Crypto World

Mastercard to Settle Card Payments via Stablecoins

Mastercard is quietly upgrading its payments back-end by testing the use of regulated stablecoins to settle card transactions. The pilot, conducted in collaboration with SoFi Technologies and its Galileo platform, aims to move settlement between banks off traditional rails and onto digital dollars, while keeping the consumer checkout experience unchanged at the point of sale. The initiative centers on SoFiUSD, a dollar-backed stablecoin issued by SoFi Bank, N.A., and is positioned within Mastercard’s broader Multi-Token Network (MTN) vision for tokenized money.

As the industry watches the evolution of stablecoins from crypto-native instruments to mainstream settlement rails, Mastercard’s approach signals a strategic pivot: the networks that power card payments may increasingly rely on regulated digital assets to clear and settle transactions faster and with greater liquidity efficiency. The company’s plan also places it in a competitive stance with Visa, which has already piloted stablecoin-backed settlement capabilities for cross-border transfers and merchant payouts.

Key takeaways

- Mastercard is testing stablecoin-backed settlement, aiming to streamline the post-transaction clearing process across its global network.

- SoFi Bank, N.A. will use SoFiUSD to settle Mastercard credit and debit transactions; Galileo Financial Technologies will enable other banks and fintech issuers to participate in stablecoin settlement through Mastercard’s system.

- The initiative targets back-end settlement rather than altering the consumer payment experience, preserving the familiar card workflow at checkout.

- Mastercard’s Multi-Token Network is designed to support multiple forms of tokenized money, including stablecoins, tokenized deposits, and digital representations of fiat currencies.

- Regulatory clarity and cross-border liquidity considerations remain pivotal as stablecoins move toward mainstream financial infrastructure; market data in 2026 show a growing stablecoin sector with substantial transaction volumes ahead.

Back-end settlement reimagined

Behind the scenes, Mastercard’s approach reframes how settlement between issuing and acquiring banks could occur. When a consumer initiates a card payment, the traditional flow involves authorization, recording, merchant confirmation, and later settlement through standard banking channels. The new model concentrates settlement on the back-end, potentially using a regulated stablecoin such as SoFiUSD to fulfill the investment obligations between banks, rather than relying solely on fiat transfers.

Under this structure, a typical transaction would proceed as usual at the point of sale, but when the time comes to settle the obligation between the issuer and the acquirer, a stablecoin-based transfer could be executed. Stablecoins operate on blockchain infrastructure, offering the possibility of around-the-clock settlement that is not constrained by conventional banking hours. If successful, this could reduce settlement latency and improve liquidity management for financial institutions involved in card networks.

How stablecoin settlement would operate

In a practical sense, the workflow might look like this: a customer pays with a card in their local currency; Mastercard determines the net settlement obligation between the issuing bank and the acquiring bank; instead of exclusively relying on traditional rails, both parties could settle using a regulated stablecoin like SoFiUSD through the Mastercard system. SoFiUSD is issued by a federally regulated bank and is described as backed by cash reserves on a 1:1 basis, positioning it closer to bank-issued digital money than to a crypto-native asset.

Such a model aligns with a broader trend toward programmable, low-latency settlements that can cross borders and operate outside standard banking hours. While the user experience remains unchanged for the consumer, the underlying transfer of value between institutions could become more fluid and resilient in digital form.

MTN: A multi-token vision for payments

The backbone of this initiative is Mastercard’s Multi-Token Network, which is intended to support multiple forms of tokenized money. By bridging traditional financial rails with tokenized assets, MTN aims to create a versatile settlement ecosystem that can accommodate regulated digital currencies alongside conventional money. In theory, this could enable quicker cross-border movements, enhanced liquidity management, and greater interoperability between banks, card networks, and digital-asset infrastructure—without sacrificing regulatory compliance.

Why this matters for regulators, issuers, and users

Stablecoins have moved from niche crypto tools to a focal point of mainstream payments strategy. The appeal lies in their potential for fast, low-friction transfers and programmable payments, which could transform how businesses manage cash flows and how cross-border settlements operate. SoFi USD’s status as a dollar-backed instrument issued by a regulated bank is intended to help ease regulatory concerns, offering a more familiar framework for financial institutions wary of unbacked crypto exposure.

According to recent data, the stablecoin market has grown substantially. As of March 2026, the market’s total value stood around $314 billion, according to DefiLlama, reflecting growing adoption and increasing scale. The year 2025 also saw record activity, with monthly stablecoin transaction volumes approaching the trillions and market participants projecting that volumes could surpass $1 trillion per month by late 2026. These indicators help explain why payment networks are exploring stablecoin settlement as a means to improve efficiency and resilience in a rapidly digitizing ecosystem.

Competition and regulatory horizons

Mastercard is not alone in pursuing stablecoin-enabled settlement. Visa has already expanded its own stablecoin settlement capabilities, including cross-border transfers and merchant payout scenarios using tokenized dollars. This competitive dynamic underscores a broader shift in how the largest card networks view the future of payments: not as a replacement for traditional rails, but as an augmentation that leverages digital assets under a regulated umbrella.

Regulation remains a central determinant of how quickly and widely these innovations can be adopted. Banks and payment networks require clarity on issues such as reserve security, consumer protections, cross-border compliance, and interoperability with various blockchain ecosystems. SoFiUSD—issued by a chartered US bank—offers a regulatory-inclined path that other institutions may find more palatable as pilots scale.

Challenges on the path to wider adoption

Despite the promise, several barriers could temper the pace of adoption. Integration complexity for banks and payment processors stands out as a practical hurdle, along with regulatory variance across jurisdictions. Liquidity management between fiat and digital assets, and achieving seamless interoperability across different blockchains and legacy financial networks, are additional technical and operational considerations. Importantly, for most consumers, the transition will be invisible at the point of sale; the benefit will be measured in faster, more predictable settlement behind the scenes.

Broader implications for the payments landscape

Mastercard’s move fits into a wider evolution in digital payments. Stablecoins are increasingly seen as infrastructure components for remittances, business-to-business payments, treasury operations, and even stablecoin-linked card programs. If the current testing proves robust, card networks could evolve into hybrid ecosystems that blend traditional rails with blockchain-enabled settlement, delivering speed and efficiency without disrupting the familiar checkout experience.

Ultimately, the timing and scale of this transition will hinge on regulatory clarity, cross-border cooperation, and the ability of banks and issuers to integrate stablecoin settlement into complex, high-volume networks. The coming quarters are likely to reveal pilots, partner churns, and potentially early live deployments that will indicate how far such a back-end upgrade can take mainstream payments.

For investors and builders, the key takeaway is that stablecoins are moving from theory to execution within major payment rails. The attention now shifts to how regulators respond, how smoothly banks can onboard into MTN-enabled workflows, and how quickly other issuers and networks adopt similar back-end settlement architectures.

Watch closely for updates on pilot outcomes, regulatory milestones, and any additional partnerships that broaden the set of stablecoins approved for settlement across major networks. The next phase will reveal whether this is a scalable blueprint for faster, more resilient payments or a pilot with limited reach.

Since Paul Atkins was sworn in as chair of the US Securities and Exchange Commission (SEC) on April 21, 2025, the agency has significantly changed its position on regulation and enforcement related to digital assets, marking a shift from the leadership of former chair Gary Gensler during the Biden administration.

During his 2024 presidential campaign, Donald Trump made removing Gensler one of his promises to the crypto industry, along with creating a national Bitcoin (BTC) stockpile and opposing the issuance of a US central bank digital currency.

His November 2024 election win led to Gensler’s resignation in January 2025 and the appointment of SEC commissioner Mark Uyeda as acting chair of the financial regulator until the Senate could confirm Atkins as Trump’s pick to lead the agency.

Even before the Senate voted to confirm Atkins, the SEC was already signaling a change in crypto regulation and enforcement under Trump. Uyeda oversaw the creation of an SEC crypto task force headed by Commissioner Hester Peirce and the agency began to drop civil enforcement actions and investigations into crypto companies, starting with Coinbase in February.

The first 12 months of Atkins’ chairmanship has seen the SEC push policies and approaches to regulation widely viewed as favorable to the crypto and blockchain industry.

In addition to wrapping up enforcement actions, the regulator has approved multiple exchange-traded funds tied to various crypto assets, signed a memorandum of understanding with the Commodity Futures Trading Commission (CFTC) over coordination on digital asset regulation and issued an interpretative notice on not treating most cryptocurrencies as securities under federal law.

Related: One year after Gary Gensler’s exit, SEC’s crypto playbook looks very different

“A year goes by quickly, but we’ve made huge progress, I think,” said Atkins in a Monday CNBC interview. “I promised a new day at the SEC when I came aboard, and we have. We’ve pivoted from the old practice of regulation through enforcement and the opaqueness of the agency, as, for example, with crypto.”

SEC chair faces scrutiny from Democratic lawmakers

While many in the crypto industry have lauded Atkins’ approach to digital assets since taking office, Congressional Democrats have criticized the SEC and chair for potential conflicts of interest following dropped investigations and enforcement actions against companies tied to Trump and his family.

Last week, Massachusetts Senator Elizabeth Warren accused the SEC chair of misleading Congress in his testimony before a House committee in February. Warren said in an April 15 letter that the SEC’s own data from the 2025 fiscal year showed the agency had fewer enforcement actions than at any point in the previous 10 years.

Magazine: Adam Back says current demand is ‘almost’ enough to send Bitcoin to $1M

Early Threats Recovery Plan

The first phase focuses on recovery actions in case of the failure of classical cryptography. Engineers will introduce a comprehensive migration trajectory, which will require users to transfer funds to quantum-secure accounts. Moreover, the strategy will guarantee that user assets are not exposed in case of a transition event caused by compromised keys. Ripple engineers are exploring zero-knowledge proof systems that prove ownership of existing accounts without disclosing any private keys. As a result, the network will be able to promote safe migrations and safeguard sensitive information. The XRP Ledger already has building blocks that facilitate this approach such as seed-based key generation.

The second step is concerned with testing the algorithms suggested by the National Institute of Standards and Technology. In addition to in-house testing, Ripple has collaborated with Project Eleven to build hybrid signing systems that fuse existing and post-quantum techniques. The next stage will involve developers starting to incorporate new signature systems with the existing elliptic curve techniques. Additionally, developer networks will begin to be tested to enable applications to be modified. Ripple will also analyse encryption tools that uphold privacy and compliance to tokenized assets.

The final stage involves a full transition toward post-quantum cryptography within the XRP Ledger ecosystem. Ripple therefore intends to implement protocol changes that will facilitate the adoption of new signature systems on a large scale. This move will transition the network from testing into full deployment in line with the stated timeline. The XRP Ledger already includes features to enable long-term resilience against quantum risks. Notably, key rotation enables users to refresh private keys without changing accounts, and deterministic generation of keys enables security upgrades to be controlled. These functionalities will provide a foundation for future upgrades as quantum technology advances.

David Schwartz raised fresh concerns about integrating decentralized finance bridges for Ripple’s RLUSD stablecoin. He focused on security risks after reviewing several cross-chain systems. Besides that, his findings showed that most protocols had strong technical foundations but still faced deployment weaknesses.

I evaluated a lot of DeFi bridging systems for use by RLUSD. I was almost exclusively focused on the security and risk aspect. One thing I noticed is that most schemes were very well designed and had really strong mechanisms available to protect against exactly the type of attack…

— David ‘JoelKatz’ Schwartz (@JoelKatz) April 20, 2026

However, he stressed that operational decisions often weaken security layers. Many teams prioritize ease of use and faster expansion across networks. Consequently, critical safeguards get overlooked, which increases exposure to exploits across connected chains.

Convenience Trade-Offs Create Vulnerabilities

Schwartz explained that several bridge systems discourage full use of key security features. He noted that developers avoid complex safeguards due to cost and operational challenges. Moreover, this approach creates gaps that attackers can exploit during high-value transactions.

Additionally, he linked this pattern to recent exploit cases in the DeFi sector. He pointed out that convenience-driven decisions reduce resilience against advanced attacks. Hence, systems that appear secure in design may fail under real-world pressure.

KelpDAO Exploit Reflects Broader Risks

The recent attack on KelpDAO involved the loss of around $292 million tied to rsETH tokens. Attackers exploited cross-chain messaging linked to LayerZero infrastructure. Significantly, the exploit relied on manipulating transaction validation processes.

On-chain data showed that about 116,500 rsETH tokens moved to attacker-controlled wallets. Moreover, the attacker used these assets as collateral on Aave V3 to borrow ETH and WETH. Consequently, the funds moved through Tornado Cash to obscure transaction trails.

Cross-Chain Weaknesses Raise RLUSD Concerns

Schwartz noted similarities between the exploit and potential risks for RLUSD integration. He suggested that ignoring LayerZero’s advanced security features may have contributed to the breach. Additionally, he described the attack as more complex than initially expected.

Moreover, he emphasized that cross-chain infrastructure introduces multiple points of failure. Each connection between networks increases risk exposure. Hence, stablecoin systems relying on such bridges must prioritize strict validation mechanisms.

Broader Ecosystem Flags Additional Risks

Concerns also extend to wrapped assets such as wXRP on other networks. An XRPL validator highlighted counterparty risks tied to issued tokens across chains. Besides that, ecosystem participants continue to evaluate governance changes for lending protocols.

However, some developers argue that proposed updates may not deliver strong utility for XRP holders. Meanwhile, discussions continue around collateral use cases and protocol efficiency.

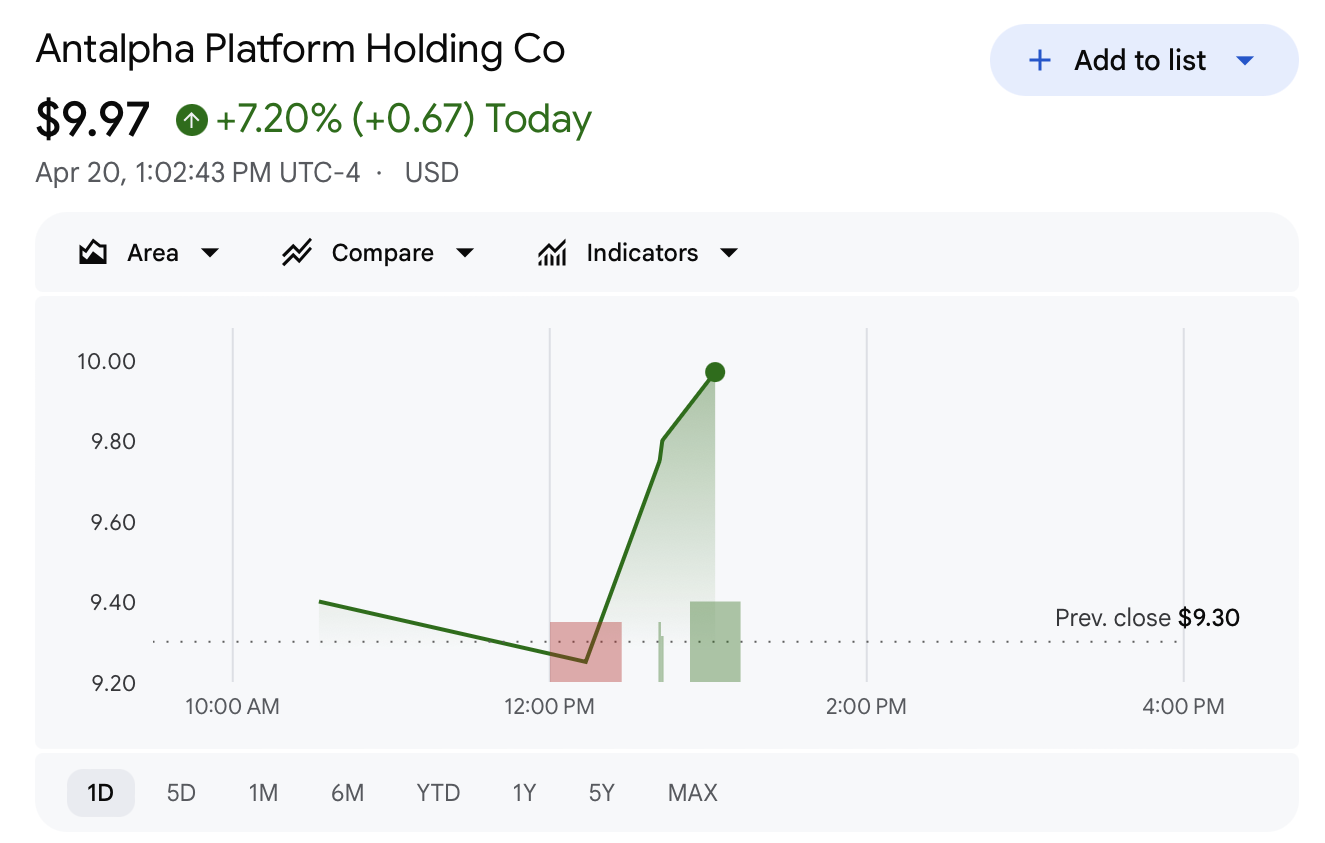

Tether has disclosed an 8.2% stake in Antalpha, acquiring about 1.95 million Antalpha shares through related entities. The position, disclosed in a Schedule 13D filed with the U.S. Securities and Exchange Commission, places the stablecoin issuer among Antalpha’s largest shareholders following the mining-focused lender’s May 2025 initial public offering. Giancarlo Devasini, Tether’s chairman, shares voting and dispositive power over the stake, according to the filing. The document also notes that Tether and its affiliates may adjust their holdings over time in response to market conditions and other factors.

Antalpha operates in the Bitcoin-backed lending and equipment-financing space, catering to mining operators. The company reported a loan portfolio of about $1.6 billion as of the end of 2024 and maintains close ties to the Bitmain ecosystem, a major supplier of mining hardware.

Antalpha raised roughly $49.3 million in its IPO, at $12.80 per share. Tether had previously signaled a potential interest in purchasing up to $25 million worth of shares.

In its latest annual figures, Antalpha posted 2025 revenue of $79.7 million, up 68% year over year, with net income rising to $18.5 million—more than triple the previous year’s figure. On the day of the disclosure, Antalpha’s stock climbed about 7.2% to around $9.97 in early trading, according to Google Finance data.

Source: Cointelegraph, based on the Schedule 13D filing and Antalpha’s financial disclosures.

Key takeaways

- Tether now holds roughly 1.95 million Antalpha shares, representing an 8.2% stake and giving the founder’s circle voting power over the position, per the Schedule 13D.

- The stake arrives after Antalpha’s May 2025 IPO, with Tether previously indicating interest in buying up to $25 million of shares.

- Antalpha’s core business centers on Bitcoin-backed lending and mining equipment financing, with a reported $1.6 billion loan portfolio at year-end 2024 and ties to the Bitmain ecosystem.

- Tether’s broader investment strategy is to deploy profits across crypto infrastructure, tokenized assets, and related tech—new bets alongside existing holdings in Eight Sleep, Gold.com, Anchorage Digital, and a Kaio-backed round.

- The stablecoin issuer remains the dominant player in the market, with USDT accounting for about $187 billion in market capitalization and the total stablecoin market near $320.7 billion.

Antalpha and the mining-finance niche

Antalpha’s business model emphasizes liquidity and equipment financing for mining operators, a space that has drawn interest from investors seeking exposure to the cyclical upswing of crypto mining. The company’s sizable loan portfolio signals a continued focus on securing scalable credit lines for operators navigating equipment cycles and capital expenditure needs. Its connection to Bitmain’s ecosystem underscores a strategic alignment with a major supplier in the mining hardware sector, potentially easing access to hardware and related financing channels for clients.

Tether’s stake: governance, strategy, and potential impacts

The Schedule 13D filing confirms that Tether’s stake in Antalpha is substantial enough to position the company as a major shareholder. With Devasini listed as sharing voting and dispositive power, the arrangement signals an intentional governance role in Antalpha’s ongoing development. While the filing notes that Tether and its affiliates may adjust their position over time, the move reflects a broader pattern of Tether diversifying beyond its core stablecoin operations into strategic investments across crypto finance, infrastructure, and real-world asset initiatives.

Cointelegraph has previously reported on Tether’s expansive capital deployment—an approach that taps profits from USDT to fund ventures across mining, AI, financial services, and tokenized assets. The recent Antalpha stake complements a portfolio that has included investments in tokenized real assets and regulated financial infrastructure. The company’s strategy has included selective allocations to fintech and on-chain finance ventures, with profits fueling these bets rather than reserve-backed liquidity alone.

Tether’s broader venture footprint and what it signals

Beyond Antalpha, Tether’s investment activity this year has spanned several notable deals. In March, the company led a $50 million funding round for Eight Sleep, a firm building sleep-focused wellness hardware and software, which valued the company at around $1.5 billion. In February, Tether acquired a roughly $150 million stake in Gold.com, representing about 12% ownership, as part of its push to widen access to tokenized gold through its XAUt stablecoin product. In the same month, Tether announced a $100 million equity investment in Anchorage Digital, a federally chartered U.S. digital asset bank that provides custody, settlement, and stablecoin issuance services to institutional clients.

CEO Paolo Ardoino has publicly highlighted the breadth of Tether’s venture exposure, noting that the firm has invested in more than 120 companies through its venture arm, with funding drawn from profits rather than from stablecoin reserves. This approach aims to diversify the company’s revenue streams and digital-asset ecosystem exposure while maintaining a cautious stance toward custodial and regulatory-compliant ventures.

Earlier this month, reports surfaced that Tether could pursue fresh capital at a valuation around $500 billion, with the company signaling that fundraising could be delayed if investor appetite does not materialize. The stake in Antalpha, along with the broader lineup of strategic bets, reinforces a narrative of continuous expansion into crypto infrastructure and related industries—an approach that aligns with Tether’s long-term ambition to anchor a broader ecosystem around stablecoins and on-chain finance.

Market context and what to watch next

Antalpha’s performance, combined with Tether’s growing investment footprint, offers a window into how stablecoin issuers are recalibrating their role in the crypto economy—from liquidity providers to strategic accelerators for on-chain assets, mining finance, and tokenized real-world assets. For investors, the key questions revolve around governance outcomes, the impact on Antalpha’s strategy and profitability, and how Tether’s venture portfolio may influence regulatory and market perceptions of stability-backed capital in crypto markets.

As the crypto landscape evolves, observers will watch how Tether’s stake translates into governance influence at Antalpha, how Antalpha leverages this partnership to scale its lending and financing operations, and how the broader set of Tether-backed ventures interacts with growth in mining, asset tokenization, and institutional-grade on-chain infrastructure.

Readers should stay attentive to Antalpha’s quarterly results and any subsequent regulatory disclosures that illuminate how such strategic holdings shape governance, risk, and value creation in the mining-finance niche and beyond.

Tether has taken an 8.2% stake in Antalpha, making the stablecoin issuer one of the company’s largest shareholders following its May 2025 initial public offering (IPO), according to a Monday filing.

The Schedule 13D filing with the US Securities and Exchange Commission indicates that Tether now holds 1.95 million shares through related entities, with Giancarlo Devasini, chairman of Tether, sharing voting and dispositive power over the position.

The filing also states that Tether and its related entities may increase or reduce their holdings over time depending on market conditions and other factors.

Antalpha provides Bitcoin-backed lending and equipment financing to mining operators, reporting a loan portfolio of about $1.6 billion as of the end of 2024, and is closely tied to the Bitmain ecosystem, a major supplier of mining hardware.

Antalpha raised about $49.3 million in last year’s IPO at $12.80 per share, according to its prospectus. Tether had previously indicated interest in purchasing as much as $25 million worth of shares.

Antalpha reported 2025 revenue of $79.7 million, up 68% year over year, while net income rose to $18.5 million, more than tripling from the previous year.

On Monday, its shares rose about 7.2% to around $9.97 in early trading, per Google Finance data.

Tether is the issuer of Tether (USDT), the largest stablecoin by market capitalization, with a market cap of about $187 billion, roughly 58.4% of the total stablecoin market, which stands near $320.7 billion, according to DefiLlama data.

Related: Tether announces $150M recovery program for Drift Protocol

Tether expands investments across crypto infrastructure and beyond

Tether’s investment in Antalpha comes as the company is using its recent profits to expand into a range of sectors tied to digital assets, including mining, artificial intelligence, financial services and tokenized assets.

Earlier on Monday, real-world asset tokenization protocol Kaio said Tether participated in an $8 million funding round.

“The participation of Tether reflects direct strategic alignment,” the announcement said. “USDT has become the dominant settlement layer for cross-border capital flows. KAIO provides the next layer: structured, compliant access to institutional-grade yield for USDT holders.”

In March, Tether led a $50 million investment in Eight Sleep, a company that develops sleep-focused products such as smart mattresses and wellness systems, valuing it at $1.5 billion.

In February, the company acquired a $150 million stake in Gold.com, representing about 12% ownership, as part of a push to expand access to tokenized gold through its XAUt product.

The same month, Tether made a $100 million equity investment in Anchorage Digital, a federally chartered US digital asset bank that provides custody, settlement and stablecoin issuance services to institutional clients.

CEO Paolo Ardoino said in July that Tether has invested in more than 120 companies through its venture arm, with those investments funded from company profits rather than stablecoin reserves.

Earlier this month, Tether was reported to be seeking fresh capital at a $500 billion valuation, with the company indicating it could delay the raise if investor demand falls short.

Magazine: Adam Back says current demand is ‘almost’ enough to send Bitcoin to $1M

Iran peace talks entered their most uncertain phase yet Monday as Vice President JD Vance prepared to lead a delegation to Islamabad alongside envoys Steve Witkoff and Jared Kushner, Axios reported, even as Iran’s Foreign Ministry formally stated it has “no plans” for a second round and Tehran suspected the invitation was cover for a surprise US military strike before Wednesday’s ceasefire expiry.

Summary

- Two US Air Force C-17 cargo planes landed at a Pakistani air base Sunday carrying security equipment, and Islamabad’s Red Zone was locked down with thousands of security personnel deployed in anticipation of a US arrival.

- Trump told Axios: “I feel fine about it. The concept of the deal is done. I think we have a very good chance to get it completed,” directly contradicting Iran’s public rejection of talks.

- Pakistan’s foreign ministry confirmed its counterpart spoke with Iran’s foreign minister by phone Sunday about “the need for continued dialogue,” leaving a narrow window for Iran to reverse its stance.

Iran peace talks are entering their most consequential 48 hours with the ceasefire set to expire Wednesday and no Iranian delegation publicly confirmed. The US delegation is traveling regardless. Pakistan has kept Islamabad under security lockdown in anticipation of a second round, with thousands of paramilitary and army personnel deployed through the Red Zone.

The US team, the same configuration that led the failed first round on April 11 and 12, is led by Vance and includes Witkoff and Kushner. Two US Air Force C-17 cargo planes had already landed at a Pakistani air base Sunday with security equipment and vehicles, signaling the delegation was committed to arriving whether or not Iran confirmed participation.

Tehran has told intermediaries it believes the US announcement of talks is designed to build a “blame game” narrative: publicly committing to negotiations while preparing military strikes to coincide with the ceasefire expiry. The Sunday seizure of the Touska, arriving hours after Trump announced the Pakistan talks, reinforced that suspicion. Iran’s Foreign Ministry described US statements about negotiations as “a media game.”

Iran’s chief negotiator Ghalibaf said in state television remarks Saturday that Iran’s armed forces remain “ready” even while pursuing diplomacy, framing the two tracks as simultaneous rather than alternative. The original ceasefire was announced hours before a midnight deadline during which Trump had threatened “a whole civilization will die tonight.” Iran’s negotiating team arrived at the first round dressed in black, in mourning for those killed in the war. The level of institutional mistrust is not rhetorical.

What Pakistan Is Attempting as Mediator

Pakistan has framed this engagement as an ongoing “Islamabad process” rather than a single discrete round, giving itself diplomatic room to survive a second collapse without the entire framework breaking down. Prime Minister Sharif spoke with Iranian President Pezeshkian on Sunday. Pakistan’s army chief Field Marshal Asim Munir has served as the primary interlocutor between delegations throughout the conflict.

Despite Iran’s public rejection, Pakistani authorities completed Red Zone security preparations, suggesting Islamabad has reasons to believe Iran may still participate. An Iranian parliamentary official told Al Jazeera that Iran would “likely” send a team Monday or Tuesday, a gap between the Foreign Ministry’s statement and the parliamentary official’s remark that Pakistan is actively working to close.

What the Outcome Means for Crypto Markets

The next 48 hours will determine which scenario plays out for Bitcoin price markets. A ceasefire extension or genuine deal replicates the April 8 template: oil crashes and BTC surges, potentially toward $80,000. A confirmed collapse with resumed strikes tests the institutional demand floor below $70,000.

The Iran nuclear sticking point remains the hardest to bridge: the US requires Iran to permanently halt uranium enrichment, and Iran has said it will not surrender its 440-kilogram stockpile. A second round would need to find a formula, such as third-party custody of the stockpile, that neither side has publicly endorsed but that both have reportedly discussed through Pakistani intermediaries.

If Michael Saylor can sustain his trailing four-week pace of bitcoin (BTC) buying, Strategy (formerly MicroStrategy) could own more than Satoshi Nakamoto by September 2026.

Buying at the world’s largest BTC treasury company now averages nearly 2,800 BTC per trading day after accelerating 40% over the last four weeks above its year-to-date average.

Strategy has publicly targeted 1 million BTC under its so-called 21/21 capital plan.

Monday’s SEC Form 8-K filing pushed the company’s holdings to 815,061 BTC. Saylor picked up 34,164 BTC last week alone, a single-week record for 2026, at an average purchase price of $74,395 per coin.

Strategy’s blended cost basis across all holdings is now $75,527, which sits within 1% of the prevailing market price of BTC.

Although there are a variety of estimates for the total holdings of Bitcoin creator Satoshi Nakamoto, 1.1 million is a common estimate. For example, Arkham Intelligence attributes 1,096,354 BTC to Satoshi from roughly 22,000 coinbase rewards of the blockchain’s earliest blocks.

Strategy is a mere 281,293 coins short of that figure.

If Saylor continues his pace over the last 30 days through autumn, Strategy could close the gap in 101 trading days, or about 147 calendar days.

Strategy could buy more bitcoin than Satoshi

Strategy can buy and hold BTC around the clock, but it cannot fund new buys 24/7. At the market (ATM) offerings of MSTR common stock; as well as the preferreds STRC, STRK, STRF, and STRD; occur when Nasdaq is open.

Any realistic projection of when Strategy might own more BTC than Satoshi has to measure pace by trading day, i.e. roughly 21 trading days per month adjusted for federal market holidays.

Year-to-date through April 19, Strategy has bought 142,561 BTC for roughly $11.13 billion across 73 trading days. That’s approximately 1,953 BTC per trading day.

Extrapolating the 2026 average through November 13 would put Strategy past Satoshi on that date.

However, the trailing four weeks are running about 40% hotter than the first quarter. Strategy’s last four weekly announcements, covering March 23 through April 19, totaled 52,962 BTC across 19 trading days.

That acceleration tracks Strategy’s March 23 expansion of its ATM sales. On that day, the company authorized another $21 billion of new MSTR common stock, $21 billion of new STRC preferreds, and a more limited $2.1 billion of STRK preferreds.

Saylor posted, “The Second Century Begins” in early March. He meant that Strategy had just completed its 100th BTC purchase since 2020. Six weeks into his “second century,” Saylor has bought another 76,330 BTC.

STRC preferred is doing most of the work

Of the roughly $11.34 billion Strategy has raised this year through its ATMs, almost all of which went to buy BTC, MSTR common stock provided about 50.8% or $5.77 billion. STRC provided 49.1% or $5.57 billion.

STRF and STRD preferreds contributed nothing, and STRK raised just $3.4 million.

Thanks to an aggressive advertising campaign likening STRC to a high-yield bank account or money market fund — in addition to a surge in trading volume to capture the dividend snapshot for STRC’s then-once-monthly, 11.5% annualized dividend — Strategy reported $2.2 billion of STRC sales, dwarfing its $366 million of MSTR sales.

Although MSTR has historically funded the vast majority of Strategy’s BTC buying, STRC funded 85% of last week’s purchase.

Last year, in contrast, Strategy sold zero STRC through its ATM from August through October 2025.

Read more: STRC controversy goes mainstream

STRC is supposed to trade near $100 per share, but shares have traded below $91 at times. The company has raised its dividend rate seven times in order to encourage bids after its price fell.

Strategy has also been stockpiling a few dollars, not just BTC.

The company disclosed $2.25 billion USD as of January 4. This cash is earmarked to service preferred dividends and bond interest payments. The reserve started at $1.44 billion in December 2025.

Got a tip? Send us an email securely via Protos Leaks. For more informed news, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Solana (SOL) price trades at $84.15 on the 12-hour chart, attempting a rebound from the $82.93 support. A hidden bullish divergence has formed between April 15 and April 19, signaling that selling momentum may be exhausting.

However, rising sell volume and a massive spike in exchange inflows complicate the setup. Someone is consistently offloading SOL into each rebound attempt, and the DeFi contagion spreading from Ethereum explains why.

Price Flashes a Rebound Signal but Sell Volume Tells a Different Story

Solana price peaked at $90.79 on April 17 before pulling back sharply. The low at $82.93 on April 19 marked a higher low compared a level reached on April 15. During that same window, the Relative Strength Index (RSI) printed a lower low. RSI is a momentum indicator that measures the speed of recent price changes.

That pattern is a hidden bullish divergence. Price made a higher low while RSI made a lower low, which typically signals that selling pressure is weakening. A rebound attempt has already started from that level.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

Yet volume tells the opposite story. Sell-side volume has been rising since April 18, even as RSI suggests momentum is fading. That combination carries a specific meaning. Fewer percentage moves per sell wave, paired with more participants, points to distribution rather than panic. Someone is consistently unloading SOL into each small rebound.

Meanwhile, the likely source is the spreading DeFi contagion. Following the KelpDAO rsETH exploit, Solana’s Kamino Prime Market USDC reserve hit 100% utilization on April 20.

Zero liquidity is available. Multiple USDC vaults are above 95% utilization. Funds with stuck USDC positions may be selling SOL on spot markets to raise cash. That pressure creates the supply cap the chart is showing.

Exchange Inflows Surge 1,102% as Hodlers Add Nearly 500K SOL

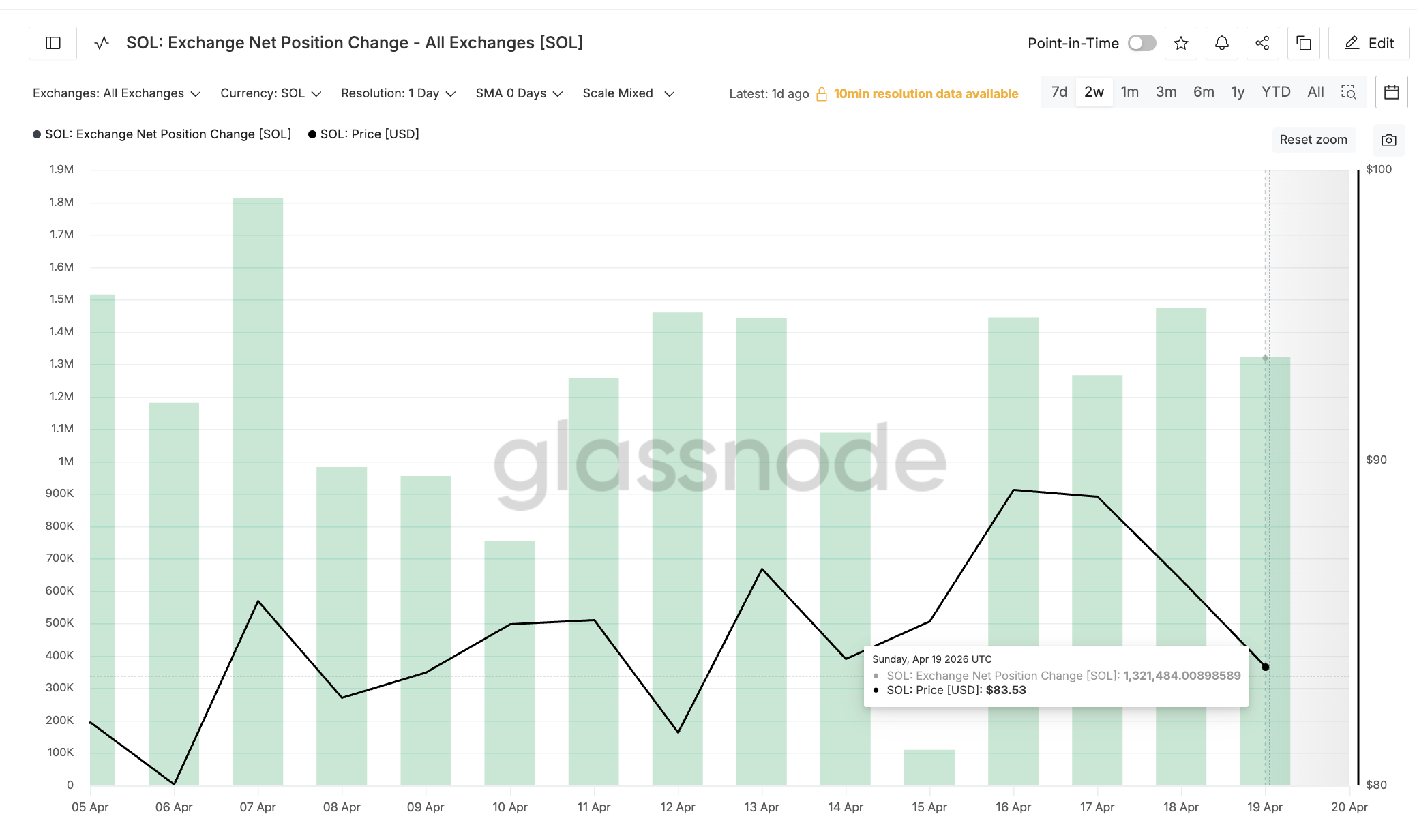

On-chain data confirms the forced-selling thesis. The SOL Exchange Net Position Change has exploded. This metric tracks the 30-day flow of coins into or out of exchange wallets.

Meanwhile, on April 15, the metric read 109,932 SOL. By April 19, it had surged to 1,321,484 SOL. That is a 1,102% increase in four days. More SOL is now sitting on exchanges, typically a precursor to selling.

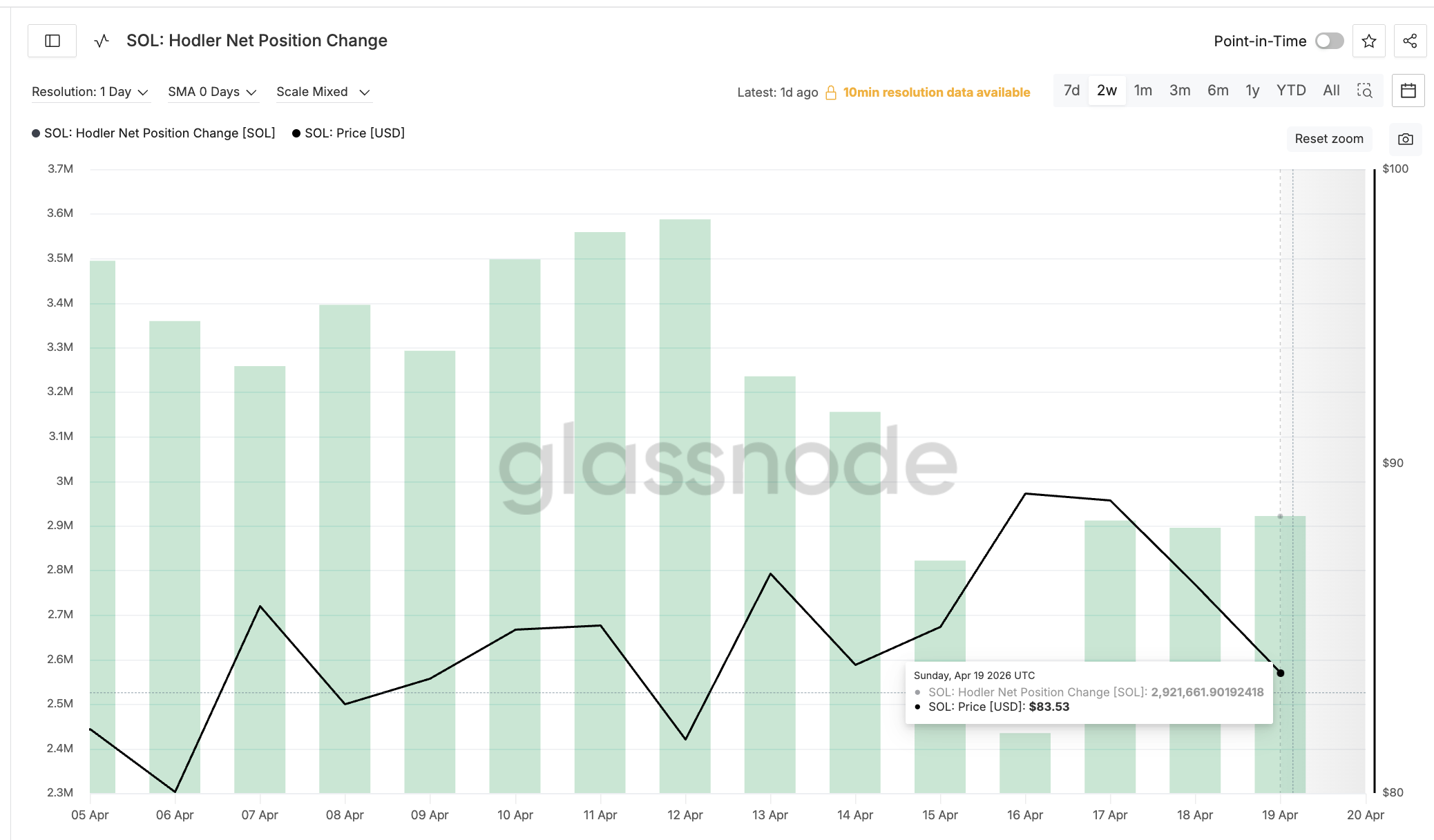

Yet the other side of the market is doing the opposite. The SOL Hodler Net Position Change is climbing. This metric tracks the 30-day change in supply held by wallets older than 155 days.

On April 16, hodlers held a net 2,434,566 SOL added over the prior month. By April 19, that figure had climbed to 2,921,661 SOL. Long-term holders added roughly 487,000 SOL in three days, a 20% jump.

The split is the key to the entire picture. Forced sellers from the DeFi crisis are possibly depositing to exchanges. Long-term holders are absorbing the supply. That structure produces a shallow rebound rather than a collapse, with each side fighting for control at specific price levels.

Solana Price Levels That Decide Between a Shallow Bounce and a Breakdown

Solana price at $84.15 sits between two tight levels. The first upside test is $85.42. A clean move above that strengthens the rebound. However, the next resistance at $90.79 is the April 17 high, a level that already rejected once. A reclaim there would neutralize the current weakness and open a path toward $93.40.

Yet if forced sellers overwhelm the hodler bid, the rebound fails. A touch of $82.93 invalidates the hidden bullish divergence. A break of $82.11, the 0.618 Fibonacci, opens $79.95 and $76.74 as the next downside targets.

Solana price at $82.93 separates a rebound that holds long-term conviction from a breakdown driven by the DeFi crisis.

The post Solana Tries to Rebound but a DeFi Contagion Sends 1.32 Million SOL to Exchanges appeared first on BeInCrypto.

Gudtrip, the AI-powered weed vape created by “vape-to-earn” firm Puffpaw, has been branded a contender for the “grifter buzzword world record” this 4/20.

On today of all days, X users decided to comment on Gudtrip’s claims that it combines “premium cannabis, blockchain rewards, and AI-powered asset tools in one product,” asking, “Is Gudtrip going for a grifter buzzword world record?”

Gudtrip says it will reward its users with “Bitcoin [BTC], Gudtrip Points, and VAPE token” when they smoke using the device.

As for the AI integration, Gudtrip says that users wishing to invest their crypto rewards can use its “open-source AI agent tools to explore supported blockchain-based strategies.”

Another X user said, “In a just world, ‘AI-powered crypto weed vape’ is an object that when conceived opens a chasm to hell beneath your feet,” while one claimed, “I’ve never seen a group of more ridiculous buzz words surrounding a drug device please dear god fuck off with your crypto/agentic AI bullshit scam thanks.”

While puffing on your vape, you’re likely to be accruing its VAPE token — the price of which Protos has been unable to confirm — rather than the 20 BTC worth $1.5 million its promotional images suggest.

Read more: Crypto’s smoking ‘solution’ will likely create more vape addicts

Just last week, shoe firm Allbirds was able to juice its stock by 508% after pivoting its operations towards investment in AI data centers.

AI has also been a major buzzword linked to many big-name layoffs this year.

Many on social media weren’t at all impressed with theGudtrip concept, with some asking for ways to short the product. Others described it as a sign of a “bubble.”

Attempting to join in on the joke that is ripping into Gudtrip’s buzzword playbook, its own founder, Reffo Tse, also asked “how do I short this?”

Read more: AI agents want to identify your crypto wallet using social media

Puffpaw’s ‘vape-to-earn’ would only make addictions worse

When Tse first released the vaping device Puffpaw, he promised to disincentivize vaping by offering users crypto rewards for using smaller amounts of nicotine.

However, it was mocked by users who noted that a vaping habit tied to a financial incentive will only incentivize continuous vaping.

UK Addiction Treatment Centres told Protos that Puffpaw wasn’t going to lower the usage of vapes. It said, “If anything, it could have the complete opposite effect because of the enticing gamification and crypto reward that comes with vaping.”

Read more: Snoop Dogg quits ‘smoke’ amid NFT, edibles launch rumors

The addiction center said Puffpaw might “worsen a person’s addiction,” and that it feels like “a corporate way of making money off people trying to quit smoking and lead healthier lives.”

The vaping product seems not to have been enough for Puffpaw’s CEO, however, and Gudtrip entered the scene in October 2025.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Crypto audiences don’t read the way they used to. They scan, they watch, and they move fast. Our latest updates to the homepage and article pages are a direct response to that reality; introducing a dedicated video block, new social media CTAs, and UI improvements across both surfaces. This builds on last year’s full site redesign across all 26 global domains, and takes it further.

What’s new at a glance

- Video block: A dedicated section for video content, now placed prominently on article pages

- Social media CTAs: New call-to-action elements connecting editorial content to BeInCrypto’s social channels

- UI improvements: Visual hierarchy and layout updates across both the homepage and article pages, reinforcing the mobile-first approach from the September redesign

Built For How People Read Today

According to Vlada Morhunova, Product Manager at BeInCrypto, internal analytics revealed a clear split between how desktop and mobile users navigate the site.

“Desktop users tend to navigate more deliberately. They browse categories, use search, and explore related content. Mobile users behave more like scanners, relying heavily on what’s immediately visible on the page. With mobile accounting for the majority of our global traffic, we needed the homepage and article page layouts to serve that scanning behavior more effectively.”

The homepage and article pages were the clear priority. They are the two highest-traffic touchpoints across the entire product, where returning readers land and where most new visitors arrive from search and social. “If we improve the experience here,” Morhunova notes, “it lifts virtually every engagement metric across the board.”

Video is Now a First-class Format

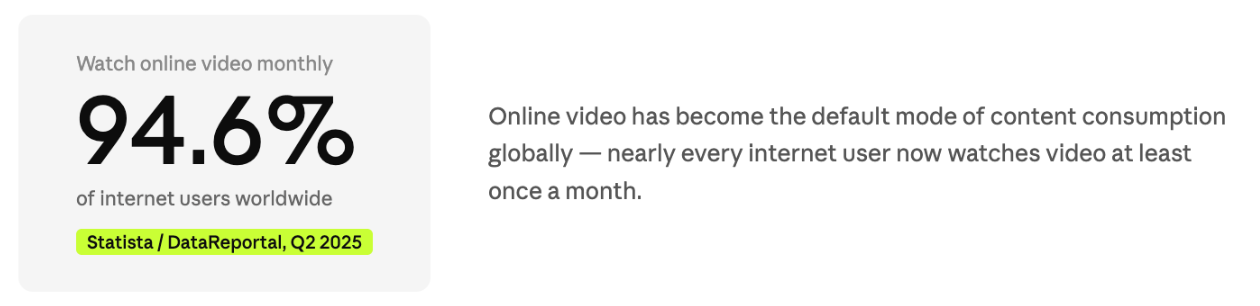

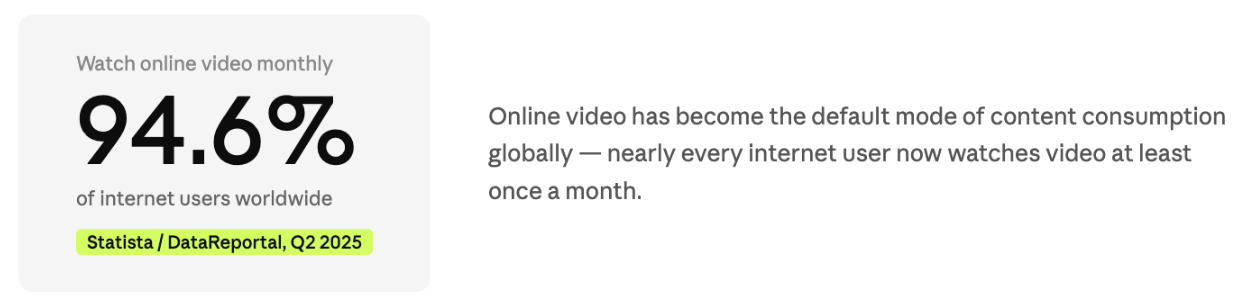

The most visible change is the dedicated video block on article pages. It responds to a well-documented shift in how audiences consume information online.

According to Statista and DataReportal data from Q2 2025, 94.6% of internet users worldwide now watch online videos on a monthly basis.

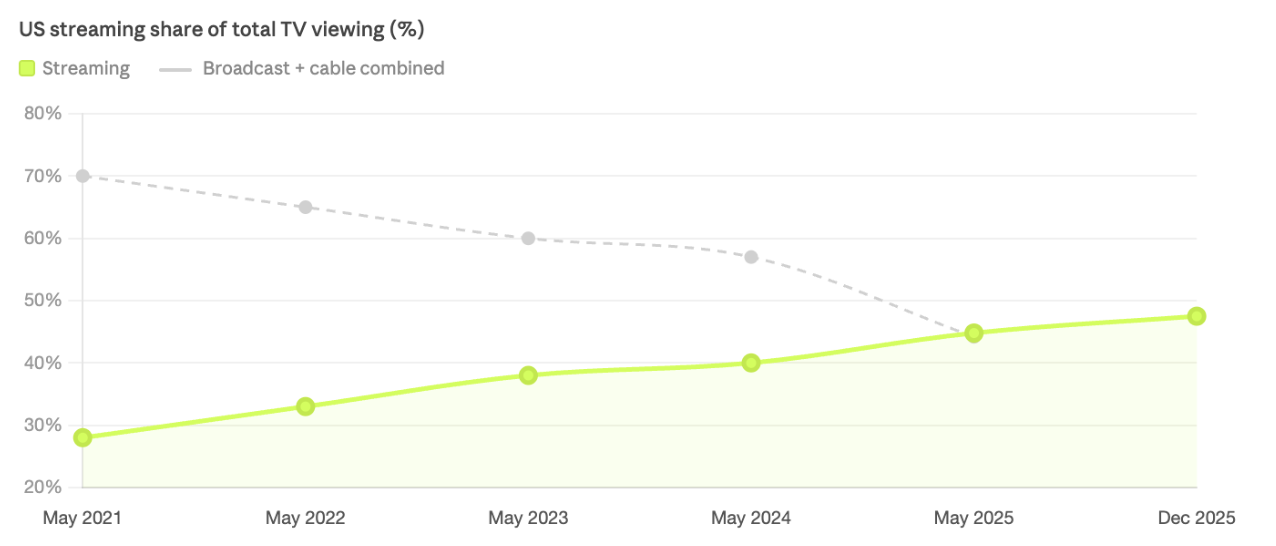

The shift from traditional to digital viewing has reached a milestone: in May 2025, streaming overtook the combined share of broadcast and cable television for the first time ever in the US, accounting for 44.8% of total TV viewing. By December 2025 that share had climbed to a record 47.5% (Nielsen The Gauge, January 2026).

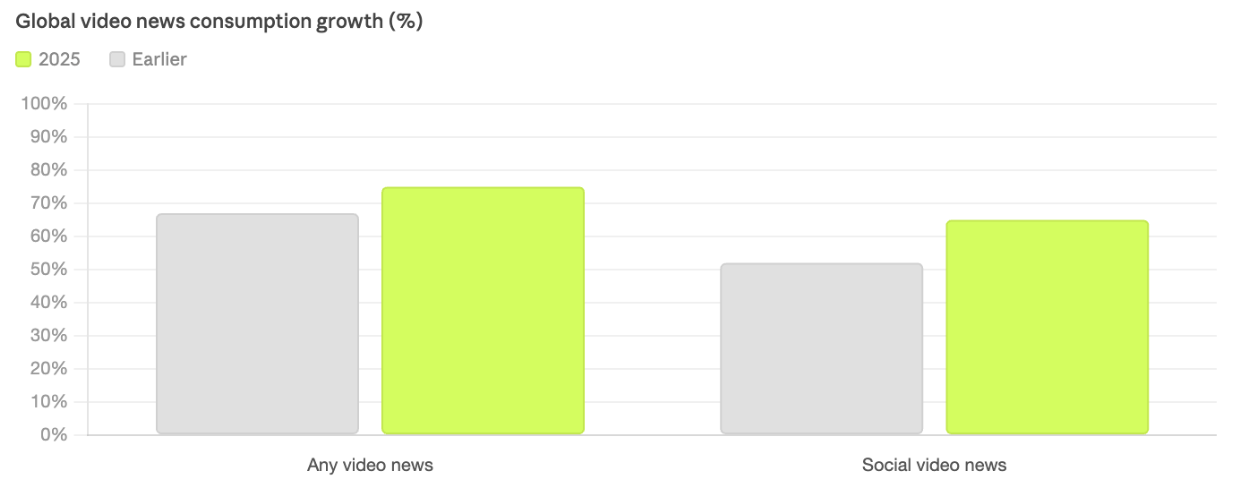

The shift is just as visible in the news sector. According to the Reuters Institute Digital News Report 2025 the proportion of people consuming video news globally jumped from 67% to 75% in just two years, with social video rising from 52% in 2020 to 65% in 2025.

At BeInCrypto’s Executive Council earlier this year, senior leaders from Bitpanda, Dune, and Libertex worked through the same signals: SimilarWeb data presented at the session showed that average monthly web traffic to the top 1,000 sites has declined more than 11% over five years. These homepage and article page updates are a product of that direction, not a reaction to it.

“Video is no longer a secondary format for us,” says Morhunova. “We’re investing significantly in video production, and the new designs reflect that by surfacing video content much earlier in the user journey. The goal is for video to be a natural part of how users consume crypto news on BeInCrypto.”

Social CTAs: Extending the Reader’s Journey

New call-to-action blocks across article pages connect editorial content to BeInCrypto’s social channels, creating more touchpoints beyond the article itself.

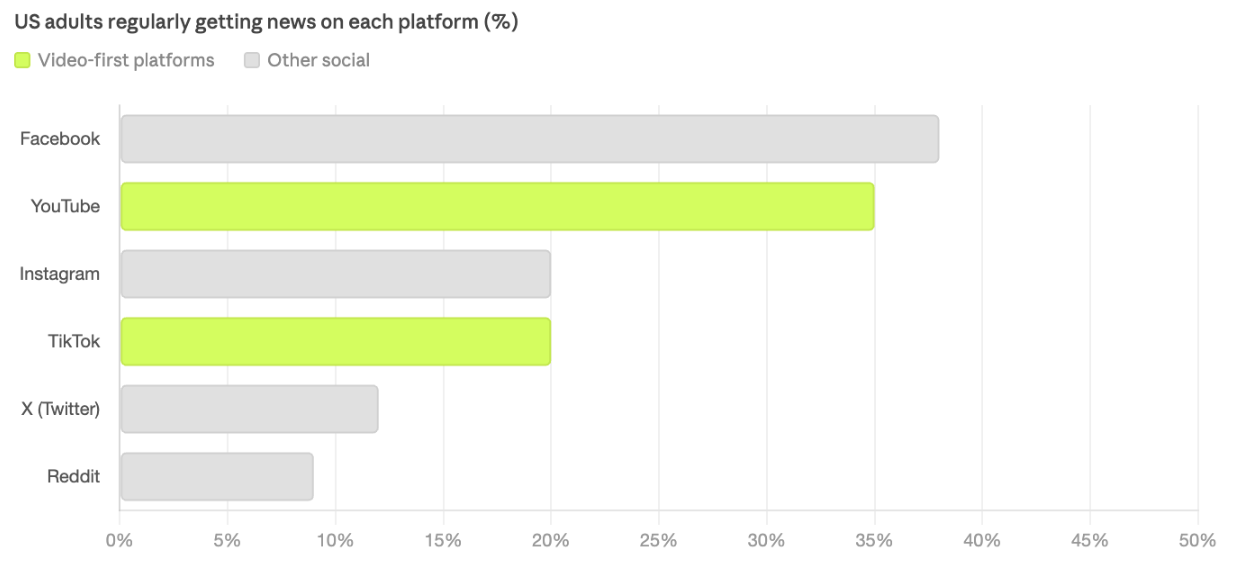

According to the Reuters Institute Digital News Report 2025, social media and video have now displaced television as the primary news source in the US for the first time. Pew Research Center data from September 2025 adds further detail: one in five US adults now regularly get news on TikTok, up from just 3% in 2020; the fastest growth of any platform Pew has studied for news consumption.

- YouTube and Facebook are the top two platforms for news overall, with 35% and 38% of US adults getting news there regularly (Pew Research Center, August 2025).

This is not a trend unique to BeInCrypto. According to Meltwater and We Are Social’s Digital 2026 report (October 2025), social media ads are now the top driver of brand awareness for internet users aged 16 to 34, ahead of both search engines and TV advertising. The platforms where people discover content are the same platforms where they discover brands. Building stronger connections between editorial and social is how media outlets stay relevant in that environment.

Part of a Broader Roadmap

The September 2025 redesign established the platform architecture. This update addresses the content surfaces that matter most. What comes next goes further: expanded markets and TradFi data widgets, the next phase of the Experts Network pages, and continued improvements across all 26 language editions.

“We’re systematically modernizing BeInCrypto’s frontend architecture to be faster, more modular, and better suited to the diverse global audience we serve,” says Morhunova.

BeInCrypto reaches millions of monthly readers across 26 languages. These updates are part of a continuous investment in the product experience that underpins that reach, and a signal to partners that the platform is evolving to match where audiences are going.

The post BeInCrypto Expands Content Experience with New Homepage and Article Features appeared first on BeInCrypto.

Junelle Lyles Speaks On Noah Lyles’ Reaction To Wedding Dress

Elements of Financial Statements

Telegraph Fantasy Football tips: Game Week 32

-

NewsBeat6 days ago

NewsBeat6 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Theodora Dress

-

Crypto World7 days ago

Crypto World7 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos5 days ago

News Videos5 days agoSecure crypto trading starts with an FIU-registered

-

Sports3 days ago

Sports3 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World7 days ago

Crypto World7 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

Business1 day ago

Business1 day agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Crypto World3 days ago

Crypto World3 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Politics3 days ago

Politics3 days agoPalestine barred from entering Canada for FIFA Congress

-

Business4 days ago

Business4 days agoCreo Medical agree sale of its manufacturing operation

-

Politics1 day ago

Politics1 day agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Entertainment7 days ago

Entertainment7 days agoBrand New Day’ Footage Reveals the Devastating Impact of ‘Now Way Home’

-

Crypto World3 days ago

Crypto World3 days agoRussia Introduces Bill To Criminalize Unregistered Crypto Services

-

Tech6 days ago

Tech6 days agoMicrosoft adds Windows protections for malicious Remote Desktop files

-

Entertainment7 days ago

Entertainment7 days agoKarol G’s ‘Ultra Raunchy’ Coachella Set Gave ‘Satanic Vibes’

-

Entertainment7 days ago

Entertainment7 days agoHow Babylon 5 Turned Brief Side Story Into Emotional Masterpiece

-

Tech5 days ago

Tech5 days ago‘Avatar: Aang, The Last Airbender’ Leaked Online. Some Fans Say Paramount Deserves the Fallout

-

Tech2 days ago

Tech2 days agoAuto Enthusiast Scores Running Tesla Model 3 for Two Grand and Turns It Into Bare-Bones Go-Kart

-

Tech7 days ago

Tech7 days agoWhat was the first ransomware attack to demand payment in Bitcoin?

-

Business7 days ago

Business7 days agoIntuitive Machines Stock Climbs 2.4% as $180M NASA Lunar Contract and $900M Revenue Outlook Fuel Momentum

You must be logged in to post a comment Login