Crypto World

Ondo Finance (ONDO) Price Prediction 2026, 2027-2030

ONDO

$0.3757

24h Volume$422.79M

Market Cap$1.83B

24h Low/High$0.3511 / $0.4289

Last updated: June 04, 2026 07:12 · Live price: $0.3757 (-10.88% 24h)

Ondo Finance Price Statistics

| Ondo Finance Price | $0.3757 |

|---|---|

| Price Change 24H | -10.88% |

| Price Change 7D | +5.32% |

| Price Change 30D | +17.49% |

| Market Cap | $1.83B (#46) |

| 24H Volume | $422.79M |

| 50-Day SMA | $0.3413 |

| 200-Day SMA | $0.3417 |

| 14-Day RSI | 44.2 |

| Technical Signal | bearish, neutral |

Ondo Finance trades between $0.43 and $0.45 in late May 2026, market cap around $2.19 billion (#44), roughly 79 percent below its $2.14 high from early 2024. The setup is unusual because most RWA platforms remain speculative. Ondo has shipped product that is processing real institutional volume. Tokenized US Treasury market on Ethereum hit $8 billion ATH in May 2026 with Ondo’s products among the leading contributors. OUSG (Ondo Short-Term US Government Treasuries) holds $680 million in TVL, with BlackRock’s BUIDL fund aongside allocations to Franklin Templeton, WisdomTree, Fidelity, and Wellington/FundBridge vehicles. Ondo Global Markets (the tokenized stocks and ETFs platform) crossed $1.5 billion in TVL by May 2026. The company acquired Oasis Pro in late 2025, securing SEC licenses that removed key US regulatory barriers for institutional products. EU regulatory approval came simultaneously, allowing tokenized stocks and ETFs across 30 European markets. ONDO is deployed across Ethereum, Solana, Sui, and the XRP Ledger with continued multi-chain expansion. The platform integrates with Ripple, J.P. Morgan, and other major institutional finance firms. On May 21, 2026, ONDO surged 10 percent on SEC rumor that tokenized stock trading might be permitted with TVL surpassing $1.5 billion. MEXC launched a $1 million Ondo Stocks Carnival the same day featuring zero-fee trading. The honest read is Ondo represents the cleanest pure-play exposure to institutional RWA tokenization in 2026, with the real advantage being that the platform actually has institutional products processing real volume rather than speculative roadmap promises. The real challenges are also concrete: ONDO token has limited direct value capture from platform operations, 4.87 billion circulating of 10 billion max supply creates ongoing unlock pressure, competition from BlackRock’s BUIDL, Franklin Templeton’s BENJI, and emerging institutional tokenization initiatives is intensifying, and broader RWA market growth could happen with or without ONDO token appreciation. This piece walks through what the data actually says, the bull case ($1.50-$4 by 2030), the base case ($0.60-$1.20), and the bear case ($0.20-$0.50), with the variables that determine which one plays out.

Short-Term Ondo Finance Price Targets

| 2026 full-year range | $0.35 – $0.80 |

|---|---|

| 2026 year-end (base) | $0.40 – $0.65 |

| 2026 year-end (bull) | $0.80 – $1.40 |

| 2026 year-end (bear) | $0.30 – $0.42 |

Long-Term Ondo Finance Price Prediction (2026-2030)

| Year | Bear case | Base case | Bull case |

|---|---|---|---|

| 2026 | $0.30 – $0.42 | $0.40 – $0.65 | $0.80 – $1.40 |

| 2027 | $0.25 – $0.40 | $0.50 – $0.80 | $1.20 – $2.20 |

| 2028 | $0.22 – $0.45 | $0.55 – $0.95 | $1.50 – $3.00 |

| 2029 | $0.20 – $0.48 | $0.60 – $1.10 | $1.50 – $3.60 |

| 2030 | $0.20 – $0.50 | $0.60 – $1.20 | $1.50 – $4.00 |

The 2030 range across scenarios is wide ($0.20 to $4.00, a 20x spread). That width reflects the core disconnect: Ondo-the-platform is clearly growing and institutional, while ONDO-the-token has limited direct value capture and ongoing supply pressure. Which scenario wins depends largely on whether governance ships a value-capture mechanism (fee distribution, staking, or buyback) while the platform keeps scaling.

Summary

Ondo Finance is two businesses in one company. The first business is tokenized US Treasuries through OUSG and USDY ($680M and growing). The second is tokenized stocks and ETFs through Ondo Global Markets ($1.5B+ TVL with EU approval across 30 markets and SEC licenses via Oasis Pro acquisition). Both businesses are real, both are growing, and both compete against institutional incumbents (BlackRock BUIDL, Franklin Templeton BENJI) with bigger balance sheets and longer institutional relationships. The bull case for 2030 ($1.50-$4) requires Ondo Global Markets to scale to $10-30 billion TVL, OUSG to grow to $5-10 billion, ONDO token value capture to materialize through governance fees or revenue distribution, regulatory clarity supporting tokenized stocks at federal level, and competitive moat maintenance against BlackRock and Franklin Templeton. The base case ($0.60-$1.20) assumes moderate growth across both business lines, ONDO maintains its position as one of multiple RWA tokenization leaders, governance value remains limited, and competitive dynamics stay balanced. The bear case ($0.20- $0.50) assumes BlackRock and traditional institutional incumbents capture the bulk of institutional tokenization volume, ONDO governance token fails to capture meaningful value despite platform growth, token unlocks continue creating supply pressure, and the broader RWA narrative cools.

Why Ondo is at $0.43 right now

The current Ondo price reflects multiple competing forces unique to RWA tokenization platforms.

The starting point: ONDO peaked at $2.14 in early 2024 during peak RWA narrative momentum. The decline to current $0.43 reflects multiple specific pressures: token unlock pressure as scheduled distributions continue, broader altcoin weakness through 2024-2026, and the disconnect between platform-level growth and token value capture that affects most governance tokens without direct fee accrual mechanisms.

The platform fundamentals are concrete and growing. OUSG holds $680 million across tokenized US Treasury products built on top of institutional money market fund vehicles (BlackRock BUIDL, Franklin Templeton BENJI, WisdomTree, Fidelity, Wellington/FundBridge). The 30-day APY of approximately 3.19 percent reflects actual short-term Treasury yields. The product structure is genuinely institutionalgrade: holders are limited to US Qualified Purchasers, the underlying assets are real-world securities, and the infrastructure is built for compliance with traditional finance regulatory frameworks.

USDY (Ondo’s dollar-yielding stablecoin alternative) provides yield-bearing dollar exposure without requiring qualified purchaser status. The product is positioned for retail and non-US institutional accessibility. Combining OUSG (institutional-restricted, higher-yield) and USDY (broader-access, loweryield) provides differentiated product set.

Ondo Global Markets is the tokenized stocks and ETFs platform. TVL crossed $1.5 billion by May 2026 with EU regulatory approval allowing the platform to offer tokenized stocks across 30 European markets. The platform allows institutional and retail users to trade tokenized representations of US stocks and ETFs with on-chain settlement.

The Oasis Pro acquisition in late 2025 secured SEC licenses for institutional products. The acquisition removed key US regulatory barriers and enables broader institutional access to Ondo’s tokenized products. The licenses cover alternative trading system operations and broker-dealer activities required for institutional tokenization.

The institutional integrations are real. Ondo integrates with Ripple (covered in detail in your XRP piece – tokenized US Treasury pilot announced February 2026 by J.P. Morgan, Mastercard, and Ondo). J.P. Morgan’s involvement extends to multiple settlement and tokenization initiatives. The integrations provide validation that institutional finance views Ondo as legitimate infrastructure partner.

The May 21, 2026 catalyst pushed ONDO 10 percent higher on SEC rumor regarding tokenized stock trading permissions. The actual SEC announcement remained pending but the rumor showed market sensitivity to regulatory developments affecting Ondo’s core business. MEXC’s $1 million Ondo Stocks Carnival the same day promoting zero-fee trading provided additional exposure and accessibility.

The competitive context matters. BlackRock’s BUIDL fund grew to over $2.5 billion. Franklin Templeton’s BENJI continued expanding. The tokenized US Treasury market on Ethereum hit $8 billion ATH in May 2026 with multiple participants. Ondo competes against well-capitalized traditional finance incumbents but with the advantage of being crypto-native and having stronger DeFi integration.

The token economics are the structural challenge. ONDO is a governance token without direct fee accrual mechanism. Platform revenue from OUSG management fees (0.15 percent), USDY yields, and Ondo Global Markets transaction fees flows to the underlying business rather than the ONDO token directly. Governance value depends on DAO decisions about future value capture mechanisms, which haven’t been clearly set.

Supply dynamics create ongoing pressure. 4.87 billion ONDO are in circulation out of 10 billion max supply. Continued scheduled unlocks add to circulating supply throughout 2026-2027 period. The January 2025 unlock of 1.94 billion tokens created significant supply expansion that the market is still absorbing.

At $0.43, the market is rewarding Ondo’s platform but penalizing the token. The platform keeps shipping product (OUSG, USDY, Mastercard, BlackRock integration) but ONDO itself has no direct fee accrual. The supply keeps expanding through unlocks. Governance tokens for traditional-finance-style infrastructure businesses are a category the market hasn’t decided how to price.

The bull case: $1.50-$4 by 2030

The bull case requires multiple variables resolving favorably and assumes ONDO captures meaningful value from platform growth.

Ondo Global Markets scaling to $10-30 billion TVL. The platform reached $1.5 billion by May 2026 with growth trajectory. Bull case requires continued scaling through expanded asset coverage (more stocks, more ETFs, additional asset classes), geographic expansion beyond current EU 30-market approval, and institutional adoption from major financial institutions seeking on-chain access to tokenized securities. The 7-10x scaling from current TVL is plausible given the broader RWA market trajectory ($8 billion tokenized Treasury market on Ethereum alone, growing).

OUSG and USDY scaling to $5-10 billion combined. The current $680 million OUSG and additional USDY represent meaningful but small share of the $8 billion tokenized Treasury market. Bull case requires Ondo capturing larger market share through superior product structure, institutional relationships, and regulatory positioning. The institutional preference for tokenization-as-service (which Ondo provides) versus building proprietary tokenization could drive market share gains.

ONDO token value capture mechanism deployment. The bull case requires the DAO or company to set direct value capture from platform revenue. Possible mechanisms: governance-driven fee distribution to ONDO holders, staking yields backed by platform revenue, buyback-and-burn programs funded by platform fees, or other mechanisms creating direct economic linkage between platform growth and token value. The mechanism doesn’t currently exist meaningfully but is a possible future development.

Regulatory clarity supporting tokenized stocks at federal level. The SEC rumor that produced May 21 catalyst would need to crystallize into actual approval for tokenized stock trading in US markets. Combined with CLARITY Act framework providing broader crypto regulatory clarity, the regulatory environment could support Ondo Global Markets US expansion. US institutional access would dramatically expand the platform’s TVL potential.

Competitive moat maintenance against BlackRock and Franklin Templeton. The bull case requires Ondo to defend its position as institutional crypto-native partner rather than getting displaced by traditional finance incumbents building proprietary tokenization. Differentiation: Ondo’s DeFi integration capabilities, multi-chain deployment (Ethereum, Solana, Sui, XRPL), and developer ecosystem create advantages BlackRock’s BUIDL doesn’t match in pure-crypto-native contexts.

The Trump administration RWA policy support. The current administration has signaled pro-tokenization policies. The CLARITY Act provides regulatory framework. Specific RWA-friendly policies (covered in your CLARITY Act and Strategic Bitcoin Reserve pieces) create supportive environment for Ondo’s institutional positioning.

The crypto cycle supporting altcoin appreciation. Bitcoin reaching new highs sustained above $150K. Altcoin rotation producing institutional capital flow to mid-cap altcoins. Broader crypto market dynamics support ONDO appreciation alongside platform-level growth.

Targets if bull case conditions materialize: – 2026 year-end: $0.80-$1.40 – 2027 year-end: $1.20-$2.20 – 2028 year-end: $1.50-$3.00 – 2029 year-end: $1.50-$3.60 – 2030 year-end: $1.50-$4.00

The upper end ($4) requires sustained execution across all variables including ONDO governance token capturing meaningful value from $30+ billion platform TVL. The lower bull case ($1.50) is achievable through platform scaling combined with moderate value capture mechanism deployment.

The base case: $0.60-$1.20 by 2030

The base case assumes meaningful platform growth with limited token value capture mechanism deployment.

Ondo Global Markets scaling to $4-8 billion TVL. Growth continues from current $1.5 billion levels through expanded asset coverage and geographic reach but at slower pace than bull case. The platform captures specific institutional niches without dominating the broader tokenized securities market.

OUSG and USDY scaling to $2-4 billion combined. Continued growth from current levels but with intensifying competitive pressure from BlackRock BUIDL, Franklin Templeton BENJI, and emerging institutional tokenization initiatives. Ondo maintains its position as significant but not dominant tokenized Treasury platform.

ONDO token value capture remains limited. The DAO discusses but doesn’t deploy transformative value capture mechanisms. Governance token continues to derive value primarily from speculative trading rather than direct economic linkage to platform revenue. Some moderate developments (staking introduction, limited governance-driven distributions) may occur.

Regulatory developments produce mixed outcomes. EU framework continues supporting platform expansion. US regulatory developments are positive but slow. CLARITY Act deployment supports general crypto adoption but specific tokenized stock SEC approval remains delayed.

Competitive dynamics stabilize. BlackRock BUIDL and Franklin Templeton BENJI capture significant institutional tokenization volume but Ondo maintains its niche. Crypto-native and DeFi-integrated positioning provides defensible competitive position without dominating.

Supply dynamics play out predictably. Continued scheduled unlocks add to circulating supply through 2027-2028 period before unlock pressure compresses. Token economics improve gradually but don’t transform.

The broader crypto cycle provides moderate support. Bitcoin reaches $130-160K range with altcoin rotation producing periodic Ondo rallies. ONDO participates in altcoin cycles without leading.

Targets in base case: – 2026 year-end: $0.40-$0.65 – 2027 year-end: $0.50-$0.80 – 2028 year-end: $0.55- $0.95 – 2029 year-end: $0.60-$1.10 – 2030 year-end: $0.60-$1.20

The base case represents moderate appreciation from current $0.43 levels but stays well below the $2.14 all-time high. The support comes from continued platform growth and gradual institutional adoption. The structural pressure comes from limited token value capture and ongoing supply expansion.

The bear case: $0.20-$0.50 by 2030

The bear case requires adverse outcomes across multiple variables.

Traditional finance incumbents dominate institutional tokenization. BlackRock BUIDL scales to $20+ billion. Franklin Templeton BENJI captures growing institutional share. Major banks (JPMorgan Onyx, State Street, BNY Mellon) build proprietary tokenization platforms. Ondo’s institutional positioning erodes to specialty product rather than primary platform.

Ondo Global Markets growth stalls. EU expansion produces limited additional TVL beyond current levels. US regulatory approval for tokenized stocks remains delayed indefinitely. The platform captures specific niches without scaling to bull-case-required levels.

ONDO token value capture fails to develop. The DAO doesn’t deploy meaningful value capture mechanisms. Governance token continues to derive value from speculation rather than fundamental economics. Token holders increasingly question the value proposition relative to direct holding of underlying assets (USDY for yield, traditional ETFs for stock exposure).

Token unlocks overwhelm demand. Continued scheduled distributions create persistent sell-pressure that fundamental demand can’t absorb. Combined with broader altcoin weakness, supply expansion pushes price below current $0.43 levels sustainably.

Regulatory deterioration. CLARITY Act stalls or fails to provide expected framework. Post-2029 administration reverses RWA-friendly policies. International regulatory pressure increases on tokenization platforms. SEC takes adverse action under shifting priorities.

Competitive displacement by emerging RWA platforms. New entrants with stronger institutional relationships, better technology, or more favorable tokenomics capture market share Ondo was positioning to serve. Securitize, Centrifuge, or new platforms grow faster than Ondo.

The RWA narrative cools. Broader institutional adoption develops slower than expected. The “tokenization will eat traditional finance” narrative that supported RWA valuations doesn’t deliver on aggressive timelines. Institutional capital flows to other crypto themes.

The macro deterioration. Higher US interest rates reduce relative attractiveness of tokenized Treasury yields. Broader altcoin weakness during sustained risk-off periods. Crypto market weakness affects all altcoins including RWA-themed assets.

Targets in bear case: – 2026 year-end: $0.30-$0.42 – 2027 year-end: $0.25-$0.40 – 2028 year-end: $0.22- $0.45 – 2029 year-end: $0.20-$0.48 – 2030 year-end: $0.20-$0.50

The bear case represents 5-55 percent downside from current $0.43 levels. Even in bear scenarios, ONDO retains some value given platform fundamentals and continued operation. Complete failure scenarios would require platform-level operational issues combined with broader market collapse.

The five variables that determine the outcome

Five variables that track which scenario is materializing.

Variable 1: Ondo Global Markets TVL trajectory. The single most important platform variable. Currently $1.5 billion. Bull case requires $10-30 billion by 2030. Monitor: monthly TVL reporting, asset coverage expansion (additional stocks, ETFs, asset classes), geographic expansion (EU markets activation, additional jurisdictions), institutional adoption announcements, and competitive positioning versus traditional finance incumbents.

Variable 2: OUSG and USDY market share in tokenized Treasury market. Currently $680 million OUSG in $8 billion total tokenized Treasury market (8.5 percent share). Bull case requires significant share expansion. Monitor: monthly OUSG and USDY market cap, total tokenized Treasury market growth, BlackRock BUIDL trajectory, Franklin Templeton BENJI growth, competitive dynamics among institutional tokenization providers.

Variable 3: ONDO token value capture mechanism deployment. Currently limited. Monitor: DAO governance proposals for fee distribution, staking mechanisms introduction, buyback-and-burn programs deployment, revenue distribution discussions, and any direct economic linkage between platform growth and ONDO token value.

Variable 4: Regulatory developments affecting institutional tokenization. SEC tokenized stock rulings, CLARITY Act deployment specifics, EU MiCA framework operational impact, additional jurisdictional approvals beyond current EU 30-market access. Monitor: SEC announcements, CLARITY Act deployment milestones, Ondo regulatory filings and approvals, competitor regulatory developments.

Variable 5: Competitive positioning versus BlackRock BUIDL and Franklin Templeton BENJI. The largest institutional incumbents in tokenization. Monitor: BlackRock BUIDL TVL trajectory, Franklin Templeton BENJI growth, JPMorgan Onyx and other bank tokenization initiatives, emerging cryptonative competitors (Securitize, Centrifuge, etc.).

The variables interact significantly. Platform TVL growth supports token interest. Market share gains create defensible competitive position. Token value capture mechanism deployment transforms governance token value proposition. Regulatory developments enable institutional adoption. Competitive positioning determines which institutional capital flows to Ondo versus competitors. All variables compound in producing the eventual price outcome.

What this means for ONDO holders and traders

What this means for ONDO holders and traders For current ONDO holders, the practical implication is the asset’s setup is solid at the platform level but uncertain at the token level. Platform fundamentals (OUSG, USDY, Ondo Global Markets growth, regulatory wins) support the broader investment thesis. Token economics (limited direct value capture, supply expansion) create headwinds that platform growth alone may not overcome.

For potential ONDO buyers, current $0.43 reflects substantial discount from all-time high combined with developing institutional adoption. The risk-reward depends on assessment of platform growth probability (high given current trajectory), value capture mechanism deployment probability (uncertain), and competitive dynamics versus traditional finance incumbents (Ondo well-positioned but facing strong competition). Entry at current levels has asymmetric upside if value capture develops, modest upside if platform grows but value capture remains limited.

For traders, ONDO has showed catalyst sensitivity around: regulatory announcements (SEC tokenized stock rumors produce 10+ percent moves), TVL milestones, institutional partnership announcements, and broader RWA narrative momentum. Trading the catalysts requires monitoring regulatory developments, partnership announcements, and TVL reporting alongside broader crypto market dynamics.

For institutional investors evaluating ONDO allocation, the platform offers exposure to institutional RWA tokenization through crypto-native infrastructure. The investment case depends on belief in RWA tokenization scaling combined with confidence that crypto-native platforms (versus traditional finance incumbents) capture meaningful share. ETF accessibility could develop following set crypto ETF patterns but is not yet available.

For developers and ecosystem participants, Ondo provides institutional-grade tokenization infrastructure that’s accessible across multiple chains (Ethereum, Solana, Sui, XRPL). The multi-chain deployment creates opportunities for DeFi protocol integration of tokenized RWA assets. The technical infrastructure supports building applications that combine traditional finance assets with DeFi composability.

For traditional finance professionals exploring tokenization, Ondo represents a tested operational alternative to building proprietary tokenization platforms. The platform’s regulatory positioning, institutional partnerships, and technical infrastructure provide reference deployment. Whether to build with Ondo versus building proprietary versus using BlackRock BUIDL or Franklin Templeton BENJI depends on specific use case requirements.

Connection to broader market dynamics

Ondo’s setup connects to several broader dynamics covered in your existing crypto.news editorial work.

The XRP institutional tokenization piece directly connects through the J.P. Morgan, Mastercard, and Ondo XRP Ledger tokenized US Treasury pilot announced February 2026. The pilot shows Ondo’s integration capabilities across major institutional infrastructure providers. The XRPL deployment provides multichain expansion that competing platforms haven’t matched at similar scale.

The CLARITY Act framework (covered in the CLARITY Act series) provides regulatory pathway for tokenized stocks and broader institutional crypto adoption. The Act’s deployment supports Ondo Global Markets US expansion and removes structural barriers for institutional participation.

The Strategic Bitcoin Reserve piece (covered in your Strategic Bitcoin Reserve analysis) creates broader pro-crypto policy environment that benefits institutional tokenization infrastructure. The administration’s crypto-friendly approach supports Ondo’s regulatory positioning.

The WLFI RWA platform comparison (covered in WLFI price prediction) provides direct competitive context. Both Ondo and WLFI’s RWA platform target institutional tokenization but with different capital bases (institutional traditional finance for Ondo, politically-aligned capital for WLFI). The two platforms occupy adjacent positioning rather than direct competition.

The Hyperliquid HYPE buyback comparison provides analytical contrast for value capture mechanisms. HYPE has aggressive direct value capture (99 percent fee-to-buyback). ONDO has indirect value capture dependent on future governance decisions. The contrast highlights why HYPE has produced stronger token appreciation despite less institutional positioning than Ondo.

The TON Pay 2.0 comparison provides framework for institutional infrastructure adoption. TON has Telegram distribution advantage. Ondo has institutional finance partnership advantage. Both target consumer/institutional adoption pathways but through different mechanisms.

The honest bottom line

Ondo is the pure-play institutional RWA tokenization investment. Not the only RWA token, but the only one where BlackRock’s BUIDL fund sits inside an Ondo product, where Mastercard is using Ondo infrastructure to settle stablecoin transactions, and where the team has been shipping institutional-grade product since before “RWA” was a category most analysts knew how to spell.

The platform fundamentals are concrete: $680 million OUSG holding BlackRock’s BUIDL fund and other institutional money market vehicles, $1.5 billion Ondo Global Markets TVL, EU regulatory approval across 30 markets, SEC licenses via Oasis Pro acquisition, J.P. Morgan and Ripple integrations, multichain deployment across Ethereum, Solana, Sui, and XRP Ledger. These are not speculative roadmap items. They are operational businesses processing real volume.

The institutional partnerships validate the positioning. BlackRock’s BUIDL backing OUSG. Franklin Templeton products in OUSG portfolio. Fidelity allocations. Wellington/FundBridge vehicles. JP Morgan tokenized Treasury pilots. Ripple integration. The institutional finance establishment treats Ondo as legitimate tokenization infrastructure partner.

The regulatory wins are substantial. EU 30-market approval for tokenized stocks and ETFs. SEC licenses via Oasis Pro. Operating across multiple jurisdictions with appropriate compliance. The regulatory positioning provides barriers to entry that competing platforms haven’t matched.

The real challenges are equally concrete. ONDO governance token lacks direct value capture mechanism from platform operations. Platform revenue flows to underlying business rather than token holders. 4.87 billion circulating of 10 billion max supply creates ongoing unlock pressure. Competition from BlackRock BUIDL and Franklin Templeton BENJI is intensifying with their stronger balance sheets and longer institutional relationships.

The 2030 range across scenarios is wide: $0.20 to $4.00, representing 20x range. The wide range reflects the disconnect between platform-level growth and token-level value capture. If platform grows substantially and value capture develops, bull case materializes. If platform grows without value capture or competition intensifies, base or bear case dominates.

For holders, the variables that matter are the ones connecting platform success to token value: governance proposals for fee distribution or buyback mechanisms (most important), Ondo Global Markets TVL trajectory (validates platform thesis), regulatory developments (enables expansion), and competitive positioning (determines market share). Platform fundamentals can be excellent while token value stays constrained without value capture mechanism deployment.

For buyers, the question is whether you’re buying ONDO as a platform-growth bet (where moderate appreciation is achievable through platform success) or as a value-capture-deployment bet (where transformative appreciation requires governance mechanism evolution). Different theses have different time horizons and risk profiles.

For the broader market, Ondo represents the test case for whether crypto-native platforms can compete with traditional finance incumbents in institutional tokenization. If Ondo successfully scales against BlackRock BUIDL and Franklin Templeton BENJI, the success shows that crypto-native infrastructure can capture institutional finance market share rather than getting displaced. The outcome affects how the broader RWA category develops.

For 2026, expect ONDO in a $0.35 to $0.80 range with significant catalysts around SEC tokenized stock approval timing, Ondo Global Markets TVL milestones, governance proposals for value capture, and broader RWA market growth. The floor near $0.35 reflects current platform positioning. The upside ($0.65 to $0.80) needs catalysts to land.

For 2027-2030, the question is whether governance evolves to capture platform value. If Ondo’s DAO ships fee distribution or buyback mechanisms while the platform keeps scaling, ONDO trades $1.50 to $4. Without value capture, even strong platform growth produces $0.60 to $1.20. Adverse competitive or regulatory dynamics produce $0.20 to $0.50.

ONDO is the trade for someone who thinks the next leg of crypto adoption comes through traditional finance tokenization rather than memecoin rotation or DeFi innovation. The platform thesis is sound and shipping. The token value capture question is what determines whether holding ONDO produces returns proportional to the platform’s success.

For analysts, the cleanest framework is: separate Ondo-the-platform (clearly growing, clearly institutional) from ONDO-the-token (limited direct value capture, ongoing supply pressure, dependent on future governance decisions). Conflating them produces analytical mess. The platform’s success doesn’t automatically translate to token appreciation without the governance evolution that enables value capture.

What everyone should watch: the next major DAO proposal addressing ONDO value capture from platform revenue. That proposal’s outcome and deployment will largely determine whether bull case or base case becomes the operative trajectory through 2030.

Ondo Finance Technical Analysis

As of June 04, 2026 07:12, Ondo Finance (ONDO) trades at $0.3757. The 50-day SMA ($0.3413) sits below the 200-day SMA ($0.3417), and the 14-day RSI of 44.2 reads as neutral. The combined short-term technical signal is bearish, neutral. Based on realized daily volatility of ~7.81%, the model projects the following short-term ranges:

Ondo Finance Short-Term Projection

| Horizon | Low | Average | High |

|---|---|---|---|

| Today | $0.3473 | $0.3766 | $0.4060 |

| This week | $0.3041 | $0.3817 | $0.4594 |

| Next week | $0.2779 | $0.3877 | $0.4975 |

| Next month | $0.2407 | $0.4015 | $0.5622 |

Short-term ranges are statistical projections from live price and realized volatility, refreshed continuously. They are not guarantees.

Ondo Finance Price Prediction FAQ

What is Ondo Finance’s price prediction today?

Based on live price and current volatility, Ondo Finance (ONDO) is projected to trade between $0.3473 and $0.4060 today, with an average around $0.3766. The current technical signal is bearish, neutral.

What is Ondo Finance’s price prediction for tomorrow?

Tomorrow, Ondo Finance is expected to stay near today’s range of $0.3473–$0.4060, barring a major catalyst. The live model refreshes this estimate continuously from market data.

What is the Ondo Finance price prediction for this week?

For this week, the model projects Ondo Finance between $0.3041 and $0.4594 (average ~$0.3817), based on a realized daily volatility of about 7.81%.

What will the price of Ondo Finance be next month?

Over the next month, Ondo Finance is projected in a $0.2407–$0.5622 range (average ~$0.4015). Short-term ranges widen with the time horizon as uncertainty grows.

What is Ondo Finance and how does it differ from other RWA platforms?

Ondo Finance is a tokenization platform that brings real-world assets like US Treasuries, stocks, and ETFs onto blockchain through institutional-grade infrastructure. Key products include OUSG (tokenized US Treasuries with $680M TVL), USDY (yield-bearing dollar alternative), and Ondo Global Markets (tokenized stocks/ETFs with $1.5B TVL). Ondo differs from competitors through: SEC licenses via Oasis Pro acquisition, EU regulatory approval across 30 markets, BlackRock BUIDL backing for OUSG, multichain deployment (Ethereum, Solana, Sui, XRP Ledger), and integration with J.P. Morgan and Ripple. Differs from BlackRock BUIDL by being crypto-native; from Securitize by having stronger DeFi integration.

Can Ondo reach $4 by 2030?

$4 is at the upper end of the bull case range ($1.50-$4 by 2030). Required conditions: Ondo Global Markets scaling to $10-30 billion TVL, OUSG and USDY combined reaching $5-10 billion, ONDO governance token deploying meaningful value capture mechanism, federal regulatory clarity for tokenized stocks, competitive moat maintenance against BlackRock and Franklin Templeton, and broader crypto cycle supporting altcoin appreciation. The base case for 2030 is $0.60-$1.20.

What is OUSG and how does it work?

OUSG (Ondo Short-Term US Government Treasuries) is a tokenized fund providing on-chain exposure to US Treasuries by investing in institutional money market funds. Portfolio primarily holds BlackRock’s BUIDL fund alongside allocations to Franklin Templeton, WisdomTree, Fidelity, and Wellington/ FundBridge vehicles. Current TVL approximately $680 million. NAV around $115. 30-day APY approximately 3.19 percent. Eligible investors limited to US Qualified Purchasers. Management fee 0.15 percent. Performance fee 0 percent. Inception January 26, 2023.

How does Ondo Global Markets work?

Ondo Global Markets is the tokenized stocks and ETFs platform that received EU regulatory approval allowing trading across 30 European markets. Platform TVL crossed $1.5 billion by May 2026. Allows institutional and retail users to trade tokenized representations of US stocks and ETFs with on-chain settlement. The Oasis Pro acquisition secured SEC licenses removing US regulatory barriers for institutional products. Continued geographic expansion and asset coverage growth represent key bull case variables.

What is the ONDO token’s relationship to platform revenue?

ONDO is currently a governance token without direct fee accrual mechanism. Platform revenue from OUSG management fees (0.15 percent), USDY yields, and Ondo Global Markets transaction fees flows to the underlying business rather than ONDO token directly. Governance value depends on DAO decisions about future value capture mechanisms which haven’t been clearly set. The token’s eventual price appreciation depends substantially on whether governance mechanism evolution creates direct economic linkage between platform growth and token value.

How does Ondo compete against BlackRock BUIDL?

BlackRock BUIDL is the largest tokenized Treasury fund ($2.5+ billion TVL). Ondo competes through: crypto-native infrastructure versus BlackRock’s traditional finance positioning, multi-chain deployment across Ethereum/Solana/Sui/XRPL versus BlackRock’s Ethereum-only initial deployment, stronger DeFi integration capabilities, OUSG product structure (which actually holds BUIDL among other vehicles, making them complementary rather than purely competitive). The competitive dynamic includes both competition (for direct institutional clients) and collaboration (OUSG uses BUIDL as portfolio holding).

What are the main risks to Ondo?

Six primary risks. First, traditional finance incumbents (BlackRock, Franklin Templeton, major banks) dominate institutional tokenization at Ondo’s expense. Second, ONDO governance token fails to develop meaningful value capture mechanism from platform revenue. Third, ongoing token unlocks create persistent sell-pressure. Fourth, regulatory deterioration affecting tokenized stocks specifically (SEC delays, EU framework changes). Fifth, Ondo Global Markets growth stalls below required levels. Sixth, broader RWA narrative cools as institutional adoption develops slower than expected.

Should I buy Ondo given the institutional partnerships?

This piece does not provide investment advice. Current $0.43 reflects substantial discount from all-time high combined with strong platform fundamentals and uncertain token value capture. The risk-reward depends on assessment of platform growth probability (high given current trajectory), value capture mechanism deployment probability (uncertain), competitive dynamics versus traditional finance (Ondo well-positioned but facing strong competition), and broader RWA market growth. Position sizing should reflect that platform success and token appreciation may follow different timelines. The five-variables framework provides objective monitoring signals.

How we forecast Ondo Finance price

Our ONDO forecasts combine platform fundamentals (OUSG and USDY TVL, Ondo Global Markets TVL, institutional partnerships, regulatory approvals) with token-level dynamics (supply schedule and unlocks, governance value-capture status) and broader crypto-cycle context. Rather than a single number, we model bear, base, and bull scenarios tied to five trackable variables, and update the figures as new data lands. Forecasts are scenario-based and inherently uncertain.

This article is for informational purposes and does not make up financial or investment advice. Cryptocurrency markets are highly volatile and price predictions are inherently speculative. The figures and analysis described reflect data available as of late May 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

Latest Ondo News

Read more – Nathan Allman’s sudden death leaves Ondo Finance at a turning point

Ondo Finance founder Nathan Allman dies unexpectedly, with Ian De Bode taking over as CEO while the RWA firm says its mission remains unchanged.

Ondo Finance’s native token $ONDO has broken above $0.46 and is trading near $0.466 with a 24 hour gain above 15 percent, according to data from Gate. Spot market shows ONDO (ONDO) testing the $0.46 level and printing around $0.466…

Read more – Ondo price confirms bull flag breakout, eyes upside to $0.55 as key metrics surge

Ondo price extended its recovery this week after confirming a bullish continuation setup on the daily chart, with rising demand for tokenized real-world assets and strong platform growth metrics reinforcing the bullish outlook. According to data from crypto.news, Ondo (ONDO)…

Read more – Ondo price pauses after rally to yearly highs, bullish setup keeps upside hopes alive

Ondo price cooled slightly on Monday after surging to its highest level of the year, though the broader technical structure still points to growing bullish momentum across the tokenized real-world asset sector. According to data from crypto.news, Ondo (ONDO) price…

The dollar’s next move hinges on tonight’s Fed decision, and this time markets genuinely don’t know what to expect. While economists still lean toward a hold—with CME FedWatch odds sitting near 68.5% for no change—Kevin Warsh’s hawkish rhetoric on having “no tolerance” for inflation, paired with growing internal FOMC support for a hike, has pushed hike odds up sharply from just 18% two weeks ago to over 30% today. Complicating things further, Warsh has deliberately scaled back forward guidance, meaning tonight’s press conference may offer fewer clues than usual.

The euro, meanwhile, has already had its say: the ECB held rates steady at 2.25% last Thursday, as expected, with Lagarde reaffirming the 2% target while flagging that energy-driven inflation risks from the Middle East conflict have yet to fully play out. Eurozone inflation cooled to 2.8% in June, but sticky services inflation near 3.5–4% keeps the door only cautiously open for a September move in either direction.

With EUR/USD trading near 1.1408, tonight’s Fed decision—not the ECB—is what will likely determine the pair’s next major direction.

EUR/USD Technical Analysis

As the EUR/USD chart shows, the pair has been consolidating within a defined range since late June, squeezed between an ascending trendline and a descending trendline, both converging around the current price near 1.1400. The 200-period EMA continues to slope lower above price, reinforcing a cautious backdrop ahead of tonight’s Fed decision.

Bullish Scenario

Should the dollar weaken on a dovish Fed outcome, price would need to break above the converging trendlines and reclaim the 0.382 Fibonacci retracement near 1.1420, with the 200-period EMA just above acting as the next key test. A confirmed break above the EMA would open the path towards the 0.5 and 0.618 retracements near 1.1480–1.1500, where stronger resistance has capped rallies since late June.

Bearish Scenario

Conversely, a hawkish surprise—or even a hike—could send the euro sharply lower, breaking both the ascending trendline and the psychological 1.1360 support level. A confirmed break here would expose the 1.1320 zone, the 0.0 Fibonacci level marking the origin of the entire recovery move, with further downside risk towards fresh multi-week lows if selling pressure accelerates.

With price coiled right at the intersection of both trendlines and the Fed decision just hours away, EUR/USD looks primed for a decisive move. Will the dollar reassert its dominance, or will the euro finally break free of this range?

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Hungary is rolling back strict crypto rules as CoinCash prepares to resume services after receiving authorization under the European Union’s Markets in Crypto-Assets (MiCA) regulation.

The Hungarian parliament voted to repeal the country’s crypto validator requirement, removing mandatory third-party approval for certain crypto transactions, the Hungarian tax and legal publication Ado.hu reported on Tuesday.

Finance Minister Kármán András said the government removed the validation requirement after the previous rules disrupted Hungary’s crypto market, prompting some service providers to halt operations in the country.

“Due to the negative and market-shaking regulations so far, many players have terminated their services related to cryptocurrencies in Hungary, but the market is now showing signs of recovery,” he wrote in a Tuesday Facebook post.

The development marks a significant shift in Hungary’s crypto sector, removing an additional approval step while leaving broader licensing and compliance requirements in place.

How Hungary’s crypto checks worked

Hungary introduced the requirement through its 2024 crypto assets law, creating a separate validation process for certain crypto conversions.

The rules, which took effect on July 1, 2025, required a licensed validator to verify details including the origin of crypto assets, wallet ownership and customer information before issuing a compliance declaration.

Related: Hungary to reverse crypto trading crackdown after EU scrutiny

The system added another transaction-level approval step alongside MiCA. Hungary also applied a shortened MiCA transition period for crypto asset service providers (CASPs), requiring compliance by July 1, 2025, compared with the EU’s maximum transition deadline of July 1, 2026.

The stricter regulatory environment prompted some crypto platforms to suspend services in Hungary, including Budapest-based crypto platform CoinCash, which voluntarily paused operations in December 2025 while pursuing MiCA authorization.

CoinCash receives Hungary’s first MiCA license

The National Bank of Hungary (MNB) granted CoinCash operator Tiwala Solutions authorization under the EU’s MiCA regulation on July 20, according to a company announcement reviewed by Cointelegraph.

“We’re the first and only Hungarian company authorised directly by the National Bank under the EU framework,” CoinCash co-founder said in a LinkedIn post on Friday.

Related: Unauthorized crypto trading now carries 2 years of prison in Hungary

The authorization covers custody, crypto-to-fiat and crypto-to-crypto exchange, transfers, investment advice and portfolio management.

CoinCash said it completed a months-long compliance review before receiving approval and paused operations while preparing to meet the requirements. The company plans to gradually resume services and expand beyond trading into additional MiCA-regulated offerings.

Magazine: The real reason DeFi projects that survived 2022 crash are shutting down now

Coinbase appointed Rob Witoff as chief technology officer on July 28, bringing an early company engineer into the role as the U.S. crypto exchange expands AI-assisted product development.

Summary

- Coinbase appointed longtime engineer Rob Witoff as chief technology officer, confirming the leadership change Tuesday.

- Witoff first joined Coinbase in 2014, returning as platform head in December 2024 after entrepreneurship.

- Coinbase cut approximately 14% of employees in May while rebuilding teams around AI-assisted workflows companywide.

Coinbase’s official leadership page now lists Witoff as CTO.

Chief Executive Brian Armstrong announced the appointment on X and credited Witoff with helping turn Coinbase into “one of the most AI-enabled companies in the world.” That description is Armstrong’s assessment rather than an independently measured ranking.

Rob Witoff returns to a role shaped by Coinbase’s early years

Witoff first joined Coinbase in 2014 and worked there until 2017. Coinbase said he led security and infrastructure, became chief architect and helped build some of the exchange’s earliest systems. He later founded institutional crypto custody company Unit 410, which Coinbase acquired.

Witoff said his interest in Bitcoin began in 2009. He recalled that Coinbase initially supported one cryptocurrency, used a single codebase and ran with a small engineering team. The account provides historical context from the incoming executive, although Coinbase has not independently detailed every technical claim in the July 27 post.

The company brought him back in December 2024 as head of platform and a member of the executive team. Witoff said his latest “tour of duty” began with a goal of making Coinbase “the best place in the world to build.” That remains a forward-looking management objective.

Coinbase CTO appointment comes during an AI overhaul

The promotion follows a broad change in how Coinbase develops software and organises teams. In May, the company announced plans to reduce its workforce by about 14%, or roughly 700 roles, while flattening management and building smaller teams around AI tools.

Armstrong said AI allowed engineers to complete work in days that previously took teams weeks. He also outlined experiments with “one person teams” combining engineering, product and design work. Those plans describe Coinbase’s intended operating model; their long-term effect on output, costs and staff workloads is not yet established.

Coinbase later said nearly all newly merged code had become AI-generated and human-reviewed. Its July engineering report said the share rose from 5.7% in the first quarter of 2025 to roughly 100% by mid-2026, while maintaining human review and compliance controls.

Witoff inherits reliability and security responsibilities

The CTO will oversee technology while Coinbase expands derivatives, stablecoin payments, prediction markets and services for AI agents. Each product increases the need for dependable infrastructure, security controls and fast incident response.

Coinbase experienced a roughly 50-minute service disruption on July 14 after a routine configuration update affected a shared production cluster. Transfers, card payments and some onchain services were interrupted. The company said customer funds were not at risk and later announced new deployment safeguards and recovery procedures.

Witoff’s background in security, architecture and platform engineering gives him direct experience with those areas. However, Coinbase has not published new performance targets, budget commitments or a separate technology roadmap tied to his appointment.

Leadership changes continue across Coinbase

The CTO appointment follows another executive transition. Chief Legal Officer Paul Grewal notified Coinbase on July 8 that he would leave his post on July 31. Molly Abraham is expected to become general counsel and corporate secretary, while Grewal will serve as an adviser through October.

As crypto.news previously reported, Coinbase’s May restructuring placed AI-native development at the centre of its operating plan. In related coverage, crypto.news reported that Coinbase had launched tools allowing authorised AI agents to trade, make payments and perform financial tasks.

Coinbase plans quarterly reviews of its AI-focused engineering interview process and 45-day and 90-day assessments for new hires. The next test for Witoff will be whether the company can keep releasing products quickly while maintaining security, reliability and regulatory controls.

It raised $400 million in June through a private placement of convertible preferred shares and warrants. The preferred shares, priced at $53 each, converted into common stock upon completion of the listing. Investors agreed not to transfer the securities below $70 until six months after the listing, according to the filing.

Ionic decommissioned bitcoin mining at its Ward County, Texas, site in December and committed its 234 MW of capacity to Nscale under a 126-month lease carrying $1.95 billion in contracted revenue, according to the registration statement.

The company said it expects as much as $195 million in revenue this year, with more than 90% coming from infrastructure leasing. It held 2,815.6 bitcoin worth $192.1 million and had no debt as of March 31.

Uzbekistan has established a special crypto mining zone across Karakalpakstan, introducing tax incentives, expanded power options, and a dedicated regulatory framework to attract licensed mining companies.

Summary

- Uzbekistan has launched the Beshkala Mining Valley as a regulated crypto mining zone across Karakalpakstan

- Licensed miners can use grid power, renewable energy, and hydrogen while receiving tax exemptions through 2035

- Mining companies must keep crypto sale proceeds in Uzbek banks and operate under state licensing rules

- The project allows miners to reuse excess heat for greenhouse farming as part of the regional development plan.

Under a presidential resolution that took effect on April 20, Uzbekistan has designated the entire Republic of Karakalpakstan as the Beshkala Mining Valley, creating a regulated environment for cryptocurrency mining while linking the initiative to the region’s economic development plans.

The resolution allows licensed mining companies operating within the zone to use electricity from the national grid, renewable energy sources such as solar power, and hydrogen-based power generation. It also creates a legal pathway for miners to sell their digital assets through Uzbekistan’s licensed crypto exchanges, foreign trading platforms, direct agreements, or by converting them into other liquid crypto assets.

Companies participating in the program must transfer revenue from crypto asset sales to bank accounts held in Uzbekistan, a requirement intended to keep transactions within the country’s regulated financial system while maintaining oversight of mining-related income.

Uzbekistan has expanded the crypto mining framework

Only legal entities registered in Karakalpakstan will qualify for resident status within the Beshkala Mining Valley. Businesses seeking to operate there must first obtain resident status through the zone’s directorate before applying for a crypto mining license issued under the supervision of the National Agency for Perspective Projects, the authority responsible for regulating the sector.

A dedicated directorate will oversee the management of the mining valley and process applications from prospective operators. Besides regulating mining activity, the administration will supervise implementation of the project’s development policies across the region.

Mining companies will also be permitted to reuse excess heat generated by their equipment for greenhouse farming on agricultural land, creating an additional use for energy produced during mining operations.

The resolution exempts income earned from mining activities from taxes and mandatory payments until Jan. 1, 2035, providing one of the main financial incentives for companies considering investment in the zone.

Crypto miners can use more than solar power

The latest framework also changes part of Uzbekistan’s previous mining policy.

Earlier licensing rules introduced in October 2023 required miners to obtain official authorization before operating and largely limited mining activities to electricity generated from solar power, except where legislation provided otherwise.

Under the new framework for the Beshkala Mining Valley, approved residents can instead draw power from the unified electricity grid alongside renewable energy and hydrogen-based generation. The updated approach gives operators more flexibility while preserving the country’s licensing requirements for crypto mining businesses.

Uzbek law continues to define crypto mining as the computational process used to maintain distributed ledgers by validating blocks and preserving network integrity. The activity remains restricted to legal entities rather than individual miners.

Mining revenue will remain inside Uzbekistan

Alongside operational rules, the government has tightened financial requirements governing proceeds from crypto mining.

Residents of the mining valley may sell mined digital assets through domestic exchanges, overseas trading platforms, direct contracts, or by exchanging them for other liquid crypto assets. Regardless of where the assets are sold, proceeds must ultimately be transferred to bank accounts located in Uzbekistan.

The framework is intended to keep mining-related revenue within the domestic banking system while allowing companies to access international cryptocurrency markets.

According to an earlier presidential decree signed on April 17 and effective from April 20, residents of the mining zone are also required to pay a monthly fee equal to 1% of mining income to the zone’s directorate, even as they benefit from tax exemptions running through the beginning of 2035.

Karakalpakstan remains central to investment plans

Creation of the Beshkala Mining Valley forms part of Uzbekistan’s ongoing efforts to attract investment into Karakalpakstan, a region that has remained a priority for economic development initiatives.

Government plans have linked the mining zone with improvements in regional living standards while encouraging more efficient use of renewable energy resources through regulated crypto mining projects.

The mining initiative follows another technology-focused program launched for Karakalpakstan in 2025, when Uzbekistan approved a separate tax-free zone for artificial intelligence and data center projects. That program offered discounted electricity prices and tax incentives to foreign investors, with reports stating that investments of at least $100 million could qualify for exemptions from taxes and customs duties until 2040.

Officials said the AI and data center project was designed to attract more than $1 billion in foreign investment by 2030, placing the new crypto mining zone within a series of long-term development initiatives targeting the region.

Russia’s Federal Security Service (FSB) charged Telegram founder Pavel Durov with aiding terrorist activity and placed him on an international wanted list, the agency said Wednesday.

The FSB accused Telegram of failing to remove channels, chats and bots allegedly used by Ukrainian intelligence and extremist groups to coordinate sabotage, attacks and cyber fraud inside Russia, according to Interfax.

Durov charges carry a sentence that could lead to life imprisonment. The FSB did not say whether Russia had requested an Interpol Red Notice, which would not, in itself, constitute an international arrest warrant.

The case escalates an investigation opened in February after Russia began restricting Telegram’s operations. The platform has been fined more than 100 million rubles ($1.25 million) this year, primarily for failing to remove content prohibited under Russian law, Interfax reported.

Telegram is one of crypto’s largest distribution platforms, hosting project communities, trading groups, bots and blockchain-based Mini Apps.

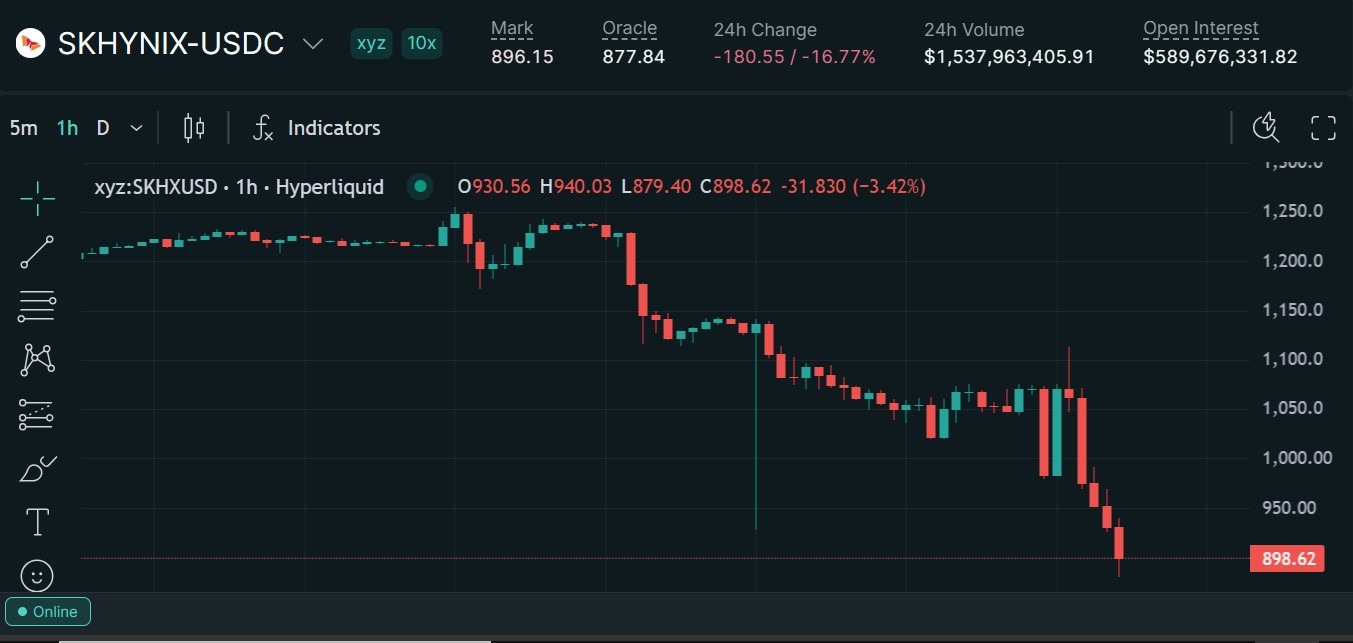

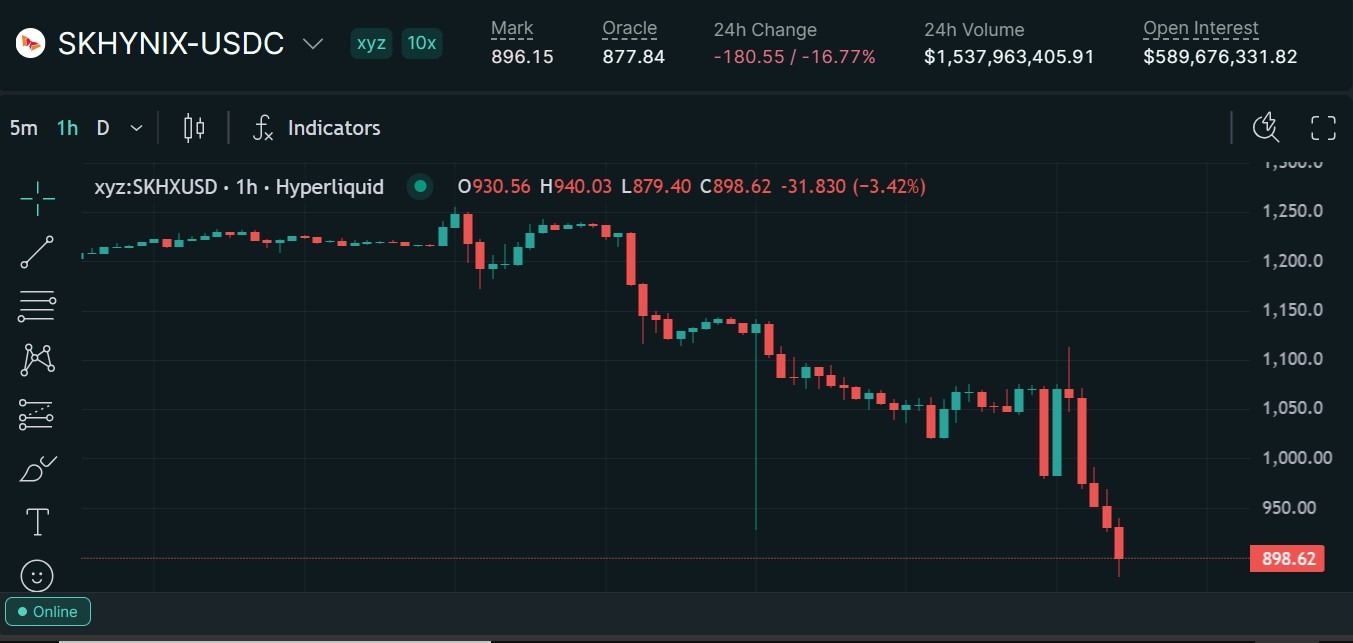

A trader realized a $2.2 million gain during this week’s SK Hynix liquidation incident on Hyperliquid.

Trade.xyz, the team that operates the market, will now cover losses tied to the same event. It maintains that the oracle systems performed as specified.

Trader Banks $2.2 Million While 960 Accounts Get Liquidated

According to Arkham, the trader, Stately, realized approximately $2.2 million in profit after part of his short position in SK Hynix was automatically reduced during an auto-deleveraging (ADL) event during a liquidation cascade.

The trader remains short SK Hynix with an open position worth $13.36 million, which now shows an additional $2.1 million in unrealized gains.

Follow us on X to get the latest news as it happens

The liquidation stems from a sharp decline in the SK Hynix perpetual contract, which fell 17.9%. BeInCrypto reported that the move triggered the liquidation of approximately $57.4 million in long positions across 960 accounts.

It is worth noting that the SK Hynix perpetual contract was launched by Trade.xyz under Hyperliquid’s HIP-3 framework, rather than by Hyperliquid itself. In a post on X, Trade.xyz addressed the incident and outlined the steps it plans to take in response.

The team said the SKHYNIX mark price fell from $1,127.90 to $917.25 at 23:01 UTC on July 27. According to the platform, the price was derived from an executed trade that was relayed by multiple independent data providers.

“The XYZ oracle was live in external pricing and tracking that venue, which serves as the primary Korean pre-market venue. The oracle system worked as intended according to its specification,” the post read.

To address the liquidation incident, the platform said it would cover liquidation losses attributable to the pricing anomaly. Eligibility rules will follow, and it expects distributions within days.

Trade.xyz framed the payout as a one-time discretionary decision rather than a precedent. It also plans to revisit how it forms prices, including signals from its own order books.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Trader Walks Away With $2.2 Million After SK Hynix Perp Crash appeared first on BeInCrypto.

The UK Financial Conduct Authority has identified cross-border payments as the strongest practical application for stablecoins after gathering feedback from banks, payment companies and crypto firms during its Stablecoin Sprint.

Summary

- FCA participants identified cross border payments as the strongest current use case for stablecoins, particularly in markets with limited access to U.S. dollars.

- The regulator said UK consumers have little incentive to switch payment methods, though merchants could benefit from lower costs and faster settlement.

- Findings from the Stablecoin Sprint have informed the FCA’s stablecoin issuer rules and will shape future policy for stablecoin payments.

- The March sprint and May trade finance roundtable brought together banks, payment firms, stablecoin issuers and fintech companies to examine payment and programmable finance use cases.

According to the UK Financial Conduct Authority, participants in its Stablecoin Sprint said stablecoins currently offer the clearest value in cross-border payments, especially in markets where access to U.S. dollars remains limited, while consumer adoption for everyday retail payments in the UK is likely to develop more slowly because existing payment systems already provide fast and low-cost transactions.

The regulator published the findings from the policy sprint, held in March 2026, alongside insights from a trade finance roundtable conducted in May. Around 75 representatives from banks, payment service providers, merchant acquirers, fintech companies, infrastructure providers, stablecoin issuers and industry groups attended the two-day event, while another 30 participants later discussed programmable payments in trade finance.

The exercise forms part of the FCA’s work on stablecoin payment regulation after it finalized rules for UK-issued stablecoins on June 30. Those rules require issuers to fully back stablecoins with reserve assets and redeem tokens at par, while the regulator said feedback gathered during the sprint will continue shaping future policy for stablecoin payments.

Stablecoin payments offer the strongest case in cross-border transfers

During the discussions, participants agreed that cross-border transfers present the strongest commercial opportunity for stablecoins because they can reduce settlement delays and improve access to dollar-based payments in countries where banking infrastructure remains limited.

The FCA said participants drew a distinction between emerging markets and established payment corridors. In mature markets where international payment services are already efficient and relatively inexpensive, firms considered the advantages of stablecoins less pronounced.

Domestic retail payments generated a different assessment. Participants told the regulator that UK consumers have little reason to replace existing payment methods because bank transfers and card payments are already widely available, inexpensive and completed quickly.

Businesses, however, could still benefit from stablecoin payments. According to the FCA, merchants identified lower transaction costs and faster settlement as potential advantages, particularly where payment delays or intermediary fees remain an issue.

Trade finance discussions held in May also examined programmable payments, with participants exploring how smart contract-based settlement could support commercial transactions through automated payment execution.

The latest findings build on the FCA’s wider crypto regulatory framework published on June 30, which established the next phase of the UK’s digital asset regime.

Under those rules, firms seeking to conduct regulated crypto activities will be able to apply for authorization from Sept. 30, 2026, before the full regime takes effect on Oct. 25, 2027. The framework covers trading platforms, custodians, staking providers and stablecoin issuers, while existing anti-money laundering registrations will not automatically transition into the new licensing system.

The FCA also adjusted part of its stablecoin framework after industry feedback. Final rules lowered the proposed capital requirement for stablecoin issuers to 1% of issued value from an earlier 2% proposal, with Executive Director for Payments and Digital Finance David Geale previously saying the regulator revised the requirement after reviewing evidence submitted by industry participants.

Most sterling-denominated stablecoins will remain under FCA supervision, while tokens considered systemically important would fall under oversight by the Bank of England.

Industry feedback has influenced earlier UK proposals

The Stablecoin Sprint findings follow several months of consultation between regulators and industry participants over how Britain should supervise fiat-backed digital assets.

In May, the Bank of England said it was reviewing parts of its proposed stablecoin framework after digital asset firms argued that reserve requirements and temporary holding limits could reduce the commercial viability of pound-backed stablecoins.

The central bank had proposed requiring issuers to keep at least 40% of reserves in non-interest-bearing deposits at the Bank of England while introducing temporary limits on individual and corporate holdings during an initial rollout period.

According to comments reported at the time, industry participants argued that ownership caps would be difficult to enforce across wallets and trading venues, while reserve requirements that generated no interest income could materially reduce issuer profitability.

Bank of England Deputy Governor Sarah Breeden said the central bank was reassessing whether those temporary holding limits remained necessary and whether reserve requirements should be adjusted.

The policy debate has also extended beyond domestic regulation. Bank of England Governor Andrew Bailey warned in May that the international growth of dollar-backed stablecoins could require closer coordination between regulators and described future discussions with the United States over global standards as a likely point of negotiation.

FCA also links stablecoins with programmable finance

Outside payments policy, the FCA has recently connected stablecoins with emerging artificial intelligence systems capable of carrying out financial decisions without continuous human involvement.

In its July review on the future of retail financial services, the regulator said autonomous AI agents managing payments, investments and savings accounts could increase demand for programmable digital money because conventional banking infrastructure may struggle to support machine-speed financial transactions.

The report identified stablecoins and tokenized bank deposits as payment infrastructure capable of supporting automated settlement through distributed ledger technology while maintaining that firms cannot transfer legal accountability to AI systems.

Every dollar Robinhood Chain earns, a tenth goes to a DAO treasury controlled by strangers. The arrangement has been covered a dozen times as good news for Arbitrum’s token.

Summary

- Robinhood Chain runs on Arbitrum’s Orbit stack, and under the Arbitrum Expansion Program every Orbit chain settling outside Arbitrum One routes 10% of net protocol revenue back to the Arbitrum ecosystem.

- The split is fixed: 8% to the Arbitrum DAO treasury, controlled by ARB tokenholders, and 2% to the Arbitrum Developer Guild.

- The figures are now real, no longer theoretical. Robinhood Chain has passed $2 million in cumulative revenue since its July 1 launch, with roughly $200,000 flowing to Arbitrum, and Arbitrum reported the network earning over $800,000 in a single seven-day stretch, annualizing near $42 million.

- The payment is calculated on net revenue after operating costs, applies to sequencer profits, and may extend to MEV capture if the chain adopts Arbitrum’s Timeboost mechanism.

- Every version of this story published so far has been written for ARB holders. The unexamined half is what the arrangement costs the brokerage, and why a company with a $2.2 billion war chest chose to pay it.

Nobody has asked the other question: what a licensed brokerage that spent a decade removing intermediaries bought by becoming a tenant.

There is a particular irony in a company whose entire founding pitch was the removal of intermediaries acquiring one. Robinhood spent a decade telling retail investors that the layers between them and the market were extractive, that commissions were a tax on participation, and that the right architecture was fewer parties taking a cut. On July 1 it launched its own blockchain, the most complete expression of that philosophy available: a settlement layer it controls, sequencing it operates, and fee revenue it collects. And under the terms of the technology stack it chose, a tenth of what that chain nets goes to somebody else. Specifically, 8% goes to a treasury controlled by holders of a governance token, and 2% funds a developer guild, both under an arrangement called the Arbitrum Expansion Program. The mechanism has been reported repeatedly since Offchain Labs disclosed it, always from one direction: what it means for ARB, why the token rallied, how a governance asset acquired a revenue claim. This piece asks the question those pieces did not. What did Robinhood buy, what is it paying, and does the arithmetic work.

What the arrangement actually is

The mechanics are specific enough to matter, and they have been reported loosely in several places.

The Arbitrum Expansion Program applies to any Layer 2 or Layer 3 chain built with Arbitrum’s Orbit toolkit that settles outside Arbitrum One or Arbitrum Nova. Those chains route 10% of net protocol revenue back to the Arbitrum ecosystem. Of that 10%, eight percentage points flow to the Arbitrum DAO treasury, which ARB tokenholders control through governance, and two percentage points fund the Arbitrum Developer Guild, which supports tooling, grants, and protocol work.

Three details in that description carry weight and are frequently dropped.Net, not gross. The calculation runs on revenue remaining after network operating costs, which ties the payment to a chain’s actual profitability instead of raw transaction throughput. That is materially friendlier to an operator than a gross fee would be, and it means a chain running at thin margins pays little regardless of volume.

Sequencer profits are the base. The revenue subject to sharing comes from the entity that orders and processes transactions, which on Robinhood Chain is Robinhood. That is the same revenue line this publication has examined as the core economics of any Layer 2, and it is precisely the line the chain exists to capture.

MEV may be included. If the chain adopts Timeboost, Arbitrum’s mechanism for capturing maximal extractable value from transaction ordering, those revenues could fall under the sharing arrangement as well. Whether Robinhood adopts it is a live question with real dollars attached, since ordering advantages on a chain hosting tokenized equities are worth considerably more than on a memecoin venue.

For contrast, Arbitrum One sends 100% of its own fees to the Arbitrum treasury. The Orbit arrangement is the lighter one, which is the point: it is the price of using the stack without settling on the flagship chain.

The numbers, now that they exist

For the first three weeks this was an abstraction. It is not anymore.

Robinhood Chain has passed $2 million in cumulative revenue since its July 1 launch, with approximately $200,000 routed to the Arbitrum ecosystem under the program. That is a clean 10%, and it is the first hard confirmation that the mechanism operates as described, not as an aspiration in a governance document.

Around that sit the throughput figures that produced it. The chain processed roughly 4 million transactions in its first week. Uniswap alone recorded $500 million in 24-hour volume on it. A single day in early July cleared $568 million. Within about two weeks the chain was clearing more than $800 million in daily decentralized exchange volume, briefly exceeding Ethereum’s, with roughly $3.9 billion across a week. Arbitrum reported the network earning over $800,000 in revenue across seven days, which annualizes near $42 million. Deposits crossed $600 million this week, rising 50% in seven days.

Now the distortion that every honest reading has to apply. The chain is running a 90-day gas subsidy, expiring around October, which means users are not paying the fees a mature chain would charge and the revenue figures are suppressed accordingly. Our audit of the chain’s first month documented how thoroughly that subsidy inflates activity metrics; it works in the opposite direction on revenue. The $42 million annualized figure is therefore both a real number and a floor, and the interesting reading comes after the subsidy lapses, when volumes and revenues both reprice. For broader context, crypto.news has also explained the subsidy distorting these numbers.

At current run rates, Arbitrum’s share is roughly $4 million a year. Against Robinhood’s quarterly revenue near $1.27 billion, that is a rounding error. Against the chain’s own economics, it is a tenth of everything.

What Robinhood bought

The arrangement only looks strange if you assume the alternative was free. It was not, and the alternatives are worth setting out because the choice reveals the strategy.

Build independently. A brokerage could commission a chain from scratch, own 100% of sequencer revenue, and pay nothing to anyone. The cost is time, engineering risk, and security. Rolling your own settlement layer means auditing it, defending it, and answering for it when something breaks, which for a regulated financial institution holding customer assets is not a theoretical exposure. It also means no ecosystem: no existing tooling, no bridges, no wallets that already work.

Use an existing chain. Deploy on Arbitrum One or Base or anywhere else, pay ordinary fees, capture nothing. This is what Robinhood actually did first, launching tokenized stock offerings on Arbitrum in 2025 before committing to its own chain, and the limitation is obvious: you are a tenant with no landlord’s economics and no control over the roadmap, the fee schedule, or who else gets to build next door.

Take the Orbit path. Get a chain you brand, control, and sequence, with Offchain Labs providing technical support, inheriting the Arbitrum ecosystem’s tooling and security assumptions, at the price of a tenth of net revenue. The launch specifications suggest what that bought: 100-millisecond block times, EVM compatibility, ETH as the gas asset instead of a new token nobody asked for, and a chain live and processing millions of transactions within a week of announcement.

Read that way, the 10% is a build-versus-buy decision resolved in favour of speed, and for a public company with a stock to defend and a crypto revenue line that fell 47% year over year in the first quarter, speed was plausibly worth more than margin. Our earnings analysis covered why the timing mattered so much.

The uncomfortable version of the same read is that Robinhood, having concluded that owning the rails is where the value sits, does not actually own them. It leases them, with favourable terms, from a decentralized organization whose token holders vote on what to do with the proceeds.

The tenant problem

That last sentence is not a rhetorical flourish. It describes a governance relationship that no traditional financial infrastructure arrangement resembles, and it has consequences nobody has priced.

The 8% going to the Arbitrum DAO treasury is controlled by ARB tokenholders through governance votes. Those holders decide how the money is deployed. They also, through the same governance process, hold influence over the direction of the technology stack Robinhood’s chain depends on. A licensed brokerage supervised by federal regulators is now a revenue contributor to, and a dependent of, an entity whose decision-making runs through token voting by anonymous participants.

For most crypto-native businesses that is unremarkable. For a public company that files with the SEC, answers to a board, and holds customer assets under regulatory obligation, it is a novel counterparty structure. The questions it raises are practical, not philosophical: what happens if governance votes to change the fee arrangement, what recourse exists if the stack’s roadmap diverges from the tenant’s needs, and how a regulated institution documents dependency on a DAO in its risk disclosures.

There is also a competitive dimension. The Orbit program applies universally, meaning any competitor can take the same path on the same terms. The arrangement Robinhood entered is not exclusive and confers no advantage over the next brokerage to build a chain, which limits how much of a moat the whole exercise creates. What it does create is a template, and the rest of the industry has noticed: our coverage of the tokenized-equity race documented Nasdaq building blockchain share issuance with Kraken’s parent and ICE working with OKX, none of which requires anyone to build from scratch.

Does the arithmetic work

Set aside the framing and ask the commercial question, because the answer determines whether any of this matters.

Roughly $42 million annualized in chain revenue, before the subsidy expires, against $4 million to Arbitrum. Against a company whose quarterly revenue runs near $1.27 billion, the chain contributes something in the low single-digit percentage range of annual revenue at current run rates, and the Arbitrum payment is immaterial to the parent by any measure.