Crypto World

Michael Saylor Reveals the One Metric Keeping MicroStrategy’s Bitcoin Play Sustainable

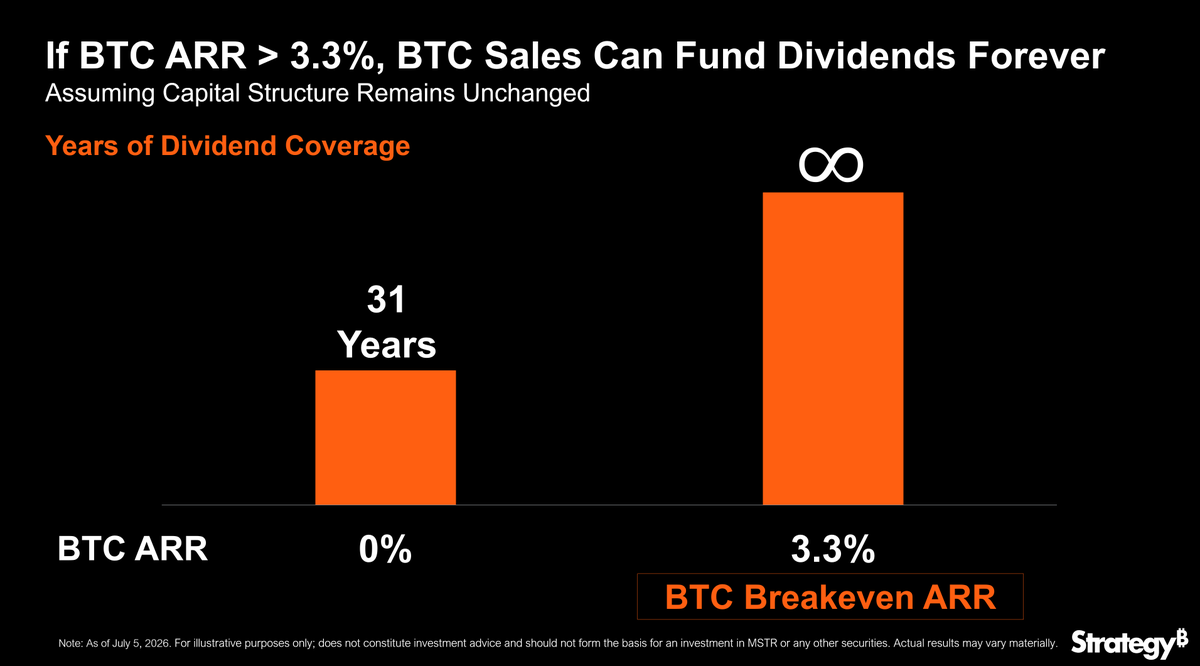

Michael Saylor spotlighted Strategy’s BTC Breakeven ARR on Tuesday, July 7. He argued Bitcoin (BTC) only needs 3.3% yearly growth to fund the firm’s preferred dividends from capital gains indefinitely.

The metric divides annual preferred dividend obligations, now roughly $1.76 billion by company figures, by the value of the corporate Bitcoin reserve. Saylor called it one of the most misunderstood numbers attached to Strategy (formerly MicroStrategy).

What BTC Breakeven ARR Means for MicroStrategy

Strategy reports holding 843,775 BTC, worth roughly $53.8 billion with Bitcoin trading near $63,603, and the stack keeps growing. The company disclosed 818,334 BTC in its May earnings release, meaning it added over 25,000 coins through a drawdown.

Saylor, the company’s founder and executive chairman, made the case in a Tuesday post on X (Twitter).

“One of the most misunderstood $MSTR metrics is BTC Breakeven ARR. If BTC appreciates faster than 3.3% over time, BTC capital gains can fund $STRC dividends indefinitely.”

A companion chart from Strategy illustrates the trade-off. At zero Bitcoin growth, the reserve plus a $2.55 billion cash buffer covers about 31 years of payments, per the company’s dashboard. The buffer alone funds roughly 17 months.

The pitch leans on a real track record. MicroStrategy has paid 23 consecutive preferred distributions totaling over $693 million since early 2025, per its Q1 release.

Critics Question the Bitcoin Dividend Math

The model assumes obligations stop compounding, and so far, they have not. Preferred dividends hit $229.5 million in the first quarter of 2026, up from $10.6 million a year earlier. Preferred equity outstanding has swelled past $13.5 billion.

Skeptics also doubt the funding side. JPMorgan recently warned that Strategy’s Bitcoin sales policy could add up to $1.25 billion in sell pressure. On-chain data already pointed to a new Bitcoin sale of 491 BTC on July 1, which was later confirmed to be 7x bigger.

Meanwhile, STRC paid an 11.5% annualized rate in May yet trades below its $100 par target. Preferred holders still price in risk despite the low breakeven hurdle.

Whether 3.3% proves a low bar depends on Bitcoin reclaiming its long-term trend, with the price down nearly 49% from its October peak.

However, coming payments may reveal how much of the burden falls on BTC sales rather than capital gains.

The post Michael Saylor Reveals the One Metric Keeping MicroStrategy’s Bitcoin Play Sustainable appeared first on BeInCrypto.

Smaller Bitcoin transfers have reached levels not seen since the collapse of cryptocurrency exchange FTX amid an ongoing suspected Coldcard hack.

Bitcoin transfers below 1 BTC climbed to their highest daily level since November 2022 on Friday, with 39,600 BTC moved, according to data shared by CryptoQuant head of research Julio Moreno on Saturday.

The figure was just 300 BTC below the 39,900 BTC transferred on Nov. 16, 2022, days after FTX filed for bankruptcy. “The Bitcoin plebs had not moved this amount of BTC in a day since the FTX collapse,” Moreno said, adding that he was encouraged to see users “taking action.”

As the suspected Coldcard hack continues to unfold, the incident has become a broader test for Bitcoin self-custody, reigniting debate over whether users are better protected by controlling their own funds or relying on third-party platforms.

Incident ongoing as Galaxy tracks three attack waves

The surge in small Bitcoin transfers came as researchers continued to uncover new victims of the suspected Coldcard hack, which first surfaced in late July and appeared to remain active at the time of publication.

Galaxy Research, the research arm of crypto investment company Galaxy Digital, reported Saturday that the latest identified wave drained an additional 207.7 BTC, worth about $13.2 million. The theft brought estimated losses to 1,367 BTC ($88.6 million) across 4,585 addresses.

Bitcoin drained from Coldcard wallets. Source: Coldcard Watch

Alex Thorn, Galaxy Digital’s head of firmwide research, warned in an X post on Sunday that the attack was still ongoing and urged users to move funds from Coldcard-generated addresses immediately if they had not already done so.

Thorn said his team continued to identify new victim and attacker addresses, adding that reports from users had helped researchers and authorities track stolen funds.

Coldcard incident reignites self-custody debate

The suspected Coldcard hack has reignited debate over the risks and benefits of Bitcoin self-custody, a core principle of crypto that allows users to control their funds without relying on third parties.

Nick Neuman, CEO of Bitcoin security company Casa, pushed back against claims that “self-custody is over,” arguing that its distributed nature gave users time to react. He estimated that potentially 10 times more Bitcoin was protected through self-custody than was stolen and identified in the attack so far.

Related: SecondFi to wind down after $2.6M ADA theft linked to wallet flaw

The debate also drew responses from traditional finance supporters. Eric Balchunas, senior ETF analyst at Bloomberg, argued that Bitcoin exchange-traded funds (ETFs) provide a safer and more convenient alternative for many users, pointing to the long operating history of the ETF industry. Others pushed back, saying the Coldcard incident was a failure of one wallet provider rather than a failure of self-custody itself.

Magazine: A quantum roadmap would push Bitcoin much higher: Charles Edwards

Minnesota’s statewide crypto ATM ban took effect on Aug. 1, 2026, stopping operators from offering virtual currency kiosks after residents reported nearly $1 million in related scam losses.

Summary

- 134 complaints produced nearly $1 million in reported Minnesota crypto kiosk losses across three years.

- August 1 rules require every Minnesota crypto kiosk offline, with public removal due December 31.

- 2025 FBI data recorded 222 Minnesota kiosk complaints and more than $4 million in losses.

Governor Tim Walz signed Senate File 3868 on May 5 after the measure cleared the state legislature.

The law covers machines that exchange cash, bank credit or another virtual currency for crypto. It does not prevent Minnesotans from buying, selling or holding digital assets through lawful online services. The ban took effect as scheduled, with physical removal due by year-end.

Minnesota crypto ATM ban stops kiosk transactions

Under the enacted Minnesota law, businesses may no longer install, operate, maintain or make a crypto kiosk available for use anywhere in the state. Existing machines had to stop processing transactions by Aug. 1, although operators have until Dec. 31 to remove them from locations visible or accessible to the public.

The Minnesota Department of Commerce said it is working with licensed money-service businesses to secure compliance. Assistant Commissioner Sara Payne said the department can take enforcement action, including legal sanctions and civil penalties, against operators that continue offering kiosk transactions. The public and retailers may also report machines that remain operational.

The state had about 350 licensed kiosks operated by roughly eight to 10 companies when the Senate approved the measure in April. The new rule focuses first on whether a machine is available for use, not whether its cabinet remains temporarily inside a store.

Scam losses pushed lawmakers past earlier safeguards

The Minnesota Department of Commerce recorded 134 crypto kiosk scam complaints from 2023 through 2025, with reported losses approaching $1 million. In 2025 alone, the department counted 70 cases, more than $540,000 in losses and an average loss of nearly $6,800 per transaction.

Officials said many schemes involved fake family emergencies, romance scams or criminals impersonating government and law enforcement personnel. Victims were often told to withdraw cash, find a kiosk and scan a QR code controlled by the scammer.

Commerce Commissioner Grace Arnold gave residents a direct warning: “If someone is telling you to act quickly and send money through a kiosk … it’s a scam.”

Minnesota had introduced licensing, transaction limits, disclosures and other kiosk safeguards in 2024. However, state officials said scammers adapted by coaching victims through warning screens and arranging deposits to avoid existing protections.

FBI data shows broader scope than state complaints

Separate FBI data recorded 222 Minnesota complaints involving crypto kiosks in 2025, with adjusted losses of $4.07 million. Those figures are not directly comparable with the state’s 70 cases and $540,000 total because the agencies use different reporting systems and complaint scopes.

The FBI also cautioned that its loss totals may include other transaction methods used in the same scam. Nationwide, the agency received 13,460 kiosk-related complaints involving $388.98 million in adjusted losses during 2025. More than half of the complaints involved people older than 50.

Minnesota’s action forms part of a wider state crackdown. Tennessee banned crypto ATMs from July 1, while Georgia imposed transaction limits, warnings and some refund requirements. Indiana had already adopted a statewide prohibition. In related coverage, Delaware and New Jersey lawmakers advanced similar proposals.

The next binding date is Dec. 31, 2026. By then, operators must remove publicly visible or accessible machines. Kiosk-only operators must also pay customers any money or crypto still held or owed because of earlier transactions, unless another lawful access method remains available.

Customers may request payment in U.S. dollars at market value or transfer to a chosen crypto wallet. A wallet transfer must occur within 30 days of the request and be recorded on the relevant blockchain. Operators must retain proof for the Minnesota commerce commissioner.

The state has taken a different approach to regulated financial institutions.Another Minnesota law effective Aug. 1 allows banks and credit unions to provide crypto custody under risk-management, cybersecurity and notice requirements.

Commerce will now test whether operators disable every kiosk, complete removals and process required customer payouts before year-end. Residents can file complaints with the department when they find a machine that remains available for use.

Decentralized exchange spot trading rose to about 24% of centralized exchange volume in July 2026, according to The Block’s current DEX-to-CEX data series.

Summary

- July’s DEX-to-CEX spot ratio reached about 24%, according to The Block’s current data series estimate.

- DefiLlama’s trailing data ranked Solana, BNB Chain and Ethereum among the largest spot ecosystems globally.

- Robinhood Chain added July activity after Uniswap deployed four protocol versions from its first day.

The reading was described as the strongest shown in the current series and continued a broader rise in onchain market share since 2024.

The Block calculates the measure by dividing monthly DEX volume by volume on a selected group of centralized exchanges. Its dashboard includes the top 30 decentralized exchanges by volume from DefiLlama. Therefore, the figure does not mean DEXs handled 24% of combined spot trading. It means DEX activity equaled roughly 24% of the covered CEX total.

DEX spot volume ratio reaches about 24% in July

The July figure followed a faster expansion that began in 2025. The ratio remained below 10% for much of 2024 before rising as traders increasingly used permissionless markets for memecoins, newly issued assets and products unavailable on large centralized platforms.

However, the reading also came during a weaker period for centralized spot trading. Talos reported that total exchange spot volume fell 28% quarter over quarter to $2.32 trillion in the second quarter of 2026. Lower CEX activity can lift the ratio even when DEX volume does not reach an absolute record.

Current DefiLlama data shows that activity remains spread across several networks. Its Aug. 2 trailing 30-day rankings listed Solana at about $49.86 billion, BNB Chain at $31.04 billion, Ethereum at $28.84 billion and Base at $22.38 billion in spot DEX volume. Robinhood Chain added another $14.48 billion over the same rolling period.

New chains and wider token access supported onchain trading

Robinhood Chain was one of July’s clearest new sources of DEX activity. Uniswap Labs announced that Uniswap v2, v3, v4 and UniswapX went live on the network on July 2, one day after its public mainnet launch. The deployment supported crypto assets and Robinhood Stock Tokens through Uniswap’s web app, wallet and API.

CoinDesk Data later estimated that Robinhood Chain averaged about $690 million in daily DEX and aggregator volume over a seven-day period. Activity peaked at $943.6 million on July 11, while Uniswap accounted for about 99.5% of the network’s seven-day DEX volume.

The stock tokens were available in more than 120 countries but were not offered to U.S. users. Early trading also included memecoins rather than being limited to tokenized equities and other real-world assets.

As crypto.news reported, Robinhood Chain drove a sharp increase in Uniswap activity and passed $1 billion in cumulative swap volume during its first ten days. However, the role of speculative tokens makes sustained activity more important than launch-week totals.

Other ecosystems entered July with established onchain liquidity. Solana DEX volume exceeded $800 billion during the first part of 2025, while Jupiter remained a major routing layer for trades.

The “record” description needs a methodology caveat

The claim that July produced the “highest level since tracking began in 2019” requires qualification. The Block’s current chart supports the reported July reading, but older reports from the same publisher described higher figures under earlier versions of its data.

In June 2025, The Block reported that DEXs reached 25% of CEX spot volume during May. One month later, it reported a 29% ratio for June. Both historical figures are above July 2026’s roughly 24% reading.

The difference may reflect historical data revisions, changes in the exchanges counted or adjustments to volume filtering. However, the public description on the current dashboard does not explain why its historical readings differ from the publisher’s earlier articles.

A separate CoinGecko study used a different group of exchanges. It placed DEX spot share at 24.5% in June 2025 before the measure returned to about 13%–14% by January 2026. CoinGecko linked the earlier peak partly to Binance Alpha 2.0 routing trades through PancakeSwap.

CoinGecko’s top-20 exchange coverage and The Block’s current top-30-DEX methodology are not directly interchangeable. July can therefore be described safely as the highest reading in the current cited series. Calling it an uncontested market-wide record would go beyond the available methodology disclosures.

What comes next for the DEX-to-CEX ratio

The August reading will show whether the ratio can remain near one-quarter of covered CEX volume after July’s new-chain activity settles. Traders will also watch whether Robinhood Chain retains its early volume and whether Solana, BNB Chain, Ethereum and Base maintain their current pace.

Absolute volume will matter alongside market share. A rising ratio caused mainly by falling CEX activity would describe a different market structure from one driven by growing DEX liquidity, more users and deeper trading pools. Changes to protocol coverage or the exchanges included in the calculation could also revise historical readings.

No verified token-price move can be attributed solely to July’s ratio. The data shows where spot trades occurred, not why individual assets moved. The next completed monthly datasets should provide a clearer test of whether July marked a durable change or a temporary peak connected to new products and network launches.

South Korea’s five major won-based crypto exchanges recorded 560.3 billion won, about $367 million, in net stablecoin outflows to overseas platforms in June 2026.

Summary

- 18 consecutive months of stablecoin outflows ended June with 560.3 billion won leaving South Korea.

- June transfers sent 2.7625 trillion won overseas and returned 2.2022 trillion won to Korean exchanges.

- Reported uses include overseas derivatives, RWA products, DeFi and staking services unavailable on Korean exchanges.

The figure extended the country’s uninterrupted outflow run to 18 months.The figures came from Financial Supervisory Service data submitted to People Power Party lawmaker Lee Jong-wook and reported by Yonhap News on Aug. 2. Upbit, Bithumb, Coinone, Korbit and Gopax sent 2.7625 trillion won in stablecoins abroad during June. They received 2.2022 trillion won from overseas exchanges.

South Korean stablecoin outflows reach 560.3 billion won

The latest monthly total continued an uninterrupted net-outflow streak that began in January 2025, when the available data series started. Every month since then, stablecoin withdrawals to foreign exchanges have exceeded deposits returning to the five Korean platforms.

June’s net outflow rose from 477.1 billion won in May but remained below January’s 1.1429 trillion won. The monthly figures show persistent outward movement despite substantial changes in the amounts transferred.

The gap also remained large during the second quarter. Between April and June, net stablecoin outflows reached 1.6872 trillion won. During the same period, Korean retail investors recorded 1.6185 trillion won in net sales of overseas stocks, according to Korea Securities Depository figures cited by Yonhap.

In June alone, overseas stock purchases exceeded sales by $472.54 million, or about 722 billion won using the month’s average exchange rate. Stablecoin net outflows therefore equaled 77.6% of Korean investors’ net overseas stock purchases. However, the comparison does not prove that both flows involved the same investors or strategies.

Overseas derivatives appear to drive stablecoin demand

The report said the transferred stablecoins are “believed to be used mainly” for products unavailable on domestic exchanges. These include crypto and equity derivatives, tokenized real-world assets, decentralized finance services and staking products.

Some overseas platforms offer futures and other leveraged products linked to cryptocurrencies and major Korean stocks, including Samsung Electronics, SK Hynix and Hyundai Motor. However, the FSS figures track transfers between exchanges rather than each wallet’s final activity. The proposed connection to specific products remains an estimate, not a transaction-by-transaction finding.

The overseas shift comes as domestic trading activity has weakened. Crypto.news reported that trading volume across the five major won exchanges fell 54.6% year over year during the first half of 2026. Lower local activity provides context, although the available data does not establish it as the cause of the overseas transfers.

Investor protection pressure meets delayed legislation

Lee called for faster safeguards, saying investors were “being left defenseless against high-risk derivatives on foreign exchanges.” He asked the government to review its investor protection and management framework as more funds move offshore.

South Korea is already working on broader digital asset rules. At a March 4 Virtual Asset Committee meeting, the Financial Services Commission discussed exchange internal controls, security standards, strict compensation duties and possible rules for stablecoin issuers. The commission said it planned further consultations before legislation moved forward.

However, the details remain unsettled. In January, the FSC cautioned that major provisions covering stablecoin issuers and ownership structures had not been finalized.

More recently, as crypto.news reported, the regulator told lawmakers it intended to prepare a consolidated Digital Asset Basic Act covering stablecoins, exchanges, disclosures and operational controls.

The next monthly exchange data will show whether July extended the outflow streak to 19 months. Regulators may also face pressure to distinguish ordinary cross-border transfers from flows connected to leveraged derivatives, DeFi and other higher-risk services.

For now, the June figures document movements between Korean and overseas exchanges. They do not identify individual users, destination platforms or final investments. Any policy response will depend on further regulatory reviews and progress on the Digital Asset Basic Act.

Bitcoin’s price dipped to another multi-week low at just over $62,000 on Saturday evening but rebounded to $63,500 on Sunday morning after US President Donald Trump said he had canceled the planned attacks against Iran.

Most larger-cap alts have turned green with minor increases, led by Cardano’s native token, which has jumped by 9%.

BTC Returns to Over $63K

The business week began on a more positive note after last weekend’s de-escalation in the Middle East. Bitcoin had remained above $64,000, and then it tapped $65,600 on a couple of occasions on Monday. However, it couldn’t continue upward, and uncertainty ahead of the FOMC meeting led investors to de-risk by offloading BTC, which resulted in a massive drop to $62,800.

Volatility remained high before and after the event, with the asset going up and down between $63,000 and $65,000. It rocketed to just over the upper boundary on Friday morning, where it was rejected once again.

The subsequent leg down was even more painful as bitcoin dipped to $62,400 for the first time in over two weeks. It managed to rebound to $63,000 on Saturday before it dropped once again to $62,100 (on most exchanges). The situation improved on Sunday morning after US President Trump canceled planned attacks against Iran, and BTC jumped to $63,500.

Its market cap has reclaimed $1.270 trillion, while its dominance over the alts remains below 57% on CG.

ADA Soars

Most larger-cap alts have turned green in the past day. XRP has defended the $1.05 support, which has been described as a major support level by analysts that can propel the next rally. SOL is up by 1%, and so is HYPE. ETH, TRX, DOGE, RAIN, and ZEC have marked minor increases.

Cardano’s native token has become today’s top performer, surging by 9% to $0.185. XLM, DOT, AVAX, NEAR, PEPE, and WLD have marked gains of up to 4%.

The total crypto market cap is up by $40 billion since yesterday’s low and is up to $2.250 trillion on CG.

The post Cardano Rockets by 9%, Bitcoin Reclaims $63K After War De-Escalation: Weekend Watch appeared first on CryptoPotato.

Bitcoin’s price is on the move today, prompted by the latest developments on the US-Iran war front, but this time in the opposite direction.

After it slipped to another multi-week low yesterday evening, the cryptocurrency has rebounded by approximately $1,500 and now sits at around $63,500. The reason for this is the major de-escalation announced by the POTUS hours ago.

US President Trump announced on his social media platform, Truth Social, that although his country’s military remains “locked and loaded” to continue attacking Iran, they were asked by the Middle Eastern country and other nations in the region to pause the strikes for now.

He added that those countries are working on a new deal that would include the “immediate, complete and total opening of the Hormuz Strait, and an end to Iran’s nuclear threat.”

“Based on this request, I have agreed, for the future benefit of the WORLD and, likewise, the survival of a successful and prosperous Iran, to cancel the attack, subject to being able to rapidly make a DEAL. The Country of Israel joins me in this commitment. Get to work, everybody, and get it DONE.”

As mentioned above, BTC reacted immediately with a notable rebound. It had dipped to an 18-day low at $62,200 yesterday evening as the tension between the two had increased once again, with new planned strikes. In addition, there are other factors, such as ETF exodus and technical indicators, that suggested the cryptocurrency could face another leg down soon.

For now, though, the war developments appear to have the most significant impact on bitcoin’s price moves, and essentially every de-escalation brings back hope to the market. The actual impact is likely to be experienced on Monday morning, as it has happened numerous times in the past several weeks.

The post Bitcoin Price Rebounds as Trump Calls Off Iran Strikes and Hints at a Deal appeared first on CryptoPotato.

Leading Bitcoin treasury company Strategy’s results for the second quarter show a loss of over $8 billion, while crypto exchange Coinbase reported a 14% quarterly revenue loss.

According to the two companies’ latest earnings reports released on Thursday, Strategy lost over $8.23 billion in its operations after recording an unrealized loss of $8.32 billion in the second quarter of 2026. The largest crypto exchange by volume in the U.S., Coinbase, also suffered a 19% annual revenue decline, while its trading volumes went down 24% to slightly above $145 billion.

Q2 2026 Bitcoin Price Cooldown Sees Strategy Draw Losses

Strategy grew its BTC holdings by 846 units within the three-month period ending June 30. In its report, the company’s chief executive, Phong Le, said it reduced its convertible debt to just under $7 billion and increased its U.S. dollar holdings and Bitcoin per share by 12% and 5%, respectively. The Bitcoin treasury had seen a $10 billion income in the second quarter of 2025, but Bitcoin’s dull price performance this year has supposedly caused a net loss of $8.22 billion.

“Our objective is for STRC to trade over time at $99 to $100. If STRC trades below $100, we intend to repurchase STRC shares in a regular and disciplined manner, scaling our repurchases according to market price and liquidity. These repurchases are an attractive use of capital that reduces our future preferred dividend requirements at a discount while allowing independent market demand to establish a healthy and sustainable market,” the CEO explained.

In the total revenue column for the quarter, Strategy announced it had a 6.9% increase in the last 12 months, jumping from $114.5 million in Q2 2025 to over $122 million in Q2 2026. The gross profits made by the company’s business reached $81.6 million, which it counted as a 69% gross margin compared to the previous year’s second quarter’s $78.7 million.

“In the midst of this phase of muted bitcoin sentiment and market skepticism, we continue to evolve our business model and establish Digital Credit as a new asset class. Our plan is to return STRC to health with stable demand, high liquidity, and low volatility trading near par. We believe this is the best way to create shareholder value over the long term,” executive chairman and founder Michael Saylor told reporters.

Coinbase Revenue Drops after Trading Slump, Prediction Market Thrives

Meanwhile, Coinbase’s first half of the year continues to yield lower-than-expected earnings following a continued loss trend in both quarters, but its prediction market sector has risen by more than $100% quarter-over-quarter. The exchange revealed its revenue had taken a 19% hit in the 12 months ending June 30, and its transaction revenue dropped 21%. As seen in the report on net losses, the trading company’s earnings before interest, taxes, depreciation, and amortization reached $208 million, while it recorded over $300 million in losses after adjustments.

Coinbase’s fee collection from subscriptions and services slumped by 5% in the quarter but accounted for almost half of its net revenue in that period. Consumer transactional revenue also fell by 20% compared to Q1 2026, which the company attributed to a 24% decline in crypto spot trading volume. At the end of the quarter, the average amount of USDC held across Coinbase products hit a record high of $20 billion, accounting for more than 30% of all USDC in circulation.

The post Strategy Posts $8.2B Q2 Loss as Coinbase Revenue Falls 19% appeared first on CryptoPotato.

Federal prosecutors are continuing to litigate the fallout from the collapse of FTX, as defense teams push back on what juries can hear and how certain market activities are regulated. In the Southern District of New York (SDNY), Michelle Bond—whose husband, former FTX executive Ryan Salame, is serving a 90-month sentence after pleading guilty in 2023—has asked the court to block references to that guilty plea in a campaign finance case.

At the same time, other SDNY-related crypto-adjacent legal fights are highlighting how prediction markets and event contracts can collide with insider-trading and commodity regulation arguments. Separate actions involving a former congressman’s Kalshi trades and a US soldier accused of making a large Polymarket bet underscore that courts may soon be forced to clarify both evidentiary rules and the legal classification of event contracts.

Key takeaways

- Michelle Bond’s legal team asked SDNY to exclude evidence tied to Ryan Salame’s guilty plea, arguing it has little relevance to Bond’s alleged intent or knowledge.

- In a separate CFTC case, former New York Rep. George Santos was ordered to pay $35,000 over trades on Kalshi’s event contracts, with the regulator citing misleading posts about his planned attendance at the 2026 State of the Union.

- A US soldier accused of earning more than $400,000 on Polymarket event contracts is seeking dismissal, challenging whether the Commodity Exchange Act can clearly apply to event contracts as “swaps.”

- Across these matters, the central pressure points are evidentiary fairness for defendants and regulatory clarity for prediction-market participants.

Bond seeks to bar Salame’s guilty plea in campaign finance fight

According to a Friday filing in the US District Court for the Southern District of New York, Michelle Bond’s attorneys asked the court to preclude the government from introducing evidence about Ryan Salame’s guilty plea or any “related plea materials” in her campaign finance case.

Bond faces charges over alleged unlawful campaign funding tied to her unsuccessful 2022 congressional run in New York. The prosecution’s theory, as described in the filing, is that contributions supporting Bond’s campaign were partially funded through FTX arrangements facilitated by Salame.

Salame pleaded guilty in 2023 and is currently serving a 90-month sentence connected to conduct arising from FTX’s 2022 collapse. In Bond’s motion, her lawyers argued that Salame’s plea—where he admitted to making political contributions in Bond’s name funded by transfers from accounts associated with an FTX-linked entity—should not be treated as evidence against Bond herself.

“The Court should preclude the government from introducing or referring to Mr. Salame’s guilty plea or any related plea materials, because their minimal probative value is substantially outweighed by the risk of unfair prejudice to Ms. Bond,” the filing states.

Bond’s team further said that the plea materials do not meaningfully bear on Bond’s state of mind. They characterized the plea as an admission of Salame’s own guilt, not proof of Bond’s knowledge or participation in the charged conduct, quoting from the motion: “[…] Mr. Salame’s plea materials lack any probative value as to Ms. Bond’s guilt, knowledge, or intent. Mr. Salame’s plea is an admission of his own guilt, not evidence of Ms. Bond’s state of mind or participation in any charged offense.”

How personal litigation could become part of the argument

Bond’s motion also requested that the court allow information connected to her “contemporaneous divorce and custody proceedings.” Her lawyers appear to be positioning that personal context to rebut the government’s characterization of Bond as an “ordinary ‘individual’ donor,” despite her and Salame having divorced before the alleged criminal conduct.

While the filing’s request reflects a broader strategy often used in criminal litigation—attempting to shape how jurors interpret the campaign contributions and the parties’ relationship—the court’s decision will determine what personal-history evidence, if any, is ultimately presented.

CFTC penalizes George Santos for Kalshi event-contract trading

Separate from the FTX-linked litigation, the US Commodity Futures Trading Commission (CFTC) has issued an order involving George Santos, a former member of the US House of Representatives who was expelled from Congress in 2023. The CFTC ordered Santos to pay $17,500 in a civil monetary penalty plus $17,570 in disgorgement from profits earned through prediction market trading on Kalshi.

According to the CFTC, the relevant trades were tied to event contracts betting on whether Santos would appear at the 2026 State of the Union in Washington, DC. The regulator said Santos posted on social media about his plans to attend or not attend the event, and that these posts contained “material misrepresentations and omissions.”

The CFTC added that after the posts, contract prices moved in a direction favorable to Santos’ positions, enabling him to earn over $17,500.

As part of the CFTC order, Santos is barred from trading on prediction market platforms for three years.

The case also sits in the shadow of Santos’ criminal proceedings. Earlier coverage notes Santos was sentenced to 87 months in prison in 2025 for wire fraud and aggravated identity theft, though he served only three months before his sentence was commuted by US President Donald Trump, as reflected in the article’s background.

Polymarket insider-trading allegations tested under “swap” debate

A more direct challenge to prediction-market regulation is underway in another SDNY matter. Gannon Ken Van Dyke, a US soldier accused of making more than $400,000 trading Polymarket event contracts, is attempting to dismiss the indictment.

As outlined in the background of the case, prosecutors allege that Van Dyke traded using nonpublic information connected to a military operation involving the removal of Venezuelan President Nicolás Maduro in January. The US Department of Justice alleges he used that alleged insider information to wager on whether Maduro would be removed from power, leading to criminal charges filed in April.

In a Friday SDNY filing, Van Dyke’s attorneys submitted a 51-page memorandum supporting a motion to dismiss. Among other arguments, they contend that the Commodity Exchange Act (CEA) is ambiguous in how it treats event contracts as “swaps,” which is relevant to three of the charges.

Van Dyke’s lawyers argue that the ambiguity affects basic fairness: if the “swap” definition is not clear across Congress, agencies, and courts, ordinary citizens may lack “fair notice” that their prediction-market wagers fall under the CEA.

“If Congress, executive branch agencies, and courts all find the ‘swap’ definition ambiguous, how can ordinary citizens have fair notice that prediction market wagers are covered by the CEA?” the filing asks.

The defense also contrasts with the position taken by the CFTC under Chair Michael Selig, which has argued it has “exclusive jurisdiction” over prediction markets by treating event contracts as “swaps.” The dismissal motion suggests that—at least for some counts—those jurisdictional assumptions may not survive if the law is too unclear.

Why these cases matter beyond one courtroom

Taken together, the filings point to two urgent fault lines for the crypto-adjacent prediction market space: what evidence courts allow juries to consider when guilt and intent are contested, and whether the regulatory framework—especially the CEA’s treatment of event contracts—offers enough clarity for enforcement.

As courts weigh motions like Bond’s request to exclude plea materials and Van Dyke’s bid to dismiss based on legal ambiguity, traders, builders, and public officials using event-contract platforms may want to watch how judges define relevance, prejudice, and “fair notice.” The next procedural rulings could signal how far prosecutors can stretch existing statutes—and how tightly defendants can force regulators to justify their classification theories.

The first half of 2026 was the most active six months for crypto exploits on record.

This is according to a new report from Blockaid, which shows hackers stole $1.1 billion across 212 incidents.

Crypto Hacks Top $1.1B in H1 2026

The Blockaid report found that four major incidents involving KelpDAO, Drift, Resolv, and CoW Swap made up roughly $707 million of the total losses.

KelpDAO suffered the largest loss, after hackers stole $292 million worth of crypto by faking a cross-chain message that siphoned off the protocol’s Ethereum reserves. Drift Protocol, a perpetuals exchange built on the Solana chain, also suffered a similarly huge hit, as it was exploited for $285 million within 12 minutes.

Blockaid linked both cases to TraderTraitor, a state-sponsored North Korean subset of the larger Lazarus Group. Humanity Protocol’s $32 million loss was also connected to the same attacker cluster, bringing DPRK-linked losses to $609 million, which is about 55% of all funds stolen during the period.

The pace of attacks also increased through the year, with monthly incidents going from 18 in January to 57 in June. April proved to be the most painful month, as the KelpDAO and Drift Protocol hacks wiped out a combined $577 million to push total losses in that month to $635 million.

Privileged key misuse was the most costly attack type in the first half of 2026, with losses of approximately $790 million, or close to three-quarters of all funds stolen in the period, said Blockaid. Unbacked mint exploits came second in value, led by the $80 million Resolve breach. But the hacks at the code level caused the most casualties, accounting for nearly four out of five attacks by count.

Attack Vectors Change as New Threats Emerge

The report named AI agents as a new target after hackers in May used a prompt injection attack to fool Bankr’s AI agent into approving an unauthorized transaction for about $216,000.

Cross-chain bridges also took a major hit, with attackers breaching the verification systems of KelpDAO and Taiko through forged proofs and attestations accepted by the destination chains.

In addition, security teams faced newer attack methods in 2026, with Blockaid identifying four incidents involving EIP-7702 wallet delegation attacks, where a wallet can hand control to a smart contract. Legacy smart contracts also continue to be a common vulnerability, with data showing around five cases in May and June, including two involving Aztec Connect and one targeting Raydium’s AMM V3.

Recent incidents outside the report period showed the same pressure on crypto infrastructure. For instance, on July 23, AFX Trade, BSquaredNetwork, and Verus were hit in separate attacks on the same day that collectively caused more than $35 million in losses. Recall that Verus had already suffered another exploit about two months earlier, and Blockaid linked both incidents to the same bridge contract and bug class.

Recovery results varied depending on the type of attack. Per the report, code-related incidents sometimes allowed teams to freeze funds or negotiate returns, while attacks involving stolen keys usually ended with the money moving through mixers or cross-chain routes.

The post Crypto Hacks Drain $1.1B in First Half of 2026 Amid 212 Security Incidents appeared first on CryptoPotato.

Holders of Strategy’s (MSTR) high-yielding preferred stock STRC will not see a dividend increase in August.

Led by Executive Chairman Michael Saylor, Strategy is maintaining the current 12% dividend on the shares.

STRC investors may have been expecting as much as a 50-basis-point hike in the dividend as Strategy has customarily raised the payout anytime the stock traded sizably below its par value ($100) for the month.

As recently as July 1, Strategy had lifted the dividend 50 basis points following June’s plunge in STRC to as low as $71.

While that hike — along with Strategy’s sale of some bitcoin to fund dividends, and a bit of stabilization in the price of bitcoin — helped STRC bounce in July to the current $89.46, that level is still significantly below par.

CEO Phong Le yesterday said Strategy’s Corporate Objective is for STRC to trade at $99-$100 over time.

Nevertheless, the company is under no obligation to raise the dividend and chose not to do so this month.

New on Disney+ and Hulu in August 2026 — List of Movies and Shows

Tarik Skubal to Dodgers nothing to complain about in Fantasy Baseball, but real baseball is another matter

Predator EXPOSED On Financial Audit

-

Sports6 days ago

Sports6 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business3 days ago

Business3 days agoWhy Trees Belong on the Risk Register

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Wit & Wisdom

-

Tech6 days ago

Tech6 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Politics1 day ago

Politics1 day agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Politics6 days ago

Politics6 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Crypto World17 hours ago

Crypto World17 hours agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics5 days ago

Politics5 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Entertainment5 days ago

Entertainment5 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

News Videos6 days ago

News Videos6 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Business4 days ago

Business4 days agoMajor shareholder moves on Canyon

-

Politics7 days ago

Politics7 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

News Videos3 days ago

News Videos3 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World1 day ago

Crypto World1 day agoXRP Ledger v3.3.0 brings five institutional features

-

Crypto World4 days ago

Crypto World4 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech5 days ago

Tech5 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos5 days ago

News Videos5 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Sports2 days ago

Sports2 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Politics3 days ago

Politics3 days agoLuke Littler’s dominance sparks GOAT debate

-

Business4 days ago

Business4 days agoJohnson & Johnson agrees to $5.5B settlement over talc cancer claims

You must be logged in to post a comment Login