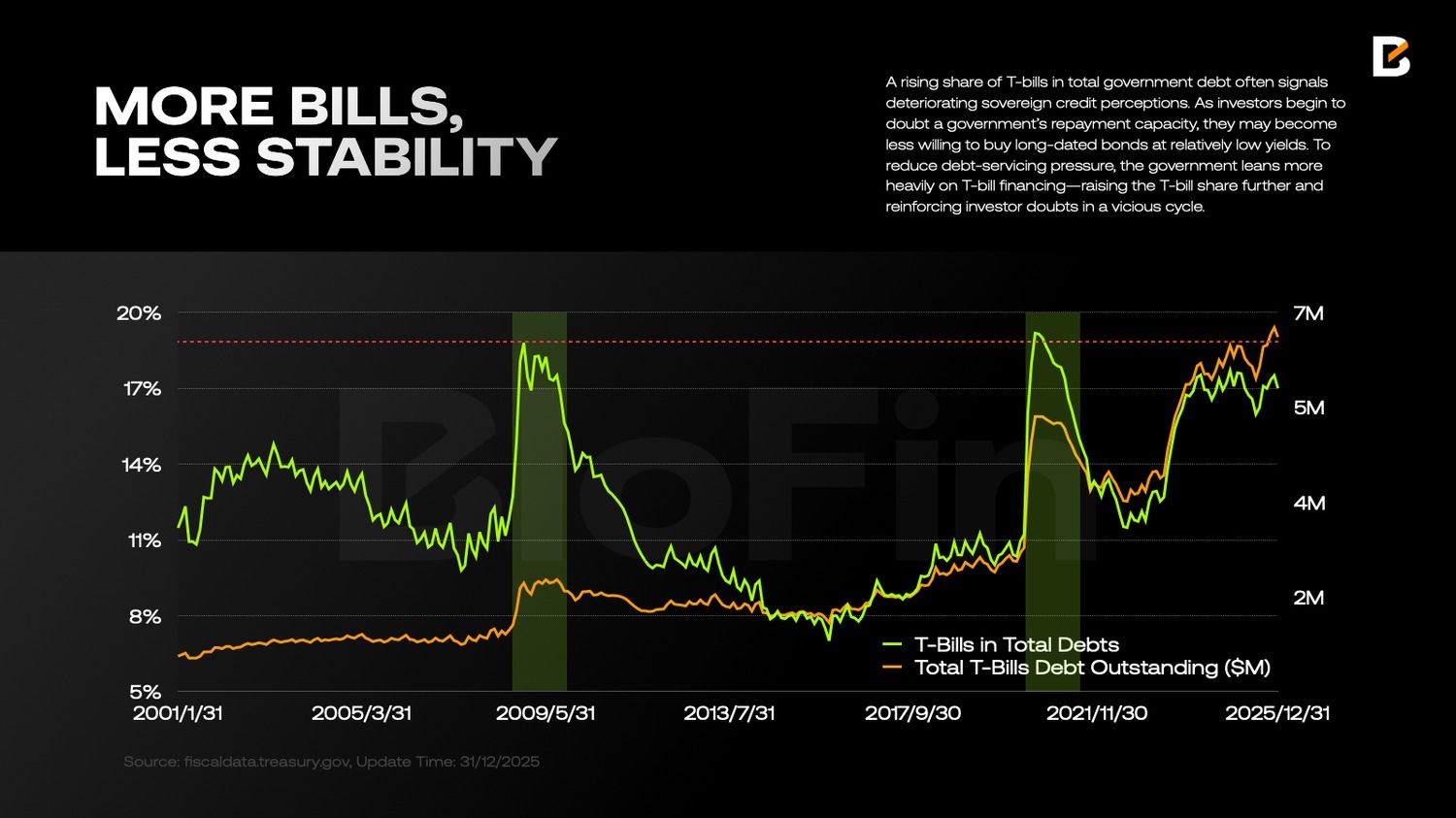

Repo transactions typically use US Treasuries—“high-quality assets”—as collateral. Historically, Treasury notes (T-notes) have been the most important form of collateral. But since mid-2023, that has changed, in part because the issuance and outstanding stock of Treasury bills (T-bills) has increased in an “exponential” fashion.

This is not benign: a rising share of T-bills in total government debt often signals deteriorating sovereign credit perceptions. As investors begin to doubt a government’s repayment capacity, they may become less willing to buy long-dated bonds at relatively low yields.

To reduce debt-servicing pressure, the government leans more heavily on T-bill financing—raising the T-bill share further and reinforcing investor doubts in a vicious cycle.

A higher T-bill share has another consequence: liquidity dynamics become less stable. Since a large portion of the liquidity supporting equities is channelled via repo, a greater reliance on T-bills implies more frequent rollovers and a shorter average liquidity “life”.

With overall leverage and margin debt already pushing beyond historical peaks, more frequent and more violent liquidity swings weaken the market’s shock-absorption capacity—setting the stage for potential cascading liquidations and large price moves.

In short: the quality of USD liquidity deteriorated markedly in 2025, with no clear sign of improvement so far.

So, in this macro context, how have investors’ expectations and portfolios changed?

Risk Premia and “Strict Diversification”

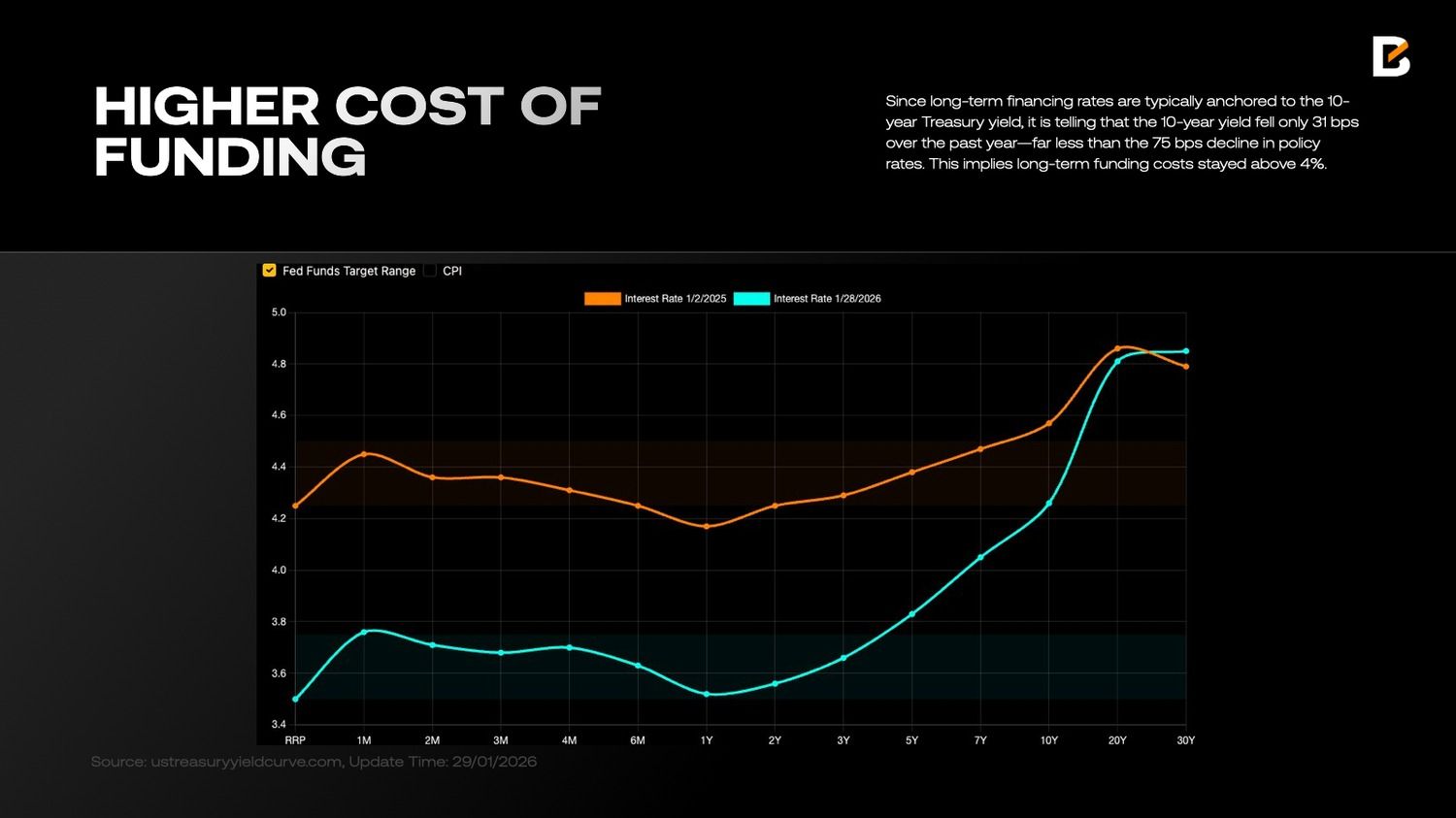

One cost of poorer-quality USD liquidity is that USD-based long-term funding costs remain elevated. This is intuitive: as USD asset markets become more fragile, US Treasury debt expands sharply (reaching USD 38.5 trillion by December 2025), and US fiscal, monetary and foreign policy turn more uncertain and less predictable, the perceived probability of systemic risk rises over time—prompting long-term Treasury investors to demand greater compensation.

Since long-term financing rates are typically anchored to the 10-year Treasury yield, it is telling that the 10-year yield fell only 31 bps over the past year—far less than the 75 bps decline in policy rates. This implies long-term funding costs stayed above 4%.

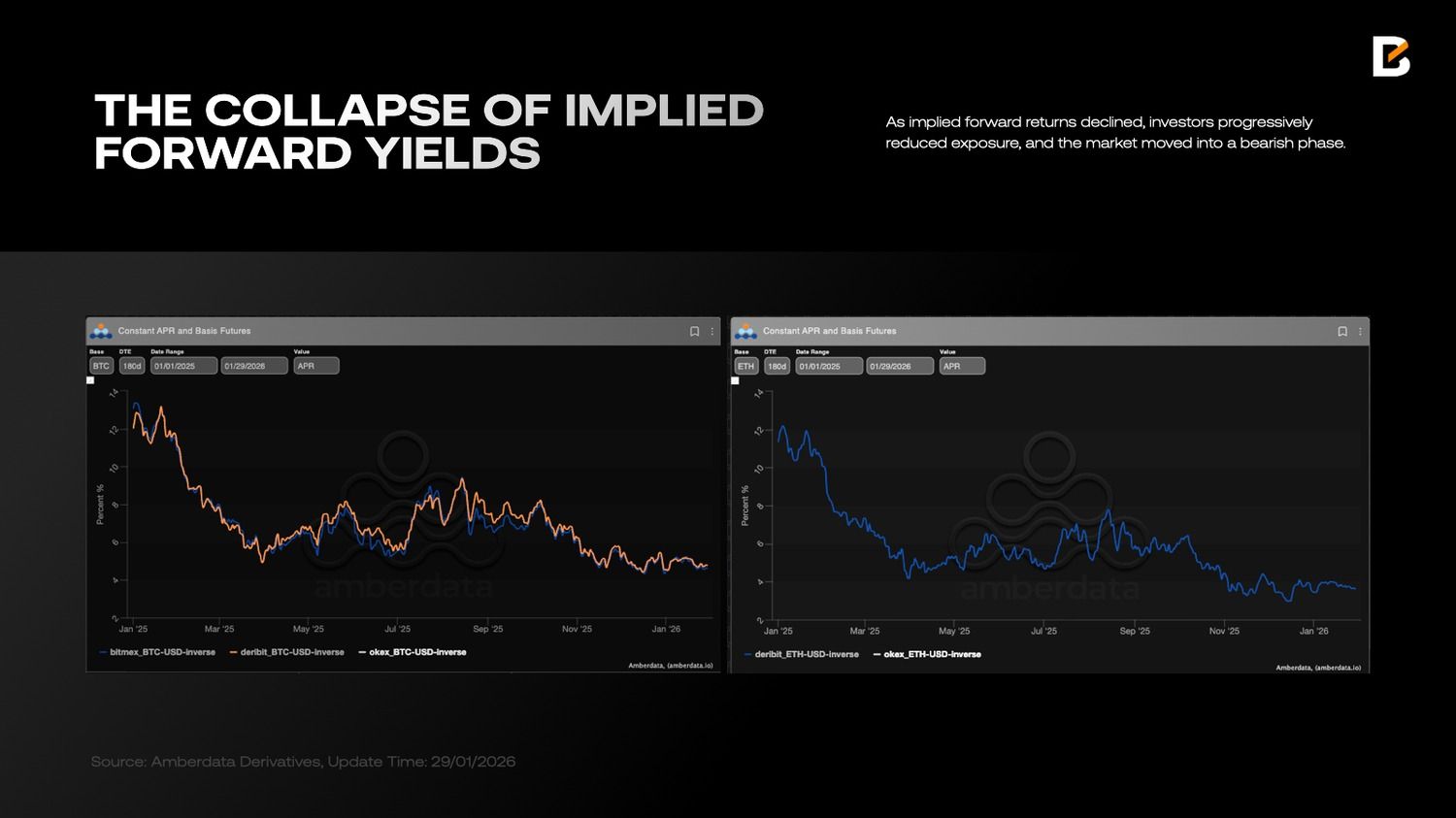

High funding costs constrain positioning. When a risk asset’s implied forward return falls below Treasury yields, holding that risk asset long-term becomes unattractive. Crypto is a textbook example: as implied forward returns declined, investors progressively reduced exposure, and the market moved into a bearish phase.

Compared with expensive long-term liquidity, short-term liquidity funded via T-bills is materially cheaper. But T-bill funding is also short-duration, creating an environment naturally favourable to speculation: investors can borrow short, apply high leverage, push prices up quickly and exit. Markets may look buoyant in the short run, but speculative froth makes rallies difficult to sustain—something clearly visible in the liquidity-sensitive crypto market.

Meanwhile, after decades, “strict diversification” made a comeback in 2025. Unlike the traditional 60/40 approach, liquidity has been spread across a broader set of instruments rather than confined to USD assets.

In fact, throughout 2025, investors steadily reduced the share of USD and USD-pegged assets in portfolios. Although persistent net outflows did not visibly hit US equities, incremental liquidity was allocated more heavily to non-US markets.

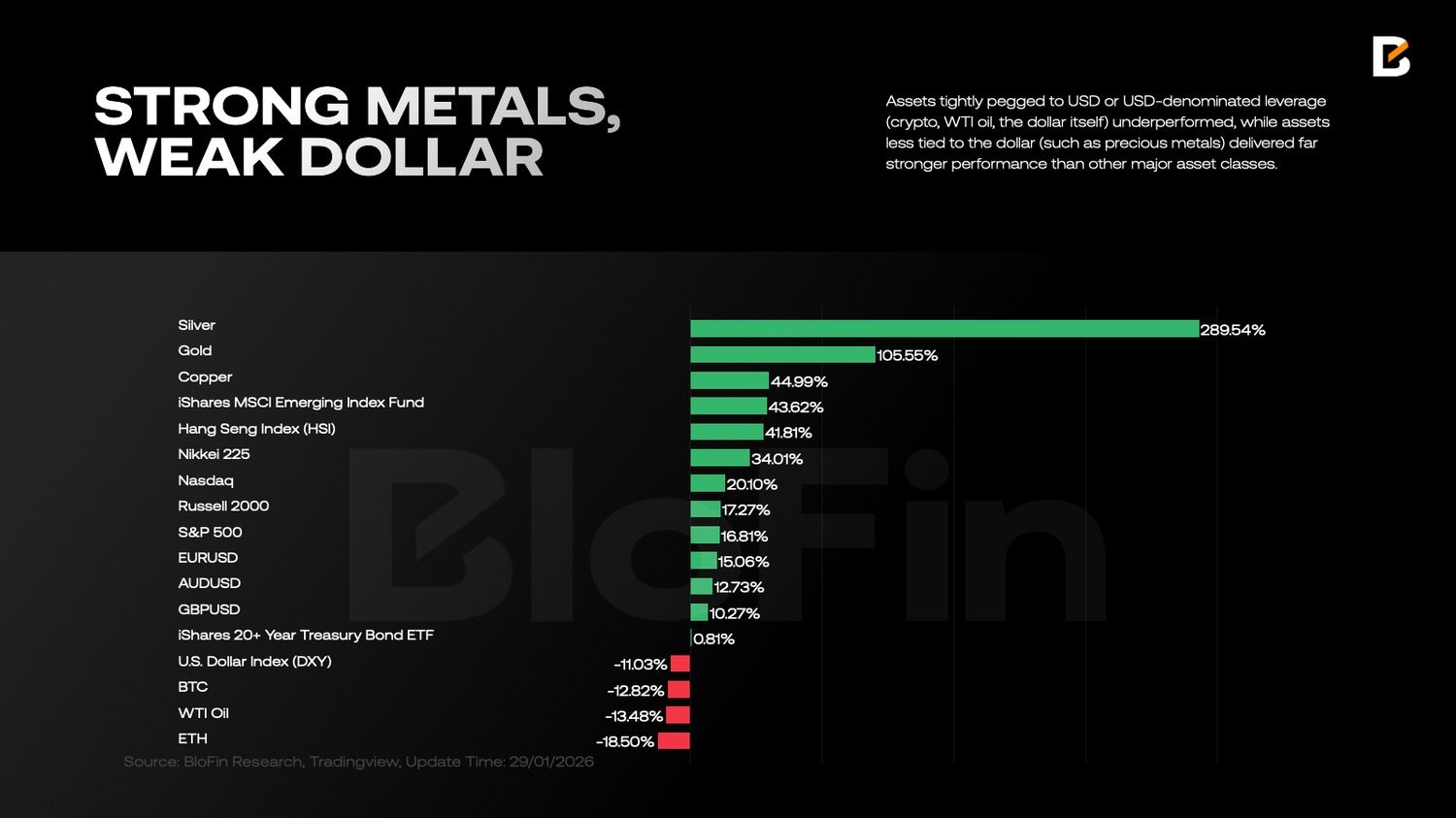

Assets tightly pegged to USD or USD-denominated leverage (crypto, WTI oil, the dollar itself) underperformed, while assets less tied to the dollar (such as precious metals) delivered far stronger performance than other major asset classes.

Notably, simply holding euros or Swiss francs performed no worse than holding the S&P 500. This suggests a profound shift in investor logic—one that goes beyond a single business cycle.

The New Order

What most deserves reassessment in 2026 is not a linear question like “will growth be stronger?”, but rather the fact that markets are adopting a new pricing grammar. Over the past two decades, returns often rested on two implicit assumptions: first, supply chains were organised around maximum efficiency, suppressing costs and stabilising inflation; second, central banks provided powerful backstops during crises, systematically compressing risk premia.

Both assumptions are now weakening. Supply chains increasingly prioritise control and redundancy; fiscal and industrial policy appears more frequently in profit models; and geopolitics has shifted from tail risk to constant noise. “Regionalisation” is less a slogan than a change in the constraint set facing the global economic system.

In this framework, the key is not to bet on a single direction, but to realign exposures to three more reliable “hard variables”: supply constraints, capital expenditure, and policy-driven order flow.

Together, they point towards a set of assets: commodity-linked equities, the AI infrastructure chain, defence and security themes, and select non-US markets that improve portfolio correlation structures. At the same time, the core question in rates and government bonds is no longer “how much tailwind will rate cuts bring?”, but how the new term structure reshapes the distribution of returns.

Regionalisation: Not “Decoupling”, but a New Cost Function

Equating “regionalisation” with “full decoupling” tends to understate its true impact. A more accurate description is that globalisation’s objective function has shifted from “efficiency at all costs” to “efficiency under security constraints”.

Once security becomes a binding constraint, many variables that previously sat outside valuation models—supply-chain redundancy, energy security, access to critical minerals, export controls on key technologies, and the rigidity of defence budgets—begin to enter discount rates and earnings expectations in various forms.

This produces two direct consequences for asset pricing. First, risk premia become less likely to revert to structurally low levels: political and policy uncertainty becomes an everyday variable, and markets require greater compensation. After all, nobody wants to bear “Cuban equity risk”, and today, even in US equities, that “Cuban equity risk” is no longer zero.

Second, global beta explains less, while regional alpha matters more: under different blocs and policy functions, the same growth and the same inflation can produce very different valuations and capital flows. For allocators, diversification in the age of regionalisation looks less like splitting assets evenly by country and more like diversifying across supply-chain position and policy elasticity.

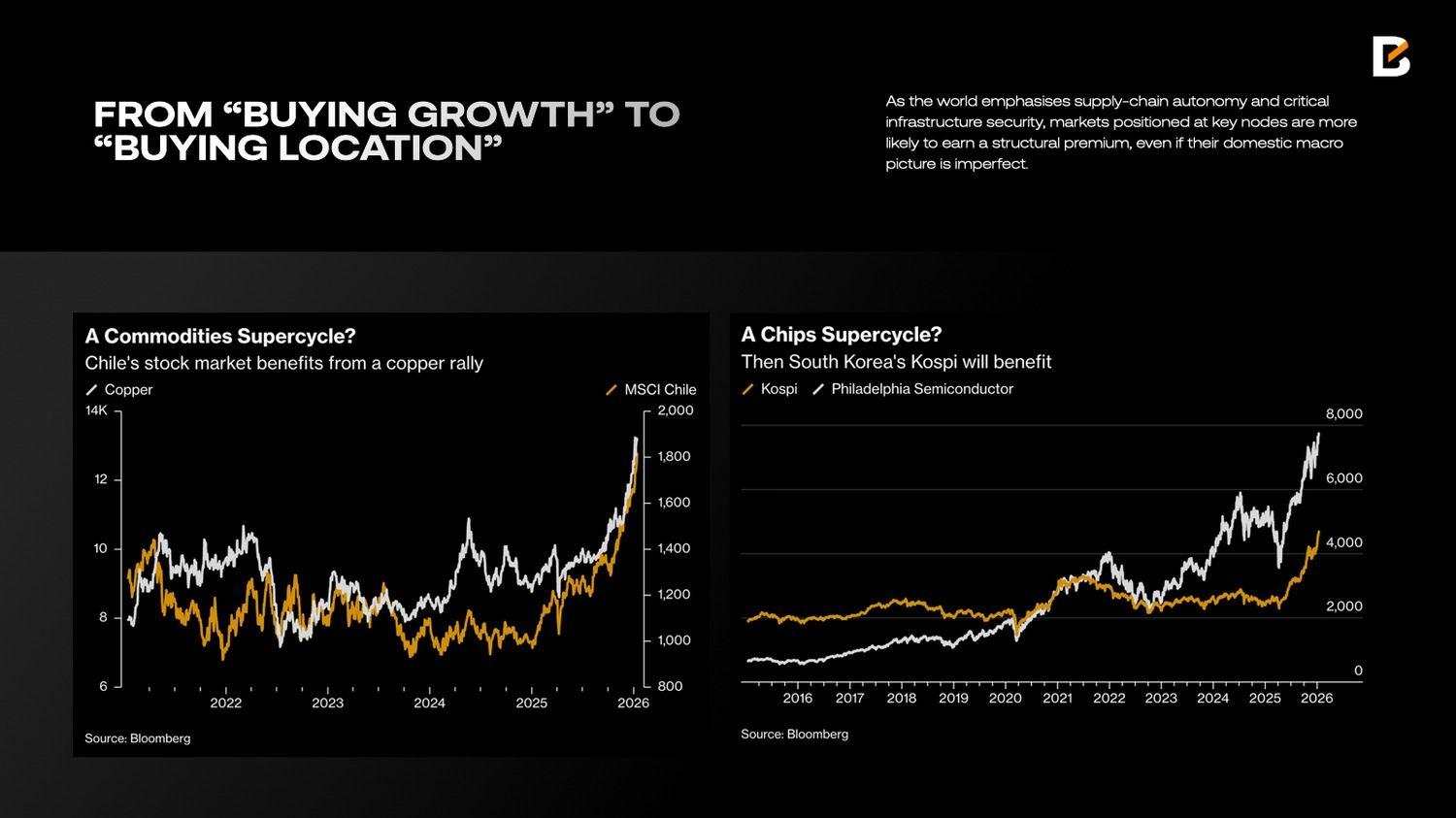

Equities: From “Buying Growth” to “Buying Location”

If 2010–2021 equity allocation was largely about “buying growth and falling discount rates”, 2026 is more about “buying location”. “Location” refers to where a market sits on three maps: the resource map, the compute map and the security map. As the world emphasises supply-chain autonomy and critical infrastructure security, markets positioned at key nodes are more likely to earn a structural premium, even if their domestic macro picture is imperfect.

In an era where security is the top priority, increasing inventories of gold, silver, copper and other non-ferrous metals can be rational even if they are not immediately needed. Supply chains can be disrupted without warning (as last year’s trade tensions showed), sharply raising costs and forcing major countries to hold larger mineral reserves against potential shocks.

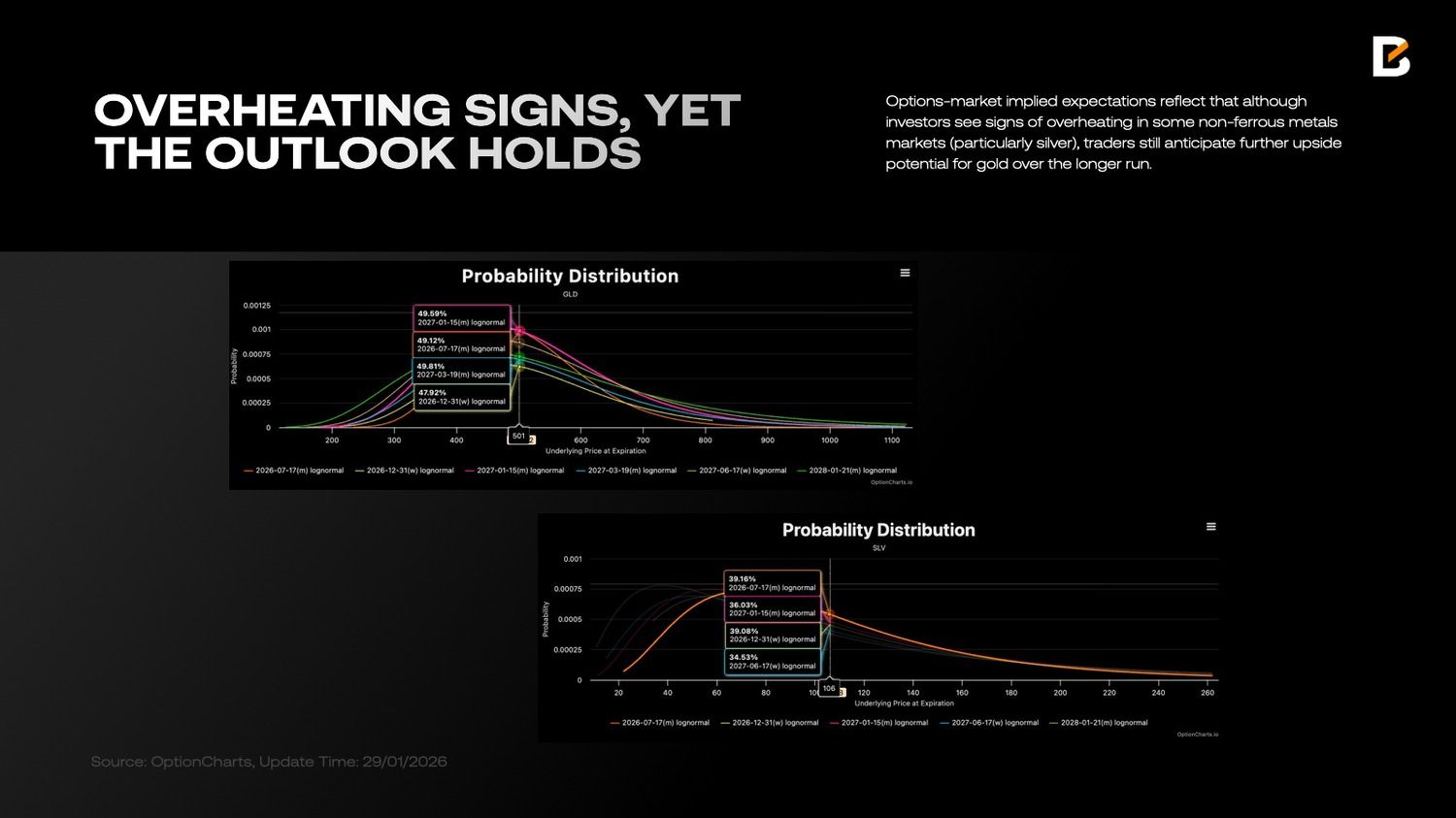

Structurally rising demand for critical minerals, combined with long-cycle supply constraints, makes commodities behave more like “supply-side assets” than mere mirrors of the traditional business cycle. Options-market implied expectations reflect this: although investors see signs of overheating in some non-ferrous metals markets (particularly silver), traders still anticipate further upside potential for gold over the longer run.

This logic also provides a clearer allocation case for equities in resource-rich countries. Copper-linked equities—Chile is a prime example—partly reflect foundational shifts in electrification and in demand for industrial infrastructure.

Precious-metals resource equities—South Africa is a typical case—combine commodity upside with the double-edged nature of risk premia: when commodities rise, profits and the currency may reinforce each other; when risk rises, politics and external financing conditions can amplify volatility. For portfolio construction, resource-country equities are better understood as a “supply-constraint factor” than simply emerging-market beta.

Another central theme is AI. AI discussions are easily pulled towards application-layer narratives, but allocators should focus on balance-sheet realities: compute, energy, data centres, networks, and cooling. These links share two traits: higher capex visibility and often benefit from joint support from policy and industry.

Rather than treating AI as another software-valuation game, it may be more robust to view it as a new wave of infrastructure build-out. Higher compute density ultimately translates into greater power and engineering demand, shifting more of the return distribution upstream and into midstream “real-economy” segments.

Under regionalisation, computing infrastructure is also spreading geographically. Higher security redundancy and localisation requirements increase the strategic value of key hardware and intermediate goods.

Markets such as Korea, positioned at the industrial interface of global compute infrastructure via semiconductors and critical electronics, are often seen as more direct equity expressions of the AI capex cycle. For portfolios, the value of this exposure is not only “faster growth”, but “more observable capex and more stable policy support”.

In addition, “defence and security” has returned to investors’ agendas for the first time since the end of the Cold War. Influenced by Trump’s “Donroeism” and the Russia–Ukraine war, both the US and Europe are placing defence higher on the priority list.

The distinctive feature of defence assets is that demand does not come from marginal household consumption; it is closer to a fiscal function constrained by national security. Once budgets step up, the political resistance to reversing them is greater, so order visibility is typically stronger. This gives defence-related equities a more defensive allocation role in a regionalised world: when conflict and sanctions risk rise, they can add resilience at the portfolio level.

That said, defence-sector price sensitivity often runs ahead of fundamentals: event-driven repricing followed by mean reversion is common. A more robust framing is to treat it as a portfolio “tail insurance” or risk-hedging factor, rather than a linear-growth core holding. Its value lies in reducing drawdowns, not in guaranteeing outperformance every quarter.

Hong Kong equities and mainland China assets are another area worth considering. Labelling them simply as “cheap” is insufficient; their allocation value stems from two factors. First, pricing often bakes in pessimistic expectations early, leaving room for rebalancing.

Second, their policy function and sector composition differ from those of US and European assets, potentially improving portfolio correlation structure. In the age of regionalisation, correlations do not automatically fall; they can rise during risk events. Structurally different assets can therefore provide more meaningful hedging.

Rates and Treasuries: Keep the Curve Steepening

The core tension in 2026 rates markets can be summarised in one line: the front end is more a function of the policy path, while the long end is more a container for term premia.

Rate-cut expectations do help front-end yields decline, but whether the long end follows depends on whether inflation tail risks, fiscal supply pressure and political uncertainty allow term premia to keep compressing. In other words, long-end “stubbornness” may not mean markets have mispriced the number of cuts; it may mean markets are repricing long-run risk.

Supply dynamics amplify this structural difference. Changes in US fiscal funding composition directly affect supply–demand across maturities: the front end is easier to absorb when money markets have capacity. In contrast, the long end is more prone to pulse-like volatility driven by risk budgets and term premia.

The portfolio implication is clear: duration exposure should be managed in layers, avoiding a one-path bet on “inflation fully disappearing and term premia returning to ultra-low levels”. Curve-structure trades (for instance, steepening strategies) persist not merely because of superior trading skill, but also because they align with the different pricing mechanisms of the front and long ends.

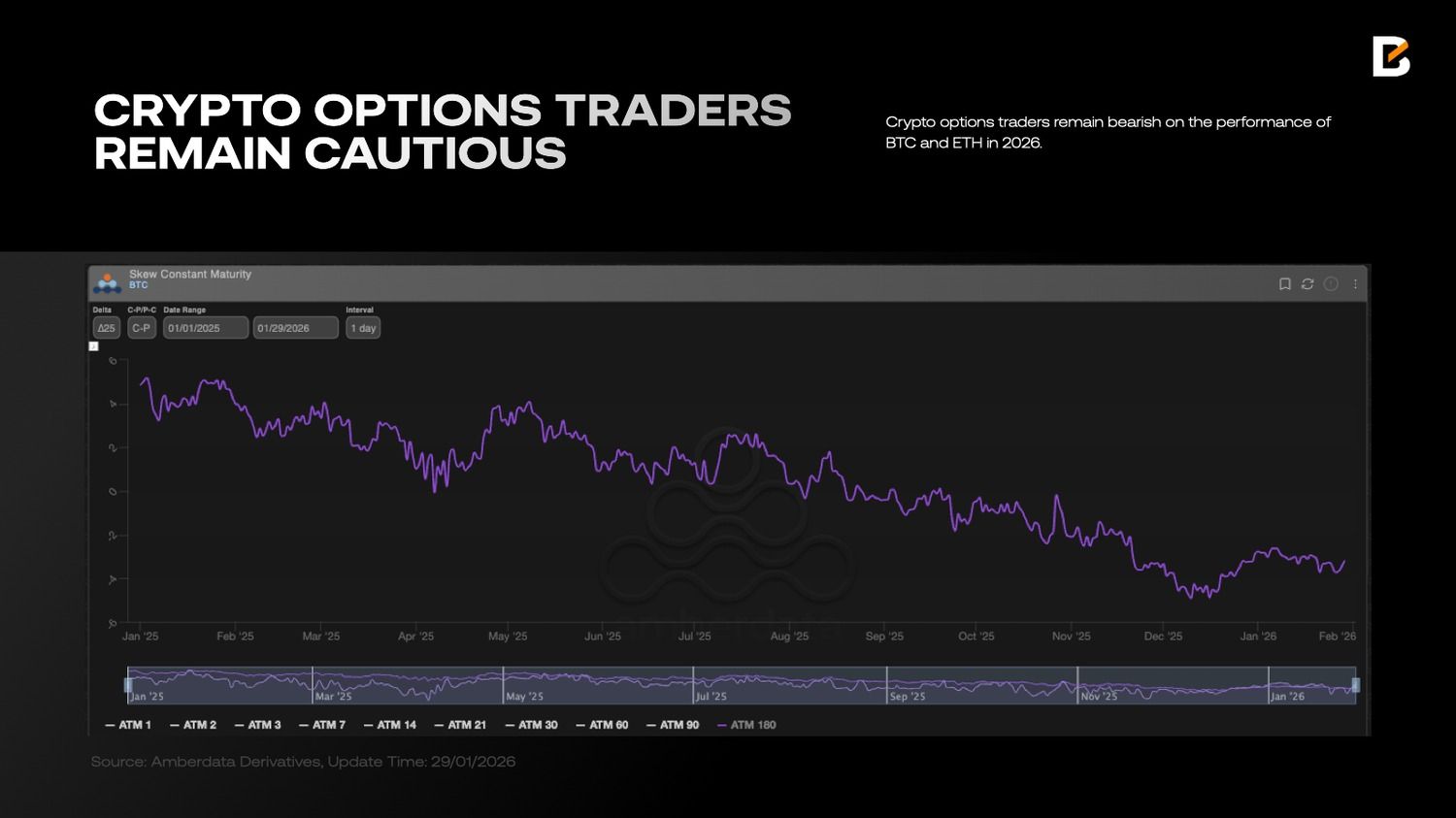

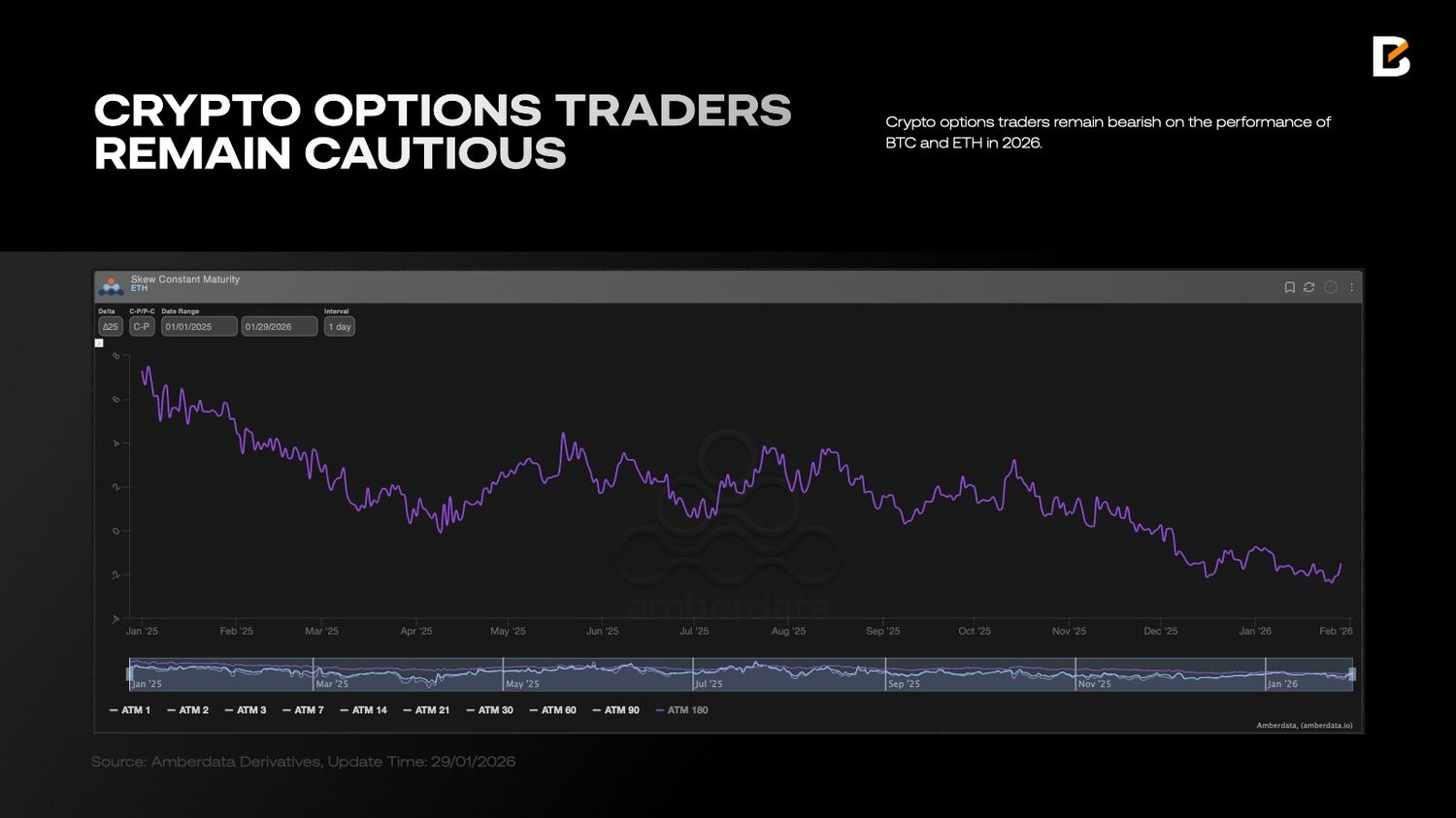

Crypto: Separate Accounting for “Digital Commodities” and Secondary Risk Assets

In 2026, the key for crypto is not simply “will it rise?”, but sharper internal differentiation. Bitcoin is more readily understood as a non-sovereign, rules-based supply asset that is portable across borders—a “digital commodity”. Under a regionalisation narrative, it is more likely to absorb demand for alternative payment systems and hedges.

By contrast, a subset of tokens that behave more like equity-style risk assets are priced more on growth stories, ecosystem expansion and risk appetite. When risk-free yields remain attractive, regulation becomes clearer, and traditional capital markets offer more mature funding and exit channels, equity-like tokens must offer higher risk compensation to justify allocation.

As a result, crypto allocation is better approached via “separate books” rather than a single basket: place bitcoin in a commodity/alternative-asset framework, using small weights to obtain portfolio-level convexity; treat equity-like tokens as high-volatility risk assets with stricter return hurdles and clearer risk budgets. The core of the regionalisation era is not to embrace every new asset, but to identify which assets remain more explainable under the new constraints.

Use Hard-Constraint Assets as the Core, Use Structural Divergence as the Return Engine

Putting the above together, a 2026 portfolio looks more like managing a set of “hard constraints”: supply constraints restore the strategic role of commodities and resource equities; capex supports earnings visibility across the AI infrastructure chain; policy-driven orders enhance the resilience of defence and security; the return of term premia reshapes the distribution of duration returns; and select non-US assets provide reflexive hedging through valuation structure and policy functions.

This does not require perfect prediction of every event. On the contrary, the rarest skill in the age of regionalisation is to place the portfolio in a position that relies less on flawless forecasting: let hard assets and infrastructure absorb structural demand; let curve structures absorb structural divergence; and let hedging factors absorb structural noise.

Trading in 2026 is no longer about “guessing the answer”, but about “acknowledging constraints”—and rewriting asset-allocation priorities accordingly.

Disclaimer: The information provided herein does not constitute investment advice, financial advice, trading advice, or any other sort of advice, and should not be treated as such. All content set out below is for informational purposes only.

Is SOL headed toward $50?

The cryptocurrency market seems to can’t catch a break lately, and numerous digital assets continue to chart painful losses.

Solana (SOL) is among the poorest performers, with its price plunging by 25% in the past week alone. According to some market observers, the bears might be just stepping in.

Major Collapse on the Horizon?

Just hours ago, SOL tumbled to approximately $95, its lowest level since February 2024. As of this writing, it trades at around $96, which is a staggering decline from the all-time high of almost $300 registered nearly a year ago.

Many industry participants are now concerned that the asset may experience a further decrease in the short term. Ali Martinez, for instance, predicted that SOL could nosedive to $74.11 and even $50.18.

The analyst, going on X as curb.sol, outlined $100 as an “extremely important level” for the token. In their view, holding that zone could result in a new bull run to a fresh all-time high, whereas the opposite scenario might lead to a crash to roughly $50 sometime this year.

For their part, Alex RT₿ assumed the price may retreat to $70-$80 if SOL breaks below the $90 support level.

Any Chance for the Bulls’ Return?

It is important to note that some analysts believe the current rates could present great buying opportunities. The one using the X handle, Lucky, told their almost two million followers that “if the market behaves well, this could be a smart entry.”

You may also like:

“Opportunities like this don’t show up often,” they added.

Mookie also recently chipped in, vowing to go all-in should SOL drop below $100.

if $SOL drops below $100 i’m going all in

Solana at $100 is def free pic.twitter.com/ORftQMa2dv

— Mookie (@MookieNFT) January 31, 2026

Meanwhile, some key indicators suggest it might be time for a rebound. SOL’s Relative Strength Index (RSI) fell well below 30, meaning the price has declined too much in a short period of time. Ratios under that level signal that SOL is oversold and due for a potential rally, whereas anything above 70 is seen as bearish territory.

Furthermore, exchange outflows have significantly surpassed inflows in the past several weeks. This suggests that investors have shifted from centralized platforms to self-custody, thereby reducing immediate selling pressure.

SECRET PARTNERSHIP BONUS for CryptoPotato readers: Use this link to register and unlock $1,500 in exclusive BingX Exchange rewards (limited time offer).

A leaked dataset of 149M stolen credentials reportedly includes login details for around 420,000 Binance accounts.

A trove of 149 million stolen credentials, including login details for 420,000 Binance accounts, was discovered circulating among cybercriminals this week.

The findings highlight a shift in crypto theft toward long-term malware infections that steal data directly from users’ devices, often long before any funds are moved.

The Scale of the Threat

According to an alert posted on February 4 by security firm Web3 Antivirus, the dataset was compiled from information-stealing malware installed on victim devices. Beyond exchange logins, the stolen data included passwords, private keys, API keys, and browser session tokens for email, social, and financial platforms.

The firm noted that these “infostealers” capture data that can later be used for account takeovers and fund theft, emphasizing that prevention requires early detection at the device level since by the time suspicious activity appears on-chain, it is often too late.

Furthermore, in a separate series of posts, Web3 Antivirus detailed how malicious AI skills on platforms like ClawHub are being used to steal crypto data. Per the security firm, these fraudulent skills, posing as wallet tools or trading bots, install information-stealing malware that can remain dormant until a victim’s crypto balance grows or specific actions are taken. This vulnerability represents a supply-chain risk that moves upstream “from wallets to the tools people trust to manage them.”

A Persistent Challenge for Users and Platforms

The gravity of losses resulting from crypto theft cannot be understated. A recent report from PeckShield noted that scams and hacks drained over $4.04 billion in 2025, with scams alone jumping 64% year-over-year. The firm observed a move toward targeting centralized exchanges and large organizations, which accounted for 75% of stolen funds in 2025.

Meanwhile, Web3 Antivirus put the volume of 2025’s illicit crypto activity at approximately $158 billion, up from $64 billion in 2024. While the on-chain security provider partly attributed the increase to better tracking and more state-linked activity, the figures show that even small success rates for thieves can result in large losses at scale.

You may also like:

The recent data thefts highlighted a gap between user and platform protection, with the company stating,

“Scams don’t succeed because users ignore advice; they succeed because risk is only surfaced after execution is already possible.”

The firm argued that platforms, which can see transaction approvals and behavioral patterns before users do, sit at “the last real control point” for preventing theft.

One of the more common attack vectors is wallet drainers, which Web3 Antivirus stated had gotten worse, with 15,530 suspicious approvals across 11,908 wallets leading to $4.25 million in losses in January. These drainers usually enter through malicious transaction approvals, making pre-signature detection extremely important.

SECRET PARTNERSHIP BONUS for CryptoPotato readers: Use this link to register and unlock $1,500 in exclusive BingX Exchange rewards (limited time offer).

The CLARITY Act debate has largely revolved around the tug-of-war between banks and crypto firms over stablecoin yield. While that conflict dominates coverage of what is framed as a market-structure bill, it obscures a quieter and potentially more consequential issue.

Once enacted, the CLARITY Act would formally legitimize regulated crypto roles and implicitly subject them to Bank Secrecy Act compliance. Even without explicit mandates, this risks entrenching a surveillance-first model that pressures intermediaries to delist privacy assets and abandon privacy-by-design before Congress has openly debated the trade-offs.

Sponsored

Sponsored

Banks Join Talks on Stablecoin Yield

On Monday, industry insiders met with advisors to US President Donald Trump to explore potential compromises in a still-contentious market structure bill.

The discussions were led by Patrick Witt, executive director of the President’s Council of Advisors on Digital Assets. The roundtable included senior figures from both the crypto sector and traditional banking.

The meeting reignited tensions between the crypto sector and traditional finance.

Critics questioned why policymakers invited Wall Street to help shape legislation governing products that directly compete with its core business. Chief among these are yield-bearing stablecoins, which many view as a direct threat to traditional bank deposits.

However, the meeting also allowed a far subtler, yet equally significant issue to slip largely unnoticed: privacy.

Sponsored

Sponsored

How CLARITY Pulls Crypto Under the Bank Secrecy Act

The CLARITY Act presents itself as a market structure framework that promises regulatory certainty for the US crypto industry. It aims to clearly assign activities to regulators and deliver long-sought legal clarity to market participants.

Yet, the bill does more than draw jurisdictional boundaries.

By formally defining regulated crypto roles, particularly for centralized exchanges and stablecoin issuers, it embeds these actors within the existing financial system.

Once those roles are legally recognized, compliance with the Bank Secrecy Act (BSA) becomes effectively unavoidable, even though the legislation does not specify how BSA requirements should apply to on-chain activity.

That lack of specificity hands key decisions to intermediaries, who would set the rules instead of Congress.

Sponsored

Sponsored

In response, exchanges and custodians default to expansive identity checks, sweeping transaction monitoring, and heightened data collection. In doing so, they establish de facto standards without a clear legislative mandate.

Within this framework, privacy-focused projects stand to bear the greatest cost.

Privacy Assets in the Line of Fire

The BSA requires financial institutions to verify customer identities and monitor for suspicious activity. In practice, this means knowing who customers are and reporting specific red flags to authorities.

Sponsored

Sponsored

What the law does not require is constant, system-wide transparency or the ability to trace every transaction back to an identity at all times.

Nonetheless, major crypto firms such as Binance, Coinbase, and Circle already operate as if it does. They equate BSA compliance with maximum on-chain visibility in order to minimize regulatory risk amid legal uncertainty.

This approach translates into strict traceability requirements and the avoidance of protocols that limit transaction visibility. Centralized exchanges typically refuse to list privacy-focused cryptocurrencies like Monero or Zcash, not because the BSA explicitly demands it, but as a precautionary measure.

As it stands, the CLARITY Act does not account for how the BSA should apply to blockchain systems where privacy and pseudonymity operate differently from traditional finance. That silence matters.

By leaving key obligations undefined, the CLARITY Act risks entrenching the most conservative, surveillance-heavy interpretation of the BSA as the default.

As a result, participants aligned with crypto’s cypherpunk roots are likely to be most affected, as privacy-oriented tools and services face the greatest restrictions.

TLDR

- UBS Group AG reported a sharp rise in net profit driven by strong client activity and cost efficiency.

- The bank maintained capital ratios well above regulatory requirements and reiterated confidence in its 2026 financial targets.

- UBS confirmed continued progress in integrating acquired Swiss accounts and winding down non-core assets.

- Despite the earnings beat, UBS shares declined nearly 5 percent after the results were announced.

- The decline followed cautious comments from UBS management regarding its timeline for crypto and tokenized asset offerings.

- CEO Sergio Ermotti stated that UBS will follow a fast follower approach instead of leading in digital asset innovation.

UBS Group AG delivered strong quarterly earnings, reporting higher net profit and capital returns, yet its shares dropped nearly 5% following the results, as investors recalibrated expectations for growth in digital assets. Despite positive performance metrics, the bank’s cautious approach to crypto and tokenized assets drew focus, overshadowing its earnings beat. Management confirmed a slow rollout of blockchain initiatives, which may have cooled sentiment among forward-looking investors.

UBS Group AG Reports Higher Profit and Strong Capital Ratios

UBS Group AG posted a surge in net profit, supported by firm client activity and solid capital positions. The bank reported higher returns on CET1 capital, reinforcing its message of stable and resilient balance sheet management. Profitability gains reflected progress in cost control and integration of acquired assets, especially in Swiss-booked businesses.

Trading activity remained robust, and client asset inflows continued across major segments during the quarter. UBS maintained capital ratios well above regulatory requirements, reinforcing its conservative financial approach. Management reiterated that 2026 targets remain on track, including plans for higher returns and improved efficiency.

The bank emphasized continued execution on its strategic roadmap, supported by disciplined risk management and sustained client engagement. UBS also confirmed further wind-down of non-core assets and steady progress on system integration. These operational improvements contributed to stronger fundamentals across the board.

Crypto Strategy Comments Drive Market Reaction

During the earnings call, CEO Sergio Ermotti addressed growing interest in crypto and tokenized asset offerings. He stated, “We are building core infrastructure but will not lead the market on this front.” The bank confirmed it would pursue a fast follower approach rather than immediate deployment of blockchain-based products.

UBS aims to offer crypto access to individual clients and tokenized deposit options to corporate customers. However, it set expectations that these developments will unfold over three to five years. Investors responded by reassessing near-term growth potential from digital assets.

The measured tone contrasted with some market hopes for faster adoption and monetization of crypto services. UBS positioned digital initiatives as long-term complements to its traditional offerings, not near-term revenue drivers. This divergence may have triggered a repricing of expectations around technology-led growth.

Strong Execution Overshadowed by Delayed Crypto Monetization

Despite delivering on financial targets, the stock declined after the report, reflecting market’s focus on future-facing initiatives. UBS delivered what it promised in capital returns, profits, and cost cuts, but offered no immediate digital catalyst. The gap between execution and investor enthusiasm over crypto timing became the central theme.

The selloff suggests the market sought faster signals on UBS’s role in tokenized finance. Although fundamentals remain firm, expectations around digital expansion weighed on investor sentiment. UBS’s conservative stance may align with its culture, but not with all shareholders’ timelines.

UBS emphasized long-term goals, targeting improved capital efficiency by 2028. Shareholder returns remain a core focus, with dividends and buybacks continuing. However, no accelerated plans were revealed for blockchain offerings.

Chicago-based derivatives exchange CME Group is examining how tokenized assets could reshape collateral and margin across financial markets, CEO Terry Duffy said during a recent earnings call. The conversations revolve around tokenized cash and a CME-issued token that could run on a decentralized network, potentially used by other market participants as margin. Duffy argued that the quality of collateral matters, suggesting that instruments issued by a systemically important financial institution would provide more confidence than tokens from smaller banks attempting to issue margin tokens. The comments signal a broader industry push to experiment with tokenized collateral as traditional markets increasingly explore blockchain-based settlement and liquidity tools.

Key takeaways

- CME Group is evaluating tokenized cash alongside a possible CME-issued token designed to operate on a decentralized network for margin purposes.

- Registry-style collateral could be favored if issued by systemically important financial institutions, rather than tokens from smaller banks.

- The discussion ties into a March collaboration with Google Cloud around tokenization and a universal ledger, indicating a concrete technical path for pilots.

- CME plans 24/7 trading for cryptocurrency futures and options in early 2026, subject to regulatory approval, reflecting a broader push toward continuous pricing and settlement.

- In parallel, CME has outlined growth in regulated crypto offerings, including futures tied to Cardano, Chainlink and Stellar, and a joint effort with Nasdaq to unify crypto index products.

Tickers mentioned: $ADA, $LINK, $XLM

Market context: The CME move comes as traditional banks and asset managers accelerate experiments with tokenized assets and stablecoins, while policymakers in the United States weigh regulatory frameworks for digital currencies and centralized versus decentralized settlement rails. The sector-wide trend includes both institutional pilots and ongoing regulatory scrutiny surrounding stablecoins and token-based payments.

Why it matters

The potential introduction of a CME-issued token or the broader use of tokenized collateral could redefine how institutions post margin and manage risk during periods of market stress. If a CME token were to gain traction among major market participants, it could provide a recognizable, regulated anchor for on-chain settlement workflows, potentially reducing settlement latency and settlement risk across a spectrum of asset classes. The emphasis on collateral quality—favoring instruments from systemically important institutions—helps address credibility concerns that have accompanied attempts by other entities to issue margin-related tokens in the past.

The development sits within a wider institutional push into tokenization and digital assets. Banks have been advancing their own experiments with tokenized cash and stablecoins to streamline cross-border payments and interbank settlements. For example, large banks have publicly discussed stablecoin exploration and related payment technologies, underscoring a broader demand for faster, more efficient settlement rails. Yet this momentum coexists with a regulatory push to address potential risks, coverage, and disclosure standards around tokenized instruments and stablecoins, including debates over yield-bearing stablecoins and the evolving legal framework in the CLARITY Act era.

Beyond the tokenization plans, CME’s broader crypto strategy—ranging from planned futures on leading tokens to a unified Nasdaq-CME Crypto Index—signals an intent to align traditional derivatives infrastructure with blockchain-enabled assets. The push toward 24/7 crypto derivatives trading marks a notable shift in market structure, as exchanges and market participants increasingly expect around-the-clock access to price discovery and settlement. The timing aligns with a confluence of industry experiments and policy discussions, creating a testing ground for tokenized collateral to become a practical, regulated element of mainstream finance.

What to watch next

- Regulatory clearances for 24/7 crypto derivatives trading expected in early 2026; approval status will shape CME’s execution timeline.

- Details on the CME-issued token’s design, governance, and interoperability with decentralized networks remain to be seen—watch for formal disclosures or filings.

- Progress of the Google Cloud-based Universal Ledger pilot for wholesale payments and asset tokenization; any case studies or results will inform practical feasibility.

- Updates on CME’s planned futures tied to Cardano (ADA), Chainlink (LINK) and Stellar (XLM) and how liquidity and risk controls will be implemented under the Nasdaq-CME alignment.

Sources & verification

- CME Group CEO Terry Duffy’s remarks on tokenized cash and potential CME-issued token during a Q4-2025 earnings call (Seeking Alpha transcript referenced in coverage).

- March press release announcing CME Group and Google Cloud’s tokenization initiative using Google Cloud’s Universal Ledger to enhance capital-market efficiency.

- Cointelegraph reporting on the CME-Google Cloud tokenization pilot and related technology discussions.

- CME’s January disclosures about expanding regulated crypto offerings with futures on Cardano (ADA), Chainlink (LINK) and Stellar (XLM) and the Nasdaq-CME Crypto Index integration.

- Regulatory context and policy discussions surrounding stablecoins and tokenization, including debates around the GENIUS Act and related rulemaking.

Key figures and next steps

Market participants will be watching for concrete technical details behind any CME-issued token, including how it would be stored, audited, and reconciled with existing collateral frameworks. The form and governance of a token designed for margin would influence whether such an asset could be widely adopted by clearing members and other systemically important institutions. As CME progresses its discussions with regulators and industry stakeholders, the potential for tokenized collateral to function as an accepted, high-credibility instrument will hinge on demonstrating robust risk controls, liquidity, and interoperability with existing settlement ecosystems.

Key figures and next steps

In the near term, observers should monitor updates on 24/7 crypto derivatives trading plans, potential regulatory approvals, and any incremental disclosures on how tokenized cash and a CME-issued token would be integrated into margin requirements. The collaboration with Nasdaq to unify crypto index offerings also merits close attention, as it could influence how institutional investors gauge exposure to digital assets in a standardized framework.

Why it matters (expanded)

For users and investors, the emergence of tokenized collateral could offer new pathways to manage liquidity and collateral agility, potentially reducing funding costs for participants who post margin across exchanges. For builders and platform teams, this trend underscores a need to design secure, auditable on-chain representations of traditional assets and to ensure that risk models and governance processes are aligned with regulated markets. For the market at large, CME’s exploration highlights how the line between on-chain assets and regulated, traditional finance is becoming more permeable, creating opportunities and challenges in equal measure.

What to watch next

- Regulatory approvals for 24/7 crypto derivatives trading anticipated in early 2026.

- Detailed disclosures on the CME-issued token’s architecture and governance in forthcoming filings or announcements.

- Milestones from the Google Cloud universal ledger pilot, including any pilot results or expansion plans.

CZ exposed a long-running fake account using AI-generated images to pose as a Binance supporter before spreading BNB-related FUD.

Changpeng “CZ” Zhao, the founder of Binance, has publicly identified and dismantled a coordinated misinformation campaign against him and the exchange.

CZ exposed a long-running fake account that apparently used AI-generated images to pose as a loyal supporter before posting critical “feedback.”

The Unraveling of a Fake Supporter

The incident began when CZ noticed a post from an account named “Wei 威 BNB” claiming to close a Binance account due to alleged manipulation. The account had 863,000 followers and used imagery from a BNB Chain event, making it appear legitimate.

However, the former Binance CEO said that concerns about the account’s veracity emerged after some close inspection. For starters, the account, which had blocked him, had posted several images purportedly featuring Zhao posing with the user, all of which appeared altered.

One photo showed Zhao wearing a shirt in a color he said he does not own, while another mixed low-resolution images of him and Binance executive Yi He with a sharper image of the account holder. CZ claimed the original photo featured Aster CEO Leonard.

He also claimed the account history suggested it either changed hands or was compromised years ago. The account’s history shows it originally belonged to a woman and posted exclusively female photos until July 2015, when it abruptly switched to crypto-only content without removing earlier material.

“Either a hacked takeover or bought,” CZ wrote.

He criticized the campaign as “lazy” and suggested it was likely orchestrated by a “self-perceived” competitor more focused on Binance than its own business.

You may also like:

Influencer ShirleyXBT also noted the account’s profile picture was an artificial copy of her own photo.

Community Backing and a Pattern of Scrutiny

The exposure drew some support from the crypto community, with World of Dypians CEO Teki thanking CZ for the clarification and admitting the initial post had briefly seemed believable.

Commentator Vegas offered a broader analysis, suggesting attackers fall into three categories: opportunists farming engagement, genuinely frustrated traders, and organized FUD campaigns. They also claimed to have been offered payment to spread negative sentiment about Binance, implying possible coordination by large market players or direct competitors.

This latest revelation has come amid sustained scrutiny of CZ and Binance. On January 28, the crypto entrepreneur faced backlash for allegedly promoting harmful market behavior after he advocated a buy-and-hold investment strategy, forcing him to clarify that his advice was personal and did not apply to every token.

Furthermore, on January 30, Binance announced it would convert the $1 billion in its SAFU insurance fund from stablecoins back into Bitcoin, a move some commentators viewed as a bullish signal but which also kept focus on the exchange’s financial strategies.

Despite the criticism, Binance’s market position is still quite strong, with data shared by CryptoQuant at the beginning of the year showing the exchange captured 41% of spot trading volume and 42% of Bitcoin perpetual futures volume among top-tier platforms in 2025.

SECRET PARTNERSHIP BONUS for CryptoPotato readers: Use this link to register and unlock $1,500 in exclusive BingX Exchange rewards (limited time offer).

BBVA, Spain’s second-largest bank by assets, said it joined Qivalis, a group of lenders aiming to introduce a regulated euro stablecoin and challenge the dominance of digital dollars.

Adding BBVA, which has $800 billion of assets, the group now includes a dozen major European Union banks, including BNP Paribas, ING and UniCredit.

The project’s goal is to create a token backed by a network of established banks, offering an alternative to crypto-native stablecoins, many of which are tied to the dollar and operated by companies based outside of the bloc.

Of the $300 billion stablecoin market, only $860 million are tied to the single currency. Tether, based in El Salvador, dominates with its $185 billion USDT, followed by New York-based Circle Internet’s (CRCL) $70 billion USDC.

A euro-pegged coin could allow EU businesses and consumers to make blockchain-based payments and settlements using euros, without relying on traditional financial rails or third-party providers outside the bloc.

“Collaboration between banks is key to create common standards that support the evolution of the future banking model,” Alicia Pertusa, head of partnerships and innovation at BBVA CIB, said in a statement.

BBVA’s involvement “reflects the increasing dedication of European banking institutions to jointly develop a European on-chain payment ecosystem based on the trust that banks provide,” said Jan-Oliver Sell, CEO of Qivalis and a former executive of Coinbase Germany. “This step consolidates Qivalis’ standing as Europe’s foremost bank-supported stablecoin initiative.”

Qivalis is currently pursuing authorization from the Dutch central bank to operate as an electronic money institution, a step required to issue stablecoins under the EU’s digital asset regulatory framework dubbed MiCA.

The project plans to debut the token in the second half of 2026.

Read more: BNP Paribas Joins EU Bank Stablecoin Venture Helmed by Ex-Coinbase Germany Exec

Join Our Telegram channel to stay up to date on breaking news coverage

The Ethereum price has surged 2% in the last 24 hours to trade at $3,350 after co-founder Vitalik Buterin called for a major simplification of the protocol.

Buterin warned that Ethereum’s increasing complexity, driven by the continuous addition of new features without removing outdated ones, poses a threat to trustlessness, self-sovereignty, and long-term sustainability. According to him, even a highly decentralized system with strong security measures can fail if its codebase becomes too complicated for users to understand or rebuild independently.

Buterin highlighted three main risks caused by protocol bloat. First, users are forced to rely on experts, or “high priests,” to explain how the system works, weakening trust. Second, Ethereum fails the “walkaway test,” as rebuilding high-quality clients would be nearly impossible if development teams disappear. Third, self-sovereignty is compromised because even technically skilled users cannot fully inspect or reason about the system.

An important, and perenially underrated, aspect of “trustlessness”, “passing the walkaway test” and “self-sovereignty” is protocol simplicity.

Even if a protocol is super decentralized with hundreds of thousands of nodes, and it has 49% byzantine fault tolerance, and nodes fully… pic.twitter.com/kvzkg11M3c

— vitalik.eth (@VitalikButerin) January 18, 2026

Buterin Calls for Ethereum “Garbage Collection”

To address these challenges, Buterin urged Ethereum developers to introduce “garbage collection,” a process aimed at simplifying the protocol. This involves removing rarely used features, reducing lines of code, limiting reliance on complex cryptographic primitives, and introducing fixed rules, or invariants, to make client behavior more predictable. He pointed to previous upgrades, such as Ethereum’s shift from proof-of-work to proof-of-stake and recent gas cost reforms, as examples of effective simplification.

Future changes could move less essential features into smart contracts, easing the burden on client developers while maintaining network security. In contrast, Solana Labs CEO Anatoly Yakovenko argued that blockchains must keep evolving to meet user and developer needs. He emphasized that constant iteration is vital for Solana’s survival, even if no single team drives the changes. Buterin, however, maintained that Ethereum should eventually reach a state where it can operate securely and predictably for decades without ongoing developer intervention.

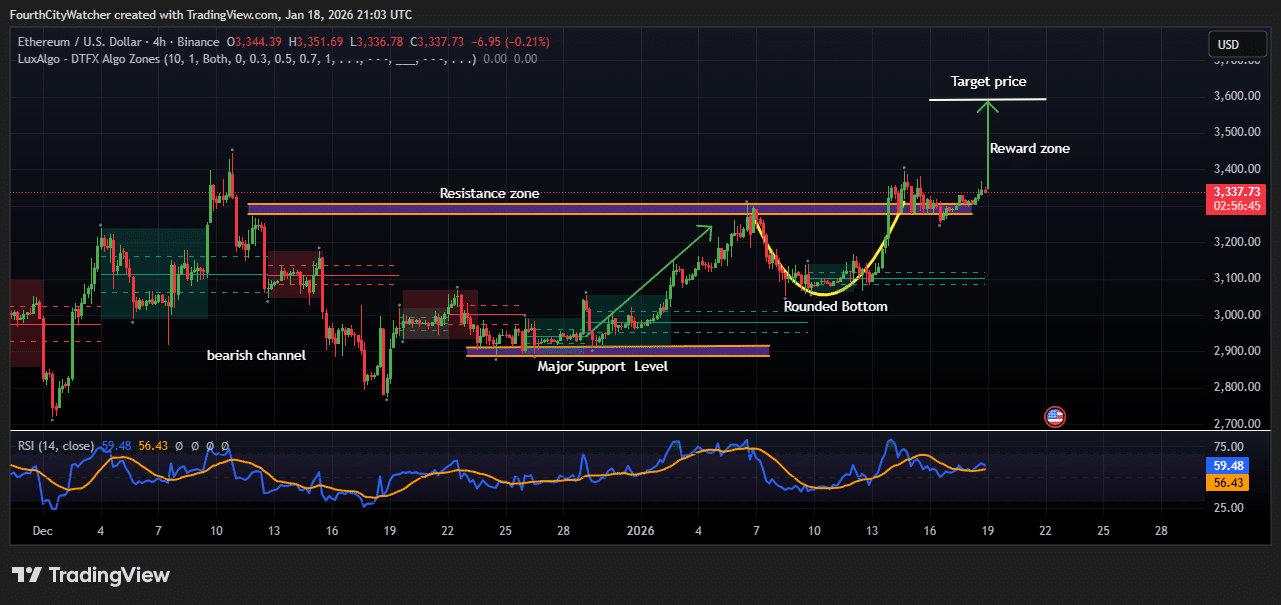

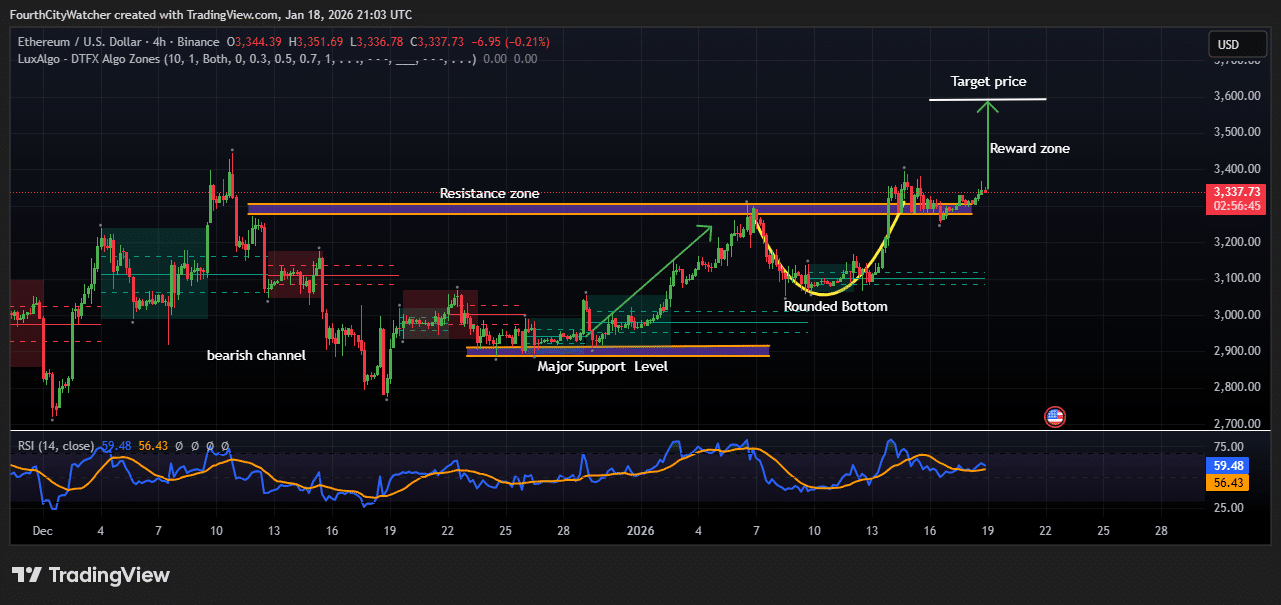

Ethereum Price Eyes Upside After Key Support Bounce

The 4-hour Ethereum chart shows clear signs of bullish momentum. Price recently bounced off a strong support level around $2,950–$3,000, which has held multiple times over the past month. This support has acted as a solid foundation, allowing Ethereum to recover from previous declines.

Before this bounce, Ethereum was moving in a bearish channel, making lower lows and lower highs. The recent breakout above this channel marked a key trend reversal, signaling that buyers are regaining control. Between January 10 and January 16, a rounded bottom pattern developed, which often signals a shift from bearish to bullish sentiment.

This pattern reflects a period of accumulation, where sellers gradually lost influence and buyers began gaining momentum. The rounded bottom now supports price consolidation above $3,300, showing that the market has stabilized and is preparing for potential further gains.

ETHUSDT Analysis Source: Tradingview

On the upside, there is a clear resistance zone between $3,350 and $3,400. Ethereum has tested this area multiple times but has struggled to break above it decisively. Currently, the price is consolidating just below this zone, forming a potential springboard for the next upward move.

A confirmed breakout above $3,400 could open the door to a reward zone near $3,550–$3,600, representing the next likely target for bullish traders. RSI analysis further supports this positive outlook. The Relative Strength Index sits around 59, below overbought levels, suggesting there is still room for Ethereum to move higher before encountering selling pressure. The RSI has steadily strengthened after recovering from previous dips, highlighting growing buying momentum in the market.

Related Articles:

Best Wallet – Diversify Your Crypto Portfolio

- Easy to Use, Feature-Driven Crypto Wallet

- Get Early Access to Upcoming Token ICOs

- Multi-Chain, Multi-Wallet, Non-Custodial

- Now On App Store, Google Play

- Stake To Earn Native Token $BEST

- 250,000+ Monthly Active Users

Join Our Telegram channel to stay up to date on breaking news coverage

Crypto World

Payments Protocol by Coinbase, Shopify Processes Just $1.2M USDC Since June: growthepie

The partnership between Shopify, Coinbase and Stripe allows Shopify merchants to accept USDC payments settled on Base.

The U.S. government is formally reversing its previous stance on banning certain activities at prediction market firms such as Kalshi and Polymarket, with U.S. Commodity Futures Trading Commission Chairman Mike Selig moving Wednesday to withdraw a proposed event-contracts rule from 2024 and scrapping an earlier advisory he said confused the industry.

In 2024, the derivatives regulator proposed a rule that would have banned contracts based on the outcome of political events, legally equating them with illicit contracts on war, terrorism and assassination and calling them “contrary to the public interest.” That rule never advanced to a final stage before President Donald Trump returned to the White House and appointed new CFTC leadership. The CFTC had allowed prediction markets based on political events to launch after losing a court fight over Kalshi’s intended offering that same year.

The recently confirmed chairman of the agency, Selig, has now cleared the decks of that and a minor advisory issued in September on certain contract markets.

“The 2024 event contracts proposal reflected the prior administration’s frolic into merit regulation with an outright prohibition on political contracts ahead of the 2024 presidential election,” Selig said in a statement. “The Commission is withdrawing that proposal and will advance a new rulemaking grounded in a rational and coherent interpretation of the Commodity Exchange Act that promotes responsible innovation in our derivatives markets in line with Congressional intent.”

Selig’s action is unsurprising, following closely on the heels of his remarks last week that signaled it was coming. He said he’d “directed CFTC staff to move forward with drafting an event contracts rulemaking.”

The Trump administration’s embrace of the prediction markets has paved the way for increased interest from companies seeking to throw their hat into the sector, such as Coinbase, or the tangential pursuit of similar products from Cboe.

The September advisory Selig pulled back had been meant to caution platforms about litigation concerns, he said, but it had “inadvertently created confusion and uncertainty for our market participants.”

The CFTC is expected to become a central voice in digital assets oversight, in which the prediction markets have had an overlapping interest. Selig is working on a number of new initiatives, and the Congress is negotiating its crypto market structure bill that — among many other points — is meant to establish the CFTC as the rightful watchdog of crypto spot markets that don’t involve securities.

Read More: U.S. SEC, CFTC chiefs push united front on paving the way for crypto

Bitcoin: $86k Bounce or $34k Crash? (The “Smart Money” Levels)

Newcastle: More questions than answers as Eddie Howe’s men yet to catch fire this season

Eli Lilly gaining in GLP-1 market over Novo Nordisk, earnings show

-

Crypto World5 days ago

Crypto World5 days agoSmart energy pays enters the US market, targeting scalable financial infrastructure

-

Crypto World6 days ago

Crypto World6 days agoSoftware stocks enter bear market on AI disruption fear with ServiceNow plunging 10%

-

Politics5 days ago

Politics5 days agoWhy is the NHS registering babies as ‘theybies’?

-

Crypto World6 days ago

Crypto World6 days agoAdam Back says Liquid BTC is collateralized after dashboard problem

-

Video2 days ago

Video2 days agoWhen Money Enters #motivation #mindset #selfimprovement

-

Tech16 hours ago

Tech16 hours agoWikipedia volunteers spent years cataloging AI tells. Now there’s a plugin to avoid them.

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread – Corporette.com

-

NewsBeat6 days ago

NewsBeat6 days agoDonald Trump Criticises Keir Starmer Over China Discussions

-

Politics3 days ago

Politics3 days agoSky News Presenter Criticises Lord Mandelson As Greedy And Duplicitous

-

Crypto World5 days ago

Crypto World5 days agoU.S. government enters partial shutdown, here’s how it impacts bitcoin and ether

-

Sports4 days ago

Sports4 days agoSinner battles Australian Open heat to enter last 16, injured Osaka pulls out

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Drops Below $80K, But New Buyers are Entering the Market

-

Crypto World3 days ago

Crypto World3 days agoMarket Analysis: GBP/USD Retreats From Highs As EUR/GBP Enters Holding Pattern

-

Crypto World5 days ago

Crypto World5 days agoKuCoin CEO on MiCA, Europe entering new era of compliance

-

Business5 days ago

Entergy declares quarterly dividend of $0.64 per share

-

Sports3 days ago

Sports3 days agoShannon Birchard enters Canadian curling history with sixth Scotties title

-

NewsBeat2 days ago

NewsBeat2 days agoUS-brokered Russia-Ukraine talks are resuming this week

-

NewsBeat2 days ago

NewsBeat2 days agoGAME to close all standalone stores in the UK after it enters administration

-

Crypto World1 day ago

Crypto World1 day agoRussia’s Largest Bitcoin Miner BitRiver Enters Bankruptcy Proceedings: Report

-

Crypto World6 days ago

Crypto World6 days agoWhy AI Agents Will Replace DeFi Dashboards