Crypto World

Nebius (NBIS) Stock Plunges 17% on Meta’s Cloud Infrastructure Ambitions

Key Takeaways

- Shares of Nebius Group (NBIS) plummeted 17% during Wednesday’s session, hitting an intraday low of $228.17 with trading volume spiking 85% above typical levels

- A Bloomberg article revealing Meta’s plans to launch a cloud infrastructure service competing with neocloud companies sparked the massive sell-off

- The decline came despite impressive quarterly results showing $399 million in revenue — a 684% year-over-year increase — and an EPS beat of $0.54

- Analyst sentiment remains cautiously optimistic with a “Moderate Buy” rating across 15 analysts; Bank of America maintains a $280 price objective

- Company executives have offloaded more than $124 million in shares over the last three months, raising questions about confidence

Meta’s Cloud Ambitions Trigger Sharp Decline in Nebius Group (NBIS) Stock

Shares of Nebius Group (NBIS) experienced a dramatic 17% decline on Wednesday, touching a session low of $228.17 before settling near $229.18. The stock had closed at $276.17 the previous day. Trading activity exploded, with more than 30 million shares changing hands — approximately 85% higher than normal daily volume.

The catalyst for this sharp downturn was a Bloomberg article detailing Meta Platforms’ intention to commercialize AI computing resources and models — including direct GPU capacity sales. This business model places Meta in direct competition with neocloud specialists such as Nebius and CoreWeave.

CoreWeave similarly experienced a decline exceeding 6% following the same disclosure.

The market reaction extends beyond simple competitive concerns. Meta currently ranks among the world’s largest purchasers of GPU computing power. A strategic pivot toward selling excess capacity rather than solely consuming it could fundamentally reshape supply dynamics across the entire industry.

Neocloud companies including Nebius have benefited tremendously from surging AI infrastructure requirements. Wednesday’s market action demonstrated how rapidly investor confidence can evaporate when threatened by well-capitalized competitors.

Robust Growth Metrics Clash With Valuation Concerns

The stock decline contrasts sharply with Nebius’s operational performance. The company delivered $399 million in quarterly revenue — representing an extraordinary 684% year-over-year expansion. Management exceeded earnings projections by $0.54 per share, posting a loss of just $0.23 compared to the consensus estimate of a $0.77 loss.

The organization’s customer acquisition pipeline has reached unprecedented levels, and underlying demand for AI infrastructure capabilities continues accelerating. However, several Wall Street analysts had previously cautioned that the stock’s valuation appeared overextended following its remarkable pre-earnings rally.

NBIS currently trades above its 50-day moving average of $215.92 and significantly above its 200-day moving average of $142.48. Even after Wednesday’s correction, the stock maintains considerable premium to these technical benchmarks.

With a price-to-earnings multiple of 73.93 and a market capitalization approaching $58 billion, valuation remains elevated. The stock’s beta coefficient of 4.03 underscores its extreme volatility — a characteristic vividly illustrated by Wednesday’s price action.

Wall Street Perspectives and Executive Stock Sales

The analyst community maintains a generally favorable outlook despite divided opinions. Fifteen analysts currently cover the stock, with nine recommending Buy and six maintaining Hold ratings, resulting in a “Moderate Buy” consensus. The mean price target stands at $203.25.

Bank of America established a $280 price objective with a Buy recommendation in early June. BNP Paribas Exane initiated research coverage in June with a Neutral stance and $255 target. Morgan Stanley maintains an Equal Weight rating alongside a $144 price target.

Insider transaction patterns present a more cautious narrative. The Chief Technology Officer divested approximately $3.7 million in stock on June 4th, representing a 5.1% reduction in personal holdings. The Chief Revenue Officer sold roughly $3 million on June 2nd, trimming his stake by 28.6%.

Collectively, company insiders have liquidated more than $124 million in stock value during the past 90 days.

Nevertheless, institutional investors have demonstrated confidence by expanding positions. Orbis Allan Gray, Fred Alger Management, and Morgan Stanley have all increased their shareholdings in recent reporting periods.

Wall Street analysts project Nebius will report a full-year loss of $1.91 per share on average.

SBI Crypto has announced it will shut down its mining pool on July 31, ending a service tied to one of Japan’s largest financial groups and giving miners less than a month to redirect their hashrate.

The pool will stop accepting mining shares, which represent a miner’s contributions in the pool, on the cutoff date, according to SBI Crypto. Shares submitted after that cutoff will not be accepted, and the firm said the pool is expected to operate normally until the shutdown date.

The company urged customers to keep mining with the pool until the cutoff so eligible shares are included in the final payout calculation.

SBI Crypto’s mining pool, according to data from Hashrateindex, accounts for roughly 2% of the Bitcoin network’s total hashrate. The firm did not disclose a reason for the closure in its shutdown notice, and it did not provide current hashrate figures for the pool.

SBI Crypto operates under SBI Group, the Japanese financial conglomerate. The mining pool opened to the public in 2021, with SBI saying at the time that it would support the pool with roughly 1.1 EH/s of its own mining power.

The U.S. Treasury’s Office of Foreign Assets Control (OFAC) added 134 crypto wallet addresses to its ISIS-Khorasan (ISIS-K) sanctions entry on Wednesday, including 131 Tron addresses and 3 Monero addresses.

The TRON wallets received more than $1.4 million since 2023 and sent more than $880,000, according to Chainalysis. Tether froze balances on all 131 Tron addresses.

ISIS-K, the Islamic State affiliate active across Afghanistan, Pakistan and parts of Central Asia, has used its media arm al-Azaim Media Foundation to solicit crypto donations through websites and messaging platforms, Chainalysis said.

Chainalysis said it identified historical donation addresses tied to the group on the Tron, Monero and Bitcoin networks.

The freeze reinforces the role of centralized stablecoin issuers in sanctions enforcement. Tether froze more than $182 million in USDT across five Tron wallets in January under its sanctions compliance policy.

OFAC also sanctioned a Brazil-linked network tied to Primeiro Comando da Capital, or PCC, which Treasury described as Latin America’s largest criminal gang.

The network laundered more than $30 million in U.S.-generated illicit proceeds and used crypto to move funds back to Brazil, according to the Treasury.

The six-figure Strategy stock purchase that FBI Director Kash Patel forgot to disclose last year is currently down 45%.

NOTUS reports that on November 21, 2025, Patel bought between $100,001 and $250,000 worth of shares in the BTC treasury firm. If he invested $100,001, it would now be worth $55,000 and if it were the full $250,000, it would be worth $137,500.

Patel didn’t disclose the purchase until May 26 this year. This is despite rules stating that executive government officials have to report trades worth over $1,000 within a 45-day period.

First-time offenders face a $200 fine, but FBI officials told NOTUS they haven’t fined Patel as of yet.

A letter written by the Deputy Assistant Attorney General William Taylor to the Office of Government Ethics claimed Patel “inadvertently omitted” the transaction after a “miscommunication.”

Taylor added, “Director Patel is in compliance with applicable laws and regulations governing conflicts of interest.”

Strategy’s stock price is also down almost -77% over the past year. The company and its founder, Michael Saylor, has previously said that BTC is an asset that traders should refrain from selling.

Read more: Kash Patel ‘spiderkash’ leak triggers dozens of Solana memecoin scams

Despite this, the company decided to sell 32 BTC (worth $2.5 million) last month. It’s since committed to selling another $1.25 billion worth of BTC in order to cover share buybacks and dividends.

Trump’s crypto ventures dwarf Patel’s Strategy trade

Patel’s Strategy trade appears insignificant when compared to the recent portfolio disclosures from President Donald Trump that reveal that his crypto-related profits from last year totaled over $1 billion.

His Office of Government Ethics disclosure revealed that he made $635 million from selling his TRUMP crypto token, and $526 million from the sale of World Liberty Financial tokens.

He also holds over $50 million worth of ETH and over $50 million worth of BTC.

This is despite the price of TRUMP falling 94% since its launch in January 2025. If someone had invested $1,000 at the time, their holding would be worth $60 today.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Crypto World

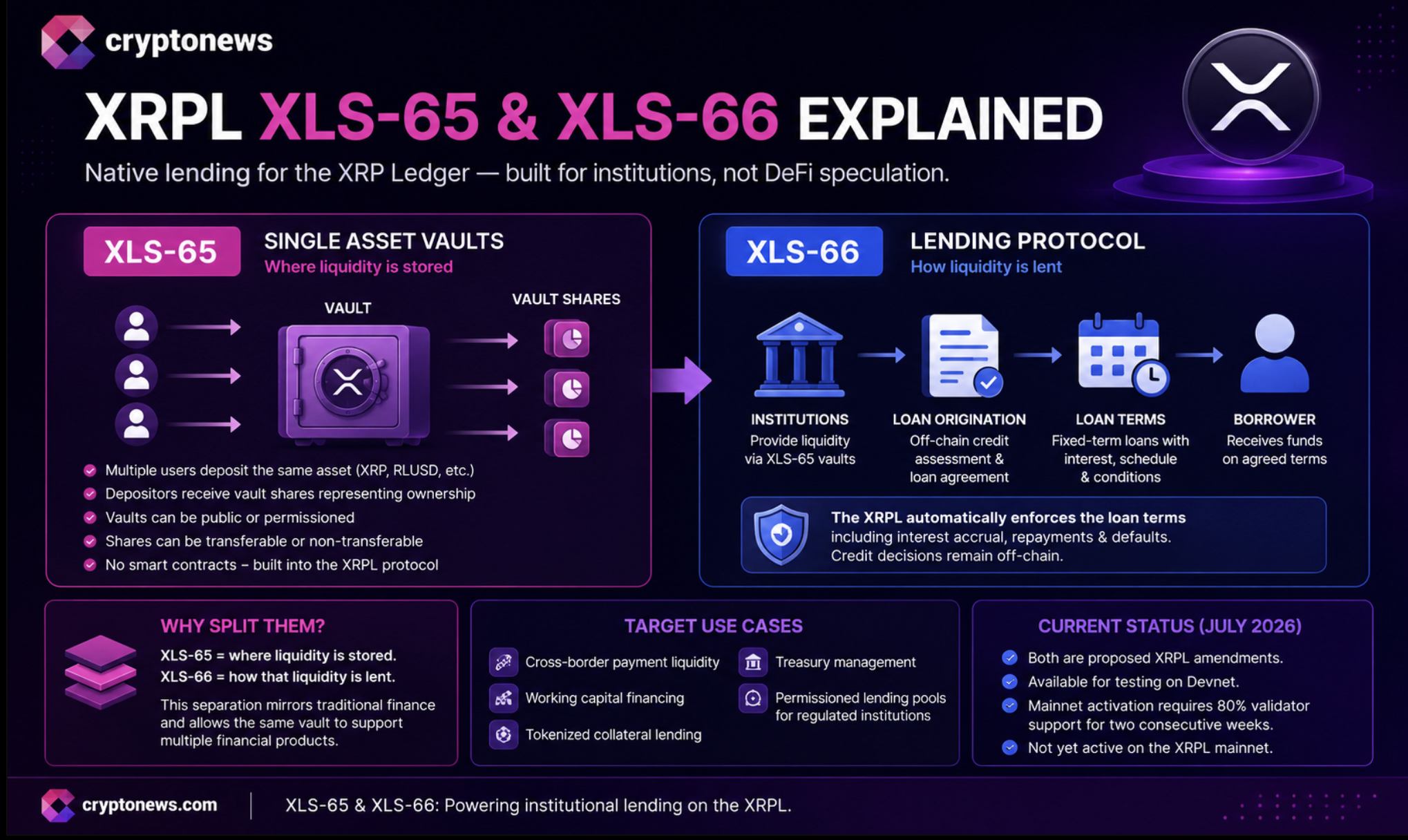

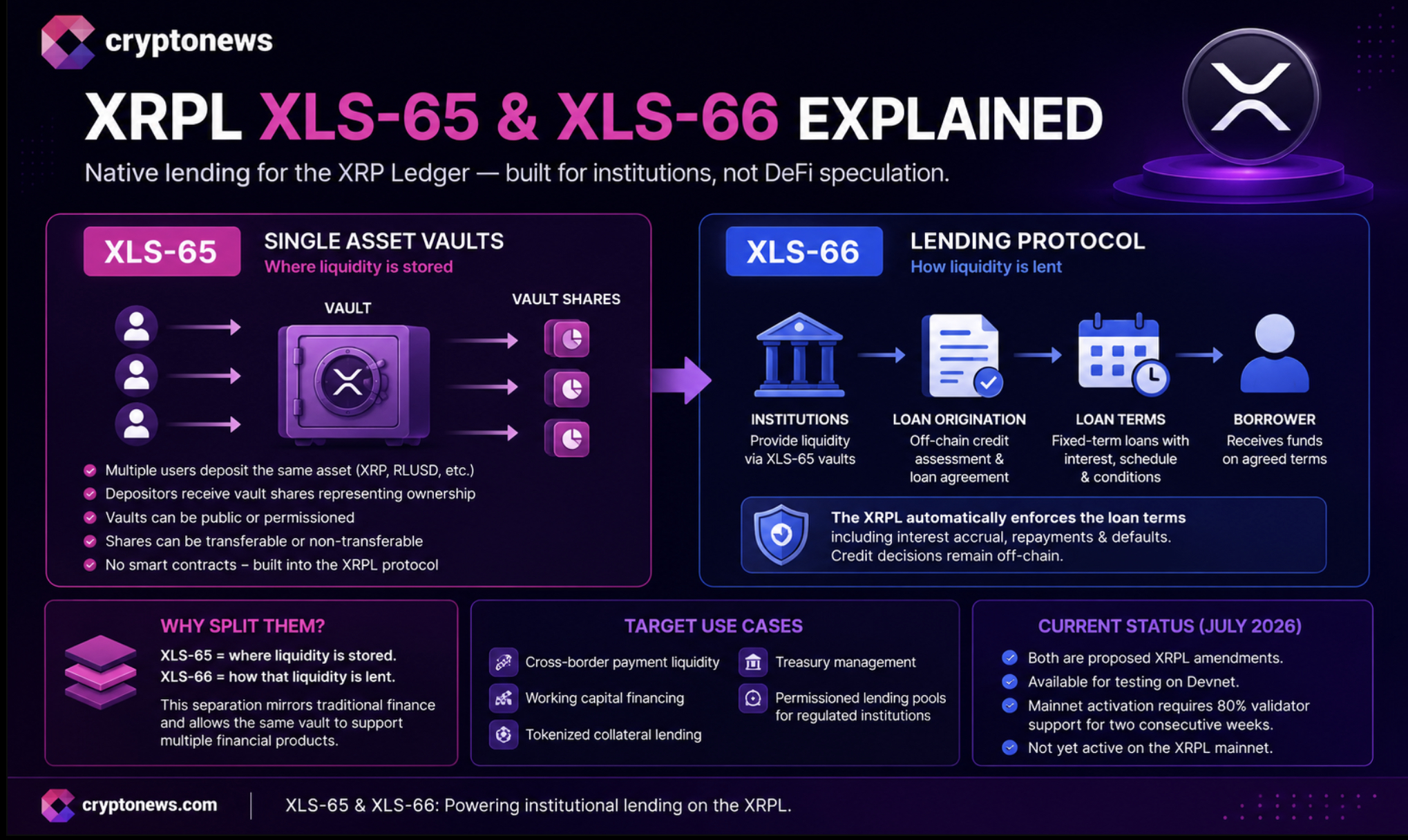

XRP Ledger Lending Amendments Face 80% Validator Hurdle as Institutional Credit Layer Takes Shape

Ripple has formally proposed two XRPL amendments, XLS-65 and XLS-66, that would embed fixed-term institutional credit infrastructure directly into the XRP Ledger. With it rolling, the validator voting is also now active following the Rippled v3.1.0 release in late January 2026.

The framework targets uncollateralized, underwritten lending for regulated financial institutions, positioning XRPL as a credit layer rather than a payments rail. It is a structural shift that hinges entirely on whether the amendments can clear an 80% validator consensus threshold.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

That threshold remains the critical unknown. As of recent tracking, XLS-65 held approximately 8 validator yes votes, or just 22.86%, while XLS-66 had secured around 7, or 20%. Both figures sit well below the sustained 80% support required over two consecutive weeks for mainnet activation.

Discover: The Best Crypto to Diversify Your Portfolio

Single Asset Vaults and the Lending Protocol Mechanics

The two amendments operate as an interlinked system. XLS-65 introduces Single Asset Vaults, permissioned pools where liquidity providers deposit a single token. It holds RLUSD, XRP, tokenized U.S. Treasuries, or other tokenized assets, which are held directly by the vault structure itself. The XLS-65d revision simplified this model by eliminating two previously required transactions, reducing overhead for both depositors and redemption flows.

XLS-66 builds the XRPL lending protocol on top of those vaults, specifying the on-ledger mechanics for loan origination, interest accrual, amortized repayment, and default enforcement via LoanSet, LoanPay, and LoanDelete transactions. Critically, underwriting and borrower credit assessment remain off-chain.

With this, institutional credit desks handle the risk evaluation while XRPL manages execution and the loan lifecycle. This is not Aave-style overcollateralized lending; it is fixed-term, underwritten credit extended to credentialed counterparties.

The compliance architecture runs through XRPL’s existing permissioned domains, credential verification, clawback mechanisms, and freeze functionality. Vault operators can restrict participation to KYC/AML-compliant entities at the protocol level, which is precisely what separates this from open DeFi.

Discover: The Best Token Presales

XRP at $1.00: What Activation Would and Would Not Prove

XRP is trading near the $1.00 level, a psychologically significant threshold that has drawn attention from technical analysts tracking a coiling triangle pattern with progressively higher lows against flat resistance.

XLS-65 and XLS-66 activation would confirm XRPL as a viable credit infrastructure layer, but the demand signal that actually moves price is institutional adoption. Price movement will depend on whether regulated entities deploy capital into RLUSD-funded vaults at scale.

The amendments are currently testable on devnet, and developers can integrate against the lending stack ahead of mainnet activation. XRP’s market performance in the near term will be shaped more by whether validator momentum accelerates toward that 80% threshold than by any single technical level. The framework is credible; the activation path is not yet assured.

Discover: The Best Crypto to Diversify Your Portfolio

The post XRP Ledger Lending Amendments Face 80% Validator Hurdle as Institutional Credit Layer Takes Shape appeared first on Cryptonews.

Tether and Circle built their businesses by keeping the interest on the dollars behind their coins. A new kind of stablecoin, run and owned by a group instead of a single company, shares that money instead. Here is how the consortium model works and why it is spreading.

Summary

- A consortium stablecoin is a fiat-backed token issued and governed by a group of companies instead of a single issuer, with two defining features: shared governance and shared reserve income.

- It contrasts with single-issuer stablecoins such as Tether’s USDT and Circle’s USDC, where one company controls the network and keeps the interest earned on reserves.

- The model is spreading because stablecoin regulation has clarified, the market has grown past $300 billion, and partners increasingly want a share of the reserve income that has made incumbents enormously profitable.

- Leading examples include Open USD, backed by more than 140 companies, the Paxos-led Global Dollar Network, and Europe’s bank-led Qivalis, while the earlier Centre Consortium behind USDC shows the model can also fracture.

- The consortium approach aligns incentives and challenges incumbent economics, but it faces real risks around coordination, governance, and the difficulty of shipping a product agreed on by many stakeholders.

A consortium stablecoin is a digital dollar, or other fiat-pegged token, that is issued and governed collectively by a group of companies rather than controlled by one. The defining idea is shared ownership of both the decisions and the economics: a board drawn from the partner companies sets the rules, and the income earned on the reserves backing the coin is distributed among those partners instead of kept by a single issuer. That structure is a deliberate break from the model that built the stablecoin giants, and it has become one of the most important trends in digital money.

This explainer covers what makes a stablecoin a consortium stablecoin, why the model is emerging now, the leading examples, and the risks that come with running a coin by committee.

Consortium versus single-issuer stablecoins

To understand the consortium model, start with the model it is reacting against. Most of today’s major stablecoins are single-issuer coins. One company creates the token, holds the dollar reserves that back it, collects the interest those reserves earn, and keeps the profit. Tether, which issues USDT, and Circle, which issues USDC, are the dominant examples, and together they control roughly 80 percent of a stablecoin market worth more than $300 billion. Their businesses are simple and enormously profitable: take in dollars, park them in safe assets like Treasury bills, and keep the yield while the token circulates freely.

That reserve income is the heart of the matter. When interest rates are meaningful, the interest on billions of dollars of reserves adds up to billions in revenue. The single issuer keeps that money, which is what makes issuing a large stablecoin one of the best businesses in finance. A partial exception is USDC, where Circle shares a large portion of the economics with Coinbase in exchange for distribution, a hint of the shared-economics idea taken further by the consortium model.

A consortium stablecoin rearranges this in two ways. First, no single company controls the network; a group governs it collectively through a shared board. Second, the reserve income is not kept by one issuer but distributed among the participating companies, usually after a management fee that funds operations. The coin still works the same way for a user, redeemable one-for-one for a dollar held in reserve, but the ownership of the decisions and the money behind it is spread across many hands instead of being concentrated in one. That is the essential difference.

The two defining features: shared governance and shared economics

Every consortium stablecoin rests on the same two pillars, and it is worth being precise about each. The first is shared, neutral governance. Instead of one company setting the token’s rules, its reserve policy, its supported chains, and its product roadmap, a board made up of the partner companies makes those decisions collectively. The stated aim is neutrality: no single participant can steer the coin to serve its own interests at the expense of the others, which is meant to make the token trustworthy as shared infrastructure rather than one firm’s product. For businesses wary of building on a competitor’s rails, that neutrality is a selling point.

The second pillar is shared economics. In a consortium model, the interest earned on the reserves is returned to the partners who adopt and distribute the coin, minus a management fee for operating costs. This directly inverts the incumbent arrangement where the issuer keeps the yield. The logic is incentive alignment: if a payment company, bank, or platform earns a share of the reserve income by supporting the coin, it has a direct financial reason to promote adoption. The coin’s growth becomes a shared commercial project instead of one issuer’s private revenue stream.

Together, these two features aim to solve problems the consortium model’s backers say businesses face with existing stablecoins. Companies often pay fees to mint or redeem at scale, do not share in the reserve revenue their volume helps generate, and have little influence over an issuer’s roadmap. A neutral, revenue-sharing, collectively governed coin is pitched as the answer to all three. Whether it delivers depends on execution, but the structure is a coherent response to the incumbents’ weaknesses.

Why consortium stablecoins are emerging now

The consortium model is not new in concept, but it has gained momentum for specific reasons in the mid-2020s. The first is regulation. In the United States, the GENIUS Act, signed into law in 2025, created a federal framework for dollar-backed stablecoins, setting standards for reserves and licensing. That clarity lowered the legal uncertainty that had kept large, regulated institutions on the sidelines, and it drew banks, payment networks, and major enterprises into a market they had previously watched from a distance. A consortium of household-name financial firms is far more plausible once the rules of the road are defined.

The second reason is the sheer size and trajectory of the market. The stablecoin sector has grown past $300 billion, and some projections see it reaching into the trillions by the end of the decade as tokens move from crypto trading into cross-border payments, merchant settlement, and corporate treasury operations. A market that large attracts competitors who want a share, and it makes the reserve income at stake enormous.

When the prize is that big, the incentive to build an alternative to the incumbents grows accordingly.

The third reason is the economics itself. As the interest income earned by single issuers has become widely understood, partners have increasingly asked why they should drive adoption of a coin whose reserve revenue flows entirely to one company. The competitive frontier has shifted from simply issuing a token to controlling the underlying network and sharing its economics. Consortium stablecoins are the natural expression of that shift, giving a broad group of participants both a say in the network and a cut of the money it generates. The result has been a wave of consortium and shared-revenue projects entering the market.

The leading examples

The clearest way to understand the model is through the projects putting it into practice. The most prominent is Open USD, or OUSD, announced in 2026 by an independent company called Open Standard and backed by a consortium of more than 140 businesses spanning payments, banking, technology, and crypto, including Visa, Mastercard, Stripe, BlackRock, BNY, Coinbase, and Google. Open USD lets businesses mint and redeem the token with no fees and no volume limits, and it shares the reserve income with participating partners after a management fee, governed by a board drawn from those partners. It is positioned as a direct challenge to Tether and Circle, and its announcement sent Circle’s stock down sharply as the market priced in the competitive threat.

Open USD is not the first of its kind. The Global Dollar Network, built around the USDG token and led by the regulated issuer Paxos, uses a similar shared-revenue structure, distributing reserve income to partners such as Robinhood, Kraken, and Galaxy Digital to encourage broad adoption. In Europe, a group of major banks including BNP Paribas, ING, UniCredit, and SEB formed a venture called Qivalis to launch a euro-pegged stablecoin, initially focused on crypto trading before expanding, as financial institutions seek shared digital-payment infrastructure they collectively control. These projects differ in detail, but they share the consortium DNA of collective governance and shared economics.

What unites the examples is a strategic bet: that the future of stablecoins is a fight over infrastructure and network control rather than individual tokens, and that a broad, aligned coalition can win it against entrenched single issuers. The breadth of the coalitions, spanning card networks, banks, technology platforms, and crypto firms, is meant to translate into real-world acceptance that a lone issuer would struggle to build. Whether that bet pays off is the open question, and history offers a cautionary example.

A cautionary precedent: the Centre Consortium

The consortium model has been tried before at the heart of the industry, and the result is instructive. When USDC launched in 2018, it was governed not by Circle alone but by the Centre Consortium, a governance body co-founded by Circle and Coinbase to oversee the coin as a neutral standard. In its early years, USDC was the shared project of two of crypto’s most important companies, with governance and economics split between them, a genuine consortium arrangement at the center of the stablecoin market.

That arrangement did not last. By 2023, Circle and Coinbase dissolved the Centre Consortium, with Circle taking full control of USDC’s issuance and governance and buying out Coinbase’s stake, replacing the shared structure with a revenue-sharing commercial agreement instead. The neutral, jointly governed body gave way to a single issuer with a distribution partner. The episode showed that a consortium can fracture, that aligning even two large partners over the long term is hard, and that the pull toward single-issuer control is strong once a coin becomes valuable.

The lesson for today’s consortium stablecoins is sobering but not disqualifying. Coordinating two founding partners proved difficult; coordinating 140 is a far larger challenge. At the same time, the Centre experience taught the industry a great deal about how to structure governance and economics, and the newer projects are designed with that history in mind. The precedent is a warning about durability, not a verdict that the model cannot work. It simply means the hardest part of a consortium stablecoin may not be launching it, but keeping the coalition together as the stakes rise.

Why the model matters

Consortium stablecoins matter because they attack the core economics of the incumbents and could reshape how digital dollars are built. By sharing reserve income, they threaten the single-issuer business model that has made Tether and Circle so profitable, and they put pressure on every issuer to justify keeping the float that stablecoins quietly earn. If businesses can earn a share of that income by supporting a shared coin, the competitive logic of the whole sector shifts, and that pressure is real regardless of which specific consortium succeeds.

The model also changes the incentives around adoption. A single issuer has to persuade partners to distribute its coin; a consortium gives those partners a financial stake in the coin’s success, turning distribution into a shared interest. Combined with neutral governance, this can make a consortium coin more attractive to businesses that do not want to depend on, or enrich, a single competitor. The breadth of backers in projects like Open USD is meant to convert that aligned interest into faster real-world acceptance across payments, banking, and commerce.

For the broader market, the rise of consortium stablecoins is part of a larger story in which crypto is replaying the history of banking, where whoever holds the deposit, or the digital dollar, ends up with more durable economics than whoever merely moves the transaction. The consortium model is an attempt to distribute that durable position across a coalition instead of concentrating it in one firm. That makes it a structurally significant development, not just another product launch, even though its ultimate success is far from guaranteed.

The risks of the consortium model

For all its appeal, the consortium model carries distinct risks that anyone evaluating it should weigh. The most fundamental is coordination. Aligning the interests of a large group of companies, each with its own priorities and competitors within the same coalition, is genuinely hard, and decision-making by committee can be slow and prone to deadlock. The Centre Consortium fractured with only two partners; a coalition of many faces a much steeper coordination challenge, and governance disputes could stall the roadmap or splinter the group.

A second risk is that consortiums have historically struggled to ship and sustain products. A launch-day roster of famous names is not the same as a working, widely adopted coin, and many industry consortiums across finance and technology have announced ambitious shared ventures that underdelivered. At announcement, a new consortium stablecoin typically has unproven contracts, reserves, and real-world usage, so the gap between a strong partner list and durable adoption is wide. The coin still has to win against the deep liquidity and entrenched network effects of incumbents like USDT and USDC, which will not stand still.

There are subtler concerns too. Concentrating governance among a group of large, powerful incumbents raises its own questions about who really controls the network and whose interests it ultimately serves. Regulatory clarity that favors well-capitalized entrants can entrench the biggest players instead of broadening competition. And a win for the consortium as a business does not automatically translate into benefits for the users, chains, or tokens associated with it. The consortium model is a serious and well-reasoned challenge to the single-issuer status quo, but it is an experiment whose durability will be settled by execution and by whether coalitions can hold together once the money at stake grows large.

Where consortium stablecoins fit among stablecoin types

To place the consortium model correctly, it helps to see the wider map of stablecoin designs, because the consortium approach is a variation on one branch of that map instead of a wholly separate species. The most common type is the fiat-backed stablecoin, where each token is backed by reserves of cash and safe assets like Treasury bills held by an issuer. Within that category sit the familiar single-issuer coins such as Tether’s USDT and Circle’s USDC, where one company holds the reserves and keeps the income. A consortium stablecoin is still a fiat-backed stablecoin; what changes is who governs it and who receives the reserve income, not what backs it.

Other branches of the map work differently. Crypto-collateralized stablecoins, such as those built on decentralized protocols, are backed not by dollars in a bank but by other cryptocurrencies locked in smart contracts, usually over-collateralized to absorb volatility. Algorithmic stablecoins attempt to hold their peg through supply-adjusting mechanisms instead of full reserves, a design that has repeatedly proven fragile and, in notable cases, collapsed. Yield-bearing stablecoins add a return for the holder on top of the peg, sharing reserve income or on-chain yield directly with users. These are distinct mechanisms for achieving or funding a stable value.

Seen against that backdrop, the consortium model is best understood as a governance-and-economics innovation layered onto the fiat-backed design. It does not change the fundamental promise, one token redeemable for one dollar held in reserve, and it does not introduce a new stability mechanism. What it changes is the ownership of the network: collective governance instead of a single controller, and shared reserve income instead of a single beneficiary. In that sense it sits alongside, not opposite, the single-issuer fiat-backed coins, offering the same product with a different distribution of power and profit.

This placement matters for how users should evaluate a consortium stablecoin. Because the backing is the same fiat-reserve model, the safety questions are the same ones that apply to any fiat-backed coin: what exactly is in the reserves, who holds and audits them, and what regulatory framework governs them. The consortium structure adds considerations about coordination and governance, but it does not remove the need to scrutinize reserves and compliance. A consortium coin is not safer or riskier by virtue of its governance alone; it is a fiat-backed stablecoin whose distinctive feature is shared control, and it should be judged on the fundamentals every stablecoin shares.

Frequently Asked Questions

What is a consortium stablecoin?

A consortium stablecoin is a fiat-backed token issued and governed by a group of companies instead of a single issuer. Its two defining features are shared governance, where a board drawn from the partners makes decisions collectively, and shared economics, where the interest earned on reserves is distributed among partners after a management fee, instead of kept by one company.

How is it different from USDT or USDC?

USDT and USDC are single-issuer stablecoins: one company, Tether or Circle, controls the network, holds the reserves, and keeps the interest those reserves earn. A consortium stablecoin spreads both control and reserve income across many partner companies. USDC is a partial hybrid, since Circle shares a large share of the economics with Coinbase, but Circle still controls issuance and governance.

What is an example of a consortium stablecoin?

The most prominent example is Open USD, backed by more than 140 companies including Visa, Mastercard, Stripe, BlackRock, and Coinbase, and governed by an independent body called Open Standard. Others include the Paxos-led Global Dollar Network, which shares reserve income with partners like Robinhood and Kraken, and Qivalis, a euro stablecoin venture formed by major European banks.

Why are consortium stablecoins becoming popular?

Three forces are driving them: clearer regulation, such as the 2025 GENIUS Act, which brought large regulated institutions into the market; the growth of the stablecoin sector past $300 billion, which raised the stakes; and a growing desire among partners to share in the reserve income that single issuers have kept. Competition has shifted from issuing tokens to controlling and sharing the underlying network.

How do consortium stablecoins make money for partners?

They share the interest earned on the reserves. A stablecoin holds dollars in safe assets like Treasury bills that earn interest, and in the consortium model that income is distributed among the participating companies after a management fee covers operating costs. This gives each partner a direct financial incentive to promote adoption, unlike single-issuer coins where the issuer keeps the reserve income.

What happened to the Centre Consortium?

The Centre Consortium was a governance body co-founded by Circle and Coinbase in 2018 to oversee USDC as a neutral standard. It was dissolved in 2023, when Circle took full control of USDC’s issuance and governance and bought out Coinbase’s stake, replacing the shared structure with a revenue-sharing agreement. It is a cautionary example that even a two-partner consortium can fracture over time.

Are consortium stablecoins safer than single-issuer ones?

Not inherently. Safety depends on the quality of the reserves, the regulatory framework, and the operator, not on whether governance is shared. A consortium can add neutrality and distributed control, but it also adds coordination risk and, at launch, unproven contracts and reserves. Users should evaluate any stablecoin on its reserve backing, regulatory standing, and transparency instead of assuming a governance model makes it safer.

What are the main risks of the consortium model?

The biggest risk is coordination: aligning many companies, some of them competitors, is hard, and committee governance can be slow or prone to disputes. Consortiums have also historically struggled to ship and sustain products, so a strong partner list may not translate into adoption. New consortium coins must also overcome the deep liquidity and network effects of entrenched incumbents like USDT and USDC.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or legal advice. The stablecoin sector is evolving rapidly, and the status of specific projects can change. Nothing here is a recommendation to buy, sell, or use any asset or product. Always do your own research and consult a qualified professional before making financial decisions. Information is accurate as of July 2, 2026, and may change.

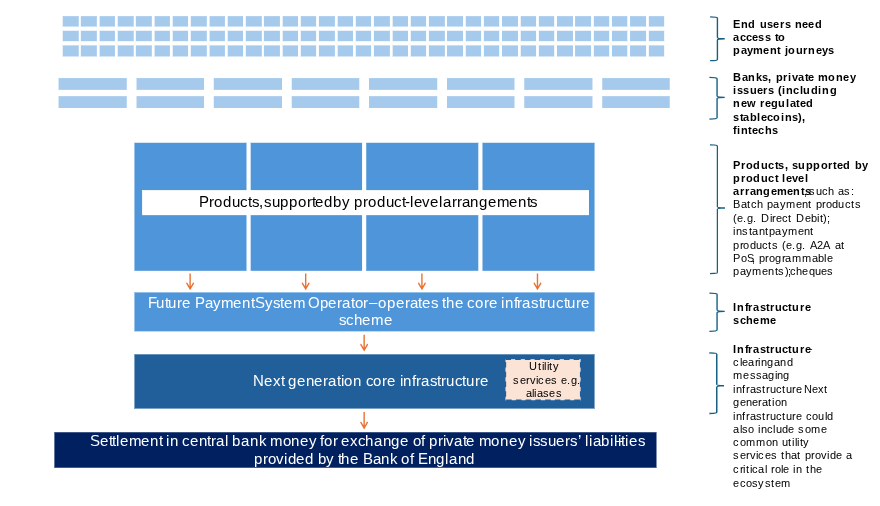

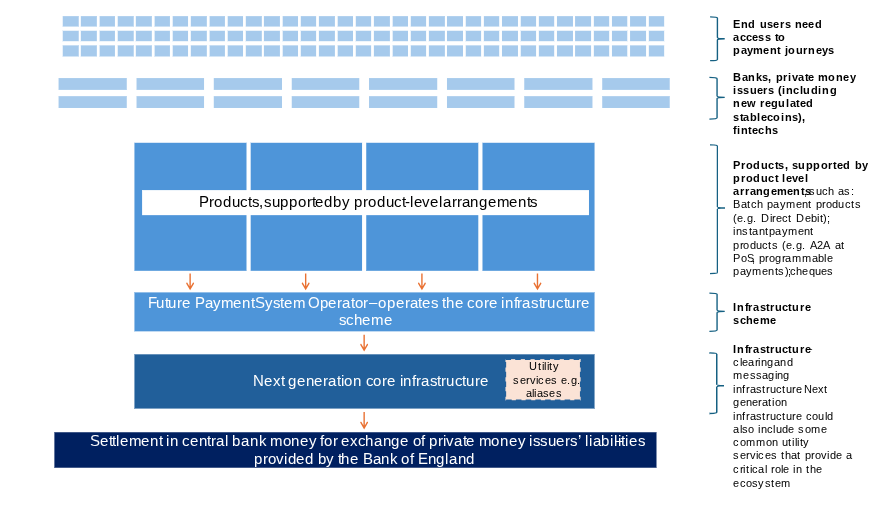

UK regulators are calling for tokenization and “new forms of digital money” to be part of the core infrastructure of the country’s future retail payment ecosystem.

In a Thursday update to the government’s roadmap for modernizing retail payment systems, HM Treasury on behalf of the Payments Vision Delivery Committee said that including tokenization and digital money would advance its efforts to create a “diverse multi-money ecosystem.”

“Programmable payments, including those that rely on tokenization,” were named as potential “product-level arrangements” that may support payment innovation in the country, the agency update said.

The update of November’s National Payments Vision document calls for infrastructure that enables emerging forms of digital money to interact with traditional payment systems.

The UK’s Financial Conduct Authority (FCA) earlier this week published its landmark crypto regulatory framework and said that the licensing window for crypto companies will open from September until Feb. 28, 2027, before the regime goes live on Oct. 25, 2027.

Under that framework, cryptocurrency firms, including trading platforms, custodians, stablecoin issuers, staking companies and other intermediaries, must obtain FCA authorization to operate in the UK under the new framework.

Illustrative diagram of roles and responsibilities outlined in Payments Vision Delivery Committee update. Source: HM Treasury

UK plans payments overhaul to support tokenization, stablecoins

In April, the UK government said it would revisit its payments rulebook to support the adoption of new payment technologies, including stablecoins and tokenization.

It said that would include a consultation on reforms for payment services and electronic money rules to create a single framework for traditional and tokenized payments, including stablecoins and tokenized deposits, according to an April 21 announcement by HM Treasury and Economic Secretary to the Treasury Lucy Rigby.

Related: Aave Labs’ Push gains UK FCA crypto registration

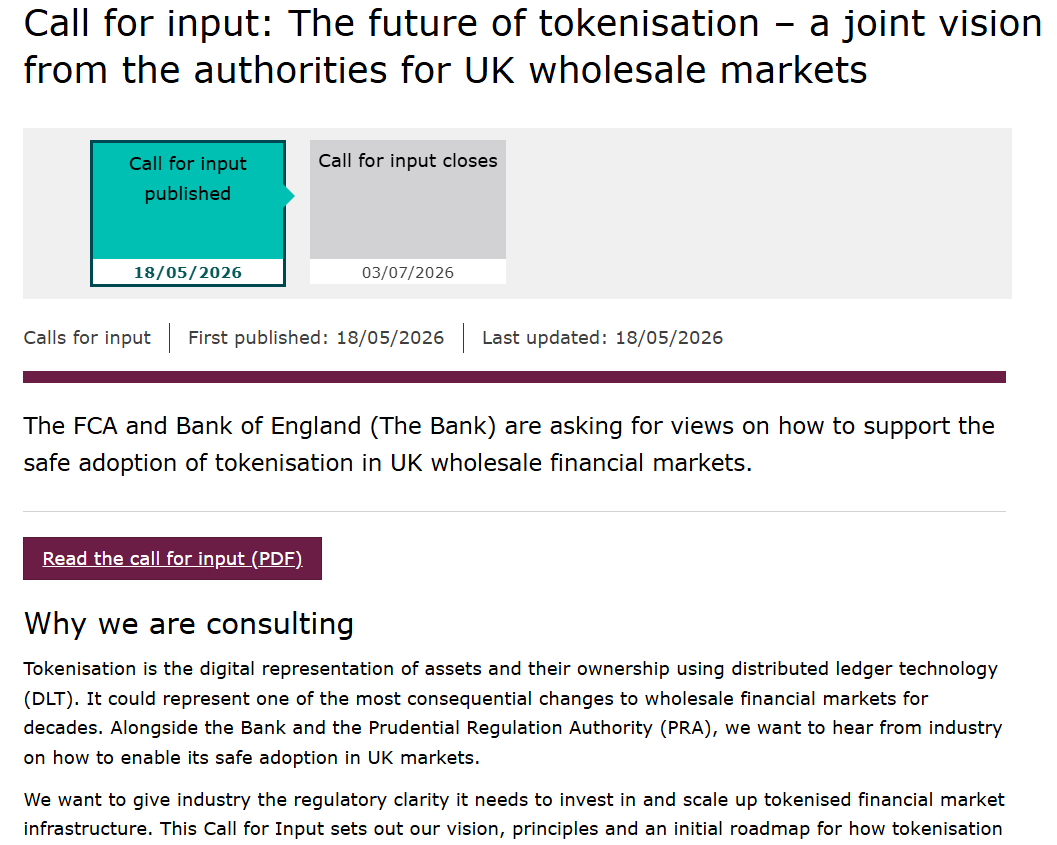

The following month, the Bank of England (BoE) proposed extending operating hours for its core settlement infrastructure toward near-24/7 availability, as part of a broader push with the FCA to prepare UK wholesale markets for tokenized finance.

The BoE said the expanded operating hours would support cross-border payments and new payment and settlement models as tokenization develops. The central bank is seeking public feedback on the proposal until July 3 and plans to publish a feedback statement in the summer.

Call for input on the future of tokenization in UK wholesale markets. Source: FCA

The FCA said just days earlier that tokenization and distributed ledger technologies could make fund management more efficient and support the innovation of the UK asset management sector.

Magazine: How crypto laws changed in 2025 — and how they’ll change in 2026

XRP continues to consolidate in a narrow range on both USDT and Bitcoin-paired charts, with the broader trend still favoring the sellers.

However, the latest technical signals suggest downside momentum may be fading as the market defends key support while early signs of bullish divergence begin to emerge.

Ripple Price Analysis: The USDT Pair

Against USDT, XRP remains confined within a well-defined descending channel, with the price trading below the 100-day and 200-day moving averages. This keeps the higher time frame structure bearish despite the recent stabilization.

The asset is currently holding around the $1.08 support area, which also coincides with a major horizontal demand zone. After the sharp sell-off in June, sellers have so far failed to extend the decline, allowing XRP to build a short-term base above support.

The RSI has formed a clear bullish divergence, printing higher lows while the price registered lower lows. This typically signals weakening bearish momentum and raises the probability of a relief rally if buyers manage to reclaim higher levels.

The first resistance lies around the $1.15 supply zone, while stronger resistance remains near the 100-day moving average around the $1.25 region. A recovery above these levels would improve the broader outlook, whereas losing the $1 support could expose the lower boundary of the channel near $0.80.

The BTC Pair

Against Bitcoin, XRP is also trading inside a long-term descending channel, reflecting persistent relative weakness. The pair remains below the major moving averages, indicating that the broader trend has yet to shift in favor of XRP.

Recently, XRP briefly broke below the key 1,700 sats low before quickly reclaiming it, creating what appears to be a fake breakdown. This rejection below support suggests sellers failed to maintain control and may have triggered a liquidity sweep before the price recovered back into the previous range.

Despite the recovery, the pair still faces immediate resistance around 1,850 sats, with a stronger supply zone located near 2,000 sats, where horizontal resistance converges with the declining 200-day moving average. A decisive move above these levels would strengthen the case for a broader recovery toward the upper boundary of the channel.

As long as XRP holds above 1,700 sats, the fake breakout scenario remains valid and could support additional upside. However, a confirmed daily close below this level would invalidate the bullish setup and likely open the door for another leg lower toward the critical 1,500 sats support area.

The post Ripple Price Analysis: Bullish Divergence Emerges as XRP Defends $1 Support Zone appeared first on CryptoPotato.

Crypto World

FBI Director Kash Patel Undisclosed Strategy Investment Raises Conflict-of-Interest Questions

FBI Director Kash Patel purchased between $100,001 and $250,000 worth of Strategy stock on November 21, 2025, and did not disclose the transaction until May 26, 2026. It is a gap of more than six months against the STOCK Act’s 45-day reporting requirement.

Why is it being questioned? The delay would be a routine compliance footnote if Strategy were an ordinary holding, but the company sits at the intersection of federal law enforcement, an active DOJ contracting relationship, and the world’s largest publicly listed Bitcoin treasury.

According to federal financial records reviewed by NOTUS, Patel explained the omission in a letter to the Office of Government Ethics, saying the transaction had been “inadvertently omitted” from an earlier filing. Two days later, Deputy Assistant Attorney General William Taylor attributed the delay to a miscommunication and stated that Patel remains in compliance with federal conflict-of-interest rules and that the stock purchase does not create a conflict with his duties as FBI director.

As of today, it is understood that DOJ ethics officials subsequently approved the corrected paperwork.

Discover: The Best Crypto to Diversify Your Portfolio

Kash Patel Under Scrutiny: A $200 Fine, Unenforced, and the Ethics Watchdog Response

Dylan Hedtler-Gaudette, acting vice president of the Project on Government Oversight, said: “Patel’s filing was clearly submitted after the legal deadline, calling it a violation of the STOCK Act.” The law sets a $200 civil penalty for first-time violations by senior executive branch officials, a figure that has drawn sustained criticism for being too low to deter. Although the Department of Justice has not issued any fine against Patel.

The procedural lapse is not isolated. According to NOTUS, more than 30 members of Congress have also filed late crypto disclosure and stock-trading reports under the STOCK Act over the past year. The nominal penalty structure makes voluntary compliance the primary mechanism, which is precisely why watchdog groups argue the existing framework is structurally inadequate for senior law-enforcement officials.

The pattern of senior government officials navigating financial disclosure rules around crypto-linked assets has added political weight to calls for tighter enforcement.

Discover: The Best Token Presales

Why Strategy Makes This a Crypto Market Issue, Not Just an FBI Compliance Story

Strategy, the company formerly known as MicroStrategy, trading under the ticker MSTR, is a Bitcoin Treasury Company and holds 847,363 BTC, a position currently valued at more than $50 billion. That concentration makes MSTR’s equity performance tightly correlated to Bitcoin price action, meaning Patel’s undisclosed position was, in practical terms, a leveraged directional bet on Bitcoin made by the director of the agency responsible for investigating cryptocurrency-related fraud.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

The conflict-of-interest question extends further. Strategy has secured millions of dollars in Department of Justice contracts over the past decade and continues to hold active federal business relationships. The FBI operates under the DOJ and routinely investigates crypto investment fraud, digital asset scams, and illicit blockchain activity.

Patel has publicly amplified the FBI’s crypto enforcement actions in recent months, including posts about major Bitcoin seizures and actions against fraud networks. Understanding the macro conditions that govern Bitcoin’s price trajectory through central bank liquidity cycles makes it clear why a senior official’s directional bet on MSTR is not a neutral financial decision.

DOJ ethics officials concluded the investment does not present a conflict of interest. Watchdog groups argue the opposite: that holding shares in a company with ongoing government contracts, particularly one whose core asset is under active federal law-enforcement scrutiny. It creates the appearance of a conflict regardless of intent.

Discover: The Best Crypto to Diversify Your Portfolio

The post FBI Director Kash Patel Undisclosed Strategy Investment Raises Conflict-of-Interest Questions appeared first on Cryptonews.

Strategy has become one of the largest corporate holders and buyers of bitcoin, with 847,363 BTC on its balance sheet. Its aggressive accumulation strategy has made the company a major source of demand for the cryptocurrency, meaning any shift toward selling the digital asset, even occasionally, could influence market liquidity, price dynamics and investor sentiment by introducing a new source of supply.

Demand for U.S. spot bitcoin exchange-traded funds (ETFs), the largest source of institutional crypto buying since their 2024 debut, has weakened sharply in recent months. The funds saw a record $4 billion in net outflows in June after a 13-day redemption streak pushed year-to-date flows into negative territory for the first time.

The bank said bitcoin came under pressure in late May and early June after Strategy disclosed in a June 1 regulatory filing that it sold 32 BTC between May 26 and May 31 to fund dividend payments. The sales compounded pressure from a broader repricing of Federal Reserve interest-rate expectations that had already weighed on bitcoin and gold.

JPMorgan noted that Michael Saylor’s Strategy has become one of bitcoin’s largest buyers, purchasing roughly $13.7 billion worth of the cryptocurrency year to date, about 70% of the bank’s estimate for total net digital asset inflows. The company holds around 4% of bitcoin’s total supply.

On 30 June, Prime Minister Keir Starmer unveiled the Defence Investment Plan, which includes a £15 billion increase in defence spending as part of a nearly £300 billion four-year budget. The market reacted quickly: on 1 July, shares of Babcock, BAE Systems and Rolls-Royce gained between 1.1% and 5.2%, providing support for the FTSE 100 during the session. Offsetting this strength, healthcare and energy stocks came under pressure, with AstraZeneca and GSK falling 1.7% and 2.5%, while Shell and BP lost more than 2% as oil prices declined. As a result, the index closed the day 0.2% lower. Over a longer-term horizon, investors remain focused on the Bank of England’s meeting on 30 July. The central bank has kept the base rate at 3.75%, while inflation risks remain elevated amid energy price dynamics and geopolitical tensions in the Middle East.

Technical Outlook

On the daily chart, the FTSE 100 (UK100 on FXOpen) has formed a symmetrical triangle, with price fluctuations narrowing between the February high and the March low. In recent sessions, the index has attempted to break above the pattern, but the move has so far been capped by the upper boundary of the current market profile at 10,520, making it too early to confirm a breakout. The key resistance level is located around 10,700, while major support lies near 9,900.

Should the index decline from current levels, the nearest support could come from the POC zone at 10,340 and the lower boundary of the market profile at 10,160. It is worth noting that trading volume remains firm, suggesting the current range may continue to develop. The RSI + MAs indicator currently reads 53, 53 and 51. All three values remain in neutral territory, confirming the current lack of directional conviction.

Summary

The narrowing price range within the symmetrical triangle points to declining volatility in the index amid a mixed fundamental backdrop. Geopolitical uncertainty surrounding US-Iran negotiations is coinciding with expectations ahead of the Bank of England’s upcoming meeting. The POC zone remains a key reference point within the current market structure.

Trade global index CFDs with zero commission and tight spreads (additional fees may apply). Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Fact check: Defence spending and fake naval officer video

Infuse Asset Management Q2 2026 Letter

SBI Crypto to shut down mining pool that holds roughly 2% of Bitcoin’s hashrate

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Weekend Open Thread: Staud – Corporette.com

Live Gold, Crypto Trading | 2 JULY | #goldtrading #cryptotrading #bitcoin – MANSI

Once You Get Money, Upgrade These 10 Things Immediately

XRP DEATHCROSS CONFIRMED = XRP MOONS !!!! 42.5% OF XRP LOSING !!!! MR POOL BOOOOOOOOM !!!!

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics6 days ago

Politics6 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Crypto World3 days ago

Crypto World3 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics7 days ago

Politics7 days agoPotential 2028er World Cup attendee leaderboard

-

Business6 days ago

Business6 days agoAsia stock markets slide as tech shares slump

-

News Videos4 days ago

News Videos4 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech7 days ago

Tech7 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World7 days ago

Crypto World7 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World5 days ago

Crypto World5 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business2 days ago

Business2 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World5 days ago

Crypto World5 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Tech3 days ago

Tech3 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Sports6 days ago

Sports6 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World7 days ago

Crypto World7 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech5 days ago

Tech5 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech5 days ago

Tech5 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World6 days ago

Crypto World6 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World6 days ago

Crypto World6 days agoRTX holders must register wallets before token distribution begins

-

Sports1 day ago

Sports1 day agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business3 days ago

Business3 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

You must be logged in to post a comment Login