Crypto World

OKX, MetaMask, Matter Labs back dispute resolution court for AI agents

A group of crypto and Web3 firms that includes OKX, MetaMask, Matter Labs and Genlayer have formed the “Internet Court” to reach dispute resolutions between AI agents.

These days, AI agents negotiate and pay one another without humans in the loop, but as with human-to-human transactions, agent-to-agent transactions will run into contractual disagreements.

The problem is that agentic systems have no way to settle these disputes, and traditional courts are not built to handle such cases. Hence the need for the 27-firm-backed protocol, led by the Genlayer Foundation, which makes AI-based payments, escrow and dispute resolution interoperable, according to a press release.

Agentic commerce is not prepared for the potential fallout when agents disagree at machine speed, according to David Riudor, CEO and co-founder of the GenLayer Foundation. “Internet Court is the shared place agents can turn to when a deal goes wrong. Machine-speed money needs machine-speed adjudication,” he said.

A key problem the dispute protocol solves is interoperability between a variety of AI commerce systems. Agentic commerce is certainly charging ahead but the infrastructure underpinning this new economy is still highly fragmented.

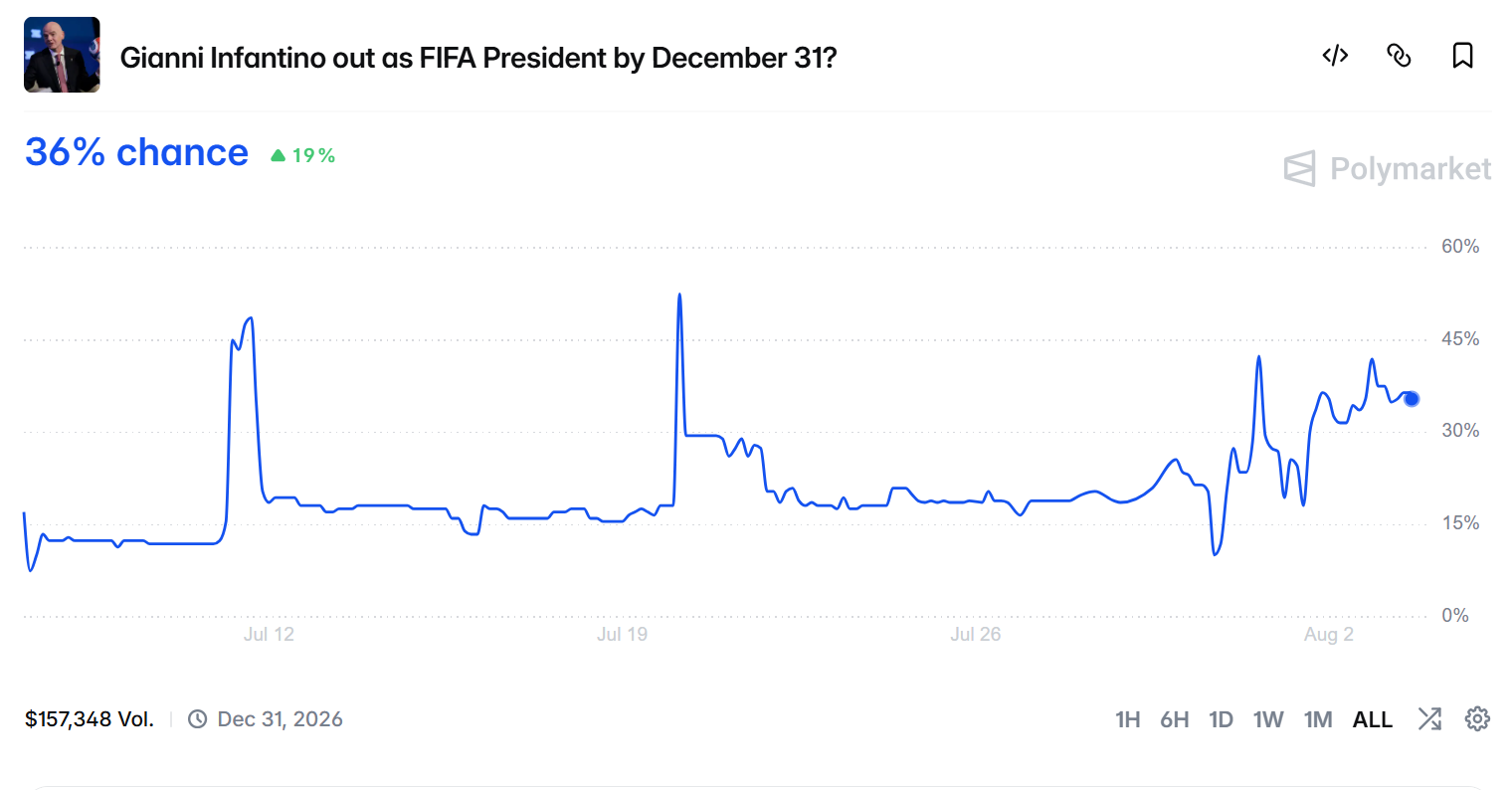

FIFA President Gianni Infantino has reportedly asked the Trump administration to help him keep his job, arranging a call with Secretary of State Marco Rubio, the New York Post reported Monday.

Polymarket traders price his exit by December 31 at 36.5%, up from roughly 19% a week ago. Almost all of the contract’s lifetime volume arrived in the past seven days.

Why Infantino Thinks Trump Owes FIFA a Favor

The reported ask lands four weeks after FIFA handed the White House a win. Its disciplinary committee cleared Folarin Balogun for Belgium, suspending the striker’s automatic red card ban on probation.

Trump had pushed for the reversal and claimed credit for it publicly.

“Thank you to FIFA for doing what was right, and reversing a great injustice!” Trump wrote on Truth Social.

Rubio is not a cold call. He sat in the Oval Office with Trump and Infantino last November. The occasion was a task force meeting on the World Cup.

FIFA’s bridge into that room is now gone. Carlos Cordeiro, the former Goldman Sachs banker who represented FIFA on the task force, resigned Friday over the sale plan. He had joined Infantino on repeated White House visits.

BeInCrypto could not independently verify the Rubio call, which the Post attributed to two people familiar with it.

Polymarket Traders Price the Fallout

The market read the revolt faster than the headlines did. It still traded near 20% on the afternoon of July 30. That was when all 55 UEFA member associations unanimously backed a boycott.

It broke above 40% the following day, once Infantino’s own executives turned on him. Chief operating officer Kevin Lamour told the Associated Press that staff had been deceived.

“It is the project of one person,” Kevin Lamour, chief operating officer of FIFA, in a statement to the Associated Press.

Follow us on X to get the latest news as it happens

Volume backs the repricing. The contract has handled $156,400 since it opened on July 6, and $151,700 of that traded in the past week. Open interest sits near $76,000.

The expiry date shapes how traders read it. The contract pays out only on a departure before December 31, while FIFA’s election falls next March. Challengers have until November 18 to declare, so the market is pricing resignation rather than defeat.

The asset in dispute is large. Cordeiro put FIFA’s revenue at $15 billion over the World Cup cycle. Josh Kushner’s fund offered $4.2 billion for 20% of a new FIFA subsidiary.

Crypto already has a claim on that value. The tournament drove $20 billion in World Cup prediction volume, Chainalysis found. FIFA’s own collectibles platform cleared at least $6 million in fees.

Whether Rubio’s call buys Infantino anything should show up in the odds before it shows up in a FIFA statement.

The post Infantino Wants to Collect on Trump’s World Cup Favor but Polymarket Says He’s 36% Out appeared first on BeInCrypto.

Miller’s previous controversies

Before being elected to the House in 2022, Miller spent six years in the Marine Corps Reserve. He also previously served in Trump’s first-term Administration, including as a senior advisor to the President.

Politico and the Washington Post have previously reported on Miller’s run-ins with the law as a young adult, including charges, which were later dismissed, for underage drinking, assault, disorderly conduct, and resisting arrest.

From 2019 to 2020, Miller dated Stephanie Grisham, a White House press secretary during Trump’s first-term Administration. Grisham has also accused Miller of abuse: she wrote in a 2021 op-ed for the Post and in a memoir the same year, without naming Miller, that her relationship with a White House staffer had “turned abusive” and that she had told Trump himself about her former partner who had “anger issues and a violent streak.”

The partner was later identified as Miller, who then sued Grisham for defamation, though he voluntarily dropped the suit in 2023 as part of a confidential settlement agreement.

BlackRock, the world’s largest asset manager, has expanded its tokenized cash platform, introducing a couple of new tokenized money market products, the firm said on Monday.

Back in May of this year, BlackRock filed for the new products with the U.S. Securities and Exchange Commission (SEC).

BlackRock is offering onchain shares of the BlackRock Select Treasury Based Liquidity Fund (BSTBL), a tokenized share class on Ethereum for an existing BlackRock money market fund. In addition, a new BlackRock Daily Reinvestment Stablecoin Reserve Vehicle (BRSRV) has also been unveiled with daily dividend reinvestment and access across multiple blockchains, said BlackRock in a press release.

Both funds intend to qualify as eligible reserve assets for permitted U.S. payment stablecoin issuers under the GENIUS Act, the asset manager said.

The move deepens BlackRock’s push into tokenized finance, blockchain-based representations of traditional financial assets such as funds, bonds or equities. Advocates say the technology can speed up settlement, enable round-the-clock trading and improve transparency.

Crypto exchange Bitget will stop accepting new registrations from Japanese users, announcing a phased exit that culminates in forced position closures by December 31, 2026.

The withdrawal comes as Japan tightens its licensing regime and grapples with severe currency turbulence.

The Timeline Japanese Users Now Face

The announcement, dated August 3, sets a clear timeline. Accounts flagged as potentially Japanese must complete that verification by November 1, 2026. Failure triggers restrictions. Users who miss the deadline face phased limitations from that date, with any remaining open positions forcibly closed by the end of December.

The exchange will email withdrawal instructions to affected users, framing the decision as part of its ongoing commitment to regulatory compliance.

The regulatory backdrop explains the move. Japan requires crypto service providers serving local residents to register with the Financial Services Agency under the Payment Services Act.

Follow us on X to get the latest news as it happens.

Enforcement risk is real for unregistered platforms. The agency issued warnings to Bitget and other overseas exchanges in November 2024. Consequences followed. Bitget’s app was later removed from Japan’s App Store, though web and Android access remained available to existing users.

Few jurisdictions demand more. Providers must meet capital, custody, consumer-protection, and anti-money-laundering standards to operate legally.

How Japan’s Yen Turmoil Compounds the Regulatory Burden

The timing coincides with acute currency pressure. The yen slid toward a 40-year low near 164 per dollar in late July, driven by rate differentials and carry-trade activity. Japan responded aggressively, with estimates suggesting authorities spent tens of billions of dollars buying yen to halt the decline.

“They have a weakening yen, and they wanted a little bit of help. And we’re always there for Japan,” US President Donald Trump told reporters on Sunday.

Washington then joined the effort. Both countries conducted a rare coordinated intervention, the first in 15 years, targeting excessive volatility and disorderly movements. The response was immediate, with the yen rebounding sharply and briefly reaching 155 per dollar.

Officials signaled more could follow. Finance Minister Satsuki Katayama and US Treasury Secretary Scott Bessent confirmed the operation and indicated readiness for further action.

The two pressures compound each other. Strict licensing raises fixed costs, while currency volatility complicates pricing and treasury management for offshore operators.

Bitget’s exit illustrates a broader pattern. Platforms must either invest heavily in registration or leave markets where regulatory barriers make operations uneconomical.

Japanese users still have room to act, with the transition window running until year-end before restrictions take full effect.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights.

The post Bitget Withdraws From Japan Amid Tightening Crypto Rules and Yen Turmoil appeared first on BeInCrypto.

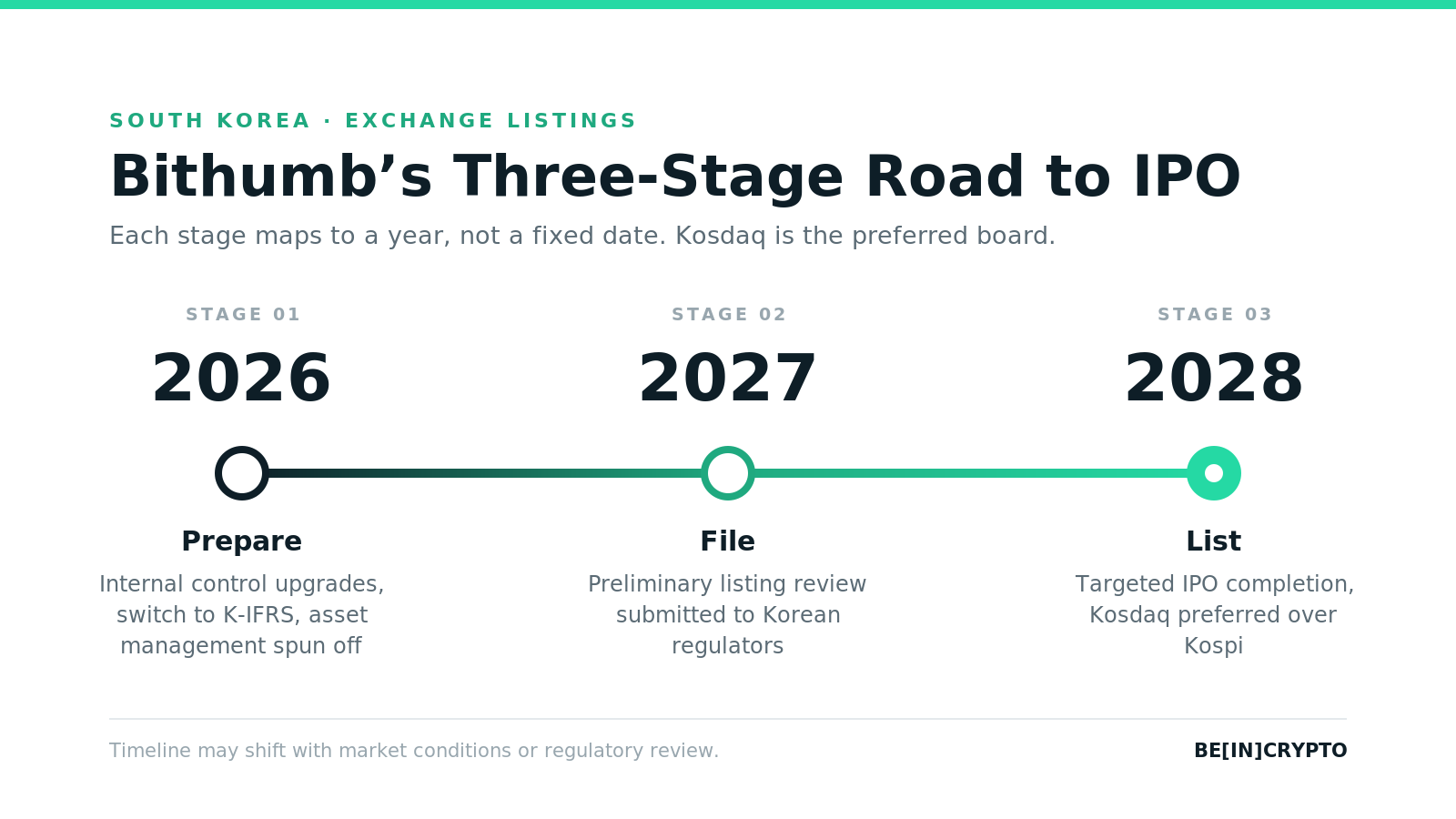

Bithumb has published a formal Bithumb IPO timeline. The plan targets a public listing by 2028.

South Korea’s second-largest exchange framed the listing as a trust-building step. Executives tied each phase to a specific governance target.

A Roadmap Shaped by Past Delays

Bithumb’s listing ambitions have shifted before. The exchange once targeted a debut in the second half of 2025. Management pushed that date back as new obligations piled up.

Shareholders backed CEO Lee Jae-won’s reappointment in March 2026. The vote came weeks after a Bitcoin (BTC) balance-display glitch drew a record fine.

The exchange also operates in a tougher home market. South Korean trading volume recently fell to a two-year low during a Kosdaq market crash. A new 22 percent crypto tax takes effect in 2027. That is the same year Bithumb plans to file its listing review.

The Bithumb IPO Timeline, Stage by Stage

The Bithumb IPO timeline runs in three stages. Each stage maps to a single year rather than a fixed date. Stage one covers 2026. It focuses on internal control upgrades and a shift from domestic accounting rules to the global K-IFRS standard.

Bithumb has also restructured internally, spinning off its asset management unit as a separate entity, Bithumb Asset. The company said the split separates responsibilities and reduces potential conflicts of interest ahead of a listing review.

Stage two opens in 2027. Bithumb plans to file for a preliminary listing review with Korean regulators that year. Stage three targets IPO completion in 2028. However, the notice cautions that the schedule could shift with market conditions or regulatory review timelines.

The exchange has indicated a preference for South Korea’s Kosdaq board. A listing on the larger Kospi market remains possible if conditions change.

The notice also spelled out promises to customers. Bithumb pledged a more transparent governance structure and stronger internal controls.

It also promised better investor protection, more frequent information disclosure, and a sustainable growth foundation as it moves toward institutional-level, global-standard management. The company said these steps aim to show it can operate like a listed company well before shares actually trade.

The plan lands as Japan and South Korea explore a broader digital asset framework. That regulatory shift could smooth Bithumb’s path toward institutional-grade compliance.

Meanwhile, the exchange keeps growing its trading business. Upbit and Bithumb listings sent one small-cap token up nearly 30% in July. That activity shows daily operations continuing alongside the listing push.

Whether Bithumb reaches 2028 on schedule may depend on more than internal readiness. It will also hinge on how regulators respond to a shrinking, more heavily taxed market in the years ahead.

The post Bithumb Lays Out a 3-Stage Path to Its South Korea IPO appeared first on BeInCrypto.

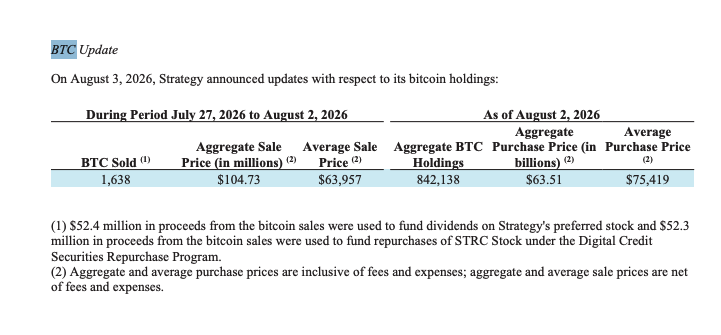

MicroStrategy added 37 bitcoin between May 26 and July 26. Last week it sold 1,638 in seven days. The company now holds less Bitcoin (BTC) than it did in spring.

Michael Saylor says Strategy expects to stay a net buyer. Its own filings show the buying stopped months ago.

The Stack Is Going Backwards

Strategy reported 843,738 BTC on May 26. Two months later, on July 26, it reported 843,775. That is a gain of 37 coins.

Then came Monday’s filing. It shows 842,138 BTC as of August 2.

The company is now 1,600 coins below where it stood in May. Ten weeks have passed with no net buying at all.

Saylor addressed the question directly on August 1, when he shut down a viral sale claim.

“We have never had a “never sell” policy. The program does not require any BTC sale, and we expect to remain a net buyer of Bitcoin over time,” the MicroStrategy chair stated.

Follow us on X to get the latest news as it happens

A $400 Million Dividend Bill

The MicroStrategy Bitcoin sale last week was not opportunistic. It paid a bill.

Strategy owes cash to holders of its preferred shares. Those pay a fixed dividend every quarter.

That cost reached $400.7 million in the second quarter. A year earlier it was $49.1 million. The bill is more than eight times larger.

Dividends and interest now run roughly $1.76 billion a year.

So the coins go out the door. Strategy sold $218.4 million of bitcoin this year through July 26. Last week added $104.7 million more.

Almost a third of the year’s selling happened in that one week.

Selling at a Loss to Buy at a Discount

Here is the trade. Strategy sold bitcoin at $63,957 a coin. Its average cost is $75,419. That is a loss of about $11,500 each.

It used half that cash to buy back 912,143 STRC shares. STRC is a Bitcoin-backed preferred share that pays 12% a year.

Each share is meant to be worth $100. Strategy paid $89.02.

So the company took a loss on bitcoin to capture an 11% discount on its own debt-like shares. Every share retired cuts the dividend bill for good.

It also sold 3,011,361 of its own ordinary shares, raising $290.6 million. Meanwhile a $1 billion approval to buy those shares back sits unused. That is the trade-off MSTR investors face.

“Strategy is evolving from one-way capital issuance to active capital management,” Phong Le, president and chief executive of Strategy, in the June 29 release

Bitcoin trades near $62,468, roughly half its October record. Strategy still owns more of it than any other company.

But the direction has changed. The next filing lands in a week.

The post MicroStrategy Added 37 Bitcoin in Two Months. Then It Sold 1,638 in One Week appeared first on BeInCrypto.

Michael Saylor’s Strategy sold 1,638 Bitcoin between July 27 and August 2, marking the year’s second-largest Bitcoin sale for the company.

Strategy sold 1,638 Bitcoin (BTC) at an average price of $63,957 for a total of $104.7 million, according to a Monday 8-K filing with the Securities and Exchange Commission. Of the proceeds, $52.4 million was used to fund dividend payments on Strategy’s STRC preferred stock, while another $52.3 million was used to repurchase STRC.

The company now holds 842,138 Bitcoin bought at an aggregate cost of $63.5 billion.

Strategy sold 3,588 Bitcoin for about $216 million on July 6. It also disclosed the sale of 32 Bitcoin in early June, its first reported Bitcoin sale since the 2022 tax-loss transaction.

Strategy bolsters USD reserve to $4 billion, repurchases STRC stock

Strategy also reported selling $290 million in MSTR shares during the same period. About $250 million of the proceeds was used to increase the USD Reserve to $4 billion, $28.9 million to fund additional repurchases of STRC stock and $11.7 million was added to Strategy’s cash balance.

In total, Strategy repurchased $81 million worth of STRC stock and increased its USD runway by 57 days to 2.3 years, announced Strategy founder and chairman Michael Saylor in a Monday X post.

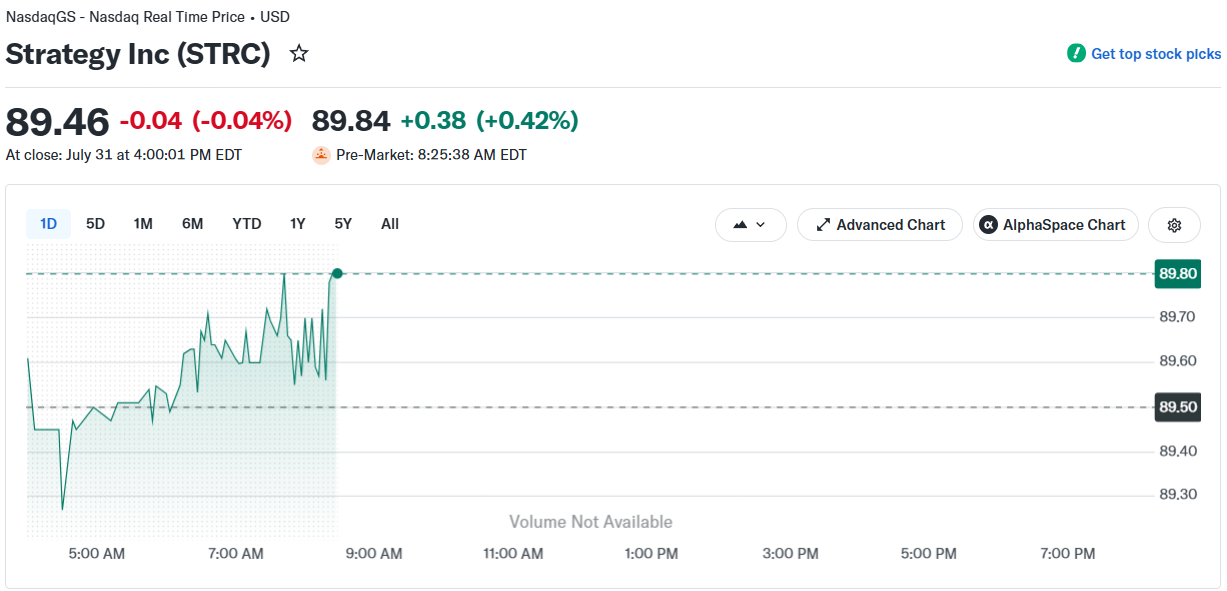

Strategy’s perpetual preferred stock, STRC, traded at $89.4, or 10.6% below its $100 intended par value, during Monday’s pre-market trading session, Yahoo Finance data shows. The company’s MSTR stock also declined 0.9% in pre-market trading on Monday.

STRC stock price, 1-day chart. Source: Yahoo Finance

STRC is one of Strategy’s main mechanisms to fund its Bitcoin accumulation. Trading below par limits Strategy’s ability to raise funds through STRC sales. It may also force the company to further increase its nominal dividend rate to attract buyers and protect STRC’s price.

Related: CLARITY Act failure could send crypto valuations lower: Bernstein

On June 24, CryptoQuant CEO Ki Young Ju said that Strategy should pause Bitcoin purchases and replenish its cash reserve, after the company’s dividend coverage fell to 14 months from seven years.

“They should pause Bitcoin purchases, rebuild cash reserves, and adopt a systematic framework for purchase timing,” wrote Ju in a June 24 X post.

In its June 29 8-K filing, Strategy unveiled a capital framework allowing Bitcoin sales to fund dividends, increased the annual dividend rate on its STRC preferred stock to 12%, and disclosed that its US dollar reserve had grown to $2.55 billion.

Magazine: Bitcoin adoption metrics say one thing, price action says another

Strategy has increased its US dollar reserve and expanded its preferred-stock repurchases. The otherwise Bitcoin-focused company is moving to strengthen its balance sheet.

The firm added $250 million to its cash reserve, bringing the total to $4 billion. It also repurchased approximately $81 million worth of its Variable Rate Series A Perpetual Stretch Preferred Stock (STRC).

Strategy increased its USD Reserve by $250M and repurchased $81M of $STRC. This increased USD Duration by 57 days to 2.3 years and tightened STRC’s BTC Credit by 5 bps. As of 8/2/26, we hold ₿842,138 in our BTC Reserve and $4.0B in our USD Reserve. $MSTR https://t.co/t7bGZJ8Q3o

— Michael Saylor (@saylor) August 3, 2026

The transaction builds on the firm’s recently introduced Digital Credit Capital Framework. The company intends to use its dollar reserve primarily to cover preferred-stock dividends and debt interest, reducing the need to sell Bitcoin during periods of market stress.

What Saylor failed to mention in the tweet was that the firm also sold some 1,638 BTC for approximately $105 million between July 27 and August 2 at an average price of $63,957 – according to the official filing.

The post Strategy Sold Over $100 Million in Bitcoin, Buys Back More STRC appeared first on CryptoPotato.

Ethereum price fell 2% to around $1,847 on Aug. 3 after another rejection near key moving averages left the $1,800 support zone exposed.

Summary

- Ethereum price fell 2.04%, reaching an intraday low of $1,828.

- ETH remains below its 50-day and 100-day moving averages at $1,889 and $1,927.

- 4-hour MACD and Chaikin Money Flow readings show weak momentum and continued selling pressure.

- A break below $1,800 could bring $1,785 and $1,700 into focus.

ETH slides after failing to reclaim $1,900

According to data from crypto.news, Ethereum (ETH) price traded at $1,847 at the time of writing, down 2.04% over the previous 24 hours. The token moved between an intraday high of $1,886 and a low of $1,829 on Binance.

The decline extended ETH’s retreat from its July 27 high near $1,975. Buyers have now failed several times to sustain a move above the resistance zone between $1,950 and $1,975.

ETH briefly rebounded after touching $1,828, but the recovery stalled around $1,850. That left the token near the lower end of its recent trading range and inside the closely watched $1,800–$1,850 support area.

The broader daily structure also remains defensive. Ethereum trades below its 50-day simple moving average at $1,889, its 100-day SMA at $1,927, and its 200-day SMA at $2,089.

Weak liquidity deepens Ethereum’s sell-off

The immediate pressure came from Ethereum’s failure to reclaim the moving-average resistance between $1,889 and $1,927. Sellers entered after the latest attempt faded, pushing ETH below $1,850 and toward its Aug. 3 low.

The 4-hour chart shows the price rolling over after forming a broad curved top below $1,975. Lower highs since late July suggest that buying demand has weakened, although ETH must still break below $1,800 to confirm a larger bearish continuation.

Momentum indicators support the cautious outlook. The 4-hour Moving Average Convergence Divergence remains below zero, with the MACD line near -10.46 and the signal line at about -9.92.

Chaikin Money Flow stands at -0.14. The negative reading indicates that selling volume has outweighed buying volume over the indicator’s measurement period.

Ethereum also faces broader liquidity pressure. A sharp weekly decline in Binance stablecoin netflows suggests less immediately available capital is entering the exchange, potentially reducing the buy-side liquidity available during market declines. However, exchange flows can change quickly and do not determine price direction alone.

Longer-term concerns include weaker institutional demand for Ethereum products relative to Bitcoin and lower mainnet fee revenue as activity shifts toward Layer-2 networks. These factors have weakened Ethereum’s investment narrative, but the current move remains primarily tied to the chart rejection and wider risk-off positioning.

Losing $1,800 could expose ETH to $1,700

The first support range sits between $1,828 and $1,800. ETH has already attracted buyers near the upper part of that zone, but repeated tests could weaken the remaining demand.

Ethereum’s lower daily moving-average ribbon stands near $1,785. A daily close below that level would strengthen the bearish setup and expose $1,700, followed by the June accumulation region around $1,550–$1,600.

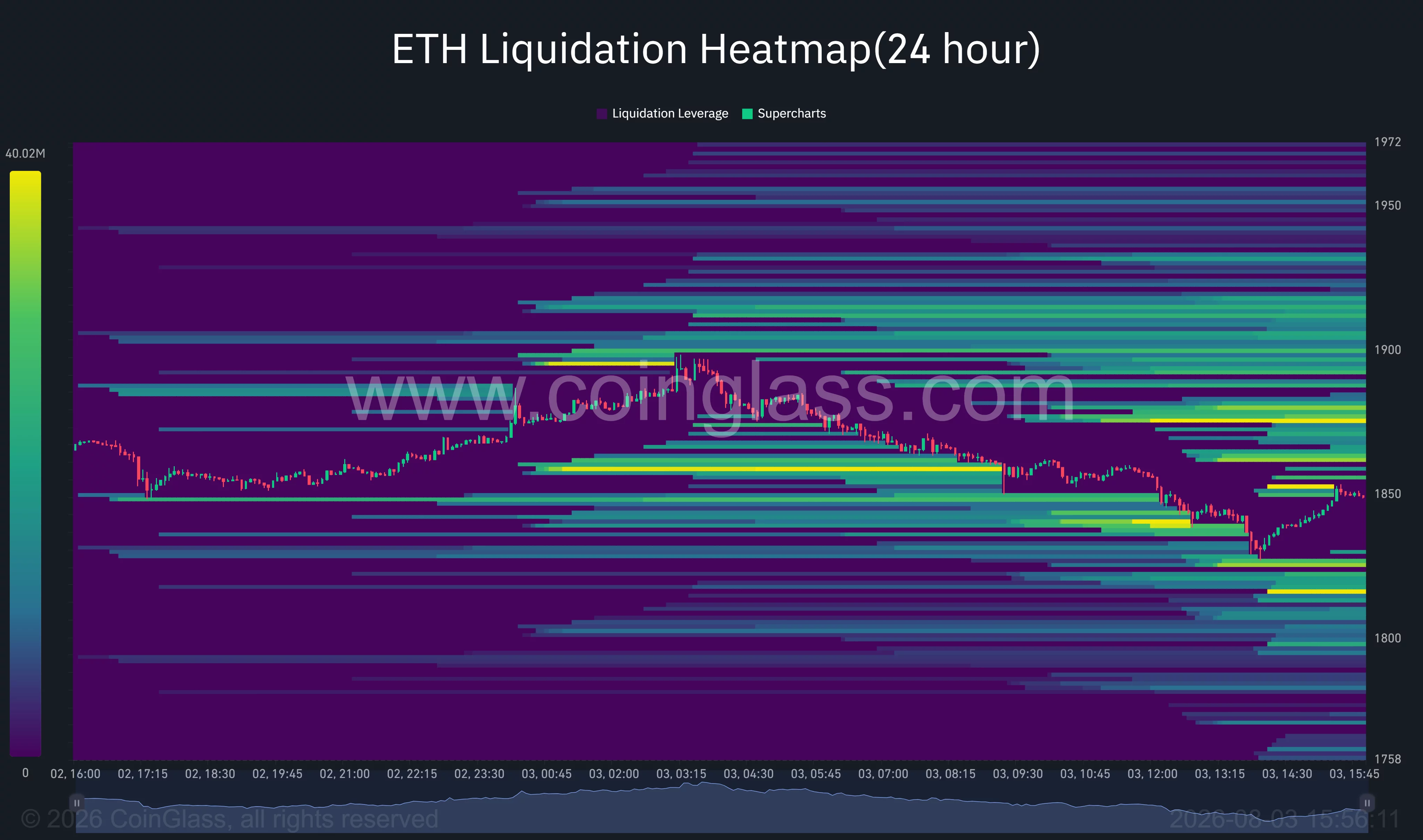

CoinGlass’ 24-hour liquidation heatmap shows nearby leveraged-position clusters around $1,840, $1,820 and $1,810. A move through those levels could liquidate leveraged long positions and accelerate short-term volatility.

The map also shows overhead liquidity around $1,860–$1,875. If ETH rebounds above that range, short liquidations could help drive the price toward $1,890 and $1,920.

On the upside, Ethereum must first reclaim its 50-day SMA at $1,889. A daily close above the 100-day SMA at $1,927 would improve the setup, while a breakout above $1,975 would invalidate the current sequence of lower highs and place $2,000 back in focus.

The daily Relative Strength Index stands at 48.81, below its signal average of 56.44. The reading points to weakening momentum but remains well above oversold territory, leaving room for further selling if $1,800 fails.

Analyst sees Ethereum at a critical support zone

Crypto analyst Ted Pillows described the current support range as decisive for Ethereum’s next move.

“ETH is currently in the $1,800–$1,850 support level,” Pillows said. “This is very crucial for Ethereum to hold, or else it could drop towards $1,700.”

His chart presents two potential paths. Holding the current zone could allow ETH to recover toward $1,950 and then $2,050, while a confirmed breakdown could send the price toward $1,700.

The forecast aligns with the support levels visible on the daily chart, but the $1,700 target would require ETH to lose both the psychological $1,800 level and support near $1,785.

Fed outlook adds pressure on US crypto investors

Changing expectations for US monetary policy remain an additional risk for Ethereum and other speculative assets. Higher Treasury yields and a stronger dollar can reduce investor demand for crypto by increasing the relative appeal of dollar-denominated assets.

Slower-than-expected Federal Reserve rate cuts would keep financial conditions tighter and could limit institutional risk-taking. Ethereum may therefore remain sensitive to upcoming US inflation, employment and Fed policy signals.

For US investors, the near-term setup depends on whether ETH can defend $1,800 as macro liquidity remains constrained. A recovery above $1,927 would improve the technical outlook, but a daily close below $1,785 would shift attention toward $1,700.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

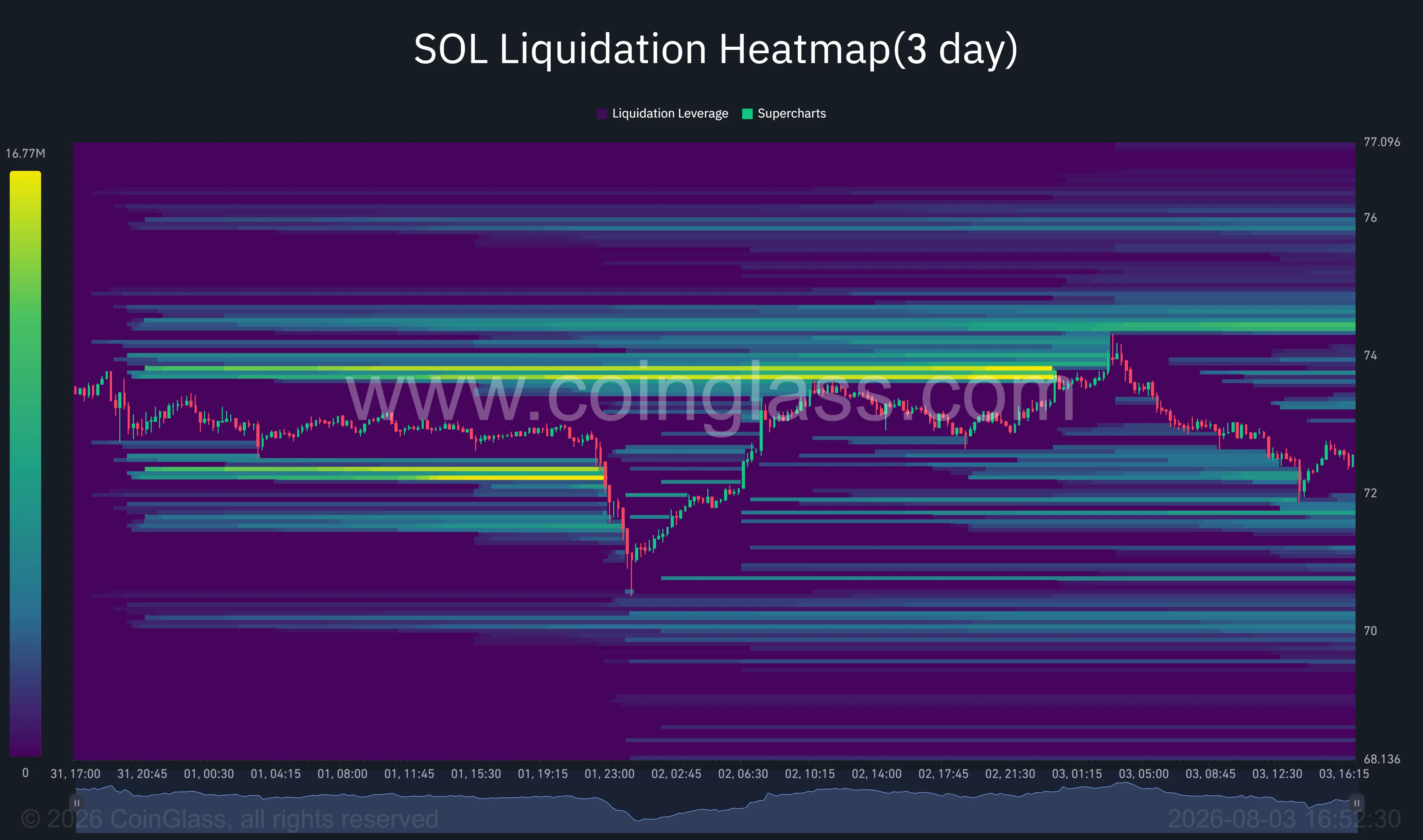

Solana price slipped below $73 on Aug. 3 as weak spot demand and sustained capital outflows raised the risk of a drop toward $70.

Summary

- Solana price fell 1.47% to $72.55, placing the token near its daily lower Bollinger Band.

- The 4-hour chart shows SOL below all four tracked moving averages, with the 200-period SMA at $76.79.

- Chaikin Money Flow dropped to -0.17, indicating that selling pressure continued to outweigh buying demand.

- Liquidation liquidity is concentrated near $73.50–$74.50, making that zone the first major upside test.

Solana price extends its decline below $73

According to data from crypto.news, Solana (SOL) price traded at $72.55 on Aug. 3, down 1.47% on the daily chart after moving between an intraday high of $73.67 and a low of $71.98.

The decline extended a broader pullback from the July high near $82.50. SOL has formed a sequence of lower highs since that peak, with sellers defending rebounds around $78 and then $76.

Price has now fallen below the daily Bollinger Band midpoint at $75.09. This level previously acted as support but has turned into the first major resistance area.

SOL briefly moved below the lower Bollinger Band at $71.49 before recovering above $72. That reaction shows buyers remain active around $71.50–$72, but the limited rebound suggests they have not regained control.

The Awesome Oscillator stood at -3.56, with its red bars expanding below zero. That reading points to strengthening bearish momentum on the daily timeframe rather than an immediate trend reversal.

Flat spot demand weakens SOL’s recovery

Solana attempted to rebound after falling toward $71 on Aug. 2, but spot demand failed to recover alongside price.

Analyst Ted Pillows described the divergence as a sign of weakness.

“$SOL is bouncing back. But spot demand is flat. Sign of weakness.”

The 4-hour Chaikin Money Flow reading supports that view. CMF fell to -0.17, meaning more capital was leaving SOL than entering it during the measured period.

Declining spot participation can leave a rebound dependent on leveraged derivatives positions. Such moves are more vulnerable to reversals because they lack the direct buying pressure needed to absorb new selling.

The weakness also comes as activity tied to speculative Solana tokens cools from previous peaks. Lower decentralized exchange activity and weaker fee generation would reduce one source of demand for SOL, which traders need to pay network fees and interact with on-chain applications.

Four-hour indicators keep sellers in control

Solana remains below every major moving average displayed on the 4-hour chart. The 20-period SMA stands at $72.96, followed by the 50-period SMA at $73.88 and the 100-period SMA at $75.06.

The 200-period SMA, currently near $76.79, represents the strongest overhead technical barrier. SOL would need to reclaim that level to weaken the current sequence of lower highs.

The moving averages are also bearishly ordered, with each shorter-term average sitting below the longer-term measures. That structure suggests the decline is established across several trading horizons.

A move above $72.96 could open a retest of $73.88. The $73.88–$75.06 range is particularly important because it combines two moving averages with liquidity visible on the three-day liquidation heatmap.

Failure to reclaim that area would leave SOL exposed to another test of $71.50. A daily close below the lower Bollinger Band could bring $70 into focus, followed by the June support region near $67.50.

Liquidation clusters could increase volatility

CoinGlass’ three-day liquidation heatmap shows the largest nearby concentration of leveraged positions above the current price, particularly around $73.50–$74.

Additional liquidity appears near $74.50 and $76, creating potential targets if SOL begins a short-covering rebound. A move into these clusters could force bearish traders to close positions, accelerating the recovery.

However, liquidity also appears below the market around $71.50 and $70. These clusters could attract price if support near $72 fails.

This leaves SOL between competing liquidity zones. The closer upside concentration could produce a short-term bounce, but the weak CMF reading and bearish moving-average structure suggest any recovery must be confirmed by stronger spot buying.

Fee-burn vote offers Solana a potential catalyst

SolanaFloor reported that proposals addressing Solana’s fee burn and token disinflation were set to enter an initial vote on Aug. 3.

According to the report, the measures would double annual disinflation to 30%, remove about $1.36 billion in projected token issuance over six years and increase daily burns from roughly 650 SOL to 9,000 SOL.

Those figures remain projected outcomes rather than confirmed changes. The proposals must progress through governance before they can alter SOL’s supply dynamics.

For US investors, the immediate backdrop also remains tied to broader risk appetite. High-beta tokens such as SOL can face added pressure when elevated Treasury yields make lower-risk dollar assets more attractive. A shift in Federal Reserve expectations or US yields could therefore affect whether buyers return at the current support zone.

The short-term outlook remains bearish below $75.06. Reclaiming that level would improve the setup and expose $76.79, while a confirmed break below $71.49 would increase the risk of a move toward $70.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

URGENT XRP HOLDERS, WATCH THIS BEFORE AUGUST 5TH

Family tributes to Ava Gillies following crash on A170

Horizon Kinetics Q2 2026 Commentary

-

Business5 days ago

Business5 days agoWhy Trees Belong on the Risk Register

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Wit & Wisdom

-

Politics3 days ago

Politics3 days agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Entertainment6 days ago

Entertainment6 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Crypto World2 days ago

Crypto World2 days agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics6 days ago

Politics6 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Business5 days ago

Business5 days agoMajor shareholder moves on Canyon

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger v3.3.0 brings five institutional features

-

News Videos4 days ago

News Videos4 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World6 days ago

Crypto World6 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech7 days ago

Tech7 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

Politics4 days ago

Politics4 days agoLuke Littler’s dominance sparks GOAT debate

-

News Videos6 days ago

News Videos6 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Business6 days ago

Business6 days agoJohnson & Johnson agrees to $5.5B settlement over talc cancer claims

-

Sports4 days ago

Sports4 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Crypto World1 day ago

Crypto World1 day agoCrypto PAC spending tops $2M in Michigan House race

-

Business3 days ago

Business3 days agoTrump Announces Hamas Disarmament Agreement as Iran Strikes Kuwait Air Base and US Attacks Pause Overnight

-

Tech5 days ago

Tech5 days agoGemini can now summarize the messiest comment threads in Google Docs

-

Crypto World3 days ago

Crypto World3 days agoNew York sues Kalshi over prediction market gambling

-

Tech1 day ago

Tech1 day agoESET tracks rise in malicious AI skills and adaptable malware

You must be logged in to post a comment Login